21st Century Oncology Of Jacksonville Inactive

Filed: 20 Jun 12, 12:00am

Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

Filed pursuant to Rule 424(b)(3)

Registration Nos. 333-181650 through 333-181650-40

Prospectus

Radiation Therapy Services, Inc.

350,000,000

Exchange Offer for 87/8% Senior Secured Second Lien Notes due 2017

Offer for outstanding 87/8% Senior Secured Second Lien Notes due 2017, in the aggregate principal amount of $350,000,000 (which we refer to as the "Old Notes") in exchange for up to $350,000,000 in aggregate principal amount of 87/8% Senior Secured Second Lien Notes due 2017 which have been registered under the Securities Act of 1933, as amended (which we refer to as the "Exchange Notes" and, together with the Old Notes, the "notes").

Terms of the Exchange Offer

Terms of the Exchange Notes

For a discussion of the specific risks that you should consider before tendering your outstanding Old Notes in the exchange offer, see "Risk Factors" beginning on page 26 of this prospectus.

There is no established trading market for the Old Notes or the Exchange Notes.

Each broker-dealer that receives Exchange Notes for its own account pursuant to the exchange offer must acknowledge that it will deliver a prospectus in connection with any resale of such Exchange Notes. A broker dealer who acquired Old Notes as a result of market making or other trading activities may use this exchange offer prospectus, as supplemented or amended from time to time, in connection with any resales of the Exchange Notes.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the Exchange Notes or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is June 20, 2012.

Each broker-dealer that receives Exchange Notes for its own account pursuant to the exchange offer must acknowledge that it will deliver a prospectus in connection with any resale of such Exchange Notes. By so acknowledging and by delivering a prospectus, a broker-dealer will not be deemed to admit that it is an "underwriter" within the meaning of the Securities Act of 1933, as amended (the "Securities Act"). A broker dealer who acquired Old Notes as a result of market making or other trading activities may use this prospectus, as supplemented or amended from time to time, in connection with any resales of the Exchange Notes. We have agreed that, for a period of up to 180 days after the closing of the exchange offer, we will make this prospectus available for use in connection with any such resale. See "Plan of Distribution."

You should rely only on the information contained in this prospectus. We have not authorized anyone to provide you with information different from that contained in this prospectus. This prospectus does not constitute an offer to sell or a solicitation of an offer to buy securities other than those specifically offered hereby or an offer to sell any securities offered hereby in any jurisdiction where, or to any person whom, it is unlawful to make such offer or solicitation. The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of our 87/8% Senior Secured Second Lien Notes due 2017.

PROSPECTUS SUMMARY | 1 | |||

RISK FACTORS | 26 | |||

USE OF PROCEEDS | 57 | |||

UNAUDITED PRO FORMA CONSOLIDATED FINANCIAL INFORMATION | 58 | |||

SELECTED HISTORICAL CONSOLIDATED FINANCIAL DATA | 62 | |||

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 65 | |||

BUSINESS | 112 | |||

MANAGEMENT | 152 | |||

EXECUTIVE COMPENSATION | 159 | |||

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT | 187 | |||

CERTAIN RELATIONSHIPS AND RELATED PARTY TRANSACTIONS | 190 | |||

DESCRIPTION OF OTHER INDEBTEDNESS | 196 | |||

DESCRIPTION OF EXCHANGE NOTES | 208 | |||

BOOK-ENTRY SETTLEMENT AND CLEARANCE | 263 | |||

CERTAIN UNITED STATES FEDERAL INCOME TAX CONSIDERATIONS | 265 | |||

PLAN OF DISTRIBUTION | 266 | |||

LEGAL MATTERS | 267 | |||

EXPERTS | 267 | |||

WHERE YOU CAN FIND ADDITIONAL INFORMATION | 267 | |||

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS | F-1 |

i

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains forward-looking statements within the meaning of Section 27A of the Securities Act and Section 21E in the Exchange Act. These statements may be identified by the use of forward-looking terminology such as "anticipate", "believe", "continue", "could", "estimate", "expect", "intend", "may", "might", "plan", "potential", "predict", "should", or "will" or the negative thereof or other variations thereon or comparable terminology. In particular, statements about our expectations, beliefs, plans, objectives, assumptions or future events or performance contained in this prospectus are forward-looking statements.

We have based these forward-looking statements on our current expectations, assumptions, estimates and projections. While we believe these expectations, assumptions, estimates and projections are reasonable, such forward-looking statements are only predictions and involve known and unknown risks and uncertainties, many of which are beyond our control. These and other important factors, including those discussed in this prospectus under the headings "prospectus Summary", "Risk Factors", "Management's Discussion and Analysis of Financial Condition and Results of Operations" and "Business", may cause our actual results, performance or achievements to differ materially from any future results, performance or achievements expressed or implied by these forward-looking statements.

Given these risks and uncertainties, you are cautioned not to place undue reliance on such forward-looking statements. The forward-looking statements included in this prospectus are made only as of the date hereof. We do not undertake and specifically decline any obligation to update any such statements or to publicly announce the results of any revisions to any of such statements to reflect future events or developments.

PRESENTATION OF FINANCIAL INFORMATION

As more fully described in this prospectus, on February 21, 2008, we consummated the merger of a wholly-owned subsidiary of Radiation Therapy Services Holdings, Inc. ("Parent") with and into Radiation Therapy Services, Inc. with Radiation Therapy Services, Inc. as the surviving corporation and as a wholly-owned subsidiary of Parent (the "Merger"). The term "Predecessor" refers to our predecessor company, Radiation Therapy Services, Inc. prior to the Merger. The term "Successor" refers to Radiation Therapy Services Holdings, Inc. and its subsidiaries following the Merger.

The Merger was accounted for under the purchase method of accounting in accordance with Financial Accounting Standards Board ("FASB") Accounting Standards Codification ("ASC") 805, "Business Combinations" ("ASC 805"). Under the purchase method of accounting, the Merger was treated as a purchase and the assets so acquired were valued on our books at our assessments of their fair market value. Therefore, the results of operations, other comprehensive income (loss), changes in equity and cash flow for the Predecessor and Successor periods are not comparable. Accordingly, our audited consolidated financial statements, included elsewhere in this prospectus include the consolidated accounts of the Successor as of December 31, 2011 and 2010 and for each of the three years in the period ended December 31, 2011.

In this prospectus, we rely on and refer to information and statistics regarding the radiation therapy services industry as well as the cancer treatment industry and, unless otherwise specified, our market share is based on our revenue rank among public and private radiation therapy services companies based on public filings with the SEC, industry presentations and industry research reports. Where possible, we obtained this information and these statistics from third-party sources, such as independent industry publications, government publications or reports by market research firms, including company research, trade interviews, and public filings with the SEC. Additionally, we have supplemented third-party information where necessary with management estimates based on our review

ii

of internal surveys, information from our customers and vendors, trade and business organizations and other contacts in markets in which we operate, and our management's knowledge and experience. However, these estimates are subject to change and are uncertain due to limits on the availability and reliability of primary sources of information and the voluntary nature of the data gathering process. As a result, you should be aware that industry data included in this prospectus, and estimates and beliefs based on that data, may not be reliable.

Numerical figures included in this prospectus have been subject to rounding adjustments. Accordingly, numerical figures shown as totals in various tables may not be arithmetic aggregations of the figures that precede them.

We have filed an application to own the rights to a copyright that protects the content of our "Gamma Function" software technology. Solely for convenience, the copyright referred to in this prospectus is listed without the © symbol, but such references are not intended to indicate in any way that we will not assert, to the fullest extent under applicable law, our right to this copyright.

iii

This summary highlights selected information contained in greater detail elsewhere in this prospectus and may not contain all of the information that may be important to you. You should carefully read the entire prospectus before making an investment decision, especially the information presented under the heading "Risk Factors" and our audited consolidated financial statements and the accompanying notes, included elsewhere in this prospectus. References in this prospectus to "we", "us", "our" and "the Company" are references to Radiation Therapy Services, Inc. and its subsidiaries, consolidated professional corporations and associations and unconsolidated affiliates, unless the context requires otherwise. References in this prospectus to "our treatment centers" refer to owned, managed and hospital-based treatment centers. Additionally, references in this prospectus to "our radiation oncologists" refer to both those professionals employed by us and those employed by professional corporations in those treatment centers we manage, unless the context requires otherwise.

We are a leading provider of advanced radiation therapy and other clinical services to cancer patients primarily in the United States and Latin America. Our core line of business is offering a comprehensive range of radiation treatment alternatives, where we focus on delivering academic quality, cost-effective patient care in a personal and convenient community setting. Our first radiation treatment center opened in 1983, and as of March 31, 2012, we operated 126 radiation treatment centers, 121 of which are freestanding facilities with the five remaining facilities operated in partnership with hospitals and other groups. Our cancer treatment centers in the United States are strategically clustered in 28 local markets across 15 states. We also operate 30 radiation treatment centers in South America, Central America, Mexico and the Caribbean as well as one center located in India where we have been able to uniquely disseminate advanced technology in a cost-effective manner to a growing healthcare population. The majority of our centers in Latin America are operated together with local minority partners. We hold market leading positions in most of our local markets in the United States and abroad.

In order to respond to the changing healthcare landscape, where providers across medical specialties collaborate to provide patient care, we are in the process of evolving from a freestanding radiation oncology centric model to an Integrated Cancer Care ("ICC") model. This new approach to focus on growing our network of employed or affiliated physicians is providing our patients with a more comprehensive treatment team to better target and treat tumors and improving our patients' experience. We currently employ or affiliate with over 415 physicians in the fields of medical oncology, breast, gynecological and general surgery, urology as well as primary care in certain key markets. In many cases, these physicians are co-located with our radiation oncologists. Our ICC model will enable us to collaborate with a broader group of physicians in other medical specialties, integrate services for related medical needs, and disseminate best practices across facilities, all of which should help us generate a stronger presence in each market we serve. In addition, we have been proactively pursuing partnership arrangements with hospitals, other providers and payers to further the mission of improving the continuum of services and clinical resources available to cancer patients. Examples of our successes in these efforts include our selection as the developer and operating partner in the first proton beam therapy center in New York as well as in our success in developing relationships where we can provide value-added services in the field of informatics, technical services and clinical research to other providers.

Our leadership in the transition to the ICC model stems from our position as the largest radiation therapy provider in the United States, by number of centers, as well as our long history of clinical innovation. Our scale along with the systems and processes we have developed to manage a large network of radiation oncology providers afford us many competitive advantages including the advanced medical and technological resources that we are able to leverage. Our physicians are able to access the

1

latest advances in treatment protocols and approaches allowing them to deliver the most effective and clinically appropriate treatments to our patients in a community setting. Our nationwide presence also enables us to implement best practices by sharing new approaches and recently developed findings across our network. We leverage our size by recruiting, developing and training key clinical personnel. For instance, we operate our own certified dosimetry and certified radiation therapy schools and have an affiliated accredited physics program. These capabilities combined with senior physician leadership, a premier medical board and substantive training and mentoring programs, have allowed us to deliver superior and innovative patient care with the highest quality standards across our centers and disciplines. Furthermore, our operational infrastructure and our network size afford us advantages in areas such as purchasing, recruiting, billing, compliance, quality assurance and clinical information systems.

Our operating philosophy is centered upon using the latest available and most advanced technology and employing or affiliating with leading physicians to deliver a variety of treatment options to our patients in each local market. To implement this philosophy, we invest in new software, training and equipment with the goal of equipping each local market with state-of-the-art technology that facilitates better clinical results. Through the use of advanced tools and comprehensive clinical protocols, we can improve therapeutic outcomes by determining the right course of treatment at the outset allowing us to precisely target and eradicate cancerous cells and tumors while sparing healthy surrounding tissues and organs. We attract and retain talented physicians and staff by providing opportunities to work in an environment that has a clinical and research focus, superior end-to-end resources and high quality patient care. We have built a national platform of cancer treatment centers while increasing both the revenue and profitability of the Company. Since the beginning of 2003, we have internally developed 24 treatment centers, acquired 70 existing treatment centers, transitioned two treatment centers from hospital-based treatment centers to freestanding treatment centers, and from 2008 to 2011, we increased our revenues at a compound annual growth rate of approximately 9.0%. We believe that as our scale continues to increase, our physician-led ICC model along with our operational and financial resources will not only differentiate us from many of our competitors, but will also enhance our attractiveness to patients, referral sources, physicians, hospital partners, employees and acquisition targets. For the year ended December 31, 2011, our total revenue was $644.7 million.

Although we are migrating to an ICC model in appropriate markets and circumstances, our primary focus and relevant industry remains related to the provision of radiation therapy for patients with cancer in the United States and Latin America.

We believe the United States radiation therapy market was approximately $8 billion in 2010. The market's growth is driven by the growing number of cancer diagnoses and the development and use of increasingly effective technologies that enable more types of cancer related tumors to be treated with radiation therapy. The American Cancer Society estimates that approximately 1.6 million new cancer cases are expected to be diagnosed in the United States in 2012. As the U.S. population ages, the number of cancer diagnoses is expected to continue to increase, as approximately 77% of all cancers are currently diagnosed in persons 55 years of age and older. Radiation therapy is a primary treatment method for cancer and, according to the American Society for Therapeutic Radiology and Oncology ("ASTRO") nearly two-thirds of patients diagnosed with cancer receive radiation therapy during their illness. Radiation therapy's share of the cancer treatment market has increased as a result of new radiation therapy technologies that better target cancerous tumors and lead to fewer side effects as compared to other forms of treatment and to previous radiation therapy treatments.

The Latin American radiation therapy market is also expected to continue to grow due to an increase in the number of cancer diagnoses as a result of the aging population. Argentina, Mexico, and Brazil represent approximately 60% of new cancer cases in Latin America and all three markets are

2

less developed than the U.S. market. As a result, mortality rates in Latin America for those diagnosed with cancer are higher than rates in the United States, indicating an opportunity to further improve the availability and type of treatment throughout Latin America. We currently operate in six countries in Latin America, including Argentina, Dominican Republic, Mexico, Guatemala, El Salvador and Costa Rica, with each country demonstrating varied payer and demographic characteristics and levels of competition and technological advancement. We have recently expanded our Latin America business into a seventh country, having executed a construction agreement to modify an existing building in Bolivia to provide radiation therapy services. Argentina, with 73% of our Latin American sales, is our largest international market and one of the most developed markets in Latin America. However, while it has an attractive payer base for our services, its penetration of developed technologies is still significantly below the U.S. levels. The underserved population is substantial across all payer levels in less developed markets like Mexico and Bolivia and therefore provides a significant opportunity. Latin American payers are highly diversified in serving the middle and lower class populations and include government, commercial and union plans as well as self pay, all of which are increasingly covering advanced technologies, such as 3D conformal and intensity modulated radiation therapy ("IMRT"), and as such, the access to more advanced technology should continue to expand.

Radiation therapy is used to treat the most common types of cancer, including prostate, breast and lung cancer. Radiation therapy uses high-energy particles or waves, such as x-rays, to destroy cancer cells by delivering high doses of radiation to the tumor through a special piece of equipment, known as a linear accelerator. In addition, when a cure is not possible, radiation therapy is often able to shrink tumors and reduce pressure thereby reducing pain while also relieving other symptoms of the cancer to enhance a patient's quality of life.

Although a significant majority of cancer patients receive radiation therapy treatment, additional treatments for cancer patients include surgery, chemotherapy and/or biological therapy often in conjunction with radiation therapy. Physicians generally choose the appropriate treatment or combination of treatments based upon the type of cancer, its stage of development and where the cancer is located. Radiation therapy patients are usually referred to a treatment center or a radiation oncologist by urologists, breast surgeons, general oncologists and general surgeons, among other sources.

Recent research and technological advances have produced new, advanced methods for radiation treatment. These advanced methods result in more effective treatments that deliver the necessary doses of radiation while minimizing the harm to healthy tissues and organs that surround the tumor. This is accomplished by modulating the intensity across the tumor and reducing the amount of radiation leakage resulting in fewer side effects and complications as well as an enhanced quality of life. For instance, the development of more intense delivery methods such as stereotactic radiosurgery ("SRS") combined with tumor tracking or respiratory gating techniques, allow cancers located in the lung and liver to be treated with significantly fewer but higher dose radiation treatments and higher control rates. This results in less dosage to normal lung or liver tissue and leads to fewer side effects than before and can present a more effective therapy than surgery. With the discovery of new, innovative means to deliver radiation therapy and the increasing awareness of advanced treatments with reduced side effects among patients and physicians, radiation therapy is expected to be a preferred method for treating cancer.

The radiation therapy competitive landscape is highly fragmented. In 2010, there were over 2,200 locations providing radiation therapy in the United States, of which approximately 960 were freestanding, or non-hospital based treatment centers. Approximately 30% of freestanding treatment centers are affiliated with the largest four provider networks, which includes Radiation Therapy Services, Inc. The Latin American radiation therapy market is similarly fragmented with most competition coming primarily from hospitals and some smaller local groups. In Argentina we are the largest of four well-established radiation therapy providers, with particularly strong market positions in

3

Buenos Aires, Cordoba and Mendoza. In other Latin American markets, we are the number one or number two provider in the majority of local markets where we operate.

The physician services industry is currently undergoing consolidation of smaller independent physician practices by larger hospital and physician practice groups. A 2010 survey conducted by theMedical Group Management Association indicated that capital investments and ongoing operating costs have pushed physicians to seek a more secure work environment at larger hospitals and physician groups. More critically, however, consolidation activity is also driven by the capabilities that strong performing hospitals and physician groups can provide. Such services include high quality facilities, state-of-the-art technology, more favorable payer contracts, consistent use of patient protocols, capital and operational support as well as greater IT capabilities. It is estimated that the current consolidation trends will help create new opportunities for physicians to deliver better care coordination to patients and reduce any existing variations in care that do not offer value. In addition, consolidation is expected to lessen the administrative burdens that physician practices face, allowing doctors to focus more on patient care and clinical outcomes. As the largest radiation therapy provider in the United States, we feel that we are well-positioned to take advantage of the current consolidation trends and lead the industry's migration to an ICC model due to the vast scale of our network, our advanced infrastructure and clinical talent as well as our successful track record of educating and disseminating advanced technology to physicians in a cost-effective manner.

We believe our radiation treatment centers, and in many markets our comprehensive cancer care centers, are distinguishable from those of many of our competitors because we offer patients an enhanced patient experience and a full spectrum of radiation therapy and cancer treatment alternatives, including many advanced radiation treatment options that are not otherwise available in certain local geographies or offered by other providers. Our radiation treatment services include external beam therapies, such as 3D conformal radiation therapy, IMRT and stereotactic radiosurgery as well as internal radiation therapy such as high-dose and low-dose rate brachytherapy. In addition, we utilize various supplementary technologies, including image guided radiation therapy, Gamma Function and respiratory gating to improve the effectiveness and safety of the radiation treatments. Finally, we provide an array of complementary support services in the areas of psychological and nutritional counseling as well as transportation assistance, consistent with applicable regulatory guidelines.

Radiation therapy is administered in one of two ways: externally or internally, with some cancers treated utilizing both approaches. External beam radiation therapy involves directing a high-energy x-ray beam generated from a linear accelerator to the patient's tumor. Most patients undergoing radiation therapy for cancer are treated with external beam radiation therapy. A course of external beam radiation therapy typically ranges from 20 to 40 treatments. Treatments are generally performed once per day with each session lasting approximately 15 minutes. Internal radiation therapy, also called brachytherapy, involves the placement of a radiation-emitting element within or adjacent to the patient's tumor. Brachytherapy usually requires an operating room procedure for either insertion of the radiation source to remain permanently in the cancerous organ or insertion of thin plastic tubes to allow for temporary placement of a radiation source within the tumor after which both the source and tubes are removed from the body.

We were recently selected as the developer and managing partner of the first medical proton beam therapy center in New York. Our partners include five of the largest cancer care programs at key academic institutions in New York including Memorial Sloan-Kettering, NYU Langone, Mt. Sinai, Continuum and Montefiore. We anticipate the proton center to be operational and treating its first patients in early 2016. In addition, we have started beta testing for adaptive radiotherapy and have developed an internal advanced development group, Aurora Development Group ("Aurora"), to focus on refining and commercializing both of these technologies which we believe will be critical treatment alternatives for cancer patients in the future.

4

The following table sets forth the forms of radiation therapy treatments and advanced services that we currently offer:

Technologies | Description | |

|---|---|---|

External Beam Therapy | ||

3D Conformal Radiation Therapy | Enables radiation oncologists to utilize medical linear accelerator x-ray machines to direct radiation beams at the cancer. | |

Intensity Modulated Radiation Therapy ("IMRT") | Enables radiation oncologists to adjust the intensity of the radiation beam and shape the radiation dose to match the size and shape of the treated tumor with a higher degree of precision than 3D conformal therapy. The net clinical result of this technology is the delivery of higher, more effective radiation doses to tumors while reducing radiation exposure of the surrounding normal, healthy organs. | |

Stereotactic Radiosurgery ("SRS") | Enables delivery of highly precise, high-dose radiation to small tumors. SRS utilizes additional treatment technologies to deliver treatment with greater precision and accuracy than either IMRT or 3D therapy. Historically, SRS was used primarily for brain tumors but recent advancements in imaging and radiation delivery technologies have allowed for expanding applications of this technology to the treatment of extra cranial cancers. | |

Internal Radiation Therapy | ||

High-Dose Rate Remote Brachytherapy | Enables radiation oncologists to treat cancer by internally delivering high doses of radiation directly to the cancer using temporarily implanted radioactive elements. | |

Low-Dose Rate Brachytherapy | Enables radiation oncologists to treat cancer by internally delivering doses of radiation directly to the cancer over an extended period of time using permanently implanted radioactive elements (e.g., prostate seed implants). | |

Advanced Services Used with External Beam Treatment Therapies | ||

Image Guided Radiation Therapy ("IGRT") | Enables radiation oncologists to utilize x-ray imaging at the time of treatment to identify the exact position of the tumor within the patient's body and adjust the radiation beam to that position for better accuracy. |

5

Technologies | Description | |

|---|---|---|

Gamma Function | Proprietary capability that for the first time enables measurement of the actual amount of radiation delivered during a treatment. Gamma Function also enables the verification of radiation delivery and the comparison to physician prescription and treatment plans. Further, it provides the physician with information to adjust for changes in tumor size and location, and ensures immediate feedback for adaption of future treatments as well as for quality assurance. | |

Respiratory Gating | Coordinates treatment beam activation with the respiratory motion of the patient, thereby permitting accurate delivery of radiation dosage to a tumor that moves with breathing, such as lung and liver cancers. | |

Operating Technologies Under Development | ||

Proton Therapy | Form of radiation treatment that utilizes subatomic particles instead of x-rays and can achieve better radiation sparing of surrounding normal organs for certain tumor types. | |

Adaptive Radiotherapy | A novel approach to radiation therapy that is currently under development at our Company and a small number of academic medical centers, adaptive radiotherapy is a process that will automatically trigger a new more informed treatment plan during the course of therapy in order to adapt to anatomic changes that occur to the tumor. For example, as a tumor shrinks during treatment, adaptive radiotherapy will respond by generating a new treatment plan customized to the smaller tumor and further spare radiation exposure of nearby healthy tissue and organs. |

6

We believe that the following competitive strengths have allowed us to achieve and maintain our position as a leading provider of radiation therapy and provide us with the necessary tools to become the leading ICC model in the United States and Latin America:

International Platform with Strong Local Market Positions—As of March 31, 2012, we serve patients in 28 domestic markets across 15 states, including Alabama, Arizona, California, Florida, Kentucky, Maryland, Massachusetts, Michigan, Nevada, New Jersey, New York, North Carolina, South Carolina, Rhode Island and West Virginia, and we recently expanded into international markets,—primarily Latin America. Most of our cancer treatment centers are strategically clustered into regional networks (which we refer to as our local markets) in order to leverage our clinical and operational expertise and resources over a larger patient population and maximize our investment in advanced technologies. For example, our local markets enable us to share scarce and expensive medical physicists, who are critical in the process of developing the radiation treatment plan for each patient as well as making sure the equipment is properly calibrated. By staffing two physicists at three to four treatment centers in each of our local markets, as opposed to each treatment center, we are able to increase resource utilization and provide enhanced and consistent treatment in a cost effective manner. Another example is our ability to provide our patients with a full set of clinical alternatives through our ICC relationships in certain markets, as well as our ability to offer them the full technological spectrum in radiation therapy, including less common treatment alternatives, by equipping each of our local markets, as opposed to each treatment center, with the necessary technology and know-how and thus doing so on a more cost-effective basis. Our scale also allows us to serve as a center for leading clinical research and technological advances, which help us attract and retain talented radiation oncologists, physicians, physicists and other professionals. Furthermore, our large platform in the United States and Latin America, and our reputation, recruiting ability and market knowledge enable us to respond quickly and efficiently to new acquisition as well as internally developed ("de novo") and joint venture opportunities. Since the beginning of 2003, we have acquired or developed 94 treatment centers, transitioned two treatment centers from hospital-based treatment centers to freestanding treatment centers, entered into 16 new local markets and expanded into international markets including Latin America and India as of March 31, 2012. Finally, our centralized approach to business functions such as purchasing, engineering and service, accounting, administration, billing and information technology enables us to leverage economies of scale in various direct and indirect costs.

Best in Class Clinical and Technological Platform—We believe that we have the best in class technology, which allows us to provide the highest quality of care and clinically advanced treatment options to our patients. We consistently upgrade our equipment and technology and we believe they will require minimal maintenance capital expenditures in the near future. We believe we are the market leader in the utilization of advanced technologies, such as IMRT, IGRT and our recently developed Gamma Function. These technologies are more effective at treating many forms of cancer than other, older technologies such as conformal beam. Our continuous and early adoption of technology platforms has allowed us to implement and share technology across centers very quickly and therefore enhance clinical expertise within the Company and the industry overall. Our Chief Technology Officer, who is certified in radiotherapy physics, has received numerous awards, serves as an adjunct professor, is a published author in a variety of fields and has spent 20 years in his current role with the Company managing 80 physicists in the United States and an internal radiation equipment development and maintenance team. He also leads our Aurora team which is recognized as a leader in establishing and disseminating advancements in radiation therapy, including important developments in proton beam therapy and adaptive radiotherapy. Our Chief Medical Officer has been with the Company for 10 years and is a leading radiation oncologist who conducts radiation therapy research projects, publishes professional journal articles and presents at national cancer treatment meetings. These members of management and the teams that they lead provide both technical and clinical expertise throughout our

7

network, enhancing the level of patient care, safety and quality control. In addition, as we have grown our field of other cancer care specialists, we have added experts in the field of urology, medical oncology and surgery, among others. These professionals have a national platform for sharing best practices and clinical outcomes, thereby improving the full continuum of care from diagnosis to discharge. We feel our clinical and technological platform provides us with a significant competitive advantage in attracting new professional talent, upgrading equipment, clinical services and operations of acquired centers and the opportunity to distinguish ourselves with referral sources, physicians, payers and patients.

Leading Radiation Oncologists—We have been successful in recruiting, acquiring practices from, and retaining radiation oncologists with excellent academic and clinical backgrounds who we believe have potential for professional growth. Our approximately 115 radiation oncologists in the domestic United States have an average of over 16 years of experience and we believe our most senior clinical leadership are regarded as industry leaders. As a physician-led organization, we value superior training, research capabilities and mentoring. In addition to being educated and trained at some of the world's most prestigious and well recognized medical training centers and universities, our physicians have held positions in radiation oncology's elite research institutes, societies and regulatory bodies. These institutions and societies include ASTRO, American College of Radiation Oncology ("ACRO"), Association of Freestanding Radiation Oncology Centers ("AFROC") and Radiation Therapy Oncology Group. Our clinical leadership also publishes frequently as academic contributors, having co-authored numerous white papers, radiation therapy research projects and empirical studies in a wide range of international and domestic medical journals. We attract and retain our existing physicians by:

Favorable Industry Dynamics—Cancer treatment is a large and growing market. In 2008, there were approximately 12.0 million people living with cancer or with a history of cancer in the United States. The market has been growing with approximately 1.6 million new cases expected to be diagnosed in the United States in 2012. Radiation therapy remains a core treatment for cancer with nearly two-thirds of cancer patients receiving radiation therapy during their illness. The U.S. radiation therapy market was estimated to be approximately $8 billion in 2010. We believe the Latin American market exceeds $1.0 billion in value for radiation therapy treatments and is growing 2-4% per year. Compared to the U.S. market, the Latin American radiation therapy market is less developed, with higher mortality rates for those diagnosed with cancer, leading to more favorable dynamics as countries seek to improve their

8

clinical offerings. We believe that several factors will contribute to the continued expansion of the cancer treatment market and increased utilization of radiation therapy as one of the primary treatment methods, including:

Stable and Growing Business with Strong Operating Cash Flow—There are several underlying factors that we believe contribute to the stability and growing performance of our business; most notably, the aging of the population and resultant rise in cancer cases, the opportunity for profitable growth in the Latin American radiation therapy market and that radiation therapy remains a primary tool used to treat cancer. Additionally, our growth is attributable to our utilization of more advanced treatment technologies, which typically generates higher revenue and margins. In addition to stable and growing revenues, our base business includes characteristics that produce significant operating cash flow such as low operating costs and minimal working capital needs. The generation of operating cash flow allows us to either reinvest in our business through capital expenditures and growth initiatives and/or reduce indebtedness, each as determined by our business and financial strategies.

Strong Track Record of Successful Acquisitions and De Novo Facility Development—We have grown at a measured pace through a focused strategy of acquisitions, development of freestanding centers and hospital based joint ventures. Since the beginning of 2003, we have acquired 70 treatment centers and transitioned two treatment centers from hospital-based treatment centers to freestanding treatment centers, and have a successful track record of integrating our acquisitions as a result of our ability to leverage regional resources and technology, improve the mix of treatments and put in place more favorable contracts for insurance and medical supplies that take advantage of our size and scale. We have also been successful at identifying opportunities where we can deploy our ICC model and drive improved financial and clinical stability through a comprehensive service offering. We have a deep corporate development team and unique market analysis software that enables us to proactively identify and prioritize acquisition targets based on demographics, payer landscape, ICC opportunity and competition, among other factors. In 2010, approximately 30% of the U.S. market's freestanding centers were affiliated with the four largest provider networks, which include Radiation Therapy Services, Inc. In addition, a significant number of hospitals and hospital management companies are looking to build or expand comprehensive cancer offerings and are interested in joint ventures with providers such as our Company. As a result, we believe our pipeline of potential targets is robust and acquisitions will remain a significant part of our core growth strategy. As a leading national platform company in the industry, we believe we are a preferred acquirer in light of the services and benefits we can offer.

Since the beginning of 2003, we have also developed 24 de novo treatment centers, including joint ventures with hospitals as of March 31, 2012, and we continue to seek opportunities to develop

9

additional de novo treatment centers as a means to strengthen our local market share. De novo treatment centers allow us to penetrate underserved markets, partner with hospitals which have significant market presence or extend our local network and typically require lower initial capital expenditures. De novo treatment centers typically generate positive cash flow within six months after opening in an existing market and twelve to fifteen months after opening in a new market.

Experienced and Committed Management Team and Equity Sponsor—Our senior management team, several of whom are practicing radiation oncologists, has extensive public and private sector experience in healthcare, in particular radiation oncology. 11 of our senior management team have been with us for an average of 14 years and average approximately 17 years in the radiation therapy industry. In addition, our recently appointed Chief Financial Officer, Chief Operating Officer, Senior Vice President of Managed Care and Senior Vice President of Marketing have deep functional expertise in relevant organizations including positions at our sponsor Vestar Capital Partners, DaVita Inc., United Health Group and Bravo Health. This new talent is augmenting a successful management team that has since 1999, led the Company in growing from $56.4 million in total revenues to $644.7 million of total revenues for the year ended December 31, 2011 and creates both management breadth and depth in a team that combines outstanding clinical and medical experience with significant operational and financial expertise. Management has over $120 million currently invested in the Company. In addition, our equity sponsor, Vestar, which along with its affiliates has over $500 million currently invested in the Company, has considerable experience making successful investments in a wide variety of industries, including healthcare.

We believe we are in a superior position relative to our competitors to capitalize on the opportunities in our markets given our size, market locations, access to capital and clinical expertise as well as our experienced physician base and management team. The key elements to our strategy are:

Maintain Emphasis on Service and Quality of Care—We focus on providing our patients with an environment that minimizes the stress and uncertainty of being diagnosed with and treated for cancer. We aim to enhance patients' overall quality of life by providing technologically advanced radiation treatment alternatives that deliver more effective radiation directly to cancerous cells while minimizing harm to surrounding tissues and organs in order to reduce side effects. As an example, one of our most recent technologies, Gamma Function, provides enhanced quality control during treatment delivery. Gamma Function effectively measures the radiation byproduct, or throughput, as the beam exits the body, thereby measuring the accuracy of the radiation delivery to the prescribed tumor site and giving the physician more frequent opportunities to re-design and improve treatment plans during a course of an overall treatment regimen. Additionally, we verify every accelerator's output daily and voluntarily re-calibrate each machine annually using the services provided by the M.D. Anderson Radiation Physics Center at the University of Texas to ensure that our stringent quality control standards are met. Over 80% of our facilities have been accredited, or are in the process of being accredited, by an independent third party, which we believe is unique in the industry. Accreditation requires centers to meet stringent and consistent quality measures over a three year period. We have a compliance program that is consistent with guidelines issued by the Office of Inspector General ("OIG") of the Department of Health and Human Services ("DHHS"). Our compliance team, led by a senior officer who has been with the Company since 2004, coupled with our in-house physics and engineering departments, complements our front-end focus on employing the best physicians and using the most advanced technologies to provide our patients with superior care in a safe and quality controlled environment.

Our treatment centers are designed to deliver high-quality radiation therapy in a patient friendly environment and are generally located in convenient, community based settings. We make every effort to see patients within 24 hours of a referral and to begin treatment as soon as possible thereafter. In

10

addition, our physicians are available to patients at any time to discuss proposed treatments, possible side effects and expected results of treatment. Finally, we offer support services in the areas of psychological and nutritional counseling as well as transportation assistance, consistent with applicable regulatory guidelines, each of which serves to improve the patient experience. We believe our focus on patient service enhances the quality of care provided, differentiates us from other ICC providers and sole radiation therapy providers and strengthens our relationships with both our referring and affiliated physicians.

Increase Revenue and Profitability of Our Existing Treatment Centers—We plan to continue to provide capital, support and technology to our existing centers to drive increased census, improve treatment mix and leverage our strong market presence to generate operating efficiencies. We believe our scale and strategy of clustering treatment centers in local markets provide unique advantages for driving referrals, improving payer relationships and enhancing our clinical reputation, all of which lead to growth in patient volume. In the beginning of 2011, we successfully initiated a physician liaison program to educate referring physicians, patients, and caregivers about our clinical and technological offerings as well as our commitment to providing a positive patient experience. Since that time, we have grown from three physician liaisons to 19 today. This program was a major contributor to improved same practice volume growth over the course of fiscal 2011 including the 3% same practice volume increase in the fourth quarter. In addition, during 2012, we plan to embark on a rebranding effort at the center level. Most of our centers today operate under the name21st Century Oncology which is no longer reflective of our ICC model, our increased technological and clinical sophistication and our focus on providing a superior patient experience. As a result, we plan to commence the rebranding of the Company toSaviaCare to highlight our patient centric focus on the "wise path to care" and the broader platform of cancer services we now offer. As part of this effort, we are revamping our marketing materials, web site and clinical information to better introduce referral sources, patients and affiliated physicians to our philosophy of care and related clinical and technological offerings, all of which should contribute to continued census growth. In addition, we have been aggressively consolidating and renegotiating our payer contracts to improve the pricing and stability of the relationships with our commercial payers while also aligning objectives through innovative payment approaches. Our early efforts in several markets have yielded encouraging results, and we expect to expand this program to new markets in 2012.

We have also restructured our operations into eight domestic regions with separate directors all reporting to our new Chief Operating Officer. We have consolidated talent at these senior positions to provide a more experienced level of business leadership and provide greater visibility for improved results while also allowing us to streamline positions at the state and center level. Currently we believe that there is an opportunity to reduce operating expense by approximately $10 million in 2012 though improved physician contracting, purchasing and reduction in other operating expenses. In addition, greater integration between our operations team and our clinical and corporate development leadership has led to enhanced market opportunities. We are now better able to target attractive ICC opportunities to improve market dynamics as well as identify a number of centers for closure where the existing patient volume could be serviced with a smaller, lower cost configuration of centers. As a result in 2011 and the beginning of 2012, we entered into 21 new ICC practice relationships including a critical arrangement with approximately 250 affiliated accredited doctors in Michigan. We also closed nine centers, including five underperforming centers in Las Vegas, Maryland, Delaware and Pennsylvania. Going forward, we believe this dual operating and clinical structure will not only continue to help us focus on increasing operating leverage but also more quickly facilitate the rollout of the ICC model and penetration of advanced technology and treatment methods across our centers.

Continue to Lead in Clinical Excellence—For more than 20 years, we believe we have differentiated ourselves from other industry participants by proactively investing in a superior, research driven clinical and technological infrastructure that has advanced our clinical treatment capabilities. In 1989, we

11

founded and continue to run the only fully accredited privately owned radiation therapy and dosimetry schools in the country. In addition, we have an affiliated physics program with the University of Pennsylvania. As a result, we have recruited, trained, certified and retained many highly talented medical physicists, dosimetrists and radiation therapists. Further, we have consistently invested in industry leading and revolutionary technologies, through partnerships with renowned research institutes, proprietary experimental research entities and other for-profit businesses. An example of this partnership, is our selection as the developer and managing director of the first proton beam therapy center in New York in concert with academic institutions including Memorial Sloan-Kettering, NYU Langone, Mt. Sinai, Continuum and Montefiore medical centers. We have also, through our own research initiatives and resources, developed and implemented treatment technologies exclusive to the Company. For example, Gamma Function is an in-house developed software tool that we use to measure the quality of radiation therapy delivered to our patients. Our internal advanced development group, Aurora, is continuing to investigate and advance the field of radiation therapy through projects such as Gamma Function, proton beam therapy and adaptive radiotherapy as well as develop applications which can be licensed to other providers.

As a result of our history and reputation for clinical excellence, we are exploring more formalized initiatives to use the scale and depth of our unique technological and clinical resources to develop new lines of "value added services". To date, we have been able to commercialize our data to lead and support studies and programs measuring quality outcomes of various treatment protocols and are currently investigating opportunities with a number of providers to license and implement our technologies at their centers.

Expand Through Acquisitions—Acquisitions are an important part of our expansion plan, and we have invested in unique tools and a substantial infrastructure to capitalize on acquisition opportunities. We seek to target centers that have certificates of need (CON), provide entry into new markets with significant market share or shore up our existing markets and have opportunities to expand our ICC model. We seek to employ the leading radiation oncologists at these centers and meaningfully enhance the business through technology migration. The foundation of our acquisition strategy is the implementation of our proven operating model at each of our newly acquired treatment centers. This includes upgrading existing equipment and technologies where applicable, enhancing treatment mix, developing ICC relationships, introducing advanced therapies and services, providing clinical expertise and enabling our new physicians and patients to access our broad network of centers, contracts and resources. For example, our existing physicians and clinical experts are often able to educate the physicians at our acquired centers on the clinical benefits of using advanced technologies such as IMRT, IGRT and Gamma Function, thereby increasing the penetration of these services in the center's overall treatment mix and resulting in higher average revenue per treatment, increased census, increased profitability and improved patient care. We are currently considering a number of acquisition opportunities, some of which could be material.

Develop New Treatment Centers in Existing and New Markets—We plan to develop treatment centers to expand our existing local markets and selectively enter new local markets. As of March 31, 2012, we had two de novo treatment centers under development in the United States and three de novo treatment centers under development in Latin America. We have significant experience in the design and construction of radiation treatment centers, having internally developed 24 treatment centers since the beginning of 2003. In 2009, we opened de novo treatment centers in Hammonton, New Jersey; Indio, California; Fort Myers, Florida; Southbridge, Massachusetts; Providence, Rhode Island and Yucca Valley, California. In 2010, we opened de novo treatment centers in Pembroke Pines, Florida and Los Angeles, California. In 2011, we opened one de novo treatment center in Andalusia, Alabama. We evaluate potential expansion into new and existing local markets based on demographic characteristics, pre-existing or potential relationships with ICC physicians or hospitals, the competitive landscape and the payer and regulatory environments. Our newly developed treatment centers typically

12

achieve positive cash flow within six to fifteen months after opening, depending upon whether it is an existing or new market, and the use of third party leasing minimizes our up front capital requirements. We may also from time to time enter new local markets through strategic alliances and joint ventures.

Continue to Develop and Expand Our ICC Model—In select local markets, it may be advantageous to affiliate with physicians in medical specialties that are not primarily focused on radiation therapy, but are involved in the continuum of care for cancer patients. We may pursue these affiliations when opportunities arise to provide our patients with a more comprehensive treatment team to better target and treat tumors as well as coordinate in the provision of care. In these instances, we believe we can further strengthen both our clinical working relationships and our standing within the local medical community. We currently operate as an ICC practice in 14 markets and have affiliations with over 415 of such physicians in the field, including medical oncology, breast, gynecological, urological and general surgical oncology as well as primary care.

We also look for similar arrangements with hospitals where we can generate greater awareness of our services with patients in the local markets while capitalizing on census already in the market.

Seek Greater Alignment As Well As Pricing Stability Through Alternative Payment Structures —The Company, through its leadership in the development of the Radiation Therapy Alliance ("RTA"), an organization representing freestanding, for-profit radiation providers, has been at the forefront of discussions on payment reform in the radiation therapy space since the RTA's inception in 2009. In 2010, after working with a pre-eminent consulting firm, the RTA drafted a proposal on a prostate cancer bundle that was well received for its quality and cost metrics. On February 22, 2012, President Obama signed into law H.R. 3630, which mandated that the Department of Health and Human Services conduct a study examining, among other things, bundled payments for cancer services. This report is due to Congress by January 1, 2013. We believe we are well positioned as the government begins to innovate with payment reform due to our proactive discussions in this area.

In addition we have begun discussions on alternative payment structures and other contracting arrangements with key commercial payers. Our early initiatives in this area have yielded positive results in preferred provider arrangements and increased volume as well as in longer dated contracts. As a national provider of radiation therapy and other cancer services, we are uniquely positioned in these discussions with public and private payers and believe alignment with payers will be critical for long-term success in our markets.

Selectively Expand in Latin America—Outside of the United States we continue to look for opportunities to selectively expand our presence in Latin America by further developing existing markets and entering new markets through either de novo treatment centers, joint ventures or acquisitions. There are several markets outside of our current Latin America footprint, such as Brazil, Mexico, Bolivia and Uruguay, which have very attractive demographic, payer and competitive characteristics and we believe we are positioned to capitalize on opportunities in these markets. Our significant foothold in the regions in which we operate, positions us to take advantage of the growing pipeline of opportunities for further acquisitions. The Latin American radiation therapy market is largely under-developed and fragmented, with physicians frequently utilizing older generation equipment and technologies. In addition, there are significant opportunities to transport equipment, which is not being utilized in the United States, to our Latin American centers and thereby increase our overall equipment utilization. Our existing physicians and clinical experts are beginning to educate the physicians at our acquired centers on the clinical benefits of using advanced technologies such as IMRT, IGRT and Gamma Function, thereby increasing the penetration of these services in the center's overall treatment mix and resulting in higher average revenue per treatment, increased profitability and improved patient care.

13

Our Latin American leadership team has significant experience working in the Latin American markets, having grown our Latin American business from 21 to 30 centers from 2009 to the end of 2011. Most recently in November 2011, we acquired a five facility practice with operations in five cities in Argentina to further expand our presence in that market. We will continue to utilize our Latin American leadership team's market knowledge and relationships to selectively grow in the region.

Founded in 1988, Vestar is a leading global private equity firm specializing in management buyouts and growth capital investments. Vestar's investment in the Company was funded by Vestar Capital Partners V, L.P., a $3.7 billion fund which closed in 2005, and affiliates.

Since the firm's founding, Vestar has completed 69 investments in the United States and Europe in companies with total value of over $40 billion. These companies have varied in size and geography and span a broad range of industries including healthcare, an area in which Vestar's principals have had meaningful experience. The firm's strategy is to invest behind incumbent management teams, family owners or corporations in a creative, flexible and entrepreneurial way with the overriding goal of building long-term investment value.

Vestar currently manages funds totaling $8 billion and has offices in New York, Denver and Boston. See "Certain Relationships and Related Party Transactions," "Security Ownership of Certain Beneficial Owners and Management" and the documents referred to herein for more information with respect to our relationship with Vestar.

14

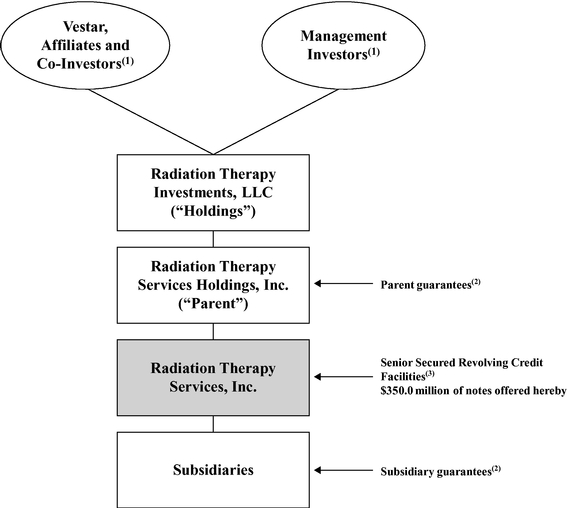

The following chart summarizes our organizational structure and our principal indebtedness.

15

On May 10, 2012, we sold, through a private placement exempt from the registration requirements of the Securities Act, $350,000,000 of our 87/8% Senior Secured Second Lien Notes due 2017, CUSIP No. 750323 AC1 and U7493A AB99, all of which are eligible to be exchanged for Exchange Notes. We refer to these notes as "Old Notes" in this prospectus.

Simultaneously with the private placement, we entered into the Registration Rights Agreement with the initial purchasers of the Old Notes. Under the Registration Rights Agreement, we are required to use our reasonable best efforts to cause a registration statement for substantially identical Notes, which will be issued in exchange for the Old Notes, to be filed with the United States Securities and Exchange Commission (the "SEC") and to complete the exchange offer within 365 days after the issue date of the Old Notes. We refer to the notes to be registered under this exchange offer registration statement as "Exchange Notes" and collectively with the Old Notes, we refer to them as the "notes" in this prospectus. You may exchange your Old Notes for Exchange Notes in this exchange offer. You should read the discussion under the headings "—Summary of Exchange Offer," "Exchange Offer" and "Description of Exchange Notes" for further information regarding the Exchange Notes.

Securities Offered | $350.0 million aggregate principal amount of 87/8% Senior Secured Second Lien Notes due 2017. | |

Exchange Offer | We are offering to exchange the Old Notes for a like principal amount at maturity of the Exchange Notes. Old Notes may be exchanged only in minimum principal denominations of $2,000 and integral principal multiples of $1,000 thereafter. The exchange offer is being made pursuant to the Registration Rights Agreement which grants holders of the Old Notes certain exchange and registration rights. This exchange offer is intended to satisfy those exchange and registration rights with respect to the Old Notes. After the exchange offer is complete, you will no longer be entitled to any exchange or registration rights with respect to your Old Notes. | |

Expiration Date; Withdrawal of Tender | The exchange offer will expire 5:00 p.m., New York City time, on July 20, 2012, or a later time if we choose to extend this exchange offer in our sole and absolute discretion. You may withdraw your tender of Old Notes at any time prior to the expiration date. All outstanding Old Notes that are validly tendered and not validly withdrawn will be exchanged. Any Old Notes not accepted by us for exchange for any reason will be returned to you at our expense as promptly as possible after the expiration or termination of the exchange offer. | |

Resales | We believe that you can offer for resale, resell and otherwise transfer the Exchange Notes without complying with the registration and prospectus delivery requirements of the Securities Act so long as: | |

• you acquire the Exchange Notes in the ordinary course of business; |

16

• you are not participating, do not intend to participate, and have no arrangement or understanding with any person to participate, in the distribution of the Exchange Notes; | ||

• you are not an "affiliate" of ours, as defined in Rule 405 of the Securities Act; and | ||

• you are not a broker-dealer. | ||

If any of these conditions is not satisfied and you transfer any Exchange Notes without delivering a proper prospectus or without qualifying for a registration exemption, you may incur liability under the Securities Act. We do not assume, or indemnify you against, any such liability. | ||

Each broker-dealer acquiring Exchange Notes issued for its own account in exchange for Old Notes, which it acquired through market-making activities or other trading activities, must acknowledge that it will deliver a proper prospectus when any Exchange Notes issued in the exchange offer are transferred. A broker-dealer may use this prospectus for an offer to resell, a resale or other retransfer of the Exchange Notes issued in the exchange offer. | ||

Conditions to the Exchange Offer | Our obligation to accept for exchange, or to issue the Exchange Notes in exchange for, any Old Notes is subject to certain customary conditions, including our determination that the exchange offer does not violate any law, statute, rule, regulation or interpretation by the Staff of the SEC or any regulatory authority or other foreign, federal, state or local government agency or court of competent jurisdiction, some of which may be waived by us. We currently expect that each of the conditions will be satisfied and that no waivers will be necessary. See "Exchange Offer—Conditions to the Exchange Offer. | |

Procedures for Tendering Old Notes held in the Form of Book-Entry Interests | The Old Notes were issued as global securities and were deposited upon issuance with Wilmington Trust, National Association, which represent a 100% interest in those Old Notes, to The Depositary Trust Company ("DTC"). | |

Beneficial interests in the outstanding Old Notes, which are held by direct or indirect participants in DTC, are shown on, and transfers of the Old Notes can only be made through, records maintained in book-entry form by DTC. |

17

You may tender your outstanding Old Notes by instructing your broker or bank where you keep the Old Notes to tender them for you. In some cases you may be asked to submit the letter of transmittal that may accompany this prospectus. By tendering your Old Notes you will be deemed to have acknowledged and agreed to be bound by the terms set forth under "Exchange Offer." Your outstanding Old Notes must be tendered in minimum denominations of $2,000 and multiples of $1,000 thereafter. | ||

In order for your tender to be considered valid, the exchange agent must receive a confirmation of book-entry transfer of your outstanding Old Notes into the exchange agent's account at DTC, under the procedure described in this prospectus under the heading "Exchange Offer," on or before 5:00 p.m., New York City time, on the expiration date of the exchange offer. | ||

United States Federal Income Tax Considerations | The exchange offer should not result in any income, gain or loss to the holders of Old Notes or to us for United States federal income tax purposes. See "Certain United States Federal Income Tax Considerations." | |

Use of Proceeds | We will not receive any proceeds from the issuance of the Exchange Notes in the exchange offer. | |

Exchange Agent | Wilmington Trust, National Association is serving as the exchange agent for the exchange offer. | |

Shelf Registration Statement | In limited circumstances, holders of Old Notes may require us to register their Old Notes under a shelf registration statement. |

Consequences of Not Exchanging Old Notes

If you do not exchange your Old Notes in the exchange offer, your Old Notes will continue to be subject to the restrictions on transfer currently applicable to the Old Notes. In general, you may offer or sell your Old Notes only:

We do not currently intend to register the Old Notes under the Securities Act. Under some circumstances, however, holders of the Old Notes, including holders who are not permitted to participate in the exchange offer or who may not freely resell Exchange Notes received in the exchange offer, may require us to file, and to cause to become effective, a shelf registration statement covering resales of Old Notes by these holders. For more information regarding the consequences of not tendering your Old Notes and our obligation to file a shelf registration statement, see "Exchange Offer—Consequences of Exchanging or Failing to Exchange Old Notes" and "Description of Exchange Notes—Registration Rights."

18

Issuer | Radiation Therapy Services, Inc., a Florida corporation. | |

Notes Offered | $350.0 million aggregate principal amount of 87/8% Senior Secured Second Lien Notes due 2017. | |

Maturity Date | The Exchange Notes will mature on January 15, 2017. | |

Interest Payment Dates | May 15 and November 15, beginning on November 15, 2012. | |

Guarantees | The Exchange Notes will be guaranteed, subject to certain limitations described herein, on a second lien senior secured basis by Parent and each of our existing and future direct and indirect domestic subsidiaries that is a guarantor under our senior secured revolving credit facility. If we fail to make payments on the Exchange Notes, our guarantors must make them instead. | |

Ranking | The Exchange Notes will be our second lien senior secured obligations and will: | |

• rank equally in right of payment to our existing and future senior indebtedness, including our senior secured revolving credit facility; | ||

• be effectively junior to our indebtedness that is either | ||

(i) secured by senior priority liens on the collateral, including our senior secured revolving credit facility or | ||

(ii) secured by assets that are not part of the collateral securing the Exchange Notes, to the extent of the value of such collateral; | ||

• be effectively senior to our senior unsecured indebtedness to the extent of the value of the collateral securing the Exchange Notes, after giving effect to first priority liens on the collateral and certain permitted liens; and | ||

• rank senior in right of payment to all of our existing and future indebtedness and other obligations that are, by their terms, expressly subordinated in right of payment to the Exchange Notes, including our senior subordinated indebtedness. | ||

Similarly, the Exchange Notes guarantees will be second lien senior secured obligations of the guarantors and will: | ||

• rank equally in right of payment to all of the applicable guarantor's existing and future senior indebtedness, including such guarantor's guarantee under our senior secured revolving credit facility; |

19

• be effectively junior to all indebtedness of the applicable guarantor that is either (i) secured by senior priority liens on the collateral, including our senior secured revolving credit facility or (ii) secured by assets that are not part of the collateral securing the Exchange Notes, to the extent of the value of such collateral; | ||

• be effectively senior to all of the applicable guarantor's senior unsecured indebtedness to the extent of the value of the collateral securing the Exchange Notes, after giving effect to first priority liens on the collateral and certain permitted liens; and | ||

• rank senior in right of payment to all of the applicable guarantor's existing and future subordinated indebtedness and other obligations that are, by their terms, expressly subordinated in right of payment to the Exchange Notes, including such guarantor's guarantee under our senior subordinated indebtedness. | ||

As of December 31, 2011, after giving effect to the completion of this offering and the application of the proceeds therefrom as described under "Use of Proceeds", (1) the Exchange Notes and related guarantees would have ranked junior to our approximately $30.6 million of senior secured indebtedness, and (2) we would have had an additional up to $140 million of unutilized capacity under our new secured revolving credit facility (excluding issued but undrawn letters of credit). | ||

Collateral | The Exchange Notes and the related guarantees will be secured by a second priority lien on substantially all of our and each guarantor's assets (whether now owned or hereafter acquired) that secure our and the guarantors' obligations under our senior secured revolving credit facility, subject to certain exceptions and permitted liens. These liens will be junior in priority to the liens on the same collateral that secure our senior secured revolving credit facility (and permitted replacements thereof) and to certain other permitted liens. The liens securing first priority lien obligations will be held by the collateral agent under our senior secured revolving credit facility. For more details, see "Description of Exchange Notes—Security". |

20

The value of collateral at any time will depend on market and other economic conditions, including the availability of suitable buyers for the collateral. The liens on the collateral may be released without the consent of the holders of the Exchange Notes if collateral is disposed of in a transaction that complies with the indenture governing the notes and the related security documents or the intercreditor agreement to be entered into relating to the collateral securing the notes and the senior secured revolving credit facility. See "Risk Factors—The value of the collateral is uncertain, and may not be sufficient to pay all or any of the notes" and "Description of Exchange Notes—Security". | ||

Intercreditor Agreement | The trustee and the collateral agent under the indenture governing the notes and the collateral agent under our senior secured revolving credit facility have entered into an intercreditor agreement as to the relative priorities of their respective security interests in our assets securing the notes and borrowings under our senior secured revolving credit facility and certain other matters relating to the administration of such security interests. Certain terms of the intercreditor agreement are described under "Description of Exchange Notes—Security—Intercreditor Agreement". | |

Optional Redemption | We may redeem some or all of the Exchange Notes at any time on or after May 15, 2014, at the redemption prices set forth under "Description of Notes—Redemption—Optional Redemption" plus accrued interest on the Exchange Notes to the date of redemption. | |

At any time prior to May 15, 2014, we may redeem the Exchange Notes, in whole or in part, at a redemption price equal to 100% of the principal amount of the Exchange Notes redeemed, plus accrued and unpaid interest to the redemption date and a "make-whole" premium. See "Description of Exchange Notes—Redemption—Optional Redemption". | ||

In addition, we may redeem up to 35% of the original principal amount of the Exchange Notes using the new cash proceeds of certain equity offerings completed on or before May 15, 2014. See "Description of Exchange Notes—Redemption—Optional Redemption". | ||

Change of Control | Upon the occurrence of a change of control, you will have the right, as holders of the Exchange Notes, to require us to repurchase some or all of your Exchange Notes at 101% of their face amount, plus accrued and unpaid interest to the repurchase date. See "Description of Exchange Notes—Change of Control". |

21

Certain Covenants | The indenture governing the Exchange Notes will contain covenants limiting our ability and the ability of our restricted subsidiaries to: | |

• incur additional debt or issue preferred shares; | ||

• pay dividends on or make distributions in respect of our equity interest or make other restricted payments; | ||

• sell certain assets; | ||

• create liens on certain assets to secure debt; | ||

• consolidate, merge, sell or otherwise dispose of all or substantially all of our assets; | ||

• enter into certain transactions with our affiliates; and | ||

• designate our subsidiaries as unrestricted subsidiaries. | ||

These covenants are subject to a number of important limitations and exceptions. See "Description of Exchange Notes—Certain Covenants". | ||

No Public Market | The Exchange Notes will be new securities for which there is currently no market. We do not intend to apply for the Exchange Notes to be listed on any securities exchange or included in any automated quotation system. | |

Use of Proceeds | We will not receive any proceeds from the issuance of the Exchange Notes pursuant to the exchange offer. | |

Risk Factors | See "Risk Factors" for a discussion of factors you should consider carefully before deciding to invest in any of the Exchange Notes. |

Our principal executive offices are located at 2270 Colonial Boulevard, Fort Myers, Florida 33907 and our telephone number is (239) 931-7275. Our website can be found on the Internet at www.rtsx.com. Information on our website is not deemed to be a part of this prospectus.

22

SUMMARY HISTORICAL CONSOLIDATED FINANCIAL AND OTHER DATA