Subject to completion, dated March 24, 2017

Preliminary Offering Circular

Our MicroLending, LLC

Up to $10,000,000

Unsecured Investment Certificates

With Maturities of 6 to 24 Months from the Date Issued

This Offering Circular relates to the offer and sale of up to $10,000,000 in principal amount (the “Offering”) of unsecured fixed-rate investment certificates (the “Certificates”) of OUR MicroLending, LLC, a Florida limited liability company (the “Company”). The Certificates are not equity securities but are unsecured debt securities. The Certificates are not savings accounts or deposits and not insured by the Federal Deposit Insurance Corporation or any other government agency. The Company’s principal office is located at 3191 Coral Way, Suite 109, Miami, Florida 33145 and its telephone number is (305) 854-8113.

The Certificates will be issued in the minimum amount of $1,000 and in multiples of $100 for any amount greater than $1,000. The Certificates will be offered in maturities of 6 to 24 months from the date issued, with a fixed interest rate depending on the term. The Company will typically issue Certificates on the same or next day, after deposit by the Company of the subscriber’s payment check and the check is collected by the Company’s bank. See “Description of Certificates” p. 20. The interest rate for each Certificate will be based on the formula set forth below and varies according to the term of the Certificate. See “Description of Certificates - Principal, maturity and interest” p. 21. The minimum and the maximum fixed interest rates that are offered will change from time to time in response to changes in the current Constant Maturity Treasury Bill Monthly Average Yield (the “T Bill”) yield data obtained from the Federal Reserve Board, or a similar credible source. The interest rates for new Certificates are set on the first Monday of each month at the start of business based on the T Bill yields that day. Such rates are paid on all Certificates issued between the start of business on that Monday and the close of business on the last day prior to the first Monday of the next month. The following table sets forth the formula for determining the interest rates for the Certificates and the initial interest rate based on the most recent T Bill yields as of March 6, 2017:

| Term | | T Bill Yield | | Interest Rate as of March 6, 2017 |

| 6 Months | | 6 Months T Bill plus 5% | | 5.84% |

| 12 Months | | 1 Year T Bill plus 6.25% | | 7.23% |

| 18 Months | | 1 Year T Bill plus 7.75% | | 8.73% |

| 24 Months | | 2 Year T Bill plus 9.00% | | 10.32% |

The initial interest rates set forth above will be effective only for Certificates issued between March 6, 2017 and April 3, 2017. The interest rates fluctuate based on the formula set forth above, and to determine the current rates, prospective investors in the Certificates should call the Company at (305) 854-8113, or consult the web pagewww.ourmicrolending.com.

We may prepay some or all of the Certificates at any time prior to their maturity without premium or penalty.

We will pay interest on Certificates quarterly, semi-annually or at maturity, at the holder’s option. All Certificates will be issued in fully registered form.

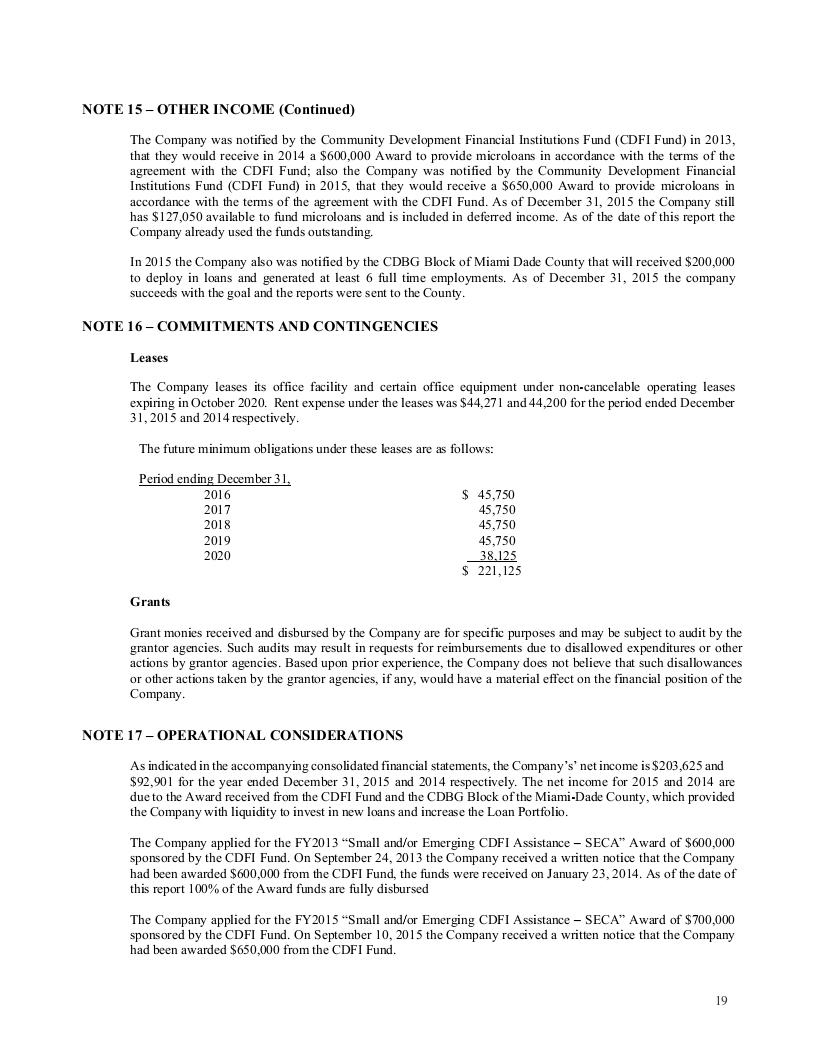

The Certificates will be subject to automatic rollover. Fifteen business days before the maturity date of the Certificate, the Company will contact the holder telephonically and send a notice to the holder by first class mail at the holder’s address that the Certificate is going to mature and request whether the holder wishes to let the Certificate rollover, or to be repaid. The Company will repay holders who notify it ten business days before the maturity date that they wish to be repaid. Unless the holder notifies the Company ten business days before the maturity date that it does not wish to let the Certificate rollover and presents the Certificate for payment, or the Company otherwise elects to repay the Certificate, the Certificate will be automatically rolled-over into a new Certificate at the interest rate then being offered by the Company based on the same term as the original Certificate. The holder may elect to roll-over all, or a portion of, the Certificates it owns. To determine the interest rate applicable to the rolled-over Certificate, holders should call the Company at (305) 854-8113, or consult the web pagewww.ourmicrolending.com. The rolled-over Certificate will bear interest at the then current interest rate for newly issued Certificates, based on the formula described above, the maturity date will be extended for an additional term of identical length as the original Certificate, and the frequency of interest payments will be identical to the frequency of the original Certificate.

Due to automatic rollover, investors will not receive payment of principal at maturity or subsequent payment dates unless the investor complies with the procedures for notification and delivery of Certificates. See “Payment or Rollover at Maturity” p. 22.

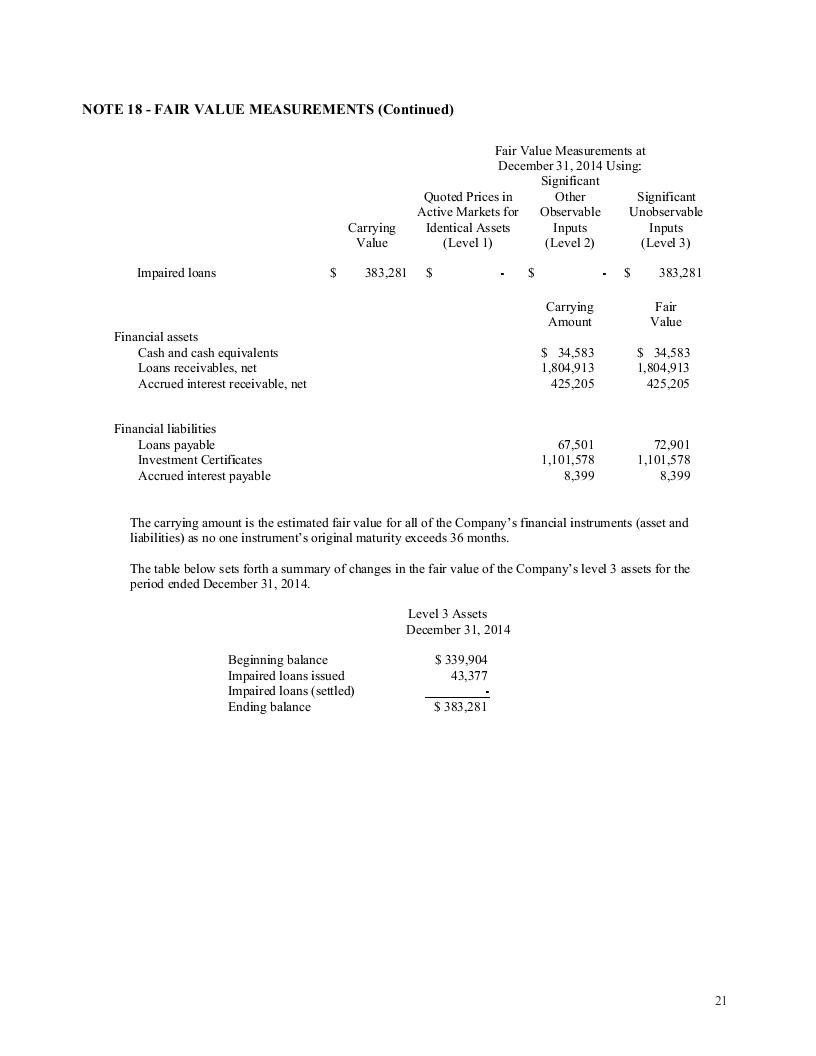

The Company is offering the Certificates directly to investors through its officers on an ongoing and continuous basis. The Certificates will be issued at their principal face value, without a discount, and are not being sold through commissioned sales agents or underwriters. See “Plan of Distribution” p. 23.

The Certificates are being offered, and will be sold, pursuant to the exemption from registration provided by Section 3(b) of the Securities Act of 1933, as amended (the “Act”), and Regulation A promulgated thereunder. The Offering is not contingent upon sales of a minimum offering amount and there is no minimum aggregate amount of Certificates that must be sold in order for us to have access to the Offering proceeds. We may accept subscriptions as they are received. The Offering will terminate upon the earlier to occur of (i) the date that is not more than one year after this Offering Circular is qualified by the Securities and Exchange Commission (the “Commission”), and (ii) the date on which $10,000,000 of Certificates qualified hereunder have been sold.

The Certificates will not be listed on any exchange or quoted on any automated dealer quotation system. Currently, there is no public market for the Certificates.

This Offering Circular shall not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sales of these securities in any state in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the laws of any such state.

INVESTMENT IN SMALL BUSINESSES INVOLVES A HIGH DEGREE OF RISK, AND INVESTORS SHOULD NOT INVEST ANY FUNDS IN THIS OFFERING UNLESS THEY CAN AFFORD TO LOSE THEIR ENTIRE INVESTMENT. YOU SHOULD CAREFULLY CONSIDER THE RISK FACTORS ON PAGE 3 BEFORE MAKING AN INVESTMENT IN THIS OFFERING.

This offering is under Tier 2 of Regulation A, and therefore not subject to the securities regulations of the various states. Generally, no sale may be made to you in this offering if the aggregate purchase price you pay is more than 10% of the greater of your annual income or net worth. Different rules apply to accredited investors and non-natural persons. Before making any representation that your investment does not exceed applicable thresholds, we encourage you to review Rule 251(d)(2)(i)(C) of Regulation A. For general information on investing, we encourage you to refer to www.investor.gov.

THE COMMISSION DOES NOT PASS UPON THE MERITS OF OR GIVE ITS APPROVAL TO ANY SECURITIES OFFERED OR THE TERMS OF THE OFFERING, NOR DOES IT PASS UPON THE ACCURACY OR COMPLETENESS OF ANY OFFERING CIRCULAR OR OTHER SELLING LITERATURE. THESE SECURITIES ARE OFFERED PURSUANT TO AN EXEMPTION FROM REGISTRATION WITH THE COMMISSION; HOWEVER, THE COMMISSION HAS NOT MADE AN INDEPENDENT DETERMINATION THAT THE SECURITIES OFFERED HEREUNDER ARE EXEMPT FROM REGISTRATION.

| | | Price to Public | | | Underwriting Discounts and commissions | | | Proceeds to Issuer | |

| Per Certificate | | $ | 1,000 | | | $ | 0 | | | $ | 1,000 | |

| Minimum Offering | | | No Minimum | | | $ | 0 | | | | No Minimum | |

| Maximum Offering | | $ | 10,000,000 | | | $ | 0 | | | $ | 10,000,000 | |

The Company is paying directly for the costs of the Offering, which are estimated to be approximately $50,000 and no portion of the proceeds from the Offering will be used for this purpose.

The approximate date of commencement of the proposed sale of Certificates to the public is as soon as practicable after this Offering Circular has been qualified by the Commission.

TABLE OF CONTENTS

THIS OFFERING CIRCULAR CONTAINS ALL OF THE REPRESENTATIONS BY THE COMPANY CONCERNING THIS OFFERING, AND NO PERSON SHALL MAKE DIFFERENT OR BROADER STATEMENTS THAN THOSE CONTAINED HEREIN. INVESTORS ARE CAUTIONED NOT TO RELY UPON ANY INFORMATION NOT EXPRESSLY SET FORTH IN THIS OFFERING CIRCULAR.

This offering is under Tier 2 of Regulation A, and therefore not subject to the securities regulations of the various states. Generally, no sale may be made to you in this offering if the aggregate purchase price you pay is more than 10% of the greater of your annual income or net worth. Different rules apply to accredited investors and non-natural persons. Before making any representation that your investment does not exceed applicable thresholds, we encourage you to review Rule 251(d)(2)(i)(C) of Regulation A. For general information on investing, we encourage you to refer to www.investor.gov.

This Offering Circular, together with the audited and interim financial statements, consists of a total of 66 pages.

OFFERING CIRCULAR SUMMARY

This summary highlights information contained elsewhere in this Offering Circular. It does not contain all of the information you should consider before purchasing our Certificates. Therefore, you should read the Offering Circular in its entirety, including the risk factors and the financial statements and related footnotes appearing elsewhere in this Offering Circular. References to “we,” “us,” “our,” or “the Company” generally refer to OUR MicroLending, LLC, a Florida limited liability company.

Our Company

On October 9, 2007, we were formed as a Florida limited liability company. From March 2008 through September 30, 2016, we have made approximately 2,045 microloans totaling more than $17,087,180 to micro and small business owners and entrepreneurs in South Florida, many of whom are immigrants and minorities. Typically, we target businesses with fewer than five employees and annual sales of $100,000 or less, and the size of our loans range between $1,500 and $50,000. The business owners applying for financing must be legal residents or citizens of the United States and their business and home addresses must be located within the South Florida target market which includes Miami-Dade, Broward and Palm Beach Counties. Our clients may be corporations, partnerships or sole proprietorships and their business must have been in actual operation for at least 24 months. Traditional sources of financing (i.e., bank or credit union loans) are largely unavailable to our target clients, and the economic downturn made borrowing even more difficult for small businesses. The major challenges of our clients in our target markets are the following: (1) local banks are not lending at the levels that they were at before the recession, and their current underwriting guidelines such as liquidity, liabilities, activity and income ratios are too strict for our target market; (2) local competitors have moved to a credit scoring model and many micro-entrepreneurs no longer qualify under their programs; (3) most borrowers in our target market operate on a cash-only basis and lack formal or regular financial statements of any kind (e.g. small grocery stores, beauty salons, house cleaning and landscaping businesses, dollar stores); and (4) many of our target market clients are home-based or in industries that are restricted for many of our local financing institutions. As a result, we find ourselves in an excellent position to increase our share of the South Florida microfinance market.

As a limited liability company we operate pursuant to an operating agreement, and our owners hold equity interests in the Company. Pursuant to our articles of organization and operating agreement, we are managed by our Managing Member, Emilio Santandreu, who is also our President and Chief Executive Officer, and additional officers appointed by our President. To date, we have funded our lending operations using the capital contributions of our owners and borrowings from our officers, family members of our officers and certain of our equity investors and proceeds from the sale of $2,629103 in principal amount of Certificates from previous Regulation A Offerings.

Our principal office is located at 3191 Coral Way, Suite 109, Miami, Florida 33145 and our telephone number is (305) 854-8113. For additional information regarding the Company or this Offering, you may write or telephone us at the address and telephone number above.

The Offering

The following provides a summary of the material terms of the offering. For a more complete understanding of the Certificates, please refer to the section of this Offering Circular entitled “Description of Certificates” p. 20.

| Issuer | OUR MicroLending, LLC, a Florida limited liability company. |

| | |

| Offering period | The Offering period will begin when this Offering is qualified by the Commission and will terminate on the earlier to occur of (i) the date that is not more than one year after this Offering Circular is qualified by the Commission, and (ii) the date on which $10,000,000 of Certificates qualified hereunder have been sold. The Certificates are being offered on an ongoing and continuous basis. |

| | |

| Securities offered | $10,000,000 in aggregate principal amount of unsecured fixed-rate Certificates. The Certificates are not equity securities but are unsecured debt securities. The Certificates are not savings accounts or deposits and not insured by the Federal Deposit Insurance Corporation or any other government agency. |

| | |

| Interest Rate | The interest rate for each Certificate will be based on the formula set forth in this Offering Circular and varies according to the term of the Certificate. The minimum and the maximum fixed interest rates that are offered will change from time to time in response to changes in the current T Bill yield data obtained from the Federal Reserve Board, or a similar credible source. The interest rates for new Certificates are set on the first Monday of each month at the start of business based on the T Bill yields that day. Such rates are paid on all Certificates issued between the start of business on that Monday and the close of business on the last day prior to the first Monday of the next month. Interest is calculated and accrues daily. To determine the current rates, prospective investors in the Certificates should call the Company at (305) 854-8113, or consult the web pagewww.ourmicrolending.com. |

| | |

| Maturity date | The Certificates will be offered in maturities of 6 to 24 months from the date issued, with a fixed interest rate depending on the term. |

| | |

| Rollover at maturity | When a Certificate matures, unless the holder notifies the Company ten (10) business days before the maturity date that it does not wish to let the Certificate rollover and presents the Certificate for payment, or the Company otherwise elects, it is automatically rolled-over into a new Certificate at the interest rate then being offered by the Company. The rolled-over Certificate will bear interest at the then current interest rate for newly issued Certificates, based on the same term as originally elected by the holder. |

| | |

| Interest payment dates | We will pay interest on Certificates quarterly, semi-annually or at maturity, at the holder’s option. |

| | |

| Guarantees | The Certificates will not be guaranteed. |

| | |

| Ranking | The Certificates will be our unsecured obligations and will: |

| | ● | rank equally with all of our existing and future unsecured indebtedness; |

| | | |

| | ● | rank senior to all of our future subordinated indebtedness, if any; |

| | | |

| | ● | be effectively subordinated to all of our and our subsidiaries’ existing and future secured obligations to the extent of the value of the assets securing such obligations; and |

| | | |

| | ● | be effectively subordinated to all existing and future indebtedness and other liabilities of our subsidiaries. |

| Optional Prepayment | We may prepay some or all of the Certificates at our option without premium or penalty. |

| | |

| Use of Proceeds | The net proceeds from this Offering will be used to fund additional microloans. |

| | |

| Risk Factors | See “Risk Factors” for a discussion of certain factors that you should carefully consider before investing in the Certificates. |

| | |

Governing law | Florida |

RISK FACTORS

An investment in our Certificates involves a high degree of risk. The following summarizes the principal factors which make the offering one of high risk or speculative. You should carefully consider each of the following risk factors and all other information set forth in this Offering Circular, including the risks and uncertainties described below, before making an investment in our Certificates.

Risks Relating to our Business

Our limited operating history and our fast growing and rapidly evolving business make it difficult to evaluate our business and future operating results on the basis of our past performance, and our future results may not meet or exceed our past performance.

We were incorporated in 2007 as a limited liability company in Florida and made our first loan in March 2008. As a result of our limited operating history, there is limited historical financial and operating information available to help prospective investors evaluate our past performance with respect to making an investment in our Certificates. Our business is growing and the results and amounts set forth in our financial statements beginning on p. 31 of this Offering Circular may not provide a reliable indication of our future performance. Accordingly, you should evaluate our business and prospects in light of the risks, uncertainties and difficulties frequently encountered by high growth companies in the early stages of development. Our failure to address these risks and uncertainties successfully could adversely affect our business and operating results.

We have experienced operating losses and our liquidity has been reduced, and we could incur losses in the future.

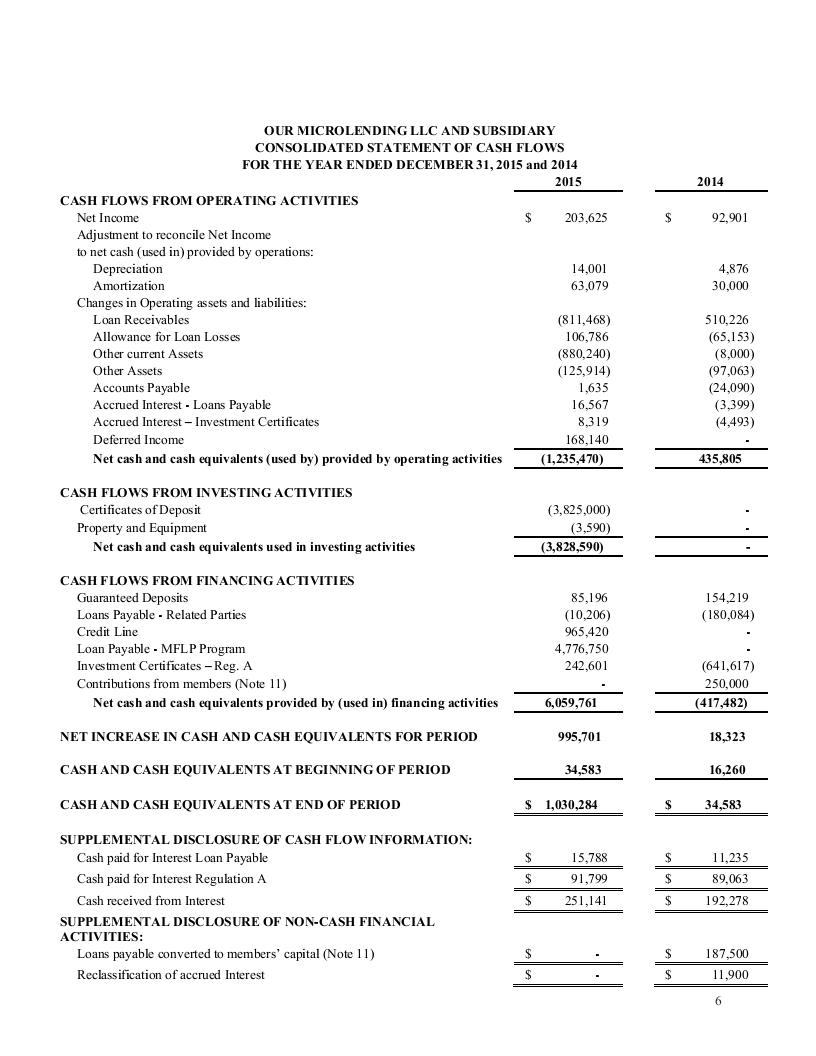

We had net loss of $(6,835) for the nine months ended September 30, 2016, a net income of $203,625 for the year ended December 31, 2015 and an accumulated deficit of $3,382,143 as of September 30, 2016. The majority of that amount was attributable to the downturn in market conditions in the credit industry in Florida and our inability to obtain necessary funding to satisfy the growing demand for microfinance during the economic downturn. Until we can increase our loan portfolio, we expect to continue to incur losses in the future. See “Business-Profitability” on p. 18 and Note 17—”Operational Considerations” to our audited 2015 and 2014 financial statements included in this Offering Circular for a description of how the Company is implementing a corrective action plan to improve profitability. We could incur losses in the future.

If we cannot secure the additional capital we need to fund our operations on acceptable terms or at all, our business will suffer.

Our business requires significant capital to grow. During the nine months ended September 30, 2016 and the year ended December 31, 2015, we funded our net cash used in operating activities of $(1,573,299) and $(1,235,470), respectively, with contributions from our equity owners and short-term loans provided by our officers, family members of our officers and certain of our equity investors and selling of Certificates from a previous Regulation A offering. See “Business−Profitability” on p. 18 and Note 11 and 12 of the 2015 and 2014 financial statements included in this Offering Circular for a description of how these persons have made contributions to fund operations. As of December 31, 2015 and 2014, we had $57,295 and $67,501 outstanding loans payable to related parties respectively and we had sold $2,634,966 principal amount of Certificates as of December 31, 2015. Expanding our geographic footprint will have an impact on our long-term capital requirements, which are expected to increase significantly. Our ability to obtain additional capital is subject to a variety of uncertainties, including our future financial position, the continued success of our core loan products, our results of operations and cash flows, any necessary government regulatory approvals, contractual consents, general market conditions for capital raising activities, and economic, political and other conditions in Florida and elsewhere. In addition, adverse developments in the United States credit markets may significantly increase our debt service costs and the overall costs of our borrowings. We may not be able to secure timely additional financing on favorable terms, or at all. The terms of any additional financing may place limits on our financial and operating flexibility. If we are unable to obtain adequate financing or financing on terms satisfactory to us, if and when we require it, our ability to grow or support our business and to respond to business challenges could be limited and our business prospects, financial condition and results of operations would be materially and adversely affected.

If we are unable to control the level of non-performing loans in the future, our collection activities are ineffective, or if our Allowance for loan losses are insufficient to cover future loan losses, our financial condition and results of operations may be materially and adversely affected.

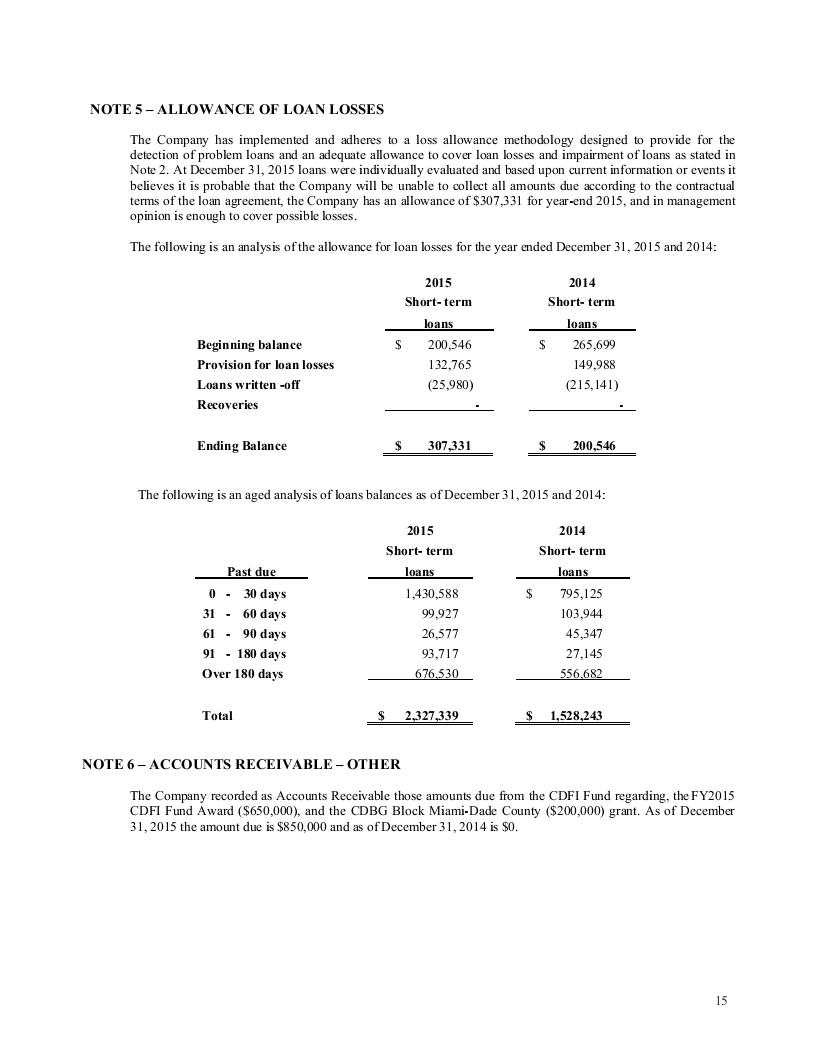

As of September 30, 2016, the aggregate principal balance of loans was $4,082,428, of which $695,100 was more than 180 days past due (17.03% of our loans outstanding); on December 31, 2015, the aggregate principal balance of loans was $2,327,339, of which $676,530 was more that 180 days past due (29.07% of our loans outstanding); on December 31, 2014, the aggregate principal balance of loans was $1,528,243, of which $556,682 was more than 180 days past due (36.43% of our loans outstanding). Non-performing or low credit quality loans can negatively impact our results of operations. See “Business-Defaults; Collection Activities” on p. 15 and Note 2 to our financial statements included in this Offering Circular for a description or our accounting policy regarding how we determine the provision for loan losses as well as our write-off policies for non-performing loans. We cannot assure you that we will be able to effectively control and reduce the level of the impaired loans in our total loan portfolio. The amount of our reported non-performing loans may increase in the future as a result of growth in our total loan portfolio, and also due to factors beyond our control, such as over-extended borrower credit that we are unaware of. If we are unable to manage our non-performing loans or adequately recover our loans, our results of operations will be adversely affected. Monthly, we also review the loans which are more than 180 days past due to determine if it is necessary to make a specific reserve for such loan. As of September 30, 2016, the allowance for loan losses was $307,331 (44.21% of our loans outstanding over 180 days past due); on December 31, 2015, the allowance for loan losses was $307,331 (45.43% of our loans outstanding over 180 days past due); on December 31, 2014, the allowance for loan losses was $200,546 (36.03% of our loans outstanding over 180 days past due).

We institute debt collection actions against defaulting clients in an attempt to mitigate the losses associated with non-performing loans. See “Business-Defaults; Collection Activities” on p. 15. In many cases, the purpose of the debt collection action is to obtain a judgment permitting foreclosure on the defaulting client’s collateral, or to obtain the collateral from the client in a privately negotiated transaction. In either case, the costs or expenses of collection, including attorneys’ fees, and selling the collateral may greatly exceed the amount of the non-performing loan. Our inability to collect against non-performing loans in a cost-effective manner could have a material adverse effect on our financial condition and results of operations.

Our current Allowance for loan losses may not be adequate to cover an increase in the amount of non-performing loans or any future deterioration in the overall credit quality of our total loan portfolio. If the quality of our total loan portfolio significantly deteriorates, we may be required to increase our allowance for loan losses, which will adversely affect our financial condition and results of operations. Our borrowers might be vulnerable if economic conditions worsen or growth rates decelerate in the United States. Moreover, there is no precise method for predicting loan and credit losses, and we cannot assure you that our monitoring and risk management procedures will effectively predict such losses or that allowance for loan losses will be sufficient to cover actual losses. If we are unable to control or reduce the level of our non-performing or poor credit quality loans, our financial condition and results of our operations could be materially and adversely affected. See “Business-Defaults; Collection Activities” on p. 15 and Note 2 to our financial statements included in this Offering Circular for a description or our accounting policy regarding how we determine the provision for loan losses as well as our write-off policies for non-performing loans.

We are not subject to regulation of any State or Federal regulatory agency.

We are not regulated or subject to the periodic examination to which commercial banks, savings banks and other thrift institutions are subject. Consequently, our loan decisions and our decisions regarding establishing allowance for loan losses are not subject to periodic review by any governmental agency. Moreover, we are not subject to regulatory oversight relating to our capital, asset quality, management or compliance with laws.

The amount of interest we may charge customers is capped by applicable law.

Our loans are subject to applicable usury laws that limit the amount of interest that we may charge our customers. The maximum interest rate permitted in Florida on the types of loans that we make and expect to make is 18% per annum. If a court were to determine that we willfully violated the usury statute, affected borrowers would be entitled to certain remedies, including forfeiture by us of double the interest charged on such loans. We do not believe that any of our existing loans currently exceed the maximum permitted rate.

A review of some of our loan transactions made in 2010 (i.e., loans already paid or otherwise written off) indicates that we may have unintentionally exceeded the maximum permitted rate. In 2010, we reimbursed the 66 affected borrowers with an aggregate reimbursement of $2,429, which is not material to our financial condition or results of operations. We subsequently adjusted our loan parameters to ensure that we do not exceed the maximum permitted rate in the future.

Usury laws limit the amount of interest we can charge on our loans, and to the extent interest rates on our borrowings increase, our financial condition and results of operations may be materially and adversely affected.

Our business depends on interest income from our loan portfolio. However, usury laws limit the amount of interest we can charge on our loans. When interest rates rise, we must pay higher interest on our borrowings while interest earned on our loans does not rise because our loans are capped at the maximum allowable interest rate. To the extent we are unable to increase the interest rate on our loans; increases in interest rates on our borrowings may materially and adversely affect our financial condition and results of operations.

If we are not able to attract, motivate, integrate or retain qualified personnel at levels of experience that are necessary to maintain our quality and reputation, it will be difficult for us to manage our business and growth.

We depend on the services of our executive officers and loan specialists for our continued operations and growth. In particular, our senior management has significant experience in the microfinance, banking and financial services industries. The loss of any of our executive officers or certain loan specialists could negatively affect our ability to execute our business strategy, including our ability to manage our rapid growth. Our business is dependent on our team of loan specialists who directly manage our relationships with our clients. Our business and profits would suffer adversely if a substantial number of our loan specialists left us or became ineffective in servicing our clients over a period of time. Our future success will depend in large part on our ability to identify, attract and retain highly skilled managerial and other personnel. Competition for individuals with such specialized knowledge and experience is intense in our industry, and we may be unable to attract, motivate, integrate or retain qualified personnel at levels of experience that are necessary to maintain our quality and reputation or to sustain or expand our operations. The loss of the services of such personnel or the inability to identify, attract and retain qualified personnel in the future would make it difficult for us to manage our business and growth and to meet key objectives.

Certain of our existing owners, including Mr. Santandreu our CEO, President and Managing Member, together may be able to exert substantial voting control over us, which may cause us to take actions that are not in our best interest.

Our ten largest owners beneficially own, in the aggregate, approximately 83.46% of our outstanding equity interests. In addition, Mr. Santandreu, our CEO, President and Managing Member, is the beneficial owner of over 47.76% of our outstanding equity interests. These owners will be able to exercise considerable influence over all matters requiring owner approval, including the election of managing members, approval of lending and investment policies and the approval of corporate transactions, such as a merger or other sale of our Company or its assets. In addition, if our owners do not act together, such matters requiring owner approval may be delayed or not occur at all, which could adversely affect our business. Moreover, these owners are not obligated to provide any business opportunities to us. If these owners invest in another company in competition with us, we may lose the support provided to us by them, which could materially and adversely affect our business, financial condition and results of operations.

We must make principal payments on our existing investment certificates and other term debt over the next 12 month period.

Over the next 12 months, $430,016.51 in existing investment Certificates will mature. As of September 30, 2016, we have Cash and Cash Equivalents of $503,189 and Certificates of Deposits of $3,825,000 that would permit us to make payments if those certificate holders decide not to roll-over their accounts.

Risks Relating to Our Participation in the Microfinance Sector

Microcredit lending poses unique risks not generally associated with other forms of lending, and, as a result, we may experience increased levels of non-performing loans and related provisions and write-offs that negatively impact our results of operations.

Our core mission is to provide loans to fund the smallest of small businesses and other income generating activities of our clients. Our clients have limited sources of income, savings and credit histories, and can only provide us with limited collateral or security for their borrowings. To the extent that the business utilizes a vehicle in the business, i.e. a delivery truck or a taxi, we require a lien on such vehicle to secure repayment of the loan. We also require that businesses grant us a general security interest in all their equipment, assets and inventory and we file a UCC-1 to perfect such security interest. In addition, we require each stockholder of the borrowing business to individually sign the loans as a co-borrower. See “Business- Credit Evaluation Process” on p. 14 of this Offering Circular.

As a result, our clients pose a higher risk of default than borrowers with greater financial resources and more established credit histories and borrowers with better access to education, employment opportunities, and social services. Due to the precarious circumstances of our clients and our non-traditional lending practices, we may, in the future, experience increased levels of non-performing loans and related provisions and write-offs that negatively impact our business and results of operations. See “Business-Defaults; Collection Activities” on p. 15 and Note 2 to our financial statements included in this Offering Circular for a description of our accounting policy regarding how we determine the provision for loan losses as well as our write-off policies for non-performing loans.

We do not rely on credit scores to determine the credit worthiness of our clients, and as a result, we may experience increased levels of non-performing loans and related provisions and write-offs that negatively impact our results of operations.

Microcredit lending is based on helping those with no access to traditional banking. We believe a potential client can have a bad credit score, due to an incident unrelated to their current business operations, and still be considered credit worthy for a targeted, proceeds-specific loan. As a result, we do not use credit reports as the sole determinant of the client’s capability and ability to pay. Rather than rely on credit scores, we rely on public record databases to verify the information provided by the borrower. We meet with clients to study their financial records, check inventory, and help create a model of estimated revenues, expenses and profits. The loan specialist assembles character and borrower profile information, including references, personal and business information. The loan specialist also makes a complete financial evaluation of the borrower’s business. The evaluation considers various attributes of the business, including how the business operates, its operating margins, and average yearly sales or at least for the last four months of operations. The loan specialist considers all of the borrower’s business and family expenses in assessing the borrower’s repayment capacity. To account for undisclosed expenses, a borrower’s repayment capacity is calculated at 70% of the business’s net operating income less the borrower’s family expenses. See “Business-Credit Evaluation Process” on p. 14.

As a result, we do not use credit reports as the sole determinant of the client’s capability and ability to pay. If the information that we gather from our clients is not correct, we may have increased levels of non-performing loans and related provisions and write-offs that negatively impact our business and results of operations. See “Business-Defaults; Collection Activities” and “Business-Credit Evaluation Process” on p. 15 and 14, respectively, and Note 2 to our financial statements included in this Offering Circular for a description or our accounting policy regarding how we determine the provision for loan losses as well as our write-off policies for non-performing loans.

Competition from private money lenders may adversely affect our profitability and position in the microcredit lending industry.

In South Florida, we face competition from lenders that target the lower-income segments of the population, particularly from private money lenders that are not banks or micro finance institutions. These types of lenders, known as “loan sharks,” are willing to make unsecured loans with virtually no conditions other than repayment and in return, charge their borrowers usurious interest rates.

If we are unable to protect our service marks, others may be able to use our service marks to compete more effectively.

We have obtained service mark registrations for our corporate name “OUR MicroLending” and our logo. However, we may not be able to protect our service marks, which we rely on to support our brand awareness with clients and prospective clients and to differentiate our product and service offerings from those of our competitors. In certain cases, we have not sought protection for our service marks in a timely matter, or at all. As a result, we may not be able to prevent the use of our name or variations thereof by any other party, nor ensure that we will continue to have a right to use it. We further cannot assure you that our goodwill in such brand name or logo will not be DES by third parties due to our failure to obtain the service marks, which in turn would have a material adverse effect on our reputation, goodwill, business, financial condition and results of operations.

Risks Related to the Certificates

We may not be able to generate sufficient cash to service our obligations under the Certificates, and as a result, you may not earn any interest on the Certificates and you may lose your entire investment because the Certificates are unsecured, we have other debt outstanding and we have suffered losses in the past and expect to continue to experience losses.

Our ability to service our obligations under the Certificates, including the repayment of the principal and the ongoing interest payments, will depend upon, among other things, our future financial and operating performance, which will be affected by prevailing economic conditions and financial, business, regulatory and other factors, many of which are beyond our control. We may not be able to generate sufficient cash to service our obligations under the Certificates, and as a result, you may not earn any interest on the Certificates and you may lose your entire investment because the Certificates are unsecured.

If we are unable to generate sufficient cash flow to meet our cash obligations, including under the Certificates, we may be forced to take actions such as:

| | ● | restructuring or refinancing our debt or the Certificates; |

| | | |

| | ● | seeking additional debt or equity capital; |

| | | |

| | ● | seeking bankruptcy protection; |

| | | |

| | ● | reducing or delaying our business activities, investments or capital expenditures; or |

| | | |

| | ● | selling assets. |

Such measures might not be successful and might not enable us to meet our cash obligations. In addition, any such financing, refinancing or sale of assets might not be available on economically favorable terms.

The Certificates are not listed on any exchange and it is not expected that a public market for the Certificates will develop.

Prior to this Offering, there has been no trading market for the Certificates, and it is not expected that a trading market will develop in the foreseeable future. Therefore, any investment in the Certificates will be highly illiquid, and investors in the Certificates may not be able to sell or otherwise dispose of their Certificates in the open market.

The Certificates are being offered pursuant to an exemption from registration provided by Section 3(b) of the Act and Regulation A promulgated thereunder. Therefore, the Certificates have not been, nor will they be for the foreseeable future, registered under the Act or any applicable securities laws of any other jurisdiction. This offering is under Tier 2 of Regulation A. Regulation A limits the amount of securities that an investor who is not an accredited investor under Rule 501(a) of Regulation D can purchase in a Tier 2 offering to no more than: (a) 10% of the greater of annual income or net worth (for natural persons); or (b) 10% of the greater of annual revenue or net assets at fiscal year end (for non-natural persons). Accordingly, each investor who purchases Certificates must do so for the investor’s own account and investment. In addition, no regulatory authority has reviewed or approved the terms of this Offering, including the disclosure of risks and the fairness of its terms. There is no public market for the Certificates, and none is expected to develop for their purchase and sale.

The Certificates will be effectively subordinated to any secured debt.

The terms of the Certificates do not prevent us from incurring additional indebtedness or securing such indebtedness with our assets. If we incur secured debt, the Certificates will be effectively subordinated to the secured debt to the extent of the value of the assets securing that debt. The effect of this subordination is that if we become involved in a bankruptcy, liquidation, dissolution, reorganization or similar proceeding, or upon a default in payment on, or the acceleration of, the secured debt, our assets that secure the debt will be available to pay obligations on the Certificates only after all secured debt has been paid in full from those assets. We may not have sufficient assets remaining to pay amounts due on any or all of the Certificates then outstanding.

Purchasers of Certificates who do not wish to roll over their Certificates at the end of the initial term may not get their principal back if they fail to follow the appropriate procedures.

Purchasers of Certificates may not get their principal back at the end of the initial term if they fail to formally request the principal at least ten days before their maturity date and present their Certificate to us. See “Description of Certificates - Payment or Rollover at Maturity” on p. 22 for more information on the procedures for obtaining principal at the end of the term of the Certificates. Otherwise, we retain the right to automatically roll over the Certificates into a new Certificate. Moreover, the interest rate on the new Certificate could be higher or lower than the rate on the initial Certificate since it will reset at then current Treasury bill rates.

No Escrow of Funds; No Minimum Offering.

An escrow account will not be established for the proceeds of the Offering because we expect to invest such funds for its business purposes as they are received. Therefore, as we receive proceeds from the Offering, they will automatically be available for use by us. There is no minimum amount that must be raised in order for the Offering to be effective.

FORWARD-LOOKING STATEMENTS

All statements contained in this Offering Circular that are not statements of historical fact constitute “forward-looking statements.” All statements regarding our expected financial condition and results of operations, business, plans and prospects are forward-looking statements. These forward-looking statements include statements as to our business strategy, our revenue and profitability, planned projects and other matters discussed in this Offering Circular regarding matters that are not historical facts. These forward-looking statements and any other projections contained in this Offering Circular (whether made by us or any third party) are predictions and involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements or other projections. Investors can generally identify forward-looking statements by the use of terminology such as “aim”, “anticipate”, “believe”, “expect”, “estimate”, “intend”, “objective”, “plan”, “project”, “shall”, “will”, “will continue”, “will pursue” “contemplate”, “future”, “goal”, “propose”, “may”, “seek”, “should”, “will likely result”, “will seek to” or other words or phrases of similar import. All forward-looking statements are subject to risks, uncertainties and assumptions about us that could cause actual results to differ materially from those contemplated by the relevant forward-looking statement.

Actual results may differ materially from those suggested by the forward looking statements due to risks or uncertainties associated with our expectations with respect to, but not limited to, regulatory changes pertaining to the industries in the United States in which we have our businesses and our ability to respond to them, our ability to successfully implement our strategy, our growth and expansion, technological changes, our exposure to market risks, general economic and political conditions, which have an impact on our business activities or investments, the monetary and fiscal policies of the United States, inflation, deflation, unanticipated turbulence in interest rates, foreign exchange rates, equity prices or other rates or prices, the performance of the financial markets in the United States and globally, changes in domestic laws, regulations and taxes and changes in competition in our industry. Important factors that could cause actual results to differ materially from our expectations include, but are not limited to, the following:

| | ● | Ability to secure additional capital on terms favorable to us; |

| | | |

| | ● | Limited operating history; |

| | | |

| | ● | Success of new loans and services introduced by us; |

| | | |

| | ● | General economic and business conditions in Florida and the United States; |

| | | |

| | ● | Changes in laws and regulations that apply to us; and |

| | | |

| | ● | Ability to attract, motivate, integrate or retain qualified personnel. |

For further discussion of factors that could cause our actual results to differ, see “Risk Factors,” and “Business” on p. 3 and 10 of this Offering Circular, respectively.

By their nature, certain market risk disclosures are only estimates and could be materially different from what actually occurs in the future. As a result, actual future gains or losses could materially differ from those that have been estimated. Forward-looking statements speak only as of the date of this Offering Circular.

DESCRIPTION OF BUSINESS AND MANAGEMENT DISCUSSION OF FINANCIAL CONDITION

Overview

Our core business is providing microloans to small business owners and entrepreneurs in South Florida, many of whom are immigrants and minorities. These businesses typically have fewer than five employees and annual sales of $100,000 or less, and the loans are provided for use in the businesses or other income generating activities and not for personal consumption. Our borrowers often have no, or very limited, access to loans from other sources other than private money lenders that we believe typically charge very high rates of interest.

On April 26, 2013, we received notice from the US Treasury Department – CDFI Fund that we formally became a Community Development Financial Institution (“CDFI”). The CDFI Fund was created for the purpose of promoting economic revitalization and community development through investment in and assistance to CDFIs. The CDFI Fund was established by the Riegle Community Development and Regulatory Improvement Act of 1994, as a bipartisan initiative. Through monetary awards and the allocation of tax credits, the CDFI Fund helps promote access to capital and local economic growth in urban and rural low-income communities across the nation. On September 24, 2013 we received a written notice that we had been awarded $600,000 from the CDFI Fund and we received the funds on January 23, 2014. By June 30, 2014 we had disbursed $600,000 or 100% of the award as new loans. The CDFI requires that we submit financial information and performance reports. On September 10, 2015 we received a written notice that we had been awarded $650,000 from the CDFI Fund and we received funds on March 21, 2016. By April 30, 2016 we had disbursed $650,000 or 100% of the award as new loans. On July 15, 2015 we received a written notice that we had been awarded $200,000 from the CDBG Block of the Miami-Dade County to provide loans in the Miami-Dade County. On September 29, 2016 we received a written notice that we had been awarded $200,000 from the CDBG Block of the Miami-Dade County to provided loans in the Miami-Dade County.

On November 2014, we signed an agreement with the State of Florida, Department of Economic Opportunity “DEO” to become Loan Administrator of the Florida Microfinance Act. Under this agreement we provide the services of non-banking financial institutions making short-term, fixed rate microloans in conjunction with providing business management training, business development training and technical assistance to small businesses. We manage a total of $4,850,000 from the State of Florida under the Florida Microfinance Act.

The Florida Microfinance Act establishes conditions for the microcredits we can disburse using funds from the State of Florida’s Microfinance Loan Program. All interest and fees charged on these loans are considered revenue to us, and they can be used for any purpose, including interest or principal payments for the Investment Certificates. Under our agreement with the State of Florida, we must pay back the loan between December 30, 2017 and June 30, 2018, unless the agreement is renewed. Our management activities therefore are focused on making high quality loans with that money. As of this date, we have no past due loans made under the Microfinance Loan Program. The Company is negotiating with the State of Florida to renew the program. If the State of Florida does not renew the program, per the agreement, the Company will have to return the total funds granted of $4,825,000, minus 1% for administration costs ( $48,250), for a total of $4,776,750 to be paid to the State of Florida by June 2018.

All of our loans are secured by collateral. To the extent that the business utilizes a vehicle in the business, i.e. a delivery truck or a taxi, we require a lien on such vehicle to secure repayment of the loan. We also require that businesses grant us a general security interest in all their equipment, assets and inventory and we file a UCC-1 to perfect such security interest. In addition, we require each stockholder of the borrowing business to individually sign the loans as a co-borrower.

In addition to being entrenched in a market with a strong demand for our services and our expertise in microfinance, we believe that our competitive strengths include our efficient operating model that leverages technology, quick turnaround times and our skilled network of specialists. Our strategy is to further expand our loans and product offerings by relying on these strengths. Our strategic goals for the next five years are to:

| | ● | build lending assets to expand service to clients within our target market; |

| | | |

| | ● | increase revenues through improved portfolio management; and |

| | | |

| | ● | expand the volume of lending through expanded development services and marketing. We believe that we can support this level of expansion and deployment. |

We intend to finance our expansion by accessing multiple sources of capital, both debt, through the offering of Certificates in this offering and, depending on market conditions, potential future offerings, and equity, from our existing stockholders. To date, we have funded our lending operations using the capital contributions of our owners and borrowings from our officers, family members of our officers and certain of our equity investors as well as using funds from the sale of Certificates from our prior Regulation A offering. Securities issued in these types of financings will adversely affect the holders of Certificates to the extent the securities are senior to the Certificates. In addition, to the extent we issue more Certificates, it will be more difficult for us to service the debt These types of financings should not affect holders of the Certificates given that the securities will not be senior to the Certificates. However, increases in our outstanding indebtedness, including an increase in the amount of Certificates outstanding, will make it more difficult to service our indebtedness, including the payments of interest and principal on the Certificates.

History and Evolution

Offices

In October 2007, we were formed as a Florida limited liability company. From March 2008 through September 30, 2016, we have made approximately 2045 microloans totaling more than $17,087,180 to micro and small business owners and entrepreneurs in South Florida, many of whom are immigrants from Latin America and the Caribbean. We currently operate in one Miami location.

Employees

We currently have three (3) full-time employees, one (2) part time employee and four ( 4) loan “specialists.” We use independent contractors as our loan solicitors instead of hiring full-time loan officers. We refer to our loan officers as “specialists” and we compensate them on a sliding-scale basis depending upon the number and quality of active loans generated by them. By hiring independent contractors and correlating their compensation to active loans, we are able to avoid the fixed salary and employee benefit costs associated with full-time employees and to more closely align compensation with actual loan revenue. Each loan specialist is responsible for covering a defined geographic region between Delray Beach and Homestead, Florida. Our loan specialists go door-to-door in commercial areas with high volumes of small businesses, including flea markets and the Miami neighborhoods of Little Havana and Little Haiti. We anticipate hiring an additional four loan specialists.

Management Experience

Our management and equity owners have extensive microfinance experience, including over nine years of experience in our Florida Company. We have been able to make the necessary marketing, legal, collection and operations adjustments in our microcredit methodology to overcome the challenges that where present in the market and have a loan portfolio that performs better every year since 2011.

Our Loan Products

We offer three products. Our first and principal product that we currently offer is the “Our Express Loan.” TheOur Express Loan product is intended for small businesses in amounts between $1,500 and $50,000. After all required documents are submitted; we typically approve our loans within 48 hours and fund our loans within 72 hours of approval. For theOur Express Loan, we require our borrowers to have owned a business for at least one year or have at least one year of provable business experience. Starting in the third quarter of 2014, we launched our second product, which is “Equipment Leasing”. This program allows microentrepreneurs to purchase the necessary equipment that they need for their business. No matter the type of equipment from a truck to a refrigerator, we can help achieve the purchase of the asset they need for their business. The maximum amount is up to $30,000 with terms of up to 24 months. To qualify for this program, the business must be currently active for at least 1 year, or the microentrepreneur have provable experience in the field. A down payment of 15% is required. We collateralize all of our loans with business equipment or vehicles depending on the borrower’s assets. Based on the quality of the borrower, we will also require guarantors or co-borrowers as a condition of our loans. These guarantors may be business partners, spouses or friends or other members of the extended family that are willing to guarantee the loan.

The third program that we also started offering in the second quarter of 2014 is the “Secured Loan”. Our secured loan is an installment type of credit to individuals to help them build or reestablish their credit. This cash-secured loan is extended when a borrower uses their liquid capital to guarantee the loan. As a socially responsible institution and following our mission, we present this product to help the community and assist those affected by the economic crisis. The amount could be from $1,500 up to $5,000. The terms could be from 6 to 12 months. No credit history is required, but the borrower must be 18 years or older, provide proof of residency and income. The cash collateral must be presented to us in the form of a certified check from a banking institution or money order.

Loan Portfolio

Since the commencement of our operations in March 2008 and through September 30, 2016 we have extended an aggregate of approximately 2045 loans. In the year ended December 31, 2009, we extended an aggregate of approximately 325 loans, an increase of approximately 15% as compared to the 282 loans extended in the year ended December 31, 2008. In the year ended December 31, 2010, we disbursed approximately 298 loans, in the year ended December 31, 2011, we disbursed approximately 131 loans and in the year ended December 31, 2012, we disbursed 102 loans. During the year ended December 31, 2013 we disbursed approximately 173. In the year ended December 31, 2014 we disbursed 243 loans, in the year ended December 31, 2015 we disbursed 274 loans and 217 loans and in the first nine months of 2016 were disbursed.

The following discloses the number and percentage of loans extended to new borrowers and the number and percentage of loans extended to existing borrowers once the prior loan was paid off (borrowers cannot have more than one loan outstanding) for the periods indicated:

| Period | New Loans | Repeat Loans | Total Loans |

| Year ended December 31, 2008 | 264 (93.62%) | 18 (6.38%) | 282 |

| Year ended December 31, 2009 | 185 (56.92%) | 140 (43.08%) | 325 |

| Year ended December 31, 2010 | 105 (35.23%) | 193 (64.77%) | 298 |

| Year ended December 31, 2011 | 47 (35.88%) | 84 (64.12%) | 131 |

| Year ended December 31, 2012 | 8 (7.84%) | 94 (92.16%) | 102 |

| Year ended December 31, 2013 | 52 (30.06%) | 121 (69.94%) | 173 |

| Year ended December 31, 2014 | 111 (45.68%) | 132 (54.32%) | 243 |

| Year ended December 31, 2015 | 118 (43.07%) | 156 (56.93%) | 274 |

| Nine months ended September 30 , 2016 | 90 (41.47%) | 127 (58.53%) | 217 |

| Total | 980 (47.92%) | 1065 (52.08%) | 2045 |

In the year ended December 31, 2009, the aggregate principal amount of all of the loans that we made was $1,753,348, a decrease of approximately 3.7% as compared to $1,820,844, in the year ended December 31, 2008. In the year ended December 31, 2010, the aggregate principal amount of all of the loans that we made was $1,654,728, a decrease of approximately 5.6% as compared to the amount of loans in 2009. In the year ended December 31, 2011, the aggregate principal amount of all of the loans that we made was $776,671, a decrease of approximately 53.06% as compared to the amount of loans in 2010. In the year ended December 31, 2012, the aggregate principal amount of the loans that we made was $927,149, an increase of approximately 19.38% as compared to the amount of loans in 2011. In the year ended December 31, 2013, the aggregate principal amount of the loans that we made was $1,386,092, an increase of approximately 49.5% as compared to the amount of loans in 2012. In the year ended December 31, 2014, the aggregate principal amount of the loans made was $2,094,998, an increase of approximately 51.14% as compared to the amount in 2013. In the year ended December 31, 2015, the aggregate principal amount of the loans made was $2,735,345, and increase of approximately 30.57% as compare to the amount in 2014.During the first nine months of 2016 the aggregate principal amount of the loans that we made was $3,231,208.

Loan amounts range from a minimum of $1,500 to a maximum of $50,000. The average amount financed in the t nine months ended September 30, 2016 was approximately $14,890, as compare to approximately $9,983 in the year ended December 31, 2015. In the year ended December 31, 2014 the average amount financed we approximately $8,621 as compared to approximately $8,012 in the year ended December 31, 2013.

As of December 31, 2014, the aggregate principal amount of loans outstanding, net of allowance of loan losses was $1,379,708. As of December 31, 2015, the aggregate principal amount of loans outstanding, net of allowance of loan losses was $2,058,118. As of September 30, 2016, the aggregate principal amount of loans outstanding, net of allowance for loan losses, was $3,694,658

Loan periods vary by borrower and are generally between six to twenty-four months. The average term of the loans extended in the year ended December 31, 2014 was 11.3 months. The average term of the loans extended in the year ended December 31, 2015 was 11.4 months. The average term of the loans extended in the period ended 1 September 30, 2016 was 12.32 months.

Our loans are repaid in monthly installments. Borrowers incur closing fees of up to 6% percent and are required to make a guaranteed deposit equal to up to 10% percent of the loan amount.

Interest Payments and Rates

The annual interest rate that we charge ranges from 15.375% to 17.98% depending upon the term of the loan. For example, loans with 6 and 7 month terms will have the lowest rate (15.375%) and as the term increases, the rate will increase up to 18%, which is the maximum amount that may be charged under Florida law. The purpose of offering slightly lower interest rates is to motivate our borrowers to accept and repay loans of shorter duration, which, in turn, will generate greater turn over of our loan portfolio.

Interest is computed on a 365/360 basis of the aggregate principal amount of the loan, net of applicable fees, at annual interest rates that are pro-rated to correspond to the term of each loan. The applicable fees are composed of loan origination fees and late fees. Loan origination fees vary from 4% to 5% of the loan amount and this fee is determined by the term of the loan, which could vary from 6-24 months. Late fees are between 5% and 10% of the borrower’s monthly payment. The total amount of interest due is calculated at inception and paid in monthly installments, together with payments of principal and fees. As of December 31, 2014, December 31, 2015 and September 30, 2016 our earned weighted average interest rates on loans outstanding were 14.44%, 14.48% and 7.50% respectively. The weighted average rates were calculated by dividing interest income for the period by the average outstanding portfolio of loans for the same period. The average outstanding portfolio was determined by adding the beginning and ending balance of the portfolio, and dividing that amount by two.

Credit Evaluation Process

Before we elect to make a microloan, our credit committee analyzes various aspects of potential borrowers, each of whom is presented to the committee by our loan specialists. Our credit committee consists of (1) the microcredit specialist, which is presenting the loan, (2) an internal credit process auditor, (3) our chief operating officer and (4) our chief executive officer. Our internal credit process auditor is responsible for reviewing the loan application and all supporting documentation to ensure that the application complies with the Company’s minimum underwriting guidelines.

Loans under $10,000 must be approved by the microcredit specialist, the internal credit process auditor and our chief operating officer. Loans in excess of $10,000 must be approved by the entire credit committee, including the chief executive officer.

Microcredit lending is based on helping those with no access to traditional banking. We believe a potential client can have a bad credit score, due to an incident unrelated to their current business operations, and still be considered credit worthy for a targeted, proceeds-specific loan. As a result we do not use credit reports as the sole method to determine the client’s ability to pay. We do require clients to authorize us to check their credit score if necessary. Pursuant to our credit manual, we check the credit score of a client: (1) if there is an incongruence between the registered documents and what the client reports, (2) if there is a disconnect between reported expenses and reported liabilities, and (3) for any loan request above $10,000.

Rather than relying solely on credit scores, we also verify the information provided by the borrowers with public records databases to cross check and verify the personal and business information provided by the client along with the assets and liabilities that they may already have with other financing institutions. The databases that we utilize are: Sunbiz.org(http://www.sunbiz.org), Lexis Nexis(https://risk.nexis.com/RiskManagement/Default.aspx?_nqs_cmd=ANNOUNCEMENTS&_nc_snum=3&ss_fromSessionStart=true&announcementId=172), Driver’s License Check(https://www6.hsmv.state.fl.us/DLCheck/dl/pages/dlCheck.jsp), Miami Dade Clerk(http://www2.miami-dadeclerk.com/Public-Records), Broward County Official Records(https://www.clerk-17th-flcourts.org/Clerkwebsite/BCCOC2/PASystemTransfer/CourtTypeSelection.aspx?Destination=CaseSearch.aspx), Palm Beach County Clerk(http://www.mypalmbeachclerk.com/cctrecordsearch.aspx), Blackbook(https://www.lendersolutionsonline.com/Account/Login.aspx), Title Check(http://www.flhsmv.gov/), and UCC Lien Check(www.floridaucc.com). We meet with clients to study their financial records, check inventory, and help create a model of estimated revenues, expenses and profits. The loan specialist assembles character and borrower profile information, including references, personal and business information. The loan specialist also makes a complete financial evaluation of the borrower’s business. The evaluation considers various attributes of the business, including how the business operates, its operating margins, and average yearly sales or at least for the last four months of operations. The loan specialist considers all of the borrower’s business and family expenses in assessing the borrower’s repayment capacity. To account for undisclosed expenses, a borrower’s repayment capacity is calculated at 70% of the business’s net operating income less the borrower’s family expenses.

Once a borrower’s ability to pay is substantiated, the loan specialist analyzes the balance sheet and other financial metrics of the borrower or its business to determine and make a recommendation on the loan amount to the credit committee. The loan amount that is approved does not always equal the amount requested by the borrower. Once the credit committee approves a potential borrower the next step in finalizing the loan is to evaluate the borrower’s collateral. The collateral must be tangible such as a vehicle, or key equipment or machinery to operate the business equal to 150% of the value of the loan amount. The collateral that we have relating to our current portfolio is primarily vehicles, including passenger cars and commercial trucks. For each of our loans in our portfolio, we have collateral equal to 150% of the original loan amount. The collateral requirement has been the same for all of our loans from March 2008 to the present. In addition, if the collateral is weak, a cosigner may be required. The guarantor/cosigner is subject to the same assessment and guidelines established for the borrower. Moreover, the cosigner information is updated each time the borrower applies for a new loan.

For loans in excess of $10,000, in addition to checking the public records database, we will obtain a credit report of the borrower or its business to assist us in our evaluation of the borrower. However, ultimately, the borrower’s credit report or score is only one factor, in addition to the borrower’s repayment capacity, the stability and operating history of the borrower’s business, the borrower’s business acumen and experience, and the type and value of the collateral.

Approximately 60% of all of our borrowers have obtained loans from us in the past. We typically require a borrower to repay any current amounts outstanding before obtaining a new loan. However, if a borrower has established a strong economic reason for a new loan and has maintained his loan in good standing, on occasion we will allow a borrower to refinance an outstanding loan with a new, larger loan.

Our loan and security documents contain customary lender remedies in the case of default by a borrower, including, as described below, the ability to obtain possession of any collateral that is securing the loan in default and declaring the loan in default and accelerating the principal due date.

Defaults; Collection Activities

An integral component of microlending is the active management of loan receivables. At OUR MicroLending, a past due loan is classified as past-due the first day after we do not receive the full interest and principal payment on its due date versus 30 days, which is the standard at many financing institution. If a borrower’s regular installment payment becomes past due, we implement a staged collection process which progresses in accordance with the amount of time a payment is past due. From 0 to 45 days, the loan specialist will visit the borrower up to three times and with each visit will deliver a letter of past due notice, which states the urgency of the payment. The first letter reminds the borrower that the payment is late, the second letter serves as a second reminder and includes information regarding late fees and interest, and the third and final letter describes the legal action that will be taken against the borrower if immediate payment does not occur. If the failure to remedy the past due payment continues beyond 45 days, during the period from 45 to 60 days, one of our officers will contact the borrower regarding the consequences of late payment. Often during this collection process, borrowers will offer to make partial payments. We believe the early detection helps borrowers from experiencing financial difficulties. When payment is due, the collection committee gathers financial information from the specialist and listens to the proposal of the client. Based on that information and the client’s proposal, we may accept partial payments in certain cases. In these cases, we will not restructure the loan, but will accept the negotiated partial payments and, to the extent that these payments are continuing to be made, will forebear from taking the further collection action discussed below. For loans for which the borrower is making partial payments, we believe that the collateral/guarantor-co-borrower is adequate and the allowance for loan loss could cover any such loan. We have no loan modifications, and therefore no trouble-debt restructurings. For loans making partial payments that were disbursed in 2008 and 2009, we have an allowance for reasonably possible loan losses of 100%. However, these loans continue to be reflected on our books as past-due and the client continues to be closely monitored by its loan specialist.

Once a loan is more than 60 days past due, we will take two types of actions. To the extent that we have received a security interest in a vehicle or other asset for which self-help is a viable remedy, we will use the self-help provisions of the Florida statutes for secured lenders and take possession of the collateral, as described below. For all loans we will employ the services of an external collector. Once a loan is more than 90 days past due, we will initiate legal collection proceedings against the borrower.

Whenever possible, after a default by a loan customer, we will attempt to use statutorily allowed “self help” remedies to obtain possession of any collateral that is securing the loan in default. Florida law permits a secured creditor, after default, to take physical possession of the collateral securing a loan, without any prior judicial intervention or blessing, so long as there is no breach of the peace in obtaining such possession. Normally, such self help remedies apply to collateral in the form of equipment or vehicles where we are able to obtain possession either because the loan customer voluntarily gives possession to us or we are able to obtain such possession by repossessing it without a breach of the peace. A breach of the peace would occur, for example, if a borrower attempted to physically stop the repossession or threatened the repossessing individuals with bodily harm.

If we are not able to use self help, then we would seek to obtain possession of the collateral by requesting an order from a court as part of a legal proceeding to collect on the debt, which would be more costly and time-consuming than using the self help provisions. In either event, whether the collateral is obtained by self help or pursuant to a judicial order, we would seek to sell the collateral to reduce the amount of the debt owed.

As a general practice, we may take a reserve equal to 5% of the principal amount of loans that we make during such month. We take a 5% general reserve based on practice in the microfinance industry and recent loss experience. However, we watch loan portfolio performance carefully and adjust the reserve as necessary. Further, our allowance for loan losses reflects probable loan losses inherent in our loan portfolio as of the date of the balance sheets included in this Offering Circular.

Monthly, we also review the loans which are more than 90 days past due to determine if it is necessary to make a specific reserve for such loan. To the extent the borrower is making partial payments on a loan, we do not take a specific reserve with respect to such loan. Interest income is discontinued at the time the loan is 90 days delinquent, unless the borrower is making partial payments on the loan. Past due status is based on the contractual terms of the loan. In all cases, loans are placed on nonaccrual status or charged-off at an earlier date if collection of principal or interest is considered doubtful. A loan is moved to nonaccrual status in accordance with this policy, typically after 90 days of non-payment.

In the fourth quarter of 2009, we decided that we needed to reevaluate our collections process in order to reduce our past-due loans. As a result we implemented the following initiatives:

Established a Collection and Portfolio Committee. Rather than relying solely on the relevant loan specialist to pursue collection of his or her loans, we adopted a collection committee who is responsible for overseeing the collection of all loans. The collection committee meets twice a month and captures the relevant data about the debt and the debtor. If the collection committee notes any weakening of our ability to collect on the debt, it reports the information to our portfolio committee in order to evaluate the appropriateness of the specific component of the allowance for loan losses. The portfolio committee meets once a month, but also meets quarterly in order to evaluate the specific component of those allowances for loan losses. The collection committee is comprised of (1) the microcredit specialist of the loan, (2)Vice President of Business Development, and (3) the Chief Operating Officer. The portfolio committee is comprised of (1)Vice President of Business Development, (2) the Chief Operating Officer, (3) the Chief Financial Officer, and (4) the Chief Executive Officer.

Accelerated the Collection Process. Rather than waiting for the loan to be 30 days past-due to reach out to the borrower, we adopted a procedure that called for sending a letter to the borrower after the first day of delay, a second letter seven (7) days after the original due date and a third letter by the 30th day after the original due date.

Provided Management with Specialized Microcredit Education. In 2009 we sent our COO, to Bogota, Colombia for training with the Fundacion Emprender, and then for an internship with Fundacion Mundial de la Mujer (that belongs to Women’s World Banking) and Finamerica, each of which are institutions that specialize in microcredits.

Hired Outside Consultants to Assist with Collections. Beginning in the second half of 2010, we have used the advice of a collection office to assist us with the collections process.

As a result of these initiatives, we have improved our collection experience for our past-due loans and the number of loans that have become past-due has decreased as follows:

| | ● | In 2008 we made 282 loans, 56 of which, or 19.86%, were more than 90 days late; |

| | | |

| | ● | In 2009 we made 325 loans, 31 of which, or 9.54%, were more than 90 day late; |

| | | |

| | ● | In 2010 we made 298 loans, 13 of which, or 4.36%, were more than 90 days late; |

| | | |

| | ● | In 2011 we made 131 loans, 4 of which, or 3.05%, were more than 90 days late; |

| | | |

| | ● | In 2012 we made 102 loans, 2 of which, or 2.08%, were more than 90 days late; |

| | | |

| | ● | In 2013 we made 173 loans, 1 of which, or 0.58%, were more than 90 days late; |

| | | |

| | ● | In 2014 we made 243 loans, 4 of which, or 1.65%, were more than 90 days late; |

| | | |

| | ● | In 2015, we made 274 loans, 21 of which, or 7.66, were more than 90 days late; and |

| | | |

| | ● | In the first nine months of 2016 we made 217 loans, none of which were more than 90 days late |

For more information regarding the number of loans made each year, see the chart on page 13.

As of December 31, 2014, December 31, 2015, and September 30, 2016, loans with an aggregate principal balance net of Allowance for loan losses of $428,628, $489,493, and $387,769 respectively, were more than 90 days past-due.

As of December 31, 2014, we had loans with an aggregate principal amount of $583,827 which were classified as more than 90 days past due. As of December 31, 2015, we had loans with an aggregate principal amount of $770,247 which were classified as more than 90 days past due. As of September 30, 2016, we had loans with an aggregate principal amount of $770,247 which were classified as more than 90 days past due.