Exhibit (a)(1)(A)

Offer to Purchase for Cash

by

by

NAUTILUS MARINE ACQUISITION CORP.

of

Up to 4,137,300 Shares of issued and outstanding Common Stock

at a Purchase Price of $10.10 Per Share

In Connection with its Consummation of a Proposed Business Transaction

Up to 4,137,300 Shares of issued and outstanding Common Stock

at a Purchase Price of $10.10 Per Share

In Connection with its Consummation of a Proposed Business Transaction

THIS OFFER AND WITHDRAWAL RIGHTS WILL EXPIRE AT 11:59 P.M., NEW YORK CITY TIME, ON MONDAY, JANUARY 7, 2013 UNLESS THE OFFER IS EXTENDED. |

If you support our proposed Acquisition of Assetplus Limited, donot tender your Common Shares in this Offer.

Nautilus Marine Acquisition Corp. (which intends to do business under the assumed name of “Nautilus Energy Services” until such time as its name is legally changed) (“Nautilus”, the “Company”, “we”, “us” “our” or similar terminology) hereby offers to purchase up to 4,137,300 shares of its issued and outstanding common stock, par value $0.0001 per share (the “Common Shares”), at a purchase price of $10.10 per share, net to the seller in cash, without interest (the “Purchase Price”), for a total Purchase Price of up to $41,786,730, upon the terms and subject to certain conditions described in this Offer to Purchase for Cash (the “Offer to Purchase”) and in the Letter of Transmittal (the “Letter of Transmittal,” which together with this Offer to Purchase, as they may be amended or supplemented from time to time, constitute the “Offer”).

If more than 4,137,300 Common Shares are validly tendered and not properly withdrawn, we may amend, terminate or extend the Offer. In accordance with the rules of the Securities and Exchange Commission (the “SEC”), in the event that more than 4,137,300 Common Shares are so tendered, we may exercise our right to amend the Offer (the “2% Amendment”) to purchase up to an additional 2% of our outstanding Common Shares without extending the Expiration Date, and thereby accept for payment all Common Shares which may be validly tendered in this Offer. However, if more than 4,137,300 Common Shares are validly tendered and not properly withdrawn, and we do not exercise our right pursuant to the 2% Amendment to purchase additional Common Shares, or if we are unable to satisfy the Acquisition Condition (as defined below), we may amend, terminate or extend the Offer. If we terminate the Offer, we willNOT: (i) purchase any Common Shares pursuant to this Offer or (ii) consummate the Acquisition (as defined below) in accordance with the terms of the Share Purchase Agreement described in this Offer to Purchase.

The Purchase Price of $10.10 is equal to the per share amount held in our trust account (the “Trust Account”) established to hold the proceeds of our initial public offering (the “IPO”). See “The Offer — Number of Shares; Purchase Price; No Proration.”

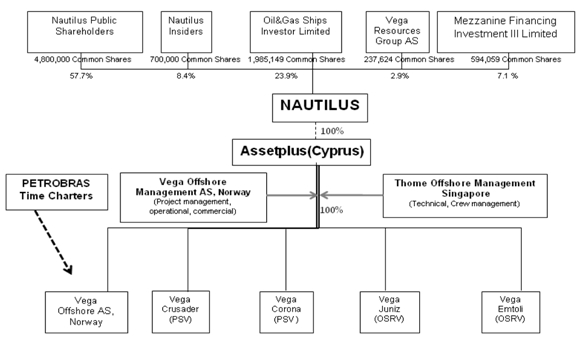

This Offer is being made in connection with a Share Purchase Agreement, dated as of December 5, 2012 (as the same may be amended, from time-to-time, the “Share Purchase Agreement”), by and among Nautilus, Assetplus Limited, a Cyprus limited liability company (“Assetplus”) and each of Vega Resource Group AS (“Vega Resource”) and Oil and Gas Ships Investor Limited (“Oil & Gas”, and together with Vega Resource,

the “Sellers”) as the ultimate beneficial owners of 100% of the issued and outstanding equity shares of Assetplus. Upon consummation of the transactions (the “Transaction”) contemplated by the Share Purchase Agreement, Nautilus will acquire from the Sellers 100% of the issued and outstanding equity shares of Assetplus, and Assetplus will become a wholly owned subsidiary of Nautilus (the “Acquisition”).

Assetplus, indirectly through its wholly-owned subsidiaries, is the owner of, or has the right to acquire, four vessels: two platform supply vessels (“PSVs”) (Vega Crusader and Vega Corona) and two oil spill response vessels (“OSRVs”) (Vega Juniz and Vega Emtoli). Assetplus, indirectly through its wholly-owned subsidiaries, has also entered into six time charter contracts with Petróleo Brasileiro S.A. or its affiliates (“Petrobras”). Each of the two PSVs and two OSRVs owned by the Vessel Owning Subsidiaries will serve four (4) of the six (6) Petrobras time charters, respectively. Assetplus intends to identify and control either through direct purchase or charter an additional two (2) vessels to service the remaining two (2) OSRV Petrobras time charter contracts for which it has not yet secured vessels. Further, Nautilus has entered into an exclusive option agreement with Vega Resource. Vega Resource has bid on two additional time charter contracts for PSVs with Petrobras, which time charters Vega Resource expects to be awarded in the first quarter of 2013. The exclusive option agreement provides Nautilus with the exclusive option following the closing of the Acquisition to acquire said time charters from Vega Resource if the same are awarded to Vega Resource. Following the Acquisition, Assetplus will be a wholly-owned subsidiary of Nautilus, and Nautilus will indirectly, through Assetplus’s subsidiaries, operate the two PSVs and the two OSRVs, all of which will be under time charters with Petrobras.

Pursuant to its articles of incorporation, as amended (the “Articles of Incorporation”), and the Business Corporations Act of the Republic of the Marshall Islands (the “BCA”), Nautilus may consummate an acquisition without shareholder approval by providing all holders of its Common Shares with the opportunity to redeem their Common Shares through a tender offer pursuant to the tender offer rules promulgated under the Securities Exchange Act of 1934, as amended (the “Exchange Act”). This Offer is being made in part to provide Nautilus shareholders with such opportunity to redeem their Common Shares and to allow the Acquisition to be completed without a shareholder vote. See “The Offer — Purpose of the Offer; Certain Effects of the Offer.”

THE OFFER IS CONDITIONED ON SATISFACTION OF THE ACQUISITION CONDITION (AS FURTHER DESCRIBED IN THIS OFFER TO PURCHASE) AND CERTAIN OTHER CONDITIONS. SEE “THE OFFER — CONDITIONS OF THE OFFER.”

Only Common Shares validly tendered and not properly withdrawn will be purchased pursuant to the Offer. Common Shares tendered pursuant to the Offer but not purchased in the Offer will be returned at our expense promptly following the expiration or termination of the Offer. See “The Offer — Procedures for Tendering Shares.”

We will fund the purchase of Common Shares in the Offer and certain other Acquisition related expenses with an aggregate of $41,786,830 from the cash available to us from the Trust Account upon consummation of the Acquisition. Except as otherwise set forth in the Share Purchase Agreement, all fees and expenses incurred by the Sellers and Assetplus, including without limitation legal fees and expenses, in connection with the Share Purchase Agreement and the Transaction will be borne by the Sellers, and all fees and expenses incurred by Nautilus, including without limitation legal fees and expenses, in connection with the Share Purchase Agreement and the Transaction will be borne by Nautilus. Furthermore, in the event that the funds available to Nautilus at Closing, and following the payment of the aggregate Purchase Price, are insufficient to satisfy in full the fees and expenses of Nautilus incurred in connection with the Transaction, certain third parties and the Insiders (as defined below) have agreed to defer the payment of all such fees and expenses in excess of $1.212 million. In addition, certain of our Insiders have committed to loan us up to an additional $200,000 pursuant to an irrevocable standby facility which may be applied towards the payment of such expenses. As of November 28, 2012, the Company had approximately $42,920 in cash and cash equivalents on hand. See “The Offer — Source and Amount of Funds.”The Offer is not conditioned on any minimum or maximum number of Common Shares being tendered. The Offer is, however, subject to the satisfaction of the Acquisition Condition. See “The Offer — Purchase of Shares and Payment of Purchase Price” and “ — Conditions of the Offer”.

The Common Shares are currently listed on the Nasdaq Capital Market (��Nasdaq”) under the symbol “NMAR.” On December 4, 2012, the last reported sale price of the Common Shares was $9.99 per share.Shareholders are urged to obtain the current market price for the Common Shares before deciding whether to tender their Common Shares pursuant to the Offer. See “Price Range of Securities and Dividends.”

We also have outstanding warrants, each to acquire one Common Share (a “Warrant”). The Warrants are also listed on Nasdaq under the symbol “NMARW”. This Offer is only open for our Common Shares.

Our intention is to consummate the Acquisition of Assetplus. Our board of directors has unanimously: (i) approved our making the Offer, (ii) declared the advisability of the Acquisition and approved the Share Purchase Agreement and the transactions contemplated by the Share Purchase Agreement, and (iii) determined that the Acquisition is in the best interests of Nautilus and its shareholders and if consummated would constitute our initial business transaction pursuant to our Articles of Incorporation. If you tender your Common Shares in the Offer, you will not be participating in the Acquisition because you will no longer hold such Common Shares in Nautilus, which will be the public holding company for the operations of Assetplus and its subsidiaries following the consummation of the Acquisition.

Therefore, our board of directors unanimously recommends that youDO NOT accept the Offer with respect to your Common Shares.

The members of our board of directors will directly benefit from the Transaction and have interests in the Transaction that may be different from, or in addition to, the interests of Nautilus shareholders. See “The Transaction — Certain Benefits of Nautilus’s Directors and Officers and Others in the Transaction.”

You must make your own decision as to whether to tender your Common Shares and, if so, how many Common Shares to tender. In doing so, you should read carefully the information in this Offer to Purchase and in the Letter of Transmittal, including the purposes and effects of the Offer. See “The Offer — Purpose of the Offer; Certain Effects of the Offer.” You should discuss whether to tender your Common Shares with your broker, if any, or other financial advisor. See “Risk Factors” for a discussion of risks that you should consider before participating in this Offer and the Acquisition.

On November 12, 2012, before we announced our intention to commence the Offer, we entered into a lock-up with put option agreement (each, a “Lock-Up Option Agreement”) with each of AQR Opportunistic Premium Offshore Fund, L.P. (“AQR OPOF”), AQR Diversified Arbitrage Fund (“AQR DAF”), Hare & Co. (“H&C”) and CNH Diversified Opportunities Master Account (“CNH”, and together with AQR OPOF, AQR DAF and H&C, the “Restricted Investors”) for 439,500, 54,300, 32,600 and 16,300 Common Shares, respectively, for an aggregate of 542,700 Common Shares (the “Locked-up Shares”), representing approximately 11.3% of the Common Shares issued in our IPO. Pursuant to the Lock-Up Option Agreements, each Restricted Investor agreed not to tender its respective Locked-up Shares in this Offer. In addition, during the period commencing on November 12, 2012 and terminating on the 11th business day following the Expiration Date (the “Lock-up Period”), each Restricted Investor is also prohibited from selling, transferring or otherwise disposing of the Lock-up Shares during the Lock-up Period. Also, pursuant to the Lock-up Option Agreement, we have granted each Restricted Investor a put right (the “Put Right”), exercisable commencing on the expiration of the Lock-up Period and terminating on the second business day thereafter, pursuant to which each Locked-up Share may be put back to us at $10.30 per share, at the option of the Restricted Investor. We would then be required to purchase for $10.30 per share each Locked-up Share validly put back to us on the second business day following the valid exercise of the Put Right. The obligations of each Restricted Investor and Nautilus under the Lock-Up Option Agreements are irrevocable and binding; however the closing of the purchase of Lock-up Shares from the Restricted Investors pursuant to the Put Right is subject to the consummation of the Offer.

In addition, each of Astra Maritime Inc. (“Astra”) and Orca Marine Corp. (“Orca”), which are owned by Prokopios (Akis) Tsirigakis, our Chairman of the Board, Co-Chief Executive Officer and President, and George Syllantavos, our Co-Chief Executive Officer, Chief Financial Officer, Secretary, Treasurer and Director, respectively, Fjord Management S.A. (“Fjord”), which is jointly owned in equal parts by Messrs.

Tsirigakis and Syllantavos, respectively, and our initial shareholders (collectively with Orca, Astra and Fjord, our “Insiders”) have agreed not to tender any Common Shares owned by them pursuant to the Offer. See “The Offer — Purpose of the Offer; Certain Effects of the Offer” and “Certain Relationships and Related Transactions — Nautilus.”

Immediately following the Closing, we intend to conduct our business under the assumed name of “Nautilus Energy Services” until such time as we legally change our name to “Nautilus Energy Services Corp.”

Neither the SEC nor any state securities commission has approved or disapproved of these Common Shares or passed upon the accuracy or adequacy of this Offer to Purchase. Any representation to the contrary is a criminal offense.

Questions and requests for assistance regarding the Offer may be directed to Morrow & Co., LLC, as information agent (the “Information Agent”) for the Offer, at the address and telephone numbers set forth on the back cover of this Offer to Purchase. You may request additional copies of the Offer to Purchase, the Letter of Transmittal, and the other Offer documents from the Information Agent at the address and telephone numbers on the back cover of this Offer to Purchase. You may also contact your broker, dealer, commercial bank, trust company or nominee for copies of these documents.

December 7, 2012

IMPORTANT NOTICES REGARDING THE OFFER

On November 12, 2012, before we announced our intention to commence the Offer, we entered into a lock-up with put option agreement (each, a “Lock-Up Option Agreement”) with each of AQR Opportunistic Premium Offshore Fund, L.P. (“AQR OPOF”), AQR Diversified Arbitrage Fund (“AQR DAF”), Hare & Co. (“H&C”) and CNH Diversified Opportunities Master Account (“CNH”, and together with AQR OPOF, AQR DAF and H&C, the “Restricted Investors”) for 439,500, 54,300, 32,600 and 16,300 Common Shares, respectively, for an aggregate of 542,700 Common Shares (the “Locked-up Shares”), representing approximately 11.3% of the Common Shares issued in our IPO. Pursuant to the Lock-Up Option Agreements, each Restricted Investor agreed not to tender its respective Locked-up Shares in this Offer. In addition, during the period commencing on November 12, 2012 and terminating on the 11th business day following the Expiration Date (the “Lock-up Period”), each Restricted Investor is also prohibited from selling, transferring or otherwise disposing of the Lock-up Shares during the Lock-up Period. Also, pursuant to the Lock-up Option Agreement, we have granted each Restricted Investor a put right (the “Put Right”), exercisable commencing on the expiration of the Lock-up Period and terminating on the second business day thereafter, pursuant to which each Locked-up Share may be put back to us at $10.30 per share, at the option of the Restricted Investor. We would then be required to purchase for $10.30 per share each Locked-up Share validly put back to us on the second business day following the valid exercise of the Put Right. The obligations of each Restricted Investor and Nautilus under the Lock-Up Option Agreements are irrevocable and binding; however the closing of the purchase of Lock-up Shares from the Restricted Investors pursuant to the Put Right is subject to the consummation of the Offer. The Lock-up Option Agreement does not affect the Restricted Investors’ rights to redemption in the event of any liquidation.

If the Offer is consummated, we will deposit the aggregate purchase price for the Locked-Up Shares in a separate escrow account to be created solely to hold such funds. If all Locked-up Shares are validly put back to us, we would purchase the same with the $5,589,810 on deposit in such escrow account. If none of the Restricted Investors exercises its Put Right, the $5,589,810 then on deposit in such escrow account would be released to us without restriction.

Each Restricted Investor has also agreed that during the Lock-up Period, it shall be prohibited from directly or indirectly purchasing, offering to purchase, promising to purchase or entering into any agreement or contract to purchase any Common Shares.

If you desire to tender all or any portion of your Common Shares, you must do one of the following before the Offer expires:

| • | if your Common Shares are registered in the name of a broker, dealer, commercial bank, trust company or other nominee, you must contact the nominee and have the nominee tender your Common Shares for you; |

| • | if you hold certificates for Common Shares registered in your own name, you must complete and sign the enclosed Letter of Transmittal according to its instructions and deliver it, together with any required signature guarantees, the certificates for your Common Shares and any other documents required by the Letter of Transmittal, to the Depositary identified on the back cover of this Offer to Purchase; or |

| • | if you are an institution participating in The Depository Trust Company, you must tender your Common Shares according to the procedure for book-entry transfer described in “The Offer — Procedures for Tendering Shares” of this Offer to Purchase. |

To validly tender Common Shares pursuant to the Offer, other than Common Shares registered in the name of a broker, dealer, commercial bank, trust company or other nominee, you must properly complete and duly execute the Letter of Transmittal.

We are not making the Offer to, and will not accept any tendered Common Shares from shareholders in any jurisdiction where it would be illegal to do so. However, we may, at our discretion, take any actions necessary for us to comply with the applicable laws and regulation to make the Offer to shareholders in any such jurisdiction.

We have not authorized any person to make any recommendation on our behalf as to whether you should tender or refrain from tendering your Common Shares pursuant to the Offer. You should rely only on the information contained in this Offer to Purchase and in the Letter of Transmittal or to which we have referred you. We have not authorized anyone to provide you with information or to make any representation in connection with the Offer other than those contained in this Offer to Purchase or in the Letter of Transmittal. If anyone makes any recommendation or gives any information or representation regarding the Offer, you must not rely upon that recommendation, information or representation as having been authorized by us, our board of directors, the Depositary or the Information Agent for the Offer. You should not assume that the information provided in this Offer to Purchase is accurate as of any date other than the date as of which it is shown, or if no date is otherwise indicated, the date of this Offer to Purchase.

Questions and requests for assistance should be directed to Morrow & Co., LLC, the information agent for the Offer, at its address and telephone numbers set forth below and on the back cover of this Offer to Purchase. Additional copies of this Offer to Purchase, the Letter of Transmittal, and other materials related to the Offer may also be obtained for free from Morrow & Co., LLC. Copies of this Offer to Purchase, the Letter of Transmittal, and any other material related to the Offer may also be obtained at the website maintained by the SEC atwww.sec.gov. You may also contact your broker, dealer, commercial bank, trust company or other nominee for assistance. See “Where You Can Find More Information.”

The Information Agent for the Offer is:

Morrow & Co., LLC

470 West Avenue, 3rd Floor,

Stamford, CT 06902

Telephone: (800) 662-5200

Banks and brokerage firms: (203) 658-9400

470 West Avenue, 3rd Floor,

Stamford, CT 06902

Telephone: (800) 662-5200

Banks and brokerage firms: (203) 658-9400

| Page | |||||||

|---|---|---|---|---|---|---|---|

| 1 | |||||||

| 15 | |||||||

| �� | 17 | ||||||

| 39 | |||||||

| 42 | |||||||

| 44 | |||||||

| 46 | |||||||

| 54 | |||||||

| 63 | |||||||

| 65 | |||||||

| 72 | |||||||

| 89 | |||||||

| 93 | |||||||

| 95 | |||||||

| 97 | |||||||

| 101 | |||||||

| 106 | |||||||

| 111 | |||||||

| 114 | |||||||

| 132 | |||||||

| 135 | |||||||

| 136 | |||||||

| 142 | |||||||

| 147 | |||||||

| 150 | |||||||

| 154 | |||||||

| 154 | |||||||

| F-1 | |||||||

Annex I — Share Purchase Agreement, dated as of December 5, 2012 by and among Nautilus Marine Acquisition Corp., Assetplus Limited and the Sellers identified therein. | |||||||

This summary term sheet highlights important information regarding the Offer (the “Offer”) described in this Offer to Purchase for cash (the “Offer to Purchase”), our Common Shares and the Acquisition (each as defined below). To understand the Offer and the Acquisition fully and for a more complete description of the terms of the Offer to Purchase and the Acquisition, you should carefully read the entire Offer to Purchase, including any Annexes, and the Letter of Transmittal (“Letter of Transmittal”) that constitute the Offer. We have included references to the sections of this Offer to Purchase where you will find a more complete description of the topics addressed in this summary term sheet.

Common Shares Subject of this Offer | Up to 4,137,300 shares of common stock, par value $0.0001 per share, of Nautilus Marine Acquisition Corp. (the “Common Shares”). However, in accordance with the rules of the Securities and Exchange Commission (the “SEC”), in the event that more than 4,137,300 Common Shares are validly tendered and not properly withdrawn, we may exercise our right to amend the Offer to accept for payment an additional amount of shares not to exceed 2% of our issued and outstanding Common Shares without extending the Expiration Date (as defined below) (such amendment, the “2% Amendment”), and thereby accept for payment all Common Shares which may be validly tendered in this Offer. | |||||

Price Offered Per Common Share | $10.10 net to the seller in cash, without interest thereon (the “Purchase Price”). | |||||

Scheduled Expiration of Offer | 11:59 p.m., New York City time, on Monday, January 7, 2013, unless the Offer is otherwise extended, which may depend on the timing and process of the SEC review of the Offer to Purchase, or terminated (the “Expiration Date”). | |||||

Party Making the Offer | Nautilus Marine Acquisition Corp., a Marshall Islands corporation. | |||||

For further information regarding the Offer, see “The Offer” beginning on page 72.

General

Who is offering to purchase the Common Shares?

Nautilus Marine Acquisition Corp. (which intends to do business under the assumed name of “Nautilus Energy Services” until such time as its name is legally changed) (“Nautilus”, the “Company”, “we,” “us” or “our”) is offering to purchase the Common Shares. For additional information on Nautilus, see “Business of Nautilus.”

What Common Shares are sought?

We are offering to purchase up to 4,137,300 of the outstanding Common Shares. The Offer is not conditioned on any minimum or maximum number of Common Shares being tendered by our shareholders. However, in accordance with the rules of the SEC, in the event that more than 4,137,300 Common Shares are validly tendered and not properly withdrawn, we may elect to exercise our right to accept for payment additional Common Shares pursuant to the 2% Amendment without extending the Expiration Date. Any additional purchases pursuant to the 2% Amendment would allow us to accept for payment all Common Shares which may be validly tendered in this Offer. See “Summary Term Sheet and Questions

1

and Answers — Why is the Offer for 4,137,300 Common Shares?” and “— What if more than 4,137,300 Common Shares are validly tendered in this Offer?”

Unless otherwise expressly stated, this Offer to Purchase assumes that no more than 4,137,300 Common Shares will be accepted for payment in this Offer, and that Nautilus will not elect to exercise its rights pursuant to the 2% Amendment to purchase any additional shares.

Why is the Offer for 4,137,300 Common Shares?

Pursuant to our articles of incorporation, as amended (the “Articles of Incorporation”) and the Business Corporations Act of the Republic of Marshall Islands (the “BCA”), Nautilus may consummate a business transaction without shareholder approval by providing all holders of its Common Shares with the opportunity to redeem their Common Shares through a tender offer pursuant to the tender offer rules promulgated under the Securities Exchange Act of 1934, as amended (the “Exchange Act”). This Offer is being made in part to provide Nautilus shareholders with such opportunity to redeem their Common Shares and to allow the Acquisition to be completed without a shareholder vote. In connection therewith, and as set forth in our SEC filings, we may accept for payment up to 4,257,425 validly tendered and not properly withdrawn Common Shares (approximately 88% of our public Common Shares) and still consummate our initial business transaction. Of our 6,000,000 issued and outstanding Common Shares, certain of our shareholders have agreed not to tender an aggregate of 1,742,700 Common Shares. See “Summary Term Sheet and Questions and Answers — What if more than 4,137,300 Common Shares are validly tendered in this Offer?” and “Additional Material Related Agreements — Lock-up Option Agreements”. Accordingly, an aggregate of 4,257,300 Common Shares may be validly tendered in this Offer, which exceeds by 120,000 the number of Common Shares we are offering to purchase. In the event more than 4,137,300 Common Shares are validly tendered in this Offer, we may exercise our right pursuant to the 2% Amendment to purchase up to 120,000 additional Common Shares without extending the Expiration Date, thereby permitting us to accept for payment up to an aggregate of 4,257,300 Common Shares and still consummate the Acquisition (as defined hereinafter). See “The Offer — Purpose of the Offer; Certain Effects of the Offer.”

What if more than 4,137,300 Common Shares are validly tendered in this Offer?

No more than 4,257,300 Common Shares may be validly tendered in this Offer, and this Offer is for 4,137,300 Common Shares. Because the total number of Common Shares which may be validly tendered does not exceed the sum of the 4,137,300 Common Shares subject to this Offer plus up to an additional 120,000 Common Shares that we may accept for payment pursuant to the 2% Amendment, our election to exercise our rights pursuant to the 2% Amendment will permit us to accept for payment up to all 4,257,300 validly tendered and not properly withdrawn Common Shares without extending the Expiration Date and still consummate the Acquisition.

Although we have 6,000,000 Common Shares issued and outstanding, it isimpossible for more than 4,257,300 Common Shares to be validly tendered in this Offer. This is because holders of an aggregate of 1,742,700 Common Shares have agreed not to tender their shares as follows : (i) an aggregate of 1,200,000 Common Shares held by Astra Maritime Inc. (“Astra”) and Orca Marine Corp. (“Orca”), which are owned by Prokopios (Akis) Tsirigakis, our Chairman of the Board, Co-Chief Executive Officer and President and George Syllantavos, our Co-Chief Executive Officer, Chief Financial Officer, Secretary, Treasurer and Director, respectively, Fjord Management S.A. (“Fjord”), which is jointly owned in equal parts by Messrs. Tsirigakis and Syllantavos, respectively, and our initial shareholders (collectively with Orca, Astra and Fjord, our “Insiders”), are subject of an agreement entered into by the Insiders in connection with our initial public offering (the “IPO”), not to tender their shares, and (ii) an aggregate of 542,700 Common Shares, equal to approximately 11.3% of the Common Shares issued in our IPO (the “Locked-up Shares”) have been locked-up pursuant to those certain lock-up with put option agreement (each, a “Lock-up Option Agreement”) that we entered into with each of AQR Opportunistic Premium Offshore Fund, L.P. (“AQR OPOF”), AQR Diversified Arbitrage Fund (“AQR DAF”), Hare & Co. (“H&C”) and CNH Diversified Opportunities Master Account (“CNH”, and together with AQR OPOF, AQR DAF and H&C, the “Restricted Investors”) for 439,500, 54,300, 32,600 and 16,300 Common Shares, respectively, on November 12, 2012, before we announced our intention

2

to commence the Offer. Pursuant to the Lock-Up Option Agreements, each Restricted Investor agreed not to tender its respective Locked-up Shares in this Offer. In addition, during the period commencing on November 12, 2012 and terminating on the 11th business day following the Expiration Date (the “Lock-up Period”), each Restricted Investor is also prohibited from selling, transferring or otherwise disposing of the Lock-up Shares during the Lock-up Period. Also, pursuant to the Lock-up Option Agreement, we have granted each Restricted Investor a put right (the “Put Right”), exercisable commencing on the expiration of the Lock-up Period and terminating on the second business day thereafter, pursuant to which each Locked-up Share may be put back to us at $10.30 per share, at the option of the Restricted Investor. We would then be required to purchase for $10.30 per share each Locked-up Share validly put back to us on the second business day following the valid exercise of the Put Right. The obligations of each Restricted Investor and Nautilus under the Lock-Up Option Agreements are irrevocable and binding; however the closing of the purchase of Lock-up Shares from the Restricted Investors pursuant to the Put Right is subject to the consummation of the Offer. The Lock-up Option Agreement does not affect the Restricted Investors’ rights to redemption in the event of any liquidation. See “Additional Material Related Agreements — Lock-up Option Agreements”.

However, if more than 4,137,300 Common Shares are validly tendered and not properly withdrawn, and we do not exercise our right pursuant to the 2% Amendment to purchase additional Common Shares, or if we are unable to satisfy the Acquisition Condition (as defined below), we may amend, terminate or extend the Offer. If we terminate the Offer, we willNOT: (i) purchase any Common Shares pursuant to this Offer or (ii) consummate the Acquisition (as defined below) in accordance with the terms of the Share Purchase Agreement described in this Offer to Purchase. Common Shares tendered pursuant to the Offer but not purchased in the Offer will be returned at our expense promptly following the expiration or termination of the Offer.

Like other tender offers commenced by special purpose acquisition corporations (“SPACs”), is the Offer subject to a “maximum tender condition”?

No. Unlike other tender offers commenced by SPACs, our Offer isnot subject to a “maximum tender condition”. Typically, a “maximum tender condition” is a nonwaivable condition to a tender offer that requires the offeror to extend or terminate its offer, and leaves the offeror unable to consummate its business combination in the event that more shares are validly tendered and not properly withdrawn than the offeror has offered to purchase. Here, there is no such condition. This is because holders of 1,742,700 Common Shares have agreed not to tender their shares in this Offer, and, in accordance with the rules of the SEC, we may exercise our right pursuant to the 2% Amendment to purchase additional Common Shares without extending the Expiration Date, we may purchase all Common Shares validly tendered in this Offer. Accordingly, we are not subject to a maximum tender condition. See “Summary Term Sheet and Questions and Answers — What if more than 4,137,300 Common Shares are validly tendered in this Offer?”

Why is Nautilus tendering for its Common Shares if Nautilus’s board recommends that I DO NOT tender my shares?

Nautilus commenced this Offer because it (i) cannot consummate the Acquisition if this Offer is not consummated prior to or concurrently with the closing of the Acquisition and (ii) is required pursuant to its Articles of Incorporation to allow shareholders who do not support the Acquisition contemplated by the Share Purchase Agreement and the other transactions contemplated thereby (collectively, the “Transaction”) an opportunity to tender their Common Shares to us for purchase.

How is the Offer different from typical tender offers?

Typically an issuer or a third party commencing a tender offer wants to purchase the entire amount of the securities they are offering to purchase, oftentimes to facilitate a business purpose, such as a business transaction. In this case, Nautilus doesnot want shareholders of Nautilus to tender Common Shares, and Nautilus’s board of directors recommends that existing shareholdersnot tender their Common Shares after they review this Offer to Purchase.

3

In addition, unlike a typical tender offer, there will be no proration. This is because we are offering to purchase 4,137,300 Common Shares, and in the event Common Shares in excess of such amount are validly tendered in this Offer, we would either exercise our right pursuant to the 2% Amendment to purchase all such shares without extending the Expiration Date, or amend, terminate or extend the Offer. Further, the Restricted Investors have agreed not tender their 542,700 Locked-Up Shares, and the Insiders agreed not to tender their 1,200,000 Common Shares, thereby limiting the number of Common Shares which may be validly tendered in this Offer. However, in the event that more than 4,137,300 Common Shares are validly tendered and we do not exercise the 2% Amendment, or our management is not reasonably certain on the Expiration Date that the Acquisition is capable of being consummated, then we may terminate or extend the Offer. Shareholders have the right, pursuant to our Articles of Incorporation to a pro rata portion of our Trust Account (as defined below), absent a business combination, only in the event of our liquidation. Consequently, if we terminate the Offer, we will NOT: (i) purchase any Common Shares pursuant to this Offer or (ii) consummate the Acquisition in accordance with the terms of the Share Purchase Agreement, and we will promptly return all Common Shares delivered pursuant to this Offer upon expiration or termination of the Offer.

What is the background of Nautilus?

Nautilus was formed in November 2010 pursuant to the laws of the Republic of the Marshall Islands for the purpose of acquiring, through a merger, capital stock exchange, asset acquisition, stock purchase, reorganization, exchangeable share transaction or other similar business transaction with one or more operating businesses or assets. Nautilus consummated its IPO of 4,800,000 units, where each unit (a “Unit”) consisted of one Common Share and one Warrant to purchase one Common Share (a “Warrant”), on July 20, 2011. On August 29, 2011, our Units automatically separated into Common Shares and Warrants, and following such separation, our Units ceased trading. The net proceeds of the IPO, together with $2,331,000 from Nautilus’s sale of 3,108,000 Warrants (the “Insider Warrants”) to the Insiders plus $480,000 in deferred underwriting commissions and discounts and $100,000 in deferred legal fees, for an aggregate of $48,480,000, were deposited in a trust account (the “Trust Account”) pending completion by Nautilus of an initial business transaction. If Nautilus does not consummate its initial business transaction by February 14, 2013, it must liquidate the Trust Account (including all deferred fees deposited therein) to the holders of the Common Shares issued in its IPO (our “public shareholders”) and dissolve. See “Information About the Companies” and “Business of Nautilus.”

Is there a Share Purchase Agreement related to the Offer?

Yes. On December 5, 2012, Nautilus entered into a Share Purchase Agreement (as it may be amended from time to time, the “Share Purchase Agreement”) with Assetplus Limited (“Assetplus”), and each of Vega Resource Group AS (“Vega Resource”) and Oil and Gas Ships Investor Limited (“Oil & Gas”, and together with Vega Resource, the “Sellers”) as ultimate beneficial owners of 100% of the issued and outstanding equity shares of Assetplus, pursuant to which Nautilus would acquire 100% of the issued and outstanding equity shares of Assetplus, and Assetplus will become a wholly-owned subsidiary of Nautilus (the “Acquisition”). Upon consummation of the Acquisition, Nautilus will indirectly own all of the issued and outstanding equity interests of Vega Offshore AS, a Norwegian company (“Vega Offshore”) and the vessel owning subsidiaries, Vega Corona AS, a Norwegian company, Vega Crusader AS, a Norwegian company, Vega Juniz AS, a Norwegian company and Vega Emtoli AS, a Norwegian company (collectively, the “Vessel Owning Subsidiaries”, and together with Vega Offshore, the “Subsidiaries”), which own or are parties to binding agreements to acquire: (i) two (2) platform supply vessels (“PSVs”) (Vega Crusader and Vega Corona) and (ii) two (2) oil spill response vessels (“OSRVs”) (Vega Juniz and Vega Emtoli). In addition, Nautilus would acquire, through its ownership of Assetplus, six (6) binding time charter agreements with Petróleo Brasileiro S.A. or its affiliates (“Petrobras”) for two PSVs (platform supply vessels) and four OSRVs (oil spill response vessels), respectively. Pursuant to our Articles of Incorporation and the BCA, Nautilus is permitted to consummate the Acquisition without shareholder approval by providing all holders of its Common Shares with the opportunity to redeem their Common Shares through a tender offer pursuant to the tender offer rules promulgated under the Exchange Act. See “The Share Purchase Agreement.”

4

Who are Assetplus and the Sellers?

Assetplus is a limited liability company incorporated under the laws of Cyprus. Assetplus (a development stage company) is a holding company and was organized on August 10, 2012 for the purpose of aggregating under one holding company all time charter, vessel acquisition or other contracts awarded to Vega Offshore and the Vessel Owning Subsidiaries and to facilitate implementation of such contracts. Assetplus is the holding company that owns all of the issued and outstanding shares of capital stock of each of Vega Offshore and the Vessel Owning Subsidiaries. All the Subsidiaries were organized under the laws of Norway. Vega Offshore and/or the Vessel Owning Subsidiaries own or are parties to binding agreements to acquire: (i) two PSVs (platform supply vessels) (Vega Crusader and Vega Corona) and (ii) two OSRVs (oil spill response vessels) (Vega Juniz and Vega Emtoli). Further, Assetplus, through Vega Offshore, is a party to six binding time charter agreements with Petrobras for two PSVs and four OSRVs, respectively (collectively, the “Time Charters”). Each Time Charter is for an initial period of four years, plus an option pursuant to which Petrobras may extend the term for additional four years. As is customary for Petrobras long period time charter contracts entered into with non-Brazilian flagged vessels, such as the Time Charters, the Time Charters contain a so-called ‘ANTAQ clause’ (ANTAQ are regulations issued by the Brazilian Water Transportation Authority) providing Petrobras with the right to terminate the Time Charter, upon 45 days notice, after the passage of 365 days, in case the vessel loses its ANTAQ license to operate in Brazilian waters. To the knowledge of Nautilus and Assetplus, this clause has never been invoked against a vessel operating in Brazil. Assetplus, through Vega Offshore and/or the Vessel Owning Subsidiaries, intends to identify and control either through direct purchase or charter an additional two (2) vessels to service the remaining two (2) OSRV Petrobras time charter contracts for which it has not yet secured vessels. Under the terms of the two (2) remaining Time Charters for which Assetplus has not yet secured vessels, if Assetplus fails to deliver the required vessels on or prior to January 14, 2013, Petrobras has the right to terminate such Time Charters. However, management expects that Petrobras will extend the cancellation date of such Time Charters for an additional period of five months, similar to the non-cancellation letters Petrobras has provided to Vega Offshore for Vega Crusader and Vega Corona. See “Business of Assetplus” and “Management of Assetplus”.

The Sellers who ultimately beneficially own all of the issued and outstanding equity shares of Assetplus, and are Vega Resource and Oil and Gas.

Vega Resource is the holding company of the Vega group of companies, which include Vega Offshore Management AS, the commercial manager of the Assetplus fleet. Prior to its acquisition by Assetplus, Vega Offshore was a subsidiary of Vega Resource. Upon consummation of Assetplus’s acquisition of all the equity interests in Vega Offshore and the Vessel Owning Subsidiaries, Assetplus became the parent of each of Vega Offshore and the Vessel Owning Subsidiaries, and indirectly owns Vega Offshore’s contracts, including the Time Charters, and owns or is a party to binding agreements to acquire the Vessel Owning Subsidiaries’ fleet of two PSVs and two OSRVs.

Vega Resource has bid on two additional time charter contracts with Petrobras for two PSVs, and expects such time charters to be awarded in the first quarter of 2013. In connection therewith, Nautilus has entered into an exclusive option agreement with Vega Resource, pursuant to which Nautilus has been granted the exclusive option following the closing of the Acquisition to acquire said time charters from Vega Resource if the same are awarded to Vega Resource (the “Exclusive Option Agreement”). See “Additional Material Related Agreements — Exclusive Option Agreement”.

What is the Structure of the Acquisition and the Acquisition Consideration?

Upon closing of the Acquisition (the “Closing”), subject to the terms of the Share Purchase Agreement, all issued and outstanding securities of Assetplus will be wholly owned by Nautilus. Nautilus, through Assetplus, will indirectly own 100% of the equity securities of each of Vega Offshore and the Vessel Owning Subsidiaries. Upon the Closing, the Sellers will be collectively entitled to receive cash and other forms of consideration (the “Acquisition Consideration”), subject to certain terms and conditions described in the Share Purchase Agreement and this Offer to Purchase, as follows:

| • | At or immediately following the Closing: |

5

| • | Nautilus will issue to the Sellers an aggregate of 1,722,773 Common Shares, valued at $10.10 per share, representing a total value of $17,400,007 (the “Initial Stock Payment” or “Equity Consideration”); |

| • | Nautilus will issue an aggregate of 594,059 Common Shares (equal to $6,000,000 in value at $10.10 per Common Share) (the “Put Shares”) to Mezzanine Financing Investment III Ltd. (“Mezzanine Financing”) in full satisfaction of (i) the $5,000,000 in loan proceeds drawn down by Assetplus on November 19, 2012 pursuant to that certain working capital loan agreement dated as of November 16, 2012, by and between Assetplus and Mezzanine Financing (the “Working Capital Facility”), and (ii) all interest and original issue discount (“OID”) amounts on such loan. The Put Shares will be covered by a six month put option (the “Put Option”), exercisable by Mezzanine Financing upon no less than 60 days prior written notice (the “Notice Period”), which notice is deliverable no earlier than the last day of the four month period following the consummation of this Offer. Upon valid exercise of the Put Option, Nautilus will purchase up to all 594,059 Put Shares from Mezzanine Financing at a price of $11.35 per Common Share in cash, which is equal to $6,742,570 (the “Put Option Value”) if the Put Option is validly exercised for all Put Shares. The Notice Period will allow Nautilus to attempt to arrange for a private transfer of the Put Shares from Mezzanine Financing to one or more third parties (the “Put Sale”). If a timely Put Sale is completed, Mezzanine Financing will receive the Put Option Value (with Nautilus contributing to Mezzanine Financing the shortfall, if any, between the actual proceeds from the Put Sale and the Put Option Value). If Nautilus is unable to complete a Put Sale during the Notice Period, Nautilus shall purchase the Put Shares from Mezzanine Financing at the Put Option Value on the final day of the Notice Period; and |

| • | Nautilus will assume, upon the Closing, the obligation to repay the outstanding indebtedness of Assetplus and its subsidiaries (collectively, the “Assumed Indebtedness”), the aggregate amount of which shall not exceed an amount of principal equal to $52,220,000 as of the Closing (the “Debt Assumption Amount”). The Assumed Indebtedness will be comprised of the following: (i) a Senior Debt Facility (as defined hereinafter) with a maximum availability of $38,220,000 and an outstanding principal balance as of the date hereof of $15,275,000; (ii) a mezzanine debt facility (comprised of one senior and one junior loan facility agreement) with an outstanding balance of $14,000,000 (collectively, the “Mezzanine Facility”); and (iii) any accrued and unpaid interest and OID on the amounts set forth in each of (i) and (ii) above. |

| • | Subsequent to the Closing, Nautilus will pay to the Sellers an aggregate of $7,150,000 in cash (the “Cash Payment” or “Cash Consideration”), either: (i) within fifteen (15) days following the Expiration Date, interest free, or (ii) within ninety (90) days following the Expiration Date, together with a 10% annual interest rate (interest to be applied beginning on the sixteenth (16th) day following the Expiration Date). The determination whether to make the Cash Payment pursuant to clause (i) or (ii) above is solely in the discretion of Nautilus. Upon receipt of the Cash Payment from Nautilus, the Sellers shall immediately pay an aggregate of $2,800,000 to Mezzanine Financing, on behalf of Assetplus, as partial repayment of the outstanding amounts on the Mezzanine Facility. |

| • | The Sellers will also be entitled to receive up to an aggregate of $6,315,040 worth of additional Common Shares (the “Earn-Out Payment” or “Contingent Consideration”) as additional consideration for the purchase of their equity interest in Assetplus if Nautilus achieves consolidated EBITDA (defined as gross revenue minus commissions minus vessel operating expenses on an annualized basis) derived from the four-vessel fleet of two PSVs and two OSRVs for the fiscal year ending December 31, 2013 equal to or in excess of $18,000,000 (the “EBITDA Earn-Out Threshold”). The Earn-Out Payment is based on a per share price equal to the greater of: (i) the 45-day value weighted average price on the issuance date and (ii) $10.10 per share. The Earn-Out Payment will be made within 30 days following the filing of Nautilus’s Form 20-F annual report for fiscal year ending December 31, 2013 (the “2013 Annual Report”). In the event that Assetplus acquires additional OSRV vessels to service the two remaining Petrobras Time Charters, then Sellers will be entitled to receive up to an aggregate of $1,614,980 worth of additional Common Shares per additional vessel (the “Additional Earn-Out Payment” or “Additional |

6

| Contingent Consideration”) if Nautilus achieves per additional vessel EBITDA for the fiscal ending December 31, 2013 equal to or in excess of $5,000,000 per additional vessel (the “Additional EBITDA Earn-Out Threshold”). |

| • | In the event that Sellers determine, prior to Closing, to acquire any vessels (and related indebtedness secured thereby) in addition to the four vessels they own (or have the right to acquire) at the time of the Share Purchase Agreement, then the parties will renegotiate the Acquisition Consideration to reflect such change in the net worth of Assetplus and its Subsidiaries. If an agreement regarding the adjustment is not reached by both parties, then Sellers will not acquire any such additional vessels prior to Closing. |

See “The Transaction,” “The Share Purchase Agreement” and “Description of Securities.”

The diagram below depicts our organizational structure immediately following this Offer and the Transaction. The voting percentages provided below (i) do not reflect the issuance of Common Shares for the Contingent Consideration, which are only issuable upon the attainment of certain financial targets that have not yet been met, (ii) assume that no shareholders tender their Common Shares pursuant to this Offer; (iii) assume that no Warrants are exercised (including the 3,108,000 Insider Warrants and any warrants issuable to Messrs. Tsirigakis and Syllantavos upon conversion of promissory notes issued to them by Nautilus); (iv) assume that no Common Shares are issued pursuant to the First Equity Incentive Plan; (v) assume that 500,000 Insider Shares were forfeited by certain of the Insiders; (vi) assumes that 500,000 Common Shares were issued to Oil and Gas; and (vii) assume the Unit Purchase Option was not exercised.

Are there any restrictions on the transfer of Equity Consideration or Contingent Consideration?

Pursuant to the terms of the Share Purchase Agreement, each of the Sellers have agreed not sell or otherwise transfer the Equity Consideration for a period of 90 days after the consummation of the Acquisition, as defined in the Share Purchase Agreement. See “Share Purchase Agreement”.

The Contingent Consideration issuable upon satisfaction of EBITDA Earn-Out Threshold is not subject to any lock-up restrictions.

7

What assumptions have we made throughout this Offer to Purchase, including when disclosing ownership information?

Unless otherwise expressly stated, this Offer to Purchase assumes that no more than 4,137,300 Common Shares will be accepted for payment in this Offer, and that Nautilus will not elect to exercise its rights pursuant to the 2% Amendment to purchase any additional shares.

In addition, we have made several assumptions with respect to ownership of our Common Shares immediately following the consummation of the Acquisition. These assumptions impact certain calculations of post-transaction ownership and voting rights throughout this Offer to Purchase. Unless otherwise expressly stated, all such calculations relating to beneficial ownership and voting rights post-transaction (i) do not reflect the issuance of Common Shares for the Contingent Consideration, which are only issuable upon the attainment of certain financial targets that have not yet been met, (ii) assume that no shareholders tender their Common Shares pursuant to this Offer; (iii) assume that no Warrants are exercised (including the 3,108,000 Insider Warrants and any warrants issuable to Messrs. Tsirigakis and Syllantavos upon conversion of promissory notes issued to them by Nautilus); (vi) assume that no Common Shares are issued pursuant to the First Equity Incentive Plan; (v) assume that 500,000 Insider Shares were forfeited by certain of the Insiders; (vi) assumes that 500,000 Common Shares were issued to Oil and Gas; and (vii) assume the Unit Purchase Option was not exercised.

How will Nautilus fund the purchase of Common Shares in the Offer?

Nautilus will use up to $41,786,730 of the $48,480,000 of funds raised in connection with its IPO, which funds are currently held in the Trust Account for the benefit of our public shareholders and which funds will become available to us upon consummation of the Acquisition, to purchase up to 4,137,000 Common Shares validly tendered and not withdrawn in the Offer. See “The Offer — Source and Amount of Funds.”

In the event that more than 4,137,300 Common Shares are validly tendered in this Offer, and we elect to exercise our rights pursuant to the 2% Amendment to purchase such additional shares without extending the Expiration Date, Nautilus would fund the purchase of up to 120,000 additional Common Shares from that certain Standby Debt Facility (the “Standby Facility”) dated December 5, 2012 and established by Orca and Astra in favor of Nautilus, at the request of Nautilus. Pursuant to the Standby Facility, Nautilus may draw down an amount equal to the lesser of: (i) $1.212 million or (ii) an amount equal to the product of the aggregate number of Common Shares validly tendered and not properly withdrawn pursuant to the Offer in excess of 4,137,300 Common Shares, multiplied by $10.10. See “The Offer — Sources and Amount of Funds” for a further description of the Standby Facility.

How will Nautilus fund the Cash Consideration payment required by the Share Purchase Agreement?

Pursuant to the Share Purchase Agreement, the Cash Consideration of $7.15 million payable by Nautilus to the Sellers is not due at Closing. Such amount is due, in the sole discretion of Nautilus, either: (i) within fifteen (15) days following the Expiration Date, interest free, or (ii) within ninety (90) days following the Expiration Date, with a 10% annual interest rate (interest to be applied beginning on the sixteenth (16th) day following the Expiration Date). As such, we believe that following the consummation of the Acquisition, we will have sufficient funds to satisfy such payment obligation from any combination of the amounts released to us from the Trust Account, our cash on hand, or our operations, each following the consummation of the Acquisition, or alternate sources of financing, if required.

Are the Offer and the Acquisition conditioned on one another?

Yes. Pursuant to the Share Purchase Agreement, it is a condition to the consummation of the Acquisition that the consummation of the Offer occurs prior to or concurrently with the Closing, and the Offer is subject to the condition that the Acquisition Condition (as described below) is satisfied. If the Acquisition Condition is not satisfied by the then scheduled Expiration Date, we will terminate or extend the Offer. In the event the Offer is terminated, we will promptly return any Common Shares, at our expense, that were delivered

8

pursuant to the Offer and we will be unable to consummate the Acquisition in accordance with the terms of the Share Purchase Agreement described in this Offer to Purchase. See “The Share Purchase Agreement.”

What is the most significant condition to the Offer?

Our obligation to purchase Common Shares validly tendered and not properly withdrawn at the Expiration Date is conditioned upon, among other things, the Acquisition, in our reasonable judgment to be determined as of immediately prior to the Expiration Date, being capable of being consummated contemporaneously with this Offer, but in no event later than three business days after the expiration of this Offer. For a description of the conditions to the Acquisition, see “Summary Term Sheet and Questions and Answers — What are the most significant conditions to the Acquisition?” below. We refer to this condition, which is not waivable, as the “Acquisition Condition”.

The conditions to the Offer, including the Acquisition Condition, which are in our control must be satisfied or waived by us at or prior to the Expiration Date. We refer to the conditions to the Offer, including the Acquisition Condition, as the “offer conditions.” See “The Offer — Conditions of the Offer.”

What are the most significant conditions to the Acquisition?

Pursuant to the Share Purchase Agreement, the consummation of the Acquisition is conditioned upon, among other things, (i) closing of the Offer prior to or concurrently with the Closing, (ii) Assetplus, together with its subsidiaries (including Vega Offshore and the Vessel Owning Subsidiaries), having outstanding indebtedness of not greater than $52,220,000, (iii) Nautilus delivering the Initial Stock Payment to the Sellers; (iv) Nautilus delivering the Put Shares to Mezzanine Financing; and (v) Sellers having delivered their shares of Assetplus to Nautilus. If these and/or any of the other conditions to the Acquisition are not met or waived, Assetplus or Nautilus, as the case may be, may choose to exercise any applicable right to terminate the Share Purchase Agreement. See “Risk Factors — Risks Related to the Transaction” and “The Share Purchase Agreement — Conditions to Closing the Transaction.”

Will there be a single controlling shareholder of Nautilus following the completion of the Acquisition?

No. However, immediately following the Acquisition the Sellers will collectively hold voting securities representing between approximately 26.7% of the voting power of Nautilus, in the event no Common Shares are validly tendered in the Offer, and approximately 53.2% of the voting power of Nautilus in the event 4,137,300 Common Shares are validly tendered and accepted for purchase in the Offer, and no Warrants are exercised, and without giving effect to any issuance of the Contingency Consideration. See “Beneficial Ownership of Nautilus Securities” for more detail on the beneficial ownership of Nautilus following the Acquisition, “The Share Purchase Agreement — Acquisition Consideration to be Delivered” for a further description of the Contingency Consideration and “— What assumptions have we made throughout this Offer to Purchase, including when discussing ownership information?” for a further description of assumptions relating to ownership and voting interests.

What is our business objective?

Our business objective is to acquire Assetplus. Upon the consummation of this Offer, we will have satisfied the Acquisition Condition and be able to facilitate our business objective.

Why are we making the Offer?

We are making the Offer in connection with the Acquisition because the provisions of our Articles of Incorporation, as disclosed in the prospectus related to our IPO, and the Share Purchase Agreement require us to conduct the Offer for Common Shares to provide our shareholders an opportunity to redeem their Common Shares for a pro-rata portion of our Trust Account upon our consummation of a business transaction. We also represented that in connection with this redemption opportunity, we would provide our shareholders with offering documents that contained substantially the same financial and other information about our proposed business transaction and redemption rights that would otherwise be required under Regulation 14A of the

9

Exchange Act, which regulates the solicitation of proxies. Accordingly, we are making the Offer so that we may provide our shareholders with appropriate disclosure regarding the business and finances of Nautilus, Assetplus and the post-transaction company so that our shareholders can decide whether to hold their Common Shares, or ask that they be redeemed by us pursuant to this Offer if the offer conditions are satisfied.

Promptly following the scheduled Expiration Date, we will publicly announce whether the Acquisition Condition, and the other conditions to this Offer have been satisfied or waived and whether the Offer has been completed, extended or terminated. If such conditions are satisfied or waived, promptly after the Expiration Date Nautilus shall purchase and pay the Purchase Price for each Common Share validly tendered and not properly withdrawn. Upon consummation of the Acquisition, which shall occur no later than three business days following the Expiration Date, Nautilus will purchase 100% of the equity securities in Assetplus from the Sellers, and Assetplus will become a wholly-owned subsidiary of Nautilus. The Acquisition would be completed without a meeting of Nautilus’s shareholders pursuant to our Articles of Incorporation and the BCA. See “The Transaction”.

How long do I have to tender my Common Shares?

You may tender your Common Shares pursuant to the Offer until the Offer expires on the Expiration Date. Consistent with a condition of the Offer, Nautilus may need to extend the Offer depending on the timing and process of the SEC staff’s review of the Offer to Purchase and related materials. The Offer will expire on Monday, January 7, 2013, at 11:59 p.m., New York City time, unless we extend or terminate the Offer. See “The Offer — Number of Shares; Purchase Price; No Proration” and “— Extension of the Offer; Termination; Amendment.” If a broker, dealer, commercial bank, trust company or other nominee holds your Common Shares, it is likely the nominee has established an earlier deadline for you to act to instruct the nominee to accept the Offer on your behalf. We urge you to contact the broker, dealer, commercial bank, trust company or other nominee to find out the nominee’s deadline. See “The Offer — Procedures for Tendering Shares.”

Can the Offer be extended, amended or terminated and, if so, under what circumstances?

We may extend or amend the Offer to the extent we determine such extension or amendment is necessary or is required by applicable law or regulation. If we extend the Offer, we will delay the acceptance of any Common Shares that have been validly tendered and not properly withdrawn pursuant to the Offer. In accordance with the rules of the SEC, we may amend the Offer pursuant to the 2% Amendment without extending the Expiration Date. We can also terminate the Offer if any of the offer conditions listed in “The Offer — Conditions of the Offer” occur, or the occurrence thereof has not been waived. See “The Offer — Extension of the Offer; Termination; Amendment.”

How will I be notified if the Offer is extended, amended or terminated?

If the Offer is extended, we will make a public announcement of the extension no later than 9:00 a.m., New York City time, on the first business day after the previously scheduled Expiration Date. We will announce any material amendment to or termination of the Offer by promptly making a public announcement of the amendment or termination. An amendment of the Offer pursuant to the 2% Amendment, by itself, would not be deemed material. See “The Offer — Extension of the Offer; Termination; Amendment.”

How do I tender my Common Shares?

If you hold your Common Shares in your own name as a holder of record and decide to tender your Common Shares, you must deliver your Common Shares by mail or physical delivery and deliver a completed and signed Letter of Transmittal or an Agent’s Message (as defined in “The Offer — Procedures for Tendering Shares”) to American Stock Transfer & Trust Company (the “Depositary”) before 11:59 p.m., New York City time, on Monday, January 7, 2013, or such later time and date to which we may extend the Offer.

10

If you hold your Common Shares in a brokerage account or otherwise through a broker, dealer, commercial bank, trust company or other nominee (i.e., in “street name”), you must contact your broker or other nominee if you wish to tender your Common Shares. See “The Offer — Procedures for Tendering Shares” and the instructions to the Letter of Transmittal.

If you are an institution participating in The Depository Trust Company, you must tender your Common Shares according to the procedure for book-entry transfer described in “The Offer — Procedures for Tendering Shares” of this Offer to Purchase.

You may contact Morrow & Co., LLC (the “Information Agent”) or your broker for assistance. The address and telephone numbers for the Information Agent are set forth on the back cover of this Offer to Purchase. See “The Offer — Procedures for Tendering Shares” and the instructions to the Letter of Transmittal.

Can I tender my Warrants?

No. Nautilus is not offering to purchase its Warrants in the Offer. Furthermore, our Warrants are not exercisable until 30 days after the consummation of the Acquisition and therefore a Warrant holder will not be able to exercise his, her or its Warrants to purchase Common Shares and then tender the Common Shares into the Offer. See “Description of Securities”.

Until what time can I withdraw previously tendered Common Shares?

You may withdraw your tendered Common Shares at any time prior 11:59 p.m., New York City time, on Monday, January 7, 2013, or such later time and date to which we may extend the Offer.In addition, unless we have already accepted your tendered Common Shares for payment, you may withdraw your tendered Common Shares at any time after 11:59 p.m., New York City time on February 5, 2013.See “The Offer — Withdrawal Rights.”

How do I properly withdraw Common Shares previously tendered?

You must deliver, on a timely basis, a written notice of your withdrawal to the Depositary at the address appearing on the back cover page of this Offer to Purchase. Your notice of withdrawal must specify your name, the number of Common Shares to be withdrawn and the name of the registered holder of such Common Shares. Certain additional requirements apply if the certificates for Common Shares to be withdrawn have been delivered to the Depositary or if your Common Shares have been tendered under the procedure for book-entry transfer set forth in “The Offer — Procedures for Tendering Shares.” See “The Offer — Withdrawal Rights.”

Has Nautilus or its board of directors adopted a position on the Offer?

Our board of directors unanimously recommends that you donot accept the Offer for your Common Shares and therefore refrain from tendering your shares because our business objective is to consummate the Acquisition of Assetplus. Our board of directors supports and has approved the Acquisition of Assetplus. Furthermore, our board of directors has determined that the Acquisition is in the best interests of Nautilus and its shareholders and if consummated would constitute our initial business transaction pursuant to our Articles of Incorporation. The members of our board, which include Insiders, will directly benefit from the Transaction and have interests in the Transaction that may be different from, or in addition to, the interests of Nautilus’s public shareholders. See “The Transaction — Certain Benefits of Nautilus’s Directors and Officers and Others in the Transaction.”

What happens if I tender my Common Shares in the Offer?

If you tender your Common Shares into the Offer, you will not be participating in the Acquisition because you will no longer hold such Common Shares in Nautilus, which will be the public holding company for the operations of Assetplus following the consummation of the Acquisition. You must make your own

11

decision as to whether to tender your Common Shares and, if so, how many Common Shares to tender. In doing so, you should read carefully the information in this Offer to Purchase and in the Letter of Transmittal.

When and how will Nautilus pay for the Common Shares I tender that are accepted for payment?

We will pay the Purchase Price in cash, without interest, for the Common Shares we purchase promptly after the expiration of the Offer if the offer conditions are satisfied. We will pay for the Common Shares accepted for purchase by depositing the aggregate Purchase Price with the Depositary promptly after the expiration of the Offer provided that the offer conditions are met. The Depositary will act as your agent and will transmit to you the payment for all of your Common Shares accepted for payment. See “The Offer — Purchase of Shares and Payment of Purchase Price.”

Will I have to pay brokerage fees and commissions if I tender my Common Shares?

If you are a holder of record of your Common Shares and you tender your Common Shares directly to the Depositary, you will not incur any brokerage fees or commissions. If you hold your Common Shares in street name through a broker, bank or other nominee and your broker tenders Common Shares on your behalf, your broker may charge you a fee for doing so. We urge you to consult your broker or nominee to determine whether any charges will apply. See “The Offer — Procedures for Tendering Shares.”

What are the U.S. federal income tax consequences if I tender my Common Shares?

The receipt of cash for your tendered Common Shares will generally be treated for U.S. federal income tax purposes either as (i) a sale or exchange eligible for capital gain or loss treatment or (ii) a corporate distribution. See “The Offer — United States Federal Income Tax Consequences.”

Will I have to pay stock transfer tax if I tender my Common Shares?

We will not pay any stock transfer taxes in connection with this Offer. If you instruct the Depositary in the Letter of Transmittal to make the payment for the Common Shares to the registered holder, you may incur domestic stock transfer tax. See “The Offer — Purchase of Shares and Payment of Purchase Price.”

What will be the purchase price for the Common Shares and what will be the form of payment?

The Purchase Price for the Offer is $10.10 per share. All Common Shares we purchase will be purchased at the Purchase Price. See “The Offer — Number of Shares; Purchase Price; No Proration.” If your Common Shares are purchased in the Offer, you will be paid the Purchase Price, in cash, without interest, promptly after the Expiration Date. Our Articles of Incorporation require that we offer a price per Common Share equal to the amount held in the Trust Account from and after such date as of two days prior to the commencement of this Offerplus interest accrued in the Trust Account until two business days prior to the consummation of the Transaction, less taxes payable and less any interests earned on the proceeds placed in the Trust Account withdrawn by Nautilus for working capital purposes, divided by 4,800,000 Common Shares sold as part of the Units in our IPO. Although we do not anticipate any change to the Purchase Price, if we need to adjust the Purchase Price to comply with our Articles of Incorporation (to the extent that, for example, either the amount of interest income accrued on the Trust Account in excess of our outstanding tax liability would cause the per-IPO share pro-rata amount to exceed $10.10 per share or the amount currently held in the Trust Account is reduced), we will amend this Offer and extend the Expiration Date for at least 10 business days. Under no circumstances will we pay interest on the Purchase Price other than as required by our Articles of Incorporation, including but not limited to, by reason of any delay in making payment. See “The Offer — Number of Shares; Purchase Price; No Proration” and “— Purchase of Shares and Payment of Purchase Price.”

12

How will the Offer and issuance of the Acquisition Consideration affect the number of Common Shares outstanding and the number of holders of Nautilus?

As of the date of this Offer to Purchase, we had 6,000,000 outstanding Common Shares, of which 4,800,000 Common Shares were issued in the IPO and we had outstanding Warrants to acquire 7,908,000 Common Shares at an exercise price of $11.50 per share that will become exercisable 30 days after the consummation of the Acquisition. If no Common Shares are tendered, we will have approximately 8,316,832 Common Shares outstanding following the issuance of the Equity Consideration and Put Shares. If the Offer is fully subscribed, we will have approximately 4,179,532 Common Shares outstanding following the purchase of Common Shares tendered pursuant to the Offer and the issuance of the Equity Consideration and Put Shares. See “The Offer — Purpose of the Offer; Certain Effects of the Offer” and “Beneficial Ownership of Nautilus Securities.”

To the extent any of our shareholders validly tender all of their Common Shares (without subsequently properly withdrawing such tendered Common Shares) and that tender is accepted, the number of our holders would be reduced. See “The Offer — Purpose of the Offer; Certain Effects of the Offer.”

Will the Insiders or Restricted Investors tender their Common Shares in the Offer?

No. Our Insiders currently hold 1,200,000 Common Shares acquired prior to our IPO (the “Insider Shares”) and have agreed not to tender any of their Insider Shares pursuant to the Offer. The Restricted Investors hold an aggregate of 542,700 Locked-up Shares, and each has entered into a Lock-Up Option Agreement pursuant to which it has agreed not to tender any of its respective Locked-up Shares pursuant to the Offer. See “The Offer — Purpose of the Offer; Certain Effects of the Offer”.

What will happen if I do not tender my Common Shares?

Shareholders who choose not to tender their Common Shares will retain their Common Shares and have a greater percentage of ownership in our outstanding Common Shares following the completion of the Offer to the extent Common Shares are validly tendered and purchased pursuant to the Offer and the Acquisition is consummated; however, such Common Shares will be subject to dilution by the issuance of the Equity Consideration, and possibly the issuance of shares pursuant to the Earn-Out Payment and Nautilus’s First Equity Incentive Plan. “The Offer — Purpose of the Offer; Certain Effects of the Offer” and “Beneficial Ownership of Nautilus Securities.”

If I object to the price being offered for my Common Shares, will I have appraisal rights?

No appraisal rights will be available to you in connection with the Offer or the Acquisition. If the Acquisition is consummated, we will purchase all Common Shares validly tendered and not properly withdrawn. See “Appraisal Rights”.

What is the recent market price for the Common Shares?

On December 4, 2012, the last reported sale price on the Nasdaq Capital Market (“Nasdaq”) was $9.99 per Common Share. You are urged to obtain current market quotations for the Common Shares before deciding whether to tender your Common Shares. See “Price Range of Securities and Dividends.”

Will the Common Shares be listed on a stock exchange following the Acquisition?

Our Common Shares are currently quoted on the Nasdaq. There can be no assurance concerning our ability to meet Nasdaq’s continued qualification standards in the future. See “Risk Factors — Risks Related to the Offer” and “— Risks Related to Nautilus”.

13

What interests do Nautilus’s directors and officers and others have in the Transaction?

Nautilus’s directors and officers have interests in the Transaction that are different from, or in addition to, your interests as a shareholder. These interests include, among other things:

| • | If Nautilus is unable to consummate the Transaction, the 1,200,000 Insider Shares, which have a value of $11,988,000 based on a closing price of $9.99 on December 4, 2012, held by the Insiders will expire worthless; |

| • | If Nautilus is unable to consummate the Transaction, the 3,108,000 Insider Warrants, which have a value of $466,200 based on the last reported closing price of $0.15 as of December 4, 2012, held by the Insiders will expire worthless; |

| • | It is anticipated that two of Nautilus’s directors (Messrs. Tsirigakis and Syllantavos) will continue to serve as directors of Nautilus following the Acquisition; |

| • | In the event of Nautilus’s liquidation upon its failure to consummate a business transaction, our co-chief executive officers, namely, Mr. Tsirigakis and Mr. Syllantavos, may be liable to pay debts and obligations to vendors in the event such vendors have not waived claims brought against the Trust Account; |

| • | In the event of Nautilus’s liquidation upon its failure to consummate a business transaction without sufficient funds to pay costs associated with such liquidation, Messrs. Tsirigakis and Syllantavos have agreed to advance Nautilus the funds necessary to pay such costs; and |

| • | The underwriters of the IPO and counsel for Nautilus as well as advisors to Nautilus pursuant to advisory agreements with Nautilus will be entitled to payment of fees in cash associated with the IPO and/or the Transaction in the event the Acquisition occurs. |

See “The Transaction — Certain Benefits of Nautilus’s Directors and Officers and Others in the Transaction.”

Who do I contact if I have questions about the Offer?

For additional information or assistance, you may contact the Information Agent at the address and telephone numbers set forth on the back cover of this Offer to Purchase. You may request additional copies of this Offer to Purchase, the Letter of Transmittal and other Offer documents from the Information Agent at Morrow & Co., LLC, 470 West Avenue, 3rd Floor, Stamford, CT 06902; telephone (800) 662-5200 (banks and brokerage firms: (203) 658-9400).

14

Some of the statements in this Offer to Purchase constitute “forward-looking statements.” When used in this Offer to Purchase, the words “anticipate”, “believe”, “continue”, “could”, “estimate”, “expect”, “intend”, “may”, “might”, “plan”, “predict”, “potential” and “should”, as they relate to us are intended to identify these forward-looking statements. All statements by us regarding our expected or projected future financial position and operating results, our business strategy, our financing plans and expected capital requirements, forecasted trends relating to Assetplus’s products or the markets in which Assetplus operates and similar matters are forward-looking statements.

Forward-looking statements are not guarantees of future performance and are subject to risks, uncertainties and other factors (many of which are beyond our control), set forth in this section and elsewhere in this Offer to Purchase, that could cause actual results to differ materially from future results expressed or implied by such forward-looking statements. Our future results may differ materially from those expressed in these forward-looking statements. These risks, uncertainties and other important factors include, but are not limited to: