Table of Contents

As filed with the Securities and Exchange Commission on February 3, 2011

Registration No. 333-171331

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1

to

FORM S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

AMERICAN PETROLEUM TANKERS PARENT LLC

(Exact name of registrant as specified in Its Charter)

Delaware (State or other jurisdiction of incorporation or organization) | 4400 (Primary Standard Industrial Classification Code Number) | 90-0587372 (I.R.S. Employer Identification Number) |

American Petroleum Tankers Parent LLC

c/o The Blackstone Group L.P.

345 Park Avenue, 29th Floor

New York, NY 10154

(215) 435-9569

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

See Table of Co-Registrants below

(Address, including zip code, and telephone number, including area code, of co-registrant’s principal executive offices)

Philip J. Doherty, Chief Financial Officer c/o The Blackstone Group L.P. 345 Park Avenue, 29th Floor New York, NY 10154 (215) 435-9569 (Name, address, including zip code, and telephone number, including area code, of agent for service) | Copies to: Michael R. Littenberg, Esq. Schulte Roth & Zabel LLP 919 Third Avenue New York, NY 10022 Ph: (212) 756-2000 Fax: (212) 593-5955 |

Approximate Date of Commencement of Proposed Offer to the Public:

As soon as practicable after this registration statement becomes effective.

If the securities being registered on this form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box: ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier registration statement for the same offering: ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non accelerated filer | x (Do not check if a small reporting company) | Small reporting company | ¨ | |||

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

| Exchange Act Rule 13e-4(i) (Cross-Border Issuer Tender Offer) | ¨ | |

| Exchange Act Rule 14d-1(d) (Cross-Border Third-Party Tender Offer) | ¨ |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

Co-Registrants

Exact Name of Co-Registrant as specified in Its Charter(1) | State or Other Jurisdiction of Incorporation or Organization | Primary Standard Industrial Classification Code Number | I.R.S. Employer Identification Number | |||||||||

AP Tankers Co. (Co-Issuer) | Delaware | 4400 | * | |||||||||

American Petroleum Tankers Holding LLC (Guarantor) | Delaware | 4400 | 80-0583752 | |||||||||

American Petroleum Tankers LLC (Guarantor) | Delaware | 4400 | 20-5277827 | |||||||||

APT Intermediate Holdco LLC (Guarantor) | Delaware | 4400 | 80-0574121 | |||||||||

JV Tanker Charterer LLC (Guarantor) | Delaware | 4400 | 26-3932121 | |||||||||

PI 2 Pelican State LLC (Guarantor) | Delaware | 4400 | 26-4193280 | |||||||||

APT Sunshine State LLC (Guarantor) | Delaware | 4400 | 80-0574135 | |||||||||

| (1) | The address and telephone number of each of the co-registrants is c/o The Blackstone Group L.P., 345 Park Avenue, 29th Floor, New York, NY 10154, (215) 776-0173. |

| * | AP Tankers Co. is a pass-through entity which does not require an I.R.S. Employer Identification Number. |

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and we are not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, Dated February 3, 2011

PRELIMINARY PROSPECTUS

AMERICAN PETROLEUM TANKERS PARENT LLC

AP TANKERS CO.

$285,000,000

OFFER TO EXCHANGE

$285,000,000 in Aggregate Principal Amount of 10 1/4% First Priority Senior Secured Notes due 2015, Series B

for all outstanding

$285,000,000 in Aggregate Principal Amount of 10 1/4% First Priority Senior Secured Notes due 2015, Series A

The exchange offer will expire at 12:00 midnight, New York City time,

on , 2011, which is 20 business days after the commencement of the exchange offer, unless extended.

The Offering:

Offered securities: the securities offered by this prospectus are 10 1/4% First Priority Senior Secured Notes due 2015, Series B (the “New Notes”), which are being issued in exchange for 10 1/4% First Priority Senior Secured Notes due 2015, Series A (the “Original Notes” and, together with the New Notes, the “Notes”), sold by us in our private placement that we consummated on May 17, 2010. The New Notes are substantially identical to the Original Notes and are governed by the same indenture governing the Original Notes.

Expiration of offering: the exchange offer expires at 12:00 midnight, New York City time, on , 2011, which is 20 business days after the commencement of the exchange offer, unless extended.

We will exchange all Original Notes that are validly tendered and not withdrawn prior to the expiration of the exchange offer.

We will not receive any proceeds from the exchange.

Each broker-dealer that receives New Notes pursuant to the exchange offer must acknowledge that it will deliver a prospectus in connection with any resale of the New Notes. If the broker-dealer acquired the Original Notes as a result of market making or other trading activities, such broker-dealer must use the prospectus for the exchange offer, as supplemented or amended, in connection with resales of the New Notes. A broker-dealer that acquired Original Notes directly from us cannot exchange the Original Notes in the exchange offer.

The New Notes:

Maturity: The New Notes will mature on May 1, 2015.

Interest Payment Dates: Interest payment dates for the New Notes are May 1 and November 1, beginning on May 1, 2011.

See “Risk Factors,” beginning on page 11, for a discussion of some factors that should be considered by holders in connection with a decision to tender Original Notes in the exchange offer.

These securities have not been approved or disapproved by the Securities and Exchange Commission or any state securities commission nor has the Securities and Exchange Commission or any state securities commission passed on the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is , .

Table of Contents

| Page | ||||

| 1 | ||||

| 11 | ||||

| 30 | ||||

| 31 | ||||

| 32 | ||||

| 33 | ||||

| 34 | ||||

MANAGEMENT’S DISCUSSIONAND ANALYSISOF FINANCIAL CONDITIONAND RESULTSOF OPERATIONS | 35 | |||

| 48 | ||||

| 57 | ||||

| 72 | ||||

SECURITY OWNERSHIPOF CERTAIN BENEFICIAL OWNERSAND MANAGEMENT | 78 | |||

| 79 | ||||

| 80 | ||||

| 82 | ||||

| 140 | ||||

| 145 | ||||

| 146 | ||||

| 146 | ||||

| 146 | ||||

| F-1 | ||||

i

Table of Contents

The following summary contains basic information about us and the exchange offer. It likely does not contain all the information that is important to you. You should carefully read and review the entire prospectus. You should read the information set forth under “Risk Factors” beginning on page 11 for more information about important factors that you should carefully consider before exchanging Original Notes for New Notes. References in this prospectus to “American Petroleum Tankers,” “APT,” “we,” “our,” “us,” and the “Company” refer to American Petroleum Tankers Holding LLC and its subsidiaries collectively, unless otherwise indicated by the context.

Our Company

We are a U.S. based provider of Jones Act marine transportation services for refined petroleum products in the U.S. domestic “coastwise” trade. Our fleet consists of five new, double-hulled product tankers. Our fleet of five vessels has a total capacity of approximately 245,000 deadweight tons (“dwt”) and an average age of approximately one year. The Merchant Marine Act of 1920 (commonly referred to as the “Jones Act”) restricts marine cargo transportation between points in the United States only to vessels documented under the U.S. flag, built in the United States, at least 75% owned by U.S. citizens (or owned by other entities meeting U.S. citizenship requirements to own vessels operating in the U.S. coastwise trade) and manned by U.S. crews.

Our customers are BP West Coast Products LLC (“BP”), an affiliate of Chevron Corporation (“Chevron”), an affiliate of Marathon Oil Corporation (“Marathon”) and the Military Sealift Command department of the U.S. Navy (“MSC”). Three of our vessels are on time charters that range from up to three years under an evergreen type arrangement (which may be terminated at any time upon 90 days notice) to seven years. Our other two vessels are contracted to MSC for one year with four approximately one-year renewal options. While MSC awarded us the contract based on a five-year analysis, MSC is only permitted to commit to annual contracts due to budgetary restrictions. However, as a result of our customization of these vessels to meet MSC’s requirements, as well as economic benefits for continued renewals, we believe it is likely that MSC will exercise its renewal options, although there can be no assurance that they will do so. In addition, the four T-5 tankers that our vessels will in part replace have been in continuous MSC service since their delivery as new buildings in the mid-1980s, despite MSC’s requirement for periodic renewals of time charters and / or operating agreements, as applicable.

Operationally, we retain all strategic and commercial management of our vessels, while the technical management of the vessels is outsourced to certain affiliates of Crowley Maritime Corporation (collectively, “Crowley” or our “Manager”). Crowley’s technical management services include crewing, maintenance and repair, purchasing, insurance and claims administration, and security as well as accounting and reporting services. Founded in 1892, Crowley is one of the oldest maritime transportation companies in the U.S., employing approximately 4,700 employees across 80 office locations. We benefit from Crowley’s operational expertise, purchasing power and relationships with vendors, suppliers and major labor organizations which are key to providing skilled and experienced crews.

Our auditor expressed substantial doubt as to our ability to continue as a going concern upon completion of its audit of us for the fiscal year 2009 due to our liquidity position and need to raise additional capital to meet our obligations and sustain our operations.

Our Competitive Strengths

We believe we are well-positioned in the Jones Act tanker market because of the following competitive strengths:

| • | Young fleet; |

| • | Stable revenues and cash flows; |

1

Table of Contents

| • | Quality technical management; |

| • | Strong credit position; and |

| • | Financial sponsor support. |

Our Business Strategy

Our primary business objective is to increase our cash flow by executing the following strategies:

| • | Operate our fleet safely and efficiently; |

| • | Maintain quality assets; |

| • | Contract a majority of our vessels on medium to long-term charters with credit worthy customers; and |

| • | Maintain relationships with high quality charter counterparties. |

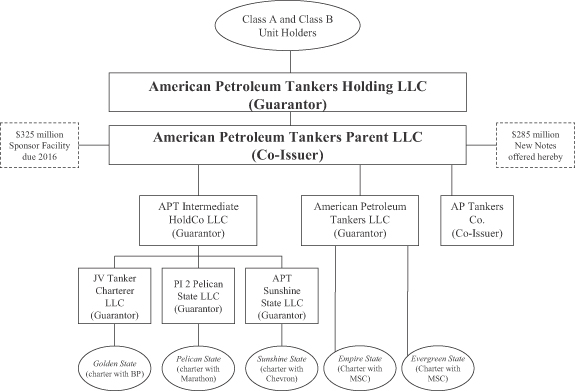

Organizational Chart

The following chart shows our organizational structure as of the date of this prospectus. All entities are wholly-owned subsidiaries of the entity immediately above such entity and all of the subsidiaries of American Petroleum Tankers Parent LLC (“APT Parent”) shown below are guarantors (the “Subsidiary Guarantors”) of the New Notes as well as American Petroleum Tankers Holding LLC (“Holding”, together with the Subsidiary Guarantors, the “Guarantors”), which is the parent company of APT Parent.

2

Table of Contents

Our Equity Sponsors

We are controlled by affiliates of The Blackstone Group L.P. (“Blackstone”), which own 75% of our equity interests in the aggregate. As of September 30, 2010, Blackstone, through its different investment businesses, had total assets under management of approximately $119.1 billion. In June 2007, Blackstone conducted an initial public offering of common units representing limited partner interests in Blackstone, which are listed on the New York Stock Exchange under the symbol “BX.”

Affiliates of Cerberus Capital Management, L.P. (“Cerberus”) own 25% of our equity interests in the aggregate. Established in 1992, Cerberus, along with its affiliates, is one of the world’s leading private investment firms. Cerberus currently holds controlling or significant minority investments in companies around the world. Cerberus invests in divestitures, turnarounds, recapitalizations, financial restructurings, public-to-privates and management buyouts in a variety of sectors.

Principal Executive Offices

Our principal executive offices are located at 345 Park Avenue, 29th Floor, New York, New York 10154, c/o The Blackstone Group L.P., and our telephone number is (215) 435-9569.

The Exchange Offer

Exchange and Registration Rights | In a registration rights agreement dated May 17, 2010 (the “Registration Rights Agreement”), the holders of our Original Notes were granted exchange and registration rights. This exchange offer is intended to satisfy these rights. You have the right to exchange the Original Notes that you hold for our registered New Notes with substantially identical terms. Once the exchange offer is complete, you will no longer be entitled to any exchange rights with respect to your Original Notes. |

Expiration Date | 12:00 midnight, New York City time, on , 2011, which is 20 business days after the commencement of the exchange offer, unless we extend the exchange offer. |

Interest on the New Notes | The New Notes will bear interest from November 1, 2010. Holders of Original Notes which are accepted for exchange will be deemed to have waived the right to receive any payment in respect of interest on those Original Notes accrued to the date of issuance of the New Notes. |

Conditions to the Exchange Offer | The exchange offer is conditioned upon some customary conditions, which we may waive. All conditions to which the exchange offer is subject must be satisfied or waived on or before the expiration of this offer. |

Procedures for Tendering Original Notes | Each holder of Original Notes wishing to accept the exchange offer must: |

| • | Complete, sign and date the letter of transmittal, or a facsimile of the letter of transmittal; or |

3

Table of Contents

| • | Arrange for the Depository Trust Company (“DTC”) to transmit required information in accordance with DTC’s procedures for transfer to the exchange agent in connection with a book-entry transfer. |

You must mail or otherwise deliver this documentation together with the Original Notes to the exchange agent. Original Notes tendered in the exchange offer must be in denominations of principal amount of $2,000 and integral multiples of $1,000 in excess of $2,000.

Special Procedures for Beneficial Holders | If you beneficially own Original Notes registered in the name of a broker, dealer, commercial bank, trust company or other nominee and you wish to tender your Original Notes in the exchange offer, you should contact the registered holder promptly and instruct them to tender on your behalf. If you wish to tender on your own behalf, you must, before completing and executing the letter of transmittal for the exchange offer and delivering your Original Notes, either arrange to have your Original Notes registered in your name or obtain a properly completed bond power from the registered holder. The transfer of registered ownership may take considerable time. |

Guaranteed Delivery Procedures | You must comply with the applicable procedures for tendering if you wish to tender your Original Notes and: |

| • | Time will not permit your required documents to reach the exchange agent by the expiration date of the exchange offer; or |

| • | You cannot complete the procedure for book-entry transfer on time; or |

| • | Your Original Notes are not immediately available. |

Withdrawal Rights | You may withdraw your tender of Original Notes at any time on or prior to 12:00 midnight, New York City time, on the expiration date, unless previously accepted for exchange. |

Failure to Exchange will Affect You Adversely | If you are eligible to participate in the exchange offer and you do not tender your Original Notes, you will not have further exchange rights and you will continue to be restricted from transferring your Original Notes. Accordingly, the liquidity of the Original Notes will be adversely affected. |

Federal Tax Considerations | We believe that the exchange of the Original Notes for New Notes pursuant to the exchange offer will not be a taxable event for United States federal income tax purposes. A holder’s holding period for New Notes will include the holding period for Original Notes, and the adjusted tax basis of the New Notes will be the same as the adjusted tax basis of the Original Notes exchanged. See “Material U.S. Federal Income Tax Consequences.” |

4

Table of Contents

Exchange Agent | The Bank of New York Mellon Trust Company N.A., trustee under the indenture under which the New Notes will be issued, is serving as exchange agent. |

Use of Proceeds | We will not receive any proceeds from the exchange offer. |

Summary Terms of New Notes

The summary below describes the principal terms of the New Notes. Some of the terms and conditions described below are subject to important limitations and exceptions. See “Description of the New Notes” for a more detailed description of the terms and conditions of the New Notes.

Issuers | APT Parent, a Delaware limited liability company, and AP Tankers Co., a Delaware corporation (“Co-Issuer” and together with APT Parent, the “Co-Issuers”). Co-Issuer is a wholly-owned subsidiary of APT Parent that conducts no business operations. |

Securities Offered | The form and terms of the New Notes will be the same as the form and terms of the Original Notes except that: |

| • | the New Notes will bear a different CUSIP number from the Original Notes; |

| • | the New Notes will have been registered under the Securities Act of 1933, or the Securities Act, and, therefore, will not bear legends restricting their transfer; and |

| • | you will not be entitled to any exchange or registration rights with respect to the New Notes. |

The New Notes will evidence the same debt as the Original Notes. They will be entitled to the benefits of the indenture governing the Original Notes and will be treated under the indenture as a single class with Original Notes.

Maturity | The New Notes will mature on May 1, 2015. |

Interest | The New Notes will bear cash interest at the rate of 10 1/4% per annum (calculated using a 360 day year consisting of 12 months of 30 days). Interest payment dates are May 1 and November 1, beginning on May 1, 2011. |

Guarantees | All payments on the New Notes, including principal and interest, will be jointly and severally guaranteed on a senior secured basis by the Guarantors. |

Collateral | The New Notes and the guarantees are secured by a first-priority lien on substantially all of our and the Guarantors’ assets, whether now owned or hereafter acquired (collectively, the “Collateral”), subject to certain exceptions and permitted liens. See “Description of the New |

5

Table of Contents

Notes—Security.” In the future, we may enter into a priority revolving credit facility, together with an intercreditor agreement whereby, in the event of a foreclosure on the Collateral or insolvency proceedings, the holders of the New Notes will receive proceeds from the Collateral only after the lenders under certain credit facilities have been repaid. In addition, the same Collateral secures our obligations under our second lien credit agreement with Blackstone Corporate Debt Administration L.L.C., as administrative agent, and The Bank of New York Mellon, as security agent (the “Sponsor Facility”) ($351.7 million outstanding as of September 30, 2010), which is subject to an intercreditor agreement. While the New Notes will initially be secured by the pledge of the Co-Issuers’ capital stock and membership interests and membership interests of the Subsidiary Guarantors, these pledges may be released to the extent that separate financial statements pursuant to Rule 3-16 of Regulation S-X would be required in connection with the filing of a registration statement related to the New Notes (so long as the Sponsor Facility and any other permitted additional pari passu obligations are also not secured by a pledge of such capital stock or membership interests). We expect that, as a result, a portion of the capital stock and membership interests of the Co-Issuers and the membership interests of the Subsidiary Guarantors will be released. See “Description of the New Notes—Security.” |

Ranking | The New Notes and the guarantees rank: |

| • | equal in right of payment with all of our and the Guarantors’ existing and future senior indebtedness, but effectively senior in right of payment to all of our and the Guarantors’ existing and future obligations to the extent of the value of the Collateral securing the Notes; |

| • | senior in right of payment to all of our and the Guarantors’ existing and future obligations that are, by their terms, expressly subordinated in right of payment to the Notes; |

| • | effectively junior in right of payment to any of our and the Guarantors’ existing and future obligations that are secured by assets other than the Collateral to the extent of the value of any such assets securing such other obligations; and |

| • | structurally junior in right of payment to any existing and future obligations of our non-guarantor subsidiaries. |

Optional Redemption | Prior to May 1, 2012, we may (i) redeem the New Notes, in whole or in part, at a price equal to 100% of the principal amount thereof plus the make whole premium described under “Description of the New Notes—Optional Redemption” or (ii) redeem from time to time during any twelve month period up to 10% of the original aggregate principal amount of the New Notes at a price equal to 103% of the principal amount thereof. See “Description of the New Notes—Optional Redemption.” |

6

Table of Contents

We may also redeem any of the New Notes at any time on or after May 1, 2012, in whole or in part, at the redemption prices described under “Description of the New Notes—Optional Redemption,” plus accrued and unpaid interest, if any, to the date of redemption.

In addition, prior to May 1, 2012, we may redeem up to 35% of the aggregate principal amount of the New Notes with the net proceeds of certain equity offerings, provided at least 65% of the aggregate principal amount of the New Notes originally issued remains outstanding immediately after such redemption. See “Description of the New Notes—Optional Redemption.”

Change of Control; Asset Sales | Upon a change of control, if we do not redeem the New Notes, each holder of New Notes is entitled to require us to purchase all or a portion of its New Notes at a purchase price equal to 101% of the principal amount thereof, plus accrued and unpaid interest. We cannot assure you that we will have the financial resources to purchase the New Notes in such circumstances. See “Description of the New Notes—Change of Control.” |

If we sell assets under certain circumstances, we are required to make an offer to purchase the New Notes at their face amount, plus accrued and unpaid interest to the purchase date. See “Description of the New Notes—Certain Covenants—Limitation on Asset Sales.”

Certain Covenants | The indenture governing the New Notes, among other things, limits our ability and the ability of our subsidiaries to: |

| • | incur certain additional indebtedness or issue certain limited liability company membership interests; |

| • | create certain liens; |

| • | pay dividends or make other equity distributions; |

| • | purchase or redeem limited liability company membership interests; |

| • | make certain investments; |

| • | sell assets; |

| • | agree to any restrictions on the ability of our restricted subsidiaries to make payments to us; |

| • | merge, consolidate, sell or otherwise dispose of all or substantially all of our assets; |

| • | enter into sale and leaseback transactions; and |

| • | engage in transactions with affiliates. |

These covenants are subject to important qualifications and exceptions. See “Description of the New Notes—Certain Covenants” in this prospectus.

7

Table of Contents

Exchange Offer; Registration Rights | You have the right to exchange the Original Notes for New Notes with substantially identical terms. This exchange offer is intended to satisfy that right. The New Notes will not provide you with any further exchange or registration rights. |

Resale Without Further Registration | We believe that the New Notes issued in the exchange offer in exchange for Original Notes may be offered for resale, resold and otherwise transferred by you without compliance with the registration and prospectus delivery provisions of the Securities Act, if: |

| • | you are acquiring the New Notes issued in the exchange offer in the ordinary course of business; |

| • | you have not engaged in, do not intend to engage in, and have no arrangement or understanding with any person to participate in the distribution of the New Notes issued to you in the exchange offer; and |

| • | you are not our “affiliate,” as defined under Rule 405 of the Securities Act. |

Each of the participating broker-dealers that receives the New Notes for its own account in exchange for Original Notes that were acquired by it as a result of market-making or other activities must acknowledge that it will deliver a prospectus in connection with the resale of the New Notes. We do not intend to list the New Notes on any securities exchange.

8

Table of Contents

Summary Consolidated Historical and Operating Data and Other Financial Information

On May 14, 2010, we consummated a restructuring of our corporate organization, resulting in: (i) the formation of Holding as the new parent holding company; (ii) the formation of APT Parent as a new wholly-owned subsidiary of Holding and Co-Issuer as a new wholly-owned subsidiary of APT Parent. As the reorganization occurred among parties under common control, the consolidated financial statements of the predecessor company, American Petroleum Tankers LLC, have become the historical financial statements of American Petroleum Tankers Holding LLC. The following tables provide summary consolidated historical financial data and should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and the related notes appearing elsewhere in this prospectus.

| For the Years Ended December 31, | For the Nine Months Ended September 30, | |||||||||||||||||||

| 2007 | 2008 | 2009 | 2009 | 2010 | ||||||||||||||||

| (dollars in thousands) | ||||||||||||||||||||

Consolidated Statements of Operations Data: | ||||||||||||||||||||

Revenues | $ | — | $ | — | $ | 28,867 | $ | 19,028 | $ | 42,883 | ||||||||||

Operating expenses | — | 214 | 11,917 | 7,695 | 16,605 | |||||||||||||||

General and administrative expenses | 298 | 201 | 1,063 | 578 | 1,376 | |||||||||||||||

Depreciation | — | — | 8,398 | 5,722 | 12,106 | |||||||||||||||

Management fees | 343 | 1,434 | 2,740 | 2,265 | 1,746 | |||||||||||||||

Settlement fees and related legal expenses | — | — | 17,901 | 17,901 | — | |||||||||||||||

Total expenses | 641 | 1,849 | 42,019 | 34,161 | 31,833 | |||||||||||||||

Operating income (loss) | (641 | ) | (1,849 | ) | (13,152 | ) | (15,133 | ) | 11,050 | |||||||||||

Interest income | 6 | 2 | 15 | 15 | 77 | |||||||||||||||

Interest expense | (1 | ) | (5 | ) | (8,639 | ) | (4,304 | ) | (32,234 | ) | ||||||||||

Debt extinguishment expense | — | — | — | — | (7,640 | ) | ||||||||||||||

Derivative (losses) gains, net | 26 | (1,175 | ) | 1,751 | 1,462 | (1,967 | ) | |||||||||||||

Net loss | $ | (610 | ) | $ | (3,027 | ) | $ | (20,025 | ) | $ | (17,960 | ) | $ | (30,714 | ) | |||||

| As of December 31, | As of September 30, | |||||||||||||||

| 2007 | 2008 | 2009 | 2010 | |||||||||||||

| (dollars in thousands) | ||||||||||||||||

Consolidated Balance Sheets: | ||||||||||||||||

Assets | ||||||||||||||||

Cash and cash equivalents | $ | 8 | $ | 16 | $ | 7,893 | $ | 24,347 | ||||||||

Total current assets | 187 | 195 | 13,616 | 122,075 | ||||||||||||

Other long-term assets | 11,382 | 7,685 | 15,706 | 13,706 | ||||||||||||

Vessels and construction in progress, net | 101,194 | 328,354 | 624,080 | 691,402 | ||||||||||||

Total assets | $ | 112,763 | $ | 336,234 | $ | 653,402 | $ | 829,122 | ||||||||

Liabilities and Members’ Equity | ||||||||||||||||

Total current liabilities, including current portion of long-term debt | $ | 15,994 | $ | 7,429 | $ | 107,143 | $ | 98,473 | ||||||||

Long term debt, net of current portion | 41,230 | 176,721 | 414,200 | 629,304 | ||||||||||||

Total liabilities | 57,224 | 184,150 | 521,343 | 727,777 | ||||||||||||

Members’ equity | 55,539 | 152,084 | 132,059 | 101,345 | ||||||||||||

Total liabilities and members’ equity | $ | 112,763 | $ | 336,234 | $ | 653,402 | $ | 829,122 | ||||||||

9

Table of Contents

| For the Years Ended December 31, | For the Nine Months Ended September 30, | |||||||||||||||||||

| 2007 | 2008 | 2009 | 2009 | 2010 | ||||||||||||||||

| (dollars in thousands) | ||||||||||||||||||||

Cash Flow Data: | ||||||||||||||||||||

Net cash provided / (used in) operating activities | $ | (580 | ) | $ | (1,362 | ) | $ | (1,659 | ) | $ | (6,697 | ) | $ | 23,399 | ||||||

Net cash provided / (used in) investing activities | (50,882 | ) | (233,393 | ) | (226,109 | ) | (221,944 | ) | (174,559 | ) | ||||||||||

Net cash provided / (used in) financing activities | 51,470 | 234,763 | 235,645 | 239,160 | 167,614 | |||||||||||||||

Other Financial Data: | ||||||||||||||||||||

Senior Debt(2) | $ | — | $ | — | $ | 96,904 | $ | 96,904 | $ | 277,623 | ||||||||||

EBITDA(1) | (615 | ) | (3,024 | ) | (3,003 | ) | (7,949 | ) | 13,549 | |||||||||||

EBITDA excluding certain charges(1) | (615 | ) | (3,024 | ) | 15,648 | 10,702 | 13,549 | |||||||||||||

| (1) | EBITDA represents net income plus interest expense (net of interest income), income tax expense and depreciation and amortization. EBITDA excluding certain charges is defined as net income plus interest expense (net of interest income), income taxes, depreciation and amortization, legal settlement expenses, and delivery fees. EBITDA and EBITDA excluding certain charges are not recognized terms under generally accepted accounting principles and do not purport to be alternatives to net income as a measure of operating performance or to cash flows from operating activities as a measure of liquidity. We use EBITDA and EBITDA excluding certain charges as operating performance measures. We believe EBITDA and EBITDA excluding certain charges provide useful information about our financial performance to investors, lenders and financial analysts since these groups have historically used EBITDA-related measures, along with other measures, to estimate the value of a company, to make informed decisions and to evaluate a company’s operating performance. EBITDA and EBITDA excluding certain charges should not be considered as alternatives to, or more meaningful than, income before income taxes or other traditional indicators of operating performance. Additionally, EBITDA and EBITDA excluding certain charges are not intended to be measures of free cash flow for management’s discretionary use, as they do not consider certain cash requirements such as tax payments and debt service requirements. Because companies do not use identical calculations, this presentation of EBITDA excluding certain charges may not be comparable to other similarly titled measures of other companies. A reconciliation of net loss to EBITDA and EBITDA excluding certain charges is included below. The charges excluded are one-time charges. |

| For the Years Ended December 31, | For the Nine Months Ended September 30, | |||||||||||||||||||

| 2007 | 2008 | 2009 | 2009 | 2010 | ||||||||||||||||

(dollars in thousands) | ||||||||||||||||||||

Net loss | $ | (610 | ) | $ | (3,027 | ) | $ | (20,025 | ) | $ | (17,960 | ) | $ | (30,714 | ) | |||||

Interest expense, net | (5 | ) | 3 | 8,624 | 4,289 | 32,157 | ||||||||||||||

Depreciation and amortization | — | — | 8,398 | 5,722 | 12,106 | |||||||||||||||

EBITDA | (615 | ) | (3,024 | ) | (3,003 | ) | (7,949 | ) | 13,549 | |||||||||||

Adjustments to EBITDA(3): | ||||||||||||||||||||

Settlement fees and related legal expenses | — | — | 17,901 | 17,901 | — | |||||||||||||||

Management delivery fees | — | — | 750 | 750 | — | |||||||||||||||

EBITDA excluding certain charges | $ | (615 | ) | $ | (3,024 | ) | $ | 15,648 | $ | 10,702 | $ | 13,549 | ||||||||

| (2) | Senior Debt is defined as the total debt secured by a first lien on our assets and does not include the Sponsor Facility. |

| (3) | EBITDA is adjusted for one-time, non-recurring charges. |

10

Table of Contents

You should carefully consider each of the risk factors set forth below, together with all of the other information contained in this prospectus, before deciding whether to tender the Original Notes in exchange for the New Notes. As a result of any of the following risks, our business, financial and other condition, results of operations, prospects and ability to service our debt could be materially adversely affected, the trading price of the New Notes could decline and you may lose all or part of your investment in the New Notes.

Risks Related To The New Notes And Our Indebtedness

Our substantial level of indebtedness could adversely affect our financial condition and prevent us from fulfilling our obligations under the Notes and our other indebtedness.

We have substantial indebtedness. As of September 30, 2010, we had total indebtedness of approximately $629.3 million, including $277.6 million outstanding under the Notes and approximately $351.7 million under the Sponsor Facility.

Our substantial indebtedness could have important consequences to you, including the following:

| • | our high level of indebtedness could make it more difficult for us to satisfy our obligations with respect to the Notes, including any repurchase obligations that may arise thereunder; |

| • | the restrictions imposed on the operation of our business may hinder our ability to take advantage of strategic opportunities to grow our business; |

| • | our ability to obtain additional financing for working capital, capital expenditures, debt service requirements, restructuring, acquisitions or general corporate purposes may be impaired, which could be exacerbated by further volatility in the credit markets; |

| • | we must use a substantial portion of our cash flow from operations to pay interest on the Notes and, to the extent incurred, our other indebtedness, which will reduce the funds available to us for operations and other purposes; |

| • | our high level of indebtedness could place us at a competitive disadvantage compared to our competitors that may have proportionately less debt; |

| • | our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate may be limited; and |

| • | our high level of indebtedness makes us more vulnerable to economic downturns and adverse developments in our business. |

Despite our current leverage, we may still be able to incur substantially more debt. This could further exacerbate the risks that we and our subsidiaries face.

We and our subsidiaries may be able to incur substantial additional indebtedness, including additional secured indebtedness, in the future. The terms of the indenture restrict, but do not completely prohibit, us from doing so. In addition, the indenture allows us to issue additional notes under certain circumstances, which will also be guaranteed by the Guarantors and will share in the Collateral. The indenture also allows us to incur certain other additional super-priority secured debt, which would be effectively senior to the Notes. In addition, the indenture does not prevent us from incurring other liabilities that do not constitute indebtedness. See “Description of the New Notes.” This may have the effect of reducing the amount of proceeds paid to you in the event of a liquidation. If new debt or other liabilities are added to our current debt levels, the related risks that we and our subsidiaries now face could intensify.

11

Table of Contents

If we enter into a priority revolving credit facility, which is permitted under the indenture (under certain circumstances), the priority of the liens and security interests on the collateral held by the holders of the Notes will change.

If we enter into a priority revolving credit facility, which is permitted under the indenture (under certain circumstances), the collateral will be subject to an intercreditor agreement pursuant to which lenders under such revolving credit facility will be entitled to repayment prior to the Notes.

If we enter into a priority revolving credit facility, our obligations under the priority revolving credit facility will be secured by a first priority lien on substantially the same collateral as the Collateral securing the Notes, in each case subject to permitted liens. As a result, our obligations under the Notes and the guarantees related thereto (which are initially secured by a first priority lien on substantially all of our assets (subject to permitted liens and excluded assets)) will be junior in priority of payment to any new revolving credit facility, in each case subject to permitted liens. The relative priority of the liens on the priority revolving credit facility collateral and the Notes collateral is governed by an intercreditor agreement. See “Description of the New Notes—Intercreditor Agreements.”

We may not be able to generate sufficient cash to service all of our indebtedness, including the Notes, and may be forced to take other actions to satisfy our obligations under our indebtedness, which may not be successful.

Our ability to make scheduled payments or to refinance our debt obligations depends on our financial and operating performance, which is subject to prevailing economic and competitive conditions and to certain financial, business and other factors beyond our control. We may not be able to maintain a level of cash flow from operating activities sufficient to permit us to pay the principal, premium, if any, and interest on our indebtedness.

If our cash flows and capital resources are insufficient to fund our debt service obligations, we may be forced to reduce or delay capital expenditures, sell assets, seek additional capital or seek to restructure or refinance our indebtedness, including the Notes. These alternative measures may not be successful and may not permit us to meet our scheduled debt service obligations. In the absence of such operating results and resources, we could face substantial liquidity problems and might be required to sell material assets or operations to attempt to meet our debt service and other obligations. The indenture restricts our ability to use the proceeds from asset sales. We may not be able to consummate those asset sales to raise capital or sell assets at prices that we believe are fair and proceeds that we do receive may not be adequate to meet any debt service obligations then due. See “Description of Certain Indebtedness” and “Description of the New Notes.”

Upon registering or exchanging the Notes with the U.S. Securities and Exchange Commission (the “SEC”), the capital stock securing the Notes will automatically be released from Collateral to the extent the pledge of such capital stock would require the filing of separate financial statements for any of our subsidiaries with the SEC.

Rule 3-16 of Regulation S-X promulgated by the SEC requires financial statements of an entity to be provided if the capital stock or other securities of such entity constitute collateral for a class of registered securities and if the greater of par value, book value or market value of such capital stock or securities equals 20% or more of the principal amount of the secured class of securities. As a result, the indenture governing the Notes and the security documents relating to the first priority security interest in the Collateral securing the Notes provide that, to the extent that separate financial statements of any of our subsidiaries would be required by the rules of the SEC due to the fact that such subsidiary’s capital stock or other securities secure the Notes will automatically be limited such that the value of the portion of such capital stock or other securities of such subsidiary will, in the aggregate, at no time exceed 19.999% of the aggregate principal amount of the then outstanding Notes. Notwithstanding any release under the indenture, a pledge of the capital stock or other securities would remain with respect to any priority revolving credit facility.

12

Table of Contents

The value of the Collateral securing the Notes may not be sufficient to satisfy our obligations under the Notes.

The fair market value of the Collateral is subject to fluctuations based on factors that include, among others, general economic conditions and similar factors. The amount to be received upon a sale of the Collateral would be dependent on numerous factors, including, but not limited to, the actual fair market value of the Collateral at such time, the timing and the manner of the sale and the availability of buyers. By its nature, portions of the Collateral may be illiquid and may have no readily ascertainable market value. In the event of a foreclosure, liquidation, bankruptcy or similar proceeding, the Collateral may not be sold in a timely or orderly manner and the proceeds from any sale or liquidation of this Collateral may not be sufficient to pay our obligations under the Notes.

To the extent that pre-existing liens, liens permitted under the indenture and other rights, including liens on excluded assets, such as those securing purchase money obligations and capital lease obligations granted to other parties (in addition to the holders of obligations secured by first priority liens), encumber any of the Collateral securing the Notes and the guarantees, those parties have or may exercise rights and remedies with respect to the Collateral that could adversely affect the value of the Collateral and the ability of the Notes collateral agent, the trustee under the indenture or the holders of the Notes to realize or foreclose on the Collateral.

In addition, the indenture governing the Notes permits us, subject to compliance with certain financial tests, to issue additional secured debt, including debt secured equally and ratably by the same assets pledged for the benefit of the holders of the Notes. This would reduce amounts payable to holders of the Notes from the proceeds of any sale of the Collateral. There may not be sufficient Collateral to pay off any additional notes we may issue together with the Notes.

Consequently, liquidating the Collateral securing the Notes and the guarantees may not result in proceeds in an amount sufficient to pay any amounts due under the Notes after also satisfying the obligations to pay any creditors with prior or super-priority liens. If the proceeds of any sale of Collateral are not sufficient to repay all amounts due on the Notes, the holders of the Notes (to the extent not repaid from the proceeds of the sale of the Collateral) would have only an unsecured, unsubordinated claim against our and the Guarantors’ remaining assets. In addition, the Notes were initially secured by the pledge of the capital stock and membership interests of the Co-Issuers and the membership interests of the Subsidiary Guarantors, these pledges may be released to the extent that separate financial statements pursuant to Rule 3-16 of Regulation S-X would be required in connection with the filing of a registration statement related to the Notes. See “Description of the New Notes—Security.” We are filing a registration statement pursuant to the terms of the Registration Rights Agreement, which will result in the application of Rule 3-16 to the New Notes upon registration. We expect that, as a result, a portion of the capital stock and membership interests of the Co-Issuer and/or the membership interests of the Subsidiary Guarantors may be released.

The sale of particular assets by us could reduce the pool of assets securing the Notes and the guarantees.

The collateral documents allow us to remain in possession of, retain exclusive control over, freely operate, and collect, invest and dispose of any income from, the Collateral securing the Notes and the guarantees.

In addition, we may not be required to comply with all or any portion of Section 314(d) of the Trust Indenture Act of 1939. See “Description of the New Notes.”

There are circumstances other than repayment or discharge of the Notes under which the Collateral securing the Notes and guarantees will be released automatically, without your consent or the consent of the trustee.

Under various circumstances, all or a portion of the Collateral may be released, including:

| • | to enable the sale, transfer or other disposal of such Collateral in a transaction not prohibited under the indenture, including the sale of any entity in its entirety that owns or holds such Collateral; and |

| • | with respect to Collateral held by a Guarantor, upon the release of such Guarantor from its guarantee. |

13

Table of Contents

In addition, the guarantee of a Subsidiary Guarantor will be released in connection with a sale of such Subsidiary Guarantor in a transaction not prohibited by the indenture.

The indenture also permits us to designate one or more of our restricted subsidiaries that is a Guarantor of the Notes as an unrestricted subsidiary. If we designate a Subsidiary Guarantor as an unrestricted subsidiary, all of the liens on any Collateral owned by such subsidiary or any of its subsidiaries and any guarantees of the Notes by such subsidiary or any of its subsidiaries will be released under the indenture. Designation of an unrestricted subsidiary will reduce the aggregate value of the Collateral securing the Notes to the extent that liens on the assets of the unrestricted subsidiary and its subsidiaries are released. In addition, the creditors of the unrestricted subsidiary and its subsidiaries will have a senior claim on the assets of such unrestricted subsidiary and its subsidiaries. See “Description of the New Notes.”

Rights of holders of the Notes in the Collateral may be adversely affected by the failure to perfect security interests in the Collateral.

Applicable law requires that a security interest in certain tangible and intangible assets can only be properly perfected and its priority retained through certain actions undertaken by the secured party. The liens on the Collateral securing the Notes may not be perfected with respect to the claims of the Notes if the Notes collateral agent does not take the actions necessary to perfect any of these liens. There can be no assurance that the collateral agent will have taken all actions necessary to create properly perfected security interests, which may result in the loss of the priority of the security interest for any asset. See “—Any future pledge of Collateral might be avoidable in bankruptcy,” “—Mortgages on two of the vessels secured by mortgages or other related Collateral were not in place at the time of the issuance of the Notes, and as such, the value of the Collateral may be impacted. Delivery of such mortgages and other Collateral after the issue date of the Notes increases the risk that the liens granted by those mortgages and other Collateral could be avoided.” In addition, applicable law requires that certain property and rights acquired after the grant of a general security interest, such as real property, equipment subject to a certificate of title and certain proceeds, can only be perfected at the time such property and rights are acquired and identified. We and the Guarantors have limited obligations to perfect the security interest of the holders of the Notes in specified Collateral. There can be no assurance that the trustee or the collateral agent will monitor, or that we will inform such trustee or collateral agent of, the future acquisition of property and rights that constitute Collateral, and that the necessary action will be taken to properly perfect the security interest in such after acquired Collateral. Neither the trustee nor the Notes collateral agent has an obligation to monitor the acquisition of additional property or rights that constitute Collateral or the perfection of any security interest. Such failure may result in the loss of the security interest in the Collateral or the priority of the security interest in favor of the Notes against third parties.

The indenture governing the Notes and our Sponsor Facility, impose significant operating and financial restrictions on us. If we default under any of these debt instruments, we may not be able to make payments on the Notes.

The indenture and our Sponsor Facility impose significant operating and financial restrictions on us. These restrictions limit our ability to, among other things: incur additional indebtedness or guarantee obligations; repay indebtedness (including the Notes) prior to stated maturities; pay dividends or make certain other restricted payments; make investments or acquisitions; create liens or other encumbrances; transfer or sell certain assets or merge or consolidate with another entity; engage in transactions with affiliates; and engage in certain business activities. In addition to the restrictions listed above, our Sponsor Facility requires us to meet a specified financial ratio test as of certain dates. Any of these provisions could limit our ability to plan for or react to market conditions and could otherwise restrict corporate activities. Our ability to comply with these provisions may be affected by events beyond our control, and an adverse development affecting our business could require us to seek waivers or amendments of covenants, alternative or additional sources of financing or reductions in expenditures. A breach of any of the covenants or restrictions contained in any of our existing or future financing agreements could result in a default or an event of default under those agreements. Such a default or event of

14

Table of Contents

default could allow the lenders under our financing agreements, if the agreements so provide, to accelerate the related debt and to declare all borrowings outstanding thereunder to be due and payable.

Mortgages on two of the vessels secured by mortgages or other related Collateral were not in place at the time of the issuance of the Original Notes, and as such, the value of the Collateral may be impacted. Delivery of such mortgages and other Collateral after the issue date of the Original Notes increases the risk that the liens granted by those mortgages and other Collateral could be avoided.

The mortgages on, and other Collateral relating to, two of the vessels secured by mortgages and the associated property and contract rights were not in place at the time of the issuance of the Original Notes as those vessels were delivered after the issuance of the Original Notes. One or more of these mortgages or other items of Collateral may constitute a significant portion of the value of the Collateral. Although the mortgages on our last two vessels have since been perfected, if we are unable to provide a perfected security interest in one or more other items intended to be Collateral, the overall value of the Collateral securing the Notes will be reduced. If we were to become subject to a bankruptcy proceeding after the issue date of the Original Notes, any collateral delivered after the issue date of the Original Notes would face a greater risk of being invalidated than if we had delivered it at the issue date. If an item of Collateral is delivered after the issue date, it may be treated under bankruptcy law as if it were delivered to secure previously existing debt, which may make it more likely to be avoided as a preference by the bankruptcy court than if the item of collateral were delivered and promptly recorded on the issue date of the Original Notes. To the extent that the grant of a security interest in such Collateral is avoided as a preference, holders of the Notes would lose the benefit of the property encumbered by that item of Collateral that was intended to constitute security for the Notes.

The Collateral is subject to casualty risks.

We intend to maintain insurance or otherwise insure against hazards in a manner appropriate and customary for our business. There are, however, certain losses that may be either uninsurable or not economically insurable, in whole or in part. See “Risk Factors—Risks Relating To Our Business Strategy and Operations—Our insurance may be insufficient to cover losses that may occur to our property or result from our operations.” In the event of a total or partial loss to any of the vessels secured by mortgages, our vessels may not be easily repaired or replaced. Accordingly, even though there may be insurance coverage, the extended period needed to repair such vessels or compensate our charterers for such crude oil or refined petroleum products could cause significant delays and costs.

Federal and state fraudulent transfer laws may permit a court to void the guarantees, and, if that occurs, you may not receive any payments on the Notes.

The issuance of the guarantees may be subject to review under federal and state fraudulent transfer and conveyance statutes. While the relevant laws may vary from state to state, under such laws the incurrence of a guarantee obligation will be a fraudulent conveyance if a Guarantor received less than reasonably equivalent value or fair consideration in exchange for issuing such guarantee, and one of the following is also true:

| • | such Guarantor was insolvent or rendered insolvent by reason of the incurrence of the indebtedness; |

| • | the Guarantor was left with an unreasonably small amount of capital to carry on the business; or |

| • | the Guarantor intended to, or believed that it would, incur debts beyond its ability to pay as they mature. |

If a court were to find that the issuance of a guarantee was a fraudulent conveyance, the court could void the payment obligations under such guarantee or subordinate such guarantee to presently existing and future indebtedness of such Guarantor, or require the holders of the Notes to repay any amounts received with respect to such guarantee. In the event of a finding that a fraudulent conveyance occurred, you may not receive any repayment on the Notes.

15

Table of Contents

Generally, an entity would be considered insolvent if, at the time it incurred indebtedness;

| • | the sum of its debts, including contingent liabilities, was greater than the fair saleable value of all its assets; |

| • | the present fair saleable value of its assets was less than the amount that would be required to pay its probable liability on its existing debts and liabilities, including contingent liabilities, as they become absolute and mature; or |

| • | it could not pay its debts as they become due. |

We cannot be certain as to the standards a court would use to determine whether or not a Guarantor was solvent at the relevant time, or regardless of the standard that a court uses, that the issuance of the guarantees would not be subordinated to our or a Guarantor’s other debt. Each guarantee contains a provision intended to limit the Guarantor’s liability to the maximum amount that it could incur without causing the incurrence of obligations under its guarantee to be a fraudulent transfer. This provision may not be effective to protect the guarantees from being voided under fraudulent transfer law, or may eliminate the Guarantor’s obligations or reduce the Guarantor’s obligations to an amount that effectively makes the guarantee worthless. In a recent Florida bankruptcy case, this kind of provision was found to be ineffective to protect the guarantees.

Any future pledge of Collateral might be avoidable in bankruptcy.

Any future pledge of Collateral in favor of the trustee, including pursuant to security documents delivered after the date of the indenture governing the Original Notes, might be avoidable by the pledgor (as debtor in possession) or by its trustee in bankruptcy if certain events or circumstances exist or occur, including if the pledgor is insolvent at the time of the pledge, the pledge permits the holders of the Original Notes to receive a greater recovery than if the pledge had not been given and a bankruptcy proceeding in respect of the pledgor is commenced within 90 days following the pledge, or, in certain circumstances, a longer period. Certain of the assets securing the Original Notes may not be subject to a valid and perfected security interest on the closing date, see “—The value of the Collateral securing the Notes may not be sufficient to satisfy our obligations under the Notes,” “—Mortgages on two of the vessels secured by mortgages or other related Collateral were not in place at the time of the issuance of the Original Notes, and as such, the value of the Collateral may be impacted. Delivery of such mortgages and other Collateral after the issue date of the Original Notes increases the risk that the liens granted by those mortgages and other Collateral could be avoided.”

In the event of our bankruptcy, the ability of the holders of the Notes to realize upon the Collateral will be subject to certain bankruptcy law limitations.

The ability of holders of the Notes to realize upon the Collateral will be subject to certain bankruptcy law limitations in the event of our bankruptcy. Under applicable U.S. federal bankruptcy laws, secured creditors are prohibited from, among other things, repossessing their security from a debtor in a bankruptcy case without bankruptcy court approval and may be prohibited from retaining security repossessed by such creditor without bankruptcy court approval. Moreover, applicable federal bankruptcy laws generally permit the debtor to continue to retain collateral, including cash collateral, even though the debtor is in default under the applicable debt instruments, provided that the secured creditor is given “adequate protection.”

The secured creditor is entitled to “adequate protection” to protect the value of the secured creditor’s interest in the Collateral as of the commencement of the bankruptcy case but the adequate protection actually provided to a secured creditor may vary according to the circumstances. Adequate protection may include cash payments or the granting of additional security if and at such times as the court, in its discretion and at the request of such creditor, determines after notice and a hearing that the Collateral has diminished in value as a result of the imposition of the automatic stay of repossession of such Collateral or the debtor’s use, sale or lease of such Collateral during the pendency of the bankruptcy case. In view of the lack of a precise definition of the term

16

Table of Contents

“adequate protection” and the broad discretionary powers of a U.S. bankruptcy court, we cannot predict whether or when the trustee under the indenture for the Notes could foreclose upon or sell the Collateral or whether or to what extent holders of the Notes would be compensated for any delay in payment or loss of value of the collateral through the requirement of “adequate protection.”

Moreover, the collateral agent and the indenture trustee may need to evaluate the impact of the potential liabilities before determining to foreclose on Collateral consisting of real property, if any, because secured creditors that hold a security interest in real property may be held liable under environmental laws for the costs of remediating or preventing the release or threatened releases of hazardous substances at such real property. Consequently, the Notes collateral agent may decline to foreclose on such Collateral or exercise remedies available in respect thereof if it does not receive indemnification to its satisfaction from the holders of the Notes.

In the event of a bankruptcy of us or any of the Guarantors, holders of the Notes may be deemed to have an unsecured claim to the extent that our obligations in respect of the Notes exceed the fair market value of the Collateral securing the Notes.

In any bankruptcy proceeding with respect to us or any of the Guarantors, it is possible that the bankruptcy trustee, the debtor-in-possession or competing creditors will assert that the fair market value of the Collateral with respect to the Notes on the date of the bankruptcy filing was less than the then-current principal amount of the Notes. Upon a finding by the bankruptcy court that the Notes are under-collateralized, the claims in the bankruptcy proceeding with respect to the Notes would be bifurcated between a secured claim in an amount equal to the value of the Collateral and an unsecured claim with respect to the remainder of its claim which would not be entitled to the benefits of security in the Collateral. Other consequences of a finding of under-collateralization would be, among other things, a lack of entitlement on the part of the Notes to receive post-petition interest and a lack of entitlement on the part of the unsecured portion of the Notes to receive “adequate protection” under federal bankruptcy laws. In addition, if any payments of post-petition interest had been made at any time prior to such a finding of under-collateralization, those payments would be recharacterized by the bankruptcy court as a reduction of the principal amount of the secured claim with respect to the Notes.

The value of the Collateral securing the Notes may not be sufficient to secure post-petition interest.

In the event of a bankruptcy, liquidation, dissolution, reorganization or similar proceeding against us, holders of the Notes will only be entitled to post-petition interest under the U.S. Bankruptcy Code to the extent that the value of their security interest in the Collateral is greater than their pre-bankruptcy claim. Holders of the Notes that have a security interest in Collateral with a value equal or less than their pre-bankruptcy claim will not be entitled to post-petition interest under the U.S. Bankruptcy Code. The value of the noteholders’ interest in the Collateral may not equal or exceed the sum of the first lien obligation and the principal amount of the Notes.

You should not expect Holding or Co-Issuer to participate in making payments on the Notes.

Holding and Co-Issuer were each formed and incorporated to accommodate the issuance of the Original Notes. Neither Holding nor Co-Issuer have any operations or assets of any kind and will not have any revenues other than as may be incidental to their activities as Guarantor or co-issuer of the Notes, respectively. You should not expect Holding or Co-Issuer to participate in servicing any of their obligations on the Notes.

An active public market may not develop for the New Notes, which may hinder your ability to liquidate your investment.

There is no active trading market for the Notes, and we do not intend to apply for the New Notes to be listed on any securities exchange or arrange for any quotation on any automated dealer quotation system. No person is obligated to make a market in the New Notes and, if it does so, it may cease its market-making in the New Notes at any time. In addition, the liquidity of the trading market in the New Notes, and the market price quoted for the

17

Table of Contents

New Notes, may be adversely affected by changes in the overall market for fixed income securities, and by changes in our financial performance or prospects, or in the prospects for companies in our industry in general. As a result, an active trading market for the New Notes may not develop. If no active trading market develops, you may not be able to resell your New Notes at their fair market value, or at all.

The Original Notes were issued with original issue discount for U.S. federal income tax purposes.

The Original Notes were issued with original issue discount (“OID”), for federal income tax purposes. The New Notes should be treated as a continuation of the Original Notes for federal income tax purposes. Consequently, holders of the Original Notes and the New Notes will be required to include amounts in respect of OID in gross income for federal income tax purposes in advance of the receipt of the cash payments to which the income is attributable. See “Material U.S. Federal Income Tax Consequences” for a more detailed discussion of the federal income tax consequences to the holders of Notes regarding the purchase, ownership or disposition thereof.

If a bankruptcy petition were filed by or against us, holders of the Notes may receive a lesser amount for their claim than they would have been entitled to receive under the indenture governing the Notes.

If a bankruptcy petition were filed by or against us under the U.S. Bankruptcy Code after the issuance of the Notes, the claim by any holder of the Notes for the principal amount of the Notes may be limited to an amount equal to the sum of:

| • | the original issue price for the Notes; and |

| • | that portion of the OID that does not constitute “unmatured interest” for purposes of the U.S. Bankruptcy Code. |

Any OID that was not amortized as of the date of the bankruptcy filing would constitute unmatured interest. Accordingly, holders of the Notes under these circumstances may receive a lesser amount than they would be entitled to under the terms of the indenture governing the Notes, even if sufficient funds are available.

A mortgagee that forecloses on vessels operating in the U.S. coastwise trade under the Jones Act will be subject to certain citizenship requirements under federal law.

Under U.S. law, owners of vessels operating in the U.S. coastwise trade must meet certain U.S. citizenship requirements. See “Risk Factors—Risks Relating to Our Business Strategy and Operations—Restrictions on foreign ownership of our vessels could limit our ability to sell off any portion of our business or result in the forfeiture of our vessels.” While mortgagees of these vessels are not required to be U.S. citizens, if a mortgagee takes possession or becomes an owner of vessels through a foreclosure proceeding, the mortgagee must meet the citizenship tests if it wants to either operate the vessels or enter into an arrangement with another person to operate the vessels on its behalf. If a mortgagee does not qualify as a United States citizen for the purpose of operating vessels in the U.S. coastwise trade, the mortgagee is only entitled to hold the vessels for resale and the vessels may not be used pending such sale. In addition, the exercise of certain remedies against the Collateral may require the prior approval of the U.S. Government.

The ability of the indenture trustee to exercise certain remedies against the vessels subject to charters in favor of MSC is limited by federal maritime law.

Pursuant to federal maritime law, the indenture trustee may be prohibited from arresting or seizing a vessel subject to a charter in favor of MSC.

18

Table of Contents

Risks Relating To Our Business Strategy And Operations

We have high levels of fixed costs that will be incurred regardless of our level of business activity.

Our business has high fixed costs that continue even if our vessels are not in service. In addition, low utilization due to reduced demand or other causes or a significant decrease in charter rates could have a significant negative effect on our business and results of operations.

We depend on Crowley and its affiliates to manage the technical operations of our business.

Our chief executive officer, Mr. Robert K. Kurz, and our chief financial officer, Mr. Philip J. Doherty, are our only employees. Pursuant to a management and construction supervision agreement and BIMCO/Shipman agreements, we outsource substantially all of our technical operations to Crowley. Crowley provides us with technical and administrative services, crewing, purchasing, insurance, shipyard supervision, accounting and reporting functions and other support services. In the event a revised administrative fee is not agreed to within 60 days of when we become a SEC reporting company as a result of the effectiveness of the registration statement related to of this exchange offer, Crowley may terminate the Crowley Management Agreement with 30 days written notice to us. See “Management—Our Manager” for a description of all of the foregoing agreements. We are dependent on the continued availability of the service of our two employees, Mr. Kurz and Mr. Doherty, who are key to our future success. The loss of the services of either Mr. Kurz or Mr. Doherty and our failure to replace their services could be significant and may adversely affect our business and results of operations.

The management and construction supervision agreement is scheduled to expire in July 2014, while two of the BIMCO/Shipman agreements will expire in July 2014, the third will expire in November 2014, the fourth will expire in June 2015 and the fifth will expire in November 2015. If during the term of these agreements we fail to make our payment obligations to Crowley or breach the terms of these agreements, Crowley has the right to terminate the agreements prior to their expiration dates. If we fail to renew any of these agreements upon or prior to their expirations, the requirements of our business will necessitate that we enter into substitute agreements with third parties for the services contemplated under the existing agreements. There can be no assurance that we will be successful in negotiating and entering into substitute agreements with third parties and, even if we succeed in doing so, the terms and conditions of these new agreements, individually or in the aggregate, may be significantly less favorable to us than the terms and conditions of our existing agreements. Furthermore, if we do enter into substitute agreements with third parties, changes in our operations to comply with the requirements of these new agreements may cause disruptions to our business, which could be significant and may adversely affect our business and results of operations.

Our operational success and ability to execute our growth strategy, including our ability to enter into new charters and expand our customer relationships, will depend significantly upon the satisfactory performance by Crowley of the services required to be performed by it and our business will be harmed if Crowley fails to perform these services satisfactorily, cancels any of its existing agreements with us or otherwise stops providing these services. Crowley provides similar services to other customers who may also be our competitors. Accordingly, we could face conflicts of interest with Crowley and the other businesses to which they provide services. Furthermore, if Crowley suffers material damage to its reputation, relationships or business generally, it may harm our ability to:

| • | renew existing charters upon their expiration; |

| • | obtain new charters; |

| • | interact successfully with shipyards; |

| • | obtain financing on commercially acceptable terms; |

| • | maintain satisfactory relationships with suppliers and other third parties; or |

| • | effectively operate our vessels. |

19

Table of Contents

We derive our revenues from a limited number of customers and the loss of any of these customers or time charters with any of them could result in an adverse effect on our business and results of operations.

We derive our revenues through charter agreements with four customers: BP, Chevron, Marathon and MSC. During the nine months ended September 30, 2010, our largest customer represented about 35% of our revenues, and another customer represented about 34% of our revenues, although these percentages will decrease now that all of our vessels have been delivered. In addition, we could lose a charterer or the benefits of a time charter because of disagreements with a customer or if a customer exercises specific limited rights to terminate a charter. The loss of any of our customers or time charter with them, or a decline in payments under our charters, could have an adverse effect on our revenues and results of operations.

Our current charter agreements with our customers are scheduled to expire at the earliest of: with respect to BP, January 2016; with respect to Marathon, July 2012; with respect to Chevron, up to three years through an evergreen type arrangement; and with respect to MSC, October 2011 for use of one vessel and January 2012 for use of the other. Generally, the commercial charter agreements do not provide for termination by our customers prior to the expiration date unless the vessel experiences a prolonged period of off-hire or we breach the terms of the charter agreement. However, Chevron may terminate its charter agreement at any time, subject to a 90 day notice period. Furthermore, charters with MSC are subject to termination for default based upon performance or termination for the convenience of the U.S. Government. There can be no assurance that, if we fail to renew our agreements or if our agreements are terminated prior to their expiration dates, we will be successful in negotiating and entering into substitute agreements with third parties and, even if we succeed in doing so, the terms and conditions of these new agreements, individually or in the aggregate, may be significantly less favorable to us than the terms and conditions of our existing agreements. Furthermore, if we do enter into substitute charter agreements with third parties, changes in our operations to comply with the requirements of these new agreements may cause disruptions to our business, which could be significant, and may result in additional costs and expenses.

As a U.S. Department of Defense (the “DoD”) contractor, we are subject to a number of procurement rules and regulations.

We must comply with and are affected by laws and regulations relating to the award, administration, and performance the DoD contracts. Laws and regulations applicable to U.S. Government contracts, including those with DoD, affect how we do business with DoD and, in some instances, impose added costs on our business. A violation of specific laws and regulations could result in the imposition of fines and penalties, the termination of our DoD contracts, or debarment from bidding on future DoD contracts.

In some instances, these laws and regulations impose terms or rights that are more favorable to the DoD than those typically available to commercial parties in negotiated transactions. For example, the U.S. Navy may terminate our MSC charters at its convenience or for default based on performance. Upon termination for convenience, we normally are entitled, subject to negotiation, to receive the purchase price for certain delivered items, reimbursement for allowable costs for work-in-process, and an allowance for profit on the contract or adjustment for loss if completion of performance would have resulted in a loss. Our ability to recover is subject to the U.S. Congress having appropriated sufficient funds to cover the termination costs. As funds are typically appropriated on a fiscal-year basis and as the costs of a termination for convenience may exceed the costs of continuing a program in a given fiscal year, many on-going programs do not have sufficient funds appropriated to cover the termination costs were the government to terminate them for convenience. The U.S. Congress is not required to appropriate additional funding under these circumstances.