UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A INFORMATION

PROXY STATEMENT PURSUANT TO SECTION 14(a) OF THE

SECURITIES EXCHANGE ACT OF 1934

Filed by the Registrant ¨ Filed by a Party other than the Registrant x

Check the appropriate box:

| ¨ | Preliminary Proxy Statement | |

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

| ¨ | Definitive Proxy Statement | |

| x | Definitive Additional Materials | |

| ¨ | Soliciting Material Pursuant to §240.14a-12 | |

TICC CAPITAL CORP.

(Name of Registrant as Specified In Its Charter)

TPG Specialty Lending, Inc.

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| x | Fee not required. | |||

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |||

| (1) | Title of each class of securities to which transaction applies:

| |||

| (2) | Aggregate number of securities to which transaction applies:

| |||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined):

| |||

| (4) | Proposed maximum aggregate value of transaction:

| |||

| (5) | Total fee paid:

| |||

| ¨ | Fee paid previously with preliminary materials. | |||

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |||

| (1) | Amount Previously Paid:

| |||

| (2) | Form, Schedule or Registration Statement No.:

| |||

| (3) | Filing Party:

| |||

| (4) | Date Filed:

| |||

TPG Specialty Lending, Inc. (“TSLX”) has filed a definitive proxy statement with the Securities and Exchange Commission (the “SEC”) and an accompanying GOLD proxy card to be used to solicit votes against TICC Capital Corp.’s (the “Company”) proposal to approve a new advisory agreement between the Company and TICC Management, LLC, to take effect upon a change of control of TICC Management, LLC, and certain related proposals, at a special meeting of stockholders of the Company scheduled to be held on October 27, 2015.

On October 21, 2015, TPG Specialty Lending, Inc. issued a press release and posted an investor presentation on http://www.changeticcnow.com/, a website established by TSLX that contains information regarding the above solicitation. This Schedule 14A filing consists of the above-mentioned press release and presentation, along with screenshots that reflect the content of pages of the website not previously filed with the SEC.

TPG Specialty Lending, Inc. Issues Presentation Detailing Why TICC Capital Corp. Stockholders Should Vote AGAINST All Proposals at Upcoming TICC Capital Corp. Special Meeting

NEW YORK—(BUSINESS WIRE)—TPG Specialty Lending, Inc. (“TSLX”; NYSE:TSLX), a specialty finance company focused on lending to middle-market companies, today issued a presentation titled “TPG Specialty Lending Proposal: The Right and Value Maximizing Choice for TICC Stockholders.” The presentation outlines why stockholders of TICC Capital Corp. (“TICC”; Nasdaq: TICC) should demand that the TICC Board conduct a fair consideration of the TSLX proposal by voting the GOLD proxy card AGAINST management’s proposals at the upcoming special meeting of stockholders on October 27, 2015.

The presentation outlines the significant concerns independent analysts, proxy advisors and fellow TICC stockholders have expressed regarding management’s proposals, and describes the clear benefits the TSLX proposal would deliver to stockholders, including:

| • | Only the TSLX proposal provides an immediate, upfront 20% premium and the opportunity to participate in an outperforming platform.1 |

| • | TICC’s dividend is unsustainable. Paying a portion of the dividend by returning stockholder capital is contributing to the continuing decline in net asset value per share. |

| • | TSLX has had lower relative fees than TICC since 2012, even if TICC had been under the Benefit Street Partners, L.L.C. (“BSP”) fee structure, after considering total stockholder economics. |

| • | TICC’s proposed transaction with BSP would result in an estimated $60 million payment2 to an external manager that has significantly underperformed the BDC sector3 and other benchmarks. |

The presentation can be found atwww.changeTICCnow.com.

About TPG Specialty Lending

TPG Specialty Lending, Inc. (“TSLX”, or the “Company”) is a specialty finance company focused on lending to middle-market companies. The Company seeks to generate current income primarily in U.S.-domiciled middle-market companies through direct originations of senior secured loans and, to a lesser extent, originations of mezzanine loans and investments in corporate bonds and equity securities. The Company has elected to be regulated as a business development company, or a BDC, under the Investment Company Act of 1940 and the rules and regulations promulgated thereunder. TSLX is externally managed by TSL Advisers, LLC, a Securities and Exchange Commission (“SEC”) registered investment adviser. TSLX leverages the deep investment, sector, and operating resources of TPG Special Situations Partners, the dedicated special situations and credit platform of TPG, with over $12 billion of assets under management, and the broader TPG platform, a global private investment firm with over $74 billion of assets under management. For more information, visit the Company’s website atwww.tpgspecialtylending.com.

Forward-Looking Statements

Information set forth herein includes forward-looking statements. These forward-looking statements include, but are not limited to, statements regarding TSLX proposed business combination transaction with TICC Capital Corp. (“TICC”) (including any financing required in connection with the proposed transaction and the benefits, results, effects and timing of a transaction), all statements regarding TPG Specialty Lending, Inc.’s (“TSLX”, or the “Company”) (and TSLX and TICC’s combined) expected future financial position, results of operations, cash flows, dividends, financing plans, business strategy, budgets, capital expenditures, competitive positions, growth opportunities, plans and objectives of management, and statements containing the words such as “anticipate,” “approximate,” “believe,” “plan,” “estimate,” “expect,” “project,” “could,” “would,” “should,” “will,” “intend,” “may,” “potential,” “upside,” and other similar expressions. Statements set forth herein concerning the business outlook or future economic performance, anticipated profitability, revenues, expenses, dividends or other financial items, and product or services line growth of TSLX (and the combined businesses of TSLX and TICC), together with other statements that are not historical facts, are forward-looking statements that are estimates reflecting the best judgment of TSLX based upon currently available information.

Such forward-looking statements are inherently uncertain, and stockholders and other potential investors must recognize that actual results may differ materially from TSLX’s expectations as a result of a variety of factors, including, without limitation, those discussed below. Such forward-looking statements are based upon management’s current expectations and include known and unknown risks, uncertainties and other factors, many of which TSLX is unable to predict or control, that may cause TSLX’s plans with respect to TICC, actual results or performance to differ materially from any plans, future results or performance expressed or implied by such forward-looking statements. These statements involve risks, uncertainties and other factors discussed below and detailed from time to time in TSLX’s filings with the Securities and Exchange Commission (“SEC”).

Risks and uncertainties related to the proposed transaction include, among others, uncertainty as to whether TSLX will further pursue, enter into or consummate the transaction on the terms set forth in the proposal or on other terms, potential adverse reactions or changes to business relationships resulting from the announcement or completion of the transaction, uncertainties as to the timing of the transaction, adverse effects on TSLX’s stock price resulting from the announcement or consummation of the transaction or any failure to complete the transaction, competitive responses to the announcement or consummation of the transaction, the risk that regulatory or other approvals and any financing required in connection with the consummation of the transaction are not obtained or are obtained subject to terms and conditions that are not anticipated, costs and difficulties related to the integration of TICC’s businesses and operations with TSLX’s businesses and operations, the inability to obtain, or delays in obtaining, cost savings and synergies from the transaction, unexpected costs, liabilities, charges or expenses resulting from the transaction, litigation relating to the transaction, the inability to retain key personnel, and any changes in general economic and/or industry specific conditions.

In addition to these factors, other factors that may affect TSLX’s plans, results or stock price are set forth in TSLX’s Annual Report on Form 10-K and in its reports on Forms 10-Q and 8-K.

Many of these factors are beyond TSLX’s control. TSLX cautions investors that any forward-looking statements made by TSLX are not guarantees of future performance. TSLX disclaims any obligation to update any such factors or to announce publicly the results of any revisions to any of the forward-looking statements to reflect future events or developments.

Third Party-Sourced Statements and Information

Certain statements and information included herein have been sourced from third parties. TSLX does not make any representations regarding the accuracy, completeness or timeliness of such third party statements or information. Except as expressly set forth herein, permission to cite such statements or information has neither been sought nor obtained from such third parties. Any such statements or information should not be viewed as an indication of support from such third parties for the views expressed herein. All information in this communication regarding TICC, including its businesses, operations and financial results, was obtained from public sources. While TSLX has no knowledge that any such information is inaccurate or incomplete, TSLX has not verified any of that information. TSLX reserves the right to change any of its opinions expressed herein at any time as it deems appropriate. TSLX disclaims any obligation to update the data, information or opinions contained herein.

Proxy Solicitation Information

The information set forth herein is provided for informational purposes only and does not constitute an offer to purchase or the solicitation of an offer to sell any securities. TSLX has filed with the SEC and mailed to TICC stockholders a definitive proxy statement and accompanying GOLD proxy card to be used to solicit votes at a special meeting of stockholders of TICC scheduled to be held on October 27, 2015 against (a) approval of the new advisory agreement between TICC and TICC Management, LLC (the “Adviser”), to take effect upon a change of control of the Adviser in connection with the entrance of the Adviser into a purchase agreement with an affiliate of Benefit Street Partners L.L.C. (“BSP”), pursuant to which BSP will acquire control of the Adviser, (b) the election of six directors nominated by TICC’s board of directors, and (c) the proposal to adjourn the meeting if necessary or appropriate to solicit additional votes.

TSLX STRONGLY ADVISES ALL STOCKHOLDERS OF TICC TO READ THE TSLX PROXY STATEMENT AND ITS OTHER PROXY MATERIALS AS THEY BECOME AVAILABLE BECAUSE THEY CONTAIN IMPORTANT INFORMATION. SUCH TSLX PROXY MATERIALS ARE AND WILL BECOME AVAILABLE AT NO CHARGE ON THE SEC’S WEB SITE ATHTTP://WWW.SEC.GOV AND AT TSLX’S WEBSITE ATHTTP://WWW.TPGSPECIALTYLENDING.COM. IN ADDITION, TSLX WILL PROVIDE COPIES OF THE PROXY STATEMENT WITHOUT CHARGE UPON REQUEST. REQUESTS FOR COPIES SHOULD BE DIRECTED TO TSLX’S PROXY SOLICITOR ATTPG@MACKENZIEPARTNERS.COM.

The participant in the solicitation is TSLX and certain of its directors and executive officers may also be deemed to be participants in the solicitation. As of the date hereof, TSLX directly beneficially owned 1,633,660 shares of common stock of TICC.

Security holders may obtain information regarding the names, affiliations and interests of TSLX’s directors and executive officers in TSLX’s Annual Report on Form 10-K for the year ended December 31, 2014, which was filed with the SEC on February 24, 2015, its proxy statement for the 2015 Annual Meeting, which was filed with the SEC on April 10, 2015, and certain of its Current Reports on Form 8-K. These documents can be obtained free of charge from the sources indicated above. Additional information regarding the interests of these participants in the proxy solicitation and a description of their direct and indirect interests, by security holdings or otherwise, will also be included in any proxy statement and other relevant materials to be filed with the SEC when they become available.

| 1 | For reference, the TSLX Proposal represents a 12.8% discount to TICC’s NAV as of June 30, 2015, a narrower discount than the price at which the shares have traded since June 30th. |

| 2 | The 9/18 Friday Bocks’d Lunch, Wells Fargo, September 17, 2015 |

| 3 | BDC benchmark is comprised of ACAS, AINV, ARCC, BKCC, FSC, GBDC, HTGC, MAIN, MCC, NMFC, PNNT, PSEC, SLRC, TCAP, and TCRD |

Contacts

Investors

TPG Specialty Lending

Robert Ollwerther,

212-430-4119

bollwerther@tpg.com

or

Lucy Lu,

212-601-4753

llu@tpg.com

or

MacKenzie Partners, Inc.

Charlie Koons,

212-929-5708

ckoons@mackenziepartners.com

or

Media

TPG Specialty Lending

Luke Barrett,

212-601-4752

lbarrett@tpg.com

or

Abernathy MacGregor

Tom Johnson or Pat Tucker

212-371-5999

tbj@abmac.com /pct@abmac.com

http://www.tpgspecialtylending.com/ TPG Specialty Lending Proposal October 2015 The Right and Value Maximizing Choice for TICC Stockholders |

1 Forward-Looking Statements Forward-Looking Statements Information set forth herein includes forward-looking statements. These forward-looking statements include, but are not limited to, statements regarding TSLX proposed business combination transaction with TICC Capital Corp. (“TICC”) (including any financing required in connection with the proposed transaction and the benefits, results, effects and timing of a transaction), all statements regarding TPG Specialty Lending, Inc.’s (“TSLX”, or the “Company”) (and TSLX and TICC’s combined) expected future financial position, results of operations, cash flows, dividends, financing plans, business strategy, budgets, capital expenditures, competitive positions, growth opportunities, plans and objectives of management, and statements containing the words such as “anticipate,” “approximate,” “believe,” “plan,” “estimate,” “expect,” “project,” “could,” “would,” “should,” “will,” “intend,” “may,” “potential,” “upside,” and other similar expressions. Statements set forth herein concerning the business outlook or future economic performance, anticipated profitability, revenues, expenses, dividends or other financial items, and product or services line growth of TSLX (and the combined businesses of TSLX and TICC), together with other statements that are not historical facts, are forward-looking statements that are estimates reflecting the best judgment of TSLX based upon currently available information. Such forward-looking statements are inherently uncertain, and stockholders and other potential investors must recognize that actual results may differ materially from TSLX’s expectations as a result of a variety of factors, including, without limitation, those discussed below. Such forward-looking statements are based upon management’s current expectations and include known and unknown risks, uncertainties and other factors, many of which TSLX is unable to predict or control, that may cause TSLX’s plans with respect to TICC, actual results or performance to differ materially from any plans, future results or performance expressed or implied by such forward-looking statements. These statements involve risks, uncertainties and other factors discussed below and detailed from time to time in TSLX’s filings with the Securities and Exchange Commission (“SEC”). Risks and uncertainties related to the proposed transaction include, among others, uncertainty as to whether TSLX will further pursue, enter into or consummate the transaction on the terms set forth in the proposal or on other terms, potential adverse reactions or changes to business relationships resulting from the announcement or completion of the transaction, uncertainties as to the timing of the transaction, adverse effects on TSLX’s stock price resulting from the announcement or consummation of the transaction or any failure to complete the transaction, competitive responses to the announcement or consummation of the transaction, the risk that regulatory or other approvals and any financing required in connection with the consummation of the transaction are not obtained or are obtained subject to terms and conditions that are not anticipated, costs and difficulties related to the integration of TICC’s businesses and operations with TSLX’s businesses and operations, the inability to obtain, or delays in obtaining, cost savings and synergies from the transaction, unexpected costs, liabilities, charges or expenses resulting from the transaction, litigation relating to the transaction, the inability to retain key personnel, and any changes in general economic and/or industry specific conditions. In addition to these factors, other factors that may affect TSLX’s plans, results or stock price are set forth in TSLX’s Annual Report on Form 10-K and in its reports on Forms 10-Q and 8-K. Many of these factors are beyond TSLX’s control. TSLX cautions investors that any forward-looking statements made by TSLX are not guarantees of future performance. TSLX disclaims any obligation to update any such factors or to announce publicly the results of any revisions to any of the forward- looking statements to reflect future events or developments. |

2 Third Party-Sourced Statements and Information | Proxy Solicitation Information Third Party-Sourced Statements and Information Certain statements and information included herein have been sourced from third parties. TSLX does not make any representations regarding the accuracy, completeness or timeliness of such third party statements or information. Except as expressly set forth herein, permission to cite such statements or information has neither been sought nor obtained from such third parties. Any such statements or information should not be viewed as an indication of support from such third parties for the views expressed herein. All information in this communication regarding TICC, including its businesses, operations and financial results, was obtained from public sources. While TSLX has no knowledge that any such information is inaccurate or incomplete, TSLX has not verified any of that information. TSLX reserves the right to change any of its opinions expressed herein at any time as it deems appropriate. TSLX disclaims any obligation to update the data, information or opinions contained herein. Proxy Solicitation Information The information set forth herein is provided for informational purposes only and does not constitute an offer to purchase or the solicitation of an offer to sell any securities. TSLX has filed with the SEC and mailed to TICC stockholders a definitive proxy statement and accompanying GOLD proxy card to be used to solicit votes at a special meeting of stockholders of TICC scheduled to be held on October 27, 2015 against (a) approval of the new advisory agreement between TICC and TICC Management, LLC (the “Adviser”), to take effect upon a change of control of the Adviser in connection with the entrance of the Adviser into a purchase agreement with an affiliate of Benefit Street Partners L.L.C. (“BSP”), pursuant to which BSP will acquire control of the Adviser, (b) the election of six directors nominated by TICC’s board of directors, and (c) the proposal to adjourn the meeting if necessary or appropriate to solicit additional votes. TSLX STRONGLY ADVISES ALL STOCKHOLDERS OF TICC TO READ THE TSLX PROXY STATEMENT AND ITS OTHER PROXY MATERIALS AS THEY BECOME AVAILABLE BECAUSE THEY CONTAIN IMPORTANT INFORMATION. SUCH TSLX PROXY MATERIALS ARE AND WILL BECOME AVAILABLE AT NO CHARGE ON THE SEC’S WEB SITE AT HTTP://WWW.SEC.GOV AND AT TSLX’S WEBSITE AT HTTP://WWW.TPGSPECIALTYLENDING.COM. IN ADDITION, TSLX WILL PROVIDE COPIES OF THE PROXY STATEMENT WITHOUT CHARGE UPON REQUEST. REQUESTS FOR COPIES SHOULD BE DIRECTED TO TSLX’S PROXY SOLICITOR AT TPG@MACKENZIEPARTNERS.COM. The participant in the solicitation is TSLX and certain of its directors and executive officers may also be deemed to be participants in the solicitation. As of the date hereof, TSLX directly beneficially owned 1,633,660 shares of common stock of TICC. Security holders may obtain information regarding the names, affiliations and interests of TSLX’s directors and executive officers in TSLX’s Annual Report on Form 10-K for the year ended December 31, 2014, which was filed with the SEC on February 24, 2015, its proxy statement for the 2015 Annual Meeting, which was filed with the SEC on April 10, 2015, and certain of its Current Reports on Form 8-K. These documents can be obtained free of charge from the sources indicated above. Additional information regarding the interests of these participants in the proxy solicitation and a description of their direct and indirect interests, by security holdings or otherwise, will also be included in any proxy statement and other relevant materials to be filed with the SEC when they become available. |

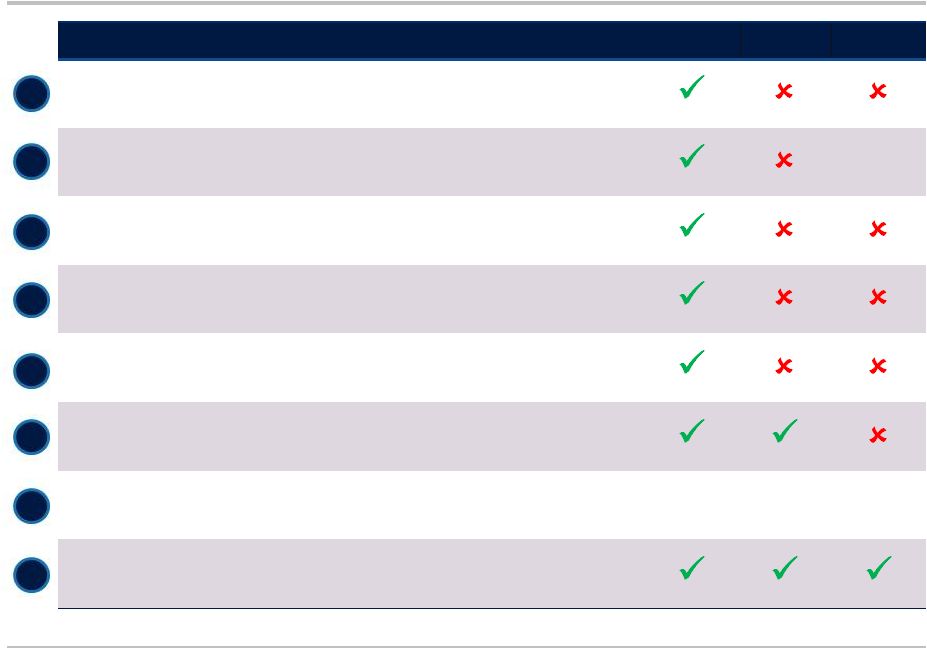

3 The Choice for Stockholders is Clear MANAGEMENT PROPOSAL 1: TO APPROVE A NEW ADVISORY AGREEMENT BETWEEN THE COMPANY AND TICC MANAGEMENT, LLC, TO TAKE EFFECT UPON A CHANGE OF CONTROL OF TICC MANAGEMENT, LLC THERE IS ONLY ONE CLEAR CHOICE THAT MAXIMIZES VALUE FOR STOCKHOLDERS Voting TICC/BSP (White): • Rewards a failed outgoing external manager • Places the future of TICC in the hands of an unproven BDC manager • Maintains unstable dividend policy Voting TSLX (Gold): • Stops a value destructive transaction • Gives opportunity to — Realize immediate 20% premium¹ — Participate in value creation of industry leader — Benefit from increased liquidity • Sends a clear message to TICC to engage with the best offer on the table for stockholders Voting NexPoint (Blue): • No upfront premium • Puts TICC in the hands of a manager with a failed history in the BDC sector • NexPoint Credit Strategies Fund (“NHF”) trades at 0.78x NAV ¹ To TICC’s closing stock price on September 15, 2015. For reference, the TSLX proposal represents a 12.8% discount to TICC’s NAV as of June 30 , 2015, a narrower discount than the price at which the shares have traded since June 30 . th th |

4 Issues for TICC Stockholders TICC has demonstrated a poor investment performance track record, coupled with decisions by its Board of Directors that are not in stockholders’ best interests and are indicative of entrenchment Discount to NAV TICC has delivered a total return of only 51.6% since its IPO, representing 154.4 points of underperformance relative to the sector¹ TICC shares traded at 0.73x NAV immediately preceding the public announcement of the TSLX proposal NAV per share has declined in seven out of the nine most recent quarters TICC tells you not to sell below NAV, yet BSP is only willing to commit to paying 0.9x NAV to repurchase shares Unsustainable Dividend TICC has under-earned its dividend by an average of 23% in the three most recent quarters and likely would have under-earned its dividend in previous quarters if not for an accounting error by TICC disclosed in Q1’2015 Analysts covering TICC forecast material dividend cuts, citing current levels as unsustainable Leverage Maxed Out A high debt to equity ratio of 0.97x severely limits TICC‘s ability to raise additional capital or repurchase shares Board Actions BSP’s acquisition of the TICC manager would result in a $60 million transfer of value to the outgoing managers, as reported by Wells Fargo Research — Actual amount has not been disclosed nor has the suspected payment been commented on by management or the Board, suggesting that the payment could be higher than currently reported TICC’s lack of engagement with TSLX regarding its offer to acquire TICC at a 20% premium is indicative of Board member entrenchment² TICC’s independent directors have conflicts of interest with the TICC management team Source: Research reports, Public filings, SNL Note: Market data as of 15-Sep-2015, the day immediately preceding the public announcement of the TSLX proposal ¹ BDC sector peers comprise ACAS, AINV, ARCC, BKCC, FSC, GBDC, HTGC, MAIN, MCC, NMFC, PNNT, PSEC, SLRC, TCAP, and TCRD. Total return is defined as change in stock price plus any paid dividends over a given time period. ² For reference, the TSLX proposal represents a 12.8% discount to TICC’s NAV as of June 30, 2015, a narrower discount than the price at which the shares have traded since June 30th. |

5 TSLX’s Superior Proposal Impact on TICC Stockholders TSLX BSP NexPoint 20% premium to TICC’s share price No value leakage to manager at expense of TICC stockholders ? Increased liquidity corresponding with larger public float Manager with track record of outperformance with a publicly traded BDC, reflected in premium stock price to net asset value Benefit from participating in value creation and potential outperformance by a top-quartile BDC Rotate TICC portfolio into higher quality, better performing assets Competitive fees Management fee 1.50 % 1.50 % 1.25 % Incentive fee 17.5 % 20.0 % 20.0 % Repurchase shares 1 2 3 4 5 6 7 ¹ For reference, the TSLX proposal represents a 12.8% discount to TICC’s NAV as of June 30, 2015, a narrower discount than the price at which the shares have traded since June 30th. ² Wells Fargo Securities, LLC Equity Research: “The Q4 2015 BDC Scorecard” dated September 10, 2015 3 BSP / NexPoint will keep TICC’s historical hurdle rate of 5.0% + interest rate on five-year U.S. Treasury Note with no Catch-Up. TSLX’s hurdle rate is 6% with a Catch-Up provision. 8 1 2 3 |

6 Independent Research Analysts Overwhelmingly Support the TSLX Offer Analyst Commentary Support for BSP Offer Support for TSLX Offer Wells Fargo Securities “[BSP’s and NexPoint’s offers] provide no immediate compensation to TICC shareholders AND the value creation rests on two managers who have [a very limited] track record of managing a…BDC” “[The TSLX proposal] creates substantial value for TICC shareholders, TSLX shareholders, as well as a combined TSLX/TICC entity” Barclays “We do not believe the proposal with [BSP] that is supported by TICC’s Board represents the best possible offer available to shareholders” “[O]n a relative basis, we believe TSLX’s offer to acquire TICC represents the best value out of the three” JMP Securities “While TICC's board of directors likely declined to engage with [TSLX], [TSLX] expressed its full commitment to realize the value in the proposed transaction...We see value [in TSLX’s offer]” KBW “Unfortunately, it is our belief that the Board is placing more value on the compensation that BSP is willing to provide to the management team to buy the contract than maximizing shareholder value. If ultimately the Board pushes the BSP offer through, this is another black eye for the BDC industry regarding shareholder returns vs. management compensation” ? Ladenburg Thalmann “In our view, the rejection of the TSLX offer calls into question of…whose interests TICC’s Board is most concerned” “We like the TSLX offer because it provides the clearest path yet to generating value for TICC shareholders” National Securities “We think shareholders stand to gain more from BSP changing the company’s strategy than the quick gain of selling now at $7.50” Source: Research Reports, Public Filings Modest Stockholder Enthusiasm for BSP and NexPoint TICC 2-Day Stock Performance (%) Date BSP Initial Offer 5.3 % 3-Aug NexPoint Intial Offer 0.9 % 17-Aug NexPoint Revised Offer 0.9 % 28-Aug BSP Revised Offer (1.3)% 3-Sep BSP 2nd Revised Offer 1.0 % 6-Oct TSLX Offer 11.8 % 15-Sep |

7 How Independent is TICC’s Special Committee? • TICC’s Board approved the advisory agreement with management every year despite drastic underperformance and, according to certain industry analysts, charged approximately 6x the fees it should properly be entitled to given the composition of TICC’s portfolio¹ • TICC Board members, including Chuck Royce, stand to personally make ~$60 million through a transaction with BSP. The exact payment has never been disclosed so stockholders are left to wonder if the payout is in fact even higher — An independent analyst noted that a member of the “independent” Special Committee is paid $280,000 per year by Chuck Royce’s other businesses ¹ TICC Reiterates Rejection of TSLX’s offer, Wells Fargo, September 22, 2015 KBW, Sept 16th “TSLX provides an interesting offer and the [TICC] Board rejects it without negotiating with TSLX. As the title of our note implies, we are questioning whether the [TICC] Board is really doing all they can to maximize shareholder value” KBW, Aug 31st “We fail to see how the board of directors at TICC can fulfill their legal fiduciary responsibility to TICC shareholders and not explore the potential for a transaction with an existing quality manager in the BDC sector” Barclays, Oct 6th “The board could have simply waited until the current advisory agreement came up for renewal. But instead, the board chose to go this route and support a proposal which pays out the current investment advisor” Egan Jones, Oct 13th “We believe that it would have been in the best interest of shareholders for the current Board to have allowed a shareholder vote on the TSLX proposal to acquire TICC” |

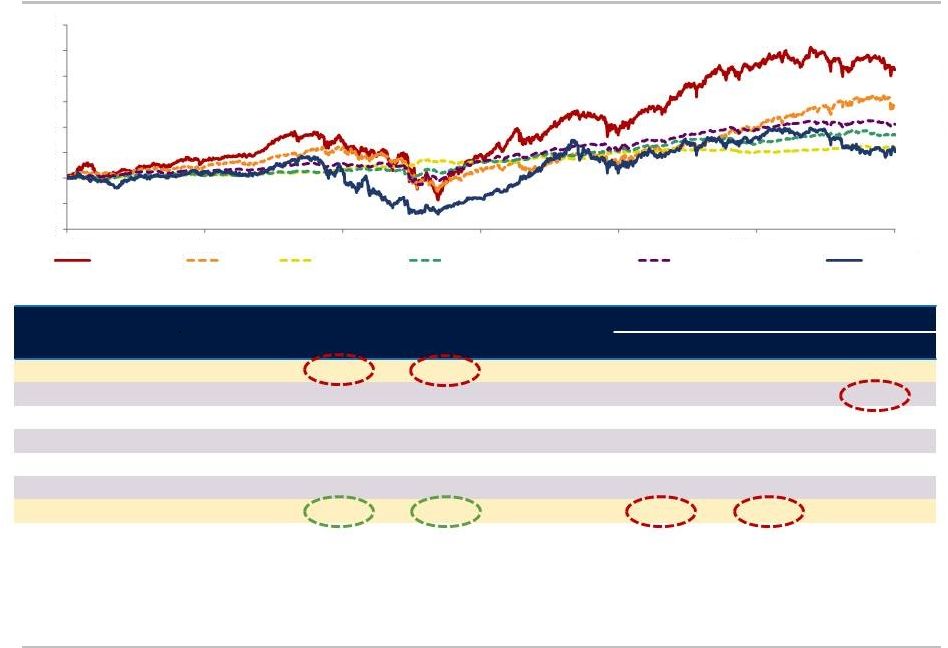

8 TICC has Drastically Underperformed a Variety of Asset Classes TICC Relative Underperformance Total Return (%) 1Y 3Y Since IPO (1) 1Y 3Y Since IPO (1) TICC (21.8)% (13.9)% 51.6% - - - BDC Composite (2) (9.8) 7.4 206.0 (12.0)% (21.3)% (154.4)% S&P 500 1.8 43.8 143.7 (23.6) (57.7) (92.1) U.S. Treasuries 3.2 3.9 60.4 (25.0) (17.9) (8.8) Investment Grade Corporate Debt 1.1 7.3 84.3 (22.8) (21.2) (32.7) High Yield Corporate Debt (1.5) 10.7 105.7 (20.3) (24.6) (54.1) TSLX (3) 12.0 % 51.6 % N/A (33.8)% (65.5)% N/A (1) TICC and benchmark returns indexed to 21-Nov-2003 (2) BDC Composite comprised of ACAS, AINV, ARCC, BKCC, FSC, GBDC, HTGC, MAIN, MCC, NMFC, PNNT, PSEC, SLRC, TCAP, and TCRD (3) TSLX 3-year total return based off of 30-Jun-2012 NAV per share, 15-Sep-2015 closing stock price, and cumulative dividends declared during the period Note: Market data as of 15-Sep-2015. For reference, the TSLX proposal represents a 12.8% discount to TICC’s NAV as of June 30, 2015, a narrower discount than the price at which the shares have traded since June 30th. Source: Bloomberg, fixed income benchmark data from Markit iBoxx 206% 144% 60% 84% 106% 52% 0% 50% 100% 150% 200% 250% 300% 350% 400% Nov-2003 Nov-2005 Oct-2007 Oct-2009 Oct-2011 Sep-2013 Sep-2015 Indexed Total Return (%) BDC Composite S&P 500 U.S. Treasuries Investment Grade Corporate Debt High Yield Corporate Debt TICC |

9 TICC has Under-Earned its Dividend and Eroded NAV TICC HAS UNDER-EARNED ITS DIVIDEND TSLX HAS CONTINUALLY EARNED ITS DIVIDEND TICC NET ASSET VALUE PER SHARE (1) TSLX NET ASSET VALUE PER SHARE (1) Earnings likely overstated due to an accounting (1) Net Asset Value Per Share includes effect of realized and unrealized gains (2) In Q1’15, TICC identified an accounting error that resulted in historical income being over-reported. As a result, net investment income incentive fees were overstated by ~$2.4mm on a cumulative basis through 2014. Without this error, TICC likely never truly “earned” its dividend Source: Public Filings “The $0.29 [TICC] dividend is not sustainable, and we expect it will be cut regardless of what happens. We have been talking about a dividend cut for over a year now” TICC TSLX $.40 $.37 $.42 $.46 $.51 $.55 $.43 $.57 $.39 $.49 NII Per Share Unearned DPS DPS $.23 $.30 $.23 $.32 $.33 $.29 $.29 $.21 $.21 $.18 NII Per Share Unearned DPS DPS $ 10.02 $ 9.75 $ 9.90 $ 9.85 $ 9.78 $ 9.71 $ 9.40 $ 8.64 $ 8.72 $ 8.60 $ 15.27 $ 15.29 $ 15.35 $ 15.52 $ 15.51 $ 15.70 $ 15.66 $ 15.53 $ 15.60 $ 15.84 error KBW, Sept 16 2 th |

10 Fees Have to Be Evaluated In Conjunction With Stockholder Returns Fees and expenses are best benchmarked against returns generated, not based on assets under management TSLX’s fees are highly competitive when looking at the historical performance of the manager and taking into account TSLX’s active management approach — Since commencement of investment activities in July 2011, TSLX has generated a total return of 62.4% — Under the direction of members of the NexPoint management team, Highland Distressed Opportunities, a BDC, generated market price returns of NEGATIVE 57% (1) before it was absorbed into Highland Credit Strategies NexPoint’s analysis assumes that they will be able to generate the same return for TICC stockholders as TSLX could, but given their respective historical performance, investors should be understandably skeptical (1) Supplement Dated April 22, 2009 to the Proxy Statement/Prospectus Dated March 5, 2009 of Highland Distressed Opportunities (2) BDC Composite comprised of ACAS, AINV, ARCC, BKCC, FSC, GBDC, HTGC, MAIN, MCC, NMFC, PNNT, PSEC, SLRC, TCAP, and TCRD Note: Market data as of 15-Sep-2015. For reference, the TSLX proposal represents a 12.8% discount to TICC’s NAV as of June 30, 2015, a narrower discount than the price at which the shares have traded since June 30th. Source: Company Filings. Financial data as of Q2 2015 • Lower fees DO NOT guarantee higher distribution – higher investment returns best support higher distributions • Fees only matter in how they factor into total shareholder returns – it’s the size of the total economic pie that matters — TSLX has delivered 44.2 percentage points higher total stockholder returns (including fees) than the BDC Composite 2 over the past 3 years • TSLX trades as a 10% premium to NAV, NexPoint Credit Strategies trades at a 24% discount to NAV — Manager performance (not just fees) drives valuation and stockholder returns |

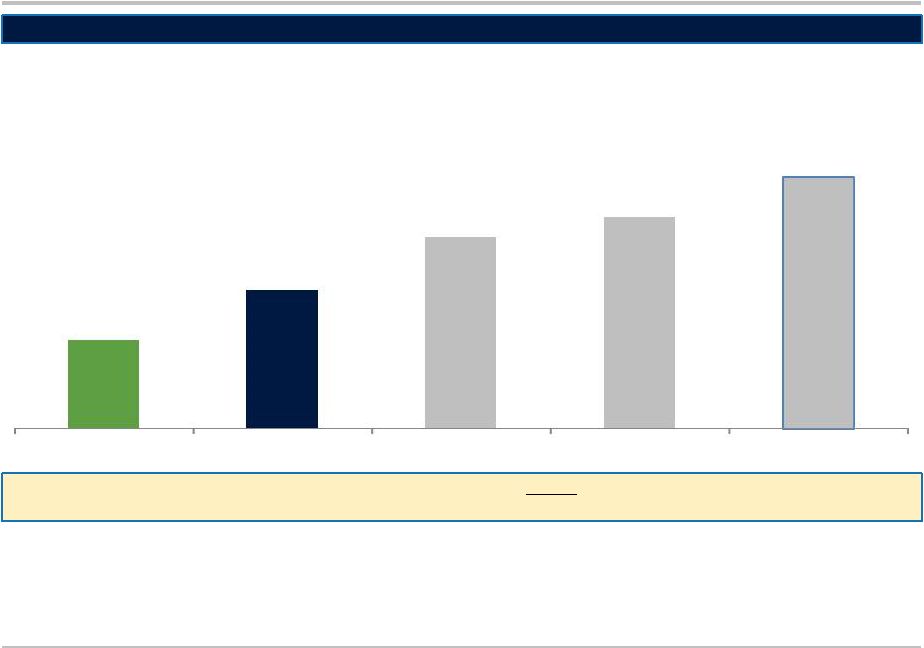

11 Fees as a Portion of Total Economics Total Shareholder Fees and Expenses as a % of Total Economics Since 2012 (1) (1) Total Economics defined as Economic Profit + Shareholder Value Gained / (Lost) due to change in Premium / (Discount) to Average NAV. Economic Profit equals Net Increase in Net Assets as a Result of Operations + Total Shareholder Fees & Expenses. Shareholder Value Gained / (Lost) due to change in Premium / (Discount) to Average NAV calculated as the change in premium (or discount) to NAV per share between the close of the trading day following the filing of 12/31/2011 financial statements and the close of the trading day following the release of 6/30/2015 financial statements multiplied by the average NAV between those trading days (calculated as shares outstanding on such trading day multiplied by the then-most recently reported NAV per share). See pages titled “Reconciliation of Certain Non-GAAP Financial Measures” for a reconciliation to the most recent comparable financial measures presented in accordance with GAAP (2) Assumes 38% reduction of Cumulative Investment Advisory Fees Paid (illustrating management fee reduction from 2.0% to 1.25% of AUM), holding economic profit constant (3) Assumes 25% reduction of Cumulative Investment Advisory Fees Paid (illustrating management fee reduction from 2.0% to 1.50% of AUM), holding economic profit constant (4) Pro forma to exclude effects of management fee waiver. See “Reconciliation of Certain Non-GAAP Financial Measures.” (5) BDC Composite comprised of ACAS, AINV, ARCC, BKCC, FSC, GBDC, HTGC, MAIN, MCC, NMFC, PNNT, PSEC, SLRC, TCAP, and TCRD. TSLX believes that Total Shareholder Fees & Expenses and Total Economics for each company in the BDC Composite was calculated on a substantially equivalent basis to the methodology shown for TSLX and TICC in “Reconciliation of Certain Non-GAAP Financial Measures,” including pro forma adjustments to exclude effects of any management or incentive fee waiver, where applicable. Source: Company Filings. Capital IQ, Financial data as of 6/30/2015. When accounting for total stockholder economics, TSLX had lower relative fees than TICC since 2012, even if TICC had been under either the BSP or NexPoint fee structures! (2) (3) (4) (5) 28 % 45 % 62 % 68 % 81 % TSLX Median of BDC Composite TICC (w/ NexPoint Fees) TICC (w/ BSP Fees) TICC |

12 Differentiated platform with proprietary lending capabilities second-to-none in the industry Investment grade credit ratings from both Standard & Poor’s and Fitch Diversified portfolio with average investment size of $35 million; largest investment position of 4.9% and largest industry concentration of 15.7% Effective voting control on 81% of debt investments Overview of TSLX Superior Investment Platform Superior Results Leading investment returns and stockholder- friendly actions have resulted in TSLX trading at a premium to NAV every day since its IPO Stable and sustainable dividend that has been over-earned with investment income in eight consecutive quarters 62.4% total return since commencement of investing activities in July 2011 44.2 percentage points BETTER total return than the BDC Composite¹ over the past three years 2Q ’15 Annualized ROAE from Net Income of 16.2%; YTD ROAE of 13.9%² (1) BDC composite comprised of ACAS, AINV, ARCC, BKCC, FSC, GBDC, HTGC, MAIN, MCC, NMFC, PNNT, PSEC, SLRC, TCAP, and TCRD (2) Return on Average Equity is calculated using weighted average equity. Weighted average equity is calculated by starting with NAV at the beginning of the period, adjusting daily for equity issuances and adjusting on the last day of the period for that period’s net income and dividends payable Source: Public Filings |

13 We Ask Again for TICC to Answer Our Four Simple Questions • Are management or interested Board members of TICC receiving compensation as part of the agreement with BSP? • What results have this management team and the Board delivered to stockholders? How do they compare with other BDCs? • Why should the TICC external manager that oversaw massive underperformance now be paid a premium to leave? Who is the TICC Board looking out for? • Is TICC’s dividend sustainable? Does TICC disagree with the five respected independent analysts who believe the TICC dividend will be cut? 1 2 3 4 Vote TSLX (Gold): • Stops a value-destructive transaction • Gives opportunity to — Realize immediate 20% premium — Participate in value creation of industry leader — Benefit from increased liquidity • Sends a clear message to TICC to engage with the best offer on the table for stockholders ¹ To TICC’s closing stock price on September 15, 2015. For reference, the TSLX proposal represents a 12.8% discount to TICC’s NAV as of June 30 , 2015, a narrower discount than the price at which the shares have traded since June 30 . 1 th th |

14 Appendix: Fees as a Portion of Total Economics |

15 Reconciliation of Certain Non-GAAP Financial Measures • Fees as a portion of Total Economics of your investment, as set forth in this presentation, may be considered a non-GAAP financial measure. TSLX provides this information to stockholders because TSLX believes it enhances stockholders’ understanding of the relative costs stockholders bear in relation to the assets generated by operations of TSLX, TICC, TICC pro forma as if it had been subject to the fee structure in the BSP proposal, TICC pro forma as if it had been subject to the fee structure in the NexPoint proposal, and comparable companies included in the BDC Composite as defined above, respectively. Non-GAAP financial measures should not be considered in isolation from, or as a substitute for, financial information presented in compliance with GAAP, and non-GAAP financial measures as used by TSLX may not be comparable to similarly titled amounts used by other companies. • Total Economics = Economic Profit + Shareholder Value Gained / (Lost) due to the Change in Premium / (Discount) to Average NAV • Economic Profit = Increase in Net Assets Resulting from Operations + Total Shareholder Fees & Expenses • Shareholder Value Gained / (Lost) Due to the Change in Premium / (Discount) to Average NAV calculated as the change in premium (or discount) to NAV per share between the close of the trading day following the filing of 12/31/2011 financial statements and the close of the trading day following the release of 6/30/2015 financial statements multiplied by the average NAV between those trading days (calculated as shares outstanding on such trading day multiplied by the then-most recently reported NAV per share). • The pages that follow illustrate the reconciliation of the net increase in net assets resulting from operations since 2012 to Economic Profit and the calculation of the ratio of Total Shareholder Fees and Expenses to Total Economics for TSLX, TICC, TICC pro forma as if it had been subject to the fee structure in the BSP proposal, and TICC pro forma as if it had been subject to the fee structure in the NexPoint proposal. – TSLX believes that Total Shareholder Fees & Expenses and Total Economics for each company in the BDC Composite was calculated on a substantially equivalent basis to the methodology shown for TSLX and TICC. – For companies that reported management or incentive fee waivers in the periods subsequent to 12/31/2011, including TSLX as well as AINV, FSC and NMFC, which are included in the BDC Composite, Total Shareholder Fees & Expenses and Economic Profit are calculated pro forma as if (i) the fee waivers had not been applied and (ii) the corresponding reduction in pre-incentive fee net investment income resulted in a reduction in incentive fees (calculated by multiplying the amount of management fees waived by the incentive fee rate for each company). No pro forma adjustments were made to NAV per share in the calculation of Shareholder Value Gained / (Lost) Due to Change in Premium / (Disc.) to Average NAV. |

16 TICC 2012 2013 2014 2015 (through June 30) Cumulative Cumulative TICC under BSP Fees 2 Cumulative TICC under NexPoint Fees 3 Net Increase in Net Assets Resulting from Operations (GAAP) $ 68,323 $ 58,945 $(3,348) $ 30,856 $ 154,776 $ 170,223 $ 177,946 Shareholder Fees & Expenses: Compensation expense (GAAP) $ 1,183 $ 1,648 $ 1,861 $ 876 $ 5,567 $ 5,567 $ 5,567 Investment advisory fees (GAAP) 11,223 19,096 21,150 10,319 61,788 46,341 38,617 Professional fees (GAAP) 1,874 1,996 2,150 1,512 7,532 7,532 7,532 Insurance (GAAP) 1 69 69 69 0 206 206 206 Directors' Fees (GAAP) 1 261 323 317 0 900 900 900 Transfer agent and custodian fees (GAAP) 1 129 229 284 0 642 642 642 General and administrative (GAAP) 1,028 1,590 1,398 1,184 5,200 5,200 5,200 Net investment income incentive fees (GAAP) 5,460 6,581 5,604 (1,505) 16,139 16,139 16,139 Capital gains incentive fees (GAAP) 5,509 (1,192) (3,873) 0 444 444 444 Total Shareholder Fees & Expenses 26,735 30,339 28,959 12,385 98,418 82,971 75,248 Economic Profit (Net Increase in Net Assets Resulting from Operations + Total Shareholder Fees & Expenses) $ 95,058 $ 89,284 $ 25,611 $ 43,242 $ 253,194 $ 253,194 $ 253,194 TICC NAV Per Share 12/31/2011 (Released 03/15/2012) $ 9.30 $ 9.30 $ 9.30 TICC Share Price 03/16/2012 10.09 $ 10.09 $ 10.09 Premium / (Discount) to NAV 03/16/2012 9 % 9 % 9 % Shares Outstanding (millions) (as of 3/16/2012) 37 37 37 TICC NAV Per Share 6/30/15 (Released 08/7/2015) $ 8.60 $ 8.60 $ 8.60 TICC Share Price 08/10/2015 6.70 6.70 6.70 Premium / (Discount) to NAV 08/10/2015 (22)% (22)% (22)% Shares Outstanding (millions) (as of 8/10/2015) 60 60 60 Change in Premium / (Discount) to NAV (31)% (31)% (31)% Shareholder Value Gained / (Lost) due to Change in Premium / (Disc.) to Average NAV $(131,605) $(131,605) $(131,605) Total Economics (Economic Profit + Shareholder Value Gained / (Lost) due to Change in Premium / (Disc.) to Average NAV ) $ 121,589 $ 121,589 $ 121,589 Ratio of Total Shareholder Fees & Expenses to Total Economics 81 % 68 % 62 % Reconciliation of Certain Non-GAAP Financial Measures (1) For the six months ended June30, 2015, directors’ fees, insurance, and transfer agent and custodian fees, which previously had been separately reported, were included in “General and administrative.” (2) Assumes 25% reduction of Cumulative Investment Advisory Fees Paid (illustrating management fee reduction from 2.0% to 1.50% of AUM), holding economic profit constant (3) Assumes 38% reduction of Cumulative Investment Advisory Fees Paid (illustrating management fee reduction from 2.0% to 1.25% of AUM), holding economic profit constant ($ in thousands, except per share amounts and where noted) |

17 Reconciliation of Certain Non-GAAP Financial Measures (1) TSLX did not have publically traded shares prior to March 2014. Share price assumed to equal NAV per share at 12/31/2011 (adjusted for December 2013 stock split) (2) Includes management fees waived by TSLX’s investment advisor prior to TSLX’s IPO in 2014, which totaled $3,704 in 2012, $7,135 in 2013 and $2,464 in 2014 (3) Pro forma adjustment to exclude impact of management fees waived on net investment income. (4) Pro forma adjustment to reduce incentive fees resulting from decrease in pre-incentive fee net investment income. Calculated by multiplying management fees waived by incentive fee rate of 15% applicable prior to TSLX’s IPO in 2014. (5) Excludes impact of pro forma adjustments described above. (6) Adjusted for December 2013 stock split ($ in thousands, except per share amounts and where noted) TSLX 2012 2013 2014 2015 (through June 30) Cumulative Increase in Net Assets Resulting from Operations (GAAP) $ 39,595 $ 66,983 $ 85,050 $ 58,573 $ 250,201 (-) Decrease in Net Investment Income ³ (3,704) (7,135) (2,464) 0 (13,303) (+) Reduction in Incentive Fee 4 556 1,070 370 0 1,995 Pro Forma Increase in Net Assets Resulting from Operations $ 36,447 $ 60,918 $ 82,956 $ 58,573 $ 238,893 Shareholder Fees & Expenses: Management fees (GAAP) $ 8,892 $ 13,376 $ 18,296 $ 10,246 $ 50,810 Incentive fees (GAAP) 6,996 11,790 17,839 12,137 48,762 (-) Reduction of Incentive Fees 4 (556) (1,070) (370) 0 (1,995) Professional fees (GAAP) 2,881 3,691 4,752 2,490 13,814 Directors' fees (GAAP) 287 285 342 186 1,100 Other general and administrative (GAAP) 1,564 2,434 3,858 2,429 10,285 Total Pro Forma Shareholder Fees & Expenses 20,064 30,506 44,717 27,488 122,776 Economic Profit (Pro Forma Increase in Net Assets Resulting from Operations + Total Pro Forma Shareholder Fees & Expenses) $ 56,511 $ 91,424 $ 127,673 $ 86,061 $ 361,669 TSLX NAV Per Share 12/31/2011 $ 14.71 TSLX Share Price 12/31/2011 1 14.71 Premium / (Discount) to NAV 12/31/2011 0 % Shares Outstanding (millions ) (as of 3/23/12) 6 14.57 TSLX NAV Per Share 6/30/2015 (released 8/4/2015) 5 $ 15.84 TSLX Share Price 8/05/2015 5 18.00 Premium / (Discount) to NAV 08/05/2015 14 % Shares Outstanding (millions ) (as of 8/5/2015) 54 Change in Premium / (Discount) to NAV 14 % Shareholder Value Gained / (Lost) Due to Change in Premium / (Disc.) to Average NAV $ 73,022 Total Economics (Economic Profit + Shareholder Value Gained / (Lost) Due to Change in Premium / (Disc.) to Average NAV) $434,691 Ratio of Total Pro Forma Shareholder Fees & Expenses to Total Economics 28 % 2 |

Home News&Fillings presentations How to vote About TPG specialty lending what people are saying contact information

persentations TPG specialty lending proposal: the right value maximizing Choice for TICC stockholders October 2015