February 2013

Creating Value at SandRidge Energy

1

DISCLAIMER

THIS PRESENTATION IS FOR GENERAL INFORMATIONAL PURPOSES ONLY. IT DOES NOT HAVE REGARD TO THE SPECIFIC

INVESTMENT OBJECTIVE, FINANCIAL SITUATION, SUITABILITY, OR THE PARTICULAR NEED OF ANY SPECIFIC PERSON WHO MAY

RECEIVE THIS PRESENTATION, AND SHOULD NOT BE TAKEN AS ADVICE ON THE MERITS OF ANY INVESTMENT DECISION. THE

VIEWS EXPRESSED HEREIN REPRESENT THE OPINIONS OF TPG-AXON MANAGEMENT LP, TPG-AXON PARTNERS GP, L.P., TPG-

AXON GP, LLC, TPG-AXON PARTNERS, LP, TPG-AXON INTERNATIONAL, L.P., TPG-AXON INTERNATIONAL GP, LLC, DINAKAR SINGH

LLC AND DINAKAR SINGH ("TPG-AXON" AND, TOGETHER WITH STEPHEN C. BEASLEY, EDWARD W. MONEYPENNY, FREDRIC G.

REYNOLDS, PETER H. ROTHSCHILD, ALAN J. WEBER AND DAN A. WESTBROOK, THE "PARTICIPANTS"), AND ARE BASED ON

PUBLICLY AVAILABLE INFORMATION WITH RESPECT TO SANDRIDGE ENERGY, INC. (THE "ISSUER").

INVESTMENT OBJECTIVE, FINANCIAL SITUATION, SUITABILITY, OR THE PARTICULAR NEED OF ANY SPECIFIC PERSON WHO MAY

RECEIVE THIS PRESENTATION, AND SHOULD NOT BE TAKEN AS ADVICE ON THE MERITS OF ANY INVESTMENT DECISION. THE

VIEWS EXPRESSED HEREIN REPRESENT THE OPINIONS OF TPG-AXON MANAGEMENT LP, TPG-AXON PARTNERS GP, L.P., TPG-

AXON GP, LLC, TPG-AXON PARTNERS, LP, TPG-AXON INTERNATIONAL, L.P., TPG-AXON INTERNATIONAL GP, LLC, DINAKAR SINGH

LLC AND DINAKAR SINGH ("TPG-AXON" AND, TOGETHER WITH STEPHEN C. BEASLEY, EDWARD W. MONEYPENNY, FREDRIC G.

REYNOLDS, PETER H. ROTHSCHILD, ALAN J. WEBER AND DAN A. WESTBROOK, THE "PARTICIPANTS"), AND ARE BASED ON

PUBLICLY AVAILABLE INFORMATION WITH RESPECT TO SANDRIDGE ENERGY, INC. (THE "ISSUER").

THE PARTICIPANTS RESERVE THE RIGHT TO CHANGE ANY OF THEIR OPINIONS EXPRESSED HEREIN AT ANY TIME AS THEY DEEM

APPROPRIATE. THE PARTICIPANTS DISCLAIM ANY OBLIGATION TO UPDATE THE INFORMATION CONTAINED HEREIN. THE

PARTICIPANTS HAVE NOT SOUGHT OR OBTAINED CONSENT FROM ANY THIRD PARTY TO USE ANY STATEMENTS OR INFORMATION

INDICATED IN THIS PRESENTATION AS HAVING BEEN OBTAINED OR DERIVED FROM STATEMENTS MADE OR PUBLISHED BY THIRD

PARTIES. ANY SUCH STATEMENTS OR INFORMATION SHOULD NOT BE VIEWED AS INDICATING THE SUPPORT OF SUCH THIRD

PARTY FOR THE VIEWS EXPRESSED HEREIN. NO WARRANTY IS MADE THAT DATA OR INFORMATION, WHETHER DERIVED OR

OBTAINED FROM FILINGS MADE WITH THE SEC OR FROM ANY THIRD PARTY, ARE ACCURATE. THE PARTICIPANTS SHALL NOT BE

RESPONSIBLE OR HAVE ANY LIABILITY FOR ANY MISINFORMATION CONTAINED IN ANY SEC FILING OR THIRD PARTY REPORT.

UNDER NO CIRCUMSTANCES IS THIS PRESENTATION TO BE USED OR CONSIDERED AS AN OFFER TO SELL OR A SOLICITATION OF

AN OFFER TO BUY ANY SECURITY.

APPROPRIATE. THE PARTICIPANTS DISCLAIM ANY OBLIGATION TO UPDATE THE INFORMATION CONTAINED HEREIN. THE

PARTICIPANTS HAVE NOT SOUGHT OR OBTAINED CONSENT FROM ANY THIRD PARTY TO USE ANY STATEMENTS OR INFORMATION

INDICATED IN THIS PRESENTATION AS HAVING BEEN OBTAINED OR DERIVED FROM STATEMENTS MADE OR PUBLISHED BY THIRD

PARTIES. ANY SUCH STATEMENTS OR INFORMATION SHOULD NOT BE VIEWED AS INDICATING THE SUPPORT OF SUCH THIRD

PARTY FOR THE VIEWS EXPRESSED HEREIN. NO WARRANTY IS MADE THAT DATA OR INFORMATION, WHETHER DERIVED OR

OBTAINED FROM FILINGS MADE WITH THE SEC OR FROM ANY THIRD PARTY, ARE ACCURATE. THE PARTICIPANTS SHALL NOT BE

RESPONSIBLE OR HAVE ANY LIABILITY FOR ANY MISINFORMATION CONTAINED IN ANY SEC FILING OR THIRD PARTY REPORT.

UNDER NO CIRCUMSTANCES IS THIS PRESENTATION TO BE USED OR CONSIDERED AS AN OFFER TO SELL OR A SOLICITATION OF

AN OFFER TO BUY ANY SECURITY.

THE PARTICIPANTS HAVE FILED WITH THE SEC A DEFINITIVE CONSENT STATEMENT AND ACCOMPANYING CONSENT CARD TO BE

USED TO SOLICIT WRITTEN CONSENTS FROM THE STOCKHOLDERS OF THE ISSUER IN CONNECTION WITH TPG-AXON'S INTENT TO

TAKE CORPORATE ACTION BY WRITTEN CONSENT. ALL STOCKHOLDERS OF THE ISSUER ARE ADVISED TO READ THE DEFINITIVE

CONSENT STATEMENT AND OTHER DOCUMENTS RELATED TO THE SOLICITATION OF WRITTEN CONSENTS BY THE PARTICIPANTS

FROM STOCKHOLDERS OF THE ISSUER BECAUSE THEY CONTAIN IMPORTANT INFORMATION, INCLUDING ADDITIONAL

INFORMATION RELATED TO THE PARTICIPANTS. THE DEFINITIVE CONSENT STATEMENT AND ACCOMPANYING CONSENT CARD

HAVE BEEN FURNISHED TO SOME OR ALL OF THE ISSUER'S STOCKHOLDERS AND ARE, ALONG WITH OTHER RELEVANT

DOCUMENTS, AVAILABLE AT NO CHARGE ON THE SEC'S WEB SITE AT HTTP://WWW.SEC.GOV. IN ADDITION, TPG-AXON WILL

PROVIDE COPIES OF THE DEFINITIVE CONSENT STATEMENT AND ACCOMPANYING CONSENT CARD WITHOUT CHARGE UPON

REQUEST.

USED TO SOLICIT WRITTEN CONSENTS FROM THE STOCKHOLDERS OF THE ISSUER IN CONNECTION WITH TPG-AXON'S INTENT TO

TAKE CORPORATE ACTION BY WRITTEN CONSENT. ALL STOCKHOLDERS OF THE ISSUER ARE ADVISED TO READ THE DEFINITIVE

CONSENT STATEMENT AND OTHER DOCUMENTS RELATED TO THE SOLICITATION OF WRITTEN CONSENTS BY THE PARTICIPANTS

FROM STOCKHOLDERS OF THE ISSUER BECAUSE THEY CONTAIN IMPORTANT INFORMATION, INCLUDING ADDITIONAL

INFORMATION RELATED TO THE PARTICIPANTS. THE DEFINITIVE CONSENT STATEMENT AND ACCOMPANYING CONSENT CARD

HAVE BEEN FURNISHED TO SOME OR ALL OF THE ISSUER'S STOCKHOLDERS AND ARE, ALONG WITH OTHER RELEVANT

DOCUMENTS, AVAILABLE AT NO CHARGE ON THE SEC'S WEB SITE AT HTTP://WWW.SEC.GOV. IN ADDITION, TPG-AXON WILL

PROVIDE COPIES OF THE DEFINITIVE CONSENT STATEMENT AND ACCOMPANYING CONSENT CARD WITHOUT CHARGE UPON

REQUEST.

INFORMATION ABOUT THE PARTICIPANTS AND A DESCRIPTION OF THEIR DIRECT OR INDIRECT INTERESTS BY SECURITY

HOLDINGS IS CONTAINED IN THE DEFINITIVE CONSENT STATEMENT ON SCHEDULE 14A FILED BY TPG-AXON WITH THE SEC ON

JANUARY 18, 2013. THIS DOCUMENT CAN BE OBTAINED FREE OF CHARGE FROM THE SOURCES INDICATED ABOVE.

HOLDINGS IS CONTAINED IN THE DEFINITIVE CONSENT STATEMENT ON SCHEDULE 14A FILED BY TPG-AXON WITH THE SEC ON

JANUARY 18, 2013. THIS DOCUMENT CAN BE OBTAINED FREE OF CHARGE FROM THE SOURCES INDICATED ABOVE.

2

Agenda

Ø Overview

Ø Company Background & Performance

Ø Management Compensation & Related Party Transactions

Ø The Path to Value

Ø Company Response

Ø Appendix: Related Party Transactions Presentation

3

A few Warren Buffett quotes…

Ø Time is the friend of the wonderful business. It's the enemy of the lousy business. If you're in a

lousy business for a long time, you're going to get a lousy result, even if you buy it cheap.

lousy business for a long time, you're going to get a lousy result, even if you buy it cheap.

Ø Whenever I read about some company undertaking a cost-cutting program, I know it's not a

company that really knows what costs are all about. Spurts don't work in this area. The really good

manager does not wake up in the morning and say, "This is the day I'm going to cut costs," any

more than he wakes up and decides to practice breathing.

company that really knows what costs are all about. Spurts don't work in this area. The really good

manager does not wake up in the morning and say, "This is the day I'm going to cut costs," any

more than he wakes up and decides to practice breathing.

Ø A company that wants to use its own stock as currency for an acquisition has no problems if the

stock is selling in the market at full intrinsic value. But suppose it is selling at only half intrinsic

value. In that case it is faced with the unhappy prospect of using a substantially undervalued

currency to pay for a fully valued property [the negotiated price of the target company]. In effect the

acquirer must give up $2 of value to receive $1 of value. Under such circumstances, a marvelous

business purchased at a fair sales price becomes a terrible buy. For gold valued as gold cannot be

purchased intelligently through the utilization of gold valued as lead.

stock is selling in the market at full intrinsic value. But suppose it is selling at only half intrinsic

value. In that case it is faced with the unhappy prospect of using a substantially undervalued

currency to pay for a fully valued property [the negotiated price of the target company]. In effect the

acquirer must give up $2 of value to receive $1 of value. Under such circumstances, a marvelous

business purchased at a fair sales price becomes a terrible buy. For gold valued as gold cannot be

purchased intelligently through the utilization of gold valued as lead.

Ø It has become fashionable at public companies to describe almost every compensation plan as

aligning the interests of management with those of shareholders. In our book, alignment means

being a partner in both directions, not just on the upside. Many 'alignment' plans flunk this basic

test, being artful forms of 'heads I win, tails you lose.‘

aligning the interests of management with those of shareholders. In our book, alignment means

being a partner in both directions, not just on the upside. Many 'alignment' plans flunk this basic

test, being artful forms of 'heads I win, tails you lose.‘

Ø I look for businesses in which I think I can predict what they're going to look like in ten to fifteen

years time.

years time.

Ø Should you find yourself in a chronically-leaking boat, energy devoted to changing vessels is likely

to be more productive than energy devoted to patching leaks.

to be more productive than energy devoted to patching leaks.

4

…as applied to SandRidge Energy

Ø Time is the friend of the wonderful business. It's the enemy of the lousy business. If you're in a lousy business for a long

time, you're going to get a lousy result, even if you buy it cheap.

time, you're going to get a lousy result, even if you buy it cheap.

Ø SandRidge has valuable assets, but its high cost structure make it a lousy business as

currently configured. Time is not our friend, since the drain from high financing and

overhead costs are a severe impediment to value creation.

currently configured. Time is not our friend, since the drain from high financing and

overhead costs are a severe impediment to value creation.

Ø Whenever I read about some company undertaking a cost-cutting program, I know it's not a company that really knows

what costs are all about. Spurts don't work in this area. The really good manager does not wake up in the morning and

say, "This is the day I'm going to cut costs," any more than he wakes up and decides to practice breathing.

what costs are all about. Spurts don't work in this area. The really good manager does not wake up in the morning and

say, "This is the day I'm going to cut costs," any more than he wakes up and decides to practice breathing.

Ø Overhead costs are massive in any context, and many appear extravagant and unrelated to

necessary operations. Management has been increasing overhead spending, rather than

reducing it, despite financing pressures. This ‘tax’ on the company is destroying value.

necessary operations. Management has been increasing overhead spending, rather than

reducing it, despite financing pressures. This ‘tax’ on the company is destroying value.

Ø A company that wants to use its own stock as currency for an acquisition has no problems if the stock is selling in the

market at full intrinsic value. But suppose it is selling at only half intrinsic value. In that case it is faced with the unhappy

prospect of using a substantially undervalued currency to pay for a fully valued property [the negotiated price of the target

company]. In effect the acquirer must give up $2 of value to receive $1 of value. Under such circumstances, a marvelous

business purchased at a fair sales price becomes a terrible buy. For gold valued as gold cannot be purchased intelligently

through the utilization of gold valued as lead.

market at full intrinsic value. But suppose it is selling at only half intrinsic value. In that case it is faced with the unhappy

prospect of using a substantially undervalued currency to pay for a fully valued property [the negotiated price of the target

company]. In effect the acquirer must give up $2 of value to receive $1 of value. Under such circumstances, a marvelous

business purchased at a fair sales price becomes a terrible buy. For gold valued as gold cannot be purchased intelligently

through the utilization of gold valued as lead.

Ø SandRidge stock trades at a significant discount to estimated NAV. Repeated deals, using

stock as currency, have resulted in 70% dilution of stockholder ownership - the highest of

its peer group to a dramatic degree.

stock as currency, have resulted in 70% dilution of stockholder ownership - the highest of

its peer group to a dramatic degree.

5

…as applied to SandRidge Energy (continued)

Ø It has become fashionable at public companies to describe almost every compensation plan as aligning the interests of

management with those of shareholders. In our book, alignment means being a partner in both directions, not just on the

upside. Many 'alignment' plans flunk this basic test, being artful forms of 'heads I win, tails you lose.‘

management with those of shareholders. In our book, alignment means being a partner in both directions, not just on the

upside. Many 'alignment' plans flunk this basic test, being artful forms of 'heads I win, tails you lose.‘

Ø We believe management incentives are completely misaligned with the interests of

shareholders. Management compensation and rewards have been extraordinary, and

grown dramatically, even as shareholder value has been dramatically destroyed. Related

party transactions also raise significant concerns regarding ethics, incentives and

alignment. It is simply appalling that the CEO’s family is one of the most significant

competitors to the company, and has bought enormous amount of mineral rights and land,

alongside, or even in advance of, SandRidge.

shareholders. Management compensation and rewards have been extraordinary, and

grown dramatically, even as shareholder value has been dramatically destroyed. Related

party transactions also raise significant concerns regarding ethics, incentives and

alignment. It is simply appalling that the CEO’s family is one of the most significant

competitors to the company, and has bought enormous amount of mineral rights and land,

alongside, or even in advance of, SandRidge.

Ø I look for businesses in which I think I can predict what they're going to look like in ten to fifteen years time.

Ø Repeated deals have resulted in significant oscillation in the company focus and asset mix

- from high-cost gas and CO2 to oil, from offshore to onshore, from vertical drilling to

horizontal drilling, from proven to unproven to mature profiles. The company now

professes a focus on the Mississippian, but its track record suggests that there can be little

predictability regarding what assets shareholders will own in the future.

- from high-cost gas and CO2 to oil, from offshore to onshore, from vertical drilling to

horizontal drilling, from proven to unproven to mature profiles. The company now

professes a focus on the Mississippian, but its track record suggests that there can be little

predictability regarding what assets shareholders will own in the future.

6

SandRidge is a ‘chronically leaking boat’ - change is necessary!

“Should you find yourself in a chronically-leaking boat, energy devoted to changing vessels is

likely to be more productive than energy devoted to patching leaks.”

likely to be more productive than energy devoted to patching leaks.”

Ø SandRidge performance since its IPO in 2007, and under the watch of the current Board, has been

a tragedy for shareholders. Value has been destroyed to an extraordinary degree, on both an

absolute and relative basis

a tragedy for shareholders. Value has been destroyed to an extraordinary degree, on both an

absolute and relative basis

Ø Corporate governance is appalling - management compensation and related party transactions

create significant concerns about ethics, incentive, and efficiency

create significant concerns about ethics, incentive, and efficiency

Ø As the company is currently run, we believe there will be little upside/return to shareholders in

coming years. Costs (financing costs and overhead expenditures) are simply too high, and burn

tremendous value, particularly given the strain of massive financing needs for years to come

coming years. Costs (financing costs and overhead expenditures) are simply too high, and burn

tremendous value, particularly given the strain of massive financing needs for years to come

Ø BUT, if the company were operated in a more efficient and focused manner, we believe there would

be very significant potential upside and return. With efficient and disciplined oversight and

leadership, we believe value can be restored and grown

be very significant potential upside and return. With efficient and disciplined oversight and

leadership, we believe value can be restored and grown

Ø Given the track record since 2007, shareholders cannot rely upon current directors to provide

necessary oversight and leadership. Therefore, change is necessary, and fortunately there is a path

to effect that change.

necessary oversight and leadership. Therefore, change is necessary, and fortunately there is a path

to effect that change.

7

Our action plan can restore and build value for shareholders

Ø Exhaustive analysis and planning for the ‘first 100 days’ has already begun, including plans

regarding formation of Board Committees, hiring of external advisors, etc.

regarding formation of Board Committees, hiring of external advisors, etc.

Ø Replace CEO Tom Ward with a well-regarded, experienced CEO. We have initiated a search

process, and we believe there are strong external, and possibly internal, candidates. We do not

want to replace the value-added operational leaders of the company - we want to replace Tom

Ward.

process, and we believe there are strong external, and possibly internal, candidates. We do not

want to replace the value-added operational leaders of the company - we want to replace Tom

Ward.

Ø Reduce overhead significantly, freeing up valuable cashflow for debt reduction.

Ø Continue exhaustive analysis, with an expectation of reducing overhead spending from $200+ million to $50 - 75

million.

million.

Ø Management compensation, travel, advertising and promotion, and excessive real estate offer obvious and

substantial targets for reduction

substantial targets for reduction

Ø Reduce debt through sale and monetization of non-core assets

Ø Examine a sale of the Dynamic Offshore Assets purchased last year

Ø Pursue a monetization of infrastructure assets

Ø Pursue additional reductions in or sale of working interests in the Mississippian to reduce the

massive capital expenditure needs of the company

massive capital expenditure needs of the company

Ø Consider a sale of the company, but plan and assume that long term value will be maximized

through efficient and focused development of the Mississippian assets

through efficient and focused development of the Mississippian assets

8

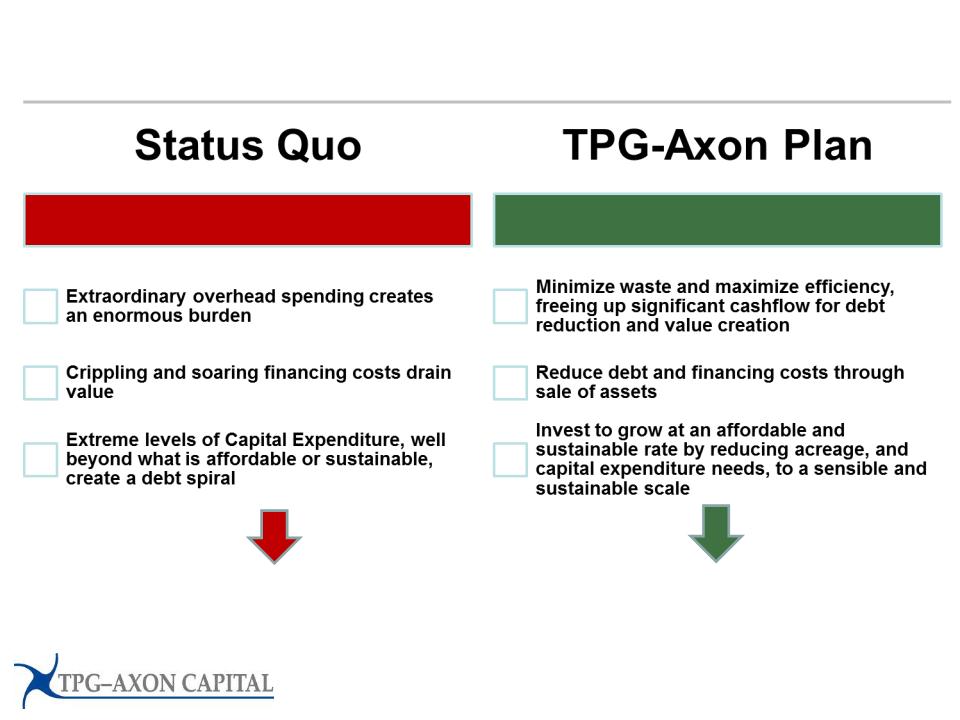

The status quo will yield little value for stockholders, but

significant value creation is possible with change

significant value creation is possible with change

Value is drained by overhead and

financing costs…little equity value left

despite the massive investment

financing costs…little equity value left

despite the massive investment

Company emerges as a well-capitalized,

high-growth energy company that could

enable stockholders to realize

NAV per share of $10 - 12 +

high-growth energy company that could

enable stockholders to realize

NAV per share of $10 - 12 +

9

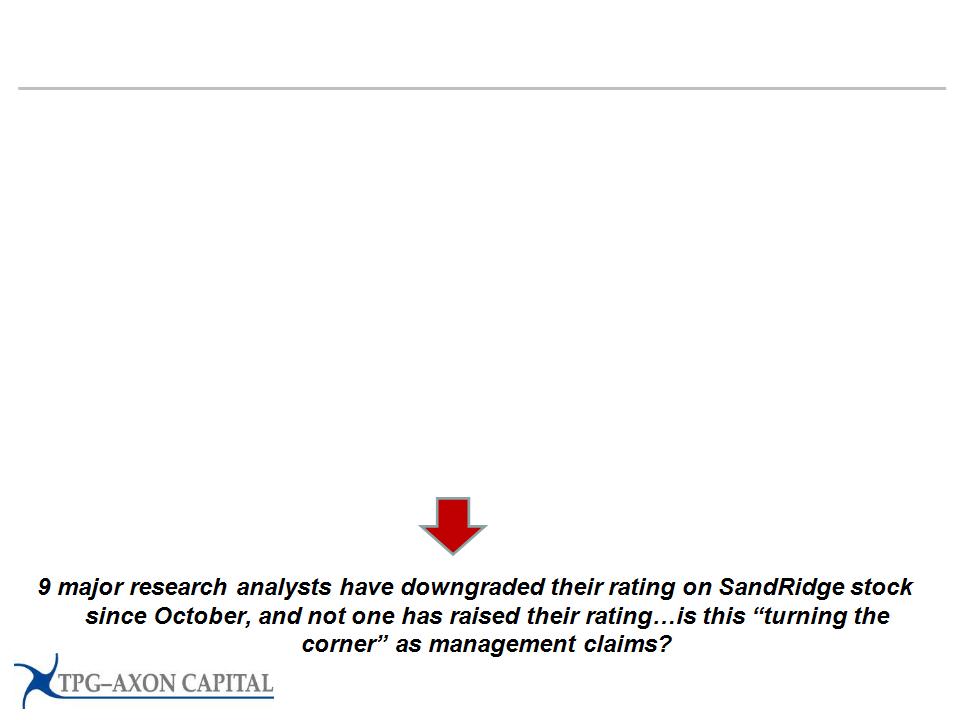

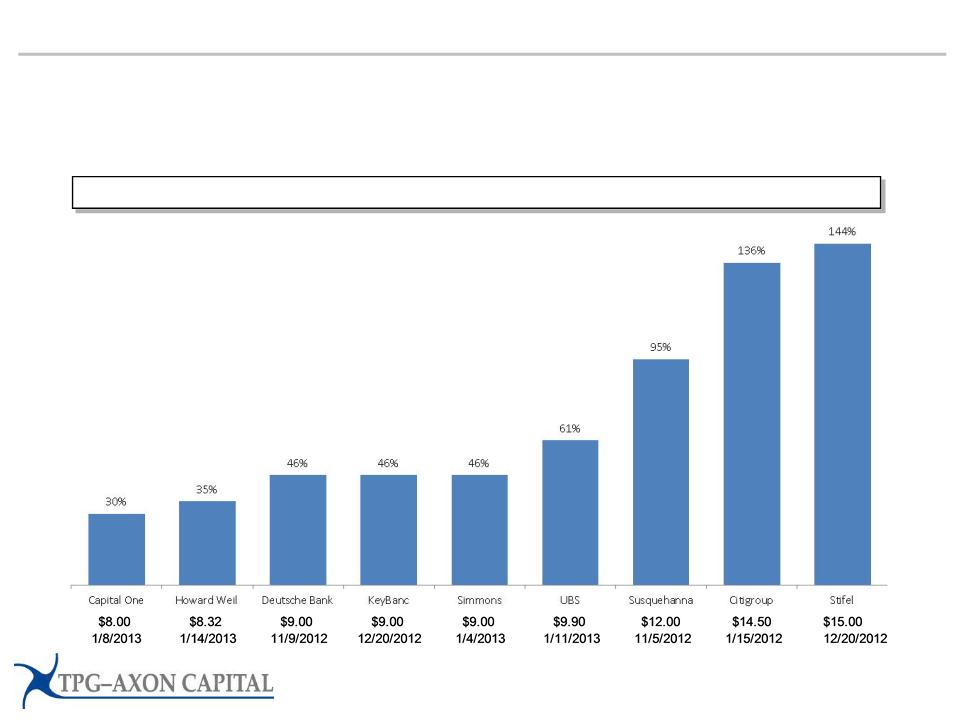

The company claims it is moving in the right direction…we disagree!

Ø Is this progress? Consider the following recent developments…

Ø 9 recent rating downgrades from research analysts

Ø Significant recent decline in the stock

Ø Reduced management guidance for Mississippian returns

Ø Weaker than expected Mississippian results from producing wells in the SandRidge Royalty

Trusts

Trusts

Ø Have the Board of Directors and Management changed their ways? Consider their

actions over the past year or so…

actions over the past year or so…

Ø Announced $21 million in compensation for Tom Ward for 2012; yet again, an extraordinary

amount relative to peers, and outrageous relative to the poor stock performance of the company

amount relative to peers, and outrageous relative to the poor stock performance of the company

Ø Amended Tom Ward’s employment agreement (December 2011) to actually expand the ability for

Tom Ward to compete with the company!

Tom Ward to compete with the company!

Ø Purchased a new, and even better, private jet for Tom Ward’s personal use - a Falcon 900EX

(which has 6,000 mile flying range and lists for $35 million)

(which has 6,000 mile flying range and lists for $35 million)

Ø Engaged in more unexpected M&A, including the acquisition of Dynamic Offshore

Ø Enacted a poison pill

10

The consent solicitation process

Ø Proposal 1: amend bylaws — amended bylaws are necessary for the removal of existing Board members

Ø (i) De-stagger the board of directors of the Company (the "Board") by providing that directors will be elected for one-

year terms beginning with the 2013 annual meeting of stockholders,

year terms beginning with the 2013 annual meeting of stockholders,

Ø (ii) Provide that the size of the Board may be fixed by either a majority vote of the Board or vote of the stockholders,

Ø (iii) Provide that vacancies on the Board may be filled by the stockholders or by a majority vote of the remaining

directors of the Board, and

directors of the Board, and

Ø (iv) Provide that directors may be removed with or without cause.

Ø Proposal 2: remove existing Board — removal of current Directors is needed to effect change

Ø Remove all seven current members of the Board: Jim J. Brewer, Everett R. Dobson, William A. Gilliland, Daniel W.

Jordan, Roy T. Oliver, Jr., Jeffrey S. Serota and Tom L. Ward (and any person or persons, other than those elected by

our Consent Solicitation, elected, appointed or designated by the Board (or any committee thereof) to fill any vacancy

or newly created directorship since December 26, 2012 and prior to the time that any of the actions proposed to be

taken by our Consent Solicitation become effective)

Jordan, Roy T. Oliver, Jr., Jeffrey S. Serota and Tom L. Ward (and any person or persons, other than those elected by

our Consent Solicitation, elected, appointed or designated by the Board (or any committee thereof) to fill any vacancy

or newly created directorship since December 26, 2012 and prior to the time that any of the actions proposed to be

taken by our Consent Solicitation become effective)

Ø Proposal 3: elect independent Nominees — we believe independent Nominees will work to drastically reduce

overhead and waste, sell extraneous assets, reduce future funding needs and consider a sale of entire company

overhead and waste, sell extraneous assets, reduce future funding needs and consider a sale of entire company

Ø Elect Stephen C. Beasley, Edward W. Moneypenny, Fredric G. Reynolds, Peter H. Rothschild, Dinakar Singh, Alan J.

Weber and Dan A. Westbrook (the "Nominees") as directors to fill the resulting vacancies on the Board (or if any

Nominee becomes unable or unwilling to serve as a director of the Company or if the size of the Board is increased, in

either case prior to the effectiveness of this Proposal, any other person who is not a director, officer, employee or

affiliate of TPG-Axon, designated as a Nominee by TPG-Axon)

Weber and Dan A. Westbrook (the "Nominees") as directors to fill the resulting vacancies on the Board (or if any

Nominee becomes unable or unwilling to serve as a director of the Company or if the size of the Board is increased, in

either case prior to the effectiveness of this Proposal, any other person who is not a director, officer, employee or

affiliate of TPG-Axon, designated as a Nominee by TPG-Axon)

Ø To be successful, we need to deliver to SandRidge consents from stockholders representing more than 50% of

outstanding shares by March 15, 2013

outstanding shares by March 15, 2013

11

Agenda

Ø Overview

Ø Company Background & Performance

Ø Management Compensation & Related Party Transactions

Ø The Path to Value

Ø Company Response

Ø Appendix: Related Party Transactions Presentation

12

Three eras of energy over the past 25 years

1990s

Is there

demand growth?

demand growth?

► US Recession… Japanese

bubble bursts… Collapse of the

Soviet Bloc… Asian Crisis

bubble bursts… Collapse of the

Soviet Bloc… Asian Crisis

► Persistently low energy prices

► Modest focus on reserve

replacement; capital

expenditure / investment

budgets were low and did not

grow for a decade

replacement; capital

expenditure / investment

budgets were low and did not

grow for a decade

► Focus was on costs (low cost of

production, and low cost of

reserve replacement)

production, and low cost of

reserve replacement)

Now

Plenty of both, but costs

and price matter!

and price matter!

► Plenty of potential supply, in

both oil and gas

both oil and gas

► Massive investment began to

bear fruit

bear fruit

► Collapse in the gas market,

since markets are local

since markets are local

► Oil has fared better, but supply

response is substantial, so

costs matter

response is substantial, so

costs matter

► Focus is now on supply…at

the right price. Efficiency

matters!

the right price. Efficiency

matters!

2003-2008

Is there

enough supply?

enough supply?

► Global synchronized

growth…booming BRICS and

other emerging markets

growth…booming BRICS and

other emerging markets

► Years of low investment

resulted in slow supply

response

resulted in slow supply

response

► Surging prices for both oil and

gas - dreams of $200 oil

gas - dreams of $200 oil

► New technologies led to a

mad rush to develop new

supplies

mad rush to develop new

supplies

► Focus was on acquiring

reserves…the more the better,

at almost at any price

reserves…the more the better,

at almost at any price

13

Ø Use of significant leverage to acquire assets, even to the extent it resulted in low credit ratings and

high cost of capital

high cost of capital

Ø After all, if prices were going to perpetually rise, the more assets the better!

Ø Likewise, financing costs don’t matter if one assumes asset values will rise dramatically

Ø But what about the risk to shareholders if the outlook changed? Or the drain on value from high

financing costs if asset values did not keep rising?

financing costs if asset values did not keep rising?

Ø Spending well in excess of organic cashflow

Ø Primary focus on acquiring early-stage assets resulted in a chronic need to seek external financing to then develop

those assets

those assets

Ø Highly reliant upon capital markets to fund cashflow deficits, including repeated issuances of equity

Ø But how can value be created when capital expenditures are funded with extremely expensive debt

capital, and shareholders are constantly diluted?

capital, and shareholders are constantly diluted?

Ø Lavish overhead spending, particularly on compensation, and CEO related party transactions

Ø Overhead spending - compensation, administration, promotional expenses, real estate, perquisites - were, and remain,

staggeringly high. As a % of market capitalization, overhead spending for SandRidge is the highest of its peer

group…only Chesapeake comes close!

staggeringly high. As a % of market capitalization, overhead spending for SandRidge is the highest of its peer

group…only Chesapeake comes close!

Ø Personal payments and related-party transactions are a distasteful hallmark of both companies…but we believe the

SandRidge related-party land transactions are particularly troubling

SandRidge related-party land transactions are particularly troubling

Chesapeake and SandRidge are the poster-children for the ‘costs do

not matter’ era

not matter’ era

14

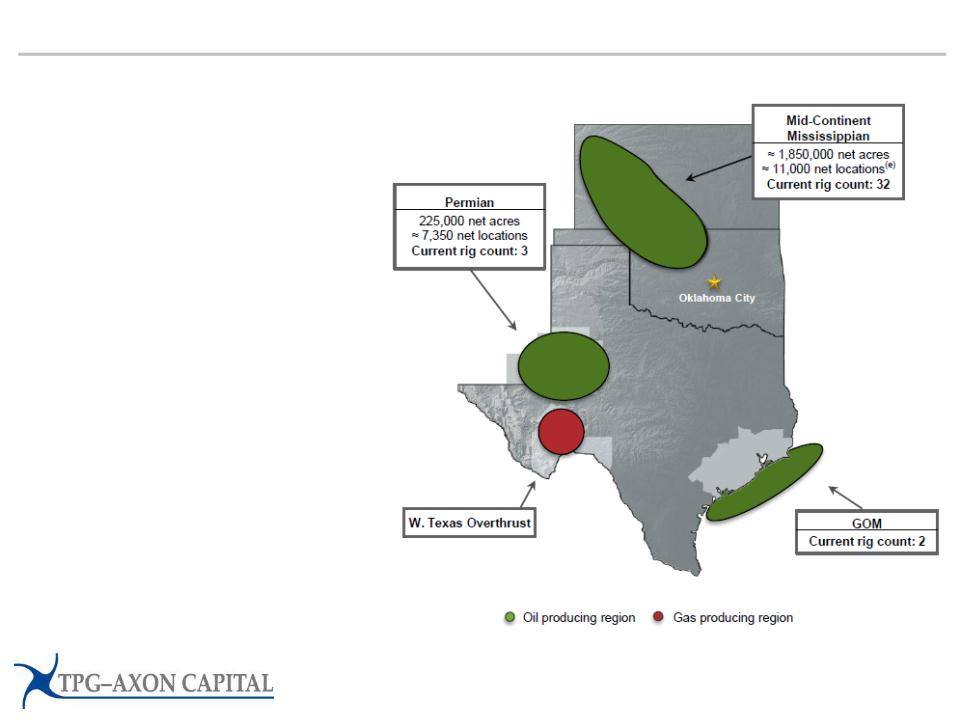

SandRidge overview

Ø SandRidge Energy is an oil & gas

exploration and production company

exploration and production company

Ø Headquartered in Oklahoma City, OK

Ø Public since 2007 (NYSE: SD)

Ø ~$3bn market capitalization, ~$9bn

enterprise value

enterprise value

Ø SandRidge has been run by Chairman

and CEO Tom Ward since 2006

Ø Mr. Ward was the co-founder and

former COO of Chesapeake Energy

former COO of Chesapeake Energy

Ø SandRidge produces ~100 mboe/d of

oil & gas across four plays

Ø Mississippian. 1.85mm net acres

across Oklahoma and Kansas

across Oklahoma and Kansas

Ø Permian. Acquired Forest Oil’s assets

and Arena Resources in 2009 and

2010. Sold ~80% of Permian position

in December 2012 for $2.6bn

and Arena Resources in 2009 and

2010. Sold ~80% of Permian position

in December 2012 for $2.6bn

Ø GOM. Acquired Dynamic Offshore in

February 2012 for $1.3bn

February 2012 for $1.3bn

Ø WTO. Legacy high-cost gas field

Source: SandRidge filings, TPG-Axon analysis of value

Sold ~80% in

December 2012

December 2012

15

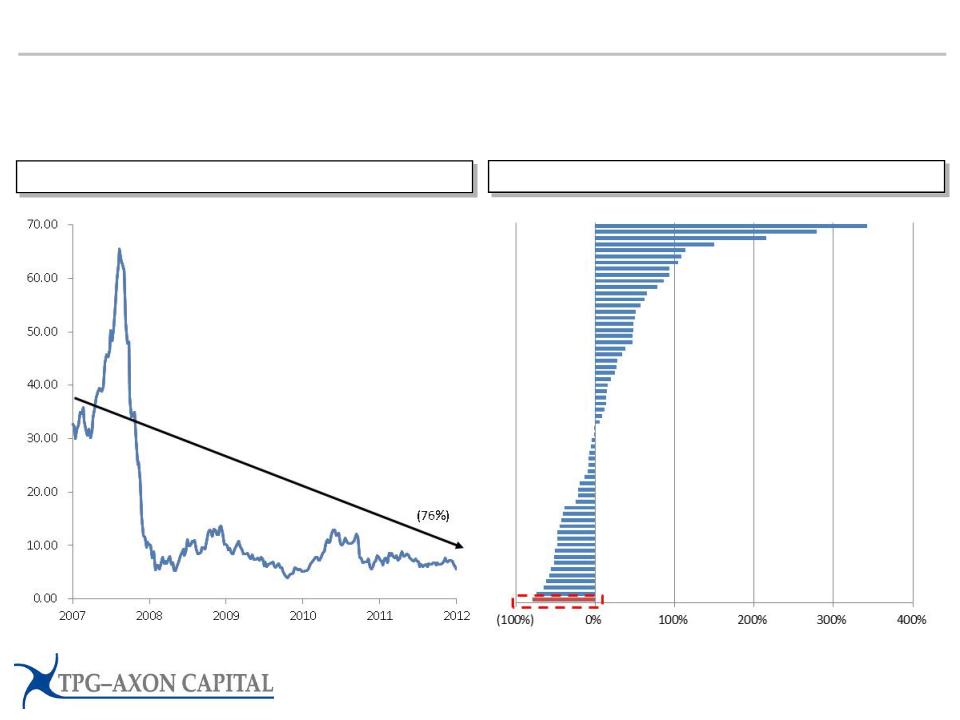

Massive destruction of shareholder value

Ø SandRidge has declined almost 80% from its IPO level in 2007, and is the single worst

performing energy stock over that period in the Russell 1000 Index

performing energy stock over that period in the Russell 1000 Index

Stock Performance Since IPO

Performance Versus Russell 1000 Energy Stocks

Source: Bloomberg

Performance from November 6, 2007 ($26.00) to February 6, 2013 ($6.15)

Relative performance based on 70 energy stocks currently in Russell 1000 Index

16

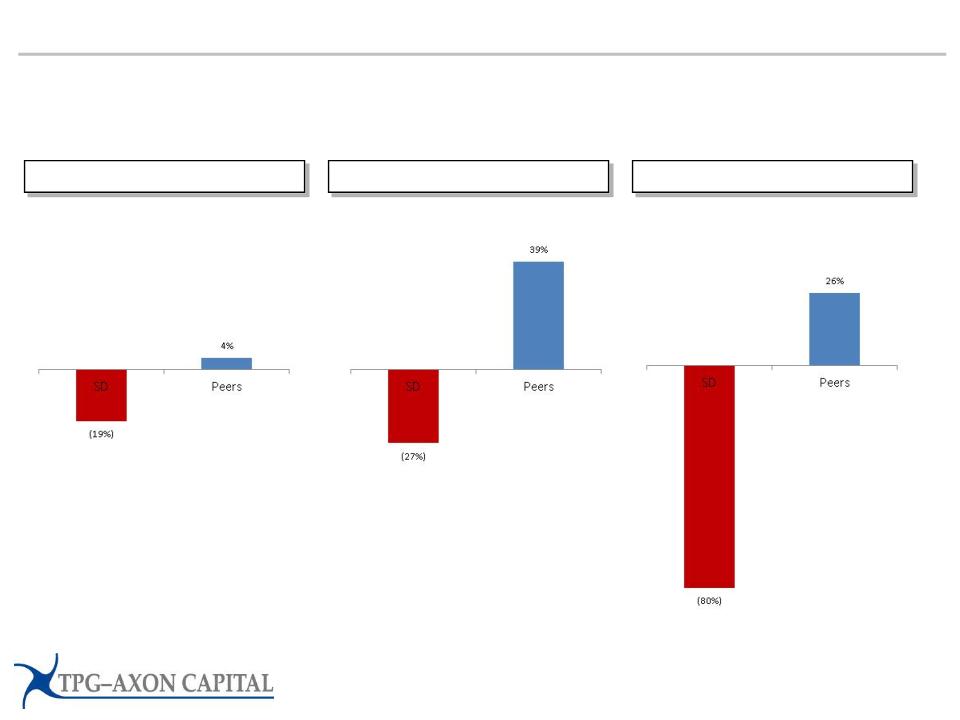

Severe and ongoing stock underperformance

Ø This underperformance is not just a function of 2008. SandRidge stock has significantly

underperformed its peer group average on a 1-Year and 3-Year and 5-Year basis

underperformed its peer group average on a 1-Year and 3-Year and 5-Year basis

1 Year Return

3 Year Return

5 Year Return

Source: Bloomberg; market data as of February 6, 2013

Peers based on SandRidge consent revocation statement on January 18, 2013

17

Massive destruction of company value under current management

Destruction of Book Value Per Share

Destruction of Net Asset Value Per Share

Ø Book value has declined a staggering 77% since the IPO, and to a degree greater than

any of its peers over this period

any of its peers over this period

Ø Net asset value has also declined dramatically since the IPO

Source: SandRidge filings, JPMorgan

18

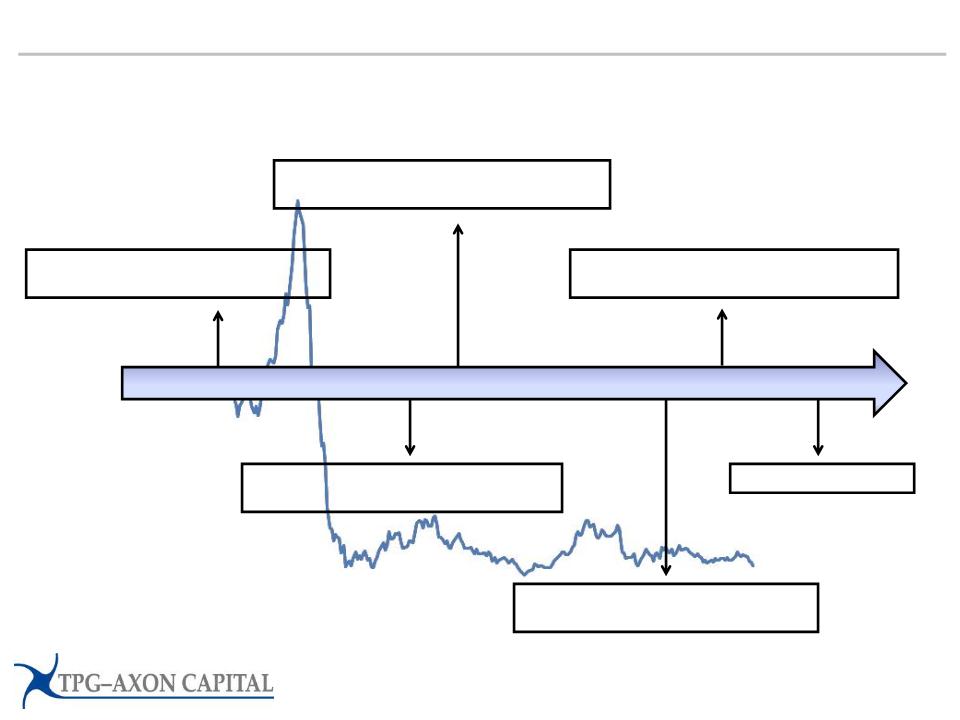

Poor strategic choices and repeated shifts in strategy

Ø To many in the investment community, SandRidge has often appeared to behave in an

unpredictable manner. SandRidge has gone through at least 5 strategic changes since going

public in 2007!

unpredictable manner. SandRidge has gone through at least 5 strategic changes since going

public in 2007!

2007 2008 2009 2010 2011 2012 2013

Developing high cost natural gas in the

West Texas Overthrust

West Texas Overthrust

Acquired mature, conventional oil and gas

production in the Permian Basin

production in the Permian Basin

Acquired high declining, offshore assets

in the Gulf of Mexico

in the Gulf of Mexico

Sold Permian assets to re-focus company

on Mississippian Lime

on Mississippian Lime

What’s next?

Developing unconventional oil and gas

production in Mississippian Lime

production in Mississippian Lime

SandRidge share price since IPO

Source: Bloomberg

19

Many analysts have been surprised, confused, and disturbed by

management actions

management actions

Ø “At the end of the day, the biggest casualty of a Permian sale may be investors’ confidence in

management, with its second significant strategic change in less than a year”.

Ryan Todd, Deutsche Bank, 11/13/2012

management, with its second significant strategic change in less than a year”.

Ryan Todd, Deutsche Bank, 11/13/2012

Ø “Since the market seems to lack confidence in the company’s financial position and strategy, we think the

company will trade at a discount to the group median until that confidence grows”.

Joseph Allman, JPMorgan, 11/16/2012

company will trade at a discount to the group median until that confidence grows”.

Joseph Allman, JPMorgan, 11/16/2012

Ø “SD’s decision to sell the Permian comes as a bit of a surprise… At this point, with the switch in strategy

and significant moving parts we are unsure if it is prudent to give SD the benefit of the doubt”.

Stephen Shepherd, Simmons, 11/9/2012

and significant moving parts we are unsure if it is prudent to give SD the benefit of the doubt”.

Stephen Shepherd, Simmons, 11/9/2012

Ø “We remain perplexed as to why a land-based E&P company would go so far out of its operating model [to

acquire Dynamic Offshore], only to several months later entertain selling a core asset with a much lower

operating risk profile”.

Curtis Trimble, Global Hunter, 11/12/2012

acquire Dynamic Offshore], only to several months later entertain selling a core asset with a much lower

operating risk profile”.

Curtis Trimble, Global Hunter, 11/12/2012

20

SandRidge expenditures put in context

Source: company filings, Bloomberg; market data as of February 6, 2013

Ø SandRidge has massive operating and financial leverage

Ø Market capitalization is a ‘sliver’ of future expenditures in overhead, interest and capital expenditures. In

just the next year, expenditures on these three will represent over 70% of the entire current market

capitalization of the company!

just the next year, expenditures on these three will represent over 70% of the entire current market

capitalization of the company!

Ø Unless all three are reduced, the risk to shareholders will be enormous, and the stock could

become the equivalent of an out-of-the-money option

become the equivalent of an out-of-the-money option

21

Chronic spending in excess of organic cashflow and lack of financial

discipline…

discipline…

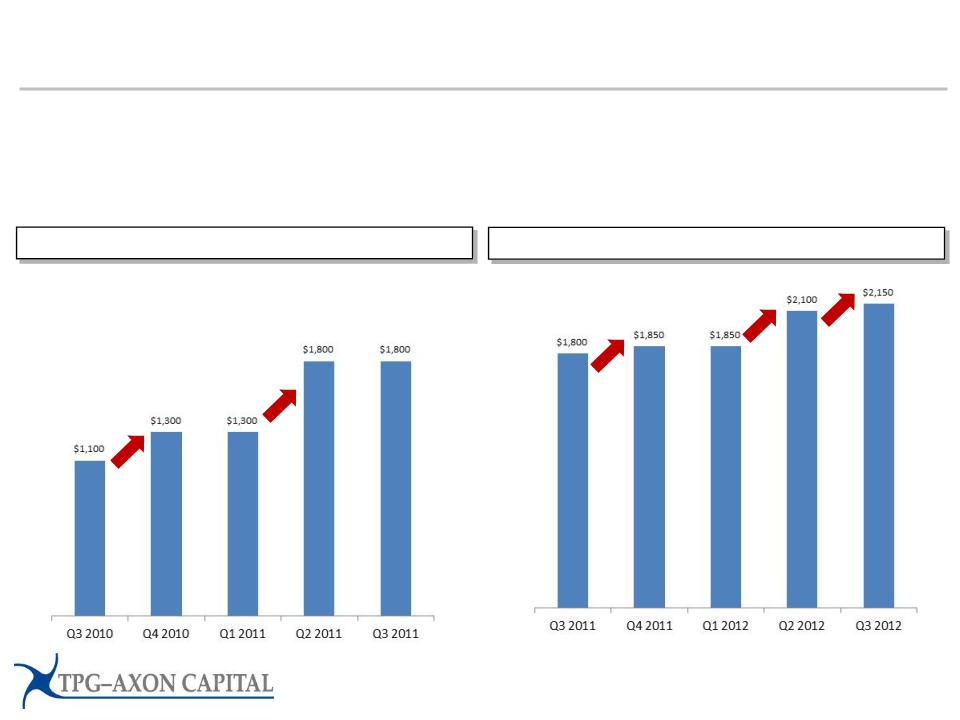

Ø The company’s capital expenditure budgets have been frequently exceeded,

damaging management credibility.

damaging management credibility.

Ø Capital expenditure guidance has been raised five times in the last two years!

Source: SandRidge filings

2011 Capital Expenditure Guidance

2012 Capital Expenditure Guidance

22

…Has resulted in severe damage to credit ratings and massive dilution

Lowest Credit Rating Among Peers

Most Equity Dilution Among Peers

Ø Management decisions have left the company vulnerable to market and economic shifts, resulting in

severe damage during economic and market downturns

severe damage during economic and market downturns

Ø Shareholder value has been drained by high financing costs, massive dilution from equity issuances,

and the sale of good assets to fund shortfalls in cashflow

and the sale of good assets to fund shortfalls in cashflow

Source: Bloomberg, Standard & Poor’s

Peers based on SandRidge consent revocation statement on January 18, 2013

S&P issuer

credit rating

credit rating

Change in shares

outstanding since

Q4 2007

outstanding since

Q4 2007

23

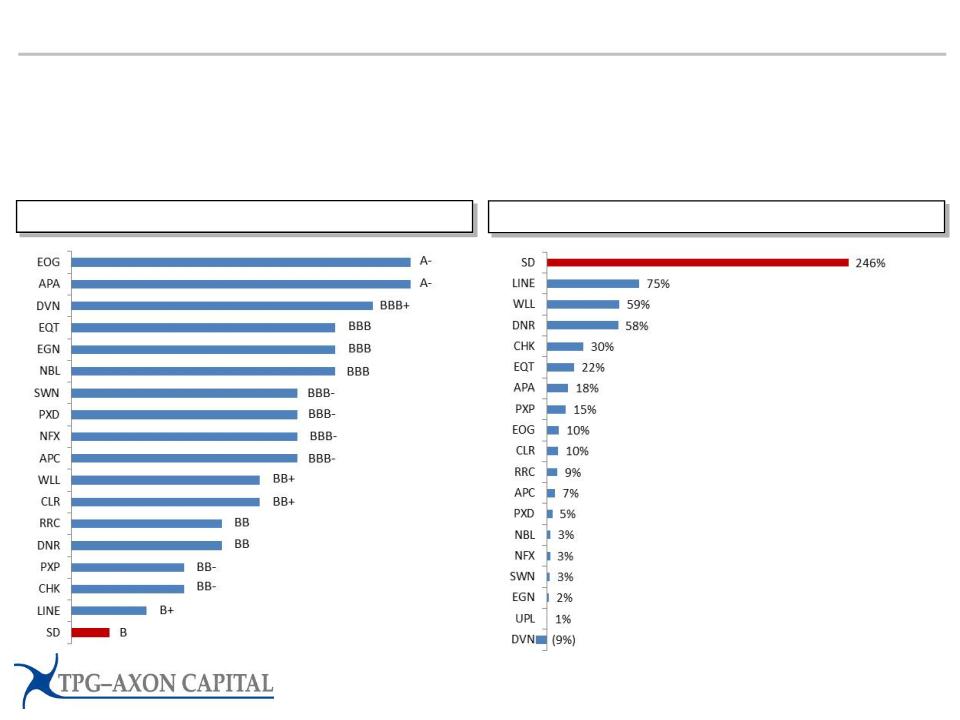

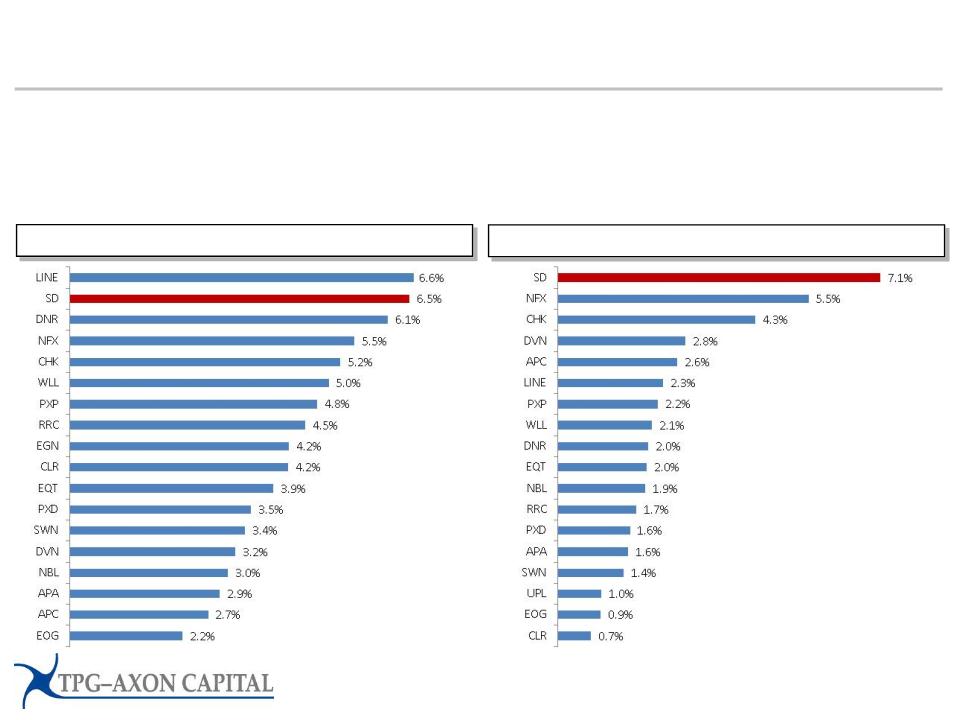

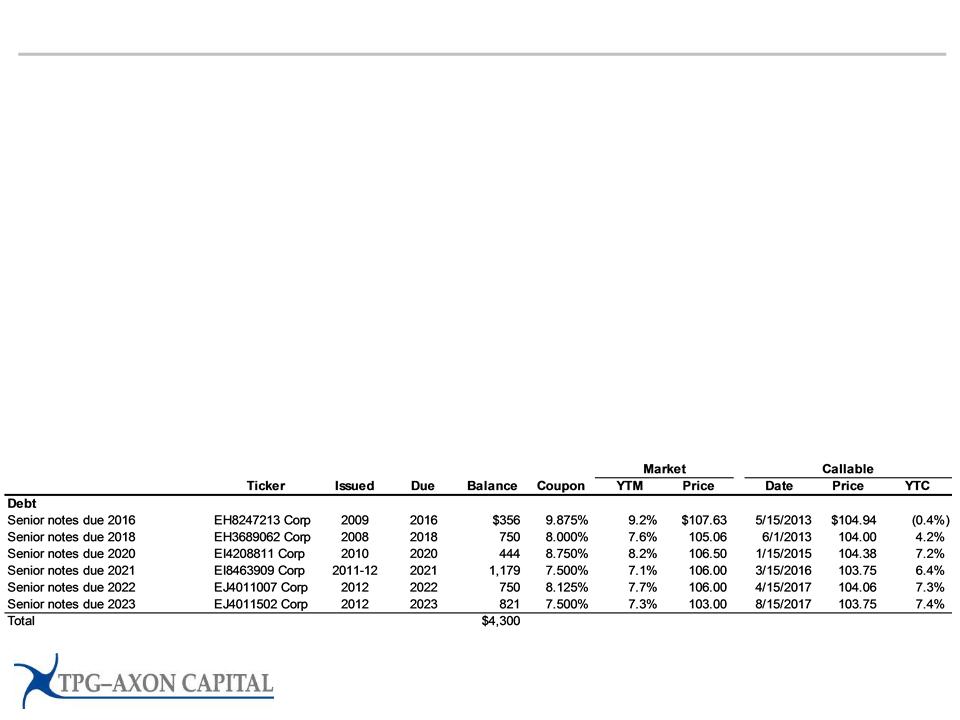

Leakage of value from high cost of capital and extraordinary overhead

spending

spending

Ø High cost of debt is an enormous tax on shareholders. Example: the difference in incremental cost of debt

between Devon Energy and SandRidge represents $100 million per year in drain to the company!

between Devon Energy and SandRidge represents $100 million per year in drain to the company!

Ø Overhead spending is the highest of any peer company, and as much as triple that of some peers.

Corporate overhead is over $200 million per year, more than 7% of its market capitalization

Corporate overhead is over $200 million per year, more than 7% of its market capitalization

Highest Cost of Debt Among Peers

Highest Overhead Costs Among Peers

Source: Bloomberg; market data as of February 6, 2013

Peers based on SandRidge consent revocation statement on January 18, 2013

Yield to maturity of

benchmark 8-10 year

senior notes

benchmark 8-10 year

senior notes

G&A expense (YTD 2012

annualized), as percentage

of market cap

annualized), as percentage

of market cap

24

Agenda

Ø Overview

Ø Company Background & Performance

Ø Management Compensation & Related Party Transactions

Ø The Path to Value

Ø Company Response

Ø Appendix: Related Party Transactions Presentation

Where do stockholder interests fit in this puzzle?

25

Extraordinary

Compensation

Massive

payments for

personal assets

payments for

personal assets

Lavish Perks

Side-dealing and competition

Management, or their families, should not be competing

with shareholders!

with shareholders!

26

Ø We believe the management and Board of Directors of any company -

including SandRidge - should have one overriding objective…creating

value for shareholders

including SandRidge - should have one overriding objective…creating

value for shareholders

Ø As a general business principle, we believe it is inappropriate and

unethical for any management or their immediate family members to

compete with the shareholders they are paid to serve

unethical for any management or their immediate family members to

compete with the shareholders they are paid to serve

Ø At SandRidge, are company management and resources focused

exclusively on building shareholder value, or have they also been used

for the benefit of others, even sometimes in direct competition with the

company?

exclusively on building shareholder value, or have they also been used

for the benefit of others, even sometimes in direct competition with the

company?

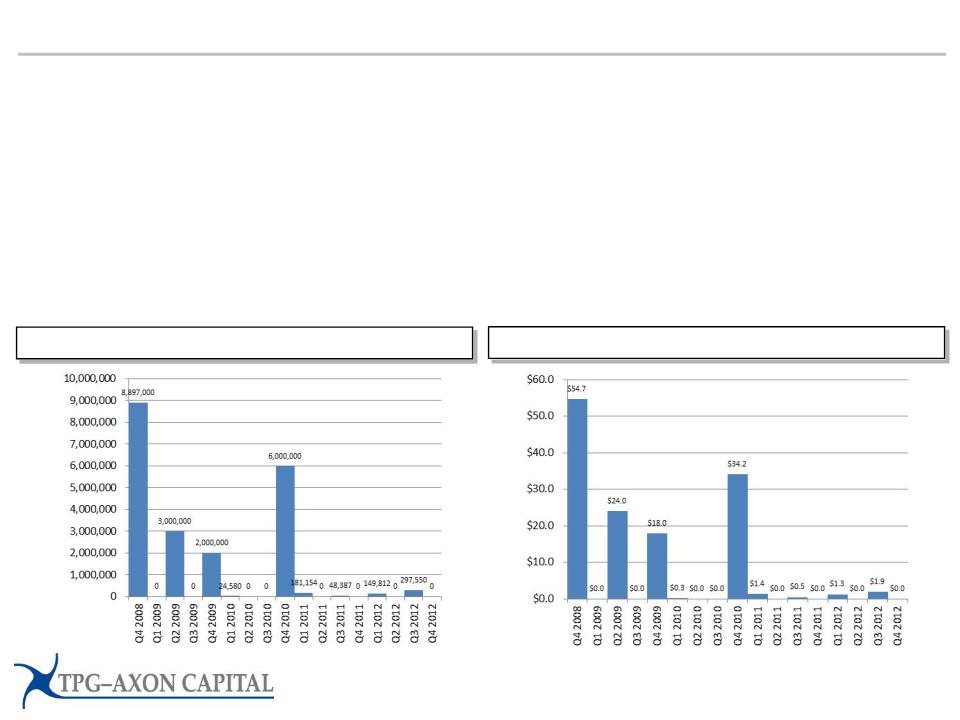

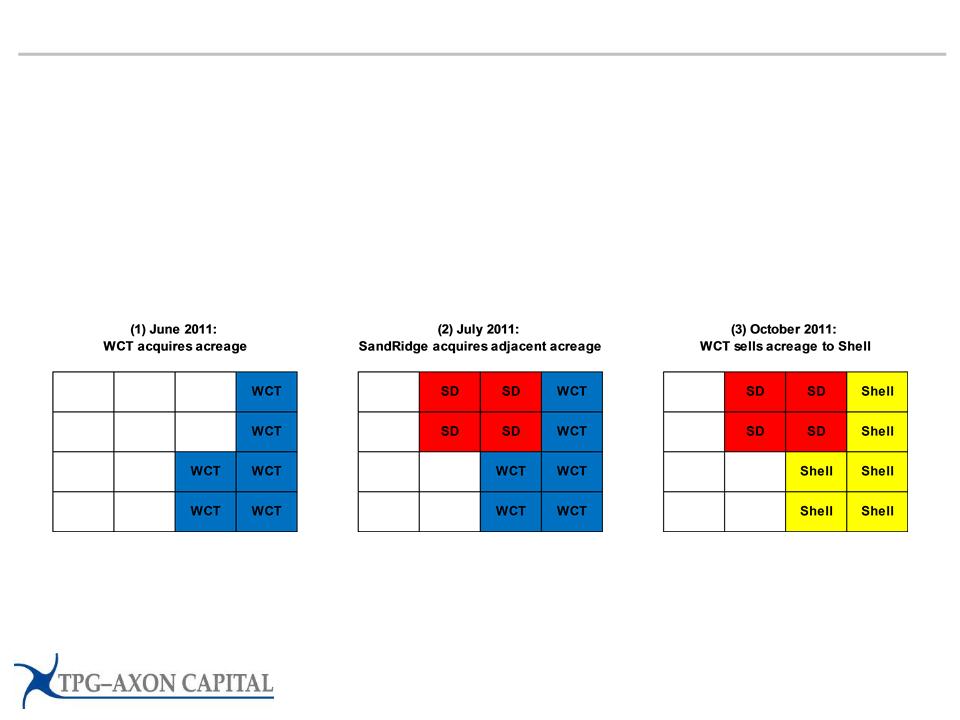

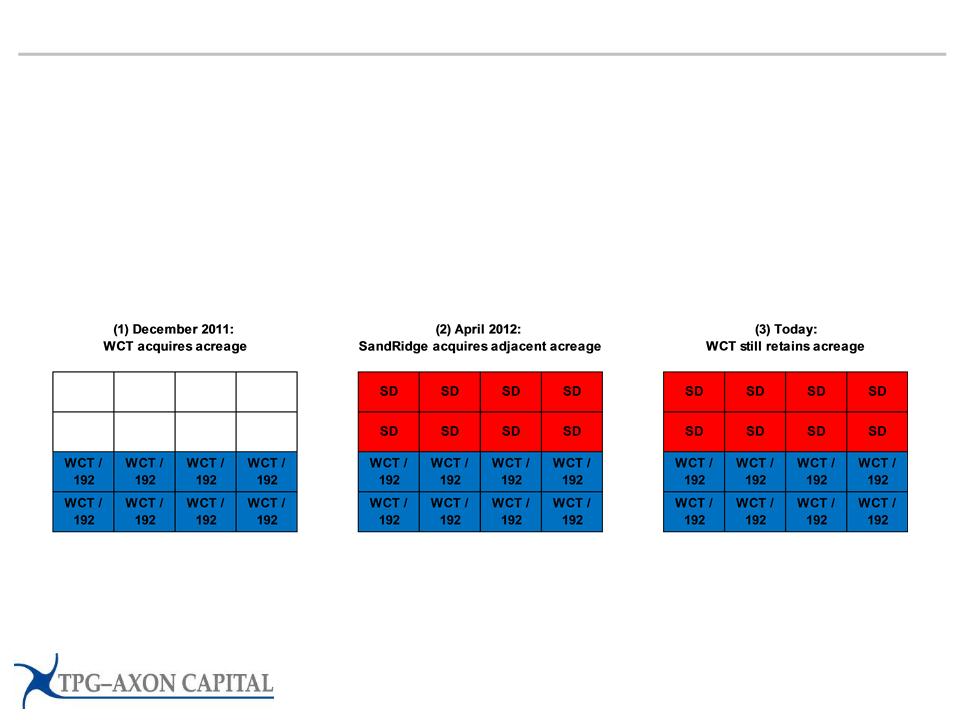

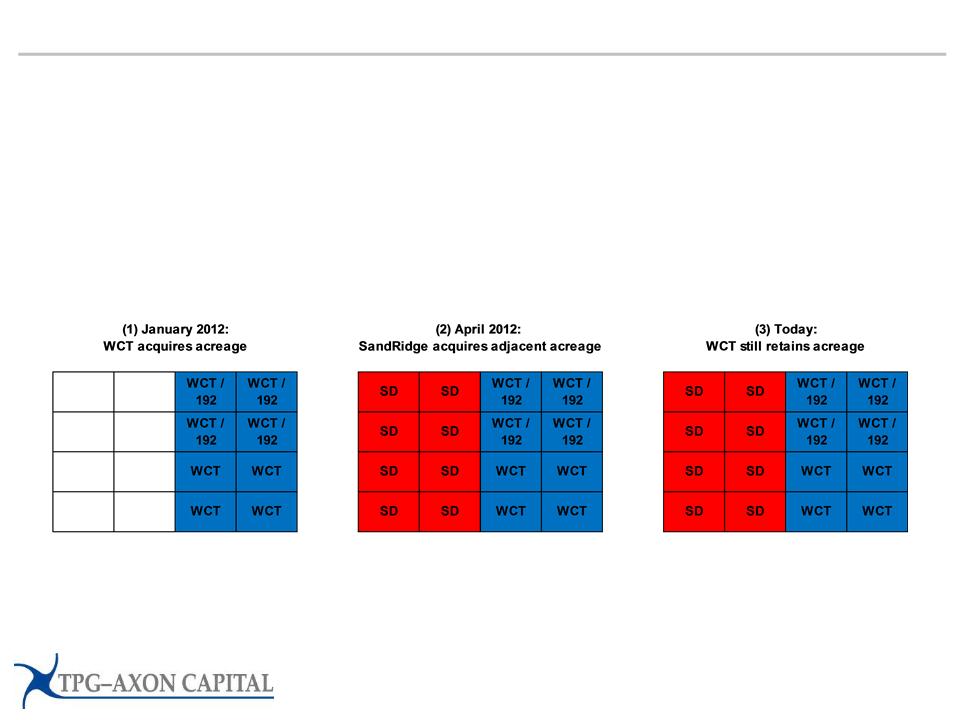

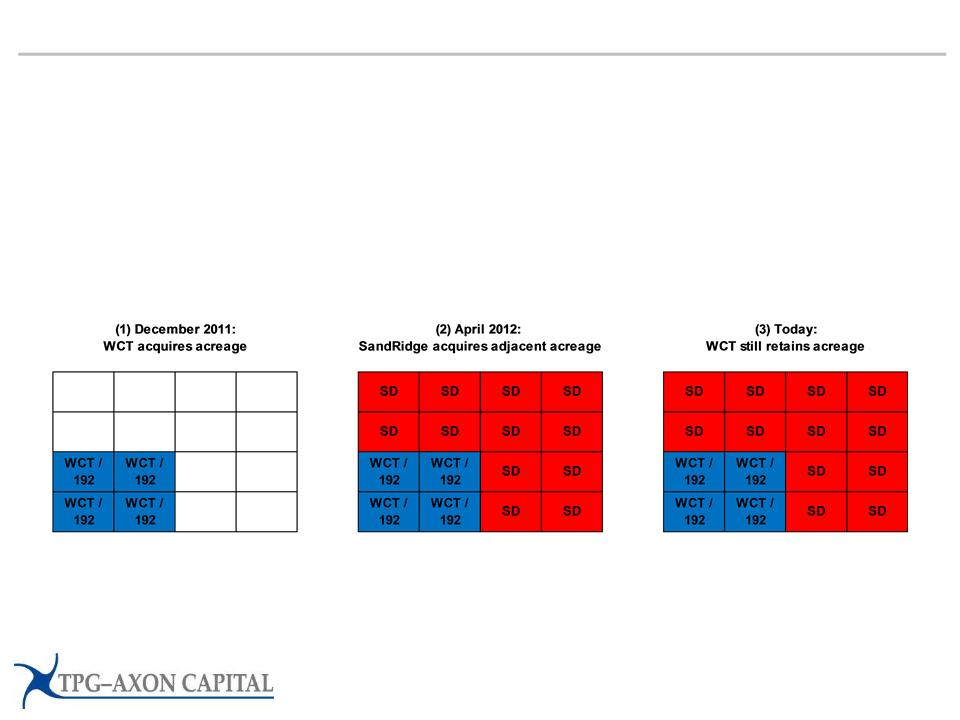

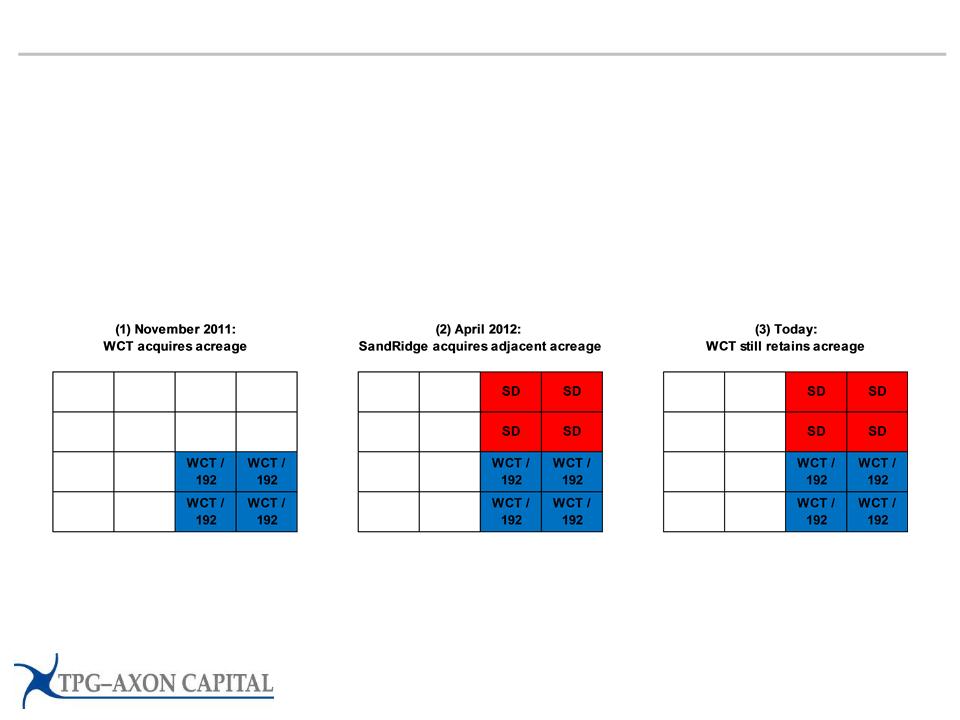

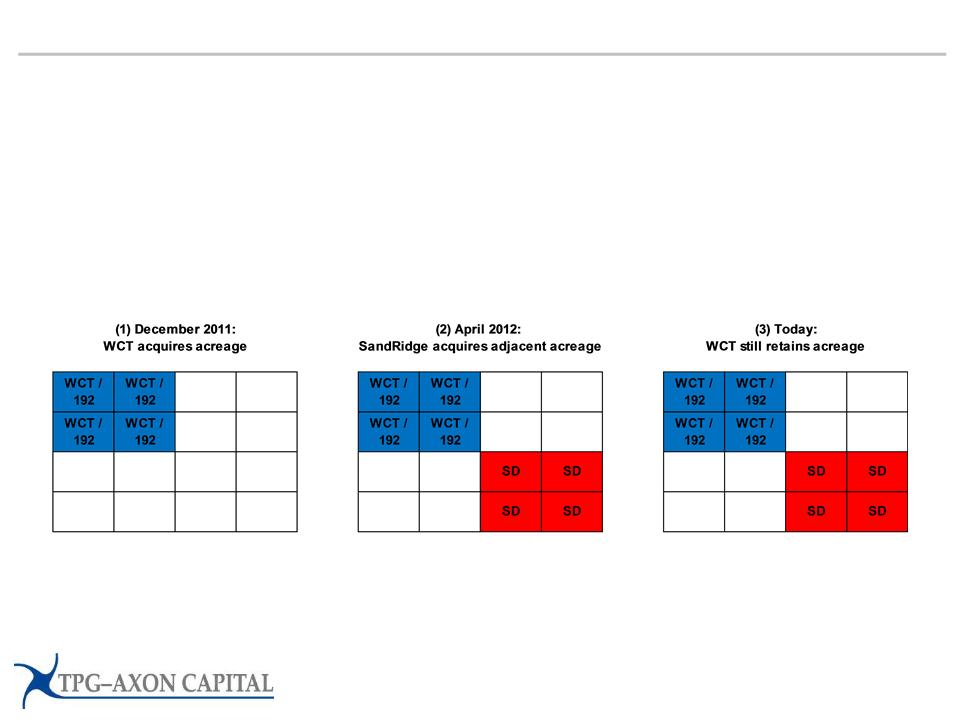

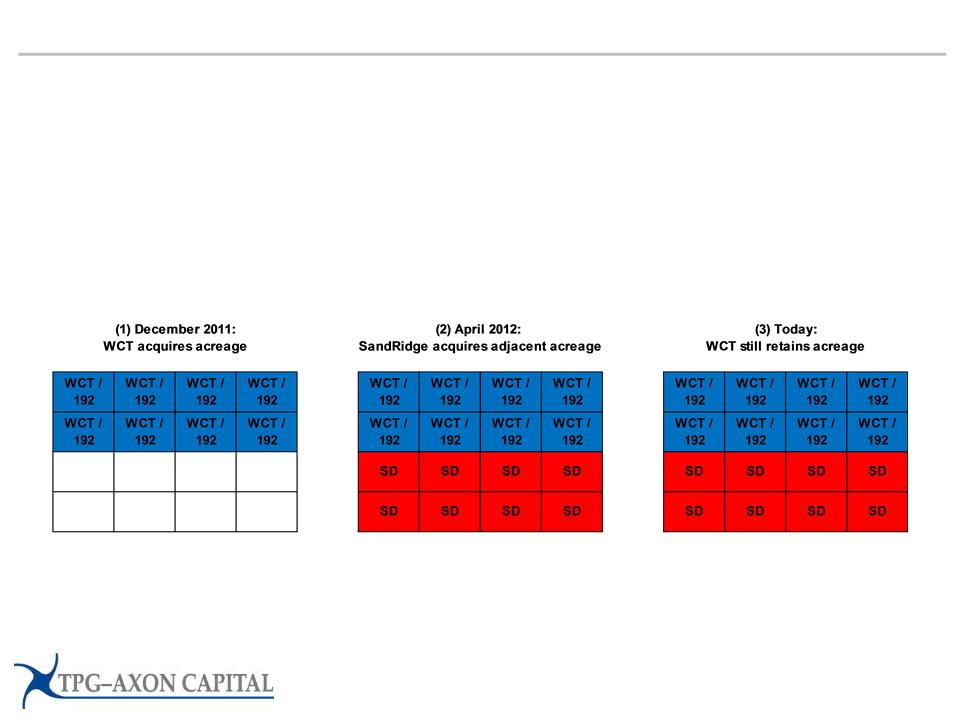

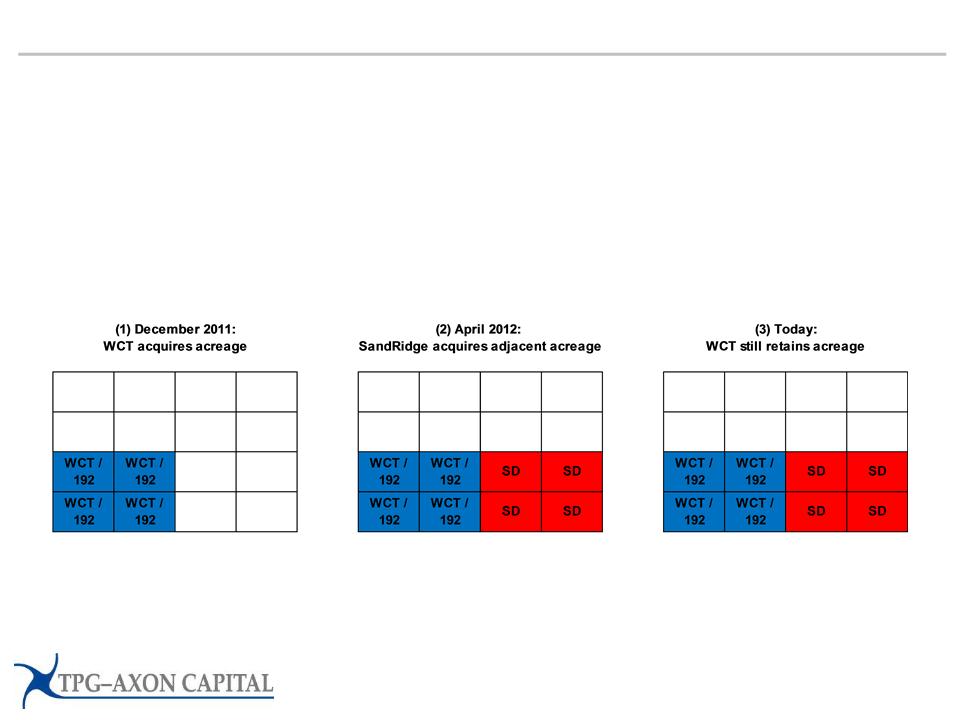

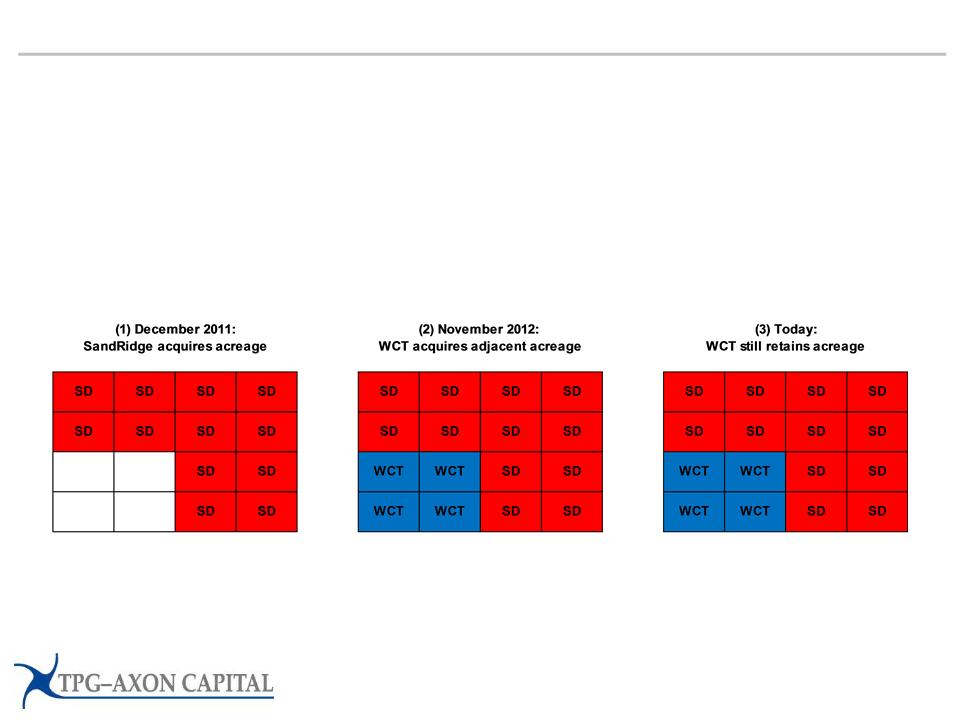

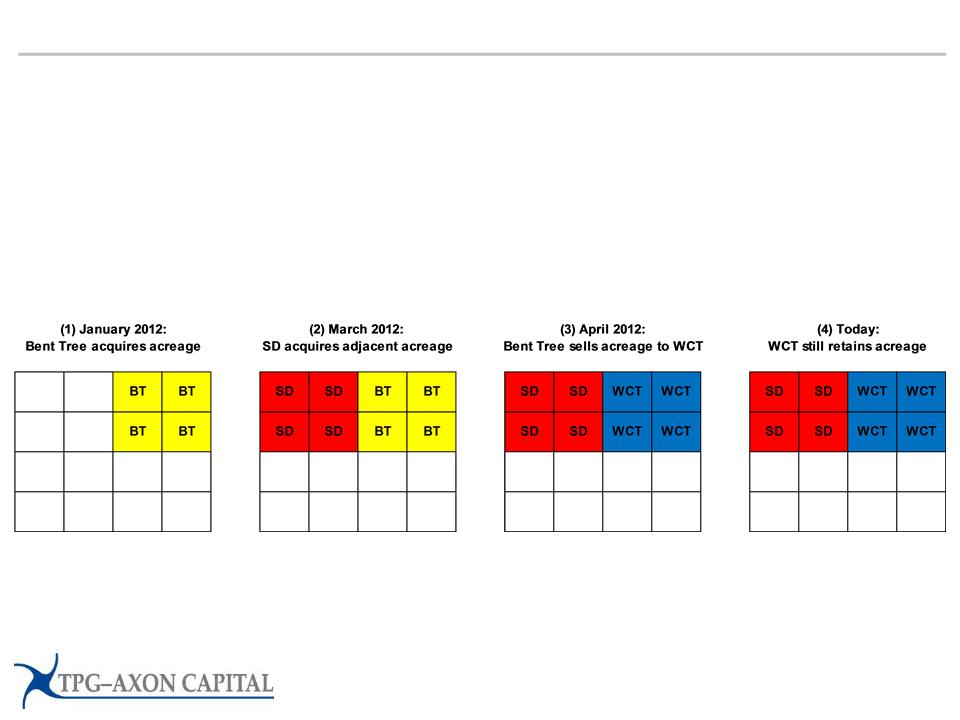

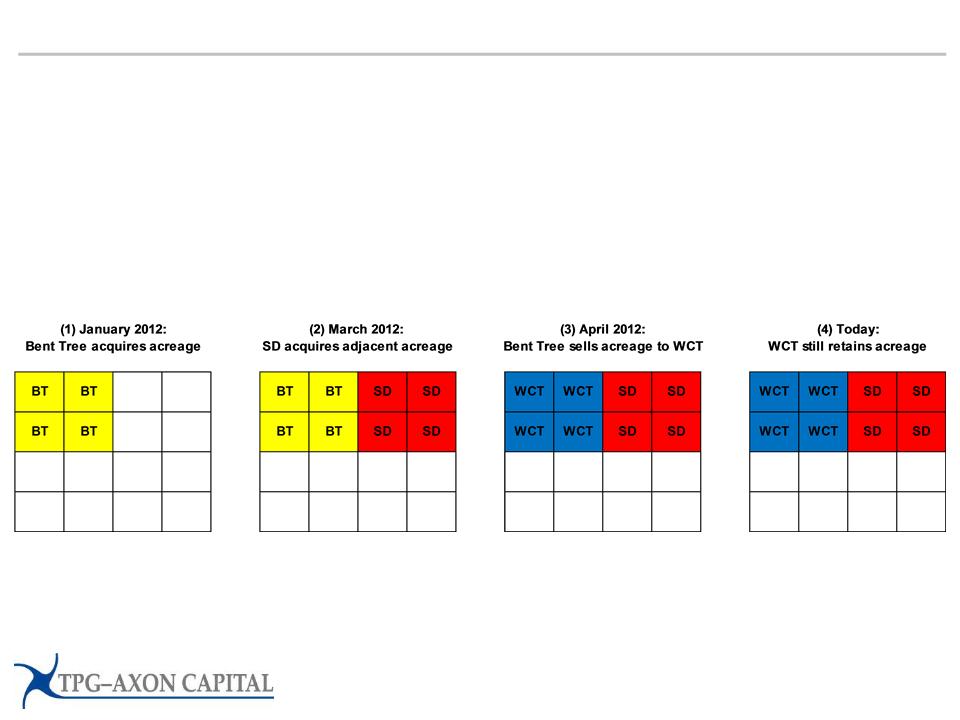

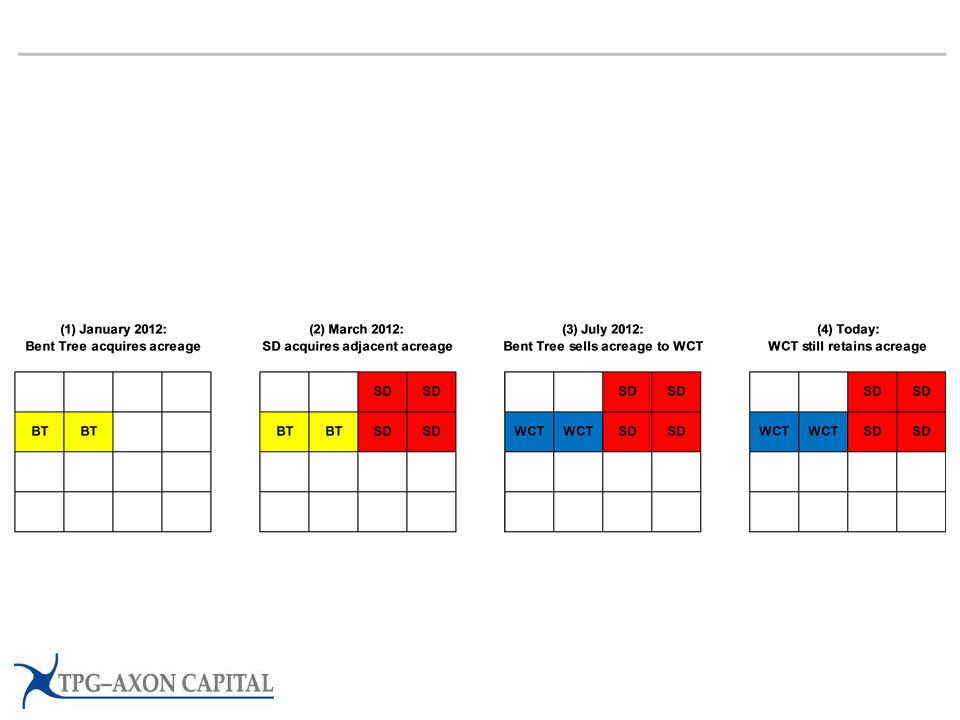

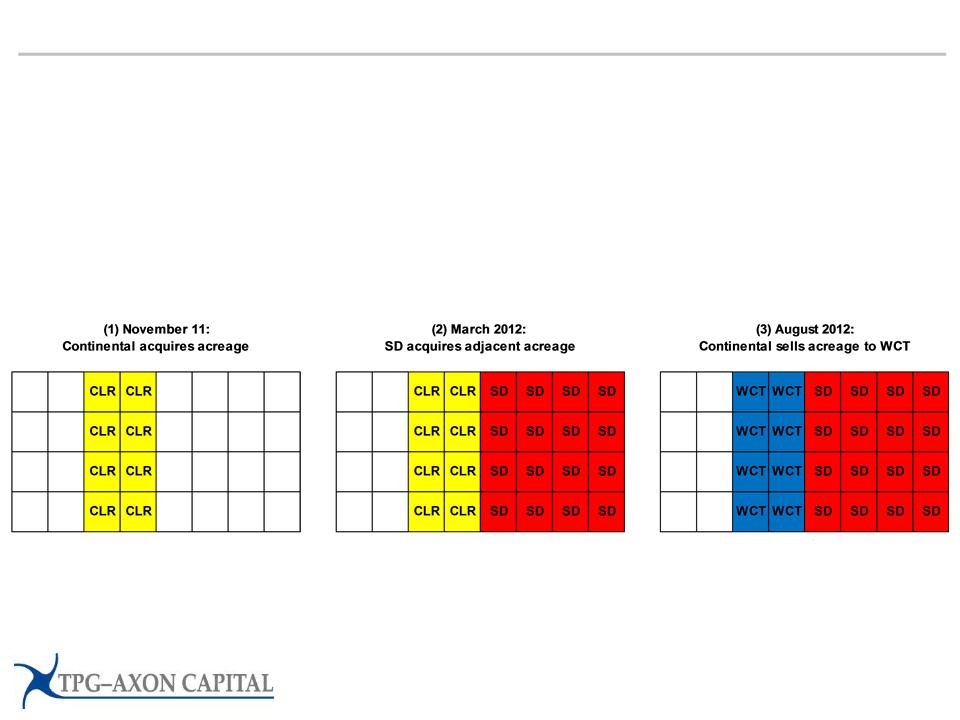

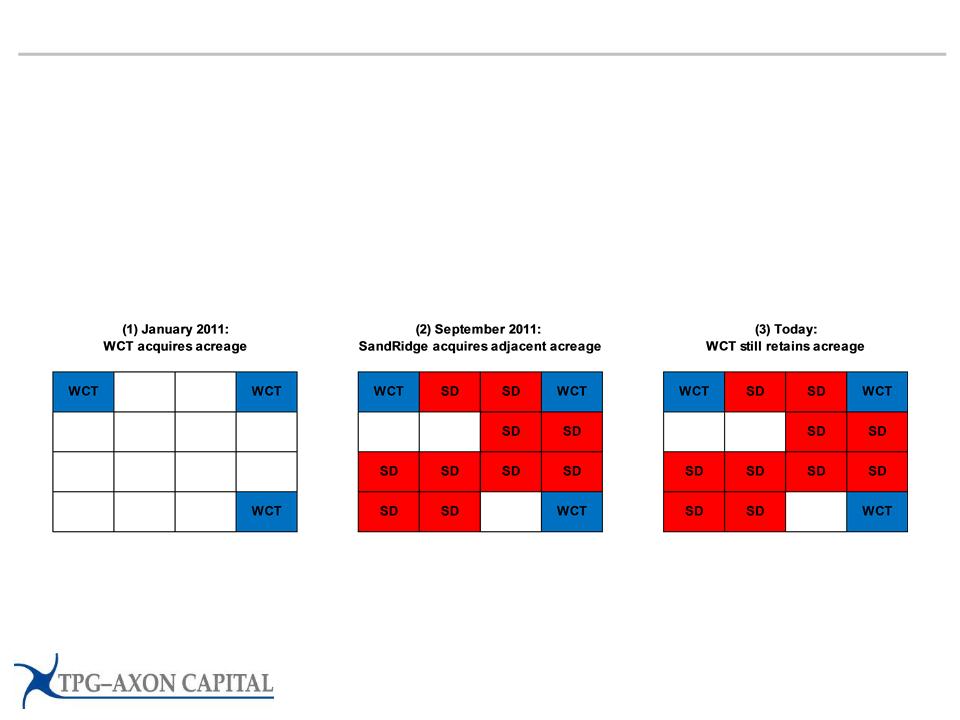

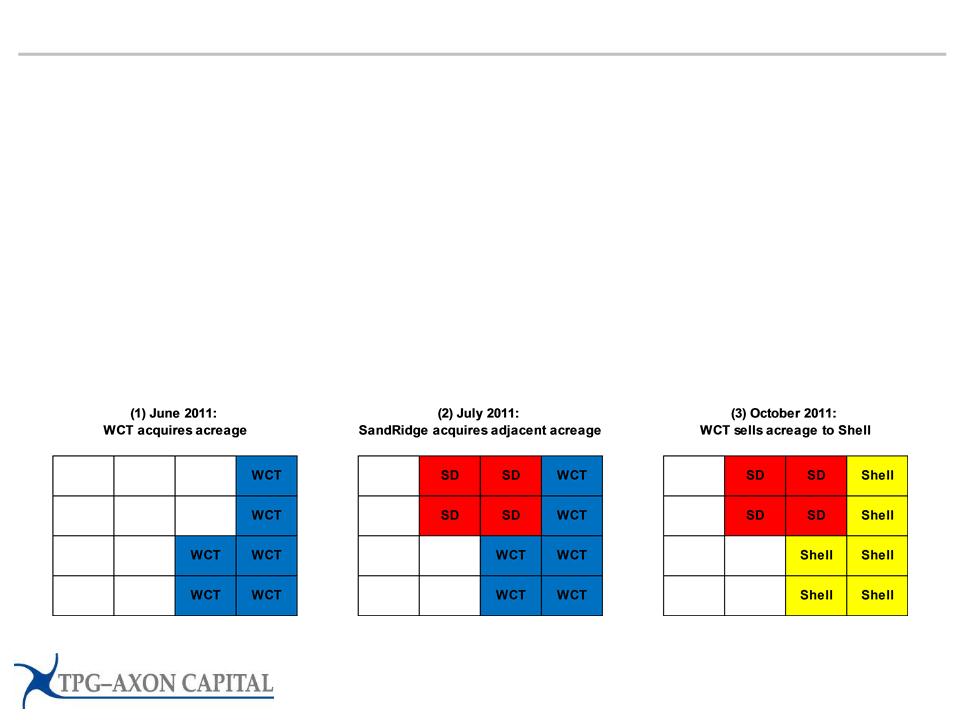

Entities related to Tom Ward have bought massive amounts of land

and mineral rights, alongside or often even in advance of, SandRidge

and mineral rights, alongside or often even in advance of, SandRidge

27

Ø Various entities controlled by trusts established by Mr. Ward, for the benefit of his children, have been

significant acquirers of land and mineral rights in the Mississippian

significant acquirers of land and mineral rights in the Mississippian

Ø The company implies these purchases are modest and coincidental; this is simply not true. These

acquisitions are vast in quantity and breadth of overlap, and extend across a majority of the relevant

counties in the Mississippian formation

acquisitions are vast in quantity and breadth of overlap, and extend across a majority of the relevant

counties in the Mississippian formation

Ø While we are still early in our analysis, from what we have seen, we believe the Ward Family has

acquired hundreds of thousands of acres, making it one of the most significant owner of mineral

rights in the Mississippian.

acquired hundreds of thousands of acres, making it one of the most significant owner of mineral

rights in the Mississippian.

Ø These acquisitions are not historical legacies; they have occurred in recent years, and appear to be

continuing.

continuing.

Ø Family controlled entities acquire land and mineral rights, often in advance of SandRidge ‘coincidentally’

developing an interest in the same area. They then either keep the rights, or sell them to third party

competitors! In some instances, they have even flipped the rights to SandRidge, just weeks or months

after acquiring them!

developing an interest in the same area. They then either keep the rights, or sell them to third party

competitors! In some instances, they have even flipped the rights to SandRidge, just weeks or months

after acquiring them!

Ø In the Appendix, we have included our original presentation from January 23, 2013. Since then, we have

uncovered additional information across many additional counties, encompassing what we believe are

hundreds of thousands of acres. We will be updating the land presentation in the near future with our

updated information

uncovered additional information across many additional counties, encompassing what we believe are

hundreds of thousands of acres. We will be updating the land presentation in the near future with our

updated information

How can this behavior be permissible?

28

Ø We believe it is unethical and appalling for a CEO or his family to be a direct competitor to the

company he is paid to serve

company he is paid to serve

Ø The conflicts of interest, and potential for misuse of information, are vast and unacceptable

Ø Presumably, the SandRidge Board of Directors agreed, which is why Tom Ward’s 2006

employment agreement prohibited him from competing with the company (including in the

accquisition of new mineral rights and land)

employment agreement prohibited him from competing with the company (including in the

accquisition of new mineral rights and land)

Ø So, how could these transactions have taken place? The company claims the entities (especially

WCT Resources as the most significant) that have acquired the land are “independent”…this is the

rationale under which the Ward Family has emerged as a major competitor to SandRidge, with the

Board’s blessing

WCT Resources as the most significant) that have acquired the land are “independent”…this is the

rationale under which the Ward Family has emerged as a major competitor to SandRidge, with the

Board’s blessing

Ø However, the Board then expanded the flexibility given Mr. Ward in an updated employment

agreement (December 2011), which gives him significantly more room to participate directly in

other competing businesses

agreement (December 2011), which gives him significantly more room to participate directly in

other competing businesses

Are these entities really “independent”?

29

Ø WCT Resources is owned by trusts established by Tom and Sch’ree Ward for the benefit of Tom

Ward’s children (Ward Children’s Trust). The trustee of Ward Children’s Trust is Scott C. Hartman,

who we believe is a SandRidge employee

Ward’s children (Ward Children’s Trust). The trustee of Ward Children’s Trust is Scott C. Hartman,

who we believe is a SandRidge employee

Ø The company states that WCT Resources is currently run by Trent Ward, Tom Ward’s son

Ø WCT Resources appears to have a fraction of the approximately 2,500 full-time employees that

SandRidge Energy does. The company’s phone voicemail lists just seven total employees in its

directory

SandRidge Energy does. The company’s phone voicemail lists just seven total employees in its

directory

Ø The address of WCT Resources was the same as SandRidge’s headquarters until last year

Ø In some prior years, based on a comparison of signatures, it appears that Tom Ward signed

company documents

company documents

Ø The current Chief Operating Officer of WCT Resources, Scott White, appears to have been a land

manager at SandRidge Energy until as recently as 2011

manager at SandRidge Energy until as recently as 2011

Ø There have been numerous transactions between Ward family members, or entities associated

with Ward family members, and WCT Resources. We have documented transactions between

TLW Cattle & Land or Sch’ree Ward, Tom Ward’s wife, and WCT Resources

with Ward family members, and WCT Resources. We have documented transactions between

TLW Cattle & Land or Sch’ree Ward, Tom Ward’s wife, and WCT Resources

Ø WCT Resources is just one of several entities controlled by members of the Ward family which

appear to be active participants in the purchase and sale of land and mineral rights in the

Mississippian

appear to be active participants in the purchase and sale of land and mineral rights in the

Mississippian

30

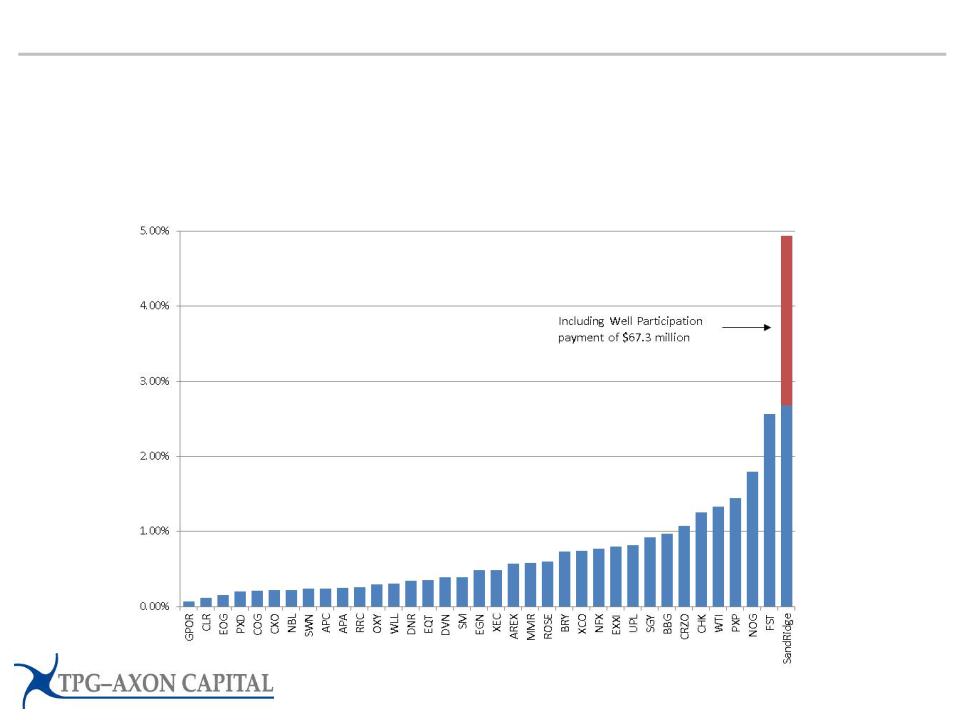

Extraordinary payments to CEO Tom Ward

Ø Despite the 80% collapse in the stock, CEO Tom Ward has received $150 million in

direct payments over the past five years, including $67 million for his interests in oil and

gas wells

direct payments over the past five years, including $67 million for his interests in oil and

gas wells

Ø Mr. Ward’s employment agreement guarantees him $18 million in annual compensation. In

2012 Mr. Ward made another $21 million, despite SandRidge stock falling 22%

2012 Mr. Ward made another $21 million, despite SandRidge stock falling 22%

Source: Bloomberg; market data as of February 6, 2013

Peers from S&P Oil & Gas index (XOP Equity)

2008 - 2011 CEO compensation, as

percentage of current market cap

percentage of current market cap

31

$67 million buyout payment to Mr. Ward at the peak of the crisis!

Ø In addition to extraordinary compensation, payments included the appalling buyout of

Mr. Ward’s oil & gas well interests in the Executive Well Participation Plan in

October 2008

Mr. Ward’s oil & gas well interests in the Executive Well Participation Plan in

October 2008

Ø The Executive Well Participation Plan allowed Tom Ward to directly participate as a

working interest owner in wells

working interest owner in wells

Ø When concerns regarding Mr. Ward’s ties to Chesapeake Energy arose this spring, Mr. Ward

repeatedly asserted to us, other shareholders, and the media that SandRidge was different

and that over time he and SandRidge recognized the inappropriateness of this practice and

eliminated it to avoid any appearance of impropriety.

repeatedly asserted to us, other shareholders, and the media that SandRidge was different

and that over time he and SandRidge recognized the inappropriateness of this practice and

eliminated it to avoid any appearance of impropriety.

Ø We investigated his claims, and were appalled by what we found. It is true that SandRidge

has eliminated their Executive Well Participation Plan, but…

has eliminated their Executive Well Participation Plan, but…

Ø …They did so by paying over $67 million to Mr. Ward, even as (1) markets were collapsing in

October 2008, and (2) the company had less than $1 million in cash and was facing a real risk

of bankruptcy.

October 2008, and (2) the company had less than $1 million in cash and was facing a real risk

of bankruptcy.

Ø Adding insult to injury, the wells that the company re-purchased from Mr. Ward were natural

gas wells, despite public proclamations by Mr. Ward and the company of the company’s the

need to abandon their natural gas focus and shift towards oil exploration and development

gas wells, despite public proclamations by Mr. Ward and the company of the company’s the

need to abandon their natural gas focus and shift towards oil exploration and development

Ø We believe the Well Participation Plan repurchase was an unconscionable indirect

transfer of wealth from stockholders to Mr. Ward

transfer of wealth from stockholders to Mr. Ward

32

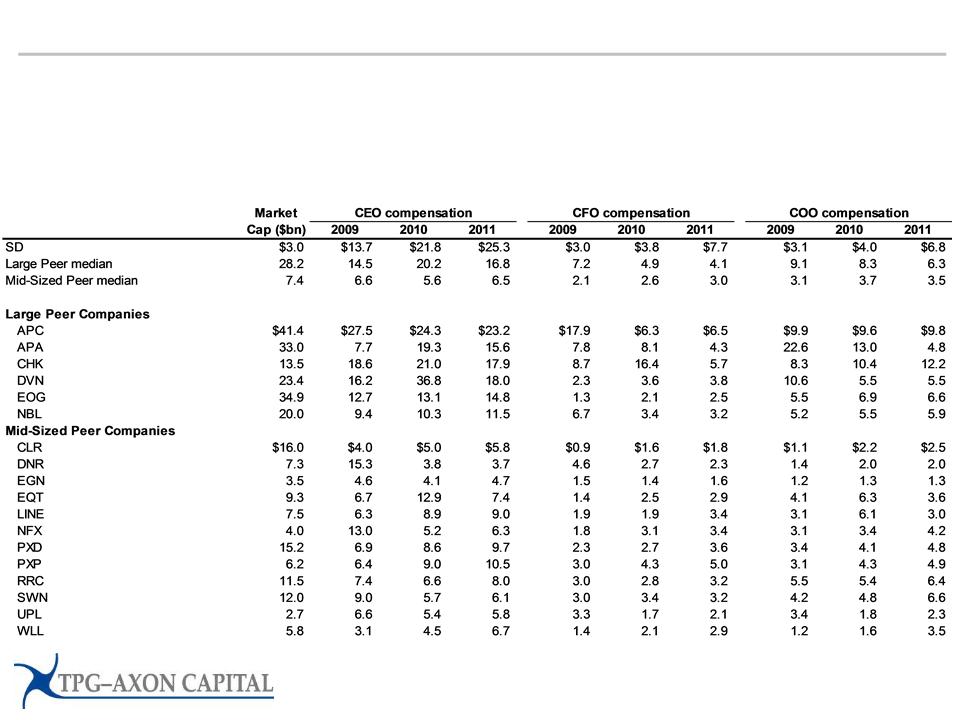

Extraordinary compensation for all top management and directors

Ø The excess compensation extends beyond Tom Ward. The COO and CFO are among the highest paid

executives of any of its peer companies, all of which have outperformed SandRidge

executives of any of its peer companies, all of which have outperformed SandRidge

Ø Even the Board is well rewarded. SandRidge directors make $360k per year. For comparison, directors at

ExxonMobil, a company 150 times larger than SandRidge, make only $285k per year.

ExxonMobil, a company 150 times larger than SandRidge, make only $285k per year.

Source: Bloomberg; market data as of February 6, 2013

Peers based on SandRidge consent revocation statement on January 18, 2013

33

Major proxy advisory services have criticized SandRidge’s excessive

compensation

compensation

ISS

Glass Lewis

Source: ISS Proxy Advisory Services (May 19, 2012);

Glass Lewis & Co (May 8, 2012); GMI Ratings (January 25, 2013)

GMI Ratings

“The rating for SandRidge Energy, Inc.

has been downgraded from D to F due

to serious concerns related to board

composition and executive

compensation”

has been downgraded from D to F due

to serious concerns related to board

composition and executive

compensation”

34

Lavish perks in addition to compensation and other payments

Ø Staggering level of perquisites, which comprise a significant drain on shareholder value

Ø SandRidge provides him with unlimited personal use of the company’s four corporate jets

Ø Mr. Ward has used the planes for frequent trips to his vacation home in Scottsdale and weekend

trips to Las Vegas, Los Angeles and the Bahamas

trips to Las Vegas, Los Angeles and the Bahamas

Ø The planes include a Falcon 900EX, one of the most expensive private business jets made

Ø SandRidge employs over 15 full time employees to maintain and fly the jets

Ø SandRidge provides support for the Oklahoma City Thunder, an NBA basketball franchise

of which Mr. Ward owns 19%

of which Mr. Ward owns 19%

Ø SandRidge pays an annual $3.3 million sponsorship fee and licenses a suite for $0.2 million per

year

year

Ø And when Mr. Ward doesn’t use his tickets, he sells them to the company! SandRidge paid him

$0.3 million for tickets in 2012

$0.3 million for tickets in 2012

Ø SandRidge spends almost $1 million per year to provide personal accounting services to

Mr. Ward

Mr. Ward

35

SandRidge Board of Directors

Ø Current directors have overseen the value destruction since SandRidge’s IPO - most

have been there for the entire time!

have been there for the entire time!

Ø William Gilliland, Daniel Jordan, Roy Oliver and Jeffrey Serota have been Board

members since the IPO

members since the IPO

Ø Everett Dobson joined in 2010, Jim Brewer in 2011

Ø Many directors have personal ties to CEO Tom Ward or have conducted personal

transactions with SandRidge

transactions with SandRidge

Ø Everett Dobson owns 3.8% of the Oklahoma City Thunder alongside Tom Ward

Ø Roy Oliver leases real estate to SandRidge and has co-invested alongside Tom Ward in

his personal investments

his personal investments

Ø Dan Jordan was a former senior executive at Riata Energy, the predecessor to

SandRidge. He has sold at least $12 million of personal assets to SandRidge in 2006 and

2007

SandRidge. He has sold at least $12 million of personal assets to SandRidge in 2006 and

2007

Ø Only one director has experience as a director of a major publicly-traded company

Source: SandRidge filings

36

The Board’s Response…

Ø SandRidge’s response to our process has been to take actions that serve to entrench

themselves

themselves

Ø A poison pill was adopted to prevent investors from accumulating more than 10% of the

shares

shares

Ø The bylaws were amended to require a vote of more than 50% of outstanding shares,

instead of the previous requirement of a majority of those shares voting

instead of the previous requirement of a majority of those shares voting

Ø SandRidge attempted to manipulate the 60-day consent solicitation period to reduce the

amount of time stockholders would have to cast their votes

amount of time stockholders would have to cast their votes

Ø SandRidge also declared that Mr. Ward’s compensation would be over $20 million for

2012

2012

37

Agenda

Ø Overview

Ø Company Background & Performance

Ø Management Compensation & Related Party Transactions

Ø The Path to Value

Ø Company Response

Ø Appendix: Related Party Transactions Presentation

38

Significant asset value remains!

Ø Despite the massive destruction of shareholder value under current management,

significant asset value remains. We believe SandRidge shares are dramatically

undervalued, as long as the Mississippian Lime can be sensibly developed

significant asset value remains. We believe SandRidge shares are dramatically

undervalued, as long as the Mississippian Lime can be sensibly developed

Source: Analyst reports, Bloomberg; market data as of February 6, 2013

Upside to Analyst NAVs

39

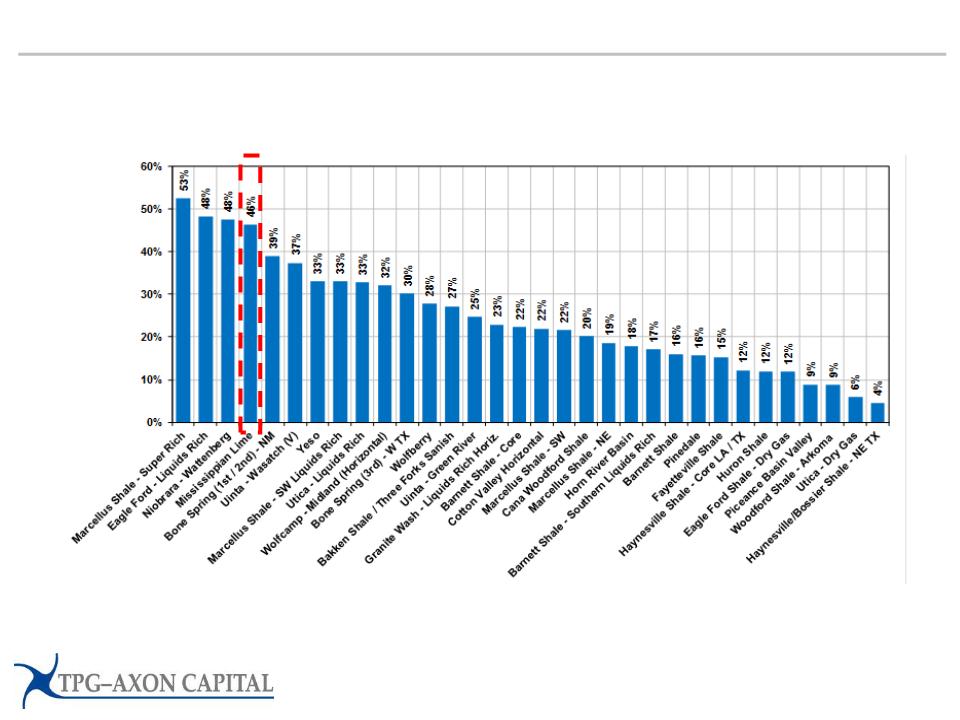

…if the Mississippian Lime can be sensibly developed

Ø The Mississippian Lime remains one of the highest return plays in the US, and will be

economic to develop under most reasonable commodity price scenarios

economic to develop under most reasonable commodity price scenarios

Source: Credit Suisse; January 2, 2013

Based on NYMEX futures, using $85.26 WTI oil and $4.68 Henry Hub gas

40

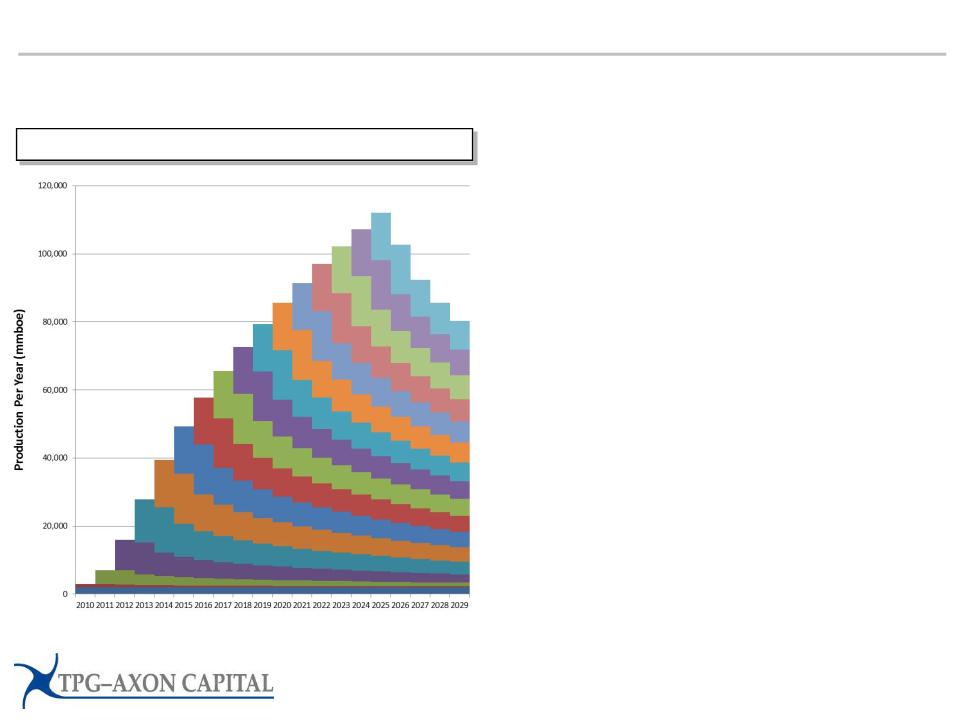

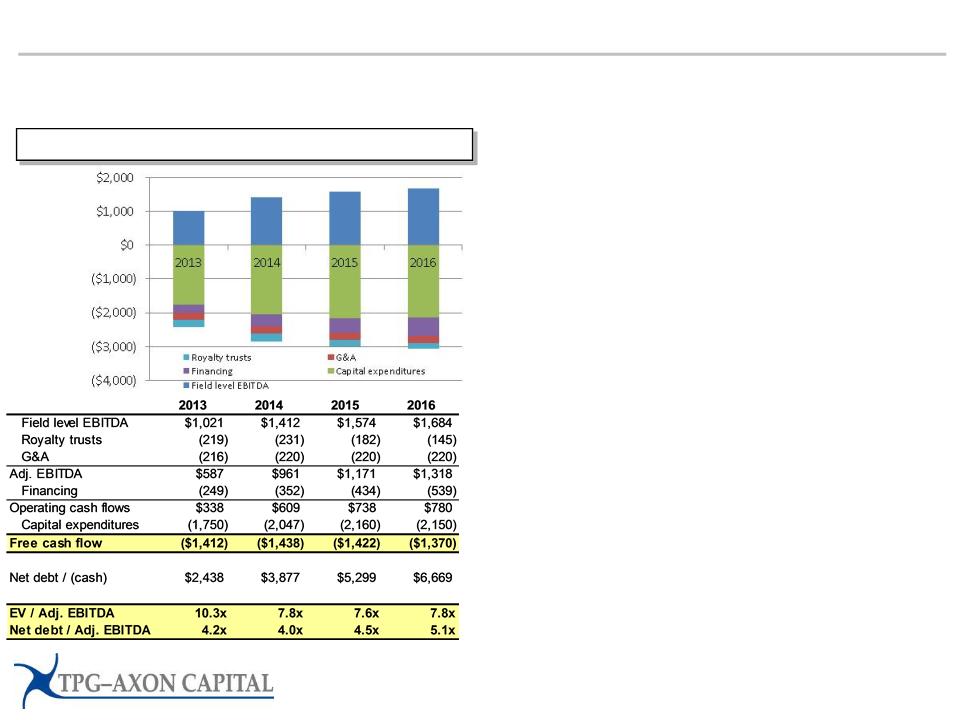

The Mississippian Lime is a growth asset

Ø SandRidge’s position in the Mississippian Lime is large, scalable and repeatable, with

significant development potential

significant development potential

Source: TPG-Axon analysis.

Assumes 40 gross rigs, 16 wells per rig-year, 65% working interest, 422 Mboe type curve

Mississippian Production

Ø With decades of drilling inventory, we

anticipate SandRidge’s production in

the Mississippian will continue to grow

anticipate SandRidge’s production in

the Mississippian will continue to grow

Ø The chart on the left shows

SandRidge’s Mississippian production

over time. The colors represent

production from wells drilled in different

years, with the height of each “stack”

representing production in a specific

calendar year

SandRidge’s Mississippian production

over time. The colors represent

production from wells drilled in different

years, with the height of each “stack”

representing production in a specific

calendar year

Ø We expect SandRidge’s capital

efficiency will improve over time, as it

“stacks” production and gains scale

efficiency will improve over time, as it

“stacks” production and gains scale

41

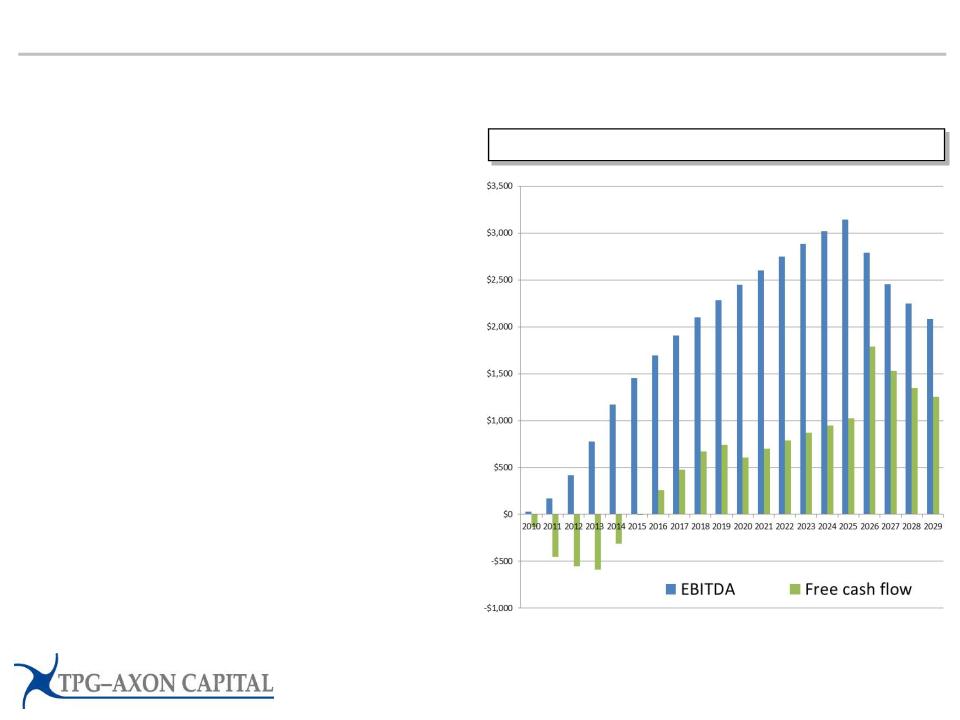

Asset value is highly dependent on costs and spending

Ø The key, as with any development, is minimizing the period of cash outflows and

lowering the cost of capital

lowering the cost of capital

Source: TPG-Axon analysis. Field level, before overhead and financing costs

Assumes 40 gross rigs, 16 wells per rig-year, 65% working interest, $3.25 million well

costs, $90 WTI oil, $4.50 Henry Hub, 422 Mboe type curve

costs, $90 WTI oil, $4.50 Henry Hub, 422 Mboe type curve

Mississippian Cash Flows

Ø The chart on the right shows estimated

SandRidge Mississippian cash flows in

future years. The cash flows are field

level, before overhead and financing

costs

SandRidge Mississippian cash flows in

future years. The cash flows are field

level, before overhead and financing

costs

Ø The present value of these

Mississippian cash flows could be

substantial for an efficient, well

capitalized company

Mississippian cash flows could be

substantial for an efficient, well

capitalized company

42

Free cash flow breakeven

Ø The type curve revision on the Q3 2012 call highlighted a problem: with lower growth

from its core asset, free cash flow breakeven was pushed out by at least a year…The

Mississippian is a solid asset, but was previously overestimated by management

from its core asset, free cash flow breakeven was pushed out by at least a year…The

Mississippian is a solid asset, but was previously overestimated by management

Source: TPG-Axon analysis. Field level, before overhead and financing costs

Assumes 40 gross rigs, 16 wells per rig-year, 65% working interest, $3.25 million well costs,

$90 WTI oil, $4.50 Henry Hub

$90 WTI oil, $4.50 Henry Hub

Old Type Curve, before Q3 call

New Type Curve, after Q3 call

456 mmboe, 45% oil

422 mmboe, 37% oil

2014 breakeven

2015 breakeven

43

What is the problem?

Ø Despite owning a valuable Mississippian asset, without change we fear shareholder

value will continue to be destroyed!

value will continue to be destroyed!

Source: TPG-Axon analysis. Based on forward curve on February 6, 2013.

Pro forma for Permian sale, with proceeds used to pay down debt and fund future capex.

Assumes current cost structure, no joint ventures and no further asset sales.

Assumes current cost structure, no joint ventures and no further asset sales.

Status Quo

Ø Attractive field level economics are

burdened by massive overhead and

financing costs, each and every year

burdened by massive overhead and

financing costs, each and every year

Ø Without restructuring, the debt-adjusted

cash flow growth is unattractive. Debt,

and the associated interest expense,

grows faster than Mississippian cash

flows

cash flow growth is unattractive. Debt,

and the associated interest expense,

grows faster than Mississippian cash

flows

44

What can be done?

Restructure both

the Board of

Directors and

management team

the Board of

Directors and

management team

Drastically

reduce overhead

and waste

reduce overhead

and waste

Reduce future

funding needs

funding needs

Sell Extraneous

Assets

Assets

þ

þ

þ

þ

45

What can be done?

ü The current Board has presided over a remarkable

destruction of value, and the transfer of wealth from

the company to Mr. Ward and entities associated

with Mr. Ward’s immediate family

destruction of value, and the transfer of wealth from

the company to Mr. Ward and entities associated

with Mr. Ward’s immediate family

ü They must be replaced with directors with proven

records of strong corporate governance and true

independence from the company

records of strong corporate governance and true

independence from the company

ü Without dramatic changes at the top, we do not

believe the company can restore the confidence of

the capital markets (necessary to reduce cost of

capital) or seriously address profligacy in expenses

believe the company can restore the confidence of

the capital markets (necessary to reduce cost of

capital) or seriously address profligacy in expenses

ü Our consent solicitation is the first step

• Amend bylaws to, among other things, de-stagger Board of

Directors and provide that directors can be removed with or

without cause

Directors and provide that directors can be removed with or

without cause

• Remove existing Board members

• Elect independent Nominees

ü Replacing CEO Tom Ward would be the second step

• We have actively engaged an executive search firm to search for

a replacement. There is significant interest in the position

a replacement. There is significant interest in the position

Restructure both

the Board of

Directors and

management team

the Board of

Directors and

management team

þ

46

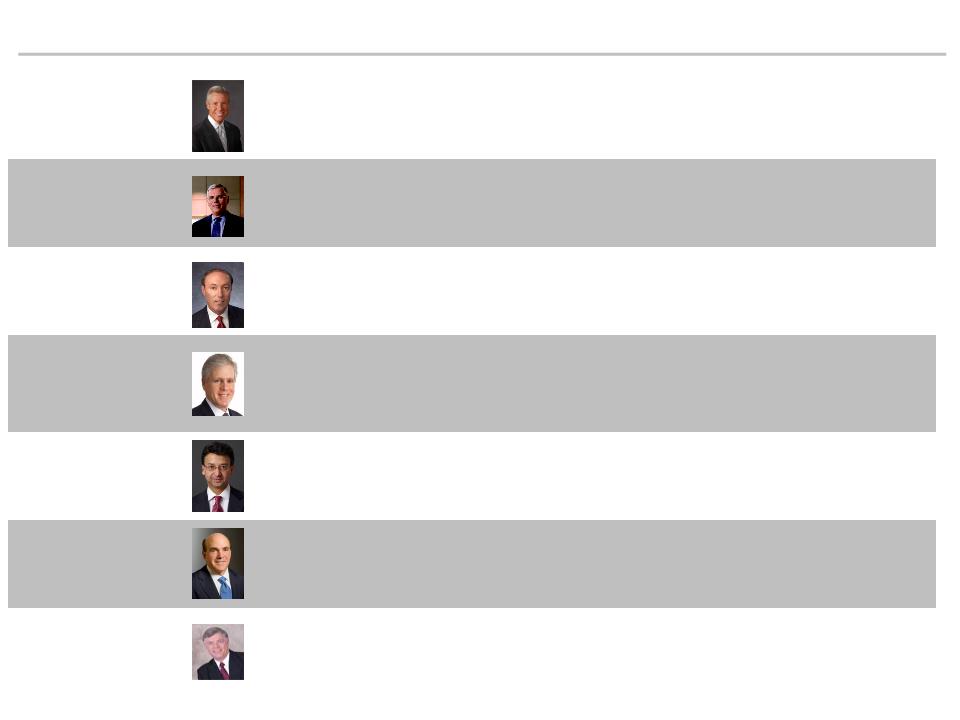

Independent Nominees

Stephen C. Beasley | Ø Former President of El Paso Eastern Pipeline Group (1987-2007) Ø CEO of Eaton Group, privately held consultancy (2008 - current) Ø Director of BPZ Resources (BPZ, 2009 - current), Williams Pipeline Partners (WMZ, 2007-2009) and Southern Union (SUG, 2009) | |

Edward W. Moneypenny | Ø Former CFO of Oryx Energy (1988-1999), the legacy Sunoco E&P sold to Kerr McGee in 1999 Ø Former CFO of Florida Progress (1999-2000), Covanta Energy (2001) and 7-Eleven (2002-2006) Ø Director of New York & Company (NWY, 2006-2012) and Timberland (TBL, 2005-2011) | |

Fredric G. Reynolds | Ø Former CFO of CBS Corporation (1994-2009) Ø Director of Kraft Foods (MDLZ, 2007 - current) and AOL (AOL, 2009 - current) | |

Peter H. Rothschild | Ø CEO of Daroth Capital Advisors (2002 - current) Ø Former Managing Director at Drexel Burnham Lambert (1984-1990), Bear Stearns (1990-1996), and Wasserstein Perella (1996-2001) Ø Director of Wendy’s (WEN, 2006-2008 and 2010 - current) and CIFC Corp (DFR, 2004 - 2011) | |

Dinakar Singh | Ø Founder of TPG-Axon Capital (2004 - current) Ø Former partner and co-head of Principal Strategies at Goldman Sachs (1990 - 2004) | |

Alan J. Weber | Ø Former CEO of US Trust (2002-2005) Ø Former Vice Chairman and CFO of Aetna (1998-2001) Ø Former senior banker at Citicorp (1971-1998) Ø Director of Broadridge Financial (BR, 2005 - current) and Diebold (DBD, 2007 - current) | |

Dan A. Westbrook | Ø Former senior executive at BP (1999 - 2005) and Amoco (1986 - 1999), with responsibility for operations in China (2001 - 2005), Argentina (1999 - 2001), North Sea / Africa / Middle East (1997 - 1999) and Russia (1994 - 1997) Ø Director of Ivanhoe Mines (IVN, 2010-2012), Synenco Energy (SYN, 2007-2008) and Enbridge Energy (general partner of EEP, 2007 - current) |

47

Independent Nominees

SandRidge Director Criteria | “Significant senior management experience” | “Experience overseeing public company financial management matters” | “Substantial experience in varied facets of the oil and natural gas industry” | “A background in investing and capital raising” |

Stephen C. Beasley | Former President of El Paso Eastern Pipeline Group | Director of BPZ Resources (audit, chair compensation), Williams Pipeline Partners (audit, chair conflicts) and Southern Union | Midstream experience at El Paso, Williams and Southern Union. Upstream experience at BPZ Resources | CEO of Eaton Group, experience as senior executive and Director |

Edward W. Moneypenny | Former CFO of Oryx Energy, Florida Progress, Covanta Energy and 7-Eleven | Director of New York & Company (audit) and Timberland (chair audit); Certified Public Accountant | CFO of Oryx Energy (1988-1999), the legacy Sunoco E&P sold to Kerr McGee in 1999 | Experience as CFO and Director |

Fredric G. Reynolds | Former CFO of CBS Corporation | Director of Kraft Foods (chair audit) and AOL (audit, chair executive committee); Certified Public Accountant | Experience as CFO and Director | |

Peter H. Rothschild | CEO of Daroth Capital Advisors | Director of Wendy’s (audit) and CIFC Corp (former Chairman) | Energy investment banker | CEO of Daroth Capital Advisors, Former Managing Director at Drexel Burnham Lambert, Bear Stearns, and Wasserstein Perella |

Dinakar Singh | Founder and President of TPG-Axon Capital | 20 years of investing experience in the oil & gas industry | Founder of TPG-Axon Capital, Former partner and co-head of Principal Strategies at Goldman Sachs | |

Alan J. Weber | Former CEO of US Trust, Vice Chairman and CFO of Aetna | Director of Broadridge Financial (audit, chair compensation) and Diebold (audit, chair investment) | Former senior banker at Citicorp, CEO of Weber Group | |

Dan A. Westbrook | Former senior executive at BP and Amoco | Director of Ivanhoe Mines (chair SH&E), Synenco Energy (chair strategic review) and Enbridge Energy | Responsibility for upstream operations in China (2001 - 2005), Argentina (1999 - 2001), North Sea / Africa / Middle East (1997 - 1999) and Russia (1994 - 1997) | Experience as senior executive and Director |

48

What can be done?

ü We believe it would be not just possible, but

necessary, to reduce overhead by up to 75%

necessary, to reduce overhead by up to 75%

• Compensation for remaining employees should be reduced to

sensible levels

sensible levels

• Extraneous assets should be sold: planes, buildings, etc.

• Extraneous expenses should be terminated: personal services

payments, advertising, luxury suites, etc.

payments, advertising, luxury suites, etc.

ü Seek to emerge as one of the leanest and

most efficient companies in the industry, in

keeping with the focused and concentrated

nature of its assets

most efficient companies in the industry, in

keeping with the focused and concentrated

nature of its assets

• If SandRidge had peer-average G&A, overhead could be

reduced by ~60%, from $220 million to $90 million. As a

focused company, with a single asset within driving distance of

Oklahoma City, SandRidge should be able to drive costs even

lower

reduced by ~60%, from $220 million to $90 million. As a

focused company, with a single asset within driving distance of

Oklahoma City, SandRidge should be able to drive costs even

lower

• As recently as 2009, G&A expenses were $100 million. The

increases since then include at least $22 million more for senior

executive compensation, $15 million more for legal and

consulting expenses, and $4 million more for advertising

increases since then include at least $22 million more for senior

executive compensation, $15 million more for legal and

consulting expenses, and $4 million more for advertising

• SandRidge has approximately 700 employees in Oklahoma

City, up from 335 HQ employees at the time of the IPO. We

note that while overall headcount has stayed stable at

approximately 2,500 employees, the headquarters headcount

has doubled - this increase in staffing at the company’s HQ has

been all corporate overhead!

City, up from 335 HQ employees at the time of the IPO. We

note that while overall headcount has stayed stable at

approximately 2,500 employees, the headquarters headcount

has doubled - this increase in staffing at the company’s HQ has

been all corporate overhead!

Drastically

reduce overhead

and waste

reduce overhead

and waste

ü The company should

dramatically reduce the

extravagance and waste that

has led to extraordinary levels

of overhead for the company

dramatically reduce the

extravagance and waste that

has led to extraordinary levels

of overhead for the company

þ

Source: SandRidge filings

49

What can be done?

ü Sell Dynamic Offshore

• We believe the Dynamic Offshore assets were a

mistake to have acquired, and make little sense for

the company to keep

mistake to have acquired, and make little sense for

the company to keep

• Sadly, while we do not believe the company can

recover what it paid for the assets, it is best to recover

what is possible now and move on

recover what it paid for the assets, it is best to recover

what is possible now and move on

ü Use the proceeds to improve the balance

sheet and funding needs, as opposed to

engage in further acquisitions

sheet and funding needs, as opposed to

engage in further acquisitions

ü Consider a sale of the company

• While we do not believe a sale of the company is

required to create significant value for shareholders,

we believe it is an option that the Board should

carefully consider

required to create significant value for shareholders,

we believe it is an option that the Board should

carefully consider

• The value of the Mississippian is extraordinary, but

so is the investment and time required to developed

those assets

so is the investment and time required to developed

those assets

• The assets may be worth the most to a company with

the cheapest cost of capital, and potentially significant

synergies

the cheapest cost of capital, and potentially significant

synergies

Sell

extraneous

assets

extraneous

assets

ü The company should both

unlock value, and improve

balance sheet and funding

needs, by selling non-core

assets

unlock value, and improve

balance sheet and funding

needs, by selling non-core

assets

þ

50

What can be done?

ü Monetize Mississippian acreage

• The company should seek to monetize a significant portion of

its undeveloped Mississippian acreage, either through a sale or

additional joint venture

its undeveloped Mississippian acreage, either through a sale or

additional joint venture

• It does not add value to have acreage we cannot efficiently

develop…if we bite off more than we can chew, stockholder value

is choked by spiraling debt and interest expense

develop…if we bite off more than we can chew, stockholder value

is choked by spiraling debt and interest expense

ü Consider monetization of water disposal

infrastructure

infrastructure

• The company should consider monetizing its water disposal

system, either through a sale to an infrastructure investor or as a

publicly traded MLP

system, either through a sale to an infrastructure investor or as a

publicly traded MLP

• Monetizing the water disposal system would: (1) provide an

efficient way of financing Mississippian development; (2) reduce

future funding requirements; and (3) support the growth of third

party volumes to leverage the existing system

efficient way of financing Mississippian development; (2) reduce

future funding requirements; and (3) support the growth of third

party volumes to leverage the existing system

• However, we recognize it is important for SandRidge to retain

control of this core asset

control of this core asset

Reduce future

funding needs

funding needs

ü Ownership in the Mississippian

should be of a size that the

company can develop

economically and efficiently

using its own balance sheet

and cash flow

should be of a size that the

company can develop

economically and efficiently

using its own balance sheet

and cash flow

þ

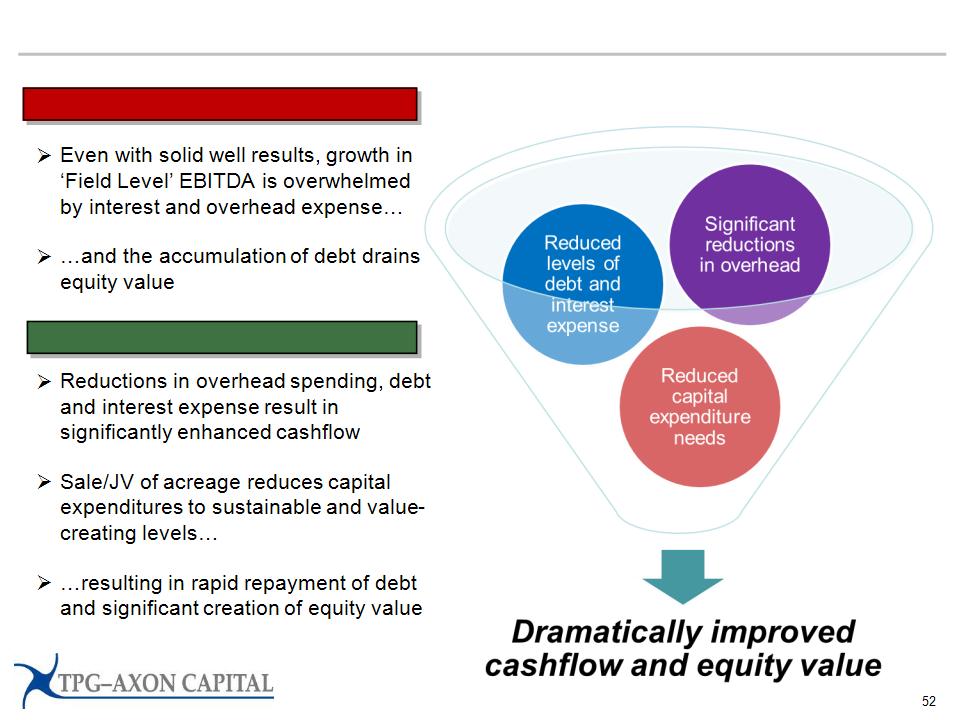

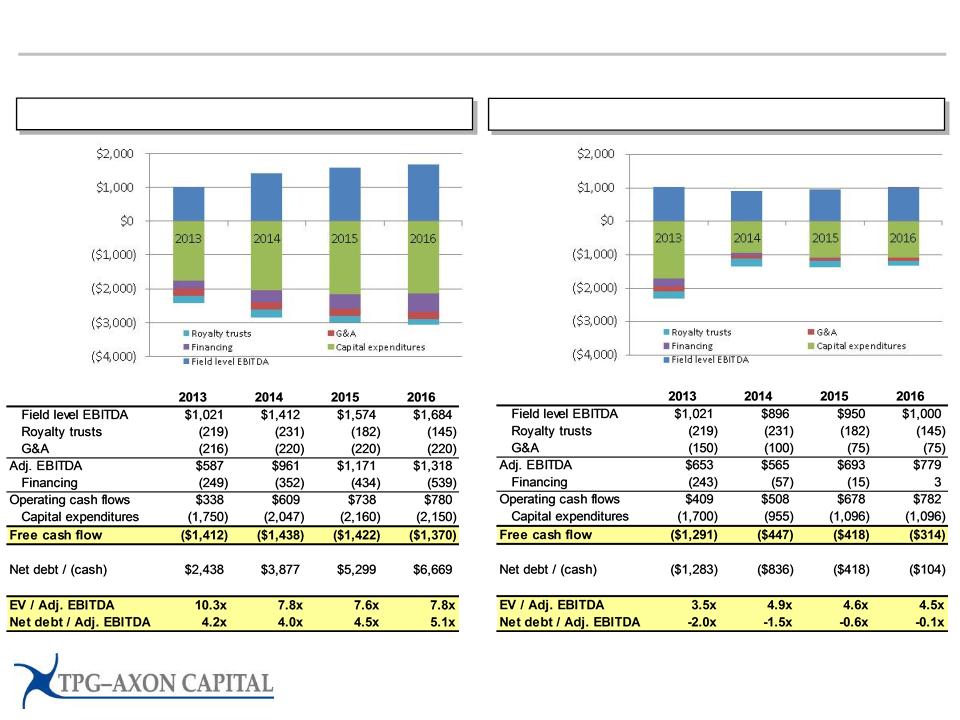

Restructuring is necessary… but can create significant value

Status Quo

TPG-Axon Plan

52

TPG-Axon plan - modeling assumptions

Ø Reduce G&A by $140 million, phased in over 2 years

Ø Reduce “midstream and other” capital expenditures by $50 million immediately

Ø Restructuring charge of $500 million for debt tenders, employee severance and

real estate expenses

real estate expenses

Drastically

reduce

overhead and

waste

reduce

overhead and

waste

Sell

extraneous

assets

extraneous

assets

Reduce future

funding needs

funding needs

Ø Sell Dynamic Offshore for $1.3 billion by YE 2013

Ø Use proceeds to pay down debt

Ø Joint venture 30 - 50 % of Mississippian acreage for $2,500/acre by YE 2013

Ø Sell water infrastructure for $1.0bn, adding $5/boe to LOEs by YE 2013

Our plan could dramatically improve stockholder value

Source: TPG-Axon analysis. (1) Cut G&A by $140mm, “midstream and other” capex by

$50mm; (2) sell Dynamic Offshore for $1.3bn; (3) joint venture 40% of Mississippian acreage

for $2,500/acre; (4) sell water infrastructure for $1.0bn, adds $5/boe to LOEs

$50mm; (2) sell Dynamic Offshore for $1.3bn; (3) joint venture 40% of Mississippian acreage

for $2,500/acre; (4) sell water infrastructure for $1.0bn, adds $5/boe to LOEs

Status Quo

Our Alternative

53

Ø The status quo will destroy stockholder value

Ø Without restructuring, the debt-adjusted cash flow growth is unattractive. Debt, and

the associated interest expense, grows faster than Mississippian cash flows

the associated interest expense, grows faster than Mississippian cash flows

Ø Our plan would create a well-capitalized, self-funding company with a high-growth

profile

profile

Ø The company would emerge with a clean balance sheet, sustainable funding, strong

growth profile and a 15-20 year drilling inventory in the Mississippian…a premier

company that we believe would likely receive a premier valuation!

growth profile and a 15-20 year drilling inventory in the Mississippian…a premier

company that we believe would likely receive a premier valuation!

Ø We believe our actions would enable shareholders to realize NAV of at least

$10-12/share¹

$10-12/share¹

Ø As shown on the previous page, debt would rapidly shrink. While we show debt

running down completely, equity value could be enhanced by accelerating

activity or returning excess capital to stockholders in the form of buybacks or

dividends while maintaining debt at a sensible level ... thus significantly boosting

stockholder value beyond levels shown

running down completely, equity value could be enhanced by accelerating

activity or returning excess capital to stockholders in the form of buybacks or

dividends while maintaining debt at a sensible level ... thus significantly boosting

stockholder value beyond levels shown

54

Our plan could dramatically improve stockholder value

¹ Based on a 8x multiple applied to ~$700mm of operating cash flows in 2015, adjusting for

deployment of balance sheet cash

deployment of balance sheet cash

55

The ‘New SandRidge’ would be a premier company

þ

Ø Pure play Mississippian Lime E&P

Ø 15 - 20 years of high quality, low-risk drilling inventory

Ø More than 1 million acres in the Mississippian

Ø Rapidly growing EBITDA and operating cash flow

Ø 20-30% annual operating cash flow growth over the next few years

Ø Self-funding

Ø Operating cash flow sufficient to run 20-25 rigs in the Mississippian

Ø Strong balance sheet

Ø Net cash balance that could be deployed in accelerating activity or returned to

shareholders in the form of buybacks or dividends

shareholders in the form of buybacks or dividends

SandRidge would be viewed - and valued -

as a premier E&P company

as a premier E&P company

56

Agenda

Ø Overview

Ø Company Background & Performance

Ø Management Compensation & Related Party Transactions

Ø The Path to Value

Ø Company Response

Ø Appendix: Related Party Transactions Presentation

57

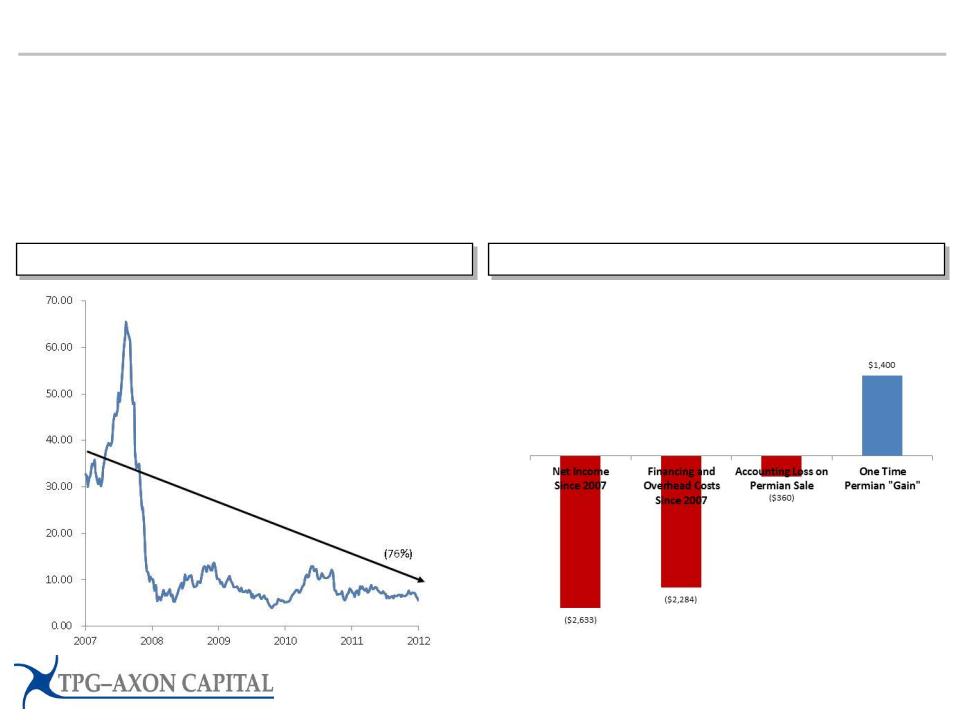

SandRidge response to our consent solicitation

Ø Their claim: “Your Board and management team has taken - and is committed to taking - substantial steps to enhance

performance and increase stockholder value going forward”

performance and increase stockholder value going forward”

Ø Our response: There is no defense for the destruction of value suffered by SandRidge shareholders under the current

management team.

management team.

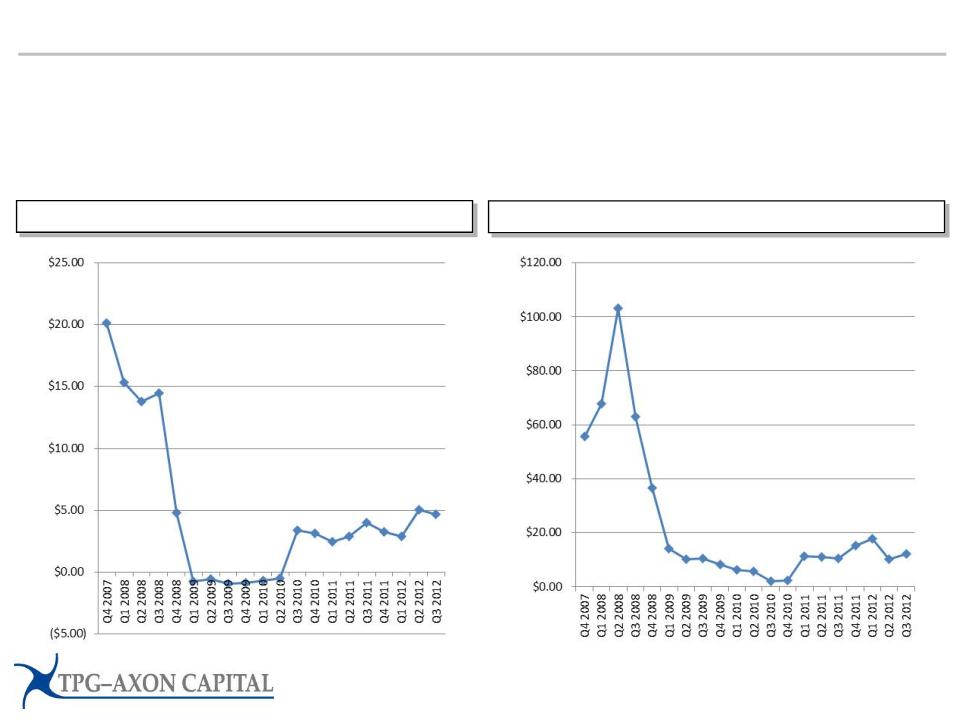

Ø Since the IPO in 2007, net income available to stockholders has been a massive loss of $2.6 billion. Despite

management claims, recent activities have not resulted in significant profit for stockholders, net of costs and losses

management claims, recent activities have not resulted in significant profit for stockholders, net of costs and losses

Source: SandRidge filings. “Financing and overhead costs” represent interest

expense, preferred dividends, minority interest payments and G&A costs

expense, preferred dividends, minority interest payments and G&A costs

Stock Performance Since IPO

Value Creation?

58

SandRidge response to our consent solicitation