UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE FISCAL YEAR ENDED December 31, 2012

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

COMMISSION FILE NUMBER: 814-00852

| GSV Capital Corp. |

| (Exact name of registrant as specified in its charter) |

| | |

| Maryland | 27-4443543 |

| (State of incorporation) | (I.R.S. Employer Identification No.) |

| | |

| 2925 Woodside Road | |

| Woodside, CA | 94062 |

| (Address of principal executive offices) | (Zip Code) |

| | |

| (650) 206-2965 |

| (Registrant’s telephone number, including area code) |

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

| | Name of Each Exchange |

| Title of Each Class | on Which Registered |

| | |

| Common Stock, par value $0.01 per share | NASDAQ Capital Market |

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter periods as the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES x NO ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | | Accelerated filer x | | Non-accelerated filer ¨ | | Smaller reporting company ¨ |

(Do not check if a smaller reporting company)

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act) YES ¨ NO x

The aggregate market value of common stock beneficially owned by non-affiliates of the Registrant on June 29, 2012, based on the closing price on that date of $9.30 on the NASDAQ Capital Market, was $178,734,356. For the purposes of calculating this amount only, all directors and executive officers of the Registrant have been treated as affiliates. There were 19,320,100 shares of the Registrant’s common stock outstanding as of March 12, 2013.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive Proxy Statement relating to the registrant’s 2013 Annual Meeting of Stockholders, to be filed with the Securities and Exchange Commission within 120 days following the end of the Company’s fiscal year, are incorporated by reference in Part III of this Annual Report on Form 10-K as indicated herein.

GSV CAPITAL CORP.

TABLE OF CONTENTS

| | | PAGE |

| | | |

| PART I. | | |

| Item 1. | Business | 4 |

| Item 1A. | Risk Factors | 27 |

| Item 1B. | Unresolved Staff Comments | 41 |

| Item 2. | Properties | 41 |

| Item 3. | Legal Proceedings | 41 |

| Item 4. | Mine Safety Disclosures | 41 |

| | | |

| PART II. | | |

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 42 |

| Item 6. | Selected Financial Data | 45 |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 46 |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 55 |

| Item 8. | Financial Statements and Supplementary Data | 57 |

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 83 |

| Item 9A. | Controls and Procedures | 83 |

| Item 9B. | Other Information | 83 |

| | | |

| PART III. | | |

| Item 10. | Directors, Executive Officers and Corporate Governance | 85 |

| Item 11. | Executive Compensation | 85 |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 85 |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | 85 |

| Item 14. | Principal Accounting Fees and Services | 85 |

| | | |

| PART IV. | | |

| Item 15. | Exhibits and Financial Statement Schedules | 86 |

| Signatures | | 87 |

PART I

GSV Capital

GSV Capital Corp. (formerly NeXt Innovation Corp., the “Company”, “we”, “our” or “GSV Capital”) is an externally managed, non-diversified closed-end management investment company that has elected to be treated as a business development company under the Investment Company Act of 1940, as amended (the “1940 Act”). Our investment objective is to maximize our portfolio’s total return, principally by seeking capital gains on our equity and equity-related investments. We invest principally in the equity securities of what we believe are rapidly growing venture capital-backed emerging companies. We acquire our investments through secondary marketplaces for private companies, negotiations with selling stockholders and direct investments with prospective portfolio companies. We may also invest on an opportunistic basis in select publicly-traded equity securities or certain non-U.S. companies that otherwise meet our investment criteria. Our investment activities are managed by GSV Asset Management, LLC (“GSV Asset Management” or “investment adviser”), and GSV Capital Service Company, LLC (“GSV Capital Service Company” or the “administrator”) provides the administrative services necessary for us to operate.

Our investment philosophy is premised on a disciplined approach of identifying potentially high-growth emerging companies across several key industry themes which may include, among others, social mobile, cloud computing and big data, internet commerce, green technology and education technology. Our investment adviser’s investment decisions are based on a disciplined analysis of available information regarding each potential portfolio company’s business operations, focusing on the company’s growth potential, the quality of recurring revenues and cash flow and cost structures, as well as an understanding of key market fundamentals. Venture capital funds or other financial or strategic sponsors have invested in many of the companies that our investment adviser evaluates.

We seek to deploy capital primarily in the form of non-controlling equity and equity-related investments, including common stock, warrants, preferred stock and similar forms of senior equity, which may or may not be convertible into a portfolio company’s common equity, and convertible debt securities with a significant equity component.

We seek to create a low-turnover portfolio that includes investments in companies representing a broad range of investment themes. As of December 31, 2012, we have completed investments in 47 companies for aggregate consideration of approximately $236.5 million (exclusive of transaction fees and costs), or 85.1% of the net proceeds from our initial public offering and subsequent follow-on offerings.

Our common stock is traded on the NASDAQ Capital Market under the symbol “GSVC”. The net asset value per share of our common stock on December 31, 2012 was $13.07. On December 31, 2012, the last reported sale price of a share of our common stock on the NASDAQ Capital Market was $8.43.

About GSV Asset Management

Our investment activities are managed by GSV Asset Management, an investment adviser registered under the Investment Advisers Act of 1940, as amended, or the “Advisers Act.” GSV Asset Management is led by Michael T. Moe, our president, chief executive officer and chairman of our board of directors. Mr. Moe is assisted by Stephen D. Bard, our chief financial officer, chief compliance officer, treasurer and corporate secretary, whom we refer to collectively as GSV Asset Management’s senior investment professionals. Mr. Moe co-founded and previously served as chairman and chief executive officer of ThinkEquity Partners, an asset management and investment banking firm focusing on venture capital, entrepreneurial and emerging private companies. Prior to founding ThinkEquity, Mr. Moe served as Head of Global Growth Research at Merrill Lynch and before that served as Head of Growth Research and Strategy at Montgomery Securities.

We believe we benefit from the ability of our investment adviser’s senior investment professionals and board of advisers (the “Advisory Board”) to identify attractive investment opportunities, conduct diligence on and value prospective investments, negotiate terms, and manage and monitor a portfolio of those investments. See “Portfolio Management — Advisory Board to GSV Asset Management.” Our investment adviser’s senior investment professionals and Advisory Board members have broad investment backgrounds, with prior experience at investment banks, commercial banks, unregistered investment funds and other financial services companies, and have collectively developed a broad network of contacts that provides us with an important source of investment opportunities.

We pay GSV Asset Management a fee for its services under the Investment Advisory Agreement consisting of two components — a base management fee and an incentive fee. See “Investment Advisory Agreement”.

Investment Opportunity

We believe that the technology industry is experiencing a convergence of numerous disruptive trends, producing new high-growth markets. The growth of both social networking and connected mobile devices, such as smartphones and tablets, has opened up new channels for communication and real-time collaboration. The number of devices and people that regularly connect to the Internet has increased dramatically in recent years, generating significant demand for always accessible, personalized and localized content and real-time online interactivity. These factors are creating opportunities for new market participants and significant growth for established companies with leading positions capitalizing on these trends.

At the same time, we believe that the initial public offering, or “IPO,” markets have experienced substantial structural changes which have made it significantly more challenging for private companies to go public. Volatile equity markets, a lack of investment research coverage for private and smaller companies and investor demand for a longer history of revenue and earnings growth have resulted in companies staying private significantly longer than in the past. In addition, increased public company compliance obligations such as those imposed by the Sarbanes-Oxley Act of 2002 have made it more costly and less attractive to become a public company. As a result, there are significantly fewer IPOs today than there were during the 1990’s, with prospective public companies taking longer to come to market. For example, from 1991 – 2000, there were 4,361 IPOs in the United States, of which 1,701 were venture-capital backed. From 2001 – 2010, there were 1,016 IPOs, of which 369 were venture-capital backed. In 2011, there were 125 IPOs, of which 52 were venture-capital backed.

Because private companies are staying private longer, private investment in late stage companies has increased. Private secondary marketplaces, such as SharesPost and SecondMarket, have emerged as a potential alternative to traditional public equity exchanges to provide liquidity to private company stockholders, including employees, particularly within the technology sector. While such private secondary marketplaces have more limited transaction volume than public exchanges, they do provide accredited investors, such as ourselves, with new channels for access to equity investments in private companies. Such markets also provide a potential source for exiting private company investments, as well as price visibility from trading on a marketplace.

Investment Strategy

We seek to create a portfolio of potentially high-growth emerging private companies via a repeatable and disciplined investment approach, as well as to provide investors with access to such companies through our publicly traded common stock.

Our investment objective is to maximize our portfolio’s total return, principally by seeking capital gains on our equity and equity-related investments. We have adopted the following business strategies to achieve our investment objective:

| · | Identify high quality growth companies.Based on our extensive experience in analyzing technology trends and markets, we have identified the technology sub-sectors of social mobile, cloud computing and big data, internet commerce, green technology and education technology, as opportunities where we believe companies are capable of producing substantial growth. We rely on our collective industry knowledge as well as an understanding of where leading venture capitalists are investing. |

We leverage a combination of our relationships throughout Silicon Valley and our independent research to identify leaders in our targeted sub-sectors that we believe are differentiated and best positioned for sustained growth. Our evaluation process is based on what we refer to as ‘‘the four Ps’’:

| · | People — Organizations led by strong management teams with in-depth operational focus |

| · | Product — Differentiated and disruptive products with leading market positioning |

| · | Potential — Large addressable markets |

| · | Predictability — Ability to forecast and drive predictable and sustainable growth |

We consider these to be the core elements for identifying rapidly growing emerging companies.

| · | Acquire positions in targeted investments.We seek to build our portfolio by sourcing investments at an acceptable price through our disciplined investing strategy. To this end, we utilize multiple methods to acquire equity stakes in private companies that are not available to many individual investors. |

Private secondary marketplaces and direct share purchases.We utilize private secondary marketplaces as a means to acquire equity and equity-related interests in privately-held companies that meet our investment criteria and that we believe are attractive candidates for investment. We believe that such markets offer new channels for access to equity investments in private companies and provide a potential source of liquidity should we decide to exit an investment. In addition, we also purchase shares directly from stockholders, including current or former employees. As certain companies grow and experience significant increased value while remaining private, employees and other stockholders may seek liquidity by selling shares directly to a third party or to a third party via a secondary marketplace. Sales of shares in private companies are typically restricted by contractual transfer restrictions and may be further restricted by provisions in company charter documents, investor rights of first refusal and co-sale and company employment and trading policies, which may impose strict limits on transfer. We believe that our investment professionals’ reputation within the industry and history of investing affords us a favorable position when seeking approval for a purchase of shares subject to such limitations.

Direct equity investments.We also seek direct investments in private companies. There is a large market among emerging private companies for equity capital investments. Many of these companies, particularly within the technology sector, lack the necessary cash flows to sustain substantial amounts of debt, and therefore have viewed equity capital as a more attractive long-term financing tool. We seek to be a source of such equity capital as a means of investing in these companies and look for opportunities to invest alongside other venture capital and private equity investors with whom we have established relationships.

| · | Create access to a diverse investment portfolio.We seek to hold a diverse portfolio of non-controlling equity investments, which we believe will minimize the impact on our portfolio of a negative downturn at any one specific company. We believe that our relatively diversified portfolio will provide a convenient means for accredited and non-accredited individual investors to obtain access to an asset class that has generally been limited to venture capital, private equity and similar large institutional investors. |

Competitive Advantages

We believe that we will benefit from the following competitive advantages in executing our investment strategy:

| · | Experienced team of investment professionals.Our investment adviser’s senior investment professionals, its Advisory Board and our board of directors have significant experience researching and investing in the types of potentially rapidly growing venture capital-backed emerging companies we are targeting for investment. Through our proprietary company evaluation process, including our identification of technology trends and themes and company research, we believe we have developed important insight into identifying and valuing emerging private companies. |

| · | Disciplined and repeatable investment process.We have established a disciplined and repeatable process to locate and acquire available shares at attractive valuations by utilizing multiple sources. In contrast to industry ‘‘aggregators’’ that accumulate stock at market prices, we conduct valuation analyses and make acquisitions only when we can invest at valuations that we believe are attractive to our investors. Following this process, we have completed investments in the 47 companies in our portfolio as of December 31, 2012. |

| · | Deep relationships with significant credibility to source and complete transactions.GSV Asset Management and its senior investment professionals are strategically located in the heart of Silicon Valley in Woodside, California. During the course of over two decades of researching and investing in emerging private companies, our investment adviser’s senior investment professionals have developed strong reputations within the investing community, particularly within technology-related sectors. Our investment adviser’s Advisory Board members and our board of directors have also developed strong relationships in the financial, investing and technology-related sectors. |

| · | Source of permanent investing capital.As a publicly-traded corporation, we have access to a source of permanent equity capital which we can use to invest in portfolio companies. This permanent equity capital is a significant differentiator from other potential investors that may be required to return capital to stockholders on a defined schedule. We believe that our ability to invest on a long-term time horizon makes us attractive to companies looking for strong, stable owners of their equity. |

| · | Early mover advantage.We believe we are one of the few publicly traded business development companies with a specific focus on investing in potentially rapidly growing venture capital-backed emerging companies. Moreover, we believe we are the only one to focus on acquiring shares in secondary transactions as a key component of our strategy. Despite our limited track record, the transactions that we have executed to date since our IPO have helped to establish our reputation with the types of secondary sellers and emerging companies that we target for investment. We have leveraged a number of relationships and channels to acquire the equity of private companies. As we continue to grow our portfolio with attractive investments, we believe that our reputation as a committed partner will be further enhanced, allowing us to source and close investments that would otherwise be unavailable. We believe that these factors collectively differentiate us from other potential investors in private company securities and will potentially enable us to complete equity transactions in desirable private companies at attractive valuations. |

Operating and Regulatory Structure

GSV Capital was formed as a Maryland corporation that is an externally managed, non-diversified closed-end management investment company. We completed our initial public offering in May 2011 and have elected to be treated as a business development company under the 1940 Act. As a business development company, we are required to meet regulatory tests, including the requirement to invest at least 70% of our gross assets in “qualifying assets.” Qualifying assets generally include, among other things, securities of “eligible portfolio companies.” “Eligible portfolio companies” generally include U.S. companies that are not investment companies and that do not have securities listed on a national exchange. If at any time less than 70% of our gross assets are comprised of qualifying assets, including as a result of an increase in the value of any non-qualifying assets or decrease in the value of any qualifying assets, we would generally not be permitted to acquire any additional non-qualifying assets until such time as 70% of our then current gross assets were comprised of qualifying assets. We would not be required, however, to dispose of any non-qualifying assets in such circumstances. See “Regulation as a Business Development Company.” In addition, we intend to elect to be treated for federal income tax purposes beginning with our 2013 taxable year, and intend to qualify annually thereafter, as a regulated investment company (“RIC”) under Subchapter M of the Internal Revenue Code of 1986, as amended (the “Code”). See “Material U.S. Federal Income Tax Considerations.”

Our investment activities are managed by GSV Asset Management and supervised by our board of directors. GSV Asset Management is an investment adviser registered under the Advisers Act. Under our investment advisory agreement, which we refer to as the Investment Advisory Agreement, we have agreed to pay GSV Asset Management an annual base management fee based on our gross assets as well as an incentive fee based on our performance. See “Investment Advisory Agreement.” We have also entered into an administration agreement, which we refer to as the Administration Agreement, under which we have agreed to reimburse GSV Capital Service Company for our allocable portion of overhead and other expenses incurred.

Investment Process

Concentrated Technology-related Focus

During the course of over two decades of researching and investing in non-public companies, we have identified five areas from which we expect to see significant numbers of high-growth companies emerge: new media, communication, alternative energy, education technology, and the consumerization of information technology. These broad markets have the potential to produce disruptive technologies, reach a large addressable market and provide significant commercial opportunities. Within these areas we have identified broad trends that could create significant positive effects on growth such as globalization, consolidation, branding, convergence and network effects. From within these broad technology themes, we have selected five sub-segments in which we target companies for investment: social mobile, cloud computing and big data, internet commerce, green technology and education technology. We remain focused on selecting market leaders within the sub-segments we have identified, while continuing to review our pipeline to ensure we are tracking the next phase of leaders.

Investment Targeting and Screening

We identify prospective portfolio companies through an extensive network of relationships developed by our investment professionals, supplemented by the knowledge and relationships of our investment adviser’s Advisory Board and our board of directors. Investment opportunities that fall within our identified themes are validated against the observed behavior of leading venture capitalists and through our own internal and external research. We evaluate potential portfolio companies across a spectrum of criteria, including “the four Ps”, industry positioning and leadership, stage of growth, and several other factors that collectively characterize our proprietary investment process. We typically seek to invest approximately 90% of our portfolio in well-established, late stage companies and the remaining approximately 10% in emerging companies that fit within our targeted areas, where we see the potential for higher returns from early investment. Based on our initial screening, we identify a select set of companies which we evaluate in greater depth.

Research and Due Diligence Process

Once we identify those companies that we believe warrant more in-depth analysis, we focus on their revenue growth, revenue quality and sustainability and earnings growth, as well as other metrics that may be strongly correlated with higher valuations. We also focus on the company’s management team and any significant financial sponsor, the current business model, competitive positioning, regulatory and legal issues, the quality of any intellectual property and other investment-specific due diligence. Each prospective portfolio company that passes our initial due diligence review is given a qualitative ranking to allow us to evaluate it against others in our pipeline, and we review and update these companies on a regular basis.

Our due diligence process will vary depending on whether we are investing through a private secondary transaction on a marketplace or with a selling stockholder or by direct equity investment. We access information on our potential investments through a variety of sources, including information made available on secondary marketplaces, publications by private company research firms, industry publications, commissioned analysis by third-party research firms, and, to a limited extent, directly from the company or financial sponsor. We utilize a combination of each of these sources to help us set a target value for the companies we ultimately select for investment.

Portfolio Construction and Sourcing

Upon completion of our research and due diligence process, we select investments for inclusion in our portfolio based on their relative qualitative ranking, fundamentals and valuation. We seek to create a relatively diversified portfolio that we expect will include investments in companies representing a broad range of investment themes. We generally choose to pursue specific investments based on the availability of shares and valuation expectations. We utilize a combination of secondary marketplaces, direct purchases from stockholders and direct equity investments in order to make investments in our portfolio companies. Once we have established an initial position in a portfolio company, we may choose to increase our stake through subsequent purchases. Maintaining a balanced portfolio is a key to our success, and as a result we constantly evaluate the composition of our investments and our pipeline to ensure we are exposed to a diverse set of companies within our target segments.

Transaction Execution

We enter into purchase agreements for each of our private company portfolio investments. Private company securities are typically subject to contractual transfer limitations, which may, among other things, give the issuer, its assignees and/or its stockholders a particular period of time, often 30 days or more, in which to exercise a veto right, or a right of first refusal over, the sale of such securities. Accordingly, the purchase agreements we enter into for secondary transactions typically require the lapse or satisfaction of these rights as a condition to closing. Under these circumstances, we are may be required to deposit the purchase price into escrow upon signing with the funds released to the seller at closing or returned to us if the closing conditions are not met.

Risk Management and Monitoring

We monitor the financial trends of each portfolio company to assess our exposure to individual companies as well as to evaluate overall portfolio quality. We establish valuation targets at the portfolio level and for gross and net exposures with respect to specific companies and industries within our overall portfolio. In cases where we make a direct investment in a portfolio company, we may also obtain board positions, board observation rights and/or information rights from that portfolio company in connection with our equity investment. We regularly monitor our portfolio for compliance with the diversification requirements for purposes of maintaining our status as a 1940 Act business development company and a RIC for tax purposes.

Portfolio Overview

At December 31, 2012, our portfolio was invested approximately 54.9% in common shares, 44.8% in preferred shares, 0.2% in membership interests, and 0.1% in equity warrants. Such percentages are not inclusive of our holdings in money market funds.

Our ten largest portfolio company investments at December 31, 2012, based on the combined fair value of the equity securities we hold in each portfolio company, were as follows:

| | | | | At December 31, 2012 | |

| Portfolio Company | | Industry | | Cost | | | Fair

Value | | | % of Net

Asset

Value | |

| Twitter, Inc. | | Social

Communication | | $ | 32,991,111 | | | $ | 36,111,400 | | | | 14.30 | % |

| Palantir Technologies, Inc. | | Cyber Security | | | 21,060,447 | | | | 21,072,414 | | | | 8.34 | |

| Violin Memory, Inc. | | Flash Memory | | | 14,818,843 | | | | 14,799,996 | | | | 5.86 | |

| Dropbox, Inc. | | Online Storage | | | 13,656,486 | | | | 14,437,346 | | | | 5.72 | |

| Chegg, Inc. | | Textbook Rental | | | 14,021,197 | | | | 14,193,544 | | | | 5.61 | |

| Avenues World Holdings LLC | | Globally-focused Private School | | | 10,025,123 | | | | 10,000,000 | | | | 3.96 | |

| Solexel, Inc. | | Solar Power | | | 10,016,559 | | | | 10,000,000 | | | | 3.96 | |

| 2U, Inc. | | Online Education | | | 10,030,724 | | | | 9,999,786 | | | | 3.96 | |

| Kno Inc. | | Digital Textbooks | | | 9,987,021 | | | | 9,928,849 | | | | 3.93 | |

| Facebook, Inc. | | Social Networking | | | 10,472,294 | | | | 9,317,000 | | | | 3.69 | |

| Total | | | | $ | 147,079,805 | | | $ | 149,860,335 | | | | 59.33 | % |

Set forth below are descriptions of the ten largest portfolio investments as of December 31, 2012:

Twitter, Inc.

Twitter is a social networking company. Twitter is a real-time information network that allows users to send and receive information.

Palantir Technologies, Inc.

Palantir solves critical intelligence and security issues for government agencies, banks, and large institutions.

Violin Memory, Inc.

Violin Memory provides scalable flash memory which improves the performance of memory on computers by reducing the power and space requirements in a data center.

Dropbox, Inc.

Dropbox is a provider of cloud storage that enables users to store and share files across the internet.

Chegg, Inc.

Chegg is an online textbook rental company with a leading market presence in the online education industry. Chegg has built a social education learning platform that assists students by providing course planning and selection services, textbooks, study materials and homework assistance.

Avenues World Holdings LLC

Avenues is a private pre-K through 12th grade school that aspires to ultimately become a single school with multiple integrated global campuses, raising the global standard for top-tier private schools.

Solexel, Inc.

Solexel is developing high-efficiency, low-cost, crystalline silicon solar cells and modules for photovoltaic electricity generation.

2U, Inc. (f/k/a 2tor, Inc.)

2U partners with universities, providing technology solutions to manage students from recruitment to post-graduation job placement, as well as develop and deliver curriculum in a virtual environment.

Kno, Inc.

Kno is a provider of education software, digital textbooks and social engagement tools for students.

Facebook, Inc.

Facebook is a leading social-networking company. Facebook’s social networking website allows users to create a personal profile, add other users to the network, and exchange messages, photographs and other information that can be shared across a network.

Managerial Assistance

As a business development company, we are required to offer, and in some cases may provide and be paid for, significant managerial assistance to portfolio companies. This assistance typically involves monitoring the operations of portfolio companies, participating in their board and management meetings, consulting with and advising their officers and providing other organizational and financial guidance.

Competition

Our primary competitors include specialty finance companies including late stage venture capital funds, private equity funds, other crossover funds, public funds investing in private companies and business development companies. Many of these entities have greater financial and managerial resources than we will have. For additional information concerning the competitive risks we face, see ‘‘Risk Factors — Risks Relating to Our Business and Structure.’’

Employees

While we have executive officers, they receive no direct compensation from us, and we have no direct employees. Our day-to-day investment operations are managed by our investment adviser. In addition, we reimburse GSV Capital Service Company for an allocable portion of expenses incurred by it in performing its obligations under the Administration Agreement, including a portion of the rent and the compensation of our chief financial officer and chief compliance officer and any administrative support personnel. See ‘‘Investment Advisory Agreement.’’

Determination of Net Asset Value

We determine the net asset value of our investment portfolio after the conclusion of each fiscal quarter in connection with the preparation of our annual and quarterly reports filed under the Exchange Act, or more frequently if required under the 1940 Act.

Securities that are publicly traded are generally valued at the close price on the valuation date; however, if they remain subject to lock-up restrictions they are discounted accordingly. Securities that are not publicly traded or for which there are no readily available market quotations, including securities that trade on secondary markets for private securities, are valued at fair value as determined in good faith by our board of directors. In connection with that determination, members of our investment adviser’s portfolio management team will prepare portfolio company valuations using the most recent portfolio company financial statements and forecasts. We also engage an independent valuation firm to perform independent valuations of our investments that are not publicly traded or for which there are no readily available market quotations. We may also engage an independent valuation firm to perform independent valuations of any securities that trade on private secondary markets, but are not otherwise publicly traded, where there is a lack of appreciable trading or a wide disparity in recently reported trades.

For those securities that are not publicly traded or for which there are no readily available market quotations, our board of directors, with the assistance of our Valuation Committee, will use the recommended valuations as prepared by management and the independent valuation firm, respectively, as a component of the foundation for its final fair value determination. Due to the uncertainty inherent in the valuation process, such estimates of fair value may differ significantly from the values that would have resulted had others made the determination using the same or different procedures or had a readily available market for the securities existed, and the differences could be material. Additionally, changes in the market environment and other events that may occur over the life of the investments may cause the gains or losses ultimately realized on these investments to be different than the gains or losses implied by the valuation currently assigned to such investments. For those investments that are publicly traded, we generally record unrealized appreciation or depreciation based on changes in the market value of the securities as of the valuation date. Publicly traded securities that remain subject to lock-up restrictions are discounted accordingly. For those investments that are not publicly traded and for which there are no readily available market quotations, we record unrealized depreciation if the underlying portfolio company has depreciated in value and our equity security has also depreciated in value, and record unrealized appreciation if the underlying portfolio company has appreciated in value and our equity security has also appreciated in value. Changes in fair value are recorded in the statement of operations as the net change in unrealized appreciation or depreciation.

We generally determine the fair value of our investments by considering a number of factors. The following represent factors that could impact our fair value determinations:

| 1. | Public trading of our portfolio securities, taking into consideration lock-up requirements and liquidity; |

| 2. | Active trading of our portfolio securities on a private secondary market, where we have determined that there is meaningful volume and the transactions are considered arm’s length by sophisticated investors; |

| 3. | Qualified funding rounds in the companies in which we are invested, where there is meaningful and reputable information available on size, valuation and investors; and |

| 4. | Additional investments by us in current portfolio companies, where the price of the new investment differs materially from prior investments. |

There is inherent subjectivity in determining the fair value of our investments. We expect that most of our portfolio investments, other than those for which market quotations are readily available and that may be sold without restriction, will be valued at fair value as determined in good faith by our board of directors, with the assistance of our valuation committee.

Investment Advisory Agreement

Management Services

GSV Asset Management serves as our investment adviser. GSV Asset Management is registered as an investment adviser under the Advisers Act. Subject to the overall supervision of our board of directors, GSV Asset Management manages the day-to-day operations of, and provides investment advisory services to, GSV Capital. Under the terms of the Investment Advisory Agreement, GSV Asset Management:

| · | determines the composition of our portfolio, the nature and timing of the changes to our portfolio and the manner of implementing such changes; |

| · | determines what securities we will purchase, retain or sell; |

| · | identifies, evaluates and negotiates the structure of the investments we make; and |

| · | closes, monitors and services the investments we make. |

GSV Asset Management’s services under the Investment Advisory Agreement are not exclusive, and it is free to furnish similar services to other entities so long as its services to us are not impaired. GSV Asset Management currently serves as the investment adviser for GSV X Fund, a global long/short absolute return fund. GSV Asset Management does not anticipate that it will ordinarily identify investment opportunities that are appropriate for both GSV Capital and the other funds that are currently or in the future may be managed by GSV Asset Management. However, to the extent it does identify such opportunities, GSV Asset Management will allocate such opportunities between GSV Capital and such other funds pursuant to an established procedure that is designed to ensure that such allocation is fair and equitable.

Management Fees

We pay GSV Asset Management a fee for its services under the Investment Advisory Agreement consisting of two components — a base management fee and an incentive fee. The cost of both the base management fee payable to GSV Asset Management, and any incentive fees earned by GSV Asset Management, are ultimately borne by our common stockholders.

The base management fee (the ‘‘Base Fee’’) is calculated at an annual rate of 2.00% of our gross assets. For the period from the close of the initial public offering through and including December 31, 2011, the Base Fee was payable monthly in arrears, and was calculated based on the initial value of our assets upon the closing of our initial public offering in April 2011. For the year ended December 31, 2012, the Base Fee was payable monthly in arrears, and was calculated based on the average value of our gross assets at the end of the two most recently completed calendar quarters, and appropriately adjusted for any equity or debt capital raises, repurchases or redemptions during the current calendar quarter. The Base Fee for any partial month or quarter was appropriately pro-rated.

The incentive fee is determined and payable in arrears as of the end of each calendar year (or upon termination of the Investment Advisory Agreement, as of the termination date), and is equal to the lesser of:

| · | 20% of our realized capital gains during such calendar year, if any, calculated on an investment-by-investment basis, subject to a non-compounded preferred return, or ‘‘hurdle,’’ and a ‘‘catch-up’’ feature, and |

| · | 20% of our realized capital gains, if any, on a cumulative basis from inception through the end of each calendar year, computed net of all realized capital losses and unrealized capital depreciation on a cumulative basis, less the aggregate amount of any previously paid incentive fees. |

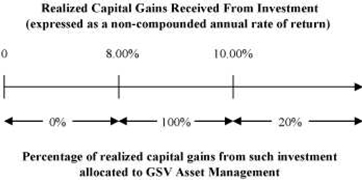

Our realized capital gains from each investment, expressed as a non-compounded annual rate of return on the cost of such investment since we initially acquired it, will be compared to a hurdle rate of 8.00% per year. We will only pay an incentive fee on any realized capital gains from an investment that exceeds the hurdle rate. We will pay GSV Asset Management an incentive fee with respect to our realized capital gains from each investment as follows:

| · | No incentive fee is payable on the amount of any realized capital gains from an investment that, when expressed as a non-compounded annual rate of return on the cost of such investment since we initially acquired it, does not exceed the hurdle rate of 8.00% per year. |

| · | We pay as an incentive fee 100% of the amount of any realized capital gains from an investment that, when expressed as a non-compounded annual rate of return on the cost of such investment since we initially acquired it, exceeds the hurdle rate of 8.00% per year but is less than a rate of 10.00% per year. We refer to this portion of our realized capital gains from each investment (which exceeds the hurdle rate but is less than 10.00%) as the ‘‘catch-up.’’ The ‘‘catch-up’’ is meant to provide our investment adviser with 20% of the amount of our realized capital gains from an investment that, when expressed as a non-compounded annual rate of return on the cost of such investment since we initially acquired it, exceeds a rate of 10.00% per year. |

| · | We pay as an incentive fee 20% of the amount of any realized capital gains from an investment that, when expressed as a non-compounded annual rate of return on the cost of such investment since we initially acquired it, exceeds a rate of 10.00% per year. |

In no event, however, will we pay an incentive fee for any calendar year that exceeds 20% of our realized capital gains, if any, on a cumulative basis from inception through the end of such calendar year, computed net of all realized capital losses and unrealized capital depreciation on a cumulative basis, less the aggregate amount of any previously paid incentive fees.

The following is a graphical representation of the calculation of our incentive fee with respect to a single investment:

For accounting purposes, in order to reflect the theoretical capital gains incentive fee that would be payable for a given period as if all unrealized gains were realized, we are required to accrue a capital gains incentive fee based upon realized capital gains and losses during the current calendar year through the end of the period, plus any unrealized capital appreciation and depreciation as of the end of the period. It should be noted that a fee so calculated and accrued would not necessarily be payable under the Investment Advisory Agreement, and may never be paid based upon the computation of capital gains incentive fees in subsequent periods. Amounts paid under the Investment Advisory Agreement will be consistent with the formula reflected in the Investment Advisory Agreement.

Example: Calculation of incentive fee

Alternative 1:

Assumptions

| · | Hurdle rate = 8.00% non-compounded annual rate of return |

| · | Hurdle rate = (purchase price) × (8% × (days owned/365)) |

| · | Catch-up rate = 10.00% non-compounded annual rate of return |

| · | Catch-up rate = (purchase price) × (10% × (days owned/365)) |

| · | Year 1: $20,000,000 investment made on March 15 in Company A (‘‘Investment A’’), and $30,000,000 investment made on February 1 in Company B (‘‘Investment B’’) |

| · | Year 2: Investment A is sold on September 15 for $25,000,000, and fair market value (‘‘FMV’’) of Investment B is determined to be $28,000,000 |

| · | Year 3: FMV of Investment B is determined to be $28,000,000 |

| · | Year 4: Investment B is sold on March 1 for $38,000,000 |

The incentive fee would be calculated as follows:

| · | Year 2: Incentive fee calculation: |

| · | Hurdle rate for Investment A = ($20,000,000) × (8% × (550 days / 365)) |

| · | Hurdle rate for Investment A = $2,410,959 |

| · | Catch-up rate for Investment A = ($20,000,000) × (10% × (550 days / 365)) |

| · | Catch-up rate for Investment A = $3,013,699 |

| · | Incentive fee on Investment A = 20% × $5,000,000 (since the hurdle rate has been satisfied and the catch up has been fully achieved) |

| · | Incentive fee on Investment A = $1,000,000 |

| · | Maximum incentive fee = 20% × (cumulative realized capital gains – (cumulative realized losses + cumulative net unrealized depreciation)) – (previously paid incentive fees) |

| · | Maximum incentive fee = 20% × ($5,000,000 - $2,000,000 (unrealized depreciation on Investment B)) |

| · | Maximum incentive fee = 20% × $3,000,000 |

| · | Maximum incentive fee = $600,000 |

| · | Incentive fee paid = $600,000 (because the incentive fee payable on Investment A exceeds the maximum incentive fee, the maximum incentive fee applies) |

| · | Year 4: Incentive fee calculation: |

| · | Hurdle rate for Investment B = ($30,000,000) × (8% × (1,124 days / 365)) |

| · | Hurdle rate for Investment B = $7,390,685 |

| · | Catch-up rate for Investment B = ($30,000,000) × (10% × (1,124 days / 365)) |

| · | Catch-up rate for Investment B = $9,238,356 |

| · | Incentive fee on Investment B = 100% × ($8,000,000 – $7,390,685 (since the hurdle rate has been satisfied, but the catch up has not been fully achieved) |

| · | Incentive fee on Investment B = $609,315 |

| · | Maximum incentive fee = 20% × (cumulative realized capital gains – (cumulative realized losses + cumulative net unrealized depreciation)) – (previously paid incentive fees) |

| · | Maximum incentive fee = (20% × $13,000,000) – ($600,000 (previously paid incentive fees)) |

| · | Maximum incentive fee = $2,000,000 |

| · | Incentive fee paid = $609,315 (because the incentive fee payable on Investment B does not exceed the maximum incentive fee) |

Alternative 2:

Assumptions

| · | Hurdle rate = 8.00% non-compounded annual rate of return |

| · | Hurdle rate = (purchase price) × (8% × (days owned/365)) |

| · | Catch-up rate = 10.00% non-compounded annual rate of return |

| · | Catch-up rate = (purchase price) × (10% × (days owned/365)) |

| · | Year 1: $20 million investment made on March 15 in Company A (‘‘Investment A’’), $30 million investment made on February 1 in Company B (‘‘Investment B’’), and $25 million investment made on September 1 in Company C (‘‘Investment C’’) |

| · | Year 2: Investment A is sold on September 15 for $50 million, FMV of Investment B is determined to be $25 million, and FMV of Investment C is determined to be $25 million |

| · | Year 3: FMV of Investment B is determined to be $27 million and Investment C is sold on December 1 for $30 million |

| · | Year 4: FMV of Investment B is determined to be $35 million |

| · | Year 5: Investment B is sold on March 1 for $20 million |

The incentive fee would be calculated as follows:

| · | Year 2: Incentive fee calculation: |

| · | Hurdle rate for Investment A = ($20,000,000) × (8% × (550 days / 365)) |

| · | Hurdle rate for Investment A = $2,410,959 |

| · | Catch-up rate for Investment A = ($20,000,000) × (10% × (550 days / 365)) |

| · | Catch-up rate for Investment A = $3,013,699 |

| · | Incentive fee on Investment A = 20% × $30,000,000 (since the hurdle rate has been satisfied and the catch up has been fully achieved) |

| · | Incentive fee on Investment A = $6,000,000 |

| · | Maximum incentive fee = 20% × (cumulative realized capital gains – (cumulative realized losses + cumulative net unrealized depreciation)) – (previously paid incentive fees) |

| · | Maximum incentive fee = 20% × ($30,000,000 - $5,000,000 (unrealized depreciation on Investment B)) |

| · | Maximum incentive fee = $5,000,000 |

| · | Incentive fee paid = $5,000,000 (because the incentive fee payable on Investment A exceeds the maximum incentive fee, the maximum incentive fee applies) |

| · | Year 3: Incentive fee calculation: |

| · | Hurdle rate for Investment C = ($25,000,000) × (8% × (822 days / 365)) |

| · | Hurdle rate for Investment C = $4,504,110 |

| · | Catch-up rate for Investment C = ($25,000,000) × (10% × (822 days / 365)) |

| · | Catch-up rate for Investment C = $5,630,137 |

| · | Incentive fee on Investment C = 100% × ($5,000,000 – $4,504,110 (since the hurdle rate has been satisfied, but the catch up has not been fully achieved)) |

| · | Incentive fee on Investment C = $495,890 |

| · | Maximum incentive fee = 20% × (cumulative realized capital gains – (cumulative realized losses + cumulative net unrealized depreciation)) – (previously paid incentive fees) |

| · | Maximum incentive fee = 20% × ($35,000,000 - $3,000,000 (unrealized depreciation on Investment B)) – ($5,000,000 (previously paid incentive fees)) |

| · | Maximum incentive fee = $1,400,000 |

| · | Incentive fee paid = $495,890 (because the incentive fee payable on Investment C does not exceed the maximum incentive fee) |

We seek to deploy capital primarily in the form of non-controlling investments in our portfolio companies. Although we primarily invest through private secondary markets, to the extent we make a direct minority investment in a portfolio company, neither we, nor our investment adviser, GSV Asset Management, may have the ability to control the timing of when we realize capital gains or losses with respect to such investment. We expect the timing of such realization events to be determined by our portfolio companies in such cases. To the extent we have non-minority investments, or the securities we hold are traded on a private secondary market or public securities exchange, GSV Asset Management will have greater control over the timing of a realization event. In such cases, our board of directors will monitor such investments in connection with their general oversight of the investment management services provided by GSV Asset Management. In addition, as of the end of each fiscal quarter, we will evaluate whether the cumulative aggregate unrealized appreciation on our portfolio would be sufficient to require us to pay an incentive fee to our investment adviser if such unrealized appreciation were actually realized as of the end of such quarter, and if so, we will accrue an expense equal to the amount of such incentive fee. Any such accrual of incentive fees will be reflected in the calculation of our net asset value.

Payment of our Expenses

All personnel of our investment adviser when and to the extent engaged in providing investment advisory services, and the compensation and expenses of such personnel allocable to such services, are provided and paid for by GSV Asset Management. We are responsible for all other costs and expenses of our operations and transactions, including (without limitation) the cost of calculating our net asset value; the cost of effecting sales and repurchases of shares of our common stock and other securities; investment advisory fees; fees payable to third parties relating to, or associated with, making investments, including fees and expenses associated with performing due diligence reviews of prospective investments (in each case subject to approval of our board of directors); transfer agent and custodial fees; fees and expenses associated with marketing efforts (including attendance at investment conference and similar events); federal and state registration fees; any exchange listing fees; federal, state and local taxes; independent directors’ fees and expenses; brokerage commissions; costs associated with our reporting and compliance obligations under the 1940 Act and applicable federal and state securities laws including costs of proxy statements, stockholders’ reports and notices; fidelity bond, directors and officers/errors and omissions liability insurance and other insurance premiums; direct costs such as printing, mailing, long distance telephone, staff, independent audits and outside legal costs and all other expenses incurred by either GSV Capital Service Company or us in connection with administering our business, including payments under the Administration Agreement that are based upon our allocable portion of overhead and other expenses incurred by GSV Capital Service Company in performing its obligations under the Administration Agreement, including a portion of the rent and the compensation of our chief financial officer and chief compliance officer and other administrative support personnel. All of these expenses are ultimately borne by our common stockholders.

Duration and Termination

The Investment Advisory Agreement was reapproved by our board of directors on March 8, 2013. Unless earlier terminated as described below, the Investment Advisory Agreement will remain in effect for a period of one year from the date it was approved by the board of directors and will remain in effect from year to year thereafter if approved annually by our board of directors or by the affirmative vote of the holders of a majority of our outstanding voting securities, including, in either case, approval by a majority of our directors who are not interested persons. The Investment Advisory Agreement will automatically terminate in the event of its assignment. The Investment Advisory Agreement may be terminated by either party without penalty upon not more than 60 days’ written notice to the other. The Investment Advisory Agreement may also be terminated, without penalty, upon the vote of a majority of our outstanding voting securities.

Indemnification

The Investment Advisory Agreement provides that, absent willful misfeasance, bad faith or gross negligence in the performance of its duties or by reason of the reckless disregard of its duties and obligations, GSV Asset Management and its officers, managers, partners, agents, employees, controlling persons, members and any other person or entity affiliated with it are entitled to indemnification from us for any damages, liabilities, costs and expenses (including reasonable attorneys’ fees and amounts reasonably paid in settlement) arising from the rendering of GSV Asset Management’s services under the Investment Advisory Agreement or otherwise as our investment adviser.

Organization of the Investment Adviser

GSV Asset Management is a Delaware limited liability company. The principal executive offices of GSV Asset Management are located at 2925 Woodside Road, Woodside, CA 94062.

Board Approval of the Investment Advisory Agreement

Our Board of Directors determined at a meeting held on March 8, 2013 to reapprove the Investment Advisory Agreement. In its consideration of the reapproval of the Investment Advisory Agreement, the Board of Directors focused on information it had received relating to, among other things:

| · | the nature, quality and extent of the advisory and other services to be provided to us by GSV Asset Management; |

| · | comparative data with respect to advisory fees or similar expenses paid by other business development companies with similar investment objectives; |

| · | our historical and projected operating expenses and expense ratio compared to business development companies with similar investment objectives; |

| · | any existing and potential sources of indirect income to GSV Asset Management or GSV Capital Service Company from their relationships with us and the profitability of those relationships, including the Investment Advisory Agreement and the Administration Agreement; |

| · | information about the services to be performed and the personnel performing such services under the Investment Advisory Agreement; |

| · | the organizational capability and financial condition of GSV Asset Management and its affiliates; |

| · | GSV Asset Management’s practices regarding the selection and compensation of brokers that may execute our portfolio transactions and the brokers’ provision of brokerage and research services to GSV Asset Management; and |

| · | the possibility of obtaining similar services from other third party service providers or through an internally managed structure. |

Based on the information reviewed and related discussions, the Board of Directors concluded that fees payable to GSV Asset Management pursuant to the Investment Advisory Agreement were reasonable in relation to the services to be provided. The Board of Directors did not assign relative weights to the above factors or the other factors considered by it. In addition, the Board of Directors did not reach any specific conclusion on each factor considered, but conducted an overall analysis of these factors. Individual members of the Board of Directors may have given different weights to different factors.

Administration Agreement

Pursuant to a separate Administration Agreement, GSV Capital Service Company, a Delaware limited liability company, furnishes us with office facilities, together with equipment and clerical, bookkeeping and record keeping services at such facilities. The principal executive offices of GSV Capital Service Company are located at 2925 Woodside Road, Woodside, CA 94062. Under the Administration Agreement, GSV Capital Service Company also performs, or oversees the performance of, our required administrative services, which includes being responsible for the financial records which we are required to maintain and preparing reports to our stockholders and reports filed with the SEC. In addition, GSV Capital Service Company assists us in determining and publishing our net asset value, overseeing the preparation and filing of our tax returns and the printing and dissemination of reports to our stockholders, and generally overseeing the payment of our expenses and the performance of administrative and professional services rendered to us by others. Payments under the Administration Agreement are based upon our allocable portion of overhead and other expenses incurred by GSV Capital Service Company in performing its obligations under the administration agreement, including a portion of the rent and the compensation of our chief financial officer and chief compliance officer and any administrative support personnel. While there is no limit on the total amount of expenses we may be required to reimburse to GSV Capital Service Company, our administrator will only charge us for the actual expenses it incurs on our behalf, or our allocable portion thereof, without any profit to GSV Capital Service Company. The Administration Agreement may be terminated by either party without penalty upon 60 days’ written notice to the other party.

The Administration Agreement provides that, absent willful misfeasance, bad faith or gross negligence in the performance of their respective duties or by reason of the reckless disregard of their respective duties and obligations, GSV Capital Service Company and its officers, manager, agents, employees, controlling persons, members and any other person or entity affiliated with it are entitled to indemnification from us for any damages, liabilities, costs and expenses (including reasonable attorneys’ fees and amounts reasonably paid in settlement) arising from the rendering of GSV Capital Service Company’s services under the Administration Agreement or otherwise as our administrator.

GSV Capital Service Company also provides administrative services to our investment adviser, GSV Asset Management. As a result, GSV Asset Management also reimburses GSV Capital Service Company for its allocable portion of GSV Capital Service Company’s overhead, including rent, the fees and expenses associated with performing compliance functions for GSV Asset Management, and its allocable portion of the compensation of any administrative support staff.

License Agreement

We have entered into a license agreement with GSV Asset Management pursuant to which GSV Asset Management has agreed to grant us a non-exclusive, royalty-free license to use the name ‘‘GSV.’’ Under this agreement, we have a right to use the GSV name for so long as the Investment Advisory Agreement with GSV Asset Management is in effect. Other than with respect to this limited license, we will have no legal right to the ‘‘GSV’’ name.

Regulation as a Business Development Company

General

A business development company is regulated by the 1940 Act. A business development company must be organized in the United States for the purpose of investing in or lending to primarily private companies and making significant managerial assistance available to them. A business development company may use capital provided by public stockholders and from other sources to make long-term, private investments in businesses. A business development company provides stockholders the ability to retain the liquidity of a publicly traded stock while sharing in the possible benefits, if any, of investing in primarily privately owned companies.

We may not change the nature of our business so as to cease to be, or withdraw our election as, a business development company unless authorized by vote of a majority of the outstanding voting securities, as required by the 1940 Act. A majority of the outstanding voting securities of a company is defined under the 1940 Act as the lesser of: (a) 67% or more of such company’s voting securities present at a meeting if more than 50% of the outstanding voting securities of such company are present or represented by proxy, or (b) more than 50% of the outstanding voting securities of such company. We do not anticipate any substantial change in the nature of our business.

As with other companies regulated by the 1940 Act, a business development company must adhere to certain substantive regulatory requirements. A majority of our directors must be persons who are not interested persons, as that term is defined in the 1940 Act. Additionally, we are required to provide and maintain a bond issued by a reputable fidelity insurance company to protect the business development company. Furthermore, as a business development company, we are prohibited from protecting any director or officer against any liability to us or our stockholders arising from willful misfeasance, bad faith, gross negligence or reckless disregard of the duties involved in the conduct of such person’s office.

As a business development company, we are generally required to meet an asset coverage ratio, defined under the 1940 Act as the ratio of our gross assets (less all liabilities and indebtedness not represented by senior securities) to our outstanding senior securities, of at least 200% after each issuance of senior securities. We may also be prohibited under the 1940 Act from knowingly participating in certain transactions with our affiliates without the prior approval of our directors who are not interested persons and, in some cases, prior approval by the SEC.

We are generally not able to issue and sell our common stock at a price below net asset value per share. See “Risk Factors — Risks Relating to Our Business and Structure — Regulations governing our operation as a business development company affect our ability to, and the way in which we, raise additional capital.” We may, however, sell our common stock, or warrants, options or rights to acquire our common stock, at a price below the then-current net asset value of our common stock if our board of directors determines that such sale is in our best interests and the best interests of our stockholders, and our stockholders approve such sale. In addition, we may generally issue new shares of our common stock at a price below net asset value in rights offerings to existing stockholders, in payment of dividends and in certain other limited circumstances.

As a business development company, we are generally limited in our ability to invest in any portfolio company in which our investment adviser or any of its affiliates currently has an investment or to make any co-investments with our investment adviser or its affiliates without an exemptive order from the SEC, subject to certain exceptions.

We are subject to periodic examination by the SEC for compliance with the 1940 Act.

As a business development company, we are subject to certain risks and uncertainties. See “Risk Factors — Risks Relating to Our Business and Structure.”

Qualifying Assets

Under the 1940 Act, a business development company may not acquire any asset other than assets of the type listed in Section 55(a) of the 1940 Act, which are referred to as qualifying assets, unless, at the time the acquisition is made, qualifying assets represent at least 70% of the business development company’s gross assets. The principal categories of qualifying assets relevant to our business are the following:

| 1. | Securities purchased in transactions not involving any public offering from the issuer of such securities, which issuer (subject to certain limited exceptions) is an eligible portfolio company, or from any person who is, or has been during the preceding 13 months, an affiliated person of an eligible portfolio company, or from any other person, subject to such rules as may be prescribed by the SEC. An eligible portfolio company is defined in the 1940 Act as any issuer which: |

| a. | is organized under the laws of, and has its principal place of business in, the United States; |

| b. | is not an investment company (other than a small business investment company wholly owned by the business development company) or a company that would be an investment company but for certain exclusions under the 1940 Act; and |

| c. | satisfies any of the following: |

| i. | does not have any class of securities that is traded on a national securities exchange; |

| ii. | has a class of securities listed on a national securities exchange, but has an aggregate market value of outstanding voting and non-voting common equity of less than $250 million; |

| iii. | is controlled by a business development company or a group of companies including a business development company and the business development company has an affiliated person who is a director of the eligible portfolio company; or |

| iv. | is a small and solvent company having gross assets of not more than $4.0 million and capital and surplus of not less than $2.0 million. |

| 2. | Securities of any eligible portfolio company which we control. |

| 3. | Securities purchased in a private transaction from a U.S. issuer that is not an investment company or from an affiliated person of the issuer, or in transactions incident thereto, if the issuer is in bankruptcy and subject to reorganization or if the issuer, immediately prior to the purchase of its securities, was unable to meet its obligations as they came due without material assistance other than conventional lending or financing arrangements. |

| 4. | Securities of an eligible portfolio company purchased from any person in a private transaction if there is no ready market for such securities and we already own 60% of the outstanding equity of the eligible portfolio company. |

| 5. | Securities received in exchange for or distributed on or with respect to securities described in 1 through 4 above, or pursuant to the exercise of warrants or rights relating to such securities. |

| 6. | Cash, cash equivalents, U.S. government securities or high-quality debt securities maturing in one year or less from the time of investment. |

If at any time less than 70% of our gross assets are comprised of qualifying assets, including as a result of an increase in the value of any non-qualifying assets or decrease in the value of any qualifying assets, we would generally not be permitted to acquire any additional non-qualifying assets, other than office furniture and equipment, interests in real estate and leasehold improvements and facilities maintained to conduct the business operations of the business development company, deferred organization and operating expenses, and other noninvestment assets necessary and appropriate to its operations as a business development company, until such time as 70% of our then current gross assets were comprised of qualifying assets. We would not be required, however, to dispose of any non-qualifying assets in such circumstances.

Managerial Assistance to Portfolio Companies

In addition, a business development company must have been organized and have its principal place of business in the United States and must be operated for the purpose of making investments in the types of securities described above in Qualifying Assets categories 1, 2 or 3. However, in order to count portfolio securities as qualifying assets for the purpose of the 70% test, the business development company must either control the issuer of the securities or must offer to make available to the issuer of the securities (other than small and solvent companies described above in Qualifying Assets category 1.c.iv.) significant managerial assistance; except that, where the business development company purchases such securities in conjunction with one or more other persons acting together, one of the other persons in the group may make available such managerial assistance. Making available managerial assistance means, among other things, any arrangement whereby the business development company, through its directors, officers or employees, offers to provide, and, if accepted, does so provide, significant guidance and counsel concerning the management, operations or business objectives and policies of a portfolio company.

Temporary Investments

Pending investment in other types of ‘‘qualifying assets,’’ as described above, our investments may consist of cash, cash equivalents, U.S. government securities or high-quality debt securities maturing in one year or less from the time of investment, which we refer to, collectively, as temporary investments, so that 70% of our assets are qualifying assets. Typically, we will invest in U.S. Treasury bills or in repurchase agreements, provided that such agreements are fully collateralized by cash or securities issued by the U.S. government or its agencies. A repurchase agreement involves the purchase by an investor, such as us, of a specified security and the simultaneous agreement by the seller to repurchase it at an agreed-upon future date and at a price which is greater than the purchase price by an amount that reflects an agreed-upon interest rate. There is no percentage restriction on the proportion of our assets that may be invested in such repurchase agreements. However, if more than 25% of our gross assets constitute repurchase agreements from a single counterparty, we would not meet the diversification tests in order to qualify as a RIC for federal income tax purposes. Thus, we do not intend to enter into repurchase agreements with a single counterparty in excess of this limit. Our investment adviser will monitor the creditworthiness of the counterparties with which we enter into repurchase agreement transactions.

Senior Securities

We are permitted, under specified conditions, to issue multiple classes of indebtedness and one class of stock senior to our common stock if our asset coverage, as defined in the 1940 Act, is at least equal to 200% immediately after each such issuance. In addition, while any senior securities remain outstanding, we must make provisions to prohibit any distribution to our stockholders or the repurchase of such securities or shares unless we meet the applicable asset coverage ratios at the time of the distribution or repurchase. We may also borrow amounts up to 5% of the value of our gross assets for temporary or emergency purposes without regard to asset coverage. For a discussion of the risks associated with leverage, see ‘‘Risk Factors — Risks Relating to Our Business and Structure — We may borrow money, which would magnify the potential for gain or loss on amounts invested and may increase the risk of investing in us.’’

Code of Ethics

We and GSV Asset Management have each adopted a code of ethics pursuant to Rule 17j-1 under the 1940 Act and Rule 204A-1 under the Advisers Act, respectively, that establishes procedures for personal investments and restricts certain transactions by our personnel. Our codes of ethics generally do not permit investments by our employees in securities that may be purchased or held by us. You may read and copy these codes of ethics at the SEC’s Public Reference Room in Washington, D.C. You may obtain information on the operation of the Public Reference Room by calling the SEC at (202) 551-8090. In addition, each code of ethics is available on the EDGAR Database on the SEC’s Internet site athttp://www.sec.gov. You may also obtain copies of the codes of ethics, after paying a duplicating fee, by electronic request at the following Email address:publicinfo@sec.gov, or by writing the SEC’s Public Reference Section, 100 F Street, N.E., Washington, D.C. 20549.

Compliance Policies and Procedures

We and our investment adviser have adopted and implemented written policies and procedures reasonably designed to detect and prevent violation of the federal securities laws and are required to review these compliance policies and procedures annually for their adequacy and the effectiveness of their implementation and designate a chief compliance officer to be responsible for administering the policies and procedures. Stephen D. Bard currently serves as our chief compliance officer.

Sarbanes-Oxley Act of 2002

The Sarbanes-Oxley Act of 2002 imposes a wide variety of regulatory requirements on publicly-held companies and their insiders. Many of these requirements affect us. For example:

| · | pursuant to Rule 13a-14 of the Exchange Act, our chief executive officer and chief financial officer must certify the accuracy of the financial statements contained in our periodic reports; |

| · | pursuant to Item 307 of Regulation S-K, our periodic reports must disclose our conclusions about the effectiveness of our disclosure controls and procedures; |

| · | pursuant to Rule 13a-15 of the Exchange Act, our management must prepare an annual report regarding its assessment of our internal control over financial reporting beginning in 2012, and must obtain an audit of the effectiveness of internal control over financial reporting performed by our independent registered public accounting firm should we become an accelerated filer; and |

| · | pursuant to Item 308 of Regulation S-K and Rule 13a-15 of the 1934 Act, our periodic reports must disclose whether there were significant changes in our internal controls over financial reporting or in other factors that could significantly affect these controls subsequent to the date of their evaluation, including any corrective actions with regard to significant deficiencies and material weaknesses. |

The Sarbanes-Oxley Act requires us to review our current policies and procedures to determine whether we comply with the Sarbanes-Oxley Act and the regulations promulgated thereunder. We will continue to monitor our compliance with all regulations that are adopted under the Sarbanes-Oxley Act and will take actions necessary to ensure that we are in compliance therewith.

Proxy Voting Policies and Procedures

We have delegated our proxy voting responsibility to GSV Asset Management. The Proxy Voting Policies and Procedures of GSV Asset Management are set forth below. The guidelines will be reviewed periodically by GSV Asset Management and our non-interested directors, and, accordingly, are subject to change. For purposes of these Proxy Voting Policies and Procedures described below, ‘‘we,’’ ‘‘our’’ and ‘‘us’’ refers to GSV Asset Management.

Introduction