UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ended December 31, 2012

Commission file number 001-35054

Marathon Petroleum Corporation

(Exact name of registrant as specified in its charter)

| | |

| Delaware | | 27-1284632 |

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

539 South Main Street, Findlay, OH 45840-3229

(Address of principal executive offices)

(419) 422-2121

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act

| | |

Title of Each Class | | Name of Each Exchange on Which Registered |

| Common Stock, par value $.01 | | New York Stock Exchange |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer þ Accelerated filer ¨ Non-accelerated filer ¨ Smaller reporting company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No þ

The aggregate market value of Common Stock held by non-affiliates as of June 30, 2012 was approximately $15.3 billion. This amount is based on the closing price of the registrant’s Common Stock on the New York Stock Exchange on June 29, 2012. Shares of Common Stock held by executive officers and directors of the registrant are not included in the computation. The registrant, solely for the purpose of this required presentation, has deemed its directors and executive officers to be affiliates.

There were 331,433,926 shares of Marathon Petroleum Corporation Common Stock outstanding as of February 15, 2013.

Documents Incorporated By Reference

Portions of the registrant’s proxy statement relating to its 2013 Annual Meeting of Shareholders, to be filed with the Securities and Exchange Commission pursuant to Regulation 14A under the Securities Exchange Act of 1934, are incorporated by reference to the extent set forth in Part III, Items 10-14 of this report.

MARATHON PETROLEUM CORPORATION

Unless otherwise stated or the context otherwise indicates, all references in this Annual Report on Form 10-K to “MPC,” “us,” “our,” “we” or “the Company” mean Marathon Petroleum Corporation and its consolidated subsidiaries, and for periods prior to its spinoff from Marathon Oil Corporation, the Refining, Marketing & Transportation Business of Marathon Oil Corporation.

Table of Contents

Disclosures Regarding Forward-Looking Statements

This Annual Report on Form 10-K, particularly Item 1. Business, Item 1A. Risk Factors, Item 3. Legal Proceedings, Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations and Item 7A. Quantitative and Qualitative Disclosures about Market Risk, includes forward-looking statements. You can identify our forward-looking statements by words such as “anticipate,” “believe,” “estimate,” “expect,” “forecast,” “goal,” “intend,” “plan,” “predict,” “project,” “seek,” “target,” “could,” “may,” “should” or “would” or other similar expressions that convey the uncertainty of future events or outcomes. In accordance with “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995, these statements are accompanied by cautionary language identifying important factors, though not necessarily all such factors, that could cause future outcomes to differ materially from those set forth in the forward-looking statements.

Forward-looking statements include, but are not limited to, statements that relate to, or statements that are subject to risks, contingencies or uncertainties that relate to:

| | • | | future levels of revenues, refining and marketing gross margins, retail gasoline and distillate gross margins, merchandise margins, income from operations, net income or earnings per share; |

| | • | | anticipated volumes of feedstock, throughput, sales or shipments of refined products; |

| | • | | anticipated levels of regional, national and worldwide prices of crude oil and refined products; |

| | • | | anticipated levels of crude oil and refined product inventories; |

| | • | | future levels of capital, environmental or maintenance expenditures, general and administrative and other expenses; |

| | • | | the success or timing of completion of ongoing or anticipated capital or maintenance projects; |

| | • | | expectations regarding the acquisition or divestiture of assets; |

| | • | | our share repurchase program, including the timing and amounts of any common stock repurchases; |

| | • | | the effect of restructuring or reorganization of business components; |

| | • | | the potential effects of judicial or other proceedings on our business, financial condition, results of operations and cash flows; and |

| | • | | the anticipated effects of actions of third parties such as competitors, or federal, foreign, state or local regulatory authorities, or plaintiffs in litigation. |

We have based our forward-looking statements on our current expectations, estimates and projections about our industry and our company. We caution that these statements are not guarantees of future performance and you should not rely unduly on them, as they involve risks, uncertainties, and assumptions that we cannot predict. In addition, we have based many of these forward-looking statements on assumptions about future events that may prove to be inaccurate. While our management considers these assumptions to be reasonable, they are inherently subject to significant business, economic, competitive, regulatory and other risks, contingencies and uncertainties, most of which are difficult to predict and many of which are beyond our control. Accordingly, our actual results may differ materially from the future performance that we have expressed or forecast in our forward-looking statements. Differences between actual results and any future performance suggested in our forward-looking statements could result from a variety of factors, including the following:

| | • | | changes in general economic, market or business conditions; |

| | • | | domestic and foreign supplies of crude oil and other feedstocks; |

| | • | | the ability of the members of the Organization of Petroleum Exporting Countries (“OPEC”) to agree on and to influence crude oil price and production controls; |

1

| | • | | domestic and foreign supplies of refined products such as gasoline, diesel fuel, jet fuel, home heating oil and petrochemicals; |

| | • | | foreign imports of refined products; |

| | • | | refining industry overcapacity or under capacity; |

| | • | | changes in the cost or availability of third-party vessels, pipelines and other means of transportation for crude oil, feedstocks and refined products; |

| | • | | the price, availability and acceptance of alternative fuels and alternative-fuel vehicles and laws mandating such fuels or vehicles; |

| | • | | fluctuations in consumer demand for refined products, including seasonal fluctuations; |

| | • | | political and economic conditions in nations that consume refined products, including the United States, and in crude oil producing regions, including the Middle East, Africa, Canada and South America; |

| | • | | actions taken by our competitors, including pricing adjustments, expansion of retail activities, and the expansion and retirement of refining capacity in response to market conditions; |

| | • | | changes in fuel and utility costs for our facilities; |

| | • | | failure to realize the benefits projected for capital projects, or cost overruns associated with such projects; |

| | • | | the ability to successfully implement new assets and growth opportunities; |

| | • | | accidents or other unscheduled shutdowns affecting our refineries, machinery, pipelines or equipment, or those of our suppliers or customers; |

| | • | | unusual weather conditions and natural disasters, which can unforeseeably affect the price or availability of crude oil and other feedstocks and refined products; |

| | • | | acts of war, terrorism or civil unrest that could impair our ability to produce or transport refined products or receive feedstocks; |

| | • | | legislative or regulatory action, which may adversely affect our business or operations; |

| | • | | rulings, judgments or settlements and related expenses in litigation or other legal, tax or regulatory matters, including unexpected environmental remediation costs, in excess of any reserves or insurance coverage; |

| | • | | labor and material shortages; |

| | • | | the maintenance of satisfactory relationships with labor unions and joint venture partners; |

| | • | | the ability and willingness of parties with whom we have material relationships to perform their obligations to us; |

| | • | | the market price of our common stock and its impact on our share repurchase program; |

| | • | | changes in the credit ratings assigned to our debt securities and trade credit, changes in the availability of unsecured credit and changes affecting the credit markets generally; and |

| | • | | the other factors described in Item 1A. Risk Factors. |

We undertake no obligation to update any forward-looking statements except to the extent required by applicable law.

2

PART I

Item 1. Business

Overview

Marathon Petroleum Corporation (“MPC”) was incorporated in Delaware on November 9, 2009 in connection with an internal restructuring of Marathon Oil Corporation (“Marathon Oil”). On May 25, 2011, the Marathon Oil board of directors approved the spinoff of its Refining, Marketing & Transportation Business (“RM&T Business”) into an independent, publicly traded company, MPC, through the distribution of MPC common stock to the stockholders of Marathon Oil common stock. In accordance with a separation and distribution agreement between Marathon Oil and MPC, the distribution of MPC common stock was made on June 30, 2011, with Marathon Oil stockholders receiving one share of MPC common stock for every two shares of Marathon Oil common stock held (the “Spinoff”). Following the Spinoff, Marathon Oil retained no ownership interest in MPC, and each company had separate public ownership, boards of directors and management. All subsidiaries and equity method investments not contributed by Marathon Oil to MPC remained with Marathon Oil and, together with Marathon Oil, are referred to as the “Marathon Oil Companies.” On July 1, 2011, our common stock began trading “regular-way” on the New York Stock Exchange (“NYSE”) under the ticker symbol “MPC”.

We are one of the largest independent petroleum product refiners, marketers and transporters in the United States. Our operations consist of three business segments:

| | • | | Refining & Marketing—refines crude oil and other feedstocks at our seven refineries in the Gulf Coast and Midwest regions of the United States (including the recently acquired Galveston Bay refinery), purchases ethanol and refined products for resale and distributes refined products through various means, including barges, terminals and trucks that we own or operate. We sell refined products to wholesale marketing customers domestically and internationally, to buyers on the spot market, to our Speedway business segment and to dealers and jobbers who operate Marathon® retail outlets; |

| | • | | Speedway—sells transportation fuels and convenience products in the retail market in the Midwest, primarily through Speedway® convenience stores; and |

| | • | | Pipeline Transportation—transports crude oil and other feedstocks to our refineries and other locations, delivers refined products to wholesale and retail market areas and includes the aggregated operations of MPLX LP and MPC’s retained pipeline assets and investments. |

See Item 8. Financial Statements and Supplementary Data – Note 11 for operating segment and geographic financial information, which is incorporated herein by reference.

On February 1, 2013, we acquired from BP Products North America Inc. and BP Pipelines (North America) Inc. (collectively, “BP”) the 451,000 barrel per calendar day refinery in Texas City, Texas, three intrastate natural gas liquid pipelines originating at the refinery, an allocation of BP’s Colonial Pipeline Company shipper history, four light product terminals, branded-jobber marketing contract assignments for the supply of approximately 1,200 branded sites and a 1,040 megawatt electric cogeneration facility. We refer to these assets as the “Galveston Bay Refinery and Related Assets”. The operating statistics included in this section do not include these assets. See Item 8. Financial Statements and Supplementary Data – Note 26 for additional information on the acquisition of these assets.

In 2012, we formed MPLX LP (“MPLX”), a master limited partnership, to own, operate, develop and acquire pipelines and other midstream assets related to the transportation and storage of crude oil, refined products and other hydrocarbon-based products. On October 31, 2012, MPLX completed its initial public offering of 19,895,000 common units, which represented the sale by us of a 26.4 percent interest in MPLX. We own a 73.6

3

percent interest in MPLX, including the general partner interest, and we consolidate this entity for financial reporting purposes since we have a controlling financial interest. Headquartered in Findlay, Ohio, MPLX’s initial assets consist of a 51 percent general partner interest in MPLX Pipe Line Holdings LP (“Pipe Line Holdings”), which owns a network of common carrier crude oil and product pipeline systems and associated storage assets in the Midwest and Gulf Coast regions of the United States, and a 100 percent interest in a butane storage cavern in West Virginia. We own the remaining 49 percent limited partner interest in Pipe Line Holdings. The operating statistics in this section include 100 percent of these assets for all time periods presented. See Item 8. Financial Statements and Supplementary Data – Note 4 for additional information on MPLX’s initial public offering.

On December 1, 2010, we completed the sale of most of our Minnesota assets. These assets included the 74,000 barrel per calendar day St. Paul Park refinery and associated terminals, 166 convenience stores primarily branded SuperAmerica® (including six stores in Wisconsin) along with the SuperMom’s® bakery (a baked goods and sandwich supply operation) and certain associated trademarks, SuperAmerica Franchising LLC, interests in pipeline assets in Minnesota and associated inventories. We refer to these assets as the “Minnesota Assets.” The operating statistics included in this section reflect the exclusion of these assets, except as otherwise indicated. See Item 8. Financial Statements and Supplementary Data – Note 7 for additional information on the disposition of these assets.

Our Competitive Strengths

High Quality Asset Base

We believe we are the largest crude oil refiner in the Midwest and the fourth largest in the United States based on crude oil refining capacity. We own a seven-plant refinery network, including our recently acquired Galveston Bay refinery, with approximately 1.7 million barrels per calendar day (“mmbpcd”) of crude oil throughput capacity. Our refineries process a wide range of crude oils, including heavy and sour crude oils, which can generally be purchased at a discount to sweet crude, and produce transportation fuels such as gasoline and distillates, specialty chemicals and other refined products.

4

Strategic Location

The geographic locations of our refineries and our extensive midstream distribution system provide us with strategic advantages. Located in Petroleum Administration for Defense District (“PADD”) II and PADD III, which consist of states in the Midwest and the Gulf Coast regions of the United States, our refineries have the ability to procure crude oil from a variety of supply sources, including domestic, Canadian and other foreign sources, which provides us with flexibility to optimize crude supply costs. For example, geographic proximity to Canadian crude oil supply sources allows our Midwest refineries to incur lower transportation costs than competitors transporting Canadian crude oil to the Gulf Coast for refining. Our refinery locations and midstream distribution system also allow us to access export markets and to serve a broad range of key end-user markets across the United States quickly and cost-effectively.

| * | As of December 31, 2012. Excludes the Galveston Bay Refinery and Related Assets. |

Attractive Growth Opportunities through Internal Projects

We believe we have attractive growth opportunities through internal capital projects. In 2012, we completed a $2.2 billion (excluding capitalized interest) heavy oil upgrading and expansion project at our Detroit, Michigan refinery. The project enables the refinery to process additional heavy, sour crude oils, including Canadian bitumen blends, which have traded at a significant discount to light sweet crude oil, and increased the refinery’s total crude oil refining capacity by approximately 14 thousand barrels per calendar day (“mbpcd”) to 120 mbpcd.

5

We plan to evaluate projects that will extract additional value from this major investment at Detroit. At our Garyville, Louisiana refinery, we have initiated projects that we expect will increase our ultra-low-sulfur diesel (“ULSD”) production and expand our gasoline and distillates export capabilities. We also have projects underway at our Robinson, Illinois refinery to increase distillate yields and at our Catlettsburg, Kentucky refinery to improve gas oil recovery and reduce purchased feedstock volumes, thus reducing our feedstock costs. We are also increasing our capacity to process condensate from the Utica Shale region at our Canton, Ohio and Catlettsburg refineries.

Acquisition of Galveston Bay Refinery and Related Assets

Through our February 1, 2013 acquisition of the Galveston Bay Refinery and Related Assets, we added 451 mbpcd of crude oil refining capacity and have diversified and further balanced our network of refining assets. Our refining capacity is now balanced between three market areas, with 646 mbpcd of capacity in the Midwest, 531 mbpcd in Texas and 522 mbpcd in Louisiana. This acquisition provides us with the opportunity to capture synergies across our existing Gulf Coast operations, increases our refining capacity for specialty chemicals and is anticipated to enhance our ability to sell refined products into export markets.

Extensive Midstream Distribution Networks

We believe the relative scale of our transportation and distribution assets and operations distinguishes us from other refining and marketing companies. We currently own, lease or have ownership interests in approximately 8,300 miles of crude oil and products pipelines, including the approximate 100 miles of natural gas liquid pipelines recently acquired with the Galveston Bay Refinery and Related Assets. Through our ownership interests in MPLX and Pipe Line Holdings, we are one of the largest petroleum pipeline companies in the United States on the basis of total volume delivered. We also own one of the largest private domestic fleets of inland petroleum product barges and one of the largest terminal operations in the United States, as well as trucking and rail assets. We operate this system in coordination with our refining and marketing network, which enables us to optimize feedstock and raw material supplies and refined product distribution, and further allows for important economies of scale across our system.

General Partner and Sponsor of MPLX

Our investment in MPLX provides us an efficient vehicle to invest in organic projects and pursue acquisitions of midstream assets. MPLX’s strong liquidity and borrowing capacity provides us a strong foundation to execute our strategy for growing our midstream logistics business. Our role as the general partner allows us to maintain strategic control of the assets so we can continue to optimize our refinery feedstock and distribution networks.

Competitively Positioned Marketing Operations

We are one of the largest wholesale suppliers of gasoline and distillates to resellers within our market area. We have two strong retail brands: Speedway® and Marathon®. We believe our 1,464 Speedway® convenience stores, which we operate through a wholly owned subsidiary, Speedway LLC, comprise the fourth largest chain of company-owned and operated retail gasoline and convenience stores in the United States. The Marathon brand is an established motor fuel brand in the Midwest and Southeast regions of the United States, and was available through approximately 5,000 retail outlets operated by jobbers and dealers in 17 states as of December 31, 2012. In addition, as part of the acquisition of the Galveston Bay Refinery and Related Assets, we were assigned retail marketing contracts for approximately 1,200 branded retail outlets that we are in the process of converting to the Marathon brand. We believe our distribution system allows us to maximize the sales value of our products and minimize cost.

6

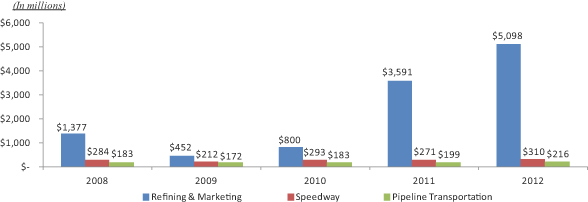

Established Track Record of Profitability and Diversified Income Stream

We have demonstrated an ability to achieve positive financial results throughout all stages of the refining cycle. We believe our business mix and strategies position us well to continue to achieve competitive financial results. As shown in the following chart, income from operations attributable to the Speedway and Pipeline Transportation segments is less sensitive to business cycles while our Refining & Marketing segment enables us to generate significant income and cash flow when market conditions are more favorable.

Marathon Petroleum Corporation

Segment Income from Operations

Strong Financial Position

As of December 31, 2012, we had $4.86 billion in cash and cash equivalents and $3.0 billion in unused committed credit facilities, excluding MPLX’s credit facility. We also had $3.36 billion of debt at year-end, which represented only 22 percent of our total capitalization. This combination of strong liquidity and manageable leverage allows us to fund our growth projects and to pursue our business strategies.

Our Business Strategies

Achieve Top-Tier Safety and Environmental Performance

We remain committed to operating our assets in a safe and reliable manner and targeting continuous improvement in our safety record across all of our operations. We have a history of safe and reliable operations, which was demonstrated with record employee and contractor safety performance across all our operations in 2012, including a world class safety record for the heavy oil upgrading and expansion project at our Detroit refinery. In addition, we remain committed to environmental stewardship by continuing to improve the efficiency of our operations while proactively meeting our regulatory requirements.

Grow Enterprise Value

We intend to grow our share price through a combination of earnings growth and return of capital to shareholders in the form of strong and growing dividends and sustained share repurchases. We have increased our quarterly dividend by 75 percent since becoming a stand-alone company in June 2011 and our board of directors has authorized share repurchases totaling $4.0 billion. We entered into two accelerated share repurchase (“ASR”) programs for a total of $1.35 billion, through which we repurchased approximately 8 percent of our outstanding common shares in 2012. After the effects of these ASR programs, $2.65 billion of the $4.0 billion total authorization is available for future repurchases.

7

Expand Midstream Business through MPLX

We expect there will be significant investment in infrastructure to connect growing North American crude oil production with existing refining assets and to move refined products to wholesale and retail marketing customers. We intend to aggressively participate in this infrastructure build out and MPLX will be the entity through which we expect to grow our midstream business. We intend to increase revenue on the MPLX network of pipeline systems through higher utilization of existing assets, by capitalizing on organic investment opportunities that may arise from the growth of MPC’s operations and from increased third-party activity in MPLX’s areas of operations. Through MPLX, we also plan to pursue acquisitions of midstream assets both within our existing geographic footprint and in new areas.

Deliver Top Quartile Refining Performance

Our refineries are well positioned to benefit from the growing crude oil and condensate production in North America, including the Bakken, Eagle Ford and Utica Shale regions, along with the Canadian oil sands. We are also well positioned to export distillates and other products as the demand continues to grow.

We intend to increase our earnings in the Refining & Marketing segment through organic investments and selective acquisitions, while maintaining financial discipline. For example, we recently completed a $2.2 billion investment (excluding capitalized interest) to upgrade and expand our Detroit refinery. This investment significantly expands our ability to process heavy crude oil at the Detroit refinery from about 20 mbpcd to 100 mbpcd. In February 2013, we closed on the 451 mbpcd Galveston Bay refinery. This acquisition increases our crude oil refining capacity by approximately 36 percent, diversifies the footprint of our refining assets, provides us with the opportunity to increase our export sales, and significantly increases our participation in the chemicals value chain. We will continue to evaluate opportunities to expand our existing asset base, with an emphasis on increasing distillates production and export capabilities.

Increase Assured Sales Volumes at our Marathon Brand and Speedway Locations

We consider assured sales as those sales we make to Marathon brand customers, our Speedway operations and to our wholesale customers with whom we have required minimum volume sales contracts. We believe having assured sales brings ratability to our distribution systems, provides a solid base to enhance our overall supply reliability and allows us to efficiently and effectively optimize our operations between our refineries, our pipelines and our terminals. The Marathon brand has been a consistent vehicle for sales volume growth in existing and contiguous markets. The acquisition of the Galveston Bay Refinery and Related Assets provides us with opportunities to further expand our market presence. Through the assignment of branded-jobber contracts representing approximately 1,200 retail outlets, we are in position to take advantage of opportunities with premier Southeast jobbers and to significantly expand our brand presence in the Southeast. We also intend to grow Speedway gasoline and distillates sales volumes through internal capital program growth projects and acquisitions that complement our existing store network.

Deliver Profitable Speedway Growth

We intend to grow Speedway’s sales and profitability by focusing on continuous improvement of existing operations, organic growth and strategic store acquisition opportunities. For example, the acquisition of 97 convenience stores in 2012 has increased Speedway’s presence in the Midwest. In addition, our industry-leading Speedy Rewards® customer loyalty program, which has over three million members, provides us with a unique competitive advantage and opportunity to increase our Speedway customer base with existing and new Speedway locations.

Utilize and Expand our High Quality Employee Workforce

We plan to utilize our high quality employee workforce by continuing to leverage our commercial skills. In addition, we plan to expand our workforce through selective hiring practices and effective training programs on safety, environmental stewardship and other professional and technical skills.

8

The above discussion contains forward-looking statements with respect to our competitive strengths and business strategies, including our share repurchase program and pursuing potential acquisitions. There can be no assurance that we will be successful, in whole or in part, in pursuing our business strategies, including our share repurchase program or pursuing potential acquisitions. Factors that could affect the share repurchase program and its timing include, but are not limited to, business conditions, availability of liquidity and the market price of our common stock. Factors that could affect pursuing potential acquisitions include, but are not limited to, our ability to implement and realize the benefits and synergies of our strategic initiatives, availability of liquidity, actions taken by competitors, regulatory approvals and operating performance. These factors, among others, could cause actual results to differ materially from those set forth in the forward-looking statements. For additional information on forward-looking statements and risks that can affect our business, see “Disclosures Regarding Forward-Looking Statements” and Item 1A. Risk Factors in this Annual Report on Form 10-K.

Refining & Marketing

Refineries

As of December 31, 2012, we owned and operated six refineries in the Gulf Coast and Midwest regions of the United States with an aggregate crude oil refining capacity of approximately 1.25 mmbpcd. The acquisition of the Galveston Bay refinery on February 1, 2013 increased our crude oil refining capacity to approximately 1.7 mmbpcd. During 2012, our refineries processed 1,195 thousand barrels per day (“mbpd”) of crude oil and 168 mbpd of other charge and blendstocks. During 2011, our refineries processed 1,177 mbpd of crude oil and 181 mbpd of other charge and blendstocks. The table below sets forth the location, crude oil refining capacity, tank storage capacity and number of tanks for each of our refineries as of December 31, 2012.

| | | | | | | | | | | | |

Refinery | | Crude Oil Refining

Capacity (mbpcd) (a) | | | Tank Shell

Capacity

(million barrels) | | | Number

of Tanks | |

| | | |

Garyville, Louisiana | | | 522 | | | | 16 | | | | 75 | |

| | | |

Catlettsburg, Kentucky | | | 240 | | | | 6 | | | | 112 | |

| | | |

Robinson, Illinois | | | 206 | | | | 6 | | | | 103 | |

| | | |

Detroit, Michigan | | | 120 | | | | 6 | | | | 86 | |

| | | |

Canton, Ohio | | | 80 | | | | 3 | | | | 73 | |

| | | |

Texas City, Texas | | | 80 | | | | 5 | | | | 60 | |

| | | | | | | | | | | | |

| | | |

Total | | | 1,248 | | | | 42 | | | | 509 | |

| | | | | | | | | | | | |

| | (a) | Refining throughput can exceed crude oil capacity due to the processing of other feedstocks in addition to crude oil and the timing of planned turnaround and major maintenance activity. | |

Our refineries include crude oil atmospheric and vacuum distillation, fluid catalytic cracking, catalytic reforming, desulfurization and sulfur recovery units. The refineries process a wide variety of crude oils and produce numerous refined products, ranging from transportation fuels, such as reformulated gasolines, blend-grade gasolines intended for blending with fuel ethanol and ULSD fuel, to heavy fuel oil and asphalt. Additionally, we manufacture aromatics, propane, propylene, cumene and sulfur. Our refineries are integrated with each other via pipelines, terminals and barges to maximize operating efficiency. The transportation links that connect our refineries allow the movement of intermediate products between refineries to optimize operations, produce higher margin products and utilize our processing capacity efficiently. For example, naphtha may be moved from Texas City to Robinson where excess reforming capacity is available. Also, by shipping intermediate products between facilities during partial refinery shutdowns, we are able to utilize processing capacity that is not directly affected by the shutdown work.

9

Garyville, Louisiana Refinery. Our Garyville, Louisiana refinery is located along the Mississippi River in southeastern Louisiana between New Orleans and Baton Rouge. The Garyville refinery is configured to process almost any grade of crude oil into products such as gasoline, distillates, fuel-grade coke, asphalt, polymer grade propylene, propane, slurry, isobutane and sulfur. An expansion project was completed in 2009 that increased Garyville’s crude oil refining capacity, making it one of the largest refineries in the U.S. Our Garyville refinery has earned designation as a U.S. Occupational Safety and Health Administration (“OSHA”) Voluntary Protection Program (“VPP”) Star site.

Catlettsburg, Kentucky Refinery. Our Catlettsburg, Kentucky refinery is located in northeastern Kentucky on the western bank of the Big Sandy River, near the confluence with the Ohio River. The Catlettsburg refinery processes sweet and sour crude oils into products such as gasoline, distillates, asphalt, heavy fuel oil, cumene, propane, propylene and petrochemicals.

Robinson, Illinois Refinery. Our Robinson, Illinois refinery is located in southeastern Illinois. The Robinson refinery processes sweet and sour crude oils into products such as multiple grades of gasoline, distillates, propane, anode-grade coke and propylene. The Robinson refinery has earned designation as an OSHA VPP Star site.

Detroit, Michigan Refinery. Our Detroit, Michigan refinery is located in southwest Detroit. It is the only petroleum refinery currently operating in Michigan. The Detroit refinery processes light sweet and heavy sour crude oils, including Canadian crude oils, into products such as gasoline, distillates, asphalt, propylene, propane, slurry and fuel-grade coke. Our Detroit refinery earned designation as a Michigan VPP Star site in 2010. In the fourth quarter of 2012, we completed a heavy oil upgrading and expansion project that enables the refinery to process up to an additional 80 mbpd of heavy sour crude oils, including Canadian bitumen blends, and increased its total crude oil refining capacity by approximately 14 mbpcd, to 120 mbpcd.

Canton, Ohio Refinery. Our Canton, Ohio refinery is located approximately 60 miles south of Cleveland, Ohio. The Canton refinery processes sweet and sour crude oils into products such as gasoline, distillates, asphalt, roofing flux, propane and slurry.

Texas City, Texas Refinery. Our Texas City, Texas refinery is located on the Texas Gulf Coast approximately 30 miles southeast of Houston, Texas. The refinery processes light sweet crude oil into products such as gasoline, chemical grade propylene, propane, slurry and aromatics. Our Texas City refinery earned designation as an OSHA VPP Star site in 2012.

As of December 31, 2012, our refineries had 24 rail loading racks and 23 truck loading racks and three of our refineries had a total of seven owned and four non-owned docks. Total throughput in 2012 was 75 mbpd for the refinery loading racks and 499 mbpd for the refinery docks.

Planned maintenance activities, or turnarounds, requiring temporary shutdown of certain refinery operating units, are periodically performed at each refinery. See Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations for additional detail.

10

Refined Product Yields

The following table sets forth our refinery production (including the St. Paul Park refinery until December 1, 2010) by product group for each of the last three years.

| | | | | | | | | | | | |

Refined Product Yields (mbpd) | | 2012 | | | 2011 | | | 2010 | |

| | | |

Gasoline | | | 738 | | | | 739 | | | | 726 | |

| | | |

Distillates | | | 433 | | | | 433 | | | | 409 | |

| | | |

Propane | | | 26 | | | | 25 | | | | 24 | |

| | | |

Feedstocks and special products | | | 109 | | | | 109 | | | | 97 | |

| | | |

Heavy fuel oil | | | 18 | | | | 21 | | | | 24 | |

| | | |

Asphalt | | | 62 | | | | 56 | | | | 76 | |

| | | | | | | | | | | | |

Total | | | 1,386 | | | | 1,383 | | | | 1,356 | |

| | | | | | | | | | | | |

Crude Oil Supply

We obtain the crude oil we refine through negotiated contracts and purchases or exchanges on the spot market. Our crude oil supply contracts are generally term contracts with market-related pricing provisions. The following table provides information on our sources of crude oil for each of the last three years (including the St. Paul Park refinery until December 1, 2010). The crude oil sourced outside of North America was acquired from various foreign national oil companies, production companies and trading companies.

| | | | | | | | | | | | |

Sources of Crude Oil Refined(mbpd) | | 2012 | | | 2011 | | | 2010 | |

| | | |

United States | | | 649 | | | | 668 | | | | 720 | |

| | | |

Canada | | | 195 | | | | 177 | | | | 115 | |

| | | |

Middle East and other international | | | 351 | | | | 332 | | | | 338 | |

| | | |

| | | | | | | | | | | | |

| | | |

Total | | | 1,195 | | | | 1,177 | | | | 1,173 | |

| | | | | | | | | | | | |

Average cost of crude oil throughput (dollars per barrel) | | | $ 102.53 | | | | $ 102.83 | | | | $ 78.57 | |

Our refineries receive crude oil and other feedstocks and distribute our refined products through a variety of channels, including pipelines, trucks, railcars, ships and barges. During 2012, we began transporting crude oil by truck from the Utica Shale region to our Canton refinery. As of December 31, 2012, we owned four transport trucks and seven trailers for this purpose.

Refined Product Marketing

We believe we are one of the largest wholesale suppliers of gasoline and distillates to resellers and consumers within our 17-state market area in the Midwest, Gulf Coast and Southeast regions of the United States. Independent retailers, wholesale customers, our Marathon brand jobbers and Speedway brand convenience stores, airlines, transportation companies and utilities comprise the core of our customer base. In addition, we sell distillates, asphalt and gasoline for export to international customers, primarily out of our Garyville refinery. Sales destined for export comprised approximately 25 percent of our distillate sales and 13 percent of our asphalt sales in 2012.

11

The following table sets forth, as a percentage of total refined product sales volume, the sales of refined products to our different customer types for the past three years (including the Minnesota Assets until December 1, 2010).

| | | | | | | | | | | | |

Refined Product Sales by Customer Type | | 2012 | | | 2011 | | | 2010 | |

| | | |

Private-brand marketers, commercial and industrial customers, including spot market | | | 72% | | | | 72% | | | | 70% | |

| | | |

Marathon-branded dealers and jobbers | | | 17% | | | | 17% | | | | 17% | |

| | | |

Speedway® convenience stores | | | 11% | | | | 11% | | | | 13% | |

The following table sets forth the approximate number of retail outlets (by state) where dealers and jobbers maintain Marathon-branded retail outlets, as of December 31, 2012.

| | | | |

State | | Approximate Number of

Marathon® Retail Outlets | |

Alabama | | | 139 | |

| |

Florida | | | 259 | |

| |

Georgia | | | 256 | |

| |

Illinois | | | 395 | |

| |

Indiana | | | 647 | |

| |

Kentucky | | | 576 | |

| |

Maryland | | | 1 | |

| |

Michigan | | | 778 | |

| |

Minnesota | | | 84 | |

| |

North Carolina | | | 311 | |

| |

Ohio | | | 860 | |

| |

Pennsylvania | | | 40 | |

| |

South Carolina | | | 128 | |

| |

Tennessee | | | 173 | |

| |

Virginia | | | 136 | |

| |

West Virginia | | | 111 | |

| |

Wisconsin | | | 70 | |

| | | | |

Total | | | 4,964 | |

| | | | |

The following table sets forth our refined products sales volumes by product group and our average sales price for each of the last three years (including the Minnesota Assets until December 1, 2010).

| | | | | | | | | | | | |

Refined Product Sales(mbpd) | | 2012 | | | 2011 | | | 2010 | |

Gasoline | | | 916 | | | | 908 | | | | 912 | |

| | | |

Distillates | | | 463 | | | | 459 | | | | 434 | |

| | | |

Propane | | | 27 | | | | 25 | | | | 24 | |

| | | |

Feedstocks and special products | | | 112 | | | | 111 | | | | 103 | |

| | | |

Heavy fuel oil | | | 19 | | | | 19 | | | | 23 | |

| | | |

Asphalt | | | 62 | | | | 59 | | | | 77 | |

| | | | | | | | | | | | |

Total | | | 1,599 | | | | 1,581 | | | | 1,573 | |

| | | | | | | | | | | | |

| | | |

Average sales price, including consumer excise taxes (dollars per barrel) | | | $ 126.13 | | | | $ 123.14 | | | | $ 94.13 | |

Gasoline and Distillates. We sell gasoline, gasoline blendstocks and distillates (including No. 1 and No. 2 fuel oils, kerosene, jet fuel and diesel fuel) to wholesale customers, Marathon-branded jobbers and dealers and our

12

Speedway® convenience stores in the Midwest, Gulf Coast and Southeast regions of the United States and on the spot market. In addition, we sell diesel fuel for export to international customers. We sold 57 percent of our gasoline sales volumes and 89 percent of our distillates sales volumes on a wholesale or spot market basis in 2012. The demand for gasoline and distillates is seasonal in many of our markets, with demand typically at its highest levels during the summer months.

We have blended ethanol into gasoline for more than 20 years and began expanding our blending program in 2007, in part due to federal regulations that require us to use specified volumes of renewable fuels. Ethanol volumes sold in blended gasoline (including the Minnesota Assets until December 1, 2010) were 68 mbpd in 2012, 70 mbpd in 2011 and 68 mbpd in 2010. The future expansion or contraction of our ethanol blending program will be driven by the economics of the ethanol supply and by government regulations. We sell reformulated gasoline, which is also blended with ethanol, in parts of our marketing territory, including Kentucky, Illinois, Indiana, Wisconsin, Pennsylvania and Texas. We also sell biodiesel-blended diesel fuel in Kentucky, West Virginia, Illinois, Ohio, North Carolina, Florida, Virginia, Pennsylvania, Georgia, Minnesota and Tennessee.

We hold a 36 percent interest in an entity that owns and operates a 110-million-gallon-per-year ethanol production facility in Clymers, Indiana. We also own a 50 percent interest in an entity that owns a 110-million-gallon-per-year ethanol production facility in Greenville, Ohio. Both of these facilities are managed by a co-owner.

Propane. We produce propane at all of our refineries. Propane is primarily used for home heating and cooking, as a feedstock within the petrochemical industry, for grain drying and as a fuel for trucks and other vehicles. Our propane sales are typically split evenly between the home heating market and industrial consumers.

Feedstocks and Special Products. We are a producer and marketer of feedstocks and specialty products. Product availability varies by refinery and includes propylene, cumene, molten sulfur, toluene, benzene, xylene and dilute naphthalene oil. We market all products domestically to customers in the chemical, agricultural and fuel blending industries. In addition, we produce fuel-grade coke at our Garyville and Detroit refineries, which is used for power generation and in miscellaneous industrial applications, and anode-grade coke at our Robinson refinery, which is used to make carbon anodes for the aluminum smelting industry.

Heavy Fuel Oil. We produce and market heavy residual fuel oil or related components at all of our refineries. Heavy residual fuel oil is primarily used in the utility and ship bunkering (fuel) industries, though there are other more specialized uses of the product.

Asphalt. We have refinery-based asphalt production capacity of up to 98 mbpcd. We market asphalt through 31 owned or leased terminals throughout the Midwest and Southeast. We have a broad customer base, including asphalt-paving contractors, government entities (states, counties, cities and townships) and asphalt roofing shingle manufacturers. We sell asphalt in the domestic and export wholesale markets via rail, barge and vessel. We also produce asphalt cements, polymer modified asphalt, emulsified asphalt and industrial asphalts.

13

Refined Product Distribution

As of December 31, 2012, we owned and operated 61 light product and 21 asphalt terminals. The acquisition of the Galveston Bay Refinery and Related Assets on February 1, 2013 increased our number of owned and operated light product terminals to 65. Our light product and asphalt terminals averaged 1,278 mbpd and 31 mbpd of throughput in 2012, respectively. In addition, we distribute refined products through one leased light product terminal, two light product terminals in which we have partial ownership interests but do not operate and approximately 61 third-party light product and 10 third-party asphalt terminals in our market area. The following table sets forth additional details about our owned and operated terminals at December 31, 2012.

| | | | | | | | | | | | | | | | |

Owned and Operated Terminals | | Number of

Terminals | | | Tank Shell

Capacity

(thousand barrels) | | | Number

of Tanks | | | Number of

Loading

Lanes | |

Light Product Terminals: | | | | | | | | | | | | | | | | |

Alabama | | | 2 | | | | 404 | | | | 20 | | | | 4 | |

Florida | | | 3 | | | | 1,942 | | | | 54 | | | | 17 | |

Georgia | | | 4 | | | | 896 | | | | 38 | | | | 9 | |

Illinois | | | 4 | | | | 1,165 | | | | 45 | | | | 14 | |

Indiana | | | 7 | | | | 3,021 | | | | 79 | | | | 19 | |

Kentucky | | | 6 | | | | 2,266 | | | | 64 | | | | 24 | |

Louisiana | | | 1 | | | | 89 | | | | 8 | | | | 2 | |

Michigan | | | 9 | | | | 2,191 | | | | 85 | | | | 28 | |

North Carolina | | | 2 | | | | 451 | | | | 17 | | | | 6 | |

Ohio | | | 13 | | | | 4,114 | | | | 164 | | | | 33 | |

Pennsylvania | | | 1 | | | | 336 | | | | 10 | | | | 2 | |

South Carolina | | | 1 | | | | 344 | | | | 13 | | | | 3 | |

Tennessee | | | 3 | | | | 727 | | | | 29 | | | | 9 | |

Virginia | | | 1 | | | | 276 | | | | 12 | | | | 2 | |

West Virginia | | | 2 | | | | 149 | | | | 10 | | | | 2 | |

Wisconsin | | | 2 | | | | 814 | | | | 20 | | | | 7 | |

| | | | | | | | | | | | | | | | |

Subtotal light product terminals | | | 61 | | | | 19,185 | | | | 668 | | | | 181 | |

| | | | |

Asphalt Terminals: | | | | | | | | | | | | | | | | |

Florida | | | 1 | | | | 254 | | | | 4 | | | | 3 | |

Illinois | | | 2 | | | | 100 | | | | 9 | | | | 6 | |

Indiana | | | 3 | | | | 703 | | | | 18 | | | | 9 | |

Kentucky | | | 4 | | | | 567 | | | | 34 | | | | 14 | |

Louisiana | | | 1 | | | | 52 | | | | 8 | | | | 2 | |

Michigan | | | 1 | | | | 12 | | | | 2 | | | | 8 | |

New York | | | 1 | | | | 112 | | | | 3 | | | | 3 | |

Ohio | | | 4 | | | | 1,919 | | | | 46 | | | | 10 | |

Pennsylvania | | | 1 | | | | 469 | | | | 14 | | | | 8 | |

Tennessee | | | 3 | | | | 951 | | | | 34 | | | | 12 | |

| | | | | | | | | | | | | | | | |

Subtotal asphalt terminals | | | 21 | | | | 5,139 | | | | 172 | | | | 75 | |

| | | | | | | | | | | | | | | | |

Total owned and operated terminals | | | 82 | | | | 24,324 | | | | 840 | | | | 256 | |

| | | | | | | | | | | | | | | | |

14

As of December 31, 2012, our marine transportation operations included 15 towboats, as well as 177 owned and 14 leased barges that transport refined products on the Ohio, Mississippi and Illinois rivers and their tributaries and inter-coastal waterways. The following table sets forth additional details about our towboats and barges.

| | | | | | | | |

Class of Equipment | | Number

in Class | | | Capacity

(thousand barrels) | |

Inland tank barges:(a) | | | | | | | | |

Less than 25,000 barrels | | | 61 | | | | 858 | |

25,000 barrels and over | | | 130 | | | | 3,784 | |

| | | | | | | | |

Total | | | 191 | | | | 4,642 | |

| | | | | | | | |

Inland towboats: | | | | | | | | |

Less than 2000 horsepower | | | 2 | | | | | |

2000 horsepower and over | | | 13 | | | | | |

| | | | | | | | |

Total | | | 15 | | | | | |

| | | | | | | | |

| | (a) | All of our barges are double-hulled. |

As of December 31, 2012, we owned 142 transport trucks and 150 trailers with an aggregate capacity of 1.4 million gallons for the movement of refined products. In addition, we had 1,944 leased and 27 owned railcars of various sizes and capacities for movement and storage of refined products. The following table sets forth additional details about our railcars.

| | | | | | | | | | | | | | | | |

| | | Number of Railcars | | | | |

Class of Equipment | | Owned | | | Leased | | | Total | | | Capacity per Railcar | |

General service tank cars | | | - | | | | 694 | | | | 694 | | | | 20,000-30,000 gallons | |

High pressure tank cars | | | - | | | | 1,041 | | | | 1,041 | | | | 33,500 gallons | |

Open-top hoppers | | | 27 | | | | 209 | | | | 236 | | | | 4,000 cubic feet | |

| | | | | | | | | | | | | | | | |

| | | 27 | | | | 1,944 | | | | 1,971 | | | | | |

| | | | | | | | | | | | | | | | |

Galveston Bay Refinery and Related Assets

Our Galveston Bay refinery, which we acquired on February 1, 2013, is located on the Texas Gulf Coast approximately 30 miles southeast of Houston, Texas. The refinery has a crude oil refining capacity of 451 mbpcd and storage tank shell capacity of approximately 16 million barrels. The refinery can process almost any grade of crude oil into products such as gasoline, distillates, fuel-grade coke, slurry, propylene, propane and aromatics. Our cogeneration facility, which supplies the Galveston Bay refinery, has 1,040 megawatts of electrical production capacity and can produce 4.6 million pounds of steam per hour.

The four light product terminals we acquired are located in Nashville, Tennessee; Charlotte, North Carolina; Selma, North Carolina and Jacksonville, Florida. The terminals have 42 storage tanks with aggregate shell capacity of 2.27 million barrels and 19 loading lanes.

The assignment of branded-jobber contracts represents approximately 1,200 retail outlets, primarily in Florida, Mississippi, Tennessee and Alabama.

Speedway

Our Speedway segment sells gasoline and merchandise through convenience stores that it owns and operates, primarily under the Speedway brand. Diesel fuel is also sold at the vast majority of these convenience stores. Speedway brand convenience stores offer a wide variety of merchandise, such as prepared foods, beverages and non-food items, including a number of private-label items. Speedy Rewards™, an industry-leading customer loyalty program, has achieved significant customer engagement over the years since its introduction in 2004. The average monthly active membership in 2012 was more than three million customers.

15

As of December 31, 2012, Speedway had 1,464 convenience stores in seven states. Revenues from sales of merchandise (including sales until December 1, 2010 from convenience stores we sold as part of the Minnesota Assets) totaled $3.06 billion in 2012, $2.92 billion in 2011 and $3.20 billion in 2010. The demand for gasoline is seasonal, with the highest demand usually occurring during the summer driving season. Margins from the sale of merchandise tend to be less volatile than margins from the retail sale of gasoline and diesel fuel.

As of December 31, 2012, the Speedway segment’s convenience stores were located in the following states:

| | | | |

State | | Number of

Convenience Stores | |

Illinois | | | 107 | |

Indiana | | | 310 | |

Kentucky | | | 140 | |

Michigan | | | 301 | |

Ohio | | | 483 | |

West Virginia | | | 60 | |

Wisconsin | | | 63 | |

| | | | |

Total | | | 1,464 | |

| | | | |

Harris Interactive’s annual Harris Poll EquiTrend® brand equity study named Speedway the number one convenience store brand with consumers nationally for 2012 and the number one gasoline brand with consumers for each of the prior three years. For 2011, Speedway was presented with a Convenience Retailing Award from CSP Information Group, Inc., for consumer experience provided by the Speedy Rewards™ program.

Pipeline Transportation

As of December 31, 2012, we owned, leased or had ownership interests in approximately 8,200 miles of crude oil and products pipelines, of which approximately 2,900 miles are owned through our investments in MPLX and Pipe Line Holdings. The acquisition of approximately 100 miles of natural gas liquid pipelines on February 1, 2013 increased the total mile count to approximately 8,300 miles.

MPLX

In 2012, we formed MPLX, a master limited partnership, to own, operate, develop and acquire pipelines and other midstream assets related to the transportation and storage of crude oil, refined products and other hydrocarbon-based products. On October 31, 2012, MPLX completed its initial public offering. We own a 73.6 percent interest in MPLX, including the general partner interest. MPLX’s assets consist of a 51 percent general partner interest in Pipe Line Holdings, which owns common carrier pipeline systems through Marathon Pipe Line LLC (“MPL”) and Ohio River Pipe Line LLC (“ORPL”), and a 100 percent interest in a one million barrel butane storage cavern in West Virginia. In addition, we own the remaining 49 percent limited partner interest in Pipe Line Holdings. As of December 31, 2012, Pipe Line Holdings, through MPL and ORPL, owned or leased and operated 1,004 miles of common carrier crude oil lines and 1,902 miles of common carrier products lines comprising 30 systems located in nine states and four tank farms in Illinois and Indiana with available storage capacity of 3.29 million barrels that is committed to MPC.

16

The table below sets forth additional detail regarding the pipeline systems and storage assets we own through Pipe Line Holdings and MPLX as of December 31, 2012.

| | | | | | | | | | | | | | | | |

Pipeline System or Storage Asset | | Origin | | Destination | | Diameter

(inches) | | Length

(miles) | | | Capacity (a) | | | Associated MPC refinery |

Crude oil pipeline systems (mbpd): | | | | | | | | | | | | | | | | |

Patoka, IL to Lima, OH crude system | | Patoka, IL | | Lima, OH | | 20”-22” | | | 302 | | | | 290 | | | Detroit, Canton |

Catlettsburg, KY and Robinson, IL crude system | | Patoka, IL | | Catlettsburg, KY &

Robinson, IL | | 20”-24” | | | 484 | | | | 481 | | | Catlettsburg, Robinson |

Detroit, MI crude system (b) | | Samaria &

Romulus, MI | | Detroit, MI | | 16” | | | 61 | | | | 320 | | | Detroit |

Wood River, IL to Patoka, IL crude system (b) | | Wood River &

Roxana, IL | | Patoka, IL | | 12”-22” | | | 115 | | | | 307 | | | All Midwest refineries |

Inactive pipelines | | | | | | | | | 42 | | | | N/A | | | |

| | | | | | | | | | | | | | | | |

Total | | | | | | | | | 1,004 | | | | 1,398 | | | |

| | | | | | | | | | | | | | | | |

Products pipeline systems (mbpd): | | | | | | | | | | | | | | | | |

Garyville, LA products system | | Garyville, LA | | Zachary, LA | | 20”-36” | | | 72 | | | | 389 | | | Garyville |

Texas City, TX products system | | Texas City, TX | | Pasadena, TX | | 16”-36” | | | 42 | | | | 215 | | | Texas City |

ORPL products system | | Various | | Various | | 6”-14” | | | 518 | | | | 242 | | | Catlettsburg, Canton |

Robinson, IL products system (b) | | Various | | Various | | 10”-16” | | | 1,173 | | | | 545 | | | Robinson |

Louisville, KY Airport products system | | Louisville, KY | | Louisville, KY | | 6”-8” | | | 14 | | | | 29 | | | Robinson |

Inactive pipelines | | | | | | | | | 83 | | | | N/A | | | |

| | | | | | | | | | | | | | | | |

Total | | | | | | | | | 1,902 | | | | 1,420 | | | |

| | | | | | | | | | | | | | | | |

Wood River, IL barge dock (mbpd) | | | | | | | | | | | | | 80 | | | Garyville |

Storage assets (thousand barrels): | | | | | | | | | | | | | | | | |

Neal, WV butane cavern (c) | | | | | | | | | | | | | 1,000 | | | Catlettsburg |

Patoka, IL tank farm | | | | | | | | | | | | | 1,386 | | | All Midwest refineries |

Wood River, IL tank farm | | | | | | | | | | | | | 419 | | | All Midwest refineries |

Martinsville, IL tank farm | | | | | | | | | | | | | 738 | | | Detroit, Canton |

Lebanon, IN tank farm | | | | | | | | | | | | | 750 | | | Detroit, Canton |

| | | | | | | | | | | | | | | | |

Total | | | | | | | | | | | | | 4,293 | | | |

| | | | | | | | | | | | | | | | |

| (a) | All capacities reflect 100 percent of the pipeline systems’ and barge dock’s average capacity in thousands of barrels per day and 100 percent of the available storage capacity of our butane cavern and tank farms in thousand of barrels. Crude oil capacity is based on light crude oil barrels. |

| (b) | Includes pipelines leased from third parties. |

| (c) | The Neal, WV butane cavern is 100 percent owned by MPLX. |

The Pipe Line Holdings common carrier pipeline network is one of the largest petroleum pipeline systems in the United States, based on total volume delivered. Third parties generated 14 percent of the crude oil and refined product shipments on these common carrier pipelines in 2012, excluding volumes shipped by MPC under joint tariffs with third parties. These common carrier pipelines transported the volumes shown in the following table for each of the last three years.

| | | | | | | | | | | | |

Pipeline Throughput(mbpd) (a)(b) | | 2012 | | | 2011 | | | 2010 | |

Crude oil pipelines | | | 1,029 | | | | 993 | | | | 883 | |

Refined products pipelines | | | 980 | | | | 1,031 | | | | 968 | |

| | | | | | | | | | | | |

Total | | | 2,009 | | | | 2,024 | | | | 1,851 | |

| | | | | | | | | | | | |

| | (a) | MPLX volumes reported in MPLX’s prospectus related to its initial public offering included our undivided joint interest crude oil pipeline systems, which were not contributed to MPLX. The undivided joint interest volumes are not included above. |

| | (b) | Volumes represent 100 percent of the throughput through these pipelines. |

17

MPC-Retained Assets and Investments

In addition to our 49% ownership interest in Pipe Line Holdings, we retained ownership interests in several crude oil and products pipeline systems and pipeline companies. As of December 31, 2012, we owned undivided joint interests in the following common carrier crude oil pipeline systems.

| | | | | | | | | | | | | | | | |

Pipeline System | | Origin | | Destination | | Diameter

(inches) | | Length

(miles) | | | Ownership

Interest | | | Operated

by MPL |

Capline | | St. James, LA | | Patoka, IL | | 40” | | | 635 | | | | 33 | % | | No |

Maumee | | Lima, OH | | Samaria, MI | | 22” | | | 95 | | | | 26 | % | | No |

| | | | | | | | | | | | | | | | |

Total | | | | | | | | | 730 | | | | | | | |

| | | | | | | | | | | | | | | | |

MPC consolidated volumes transported through our common carrier pipelines, which include MPLX and our undivided joint interests, are shown in the following table for each of the last three years.

| | | | | | | | | | | | |

MPC Consolidated Pipeline Throughput(mbpd) | | 2012 | | | 2011 | | | 2010 | |

Crude oil pipelines | | | 1,190 | | | | 1,184 | | | | 1,204 | |

Refined products pipelines | | | 980 | | | | 1,031 | | | | 968 | |

| | | | | | | | | | | | |

Total | | | 2,170 | | | | 2,215 | | | | 2,172 | |

| | | | | | | | | | | | |

As of December 31, 2012, we had partial ownership interests in the following pipeline companies.

| | | | | | | | | | | | | | | | |

Pipeline Company | | Origin | | Destination | | Diameter

(inches) | | Length

(miles) | | | Ownership

Interest | | | Operated

by MPL |

Crude oil pipeline companies: | | | | | | | | | | | | | | | | |

LOCAP LLC | | Clovelly, LA | | St. James, LA | | 48” | | | 57 | | | | 59 | % | | No |

LOOP LLC | | Offshore Gulf of Mexico | | Clovelly, LA | | 48” | | | 48 | | | | 51 | % | | No |

| | | | | | | | | | | | | | | | |

Total | | | | | | | | | 105 | | | | | | | |

| | | | | | | | | | | | | | | | |

Products pipeline companies: | | | | | | | | | | | | | | | | |

Centennial Pipeline LLC (a) | | Beaumont, TX | | Bourbon, IL | | 24”-26” | | | 795 | | | | 50 | % | | Yes |

Explorer Pipeline Company | | Lake Charles, LA | | Hammond, IN | | 12”-28” | | | 1,883 | | | | 17 | % | | No |

Muskegon Pipeline LLC | | Griffith, IN | | Muskegon, MI | | 10” | | | 170 | | | | 60 | % | | Yes |

Wolverine Pipe Line Company | | Chicago, IL | | Bay City &

Ferrysburg, MI | | 6”-18” | | | 743 | | | | 6 | % | | No |

| | | | | | | | | | | | | | | | |

Total | | | | | | | | | 3,591 | | | | | | | |

| | | | | | | | | | | | | | | | |

| (a) | Includes 48 miles of inactive pipeline. |

18

We also own 183 miles of private crude oil pipelines and 658 miles of private refined products pipelines that are operated by MPL for the benefit of our Refining & Marketing segment on a cost recovery basis. The following table provides additional information on these assets.

| | | | | | | | | | |

Private Pipeline Systems | | Diameter

(inches) | | Length

(miles) | | | Capacity

(mbpd) | |

Crude oil pipeline systems: | | | | | | | | | | |

Lima, OH to Canton, OH | | 12”-16” | | | 153 | | | | 84 | |

St. James, LA to Garyville, LA | | 30” | | | 20 | | | | 620 | |

Other | | | | | 2 | | | | 15 | |

Inactive pipelines | | | | | 8 | | | | N/A | |

| | | | | | | | | | |

Total | | | | | 183 | | | | 719 | |

| | | | | | | | | | |

Products pipeline systems: | | | | | | | | | | |

Robinson, IL to Lima, OH | | 8” | | | 250 | | | | 18 | |

Louisville, KY to Lexington, KY (a) | | 8” | | | 87 | | | | 37 | |

Woodhaven, MI to Detroit, MI | | 4” | | | 26 | | | | 11 | |

Illinois pipeline systems | | 4”-8” | | | 118 | | | | 32 | |

Ohio pipeline systems | | 4”-6” | | | 61 | | | | 39 | |

Inactive pipelines | | | | | 116 | | | | N/A | |

| | | | | | | | | | |

Total | | | | | 658 | | | | 137 | |

| | | | | | | | | | |

| | (a) | We own a 65 percent undivided joint interest in the Louisville, KY to Lexington, KY system. |

As of December 31, 2012, we owned 60 private tanks with storage capacity of approximately 6.5 million barrels, which are located along MPLX pipelines.

Galveston Bay Refinery and Related Assets

As part of the February 1, 2013 acquisition of the Galveston Bay Refinery and Related Assets, we acquired approximately 100 miles of natural gas liquid pipelines consisting of three intrastate systems originating at the Galveston Bay refinery. The pipelines are each eight inches in diameter and have a total capacity of approximately 40 mbpd.

Competition, Market Conditions and Seasonality

The downstream petroleum business is highly competitive, particularly with regard to accessing crude oil and other feedstock supply and the marketing of refined products. We compete with a large number of other companies to acquire crude oil for refinery processing and in the distribution and marketing of a full array of petroleum products. Based upon the “The Oil & Gas Journal 2012 Worldwide Refinery Survey” and our acquisition of the Galveston Bay refinery on February 1, 2013, we ranked fourth among U.S. petroleum companies on the basis of U.S. crude oil refining capacity as of February 1, 2013. We compete in four distinct markets for the sale of refined products—wholesale, spot, branded and retail distribution. We believe we compete with about 60 companies in the sale of refined products to wholesale marketing customers, including private-brand marketers and large commercial and industrial consumers; about 80 companies in the sale of refined products in the spot market; 11 refiners or marketers in the supply of refined products to refiner-branded dealers and jobbers; and approximately 250 retailers in the retail sale of refined products. In addition, we compete with producers and marketers in other industries that supply alternative forms of energy and fuels to satisfy the requirements of our industrial, commercial and individual consumers. We do not produce any of the crude oil we refine.

19

We also face strong competition for sales of retail gasoline, diesel fuel and merchandise. Our competitors include service stations and convenience stores operated by fully integrated major oil companies and their dealers and jobbers and other well-recognized national or regional convenience stores and travel centers, often selling gasoline, diesel fuel and merchandise at aggressively competitive prices. Non-traditional retailers, such as supermarkets, club stores and mass merchants, have affected the convenience store industry with their entrance into the retail transportation fuel business. Energy Analysts International, Inc. estimates such retailers had 12.4 percent of the U.S. gasoline market in 2012.

Our pipeline transportation operations are highly regulated, which affects the rates that our common carrier pipelines can charge for transportation services and the return we obtain from such pipelines.

Market conditions in the oil and gas industry are cyclical and subject to global economic and political events and new and changing governmental regulations. Our operating results are affected by price changes in crude oil, natural gas and refined products, as well as changes in competitive conditions in the markets we serve. Price differentials between sweet and sour crude oil also affect our operating results.

Demand for gasoline, diesel fuel and asphalt is higher during the spring and summer months than during the winter months in most of our markets, primarily due to seasonal increases in highway traffic and construction. As a result, the operating results for each of our segments for the first and fourth quarters are generally lower than for those in the second and third quarters of each calendar year.

Environmental Matters

Our management is responsible for ensuring that our operating organizations maintain environmental compliance systems that support and foster our compliance with applicable laws and regulations, and for reviewing our overall performance associated with various environmental compliance programs. We also have a Corporate Emergency Response Team, composed primarily of senior management, which oversees our response to any major environmental or other emergency incident involving us or any of our facilities.

We believe it is likely that the scientific and political attention to issues concerning the extent and causes of climate change will continue, with the potential for further regulations that could affect our operations. Currently, various legislative and regulatory measures to address greenhouse gases are in various phases of review, discussion or implementation. The cost to comply with these laws and regulations cannot be estimated at this time, but could be significant. For additional information, see Item 1A. Risk Factors. We estimate and publicly report greenhouse gas emissions from our operations and products we produce. Additionally, we continuously strive to improve operational and energy efficiencies through resource and energy conservation where practicable and cost effective.

Our operations are also subject to numerous other laws and regulations relating to the protection of the environment. These environmental laws and regulations include, among others, the Clean Air Act with respect to air emissions, the Clean Water Act with respect to water discharges, the Resource Conservation and Recovery Act (“RCRA”) with respect to solid and hazardous waste treatment, storage and disposal, the Comprehensive Environmental Response, Compensation, and Liability Act (“CERCLA”) with respect to releases and remediation of hazardous substances and the Oil Pollution Act of 1990 (“OPA-90”) with respect to oil pollution and response. In addition, many states where we operate have similar laws. New laws are being enacted and regulations are being adopted by various regulatory agencies on a continuing basis, and the costs of compliance with any new laws and regulations are very difficult to estimate at this time.

For a discussion of environmental capital expenditures and costs of compliance for air, water, solid waste and remediation, see Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Environmental Matters and Compliance Costs.

20

Air

We are subject to substantial requirements in connection with air emissions from our operations. The U.S. Environmental Protection Agency (“EPA”) issued an “endangerment finding” in 2009 that greenhouse gas emissions contribute to air pollution that endangers public health and welfare. Related to this endangerment finding, in April 2010, the EPA finalized a greenhouse gas emissions standard for mobile sources (cars and light duty vehicles). The endangerment finding along with the mobile source standard and the EPA’s determination that greenhouse gases are subject to regulation under the Clean Air Act, and the EPA’s so-called “tailoring rule” led to permitting of larger stationary sources of greenhouse gas emissions, including refineries. Legal challenges filed against these EPA actions were overruled by the D.C. Circuit Court of Appeals, but several parties will seek further review by the U.S. Supreme Court. We also expect refinery-specific New Source Performance Standards will be proposed in 2013. Congress may again consider legislation on greenhouse gas emissions or a carbon tax. Private parties have sued utilities and other emitters of greenhouse gas emissions, but we have not been named in any of those lawsuits. Private-party litigation is also pending against federal and certain state governmental entities seeking additional greenhouse gas emission reductions beyond those currently being undertaken. Although there may be an adverse financial impact (including compliance costs, potential permitting delays and potential reduced demand for certain refined products made from crude oil) associated with any legislation, regulation, litigation or other action, the extent and magnitude of that impact cannot be reasonably estimated due to the uncertainty regarding the additional measures and how they will be implemented.

Of particular significance to our refining operations were EPA Mobile Source Air Toxics II (“MSAT II”) regulations that require reduced benzene levels in refined products. We spent approximately $620 million over a four-year period to complete all MSAT II projects, and all units were in operation as of December 31, 2011.

The EPA has reviewed and has revised or will propose to revise the National Ambient Air Quality Standards (“NAAQS”) for criteria air pollutants. The NAAQS are subject to multiple court challenges, making final compliance plans uncertain. The EPA promulgated a revised ozone standard in March 2008 and commenced a multi-year process to develop the implementing rules required by the Clean Air Act. In 2013, the EPA is expected to propose a stricter ozone standard as part of EPA’s periodic review of that standard. Also, in 2010, the EPA adopted new short-term standards for nitrogen dioxide and sulfur dioxide, and in December 2012 issued a more stringent fine particulate matter (PM 2.5) standard. We cannot reasonably estimate the final financial impact of these proposed and revised NAAQS standards until the standards are finalized, individual state implementing rules are established and judicial challenges are resolved.

In December 2012, the EPA signed final reconsideration amendments to the Boiler and Process Heater Maximum Achievable Control Technology (“Boiler MACT”) rule. This rule had been finalized in March 2011 with work practice standards that are applicable to refinery and natural gas fired equipment. While EPA retained the work practice standards for most refinery equipment, we are currently evaluating the financial impact of the Boiler MACT rule as a result of the reconsideration amendments. Further changes to the rule may occur because of potential litigation.

In 2013, the EPA is expected to propose a Refinery Sector Rule. This rule may require various refinery unit modifications, additional controls, lower emission standards and ambient air monitoring. We cannot reasonably estimate the financial impact of this rule until it is proposed and finalized.

Water

We maintain numerous discharge permits as required under the National Pollutant Discharge Elimination System program of the Clean Water Act and have implemented systems to oversee our compliance efforts. In addition, we are regulated under OPA-90, which among other requirements, requires the owner or operator of a tank vessel or a facility to maintain an emergency plan to respond to releases of oil or hazardous substances. Also, in case of any such release, OPA-90 requires the responsible company to pay resulting removal costs and damages. OPA-90 also

21

provides for civil penalties and imposes criminal sanctions for violations of its provisions. We have implemented emergency oil response plans for all of our components and facilities covered by OPA-90 and we have established Spill Prevention, Control and Countermeasures plans for all facilities subject to such requirements.

Additionally, OPA-90 requires that new tank vessels entering or operating in U.S. waters be double-hulled and that existing tank vessels that are not double-hulled be retrofitted or removed from U.S. service, according to a phase-out schedule. All of the barges used for river transport of our raw materials and refined products meet the double-hulled requirements of OPA-90. We operate facilities at which spills of oil and hazardous substances could occur. Some coastal states in which we operate have passed state laws similar to OPA-90, but with expanded liability provisions, including provisions for cargo owner responsibility as well as ship owner and operator responsibility.

Solid Waste

We continue to seek methods to minimize the generation of hazardous wastes in our operations. RCRA establishes standards for the management of solid and hazardous wastes. Besides affecting waste disposal practices, RCRA also addresses the environmental effects of certain past waste disposal operations, the recycling of wastes and the regulation of underground storage tanks (“USTs”) containing regulated substances. We have ongoing RCRA treatment and disposal operations at one of our facilities and primarily utilize offsite third-party treatment and disposal facilities. Ongoing RCRA-related costs, however, are not expected to be material to our results of operations or cash flows.

Remediation

We own or operate, or have owned or operated, certain retail outlets where, during the normal course of operations, releases of refined products from USTs have occurred. Federal and state laws require that contamination caused by such releases at these sites be assessed and remediated to meet applicable standards. The enforcement of the UST regulations under RCRA has been delegated to the states, which administer their own UST programs. Our obligation to remediate such contamination varies, depending on the extent of the releases and the stringency of the laws and regulations of the states in which we operate. A portion of these remediation costs may be recoverable from the appropriate state UST reimbursement funds once the applicable deductibles have been satisfied. We also have ongoing remediation projects at a number of our current and former refinery, terminal and pipeline locations. Penalties or other sanctions may be imposed for noncompliance.