| ATTORNEYS AT LAW 777 East Wisconsin Avenue Milwaukee, WI 53202-5306 414.271.2400 TEL 414.297.4900 FAX www.foley.com

WRITER’S DIRECT LINE pfetzer@foley.com EMAIL |

December 16, 2015

Mr. David L. Orlic

Special Counsel

Office of Mergers and Acquisitions

Division of Corporation Finance

U.S. Securities and Exchange Commission

100 F Street NE

Washington, DC 20549

| Re: | Arotech Corporation | |

| Definitive Additional Solicitating Material on Schedule 14A | ||

| Filed December 10, 2015 by Ephraim Fields et al. | ||

| File No. 000-23336 |

Dear Mr. Orlic:

On behalf of our client, Mr. Ephraim Fields (“Mr. Fields”), set forth below are Mr. Fields’ responses to the December 10, 2015 comments of the Staff (the “Staff”) of the Securities and Exchange Commission (the “Commission”) on the Schedule 14A referenced above (the “Schedule 14A”). The numbered items set forth below repeat (in bold italics) the comments of the Staff, and following such comments are Mr. Fields’ responses (in regular type).

General

| 1. | Please provide support for the following assertions: |

Response: In future filings, Mr. Fields will ensure that support for such statements is more fully contained in the filing.

| · | The inherent value of the company’s assets significantly exceeds the company’s current stock price |

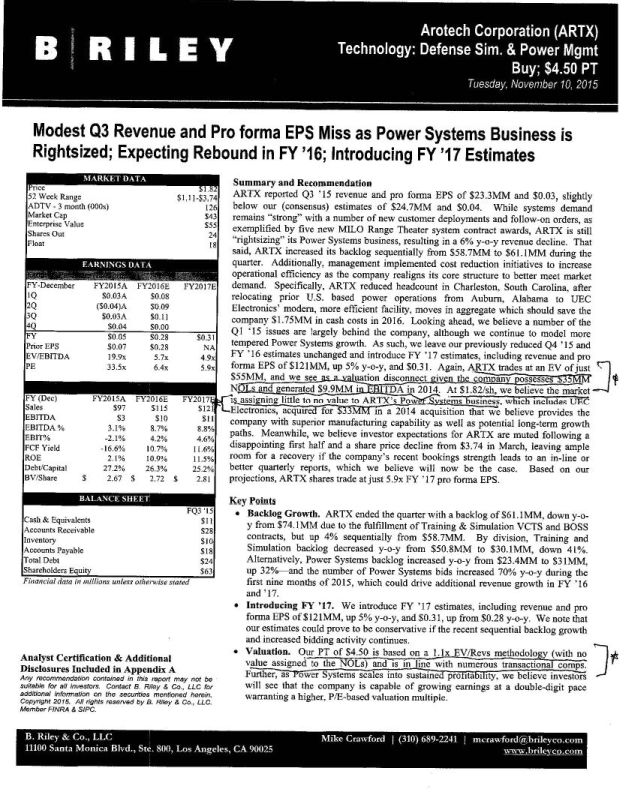

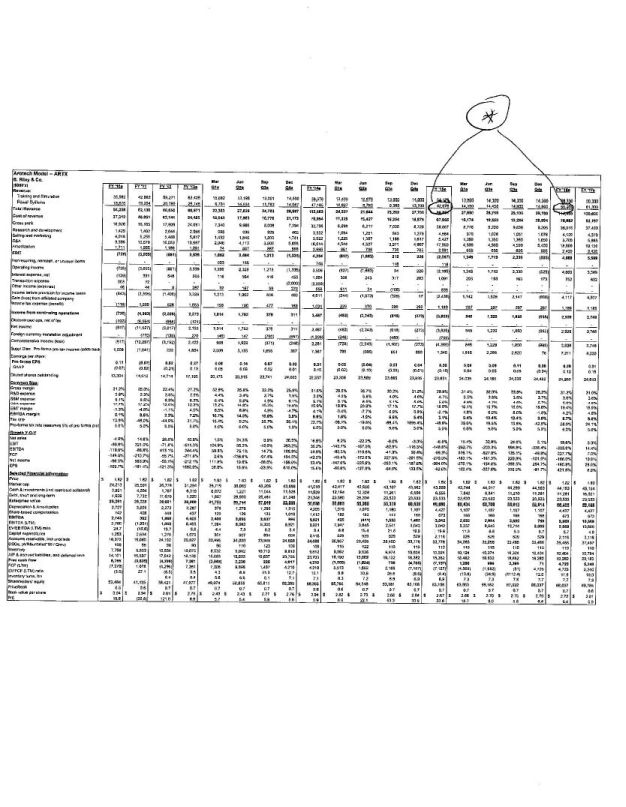

Response: This statement is supported by the following information: “ARTX trades at an EV of just $55MM, and we see as a valuation disconnect given the company possesses $35MM NOLs and generated $9.9MM in EBITDA in 2014.” (Source: B. Riley Research Report dated November 10, 2015, a copy of which is attached hereto asExhibit A (the “Research Report”), based on a stock price of $1.82. This $1.82 stock price is 11% higher than the closing stock price the day before Mr. Fields filed the Schedule 14A. With regard to the Research Report, we note that B. Riley is the only sell side firm that covers the company and the Research Report is the most recent available.)

The Research Report states: “Our PT [Price Target] of $4.50 is based on a 1.1x EV/Revs methodology (with no value assigned to the NOLs) and is in line with numerous transactional comps”. This price target supports Mr. Fields’ belief that the inherent value of the company’s assets significantly exceeds its current stock price.

U.S. Securities and Exchange Commission

December 16, 2015

Page 2

| · | The Training/Simulation division alone is worth more than the company’s entire current enterprise value |

Response: The Research Report states: “At $1.82/sh we believe the market is assigning little to no value to ARTX’s Power Systems business….” This supports the contention that such division alone is worth more than the company’s entire current enterprise value.

| · | The Power Systems division could generate increased profitability next year |

Response: This statement is supported by the company’s own disclosure: “At the same time, we expect our focus on improving efficiencies, growing the revenue base, and right-sizing overheads to improve the performance of our Power Systems division and enhance operational efficiency, will lead to improved financial results going into 2016.” (Source: Company’s press release dated November 9, 2015, a copy of which is attached hereto asExhibit B.) Further, the Research Report noted that it projects Power Systems revenue will increase from $42.7 million in 2015 to $58.2 million in 2016.

| · | Iron Flow has significant additional value |

Response: This statement is based on the fact that the company has consistently touted the potential market for the iron flow battery, noting that “[a]ccording to the Boston Consulting Group, the grid storage market is estimated to exceed $400 billion by 2030. This represents a global storage capacity of 430 giga-watts. To give some perspective, grid storage currently approximates 100 giga-watts, so the market is expected to more than quadruple in only 16 years.” (Source: Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2014 (“2014 Annual Report”), as filed via EDGAR on March 20, 2015.) The company then goes on to note that “the iron flow battery has yielded what we believe to be promising results in lab tests.” (Source: 2014 Annual Report.)

The company has even gone to the expense and effort to filing a patent application covering the new technology. (Source: 2014 Annual Report.) In addition, based on the company’s public filings, the company is investing $500,000 in the iron flow battery this year alone. In addition, as noted in the company’s press release dated January 7, 2015 (a copy of which is attached hereto asExhibit C) the Israeli Government gave the company a $750,000 grant to help fund Iron Flow. All of this supports the view that the iron flow battery has significant value.

| · | The results to-date of UEC have disappointed |

Response: UEC was acquired on April 1, 2014, and the company paid over $35 million (a sum which approximates ARTX’s current market capitalization). The company reported it as a material acquisition. That this acquisition has been a disappointment is supported by the fact that ARTX’s stock price was $6.22 the day before the acquisition was announced, and since then the stock price has declined rapidly and consistently and is down 73% in aggregate.

U.S. Securities and Exchange Commission

December 16, 2015

Page 3

In further response to your comment letter, Mr. Fields acknowledges that:

| · | the filing person is responsible for the adequacy and accuracy of the disclosure in the filing; |

| · | staff comments or changes to disclosure in response to staff comments do not foreclose the Commission from taking any action with respect to the filing; and |

| · | the filing person may not assert staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States. |

If you would like to discuss the responses, you may contact Peter D. Fetzer at (414) 297-5596.

| Very truly yours, Peter D. Fetzer |

| Exhibit A-1 |

| Exhibit A-2 |

| Exhibit A-3 |

| Exhibit B-1 |

| Exhibit B-2 |

| Exhibit B-3 |

| Exhibit B-4 |

| Exhibit B-5 |

| Exhibit B-6 |

| Exhibit B-7 |

| Exhibit B-8 |

| Exhibit C-1 |

| Exhibit C-2 |