Sterne Agee

Financial Institutions Investor Conference

February 11 - 12, 2013

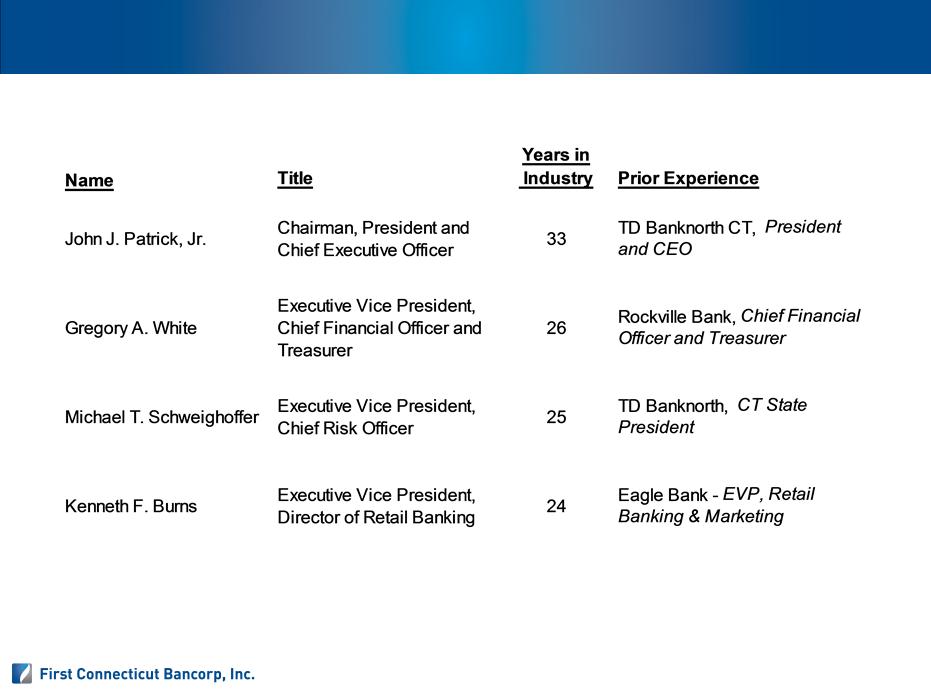

John J. Patrick, Jr. Chairman, President and CEO

Gregory A. White EVP, Chief Financial Officer

Michael T. Schweighoffer EVP, Chief Risk Officer

Kenneth F. Burns EVP, Director of Retail Banking

A Great Past…Dynamic Present…

And a Bright Future

Forward Looking Statements

Disclaimer & Forward-Looking Statements

Statements in this document and presented orally at the conference, if any, concerning future results,

performance, expectations or intentions are forward-looking statements. Actual results, performance or

developments may differ materially from forward-looking statements as a result of known or unknown risks,

uncertainties and other factors, including those identified from time to time in the Company’s filings with the

Securities and Exchange Commission, press releases and other communications. Actual results also may differ

based on the Company’s ability to successfully maintain and integrate customers from acquisitions.

performance, expectations or intentions are forward-looking statements. Actual results, performance or

developments may differ materially from forward-looking statements as a result of known or unknown risks,

uncertainties and other factors, including those identified from time to time in the Company’s filings with the

Securities and Exchange Commission, press releases and other communications. Actual results also may differ

based on the Company’s ability to successfully maintain and integrate customers from acquisitions.

The Company intends any forward-looking statements to be covered by the Litigation Reform Act of 1995 and is

including this statement for purposes of said safe harbor provisions. Readers and attendees are cautioned not to

place undue reliance on forward-looking statements, which speak only as of the date of this presentation. Except

as required by applicable law or regulation, the Company undertakes no obligation to update any forward-looking

statements to reflect events or circumstances that occur after the date as of which such statements are made.

including this statement for purposes of said safe harbor provisions. Readers and attendees are cautioned not to

place undue reliance on forward-looking statements, which speak only as of the date of this presentation. Except

as required by applicable law or regulation, the Company undertakes no obligation to update any forward-looking

statements to reflect events or circumstances that occur after the date as of which such statements are made.

The Company’s capital strategy includes deployment of excess capital, the success of which efforts cannot be

guaranteed.

guaranteed.

2

Ø Farmington Bank, founded in 1851, is a wholly owned subsidiary of

First Connecticut Bancorp, Inc.

First Connecticut Bancorp, Inc.

Ø A community bank with strong capital position, positive trends in loan

and deposit growth, and solid asset quality

and deposit growth, and solid asset quality

Ø Experienced management team focused on organic growth strategy

Ø Clear strategic priorities

Ø Strong, scalable franchise in central Connecticut

Ø Broad risk management program focused on “best practices”

Ø Culture that encourages a decision-making process that allows for

teamwork, yet places clear responsibility and authority with the

individual

teamwork, yet places clear responsibility and authority with the

individual

Executive Summary

3

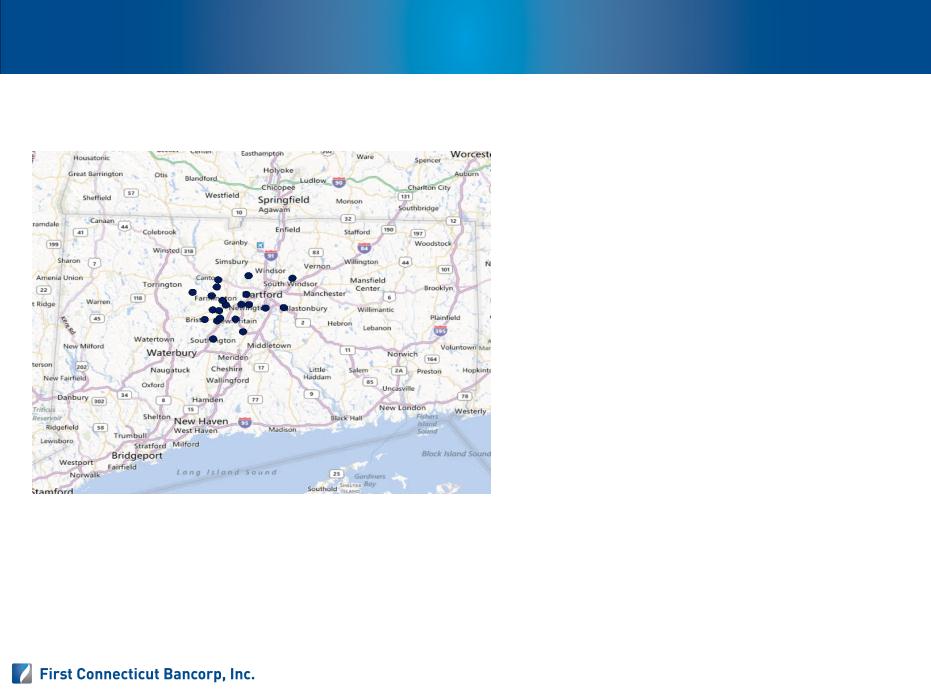

Franchise Overview

§ 19 branch offices

§ Executing on de novo strategy of adding 2-3 branches a year through mid-2014, then reassess

§ Strategically located in affluent Hartford, CT suburbs

19 Branches And Expanding

First Connecticut Bancorp, Inc. - NASDAQ (FBNK)

Farmington Bank - wholly owned subsidiary

Headquarters: Farmington, Connecticut

Assets: $1.8 billion

Loans: $1.5 billion

Deposits: $1.3 billion

Capital: $242 million

(as of 9/30/12)

Corporate Profile

4

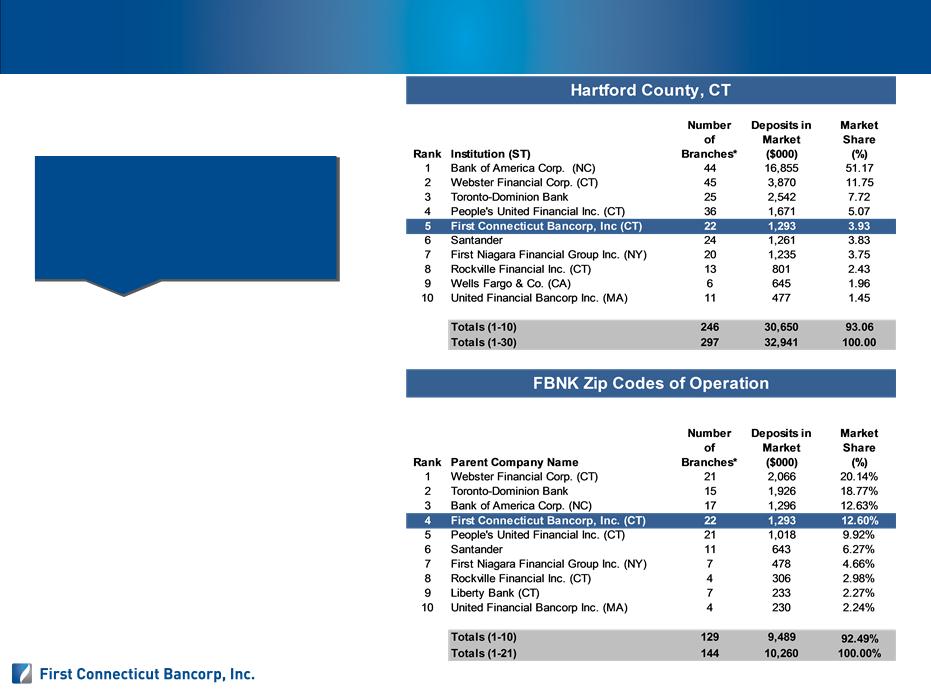

Market Position

5

Source: SNL Financial

*includes limited service branches

Note: Deposit data as of 6/30/2012;

Pro forma for pending and recently completed transactions

Too big to be small…….

Too small to be big…….

Leadership Team

6

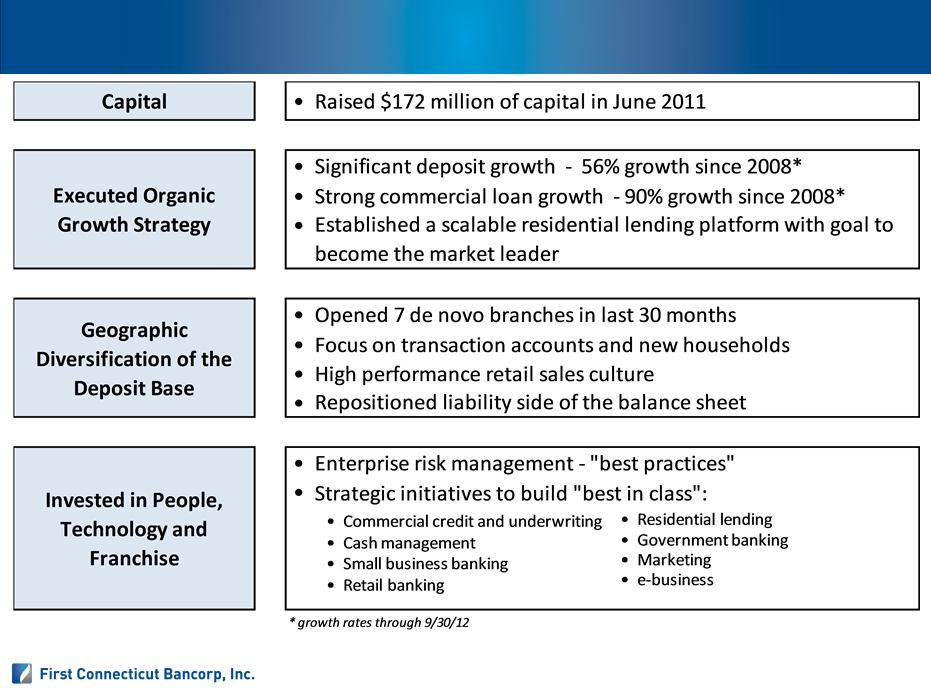

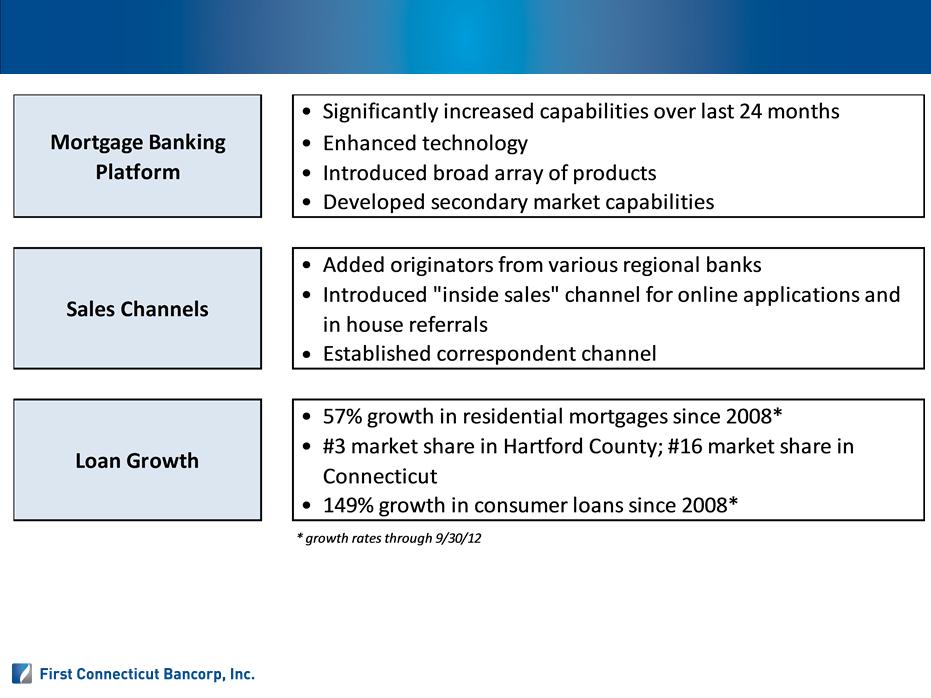

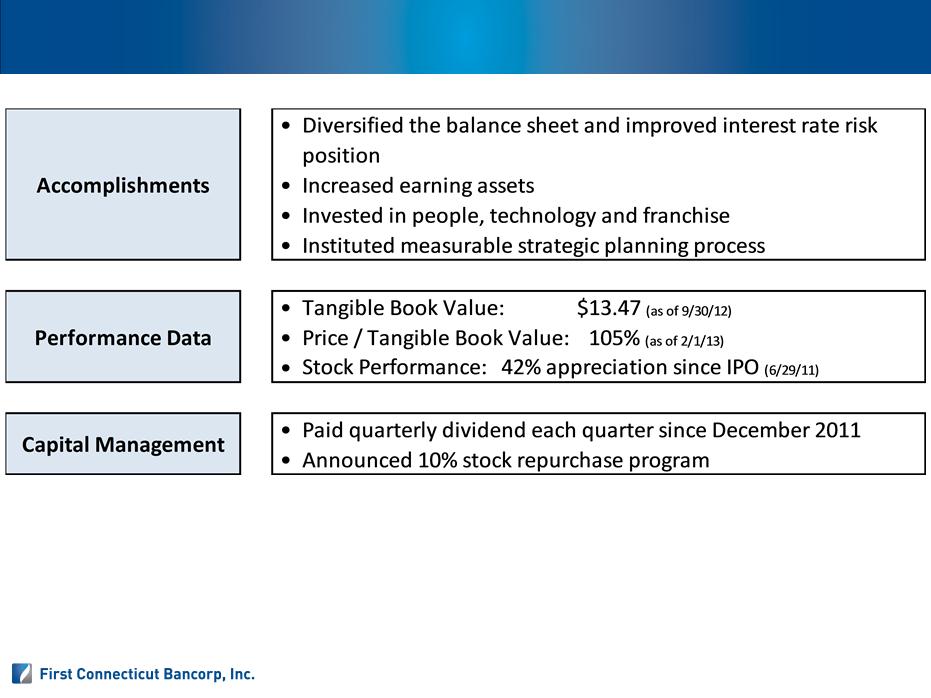

Strategic Accomplishments

7

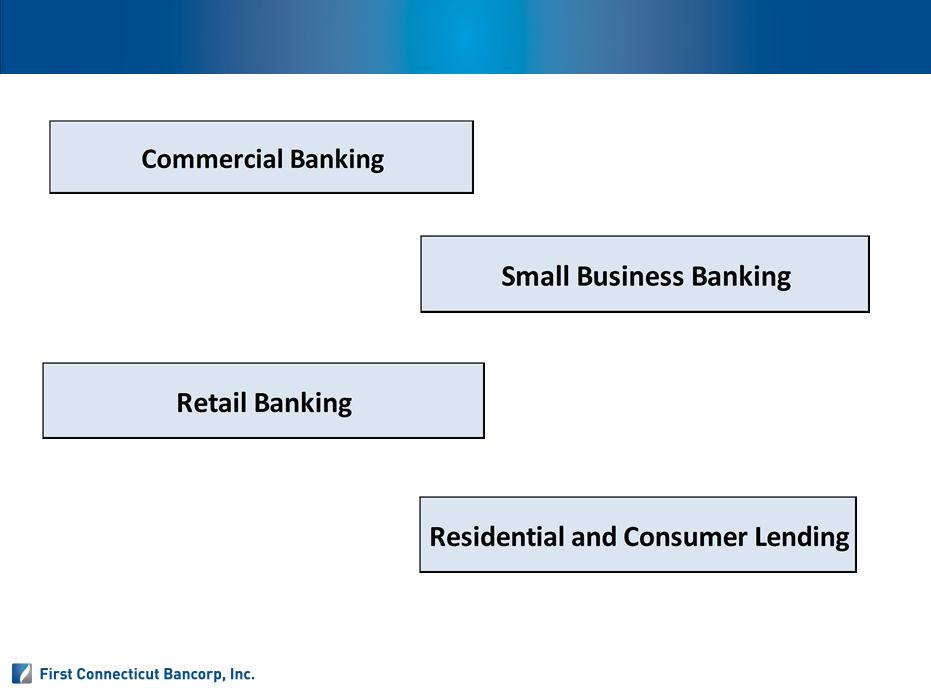

Our Core Business

8

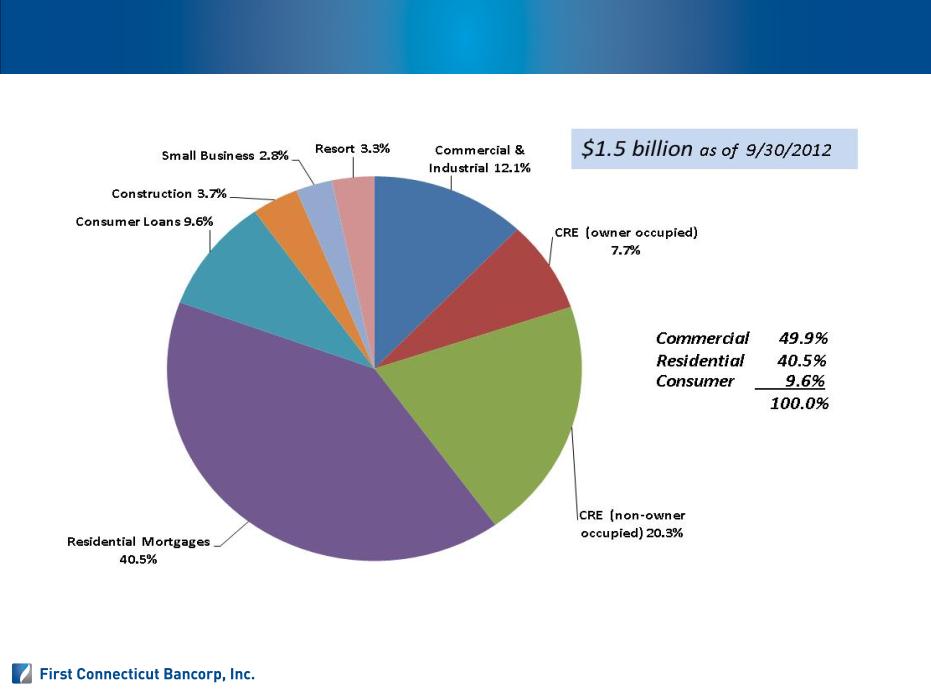

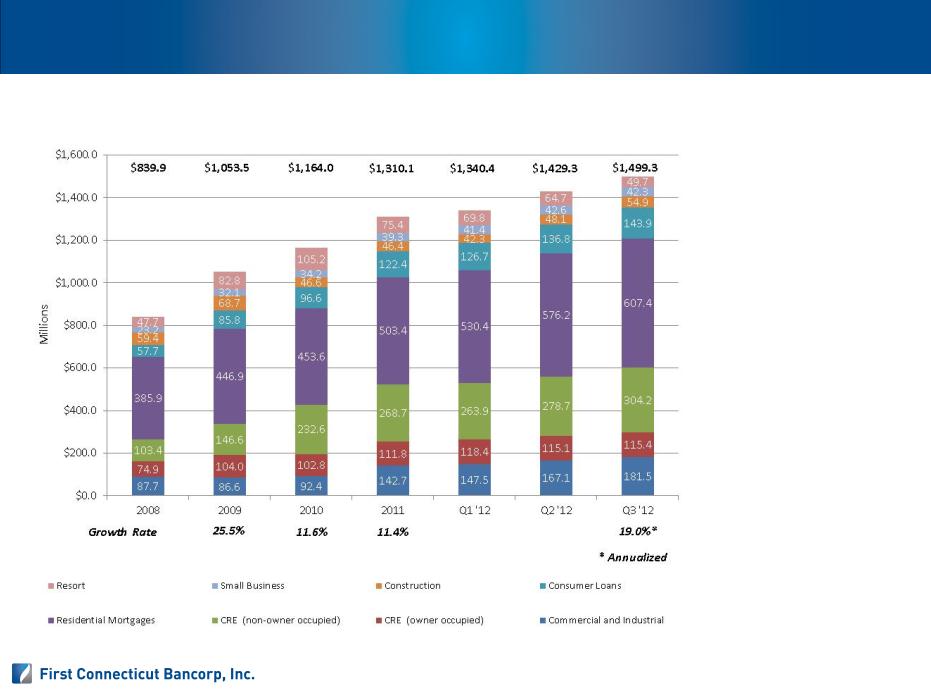

Diversified Loan Portfolio

9

Total Loan Growth

29% growth since

2010, despite

strategic reduction of

$55.5 million in

resort loan portfolio

2010, despite

strategic reduction of

$55.5 million in

resort loan portfolio

10

Total Loans (period ended)

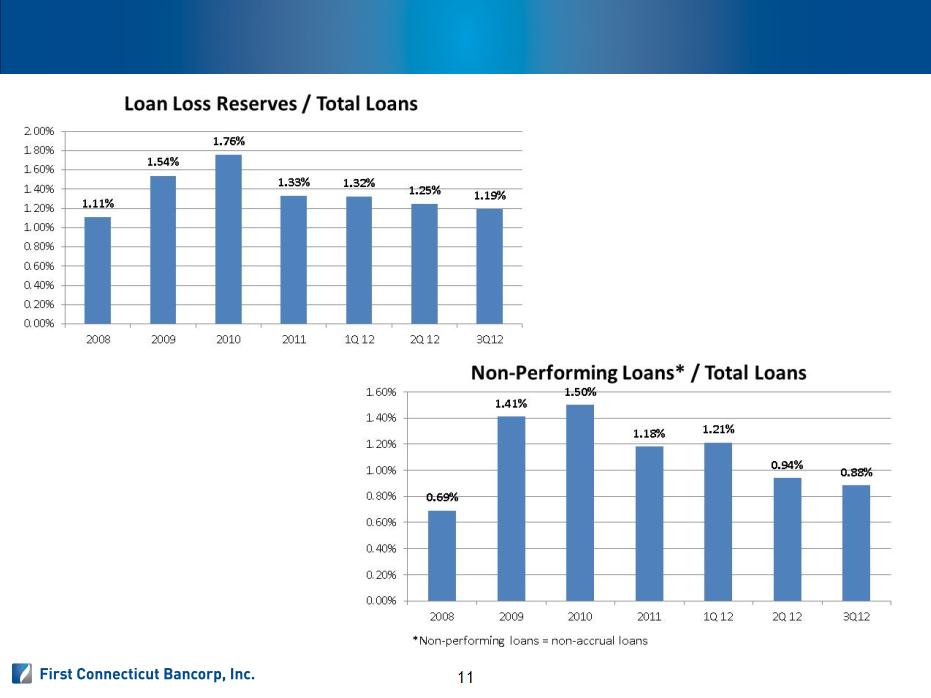

Asset Quality Metrics

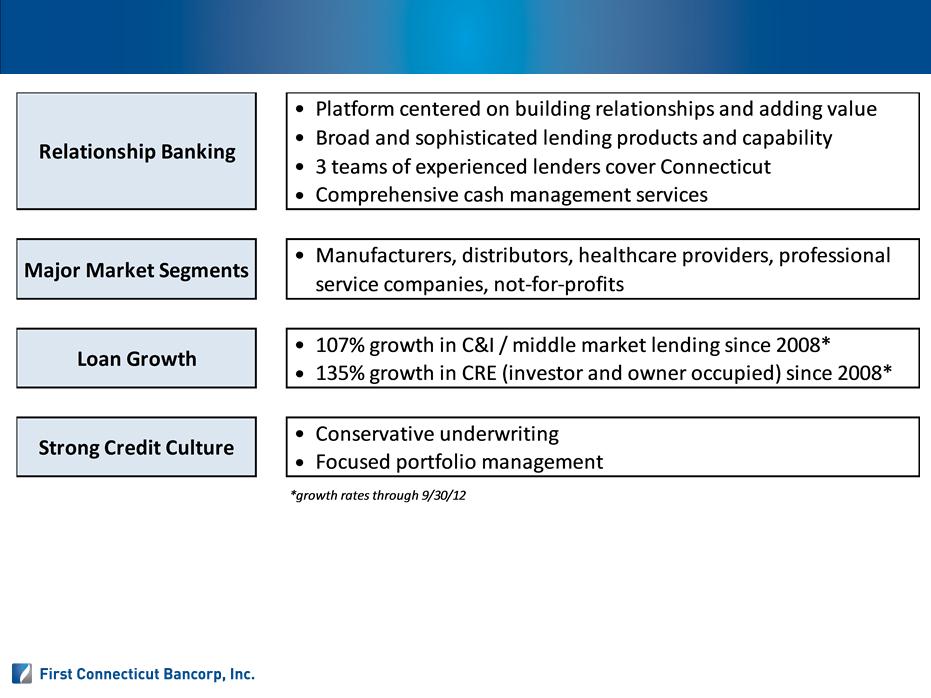

Commercial Banking

12

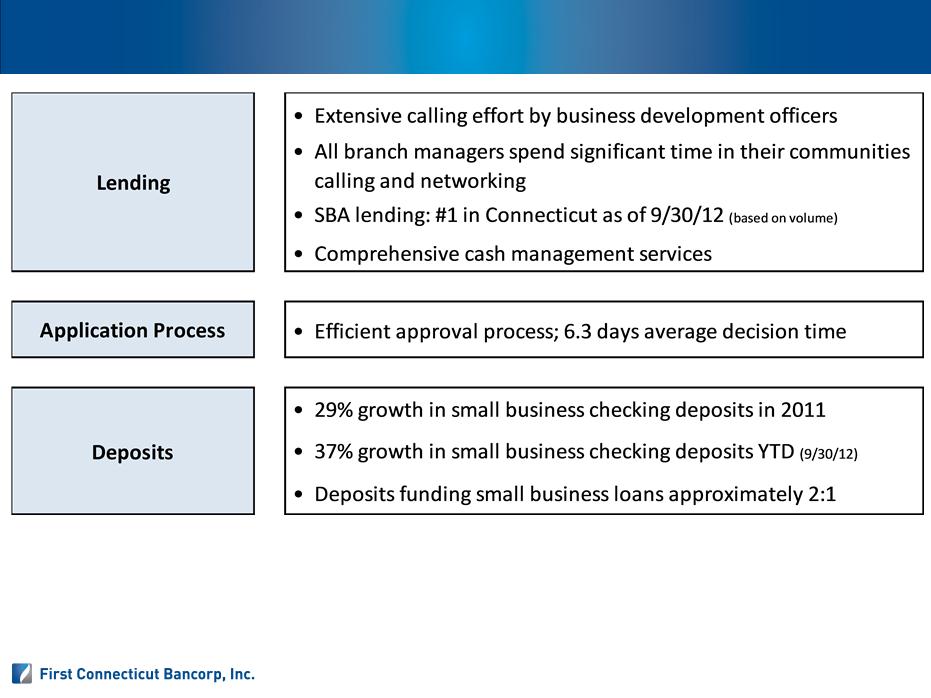

Small Business Banking

13

Residential Mortgage and Consumer Lending

14

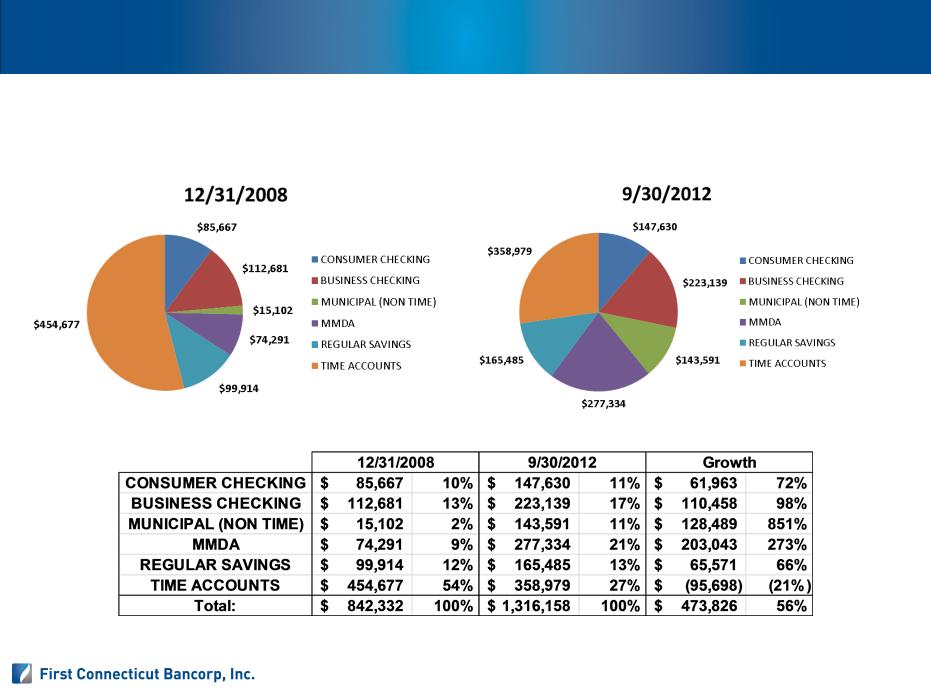

Diversified Deposit Base

Deposit Composition 2008 vs 9/30/12 (000’s)

15

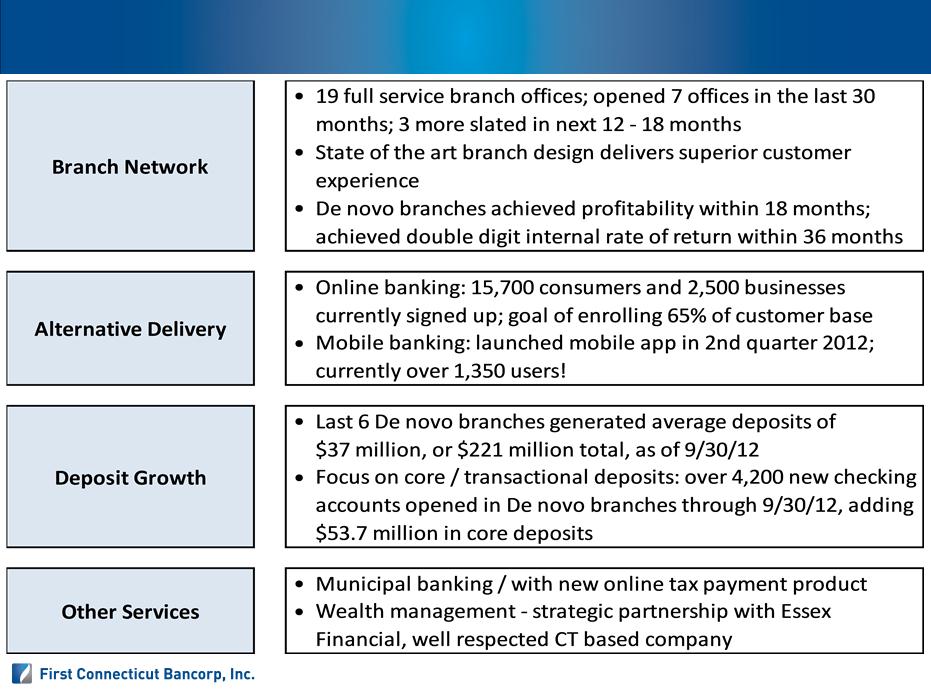

Retail Banking

16

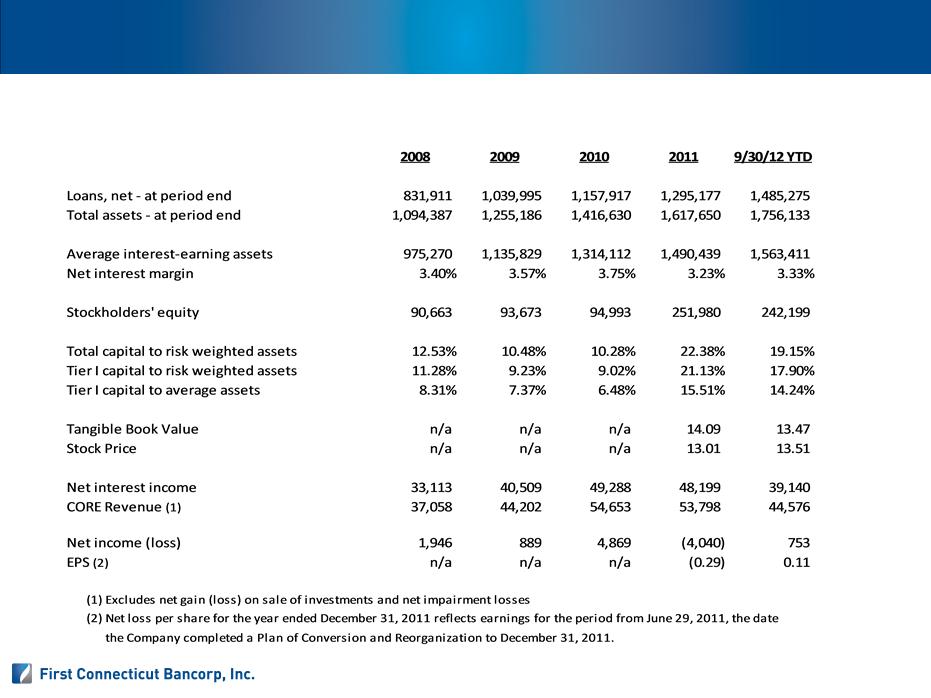

Financial Performance

17

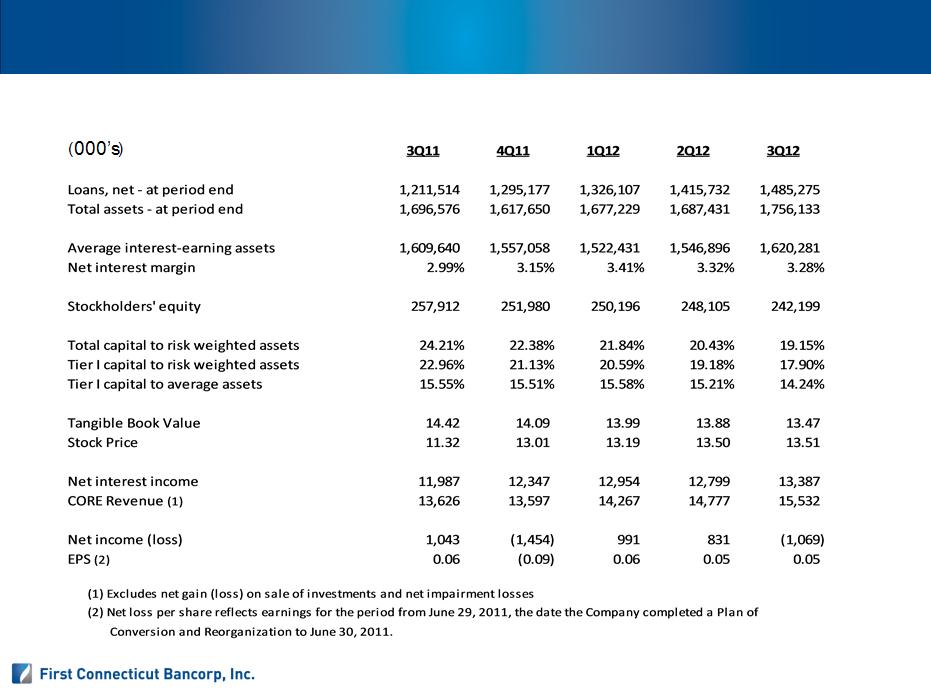

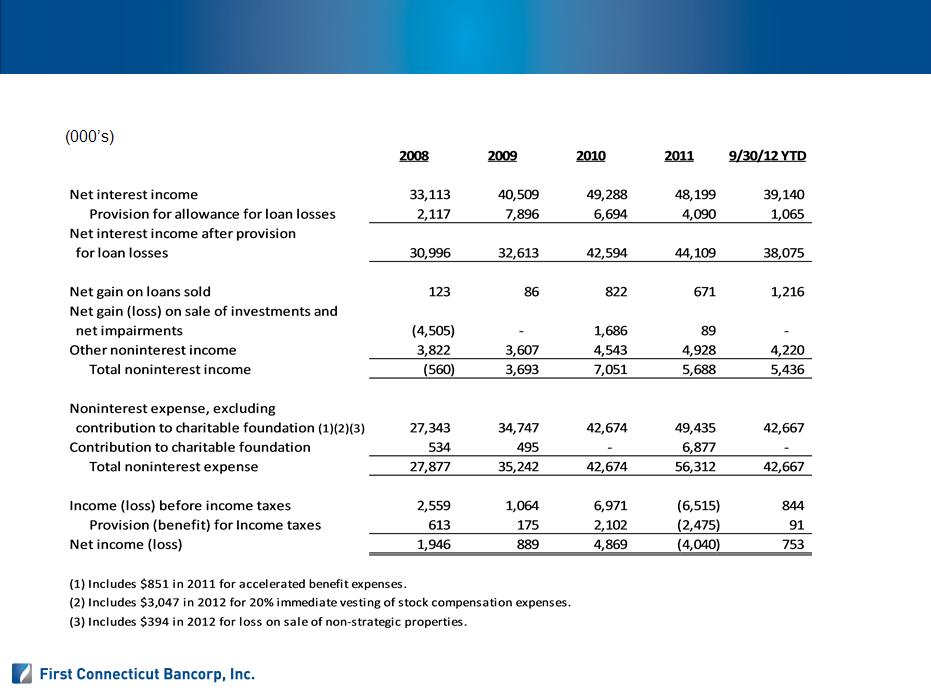

Selected Annual Financial Data

(000’s)

Financial Performance

18

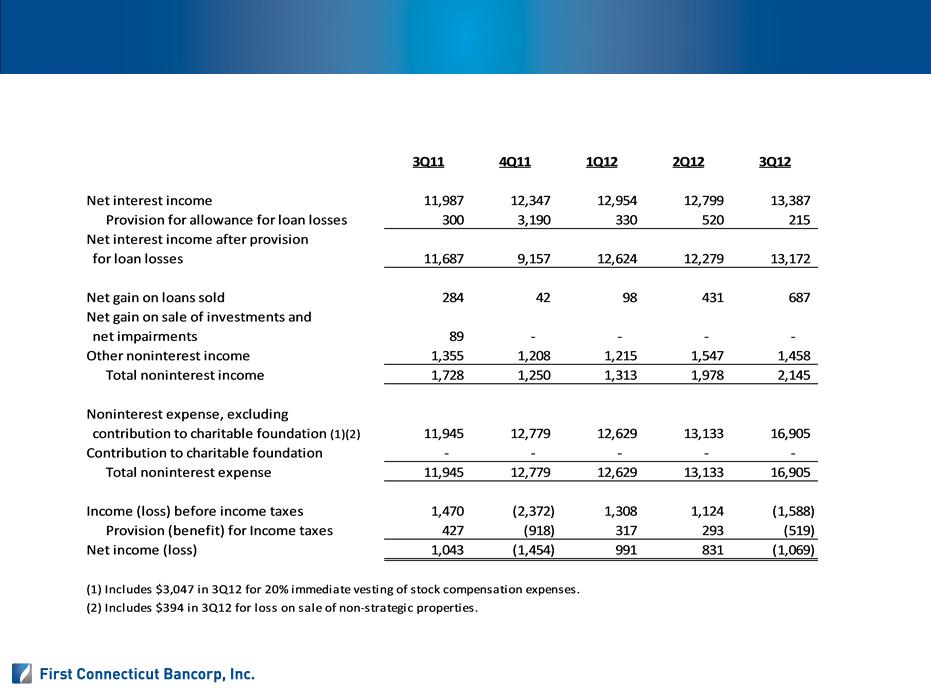

Selected Quarterly Financial Data

Financial Performance

19

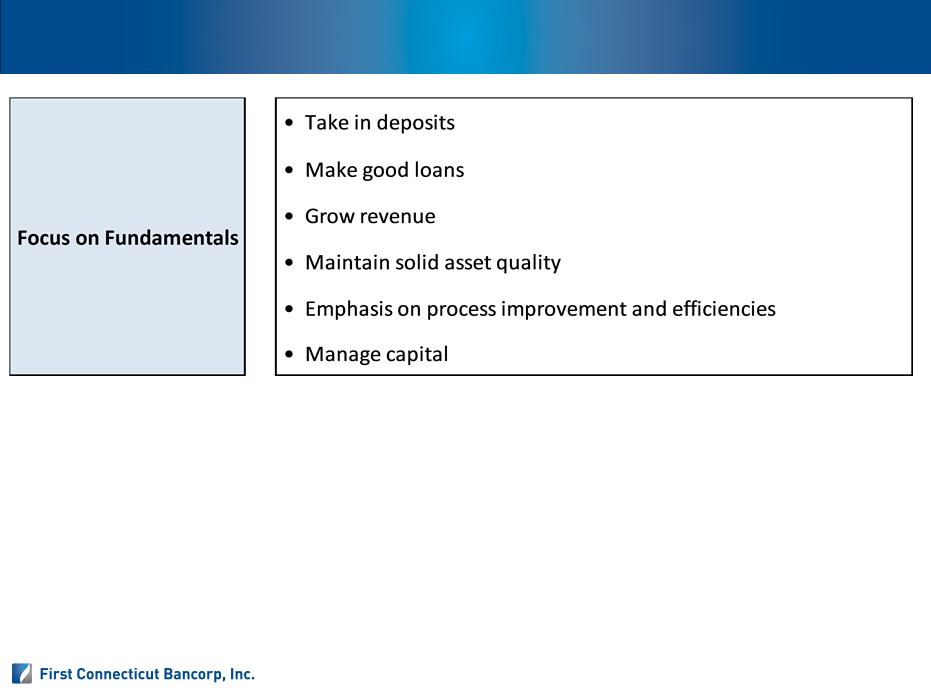

Strategic Direction

20

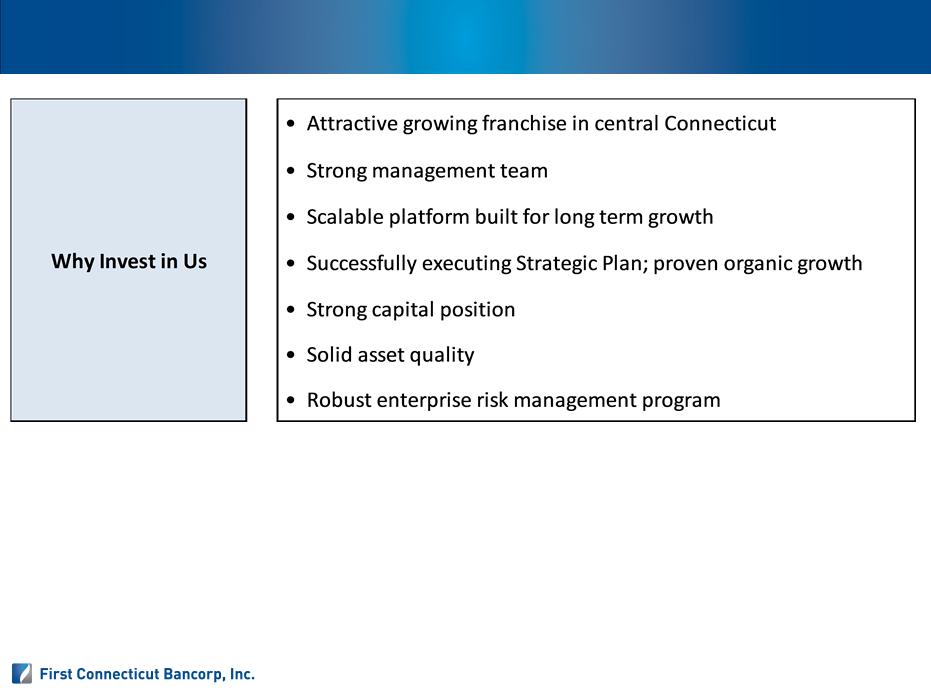

Conclusion

21

Supplemental Information

Appendix

22

Income Statement 2008 - 9/30/12

Select Financial Data

23

Select Financial Data

24

Income Statement last 5 quarters

(000’s)

Select Financial Data

25

Select Financial Data

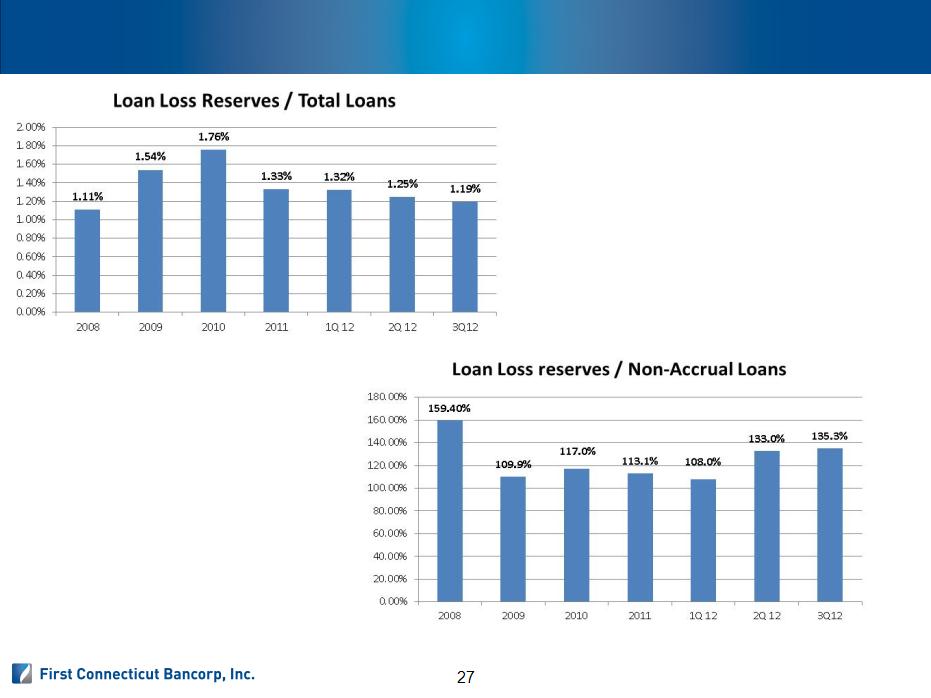

Asset Quality Metrics

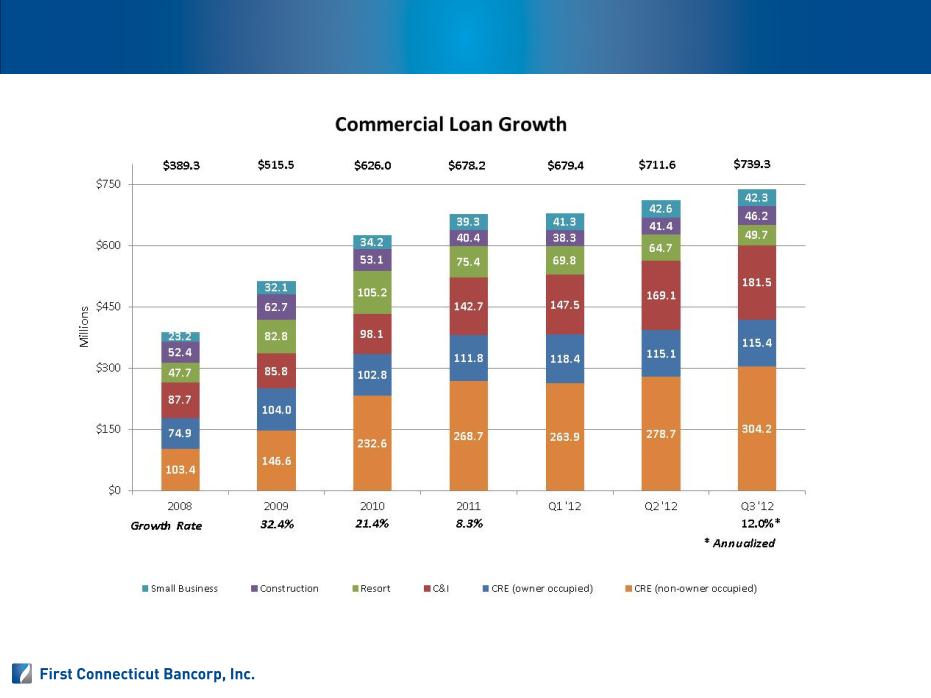

Commercial Loan Growth

28

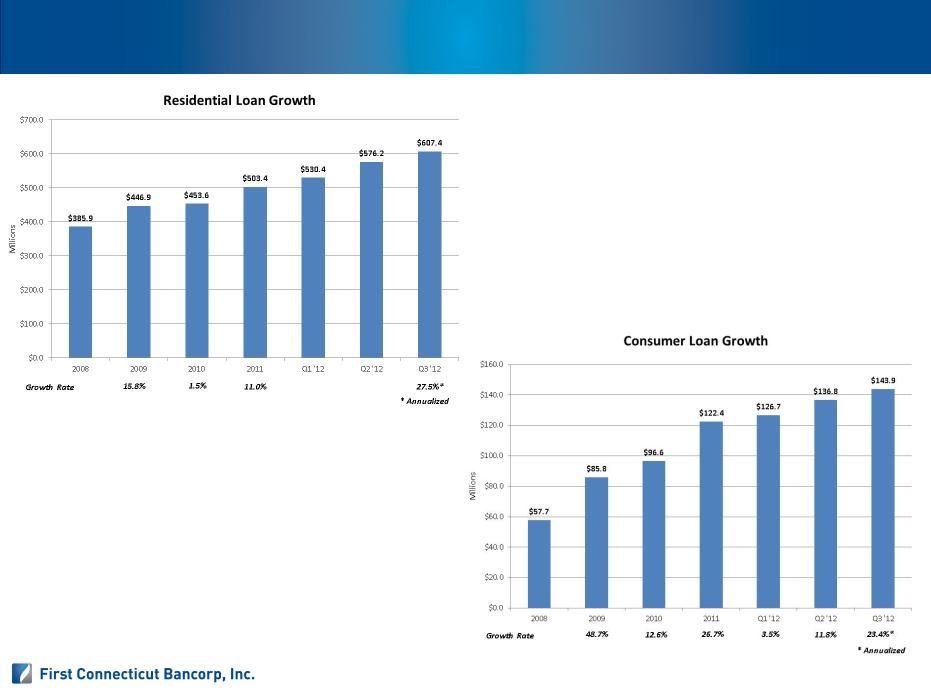

Residential and Consumer Loan Growth

29

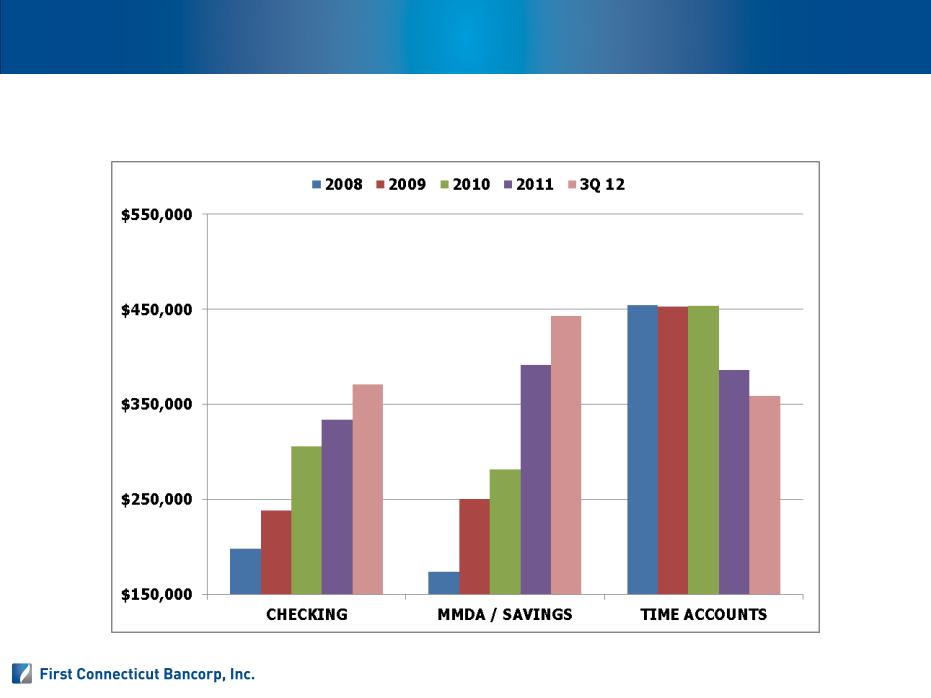

Deposit Diversification

Checking & MMDA / Savings vs Time Deposits (000’s)

30

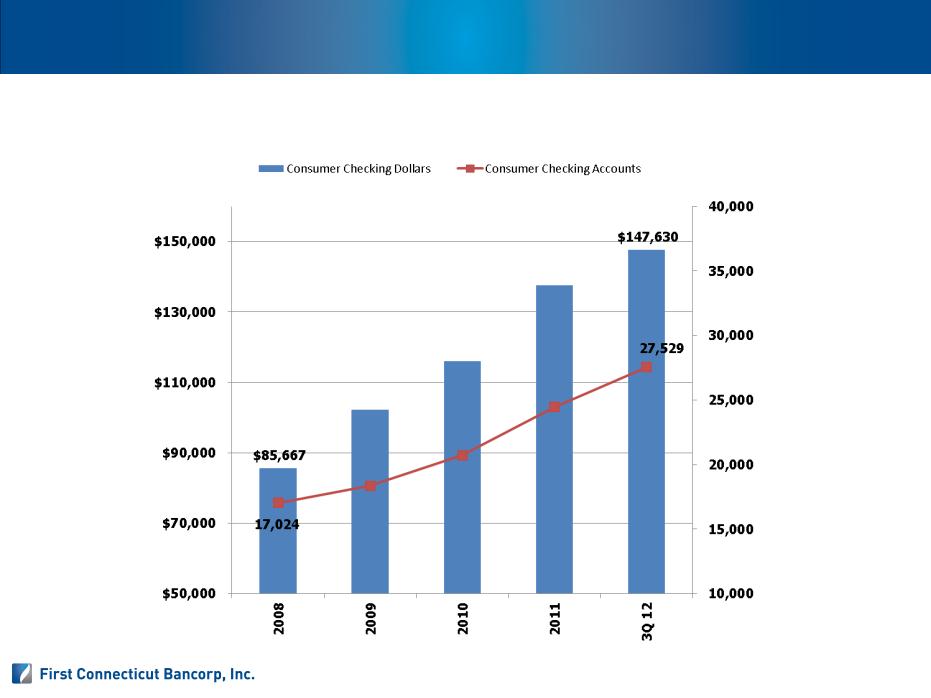

Checking Growth

Consumer Checking Growth ($000’s)

31

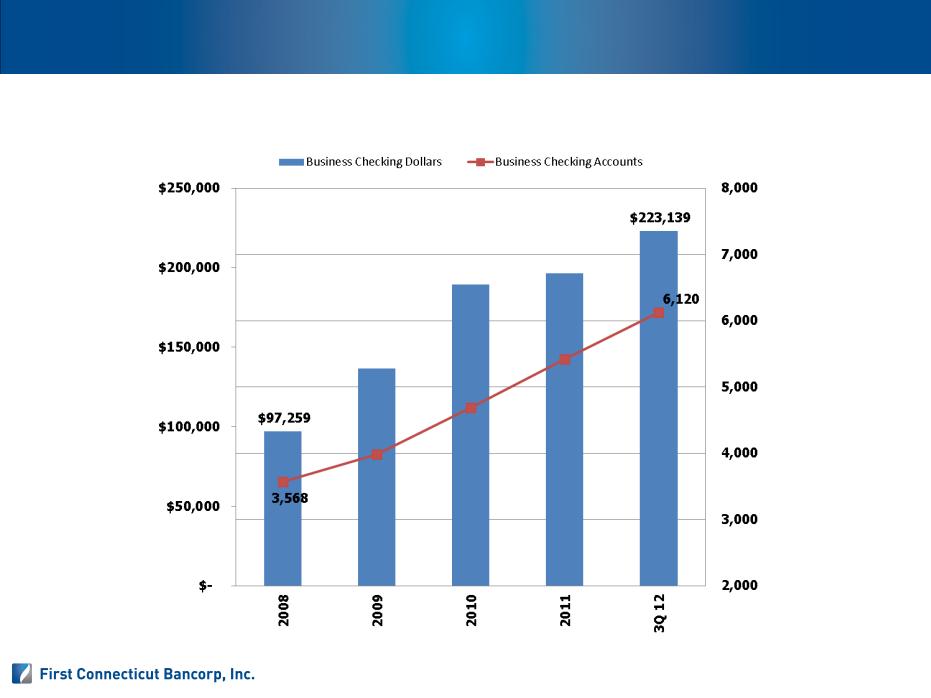

Checking Growth

Business Checking Growth ($000’s)

32

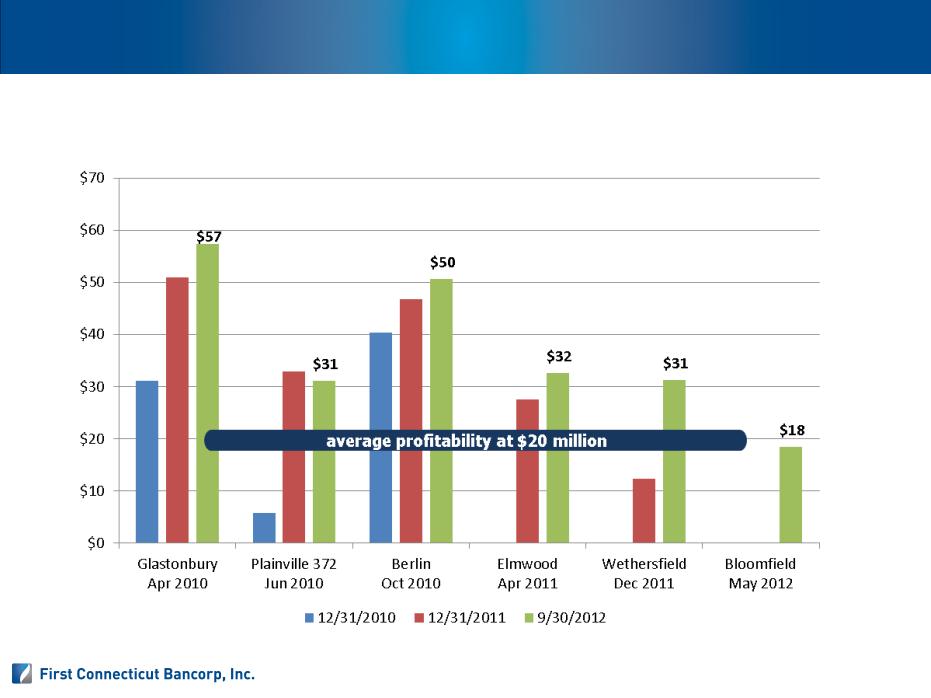

De Novo Branch Profitability

33

De Novo Branch Deposit

Growth & Point of Profitability

(In Millions)

Growth & Point of Profitability

(In Millions)

John J. Patrick, Jr.

Chairman, President and Chief Executive Officer

Gregory A. White

Executive Vice President, Chief Financial Officer

Investor Information:

Jennifer H. Daukas

Vice President, Investor Relations Officer

860-284-6359 or jdaukas@farmingtonbankct.com

Corporate Contacts

34