Free signup for more

- Track your favorite companies

- Receive email alerts for new filings

- Personalized dashboard of news and more

- Access all data and search results

Filing tables

FBNK similar filings

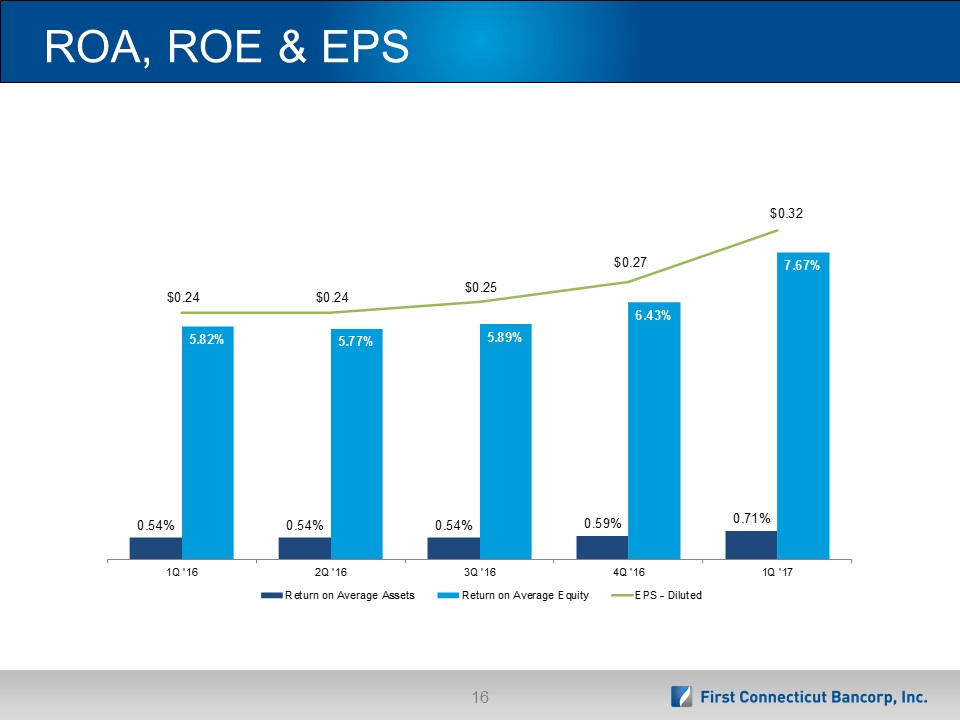

- 19 Jul 17 First Connecticut Bancorp, Inc. reports second quarter 2017 earnings of $0.32 diluted earnings per share

- 19 Jun 17 First Connecticut Bancorp, Inc. Announces Second Quarter (Q2 2017) Earnings Release and Conference Call

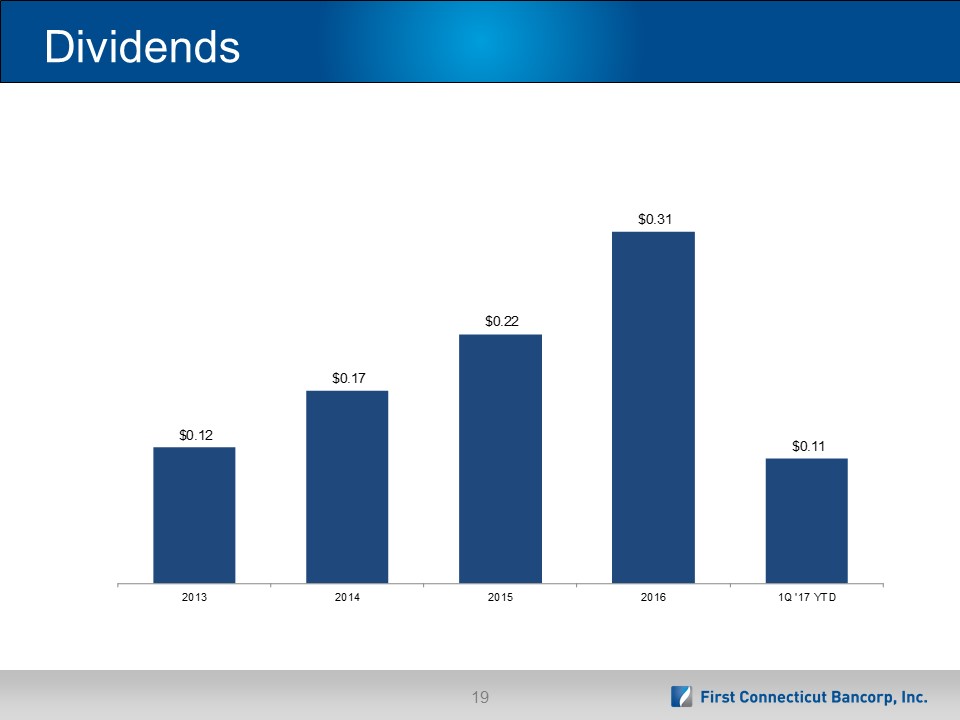

- 23 May 17 First Connecticut Bancorp, Inc. Increases Quarterly Dividend

- 15 May 17 Regulation FD Disclosure

- 11 May 17 Submission of Matters to a Vote of Security Holders

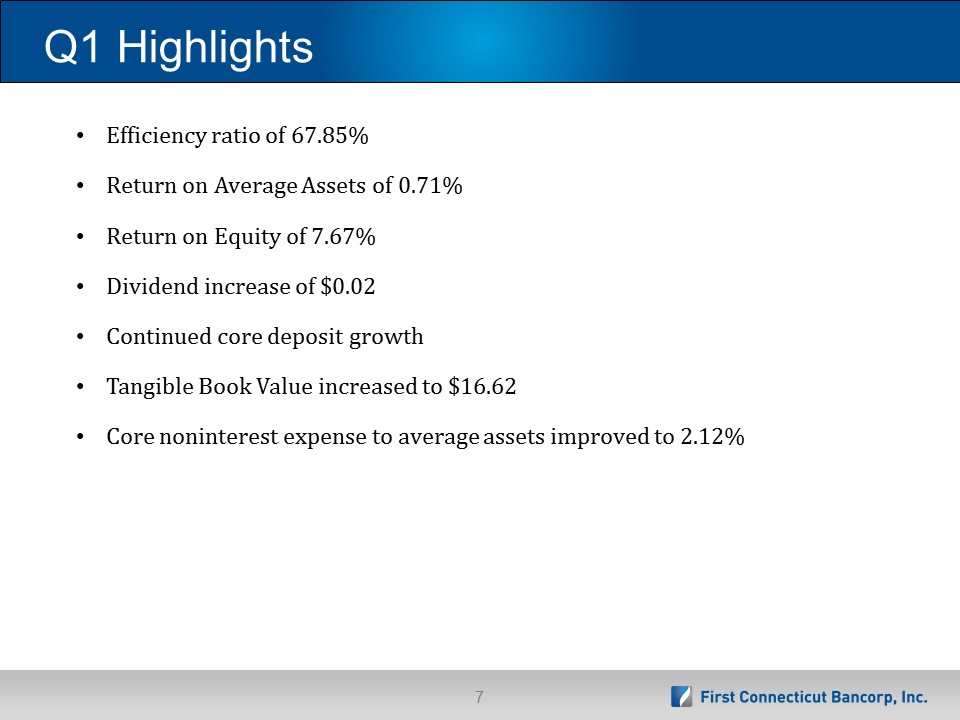

- 18 Apr 17 First Connecticut Bancorp, Inc. reports first quarter 2017 earnings of $0.32 diluted earnings per share

- 4 Apr 17 First Connecticut Bancorp, Inc. Announces First Quarter (Q1 2017) Earnings Release and Conference Call

Filing view

External links