Exhibit (a)(1)

NATURAL RESOURCES USA CORPORATION

GOING-PRIVATE TRANSACTION STATEMENT

November 17, 2011

This transaction statement (the “Transaction Statement”) describes the “going-private” transaction involving Natural Resources USA Corporation, referred to herein as NRUC, how it affects you, and what your rights are with respect to the transaction as a shareholder of NRUC. It also includes the position of Green SEA Resources Inc. and GSR Acquisition Corp., referred to herein (unless noted or the context requires otherwise) as we, us or GSR, on the fairness of the transaction to the minority shareholders, including the unaffiliated shareholders, of NRUC. Under the terms of the proposed going-private transaction, each share of NRUC common stock owned by you will be cancelled in exchange for the right to receive cash in the amount of $0.57 per share, without interest. Additionally, all outstanding options (other than options owned by GSR), whether or not exercisable, will be cancelled in exchange for an amount equal in cash to the number of shares subject to each option times the excess, if any, of the merger consideration less the applicable exercise price of that option, less any required withholding taxes. All “out-of-the-money” options will be cancelled for no consideration. Please read this summary and the remainder of this document very carefully.

The name of the company that is the subject of this Transaction Statement is Natural Resources USA Corporation, a Utah corporation, its principal executive offices are located at 3200 County Road 31, Rifle, Colorado 81650, and its telephone number is (214) 253-2556.

Neither the Securities and Exchange Commission (the “SEC”) nor any state securities commission has approved or disapproved of the transaction, passed upon the merits or fairness of the transaction or passed upon the adequacy or accuracy of the disclosure in this document. Any representation to the contrary is a criminal offense.

QUESTIONS AND ANSWERS

Questions and Answers About the Going-Private Transaction

The following questions and answers briefly address some questions you may have regarding the going-private transaction. We strongly encourage you to read the more detailed information contained in this Transaction Statement, the appendices to this Transaction Statement and the documents referred to and incorporated by reference in this Transaction Statement.

| Q: | What is the proposed transaction? |

| A: | Green SEA Resources Inc. beneficially owns approximately 95% of the outstanding common stock of NRUC, which it will contribute to its wholly-owned subsidiary, GSR Acquisition Corp., pursuant to the terms of a contribution agreement between Green SEA Resources Inc. and GSR Acquisition Corp. (attached hereto asAppendix A) (the “Contribution Agreement”) prior to the mailing of this Transaction Statement. Following the contribution, GSR Acquisition Corp. will adopt a plan of merger (the form of which is attached hereto asAppendix B) whereby it will effect a short-form merger and merge with and into NRUC, with NRUC being the surviving corporation, in accordance with Section 1104 of the Utah Revised Business Corporations Act (“URBC”). Following the effectiveness of the short-form merger, you will no longer own any shares of NRUC and your shares will represent the right to receive cash in the amount of $0.57 per share of NRUC common stock, without interest. |

| Q: | What will I receive in connection with the transaction? |

| A: | Pursuant to the short-form merger, each holder of outstanding shares of common stock of NRUC (other than GSR Acquisition Corp.) will be entitled to receive cash in the amount of $0.57 per share, without interest. |

| Q: | When does Green SEA Resources Inc. and GSR Acquisition Corp. expect to complete the short-form merger? |

1

| A: | Green SEA Resources Inc. and GSR Acquisition Corp. expect to complete the short-form merger after all conditions to the Contribution Agreement and plan of merger are satisfied or waived and all required regulatory approvals are received. Green SEA Resources Inc. and GSR Acquisition Corp. currently expect to complete the short-form merger during the fourth quarter of 2011. It is possible, however, that factors outside of either company’s control could result in the completion of the short-form merger at a later time or a failure to complete the short-form merger at all. |

| Q: | Is my vote required? |

| A: | No. Because GSR Acquisition Corp. will hold greater than 90% of the outstanding shares of each class of capital stock of NRUC, we are entitled to effect the short-form merger without any vote of the shareholders or the board of directors of NRUC, as permitted by Section 1104 of the URBC. |

| Q: | Why am I receiving these materials? |

| A: | We are required to provide you with this Transaction Statement pursuant to Rule 13e-3 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and Section 1104 of the URBC. |

| Q: | May I exercise dissent rights related to the proposed transaction? |

| A: | Yes. If you do not believe $0.57 per share of NRUC common stock represents the fair value for your shares of NRUC common stock, you may exercise your dissent rights to demand fair value for your shares of NRUC common stock, which may be more than the $0.57 per share merger consideration. |

| Q: | How may I preserve and timely exercise my dissent rights? |

| A: | In order to exercise your dissent rights, you must follow certain procedures under Part 13 of the URBC as described in detail in this Transaction Statement, which include, but are not limited to, making a written demand for payment using the Form for Demanding Payment by a Dissenting Shareholder attached asAppendix B to the Notice of Merger and Dissenter’s Rights accompanying this Transaction Statement within 30 days after the mailing date of the Transaction Statement and Notice of Merger and Dissenter’s Rights in accordance with the instructions set forth therein. See “ADDITIONAL INFORMATION—Terms of the Transaction—Dissent Rights” in this Transaction Statement. See also the Notice of Merger and Dissenter’s Rights accompanying this Transaction Statement. Any failure to comply with such procedures will result in the loss of your dissent rights. If you seek to exercise your statutory right of dissent, we strongly encourage you to readAppendix D to the Transaction Statement in its entirety and seek advice from legal counsel and your financial advisor. |

| Q: | What is our position regarding the fairness of the short-form merger? |

| A: | Each of the boards of directors of Green SEA Resources Inc. and GSR Acquisition Corp. have determined that the short-form merger is both substantively and procedurally fair to the minority shareholders, including the unaffiliated shareholders, of NRUC. The basis for this determination is set forth in detail in this Transaction Statement and the documents incorporated by reference in this Transaction Statement. |

2

SUMMARY TERM SHEET

Summary Terms

Relationship of the Parties | NRUC is a Utah corporation that identifies and develops natural resource assets in a clean, efficient and environment-friendly manner. NRUC actively participates in the management and development of: | |

• Natural sodium bicarbonate;

• Water rights assets; and

• Oil shale research.

| ||

| NRUC owns Bureau of Land Management leases in Colorado covering large-scale deposits of naturally occurring sodium bicarbonate (baking soda). It also owns various water rights assets and sodium leases and it is currently seeking a Research Development and Demonstration lease from the Bureau of Land Management for the purpose of investigating the recovery of oil from oil shale. See “ADDITIONAL INFORMATION—Information about NRUC” in this Transaction Statement. | ||

| Green SEA Resources Inc. beneficially owns approximately 95% of the outstanding common stock, par value $0.01 per share, of NRUC. Green SEA Resources Inc. is a private Canadian company wholly-owned within the Sentient Group of Global Resource Funds (“The Sentient Group”). GSR Acquisition Corp. is a wholly-owned subsidiary of Green SEA Resources Inc., incorporated by Green SEA Resources Inc. in Utah in connection with the going-private transaction. Certain of Green SEA Resources Inc.’s and GSR Acquisition Corp.’s directors and officers are also directors of NRUC. See “ADDITIONAL INFORMATION—Identity and Background of GSR, SURF and the Sentient General Partner” andSchedule I to this Transaction Statement. | ||

Short-Form Merger and Merger Consideration | Prior to the mailing of this Transaction Statement and pursuant to the terms of the Contribution Agreement between Green SEA Resources Inc. and GSR Acquisition Corp. (attached hereto asAppendix A), Green SEA Resources Inc. will contribute, among other things, all of its shares of common stock of NRUC to GSR Acquisition Corp. Because GSR Acquisition Corp. will own greater than 90% of the outstanding shares of NRUC following the contribution, GSR Acquisition Corp. will adopt a plan of merger prior to the mailing of the Transaction Statement (the form of which is attached hereto asAppendix B), whereby it will effect a “short form” merger and merge GSR Acquisition Corp. with and into NRUC, with NRUC being the surviving corporation, in accordance with Section 1104 of the URBC. Pursuant to the short-form merger, each outstanding share of common stock of NRUC (other than shares held by GSR Acquisition Corp.) will be entitled to receive cash in the amount of $0.57 per share, without interest. If you properly perfect your dissent rights, you will have the right to demand the fair value of your NRUC common stock. | |

| After the short-form merger, we intend to terminate the registration of the common stock of NRUC under the Exchange Act. | ||

| See “SPECIAL FACTORS—PURPOSES, ALTERNATIVES, REASONS AND EFFECTS OF THE SHORT-FORM MERGER—Effects,” “ADDITIONAL INFORMATION—Terms of the Transaction—Material Terms” and “ADDITIONAL | ||

3

| INFORMATION—Terms of the Transaction—Dissent Rights” in this Transaction Statement. | ||

| This Transaction Statement is being disseminated because the short-form merger is a Rule 13e-3 transaction as defined in Rule 13e-3 under the Exchange Act and in order to comply with Section 1104 of the URBC. | ||

Treatment of Option Holders | The plan of merger will provide that immediately prior to the closing of the short-form merger, all outstanding options (other than options owned by GSR), whether or not exercisable, will be cancelled in exchange for an amount in cash equal to the number of shares subject to each option times the excess, if any, of the merger consideration less the applicable exercise price of that option, less any required withholding taxes. All “out-of-the-money” options (i.e., the merger consideration is less than or equal to the applicable exercise price of an option) will be cancelled for no consideration. See “SPECIAL FACTORS—PURPOSES, ALTERNATIVES, REASONS AND EFFECTS OF THE SHORT-FORM MERGER—Effects—Treatment of options” and “ADDITIONAL INFORMATION—Terms of the Transaction—Material Terms” in this Transaction Statement. | |

Purpose of the Short-Form Merger | The purpose of the short-form merger is for us to acquire all of the shares of NRUC not directly owned by us, and to provide a source of immediate liquidity for the minority shareholders of NRUC. Additionally, following the closing of the short-form merger, we will deregister the NRUC common stock under the Exchange Act and eliminate any future reporting obligations of NRUC thereunder. See “SPECIAL FACTORS—PURPOSES, ALTERNATIVES, REASONS AND EFFECTS OF THE SHORT-FORM MERGER—Purposes” in this Transaction Statement. | |

Tax Consequences | In general, for United States federal income tax purposes, the short-form merger will be taxable to the minority shareholders of NRUC. See “SPECIAL FACTORS—CERTAIN U.S. FEDERAL INCOME TAX CONSIDERATIONS” in this Transaction Statement. | |

No Shareholder or Board Vote | Because GSR Acquisition Corp. will hold greater than 90% of the outstanding shares of each class of capital stock of NRUC following the transactions contemplated by the Contribution Agreement, we are entitled to effect the short-form merger without any vote of the shareholders or board of directors of NRUC, as permitted by Section 1104 of the URBC. See “SPECIAL FACTORS—FAIRNESS OF THE SHORT-FORM MERGER” and “ADDITIONAL INFORMATION—Terms of the Transaction—Material Terms” in this Transaction Statement. | |

Surrender of Certificates and Payment for Shares | You will be paid for your shares of NRUC common stock promptly after the effective date of the short-form merger. Instructions for surrendering your stock certificates to the paying agent in order to receive the merger consideration are set forth in a letter of transmittal (the “Letter of Transmittal”) that will be delivered to you by the paying agent promptly following the effectiveness of the short-form merger and which should be read carefully. Sending your stock certificates with a properly signed Letter of Transmittal will waive your dissent rights described below. See “ADDITIONAL INFORMATION— | |

4

| Terms of the Transaction—Material Terms” in this Transaction Statement. | ||

Source and Amount of Funds | The total amount of funds required to pay the merger consideration to the minority shareholders of NRUC, and to option holders of “in-the-money” options (other than GSR) and to pay related fees and expenses is estimated to be approximately $11,070,000. In connection with the short-form merger and pursuant to the Contribution Agreement, an affiliate of The Sentient Group will contribute funds sufficient to cover the merger consideration and the option consideration to Green SEA Resources Inc. which will contribute those funds to GSR Acquisition Corp. These funds are not subject to any financing condition. See “ADDITIONAL INFORMATION—Source and Amount of Funds or Other Consideration” in this Transaction Statement. | |

Fairness of the Short-Form Merger

GSR’s Position on the Fairness of the Short-Form Merger | We have determined that the short-form merger is both substantively and procedurally fair to the minority shareholders, including the unaffiliated shareholders. For the purposes of this Transaction Statement, the term “minority shareholders” means those holders of common stock of NRUC other than GSR, but including all unaffiliated shareholders. The term “unaffiliated shareholders” means those holders of less than 10% of the common stock of NRUC who are neither directors nor officers of NRUC. Each of our boards of directors also believe that the $0.57 per share consideration to be paid for shares of NRUC common stock is fair, from a financial point of view, to the minority shareholders, including the unaffiliated shareholders. In the course of reaching this determination, and in discussions with our advisors, we considered a number of factors that supported our decision, including the following: |

• GSR engaged Cutfield Freeman & Co Ltd. (“CF&Co”), an independent financial advisor, to conduct an independent valuation of NRUC, prepare a report regarding such valuation and provide an opinion in such report as to the fairness, from a financial point of view, to NRUC���s shareholders (other than GSR) of the merger consideration proposed by GSR to be received by such shareholders. The CF&Co valuation report and fairness opinion, effective as of August 1, 2011 and dated as of October 20, 2011 (the “Valuation Report and Fairness Opinion”), includes a valuation of $0.562 per share for the common stock held by the minority shareholders of NRUC and states that the amount of the merger consideration determined by GSR is fair, from a financial point of view, to the minority shareholders, including the unaffiliated shareholders, of NRUC. A copy of the | ||

5

Valuation Report and Fairness Opinion of CF&Co is attached to this Transaction Statement asAppendix C.

• CF&Co prepared the fair market value valuation of NRUC on a “sum-of-the-parts” basis, valuing each of NRUC’s three business interests on a stand-alone basis. The sodium bicarbonate business was valued on a discounted cash flow basis at $66 million. The water rights were valued at $54 million by discounting the value of a cash sale of the “core” water rights in five years and applying a probability weighting of concluding a transaction and valuing the conditional water rights based on an analysis of a structured sale, a sale to a municipality and certain precedent transactions. The oil shale deposits were valued based on two precedent transactions in the region at $76 million (including $47 million of water rights attributed to oil shale), reflecting option value over the contained oil and the related water rights. A balance sheet adjustment of $2 million was added for a total valuation of $198 million for NRUC, or $0.562 per share.

• The short-form merger represents an opportunity for the minority shareholders to receive (without the payment of any brokerage fees or commissions) cash for each share of NRUC common stock, at a price that may be otherwise difficult for the minority shareholders to receive given the limited liquidity of the NRUC common stock. The merger consideration provides certainty of value to the minority shareholders and immediate liquidity.

• The average daily trading volume for the common stock of NRUC for the three-month period prior to August 2, 2011, the last trading day prior to first public announcement of the short-form merger, was approximately 1400 shares. There is a limited trading market and limited liquidity for the NRUC common stock, and any third-party proposal to acquire the NRUC common stock would be unlikely to proceed without our consent as a result of our beneficial ownership of approximately 95% of the outstanding common stock of NRUC. As a result, it may be difficult for the minority shareholders to sell significant blocks of common stock of NRUC without adversely impacting the trading price.

• NRUC has incurred significant costs but not been able to realize many of the benefits that result from being a publicly traded company.

• The minority shareholders of NRUC are entitled to exercise dissent rights under the URBC and demand “fair value” for their shares, which may be more than the cash consideration offered in the short-form merger. |

6

• The short-form merger would shift the risk of future financial performance of NRUC from the minority shareholders entirely to GSR.

• We do not intend to sell our majority holdings in NRUC, and we do not intend to seek a buyer for NRUC in the foreseeable future.

• A greater than 90% shareholder of a Utah corporation has a statutory right under Section 1104 of the URBC to effect a short-form merger without any action by the corporation, its board of directors or its other shareholders. | ||

| See “SPECIAL FACTORS—FAIRNESS OF THE SHORT-FORM MERGER” in this Transaction Statement. | ||

Dissent Rights | You have a statutory right to dissent from the short-form merger and demand payment of the fair value of your NRUC common stock in accordance with Sections 1301, et seq. of the URBC, plus a fair rate of interest, if any, from the date of the consummation of the short-form merger. This value may be more than the $0.57 per share merger consideration. In order to qualify for these rights, you must make a written payment demand within 30 days after the mailing date of the Notice of Merger and Dissent Rights accompanying this Transaction Statement and otherwise comply with the procedures for exercising dissent rights set forth in the URBC. The statutory right of dissent is set out in Sections 1301, et seq. of the URBC, which are attached to this Transaction Statement asAppendix D. Any failure to comply with the statute’s terms will result in an irrevocable loss of such right. Shareholders seeking to exercise their statutory right of dissent are encouraged to readAppendix D in its entirety and seek advice from legal counsel. See “ADDITIONAL INFORMATION—Terms of the Transaction—Dissent Rights” in this Transaction Statement and the Notice of Merger and Dissent Rights accompanying this Transaction Statement. | |

Consequences of the Short-Form Merger

Effects of the Short-Form Merger | Completion of the short-form merger will have the following consequences: | |

• GSR Acquisition Corp. will be merged with and into NRUC, with NRUC being the surviving entity.

• Each of your shares of NRUC common stock will be cancelled and converted into the right to receive $0.57 in cash, without interest, brokerage fees or commissions, unless you properly exercise your statutory dissent rights under the URBC.

• All outstanding options (other than any options owned by GSR), whether or not exercisable, will be cancelled in exchange for an amount in cash equal to the number of shares subject to each option times the excess, if any, of the merger consideration less the applicable exercise price of that option, less any required withholding taxes. All |

7

“out-of-the-money” options (i.e., the merger consideration is less than or equal to the applicable exercise price of an option) will be cancelled for no consideration.

• NRUC will terminate the registration of its common stock under the Exchange Act and NRUC will no longer be subject to the reporting and other disclosure obligations of the Exchange Act, including requirements to file annual and other periodic reports or to provide the type of going-private disclosure contained in this Transaction Statement.

• Following the termination of NRUC’s obligations under the Exchange Act, NRUC will no longer incur the costs associated with being a public company, including associated legal, audit and other fees.

• We will have the exclusive opportunity to participate in the future earnings and growth, if any, of NRUC’s operations, but will bear the risk of losses that may result from NRUC’s operations or a decline in its value after the short-form merger. | ||

| See “SPECIAL FACTORS—PURPOSES, ALTERNATIVES, REASONS AND EFFECTS OF THE SHORT-FORM MERGER—Effects” in this Transaction Statement. | ||

For More Information | You may read and copy any of the documents incorporated by reference at the public reference room of the SEC at 100 F Street, N.E., Washington, D.C. 20549. Please call the Securities and Exchange Commission at 1-800-SEC-0330 for further information on the public reference room. These SEC filings are also available to the public from commercial document retrieval services and at the SEC’s Internet web site at www.sec.gov. See “ADDITIONAL INFORMATION—Information about NRUC,” and “ADDITIONAL INFORMATION—Identity and Background of GSR, SURF and the Sentient General Partner” in this Transaction Statement. | |

| If you have any questions about the going-private transaction, please call D’Arcy P. Doherty, Vice President, Legal and General Counsel of Green SEA Resources Inc., at 416-649-9283. | ||

8

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Transaction Statement and the documents incorporated by reference in this Transaction Statement, including NRUC’s Amended Transition Report on Form 10-KT/A for the transition period from July 1, 2010 to December 31, 2010 filed with the SEC on September 14, 2011; NRUC’s Quarterly Reports on Forms 10-Q for the quarters ended March 31, 2011 and June 30, 2011 each filed with the SEC on October 20, 2011 and NRUC’s Quarterly Report on Form 10-Q for the quarter ended September 30, 2011 filed with the SEC on November 14, 2011; and the Valuation Report and Fairness Opinion, include certain forward–looking statements. These statements appear throughout this Transaction Statement and include statements regarding the intent, belief, or current expectations of GSR, including statements concerning GSR’s strategies following completion of the short-form merger. Such forward–looking statements are not guarantees of future performance and involve risks and uncertainties. Actual results may differ materially from those described in such forward–looking statements as a result of various factors, such as positions and strategies of competitors; cash availability/liquidity; the risks inherent with predicting cash flows, revenue and earnings outcomes, as well as all other factors identified in the “Risk Factors” sections included in NRUC’s Amended Transition Report on Form 10-KT/A for the transition period ended December 31, 2010, and as otherwise described in NRUC’s filings with the SEC from time to time.

Pursuant to Section 21E(b)(1)(E) of the Exchange Act, the safe harbor provisions of the Private Securities Litigation Reform Act of 1995 do not apply to statements made in connection with a going-private transaction. As such, the safe harbor provisions in NRUC’s Amended Transition Report on Form 10-KT/A for the transition period ended December 31, 2010 filed with the SEC on September 14, 2011, NRUC’s Quarterly Reports on Forms 10-Q for the quarters ended March 31, 2011 and June 30, 2011 each filed with the SEC on October 20, 2011 and NRUC’s Quarterly Report on Form 10-Q for the quarter ended September 30, 2011 filed with the SEC on November 14, 2011 do not apply to any forward-looking statements we made in connection with the going-private transaction.

SPECIAL FACTORS

PURPOSES, ALTERNATIVES, REASONS AND EFFECTS OF THE SHORT-FORM MERGER

Background of the Short-Form Merger

Prior to May 2007, AmerAlia, Inc. (now NRUC) owned 100% of the outstanding common stock of Natural Soda Holdings, Inc., which in turn owned 100% of the outstanding common stock of Natural Soda, Inc. (“NSI”). NSI is an operating company that produces and sells sodium bicarbonate (baking soda).

In 2003, a trust and a fund managed by Sentient Asset Management (the “Sentient Entities”) provided Natural Soda Holdings, Inc. with short-term debt financing which was refinanced on a long-term basis in 2004. In May 2007, the Sentient Entities converted a portion of the debt owed by Natural Soda Holdings, Inc. and NSI into a 53.5% equity interest in NSI. In August 2007, the Sentient Entities purchased approximately 46% of the equity in AmerAlia, Inc. from a major shareholder of AmerAlia, Inc., and also acquired additional debt obligations of AmerAlia, Inc. from the same major shareholder.

As part of a restructuring transaction in October 2008:

| • | the Sentient Entities transferred their various interests to Sentient USA Resources Fund, L.P. (“SURF”); |

| • | NSI became a wholly-owned subsidiary of Natural Soda Holdings, Inc.; |

| • | SURF converted its loans to Natural Soda Holdings, Inc. into Natural Soda Holdings, Inc. equity and AmerAlia, Inc.’s ownership in Natural Soda Holdings, Inc. was reduced from 100% to 18%; and |

| • | SURF converted its loans to AmerAlia, Inc. into additional common stock of AmerAlia, Inc. |

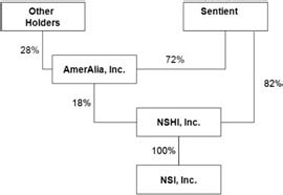

This reorganization resulted in the ownership structure shown below.

9

In connection with this restructuring, AmerAlia, Inc., also received approximately $10 million in cash, settled approximately $12 million of debt, terminated indemnification rights relating to the extinguishment of an AmerAlia, Inc. $9.9 million bank loan and extinguished other obligations in exchange for the issue of 48,961,439 shares of its common stock.

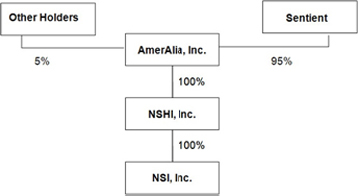

Finally, on June 30, 2010, AmerAlia, Inc. issued 286,119,886 shares of its common stock to SURF in exchange for the 82% of Natural Soda Holdings, Inc. SURF held with the following resulting structure shown below.

On September 14, 2010 at a Special Meeting of the Shareholders of AmerAlia, Inc., the shareholders approved the amendment of the articles of incorporation to change the name of AmerAlia, Inc. to Natural Resources USA Corporation.

On March 15, 2011, SURF entered into an Exchange Agreement and Plan of Reorganization (the “Exchange Agreement”) with Green SEA Resources Inc. Pursuant to the Exchange Agreement, SURF exchanged all of its ownership in NRUC for 20,084,954 common shares of Green SEA Resources Inc. The interests of NRUC that were exchanged were (i) all of the shares of common stock of NRUC owned by SURF, a total of 334,074,381 shares of common stock, plus (ii) a limited option to acquire up to 5,500,000 shares of common stock of NRUC.

On June 14, 2011, the investment committee of the board of directors of Green SEA Resources Inc. held a meeting to consider whether to explore taking NRUC private. At the meeting, Green SEA Resources Inc.’s U.S. legal advisors reviewed with the investment committee various alternative transaction structures to effect a going-private transaction of NRUC. It was determined that Green SEA Resources Inc. should retain an independent financial advisor to conduct an independent valuation of NRUC, and CF&Co was selected as such advisor.

On June 24, 2011, Green SEA Resources Inc. retained CF&Co as its financial advisor to conduct an independent valuation of NRUC.

On August 2, 2011, the investment committee of the board of directors of Green SEA Resources Inc. held a meeting to consider the potential benefits of taking NRUC private. At the meeting, representatives of CF&Co reviewed their valuation of NRUC. Following discussion and after management of Green SEA Resources Inc.

10

assessed the reasonableness of the assumptions underlying CF&Co’s valuation, the investment committee voted unanimously to approve and recommend to the board of directors of Green SEA Resources Inc. that it effect a going-private transaction pursuant to a short-form merger.

On August 2, 2011, GSR Acquisition Corp. was incorporated as a Utah corporation.

On August 3, 2011, we filed Amendment No. 10 to Schedule 13D with the SEC disclosing the intention of the investment committee of the board of directors of Green SEA Resources Inc. to recommend to the board of directors of Green SEA Resources Inc. that it effect the going-private transaction pursuant to a short-form merger.

On August 7, 2011, the board of directors of Green SEA Resources Inc. held a meeting to consider the approval of, among other things, the going-private transaction pursuant to a short-form merger under Utah law. Present at the meeting were the board of directors, members of management of Green SEA Resources Inc., CF&Co and certain of Green SEA Resources Inc.’s legal advisors. At this meeting, Green SEA Resources Inc.’s U.S. legal advisors reviewed with the board of directors the terms of the Contribution Agreement and plan of merger and the other agreements and forms to be filed in connection with a going-private transaction. At this meeting, representatives of CF&Co presented to the board of directors its initial financial analysis with respect to their valuation of NRUC and rendered to the board of directors a written fairness opinion, effective August 1, 2011, stating that the $0.57 per share merger consideration proposed by GSR to be provided to the minority shareholders, including the unaffiliated shareholders, was fair, from a financial point of view, to such shareholders. Following discussion, all of the members of the board of directors of Green SEA Resources Inc., other than William Gunn (who was a member of the board at this time and abstained from the vote as a result of his position as Chief Executive Officer of NRUC), approved the terms and provisions of, and the transactions contemplated by, the short-form merger, including the Contribution Agreement and plan of merger.

All of the directors of GSR Acquisition Corp. were present at the meeting of the board of directors of Green SEA Resources Inc. held on August 7, 2011 in their capacities as directors and/or members of management of Green SEA Resources Inc., as applicable. The short-form merger and related transaction agreements were also approved by the board of directors of GSR Acquisition Corp. by written consent on August 7, 2011.

On August 8, 2011, we filed a Schedule 13E-3, and Amendment No. 11 to Schedule 13D with the SEC relating to the going-private transaction pursuant to a short-form merger.

On September 14, 2011, NRUC filed an Amended Transition Report on Form 10-KT/A for the transition period ended December 31, 2010 with the SEC to amend and restate its audited consolidated financial statements and related disclosures. Following such restatement, the evaluation of certain income tax filings of NRUC, and the filing of NRUC’s financial statements for the quarters ended March 31 and June 30, 2011, CF&Co, at the request of GSR, updated its initial financial analysis and fairness opinion, as reflected in the Valuation Report and Fairness Opinion, to reflect a decrease in the valuation of NRUC’s sodium bicarbonate business by $1 million, and a reduction in the overall valuation of NRUC from $0.565 per share to $0.562 per share from CF&Co’s initial analysis. The amount of such reduction in the overall value of NRUC was considered to be immaterial and we determined not to alter the consideration being offered in connection with the going-private transaction.

Purposes

The purpose of the short-form merger is to allow us to acquire the minority interest in NRUC. The short-form merger will also provide a source of immediate liquidity for the minority shareholders of NRUC. This transaction will also allow us to terminate the registration of NRUC’s common stock under the Exchange Act. Following the reorganization and transfer of NRUC ownership to Green SEA Resources Inc. pursuant to the Exchange Agreement, management of Green SEA Resources Inc. began to consider the advantages and disadvantages of continuing NRUC as a public company, the costs associated with operating NRUC as a public company and compliance issues relating to NRUC’s reporting obligations under the Exchange Act. We believe that, from NRUC’s perspective, the short-form merger is desirable because it will relieve NRUC of the substantial costs of remaining a public company with reporting requirements. As evidenced by the late filings of NRUC’s Quarterly Reports on Form 10-Q for the quarters ended March 31 and June 30, 2011 and the quotation of NRUC’s stock ceasing on the Over-the-Counter Bulletin Board (the “OTC Bulletin Board”) on June 6, 2011 due to such late filings, we believe NRUC is currently

11

experiencing difficulties with complying with its reporting obligations under the Exchange Act. Because of the limited internal resources and personnel currently available at NRUC to attend to Exchange Act compliance and reporting matters, we believe that similar deficiencies would likely continue to occur if NRUC were to remain a public company without dedicating additional internal resources to such matters. The direct and indirect costs associated with NRUC’s compliance with the filing and reporting requirements of the Exchange Act have an adverse effect on NRUC’s financial performance, and the various costs associated with remaining a public company are expected to remain substantial and possibly increase as a result of recent legislative and regulatory initiatives to improve corporate governance. We believe that, from NRUC’s perspective, such costs create a burden that adversely impacts NRUC’s ability to efficiently and profitably operate its business.

The most recent NRUC consolidated financial statements show annual general and administrative expenses of approximately $4.7 million per annum. We estimate the cost savings to NRUC will be approximately $1.5 million per annum on an ongoing basis if NRUC is no longer a public company subject to the reporting requirements of the Exchange Act and other overhead expenses associated with being a public company.

Based on NRUC’s size and resources, we do not believe the costs associated with NRUC remaining a public company are justified for NRUC. In light of these disproportionate costs, we believe that it is desirable for NRUC to eliminate the administrative, legal and financial burden of NRUC remaining a public company subject to the reporting requirements of the Exchange Act.

Alternatives

We believe that using a short-form merger to effect the going-private transaction is the quickest and most cost effective way for us to acquire the outstanding minority interest in NRUC, and will provide such holders of NRUC common stock with immediate liquidity which otherwise may not be available. We considered and rejected various alternative transactions to accomplish the proposed going-private transaction, as described below, and determined to effect a short-form merger as it is legally permissible under Utah law and affords minority shareholders dissent rights to demand fair value for their shares of NRUC common stock. The alternatives considered included:

Long-form Merger. We considered and rejected the alternative of a long-form merger because of the additional cost and delay likely associated with such a transaction. We would expect a long-form merger to require additional time to close as it would require a special committee of the board of NRUC and a vote of the NRUC shareholders, which in contrast is not required under Utah law for the short-form merger. The added time required to establish a special committee and hold a shareholder meeting would create additional third-party costs, such as additional legal and other advisory fees and expenses, which we estimate could be approximately $750,000 to $1 million in excess of the costs associated with the short-form merger. Additionally, if a long-form merger was not successfully consummated, we could still effect a short-form merger.

Tender Offer. We also considered a tender offer to purchase all of the NRUC common stock held by minority shareholders. If we were to structure the transaction as a tender offer, it is unlikely that all of the minority shareholders would tender their shares and, therefore, we would need to effect a short-form merger following the tender offer process (which is customary in these types of transactions). As a result, we estimated that we would need to pay approximately $750,000 to $1 million in excess of the costs associated with the short-form merger because of the additional legal, filing and other third-party fees associated therewith. This alternative was rejected based upon the additional cost and delay likely resulting from a failure of all of the minority shareholders to tender their shares.

Asset Purchase. We also rejected the purchase of the assets of NRUC for similar reasons to those provided in connection with the evaluation of a long-form merger.

Reasons

In determining whether to effect the short-form merger, we considered several factors, including:

| • | the valuation analysis that CF&Co performed; |

| • | the fairness opinion that CF&Co delivered finding that the $0.57 per share merger consideration proposed by GSR to be received by the minority shareholders, including the unaffiliated shareholders, is fair, from a financial point of view, to such shareholders; |

| • | the elimination of additional burdens on management associated with public reporting and other tasks resulting from NRUC’s public company status, including, for example, the dedication of time and resources of NRUC’s management and board of directors to comply with the Sarbanes-Oxley Act of 2002 (“Sarbanes-Oxley”) and shareholder, investor and public relations; |

| • | the significant decrease in costs, particularly those associated with being a public company (for example, as a privately-held entity, NRUC would no longer be required to file quarterly, annual or other periodic reports with the SEC, publish and distribute to its shareholders annual reports and proxy statements or be subject to various Sarbanes-Oxley related requirements), that we anticipate could result in significant cost savings; |

| • | the elimination of certain impediments to obtaining capital that can be used to support NRUC’s undertakings to grow its operations through the acquisition of existing businesses; and |

| • | recent public capital market trends affecting small-cap companies, including perceived lack of interest by institutional investors in companies with a limited public float and reduced liquidity due to the recent economic downturn. |

12

In our view, there are no significant advantages to leaving NRUC as a public company. The disadvantages of leaving NRUC as a public company are the high costs and substantial burdens of maintaining NRUC’s status as a public company without the ability to achieve meaningful benefits from such status.

We determined to effect the short-form merger as promptly as practicable because we wish to immediately realize the benefits of taking NRUC private. The short-form merger allows the minority shareholders to receive cash for their shares of NRUC common stock quickly and allows us to merge GSR Acquisition Corp. with and into NRUC without any action by the board of directors of NRUC or the minority shareholders.

Effects

General. Upon completion of the short-form merger, we will receive the entire right to participate in any and all future increases in the value of NRUC’s business, and we will bear the entire risk of any losses incurred in the operation of NRUC’s business and any decrease in the value of NRUC’s business, including any increases and decreases in the net book value and net earnings of NRUC. Once the short-form merger is completed, the minority shareholders will no longer be able to benefit from a sale of NRUC to a third-party (although no third-party sale is contemplated at this time). From NRUC’s perspective, after the short-form merger, NRUC’s operations and management will be under the exclusive control of GSR.

Shareholders other than GSR. Upon completion of the short-form merger, the minority shareholders will no longer have any interest in, and will not be shareholders of, NRUC and, therefore, will not participate in NRUC’s future earnings and potential growth. In addition, the minority shareholders will not share in any distribution of proceeds after any sales of businesses of NRUC. All of the minority shareholders’ other indicia of stock ownership, such as the rights to vote on certain corporate decisions, to vote on the election of directors, to receive distributions upon the liquidation of NRUC and to receive dissent rights upon certain mergers or consolidations of NRUC (unless such dissent rights are perfected in connection with the short-form merger), as well as the benefit of potential increases in the value of a minority shareholder’s holdings in NRUC based on any improvements in NRUC’s future performance, will be extinguished upon completion of the short-form merger.

Upon completion of the short-form merger, the minority shareholders also will not bear the risks of potential decreases in the value of their holdings in NRUC based on any downturns in NRUC’s future performance or the stock market. Instead, the minority shareholders will have liquidity in the form of the merger consideration in place of an ongoing equity interest in NRUC.

The shares of NRUC Common Stock. If the short-form merger is consummated, public trading of the shares of NRUC common stock will cease. The NRUC common stock recently ceased being quoted on the OTC Bulletin Board. Following the short-form merger, we intend to deregister the NRUC common stock under the Exchange Act. As a result, NRUC will no longer be required under the federal securities laws to file reports with the SEC and will no longer be subject to the proxy rules under the Exchange Act. In addition, the principal shareholders of NRUC will no longer be subject to the reporting and short swing profit provisions of Section 16 of the Exchange Act.

Treatment of Options. In connection with and immediately prior to the consummation of the short-form merger, we will take steps to accelerate the vesting of all unvested options to purchase NRUC common stock. All unexercised options (other than any options owned by GSR) that are “in the money” (meaning that the per-share exercise price is less than the per-share merger consideration) immediately prior to the consummation of the short-form merger will be converted into the right to receive an amount equal to the short-form merger consideration of $0.57 per share subject to such options, minus the exercise price per option, less any required withholding taxes. All unexercised options that are “underwater” (meaning that the exercise price is greater than or equal to the merger consideration) immediately prior to the consummation of the short-form merger will be cancelled without payment.

Directors. The boards of directors of each of Green SEA Resources Inc. and GSR Acquisition Corp. consist of the persons listed inSchedule I to this Transaction Statement.

CERTAIN U.S. FEDERAL INCOME TAX CONSIDERATIONS

The following is a summary of certain material U.S. federal income tax considerations applicable to minority shareholders who are U.S. Shareholders (as defined below) relating to the short-form merger. This summary is based upon the United States Internal Revenue Code of 1986, as amended (the “Code”), Treasury Regulations, administrative pronouncements, and judicial decisions, in each case as in effect on the date hereof, all of which are

13

subject to change (possibly with retroactive effect). No ruling will be requested from the U.S. Internal Revenue Service (the “IRS”) regarding the tax consequences of the short-form merger and there can be no assurance that the IRS will agree with the discussion set forth below. The discussion does not address aspects of U.S. federal taxation other than income taxation, nor does it address aspects of U.S. federal income taxation that may be applicable to particular shareholders, including but not limited to shareholders who are dealers in securities, life insurance companies, tax-exempt organizations, banks, foreign persons, persons who hold shares through partnerships or other pass-through entities, persons who own, directly or indirectly, 5% or more, by voting power or value, of the outstanding shares, persons whose functional currency is not the U.S. dollar or who acquired their shares in a compensatory transaction and persons who hold shares as part of a straddle, hedge, constructive sale or other integrated transaction for tax purposes. This summary is limited to persons who hold their shares as a “capital asset” within the meaning of Section 1221 of the Code. The discussion also does not address the U.S. federal income tax consequences to holders of options to purchase shares or holders of stock or securities convertible or exchangeable into shares. In addition, it does not address state, local or foreign tax consequences. U.S. Shareholders are urged to consult their tax advisors with respect to the United States federal, state, local and foreign tax consequences to their particular situations of the short-form merger or other transactions described this Transaction Statement.

This summary is of a general nature only and is not intended to be, and should not be construed to be, legal, business or tax advice to any particular shareholder. Each U.S. Shareholder should seek tax advice based on such U.S. Shareholder’s particular circumstances from an independent tax advisor.

As used herein, the term “U.S. Shareholder” means a beneficial owner of shares that is, for United States federal income tax purposes (i) a citizen or resident of the United States; (ii) a corporation, or other entity taxable as a corporation, created or organized under the laws of the United States or any political subdivision thereof or therein; (iii) an estate the income of which is subject to United States federal income taxation regardless of its source; or (iv) a trust if a U.S. court is able to exercise primary jurisdiction over administration of the trust and one or more U.S. persons have authority to control all substantial decisions of the trust, or the trust has elected to be treated as a U.S. person.

If a partnership is a beneficial owner of the shares, the tax treatment of a partner will generally depend upon the status of the partner and the activities of the partnership. If you are a partner of a partnership that holds the shares, you should consult your tax advisor regarding the tax consequences of the short-form merger.

The receipt of cash by a U.S. Shareholder pursuant to the short-form merger or pursuant to the U.S. Shareholder’s statutory dissenters rights, will be a taxable transaction for U.S. federal income tax purposes. A U.S. Shareholder will generally recognize U.S. source capital gain or loss on the disposition of shares equal to the difference, if any, between the amount of cash the U.S. Shareholder receives in the short-form merger and the U.S. Shareholder’s adjusted tax basis in the shares. A U.S. Shareholder’s basis in a share will generally be the cost at which it was purchased. Capital gain or loss will be long-term capital gain or loss if the U.S. Shareholder held the shares for more than one year at the time of disposition. Long-term capital gain recognized by a U.S. Shareholder that is an individual, estate or trust will be taxable at a maximum rate of 15%. No reduced rate applies to capital gain recognized by a U.S. Shareholder that is a corporation. For all U.S. Shareholders, capital losses are generally deductible only against capital gains and not against ordinary income. In the case of an individual, the aggregate amount of capital losses in excess of capital gains may offset up to $3,000 annually of ordinary income.

Information Reporting and Backup Withholding Tax

Payments to certain U.S. Shareholders of the proceeds of the sale of the shares may be subject to information reporting and U.S. federal backup withholding tax at the rate of 28% (subject to periodic adjustment) if the U.S. Shareholder fails to supply an accurate taxpayer identification number or otherwise fails to comply with applicable U.S. information reporting or certification requirements. Any amount withheld from a payment to a U.S. Shareholder under the backup withholding rules is allowable as a credit against the U.S. Shareholder’s U.S. federal income tax, provided that the required information is furnished to the IRS.

Each U.S. Shareholder should seek U.S. federal tax advice, based on such U.S. Shareholder’s particular circumstances, from an independent tax advisor.

14

FAIRNESS OF THE SHORT-FORM MERGER

Fairness. Green SEA Resources Inc. beneficially owns approximately 95% of the outstanding common stock of NRUC. Thus, Green SEA Resources Inc. may be deemed an “affiliate” of NRUC within the meaning of Rule 13e-3 under the Exchange Act. Accordingly, the rules of the SEC require us to express our reasonable belief as to the substantive and procedural fairness of the short-form merger to the minority shareholders, including the unaffiliated shareholders, of NRUC. In compliance with Rule 13e-3 under the Exchange Act, each of the boards of directors of Green SEA Resources Inc. and GSR Acquisition Corp. have considered the fairness of the short-form merger to the minority shareholders, including the unaffiliated shareholders, and concluded that the short-form merger is both substantively and procedurally fair to them and that at least fair value is being paid for the NRUC common stock.

Factors considered in determining fairness. In reaching the determination that the short-form merger is substantively and procedurally fair to the minority shareholders, including the unaffiliated shareholders, each of the boards of directors of Green SEA Resources Inc. and GSR Acquisition Corp. considered the following material factors:

| • | Financial Analyses Performed by CF&Co.CF&Co, an independent financial advisor, conducted an independent analysis of the value of the NRUC common stock resulting from the application of various valuation methodologies, and prepared a Valuation Report and Fairness Opinion. The Valuation Report and Fairness Opinion incorporates the restatement of NRUC’s audited consolidated financial statements for the transition period ended December 31, 2010, the evaluation of certain income tax filings of NRUC, and the preparation of NRUC’s financial statements for the quarters ended March 31 and June 30, 2011. The restatement of NRUC’s financial statements resulted in a total reduction of $2,943,341 in net income after tax as of December 31, 2010 and did not materially change the amount of the balance sheet adjustment included in CF&Co’s initial analysis that was performed prior to the restatement and quarterly filings. An evaluation relating to the restatement of NRUC’s financial statements and certain income tax filings of NRUC clarified that NSI is expected to pay more taxes than previously forecasted in future periods due to a reduction in tax losses specifically related to NSI resulting in a reduction in the value of NRUC’s sodium bicarbonate business by $1 million, according to CF&Co. The amount of such reduction is considered to be immaterial to the overall value of NRUC and we determined not to alter the consideration originally offered in connection with the going-private transaction as a result of the restatement, the evaluation of certain income tax filings and the quarterly filings. The restatement of NRUC’s financial statements also resulted in an increased amount of NRUC tax losses. These additional tax losses, however, are not being utilized for purposes of valuing NRUC because we believe that NRUC will have already exceeded the cumulative tax loss carry forward limit in the U.S. based on the amount of tax losses already included in CF&Co’s initial analysis. These factors do not alter the analysis of CF&Co, or the analysis of either of the boards of directors of Green SEA Resources Inc. and GSR Acquisition Corp., regarding whether the consideration to be provided is fair because the restatement and the financial statements for the quarters ended March 31 and June 30, 2011 resulted in an immaterial decrease in the valuation of NRUC. |

CF&Co prepared the valuation of NRUC on a “sum-of-the-parts” basis, valuing each of NRUC’s three business interests on a stand-alone basis. The sodium bicarbonate business was valued on a discounted cash flow basis at $66 million. The water rights were valued at $54 million by discounting the value of a cash sale of the “core” water rights in five years and applying a probability weighting of concluding a transaction and valuing the conditional water rights based on an analysis of a structured sale, a sale to a municipality and certain precedent transactions. The oil shale deposits were valued based on two precedent transactions in the region at $76 million (including $47 million of water rights attributed to oil shale), reflecting option value over the contained oil and the related water rights. A balance sheet adjustment of $2 million was added for a total valuation of $198 million for NRUC, or $0.562 per share.

Each of the boards of directors of Green SEA Resources Inc. and GSR Acquisition Corp. has adopted the financial analyses of CF&Co and utilized these analyses as one of the material factors used in reaching the determination that the short-form merger is substantively and procedurally fair to the

15

minority shareholders, including the unaffiliated shareholders. For a more detailed discussion of the financial analyses performed by CF&Co, see “—Details of the Financial Analyses” below.

| • | Fairness Opinion of CF&Co. As described in “REPORTS, OPINIONS, APPRAISALS AND NEGOTIATIONS—Valuation Report and Fairness Opinion by CF&Co” below, CF&Co provided a fairness opinion to GSR dated effective August 1, 2011 determining that the $0.57 per share merger consideration to be paid to the minority shareholders, including the unaffiliated shareholders, in connection with the short-form merger is fair from a financial point of view. A copy of CF&Co’s fairness opinion is included in the Valuation Report and Fairness Opinion that is attached hereto asAppendix C. Each of the boards of directors of Green SEA Resources Inc. and GSR Acquisition Corp. has adopted the fairness opinion of CF&Co and utilized the fairness opinion as one of the material factors used in reaching the determination that the short-form merger is substantively and procedurally fair to the minority shareholders, including the unaffiliated shareholders. The restatement of NRUC’s financial statements, the evaluation of certain income tax filings of NRUC, and the financial statements for the quarters ended March 31 and June 30, 2011, did not alter the analysis, or the fairness opinion, of CF&Co, or the analysis of either of the boards of directors of Green SEA Resources Inc. and GSR Acquisition Corp., regarding whether the consideration to be provided is fair because such factors resulted in an immaterial decrease in the valuation of NRUC. |

| • | Cash payment for stock. The merger allows the minority shareholders, including the unaffiliated shareholders, to realize (without the payment of any brokerage fees or commissions) $0.57 per share in cash for their shares of common stock of NRUC, a price that may otherwise be difficult for the minority shareholders, including the unaffiliated shareholders, of NRUC to attain given the lack of liquidity in the common stock of NRUC. The merger consideration provides certainty of value to the minority shareholders, including the unaffiliated shareholders, and immediate liquidity. |

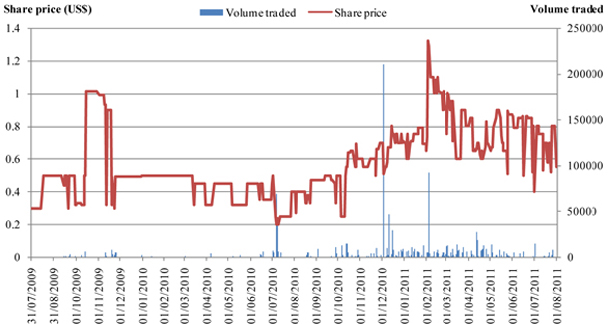

| • | Limited Trading Market and Liquidity/Market Prices.Each of the boards of directors considered the fact that there is a limited trading market and limited liquidity for NRUC common stock (the average daily trading volume during the three-month period prior to August 2, 2011, the last trading day prior to the first public announcement of the short-form merger, was approximately 1400 shares), and any proposal to acquire the shares by an independent entity would be unlikely to proceed without our consent due to our beneficial ownership of approximately 95% of the outstanding common stock of NRUC. Accordingly, we believe that it may be difficult for the minority shareholders, including the unaffiliated shareholders, to sell significant blocks of common stock of NRUC without adversely impacting the trading price. Additionally, even though the high share prices of NRUC common stock during the first, second and third quarters of 2011 were $1.32, $0.90 and $0.80, respectively, we believe that the over-the-counter trading market for NRUC shares is not a reliable basis for valuation. As noted above, NRUC’s shares are thinly traded on the Pink Sheets with a wide bid-ask spread and the trading market is susceptible to large movements on very small trades. Further, to the best of our knowledge NRUC’s common stock is not covered by securities analysts. |

| • | Limited Public Company Benefits.NRUC has incurred significant costs but has not been able to realize many of the benefits that result from being a publicly traded company as a result of the limited liquidity and low trading price of its common stock. We believe that such factors have and will continue to have an adverse impact on the trading price of shares of NRUC’s common stock. |

| • | Dissent Rights. Although the short-form merger does not require the approval of a majority of the minority shareholders (we note that no vote of the minority or unaffiliated shareholders is required to effect the short-form merger), or an unaffiliated representative of the minority or unaffiliated shareholders to negotiate on their behalf, or a special committee of NRUC directors appointed to evaluate the short-form merger, each of the boards of directors of Green SEA Resources Inc. and GSR Acquisition Corp. believe that the short-form merger is procedurally fair to the minority shareholders, including the unaffiliated shareholders, because the minority shareholders, including the unaffiliated shareholders, are entitled to exercise dissent rights and demand “fair value” for their shares of NRUC common stock. State law provides minority shareholders, including the unaffiliated shareholders, with an opportunity to seek “fair value” of their shares of NRUC common stock if they believe they are not receiving fair value pursuant to the short-form merger. See “ADDITIONAL INFORMATION—Terms of the Transaction—Dissent Rights” in this Transaction Statement. |

16

| • | Elimination of Future Financial Performance Risks of NRUC. The short-form merger would shift the risk of the future financial performance of NRUC entirely to Green SEA Resources Inc. who has the power to control NRUC’s business. In addition, the short-form merger would eliminate the exposure of the minority shareholders, including the unaffiliated shareholders, to any future declines in the price of the shares of NRUC common stock. |

| • | No Third-Party Offers.We do not intend to sell our majority holdings in NRUC, and we do not intend to seek a buyer for NRUC in the foreseeable future. These facts foreclosed the opportunity to consider an alternative transaction with a third-party purchaser of NRUC or otherwise provide liquidity in the form of a third-party offer to the minority shareholders, including the unaffiliated shareholders. |

| • | Net Book Value Multiple Valuation.Neither of the boards of directors of Green SEA Resources Inc. and GSR Acquisition Corp. valued NRUC based upon a multiple of its net book value because net book value multiples are traditionally not utilized to value companies in industries such as NRUC’s but rather are often used as a valuation method with respect to companies in the financial industry. |

| • | Going Concern Value. A primary aspect of a going concern valuation is the discounted cash flow methodology, which was used in connection with the financial analyses performed by CF&Co discussed in this Transaction Statement. See “FAIRNESS OF THE SHORT-FORM MERGER—Details of the Financial Analyses” and CF&Co’s Amended and Restated Valuation Report and Fairness Opinion attached hereto asAppendix C. |

| • | Liquidation Value Analysis. Neither the board of directors of Green SEA Resources Inc. nor the board of directors of GSR Acquisition Corp. considered implied liquidation value of NRUC because we do not intend to sell our majority holdings in NRUC, and we do not intend to seek a buyer for NRUC in the foreseeable future. |

| • | Restatement of Financial Statements. On September 14, 2011, NRUC restated its financial statements for the transition period ended December 31, 2010. The restatement resulted in a total reduction of $2,943,341 in net income after tax as of December 31, 2010. The restatement did not materially change the amount of the balance sheet adjustment included in the CF&Co valuation. The restatement does not alter the analysis of CF&Co, or the analysis of the boards of directors of Green SEA Resources Inc. and GSR Acquisition Corp., regarding whether the merger consideration to be provided is fair because the restatement resulted in an immaterial decrease in the valuation of NRUC. |

Factors not considered in determining fairness.Neither of the boards of directors of Green SEA Resources Inc. and GSR Acquisition Corp. considered the following factors to be material in determining the fairness of the short-form merger:

| • | Firm Offers. We are not aware of any firm offers to purchase NRUC that have been made during the past two years by any unaffiliated person. |

| • | Merger, Sale or Sale of Assets. NRUC has not engaged in a merger or sale process (including a sale of all or substantially all of its assets) in the past two years. |

| • | Acquisition of Control. No third-party can acquire control of NRUC without negotiating with us because of our majority ownership of NRUC. |

Details of the Financial Analyses. In producing the valuation included in the Valuation Report and Fairness Opinion, CF&Co conducted the following analyses. The full text of CF&Co’s Valuation Report and Fairness Opinion dated effective as of August 1, 2011 and dated as of October 20, 2011, which sets forth the assumptions made, matters considered and limitations of the analyses undertaken is attached hereto asAppendix C and is incorporated herein by reference. Holders of NRUC shares are urged to, and should, read the Valuation Report and Fairness Opinion carefully and in its entirety in connection with the short-form merger.

| • | CF&Co prepared the fair market value valuation of NRUC on a “sum-of-the-parts” basis, valuing each of NRUC’s three business interests on a stand-alone basis, for a total value of $198 million. |

17

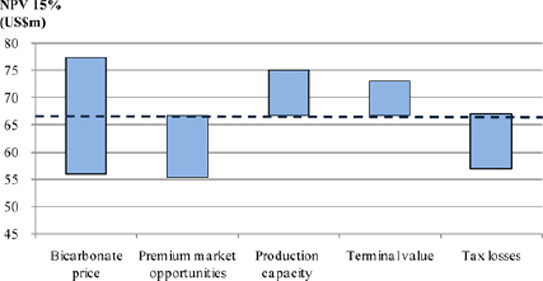

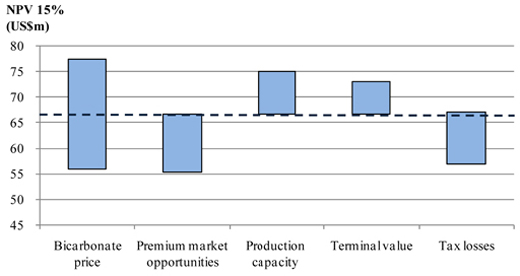

(1) The sodium bicarbonate business of NRUC, which is an operating business, was valued on a discounted cash flow basis at $66 million. CF&Co used a 15% discount rate for the existing operation and base case expansion, which is consistent with CF&Co’s calculation of NRUC’s weighted average cost of capital. CF&Co used a 20% discount rate for assessing potential premium market opportunities. CF&Co included in its analysis a discounted terminal value calculated by applying an appropriate multiple to projected 2030 earnings before interest, taxes, depreciation and amortization (as determined by CF&Co). The valuation of the sodium bicarbonate business was cross-checked against market multiples (enterprise value/EBITDA and price/earnings) relative to certain comparable companies.

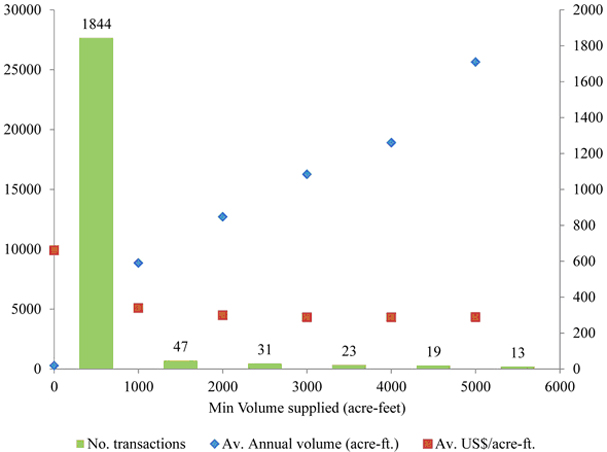

(2) The water rights were valued at $54 million by discounting the value of a cash sale of the “core” water rights in five years and applying a probability weighting of concluding a transaction and valuing the conditional water rights based on an analysis of a structured sale, a sale to a municipality and certain precedent transactions. CF&Co evaluated data from over 2,000 water rights transactions in Colorado over a period of approximately 20 years in connection with its analysis.

Each of the filing persons believe that the CF&Co valuation is consistent with the disclosures provided by NRUC with respect to the future value of its water rights because the value is subject to a number of risks that should be appropriately discounted, including the risk that such rights are not currently saleable. As a result, the CF&Co valuation discounted the value of the water rights to reflect what a buyer might pay to acquire the assets today based upon the small number of potential buyers available and political, legal, environmental and technical issues relating to the oil shale industry, and the difficulties and uncertainties inherent in concluding such a sale.

(3) The oil shale deposits in the leases held by NRUC were valued based on two precedent transactions in the region at $76 million (including $47 million of water rights attributed to oil shale), reflecting option value over the contained oil and the related water rights. The large potential value in the oil shale was balanced against the early stage of development and the unproven extraction technology. Additionally, in this market, the majority of oil shale projects are owned by larger international oil companies that do not transact in this market. As a result, it is not unusual to only rely on two precedent transactions of a comparable size and scope.

| • | A balance sheet adjustment of $2 million was added for a total valuation of $198 million for NRUC, or $0.562 per share. The CF&Co valuation of NRUC’s three business interests on a stand-alone basis provides an enterprise value and requires an adjustment to reflect NRUC’s balance sheet in order to fully reflect the price at which a 100% sale of NRUC would be conducted. In order to establish the equity value, CF&Co assessed NRUC’s financial statements for items which are not captured by its financial modeling and valuation metrics. These items included NRUC cash and asset retirement obligations. |

Certain negative considerations. Each of the boards of directors of Green SEA Resources Inc. and GSR Acquisition Corp. considered the following factors, each of which we considered negative, in our deliberations concerning the fairness of the terms of the short-form merger to the minority shareholders, including the unaffiliated shareholders, and its procedural fairness:

| • | Termination of participation in future growth of NRUC. Following the successful completion of the short-form merger, the minority shareholders, including the unaffiliated shareholders, will involuntarily have their interests in NRUC liquidated and will cease to be shareholders of NRUC; therefore, after the short-form merger is effected, the minority shareholders, including the unaffiliated shareholders, will not have the right to retain their shares and sell them at a time and a price of their choosing nor will they otherwise have the right to participate in the future earnings or growth, if any, of NRUC or benefit from increases, if any, in the value of NRUC or its shares of common stock. |

| • | Conflicts of interest. With respect to the determination of the merger consideration, our financial interests are adverse to the financial interests of the minority shareholders, including the unaffiliated shareholders. In addition, officers and directors of NRUC have actual or potential conflicts of interest in connection with the short-form merger. Some of our directors and officers are also directors of NRUC. |

| • | No minority shareholder approval. Because the going-private transaction is structured as a short-form merger under the URBC, the minority shareholders, including the unaffiliated shareholders, are not required to vote on the short-form merger. |

| • | No NRUC board of directors, unaffiliated representative or special committee approval/evaluation. Because the going-private transaction is structured as a short-form merger under the URBC, the board of directors of NRUC was not required to vote on the short-form merger, nor was an unaffiliated representative or a special committee required to be appointed to evaluate the short-form merger. |

18

| • | Short-form merger is a taxable transaction. In general, for United States federal income tax purposes, the short-form merger will be treated as a taxable transaction for U.S. federal income tax purposes. |

After giving these factors due consideration, each of the boards of directors of Green SEA Resources Inc. and GSR Acquisition Corp. concluded that none of these factors, alone or in the aggregate, is significant enough to outweigh the factors and analyses that we considered to support the belief of each of the boards of directors that the short-form merger is substantively and procedurally fair to the minority shareholders, including the unaffiliated shareholders.

In determining not to seek approval of the short-form merger by the minority shareholders, including the unaffiliated shareholders, of NRUC, and in considering the absence of an unaffiliated representative of the minority shareholders or the unaffiliated shareholders, and of a special committee of the directors of NRUC to evaluate the short-form merger, we relied on the statutory right of a holder of at least 90% of the outstanding stock of a corporation under Section 1104 of the URBC to effect a short-form merger without any minority or unaffiliated shareholder action and without the requirement of a special committee or unaffiliated representative of the minority or unaffiliated shareholders. Pursuant to the URBC, (i) the minority shareholders, including the unaffiliated shareholders, of NRUC will be entitled to exercise statutory dissent rights under Part 13 of the URBC and (ii) the minority shareholders, including the unaffiliated shareholders, will receive advance notice of the short-form merger, and we have disclosed fully the relevant information that is reasonably necessary to permit minority shareholders, including unaffiliated shareholders, of NRUC to determine whether to accept the merger consideration or to exercise their statutory dissent rights with respect to their shares of NRUC common stock.

In view of the number and wide variety of factors considered in connection with making a determination as to the fairness of the short-form merger to the minority shareholders, including the unaffiliated shareholders, and the complexity of these matters, each of the boards of directors of Green SEA Resources Inc. and GSR Acquisition Corp. did not find it practicable to, nor did they attempt to, rank or otherwise assign relative weights to the specific factors considered. Moreover, neither of our boards of directors has undertaken to make any specific determination or assign any particular weight to any single factor, but have conducted an overall analysis of the factors described above.

We have not considered any factors, other than as stated above, regarding the substantive or procedural fairness of the short-form merger to the minority shareholders, including the unaffiliated shareholders, as it is the view of each of the boards of directors of Green SEA Resources Inc. and GSR Acquisition Corp. that the factors considered provided a reasonable basis to form our belief.

Recent purchases of shares of NRUC stock by GSR.

Prior to May 2007, AmerAlia, Inc. (now NRUC) owned 100% of the outstanding common stock of Natural Soda Holdings, Inc., which in turn owned 100% of the outstanding common stock of NSI. NSI is an operating company that produces and sells sodium bicarbonate (baking soda).

In 2003, the Sentient Entities provided Natural Soda Holdings, Inc. with short-term debt financing which was refinanced on a long-term basis in 2004. In May 2007, the Sentient Entities converted a portion of the debt owed by Natural Soda Holdings, Inc. and NSI into a 53.5% equity interest in NSI. In August 2007, the Sentient Entities purchased approximately 46% of the equity in AmerAlia, Inc. from a major shareholder of AmerAlia, Inc., and also acquired additional debt obligations of AmerAlia, Inc. from the same major shareholder.

As part of a restructuring transaction in October 2008:

| • | the Sentient Entities transferred their various interests to SURF; |

| • | NSI became a wholly-owned subsidiary of Natural Soda Holdings, Inc.; |

| • | SURF converted its loans to Natural Soda Holdings, Inc. into Natural Soda Holdings, Inc. equity and AmerAlia, Inc.’s ownership in Natural Soda Holdings, Inc. was reduced from 100% to 18%; and |

| • | SURF converted its loans to AmerAlia, Inc. into additional common stock of AmerAlia, Inc. |

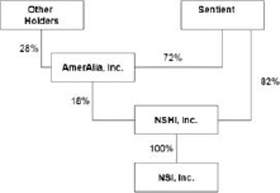

This reorganization resulted in the ownership structure shown below.

19

December 31, 2008 to June 29, 2010

In connection with this restructuring, AmerAlia, Inc., also received approximately $10 million in cash, settled approximately $12 million of debt, terminated indemnification rights relating to the extinguishment of an AmerAlia, Inc. $9.9 million bank loan and extinguished other obligations in exchange for the issue of 48,961,439 shares of its common stock.

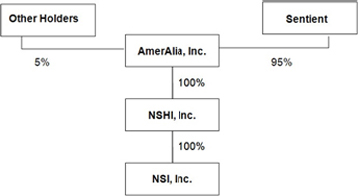

Finally, on June 30, 2010, AmerAlia, Inc. issued 286,119,886 shares of its common stock to SURF in exchange for the 82% of Natural Soda Holdings, Inc. SURF held with the following resulting structure shown below.

On September 14, 2010 at a Special Meeting of the Shareholders of AmerAlia, Inc., the shareholders approved the amendment of the articles of incorporation to change the name of AmerAlia, Inc. to Natural Resources USA Corporation.

On March 15, 2011, SURF entered into the Exchange Agreement with Green SEA Resources Inc. Pursuant to the Exchange Agreement, SURF exchanged all of its ownership in NRUC for 20,084,954 common shares of Green SEA Resources Inc. The interests of NRUC that were exchanged were (i) all of the shares of common stock of NRUC owned by SURF, a total of 334,074,381 shares of common stock, plus (ii) a limited option to acquire up to 5,500,000 shares of common stock of NRUC.

Prior to the mailing of this Transaction Statement and pursuant to the terms of the Contribution Agreement, Green SEA Resources Inc. will transfer all of its shares of common stock of NRUC and its right to acquire up to 5,500,000 shares of common stock of NRUC to GSR Acquisition Corp.

20

REPORTS, OPINIONS, APPRAISALS AND NEGOTIATIONS

Valuation Report and Fairness Opinion by CF&Co

In considering the fairness of the short-form merger from a financial point of view to the minority shareholders, including the unaffiliated shareholders, Green SEA Resources Inc. engaged CF&Co on June 24, 2011 to perform an independent third-party valuation of NRUC, provide an opinion as to the fairness, from a financial point of view, to NRUC’s shareholders (other than GSR) of the $0.57 per share merger consideration proposed by GSR to be received by such shareholders and to provide a Valuation Report and Fairness Opinion. CF&Co consented to the references to their Valuation Report and Fairness Opinion in this Transaction Statement and to the inclusion of the Valuation Report and Fairness Opinion asAppendix C to this Transaction Statement.

CF&Co received a fee of $150,000 for such services, all of which was paid upon delivery of an initial version of the Valuation Report and Fairness Opinion. No part of such fee is contingent upon consummation of the short-form merger. In addition, GSR agreed to reimburse CF&Co for its reasonable out-of-pocket expenses related to its engagement, including the fees and expenses of counsel, whether or not the short-form merger is consummated. GSR also agreed to indemnify CF&Co for certain potential liabilities relating to or arising out of its engagement.

CF&Co is an independent financial advisory firm and is continually engaged in the valuation of businesses and their securities in connection with mergers and acquisitions and valuations for other corporate purposes. CF&Co provides advice to companies in the mining and metals processing industries, in which industries CF&Co’s directors have extensive experience.