China Hydroelectric Corporation (NYSE: CHC) Presentation from 40% Shareholders September 2012 See special note regarding this presentation on page 2 Exhibit 99.1 |

This presentation includes information based on data found in filings with the Securities and Exchange Commission, independent industry publications and other sources. Although we believe that the data is reliable, we do not guarantee the accuracy or completeness of this information and have not independently verified any such information. No representation or warranty, express or implied, is made as to the accuracy or completeness of any information included or otherwise used herein, and nothing contained herein is, or shall be relied upon as, a representation or warranty, whether as to the past, the present or the future. We have not sought, nor have we received, permission from any third-party to include their information in this presentation. Many of the statements in this presentation reflect our subjective belief. Although we have reviewed and analyzed the information that has informed our opinions, we do not guarantee the accuracy of any such beliefs. CPI Ballpark Investments Ltd. (“CPI Ballpark”), Swiss Re Financial Products Corporation, China Environment Fund III, L.P., Aqua Resources Asia Holdings Limited, Abrax and IWU International Ltd. (collectively, the “Shareholder Group” or “We”) do not have any obligation to update or otherwise revise these materials. The information contained in these materials does not purport to be an appraisal of any of the assets or liabilities of CHC or any of its subsidiaries, and does not express any opinion as to the price at which the securities of any such entities may trade at any time. The information and opinions provided in these materials take no account of any investor's individual circumstances and should not be taken as specific advice on the merits of any investment decision. Moreover, nothing contained herein is intended or written, or should be construed, as providing any legal, tax or accounting advice, and thus, among other things, nothing contained herein is intended or written to be used, or can be used, for the purpose of avoiding tax-related penalties. The Shareholder Group does not accept any liability whatsoever for any direct or consequential loss howsoever arising, directly or indirectly, from any use of these materials. Sections of this presentation refer to the track record of members of the Shareholder Group and our nominees for the board of directors. We believe that our nominees have had successful experiences in other companies that have resulted in an increase in shareholder value that benefited all shareholders. However, this success is not necessarily indicative of future results at CHC if our nominees were to be elected to the CHC Board of Directors. SECURITY HOLDERS ARE ADVISED TO READ THE NOTICE OF EGM AND PROXY MATERIALS AND OTHER DOCUMENTS RELATED TO THE SOLICITATION OF PROXIES CONTAINED IN THE SCHEDULE 13D/A FILED BY THE SHAREHOLDER GROUP WITH THE SECURITIES AND EXCHANGE COMMISSION ON AUGUST 30, 2012 (AS AMENDED, THE “SCHEDULE 13D”). INFORMATION RELATING TO THE SHAREHOLDER GROUP IS CONTAINED IN THE SCHEDULE 13D. EXCEPT AS OTHERWISE DISCLOSED IN THE SCHEDULE 13D, THE MEMBERS OF THE SHAREHOLDER GROUP HAVE NO INTEREST IN CHC OTHER THAN THROUGH THE BENEFICIAL OWNERSHIP OF ORDINARY SHARES AND AMERICAN DEPOSITARY SHARES. THE SCHEDULE 13D IS AVAILABLE AT NO CHARGE AT THE SECURITIES AND EXCHANGE COMMISSION’S WEBSITE AT HTTP://WWW.SEC.GOV. 2 Special Note Regarding This Presentation |

3 Table of Contents 1. Who We Are 2. CHC and its Operations 3. Our Concerns and Reasons for the EGM 4. The Way Forward 5. Summary Appendix |

4 1. Who We Are |

5 The 40% Shareholders We are a group of 40% shareholders (the “Shareholder Group”) — NewQuest Capital: Spin-out of Bank of America Merrill Lynch’s Asian Private Equity team backed by large US, European and Asian institutional investors. — Swiss Re Financial Products Corporation: Part of Swiss Re, a leading provider of (re)insurance products. — China Environment Fund: Clean-tech focused funds with core philosophy of “Doing Well by Doing Good”. — Aqua Resources: London Stock Exchange listed fund managing investments in water related assets globally. — Abrax: Family office with significant investment experience globally and in China; Actively works with state agencies. — IWU International: Family office with significant experience in power utilities in China. Additional details of each shareholder can be found in the Appendix. Members of the Shareholder Group have in the aggregate invested approximately US$170M in CHC since 2008, and have maintained their holdings since their initial investments. We are long-term and active investors in the Company, and certain members of the Shareholder Group have attempted to work with the Company to try to create value. Certain members of the Shareholder Group have collectively invested nearly US$1B in over 25 projects in clean tech, renewable and energy businesses across Asia. |

6 2. CHC and its Operations |

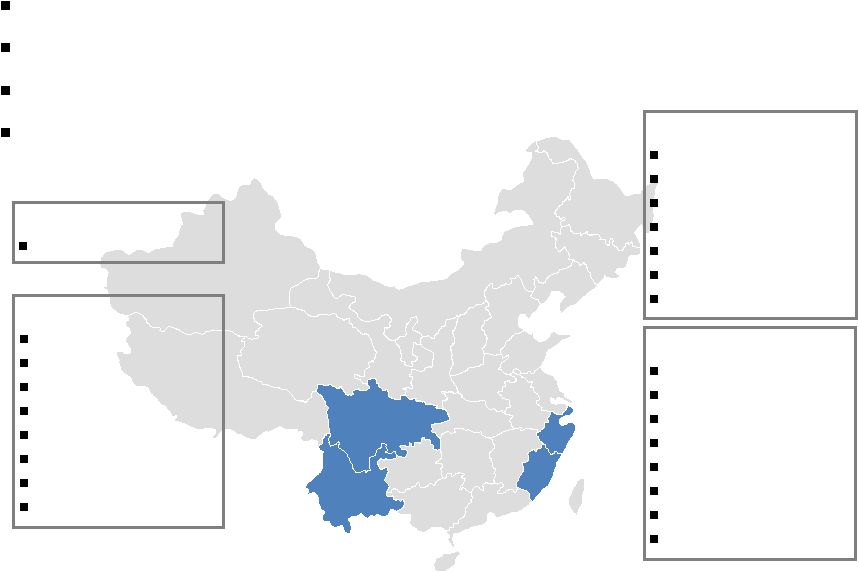

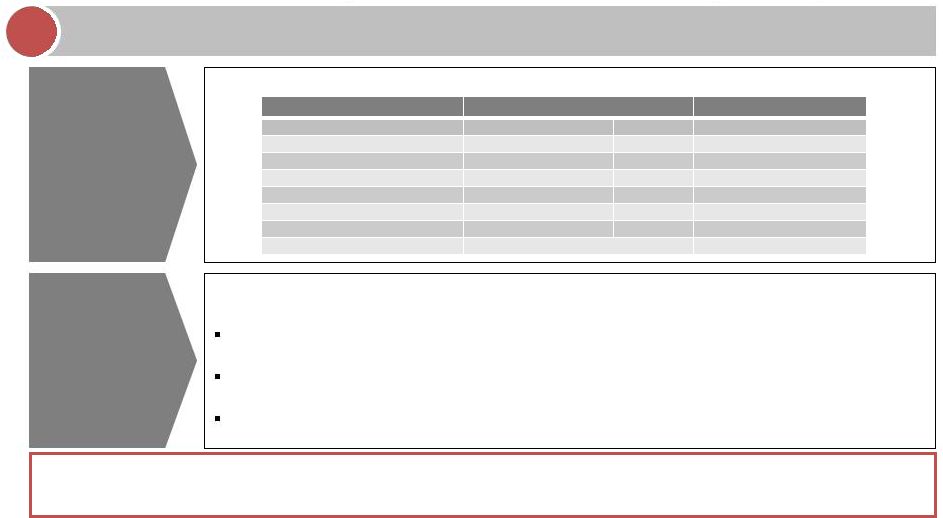

7 China Hydroelectric Corporation Established in July 2006, CHC was formed to acquire, own and operate small hydroelectric power projects (each less than 50MW) in China. From November 2006 to October 2009, the Company raised approximately US$350M through four private rounds of financing, and further raised approximately US$100M through an IPO in January 2010. As of June 30, 2012, the Company owns 26 hydroelectric power projects across four provinces in China with a total installed capacity of 548MW. Approximately 675 employees in China and 5 in US. Sichuan Yunnan Fujian Zhejiang Source: CHC SEC filings (1) 74% ownership (2) 55% ownership Yingchuan (40.0MW) Wuliting (42.0MW) Shapulong (25.0MW) Ruiyang (32.0 MW) Jiulongshan I (25.0MW) Jiulongshan II (12.6MW) Zhougongyuan (16.0MW) Zhejiang Province (193MW) Sichuan Province (12MW) Liyuan (12.0MW) Binglangjiang I (21.0MW) Binglangjiang II (20.0MW) Husahe (18.7MW) Aluhe (10.0MW) Latudi (18.9MW) Zilenghe (25.2MW) Xiaopengzu (44.0MW) Dazhaihe (15.0MW) Yunnan Province (173MW) Fujian Province (170MW) Yuheng (30.0MW) Banzhu (45.0MW) Wangkeng (40.0MW) Jinwei (1) (16.0MW) Jintang (1) (11.6MW) Jinlong (2) (10.0MW) Qianling & Jinjiu (13.0MW) Dongguan (4.8MW) |

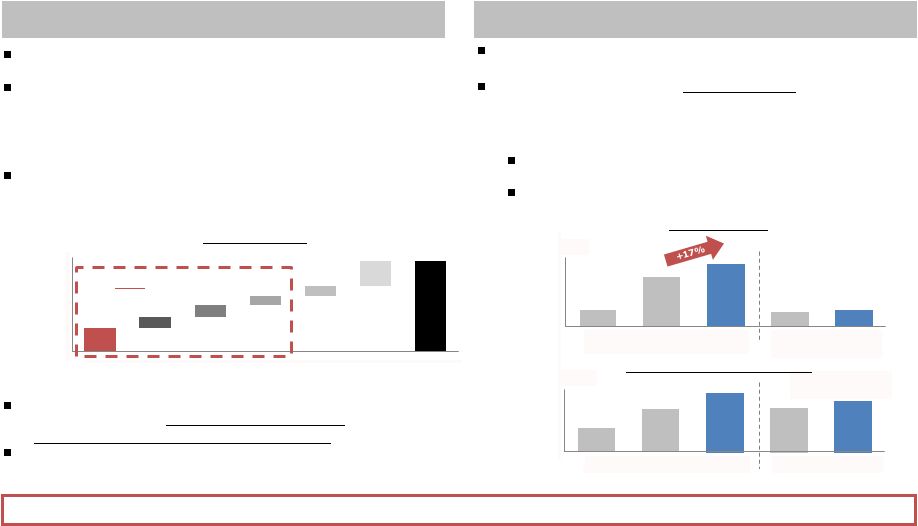

8 CHC’s Business Model Based on sale of electricity to local grids generated from water flowing through CHC hydro plants. As the Company has stated in its FY2011 results press release, “The single most important factor affecting our operating results is the amount of electric power we are able to generate, and this of course is dependent on two principal factors”: A. Rainfall B. Facility / equipment operating normally Relatively straightforward operations Renewable energy laws in China require local grids to purchase power generated by small hydro plants. As such, all CHC hydro plants have entered into contracts with local grids to sell all of their power generated. Electricity sales Tariffs for electricity sales are fixed by the government and have been adjusted from time to time. Tariffs Source: CHC SEC filings In its current state, rainfall ultimately determines CHC’s revenue, but its management drives profitability Six months ended June 30 1H2010 1H2011 1H2012 (1) Installed capacity at period end (MW) 431 564 549 Precipitation % of long-term average Zhejiang 142% 71% 140% Fujian 125% 52% 122% Yunnan N/M 100% 86% Electricity produced (millions kWh) 784.6 708.8 1057.1 Change -10% 49% Revenue (US$M) 38.3 32.0 56.4 Change -17% 76% (1) For continuing operations only 1 2 3 |

3. Our Concerns and Reasons for the EGM 9 |

10 Board and Senior Management Have Failed to Turn Around Dismal Stock Performance Conflicts of Interest are Pervasive at the Board and Senior Management Level Board and Senior Management are Obstacles to Unlocking Value Current CHC Board of Directors and Senior Management Four Simple Themes Liquidity Crisis Remains Unresolved |

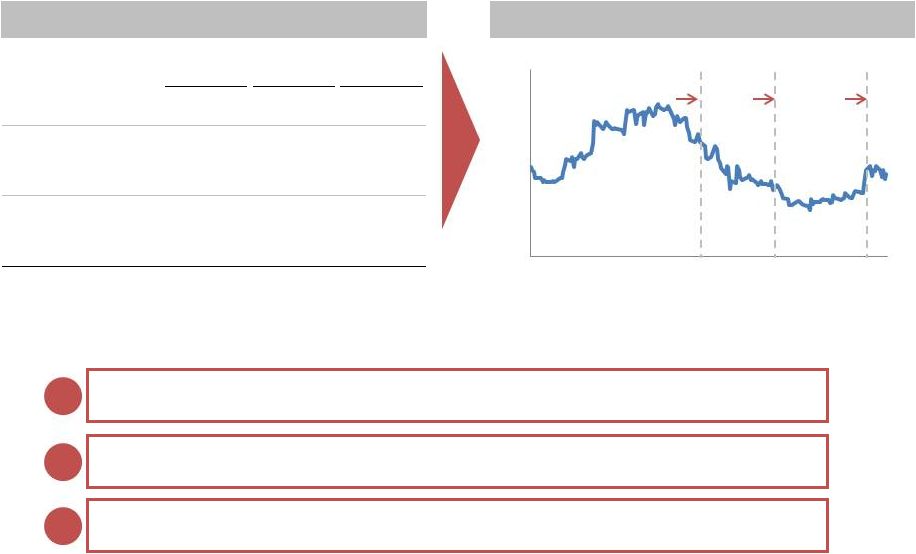

11 Stock Performance Has Been Very Disappointing CHC Share Price Dropped >92% Shareholder Value Continues To Be Destroyed CHC’s share price declined over 92% from the IPO price of US$14.80/ADS as of Jan 25, 2012, to US$1.10/ADS as of Aug 31, 2012. During the same period, the Halter USX China Index of comparable US-listed Chinese companies declined only 21.5% and the S&P500 increased by 28.2%. CHC’s market capitalization is now only US$59M (as of Aug 31, 2012) as compared to US$754M at the IPO. Note: As of August 31, 2012 Source: CHC SEC filings and Capital IQ The Board and Senior Management have failed to turn around CHC’s stock price and market cap, which have dropped over 92% during their tenure (1) Includes shares issued by way of exercise of warrants during August 2011 0 20 40 60 80 100 120 140 Jan 2010 Jul 2010 Jan 2011 Aug 2011 Feb 2012 Aug 2012 CHC S&P500 Index Halter USX China Index (Prices indexed to 100) CHC -92.6% from IPO price) Halter USX China Index -21.5% S&P500 Index +28.2% ( 754 0 100 200 300 400 500 600 700 800 At IPO Jun 30, 2010 Dec 31, 2010 Jun 30, 2011 Dec 30, 2011 Aug 31, 2012 (US$M) (1) (1) 384 378 208 62 59 Market Capitalization |

(US$M) 1H2011 1H2012 (1) Growth Revenue 32.0 56.4 76% EBITDA 20.2 41.8 107% EBITDA margin 63% 74% Net Income (7.2) 7.2 N/A Net margin -23% 13% 12 Stock Price Continues to be Depressed Despite Record Results Note: From January 3 to August 31, 2012 Despite improvements in financial performance due to increased rainfall during 1H2012, CHC’s stock price continues to trade at depressed levels as a result, we believe, of the Company’s failure to address investor concerns: 1 Lingering unresolved liquidity issues 2 Excessive “cash” general and administrative expenses 3 Warrant and Employee Stock Option Plan (“ESOP”) Restructuring Record results for first half of 2012… … Did not result in any share price improvement in year-to-date 2012 April 26: FY2011 Earnings Release June 14: 1Q2012 Earnings Release August 16: 2Q2012 Earnings Release Source: CHC SEC filings and Capital IQ (1) For continuing operations only 0.00 0.50 1.00 1.50 2.00 2.50 Jan 2012 Mar 2012 May 2012 Jul 2012 Aug 2012 (US$ per ADS) CHC -8% |

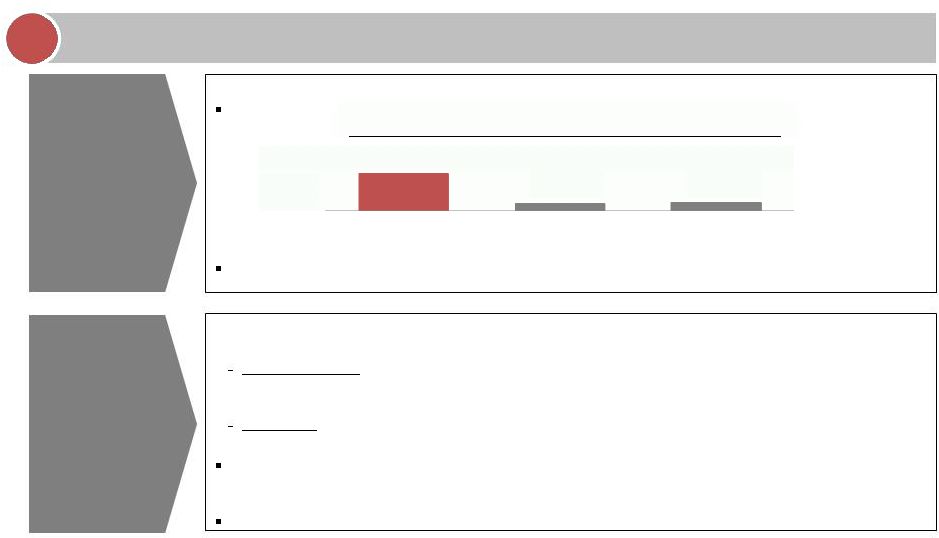

13 Key Contributors to Stock Price Decline Liquidity Condition Remains Unresolved G&A Expenses are Excessive and Continue To Grow CHC has been facing a liquidity shortfall since mid-2011 and has struggled to meet its payment obligations. Instead of striving to find a comprehensive, long-term solution, the Company has resorted to piecemeal financings, among which have included: 1. Expensive short-term loans (at interest rates up to 21.6% per annum) 2. Sale of 16MW Yuanping asset in Fujian (1) 3. Restructuring and partial exercise of warrants held by Vicis Capital While Senior Management boasts that it has secured approximately US$74M in new financings to date, there is still a working capital deficit of nearly US$130M and almost US$180M in principal due by 2015. Despite new financings and improved performance, the Company and its auditor have continued to raise “substantial doubts about [the Company’s] ability to continue as a going concern.” It is apparent the Company has no comprehensive plan to resolve its liquidity problems. Board and Senior Management have done very little to address these concerns in a meaningful way General and administrative expense excluding stock based compensation (“Cash G&A Expenses”) (2) continues to rise. Particularly, Cash G&A Expenses grew 17% in 2011, in a year where: — Installed capacity size remained the same — CHC reported one of its worst years of financial performance — There are severe liquidity and going concern issues Instead of controlling expenses, Cash G&A Expenses continued to increase from 1H2011 to 1H2012. Senior Management claims of reducing G&A Expenses has largely been a result of reduction in non-cash G&A Expenses due to restructuring of ESOP. Debt Maturity Profile Over 60% due between 2012-15 Note: As of December 31, 2011 0 50 100 150 200 250 300 2012 2013 2014 2015 2016 After 2016 Total 72.5 37.1 36.6 31.5 31.9 78.3 287.9 (US$M) Cash G&A Expenses Cash G&A Expenses Per MW Capacity MW capacity (period end) 5.0 10.0 15.0 20.0 (US$M) 8.5 15.8 18.5 8.2 8.6 2009 2010 2011 1H11 1H12 (3) (3) (3) 15.0 20.0 25.0 30.0 35.0 US$K/MW) 2009 2010 2011 1H11 1H12 (3) (3) (3) 377 549 548 564 548 Source: CHC SEC filings, filings of Fujian MinDong Electric Power Co., Ltd. on the Shenzhen Stock Exchange and Capital IQ (1) The Company also attempted to sell another asset in Fujian but was rejected by the buyer’s shareholders as disclosed in the buyer’s filings on the Shenzhen Stock Exchange on August 8, 2012; (2) General and administrative expense (“G&A Expenses) includes hydropower project-related expenses and corporate overhead expenses, including non-hydropower project related salaries and benefits, office lease, employee stock option expense (“ESOP Expenses”), professional fees and others. Cash G&A Expenses excludes ESOP Expenses which is not paid out in cash but recorded as an accounting expense; (3) Represents continuing operations; (4) Annualized 22.6 28.8 33.9 29.2 31.3 (4) (4) |

14 Pervasive Conflict of Interests and Corporate Governance Issues at Senior Management and Board Level Source: CHC SEC filings and Capital IQ (1) Includes 20 US-listed Chinese foreign private issuers with FY2011 revenues of US$50-100M. Director/ executive cash compensation data from SEC filings of each company. Excessive Executive Cash Compensation Questionable ESOP Manipulation Board approved restructuring of ESOP through two transactions which we believe were deliberately designed to mask the true impact to P&L of the Company and dilution to shareholders December 22, 2011: 10.38M options with a strike price ranging between US$4.93 - $7.70 per share (or US$14.79 – 23.10 per ADS) were cancelled and exchanged for 417K options (~5% of cancelled options) with a strike price of US$0.46 per share (or US$1.38 per ADS) which were vested immediately. May 1, 2012: 9.98M options were re-issued to replace the cancelled options in December 2011 at a strike price of US$0.62 per share (or US$1.86 per ADS). Further, the timing of the new issuance on May 1 is questionable as all the outstanding ESOP were immediately issued after the Company’s announcement of its worst year of financial performance on April 26 but before positive announcements of tariff hikes on May 14 and May 21 and record first quarter results on June 14. 95% of the new options issued in May 2012 went to top 4 management team members. Excessive Executive Compensation and Manipulation of ESOP 1 Compensation to senior executives is highly disproportionate and unjustified Salaries are nearly 5x peer companies in China with a similar revenue base. Senior management continues to take home 60-100% of their fixed salary as cash bonuses in spite of failure to perform on every material parameter. Executive/Director Cash Compensation as % of Revenue (FY2011) 6.3% 1.2% 1.4% 0.0% 5.0% 10.0% CHC Median Mean US-listed Chinese Foreign Issuers (Revenue: US$50-100M) (1) |

15 Pervasive Conflict of Interests and Corporate Governance Issues at Senior Management and Board Level (Cont’d) Source: CHC SEC filings and GovernanceMetrics International (2012) Senior Management team members not only receive excessive pay, but also work for other entities managed by John Kuhns Chairman of Board and CEO roles rest with the same individual Time and Attention Diverted to Other Businesses and Combined Chairman / CEO Role 2 Company Role 1 China Silicon Corporation Chairman / CEO 2 China Natural Energy Corporation Chairman / CEO 3 China Electrode Corporation Chairman / CEO 4 China Board Mill Corporation Chairman / CEO 5 Master Silicon Carbide Industries, Inc. Chairman / CEO 6 China New Energy Group Company Director / Legal Rep. in PRC 7 China Hand Advisors, Inc. Director 8 Kuhns Brothers & Co., Inc. Chairman / CEO 9 Kuhns Brothers Securities Corporation Chairman / CEO 10 Kuhns Brothers, Inc. Director 11 Kuhns Brothers Capital Management, Inc. Director 12 Kuhns Brothers Advisors, Inc. Director 13 Kuhns Brothers Enterprises Corporation Director 14 White Hollow Farms, Inc. Director 15 White Hollow Vineyards, Inc. Director 16 Lime Rock Ventures, Inc. Director 17 Watch Hill Farms, Inc. Director 18 Corona Equities, Inc. Director 19 Global Photonics Energy Corporation Director 20 Craton Equity Partners Director 21 Project Midway, Inc. Director Heavy Involvement in Other Businesses Sub-standard Corporate Governance Other Companies Managed Directly by John Kuhns Additionally, five year shareholder returns to such companies are nearly 30% lower than those with separate chairman and CEOs. Furthermore, studies have shown that executives with a joint chairman/CEO role are paid more than the combined cost of a CEO and a separate chairman. All authority is vested in Mr. Kuhns. There are few checks and balances, and no balance of power. Mary Fellows, EVP and Secretary of CHC, is also EVP and/or director of at least 6 other companies managed directly by Mr. Kuhns. Mr. Kuhns is CEO and/or director of at least 21 other companies (see table to right). |

16 Pervasive Conflict of Interests and Corporate Governance Issues at Senior Management and Board Level (Cont’d) Source: CHC SEC filings Questionable Related Party Transactions which Raise Red Flags 3 Shared Offices Rental of New York Office paid to Kuhns Brothers, Inc. We believe that CHC shares its China office space with fund affiliated with John Kuhns Related Services Financial advisory services paid by CHC to Kuhns Brothers Inc. Related transactions with “independent” directors Unexplained related party transactions disclosed in CHC’s 2Q2012 Earnings Release Kuhns Brothers, Inc. received financial advisory fees for advising CHC in 2009. Anthony Dixon received consulting fees in relation to a project acquisition by CHC in 2007. Richard Hochman received commissions from CHC’s placement agent, Morgan Joseph & Co. in relation to financings by CHC in 2008. There are unexplained related party transactions in the Company’s most recent earnings release. The Shareholder Group has reason to believe that such transactions involved payments by CHC on behalf of Mr. Kuhns’ other companies unrelated to CHC when CHC has its own liquidity issues. CHC rents prime office space in Manhattan from Kuhns Brothers, Inc., a financial advisory firm founded by John Kuhns, for US$288k per year. CHC’s New York office space is shared with other businesses managed by Mr. Kuhns. Analysis suggests that at current market rates, CHC is paying for an equivalent of over 5,000 sq.ft. of space for approximately 5 employees based in New York. China Hand Fund (John Kuhns’ private equity fund) shares a portion of CHC’s Beijing office. |

17 Pervasive Conflict of Interests and Corporate Governance Issues at Senior Management and Board Level (Cont’d) We believe that the complex relationship between Vicis Capital (1) and Mr. Kuhns has led to shareholder bias at the Board and Senior Management Level 4 We believe that conflicts and corporate governance issues have rendered it impossible for the Company to act in the best interest of all shareholders and, if remained unchecked, will continue to result in further value destruction Intricate Relationship with Vicis Vicis has invested in many other businesses of John Kuhns Opportunistic Warrant Restructuring Opportunistic restructuring of Vicis Warrants Source: Based on SEC filings of CHC, China New Energy Group Company and Master Silicon Carbide Industries. (1) Vicis Capital (“Vicis”) is a US-based hedge fund that owns a 24% equity stake and is the largest shareholder in CHC. Company Vicis & Related Parties Role of John Kuhns Board Representative Inv (US$) China Hydroelectric Corporation Shadron Stastney ~100M Chairman/CEO China New Energy Group Company Shadron Stastney ~30M Board Member Master Silicon Carbide Industries Shadron Stastney 20M President & CEO China Board Mill Corporation Shadron Stastney N/A Chairman/CEO China Silicon Corporation Shadron Stastney N/A Chairman/CEO China Natural Energy Corporation Shadron Stastney N/A Chairman/CEO China Hand Fund Vicis is a Significant L.P. Controls the Company Approved by the Board in August 2011, warrants held by Vicis that were about to expire in less than two months were restructured to a significantly lower exercise price (from US$15.00 to US$3.45 per ADS). Restructured warrants were subsequently partially exercised (the amount exercised was not sufficient to resolve the liquidity issue CHC was facing). Shadron Stastney is a member of the CHC Board and a partner at Vicis. |

18 Board and Senior Management are Obstacles to Value Creation The Shareholder Group believes that the current Board will be unable to address the serious issues facing the Company and value will continue to be destroyed Despite recent performance due to record rainfall and some replacement loans, CHC still finds itself in precarious liquidity position recognizing that there is still “substantial doubt about its ability to remain a going concern.” Any efforts to address this issue have been piecemeal at best, and primarily driven by local management in China. We do not believe the current Board and Senior Management take the liquidity issue seriously, nor that they will ever be able to effectively find a solution for CHC’s near and long-term cash needs. With the current Senior Management, we believe that it will be impossible to pursue any strategic initiatives that might weaken their entrenched position within the Company while unlocking value for shareholders. Instead, we anticipate that they will continue to seek to benefit from and exploit their conflicts of interests at the expense of CHC shareholders. The Shareholder Group believes that the recent engagement of Morgan Stanley by Senior Management after the Shareholders EGM notice is too little too late, particularly given Senior Management’s prior track record of spending money on financial advisory services that resulted in our situation today. The Shareholder Group is not confident that this approach will yield significant results in the short term, but remains willing to engage with Morgan Stanley. Senior Management and the Board have repeatedly ignored concerns raised by shareholders and potential financing partners to address excessive G&A Expenses. This can only be explained by the fact that: (i) Senior Management seeks to further entrench itself without regard to shareholder value, and (ii) the Board has turned a blind eye in its explicit support for management in this regard. Senior Management’s mismanagement and inactions have destroyed value in other companies that they have previously managed both inside and outside of China, and have ended disastrously for shareholders of these companies. The Shareholder Group fears CHC will suffer a similar fate without the proposed changes. Please refer to Appendix: "Questionable Track Record of Senior Management" for more details. Incapable of Addressing Liquidity Concerns Unwillingness to Improve Margins No Strategic Initiatives Poor Management Track Record |

19 Members of the Shareholder Group Have Made Multiple Attempts to Assist the Company Concerns on Excessive G&A Expenses Since July 2011, members of the Shareholder Group have expressed concerns regarding the Company’s high G&A Expenses in various forums, including earnings calls and formal correspondence to the Board. Since June 2011, members of the Shareholder Group have offered assistance to resolve the Company’s liquidity crisis, and introduced multiple international banks (including Morgan Stanley), private equity investors, and development finance institutions to the Company for potential equity and debt solutions, which certain potential investors rejected due to lack of faith in the current Senior Management and Board. Concerns on Liquidity Issue Since April 2011, CPI Ballpark, as a 24% shareholder, has repeatedly requested, but has ultimately been denied, a board seat despite promises by John Kuhns to the contrary. Board Representation to Voice Concerns |

20 Why Call an EGM to Replace Certain Members of the Board? The Shareholder Group feels it has exhausted all possible options The Board and Senior Management have not meaningfully engaged with members of the Shareholder Group to address the issues raised The situation of the Company is quite severe and must be addressed immediately The changes proposed by the Shareholder Group are necessary to stop further value destruction to the Company and will cause little disruption to the on-shore operations in China Not only has the Board presided over an unprecedented 92% stock price decline from the IPO, the Company is facing alarming liquidity issues that threaten the sustainability of the Company, all of which the Board has failed to successfully resolve. Certain members of the Shareholder Group have reached out to the Board on multiple occasions over an extended period in attempt to amicably resolve the issues, but have been repeatedly ignored or rejected. We believe that members of the Board are entrenched and have too many personal and/or business dealings with John Kuhns to challenge him or to bring about change in the Company. |

21 Purpose of the EGM The Shareholder Group called an extraordinary general meeting of shareholders of CHC (“EGM”) with the following proposals. Remove the following 5 individuals from the Board: And Elect the following four individuals to the Board: Based on discussions, we believe that two existing directors, Dr. You-Su Lin and Dr. Yong Cao, will remain as directors to form a six-member board. John D. Kuhns Richard H. Hochman Shadron Lee Stastney Anthony H. Dixon Stephen Outerbridge Moonkyung Kim Jui Kian Lim Amit Gupta Yun Pun Wong |

4. The Way Forward 22 |

23 Proposed Director Nominees Candidate Key Value Add Background Moonkyung Kim • Domain knowledge – renewable energy • Corporate Governance • CSR Initiatives • Founder, Managing Director and board member of Peony Investments (Hong Kong) Limited, providing investment, advisory, and board leadership to green businesses. • Over 15 years of experience in the energy and environmental sectors serving in roles including engineering, advising, strategic consulting, investing and entrepreneurship. • Senior advisor to SOW Asia Foundation, a non-profit venture philanthropic organization in Hong Kong. • Prior work experience includes Nomura, DFJ Element Ventures and Booz Allen. • Prior experience on board of renewable energy companies. • Master of Business Administration degree from the Wharton School of the University of Pennsylvania and Bachelor of Science with honors in Environmental Engineering from Harvard University. Jui Kian Lim • Project Finance expertise • Deep domain knowledge - water and infrastructure assets • Managing Director and Head of Asia Environment Group for FourWinds Capital Management (HK) Ltd. • More than 17 years of experience in the Asian infrastructure and environment sectors. • Currently serves as a director and member of audit committee of New Environmental Energy Holdings Limited (SEHK: 3989) and a director at Phaunos China Limited, Robinson Investments Limited and Ranhill Water Technologies (Cayman) Limited. • Also a director of FourWinds Capital Management (HK) Limited and Aqua Resources Asia Holdings Limited. • Extensive experience in project development and project financing raising more than US$500M at Veolia Water Asia Pacific. • Deep understanding of infrastructure and water sectors through positions at JPMorgan Chase, Veolia Water, Peregrine Securities and Morgan Grenfell/Deutsche Securities. • Earned MSc (Economics) from the London School of Economics in 1994. Amit Gupta • Domain knowledge – power and renewable energy • Operational experience • Observer of CHC prior to IPO • Partner and Chief Operating Office at NewQuest Capital Partners. • Oversees investments in the power and financial services sector for NewQuest Capital. • Previously an observer on the boards of CHC and RRB Energy Limited. • Currently represents NewQuest as non-execute director on OM Logistics Limited and Ittiam Systems • Executive director of NewQuest Capital Advisors (HK) Limited and director of CPI Ballpark Investments Ltd. and NewQuest Asia Investments Limited. • Prior experience at Bank of America Merrill Lynch managing several investments in power and renewable energy across Asia. • MBA from Indian Institute of Management (IIM), Bangalore India (placed in Director’s Merit List) and an undergraduate degree in electrical engineering from REC Kurukshetra India. Yun Pun Wong • Audit Committee Financial Expert • Finance and Audit • CFO and Executive Director of Tsing Capital, a clean-tech focused venture capital firm in China • Served as the CFO and Senior Director of Spring Capital, the CFO of Natixis Private Equity Asia and Associate Director of Finance for JAFCO Asia. Also worked in other international organizations like PricewaterhouseCoopers. • Graduated from the Hong Kong Polytechnic University and holds a Master of Business from the Curtin University, Australia. Fellow member of Hong Kong Institute of Certified Public Accountants. Below are the names and backgrounds of the nominated board members. Notes: The Shareholder Group nominates 4 new directors. Including 2 existing directors, Dr. You-Su Lin and Dr. Yong Cao, the new board of directors will consist of 6 members. |

24 Issues to Address Liquidity Concerns A Target Proposed Actions Steps Ensure liquidity to service debt payments in near term Modify debt and debt profile of the Company to avoid similar situations in future Reduction in cash G&A Expenses to increase ability to service debt Form special committee of the Board to: — Approach banking networks for possible debt refinancing and/or new debt issuance — Consider divestment of non-core assets at premium to book value or fair market value (which is considerably higher than what the current share price reflects) Cash G&A Expenses Reduction C Set target for 25% reduction in Cash G&A Expenses in 2013; and 35% reduction in 2014 without affecting China operations Discuss and work with local management to reduce G&A Expenses on fronts that have been identified by the Shareholder Group. New CEO and existing local management to work with new Board to identify other areas of expense reduction without affecting the local operations. Staffing B Recruit CEO and in-house General Counsel We are considering several candidates for the proposed positions. Work with new CEO and General Counsel to evaluate any internal and external resources required to streamline operations. Aligning Management Incentives D Strategic Alternatives E Ensure that management incentives are aligned to all stakeholders objectives including shareholders New hires to be based close to operations and enter into fulltime employment contracts in China. Compensation Committee to work on new long term ESOP plan that is widespread and treats local China team at par with leadership. Additional defined incentives linked to operational efficiencies and performance of the assets Reduce related party transactions. Implement shareholder vote for executive compensation to keep the management accountable. Develop strategic alternatives to build medium and long term value for stakeholders New Board to work with management to consider possible strategic options including: — Dual listing on stock exchanges closer to China — Strategic JVs or partnerships with Chinese utilities; — Raise longer term funding from global development institutions — Capital raising for expansion — Consider divestment of non-core assets to solve liquidity issues, if required |

25 Immediate Concern Immediate reduction of G&A Expenses to increase cash flow for debt servicing Shareholder Group to reach out to their own extensive local banking networks in China for new loans or refinancing of existing loans Local management and finance staff to continue dialogue with existing banks on re-financings and new loans Re-engage previous dialogues with development financing institutions and international investment banks on offshore financing solutions Special Committee to assess (1) financial condition of each individual asset, (2) restructuring of debt profile and (3) immediate liquidity needs and resolutions Liquidity Crisis |

5. Summary 26 |

27 Summary 1. The Shareholder Group holding a 40% stake in CHC has called an EGM to demand change and to replace certain directors. 2. The current Board and Senior Management have: (a) failed to prevent a steep stock price decline and to turn around stock price, (b) failed to successfully address liquidity issues and high Cash G&A Expenses, (c) supported questionable ESOP restructurings and compensation schemes, (d) engaged in questionable related party and conflict of interest dealings, and (e) ignored requests from the Shareholder Group for improvement and change. 3. The Shareholder Group has put up a slate of nominees who plan to immediately: (a) address liquidity crisis, (b) reduce G&A Expenses, (c) maintain existing operations in China and evaluate staffing needs elsewhere, (d) evaluate and implement a fair employee incentive program, and (e) assess strategic alternatives to build value. |

Appendix 28 |

29 The 40% Shareholder Group Strong and Reputable Shareholders Company Name Description NewQuest Capital Partners • Spin-off from Bank of American Merrill Lynch’s Asian Private Equity team. • About US$400M fund managed by partners with prior experience in internationally reputed firms including IFC, Bank of America Merrill Lynch and 3i. • Backed by some of the largest, credible, US regulated fund of funds including HarbourVest, Paul Capital, LGT and Axiom Asia. • Core focus to work with company management and provide strategic inputs to add value. China Environment Fund • US$600M funds managed by Tsing Capital. • Focused clean-tech funds believe in core philosophy of “Doing Well by Doing Good”. • Backed by most the reputed international development finance institutions and world class institutional investors. • Successful track record of working with its portfolio companies in helping them scale-up. Swiss Re Financial Products Corporation • Part of Swiss Re, a leading wholesale provider of reinsurance, insurance and other insurance-based forms of risk transfer. Aqua Resources • London Stock Exchange listed closed-end fund that manages investment in water related assets globally. • Key shareholders include JP Morgan and several esteemed pension funds. Abrax • Family office with team and founder having significant experience in working with portfolio companies globally and particularly in China. • Actively works with state agencies and private companies for business and social issues. IWU International Ltd • Family office with significant experience in China. • Works closely with power utilities and other portfolio companies globally, especially in China. Along with bringing credibility and incentive alignment to the Company, the Shareholder Group also brings with it many areas of operational support. Collectively the below investors own 40% of the Company. |

Company Background Issues/Concerns Catalyst Energy (1984 – 1987) Kuhns founded Catalyst Energy and took it public in 1984. ¹ Share price tanked from peak of US$29 to $3.75 in 1987. New York Times mentioned that he “alienated key investors and sent Catalyst’s stock into a tailspin.” 1 It was alleged that Kuhns received US$1.3M in salary, bonuses and benefits 2 during his three years as CEO, and sold Catalyst Energy shares for more than US$3M. ¹ New World Power (1989 – 1996) Kuhns founded New World Power and took it public in 1992. In total, the company raised ~US$63M in equity. ³ The company reported net loss of $41.3M in 1995 and went through debt restructuring, asset sale and reorganization in 1996; Kuhns stepped down as CEO (pressured by creditors) and was not re-nominated to serve as Chairman in 1996. 2&5 The company’s auditor raise[d] substantial doubt about the company's ability to continue as a going concern. 5 It was alleged that Kuhns received ~US$1.5M in salary and benefits from 1993-1995; As part of severance benefit, the company’s headquarter in Lime Rock, Connecticut was transferred to him (building and leasehold improvement worth at least US$1.5M). 2&4 SEC issued cease and desist orders under securities law following his failures to file reports reflecting his sales of over US$3M of NWP stock while the stock was falling. 2&6 The company paid US$1.3M to Kuhns’ wholly-owned construction company from 1993-1995 for development of the headquarters, which he received as severance. 4 Questionable Track Record of Senior Management 30 1 30 March 1988, The New York Times, Article “A Highflier’s One Final Gamble” by Alison Leigh Cowan 2 Schedule 14A (Information Required in Proxy Statement) Dominion Bridge 3 26 October 1992, Dow Jones News Service, Article “New World Power Corp Ini 1M shares prices at $7”. 4 Distributed Power (Previously known as New World Power) 10-K filed in July 1996 5 Distributed Power (Previously known as New World Power) 10-K filed in May 1997 6 Distributed Power (Previously known as New World Power) SC 13-D in January 1996 7 Master Silicon Carbide Industries, 10-K filed in April 2012 8 Master Silicon Carbide Industries, 10-Q filed in May 2012 9 Master Silicon Carbide Industries, 15-12G filed in June 2012 10 China New Energy Group, 10-K filed in April 2010 11 China New Energy Group, 10-Q filed in November 2010 12 China New Energy Group, 8-K filed in January 2011 13 China New Energy Group, 15-12B filed in September 2012 14 Capital IQ and Thompson One Master Silicon Carbide Industries (2008 – current) Kuhns has been Chairman of the Board, President and CEO since 2008. 7 The company had negative EPS since 2008 and delisted in 2012. 7&9 According to the March 2012 10-Q, the company's financial position “raises substantial doubt about the Company’s ability to continue as a going concern.” 8 The company raised US$10M in 2008 (China Hand Fund I, LLC) and another US$10M in 2009 (Vicis Capital Master Fund). 8 Salaries: Kuhns – US$175K p.a., Fellows – US$100K p.a. 7 Kuhns Brothers – US$150K p.a. management fees 8 Rental fee of US$90K paid to Kuhns Brothers to lease NY Office Space 8 Company notified of delisting in June 2012 9 China New Energy Group (2008 – current) Kuhns became a Director in 2008, and along with Stastney and Fellows, serve on the Compensation Committee. He also serves on the Audit Committee. 10 China Hand invested US$29M from 2008-2010, and sold substantially to Vicis and related entities in the same periods 10&11 Bought assets with initial payment of US$17.6M in January 2011 12 The company traded at ~US$1 per share in 2009 and is now trading at ~US$0.03 on the OTC markets. 14 Kuhns, Fellows, Stastney receive US$20K each p.a. 10 Kuhns Brothers was paid an advisory fees of 10% of proceeds raised i.e. US$1.4M and warrants to purchase 10.4M shares as placement agents for the private placement of US$14.4M from China Hand Fund I, LLC. The fund is managed by John Kuhns. 10&14 The company has not filed recent annual reports and was recently notified of listing termination. 13 ” “ |

Proposed Board Committees of New Slate 31 Audit Compensation Corporate Governance and Nomination Moonkyung Kim Jui Kian Lim Amit Gupta Yun Pun Wong Financial Expert Dr. You-Su Lin Dr. Yong Cao Proposed Board Committees |

32 The Shareholder Group Validly Called an EGM The Company is incorporated under the laws of the Cayman Islands, and the manner in which an extraordinary general meeting (“EGM”) of the Company is to be convened and held is governed by the Company’s memorandum and articles of association (“M&A”). The Company is attempting to use its obligations under the Listed Company Manual of the New York Stock Exchange (“NYSE”) to disenfranchise the shareholders. The NYSE Listed Company Manual states that it is the responsibility of the Company and the Board to notify the NYSE regarding the setting of a record date. The Company is violating the NYSE listing rules by not giving the NYSE notice of the record date established for the EGM, despite multiple requests to do so by the Shareholder Group. Notification to NYSE regarding the record date has no bearing on the Shareholder Group’s right to call an EGM under Cayman law or Company’s M&A. Requirements under Company’s M&A Shareholder Group Actions One-third of the issued and outstanding share capital may call an EGM On August 30, 2012, over one-third of the issued and outstanding share capital of the Company filed a notice to call an EGM. 21 clear days’ notice to be given for EGM EGM notice was filed and delivered to shareholders on August 30, 2012 for EGM scheduled on September 28, 2012, which is over 21 clear days’ notice. EGM notice to specify time, place of the meeting, and general nature of business to be conducted at EGM EGM notice specifies that EGM shall be held at 9 a.m. Hong Kong time, at the offices of O’Melveny & Myers, 31st Floor, AIA Central, 1 Connaught Road, Central, Hong Kong to consider the removal and election of directors set forth in the EGM Notice. “If the Board does not fix a record date for any general meeting, the record date for determining the Members entitled to a notice of or to vote at such meeting shall be at the close of business on the day next preceding the day on which notice is given.” EGM notice was dated August 30, 2012, and Record Date was set August 29, 2012, which is “the day next preceding the day on which notice is given.” |