SAExploration Holdings, Inc.

3333 8th Street SE, 3rd Floor

Calgary, Alberta T2G 3A4

July 8, 2013

Via EDGAR AND FedEx

Securities and Exchange Commission

100 F. St, N.E.

Washington, D.C. 20549

| Attn: | Mr. Larry Spirgel Assistant Director |

Mr. Joe Cascarano, Staff Accountant

| Re: | SAExploration Holdings, Inc. |

Item 4.01 Form 8-K

Filed June 28, 2013

File No. 001-35471

Gentlemen:

SAExploration Holdings, Inc. (the “Company”) does hereby submit correspondence relating to the Company’s responses to the comments of the staff of the Securities and Exchange Commission (the “Commission”) set forth in the Commission’s letter to the Company dated July 3, 2013, regarding the Current Report on Form 8-K filed by the Company with the Commission on June 28, 2013 (the “Original Filing”), as follows:

Form 8-K

Item 4.01

Comment:

| 1. | You currently disclose that there have been no disagreements with your former accountant or reportable events during the fiscal year ended December 31, 2012 and any interim period preceding the dismissal. Please amend your filing to cover any interim period from the date of the last audited financial statements through June 24, 2013, the date of dismissal. See Item 304(a)(1)(iv) and (v) of Reg. S-K. |

Response:

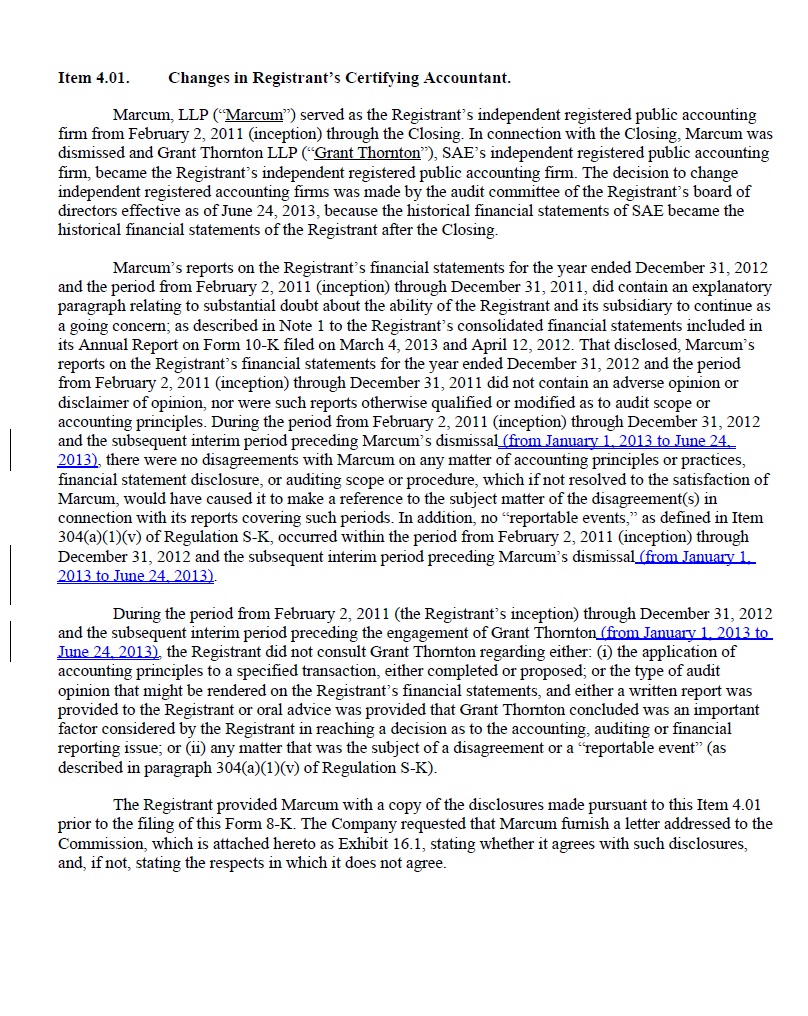

The company filed an amendment to the Original Filing on the date hereof (the “Amendment”) restating the disclosure in Item 4.01 to specify the dates of the interim period referenced in your comment. For your convenience, we are enclosing a marked copy of the Item 4.01 disclosure contained in the Amendment to note the changes from the Original Filing.

Securities and Exchange Commission

July 8, 2013

Page2

Comment:

| 2. | To the extent that you make changes to the Form 8-K to comply with our comment, please obtain and file an updated Exhibit 16 letter from the former accountant stating whether the accountant agrees with the statements made in the revised Form 8-K. |

Response:

An updated Exhibit 16 letter was filed as Exhibit 16.1 to the Amendment.

The Company acknowledges that: (i) it is responsible for the adequacy and accuracy of the disclosure in the filing; (ii) staff comments or changes to disclosure in response to the above staff comments do not foreclose the Commission from taking any action with respect to the filing; and (iii) the Company may not assert staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States.

Please contact the undersigned (713-816-6392) with any questions or further comments you may have.

Very truly yours,

/s/ Brent Whiteley

Brent Whiteley

Chief Financial Officer and General Counsel

Enclosure