Exhibit 99.1

September 17, 2012

Neil Austrian

Chairman and CEO

Office Depot, Inc.

6600 North Military Trail

Boca Raton, FL 33496

cc: Board of Directors

Dear Neil,

We enjoyed meeting with you on September 5th and appreciated the opportunity to discuss your views on Office Depot, Inc. (“Office Depot” or the “Company”), the challenges it faces, and the future opportunities it hopes to capture.

Starboard Value LP, together with its affiliates (“Starboard”), currently owns approximately 13.3% of the outstanding common shares of Office Depot, making us the Company’s largest common shareholder. Our substantial investment in Office Depot is based upon (i) our extensive due diligence on the Company and each of its business units, (ii) an analysis of its operating and financial performance, and (iii) a review of the competitive landscape in the office supply superstore (OSS) sector. Based upon our findings, we strongly believe that Office Depot’s shares are deeply undervalued and that a substantial opportunity exists to improve the Company’s performance and valuation based on actions that are within the control of Office Depot’s management team and Board of Directors (the “Board”).

By way of background, Starboard is an investment management firm that seeks to invest in undervalued and underperforming public companies. Our approach to each investment is to actively engage and work closely with management and the board of directors in a constructive manner to identify and execute on opportunities to unlock value for the benefit of all shareholders. Our principals and investment team have extensive experience and a successful track record of enhancing value at portfolio companies through a combination of strategic refocusing, improved operational execution, and more efficient capital allocation.

The purpose of this letter is to broadly outline our initial thoughts and perspectives on Office Depot for your benefit, as well as for the benefit of your management team, the Board, and our fellow shareholders. We look forward to continuing our dialog with you and your senior management team so we can further elaborate in greater detail on the points highlighted in this letter.

Historical Performance

Over the past several years, the OSS sector has been challenged by a confluence of factors that has resulted in sales deleveraging and margin compression across the peer group. While these factors are partially to blame for the deterioration in Office Depot’s financial performance, a comparison to its closest peers demonstrates that the Company has not adequately adapted to new market realities and has not reduced spending levels sufficiently to offset declines in revenues. As shown in the table below, Office Depot generated operating margins of 0.7% over the last twelve months, well below the operating margins of both Staples, Inc. (“Staples”) and OfficeMax Incorporated (“OfficeMax”) of 6.4% and 1.9%, respectively.

While a portion of the relative underperformance versus Staples may be attributable to the difference in revenue scale, we do not believe there are any structural dissimilarities that should cause the dramatic underperformance of Office Depot’s margins. Further, Office Depot’s operating margins are also substantially below those of OfficeMax, despite Office Depot’s significant scale advantage.

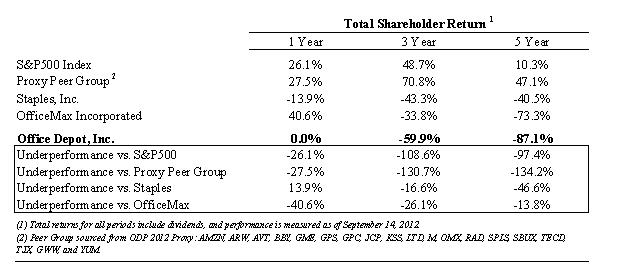

It appears that Office Depot’s poor operating performance has also had a damaging impact on stock price performance on both a relative and absolute basis. Even despite the substantial increase in stock price over the last two weeks, Office Depot’s shares have dramatically underperformed over almost any time period versus Staples and OfficeMax, its Proxy Peer Group, and the S&P500.

2

As shown in the table above, Office Depot underperformed its Proxy Peer Group by 27.5%, 130.7%, and 134.2% over the past one-, three-, and five-year periods, respectively. We believe such dramatic underperformance relative to its peer group and direct competitors can only be explained by company-specific issues.

Opportunities for Improved Operating Performance

We believe there are a variety of opportunities to dramatically improve operating and financial performance at Office Depot. We recognize and appreciate that management has taken some actions to reduce costs, drive efficiencies, improve the store format, and address low margin products in order to improve operating margins at the Company. While these initiatives represent a step in the right direction, they clearly have not been adequate enough, as is evidenced by the dramatic decline in profitability and underperformance compared to peers. We believe management must act now with a renewed sense of urgency and discipline to rationalize general and administrative expenses, significantly reduce advertising expenses, and execute on several other strategic initiatives to dramatically improve the operating performance of the Company.

General and Administrative (“G&A”) and Advertising Expenses

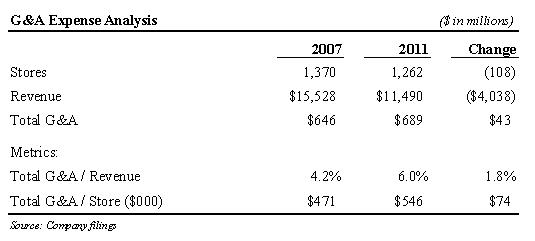

We believe Office Depot can meaningfully reduce G&A and advertising expenses to drive significantly improved profitability. From 2007 to 2011, Office Depot’s total store count declined from 1,370 to 1,262 and its total revenue declined from $15.5 billion to $11.5 billion; yet, total G&A expenses actually increased by $43 million from $646 million to $689 million over this same time period. As a percentage of revenue, total G&A expenses increased from 4.2% in 2007 to 6.0% in 2011. G&A expenses per store increased from approximately $471,000 in 2007 to $546,000 in 2011.

3

We seriously question why the Company’s G&A expenses increased by $43 million while the store count declined by 108 stores and revenue declined by $4.0 billion. By simply reducing G&A expense ratios back to 2007 levels, we believe Office Depot could improve profitability by approximately $94 million to $211 million.

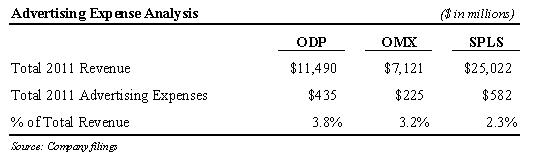

Additionally, Office Depot’s advertising expenditures, which are reported separately from G&A expenses, are substantially higher as a percentage of revenue than they are for either Staples or OfficeMax. As indicated in the table below, in 2011, Office Depot spent $435 million, or 3.8% of revenue, on advertising expenses versus Staples, which spent $582 million, or 2.3% of revenue, and OfficeMax, which spent $225 million, or 3.2% of revenue. Given Office Depot’s significantly larger scale than OfficeMax, we question why the Company is spending a higher percentage of revenue on advertising dollars.

Further heightening our concern, Office Depot’s significantly higher advertising spend as a percentage of sales has not translated to higher revenue growth relative to peers. In fact, from 2007 to 2011, Office Depot’s revenue declined by 26.0% compared to a decline of 21.6% for OfficeMax and approximately 8.6% for Staples1, despite the fact that Office Depot spent more on advertising as a percentage of revenue.

1 Estimated Staples revenue decline from 2007 to 2011 adjusts 2007 revenue by $8.0 billion to reflect the Corporate Express acquisition as per Staples transcript dated August 19, 2008.

4

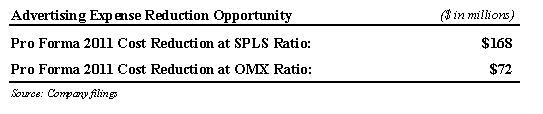

As shown in the table below, we believe Office Depot could potentially reduce advertising expenses by between $72 million and $168 million, while remaining competitive in the industry. This would still imply spending between $267 million and $363 million on advertising each year. However, reducing advertising spending alone is not enough without also improving both the efficiency and return on advertising dollars invested.

Based on our recommended reductions in G&A and advertising expenses alone, we estimate that Office Depot could improve profitability by approximately $166 million to $379 million. This compares to consensus analyst estimates for 2012 EBITDA of $286 million2, an improvement of between 58% and 133%, without even addressing in-store expense reduction and other opportunities.

Additional Opportunities for Improvement

In addition to the opportunities highlighted above, we have identified several other areas for substantial margin improvement. First, we believe the Company can significantly increase the mix of higher-margin services, such as copy and print services, technology services, security solutions, and shipping services in its North American Retail Division. As an example, services account for approximately 9% of Staples’ North American Retail revenue, substantially higher than at Office Depot. Services generally carry gross margins of 60% compared to Office Depot’s average store gross margins of approximately 30%, as well as substantially higher operating margins. For every one percent increase in the mix of services revenue, we believe Office Depot could improve operating income by $7 million to $10 million in its North American Retail business.

Second, while Office Depot’s current private label penetration is roughly in line with peers at approximately 25%, we believe there is a considerable opportunity to improve gross margins through direct sourcing. Currently, we believe direct sourced penetration at Office Depot is approximately 11-12%; however, we believe there is an opportunity to increase direct sourced penetration to approximately 20%. Industry analysts note that the margin benefit of direct sourced, private label stock-keeping units (SKUs) is approximately 400 to 600 basis points higher than private label products sourced through an agent, which is currently Office Depot’s primary method of sourcing private label SKUs. By increasing direct sourced penetration from 11% to 20%, we believe Office Depot could increase operating income by $30 million to $45 million.

5

Third, we believe there is a substantial opportunity to improve gross margins and reduce inventory by lowering the number of SKUs in order to obtain more scale in purchasing to reduce procurement expense. For example, Office Depot currently has approximately 9,000 SKUs per store versus Staples at approximately 7,000 SKUs per store.

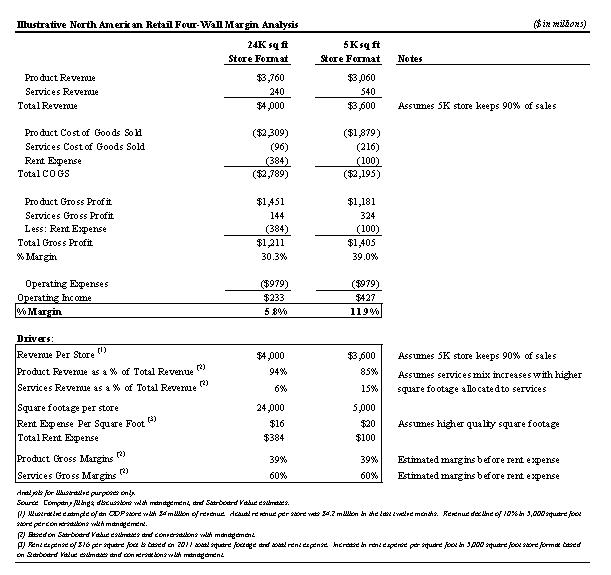

Fourth, in its North American Retail business, we believe Office Depot has a compelling opportunity to dramatically improve the economics of its stores by downsizing to smaller store formats. Currently, Office Depot’s average square footage per store of approximately 23,500 square feet is larger than Staples at approximately 21,500 square feet and OfficeMax at approximately 22,500 square feet.3 According to the Company, the new 5,000 square foot format store, relative to its existing 24,000 square foot format, can retain up to 90% of total store sales, while at the same time significantly reducing occupancy costs, improving labor utility, and reducing inventory investment by 50%. Given these economics, we believe this new store format can substantially increase operating margins compared to the Company’s current store format. Further, the leases of approximately 45% and 67% of the Company’s domestic store fleet come up for renewal over the next three and five years, respectively.4 While it may not be appropriate to downsize and remodel every store, there is nonetheless a significant opportunity to dramatically improve the store economics with the new 5,000 square foot format. In fact, based on our analysis below, we believe that the lower rent expense and higher mix of services in the 5,000 square foot stores, even when assuming the same operating expenses as the 24,000 square foot stores, will improve four-wall operating margins from approximately 5.8%5 in the 24,000 square foot stores to well over 10% in the 5,000 square foot stores.

3 Square footage per store calculated from data provided in Office Depot, Staples, and OfficeMax filings.

5 Four-wall operating margin analysis based on conversations with the Company and calculated as reported segment operating margin excluding estimated allocated of divisional G&A expense.

6

Based on the illustrative analysis above, assuming the Company downsizes between 250 and 375 stores to the new 5,000 square foot format, or 50% to 75% of stores which come up for lease renewal over the next three years, we believe operating income could be improved by approximately $50 million to $75 million.

Lastly, we believe there is substantial opportunity for improvement in Office Depot’s North American Business Solutions Division (BSD), which sells products directly to business customers through catalogs and online through the Company’s internet sites. In this business, we believe the Company could improve profitability by fully integrating its contract organization acquisitions to reduce redundancies, increasing the mix of private label products, consolidating the number of SKUs, increasing the use of direct sourcing of private label products, and increasing the mix of small-to medium-sized business (SMB) customers. Currently, Office Depot’s mix of SMBs is approximately only 35% of BSD revenue, compared to Staples’s SMB mix of between 50% and 75%. SMBs offer margins more than 1,000 basis points higher than larger national accounts, which currently comprise the majority of Office Depot’s BSD revenue. Rather than focusing on higher revenue but less profitable accounts, Office Depot should instead dramatically increase its penetration into lower revenue but significantly more profitable SMBs. In order to accomplish this, the Company must increase the mix of its sales force towards SMBs and away from large national accounts. Assuming the Company can improve its mix of SMBs from 35% to 45%, still substantially below Staples, we believe that operating income could improve by approximately $30 million to $40 million.

7

We understand and appreciate that you have identified some of the operational improvements discussed above. However, the Company needs to act on these initiatives with a greater sense of urgency and better execution, while also accomplishing the G&A and advertising expense efficiencies mentioned previously in this letter.

Non-Core Asset: Office Depot de Mexico

In addition to the substantial opportunities to improve the operating and financial performance of Office Depot as highlighted above, the Company also owns a non-core asset that we believe has substantial hidden value. Office Depot de Mexico, a 50/50 joint venture between Office Depot and Grupo Gigante, S.A.B. de C.V. (ticker: GIGANTE MM MXN), operates 252 retail stores and distribution facilities primarily in Mexico, as well as in Colombia, Costa Rica, El Salvador, Guatemala, Honduras, and Panama. We believe this highly profitable joint venture is unrecognized in Office Depot’s enterprise value given that Office Depot de Mexico is not consolidated in the Company’s financial statements and analysts value Office Depot primarily based on consolidated EBITDA (which does not include Office Depot de Mexico).

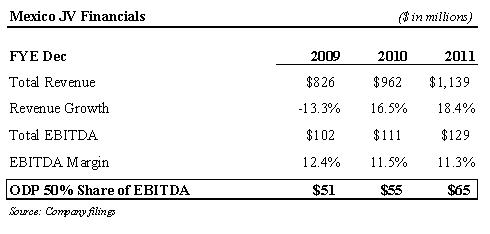

Office Depot de Mexico is a market leader in the attractive Mexican, Central American, and South American markets, which are characterized by faster growth, less competition, and far better profit margins than Office Depot’s core US market. In fact, Office Depot de Mexico grew revenue at a 17.5% compounded annual rate from $826 million in 2009 to $1.14 billion in 2011, and EBITDA from $102 million in 2009 to $129 million in 2011. Office Depot’s share of this EBITDA was approximately $65 million in 2011, versus consolidated EBITDA for Office Depot, excluding contribution from Office Depot de Mexico, of $303 million.

8

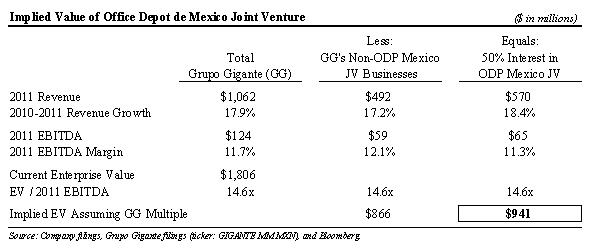

We believe Office Depot’s 50% stake in the Office Depot de Mexico joint venture is extremely valuable. Grupo Gigante's 50% share of the Office Depot de Mexico joint venture accounted for approximately 54% of Grupo Gigante’s total revenue and 52% of its total EBITDA in 2011. Since Grupo Gigante’s remaining businesses, which include supermarkets, restaurants, and home improvement retail stores, generate a similar growth and margin profile to Office Depot de Mexico, we believe the market should ascribe a similar valuation multiple to Grupo Gigante’s 50% stake in Office Depot de Mexico as it does to Grupo Gigante’s remaining businesses. At Grupo Gigante’s current enterprise value of $1.8 billion, which represents 14.6x EV/EBITDA, this implies that the market is valuing Grupo Gigante’s 50% stake in Office Depot de Mexico at more than $900 million. This value is equivalent to approximately 76% of Office Depot’s entire enterprise value today of $1.2 billion.

While we understand that Grupo Gigante’s controlling interest in Office Depot de Mexico may warrant a premium valuation, we believe there is significant value in Office Depot’s stake in the joint venture that is not being ascribed value in the public market. As further evidence, in July 2008, Grupo Gigante publicly offered $430 million, or an estimated 8x trailing EBITDA, to acquire Office Depot’s stake in Office Depot de Mexico. This 8x multiple, which is well below Grupo Gigante’s current multiple of 14.6x, implies a value of more than $500 million based on 2011 EBITDA.

Valuation

As discussed, we believe that Office Depot shares are deeply undervalued. We believe the current market price fails to reflect:

| i) | the substantial value of Office Depot’s core operating assets if operated with performance more in-line with the potential outlined in this letter, and |

| ii) | the Company’s non-core 50% interest in the Office Depot de Mexico joint venture. |

9

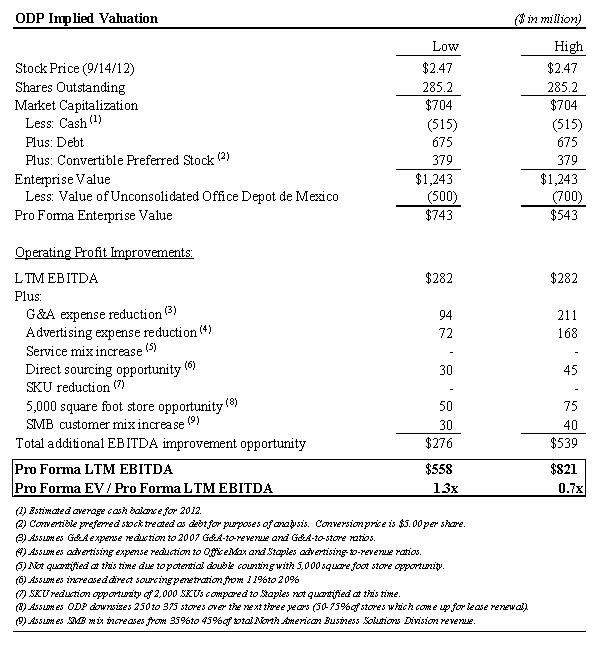

Assuming a value of $500 million to $700 million for the Company’s stake in Office Depot de Mexico, ODP shares currently trade at only 1.9x to 2.6x LTM EBITDA. Further, assuming Office Depot successfully implements many of the recommendations we have discussed in this letter, we believe the Company could improve EBITDA from $282 million to between $558 million and $821 million. On a pro forma basis for these changes, and including $500 million to $700 million of value for the Company’s stake in Office Depot de Mexico, ODP shares currently trade at only 0.7x to 1.3x pro forma EBITDA.

10

Conclusion

As mentioned above, we strongly believe that Office Depot is deeply undervalued and that there are opportunities to substantially improve operating performance and valuation based on actions within the control of management and the Board. ODP’s stock price has underperformed over almost any time period, and we believe it is time for management and the Board to take immediate action to address this underperformance. We look forward to working with you, senior management, and the Board to address the challenges and opportunities facing the Company, and to ensure that Office Depot is run with the best interests of all shareholders as the primary objective.

Best Regards,

Jeffrey C. Smith

Starboard Value LP

11