Exhibit 99.1

June 17, 2013

Members of the Board of Directors of Smithfield Foods, Inc.

Smithfield Foods, Inc.

200 Commerce Street

Smithfield, Virginia 23430

Dear Members of the Board,

Starboard Value LP, together with its affiliates (“Starboard”), currently owns securities representing beneficial ownership of approximately 5.7% of Smithfield Foods, Inc. (“Smithfield” or the “Company”). We have been a shareholder of Smithfield since March 2013, several months prior to the announcement on May 29, 2013 that Smithfield and Shuanghui International Holdings Limited (“Shuanghui”) entered into a definitive merger agreement valuing Smithfield at approximately $7.4 billion, or $34.00 per share (the "Proposed Merger"). We initially invested in Smithfield because we believed that the Company was significantly undervalued and that there were opportunities within the control of management and the Board of Directors (the "Board") to substantially improve value for the benefit of shareholders. Specifically, our research indicated that the sum-of-the-parts value of the Company’s operating divisions, which include Hog Production, International, and Pork, was well in excess of the then-current trading price of Smithfield. Our analysis indicated that a separation of these businesses was entirely feasible and could be accomplished without significant tax leakage. Also, we believed that there were several likely strategic acquirors for each of these divisions. On a standalone basis, we had also identified opportunities for increased operational efficiencies that, particularly in the Pork division, could dramatically improve operating margins and profitability. Based on these factors, we felt Smithfield was an attractive investment with significant potential upside based on improved execution and a separation of the operating divisions.

As a significant stakeholder of the Company, we are sending you this letter in order to:

| (1) | Share our in-depth research and analysis on Smithfield with management and the Board, which we believe clearly demonstrates that Smithfield could be worth well in excess of $34.00 per share if the Company had fully shopped its operating divisions to all such potentially interested parties; |

| (2) | Inform the Board that we believe there are numerous interested parties for each of the Company's operating divisions, and that a piece-by-piece sale of the Company's businesses could result in greater value to the Company’s shareholders than the Proposed Merger; and |

1

| (3) | Inform the Board of our intention to fully explore the possibility of whether greater value could be realized by way of a piece-by-piece sale of the Company's valuable, yet disparate, operating divisions to interested third parties. In this way, we can be satisfied that Starboard fulfilled its duty to its investors while at the same time serving the interests of shareholders by providing them with another metric by which to critically evaluate the Proposed Merger. |

We fully understand that under the Merger Agreement, Smithfield is contractually prohibited from seeking superior offers for the Company or from contacting third parties who may be interested in acquiring certain of the Company's operating divisions. In light of this limitation, Starboard is seeking to identify and connect any strategic or financial buyers for the Company's individual business units to determine if it would be possible to structure a sum-of-the-parts transaction that could deliver greater value for shareholders than the Proposed Merger. We hope that our efforts will lead to the submission of a Superior Proposal under the terms of the Merger Agreement.

By way of background, Starboard is an investment management firm that seeks to invest in undervalued and underperforming public companies. Our approach to such investments is to actively engage and work closely with management teams and boards of directors in a constructive manner to identify and execute on opportunities to unlock value for the benefit of all shareholders. Our principals and investment team have extensive experience and a successful track record of enhancing value at portfolio companies through a combination of improved operational execution and strategic transactions.

Introduction

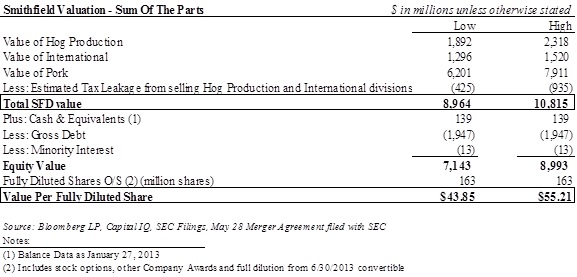

We believe the Proposed Merger goes a long way towards closing the gap between the pre-deal market value of Smithfield and the intrinsic value of the business. However, we believe the Proposed Merger still significantly understates a conservative sum-of-the-parts valuation of the Company, which we estimate to be worth between $9 billion and $10.8 billion after tax, or approximately $44 to $55 per share, representing an approximate 29%-62% premium to the $34 per share Shuanghui deal.

Our sum of the parts analysis is based upon publicly available information, our knowledge of the industry, and extensive due diligence, but there may be information within the Company’s possession, such as tax basis, and other attributes which would likely impact our analysis. As shown in the table below, we assume that upon acquiring Smithfield, a potential acquiror would sell both the Hog Production and International divisions. We believe this would result in a conservatively estimated tax liability of $425 million to $935 million. If a proposed acquiror does not sell all of these two divisions, then any tax liability would be lower.

2

Smithfield is the largest hog producer and pork processor in the world with three main divisions: Hog Production, International, and Pork. The Hog Production segment is the largest hog farming operation in the world with approximately 851,000 sows producing approximately 16 million hogs annually. The International division consists of a number of interests in market leading hog farming, meat processing, and branded meat operations in Poland, Romania, UK and Mexico, among other countries. Lastly, the Pork division is the largest pork processing operation in the world, producing and marketing internationally fresh pork and packaged meat products under a variety of brand names.

For long before the announced transaction, public investors have applied a conglomerate discount to the value of Smithfield because of the disparate nature of the divisions and the vastly different operational and financial characteristics of these businesses. We believe the price offered by Shuanghui reflects such a conglomerate discount, and a better outcome may have been achieved had the Company explored a separation and sale of the operating divisions individually.

In addition, while Smithfield has historically operated as a vertically integrated pork processor, we believe there are no major structural hurdles preventing each of the Company’s divisions from operating well as part of, or combined with, other companies. Specifically, we believe that the Pork division, touted by the company management as the main beneficiary of partial vertical integration, would be able to leverage its size and bargaining power to contractually secure a steady supply of high quality, genetically consistent, and traceable hogs similar to the arrangements employed by other leading meat processing companies that are not vertically integrated.

3

In fact, Smithfield currently has many of these arrangements already in place with some of its largest hog suppliers. Since the early 2000’s, Smithfield has “[…] established multi-year agreements with Maxwell Foods, Inc. and Prestage Farms, Inc., which provide [the Company] with a stable supply of high-quality hogs at market-indexed prices[…] In addition, [The company has] sublicensed some [genetic lines of specialized breeding stock] to some of […]strategic hog production partners.” 1 Hormel, Smithfield’s main comparable company, further notes that “…Supply contracts have become prevalent in [the pork] industry”, and that “in fiscal 2012, [it] purchased approximately 97% of its hogs under supply contracts”. 2 It is our expectation that potential acquirors of Smithfield’s separate units would establish mutually beneficial long term supply agreements to provide the Hog Production division with visibility of sales and the Pork division with the security of hog supply.

It is our belief that the divisions of Smithfield are easily separable and had the Company explored a sale of these businesses in separate transactions, shareholders may have received far more value than the $34 per share consideration contemplated by the Proposed Merger. We question whether the Board gave sufficient consideration to a sale of the divisions in separate transactions, or whether it focused primarily on an all-cash transaction for the Company as a whole, which we believe would entail a much more limited universe of potential buyers.

It is incumbent upon Starboard to fully explore whether strategic or financial buyers are interested in the Company's operating divisions in order to confirm our belief that the sum of Smithfield's parts are indeed greater than its whole. We are therefore looking to identify and engage in discussions with any third parties who may be interested in acquiring any of Smithfield's operating units. While we recognize the Company's limitations under the Merger Agreement, if interested acquirors emerge whose offers for the Company's individual units represent in the aggregate superior value than the Proposed Merger, we believe the Board must consider a Change in Company Board Recommendation under the terms of the Merger Agreement.

Hog Production Division

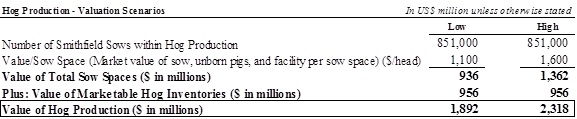

Smithfield’s Hog Production division is the largest hog farming operation in the world with approximately 851,000 sows producing approximately 16 million hogs annually. Given the commodity nature of feed inputs and hog prices, which can cause large temporary fluctuations in the profitability of hog farming businesses, acquirors generally value these businesses on an asset value basis. This primarily includes the value of sows (adult female pigs) at market prices, unborn pigs carried by sows, live hog inventory (based on futures market prices) and, to a lesser extent, the value of the land and production facilities at the farms.

Smithfield’s management has previously stated that Hog Production “[ ]…is one of the most valuable assets within the Company.” We agree. In fact, assuming only a pure liquidation value (which would be an unrealistic, and extremely low, case) of Smithfield’s sows and live hog inventory based on the sole slaughter value of the animals at current futures prices, we estimate the Hog Production division to be worth at least $1.4 billion, as shown in the table below:

1 2008-2012 SFD Forms 10-K

2 2012 HRL Form 10-K

4

However, Smithfield’s sows are realistically worth far more than their slaughter value. Based on conversations with industry sources, including Smithfield’s own hog suppliers, we believe that sows are currently being sold at prices ranging from $400 to $500 per head depending on the number of litters remaining. In addition, not only do Smithfield’s sows have productive value, but a substantial portion are generally carrying about 13 unborn hogs at any given time, currently being priced at $20 per head in the market. Assuming that 50% of Smithfield’s sows carry 13 unborn hogs each, the value of the current unborn hogs sold with each sow would be $130 per sow. In addition, in any sale of a sow farm, the acquiror will also purchase the farm’s buildings, equipment, and land (assuming it is owned). In general, the facilities associated with the sows in a sale of a farm, excluding the land, currently command an additional valuation of $600 to well over $1,000 per sow space. This value for facilities compares to the multiple at which we believe Smithfield sold its 30,000-sow space Dalhart, TX farm, which only included facilities and did not include any animals, to Cargill, in May 2011 for a price of approximately $1,000 per sow space.

Added together, current transactions for sow farms, including sows, unborn pigs, facilities, and equipment, but excluding land and live hog inventory, imply a price of approximately $1,100 to $1,600 per sow space (sow, unborn pigs and facility space).

5

Assuming a value range of $1,100 to $1,600 per sow space and adding the value of Smithfield’s current live hog inventories, we estimate the pre-tax value of the Hog Production division to be between $1.9 billion and $2.3 billion:

We understand that some of Smithfield’s sows are housed in contracted facilities that are not company owned and which should understandably command lower values than sows in owned farms. However, our analysis ascribes no value to Smithfield’s considerable land assets, which in certain geographies can increase the value of a farm to well over $2,000 per sow space. In fact, according to Smithfield’s latest form 10-K, the Company’s land on its balance sheet at historical cost is valued at $269 million. It is our understanding that a significant amount of that value is associated with the Hog Production division. Therefore, we believe our $1,100 to $1,600 per sow space to be highly conservative and below what we would expect in a negotiated transaction.

In addition, while we believe the valuations above to be suitable for individual farms, we note that Smithfield’s Hog Production operations are the largest in the world and have strategic value to the entire U.S. agricultural sector and global pork supply chain. Therefore, we believe Smithfield’s Hog Production division should command a premium valuation to the smaller comparable transactions that have recently taken place across the United States. In fact, our research indicates that large sow farms are currently being negotiated at prices in excess of $2,000 per sow space. At $2,000 per sow space, the value of Smithfield’s Hog Production division would be approximately $2.7 billion instead of the $2.3 billion we are using above.

International Division

The International division primarily consists of Fresh and Packaged Meat companies with leading market shares across Western European markets. These high quality businesses have demonstrated remarkable resilience by actually growing since the onset of the recession across Western Europe.

In Poland, Smithfield generates most of its $1.5 billion in net sales through Animex, Poland’s largest producer of fresh and packaged pork, beef, and poultry, with an estimated market share of 15%, and one of the largest Pan-European branded food marketing companies. The remainder of Smithfield’s Polish sales is generated by AgriPlus, one of the top hog producers in Poland. While we believe Smithfield’s Polish operations would command a premium valuation given their market leading position and strong sales and profitability growth, we are valuing this business at 6.5x – 7.5x EBITDA, to take into account the approximately 25% of sales generated by the more volatile hog production operations.

6

In Romania, Smithfield generates approximately 60% of its $400 million in gross sales through Smithfield Ferme, one of the largest hog producers in the country, with the balance of revenue coming from Smithfield Prod, Romania’s largest producer of fresh pork with an estimated market share of 30%. We value the Romanian operations at 5.5x – 6.5x EBITDA to reflect a larger percentage of operating earnings derived from more volatile hog production operations. We believe this multiple is conservative considering the sales and margin growth achieved since Romania was authorized to export pork products to the European Union in Q4 2012, which is expected to continue.

While we believe a more accurate valuation of the operations in Poland and Romania would consist of valuing hog farming, processing and branded food operations separately, Smithfield does not provide enough public information for this analysis. Therefore we have conservatively decided to apply a discounted range of multiples to European branded meat and food processing companies:

The International division also includes a 37% stake in the publicly listed Campofrio Food Group, one of the largest Pan-European branded meat companies with a portfolio of market leading brands generating over $2 billion in sales per year. While we prudently value this business at its quoted market value, we believe this valuation understates the true value that this business would garner in a negotiated transaction. Smithfield owns 37% of Campofrio and, together with Oaktree, a 17% shareholder, would represent a majority of shares outstanding. We believe there is a possibility that an acquiror of Smithfield’s stake in Campofrio would be able to work with the management of Campofrio to realize a premium valuation.

In total, using conservative valuation multiples, we believe the value the International operations to be between $1.3 billion and $1.5 billion:

7

Pork Division

Smithfield’s Pork division is the Company’s largest segment by revenue and EBITDA, generating approximately $11 billion in sales and over $700 million in EBITDA. The Pork division is the largest pork processing operation in the world, producing over seven million pounds of fresh pork and packaged meat at 40 plants in the U.S. These products are marketed domestically and globally.

The Fresh Pork business, which generates approximately 45% of the total Pork division’s revenue, consists of sales of unprocessed, trimmed cuts of pork sold primarily to foodservice, deli, and retail customers. The Packaged Meats business, which generates the remaining 55% of sales, consists of packaged meats products such as bacon, ham, and sausage as well as ready-to-eat meats. These products are marketed under a number of brand labels such as Smithfield, Farmland, Eckrich, and Armour, many of which hold either number one or number two market share across a number of processed pork product categories.

Not only is the Pork division Smithfield’s largest contributor by revenue and EBITDA, but we also believe that it is by far the most valuable business inside of the Company. Over the last five years, Smithfield’s Pork division has grown revenue by approximately 7% per year and generated EBITDA margins, before corporate overhead allocation, of between 4% and 9%:

8

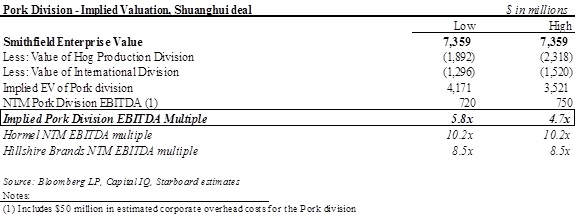

The consistent financial performance of the fresh pork and packaged meats business has resulted in significant public market valuations for pure-play comparable companies. In fact, Smithfield’s two largest competitors, Hillshire Brands and Hormel Foods, currently trade at between 8.5x and 10.2x NTM EBITDA respectively. Yet, despite the substantial value that should be associated with Smithfield’s Pork division, as is evident by its closest competitors, we believe that Shuanghui’s offer of $34.00 per share values this asset, after backing out the value of the Hog Production and International operations, at only 4.7x to 5.8x EBITDA:

While we acknowledge that Smithfield’s Pork division may deserve a lower EBITDA multiple than Hormel and Hillshire because it derives a larger proportion of sales from fresh pork and because it caters more to the ‘value’ segment of the packaged meat market, we do not believe a discount of approximately 50% is justified. We believe a multiple of only half that of Hormel’s and Hillshire’s completely ignores the importance of Smithfield’s Pork division for the global pork industry and its growth potential, already demonstrated with top line growth of approximately 20% over the last three years.

However, even more important, is that the implied EBITDA multiple of Shuanghui's offer drops significantly when considering the material operational improvement opportunities inside the Pork division, on a stand-alone basis, which we believe are completely within the control of management. In fact, based on our analysis, we believe that Smithfield could improve the profitability of the Pork division by approximately $170 million to $220 million within the next 12 to 18 months. Accounting for this improvement in operating profit, which we detail below, we actually believe that Shuanghui is paying only 3.6x to 4.7x EBITDA for this highly valuable asset:

9

Fresh Pork Performance

As noted above, Smithfield’s Fresh Pork business consists of sales of unprocessed, trimmed cuts of pork across the retail, foodservice, and deli channels. While there are no publicly traded pure-play comparable companies, we consider Tyson’s Pork division the most appropriate benchmark to gauge Smithfield’s Fresh Pork performance given the similarity in products, size, and end markets. Since 2008, and after a restructuring implemented in 2009, Smithfield’s Fresh Pork division has consistently underperformed Tyson on both capacity utilization - measured on the industry standard 6-day week as used by Tyson and competitors - and EBIT/head metrics. The latter figure, different from the fully loaded numbers reported by Tyson, does not include any corporate overhead allocation which Smithfield excludes from its operating earnings calculation and that, if accounted for, would further depress Smithfield’s EBIT/head metrics:

10

We believe this underperformance can be addressed by management or any potential acquiror over the next 12-18 months by:

| 1) | Consolidating processing capacity by selling or decommissioning older, smaller or inefficient plants catering to the same geographical areas |

| 2) | Reallocating Fresh and Packaged Pork packing load to the biggest or most efficient plants currently operated by the Company |

| 3) | Increasing daily shifts at the most efficient plants to align effective available capacity to industry average |

| 4) | Marketing available capacity to other Fresh Pork and Packaged Meat companies via co-packing contracts to reduce the fixed operating costs currently weighing on EBIT/head metrics |

Through a combination of the above options, we believe that Smithfield would be able to materially increase EBIT/head and operating profit margins by 250bps to 300bps, or $120 million to $150 million in additional operating earnings. In extracting such efficiencies, Smithfield would also be aided by its larger total Fresh Pork processing capacity spread across a lower number of plants compared to Tyson - nine plants for Tyson vs. eight for Smithfield - which would imply a lower fixed cost burden per each processed head. It is also worth noting that the projected margin improvement does not include any synergy from which a strategic buyer would be able to benefit by optimizing corporate overhead costs, currently absorbing approximately $100 million of operating earnings across the entire company, 50% of which we allocate to the entire Pork division.

11

Packaged Meat Performance

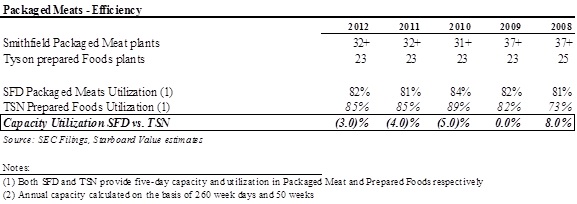

As noted above, Smithfield’s Packaged Meats business produces a number of added value meat products such as bacon, ham, and sausage as well as ready-to-eat meats. The Company markets these products under twelve core brands such as Smithfield, Farmland, Eckrich, and Armour, many of which hold either number one or number two market share across a number of processed pork goods categories. Given the homogeneity of products and the available information on profitability and capacity utilization, we compare Smithfield’s Packaged Meat’s performance to both Hormel and Tyson.

Since Hormel generates the majority of its operating income from its processed pork products we believe it represents a helpful benchmark for Smithfield’s Packaged Meats profitability. As shown in the table below, over the last five years Smithfield’s Packaged Meats EBITDA margins have consistently trailed Hormel’s by approximately 300bps. This underperformance is before any corporate overhead allocation which Smithfield excludes from its reported segment results. If an allocation of corporate overhead was included, this gap would be even wider:

While some of this margin differential can be ascribed to Hormel’s continuous investment in brands, which lead to higher gross margins, we still believe Smithfield’s Packaged Meats business has a sizeable opportunity within the control of the Company to improve operations and expand margins.

Since Hormel does not provide capacity utilization information, we have opted to conservatively use Tyson’s Prepared Food utilization to benchmark Smithfield’s Packaged Meats efficiency. We believe Tyson’s Prepared Foods is the most relevant benchmark because it processes a variety of proteins with similar manufacturing techniques, therefore providing a useful performance ‘floor’ to gauge Smithfield, which processes exclusively pork. While we consider Smithfield’s Packaged Meats and Tyson’s Prepared Foods’ utilization rates to be comparable, we do not believe comparing their profitability is appropriate, given the difference in pricing and margins of chicken and beef compared to pork.

12

As shown in the table below, since 2009, Smithfield’s Packaged Meats’ capacity utilization has consistently lagged behind Tyson’s Prepared Foods’:

Smithfield’s lower utilization rate is even more surprising considering that its manufacturing process should be simpler and benefit from processing solely pork with a continuous supply, compared to Tyson’s Prepared Foods, which processes pork, beef, and chicken. Additionally, while the Independent Operating Companies within the Pork group have been reduced from seven to three as part of the 2009 restructuring, we believe there are still meaningful inefficiencies stemming from an uncoordinated approach to product manufacturing which continues to impact the profitability of Smithfield’s Packaged Meats. For example, a substantial number of Packaged Meats processing plants appear to be processing products by brand, rather than by product. This results in a larger number of under-utilized processing plants that are manufacturing duplicative products. Instead, Smithfield could substantially reduce its manufacturing footprint by taking more of a product approach regardless of brand. We believe this would reduce manufacturing capacity and improve utilization rates thereby improving profitability within the packaged meats business.

Based on our estimates, we believe that at least 30% of the current ~300bps margin gap vs. Hormel can be captured by initiatives within the control of management such as consolidation of plant capacity and further reduction of Independent Operating Companies, which we estimate would produce at least $50 million to $70 million in additional operating profit.

Finally, while not included in our analysis, we believe a longer term opportunity exists to further expand margin by an additional 200bps through continuous investment in a reduced number of brands and increased marketing spend that CPG companies like Hormel and Hillshire have been able to successfully and consistently execute. We estimate such an opportunity to be material and achievable by any strategic acquiror interested in Smithfield’s Packaged Meat division.

13

***********

Accounting for the above operational improvements, we estimate that Smithfield could achieve Pro-Forma EBITDA of between $890 million and $970 million over the next 12-18 months, which suggests a multiple implied by the Shuanghui acquisition of only 3.6x to 4.7x Pro-Forma EBITDA:

Discounting Hormel and Hillshire Brands’ public market multiples by 1.5x to 2.0x EBITDA to account for the higher mix of fresh pork and lower margins of Smithfield’s Pork division, we estimate that the Pork division should be worth between $6.2 billion and $7.9 billion:

We Believe the Sum of Smithfield's Parts in an Alternative Transaction Structure is Greater than the $34 Cash Consideration under the Proposed Merger

We believe the Proposed Merger significantly understates a conservative sum-of-the-parts valuation of Smithfield, which we estimate to be worth between $9 billion and $10.8 billion after tax leakage, or approximately $44 to $55 per share, representing an approximate 29%-62% premium to the Shuanghui deal:

14

We question whether the Board conducted a full strategic process to determine whether a piece-by-piece sale of the Company's valuable, yet disparate, operating divisions could have provided greater value to shareholders than the Proposed Merger.

To be clear, the purpose of our letter is not necessarily to come out in opposition to the Proposed Merger. As stated above, we believe the Proposed Merger goes a long way towards unlocking the intrinsic value of the Company for shareholders. We would be remiss, however, to let an opportunity slip by to determine whether the Company could realize even greater value for shareholders. We believe our involvement will be welcomed and supported by the numerous Smithfield investors who, like us, recognize the additional value that the Company’s assets have over and above the current offer. Lending further credence to our views, we note that on the day the deal with Shuanghui was announced, the market capitalization of Henan Shuanghui, China’s largest meat processing company majority owned by Shuangui International, increased by approximately $1.2 billion.

Conclusion

As one of Smithfield's largest beneficial owners, our interests are aligned with those of all shareholders. While the current transaction represents a premium to the historical Smithfield trading range based on management's current standalone plan, we believe superior value may be achieved through a transaction based on the considerable value of each of the Company's divisions. We look forward to determining whether there are potential interested parties who could facilitate a sum-of-the-parts transaction structure that could deliver even greater value for shareholders than the Proposed Merger at this time. By sending this letter to the Board, Starboard is not taking any position or making any recommendation on the Proposed Merger and reserves all rights related thereto.

15

Best Regards,

/s/ Jeffrey C. Smith

Jeffrey C. Smith

Managing Member

Starboard Value LP

/s/ Jeffrey C. Smith

Jeffrey C. Smith

Managing Member

Starboard Value LP

About Starboard Value:

Starboard Value LP is a New York-based investment adviser with a focused and differentiated fundamental approach to investing in publicly traded U.S. small cap companies. Starboard invests in deeply undervalued small cap companies and actively engages with management teams and boards of directors to identify and execute on opportunities to unlock value for the benefit of all shareholders.

Investor Contacts:

Gavin Molinelli, (212) 201-4828

Cristiano Amoruso, (212) 845-7947

www.starboardvalue.com

16