Exhibit 99.1

STRATEGY EXCELLENCE GROWTH

Credit Suisse Energy Summit

Vail, CO

February 12, 2014

Pacific Drilling

Forward Looking Statements

Certain statements and information contained in this presentation (and oral statements made regarding the subjects of this presentation) constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements typically include words or phrases such as “believe,” “expect,” “anticipate,” “project,” “plan,” “intend,” “foresee,” “our ability to,” “estimate,” “potential,” “will,” “should,” “would,” “could” or other similar words, which are generally not historical in nature. Such forward-looking statements specifically include statements involving payment and timing of any future dividends; future operational performance and cashflow; revenue efficiency levels; client contract opportunities; estimated duration of client contracts; contract dayrate amounts; future contract commencement dates and locations; backlog; construction, timing and delivery of newbuild drillships; capital expenditures; growth opportunities; market conditions; cost adjustments; estimated rig availability; new rig commitments; the expected period of time and number of rigs that will be in a shipyard for repairs, maintenance, enhancement or construction; direct rig operating costs; compensation levels; shore based support costs; selling, general and administrative expenses; income tax expense; expected amortization of deferred revenue; expected amortization of deferred mobilization expenses; and expected depreciation and interest expense for the existing credit facilities and senior bonds. These forward-looking statements are based on our current expectations and beliefs concerning future developments and their potential effect on us. While management believes that these forward-looking statements are reasonable as and when made, there can be no assurance that future developments affecting us will be those that we anticipate. In particular, with respect to our any forward looking statements regarding the payment and timing of any future dividends, the declaration of any dividend payments is at the discretion of our Board of Directors, subject to the laws of Luxemburg, and heavily dependent on our company realizing projected cashflows, which could be materially impacted by the factors listed below, among others, including many factors that are outside of our control. There can be no assurance that we will make dividend payments within the period forecasted or at all. All comments concerning our expectations for future revenue and operating results are based on our forecasts for our existing operations and do not include the potential impact of any future acquisitions. Our forward-looking statements involve significant risks and uncertainties (some of which are beyond our control) and assumptions that could cause actual results to differ materially from our historical experience and our present expectations, plans or projections. Important factors that could cause actual results to differ materially from projected cashflows and other projections in the forward-looking statements include, but are not limited to: our ability to secure and maintain drilling contracts, including possible cancellation or suspension of drilling contracts as a result of mechanical difficulties, performance or other reasons; risks inherent to shipyard rig construction, repair, maintenance or enhancement, including delays; unplanned downtime and other risks associated with offshore rig operations, including unscheduled repairs or maintenance; relocations, severe weather or hurricanes; changes in worldwide rig supply and demand, competition and technology; future levels of offshore drilling activity; impact of potential licensing or patent litigation; actual contract commencement dates; environmental or other liabilities, risks or losses; governmental regulatory, legislative and permitting requirements affecting drilling operations; our ability to attract and retain skilled personnel on commercially reasonable terms; governmental action, civil unrest and political and economic uncertainties; terrorism, piracy and military action; and the outcome of litigation, legal proceedings, investigations or other claims or contract disputes.

For additional information regarding known material risk factors that could cause our actual results to differ from our projected results, please see our filings with the Securities and Exchange Commission (SEC), including our Annual Report on Form 20-F and Current Reports on Form 6-K. These documents are available through our website at www.pacificdrilling.com or through the SEC’s Electronic Data and Analysis Retrieval System at www.sec.gov.

Existing and prospective investors are cautioned not to place undue reliance on forward-looking statements, which speak only as of the date hereof. We undertake no obligation to publicly update or revise any forward-looking statements after the date they are made, whether as a result of new information, future events or otherwise.

Pacific Drilling

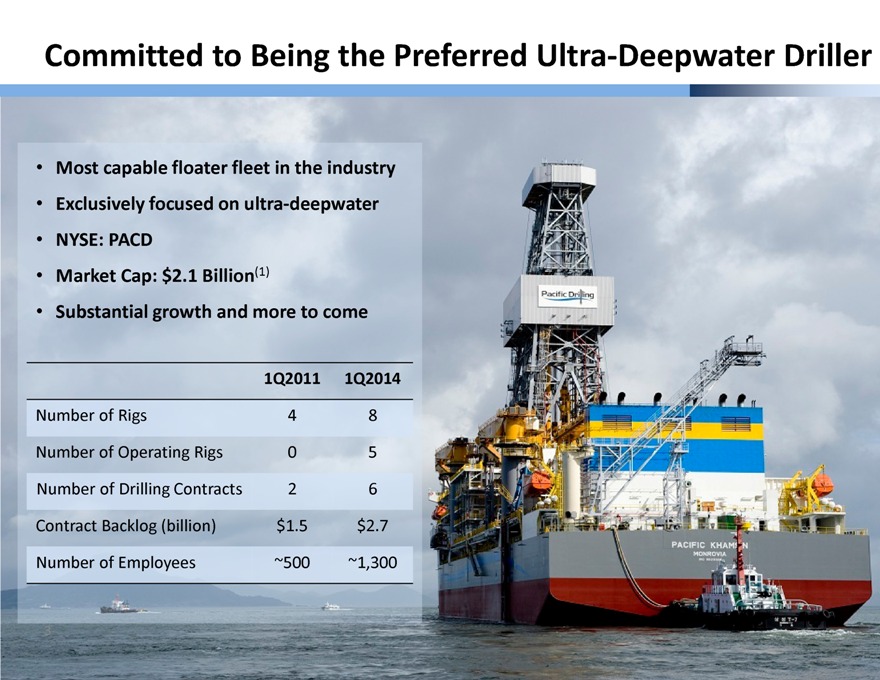

Committed to Being the Preferred Ultra-Deepwater Driller

Most capable floater fleet in the industry

Exclusively focused on ultra-deepwater

NYSE: PACD

Market Cap: $2.1 Billion(1)

Substantial growth and more to come

1Q2011 1Q2014

Number of Rigs 4 8

Number of Operating Rigs 0 5

Number of Drilling Contracts 2 6

Contract Backlog (billion) $1.5 $2.7

Number of Employees ~500 ~1,300

3

Financial Performance Highlights

($m) 180 160 140 120 100 80 60 40

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13

Dayrate Revenue Direct

Rig Related Operating Expenses

Adjusted EBITDA

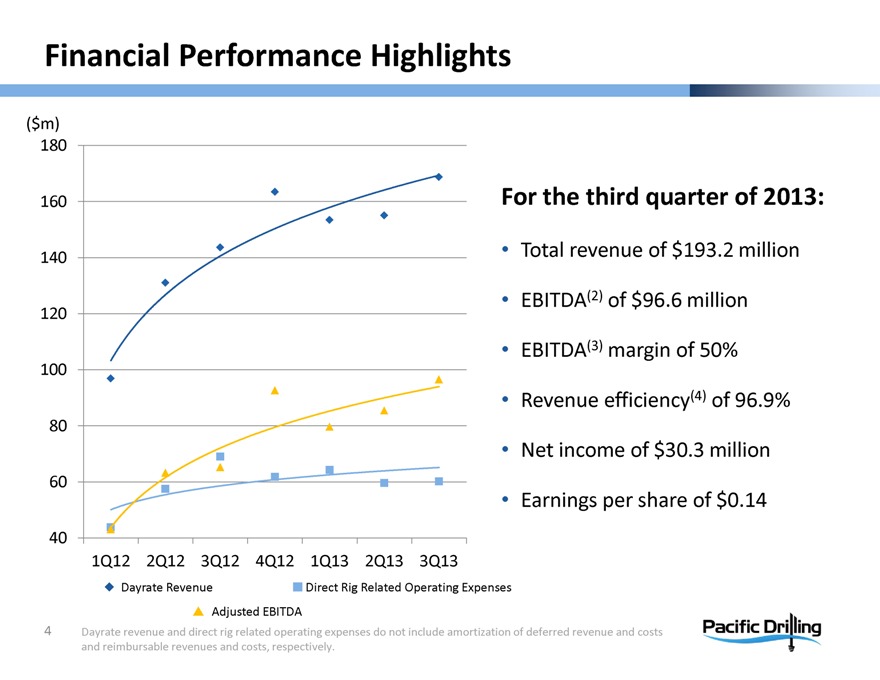

For the third quarter of 2013:

Total revenue of $193.2 million

EBITDA(2) of $96.6 million

EBITDA(3) margin of 50%

Revenue efficiency(4) of 96.9%

Net income of $30.3 million

Earnings per share of $0.14

4

Dayrate revenue and direct rig related operating expenses do not include amortization of deferred revenue and costs and reimbursable revenues and costs, respectively.

Pacific Drilling

Positioned for Further Success

STRATEGY

EXCELLENCE

GROWTH

5

Pacific Drilling

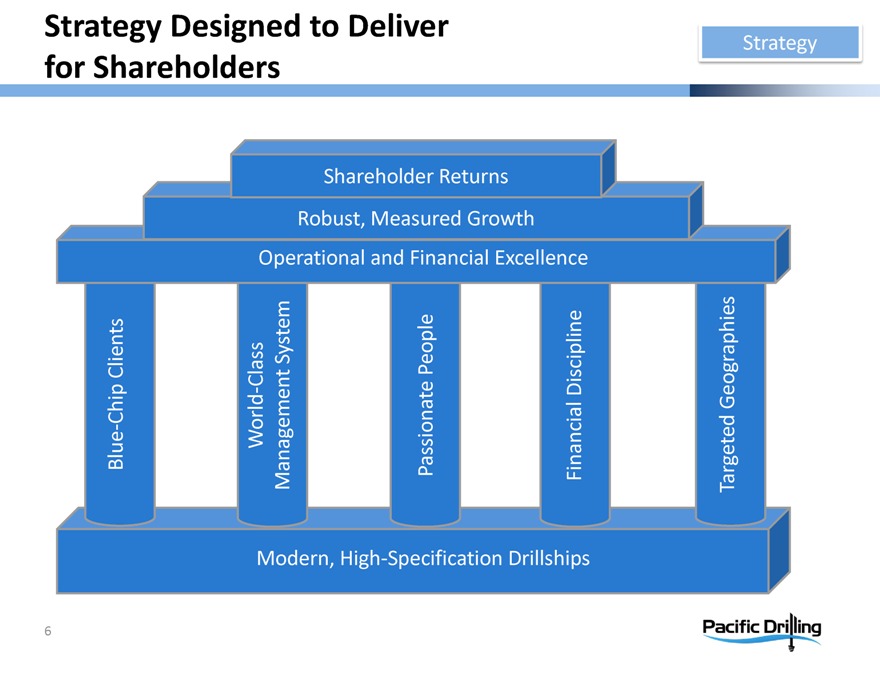

Strategy Designed to Deliver for Shareholders

Strategy

Shareholder Returns

Robust, Measured Growth Operational and Financial Excellence

Blue-Chip Clients

World-Class Management System

Passionate People

Financial Discipline

Targeted Geographies

Modern, High-Specification Drillships

6

Pacific Drilling

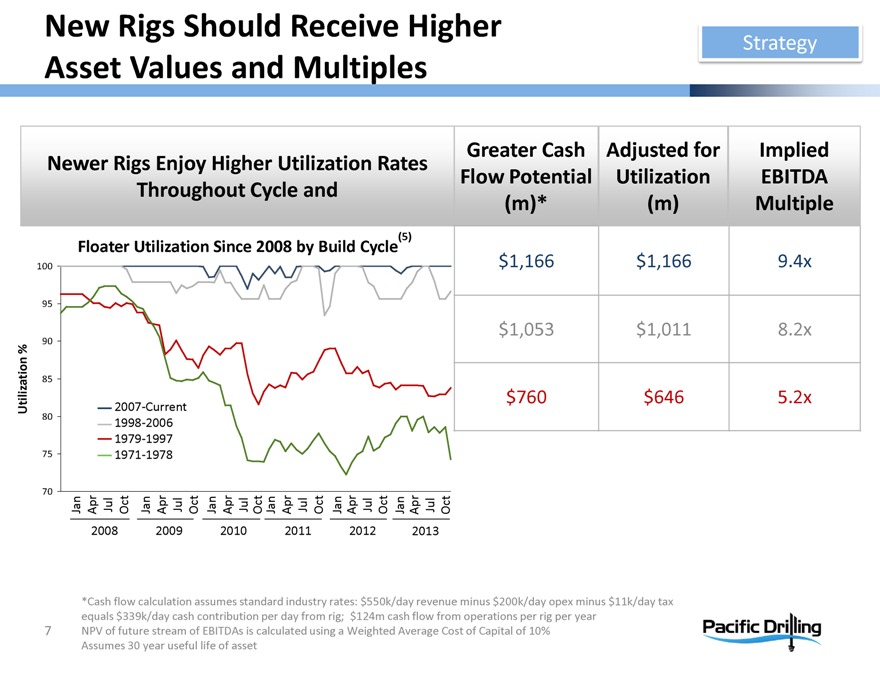

New Rigs Should Receive Higher Asset Values and Multiples

Strategy

Newer Rigs Enjoy Higher Utilization Rates Throughout Cycle and

Floater Utilization Since 2008 by Build Cycle (5)

70 75 80 85 90 95 100

2008 2009 2010 2011 2012 2013

Jan Apr Jul Oct Jan Apr Jul Oct Jan Apr Jul Oct Jan Apr Jul Oct Jan Apr Jul Oct Jan Apr Jul Oct

2007-Current 1998-2006 1979-1997 1971-1978

Utilization %

Greater Cash Flow Potential (m)*

Adjusted for Utilization (m)

Implied EBITDA Multiple

$1,166 $1,166 9.4x $1,053 $1,011 8.2x $760 $646 5.2x

*Cash flow calculation assumes standard industry rates: $550k/day revenue minus $200k/day opex minus $11k/day tax equals $339k/day cash contribution per day from rig; $124m cash flow from operations per rig per year NPV of future stream of EBITDAs is calculated using a Weighted Average Cost of Capital of 10% Assumes 30 year useful life of asset

7

Pacific Drilling

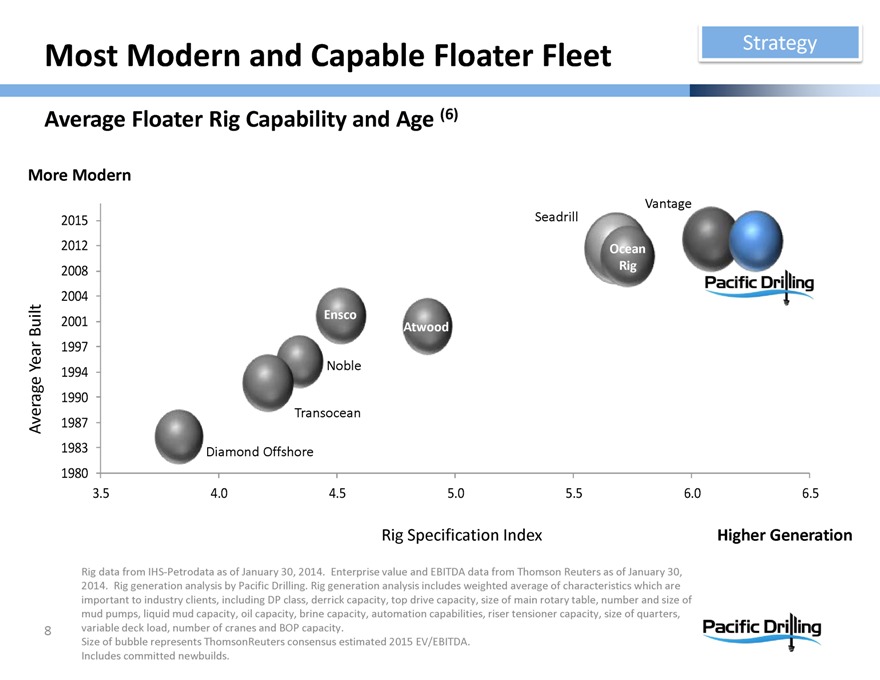

Most Modern and Capable Floater Fleet

Strategy

Average Floater Rig Capability and Age (6)

More Modern

Average Year Built

2015 2012 2008 2004 2001 1997 1994 1990 1987 1983 1980

Pacific Drilling

Vantage

Seadrill

Ocean

Rig

Ensco

Atwood

Noble

Transocean

Diamond Offshore

3.5 4.0 4.5 5.0 5.5 6.0 6.5

Rig Specification Index

Higher Generation

Rig data from IHS-Petrodata as of January 30, 2014. Enterprise value and EBITDA data from Thomson Reuters as of January 30, 2014. Rig generation analysis by Pacific Drilling. Rig generation analysis includes weighted average of characteristics which are important to industry clients, including DP class, derrick capacity, top drive capacity, size of main rotary table, number and size of mud pumps, liquid mud capacity, oil capacity, brine capacity, automation capabilities, riser tensioner capacity, size of quarters, variable deck load, number of cranes and BOP capacity.

Size of bubble represents ThomsonReuters consensus estimated 2015 EV/EBITDA. Includes committed newbuilds.

8

Pacific Drilling

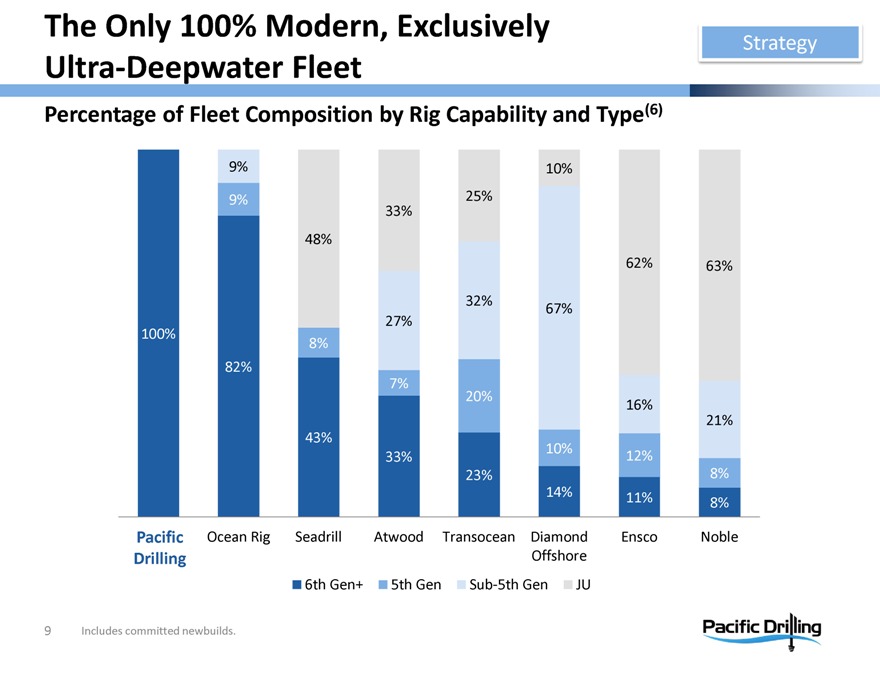

The Only 100% Modern, Exclusively Ultra-Deepwater Fleet

Strategy

Percentage of Fleet Composition by Rig Capability and Type(6)

Pacific Drilling

Ocean Rig

Seadrill

Atwood

Transocean

Diamond Offshore

Ensco

Noble

9%

10%

9%

25%

33%

48%

62%

63%

32%

67%

27%

100%

8%

82%

7%

20%

16%

21%

43%

10%

33%

12%

23%

8%

14%

11%

8%

6th Gen+ 5th Gen Sub-5th Gen JU

Includes committed newbuilds.

9

Pacific Drilling

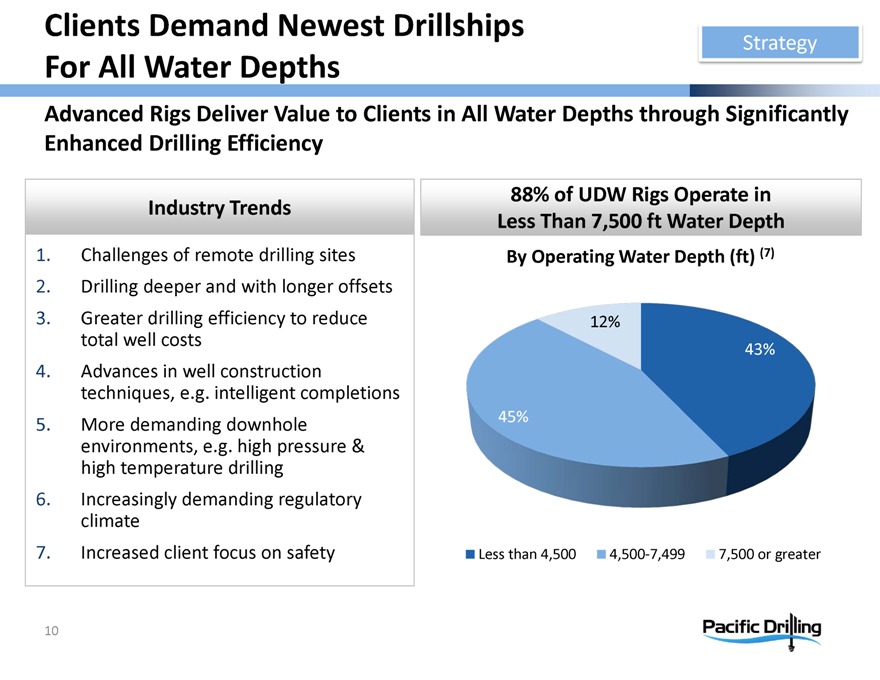

Clients Demand Newest Drillships For All Water Depths

Strategy

Advanced Rigs Deliver Value to Clients in All Water Depths through Significantly Enhanced Drilling Efficiency

Industry Trends

1. Challenges of remote drilling sites

2. Drilling deeper and with longer offsets

3. Greater drilling efficiency to reduce total well costs

4. Advances in well construction techniques, e.g. intelligent completions

5. More demanding downhole environments, e.g. high pressure & high temperature drilling

6. Increasingly demanding regulatory climate

7. Increased client focus on safety

88% of UDW Rigs Operate in Less Than 7,500 ft Water Depth

By Operating Water Depth (ft) (7)

12% 43% 45%

Less than 4,500 4,500-7,499 7,500 or greater

10

Pacific Drilling

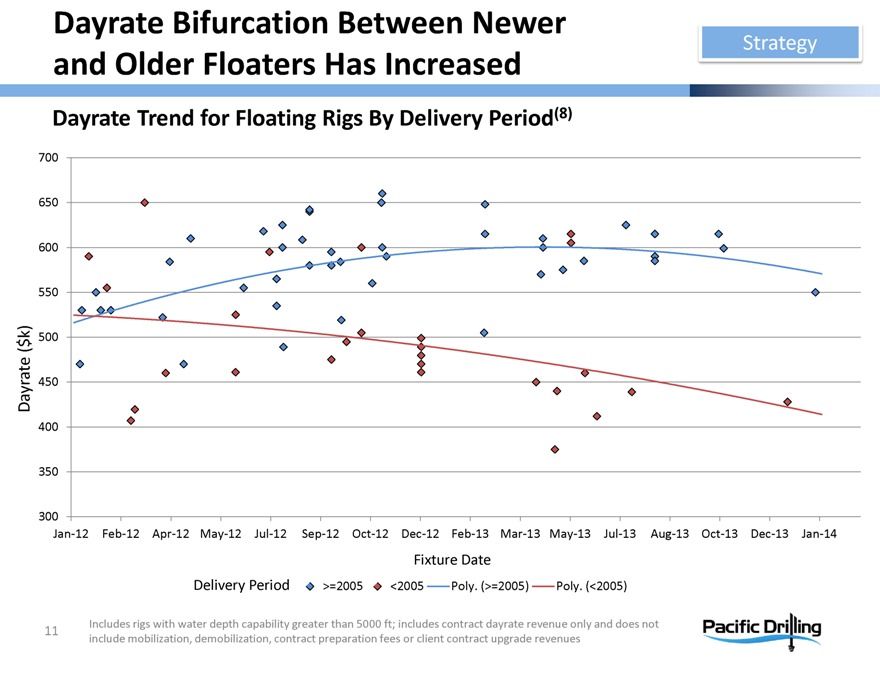

Dayrate Bifurcation Between Newer and Older Floaters Has Increased

Strategy

Dayrate Trend for Floating Rigs By Delivery Period(8)

Dayrate ($k)

700 650 600 550 500 450 400 350 300

Jan-12 Feb-12 Apr-12 May-12 Jul-12 Sep-12 Oct-12 Dec-12 Feb-13 Mar-13 May-13 Jul-13 Aug-13 Oct-13 Dec-13 Jan-14

Fixture Date

Delivery Period >=2005 <2005 Poly. (>=2005) Poly. (<2005)

Includes rigs with water depth capability greater than 5000 ft; includes contract dayrate revenue only and does not include mobilization, demobilization, contract preparation fees or client contract upgrade revenues

11

Pacific Drilling

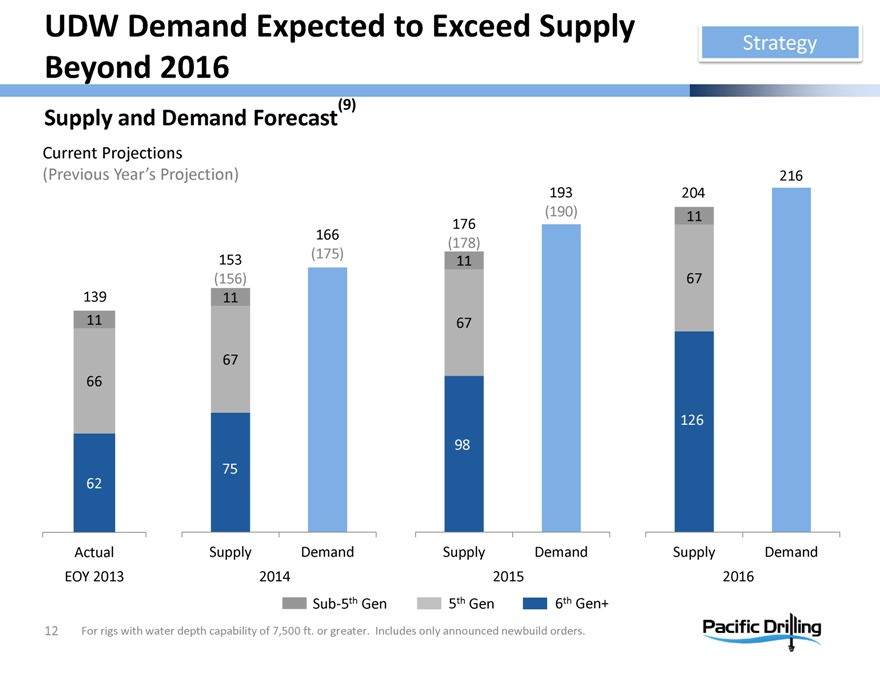

UDW Demand Expected to Exceed Supply Beyond 2016

Strategy

Supply and Demand Forecast(9)

Current Projections

(Previous Year’s Projection)

139 11 66 62

153 (156) 11 67 75

166 (175)

176 (178) 11 67 98

193 (190)

204 11 67 126

216

Actual Supply Demand Supply Demand Supply Demand

EOY 2013 2014 2015 2016

Sub-5th Gen

5th Gen

6th Gen+

For rigs with water depth capability of 7,500 ft. or greater. Includes only announced newbuild orders.

12

Pacific Drilling

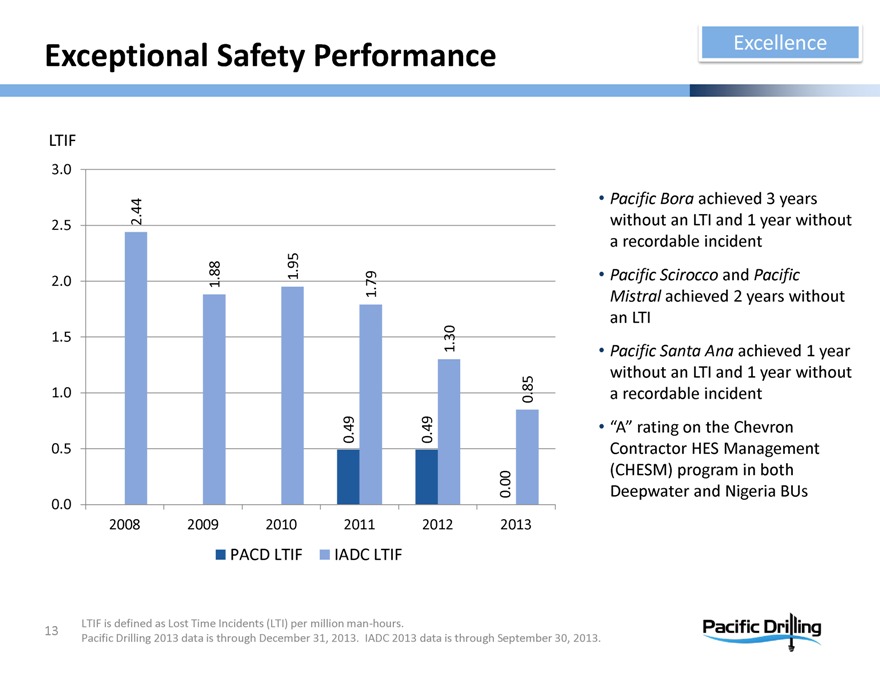

Exceptional Safety Performance

Excellence

LTIF 3.0 2.5 2.0 1.5 1.0 0.5 0.0

2.44 1.88 1.95 0.49 1.79 0.49 1.30 0.00 0.85

2008 2009 2010 2011 2012 2013

PACD LTIF IADC LTIF

Pacific Bora achieved 3 years without an LTI and 1 year without a recordable incident

Pacific Scirocco and Pacific Mistral achieved 2 years without an LTI

Pacific Santa Ana achieved 1 year without an LTI and 1 year without a recordable incident

“A” rating on the Chevron Contractor HES Management (CHESM) program in both Deepwater and Nigeria BUs

LTIF is defined as Lost Time Incidents (LTI) per million man-hours.

Pacific Drilling 2013 data is through December 31, 2013. IADC 2013 data is through September 30, 2013.

13

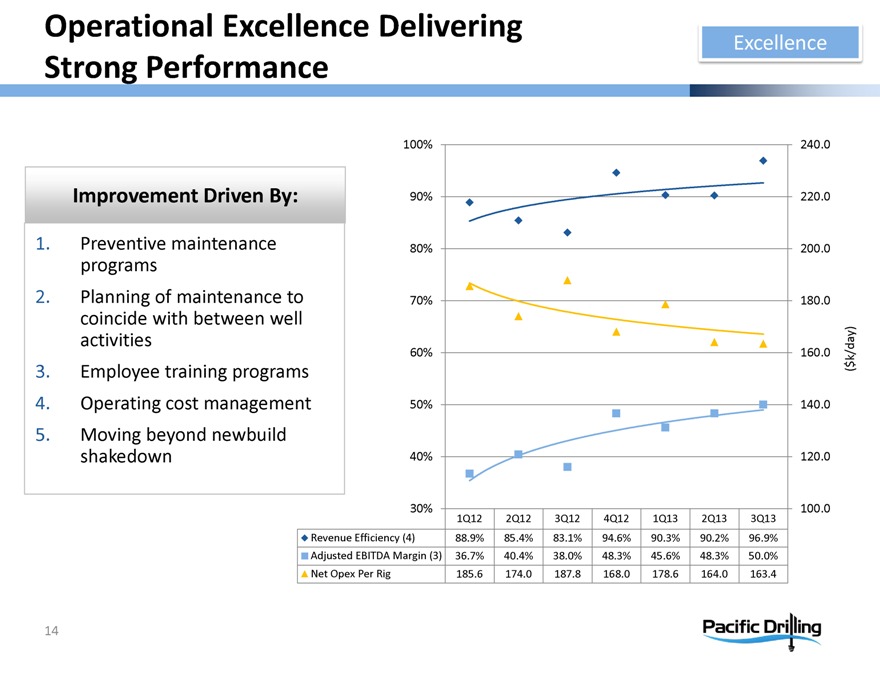

Pacific Drilling

Operational Excellence Delivering

Strong Performance

Excellence

Improvement Driven By:

1. Preventive maintenance programs

2. Planning of maintenance to coincide with between well activities

3. Employee training programs

4. Operating cost management

5. Moving beyond newbuild shakedown

100% 90% 80% 70% 60% 50% 40% 30%

240.0 220.0 200.0 180.0 160.0 ($k/day) 140.0 120.0 100.0

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13

Revenue Efficiency (4)

88.9% 85.4% 83.1% 94.6% 90.3% 90.2% 96.9%

Adjusted EBITDA Margin (3)

36.7% 40.4% 38.0% 48.3% 45.6% 48.3% 50.0%

Net Opex Per Rig

185.6 174.0 187.8 168.0 178.6 164.0 163.4

14

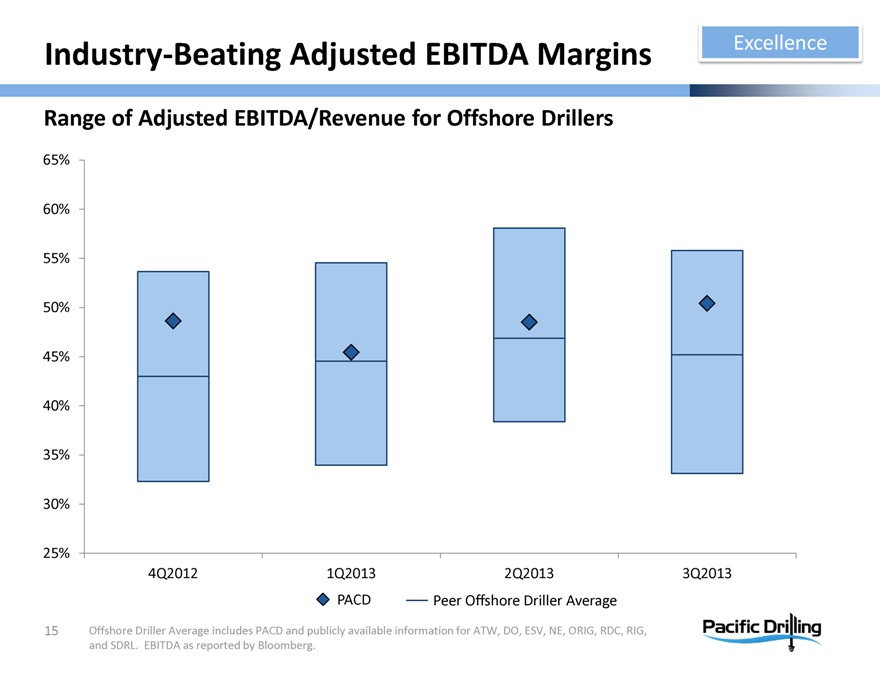

Pacific Drilling

Industry-Beating Adjusted EBITDA Margins

Excellence

Range of Adjusted EBITDA/Revenue for Offshore Drillers

65% 60% 55% 50% 45% 40% 35% 30% 25%

4Q2012 1Q2013 2Q2013 3Q2013

PACD Peer Offshore Driller Average

Offshore Driller Average includes PACD and publicly available information for ATW, DO, ESV, NE, ORIG, RDC, RIG, and SDRL. EBITDA as reported by Bloomberg.

15

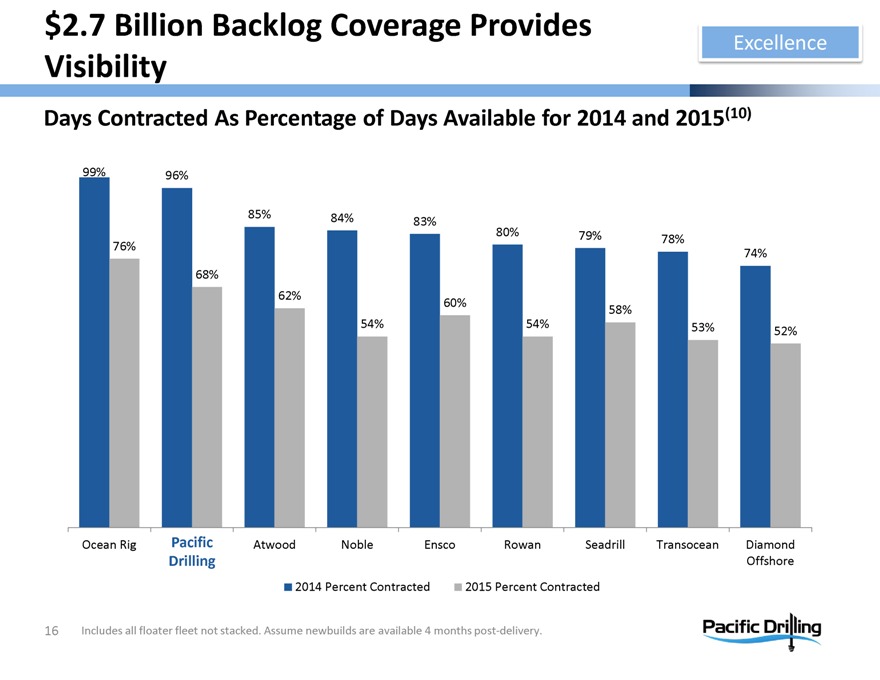

Pacific Drilling

$2.7 Billion Backlog Coverage Provides Visibility

Excellence

Days Contracted As Percentage of Days Available for 2014 and 2015(10)

99% 76%

96% 68%

85% 62%

84% 54%

83% 60%

80% 54%

79% 58%

78% 53%

74% 52%

Ocean Rig

Pacific Drilling

Atwood

Noble

Ensco

Rowan

Seadrill

Transocean

Diamond Offshore

2014 Percent Contracted 2015 Percent Contracted

Includes all floater fleet not stacked. Assume newbuilds are available 4 months post-delivery.

16

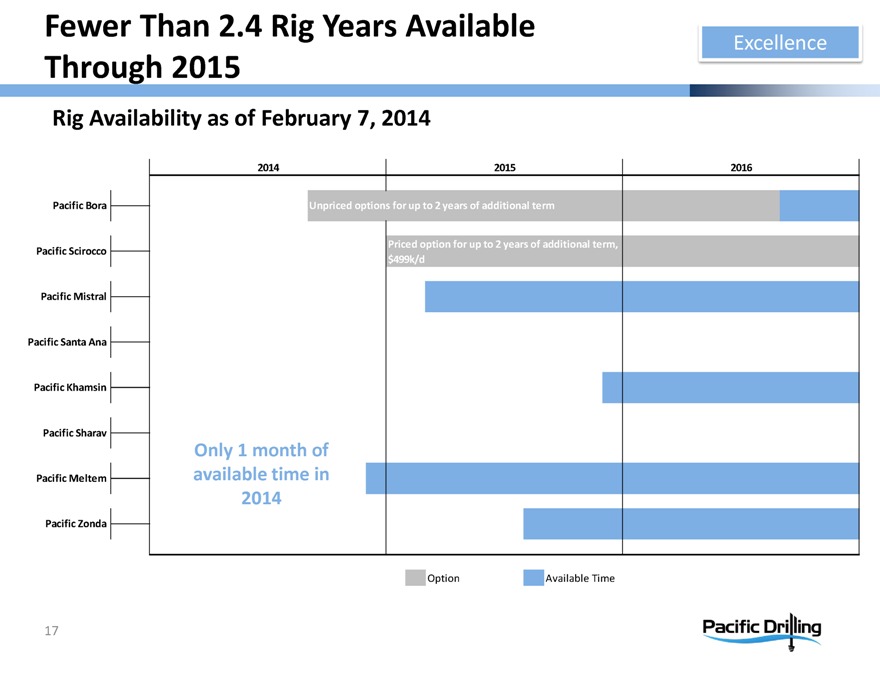

Pacific Drilling

Fewer Than 2.4 Rig Years Available Through 2015

Excellence

Rig Availability as of February 7, 2014

2014 2015 2016

Pacific Bora

Pacific Scirocco

Pacific Mistral

Pacific Santa Ana

Pacific Khamsin

Pacific Sharav

Pacific Meltem

Pacific Zonda

Unpriced options for up to 2 years of additional term

Priced option for up to 2 years of additional term, $499k/d

Only 1 month of available time in 2014

Option Available Time

17

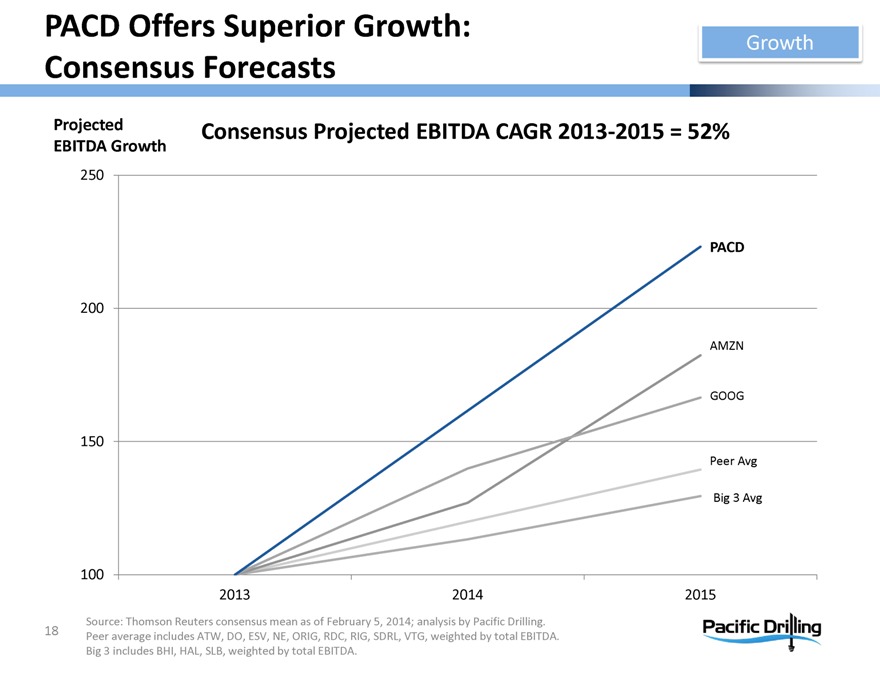

Pacific Drilling

PACD Offers Superior Growth: Consensus Forecasts

Growth

Projected EBITDA Growth

Consensus Projected EBITDA CAGR 2013-2015 = 52%

250 200 150 100

PACD AMZN GOOG Peer Avg Big 3 Avg

2013 2014 2015

Source: Thomson Reuters consensus mean as of February 5, 2014; analysis by Pacific Drilling. Peer average includes ATW, DO, ESV, NE, ORIG, RDC, RIG, SDRL, VTG, weighted by total EBITDA. Big 3 includes BHI, HAL, SLB, weighted by total EBITDA.

18

Pacific Drilling

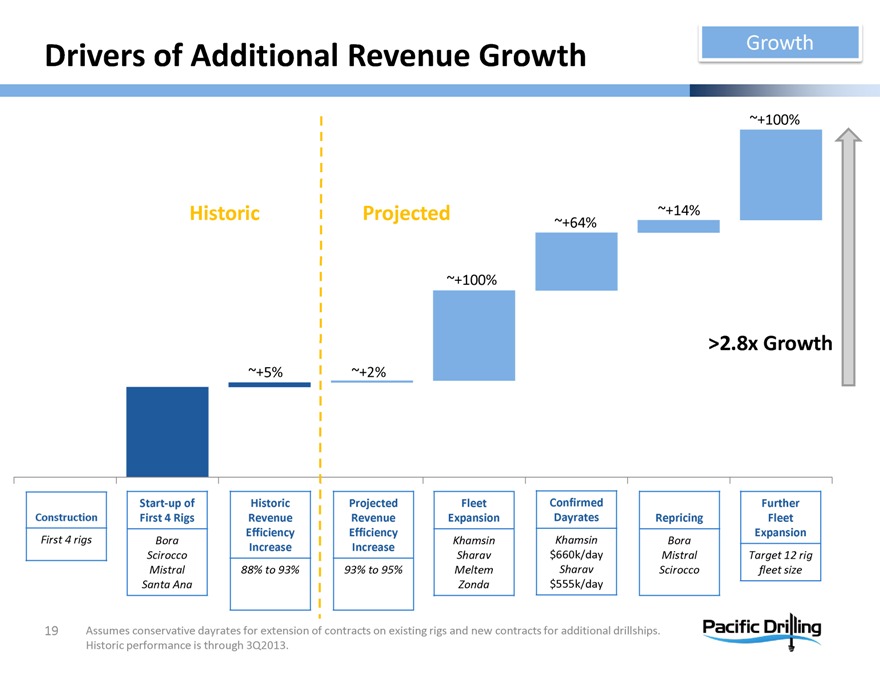

Drivers of Additional Revenue Growth

Growth

Historic Projected

~+5% ~+2% ~+100% ~+64% ~+14% ~+100% >2.8x Growth

Construction First 4 rigs

Start-up of First 4 Rigs Bora Scirocco Mistral Santa Ana

Historic Revenue Efficiency Increase 88% to 93%

Projected Revenue Efficiency Increase 93% to 95%

Fleet Expansion Khamsin Sharav Meltem Zonda

Confirmed Dayrates Khamsin $660k/day Sharav $555k/day

Repricing Bora Mistral Scirocco

Further Fleet Expansion Target 12 rig fleet size

Assumes conservative dayrates for extension of contracts on existing rigs and new contracts for additional drillships. Historic performance is through 3Q2013.

19

Pacific Drilling

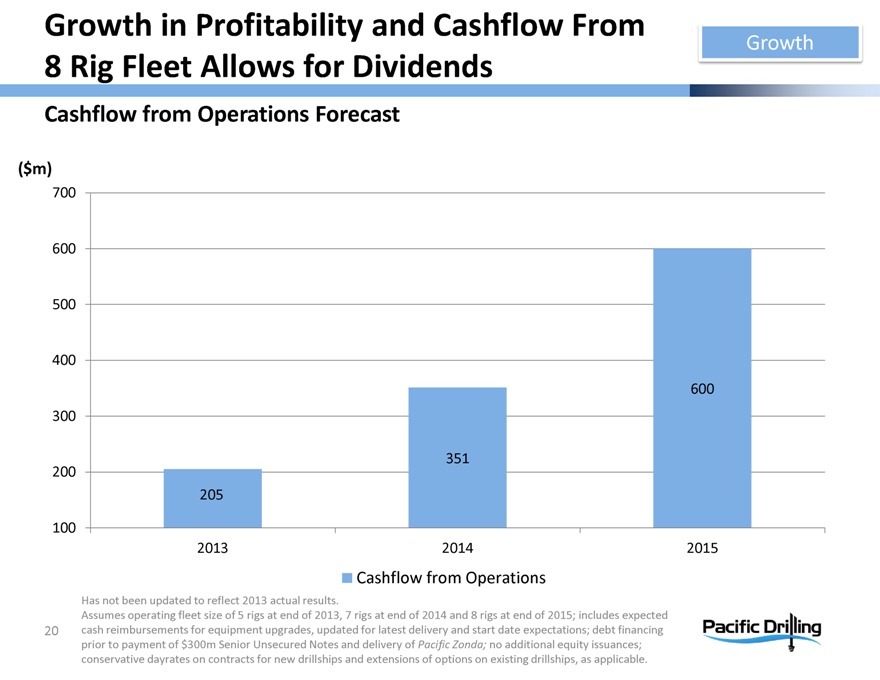

Growth in Profitability and Cashflow From

8 Rig Fleet Allows for Dividends

Growth

Cashflow from Operations Forecast

($m)

700 600 500 400 300 200 100

205 351 600

2013 2014 2015

Cashflow from Operations

Has not been updated to reflect 2013 actual results.

Assumes operating fleet size of 5 rigs at end of 2013, 7 rigs at end of 2014 and 8 rigs at end of 2015; includes expected cash reimbursements for equipment upgrades, updated for latest delivery and start date expectations; debt financing prior to payment of $300m Senior Unsecured Notes and delivery of Pacific Zonda; no additional equity issuances; conservative dayrates on contracts for new drillships and extensions of options on existing drillships, as applicable.

20

Pacific Drilling

Our Current Priorities and Potential Catalysts

Drilling contracts

Pacific Bora option exercise

Pacific Mistral extension

Pacific Scirocco option exercise

Pacific Meltem maiden contract

Continued excellence in operations

Dividend initiation

21

Pacific Drilling

Investor Contact

Pacific Drilling

Amy Roddy

VP Investor Relations

3050 Post Oak Blvd #1500 Houston, Texas USA

Phone: +1 832-255-0502

Email: Investor@pacificdrilling.com

www.pacificdrilling.com

22

Pacific Drilling

Footnotes

1. Closing stock price of $9.74 as of February 5, 2014 and 217m shares outstanding.

2. EBITDA and adjusted EBITDA are non-GAAP measures. Please refer to the reconciliation, included later in this press release, of net income to EBITDA and adjusted EBITDA along with the statement indicating why management believes the non-GAAP measure provides useful information for investors.

3. EBITDA margin is defined as EBITDA divided by contract drilling revenue. Adjusted EBITDA margin is defined as adjusted EBITDA divided by contract drilling revenue. Management uses this operational metric to track company results and believes that this measure provides additional information that consolidates the impact of our operating efficiency as well as the operating and support costs incurred in achieving the revenue performance.

4. Revenue efficiency is defined as actual contractual dayrate revenue (excludes mobilization fees, upgrade reimbursements and other revenue sources) divided by the maximum amount of contractual dayrate revenue that could have been earned during such period.

5. Utilization data from IHS-Petrodata through December 31, 2013. “2007-Current” adjusted to remove impact of Ocean Courage and Petrobras 10,000 in 2009, which were subject to construction finance issues and unable to work.

6. Rig data from IHS-Petrodata as of January 30, 2014. Enterprise value and EBITDA data from Thomson Reuters as of January 30, 2014. Rig generation analysis by Pacific Drilling. Rig generation analysis includes weighted average of characteristics which are important to industry clients, including DP class, derrick capacity, top drive capacity, size of main rotary table, number and size of mud pumps, liquid mud capacity, oil capacity, brine capacity, automation capabilities, riser tensioner capacity, size of quarters, variable deck load, number of cranes and BOP capacity.

7. Data from IHS-Petrodata as of February 5, 2014. Analysis by Pacific Drilling using most recent well depth data available for each rig.

8. Data from IHS-Petrodata as of January 31, 2014. Analysis by Pacific Drilling. Priced option exercises, sublets and contracts for less than 1 year in duration not included.

9. Supply data from IHS-Petrodata as of December 2013. Newbuild supply weighted by portion of the year during which it is eligible to work. Demand analysis by Pacific Drilling as of December 2013. Demand projections should be regarded as our general estimate of forecasted market conditions.

Our projections are derived from internal analysis and include uncertainty. Our internal analysis incorporates factors including, but not limited to, known tenders existing in the marketplace, potential future tenders as projected by IHS-Petrodata, perceptions of operator intent derived through marketing discussions, news articles regarding political conditions and potential regulatory developments in deepwater-active countries, and presentations by peers, deepwater operators, and analysts. We label the most likely outcome as the ‘base case.’ The numbers presented on this slide correspond to our ‘base case’.

10. Data from IHS-Petrodata as of January 28, 2014. Analysis by Pacific Drilling.

23

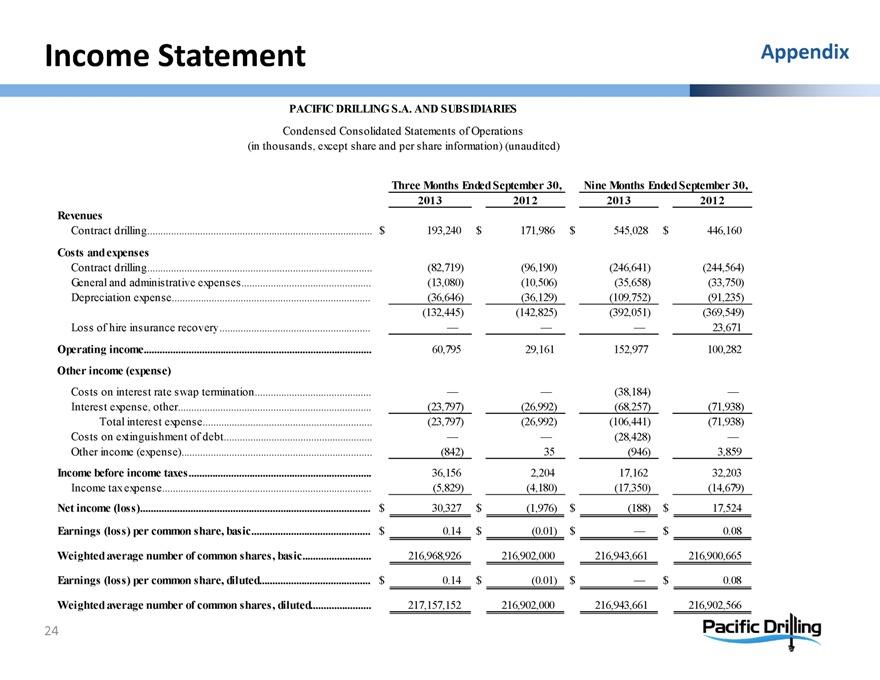

Pacific Drilling

Income Statement

Appendix

PACIFIC DRILLING S.A. AND SUBSIDIARIES

Condensed Consolidated Statements of Operations (in thousands, except share and per share information) (unaudited)

Three Months Ended September 30,

Nine Months Ended September 30,

2013 2012 2013 2012

Revenues

Contract drilling

Costs and expenses

Contract drilling

General and administrative expenses

Depreciation expense

Loss of hire insurance recovery

Operating income

Other income (expense)

Costs on interest rate swap termination

Interest expense, other

Total interest expense

Costs on extinguishment of debt

Other income (expense)

Income before income taxes

Income tax expense

Net income (loss)

Earnings (loss) per common share, basic

Weighted average number of common shares, basic

Earnings (loss) per common share, diluted

Weighted average number of common shares, diluted

$193,240 (82,719) (13,080) (36,646) (132,445) — 60,795 — (23,797) (23,797) — (842) 36,156 (5,829) $30,327 $0.14 216,968,926 $0.14 217,157,152

$171,986 (96,190) (10,506) (36,129) (142,825) — 29,161 — (26,992) (26,992) — 35 2,204 (4,180) $(1,976) $(0.01) 216,902,000 $(0.01) 216,902,000

$545,028 (246,641) (35,658) (109,752) (392,051) — 152,977 (38,184) (68,257) (106,441) (28,428) (946) 17,162 (17,350) $(188) $— 216,943,661 $— 216,943,661

$446,160 (244,564) (33,750) (91,235) (369,549) 23,671 100,282 — (71,938) (71,938) — 3,859 32,203 (14,679) $17,524 $0.08 216,900,665 $0.08 216,902,566

24

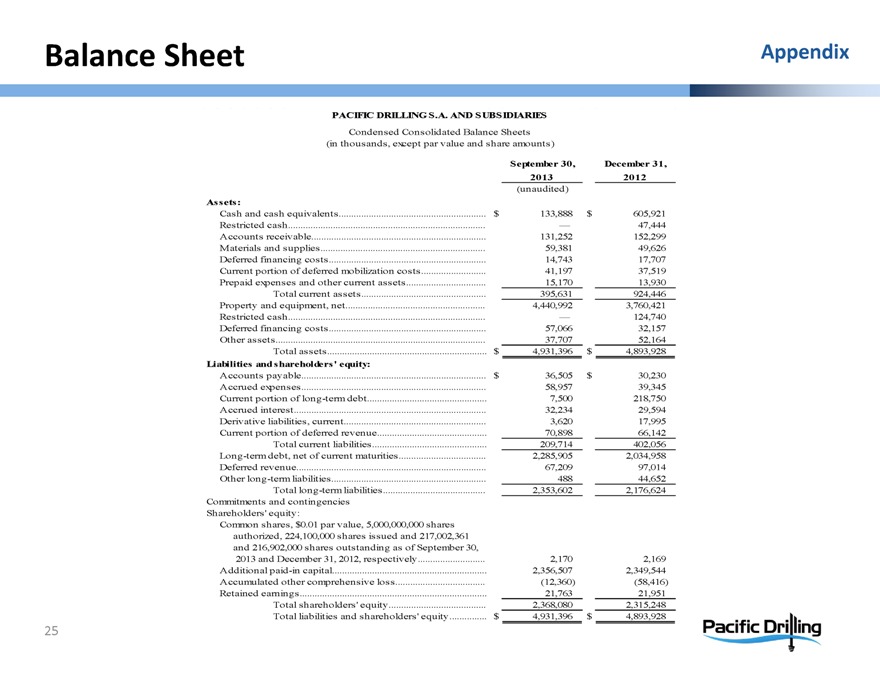

Pacific Drilling

Balance Sheet

Appendix

PACIFIC DRILLING S.A. AND SUBSIDIARIES

Condensed Consolidated Balance Sheets (in thousands, except par value and share amounts)

September 30, 2013

December 31, 2012 (unaudited)

Assets:

Cash and cash equivalents

Restricted cash

Accounts receivable

Materials and supplies

Deferred financing costs

Current portion of deferred mobilization costs

Prepaid expenses and other current assets

Total current assets

Property and equipment, net

Restricted cash

Deferred financing costs

Other assets

Total assets

Liabilities and shareholders’ equity:

Accounts payable

Accrued expenses

Current portion of long-term debt

Accrued interest

Derivative liabilities, current

Current portion of deferred revenue

Total current liabilities

Long-term debt, net of current maturities

Deferred revenue

Other long-term liabilities

Total long-term liabilities

Commitments and contingencies

Shareholders’ equity:

Common shares, $0.01 par value, 5,000,000,000 shares authorized, 224,100,000 shares issued and 217,002,361 and 216,902,000 shares outstanding as of September 30, 2013 and December 31, 2012, respectively

Additional paid-in capital

Accumulated other comprehensive loss

Retained earnings

Total shareholders’ equity

Total liabilities and shareholders’ equity

$133,888 — 131,252 59,381 14,743 41,197 15,170 395,631 4,440,992 — 57,066 37,707 $4,931,396 $36,505 58,957 7,500 32,234 3,620 70,898 209,714 2,285,905 67,209 488 2,353,602 2,170 2,356,507 (12,360) 21,763 2,368,080 $4,931,396

$605,921 47,444 152,299 49,626 17,707 37,519 13,930 924,446 3,760,421 124,740 32,157 52,164 $4,893,928 $30,230 39,345 218,750 29,594 17,995 66,142 402,056 2,034,958 97,014 44,652 2,176,624 2,169 2,349,544 (58,416) 21,951 2,315,248 $4,893,928

25

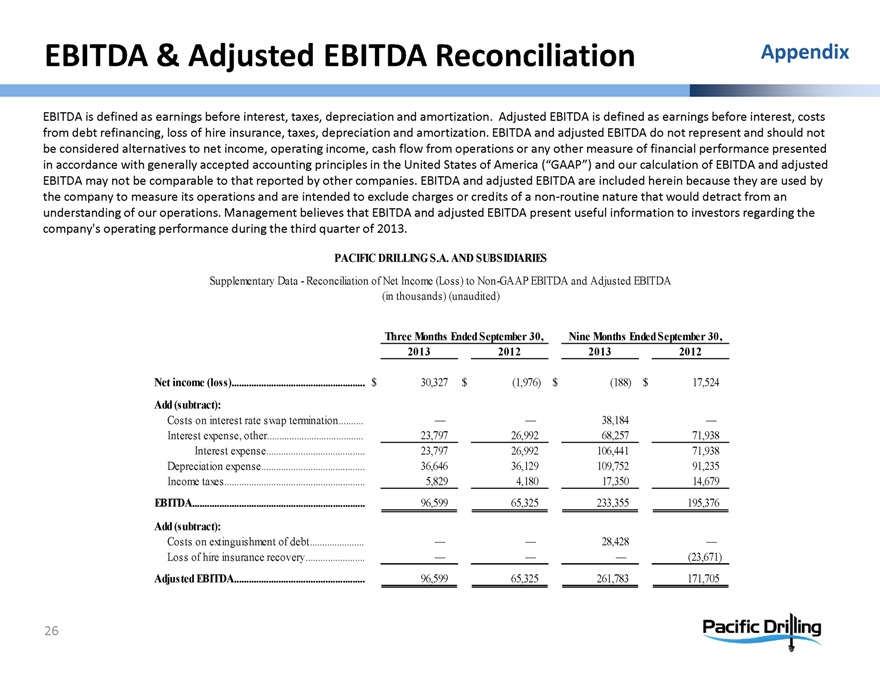

Pacific Drilling

EBITDA & Adjusted EBITDA Reconciliation

Appendix

EBITDA is defined as earnings before interest, taxes, depreciation and amortization. Adjusted EBITDA is defined as earnings before interest, costs from debt refinancing, loss of hire insurance, taxes, depreciation and amortization. EBITDA and adjusted EBITDA do not represent and should not be considered alternatives to net income, operating income, cash flow from operations or any other measure of financial performance presented in accordance with generally accepted accounting principles in the United States of America (“GAAP”) and our calculation of EBITDA and adjusted EBITDA may not be comparable to that reported by other companies. EBITDA and adjusted EBITDA are included herein because they are used by the company to measure its operations and are intended to exclude charges or credits of a non-routine nature that would detract from an understanding of our operations. Management believes that EBITDA and adjusted EBITDA present useful information to investors regarding the company’s operating performance during the third quarter of 2013.

PACIFIC DRILLING S.A. AND SUBSIDIARIES

Supplementary Data - Reconciliation of Net Income (Loss) to Non-GAAP EBITDA and Adjusted EBITDA (in thousands) (unaudited)

Three Months Ended September 30,

Nine Months Ended September 30,

2013 2012 2013 2012

Net income (loss)

Add (subtract):

Costs on interest rate swap termination

Interest expense, other

Interest expense

Depreciation expense

Income taxes

EBITDA

Add (subtract):

Costs on extinguishment of debt

Loss of hire insurance recovery

Adjusted EBITDA

$30,327 — 23,797 23,797 36,646 5,829 96,599 — — 96,599

$(1,976) — 26,992 26,992 36,129 4,180 65,325 — — 65,325

$(188) 38,184 68,257 106,441 109,752 17,350 233,355 28,428 — 261,783

$17,524 — 71,938 71,938 91,235 14,679 195,376 — (23,671) 171,705

26

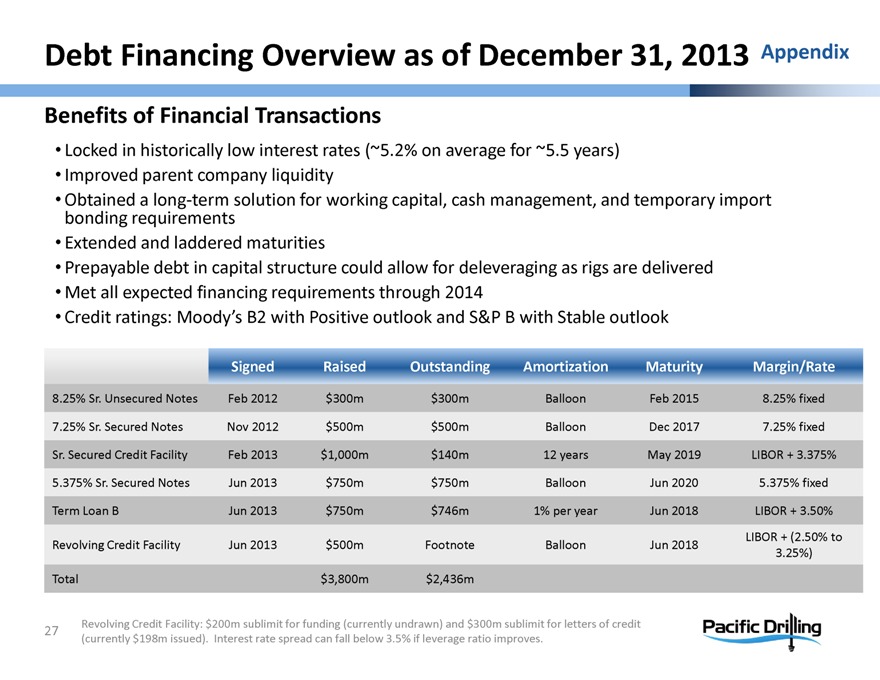

Pacific Drilling

Debt Financing Overview as of December 31, 2013

Appendix

Benefits of Financial Transactions

Locked in historically low interest rates (~5.2% on average for ~5.5 years)

Improved parent company liquidity

Obtained bonding requirements a long-term solution for working capital, cash management, and temporary import

Extended and laddered maturities

Prepayable debt in capital structure could allow for deleveraging as rigs are delivered

Met all expected financing requirements through 2014

Credit ratings: Moody’s B2 with Positive outlook and S&P B with Stable outlook

Signed Raised Outstanding Amortization Maturity Margin/Rate

8.25% Sr. Unsecured Notes Feb 2012 $300m $300m Balloon Feb 2015 8.25% fixed

7.25% Sr. Secured Notes Nov 2012 $500m $500m Balloon Dec 2017 7.25% fixed

Sr. Secured Credit Facility Feb 2013 $1,000m $140m 12 years May 2019 LIBOR + 3.375%

5.375% Sr. Secured Notes Jun 2013 $750m $750m Balloon Jun 2020 5.375% fixed

Term Loan B Jun 2013 $750m $746m 1% per year Jun 2018 LIBOR + 3.50%

Revolving Credit Facility Jun 2013 $500m Footnote Balloon Jun 2018 LIBOR + (2.50% to 3.25%)

Total $3,800m $2,436m

Revolving Credit Facility: $200m sublimit for funding (currently undrawn) and $300m sublimit for letters of credit (currently $198m issued). Interest rate spread can fall below 3.5% if leverage ratio improves.

27

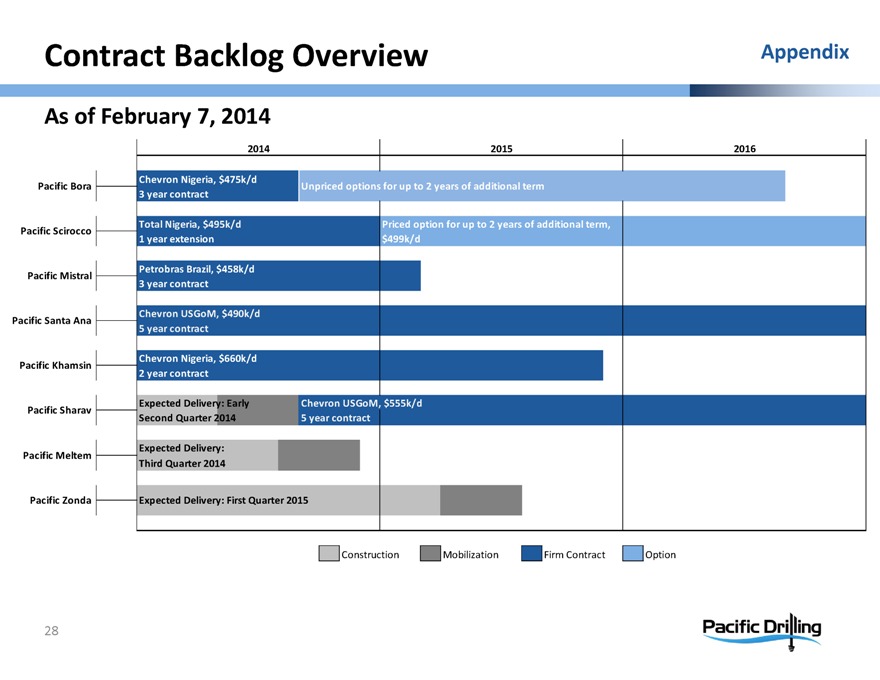

Pacific Drilling

Contract Backlog Overview

Appendix

As of February 7, 2014

2014 2015 2016

Pacific Bora Chevron Nigeria, $475k/d 3 year contract Unpriced options for up to 2 years of additional term

Pacific Scirocco

Total Nigeria, $495k/d 1 year extension

Priced option for up to 2 years of additional term, $499k/d

Pacific Mistral

Petrobras Brazil, $458k/d

3 year contract

Pacific Santa Ana

Chevron USGoM, $490k/d

5 year contract

Pacific Khamsin

Chevron Nigeria, $660k/d

2 year contract

Pacific Sharav

Expected Delivery: Early

Chevron USGoM, $555k/d

Second Quarter 2014

5 year contract

Pacific Meltem

Expected Delivery:

Third Quarter 2014

Pacific Zonda

Expected Delivery: First Quarter 2015

Construction Mobilization Firm Contract Option

28

Pacific Drilling