UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

(RULE 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of

the Securities Exchange Act of 1934 (Amendment No. )

Filed by the Registrant ☒

Filed by a Party other than the Registrant ☐

Check the appropriate box:

| ☐ | Preliminary Proxy Statement | |

| ☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

| ☒ | Definitive Proxy Statement | |

| ☐ | Definitive Additional Materials | |

| ☐ | Soliciting Material Pursuant to §240.14a-12 | |

Carlyle Credit Income Fund

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| ☒ | No fee required. | |||

| ☐ | Fee computed on table below per Exchange Act Rules 14a-6(i)(l) and 0-11. | |||

| (1) | Title of each class of securities to which transaction applies:

| |||

| (2) | Aggregate number of securities to which transaction applies:

| |||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined):

| |||

| (4) | Proposed maximum aggregate value of transaction:

| |||

| (5) | Total fee paid:

| |||

| ☐ | Fee paid previously with preliminary materials. | |||

| ☐ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11 (a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |||

| (1) | Amount Previously Paid:

| |||

| (2) | Form, Schedule or Registration Statement No.:

| |||

| (3) | Filing party:

| |||

| (4) | Date Filed:

| |||

CARLYLE CREDIT INCOME FUND

(the “Fund”)

One Vanderbilt Avenue, Suite 3400

New York, New York 10017

NOTICE OF ANNUAL MEETING OF SHAREHOLDERS

July 19, 2024

To the Shareholders of the Fund:

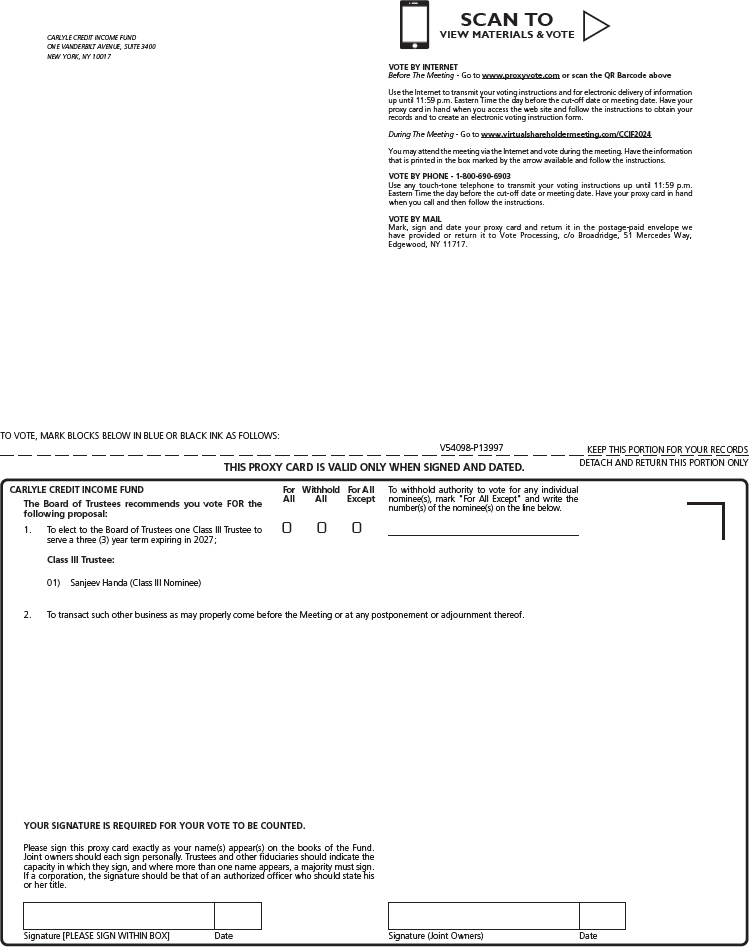

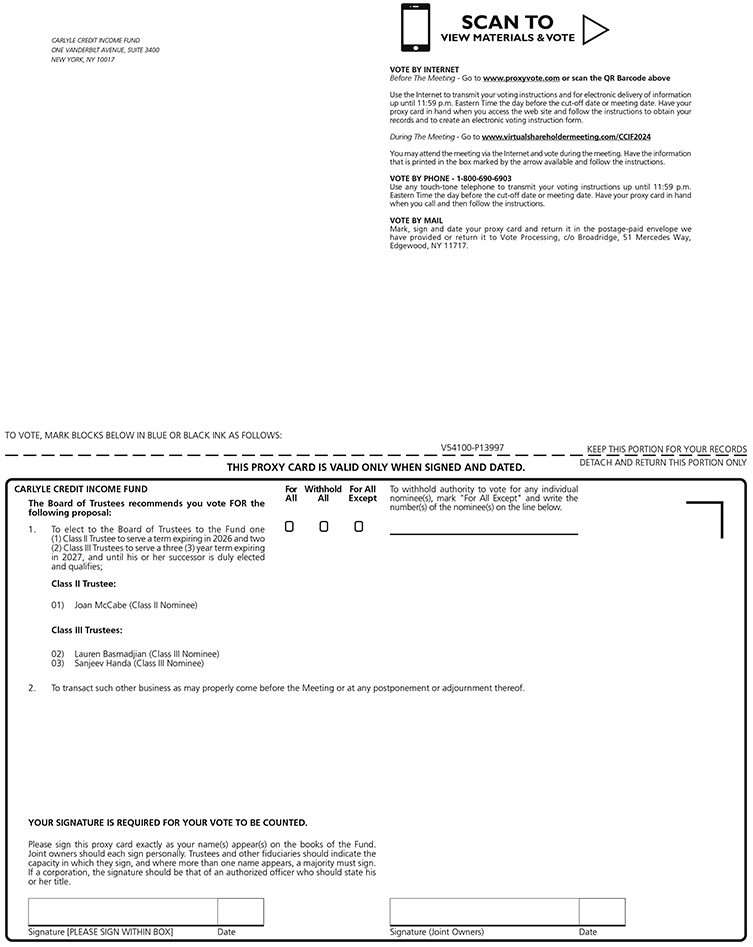

Notice is hereby given that an Annual Meeting of Shareholders (the “Meeting”) of the Fund will be held virtually at www.proxyvote.com on September 5, 2024 at 10:00 a.m. (Eastern Time), for the following purposes:

| 1) | to elect to the Board of Trustees to the Fund one (1) Class II Trustee to serve a term expiring in 2026 and two (2) Class III Trustees to serve a three (3) year term expiring in 2027, and until his or her successor is duly elected and qualifies; and |

| 2) | to transact such other business as may properly come before the Meeting or any postponements or adjournments thereof. |

Participating in the Meeting are holders of common shares of beneficial interest (“Common Shares”), and the holders of mandatory redeemable preferred shares of beneficial interest (“Preferred Shares”).

The proposal to elect the Trustees is discussed in greater detail in the attached Proxy Statement.

The close of business on July 9, 2024 has been fixed as the record date for the determination of shareholders entitled to notice of and to vote at the Meeting and any postponements or adjournments thereof.

YOUR VOTE IS IMPORTANT REGARDLESS OF THE SIZE OF YOUR HOLDINGS IN THE FUND. WHETHER OR NOT YOU PLAN TO ATTEND THE MEETING, WE ASK THAT YOU PLEASE COMPLETE AND SIGN THE ENCLOSED PROXY CARD AND RETURN IT PROMPTLY IN THE ENCLOSED ENVELOPE, WHICH NEEDS NO POSTAGE IF MAILED IN THE UNITED STATES.

By Order of the Board of Trustees of: | ||

| Carlyle Credit Income Fund | ||

| /s/ Jennifer Juste | ||

| Jennifer Juste | ||

| Chief Compliance Officer | ||

CARLYLE CREDIT INCOME FUND

(the “Fund”)

One Vanderbilt Avenue, Suite 3400

New York, New York 10017

ANNUAL MEETING OF SHAREHOLDERS

To Be Held September 5, 2024

PROXY STATEMENT

INTRODUCTION

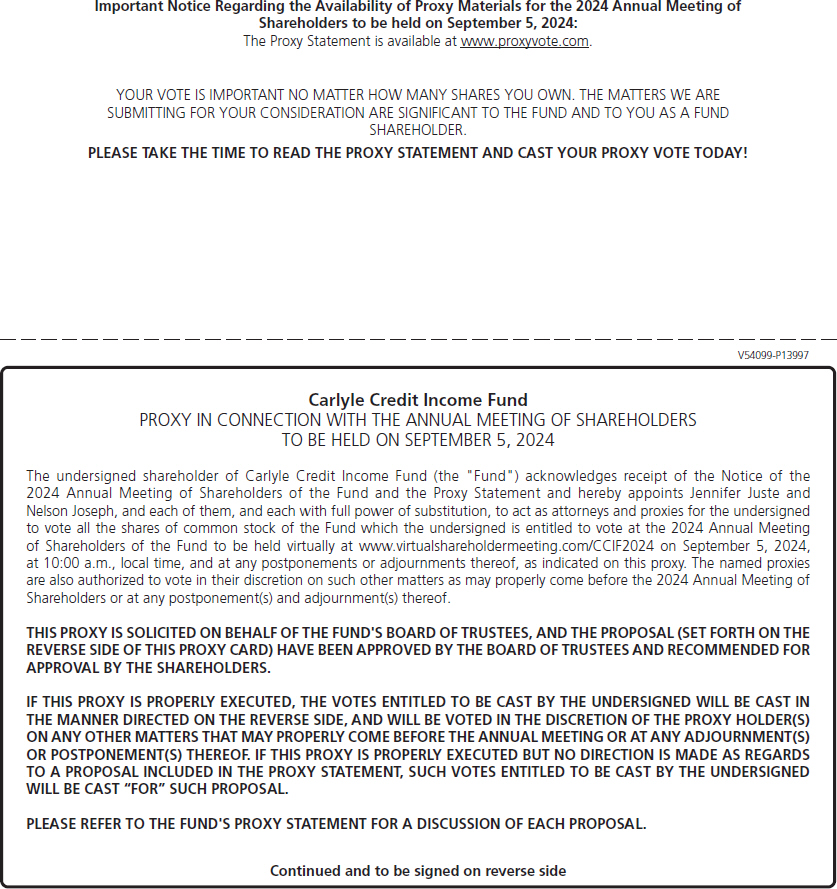

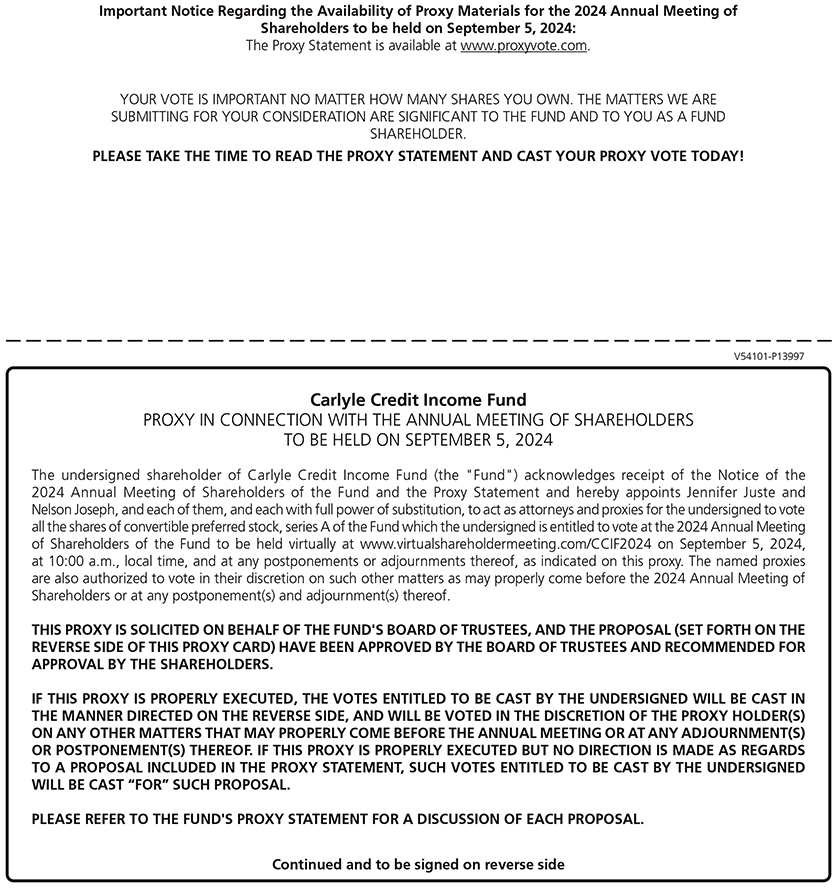

This Proxy Statement is furnished in connection with the solicitation of proxies by the Board of Trustees (the “Board”) of the Fund for use at the Annual Meeting of Shareholders of the Fund (the “Meeting”) to be held virtually at www.proxyvote.com on September 5, 2024, at 10:00 a.m. (Eastern Time), and at any postponements or adjournments thereof. Shareholders of the Fund will meet and vote at the Meeting as to the proposal described herein. The Notice of the Meeting and the Proxy Statement with the accompanying proxy card will be mailed to shareholders on or about July 19, 2024.

Important Notice Regarding the Availability of Proxy Materials for the Meeting To Be Held on September 5, 2024

This Proxy Statement is available online free of charge at www.proxyvote.com.

Other Methods of Proxy Solicitation

In addition to the solicitation of proxies by Internet or mail, regular employees of Carlyle Global Credit Investment Management (the “Adviser”) and officers and employees of Equiniti Trust Company LLC, the Fund’s transfer agent may also solicit proxies by telephone, Internet or in person and will not receive any compensation therefor from the Fund. The Fund has also engaged Broadridge Financial Solutions, Inc. (“Broadridge”), an independent proxy solicitation firm, to assist in the distribution of the proxy materials and the solicitation and tabulation of proxies. The cost of Broadridge’s services with respect to the Fund is estimated to be approximately $39,061, plus reasonable out-of-pocket expenses. The Fund will pay all expenses incurred in connection with preparing the Proxy Statement and its enclosures and expenses associated with proxy solicitation. The Fund will also reimburse brokerage firms and others for their expenses in forwarding solicitation materials to the beneficial owners of the Fund’s Shares (as defined below).

The Fund’s most recent annual and semi-annual report, including audited financial statements for the year ended September 30, 2023, is available upon request, without charge, by writing to the Fund at One Vanderbilt Avenue, Suite 3400, New York, New York 10017, by calling the Fund at 1-866-277-8243, or via the Internet at www.carlylecreditincomefund.com.

You can vote your shares by completing and signing the enclosed proxy card(s) and mailing it (them) in the enclosed postage-paid envelope. You may also vote by attending the Meeting and voting. In addition, you may also vote by touch-tone telephone by calling the toll-free number printed on your proxy card(s) and following the recorded instructions or via internet by visiting the website printed on your proxy card(s) and following the on-screen instructions.

Shareholders of record will be entitled to receive notice of, and to participate and to vote at, the Meeting and any postponement or adjournment thereof.

1

You may provide proxy instructions by completing, signing and returning the enclosed proxy card (the “Proxy Card”) by mail in the enclosed envelope. The persons designated on the Proxy Card as proxies will vote your shares as you instruct on each Proxy Card. If you return a signed Proxy Card without any voting instructions, your shares will be voted “FOR” the Trustee nominees in accordance with the recommendation of the Board. The persons designated on the Proxy Card as proxies will also be authorized to vote (or to withhold their votes) in their discretion on any other matters which properly come before the Meeting. They may also vote in their discretion to adjourn the Meeting. If you sign and return a Proxy Card, you may still attend the Meeting to vote your shares in person. If your shares are held of record by a broker and you wish to vote in person at the Meeting, you should obtain a legal proxy from your broker and present it at the Meeting. You may revoke your proxy by (1) giving written notice before the Meeting of the revocation to the Fund stating that the proxy is revoked; (2) executing a subsequent proxy; or (3) attending the Meeting and voting in person. If your shares are held in the name of your broker, you will have to make arrangements with your broker to revoke any previously executed proxy.

If the enclosed proxy card is properly executed and returned in time to be voted at the Meeting and has not been revoked, the Shares (as defined below) represented thereby will be voted “FOR” the proposal listed in the Notice, unless instructions to the contrary are marked thereon, and in the discretion of the proxy holders as to the transaction of any other business that may properly come before the Meeting or any postponements or adjournments thereof. Any shareholder who has given a proxy has the right to revoke it at any time prior to its exercise either by attending the Meeting and voting his or her shares or by submitting a letter of revocation or a later-dated proxy to the Fund at the above address prior to the date of the Meeting.

The holders of one third of the Common Shares entitled to vote on any matter at the Meeting present or by proxy shall constitute a quorum at the Meeting for purposes of conducting business. The holders of one third of the Preferred Shares entitled to vote on any matter at the Meeting present or by proxy shall constitute a quorum at the Meeting for purposes of conducting business. If a quorum is not present at the Meeting, or if a quorum is present at the Meeting, but sufficient votes to approve any of the proposed items are not received, the chair of the Meeting may propose one or more adjournments of the Meeting to permit further solicitation of proxies. A shareholder vote may be taken on one or more of the proposals in this Proxy Statement prior to such adjournment if sufficient votes have been received for approval and it is otherwise appropriate. In the absence of a quorum, the Meeting may be adjourned by either a vote of a majority of the Shares present and entitled to vote at such meeting, or by the chair of such meeting in his or her sole discretion. If a quorum is present, the persons named as proxies will vote those proxies that they are entitled to vote “FOR” any proposal in favor of such adjournment and will vote those proxies required to be voted “AGAINST” any proposal against such adjournment.

The close of business on July 9, 2024, has been fixed as the “Record Date” for the determination of shareholders entitled to notice of and to vote at the Fund’s Meeting and all postponements or adjournments thereof.

The Fund issues common shares of beneficial interest (“Common Shares”) and preferred shares of beneficial interest (“Preferred Shares”), no par value (the “Shares”).

As of the Record Date, there were 13,364,911 of Common Shares outstanding and 2,080,000 of Preferred Shares outstanding. Shareholders of the Fund vote to elect the Class II and Class III Trustees, as indicated below. The following tables set forth the Class II and Class III Trustee nominees by share class:

Share Class | Class II Trustee Nominee | Class III Trustee Nominee | ||

Preferred Shares | Joan McCabe* | Lauren Basmadjian* | ||

Common Shares and Preferred Shares | Sanjeev Handa | |||

| * | Only holders of Preferred Shares may vote for this nominee. |

2

In order that your Shares may be represented at the Meeting, you are requested to vote on the following matter:

PROPOSAL:

ELECTION OF CLASS II AND CLASS III NOMINEES

TO THE FUND’S BOARD OF TRUSTEES

Election of Class II and Class III Nominees (“Nominees”) for the Fund’s Board of Trustees (the “Board”)

The Fund’s Board is currently comprised of five Trustees, three of whom are not “interested persons” of the Fund as that term is defined in the Investment Company Act of 1940, as amended (the “1940 Act”) (the “Independent Trustees”): Lauren Basmadjian, Mark Garbin, Sanjeev Handa, Brian Marcus, and Joan McCabe. At a meeting of the Board held on May 28, 2024, the Board, upon the recommendation of the Board’s Nominating and Governance Committee, determined to submit to a vote of shareholders re-election of Ms. Basmadjian as an interested Trustee of the Fund and re-election of Mr. Handa and Ms. McCabe as Independent Trustees of the Fund. If elected by shareholders at the Meeting, Ms. McCabe will hold office for a two-year term and until her successor is duly elected and qualifies. If elected by shareholders at the Meeting, Ms. Basmadjian and Mr. Handa will hold office for a three-year term and until his or her successor is duly elected and qualifies.

In addition, Section 18 of the 1940 Act, requires that the holders of any preferred shares, voting separately as a single class without regard to series, have the right to elect at least two trustees at all times. In this regard, the holders of Preferred Shares have the exclusive right to separately elect Ms. McCabe as a Class II Trustee and as a Preferred Shares Trustee and Ms. Basmadjian as a Class III Trustee and as a Preferred Shares Trustee, in addition to the right to vote for Mr. Handa, together with the holders of the Common Shares.

Unless authority is withheld, it is the intention of the persons named in the proxy to vote the proxy “FOR” the election of Mses. Basmadjian and McCabe and Mr. Handa, and Mses. Basmadjian and McCabe and Mr. Handa have each indicated his or her consent to serve as a Trustee if approved by shareholders at the Meeting. If Mses. Basmadjian and McCabe or Mr. Handa declines or otherwise becomes unavailable for election, however, the proxy confers discretionary power on the persons named therein to vote in favor of a substitute nominee or nominees.

The Fund’s Board is responsible for the management of the business and affairs of the Fund in accordance with the laws of the State of Delaware. The Board appoints officers who are responsible for the day-to-day operations of the Fund and who execute policies authorized by the Board.

The current Trustees of the Fund know of no reason why Mses. Basmadjian and McCabe or Mr. Handa will be unable to serve.

Information about each Nominee’s and each Trustee’s Experience

Provided below is a brief summary of the specific experience, qualifications, attributes or skills of Mses. Basmadjian and McCabe and Mr. Handa that warrant their consideration as Nominees for the Fund’s Board.

Ms. Basmadjian was selected to join the Board based upon the following: her character and integrity; her over 20 years of experience in financial and corporate markets; her experience in management roles at The Carlyle Group, Inc. and serving on the Investment Committees for all of The Carlyle Group Inc.’s US Loan, CLO and liquid and illiquid credit investing activities; her prior experience at Octagon Credit Investors, LLC and Chase Securities, Inc.; and her willingness to serve and willingness and ability to commit the time necessary to perform the duties of a Trustee.

Mr. Handa was selected to join the Board based upon the following: his character and integrity; his over 30 years of experience in the financial industry sector, including global experience in the financial, real estate

3

and securitization markets; his experience as a board member of White Oak Partners, The Cooper Union for Advancement of Science and Art, where he is also a member of the Investment Committee, Fitch Ratings, Inc., Fitch Ratings, Ltd., and OHA CLO Enhanced Equity II Genpar LLP; and his willingness to serve and willingness and ability to commit the time necessary to perform the duties of a Trustee.

Ms. McCabe was selected to join the Board based upon the following: her character and integrity; her over 30 years of financial and corporate experience, including investing in private equity along with debt financings for those private equity investments; her experience as a board member of Gulfstream Goodwill Inc., Gulfstream Goodwill Academy, Inc. and Elevation Brands; her prior experience at as a board member of Goodwill International, Inc. and Sensible Organics; and her willingness to serve and willingness and ability to commit the time necessary to perform the duties of a Trustee.

No factor, by itself, was controlling. In addition to the information provided in the table included below, Mses. Basmadjian and McCabe and Mr. Handa each possess significant experience as investment professionals. References to the qualifications, attributes and skills of the Nominees are pursuant to requirements of the U.S. Securities and Exchange Commission (“SEC”), do not constitute holding out the Board or any Trustees as having any special expertise or experience, and shall not impose any greater responsibility or liability on any such person or on the Board by reason thereof.

Biographical descriptions of the Board’s Trustees and the Nominees are set forth below.

Nominees

Lauren Basmadjian, an interested Trustee, has over 20 years of experience in financial and corporate markets. She is a Managing Director, Co-Head of Liquid Credit and Head of US Loans & Structured Credit within The Carlyle Group Inc.’s Global Credit platform, overseeing over $48 billion of AUM. She is based in New York and sits on the Investment Committees for all of The Carlyle Group Inc.’s US Loan, CLO and Liquid and Illiquid Credit investing activities. Ms. Basmadjian joined The Carlyle Group Inc. in 2020 after 19 years at Octagon Credit Investors, LLC, where she was a Senior Portfolio Manager, member of the Investment Committee and managed XAI Octagon Floating Rate & Alternative Income Term Trust, a public 1940 Act fund invested in CLO tranches and leveraged loans. Prior to becoming a Portfolio Manager, Ms. Basmadjian managed Octagon’s workout efforts and also oversaw the leisure & entertainment, retail, consumer products, business services, food & beverage and technology industries. Before joining Octagon, Ms. Basmadjian worked in the Acquisition Finance Group at Chase Securities, Inc. She graduated Cum Laude from the Stern School of Business at New York University with a B.S. in Finance and Economics.

Sanjeev Handa, an Independent Trustee, has over 30 years of experience in the financial industry sector, including global experience in the financial, real estate and securitization markets. Mr. Handa is also an advisory board member of White Oak Partners (since 2021), and a member of the Investment Committee of the Board of Trustees of The Cooper Union for Advancement of Science and Art. He also formerly served as an independent director of Fitch Ratings, Inc. and Fitch Ratings, Ltd. (2015-2020). Mr. Handa also serves as an independent director of OHA CLO Enhanced Equity II Genpar LLP (since 2021). Mr. Handa has extensive experience with respect to investments and also to compliance and corporate governance matters as a result of, among other things, his service as a board member to another investment company. He also serves as an audit committee chairperson and audit committee financial expert for another investment company.

Joan McCabe, an Independent Trustee, has over 30 years of financial and corporate experience, including investing in private equity along with debt financings for those private equity investments. Ms. McCabe is also a board member of Gulfstream Goodwill, Inc. (since 2017 and current Board Chair), Gulfstream Goodwill Academy, Inc. (since 2018) and Elevation Brands (since 2017). She formerly served as a board member of Goodwill International, Inc. (2015-2021) and Sensible Organics (2017-2021). Ms. McCabe has served as a board member to a variety of companies, including another investment company, and her diverse experience and financial background, among other things, qualifies her to serve as a Trustee.

4

Other Trustees

Brian Marcus, an Interested Trustee, has over 15 years of experience in highly regulated financial markets. Additionally, he is a Managing Director of Carlyle Global Credit Investment Management L.L.C. He also focuses on strategic growth opportunities for the Global Credit platform of The Carlyle Group Inc. (the ultimate parent company of CGCIM). He also helped develop TCG Capital Markets L.L.C., an SEC-registered broker/dealer affiliate of The Carlyle Group Inc. and has been involved in acquisitions of credit management platforms. Prior to coming to Carlyle, Mr. Marcus was with Morgan Stanley in the Principal Investments area, which used the firm’s capital in a diverse array of investments including private equity, distressed debt, and mezzanine. In this role, Mr. Marcus served as a director on a number of Boards. Previously, Mr. Marcus worked at Lehman Brothers in the mergers and acquisitions group. He received a B.S. in Economics from the Wharton School of the University of Pennsylvania and currently holds Series 7, 55 and 63 licenses. His service as an officer for another investment company contributes to his qualifications to serve as a Trustee of the Fund.

Mark Garbin, an Independent Trustee, has over 30 years of experience in corporate balance sheet and income statement risk management for large asset managers. Mr. Garbin has extensive derivatives experience and has provided consulting services to alternative asset managers. Mr. Garbin holds the CFA and Professional Risk Manager (PRM) Charters and has advanced degrees in international business, negotiation and derivatives. He also has extensive experience with respect to investments and also to compliance and corporate governance matters as a result of, among other things, his service as a board member to other investment companies.

Additional Information about the Trustees/Nominees and the Fund’s Officers

Set forth in the table below are the Nominees, Trustees and officers of the Fund, as well as their age, information relating to their respective positions held with the Fund, a brief statement of their principal occupations during the past five years and other directorships, if any.

Independent Trustees/Nominees of the Fund

| Name, Age and Address(1) | Position(s) Held with the Fund | Term of Office and Length of Time Served | Principal Occupation(s) During Past 5 Years | Number of Registered Investment Companies in Fund Complex Overseen by Trustee/ Nominee(2) | Other Directorships Held by Trustee/Nominee(3) | |||||

| Sanjeev Handa (1961) | Nominee and Trustee | Class III Board member until 2024 annual shareholder meeting–since July 2023 | Managing Member, Old Orchard Lane, LLC (since 2014); Adjunct Professor, Fairfield University (since 2020) | 2 | Advisory Board Member of White Oak Partners (since 2021) and Independent Director of OHA CLO Enhanced Equity II Genpar LLP (since 2021), Independent Trustee, Carlyle Tactical Private Credit Fund (since March 2018); Board of Trustees Investment Committee Member for the Cooper Union for Advancement of Science and Art (since 2016); Board of Directors Member for the Mutual Fund Directors Forum (Since 2022); Independent Director of Fitch Ratings, Inc.(2015-2020). |

5

| Name, Age and Address(1) | Position(s) Held with the Fund | Term of Office and Length of Time Served | Principal Occupation(s) During Past 5 Years | Number of Registered Investment Companies in Fund Complex Overseen by Trustee/ Nominee(2) | Other Directorships Held by Trustee/Nominee(3) | |||||

| Joan McCabe (1955) | Nominee and Trustee | Class II Board member–since July 2023 | Managing Member, JMYME, LLC (since 2020); and CEO/Founder, Lipotriad LLC (2015–2019) | 2 | Board member of Elevation Brands (since 2017 to 11/2022); Sensible Organics (2017–2021); Goodwill International, Inc. (2015–2021); Gulfstream Goodwill, Inc. (since 2017; Board Chair since 2021); Gulfstream Goodwill Academy, Inc. (since 2017), Goodwill International (2015–2021) Independent Trustee Carlyle Tactical Private Credit Fund (since 2018). | |||||

| Other Independent Trustees | ||||||||||

| Mark Garbin (1951) | Trustee | Class I Board member until 2025 annual shareholder meeting–since July 2023 | Managing Principal, Coherent Capital Management LLC (since 2008) | 2 | Independent Trustee of Two Roads Shared Trust (since 2012), Forethought Variable Insurance Trust (since 2013), Northern Lights Fund Trust (since 2013), Northern Lights Variable Trust (since 2013), iCapital KKR Private Markets Fund (since 2014), Independent Director of OHA CLO Enhanced Equity II Genpar LLP (since 2021), and Independent Trustee, Carlyle Tactical Private Credit Fund (since 2018). | |||||

| Interested Trustee/Nominee(2) | ||||||||||

| Lauren Basmadjian (1979) | Trustee | Class III Board member until 2024 annual shareholder meeting–since July 2023 | Managing Director, The Carlyle Group Inc. (Since 2020); Senior Portfolio Manager, Octagon Credit Investors, LLC (2001 to 2020) | 1 | None. | |||||

6

| Name, Age and Address(1) | Position(s) Held with the Fund | Term of Office and Length of Time Served | Principal Occupation(s) During Past 5 Years | Number of Registered Investment Companies in Fund Complex Overseen by Trustee/ Nominee(2) | Other Directorships Held by Trustee/Nominee(3) | |||||

| Other Interested Trustee(2) | ||||||||||

| Brian Marcus (1983) | Trustee | Class I Board member until 2025 annual shareholder meeting–since July 2023 | Managing Director, The Carlyle Group Inc. (Since 2021); Principal, Carlyle Group (2018–2020); Vice President, The Carlyle Group Inc. (2015–2017) | 2 | None. | |||||

| (1) | The address of each Trustee is care of the Secretary of the Fund at One Vanderbilt Avenue, Suite 3400, New York, NY 10017. |

| (2) | “Interested person,” as defined in the 1940 Act, of the Fund. Mr. Marcus and Ms. Basmadjian are interested persons of the Fund due to their affiliation with the Adviser. |

No Trustee or Nominee who is not an interested person of the Fund, or any immediate family member of such person, owns securities in the Adviser, or a person directly or indirectly controlling, controlled by, or under common control with the Adviser.

Officers of the Fund

| Name, Age and Address(1) | Position(s) Held with the Fund | Term of Office and Length of Time Served | Principal Occupation(s) During Past 5 Years | |||

Lauren Basmadjian (1979) | President, Principal Executive Officer | Indefinite Length–since July 2023 | Managing Director, The Carlyle Group Inc. (Since 2020); Senior Portfolio Manager, Octagon Credit Investors, LLC (2001 to 2020) | |||

Nelson Joseph (1979) | Principal Financial Officer, Principal Accounting Officer, and Treasurer | Indefinite Length–since July 2023 | Principal, Carlyle Group (Since 2023); Director, Apollo Global Management LLC (2016–2022) | |||

Joshua Lefkowitz (1974) | Secretary; Chief Legal Officer | Indefinite Length–since July 2023 | Managing Director and Chief Legal Officer (Global Credit), Carlyle Group (Since 2018); Principal and Associate General Counsel, Ares Management, Ltd. (Jan 2017–Mar 2018); Vice President and Associate General Counsel, American Capital, Ltd. (Mar 2006–Jan 2017) | |||

7

| Name, Age and Address(1) | Position(s) Held with the Fund | Term of Office and Length of Time Served | Principal Occupation(s) During Past 5 Years | |||

Jennifer Juste 1980 | Chief Compliance Officer | Indefinite Length–since May 2024 | Vice President, Carlyle Group (Since 2022); Natixis Investment Managers 2019–2022 (Deputy Chief Compliance Officer/Deputy General Counsel Mirova US LLC 2020–2022 and Chief Compliance Officer/ General Counsel Ostrum US LLC 2019–2020) |

| (1) | The address of each officer is care of the Secretary of the Fund at One Vanderbilt Avenue, Suite 3400, New York, NY 10017. |

Compensation of Trustees

The following table shows information regarding the compensation to be earned by the Trustees, none of whom is an employee of the Fund, for services as a Trustee for the fiscal year ended September 30, 2023. The Trustees who are “interested persons”, as defined in the 1940 Act, of the Fund and the Fund’s officers do not receive compensation from the Fund.

| Compensation(1) | ||||

Name of Trustee/Nominee | Aggregate Compensation From the Fund | |||

Interested Trustees/Nominee | ||||

Lauren Basmadjian(2) | None | |||

Brian Marcus(2) | None | |||

Independent Trustees/Nominees | ||||

Sanjeev Handa | $ | 45,000 | ||

Mark Garbin | $ | 40,000 | ||

Joan McCabe | $ | 40,000 | ||

| (1) | Includes all amounts paid for serving as Trustee of the Fund, as well as serving as chairperson of a committee. |

| (2) | Ms. Basmadjian and Mr. Marcus, each an Interested Trustee, are not compensated by the Fund or the Fund Complex for his or her services. |

The Fund’s Board met six times during the fiscal year ended September 30, 2023. Each Trustee then serving in such capacity attended at least 75% of the meetings of the Board and of any Committee of which he or she is a member.

Board Committees

In addition to serving on the Board, the Independent Trustees also serve on the following committees which have been established by the Board to handle certain designated responsibilities. The Board has designated a chairperson of each committee. The Board may establish additional committees, change the membership of any committee, fill all vacancies, and designate alternate members to replace any absent or disqualified member of any committee, or to dissolve any committee as it deems necessary and in the Fund’s best interest.

Audit Committee. The members of the Fund’s Audit Committee are Sanjeev Handa, Mark Garbin, and Joan McCabe, each of whom meets the independence standards established by the SEC for audit committees and is independent for purposes of the 1940 Act. Sanjeev Handa serves as Chair of the Fund’s Audit Committee. The Board has determined that Mr. Handa is an “audit committee financial expert” as that term is defined under Item 407 of Regulation S-K of the Exchange Act. The Fund’s Audit Committee operates pursuant to a written

8

charter and meets periodically as necessary. A copy of the Audit Committee’s charter is attached hereto as Appendix A. The Audit Committee is responsible for selecting, engaging and discharging the Fund’s independent registered public accounting firm, reviewing the plans, scope and results of the audit engagement with the Fund’s independent registered public accounting firm, approving professional services provided by the Fund’s independent registered public accounting firm (including compensation therefor), reviewing the independence of the Fund’s independent registered public accounting firm and reviewing the adequacy of the Fund’s internal controls over financial reporting.

The Fund’s Audit Committee met four times during the fiscal year ended September 30, 2023. None of the members of the Audit Committee is an “interested person” of the Fund.

Nominating and Governance Committee. The members of the Fund’s Nominating and Governance Committee are Joan McCabe, Mark Garvin, and Sanjeev Handa, each of whom meets the independence standards established by the SEC for governance committees and is independent for purposes of the 1940 Act. Joan McCabe serves as Chair of the Fund’s Nominating and Governance Committee. The Fund’s Nominating and Governance Committee operates pursuant to a written charter and meets periodically as necessary. A copy of the Nominating and Governance Committee’s charter is attached hereto as Appendix B. The Nominating and Governance Committee is responsible for selecting, researching, and nominating trustees for election by shareholders, periodically reviewing the composition of the Board in light of the current needs of the Board and the Fund, and determining whether it may be appropriate to add or remove individuals after considering issues of judgment, diversity, age, skills, background and experience. The Nominating and Governance Committee will consider proposed nominations for trustees by shareholders who have sent nominations (which include the biographical information and the qualifications of the proposed nominee) to the Principal Executive Officer of the Fund, as the Nominating and Governance Committee deems appropriate.

The Fund’s Nominating and Governance Committee met two times during the fiscal year ended September 30, 2023. None of the members of the Nominating and Governance Committee is an “interested person” of the Fund.

Independent Trustees Committee. The members of the Fund’s Independent Trustees Committee are Mark Garbin, Joan McCabe, and Sanjeev Handa, each of whom meets the independence standards established by the SEC for governance committees and is independent for purposes of the 1940 Act. Mark Garbin serves as Chair of the Fund’s Independent Trustees Committee. The Fund’s Independent Trustees Committee operates pursuant to a written charter and meets periodically as necessary. A copy of the Independent Trustees Committee’s charter is attached hereto as Appendix C. The Independent Trustees Committee is responsible for addressing conflict of interest matters including, but not limited to, the approval of certain co-investment transactions conducted by the Fund in reliance on co-investment exemptive relief.

The Fund’s Independent Trustees Committee met two times during the fiscal year ended September 30, 2023. None of the members of the Independent Trustees Committee is an “interested person” of the Fund.

Board Leadership Structure

The Board is currently composed of five Trustees, three of whom are Independent Trustees. The Fund’s business and affairs are managed under the direction of its Board. Among other things, the Board sets broad policies for the Fund and approves the appointment of the Fund’s administrator and officers. The role of the Board, and of any individual Trustee, is one of oversight and not of management of the Fund’s day-to-day affairs.

Under the Fund’s By-Laws, the Board may designate one of the Trustees as chair to preside over meetings of the Board and meetings of shareholders, and to perform such other duties as may be assigned to him or her by the Board. Presently, Lauren Basmadjian serves as Chair of the Board and is an Interested Trustee by virtue of her employment relationship with the Adviser. The Board believes that it is in the best interests of Fund

9

shareholders for Ms. Basmadjian to serve as Chair of the Board because of her significant experience in matters of relevance to the Fund’s business. The Board does not, at the present time, have a lead Independent Trustee; the Board has determined that the compositions of the Audit Committee, the Nominating and Governance Committee, and the Independent Trustees Committee are appropriate means to address any potential conflicts of interest that may arise from the Chair’s status as an Interested Trustee. The Board believes that flexibility to determine its chair and to recognize its leadership structure is in the best interests of the Fund and its shareholders at this time.

All of the Independent Trustees play an active role on the Board. The Independent Trustees compose a majority of the Board and will be closely involved in all material deliberations related to the Fund. The Board believes that, with these practices, each Independent Trustee has an equal involvement in the actions and oversight role of the Board and equal accountability to the Fund and its shareholders. The Independent Trustees are expected to meet separately (i) as part of each regular Board meeting and (ii) with the Fund’s chief compliance officer, as part of at least one Board meeting each year.

The Board believes that its leadership structure is the optimal structure for the Fund at this time. The Board, which will review its leadership structure periodically as part of its annual self-assessment process, further believes that its structure is presently appropriate to enable it to exercise its oversight of the Fund.

Board Role in Risk Oversight

The Trustees meet periodically throughout the year to discuss and consider matters concerning the Fund and to oversee the Fund’s activities, including its investment performance, compliance program and risks associated with its activities. Risk management is a broad concept comprising many disparate elements (for example, investment risk, issuer and counterparty risk, compliance risk, operational risk, and business continuity risk). The Board implements its risk oversight function both as a whole and through its committees. The Board has adopted, and periodically reviews, policies and procedures designed to address risks associated with the Fund’s activities. In the course of providing oversight, the Board and its committees will receive reports on the Fund’s and the Adviser’s activities, including reports regarding the Fund’s investment portfolio and financial accounting and reporting. The Board also receives a quarterly report from the Fund’s chief compliance officer, who reports on the Fund’s compliance with the federal and state securities laws and its internal compliance policies and procedures as well as those of the Adviser, administrator and transfer agent. The Audit Committee’s meetings with the Fund’s independent registered public accounting firm also contribute to its oversight of certain internal control risks. In addition, the Board meets periodically with the Adviser to receive reports regarding the Fund’s operations, including reports on certain investment and operational risks, and the Independent Trustees will be encouraged to communicate directly with senior members of Fund management.

The Board believes that this role in risk oversight is appropriate. The Board believes that the Fund has robust internal processes in place and a strong internal control environment to identify and manage risks. However, not all risks that may affect the Fund can be identified or processes and controls developed to eliminate or mitigate their occurrence or effects, and some risks are beyond the control of the Fund, the Adviser and the Fund’s other service providers.

Shareholder Communications

Shareholders may send communications to the Board. Shareholders should send communications intended for the Board by addressing the communication directly to the Board (or individual Trustees) and/or otherwise clearly indicating in the salutation that the communication is for the Board (or individual Trustees) and by sending the communication to either the Fund’s office or directly to such Trustee(s) at the address specified for such Trustee above. Other shareholder communications received by the Fund not directly addressed and sent to the Board will be reviewed and generally responded to by management, and will be forwarded to the Board only at management’s discretion based on the matters contained therein.

10

Audit Committee Reports

The Audit Committee acts according to an Audit Committee charter. Sanjeev Handa serves as Chair of the Audit Committee of the Fund’s Board. The Audit Committee is responsible for assisting the Board in fulfilling its oversight responsibilities relating to accounting and financial reporting policies and practices of the Fund, including, but not limited to, the adequacy of the Fund’s accounting and financial reporting processes, policies and practices; the integrity of the Fund’s financial statements; the adequacy of the Fund’s overall system of internal controls; the Fund’s compliance with legal and regulatory requirements; the qualification and independence of the Fund’s independent registered public accounting firm; the performance of the Fund’s internal audit function provided by the Adviser and the Fund’s other service providers; and the review of the report required to be included in the Fund’s annual proxy statement by the rules of the SEC. The Audit Committee is also required to prepare an audit committee report to be included in the Fund’s annual proxy statement as required by Item 407(d)(3)(i) of Regulation S-K. The Audit Committee operates pursuant to a charter that was most recently reviewed by the Fund’s Board on July 13, 2023. A copy of the Audit Committee’s charter is attached hereto as Appendix A. As set forth in the charter, the function of the Audit Committee is oversight; it is the responsibility of the Adviser to maintain appropriate systems for accounting and internal control, and the independent auditors’ responsibility to plan and carry out a proper audit. The independent registered public accounting firm is ultimately accountable to the Fund’s Board and Audit Committee, as representatives of the Fund’s shareholders. The independent registered public accounting firm for the Fund reports directly to the Audit Committee.

In performing its oversight function, at a meeting held on November 28, 2023, the Audit Committee reviewed and discussed with management of the Fund and the independent registered public accounting firm, Ernst & Young LLP (“EY”), the audited financial statements of the Fund as of and for the fiscal year ended September 30, 2023, and discussed the audit of such financial statements with the independent registered public accounting firm.

The Audit Committee has: (a) reviewed and discussed the Fund’s audited financial statements with the management of the Fund; (b) discussed with the independent registered public accounting firm the matters required to be discussed by the Public Company Accounting Oversight Board (“PCAOB”) Auditing Standard No. 16, as modified or supplemented; (c) received the written disclosures and the letter from the independent registered public accounting firm required by applicable requirements of the PCAOB Ethics and Independence Rule 3526 regarding the independent registered public accounting firm’s communications with the Audit Committee concerning independence, and has discussed with the independent registered public accounting firm the independent registered public accounting firm’s independence.

The members of the Audit Committee are not, and do not represent themselves to be, professionally engaged in the practice of auditing or accounting and are not employed by the Fund for accounting, financial management or internal control purposes. Moreover, the Audit Committee relies on and makes no independent verification of the facts presented to it or representations made by management or the Fund’s independent registered public accounting firm. Accordingly, the Audit Committee’s oversight does not provide an independent basis to determine that management has maintained appropriate accounting and/or financial reporting principles and policies, or internal controls and procedures designed to assure compliance with accounting standards and applicable laws and regulations. Furthermore, the Audit Committee’s considerations and discussions referred to above do not provide assurance that the audit of the Fund’s financial statements has been carried out in accordance with generally accepted accounting standards or that the financial statements are presented in accordance with generally accepted accounting principles.

Based on its consideration of the audited financial statements and the discussions referred to above with management and the Fund’s independent registered public accounting firm, and subject to the limitations on the responsibilities and role of the Audit Committee set forth in the charter and those discussed above, the Audit Committee recommended to the Board that the Fund’s audited financial statements be included in the Fund’s Annual Report for the fiscal year ended September 30, 2023.

11

SUBMITTED BY THE AUDIT COMMITTEE OF THE FUND’S BOARD

Sanjeev Handa, Audit Committee Chair

Mark Garbin

Joan McCabe

Other Board Related Matters

The Fund does not require Trustees to attend its Annual Meeting of Shareholders.

REQUIRED VOTE

The election of Ms. McCabe as a Class II Trustee of the Fund and Ms. Basmadjian and Mr. Handa as Class III Trustees of the Fund requires the affirmative vote of the holders of a plurality of the votes cast by holders of shares of beneficial interest of the Fund entitled to vote represented at the Meeting, if a quorum is present.

THE FUND’S BOARD, INCLUDING THE INDEPENDENT TRUSTEES, UNANIMOUSLY RECOMMENDS THAT THE SHAREHOLDERS VOTE “FOR” THE ELECTION OF THE FUND’S CLASS II AND CLASS III NOMINEES.

12

NOMINEE/TRUSTEE BENEFICIAL OWNERSHIP OF FUND SHARES

The following table shows the dollar range of shares beneficially owned by each Trustee/Nominee in the Fund and the Fund Complex as of June 30, 2024:

Name of Trustee/Nominee | Dollar Range of Equity Securities in Fund | Aggregate Dollar Range of Equity Securities in all Registered Investment Companies Overseen by Trustee/Nominee in Family of Investment Companies | ||||||

| Interested Trustees/Nominee | ||||||||

| Lauren Basmadjian | $100,001–$500,000 | $100,001–$500,000 | ||||||

| Brian Marcus | None | $100,001–$500,000 | ||||||

| Independent Trustees/Nominees | ||||||||

| Mark Garbin | None | $50,001–$100,000 | ||||||

| Sanjeev Handa | $10,001–$50,000 | $100,001–$500,000 | ||||||

| Joan McCabe | $100,001–$500,000 | Over $1,000,000 | ||||||

As of June 30, 2024, the Nominees, Trustees and officers of the Fund as a group owned less than 1% of the outstanding shares of beneficial interest of the Fund.

13

FIVE PERCENT SHAREHOLDERS

As of July 11, 2024, management knew of the following persons or entities who owned beneficially 5% or more of the outstanding shares of beneficial interest of the Fund:

Title of Class | Name and Address of Beneficial Owner | Amount and Nature of Beneficial | Percent of Class | |||||

Preferred | Eagle Point Credit Management LLC 600 Steamboat Road, Suite 202 Greenwich, Connecticut 06830 | 668,069 Shares with sole voting power and sole dispositive power(1) | 32.12 | % | ||||

Preferred | Karpus Investment Management 183 Sully’s Trail Pittsford, New York 14534 | 69,305 Shares with sole voting power and sole dispositive power(2) | 5.78 | % | ||||

Common | Relative Value Partners Group, LLC 1033 Skokie Blvd., Suite 470 Northbrook, Illinois 60062 | 140,666 Shares with sole voting power and sole dispositive power(3) | 6.76 | % | ||||

Common | The Carlyle Group 1001 Pennsylvania Avenue NW, Suite 220 South Washington, D.C. 20004 | 4,785,628 Shares with shared voting power and shared dispositive power(4) | 41.00 | % | ||||

Common | Almitas Capital LLC 1460 4th Street, Suite 300 Santa Monica, CA 90401 | 546,229 Shares with shared voting power and shared dispositive power(5) | 5.26 | % | ||||

Common | Sit Investment Associates, Inc. 3300 IDS Center 80 South Eighth Street Minneapolis, MN 55402 | 573,536 Shares with sole voting power and sole dispositive power(6) | 5.53 | % | ||||

| (1) | Based on a Schedule 13D/A filed with the SEC on February 23, 2024. |

| (2) | Based on a Schedule 13G filed with the SEC on February 13, 2024. |

| (3) | Based on a Schedule 13G filed with the SEC on February 12, 2024. |

| (4) | Based on a Schedule 13D/A filed with the SEC on September 14, 2023. |

| (5) | Based on a Schedule 13G/A filed with the SEC on February 14, 2023. |

| (6) | Based on a Schedule 13G filed with the SEC on February 14, 2023. |

ADDITIONAL INFORMATION

To request a copy of the Fund’s prospectus, statement of additional information, semi-annual report or annual report, without charge, please call 1-866-277-8243 or write to at One Vanderbilt Avenue, Suite 3400, New York, New York 10017.

Independent Registered Public Accounting Firm

On July 17, 2023, Grant Thornton LLP (“Grant Thornton”) was dismissed as the independent registered public accountants of the Fund upon the appointment of the Adviser as investment adviser of the Fund. Grant Thornton’s reports on the financial statements of the Fund for the past two years did not contain an adverse opinion or disclaimer of opinion, and were not qualified or modified as to uncertainty, audit scope or accounting principles. During the period Grant Thornton was engaged: (i) there were no disagreements with Grant Thornton on any matter of accounting principles or practices, financial statement disclosure, or auditing scope or procedure

14

which, if not resolved to Grant Thornton’s satisfaction, would have caused it to make reference to that matter in connection with its reports on the Fund’s financial statements for such periods; and (ii) there were no “reportable events” of the kind described in Item 304(a)(1)(v) of Regulation S-K under the Securities Exchange Act of 1934, as amended.

Effective July 17, 2023, based on the recommendation of the Audit Committee of the Board of Trustees, the Board of Trustees approved the appointment of Ernst & Young LLP (“EY”), One Manhattan West, 395 9th Avenue, New York, NY 10001, as the independent registered public accounting firm of the Fund for the fiscal year ended September 30, 2023. During the Fund’s fiscal years ended September 30, 2021 and September 30, 2022, and in the subsequent interim period through July 17, 2023, neither the Fund, nor anyone on its behalf, consulted with EY on items which: (i) concerned the application of accounting principles to a specified transaction, either completed or proposed, or the type of audit opinion that might be rendered on the Fund’s financial statements; or (ii) concerned the subject of a disagreement (as described in paragraph (a)(1)(iv) of Item 304 of Regulation S-K) or reportable events (as described in paragraph (a)(1)(v) of said Item 304).

The Fund does not know of any direct financial or material indirect financial interest of EY in the Fund.

Representatives of EY are not expected to be present at the Meeting but have been given the opportunity to make a statement if they so desire and will be available should any matter arise requiring their response.

Principal Accounting Fees and Services

The following table sets forth for the Fund the aggregate fees billed by the independent auditors to the Fund for the last two fiscal years, as a result of professional services rendered for:

(1) Audit Fees for professional services provided by the independent auditors for the audit of the Fund’s annual financial statements or services that are normally provided by the accountant in connection with statutory and regulatory filings or engagements;

(2) Audit-Related Fees for assurance and related services by the independent auditors that are reasonably related to the performance of the audit of the Fund’s financial statements and are not reported under “Audit Fees”;

(3) Tax Fees for professional services by the independent auditors for tax compliance, tax advice and tax planning; and

(4) All Other Fees for products and services provided by the independent auditors other than those services reported in above under “Audit Fees,” “Audit Related Fees” and “Tax Fees”.

Audit Fees | Audit-Related Fees | Tax Fees | All Other Fees | |||

| July 17, 2023 to September 30, 2023 (EY) | July 17, 2023 to September 30, 2023 (EY) | July 17, 2023 to September 30, 2023 (EY) | July 17, 2023 to September 30, 2023 (EY) | |||

| $271,000 | $0 | $0 | $0 | |||

| October 1, 2022 to September 30, 2023 (Grant Thornton) | October 1, 2022 to September 30, 2023 (Grant Thornton) | October 1, 2022 to September 30, 2023 (Grant Thornton) | October 1, 2022 to September 30, 2023 (Grant Thornton) | |||

| $0 | $0 | $0 | $68,900 | |||

| October 1, 2021 to September 30, 2022 (Grant Thornton) | October 1, 2021 to September 30, 2022 (Grant Thornton) | October 1, 2021 to September 30, 2022 (Grant Thornton) | October 1, 2021 to September 30, 2022 (Grant Thornton) | |||

| $190,868 | $— | $5,350 | $— | |||

15

The Fund’s Audit Committee Charter requires that the Audit Committee pre-approve (i) all audit and non-audit services that the Fund’s independent auditors provide to the Fund, and (ii) all non-audit services that the Fund’s independent auditors provide to the Adviser and any entity controlling, controlled by, or under common control with the Adviser that provides ongoing services to the Fund, if the engagement relates directly to the operations and financial reporting of the Fund; provided that the Committee may implement policies and procedures by which such services are approved other than by the full Committee prior to their ratification by the Committee. All of the audit, audit-related, tax and other services described above for which the independent auditor billed the Fund fees for the fiscal year ended September 30, 2023, were pre-approved by the Audit Committee.

There were no non-audit fees billed by EY or Grant Thornton for services rendered to the Fund, the Adviser and any entity controlling, controlled by, or under common control with the Adviser that provides ongoing services to the Fund during that last two fiscal years.

The Investment Adviser and Administrator

Carlyle Global Credit Investment Management L.L.C., a wholly owned subsidiary of Carlyle Investment Management L.L.C, is the Fund’s investment adviser, effective at the close of business on July 14, 2023. Prior to that date, the Fund’s investment adviser was Oakline Advisors LLC.

SS&C Technologies, Inc. is the administrator for the Fund, and its business address is 80 Lamberton Road Windsor, CT 06095.

Section 16(a) Beneficial Ownership Reporting Compliance

Based solely on a review of the reports filed with the SEC and upon representations that no applicable forms were required to be filed pursuant to Section 16(a) of the Exchange Act, the Fund believes that during the fiscal year ended September 30, 2023, its officers and Trustees complied with all applicable Section 16(a) filing requirements.

Broker Non-Votes and Abstentions

The affirmative vote of a plurality of votes cast for each of the Class II and Class III Nominees by the holders entitled to vote is necessary for the election of the Class II and Class III Nominees.

For the purpose of electing the Class II and Class III Nominees, abstentions or broker non-votes will not be counted as votes cast and will have no effect on the result of the election. Abstentions or broker non-votes, however, will be considered to be present at the Meeting for purposes of determining the existence of the Fund’s quorum.

Shareholders of the Fund will be informed of the voting results of the Meeting in the Fund’s Semi-Annual Report for the period ending September 30, 2024.

OTHER MATTERS TO COME BEFORE THE MEETING

The Trustees of the Fund do not intend to present any other business at the Meeting, nor are they aware that any shareholder intends to do so. If, however, any other matters, including adjournments, are properly brought before the Meeting, the persons named in the accompanying form of proxy will vote thereon in accordance with their judgment.

16

Shareholder Communications with Board

Shareholders may mail written communications to the Fund’s Board, to committees of the Board or to specified individual Trustees in care of the Secretary of the Fund at One Vanderbilt Avenue, Suite 3400, New York, NY 10017. All shareholder communications received by the Secretary will be forwarded promptly to the Board, the Board’s committee or the specified individual Trustees, as applicable, except that the Secretary may, in good faith, determine that a shareholder communication should not be so forwarded if it does not reasonably relate to the Fund or its operations, management, activities, policies, service providers, Board, officers, shareholders or other matters relating to an investment in the Fund or is purely ministerial in nature.

Persons to be Named as Proxies

The Board has named Jennifer Juste and Nelson Joseph to serve as proxies (with full power of substitution) who are authorized to vote shares of the Fund owned by record shareholders.

SHAREHOLDER PROPOSALS

For nominations or other business to be properly brought before an annual meeting by a shareholder, the shareholder must have given timely notice thereof in writing to the Secretary and such other proposed business must otherwise be a proper matter for action by the shareholders. To be timely, a shareholder’s notice shall set forth all information required by the current By-Laws and shall be delivered to the Secretary at the principal executive office of the Fund, One Vanderbilt Avenue, Suite 3400, New York, NY 10017, not earlier than the 150th day or later than 5:00 p.m., Eastern Time, on the 120th day prior to the first anniversary of the date of the proxy statement for the preceding year’s annual meeting; provided, however, that in the event that the date of the annual meeting is advanced or delayed by more than 30 days from the date of the preceding year’s annual meeting, notice by the shareholder to be timely must be so delivered not earlier than the 150th day prior to the date of such annual meeting and not later than the close of business on the later of the 120th day prior to the date of such annual meeting or the tenth day following the day on which public announcement of the date of such meeting is first made. In no event shall the public announcement of a postponement or adjournment of an annual meeting commence a new time period (or extend any time period) for the giving of a shareholder’s notice as described above. Nominations of individuals for election to the Board of Trustees and the proposal of other business to be considered by the shareholders may be made at an annual meeting of shareholders only (1) pursuant to the Fund’s notice of meeting (or any supplement thereto), (2) by or at the direction of the Board of Trustees or any committee thereof or (3) by any shareholder of the Fund who was a shareholder of record both at the time of giving of notice by the shareholder and at the time of the annual meeting, who is entitled to vote at the meeting in the election of any individual so nominated or on any such other business.

Shareholder proposals that are submitted in a timely manner will not necessarily be included in the Fund’s proxy materials. Inclusion of such proposals is subject to limitations under the federal securities laws.

IF VOTING BY PAPER PROXIES, IT IS IMPORTANT THAT PROXIES BE RETURNED PROMPTLY. SHAREHOLDERS WHO DO NOT EXPECT TO ATTEND A MEETING ARE THEREFORE URGED TO COMPLETE, SIGN, DATE, AND RETURN THE PROXY CARD AS SOON AS POSSIBLE IN THE ENCLOSED POSTAGE-PAID ENVELOPE.

17

APPENDIX A

AUDIT COMMITTEE CHARTER

FOR CARLYLE CREDIT INCOME FUND

This document (the “Charter”) constitutes the Charter of the Audit Committee (the “Audit Committee” or “Committee”) of Carlyle Credit Income Fund (the “Fund”), a registered investment company. The Fund is advised by Carlyle Global Credit Investment Management L.L.C. (the “Adviser”). State Street Bank and Trust Company (the “Administrator”) provides administrative services to the Fund.

I. Organization. The Audit Committee of the Fund shall consist of at least three members appointed by the Board of Trustees of the Fund (the “Board”). The Board may replace members of the Audit Committee for any reason.

No member of the Audit Committee shall be an “interested person” of the Fund, as that term is defined in Section 2(a)(19) of the Investment Company Act of 1940, as amended (the “1940 Act”). Audit Committee members must also meet the independence standards set forth in the Fund’s Nominating and Governance Committee Charter and Rule 10A-3(b)(1)(iii)1 under the Securities Exchange Act of 1934, as amended (the “1934 Act”) and any other applicable listing exchange rules. No member of the Audit Committee shall receive, directly or indirectly, any consulting, advisory or other compensatory fee from the Funds except compensation for service as a member of the Board or a committee of the Board.

Each member of the Audit Committee must be financially literate, as that qualification is interpreted by the Board in its business judgment, or must become financially literate within a reasonable time after appointment to the Audit Committee. The Board may presume that an “audit committee financial expert” as defined in Item 3 of Form N-CSR (“ACFE”) satisfies the requirement in the foregoing sentence. The Board, with the assistance of the Committee, shall determine whether any member of the Audit Committee is an ACFE. The Committee’s composition shall meet such other regulatory requirements relating to audit committees established from time to time by the U.S. Securities and Exchange Commission (the “SEC”) and any other applicable governmental entity or self-regulatory organization or law to which the Fund is subject.

II. Committee Purpose. The purposes of the Audit Committee are:

A. to oversee the accounting and financial reporting processes of the Fund and its internal control over financial reporting and, as the Committee deems appropriate, to inquire into the internal control over financial reporting of certain third-party service providers;

B. to oversee, or, as appropriate, assist Board oversight of, the quality and integrity of the Fund’s financial statements and the independent audits thereof;

C. to oversee, or, as appropriate, assist Board oversight of, the Fund’s compliance with legal and regulatory requirements that relate to the Fund’s accounting and financial reporting, internal control over financial reporting and independent audits;

| 1 | In order to be considered to be independent for purposes of Rule 10A-3(b)(i), a member of an audit committee of a listed issuer that is an investment company may not, other than in his or her capacity as a member of the audit committee, the board of trustees, or any other board committee: |

| • | Accept directly or indirectly any consulting, advisory, or other compensatory fee from the issuer or any subsidiary thereof, provided that, unless the rules of the national securities exchange or national securities association provide otherwise, compensatory fees do not include the receipt of fixed amounts of compensation under a retirement plan (including deferred compensation) for prior service with the listed issuer (provided that such compensation is not contingent in any way on continued service); or |

| • | Be an “interested person” of the issuer as defined in section 2(a)(19) of the Investment Company Act of 1940. |

18

D. to approve, prior to appointment, the engagement of the Fund’s independent auditor (the “Auditor”) and, in connection therewith, to oversee the compensation and review and evaluate the qualifications, independence and performance of the Auditor;

E. to act as a liaison between the Auditor and the full Board; and

F. to assist Board oversight of the Fund’s internal audit function (if any).

The Auditor for the Fund shall report directly to the Audit Committee.

III. Duties and Powers of the Audit Committee. To carry out its purposes, the Audit Committee shall have the following duties and powers:

A. to approve, prior to appointment, the engagement of the Auditor to annually audit and provide its opinion on the Fund’s financial statements, to recommend to those Board members who are not “interested persons” (as that term is defined in Section 2(a)(19) of the 1940 Act) of the Fund the selection, retention or termination of the Auditor and, in connection therewith, to review and evaluate matters potentially affecting the independence and capabilities of the Auditor. In evaluating the Auditor’s qualifications, performance and independence, the Audit Committee must, among other things, obtain and review a report by the Auditor, at least annually, describing the following items:

1. all relationships between the Auditor and the Fund, including each non-audit service provided to the Fund and the matters set forth in Public Company Accounting Oversight Board (“PCAOB”) Rule 3526, Communication with Audit Committees Concerning Independence;

2. any material issues raised by the most recent internal quality control review, or peer review, of the audit firm, or by any inquiry or investigation by governmental or professional authorities, within the preceding five years, respecting one or more independent audits carried out by the firm, and any steps taken to deal with any such issues; and

3. the audit firm’s internal quality-control procedures.

B. to approve, prior to appointment, the engagement of the Auditor to provide other audit services to the Fund or to provide non-audit services to the Fund, it’s the Adviser or any entity controlling, controlled by, or under common control with the Adviser (“adviser affiliate”) that provides ongoing services to the Fund, if the engagement relates directly to the operations and financial reporting of the Fund;

C. to develop, to the extent deemed appropriate by the Audit Committee, policies and procedures for pre-approval of the engagement of the Auditor to provide any of the services described in 2 above;

D. to consider the controls applied by the Auditor and any measures taken by management in an effort to assure that all items requiring preapproval by the Audit Committee are identified and referred to the Committee in a timely fashion;

E. to consider whether the non-audit services provided by the Auditor to the Fund’s Adviser or any adviser affiliate that provides ongoing services to the Fund, which services were not preapproved by the Audit Committee, are compatible with maintaining the Auditor’s independence;

F. to review the arrangements for and scope of the annual audit and any special audits;

G. to review and approve the fees proposed to be charged to the Fund by the Auditor for each audit and non-audit service;

H. to consider information and comments from the Auditor with respect to the Fund’s accounting and financial reporting policies, procedures and internal control over financial reporting (including the Fund’s critical accounting policies and practices), to consider management’s responses to any such comments and, to the extent the Audit Committee deems necessary or appropriate, to promote improvements in the quality of the Fund’s accounting and financial reporting;

I. to consider information and comments from the Auditor with respect to, and meet with the auditor to discuss any matters of concern relating to, the Fund’s financial statements, including any adjustments to

19

such statements recommended by the Auditor, to review the Auditor’s opinion on the Fund’s financial statements and to review and discuss with management and the Auditor the Fund’s annual audited financial statements and other periodic financial statements, including any disclosures under “Management’s Discussion of Fund Performance;”

J. to consider and review any matters required to be discussed pursuant to applicable PCAOB Statements of Auditing Standards, Generally Accepted Auditing Standards and the rules and regulations of the SEC or other matters arising out of the audit that are significant to the oversight of the Fund’s financial reporting process;

K. to review tax matters affecting the Fund, including:

1. compliance with the provisions of the Internal Revenue Code of 1986, as amended (the “Code”), and regulations, including annual reviews for the Fund concerning its qualification as a regulated investment company under the Code; and

2. tax legislation and rulings;

L. to consider and review reports on capital gains and other items pertaining to Fund dividends and their accruals;

M. to help resolve disagreements between management and the Auditor regarding financial reporting;

N. to consider any reports of difficulties that may have arisen in the course of the audit, including any limitations on the scope of the audit, and management’s response thereto;

O. to review with the Fund’s principal executive officer and/or principal financial officer in connection with required certifications on Form N-CSR any significant deficiencies in the design or operation of internal control over financial reporting or material weaknesses therein and any reported evidence of fraud involving management or other employees who have a significant role in the Fund’s internal control over financial reporting;

P. to make a report as required by Item 407(d) of Regulation S-K indicating whether the Committee: (i) reviewed and discussed the financial statements with management; (ii) discussed with the independent auditor the matters required by applicable auditing standards; and (iii) received the written disclosures and the letter from the independent auditor required by applicable requirements of the PCAOB regarding the independent auditor’s communications with the Committee concerning independence, and discussed with the independent auditor their independence. The Committee’s report should also indicate whether the Committee, based on its review and its discussions with management and the independent auditor, recommends to the Board that the financial statements be included in the Fund’s annual report for the last fiscal year;

Q. to review reports and materials submitted by the Auditor regarding valuation of portfolio investments, including determinations of fair value or the procedures for the determination of the fair value of any such investments that do not have readily ascertainable market values, and the use of third party pricing services by management;

R. to review periodically, in accordance with the Fund’s Whistleblower Policy, matters submitted to the Committee regarding complaints received by the Fund relating to accounting, internal accounting controls, or auditing matters, and the confidential, anonymous submission by employees of the Fund, the Adviser, administrator, transfer agent, distributor, or any other provider of accounting related services for the Fund of concerns about accounting or auditing matters, and to address reports from attorneys or the Auditor of possible violations of federal or state law or fiduciary duty;

S. to review in a general manner, but not as a committee to assume responsibility for, the Fund’s processes with respect to risk assessment and risk management;

T. to set clear policies relating to the hiring by entities within the Fund’s investment company complex2 of employees or former employees of the independent auditor;

20

U. to investigate or initiate an investigation of reports of improprieties or suspected improprieties in connection with the Fund’s accounting or financial reporting;

V. to report its activities to the full Board on a regular basis and to make such recommendations with respect to the above and other matters as the Audit Committee may deem necessary or appropriate;

W. to perform such other functions and to have such powers as may be necessary or appropriate in the efficient and lawful discharge of the powers provided in this Charter;

X. to review and discuss the Fund’s audited annual financial statements and unaudited semiannual reports with the Adviser and, in the case of the audited financials, the independent auditor, including the Fund’s disclosures under “Management’s Discussion of Fund Performance;”

Y. to consider and, if appropriate, recommend or approve the publication of the Fund’s annual audited financial statements in the Fund’s annual report in advance of the printing and publication of the annual report, based on its review and discussions of such annual report with the independent auditor, the Fund’s officers and the Adviser; and (if applicable) prepare the audit committee report required to be included in the Fund’s proxy statement for its annual meeting of shareholders (if such meeting is required by law);

Z. to, at least annually, obtain and review a report by the Auditor describing: (i) the Auditor’s internal quality-control procedures; (ii) any material issues raised by the most recent internal quality-control review, or peer review, of the Auditor, or by any inquiry or investigation by governmental or professional authorities, within the preceding five years, respecting one or more independent audits carried out by the Auditor, and any steps taken to deal with such issues; and (iii) (to assess the Auditor’s independence) all relationships between the Auditor and the Fund;

AA. to discuss policies with respect to risk assessment and risk management, including (i) a discussion of the Fund’s guidelines and policies to govern the process by which Fund management assesses and manages the Fund’s exposure to risk; (ii) a discussion of the Fund’s major financial risk exposures and the steps Fund management has taken to monitor and control such exposures; and (iii) a general review of the processes which Fund management have in place to manage and assess risk, if any;

BB. to review hiring policies of the Adviser and the Fund, if any, for employees and former employees of the Auditor; and

CC. to discuss, to the extent applicable, any press release containing earnings or financial information or any such information provided to the public or analysts and rating agencies.

The Audit Committee shall have the resources and authority appropriate to discharge its responsibilities, including appropriate funding, as determined by the Audit Committee, for payment of compensation to the Auditor for the purpose of conducting the audit and rendering its audit report, the authority to retain and compensate special counsel and other experts or consultants as the Audit Committee deems necessary, the authority to obtain specialized training for Audit Committee members, at the expense of the Fund, as appropriate, and ordinary administrative expenses of the Audit Committee.

| 2 | “Investment company complex” includes: |

| • | the fund and its investment adviser or sponsor; |

| • | any entity controlling, controlled by or under common control with the investment adviser or sponsor, if the entity: (i) is an investment adviser or sponsor; or (ii) is engaged in the business of providing administrative, custodian, underwriting or transfer agent services to any investment company, investment adviser or sponsor; and |

| • | any investment company, hedge fund or unregistered fund that has an investment adviser included in the definition set forth in either of the two bullet points above. |

An investment adviser, for these purposes, does not include a sub-adviser whose role is primarily portfolio management and that is subcontracted with or overseen by another investment adviser. Sponsor refers to the sponsor of a unit investment trust.

21

The Audit Committee may, in accordance with applicable laws, delegate any portion of its authority to a subcommittee of one or more members, including the authority to grant pre-approvals of audit and permitted non-audit services, pursuant to the details of the pre-approval policies and procedures adopted by the Audit Committee. Any decisions of the subcommittee to grant pre-approvals shall be presented to the full Audit Committee at its next regularly scheduled meeting.

IV. Role and Responsibilities of the Audit Committee. The function of the Audit Committee is oversight; it is management’s responsibility to maintain appropriate systems for accounting and internal control over financial reporting, and the Auditor’s responsibility to plan and carry out a proper audit. Specifically, the Fund’s management is responsible for: (i) the preparation, presentation and integrity of the Fund’s financial statements; (ii) the maintenance of appropriate accounting and financial reporting principles and policies; and (iii) the maintenance of internal control over financial reporting and other procedures designed to assure compliance with accounting standards and related laws and regulations. The Auditor is responsible for planning and carrying out an audit consistent with applicable legal and professional standards and the terms of its engagement letter. Nothing in this Charter shall be construed to reduce the responsibilities or liabilities of the Fund’s service providers, including the Auditor.

Although the Audit Committee is expected to take a detached and questioning approach to the matters that come before it, the review of the Fund’s financial statements by the Audit Committee is not an audit, nor does the Committee’s review substitute for the responsibilities of the Fund’s management for preparing, or the Auditor for auditing, the financial statements. Members of the Audit Committee are not full-time employees of the Fund and, in serving on this Committee, are not, and do not hold themselves out to be, acting as accountants or auditors. As such, it is not the duty or responsibility of the Committee or its members to conduct “field work” or other types of auditing or accounting reviews or procedures.

In discharging his or her duties, a member of the Audit Committee is entitled to rely on information, opinions, reports, or statements, including financial statements and other financial data, if prepared or presented by: (i) one or more officers of the Fund whom the trustee reasonably believes to be reliable and competent in the matters presented; (ii) legal counsel, public accountants, or other persons as to matters the trustee reasonably believes are within the person’s professional or expert competence; or (iii) a Board committee of which the trustee is not a member.

V. Operations of the Audit Committee.

A. The Audit Committee shall meet on a regular basis and may hold special meetings when necessary. The chair or a majority of the members shall be authorized to call a meeting of the Audit Committee and send notice thereof.

B. Audit Committee members may attend Committee meetings telephonically (although they are encouraged to attend in person), and the Committee may act by written consent, to the extent permitted by law and by the Fund’s By-Laws.

C. The Audit Committee shall have the authority to meet privately and to admit non-members individually by invitation.

D. The Audit Committee shall regularly meet, in separate executive sessions, with representatives of Fund management, the Fund’s internal auditor or other personnel responsible for the Fund’s internal audit function (if any) and the Auditor. The Committee may also request to meet with internal legal counsel and compliance personnel of the Fund’s investment adviser and with entities that provide significant accounting or administrative services to the Fund to discuss matters relating to the Fund’s accounting and compliance as well as other Fund related matters.

E. The Audit Committee shall prepare and retain minutes of its meetings and appropriate documentation of decisions made outside of meetings by delegated authority.

22

F. The Audit Committee may select one of its members to be the chair and may select a vice chair.