united states

securities and exchange commission

washington, d.c. 20549

form n-csr

certified shareholder report of registered management

investment companies

Investment Company Act file number 811-22549

Northern Lights Fund Trust II

(Exact name of registrant as specified in charter)

225 Pictoria Drive, Suite 450, Cincinnati, Ohio 45246

(Address of principal executive offices) (Zip code)

Kevin Wolf, Ultimus Fund Solutions, LLC

80 Arkay Drive, Hauppauge, NY 11788

(Name and address of agent for service)

Registrant's telephone number, including area code: 631-470-2619

Date of fiscal year end: 3/31

Date of reporting period: 3/31/24

Item 1. Reports to Stockholders. [Insert annual report.]

Hodges Fund

Retail Class (Symbol: HDPMX)

Small Cap Fund

Retail Class (Symbol: HDPSX)

Institutional Class (Symbol: HDSIX)

Small Intrinsic Value Fund

Retail Class (Symbol: HDSVX)

Blue Chip Equity Income Fund

Retail Class (Symbol: HDPBX)

Annual Report | March 31, 2024

| | Advised by: |

| | Hodges Capital Management |

| | 2905 Maple Avenue |

| | Dallas, Texas 75201 |

| | |

| https://www.hodgesfunds.com/ | 1-866-811-0224 |

The U.S. Securities and Exchange Commission (“SEC”) has not approved or disapproved of these securities or determined if this Prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

Table of Contents

| Shareholder Letter | 1 |

| | |

| Portfolio Review | 8 |

| | |

| Schedules of Investments | 12 |

| | |

| Statements of Assets and Liabilities | 26 |

| | |

| Statements of Operations | 27 |

| | |

| Statements of Changes in Net Assets | 28 |

| | |

| Financial Highlights | 32 |

| | |

| Notes to Financial Statements | 37 |

| | |

| Report of Independent Registered Public Accounting Firm | 47 |

| | |

| Expense Examples | 48 |

| | |

| Approval of Investment Advisory Agreement | 49 |

| | |

| Supplemental Information | 53 |

| | |

| Additional Information | 55 |

| | |

| Privacy Notice | 56 |

| Hodges Funds Annual Shareholder Letter |

| April 15, 2024 |

It may be hard to believe, but the past twelve months ending March 31, 2024, resulted in a stellar rally for U.S. stocks, with the broader market beginning to show strength outside of technology stocks. The S&P 500 Index posted a gain of 29.88% over the past year. Furthermore, the number of stocks trading above their 200 -day moving average on March 31, 2024, was the highest level in three years at 85%. Investor sentiment improved in recent months despite mixed signals surrounding the likelihood and timing of central bank interest rate cuts in 2024. Although trailing the S&P 500, small-caps, as measured by the Russell 2000, increased by 19.71% for the twelve months ending March 31. With the Hodges Mutual Funds fiscal year ending March 31, three of our four fund strategies beat their respective benchmarks over the past year. Positive relative performance in these fund strategies was primarily attributed to our steadfast focus on companies with sound business fundamentals and reasonable valuations.

Over the past several months, we have seen a healthy broadening of capital flows into sectors outside of mega-cap technology. This favored stocks with improving balance sheets, whose underlying assets can produce stable cash flow and earnings in a normalizing credit environment. As a result, the energy, industrial, financial, and materials sectors within the S&P 500 outperformed technology for a change. According to the most recent data published by FactSet, the S&P 500 traded at approximately 20.5X its forward earnings estimate at the end of March compared to 19.3X at the start of the year and its 5-year average of 19.1X. The inverse of the current S&P 500 PE multiple is an earnings yield of 4.88%, which was still above the 10-year treasury yield of 4.20% at the end of the recent quarter. It is worth acknowledging that PE multiples remain highly bifurcated between growth and value stocks.

For the balance of 2024, our investment team is laser-focused on the fundamentals of individual stock selection and the prospects for earnings power in the months ahead. While many economic pundits have predicted a U.S. recession for the past couple of years, a decline in real GDP for two consecutive quarters has not materialized. However, we have observed that specific sectors, such as financials, energy, and industrials, have already experienced an earnings recession or at least a significant contraction in profit margins over the past 18 months. Moreover, we now see the early signs of an earnings recovery for many economically sensitive stocks, especially within small caps, in the second half of 2024. Moreover, inflation appears to be moderating compared to this time a year ago, albeit slower than some predicted. Given the prospects for a more normalizing environment for inflation, we would not be surprised to see new leadership emerge within the domestic market or at least a broader number of stocks participating in any upside from earnings growth and PE multiple expansion.

Furthermore, we believe this is an ideal time to focus on quality stocks at a fair price rather than growth at any price, which is not always measured by market capitalization or reflected in market sentiment. We define quality as those well-managed companies with structural competitive advantages resulting from a differentiated niche, proprietary technology, or unique barrier to entry. Other factors include conservative balance sheets, low-cost operations, and ample liquidity to weather a downturn and, in many cases, take market share from weak competitors.

Our recent discussions with public company management teams over the past few months suggest that supply chains are stable for most industries, input costs have moderated, and demand remains healthy. Although the U.S. economy remains near full employment, consumer spending appears more erratic this year as low savings rates and higher credit card balances curtail discretionary consumption of some goods and services. The housing market is holding up better than feared in many regions due to a lack of existing homes for sale. Many small industrial companies that we have spoken with appear positioned to benefit from onshoring and nearshoring of supply chains and increased infrastructure-related spending. In this environment, active portfolio management becomes essential to navigate quickly changing business conditions across many sectors and position portfolios to potentially benefit from shifting economic trends and structural changes across different industries.

In summary, we are spending little time trying to predict short-term fluctuations in interest rates, foreign currencies, or commodity prices. Instead, we are paying close attention to prevailing trends and, more importantly, the earning power our portfolio companies exhibit within their unique businesses. As a result, the investment team at Hodges Capital is rigorously looking for undervalued companies that we believe are well-run and control their destiny by

relying on ingenuity and well-calculated business decisions rather than day-to-day momentum in the stock market. Although many uncertainties exist surrounding the global economy, geopolitical tensions, inflation, and the upcoming elections, we are overweighting our portfolios with growth and value stocks that we expect to create long-term shareholder value in today’s environment. In these uncertain times, we want to reassure Hodges Funds investors that our fundamental investment approach remains steadfast. Moreover, we view the current landscape as an opportune moment for our portfolio managers to meticulously handpick individual stocks that we believe will yield lasting value for our shareholders. Your trust in us means everything, and we are dedicated to upholding our investment discipline.

Returns (Retail Class) as of 03/31/2024:

| | | | | | |

| 1 Yr | 3 Yrs | 5 Yrs | 10 Yrs | Since Inception |

| Hodges Fund | | | | | |

| (HDPMX) 10/09/1992 | 33.52% | 6.29% | 12.78% | 8.12% | 9.87% |

| S&P 500® Index | 29.88% | 11.49% | 15.05% | 12.96% | 10.64% |

Hodges Small Cap Fund

(HDPSX) 12/18/2007 | 21.80% | 5.49% | 12.16% | 7.64% | 9.72% |

| Russell 2000® Return Index | 19.71% | -0.10% | 8.10% | 7.58% | 8.05% |

Small Intrinsic Value Fund

(HDSVX) 12/26/2013 | 19.97% | 8.30% | 14.63% | 9.19% | 9.34% |

| Russell 2000® Value Return Index | 18.75% | 2.22% | 8.17% | 6.87% | 6.89% |

| Russell 2000® Index | 19.71% | -0.10% | 8.10% | 7.58% | 7.51% |

Blue Chip Equity Income Fund

(HDPBX) 09/10/2009 | 27.32% | 12.48% | 14.75% | 11.18% | 12.02% |

| Russell 1000® Total Return Index | 29.87% | 10.45% | 14.76% | 12.68% | 13.86% |

| Average Annualized | | | | |

| | | | | |

| | HDPSX | HDPMX | HDSVX | HDPBX |

| Gross Expense Ratio | 1.40% | 1.35% | 1.87% | 1.58% |

| Net Expense Ratio | 1.40%* | 1.18%* | 1.29%* | 1.30%* |

| | | | | |

* The Advisor has contractually agreed to reduce its fees at least until September 30, 2025. This figure excludes Acquired Fund Fees and Expenses, interest, taxes, and extraordinary expenses. The Advisor is permitted, with Board approval, to be reimbursed for fee reduction and/or expense payments made in the prior three years from the date the fees were waived and/or expenses were paid. Please see prospectus for details. |

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The current performance of the Funds may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by calling 866-811-0224. The Funds impose a 1.00% redemption fee on shares held for thirty days or less (60 days or less for Institutional Class shares). Performance data quoted does not reflect the redemption fee. If reflected, total returns would be reduced. Performance reflected is net of all other fees and expenses.

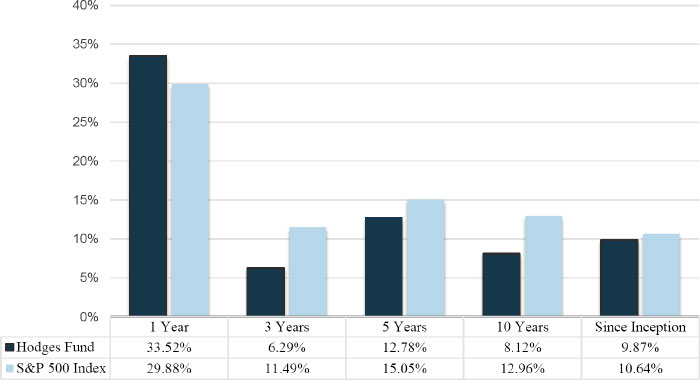

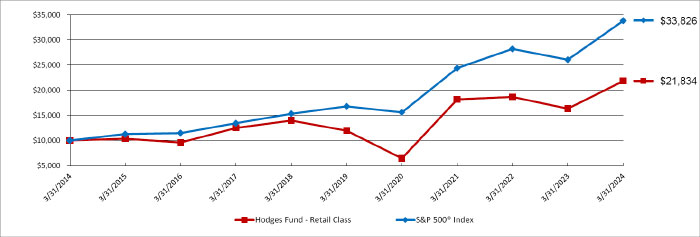

Hodges Fund (HDPMX)

The Fund’s one-year performance amounted to a 33.52% gain as of March 31, 2024, compared to a 29.88% gain for the S&P 500 Index during the same period. Although the portfolio has been underweighted among the seven largest momentum stocks in the S&P 500, positive performance over the past twelve months has been attributed to stock selection in a broad range of industrial, energy, consumer discretionary, and technology stocks. The Hodges Fund’s turnover returned to normal as we have carefully updated the portfolio holdings into stocks that we believe offer above-average returns relative to their downside risks over the next twelve to eighteen months.

The Hodges Fund’s portfolio managers remain focused on investments where we have the highest conviction based on fundamentals and relative valuations. The number of positions held in the Fund was 38 on March 31, 2024. The top ten holdings represented 46.82% of the Fund’s holdings. They included Matador Resources Co (MTDR), Uber Technologies (UBER), Encore Wire Corp (WIRE), DraftKings Inc (DKNG), Freeport McMoran Inc (FCX), Texas Pacific Land Corp (TPL), Cleveland-Cliffs Inc (CLF), Airbnb (ABNB), On Holding (ONON), and DoubleVerify Holdings Inc (DV).

Hodges Fund vs S&P 500 Index

As of 03/31/2024

Inception: 10/09/1992 Annualized

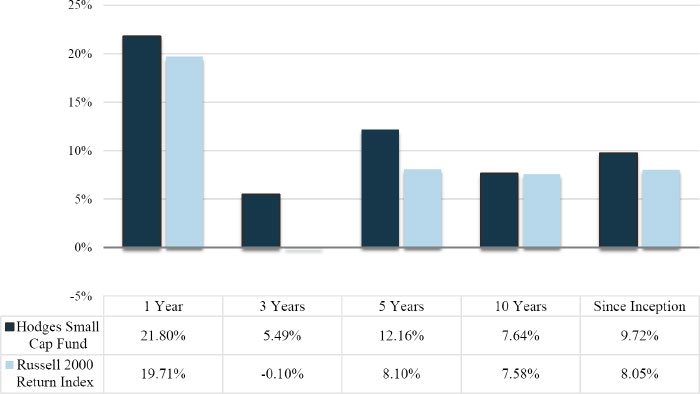

Hodges Small Cap Fund (HDPSX)

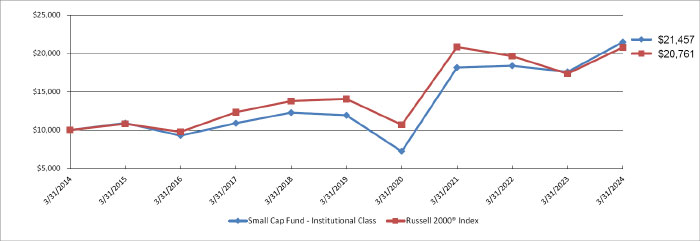

The Small Cap Fund’s one-year performance as of March 31, 2024, amounted to a gain of 21.80% compared to 19.71% for the Russell 2000 Index during the same period. The Fund’s active return above the benchmark in the most recent quarter was more than 99% attributed to stock selection and less than 1% the result of sector allocation. The leading contributors to performance in the recent quarter included Eagle Materials Inc (EXP), SM Energy (SM), Taylor Morrison Home Corp (TMHC), and Encore Wire (WIRE). Although small-cap stocks underperformed large-cap stocks during the recent quarter, we still consider the current risk/reward for holding quality small-cap stocks attractive. While small-cap stocks tend to experience greater volatility during market turmoil, we expect this segment to generate above-average relative risk-adjusted returns over the long term.

The Hodges Small Cap Fund remains well diversified across industrials, transportation, healthcare, technology, and consumer-related names, which we expect to contribute to the Fund’s long-term performance. The Fund recently took profits in several stocks that appeared overvalued relative to their underlying fundamentals and established new positions with an attractive risk/reward profile. The Fund had a total of 51 positions on March 31, 2024. The top ten holdings amounted to 36.84% of the Fund’s holdings and included Matador Resources (MTDR), Encore Wire Corp (WIRE), Eagle Materials Inc (EXP), Cleveland-Cliffs Inc (CLF), Shoe Carnival Inc (SCVL), Taylor Morrison Home Corp (TMHC), Texas Pacific Land Corp (TPL), On Holding (ONON), Permian Resources (PR), and Topgolf Callaway Brands (MODG).

Hodges Small Cap Fund vs Russell 2000 Return Index

As of 03/31/2024

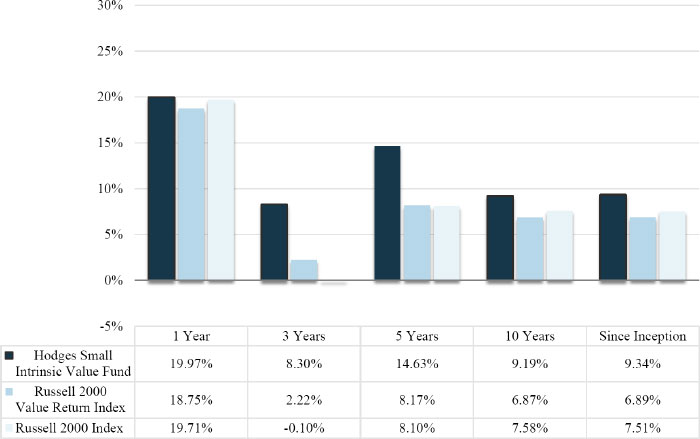

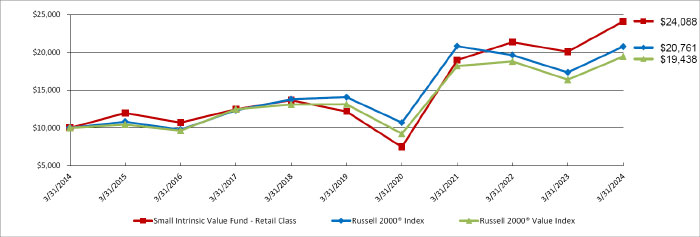

Hodges Small Intrinsic Value Fund (HDSVX)

The Fund’s one-year return for the fiscal year ending March 31, 2024, amounted to a 19.97% increase compared to 18.75% for the Russell 2000 Value Index. Recent outperformance relative to the benchmark was again entirely attributed to stock selection. Although a broad number of holdings contributed to the strategy’s relative performance, we believe it is also worth noting that the top three stocks that contributed to performance in the first quarter were also the top three stocks in terms of weighting to the portfolio. The number of positions held in the Fund amounted to 50 holdings. On March 31, 2024, the top holdings represented 35.83% of the Fund’s holdings. They included Eagle Materials Inc (EXP), Shoe Carnival Inc (SCVL), SunOpta (STKL), Triumph Financial (TFIN), Ethan Allen Interiors Inc (ETD), Aviat Networks (AVNW), Cleveland-Cliffs Inc (CLF), Banc of California (BANC), and Taylor Morrison Home Corp (TMHC).

Hodges Small Intrinsic Value Fund vs

Russell 2000 Value Return Index & Russell 2000 Index

As of 03/31/2024

Inception: 12/26/2013 Annualized

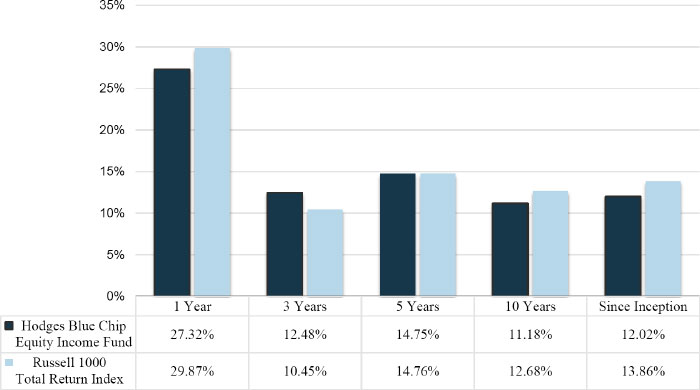

Hodges Blue Chip Equity Income Fund (HDPBX)

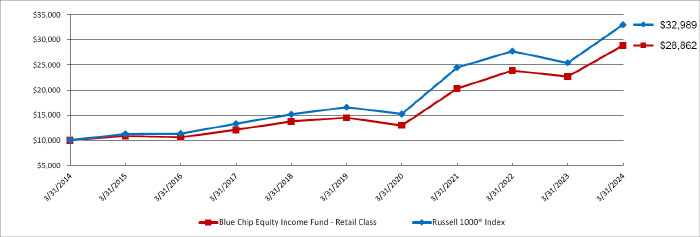

The Hodges Blue Chip Equity Income Fund experienced a one-year return of 27.32% compared to 29.87% for the Russell 1000 Total Return Index. Over the past twelve months, negative relative performance was attributed to underperformance among a handful of energy, consumer, and technology stocks. We believe the current investment landscape offers ample opportunities among high-quality, dividend-paying stocks with solid upside potential. We expect underleveraged balance sheets and corporate profits across most blue-chip stocks to support stable dividends over the next several years. The Blue Chip Equity Income Fund remains well-diversified in companies that we believe can generate above-average income and total returns on a risk-adjusted basis. The number of positions held in the Fund on March 31, 2024 was 28. The top ten holdings at the end of the quarter represented 46.42% of the Fund’s holdings and included Microsoft Corp (MSFT), Nvidia (NVDA), Apple Inc (AAPL), Goldman Sachs Group Inc (GS), Costco Wholesale (COST), JP Morgan (JPM), Exxon Mobil (XOM), Deere & Co (DE), Taiwan Semiconductor (TSM), and Walmart Inc (WMT).

Hodges Blue Chip Equity Income Fund vs

Russell 1000 Total Return Index

As of 03/31/2024

In conclusion, we remain optimistic regarding the long-term investment opportunities surrounding the Hodges Mutual Funds. By offering four distinct mutual fund strategies covering most segments of the domestic equity market, we can serve most financial advisors and individual investors’ diverse needs. Moreover, our entire investment team is highly committed to rigorously studying companies, meeting with management teams, and observing trends to navigate today’s ever-changing financial markets. Feel free to contact us directly if we can address any specific questions.

The above discussion is based on the opinions of Eric Marshall, CFA, and is subject to change. It is not intended to be a forecast of future events, a guarantee of future results, and is not a recommendation to buy or sell any security. The Hodges Funds ’ portfolio composition and company ownership are subject to daily change.

The Fund’s investment objectives, risks, charges, and expenses must be considered carefully before investing. The statutory and summary prospectuses contain this and other important information about the Hodges Funds, and it may be obtained by calling 866-811-0224, or visiting hodgescapital.com/mutual-funds. Read it carefully before investing.

Mutual fund investing involves risk. Principal loss is possible. Investments in foreign securities involve greater volatility, political, economic, and currency risks, and differences in accounting methods. These risks are greater for investments in emerging markets. Options and future contracts have the risks of unlimited losses of the underlying holdings due to unanticipated market movements and failure to correctly predict the direction of securities prices, interest rates and currency exchange rates. These risks may be greater than risks associated with more traditional investments. Short sales of securities involve the risk that losses may exceed the original amount invested. Investments in debt securities typically decrease in value when interest rates rise.

This risk is usually greater for longer term debt securities. Investments in small and medium capitalization companies involve additional risks such as limited liquidity and greater volatility. Non-diversified funds are more exposed to individual stock volatility than a diversified fund. Investments in companies that demonstrate special situations or turnarounds, meaning companies that have experienced significant business problems but are believed to have favorable prospects for recovery, involve greater risk.

Value investing carries the risk that the market will not recognize a security’s inherent value for a long time, or that a stock judged to be undervalued may be appropriately priced or overvalued.

Diversification does not assure a profit or protect against a loss in a declining market.

Fund holdings and/or sector allocations are subject to change at any time and are not recommendations to buy or sell any security.

Investment performance reflects fee waivers in effect. In the absence of such waivers, total return would be reduced.

The S&P 500 Index is a broad-based unmanaged index of 500 stocks that is widely recognized as representative of the equity market in general. The Russell 1000 Total Return Index is a subset of the Russell 3000 Index and consists of the 1,000 largest companies comprising over 90% of the total market capitalization of all listed stocks. The Russell 2000 Index consists of the smallest 2,000 companies in a group of 3,000 U.S. companies in the Russell 3000 Index, as ranked by market capitalization. The Russell 2500 Index consists of the smallest 2,500 companies in a group of 3,000 U.S. companies in the Russell 3000 Index, as ranked by market capitalization. The Russell 3000 Index is a stock index consisting of the 3000 largest publicly listed companies, representing about 98% of the total capitalization of the entire U.S. stock market. You cannot invest directly in an index. The Russell 2000 Value Index measures the performance of the small-cap value segment of the U.S. equity universe. It includes those Russell 2000 companies with lower price-to-book ratios and lower forecasted growth values. The Russell 2000 Value Index is constructed to provide a comprehensive and unbiased barometer for the small-cap value segment. The Index is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true small-cap opportunity set and that the represented companies continue to reflect value characteristics.

Cash Flow: A revenue or expense stream that changes a cash account over a given period.

Price/earnings (P/E): The most common measure of how expensive a stock is.

Earnings Growth is not a measure of the Fund’s future performance.

Hodges Capital Management is the Advisor to the Hodges Funds.

The Hodges Funds are distributed by Northern Lights Distributors, LLC.

| HODGES CAPITAL MANAGEMENT 2905 Maple Avenue • Dallas, Texas 75201 • 888-878-4426 • www.hodgescapital.com |

| Copyright © 2024 Hodges Capital Management. All rights reserved. 03/31/2024 |

| HODGES FUND |

| PORTFOLIO REVIEW (Unaudited) |

| March 31, 2024 |

The Fund’s performance figures* for the periods ended March 31, 2024, compared to its benchmark:

| | | Annualized |

| | | | | | Since Inception |

| | One Year | Three Year | Five Year | Ten Year | (10/9/92) |

| Hodges Fund - Retail Class | 33.52% | 6.29% | 12.78% | 8.12% | 9.87% |

| S&P 500® Index** | 29.88% | 11.49% | 15.05% | 12.96% | 10.64% |

Comparison of the Change in Value of a $10,000 Investment

| * | The performance data quoted here represents past performance. The performance comparison includes reinvestment of all dividends and capital gain distributions, if any. Current performance may be lower or higher than the performance data quoted above. Past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares. The Fund’s total annual operating expenses are 1.35% for Retail Class shares per the September 25, 2023, prospectus. After fee waivers, the Fund’s total annual operating expenses are 1.18% for Retail Class shares. For performance information current to the most recent month-end, please call toll-free 1-866-811-0224. |

| ** | The S&P 500® Index is a widely accepted, unmanaged index of U.S. stock market performance which does not take into account charges, fees and other expenses. Investors cannot invest directly in an index. |

| Sector Holdings as of March 31, 2024 (as a percentage of net assets) | | % of Net Assets | |

| Metals & Mining | | | 13.8 | % |

| Oil & Gas Producers | | | 12.1 | % |

| Internet Media & Services | | | 12.1 | % |

| Leisure Facilities & Services | | | 10.7 | % |

| Semiconductors | | | 9.9 | % |

| Call Options Purchased | | | 7.0 | % |

| Software | | | 6.2 | % |

| Banking | | | 3.9 | % |

| Real Estate Investment Trusts | | | 3.7 | % |

| Biotechnology & Pharmaceuticals | | | 3.6 | % |

| Other1 | | | 16.4 | % |

| Other/Cash Equivalents | | | 0.6 | % |

| | | | 100.0 | % |

| 1 | Other represents less than 3.6% weightings in the following categories: Apparel & Textile Products, Construction Materials, E-Commerce Discretionary, Engineering & Construction, Food, Leisure Products, Machinery and Technology Services. |

Please refer to the Schedule of Investments in this annual report for a detailed analysis of the Fund’s holdings.

| SMALL CAP FUND |

| PORTFOLIO REVIEW (Unaudited) |

| March 31, 2024 |

The Fund’s performance figures* for the periods ended March 31, 2024, compared to its benchmark:

| | | | | Annualized | | |

| | | | | | Since Inception | Since Inception |

| | One Year | Three Year | Five Year | Ten Year | 12/18/2007 | 12/12/2008 |

| Small Cap Fund - Retail Class | 21.80% | 5.49% | 12.16% | 7.64% | 9.72% | N/A |

| Small Cap Fund - Institutional Class | 22.07% | 5.75% | 12.45% | 7.93% | N/A | 15.20% |

| Russell 2000® Index** | 19.71% | (0.10)% | 8.10% | 7.58% | 8.05% | 11.92% |

Comparison of the Change in Value of a $10,000 Investment

| * | The performance data quoted here represents past performance. The performance comparison includes reinvestment of all dividends and capital gain distributions, if any. Current performance may be lower or higher than the performance data quoted above. Past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares. The Fund’s total annual operating expenses are 1.40% for Retail Class shares per the September 25, 2023, prospectus. For performance information current to the most recent month-end, please call toll-free 1-866-811-0224. |

| ** | The Russell 2000® Index is a stock market index that measures the performance of the largest 2,000 small-cap companies in the United States. Investors cannot invest directly in an index. |

| Sector Holdings as of March 31, 2024 (as a percentage of net assets) | | % of Net Assets | |

| Oil & Gas Producers | | | 11.7 | % |

| Retail - Discretionary | | | 9.6 | % |

| Banking | | | 8.5 | % |

| Metals & Mining | | | 8.4 | % |

| Software | | | 6.4 | % |

| Leisure Facilities & Services | | | 5.9 | % |

| Food | | | 5.9 | % |

| Leisure Products | | | 5.1 | % |

| Transportation & Logistics | | | 4.6 | % |

| Construction Materials | | | 4.3 | % |

| Other1 | | | 29.8 | % |

| Liabilities in Excess of Other Assets | | | (0.2 | )% |

| | | | 100.0 | % |

| 1 | Other represents less than 4.3% weightings in the following categories: Aerospace & Defense, Apparel & Textile Products, Asset Management, Biotechnology & Pharmaceuticals, Containers & Packaging, Electrical Equipment, Home Construction, Machinery, Real Estate Investment Trust, Semiconductors, Specialty Finance, Steel, Technology Hardware and Technology Services. |

Please refer to the Schedule of Investments in this annual report for a detailed analysis of the Fund’s holdings.

| SMALL INTRINSIC VALUE FUND |

| PORTFOLIO REVIEW (Unaudited) |

| March 31, 2024 |

The Fund’s performance figures* for the periods ended March 31, 2024, compared to its benchmark:

| | | Annualized |

| | One Year | Three Year | Five Year | Ten Year | Since Inception |

| Small Intrinsic Value Fund - Retail Class | 19.97% | 8.30% | 14.63% | 9.19% | 9.34% |

| Russell 2000® Index** | 19.71% | (0.10)% | 8.10% | 7.58% | 7.51% |

| Russell 2000® Value Index*** | 18.75% | 2.22% | 8.17% | 6.87% | 6.89% |

Comparison of the Change in Value of a $10,000 Investment

| * | The performance data quoted here represents past performance. The performance comparison includes reinvestment of all dividends and capital gain distributions, if any. Current performance may be lower or higher than the performance data quoted above. Past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares. The Fund’s total annual operating expenses are 1.87% for Retail Class shares per the September 25, 2023, prospectus. After fee waivers, the Fund’s total annual operating expenses are 1.29% for Retail Class shares. For performance information current to the most recent month-end, please call toll-free 1-866-811-0224. |

| ** | The Russell 2000® Index is a stock market index that measures the performance of the largest 2,000 small-cap companies in the United States. Investors cannot invest directly in an index. |

| ** | The Russell 2000® Value Index is a stock market index that measures the performance of the largest 2,000 small-cap companies in the United States. This index focuses on companies with lower forecasted growth values compared to the Russell 2000® Index. Investors cannot invest directly in an index. |

| Sector Holdings as of March 31, 2024 (as a percentage of net assets) | | % of Net Assets | |

| Banking | | | 17.3 | % |

| Retail - Discretionary | | | 11.7 | % |

| Metals & Mining | | | 5.2 | % |

| Food | | | 5.2 | % |

| Oil & Gas Producers | | | 4.7 | % |

| Semiconductors | | | 4.7 | % |

| Leisure Products | | | 4.6 | % |

| Construction Materials | | | 4.4 | % |

| Oil & Gas Services & Equipment | | | 4.3 | % |

| Technology Hardware | | | 4.2 | % |

| Other1 | | | 27.9 | % |

| Other/Cash Equivalents | | | 5.8 | % |

| | | | 100.0 | % |

| 1 | Other represents less than 4.2% weightings in the following categories: Biotechnology & Pharmaceuticals, Containers & Packaging, E-Commerce Discretionary, Electrical Equipment, Engineering & Construction, Home Construction, Insurance, Leisure Facilities & Services, Machinery, Real Estate Owners & Developers, Retail - Consumer Staples, Steel, Technology Services, Transportation & Logistics, Transportation Equipment and Wholesale - Consumer Staples. |

Please refer to the Schedule of Investments in this annual report for a detailed analysis of the Fund’s holdings.

| BLUE CHIP EQUITY INCOME FUND |

| PORTFOLIO REVIEW (Unaudited) |

| March 31, 2024 |

The Fund’s performance figures* for the periods ended March 31, 2024, compared to its benchmark:

| | | | Annualized | |

| | One Year | Three Year | Five Year | Ten Year | Since Inception |

| Blue Chip Equity Income Fund - Retail Class | 27.32% | 12.48% | 14.75% | 11.18% | 12.02% |

| Russell 1000® Index** | 29.87% | 10.45% | 14.76% | 12.68% | 13.86% |

Comparison of the Change in Value of a $10,000 Investment

| * | The performance data quoted here represents past performance. The performance comparison includes reinvestment of all dividends and capital gain distributions, if any. Current performance may be lower or higher than the performance data quoted above. Past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares. The Fund’s total annual operating expenses are 1.58% for Retail Class shares per the September 25, 2023, prospectus. After fee waivers, the Fund’s total annual operating expenses are 1.30% for Retail Class shares. For performance information current to the most recent month-end, please call toll-free 1-866-811-0224. |

| ** | The Russell 1000® Index is a market index that tracks the 1000 largest companies by market capitalization in the United States. Investors cannot invest directly in an index. |

| Sector Holdings as of March 31, 2024 (as a percentage of net assets) | | % of Net Assets | |

| Oil & Gas Producers | | | 10.2 | % |

| Semiconductors | | | 9.9 | % |

| Retail - Consumer Staples | | | 8.4 | % |

| Institutional Financial Services | | | 8.0 | % |

| Biotechnology & Pharmaceuticals | | | 7.9 | % |

| Banking | | | 7.6 | % |

| Machinery | | | 7.5 | % |

| Transportation & Logistics | | | 6.7 | % |

| Software | | | 6.1 | % |

| Retail - Discretionary | | | 5.3 | % |

| Other1 | | | 20.7 | % |

| Other/Cash Equivalents | | | 1.7 | % |

| | | | 100.0 | % |

| 1 | Other represents less than 5.3% weightings in the following categories: Aerospace & Defense, Beverages, E-Commerce Discretionary, Insurance, Leisure Facilities & Services and Technology Hardware. |

Please refer to the Schedule of Investments in this annual report for a detailed analysis of the Fund’s holdings.

| HODGES FUND |

| SCHEDULE OF INVESTMENTS |

| March 31, 2024 |

| Shares | | | | | Fair Value | |

| | | | | COMMON STOCKS — 92.4% | | | | |

| | | | | APPAREL & TEXTILE PRODUCTS - 3.3% | | | | |

| | 175,000 | | | On Holding A.G.(a) | | $ | 6,191,500 | |

| | | | | | | | | |

| | | | | BANKING - 3.9% | | | | |

| | 300,000 | | | Banc of California, Inc. | | | 4,563,000 | |

| | 180,000 | | | First Horizon Corporation | | | 2,772,000 | |

| | | | | | | | 7,335,000 | |

| | | | | BIOTECHNOLOGY & PHARMACEUTICALS - 3.6% | | | | |

| | 400,000 | | | Ironwood Pharmaceuticals, Inc.(a) | | | 3,484,000 | |

| | 25,000 | | | Novo Nordisk A/S - ADR | | | 3,210,000 | |

| | | | | | | | 6,694,000 | |

| | | | | CONSTRUCTION MATERIALS - 2.2% | | | | |

| | 15,000 | | | Eagle Materials, Inc. | | | 4,076,250 | |

| | | | | | | | | |

| | | | | E-COMMERCE DISCRETIONARY - 2.6% | | | | |

| | 135,000 | | | Beyond, Inc.(a) | | | 4,847,850 | |

| | | | | | | | | |

| | | | | ENGINEERING & CONSTRUCTION - 1.4% | | | | |

| | 30,000 | | | Arcosa, Inc. | | | 2,575,800 | |

| | | | | | | | | |

| | | | | FOOD - 1.1% | | | | |

| | 35,000 | | | Tyson Foods, Inc., Class A | | | 2,055,550 | |

| | | | | | | | | |

| | | | | INTERNET MEDIA & SERVICES - 12.1% | | | | |

| | 40,000 | | | Airbnb, Inc., Class A(a) | | | 6,598,400 | |

| | 75,000 | | | Maplebear, Inc.(a) | | | 2,796,750 | |

| | 170,000 | | | Uber Technologies, Inc.(a) | | | 13,088,300 | |

| | | | | | | | 22,483,450 | |

| | | | | LEISURE FACILITIES & SERVICES - 10.7% | | | | |

| | 200,000 | | | DraftKings, Inc., Class A(a) | | | 9,082,000 | |

| | 250,000 | | | Norwegian Cruise Line Holdings Ltd.(a) | | | 5,232,500 | |

| | 55,000 | | | Wynn Resorts Ltd. | | | 5,622,650 | |

| | | | | | | | 19,937,150 | |

| | | | | | | | | |

See accompanying notes to financial statements.

| HODGES FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| March 31, 2024 |

| Shares | | | | | Fair Value | |

| | | | | COMMON STOCKS — 92.4% (Continued) | | | | |

| | | | | LEISURE PRODUCTS - 1.1% | | | | |

| | 125,000 | | | Topgolf Callaway Brands Corporation(a) | | $ | 2,021,250 | |

| | | | | | | | | |

| | | | | MACHINERY - 2.4% | | | | |

| | 100,000 | | | Symbotic, Inc.(a) | | | 4,500,000 | |

| | | | | | | | | |

| | | | | METALS & MINING - 13.8% | | | | |

| | 300,000 | | | Cleveland-Cliffs, Inc.(a) | | | 6,822,000 | |

| | 45,000 | | | Encore Wire Corporation | | | 11,825,100 | |

| | 150,000 | | | Freeport-McMoRan, Inc. | | | 7,053,000 | |

| | | | | | | | 25,700,100 | |

| | | | | OIL & GAS PRODUCERS - 12.1% | | | | |

| | 45,000 | | | Chesapeake Energy Corporation | | | 3,997,350 | |

| | 200,000 | | | Matador Resources Company | | | 13,354,000 | |

| | 300,000 | | | Permian Resources Corporation | | | 5,298,000 | |

| | | | | | | | 22,649,350 | |

| | | | | REAL ESTATE INVESTMENT TRUST - 3.7% | | | | |

| | 12,000 | | | Texas Pacific Land Corporation | | | 6,942,120 | |

| | | | | | | | | |

| | | | | SEMICONDUCTORS - 9.9% | | | | |

| | 45,000 | | | Coherent Corporation(a) | | | 2,727,900 | |

| | 40,000 | | | Micron Technology, Inc. | | | 4,715,600 | |

| | 6,000 | | | NVIDIA Corporation | | | 5,421,360 | |

| | 75,000 | | | ON Semiconductor Corporation(a) | | | 5,516,250 | |

| | | | | | | | 18,381,110 | |

| | | | | SOFTWARE - 6.2% | | | | |

| | 175,000 | | | DoubleVerify Holdings, Inc.(a) | | | 6,153,000 | |

| | 115,000 | | | Evolent Health, Inc., Class A(a) | | | 3,770,850 | |

| | 519,077 | | | Upland Software, Inc.(a) | | | 1,603,948 | |

| | | | | | | | 11,527,798 | |

| | | | | | | | | |

See accompanying notes to financial statements.

| HODGES FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| March 31, 2024 |

| Shares | | | | | | | | | | | | | | | | | Fair Value | |

| | | | | COMMON STOCKS — 92.4% (Continued) | | | | | | |

| | | | | TECHNOLOGY SERVICES - 2.3% | | | | | | |

| | 65,000 | | | Shift4 Payments, Inc.(a) | | | | $ | 4,294,550 | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | TOTAL COMMON STOCKS (Cost $104,583,905) | | | | | 172,212,828 | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | SHORT-TERM INVESTMENT — 0.4% | | | | | | |

| | | | | MONEY MARKET FUND - 0.4% | | | | | | |

| | 759,339 | | | First American Treasury Obligations Fund, Class X, 5.22% (Cost $759,339) (b) | | | | | 759,339 | |

| | | | | | | | | | | |

| Contracts(c) | | | | | Broker/Counterparty | | Expiration

Date | | Exercise

Price | | | Notional

Value | | | | |

| | | | | CALL OPTIONS PURCHASED - 7.0% | | | | | | | | | | | | |

| | | | | EQUITY OPTIONS PURCHASED - 7.0% | | | | | | | | | | | | |

| | 500 | | | Alphabet, Inc. | | WFC | | 05/17/2024 | | $ | 125 | | | $ | 7,613,000 | | | | 1,450,000 | |

| | 35 | | | Booking Holdings, Inc. | | WFC | | 04/19/2024 | | | 2,750 | | | | 12,697,580 | | | | 3,104,500 | |

| | 250 | | | CyberArk Software Ltd. | | WFC | | 04/19/2024 | | | 140 | | | | 6,640,750 | | | | 3,157,500 | |

| | 500 | | | JPMorgan Chase & Company | | WFC | | 05/17/2024 | | | 135 | | | | 10,015,000 | | | | 3,271,250 | |

| | 500 | | | Owens Corning | | WFC | | 05/17/2024 | | | 125 | | | | 8,340,000 | | | | 2,147,500 | |

| | | | | TOTAL CALL OPTIONS PURCHASED (Cost - $7,353,848) | | | | | | | | | | | 13,130,750 | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | TOTAL INVESTMENTS - 99.8% (Cost $112,697,092) | | | | | | | | | $ | 186,102,917 | |

| | | | | OTHER ASSETS IN EXCESS OF LIABILITIES - 0.2% | | | | | | | | | | 408,582 | |

| | | | | NET ASSETS - 100.0% | | | | | | | | | $ | 186,511,499 | |

| ADR | - American Depositary Receipt |

| | |

| A/S | - Anonim Sirketi |

| | |

| Ltd. | - Limited Company |

| | |

| REIT | - Real Estate Investment Trust |

| | |

| WFC | - Wells Fargo & Co. |

| (a) | Non-income producing security. |

| | |

| (b) | Rate disclosed is the seven day effective yield as of March 31, 2024. |

| | |

| (c) | Each option contract allows the holder of the option to purchase or sell 100 shares of the underlying security. |

See accompanying notes to financial statements.

| HODGES SMALL CAP FUND |

| SCHEDULE OF INVESTMENTS |

| March 31, 2024 |

| Shares | | | | | Fair Value | |

| | | | | COMMON STOCKS — 100.2% | | | | |

| | | | | AEROSPACE & DEFENSE - 1.8% | | | | |

| | 185,000 | | | Kratos Defense & Security Solutions, Inc.(a) | | $ | 3,400,300 | |

| | | | | | | | | |

| | | | | APPAREL & TEXTILE PRODUCTS - 2.8% | | | | |

| | 150,000 | | | On Holding A.G.(a) | | | 5,307,000 | |

| | | | | | | | | |

| | | | | ASSET MANAGEMENT - 0.6% | | | | |

| | 30,000 | | | Assetmark Financial Holdings, Inc.(a) | | | 1,062,300 | |

| | | | | | | | | |

| | | | | BANKING - 8.5% | | | | |

| | 250,000 | | | Banc of California, Inc. | | | 3,802,500 | |

| | 120,000 | | | Hilltop Holdings, Inc. | | | 3,758,400 | |

| | 80,000 | | | Independent Bank Group, Inc. | | | 3,652,000 | |

| | 50,000 | | | Prosperity Bancshares, Inc. | | | 3,289,000 | |

| | 25,000 | | | Texas Capital Bancshares, Inc.(a) | | | 1,538,750 | |

| | | | | | | | 16,040,650 | |

| | | | | BIOTECHNOLOGY & PHARMACEUTICALS - 2.2% | | | | |

| | 100,000 | | | Halozyme Therapeutics, Inc.(a) | | | 4,068,000 | |

| | | | | | | | | |

| | | | | CONSTRUCTION MATERIALS - 4.3% | | | | |

| | 30,000 | | | Eagle Materials, Inc. | | | 8,152,500 | |

| | | | | | | | | |

| | | | | CONTAINERS & PACKAGING - 2.3% | | | | |

| | 150,000 | | | Graphic Packaging Holding Company | | | 4,377,000 | |

| | | | | | | | | |

| | | | | ELECTRICAL EQUIPMENT - 1.9% | | | | |

| | 165,000 | | | Kimball Electronics, Inc.(a) | | | 3,572,250 | |

| | | | | | | | | |

| | | | | FOOD - 5.9% | | | | |

| | 60,000 | | | BellRing Brands, Inc.(a) | | | 3,541,800 | |

| | 40,000 | | | Cal-Maine Foods, Inc. | | | 2,354,000 | |

| | 750,000 | | | SunOpta, Inc.(a) | | | 5,152,500 | |

| | | | | | | | 11,048,300 | |

| | | | | | | | | |

See accompanying notes to financial statements.

| HODGES SMALL CAP FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| March 31, 2024 |

| Shares | | | | | Fair Value | |

| | | | | COMMON STOCKS — 100.2% (Continued) | | | | |

| | | | | HOME CONSTRUCTION - 3.2% | | | | |

| | 95,000 | | | Taylor Morrison Home Corporation(a) | | $ | 5,906,150 | |

| | | | | | | | | |

| | | | | LEISURE FACILITIES & SERVICES - 5.9% | | | | |

| | 210,000 | | | Cinemark Holdings, Inc.(a) | | | 3,773,700 | |

| | 200,000 | | | Norwegian Cruise Line Holdings Ltd.(a) | | | 4,186,000 | |

| | 20,000 | | | Texas Roadhouse, Inc. | | | 3,089,400 | |

| | | | | | | | 11,049,100 | |

| | | | | LEISURE PRODUCTS - 5.1% | | | | |

| | 25,000 | | | Brunswick Corporation | | | 2,413,000 | |

| | 325,000 | | | Topgolf Callaway Brands Corporation(a) | | | 5,255,250 | |

| | 60,000 | | | Vista Outdoor, Inc.(a) | | | 1,966,800 | |

| | | | | | | | 9,635,050 | |

| | | | | MACHINERY - 1.3% | | | | |

| | 11,000 | | | Alamo Group, Inc. | | | 2,511,630 | |

| | | | | | | | | |

| | | | | METALS & MINING - 8.4% | | | | |

| | 325,000 | | | Cleveland-Cliffs, Inc.(a) | | | 7,390,500 | |

| | 32,000 | | | Encore Wire Corporation | | | 8,408,960 | |

| | | | | | | | 15,799,460 | |

| | | | | OIL & GAS PRODUCERS - 11.7% | | | | |

| | 175,000 | | | Matador Resources Company | | | 11,684,750 | |

| | 300,000 | | | Permian Resources Corporation | | | 5,298,000 | |

| | 100,000 | | | SM Energy Company | | | 4,985,000 | |

| | | | | | | | 21,967,750 | |

| | | | | REAL ESTATE INVESTMENT TRUST - 3.1% | | | | |

| | 10,200 | | | Texas Pacific Land Corporation | | | 5,900,802 | |

| | | | | | | | | |

| | | | | RETAIL - DISCRETIONARY - 9.6% | | | | |

| | 50,000 | | | Academy Sports & Outdoors, Inc. | | | 3,377,000 | |

| | 90,000 | | | Ethan Allen Interiors, Inc. | | | 3,111,300 | |

| | 10,000 | | | Group 1 Automotive, Inc. | | | 2,922,300 | |

| | 7,500 | | | RH(a) | | | 2,611,950 | |

| | 165,000 | | | Shoe Carnival, Inc. | | | 6,045,600 | |

| | | | | | | | 18,068,150 | |

| | | | | | | | | |

See accompanying notes to financial statements.

| HODGES SMALL CAP FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| March 31, 2024 |

| Shares | | | | | Fair Value | |

| | | | | COMMON STOCKS — 100.2% (Continued) | | | | |

| | | | | SEMICONDUCTORS - 2.5% | | | | |

| | 30,000 | | | Coherent Corporation(a) | | $ | 1,818,600 | |

| | 40,000 | | | Diodes, Inc.(a) | | | 2,820,000 | |

| | | | | | | | 4,638,600 | |

| | | | | SOFTWARE - 6.4% | | | | |

| | 80,000 | | | Alkami Technology, Inc.(a) | | | 1,965,600 | |

| | 85,000 | | | Digi International, Inc.(a) | | | 2,714,050 | |

| | 90,000 | | | Evolent Health, Inc., Class A(a) | | | 2,951,100 | |

| | 41,628 | | | Varonis Systems, Inc.(a) | | | 1,963,593 | |

| | 220,000 | | | Zeta Global Holdings Corporation(a) | | | 2,404,600 | |

| | | | | | | | 11,998,943 | |

| | | | | SPECIALTY FINANCE - 1.0% | | | | |

| | 15,000 | | | FirstCash Holdings, Inc. | | | 1,913,100 | |

| | | | | | | | | |

| | | | | STEEL - 3.5% | | | | |

| | 50,000 | | | Carpenter Technology Corporation | | | 3,571,000 | |

| | 50,000 | | | Commercial Metals Company | | | 2,938,500 | |

| | | | | | | | 6,509,500 | |

| | | | | TECHNOLOGY HARDWARE - 2.4% | | | | |

| | 95,000 | | | Knowles Corporation(a) | | | 1,529,500 | |

| | 70,000 | | | NCR Voyix Corporation(a) | | | 884,100 | |

| | 45,000 | | | PAR Technology Corporation(a) | | | 2,041,200 | |

| | | | | | | | 4,454,800 | |

| | | | | TECHNOLOGY SERVICES - 1.2% | | | | |

| | 35,000 | | | Shift4 Payments, Inc.(a) | | | 2,312,450 | |

| | | | | | | | | |

| | | | | TRANSPORTATION & LOGISTICS - 4.6% | | | | |

| | 100,000 | | | Alaska Air Group, Inc.(a) | | | 4,299,000 | |

| | 25,000 | | | Kirby Corporation(a) | | | 2,383,000 | |

| | 125,000 | | | Navigator Holdings Ltd. | | | 1,918,750 | |

| | | | | | | | 8,600,750 | |

| | | | | | | | | |

See accompanying notes to financial statements.

| HODGES SMALL CAP FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| March 31, 2024 |

| Shares | | | | | Fair Value | |

| | | | | TOTAL COMMON STOCKS (Cost $115,577,317) | | $ | 188,294,535 | |

| | | | | | | | | |

| | | | | TOTAL INVESTMENTS - 100.2% (Cost $115,577,317) | | $ | 188,294,535 | |

| | | | | LIABILITIES IN EXCESS OF OTHER ASSETS - (0.2)% | | | (350,974 | ) |

| | | | | NET ASSETS - 100.0% | | $ | 187,943,561 | |

| Ltd. | - Limited Company |

| | |

| REIT | - Real Estate Investment Trust |

| (a) | Non-income producing security. |

See accompanying notes to financial statements.

| HODGES SMALL INTRINSIC VALUE FUND |

| SCHEDULE OF INVESTMENTS |

| March 31, 2024 |

| Shares | | | | | Fair Value | |

| | | | | COMMON STOCKS — 94.2% | | | | |

| | | | | BANKING - 17.3% | | | | |

| | 120,000 | | | Banc of California, Inc. | | $ | 1,825,200 | |

| | 11,000 | | | BancFirst Corporation | | | 968,330 | |

| | 50,000 | | | Hilltop Holdings, Inc. | | | 1,566,000 | |

| | 64,000 | | | Home BancShares, Inc. | | | 1,572,480 | |

| | 28,000 | | | Independent Bank Group, Inc. | | | 1,278,200 | |

| | 27,000 | | | Texas Capital Bancshares, Inc.(a) | | | 1,661,850 | |

| | 26,000 | | | Triumph Financial, Inc.(a) | | | 2,062,320 | |

| | | | | | | | 10,934,380 | |

| | | | | BIOTECHNOLOGY & PHARMACEUTICALS - 2.0% | | | | |

| | 31,200 | | | Halozyme Therapeutics, Inc.(a) | | | 1,269,216 | |

| | | | | | | | | |

| | | | | CONSTRUCTION MATERIALS - 4.4% | | | | |

| | 10,300 | | | Eagle Materials, Inc. | | | 2,799,025 | |

| | | | | | | | | |

| | | | | CONTAINERS & PACKAGING - 0.3% | | | | |

| | 6,800 | | | Myers Industries, Inc. | | | 157,556 | |

| | | | | | | | | |

| | | | | E-COMMERCE DISCRETIONARY - 0.8% | | | | |

| | 182,000 | | | Stitch Fix, Inc., Class A(a) | | | 480,480 | |

| | | | | | | | | |

| | | | | ELECTRICAL EQUIPMENT - 2.1% | | | | |

| | 60,400 | | | Kimball Electronics, Inc.(a) | | | 1,307,660 | |

| | | | | | | | | |

| | | | | ENGINEERING & CONSTRUCTION - 0.9% | | | | |

| | 110,000 | | | Southland Holdings, Inc.(a) | | | 566,500 | |

| | | | | | | | | |

| | | | | FOOD - 5.2% | | | | |

| | 20,600 | | | Cal-Maine Foods, Inc. | | | 1,212,310 | |

| | 302,000 | | | SunOpta, Inc.(a) | | | 2,074,740 | |

| | | | | | | | 3,287,050 | |

| | | | | HOME CONSTRUCTION - 3.8% | | | | |

| | 9,200 | | | Griffon Corporation | | | 674,728 | |

| | 27,500 | | | Taylor Morrison Home Corporation(a) | | | 1,709,675 | |

| | | | | | | | 2,384,403 | |

| | | | | | | | | |

See accompanying notes to financial statements.

| HODGES SMALL INTRINSIC VALUE FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| March 31, 2024 |

| Shares | | | | | Fair Value | |

| | | | | COMMON STOCKS — 94.2% (Continued) | | | | |

| | | | | INSURANCE - 0.9% | | | | |

| | 34,350 | | | Tiptree, Inc. | | $ | 593,568 | |

| | | | | | | | | |

| | | | | LEISURE FACILITIES & SERVICES - 2.0% | | | | |

| | 49,000 | | | Cinemark Holdings, Inc.(a) | | | 880,530 | |

| | 30,400 | | | Potbelly Corporation(a) | | | 368,144 | |

| | | | | | | | 1,248,674 | |

| | | | | LEISURE PRODUCTS - 4.6% | | | | |

| | 17,300 | | | Brunswick Corporation | | | 1,669,796 | |

| | 77,000 | | | Topgolf Callaway Brands Corporation(a) | | | 1,245,090 | |

| | | | | | | | 2,914,886 | |

| | | | | MACHINERY - 3.5% | | | | |

| | 3,000 | | | Alamo Group, Inc. | | | 684,990 | |

| | 38,700 | | | Ichor Holdings Ltd.(a) | | | 1,494,594 | |

| | | | | | | | 2,179,584 | |

| | | | | METALS & MINING - 5.2% | | | | |

| | 83,900 | | | Cleveland-Cliffs, Inc.(a) | | | 1,907,886 | |

| | 5,300 | | | Encore Wire Corporation | | | 1,392,734 | |

| | | | | | | | 3,300,620 | |

| | | | | OIL & GAS PRODUCERS - 4.7% | | | | |

| | 9,200 | | | Chord Energy Corporation | | | 1,639,808 | |

| | 8,400 | | | Gulfport Energy Corporation(a) | | | 1,345,008 | |

| | | | | | | | 2,984,816 | |

| | | | | OIL & GAS SERVICES & EQUIPMENT - 4.3% | | | | |

| | 65,000 | | | Atlas Energy Solutions, Inc. | | | 1,470,300 | |

| | 156,000 | | | ProPetro Holding Corporation(a) | | | 1,260,480 | |

| | | | | | | | 2,730,780 | |

| | | | | REAL ESTATE OWNERS & DEVELOPERS - 1.8% | | | | |

| | 49,000 | | | Stratus Properties, Inc.(a) | | | 1,118,670 | |

| | | | | | | | | |

| | | | | RETAIL - CONSUMER STAPLES - 0.9% | | | | |

| | 8,700 | | | Sprouts Farmers Market, Inc.(a) | | | 560,976 | |

| | | | | | | | | |

| | | | | RETAIL - DISCRETIONARY - 11.7% | | | | |

| | 15,100 | | | Academy Sports & Outdoors, Inc. | | | 1,019,854 | |

| | | | | | | | | |

See accompanying notes to financial statements.

| HODGES SMALL INTRINSIC VALUE FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| March 31, 2024 |

| Shares | | | | | Fair Value | |

| | | | | COMMON STOCKS — 94.2% (Continued) | | | | |

| | | | | RETAIL - DISCRETIONARY - 11.7% (Continued) | | | | |

| | 6,800 | | | Builders FirstSource, Inc.(a) | | $ | 1,418,140 | |

| | 59,600 | | | Ethan Allen Interiors, Inc. | | | 2,060,372 | |

| | 58,000 | | | Shoe Carnival, Inc. | | | 2,125,120 | |

| | 49,000 | | | Sleep Number Corporation(a) | | | 785,470 | |

| | | | | | | | 7,408,956 | |

| | | | | SEMICONDUCTORS - 4.7% | | | | |

| | 11,400 | | | Diodes, Inc.(a) | | | 803,700 | |

| | 28,970 | | | Photronics, Inc.(a) | | | 820,430 | |

| | 40,000 | | | Tower Semiconductor Ltd.(a) | | | 1,338,001 | |

| | | | | | | | 2,962,131 | |

| | | | | STEEL - 2.0% | | | | |

| | 21,565 | | | Commercial Metals Company | | | 1,267,375 | |

| | | | | | | | | |

| | | | | TECHNOLOGY HARDWARE - 4.2% | | | | |

| | 51,530 | | | Aviat Networks, Inc.(a) | | | 1,975,660 | |

| | 53,900 | | | NCR Voyix Corporation(a) | | | 680,757 | |

| | | | | | | | 2,656,417 | |

| | | | | TECHNOLOGY SERVICES - 0.8% | | | | |

| | 150,000 | | | Research Solutions, Inc.(a) | | | 474,000 | |

| | | | | | | | | |

| | | | | TRANSPORTATION & LOGISTICS - 1.8% | | | | |

| | 73,600 | | | Navigator Holdings Ltd. | | | 1,129,760 | |

| | | | | | | | | |

| | | | | TRANSPORTATION EQUIPMENT - 3.2% | | | | |

| | 27,015 | | | Blue Bird Corporation(a) | | | 1,035,755 | |

| | 18,900 | | | Greenbrier Companies, Inc. (The) | | | 984,690 | |

| | | | | | | | 2,020,445 | |

| | | | | WHOLESALE - CONSUMER STAPLES - 1.1% | | | | |

| | 25,000 | | | Calavo Growers, Inc. | | | 695,249 | |

| | | | | | | | | |

| | | | | TOTAL COMMON STOCKS (Cost $47,030,385) | | | 59,433,177 | |

| | | | | | | | | |

See accompanying notes to financial statements.

| HODGES SMALL INTRINSIC VALUE FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| March 31, 2024 |

| Shares | | | | | Expiration Date | | Exercise Price | | | Fair Value | |

| | | | WARRANT — 0.0%(b) | | | | | | | | |

| | | | | ENGINEERING & CONSTRUCTION - 0.0%(b) | | | | | | | | | | |

| | 25,000 | | | Southland Holdings, Inc. (Cost $15,185) | | 09/02/2026 | | $ | 11.50 | | | $ | 11,070 | |

| | | | | | | | | | | | | | | |

| | | | | SHORT-TERM INVESTMENT — 6.8% | | | | | | | | | | |

| | | | | MONEY MARKET FUND - 6.8% | | | | | | | | | | |

| | 4,299,151 | | | First American Treasury Obligations Fund, Class X, 5.22% (Cost $4,299,151)(c) | | | | 4,299,151 | |

| | | | | | | | | | | | | | | |

| | | | | TOTAL INVESTMENTS - 101.0% (Cost $51,344,721) | | | $ | 63,743,398 | |

| | | | | LIABILITIES IN EXCESS OF OTHER ASSETS - (1.0)% | | | | (654,623 | ) |

| | | | | NET ASSETS - 100.0% | | | $ | 63,088,775 | |

| (a) | Non-income producing security. |

| | |

| (b) | Percentage rounds to less than 0.1%. |

| | |

| (c) | Rate disclosed is the seven day effective yield as of March 31,2024. |

See accompanying notes to financial statements.

| HODGES BLUE CHIP EQUITY INCOME FUND |

| SCHEDULE OF INVESTMENTS |

| March 31, 2024 |

| Shares | | | | | Fair Value | |

| | | | | COMMON STOCKS — 98.3% | | | | |

| | | | | AEROSPACE & DEFENSE - 3.3% | | | | |

| | 7,000 | | | Boeing Company (The)(a) | | $ | 1,350,930 | |

| | | | | | | | | |

| | | | | BANKING - 7.6% | | | | |

| | 35,000 | | | Bank of America Corporation | | | 1,327,200 | |

| | 9,000 | | | JPMorgan Chase & Company | | | 1,802,700 | |

| | | | | | | | 3,129,900 | |

| | | | | BEVERAGES - 3.0% | | | | |

| | 7,000 | | | PepsiCo, Inc. | | | 1,225,070 | |

| | | | | | | | | |

| | | | | BIOTECHNOLOGY & PHARMACEUTICALS - 7.9% | | | | |

| | 5,000 | | | AbbVie, Inc. | | | 910,500 | |

| | 10,000 | | | Merck & Company, Inc. | | | 1,319,500 | |

| | 8,000 | | | Novo Nordisk A/S - ADR | | | 1,027,200 | |

| | | | | | | | 3,257,200 | |

| | | | | E-COMMERCE DISCRETIONARY - 3.5% | | | | |

| | 8,000 | | | Amazon.com, Inc.(a) | | | 1,443,040 | |

| | | | | | | | | |

| | | | | INSTITUTIONAL FINANCIAL SERVICES - 8.0% | | | | |

| | 4,500 | | | Goldman Sachs Group, Inc. (The) | | | 1,879,605 | |

| | 15,000 | | | Morgan Stanley | | | 1,412,400 | |

| | | | | | | | 3,292,005 | |

| | | | | INSURANCE - 2.5% | | | | |

| | 2,500 | | | Berkshire Hathaway, Inc., Class B(a) | | | 1,051,300 | |

| | | | | | | | | |

| | | | | LEISURE FACILITIES & SERVICES - 3.4% | | | | |

| | 5,000 | | | McDonald’s Corporation | | | 1,409,750 | |

| | | | | | | | | |

| | | | | MACHINERY - 7.5% | | | | |

| | 4,000 | | | Caterpillar, Inc. | | | 1,465,720 | |

| | 4,000 | | | Deere & Company | | | 1,642,960 | |

| | | | | | | | 3,108,680 | |

| | | | | OIL & GAS PRODUCERS - 10.2% | | | | |

| | 10,000 | | | ConocoPhillips | | | 1,272,800 | |

| | 15,000 | | | Exxon Mobil Corporation | | | 1,743,600 | |

| | | | | | | | | |

See accompanying notes to financial statements.

| HODGES BLUE CHIP EQUITY INCOME FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| March 31, 2024 |

| Shares | | | | | Fair Value | |

| | | | | COMMON STOCKS — 98.3% (Continued) | | | | |

| | | | | OIL & GAS PRODUCERS - 10.2% (Continued) | | | | |

| | 15,000 | | | ONEOK, Inc. | | $ | 1,202,550 | |

| | | | | | | | 4,218,950 | |

| | | | | RETAIL - CONSUMER STAPLES - 8.4% | | | | |

| | 2,500 | | | Costco Wholesale Corporation | | | 1,831,575 | |

| | 27,000 | | | Walmart, Inc. | | | 1,624,590 | |

| | | | | | | | 3,456,165 | |

| | | | | RETAIL - DISCRETIONARY - 5.3% | | | | |

| | 2,750 | | | Home Depot, Inc. (The) | | | 1,054,900 | |

| | 4,500 | | | Lowe’s Companies, Inc. | | | 1,146,285 | |

| | | | | | | | 2,201,185 | |

| | | | | SEMICONDUCTORS - 9.9% | | | | |

| | 2,750 | | | NVIDIA Corporation | | | 2,484,790 | |

| | 12,000 | | | Taiwan Semiconductor Manufacturing Company Ltd. - ADR | | | 1,632,600 | |

| | | | | | | | 4,117,390 | |

| | | | | SOFTWARE - 6.1% | | | | |

| | 6,000 | | | Microsoft Corporation | | | 2,524,320 | |

| | | | | | | | | |

| | | | | TECHNOLOGY HARDWARE - 5.0% | | | | |

| | 12,000 | | | Apple, Inc. | | | 2,057,760 | |

| | | | | | | | | |

| | | | | TRANSPORTATION & LOGISTICS - 6.7% | | | | |

| | 30,000 | | | Delta Air Lines, Inc. | | | 1,436,100 | |

| | 5,500 | | | Union Pacific Corporation | | | 1,352,615 | |

| | | | | | | | 2,788,715 | |

| | | | | | | | | |

| | | | | TOTAL COMMON STOCKS (Cost $24,227,589) | | | 40,632,360 | |

| | | | | | | | | |

See accompanying notes to financial statements.

| HODGES BLUE CHIP EQUITY INCOME FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| March 31, 2024 |

| Shares | | | | | Fair Value | |

| | | | | SHORT-TERM INVESTMENT — 1.8% | | | | |

| | | | | MONEY MARKET FUND - 1.8% | | | | |

| | 761,983 | | | First American Treasury Obligations Fund, Class X, 5.22% (Cost $761,983)(b) | | $ | 761,983 | |

| | | | | | | | | |

| | | | | TOTAL INVESTMENTS - 100.1% (Cost $24,989,572) | | $ | 41,394,343 | |

| | | | | LIABILITIES IN EXCESS OF OTHER ASSETS - (0.1)% | | | (52,974 | ) |

| | | | | NET ASSETS - 100.0% | | $ | 41,341,369 | |

| ADR | - American Depositary Receipt |

| (a) | Non-income producing security. |

| (b) | Rate disclosed is the seven day effective yield as of March 31, 2024. |

See accompanying notes to financial statements.

| HODGES MUTUAL FUNDS |

| STATEMENTS OF ASSETS AND LIABILITIES |

| March 31, 2024 |

| | | | | | | | | Small Intrinsic | | | Blue Chip Equity | |

| | | Hodges Fund | | | Small Cap Fund | | | Value Fund | | | Income Fund | |

| ASSETS: | | | | | | | | | | | | | | | | |

| Investments in securities, at cost | | $ | 112,697,092 | | | $ | 115,577,317 | | | $ | 51,344,721 | | | $ | 24,989,572 | |

| Investments in securities, at value | | | 186,102,917 | | | | 188,294,535 | | | | 63,743,398 | | | | 41,394,343 | |

| Cash | | | — | | | | — | | | | — | | | | 7,150 | |

| Receivable for fund shares sold | | | 24,124 | | | | 2,510 | | | | 52,901 | | | | 382 | |

| Dividends and interest receivable | | | 115,077 | | | | 92,836 | | | | 45,511 | | | | 45,039 | |

| Receivable for securities sold | | | 1,414,692 | | | | 107,690 | | | | — | | | | 365,342 | |

| Other assets | | | — | | | | 18,109 | | | | 6,025 | | | | 2,383 | |

| Total Assets | | | 187,656,810 | | | | 188,515,680 | | | | 63,847,835 | | | | 41,814,639 | |

| | | | | | | | | | | | | | | | | |

| LIABILITIES: | | | | | | | | | | | | | | | | |

| Due to custodian | | | — | | | | 180,517 | | | | — | | | | — | |

| Payable for fund shares redeemed | | | 23,620 | | | | 155,595 | | | | 25,546 | | | | 3,448 | |

| Payable for securities purchased | | | 915,092 | | | | — | | | | 657,328 | | | | 384,018 | |

| Accrued advisory fee | | | 118,915 | | | | 160,635 | | | | 27,219 | | | | 34,283 | |

| Payable to related parties | | | 11,103 | | | | 20,037 | | | | 6,084 | | | | 16,700 | |

| Distribution (12b-1) fees payable | | | 38,312 | | | | 29,732 | | | | 12,913 | | | | 8,520 | |

| Other accrued expenses | | | 38,269 | | | | 25,603 | | | | 29,970 | | | | 26,301 | |

| Total Liabilities | | | 1,145,311 | | | | 572,119 | | | | 759,060 | | | | 473,270 | |

| NET ASSETS | | $ | 186,511,499 | | | $ | 187,943,561 | | | $ | 63,088,775 | | | $ | 41,341,369 | |

| | | | | | | | | | | | | | | | | |

| COMPONENTS OF NET ASSETS | | | | | | | | | | | | | | | | |

| Paid in capital | | $ | 110,335,219 | | | $ | 100,616,265 | | | $ | 50,016,516 | | | $ | 24,620,994 | |

| Total distributable earnings | | | 76,176,280 | | | | 87,327,296 | | | | 13,072,259 | | | | 16,720,375 | |

| NET ASSETS | | $ | 186,511,499 | | | $ | 187,943,561 | | | $ | 63,088,775 | | | $ | 41,341,369 | |

| | | | | | | | | | | | | | | | | |

| NET ASSET VALUE PER SHARE RETAIL CLASS SHARES | | | | | | | | | | | | | | | | |

| Net assets | | $ | 186,511,499 | | | $ | 145,978,607 | | | $ | 63,088,775 | | | $ | 41,341,369 | |

| Shares of Beneficial Interest Outstanding ($0.01 par value, unlimited authorized shares) | | | 2,740,318 | | | | 6,597,709 | | | | 3,134,617 | | | | 1,816,103 | |

| Net asset value, offering and redemption price per share | | $ | 68.06 | | | $ | 22.13 | | | $ | 20.13 | | | $ | 22.76 | |

| INSISTUTIONAL CLASS SHARES | | | | | | | | | | | | | | | | |

| Net assets | | $ | — | | | $ | 41,964,954 | | | $ | — | | | $ | — | |

| Shares of Beneficial Interest Outstanding ($0.01 par value, unlimited authorized shares) | | | — | | | | 1,765,190 | | | | — | | | | — | |

| Net asset value, offering and redemption price per share | | $ | — | | | $ | 23.77 | | | $ | — | | | $ | — | |

See accompanying notes to financial statements.

| HODGES MUTUAL FUNDS |

| STATEMENTS OF OPERATIONS |

| FOR THE YEAR ENDED MARCH 31, 2024 |

| | | | | | | | | Small Intrinsic | | | Blue Chip Equity | |

| | | Hodges Fund | | | Small Cap Fund | | | Value Fund | | | Income Fund | |

| INVESTMENT INCOME: | | | | | | | | | | | | | | | | |

| Dividends and interest net of $4,610, $-, $-, and $4,337 foreign withholding tax, respectively | | $ | 863,159 | | | $ | 1,418,798 | | | $ | 488,973 | | | $ | 711,384 | |

| Other income | | | 682 | | | | 700 | | | | 616 | | | | 610 | |

| Total investment income | | | 863,841 | | | | 1,419,498 | | | | 489,589 | | | | 711,994 | |

| | | | | | | | | | | | | | | | | |

| EXPENSES: | | | | | | | | | | | | | | | | |

| Investment advisory fees | | | 1,356,409 | | | | 1,468,910 | | | | 384,484 | | | | 227,748 | |

| Distribution (12b-1) fees: | | | | | | | | | | | | | | | | |

| Retail Class | | | 398,944 | | | | 337,717 | | | | 113,084 | | | | 87,596 | |

| Shareholder Servicing fees | | | 75,067 | | | | 136,811 | | | | 43,728 | | | | 14,480 | |

| Administration fees | | | 61,784 | | | | 77,403 | | | | 30,544 | | | | 26,381 | |

| Transfer agent fees | | | 40,948 | | | | 35,870 | | | | 17,819 | | | | 22,849 | |

| Registration fees | | | 39,859 | | | | 51,751 | | | | 38,820 | | | | 30,508 | |

| Accounting fees | | | 39,601 | | | | 48,389 | | | | 14,753 | | | | 10,901 | |

| Shareholder reports | | | 21,959 | | | | 17,590 | | | | 17,649 | | | | 5,579 | |

| Legal fees | | | 17,847 | | | | 16,247 | | | | 17,747 | | | | 17,264 | |

| Audit and tax fees | | | 17,657 | | | | 17,651 | | | | 17,671 | | | | 17,665 | |

| Trustee fees and expenses | | | 14,316 | | | | 14,474 | | | | 13,465 | | | | 13,340 | |

| Custody fees | | | 11,293 | | | | 10,387 | | | | 5,784 | | | | 5,513 | |

| Professional fees | | | 10,988 | | | | 11,490 | | | | 7,525 | | | | 9,437 | |

| Insurance fees | | | 6,242 | | | | 5,926 | | | | 5,646 | | | | 5,592 | |

| Intererst expense - Line of Credit | | | 1,800 | | | | 1,244 | | | | — | | | | 39 | |

| Other expenses | | | 714 | | | | 570 | | | | 6,640 | | | | 2,074 | |

| Total expenses | | | 2,115,428 | | | | 2,252,430 | | | | 735,359 | | | | 496,966 | |

| Expenses waived | | | (228,346 | ) | | | — | | | | (151,086 | ) | | | (41,331 | ) |

| Expenses recaptured | | | — | | | | 10,317 | | | | — | | | | — | |

| Net expenses | | | 1,887,082 | | | | 2,262,747 | | | | 584,273 | | | | 455,635 | |

| NET INVESTMENT INCOME/(LOSS) | | | (1,023,241 | ) | | | (843,249 | ) | | | (94,684 | ) | | | 256,359 | |

| | | | | | | | | | | | | | | | | |

| NET REALIZED AND UNREALIZED GAIN ON INVESTMENTS & WRITTEN OPTIONS | | | | | | | | | | | | | | | | |

| Net realized gain/(loss) from: | | | | | | | | | | | | | | | | |

| Investments | | | 5,482,349 | | | | 18,633,049 | | | | 906,338 | | | | 1,108,590 | |

| Written Options | | | (127,904 | ) | | | — | | | | — | | | | — | |

| Net realized gain | | | 5,354,445 | | | | 18,633,049 | | | | 906,338 | | | | 1,108,590 | |

| | | | | | | | | | | | | | | | | |

| Net change in unrealized appreciation on investments | | | 42,839,828 | | | | 16,655,533 | | | | 8,455,776 | | | | 7,230,017 | |

| | | | | | | | | | | | | | | | | |

| Net realized and unrealized gain on investments | | | 48,194,273 | | | | 35,288,582 | | | | 9,362,114 | | | | 8,338,607 | |

| | | | | | | | | | | | | | | | | |

| NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | 47,171,032 | | | $ | 34,445,333 | | | $ | 9,267,430 | | | $ | 8,594,966 | |

See accompanying notes to financial statements.

| HODGES MUTUAL FUNDS |

| STATEMENTS OF CHANGES IN NET ASSETS |

| | | Hodges Fund | |

| | | Year Ended | | | Year Ended | |

| | | March 31, | | | March 31, | |

| | | 2024 | | | 2023 | |

| NET ASSETS - BEGINNING OF YEAR | | $ | 150,935,481 | | | $ | 186,382,597 | |

| | | | | | | | | |

| OPERATIONS | | | | | | | | |

| Net investment loss | | | (1,023,241 | ) | | | (435,763 | ) |

| Net realized gain from investments | | | 5,354,445 | | | | 2,297,544 | |

| Net change in unrealized appreciation/(depreciation) on investments | | | 42,839,828 | | | | (25,831,475 | ) |

| Net increase/(decrease) in net assets resulting from operations | | | 47,171,032 | | | | (23,969,694 | ) |

| | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS | | | | | | | | |

| Retail Class | | | (1,229,355 | ) | | | (685,796 | ) |

| Total distributions to shareholders | | | (1,229,355 | ) | | | (685,796 | ) |

| | | | | | | | | |

| CAPITAL SHARE TRANSACTIONS | | | | | | | | |

| Sale of shares - Retail Shares | | | 9,585,251 | | | | 8,346,430 | |

| Reinvestment of distributions - Retail Class | | | 1,193,387 | | | | 666,867 | |

| Redemption of shares - Retail Class* | | | (21,144,297 | ) | | | (19,804,923 | ) |

| | | | | | | | | |

| Net decrease from capital share transactions | | | (10,365,659 | ) | | | (10,791,626 | ) |

| | | | | | | | | |

| Total increase/(decrease) in net assets | | | 35,576,018 | | | | (35,447,116 | ) |

| | | | | | | | | |

| NET ASSETS - END OF YEAR | | $ | 186,511,499 | | | $ | 150,935,481 | |

| | | | | | | | | |

| SHARE ACTIVITY | | | | | | | | |

| Retail Class: | | | | | | | | |

| Sold | | | 165,916 | | | | 164,324 | |

| Issued on reinvestment of distributions | | | 20,508 | | | | 13,359 | |

| Redeemed | | | (384,056 | ) | | | (403,531 | ) |

| Net decrease | | | (197,632 | ) | | | (225,848 | ) |

| * | Net of redemption fees of $7,192 and $2,335, respectively. |

See accompanying notes to financial statements.

| HODGES MUTUAL FUNDS |

| STATEMENTS OF CHANGES IN NET ASSETS |

| | | Small Cap Fund | |

| | | Year Ended | | | Year Ended | |

| | | March 31, | | | March 31, | |

| | | 2024 | | | 2023 | |

| NET ASSETS - BEGINNING OF YEAR | | $ | 177,544,856 | | | $ | 207,882,458 | |

| | | | | | | | | |

| OPERATIONS | | | | | | | | |

| Net investment income/(loss) | | | (843,249 | ) | | | 31,829 | |

| Net realized gain from investments | | | 18,633,049 | | | | 10,493,744 | |

| Net change in unrealized appreciation/(depreciation) on investments | | | 16,655,533 | | | | (21,019,131 | ) |

| Net increase/(decrease) in net assets resulting from operations | | | 34,445,333 | | | | (10,493,558 | ) |

| | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS | | | | | | | | |

| Retail Class | | | (6,568,359 | ) | | | (8,378,272 | ) |

| Institutional Class | | | (1,770,930 | ) | | | (2,211,622 | ) |

| Total distributions to shareholders | | | (8,339,289 | ) | | | (10,589,894 | ) |

| | | | | | | | | |

| CAPITAL SHARE TRANSACTIONS | | | | | | | | |

| Sale of shares - Retail Shares | | | 3,594,547 | | | | 7,149,799 | |

| Sale of shares - Institutional Shares | | | 6,978,959 | | | | 6,034,690 | |

| Reinvestment of distributions - Retail Class | | | 6,466,865 | | | | 8,224,458 | |

| Reinvestment of distributions - Institutional Class | | | 1,722,703 | | | | 2,139,821 | |

| Redemption of shares - Retail Class* | | | (23,671,458 | ) | | | (20,607,147 | ) |

| Redemption of shares - Institutional Class^ | | | (10,798,955 | ) | | | (12,195,771 | ) |

| | | | | | | | | |

| Net decrease from capital share transactions | | | (15,707,339 | ) | | | (9,254,150 | ) |

| | | | | | | | | |

| Total increase/(decrease) in net assets | | | 10,398,705 | | | | (30,337,602 | ) |

| | | | | | | | | |

| NET ASSETS - END OF YEAR | | $ | 187,943,561 | | | $ | 177,544,856 | |

| | | | | | | | | |

| SHARE ACTIVITY | | | | | | | | |

| Retail Class: | | | | | | | | |

| Sold | | | 181,529 | | | | 351,720 | |

| Issued on reinvestment of distributions | | | 349,560 | | | | 436,542 | |

| Redeemed | | | (1,213,486 | ) | | | (1,053,459 | ) |

| Net decrease | | | (682,397 | ) | | | (265,197 | ) |

| | | | | | | | | |

| Institutional Class: | | | | | | | | |

| Sold | | | 331,447 | | | | 281,217 | |

| Issued on reinvestment of distributions | | | 86,742 | | | | 106,459 | |

| Redeemed | | | (516,473 | ) | | | (589,820 | ) |

| Net decrease | | | (98,284 | ) | | | (202,144 | ) |

| * | Net of redemption fees of $5,885 and $13,806, respectively. |

| ^ | Net of redemption fees of $1,623 and $3,992, respectively. |

See accompanying notes to financial statements.

| HODGES MUTUAL FUNDS |

| STATEMENTS OF CHANGES IN NET ASSETS |

| | | Small Intrinsic Value Fund | |

| | | Year Ended | | | Year Ended | |

| | | March 31, | | | March 31, | |

| | | 2024 | | | 2023 | |

| NET ASSETS - BEGINNING OF YEAR | | $ | 38,374,072 | | | $ | 17,576,795 | |

| | | | | | | | | |

| OPERATIONS | | | | | | | | |

| Net investment income/(loss) | | | (94,684 | ) | | | 180,780 | |

| Net realized gain/(loss) from investments | | | 906,338 | | | | (3,954 | ) |

| Net change in unrealized appreciation/(depreciation) on investments | | | 8,455,776 | | | | (930,891 | ) |

| Net increase/(decrease) in net assets resulting from operations | | | 9,267,430 | | | | (754,065 | ) |

| | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS | | | | | | | | |

| Retail Class | | | (26,803 | ) | | | (967,105 | ) |

| Total distributions to shareholders | | | (26,803 | ) | | | (967,105 | ) |

| | | | | | | | | |

| CAPITAL SHARE TRANSACTIONS | | | | | | | | |

| Sale of shares - Retail Shares | | | 21,179,948 | | | | 25,275,624 | |

| Reinvestment of distributions - Retail Class | | | 26,546 | | | | 956,580 | |

| Redemption of shares - Retail Class* | | | (5,732,418 | ) | | | (3,713,757 | ) |

| | | | | | | | | |

| Net increase from capital share transactions | | | 15,474,076 | | | | 22,518,447 | |

| | | | | | | | | |

| Total increase in net assets | | | 24,714,703 | | | | 20,797,277 | |

| | | | | | | | | |

| NET ASSETS - END OF YEAR | | $ | 63,088,775 | | | $ | 38,374,072 | |

| | | | | | | | | |

| SHARE ACTIVITY | | | | | | | | |

| Retail Class: | | | | | | | | |

| Sold | | | 1,164,839 | | | | 1,489,965 | |

| Issued on reinvestment of distributions | | | 1,520 | | | | 58,150 | |

| Redeemed | | | (317,209 | ) | | | (219,688 | ) |

| Net increase | | | 849,150 | | | | 1,328,427 | |

| * | Net of redemption fees of $4,782 and $182, respectively. |

See accompanying notes to financial statements.

| HODGES MUTUAL FUNDS |

| STATEMENTS OF CHANGES IN NET ASSETS |

| | | Blue Chip Equity Income Fund | |

| | | Year Ended | | | Year Ended | |

| | | March 31, | | | March 31, | |

| | | 2024 | | | 2023 | |

| NET ASSETS - BEGINNING OF YEAR | | $ | 27,929,273 | | | $ | 30,140,400 | |

| | | | | | | | | |

| OPERATIONS | | | | | | | | |

| Net investment income | | | 256,359 | | | | 223,110 | |

| Net realized gain/(loss) from investments | | | 1,108,590 | | | | (780,034 | ) |

| Net change in unrealized appreciation/(depreciation) on investments | | | 7,230,017 | | | | (1,073,740 | ) |

| Net increase/(decrease) in net assets resulting from operations | | | 8,594,966 | | | | (1,630,664 | ) |

| | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS | | | | | | | | |

| Retail Class | | | (257,271 | ) | | | (2,218,532 | ) |

| Total distributions to shareholders | | | (257,271 | ) | | | (2,218,532 | ) |

| | | | | | | | | |

| CAPITAL SHARE TRANSACTIONS | | | | | | | | |

| Sale of shares - Retail Shares | | | 10,239,945 | | | | 2,542,305 | |

| Reinvestment of distributions - Retail Class | | | 246,346 | | | | 2,101,392 | |

| Redemption of shares - Retail Class* | | | (5,411,890 | ) | | | (3,005,628 | ) |

| | | | | | | | | |

| Net increase from capital share transactions | | | 5,074,401 | | | | 1,638,069 | |

| | | | | | | | | |

| Total increase/(decrease) in net assets | | | 13,412,096 | | | | (2,211,127 | ) |

| | | | | | | | | |

| NET ASSETS - END OF YEAR | | $ | 41,341,369 | | | $ | 27,929,273 | |

| | | | | | | | | |

| SHARE ACTIVITY | | | | | | | | |

| Retail Class: | | | | | | | | |

| Sold | | | 526,091 | | | | 133,388 | |

| Issued on reinvestment of distributions | | | 12,089 | | | | 123,619 | |

| Redeemed | | | (272,598 | ) | | | (165,645 | ) |

| Net increase | | | 265,582 | | | | 91,362 | |

| * | Net of redemption fees of $22 and $10, respectively. |

See accompanying notes to financial statements.

| HODGES MUTUAL FUNDS |

| FINANCIAL HIGHLIGHTS |

| Per Share Data and Ratios for a Share of Beneficial Interest Oustanding Throughout Each Year |

| | | Hodges Fund - Retail Shares | |

| | | For the years ended March 31, | |

| | | 2024 | | | 2023 | | | 2022 | | | 2021 | | | 2020 | |

| Net Asset Value - Beginning of Year | | $ | 51.37 | | | $ | 58.91 | | | $ | 57.39 | | | $ | 20.36 | | | $ | 37.76 | |

| Investment operations: | | | | | | | | | | | | | | | | | | | | |

| Net investment loss1 | | | (0.36 | ) | | | (0.14 | ) | | | (0.46 | ) | | | (0.31 | ) | | | (0.19 | ) |

| Net realized and unrealized gain/(loss) on investments | | | 17.49 | | | | (7.17 | ) | | | 1.98 | | | | 37.34 | | | | (17.21 | ) |

| Total from investment operations | | | 17.13 | | | | (7.31 | ) | | | 1.52 | | | | 37.03 | | | | (17.40 | ) |

| Distributions to shareholders: | | | | | | | | | | | | | | | | | | | | |

| From net realized gain on investments | | | (0.44 | ) | | | (0.23 | ) | | | — | | | | — | | | | — | |

| Total distributions to shareholders | | | (0.44 | ) | | | (0.23 | ) | | | — | | | | — | | | | — | |

| Paid in capital from redemption fees2 | | | 0.00 | | | | 0.00 | | | | 0.00 | | | | 0.00 | | | | 0.00 | |

| Net Asset Value - End of Year | | $ | 68.06 | | | $ | 51.37 | | | $ | 58.91 | | | $ | 57.39 | | | $ | 20.36 | |

| Total return | | | 33.50 | % 3 | | | (12.44 | )% | | | 2.70 | % | | | 181.74 | % | | | (46.05 | )% |

| Ratios/Supplemental Data: | | | | | | | | | | | | | | | | | | | | |

| Ratios of expenses to average net assets: | | | | | | | | | | | | | | | | | | | | |

| Before fees waived and expenses absorbed | | | 1.32 | % | | | 1.37 | % | | | 1.35 | % | | | 1.40 | % | | | 1.37 | % |

| After fees waived and expenses absorbed4 | | | 1.18 | % | | | 1.18 | % | | | 1.17 | % | | | 1.16 | % | | | 1.18 | % |

| Ratios of net investment loss to average net assets: | | | | | | | | | | | | | | | | | | | | |

| Before fees waived and expenses absorbed | | | (0.78 | )% | | | (0.48 | )% | | | (0.93 | )% | | | (1.03 | )% | | | (0.75 | )% |

| After fees waived and expenses absorbed4 | | | (0.64 | )% | | | (0.29 | )% | | | (0.76 | )% | | | (0.79 | )% | | | (0.56 | )% |

| Portfolio turnover rate | | | 103 | % | | | 74 | % | | | 96 | % | | | 220 | % | | | 107 | % |

| Net Assets at end of year (millions) | | $ | 186.5 | | | $ | 150.9 | | | $ | 186.4 | | | $ | 210.7 | | | $ | 73.9 | |

| 1 | Calculated using the average shares method. |

| 2 | Represents less than $0.005. |

| 3 | Includes adjustments in accordance with accounting principles generally accepted in the United States and consequently, the net asset value for financial statement reporting purposes and the returns based upon those net assets may differ from the net asset values and returns for shareholder processing. |

| 4 | Effective September 1, 2020, the Advisor contractually agreed to limit the Retail Class shares’ annual ratio of expenses to 1.15% of the Retail Class’ daily net assets. Effective September 1, 2021, the annual ratio of expenses returned to 1.18% of the Retail Class’ daily net assets. See Note 3. |

See accompanying notes to financial statements.

| HODGES MUTUAL FUNDS |

| FINANCIAL HIGHLIGHTS |

| Per Share Data and Ratios for a Share of Beneficial Interest Oustanding Throughout Each Year |

| | | Small Cap Fund - Retail Shares | |

| | | For the years ended March 31, | |

| | | 2024 | | | 2023 | | | 2022 | | | 2021 | | | 2020 | |

| Net Asset Value - Beginning of Year | | $ | 19.15 | | | $ | 21.35 | | | $ | 25.28 | | | $ | 10.10 | | | $ | 18.13 | |

| Investment operations: | | | | | | | | | | | | | | | | | | | | |

| Net investment loss1 | | | (0.11 | ) | | | (0.01 | ) | | | (0.15 | ) | | | (0.13 | ) | | | (0.07 | ) |

| Net realized and unrealized gain/(loss) on investments | | | 4.09 | | | | (1.01 | ) | | | 0.56 | | | | 15.31 | | | | (6.58 | ) |

| Total from investment operations | | | 3.98 | | | | (1.02 | ) | | | 0.41 | | | | 15.18 | | | | (6.65 | ) |