UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 |

| |

| FORM 10-Q |

| |

| [X] | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 for the quarterly period ended March 31, 2012 |

| OR |

| [ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 for the transition period from _________ to ___________ |

Commission File Number | Registrant; State of Incorporation; Address and Telephone Number | IRS Employer Identification No. |

| | | |

| 1-11459 | PPL Corporation (Exact name of Registrant as specified in its charter) (Pennsylvania) Two North Ninth Street Allentown, PA 18101-1179 (610) 774-5151 | 23-2758192 |

| | | |

| 1-32944 | PPL Energy Supply, LLC (Exact name of Registrant as specified in its charter) (Delaware) Two North Ninth Street Allentown, PA 18101-1179 (610) 774-5151 | 23-3074920 |

| | | |

| 1-905 | PPL Electric Utilities Corporation (Exact name of Registrant as specified in its charter) (Pennsylvania) Two North Ninth Street Allentown, PA 18101-1179 (610) 774-5151 | 23-0959590 |

| | | |

| 333-173665 | LG&E and KU Energy LLC (Exact name of Registrant as specified in its charter) (Kentucky) 220 West Main Street Louisville, KY 40202-1377 (502) 627-2000 | 20-0523163 |

| | | |

| 1-2893 | Louisville Gas and Electric Company (Exact name of Registrant as specified in its charter) (Kentucky) 220 West Main Street Louisville, KY 40202-1377 (502) 627-2000 | 61-0264150 |

| | | |

| 1-3464 | Kentucky Utilities Company (Exact name of Registrant as specified in its charter) (Kentucky and Virginia) One Quality Street Lexington, KY 40507-1462 (502) 627-2000 | 61-0247570 |

Indicate by check mark whether the registrants (1) have filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrants were required to file such reports), and (2) have been subject to such filing requirements for the past 90 days.

| | PPL Corporation | Yes X | No | |

| | PPL Energy Supply, LLC | Yes X | No | |

| | PPL Electric Utilities Corporation | Yes X | No | |

| | LG&E and KU Energy LLC | Yes X | No | |

| | Louisville Gas and Electric Company | Yes X | No | |

| | Kentucky Utilities Company | Yes X | No | |

Indicate by check mark whether the registrants have submitted electronically and posted on their corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrants were required to submit and post such files).

| | PPL Corporation | Yes X | No | |

| | PPL Energy Supply, LLC | Yes X | No | |

| | PPL Electric Utilities Corporation | Yes X | No | |

| | LG&E and KU Energy LLC | Yes X | No | |

| | Louisville Gas and Electric Company | Yes X | No | |

| | Kentucky Utilities Company | Yes X | No | |

Indicate by check mark whether the registrants are large accelerated filers, accelerated filers, non-accelerated filers, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| | | Large accelerated filer | Accelerated filer | Non-accelerated filer | Smaller reporting company |

| | PPL Corporation | [ X ] | [ ] | [ ] | [ ] |

| | PPL Energy Supply, LLC | [ ] | [ ] | [ X ] | [ ] |

| | PPL Electric Utilities Corporation | [ ] | [ ] | [ X ] | [ ] |

| | LG&E and KU Energy LLC | [ ] | [ ] | [ X ] | [ ] |

| | Louisville Gas and Electric Company | [ ] | [ ] | [ X ] | [ ] |

| | Kentucky Utilities Company | [ ] | [ ] | [ X ] | [ ] |

Indicate by check mark whether the registrants are shell companies (as defined in Rule 12b-2 of the Exchange Act).

| | PPL Corporation | Yes | No X | |

| | PPL Energy Supply, LLC | Yes | No X | |

| | PPL Electric Utilities Corporation | Yes | No X | |

| | LG&E and KU Energy LLC | Yes | No X | |

| | Louisville Gas and Electric Company | Yes | No X | |

| | Kentucky Utilities Company | Yes | No X | |

Indicate the number of shares outstanding of each of the issuer's classes of common stock, as of the latest practicable date.

| | PPL Corporation | Common stock, $.01 par value, 580,021,834 shares outstanding at April 30, 2012. |

| | | |

| | PPL Energy Supply, LLC | PPL Corporation indirectly holds all of the membership interests in PPL Energy Supply, LLC. |

| | | |

| | PPL Electric Utilities Corporation | Common stock, no par value, 66,368,056 shares outstanding and all held by PPL Corporation at April 30, 2012. |

| | | |

| | LG&E and KU Energy LLC | PPL Corporation directly holds all of the membership interests in LG&E and KU Energy LLC. |

| | | |

| | Louisville Gas and Electric Company | Common stock, no par value, 21,294,223 shares outstanding and all held by LG&E and KU Energy LLC at April 30, 2012. |

| | | |

| | Kentucky Utilities Company | Common stock, no par value, 37,817,878 shares outstanding and all held by LG&E and KU Energy LLC at April 30, 2012. |

This document is available free of charge at the Investor Center on PPL Corporation's website at www.pplweb.com. However, information on this website does not constitute a part of this Form 10-Q.

PPL CORPORATION

PPL ENERGY SUPPLY, LLC

PPL ELECTRIC UTILITIES CORPORATION

LG&E AND KU ENERGY LLC

LOUISVILLE GAS AND ELECTRIC COMPANY

KENTUCKY UTILITIES COMPANY

FORM 10-Q

FOR THE QUARTER ENDED MARCH 31, 2012

Table of Contents

This combined Form 10-Q is separately filed by the following individual registrants: PPL Corporation, PPL Energy Supply, LLC, PPL Electric Utilities Corporation, LG&E and KU Energy LLC, Louisville Gas and Electric Company and Kentucky Utilities Company. Information contained herein relating to any individual registrant is filed by such registrant solely on its own behalf, and no registrant makes any representation as to information relating to any other registrant, except that information under "Forward-Looking Information" relating to PPL Corporation subsidiaries is also attributed to PPL Corporation and information relating to the subsidiaries of LG&E and KU Energy LLC is also attributed to LG&E and KU Energy LLC.

| | | Page |

| | | |

| | |

| | |

| PART I. FINANCIAL INFORMATION | | |

| | Item 1. Financial Statements | | |

| | | PPL Corporation and Subsidiaries | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | PPL Energy Supply, LLC and Subsidiaries | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | PPL Electric Utilities Corporation and Subsidiaries | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | LG&E and KU Energy LLC and Subsidiaries | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | Louisville Gas and Electric Company | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | Kentucky Utilities Company | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | Combined Notes to Condensed Financial Statements (Unaudited) | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | Item 2. Management's Discussion and Analysis of Financial Condition and Results of Operations | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | |

| | | |

| PART II. OTHER INFORMATION | |

| | | |

| | | |

| | | |

| | | |

| |

| |

| |

| |

| |

| |

GLOSSARY OF TERMS AND ABBREVIATIONS

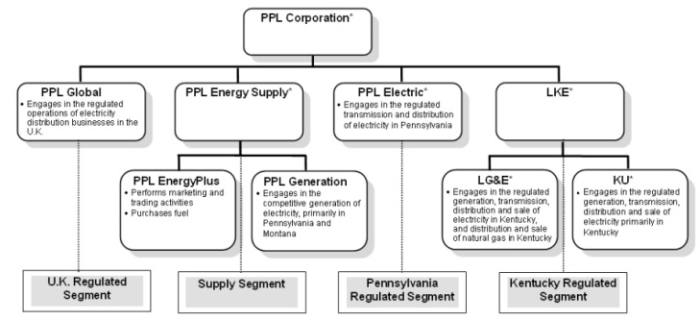

PPL Corporation and its current and former subsidiaries

Central Networks - collectively Central Networks East plc, Central Networks Limited and certain other related assets and liabilities. On April 1, 2011, PPL WEM Holdings plc (formerly WPD Investment Holdings Limited) purchased all of the outstanding ordinary share capital of these companies from E.ON AG subsidiaries. Central Networks West plc (subsequently renamed Western Power Distribution (West Midlands) plc), wholly owned by Central Networks Limited (subsequently renamed WPD Midlands Holdings Limited), and Central Networks East plc (subsequently renamed Western Power Distribution (East Midlands) plc) are British regional electricity distribution utility companies.

KU - Kentucky Utilities Company, a public utility subsidiary of LKE engaged in the regulated generation, transmission, distribution and sale of electricity, primarily in Kentucky. The subsidiary was acquired by PPL through the acquisition of LKE in November 2010.

LG&E - Louisville Gas and Electric Company, a public utility subsidiary of LKE engaged in the regulated generation, transmission, distribution and sale of electricity and the distribution and sale of natural gas in Kentucky. The subsidiary was acquired by PPL through the acquisition of LKE in November 2010.

LKE - LG&E and KU Energy LLC (formerly E.ON U.S. LLC), a subsidiary of PPL and the parent of LG&E, KU and other subsidiaries. PPL acquired E.ON U.S. LLC in November 2010 and changed the name to LG&E and KU Energy LLC. Within the context of this document, references to LKE also relate to the consolidated entity.

LKS - LG&E and KU Services Company, a subsidiary of LKE that provides services for LKE and its subsidiaries. The subsidiary was acquired by PPL through the acquisition of LKE in November 2010.

PPL - PPL Corporation, the parent holding company of PPL Electric, PPL Energy Funding, LKE and other subsidiaries.

PPL Capital Funding - PPL Capital Funding, Inc., a wholly owned financing subsidiary of PPL.

PPL Electric - PPL Electric Utilities Corporation, a public utility subsidiary of PPL that transmits and distributes electricity in its Pennsylvania service area and provides electric supply to retail customers in this area as a PLR.

PPL Energy Funding - PPL Energy Funding Corporation, a subsidiary of PPL and the parent holding company of PPL Energy Supply, PPL Global (effective January 2011) and other subsidiaries.

PPL EnergyPlus - PPL EnergyPlus, LLC, a subsidiary of PPL Energy Supply that markets and trades wholesale and retail electricity and gas, and supplies energy and energy services in competitive markets.

PPL Energy Supply - PPL Energy Supply, LLC, a subsidiary of PPL Energy Funding and the parent company of PPL Generation, PPL EnergyPlus and other subsidiaries. In January 2011, PPL Energy Supply distributed its membership interest in PPL Global, representing 100% of the outstanding membership interests of PPL Global, to PPL Energy Supply's parent, PPL Energy Funding.

PPL Generation - PPL Generation, LLC, a subsidiary of PPL Energy Supply that owns and operates U.S. generating facilities through various subsidiaries.

PPL Global - PPL Global, LLC, a subsidiary of PPL Energy Funding that primarily owns and operates a business in the U.K., WPD, that is focused on the regulated distribution of electricity. In January 2011, PPL Energy Supply, PPL Global's former parent, distributed its membership interest in PPL Global, representing 100% of the outstanding membership interest of PPL Global, to its parent, PPL Energy Funding.

PPL Martins Creek - PPL Martins Creek, LLC, a subsidiary of PPL Generation that owns generating operations in Pennsylvania.

PPL Montana - PPL Montana, LLC, an indirect subsidiary of PPL Generation that generates electricity for wholesale sales in Montana and the Pacific Northwest.

PPL Services - PPL Services Corporation, a subsidiary of PPL that provides services for PPL and its subsidiaries.

PPL Susquehanna - PPL Susquehanna, LLC, the nuclear generating subsidiary of PPL Generation.

PPL WEM - PPL WEM Holdings plc (formerly WPD Investment Holdings Limited), an indirect, wholly owned U.K. subsidiary of PPL Global. PPL WEM indirectly wholly owns both WPD (East Midlands) and WPD (West Midlands).

PPL WW - PPL WW Holdings Limited (formerly Western Power Distribution Holdings Limited), an indirect, wholly owned U.K. subsidiary of PPL Global. PPL WW Holdings indirectly wholly owns WPD (South Wales) and WPD (South West).

WPD - refers to PPL WW and PPL WEM and their subsidiaries.

WPD (East Midlands) - Western Power Distribution (East Midlands) plc, a British regional electricity distribution utility company. The company (formerly Central Networks East plc) was acquired and renamed in April 2011.

WPD Midlands - refers to Central Networks, which was renamed after the acquisition.

WPD (South Wales) - Western Power Distribution (South Wales) plc, a British regional electricity distribution utility company.

WPD (South West) - Western Power Distribution (South West) plc, a British regional electricity distribution utility company.

WPD (West Midlands) - Western Power Distribution (West Midlands) plc, a British regional electricity distribution utility company. The company (formerly Central Networks West plc) was acquired and renamed in April 2011.

WKE - Western Kentucky Energy Corp., a subsidiary of LKE that leased certain non-utility generating plants in western Kentucky until July 2009. The subsidiary was acquired by PPL through the acquisition of LKE in November 2010.

Other terms and abbreviations

£ - British pound sterling.

2010 Equity Unit(s) - a PPL equity unit, issued in June 2010, consisting of a 2010 Purchase Contract and, initially, a 5.0% undivided beneficial ownership interest in $1,000 principal amount of PPL Capital Funding 4.625% Junior Subordinated Notes due 2018.

2010 Purchase Contract(s) - a contract that is a component of a 2010 Equity Unit that requires holders to purchase shares of PPL common stock on or prior to July 1, 2013.

2011 Bridge Facility - the £3.6 billion Senior Bridge Term Loan Credit Agreement between PPL Capital Funding and PPL WEM, as borrowers, and PPL, as guarantor, and lenders party thereto, used to fund the April 1, 2011 acquisition of Central Networks, as amended by Amendment No. 1 thereto dated April 15, 2011.

2011 Equity Unit(s) - a PPL equity unit, issued in April 2011, consisting of a 2011 Purchase Contract and, initially, a 5.0% undivided beneficial ownership interest in $1,000 principal amount of PPL Capital Funding 4.32% Junior Subordinated Notes due 2019.

2011 Form 10-K - Annual Report to the SEC on Form 10-K for the year ended December 31, 2011.

2011 Purchase Contract(s) - a contract that is a component of a 2011 Equity Unit that requires holders to purchase shares of PPL common stock on or prior to May 1, 2014.

Acid Rain Program - allowance trading system established by the Clean Air Act to reduce levels of sulfur dioxide. Under this program, affected power plants are allocated allowances based on their fuel consumption during specified baseline years and a specific emissions rate.

Act 129 - became effective in October 2008. The law amends the Pennsylvania Public Utility Code and creates an energy efficiency and conservation program and smart metering technology requirements, adopts new PLR electricity supply procurement rules, provides remedies for market misconduct and makes changes to the existing Alternative Energy Portfolio Standard.

AFUDC - Allowance for Funds Used During Construction, the cost of equity and debt funds used to finance construction projects of regulated businesses, which is capitalized as part of construction costs.

A.M. Best - A.M. Best Company, a company that reports on the financial condition of insurance companies.

AOCI - accumulated other comprehensive income or loss.

ARO - asset retirement obligation.

Baseload generation - includes the output provided by PPL's nuclear, coal, hydroelectric and qualifying facilities.

Basis - when used in the context of derivatives and commodity trading, the commodity price differential between two locations, products or time periods.

Bcf - billion cubic feet.

Bluegrass CTs - three natural gas combustion turbines owned by Bluegrass Generation. LG&E and KU entered into an Asset Purchase Agreement with Bluegrass Generation for the purchase of these combustion turbines, subject to certain conditions including receipt of applicable regulatory approvals and clearances.

Bluegrass Generation - Bluegrass Generation Company, L.L.C., an exempt wholesale electricity generator in LaGrange, Kentucky.

BREC - Big Rivers Electric Corporation, a power-generating rural electric cooperative in western Kentucky.

CAIR - the EPA's Clean Air Interstate Rule.

Clean Air Act - federal legislation enacted to address certain environmental issues related to air emissions, including acid rain, ozone and toxic air emissions.

COLA - license application for a combined construction permit and operating license from the NRC for a nuclear plant.

CPCN - Certificate of Public Convenience and Necessity. Authority granted by the KPSC pursuant to Kentucky Revised Statute 278.020 to provide utility service to or for the public or the construction of any plant, equipment, property or facility for furnishing of utility service to the public.

CSAPR - Cross-State Air Pollution Rule, the CSAPR implements Clean Air Act requirements concerning the transport of air pollution from power plants across state boundaries. The CSAPR replaces the 2005 CAIR, which the U.S. Court of Appeals for the D.C. Circuit ordered the EPA to revise in 2008. The court has granted a stay allowing CAIR to remain in place pending a ruling on the legal challenges to the CSAPR.

Customer Choice Act - the Pennsylvania Electricity Generation Customer Choice and Competition Act, legislation enacted to restructure the state's electric utility industry to create retail access to a competitive market for generation of electricity.

Depreciation not normalized - the flow-through income tax impact related to the state regulatory treatment of depreciation-related timing differences.

Dodd-Frank Act - the Dodd-Frank Wall Street Reform and Consumer Protection Act that was signed into law in July 2010.

DOE - Department of Energy, a U.S. government agency.

DPCR4 - Distribution Price Control Review 4, the U.K. 5-year rate review period applicable to WPD that commenced April 1, 2005.

DRIP - Dividend Reinvestment and Direct Stock Purchase Plan.

DSM - Demand Side Management. Pursuant to Kentucky Revised Statute 278.285, the KPSC may determine the reasonableness of DSM plans proposed by any utility under its jurisdiction. Proposed DSM mechanisms may seek full recovery of DSM programs and revenues lost by implementing those programs and/or incentives designed to provide financial rewards to the utility for implementing cost-effective DSM programs. The cost of such programs shall be assigned only to the class or classes of customers which benefit from the programs.

ECR - Environmental Cost Recovery. Pursuant to Kentucky Revised Statute 278.183, effective January 1993, Kentucky electric utilities are entitled to the current recovery of costs of complying with the Clean Air Act, as amended, and those federal, state or local environmental requirements which apply to coal combustion and by-products from the production of energy from coal.

E.ON AG - a German corporation and the parent of E.ON UK plc, the former parent of Central Networks, and the indirect parent of E.ON US Investments Corp., the former parent of LKE.

EPA - Environmental Protection Agency, a U.S. government agency.

EPS - earnings per share.

Equity Units - refers collectively to the 2011 and 2010 Equity Units.

ESOP - Employee Stock Ownership Plan.

Euro - the basic monetary unit among participating members of the European Union.

FERC - Federal Energy Regulatory Commission, the federal agency that regulates, among other things, interstate transmission and wholesale sales of electricity, hydroelectric power projects and related matters.

Fitch - Fitch, Inc., a credit rating agency.

FTR - financial transmission rights, which are financial instruments established to manage price risk related to electricity transmission congestion. They entitle the holder to receive compensation or require the holder to remit payment for certain congestion-related transmission charges based on the level of congestion in the transmission grid.

Fundamental Change - as it relates to the terms of the 2011 and 2010 Equity Units, will be deemed to have occurred if any of the following occurs with respect to PPL, subject to certain exceptions: (i) a change of control; (ii) a consolidation with or merger into any other entity; (iii) common stock ceases to be listed or quoted; or (iv) a liquidation, dissolution or termination.

GAAP - Generally Accepted Accounting Principles in the U.S.

GBP - British pound sterling.

GHG - greenhouse gas(es).

GWh - gigawatt-hour, one million kilowatt-hours.

Intermediate and peaking generation - includes the output provided by PPL's oil- and natural gas-fired units.

Ironwood Acquisition - In April 2012, PPL Ironwood Holdings, LLC, an indirect, wholly owned subsidiary of PPL Energy Supply, completed the acquisition from a subsidiary of The AES Corporation of all of the equity interests of AES Ironwood, L.L.C. (subsequently renamed PPL Ironwood, LLC) and AES Prescott, L.L.C. (subsequently renamed PPL Prescott, LLC), which own and operate, respectively, the Ironwood Facility.

Ironwood Facility - a natural gas-fired power plant in Lebanon, Pennsylvania with a summer rating of 657 MW.

IRS - Internal Revenue Service, a U.S. government agency.

ISO - Independent System Operator.

KPSC - Kentucky Public Service Commission, the state agency that has jurisdiction over the regulation of rates and service of utilities in Kentucky.

LIBOR - London Interbank Offered Rate.

Long Island generation business - includes a 79.9 MW gas-fired plant in the Edgewood section of Brentwood, New York and a 79.9 MW oil-fired plant in Shoreham, New York and related tolling agreements. This business was sold in February 2010.

Moody's - Moody's Investors Service, Inc., a credit rating agency.

MW - megawatt, one thousand kilowatts.

NDT - PPL Susquehanna's nuclear plant decommissioning trust.

NERC - North American Electric Reliability Corporation.

NGCC - Natural gas-fired combined-cycle turbine.

NPDES - National Pollutant Discharge Elimination System.

NPNS - the normal purchases and normal sales exception as permitted by derivative accounting rules. Derivatives that qualify for this exception receive accrual accounting treatment.

NRC - Nuclear Regulatory Commission, the federal agency that regulates nuclear power facilities.

OCI - other comprehensive income or loss.

Ofgem - Office of Gas and Electricity Markets, the British agency that regulates transmission, distribution and wholesale sales of electricity and related matters.

Opacity - the degree to which emissions reduce the transmission of light and obscure the view of an object in the background. There are emission regulations that limit the opacity in power plant stack gas emissions.

OVEC - Ohio Valley Electric Corporation, located in Piketon, Ohio, an entity in which LKE indirectly owns an 8.13% interest (consists of LG&E's 5.63% and KU's 2.50% interests), which is accounted for as a cost-method investment. OVEC owns and operates two coal-fired power plants, the Kyger Creek plant in Ohio and the Clifty Creek plant in Indiana, with combined nameplate capacities of 2,390 MW.

PADEP - the Pennsylvania Department of Environmental Protection, a state government agency.

PJM - PJM Interconnection, L.L.C., operator of the electric transmission network and electric energy market in all or parts of Delaware, Illinois, Indiana, Kentucky, Maryland, Michigan, New Jersey, North Carolina, Ohio, Pennsylvania, Tennessee, Virginia, West Virginia and the District of Columbia.

PLR - Provider of Last Resort, the role of PPL Electric in providing default electricity supply to retail customers within its delivery area who have not chosen to select an alternative electricity supplier under the Customer Choice Act.

PP&E - property, plant and equipment.

Predecessor - refers to the LKE, LG&E and KU pre-acquisition activity covering the time period prior to November 1, 2010.

PUC - Pennsylvania Public Utility Commission, the state agency that regulates certain ratemaking, services, accounting and operations of Pennsylvania utilities.

Purchase Contract(s) - refers collectively to the 2010 and 2011 Purchase Contracts.

RAV - regulatory asset value. This term is also commonly known as RAB or regulatory asset base.

RECs - renewable energy credits.

Registrants - PPL, PPL Energy Supply, PPL Electric, LKE, LG&E and KU, collectively.

Regulation S-X - SEC regulation governing the form and content of and requirements for financial statements required to be filed pursuant to the federal securities laws.

Rev. Proc(s). - Revenue Procedure(s), an official published statement by the IRS of a matter of procedural importance to both taxpayers and the IRS concerning administration of the tax laws.

RMC - Risk Management Committee.

S&P - Standard & Poor's Ratings Services, a credit rating agency.

Sarbanes-Oxley - Sarbanes-Oxley Act of 2002, which sets requirements for management's assessment of internal controls for financial reporting. It also requires an independent auditor to make its own assessment.

SCR - selective catalytic reduction, a pollution control process for the removal of nitrogen oxide from exhaust gases.

Scrubber - an air pollution control device that can remove particulates and/or gases (such as sulfur dioxide) from exhaust gases.

SEC - the U.S. Securities and Exchange Commission, a U.S. government agency whose primary mission is to protect investors and maintain the integrity of the securities markets.

Securities Act of 1933 - the Securities Act of 1933, 15 U.S. Code, Sections 77a-77aa, as amended.

SIFMA Index - the Securities Industry and Financial Markets Association Municipal Swap Index.

SMGT - Southern Montana Electric Generation & Transmission Cooperative, Inc., a Montana cooperative and purchaser of electricity under a long-term supply contract with PPL EnergyPlus expiring in June 2019.

SNCR - selective non-catalytic reduction, a pollution control process for the removal of nitrogen oxide from exhaust gases using ammonia.

Successor - refers to the LKE, LG&E and KU post-acquisition activity covering the time period after October 31, 2010.

Superfund - federal environmental legislation that addresses remediation of contaminated sites; states also have similar statutes.

TC2 - Trimble County Unit 2, a coal-fired plant located in Kentucky with a net summer capacity of 732 MW. LKE indirectly owns a 75% interest (consists of LG&E's 14.25% and KU's 60.75% interests) in TC2 or 549 MW of the capacity.

Tolling agreement - agreement whereby the owner of an electric generating facility agrees to use that facility to convert fuel provided by a third party into electricity for delivery back to the third party.

TRA - Tennessee Regulatory Authority, the state agency that has jurisdiction over the regulation of rates and service of utilities in Tennessee.

VaR - value-at-risk, a statistical model that attempts to estimate the value of potential loss over a given holding period under normal market conditions at a given confidence level.

VIE - variable interest entity.

Volumetric risk - the risk that the actual load volumes provided under full-requirement sales contracts could vary significantly from forecasted volumes.

VSCC - Virginia State Corporation Commission, the state agency that has jurisdiction over the regulation of Virginia corporations, including utilities.

VWAP - as it relates to the 2011 and 2010 Equity Units issued by PPL, the per share volume-weighted-average price as displayed under the heading Bloomberg VWAP on Bloomberg page "PPL <EQUITY> AQR" (or its equivalent successor if such page is not available) in respect of the period from the scheduled open of trading on the relevant trading day until the scheduled close of trading on the relevant trading day (or if such volume-weighted-average price is unavailable, the market price of one share of PPL common stock on such trading day determined, using a volume-weighted-average method, by a nationally recognized independent investment banking firm retained for this purpose by PPL).

FORWARD-LOOKING INFORMATION

Statements contained in this Form 10-Q concerning expectations, beliefs, plans, objectives, goals, strategies, future events or performance and underlying assumptions and other statements which are other than statements of historical fact are "forward-looking statements" within the meaning of the federal securities laws. Although the Registrants believe that the expectations and assumptions reflected in these statements are reasonable, there can be no assurance that these expectations will prove to be correct. Forward-looking statements are subject to many risks and uncertainties, and actual results may differ materially from the results discussed in forward-looking statements. In addition to the specific factors discussed in each Registrant's 2011 Form 10-K and in "Item 2. Management's Discussion and Analysis of Financial Condition and Results of Operations" in this Form 10-Q report, the following are among the important factors that could cause actual results to differ materially from the forward-looking statements.

| · | fuel supply cost and availability; |

| · | continuing ability to recover fuel costs and environmental expenditures in a timely manner at LG&E and KU, and natural gas supply costs at LG&E; |

| · | weather conditions affecting generation, customer energy use and operating costs; |

| · | operation, availability and operating costs of existing generation facilities; |

| · | the length of scheduled and unscheduled outages at our generating facilities; |

| · | transmission and distribution system conditions and operating costs; |

| · | potential expansion of alternative sources of electricity generation; |

| · | potential laws or regulations to reduce emissions of "greenhouse" gases or other emissions and the physical effects of climate change; |

| · | collective labor bargaining negotiations; |

| · | the outcome of litigation against the Registrants and their subsidiaries; |

| · | potential effects of threatened or actual terrorism, war or other hostilities, cyber-based intrusions or natural disasters; |

| · | the commitments and liabilities of the Registrants and their subsidiaries; |

| · | market demand and prices for energy, capacity, transmission services, emission allowances, RECs and delivered fuel; |

| · | competition in retail and wholesale power and natural gas markets; |

| · | liquidity of wholesale power markets; |

| · | defaults by counterparties under energy, fuel or other power product contracts; |

| · | market prices of commodity inputs for ongoing capital expenditures; |

| · | capital market conditions, including the availability of capital or credit, changes in interest rates and certain economic indices, and decisions regarding capital structure; |

| · | stock price performance of PPL; |

| · | volatility in the fair value of debt and equity securities and its impact on the value of assets in the NDT funds and in defined benefit plans, and the potential cash funding requirements if fair value declines; |

| · | interest rates and their effect on pension, retiree medical, and nuclear decommissioning liabilities, and interest payable on certain debt securities; |

| · | volatility in or the impact of other changes in financial or commodity markets and economic conditions; |

| · | the profitability and liquidity, including access to capital markets and credit facilities, of the Registrants and their subsidiaries; |

| · | new accounting requirements or new interpretations or applications of existing requirements; |

| · | changes in securities and credit ratings; |

| · | foreign currency exchange rates; |

| · | current and future environmental conditions, regulations and other requirements and the related costs of compliance, including environmental capital expenditures, emission allowance costs and other expenses; |

| · | legal, regulatory, political, market or other reactions to the 2011 incident at the nuclear generating facility at Fukushima, Japan, including additional NRC requirements; |

| · | political, regulatory or economic conditions in states, regions or countries where the Registrants or their subsidiaries conduct business; |

| · | receipt of necessary governmental permits, approvals and rate relief; |

| · | new state, federal or foreign legislation, including new tax, environmental, healthcare or pension-related legislation; |

| · | state, federal and foreign regulatory developments; |

| · | the outcome of any rate cases or other cost recovery filings by PPL Electric at the PUC or the FERC, by LG&E at the KPSC, by KU at the KPSC, VSCC, TRA or the FERC, or by WPD at Ofgem in the U.K.; |

| · | the impact of any state, federal or foreign investigations applicable to the Registrants and their subsidiaries and the energy industry; |

| · | the effect of any business or industry restructuring; |

| · | development of new projects, markets and technologies; |

| · | performance of new ventures; and |

| · | business dispositions or acquisitions and our ability to successfully operate such acquired businesses and realize expected benefits from business acquisitions, including PPL's 2011 acquisition of WPD Midlands and 2010 acquisition of LKE. |

Any such forward-looking statements should be considered in light of such important factors and in conjunction with other documents of the Registrants on file with the SEC.

New factors that could cause actual results to differ materially from those described in forward-looking statements emerge from time to time, and it is not possible for the Registrants to predict all such factors, or the extent to which any such factor or combination of factors may cause actual results to differ from those contained in any forward-looking statement. Any forward-looking statement speaks only as of the date on which such statement is made, and the Registrants undertake no obligation to update the information contained in such statement to reflect subsequent developments or information.

PART I. FINANCIAL INFORMATION |

| ITEM 1. Financial Statements |

| | | | | | | | | | |

| CONDENSED CONSOLIDATED STATEMENTS OF INCOME |

| PPL Corporation and Subsidiaries |

| (Unaudited) |

| (Millions of Dollars, except share data) |

| | | | | | | | | | |

| | | | | | Three Months Ended March 31, |

| | | | | | 2012 | | 2011 |

| Operating Revenues | | | | |

| | Utility | | $ | 1,714 | | $ | 1,536 |

| | Unregulated retail electric and gas | | | 223 | | | 147 |

| | Wholesale energy marketing | | | | | | |

| | | Realized | | | 1,208 | | | 1,038 |

| | | Unrealized economic activity (Note 14) | | | 852 | | | 57 |

| | Net energy trading margins | | | 8 | | | 11 |

| | Energy-related businesses | | | 107 | | | 121 |

| | Total Operating Revenues | | | 4,112 | | | 2,910 |

| | | | | | | |

| Operating Expenses | | | | | | |

| | Operation | | | | | | |

| | | Fuel | | | 424 | | | 475 |

| | | Energy purchases | | | | | | |

| | | | Realized | | | 883 | | | 671 |

| | | | Unrealized economic activity (Note 14) | | | 591 | | | (18) |

| | | Other operation and maintenance | | | 706 | | | 583 |

| | Depreciation | | | 264 | | | 208 |

| | Taxes, other than income | | | 91 | | | 73 |

| | Energy-related businesses | | | 102 | | | 113 |

| | Total Operating Expenses | | | 3,061 | | | 2,105 |

| | | | | | | | | | |

Operating Income | | | 1,051 | | | 805 |

| | | | | | | | | | |

Other Income (Expense) - net | | | (17) | | | (5) |

| | | | | | | |

Other-Than-Temporary Impairments | | | | | | 1 |

| | | | | | | | | | |

Interest Expense | | | 230 | | | 174 |

| | | | | | | | | | |

Income from Continuing Operations Before Income Taxes | | | 804 | | | 625 |

| | | | | | | | | | |

Income Taxes | | | 259 | | | 223 |

| | | | | | | | | | |

Income from Continuing Operations After Income Taxes | | | 545 | | | 402 |

| | | | | | | | | | |

Income (Loss) from Discontinued Operations (net of income taxes) | | | | | | 3 |

| | | | | | | | | | |

Net Income | | | 545 | | | 405 |

| | | | | | | | | | |

Net Income Attributable to Noncontrolling Interests | | | 4 | | | 4 |

| | | | | | | | | | |

Net Income Attributable to PPL Corporation | | $ | 541 | | $ | 401 |

| | | | | | | | | | |

| Amounts Attributable to PPL Corporation: | | | | | | |

| | Income from Continuing Operations After Income Taxes | | $ | 541 | | $ | 398 |

| | Income (Loss) from Discontinued Operations (net of income taxes) | | | | | | 3 |

| | Net Income | | $ | 541 | | $ | 401 |

| | | | | | | | | | |

| Earnings Per Share of Common Stock: | | | | | | |

| | Income from Continuing Operations After Income Taxes Available to PPL | | | | |

| | Corporation Common Shareowners: | | | | | | |

| | | Basic | | $ | 0.93 | | $ | 0.82 |

| | | Diluted | | $ | 0.93 | | $ | 0.82 |

| | Net Income Available to PPL Corporation Common Shareowners: | | | | | | |

| | | Basic | | $ | 0.93 | | $ | 0.82 |

| | | Diluted | | $ | 0.93 | | $ | 0.82 |

| | | | | | | | | | |

Dividends Declared Per Share of Common Stock | | $ | 0.360 | | $ | 0.350 |

| | | | | | | | | | |

Weighted-Average Shares of Common Stock Outstanding (in thousands) | | | | | | |

| | | Basic | | | 579,041 | | | 484,138 |

| | | Diluted | | | 579,527 | | | 484,345 |

| | | | | | | | | | |

| The accompanying Notes to Condensed Financial Statements are an integral part of the financial statements. |

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME |

| PPL Corporation and Subsidiaries |

| (Unaudited) |

| (Millions of Dollars) |

| | | | | Three Months Ended March 31, |

| | | | | 2012 | | 2011 |

| | | | | | | | | |

Net income | | $ | 545 | | $ | 405 |

| | | | | | | | | |

| Other comprehensive income (loss): | | | | | | |

| Amounts arising during the period - gains (losses), net of tax (expense) benefit: | | | | | | |

| | Foreign currency translation adjustments, net of tax of $2, $1 | | | 76 | | | 67 |

| | Available-for-sale securities, net of tax of ($28), ($12) | | | 22 | | | 12 |

| | Qualifying derivatives, net of tax of ($62), ($32) | | | 66 | | | 37 |

| | Equity investees' other comprehensive income (loss), net of tax of $2, $0 | | | (4) | | | (1) |

| Reclassifications to net income - (gains) losses, net of tax expense (benefit): | | | | | | |

| | Available-for-sale securities, net of tax of $2, $5 | | | (3) | | | (7) |

| | Qualifying derivatives, net of tax of $87, $51 | | | (122) | | | (69) |

| | Equity investees' other comprehensive (income) loss, net of tax of $0, $0 | | | | | | 2 |

| | Defined benefit plans: | | | | | | |

| | | Prior service costs, net of tax of ($1), ($2) | | | 3 | | | 3 |

| | | Net actuarial loss, net of tax of ($4), ($4) | | | 20 | | | 11 |

Total other comprehensive income (loss) attributable to PPL Corporation | | | 58 | | | 55 |

| | | | | | | | | |

Comprehensive income (loss) | | | 603 | | | 460 |

| | Comprehensive income attributable to noncontrolling interests | | | 4 | | | 4 |

| | | | | | | | | |

Comprehensive income (loss) attributable to PPL Corporation | | $ | 599 | | $ | 456 |

| | | | | | | | | |

| The accompanying Notes to Condensed Financial Statements are an integral part of the financial statements. |

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS |

| PPL Corporation and Subsidiaries |

| (Unaudited) |

| (Millions of Dollars) |

| | | | | | | | | | |

| | | | | | Three Months Ended March 31, |

| | | | | | 2012 | | 2011 |

| Cash Flows from Operating Activities | | | | | | |

| | Net income | | $ | 545 | | $ | 405 |

| | Adjustments to reconcile net income to net cash provided by operating activities | | | | | | |

| | | Depreciation | | | 264 | | | 208 |

| | | Amortization | | | 55 | | | 47 |

| | | Defined benefit plans - expense | | | 42 | | | 39 |

| | | Deferred income taxes and investment tax credits | | | 257 | | | 204 |

| | | Unrealized (gains) losses on derivatives, and other hedging activities | | | (235) | | | (96) |

| | | Other | | | 20 | | | 10 |

| | Change in current assets and current liabilities | | | | | | |

| | | Accounts receivable | | | 32 | | | (57) |

| | | Accounts payable | | | (99) | | | (112) |

| | | Unbilled revenues | | | 59 | | | 199 |

| | | Prepayments | | | (100) | | | (85) |

| | | Counterparty collateral | | | 65 | | | (195) |

| | | Taxes | | | 66 | | | 10 |

| | | Accrued interest | | | 37 | | | 55 |

| | | Other | | | (45) | | | (5) |

| | Other operating activities | | | | | | |

| | | Defined benefit plans - funding | | | (208) | | | (438) |

| | | Other assets | | | (12) | | | (4) |

| | | Other liabilities | | | (15) | | | 11 |

| | | | Net cash provided by operating activities | | | 728 | | | 196 |

| Cash Flows from Investing Activities | | | | | | |

| | Expenditures for property, plant and equipment | | | (682) | | | (428) |

| | Proceeds from the sale of certain non-core generation facilities | | | | | | 381 |

| | Purchases of nuclear plant decommissioning trust investments | | | (38) | | | (79) |

| | Proceeds from the sale of nuclear plant decommissioning trust investments | | | 34 | | | 75 |

| | Proceeds from the sale of other investments | | | 16 | | | 163 |

| | Net (increase) decrease in restricted cash and cash equivalents | | | (22) | | | (7) |

| | Other investing activities | | | (19) | | | (7) |

| | | | Net cash provided by (used in) investing activities | | | (711) | | | 98 |

| Cash Flows from Financing Activities | | | | | | |

| | Issuance of common stock | | | 16 | | | 16 |

| | Payment of common stock dividends | | | (203) | | | (170) |

| | Net increase (decrease) in short-term debt | | | 93 | | | 187 |

| | Other financing activities | | | (30) | | | (20) |

| | | | Net cash provided by (used in) financing activities | | | (124) | | | 13 |

Effect of Exchange Rates on Cash and Cash Equivalents | | | 8 | | | 13 |

Net Increase (Decrease) in Cash and Cash Equivalents | | | (99) | | | 320 |

Cash and Cash Equivalents at Beginning of Period | | | 1,202 | | | 925 |

Cash and Cash Equivalents at End of Period | | $ | 1,103 | | $ | 1,245 |

| | | | | | | | | | |

| The accompanying Notes to Condensed Financial Statements are an integral part of the financial statements. |

|

| PPL Corporation and Subsidiaries |

| (Unaudited) |

| (Millions of Dollars, shares in thousands) |

| | | | | | March 31, | | December 31, |

| | | | | | 2012 | | 2011 |

| Assets | | | | | | |

| | | | | | | | | | |

| Current Assets | | | | | | |

| | Cash and cash equivalents | | $ | 1,103 | | $ | 1,202 |

| | Short-term investments | | | | | | 16 |

| | Restricted cash and cash equivalents | | | 172 | | | 152 |

| | Accounts receivable (less reserve: 2012, $69; 2011, $54) | | | | | | |

| | | Customer | | | 723 | | | 742 |

| | | Other | | | 84 | | | 85 |

| | Unbilled revenues | | | 774 | | | 830 |

| | Fuel, materials and supplies | | | 669 | | | 654 |

| | Prepayments | | | 261 | | | 160 |

| | Price risk management assets | | | 3,230 | | | 2,548 |

| | Regulatory assets | | | 15 | | | 9 |

| | Other current assets | | | 31 | | | 28 |

| | Total Current Assets | | | 7,062 | | | 6,426 |

| | | | | | | | | | |

| Investments | | | | | | |

| | Nuclear plant decommissioning trust funds | | | 693 | | | 640 |

| | Other investments | | | 75 | | | 78 |

| | Total Investments | | | 768 | | | 718 |

| | | | | | | | | | |

| Property, Plant and Equipment | | | | | | |

| | Regulated utility plant | | | 23,544 | | | 22,994 |

| | Less: accumulated depreciation - regulated utility plant | | | 3,701 | | | 3,534 |

| | | Regulated utility plant, net | | | 19,843 | | | 19,460 |

| | Non-regulated property, plant and equipment | | | | | | |

| | | Generation | | | 10,536 | | | 10,514 |

| | | Nuclear fuel | | | 718 | | | 658 |

| | | Other | | | 661 | | | 637 |

| | Less: accumulated depreciation - non-regulated property, plant and equipment | | | 5,758 | | | 5,676 |

| | | Non-regulated property, plant and equipment, net | | | 6,157 | | | 6,133 |

| | Construction work in progress | | | 1,706 | | | 1,673 |

| | Property, Plant and Equipment, net (a) | | | 27,706 | | | 27,266 |

| Other Noncurrent Assets | | | | | | |

| | Regulatory assets | | | 1,334 | | | 1,349 |

| | Goodwill | | | 4,161 | | | 4,114 |

| | Other intangibles (a) | | | 1,064 | | | 1,065 |

| | Price risk management assets | | | 1,186 | | | 920 |

| | Other noncurrent assets | | | 801 | | | 790 |

| | Total Other Noncurrent Assets | | | 8,546 | | | 8,238 |

| | | | | | | |

Total Assets | | $ | 44,082 | | $ | 42,648 |

| (a) | At March 31, 2012 and December 31, 2011, includes $417 million and $416 million of PP&E, consisting primarily of "Generation," including leasehold improvements, and $10 million and $11 million of "Other intangibles" from the consolidation of a VIE that is the owner/lessor of the Lower Mt. Bethel plant. |

The accompanying Notes to Condensed Financial Statements are an integral part of the financial statements.

| CONDENSED CONSOLIDATED BALANCE SHEETS |

| PPL Corporation and Subsidiaries |

| (Unaudited) |

| (Millions of Dollars, shares in thousands) |

| | | | | | March 31, | | December 31, |

| | | | | | 2012 | | 2011 |

| Liabilities and Equity | | | | | | |

| | | | | | | | | | |

| Current Liabilities | | | | | | |

| | Short-term debt | | $ | 674 | | $ | 578 |

| | Accounts payable | | | 1,027 | | | 1,214 |

| | Taxes | | | 132 | | | 65 |

| | Interest | | | 326 | | | 287 |

| | Dividends | | | 214 | | | 207 |

| | Price risk management liabilities | | | 2,149 | | | 1,570 |

| | Regulatory liabilities | | | 74 | | | 73 |

| | Other current liabilities | | | 1,292 | | | 1,261 |

| | Total Current Liabilities | | | 5,888 | | | 5,255 |

| | | | | | | | | | |

Long-term Debt | | | 18,076 | | | 17,993 |

| | | | | | | | | | |

| Deferred Credits and Other Noncurrent Liabilities | | | | | | |

| | Deferred income taxes | | | 3,589 | | | 3,326 |

| | Investment tax credits | | | 295 | | | 285 |

| | Price risk management liabilities | | | 1,074 | | | 840 |

| | Accrued pension obligations | | | 1,105 | | | 1,299 |

| | Asset retirement obligations | | | 491 | | | 484 |

| | Regulatory liabilities | | | 1,009 | | | 1,010 |

| | Other deferred credits and noncurrent liabilities | | | 1,020 | | | 1,060 |

| | Total Deferred Credits and Other Noncurrent Liabilities | | | 8,583 | | | 8,304 |

| | | | | | | | | | |

| Commitments and Contingent Liabilities (Notes 6 and 10) | | | | | | |

| | | | | | | | | | |

| Equity | | | | | | |

| | PPL Corporation Shareowners' Common Equity | | | | | | |

| | | Common stock - $0.01 par value (a) | | | 6 | | | 6 |

| | | Additional paid in capital | | | 6,862 | | | 6,813 |

| | | Earnings reinvested | | | 5,129 | | | 4,797 |

| | | Accumulated other comprehensive loss | | | (730) | | | (788) |

| | | Total PPL Corporation Shareowners' Common Equity | | | 11,267 | | | 10,828 |

| | Noncontrolling Interests | | | 268 | | | 268 |

| | Total Equity | | | 11,535 | | | 11,096 |

| | | | | | | | | | |

Total Liabilities and Equity | | $ | 44,082 | | $ | 42,648 |

| (a) | 780,000 shares authorized; 579,520 and 578,405 shares issued and outstanding at March 31, 2012 and December 31, 2011. |

The accompanying Notes to Condensed Financial Statements are an integral part of the financial statements.

|

| PPL Corporation and Subsidiaries |

| (Unaudited) |

| (Millions of Dollars) |

| |

| | | | | PPL Corporation Shareowners | | | | | | |

| | | | | Common | | | | | | | | | | | | | | | | | | |

| | | | | stock | | | | | | | | | | | | Accumulated | | | | | | |

| | | | | shares | | | | | | Additional | | | | | | other | | | Non- | | | |

| | | | | outstanding | | | Common | | | paid-in | | | Earnings | | | comprehensive | | | controlling | | | |

| | | | | (a) | | | stock | | | capital | | | reinvested | | | loss | | | interests | | | Total |

| | | | | | | | | | | | | | | | | | | | |

December 31, 2011 | | 578,405 | | $ | 6 | | $ | 6,813 | | $ | 4,797 | | $ | (788) | | $ | 268 | | $ | 11,096 |

Common stock issued (b) | | 1,115 | | | | | | 32 | | | | | | | | | | | | 32 |

Stock-based compensation (c) | | | | | | | | 17 | | | | | | | | | | | | 17 |

Net income | | | | | | | | | | | 541 | | | | | | 4 | | | 545 |

| Dividends, dividend equivalents | | | | | | | | | | | | | | | | | | | | |

| | and distributions (d) | | | | | | | | | | | (209) | | | | | | (4) | | | (213) |

| Other comprehensive | | | | | | | | | | | | | | | | | | | | |

| | income (loss) | | | | | | | | | | | | | | 58 | | | | | | 58 |

March 31, 2012 | | 579,520 | | $ | 6 | | $ | 6,862 | | $ | 5,129 | | $ | (730) | | $ | 268 | | $ | 11,535 |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

December 31, 2010 | | 483,391 | | $ | 5 | | $ | 4,602 | | $ | 4,082 | | $ | (479) | | $ | 268 | | $ | 8,478 |

Common stock issued (b) | | 1,227 | | | | | | 40 | | | | | | | | | | | | 40 |

Stock-based compensation (c) | | | | | | | | (5) | | | | | | | | | | | | (5) |

Net income | | | | | | | | | | | 401 | | | | | | 4 | | | 405 |

| Dividends, dividend equivalents | | | | | | | | | | | | | | | | | | | | |

| | and distributions (d) | | | | | | | | | | | (171) | | | | | | (4) | | | (175) |

| Other comprehensive | | | | | | | | | | | | | | | | | | | | |

| | income (loss) | | | | | | | | | | | | | | 55 | | | | | | 55 |

March 31, 2011 | | 484,618 | | $ | 5 | | $ | 4,637 | | $ | 4,312 | | $ | (424) | | $ | 268 | | $ | 8,798 |

| (a) | Shares in thousands. Each share entitles the holder to one vote on any question presented to any shareowners' meeting. |

| (b) | Each period includes shares of common stock issued through various stock and incentive compensation plans. |

| (c) | The three months ended March 31, 2012 and 2011 include $29 million and $17 million of stock-based compensation expense related to new and existing unvested equity awards. These periods also include the reclassification of $(12) million and $(22) million related primarily to the reclassification from "Stock-based compensation" to "Common stock issued" for the issuance of common stock after applicable equity award vesting periods and tax adjustments related to stock-based compensation. |

| (d) | "Earnings reinvested" includes dividends and dividend equivalents on PPL Corporation common stock and restricted stock units. "Noncontrolling interests" includes dividends, redemptions and distributions to noncontrolling interests. |

The accompanying Notes to Condensed Financial Statements are an integral part of the financial statements.

|

| PPL Energy Supply, LLC and Subsidiaries |

| (Unaudited) |

| (Millions of Dollars) |

| | | | | | Three Months Ended March 31, |

| | | | | | 2012 | | 2011 |

| Operating Revenues | | | | | | |

| | Wholesale energy marketing | | | | | | |

| | | Realized | | $ | 1,208 | | $ | 1,038 |

| | | Unrealized economic activity (Note 14) | | | 852 | | | 57 |

| | Wholesale energy marketing to affiliate | | | 21 | | | 6 |

| | Unregulated retail electric and gas | | | 224 | | | 147 |

| | Net energy trading margins | | | 8 | | | 11 |

| | Energy-related businesses | | | 96 | | | 110 |

| | Total Operating Revenues | | | 2,409 | | | 1,369 |

| | | | | | | | | | |

| Operating Expenses | | | | | | |

| | Operation | | | | | | |

| | | Fuel | | | 211 | | | 260 |

| | | Energy purchases | | | | | | |

| | | | Realized | | | 659 | | | 314 |

| | | | Unrealized economic activity (Note 14) | | | 591 | | | (18) |

| | | Energy purchases from affiliate | | | 1 | | | 1 |

| | | Other operation and maintenance | | | 255 | | | 245 |

| | Depreciation | | | 64 | | | 59 |

| | Taxes, other than income | | | 18 | | | 16 |

| | Energy-related businesses | | | 92 | | | 108 |

| | Total Operating Expenses | | | 1,891 | | | 985 |

| | | | | | | | | | |

Operating Income | | | 518 | | | 384 |

| | | | | | | | | | |

Other Income (Expense) - net | | | 5 | | | 14 |

| | | | | | | | | | |

Other-Than-Temporary Impairments | | | | | | 1 |

| | | | | | | | | | |

Interest Income from Affiliates | | | | | | 3 |

| | | | | | | | | | |

Interest Expense | | | 37 | | | 47 |

| | | | | | | | | | |

Income from Continuing Operations Before Income Taxes | | | 486 | | | 353 |

| | | | | | | | | | |

Income Taxes | | | 177 | | | 142 |

| | | | | | | | | | |

Income from Continuing Operations After Income Taxes | | | 309 | | | 211 |

| | | | | | | | | | |

Income (Loss) from Discontinued Operations (net of income taxes) | | | | | | 3 |

| | | | | | | | | | |

Net Income Attributable to PPL Energy Supply | | $ | 309 | | $ | 214 |

| | | | | | | | | | |

| The accompanying Notes to Condensed Financial Statements are an integral part of the financial statements. |

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME |

| PPL Energy Supply, LLC and Subsidiaries |

| (Unaudited) |

| (Millions of Dollars) |

| | | | | Three Months Ended March 31, |

| | | | | 2012 | | 2011 |

| | | | | | | | | |

Net income | | $ | 309 | | $ | 214 |

| | | | | | | | | |

| Other comprehensive income (loss): | | | | | | |

| Amounts arising during the period - gains (losses), net of tax (expense) benefit: | | | | | | |

| | Available-for-sale securities, net of tax of ($28), ($12) | | | 22 | | | 12 |

| | Qualifying derivatives, net of tax of ($57), ($34) | | | 56 | | | 50 |

| Reclassifications to net income - (gains) losses, net of tax expense (benefit): | | | | | | |

| | Available-for-sale securities, net of tax of $2, $5 | | | (3) | | | (7) |

| | Qualifying derivatives, net of tax of $93, $54 | | | (139) | | | (79) |

| | Equity investee's other comprehensive (income) loss, net of tax of $0, $0 | | | | | | 2 |

| | Defined benefit plans: | | | | | | |

| | | Prior service costs, net of tax of ($1), ($1) | | | 1 | | | 1 |

| | | Net actuarial loss, net of tax of $2, $0 | | | 5 | | | 1 |

Total other comprehensive income (loss) attributable to PPL Energy Supply | | | (58) | | | (20) |

| | | | | | | | | |

Comprehensive income (loss) attributable to PPL Energy Supply | | $ | 251 | | $ | 194 |

| | | | | | | | | |

| The accompanying Notes to Condensed Financial Statements are an integral part of the financial statements. |

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS |

| PPL Energy Supply, LLC and Subsidiaries |

| (Unaudited) |

| (Millions of Dollars) |

| | | | | | | | | | |

| | | | | | Three Months Ended March 31, |

| | | | | | 2012 | | 2011 |

| Cash Flows from Operating Activities | | | | | | |

| | Net income | | $ | 309 | | $ | 214 |

| | Adjustments to reconcile net income to net cash provided by operating activities | | | | | | |

| | | Depreciation | | | 64 | | | 59 |

| | | Amortization | | | 38 | | | 33 |

| | | Defined benefit plans - expense | | | 10 | | | 9 |

| | | Deferred income taxes and investment tax credits | | | 161 | | | 105 |

| | | Unrealized (gains) losses on derivatives, and other hedging activities | | | (260) | | | (105) |

| | | Other | | | 17 | | | 13 |

| | Change in current assets and current liabilities | | | | | | |

| | | Accounts receivable | | | 37 | | | 69 |

| | | Accounts payable | | | (24) | | | (92) |

| | | Unbilled revenues | | | 6 | | | 122 |

| | | Fuel, materials and supplies | | | (51) | | | (17) |

| | | Prepayments | | | (7) | | | 51 |

| | | Taxes | | | (26) | | | 42 |

| | | Counterparty collateral | | | 65 | | | (195) |

| | | Accrued interest | | | 23 | | | 25 |

| | | Other | | | (26) | | | (12) |

| | Other operating activities | | | | | | |

| | | Defined benefit plans - funding | | | (69) | | | (127) |

| | | Other assets | | | (12) | | | (3) |

| | | Other liabilities | | | (1) | | | 11 |

| | | | Net cash provided by operating activities | | | 254 | | | 202 |

| Cash Flows from Investing Activities | | | | | | |

| | Expenditures for property, plant and equipment | | | (199) | | | (127) |

| | Proceeds from the sale of certain non-core generation facilities | | | | | | 381 |

| | Purchases of nuclear plant decommissioning trust investments | | | (38) | | | (79) |

| | Proceeds from the sale of nuclear plant decommissioning trust investments | | | 34 | | | 75 |

| | Net (increase) decrease in notes receivable from affiliates | | | 198 | | | (458) |

| | Net (increase) decrease in restricted cash and cash equivalents | | | (19) | | | (5) |

| | Other investing activities | | | (17) | | | (11) |

| | | | Net cash provided by (used in) investing activities | | | (41) | | | (224) |

| Cash Flows from Financing Activities | | | | | | |

| | Distributions to Member | | | (557) | | | (81) |

| | Cash included in net assets of subsidiary distributed to Member | | | | | | (325) |

| | Net increase (decrease) in short-term debt | | | 100 | | | 350 |

| | | | Net cash provided by (used in) financing activities | | | (457) | | | (56) |

Net Increase (Decrease) in Cash and Cash Equivalents | | | (244) | | | (78) |

| | Cash and Cash Equivalents at Beginning of Period | | | 379 | | | 661 |

| | Cash and Cash Equivalents at End of Period | | $ | 135 | | $ | 583 |

| | | | | | | | | | |

| The accompanying Notes to Condensed Financial Statements are an integral part of the financial statements. |

|

| PPL Energy Supply, LLC and Subsidiaries |

| (Unaudited) |

| (Millions of Dollars) |

| | | | | | March 31, | | December 31, |

| | | | | | 2012 | | 2011 |

| Assets | | | | | | |

| | | | | | | | | | |

| Current Assets | | | | | | |

| | Cash and cash equivalents | | $ | 135 | | $ | 379 |

| | Restricted cash and cash equivalents | | | 164 | | | 145 |

| | Accounts receivable (less reserve: 2012, $26; 2011, $15) | | | | | | |

| | | Customer | | | 134 | | | 169 |

| | | Other | | | 24 | | | 31 |

| | Accounts receivable from affiliates | | | 93 | | | 89 |

| | Unbilled revenues | | | 396 | | | 402 |

| | Note receivable from affiliate | | | | | | 198 |

| | Fuel, materials and supplies | | | 347 | | | 298 |

| | Prepayments | | | 21 | | | 14 |

| | Price risk management assets | | | 3,222 | | | 2,527 |

| | Other current assets | | | 14 | | | 11 |

| | Total Current Assets | | | 4,550 | | | 4,263 |

| | | | | | | | |

| Investments | | | | | | |

| | Nuclear plant decommissioning trust funds | | | 693 | | | 640 |

| | Other investments | | | 45 | | | 40 |

| | Total Investments | | | 738 | | | 680 |

| | | | | | | | |

| Property, Plant and Equipment | | | | | | |

| | Non-regulated property, plant and equipment | | | | | | |

| | | Generation | | | 10,544 | | | 10,517 |

| | | Nuclear fuel | | | 718 | | | 658 |

| | | Other | | | 251 | | | 245 |

| | Less: accumulated depreciation - non-regulated property, plant and equipment | | | 5,651 | | | 5,573 |

| | | Non-regulated property, plant and equipment, net | | | 5,862 | | | 5,847 |

| | Construction work in progress | | | 704 | | | 639 |

| | Property, Plant and Equipment, net (a) | | | 6,566 | | | 6,486 |

| | | | | | | | |

| Other Noncurrent Assets | | | | | | |

| | Goodwill | | | 86 | | | 86 |

| | Other intangibles (a) | | | 387 | | | 386 |

| | Price risk management assets | | | 1,149 | | | 896 |

| | Other noncurrent assets | | | 390 | | | 382 |

| | Total Other Noncurrent Assets | | | 2,012 | | | 1,750 |

| | | | | | | | |

Total Assets | | $ | 13,866 | | $ | 13,179 |

| (a) | At March 31, 2012 and December 31, 2011, includes $417 million and $416 million of PP&E, consisting primarily of "Generation," including leasehold improvements, and $10 million and $11 million of "Other intangibles" from the consolidation of a VIE that is the owner/lessor of the Lower Mt. Bethel plant. |

The accompanying Notes to Condensed Financial Statements are an integral part of the financial statements.

| CONDENSED CONSOLIDATED BALANCE SHEETS |

| PPL Energy Supply, LLC and Subsidiaries |

| (Unaudited) |

| (Millions of Dollars) |

| | | | | | | March 31, | | | December 31, |

| | | | | | | 2012 | | | 2011 |

| Liabilities and Equity | | | | | | |

| | | | | | | | | | |

| Current Liabilities | | | | | | |

| | Short-term debt | | $ | 500 | | $ | 400 |

| | Accounts payable | | | 427 | | | 472 |

| | Accounts payable to affiliates | | | 19 | | | 14 |

| | Taxes | | | 64 | | | 90 |

| | Interest | | | 53 | | | 30 |

| | Price risk management liabilities | | | 2,129 | | | 1,560 |

| | Counterparty collateral | | | 213 | | | 148 |

| | Deferred income taxes | | | 367 | | | 315 |

| | Other current liabilities | | | 170 | | | 196 |

| | Total Current Liabilities | | | 3,942 | | | 3,225 |

| | | | | | | | | | |

Long-term Debt | | | 3,024 | | | 3,024 |

| | | | | | | |

| Deferred Credits and Other Noncurrent Liabilities | | | | | | |

| | Deferred income taxes | | | 1,308 | | | 1,223 |

| | Investment tax credits | | | 148 | | | 136 |

| | Price risk management liabilities | | | 1,025 | | | 785 |

| | Accrued pension obligations | | | 150 | | | 214 |

| | Asset retirement obligations | | | 353 | | | 349 |

| | Other deferred credits and noncurrent liabilities | | | 185 | | | 186 |

| | Total Deferred Credits and Other Noncurrent Liabilities | | | 3,169 | | | 2,893 |

| | | | | | | | | | |

| Commitments and Contingent Liabilities (Note 10) | | | | | | |

| | | | | | | |

| Equity | | | | | | |

| | Member's equity | | | 3,713 | | | 4,019 |

| | Noncontrolling interests | | | 18 | | | 18 |

| | Total Equity | | | 3,731 | | | 4,037 |

| | | | | | | | | | |

Total Liabilities and Equity | | $ | 13,866 | | $ | 13,179 |

| | | | | | | | | | |

| The accompanying Notes to Condensed Financial Statements are an integral part of the financial statements. |

|

| PPL Energy Supply, LLC and Subsidiaries |

| (Unaudited) |

| (Millions of Dollars) |

| | | | | | | | | | |

| | | | | | Non- | | | |

| | | Member's | | controlling | | | |

| | | equity | | interests | | Total |

| | | | | | | | | | |

December 31, 2011 | | $ | 4,019 | | $ | 18 | | $ | 4,037 |

Net income | | | 309 | | | | | | 309 |

Other comprehensive income (loss) | | | (58) | | | | | | (58) |

Distributions | | | (557) | | | | | | (557) |

March 31, 2012 | | $ | 3,713 | | $ | 18 | | $ | 3,731 |

| | | | | | | | | | |

December 31, 2010 | | $ | 4,491 | | $ | 18 | | $ | 4,509 |

Net income | | | 214 | | | | | | 214 |

Other comprehensive income (loss) | | | (20) | | | | | | (20) |

Distributions | | | (81) | | | | | | (81) |

Distribution of membership interest in PPL Global (a) | | | (1,288) | | | | | | (1,288) |

March 31, 2011 | | $ | 3,316 | | $ | 18 | | $ | 3,334 |

| (a) | In January 2011, PPL Energy Supply distributed its entire membership interest in PPL Global to PPL Energy Supply's parent, PPL Energy Funding. The distribution was made based on the book value of the assets and liabilities of PPL Global with financial effect as of January 1, 2011, and no gains or losses were recognized on the distribution. |

The accompanying Notes to Condensed Financial Statements are an integral part of the financial statements.

(THIS PAGE LEFT BLANK INTENTIONALLY.)

|

| PPL Electric Utilities Corporation and Subsidiaries |

| (Unaudited) |

| (Millions of Dollars) |

| | | | | Three Months Ended March 31, |

| | | | | 2012 | | 2011 |

| Operating Revenues | | | | | | |

| | Retail electric | | $ | 457 | | $ | 554 |

| | Electric revenue from affiliate | | | 1 | | | 4 |

| | Total Operating Revenues | | | 458 | | | 558 |

| | | | | | | | | |

| Operating Expenses | | | | | | |

| | Operation | | | | | | |

| | | Energy purchases | | | 153 | | | 251 |

| | | Energy purchases from affiliate | | | 21 | | | 6 |

| | | Other operation and maintenance | | | 140 | | | 130 |

| | Depreciation | | | 39 | | | 33 |

| | Taxes, other than income | | | 26 | | | 35 |

| | Total Operating Expenses | | | 379 | | | 455 |

| | | | | | | | | |

Operating Income | | | 79 | | | 103 |

| | | | | | | | | |

Other Income (Expense) - net | | | 1 | | | |

| | | | | | | | | |

Interest Income from Affiliate | | | 1 | | | |

| | | | | | | | | |

Interest Expense | | | 24 | | | 24 |

| | | | | | | | | |

Income Before Income Taxes | | | 57 | | | 79 |

| | | | | | | | | |

Income Taxes | | | 20 | | | 23 |

| | | | | | | | | |

Net Income (a) | | | 37 | | | 56 |

| | | | | | | | | |

Distributions on Preferred Securities | | | 4 | | | 4 |

| | | | | | | | | |

Net Income Available to PPL Corporation | | $ | 33 | | $ | 52 |

| (a) | Net income approximates comprehensive income. |

| | The accompanying Notes to Condensed Financial Statements are an integral part of the financial statements. |

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS |

| PPL Electric Utilities Corporation and Subsidiaries |

| (Unaudited) |

| (Millions of Dollars) |

| | | | | | | | | | |

| | | | | | Three Months Ended March 31, |

| | | | | | 2012 | | 2011 |

| Cash Flows from Operating Activities | | | | | | |

| | Net income | | $ | 37 | | $ | 56 |

| | Adjustments to reconcile net income to net cash provided by (used in) operating activities | | | | | | |

| | | Depreciation | | | 39 | | | 33 |

| | | Amortization | | | 4 | | | |

| | | Defined benefit plans - expense | | | 9 | | | 4 |

| | | Deferred income taxes and investment tax credits | | | 58 | | | (29) |

| | | Other | | | 5 | | | 3 |

| | Change in current assets and current liabilities | | | | | | |

| | | Accounts receivable | | | (11) | | | (61) |

| | | Accounts payable | | | (25) | | | (52) |

| | | Unbilled revenues | | | 23 | | | 33 |

| | | Prepayments | | | (70) | | | 17 |

| | | Regulatory assets and liabilities | | | | | | 37 |

| | | Taxes | | | | | | 27 |

| | | Other | | | (1) | | | (17) |

| | Other operating activities | | | | | | |

| | | Defined benefit plans- funding | | | (54) | | | (98) |

| | | Other assets | | | | | | 1 |

| | | Other liabilities | | | (24) | | | (1) |

| | | | Net cash provided by (used in) operating activities | | | (10) | | | (47) |

| | | | | | | | | | |

| Cash Flows from Investing Activities | | | | | | |

| | Expenditures for property, plant and equipment | | | (121) | | | (129) |

| | Other investing activities | | | (1) | | | 4 |

| | | | Net cash provided by (used in) investing activities | | | (122) | | | (125) |

| | | | | | | | | | |

| Cash Flows from Financing Activities | | | | | | |

| | Common stock dividends to PPL | | | (35) | | | (18) |

| | Dividends on preferred securities | | | (4) | | | (4) |

| | | | Net cash provided by (used in) financing activities | | | (39) | | | (22) |

| | | | | | | | | | |

Net Increase (Decrease) in Cash and Cash Equivalents | | | (171) | | | (194) |

Cash and Cash Equivalents at Beginning of Period | | | 320 | | | 204 |

Cash and Cash Equivalents at End of Period | | $ | 149 | | $ | 10 |

| | | | | | | | | | |

| The accompanying Notes to Condensed Financial Statements are an integral part of the financial statements. |

|

| PPL Electric Utilities Corporation and Subsidiaries |

| (Unaudited) |

| (Millions of Dollars, shares in thousands) |

| | | | | | | | | | |

| | | | | | March 31, | | December 31, |

| | | | | | 2012 | | 2011 |

| Assets | | | | | | |

| | | | | | | | | | |

| Current Assets | | | | | | |

| | Cash and cash equivalents | | $ | 149 | | $ | 320 |

| | Accounts receivable (less reserve: 2012, $17; 2011, $17) | | | | | | |

| | | Customer | | | 287 | | | 271 |

| | | Other | | | 8 | | | 9 |

| | Accounts receivable from affiliates | | | 32 | | | 35 |

| | Unbilled revenues | | | 75 | | | 98 |

| | Materials and supplies | | | 39 | | | 42 |

| | Prepayments | | | 148 | | | 78 |

| | Other current assets | | | 32 | | | 30 |

| | Total Current Assets | | | 770 | | | 883 |

| | | | | | | | | | |

| Property, Plant and Equipment | | | | | | |

| | Regulated utility plant | | | 5,932 | | | 5,830 |

| | Less: accumulated depreciation - regulated utility plant | | | 2,241 | | | 2,217 |

| | | Regulated utility plant, net | | | 3,691 | | | 3,613 |

| | Other, net | | | 2 | | | 2 |

| | Construction work in progress | | | 235 | | | 242 |

| | Property, Plant and Equipment, net | | | 3,928 | | | 3,857 |

| | | | | | | | | | |

| Other Noncurrent Assets | | | | | | |

| | Regulatory assets | | | 731 | | | 729 |

| | Intangibles | | | 157 | | | 155 |

| | Other noncurrent assets | | | 81 | | | 81 |

| | Total Other Noncurrent Assets | | | 969 | | | 965 |

| | | | | | | | | | |

Total Assets | | $ | 5,667 | | $ | 5,705 |

| | | | | | | | | | |

| The accompanying Notes to Condensed Financial Statements are an integral part of the financial statements. |

| CONDENSED CONSOLIDATED BALANCE SHEETS |

| PPL Electric Utilities Corporation and Subsidiaries |

| (Unaudited) |

| (Millions of Dollars, shares in thousands) |

| | | | | | | | | | |

| | | | | | March 31, | | December 31, |

| | | | | | 2012 | | 2011 |

| Liabilities and Equity | | | | | | |

| | | | | | | | | | |

| Current Liabilities | | | | | | |

| | Accounts payable | | $ | 150 | | $ | 171 |

| | Accounts payable to affiliates | | | 61 | | | 64 |

| | Interest | | | 19 | | | 24 |

| | Regulatory liabilities | | | 53 | | | 53 |

| | Customer deposits and prepayments | | | 16 | | | 39 |

| | Vacation | | | 24 | | | 22 |

| | Other current liabilities | | | 69 | | | 47 |

| | Total Current Liabilities | | | 392 | | | 420 |

| | | | | | | | | | |

Long-term Debt | | | 1,718 | | | 1,718 |

| | | | | | | | | | |

| Deferred Credits and Other Noncurrent Liabilities | | | | | | |

| | Deferred income taxes | | | 1,167 | | | 1,115 |

| | Investment tax credits | | | 4 | | | 5 |

| | Accrued pension obligations | | | 136 | | | 186 |

| | Regulatory liabilities | | | 12 | | | 7 |

| | Other deferred credits and noncurrent liabilities | | | 115 | | | 129 |

| | Total Deferred Credits and Other Noncurrent Liabilities | | | 1,434 | | | 1,442 |

| | | | | | | | | | |

| Commitments and Contingent Liabilities (Notes 6 and 10) | | | | | | |

| | | | | | | | | | |

| Shareowners' Equity | | | | | | |

| | Preferred securities | | | 250 | | | 250 |

| | Common stock - no par value (a) | | | 364 | | | 364 |

| | Additional paid-in capital | | | 979 | | | 979 |

| | Earnings reinvested | | | 530 | | | 532 |

| | Total Equity | | | 2,123 | | | 2,125 |

| | | | | | | | | | |

Total Liabilities and Equity | | $ | 5,667 | | $ | 5,705 |

| (a) | 170,000 shares authorized; 66,368 shares issued and outstanding at March 31, 2012 and December 31, 2011. |

The accompanying Notes to Condensed Financial Statements are an integral part of the financial statements.

CONDENSED CONSOLIDATED STATEMENTS OF SHAREOWNERS' EQUITY |

| PPL Electric Utilities Corporation and Subsidiaries |

| (Unaudited) |

| (Millions of Dollars) |

| | | | | | | | | | | | | | | |

| | | | | Common | | | | | | | | | | |

| | | | | stock | | | | | | | | | | |

| | | | | shares | | Preferred | | | | Additional | | | | |

| | | | | outstanding | | securities | | Common | | paid-in | | Earnings | | |

| | | | | (a) | | (b) | | stock | | capital | | reinvested | | Total |

| | | | | | | | | | | | | | | | | | | | |

December 31, 2011 | | 66,368 | | $ | 250 | | $ | 364 | | $ | 979 | | $ | 532 | | $ | 2,125 |

Net income | | | | | | | | | | | | | | 37 | | | 37 |

Cash dividends declared on preferred securities | | | | | | | | | | | | | | (4) | | | (4) |

Cash dividends declared on common stock | | | | | | | | | | | | | | (35) | | | (35) |

March 31, 2012 | | 66,368 | | $ | 250 | | $ | 364 | | $ | 979 | | $ | 530 | | $ | 2,123 |

| | | | | | | | | | | | | | | | | | | | |

December 31, 2010 | | 66,368 | | $ | 250 | | $ | 364 | | $ | 879 | | $ | 451 | | $ | 1,944 |

Net income | | | | | | | | | | | | | | 56 | | | 56 |

Cash dividends declared on preferred securities | | | | | | | | | | | | | | (4) | | | (4) |

Cash dividends declared on common stock | | | | | | | | | | | | | | (18) | | | (18) |

March 31, 2011 | | 66,368 | | $ | 250 | | $ | 364 | | $ | 879 | | $ | 485 | | $ | 1,978 |

| (a) | Shares in thousands. All common shares of PPL Electric stock are owned by PPL. |

| (b) | In April 2012, PPL Electric gave notice that it had elected to redeem all of its outstanding preference stock on June 18, 2012. See Note 7 for additional information. |

| | The accompanying Notes to Condensed Financial Statements are an integral part of the financial statements. |

|

| LG&E and KU Energy LLC and Subsidiaries |

| (Unaudited) | | | | | | |

| (Millions of Dollars) |

| | | | | | | | | | |

| | | | | | Three Months Ended March 31, |

| | | | | | 2012 | | 2011 |

| | | | | | | |

Operating Revenues | | $ | 705 | | $ | 766 |

| | | | | | | |

| Operating Expenses | | | | | | |

| | Operation | | | | | | |

| | | Fuel | | | 213 | | | 215 |

| | | Energy purchases | | | 74 | | | 107 |

| | | Other operation and maintenance | | | 206 | | | 181 |

| | Depreciation | | | 86 | | | 81 |

| | Taxes, other than income | | | 11 | | | 9 |

| | Total Operating Expenses | | | 590 | | | 593 |

| | | | | | | | | | |

Operating Income | | | 115 | | | 173 |

| | | | | | | | | | |

Other Income (Expense) - net | | | (3) | | | (1) |

| | | | | | | |

Interest Expense | | | 38 | | | 36 |

| | | | | | | | | | |

Income Before Income Taxes | | | 74 | | | 136 |

| | | | | | | | | | |

Income Taxes | | | 21 | | | 49 |

| | | | | | | | | | |

| Net Income | | $ | 53 | | $ | 87 |

The accompanying Notes to Condensed Financial Statements are an integral part of the financial statements.

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME |

| LG&E and KU Energy LLC and Subsidiaries |

| (Unaudited) |

| (Millions of Dollars) |

| | | | | | | | | | |

| | | | | | Three Months Ended March 31, |

| | | | | | 2012 | | 2011 |

| | | | | | | | | | |

Net income | | $ | 53 | | $ | 87 |

| | | | | | | | | | |

| Other comprehensive income (loss): | | | | | | |

| Amounts arising during the period - gains (losses), net of tax (expense) | | | | | | |

| | benefit: | | | | | | |

| | | Equity investee's other comprehensive income (loss), net | | | | | | |

| | | | of tax of $2, $0 | | | (4) | | | (1) |

| Reclassification to net income - (gains) losses, net of tax expense | | | | | | |

| | (benefit): | | | | | | |