Exhibit 99.1

Investor Presentation January 6 - 7, 2022 DRAFT 1/5/2022 | 9:20 AM PT

Important Disclosures p. 2 Forward - Looking Statements This presentation and the accompanying oral presentation includes forward - looking statements, as that term is defined for purposes of applicable securities laws, about our industry, our future financial performance, business plans and expectations. These statements are, in essence, attempts to anticipate or forecast future events, and thus subject to many risks and uncertainties. These forward - looking statements are based on our management's current expectations, beliefs, projections, and related to future plans and strategies, anticipated events, outcomes, or trends, as well as a number of assumptions concerning future events, are not historical facts and are identified by words such as “will,” “may,” “could,” “should,” “would,” “believe,” “expect,” anticipate” and similar expressions. Forward - looking statements in this presentation include, among other matters, statements regarding our business plans and strategies, share repurchase plans, general economic trends, strategic initiatives we have announced, including forecasted reductions in the Company’s cost structure and future run rates, growth scenarios and performance targets and guidance with respect to loans held for investment, average deposits, net interest margin noninterest income and noninterest expense. Readers should note, however, that all statements in this presentation other than assertions of historical fact are forward - looking in nature. These statements are subject to risks, uncertainties, assumptions and other important factors set forth in our SEC filings, including but not limited to our Annual Report on Form 10 - K for the year ended December 31, 2020, and in our subsequent quarterly reports on Form 10 - Q and current reports on Forms 8 - K. Many of these factors and events that affect the volatility in our stock price and shareholders’ response to those events and factors are beyond our control. Such factors could cause actual results to differ materially and adversely from the results discussed or implied in the forward - looking statements. These risks include, without limitation, changes in general political and economic conditions that impact our markets and our business, actions by the Federal Reserve Board and financial market conditions that affect monetary and fiscal policy, regulatory and legislative findings or actions that may increase capital requirements or otherwise constrain our ability to do business, including restrictions that could be imposed by our regulators on certain aspects of our operations, our growth initiatives and acquisition activities, and our capital management plan, risks related to our ability to: retain adequate key personnel to operate our business, realize the expected cost savings from restructuring activities and cost containment measures that we have undertaken or have announced, continue to expand our commercial and consumer banking operations, grow our franchise and capitalize on market opportunities, cost - effectively manage our overall growth efforts to attain the desired operational and financial outcomes, manage the losses inherent in our loan portfolio, manage the growth and increasing concentration of commercial real estate in our loan portfolio, improve long - term shareholder value through effective use of our surplus capital, make accurate estimates of the value of our non - cash assets and liabilities, maintain electronic and physical security of customer data, respond to our restrictive and complex regulatory environment and effectively respond to the changes in the global, national, state and local markets caused by or related to the COVID - 19 pandemic, and the success of mitigation measures, including vaccine programs. Actual results may fall materially short of our expectations and projections, and we may be unable to execute on our strategic initiatives, or we may change our plans or take additional actions that differ in material ways from our current intentions. Accordingly, we can give no assurance of future performance, and you should not rely unduly on forward - looking statements. All forward - looking statements are based on information available to us as of the date hereof, and we do not undertake to update or revise any forward - looking statements for any reason. As used in this presentation, “HMST,” “HomeStreet,” the “Company,” “we,” “us,” “our,” or similar references refer to HomeStreet, Inc., a Washington corporation, and its consolidated subsidiaries, HomeStreet Bank (the “Bank”) and HomeStreet Capital Corporation (“Capital”). Non - GAAP Financial Measures This presentation contains supplemental financial information determined by methods other than in accordance with U.S. generally accepted accounting principles (“GAAP”). Information on any non - GAAP financial measures such as core measures or tangible measures referenced in this presentation, including a reconciliation of those measures to GAAP measures, may be found in the appendix to this presentation.

Today’s Presenters Mr. Mason has been the Company’s Chief Executive Officer and HomeStreet Bank’s Chairman and Chief Executive Officer since January 2010 and the Chairman of the Company since March 2015. From January 2010 until March 2015, Mr. Mason was the Vice Chairman of the Company’s Board. From 1998 to 2002, Mr. Mason was President, Chief Executive Officer and Chief Lending Officer for Bank Plus Corporation and its wholly owned banking subsidiary, Fidelity Federal Bank, where Mr. Mason also served as the Chief Financial Officer from 1994 to 1995 and as Chairman of the board of directors from 1998 to 2002. From February 2008 to October 2008, Mr. Mason served as President of a startup energy company, TEFCO, LLC. He has also served on the boards of directors of Hanmi Financial Corp., San Diego Community Bank, and The Bjurman Barry Family of Mutual Funds. Mr. Mason is on the boards of directors of the Pacific Bankers Management Institute (the parent company of the Pacific Coast Banking School) and The Washington Bankers Association, and is an advisory board member of Seattle University’s Albers School of Business and Economics. Mr. Mason is a certified public accountant (inactive) and holds a bachelor’s degree in Business Administration with an emphasis in Accounting from California State Polytechnic University. Mark Mason Chairman, Chief Executive Officer and President Mr. Michel joined HomeStreet in May 2020 and serves as Executive Vice President, Chief Financial Officer. His duties include the management of treasury, financial reporting, management reporting, financial planning, and tax. Prior to joining HomeStreet, Mr. Michel was Chief Financial Officer of First Foundation, Inc., from 2007 through 2020. His prior experience includes Chief Financial Officer and senior finance roles at other banks and specialty finance companies, and he was a Senior Manager at Deloitte & Touche. Mr. Michel holds a BA in Accounting from the University of Notre Dame and is a Certified Public Accountant - California (inactive). John Michel Executive Vice President & Chief Financial Officer p. 3

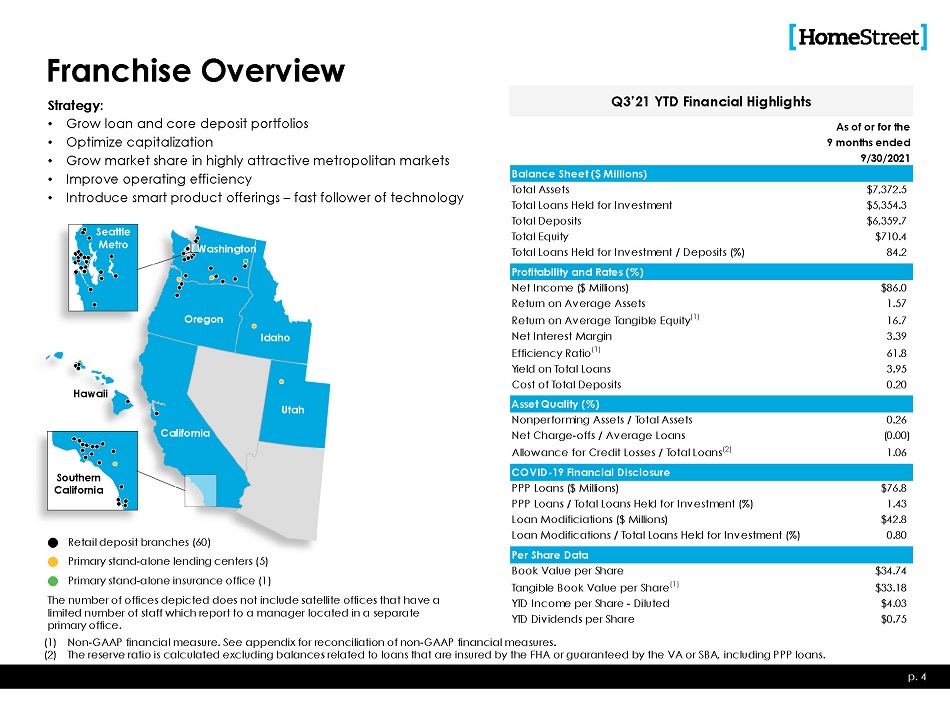

Se attle Metro U tah California H a w ai i Southern Cali fo r nia Franchise Overview Strategy: • Grow loan and core deposit portfolios • Optimize capitalization • Grow market share in highly attractive metropolitan markets • Improve operating efficiency • Introduce smart product offerings – fast follower of technology Retail deposit branches (60) Primary stand - alone lending centers (5) Primary stand - alone insurance office (1) The number of offices depicted does not include satellite offices that have a limited number of staff which report to a manager located in a separate primary office. p. 4 Washington Total Loans Held for Investment / Deposits (%) 84.2 Profitability and Rates (%) Net Income ($ Millions) $86.0 Return on Average Assets 1.57 Oregon Return on Average Tangible Equity (1) 16.7 Idaho Net Interest Margin 3.39 Efficiency Ratio (1) 61.8 Y i e l d o n T o t a l L o a n s 3.95 Cost of Total Deposits 0.20 Q3’21 YTD Financial Highlights As of or for the 9 m o n t h s e n d e d 9/30/2021 Balance Sheet ($ Millions) T o t a l A ss e t s $7,372.5 Total Loans Held for Investment $5,354.3 Total Deposits $6,359.7 T o t a l E q u it y $710.4 A ss e t Q u a li t y ( % ) Nonperforming Assets / Total Assets Net Charge - offs / Average Loans Allowance for Credit Losses / Total Loans (2) 0.26 (0.00) 1.06 COVID - 19 Financial Disclosure PPP Loans ($ Millions) PPP Loans / Total Loans Held for Investment (%) Loan Modificiations ($ Millions) Loan Modifications / Total Loans Held for Investment (%) $76 . 8 1 . 43 $42 . 8 0 . 80 Per Share Data Book Value per Share Tangible Book Value per Share (1) Y T D I n c o m e p e r S h a r e - Dilut ed Y T D Di v i d e n d s p e r S h a r e $34 . 74 $33 . 18 $4 . 03 $0 . 75 (1) Non - GAAP financial measure. See appendix for reconciliation of non - GAAP financial measures. (2) The reserve ratio is calculated excluding balances related to loans that are insured by the FHA or guaranteed by the VA or SBA, including PPP loans.

HomeStreet Turns 100 • On August 18, 2021, HomeStreet, Inc. celebrated its 100 th anniversary • At that time, incorporations were either delivered by horseback, steam wheeler, or train • Of the nearly 2,900 incorporations filed that year, only 33 exist today • Things have changed much during the past century, but HomeStreet has always served its communities with the highest standards and care, surviving the Great Depression, wars, the Thrift Crisis, the Great Recession, and the current pandemic • We don’t know what challenges will face us in the future, but with our culture, employees and loyal customers we feel confident we will continue to thrive p . 5 University Village Apartments, Seattle, WA.

HomeStreet Bank Transformation Since the early 2010s, HomeStreet has been executing a strategy to convert from a legacy thrift to a full - service commercial and consumer bank. This conversion focused on the development of commercial lending and deposit product lines and reducing the size of our single family mortgage operations. S&P has recently recognized our successful conversion and HomeStreet’s Global Industry Classification Standard (“GICS”) code was changed to Regional Bank effective as of November 1, 2021. (GICS Code 40101015) Currently, HomeStreet is included in the following indices: • S&P Regional Banks Select Industry Index (as of December 2021) • S&P United States BMI Banks Index • S&P U.S. BMI Banks - Western Region • Russell 3000 • Nasdaq Composite Index As a result of the change in classification, HomeStreet may qualify for inclusion in other bank - only indices after the effective date. p . 6

Credit Investor Highlights p. 7 (1) Financial data as of or for the nine months ended 9/30/2021. (2) Non - GAAP financial measure. See appendix for reconciliation of non - GAAP financial measures. (3) Deposit market share data per S&P Global and FDIC Summary of Deposits as of 6/30/2021. (4) Data per S&P Global as of 9/30/2021. • Experienced management team successfully shifting to a full - service commercial and consumer bank and reducing the size of single family mortgage operations • Core earnings profile has helped build a strong capital base » 1.57% core return on average assets (1)(2) » 16.7% core return on average tangible equity (1)(2) • Solid asset quality and conservative credit culture with a history of strong credit quality » 0.26% nonperforming assets / total assets (1) » 0.00% net charge - offs / average loans (1) • Healthy capital position with excess capital to strategically deploy » 9.24% tangible common equity / tangible assets (1)(2) » 10.00% tier 1 leverage ratio (1) » 13.01% total risk - based capital ratio (1) • Significant presence in some of the largest, fastest growing and wealthiest metropolitan areas in the country » Deposit weighted average population growth and median household income growth in our markets are both above the nationwide average (3) » #8 in deposit market share in the Seattle - Tacoma - Bellevue, WA MSA (3) • Scarcity value – 5 th largest bank by assets headquartered in Washington (4)

Financial Highlights

Third Quarter 2021 Highlights p. 9 Quarterly Results • Net income of $27.2 million, or $1.31 per share • ROAE of 14.8%, ROATE of 15.6% (1) and ROAA of 1.48% • Efficiency ratio of 62.8% (1) • Net interest margin remained steady at 3.42% • Cost of deposits of 0.15% on September 30, 2021 • Noninterest bearing deposits: 26.8% of total deposits on September 30, 2021 • Book Value per share of $34.74 and tangible book value per share of $33.18 (1) on September 30, 2021 Year to Date Results • Net income of $86.0 million, or $4.03 per share • ROAE of 15.8%, ROATE of 16.7% (1) and ROAA of 1.57% • Efficiency ratio of 61.8% (1) Other Results • Repurchased a total of 372 , 622 shares at an average price of $ 40 . 26 per share during the quarter . 6 . 9 % of outstanding shares repurchased since beginning of the year • Declared and paid a quarterly cash dividend of $ 0 . 25 per share HomeStreet’s results during the first nine months of 2021 reflect its diversified business model, the benefits of its conservative credit culture and continuing focus on operating efficiency. (1) Non - GAAP financial measure. See appendix for reconciliation of non - GAAP financial measures.

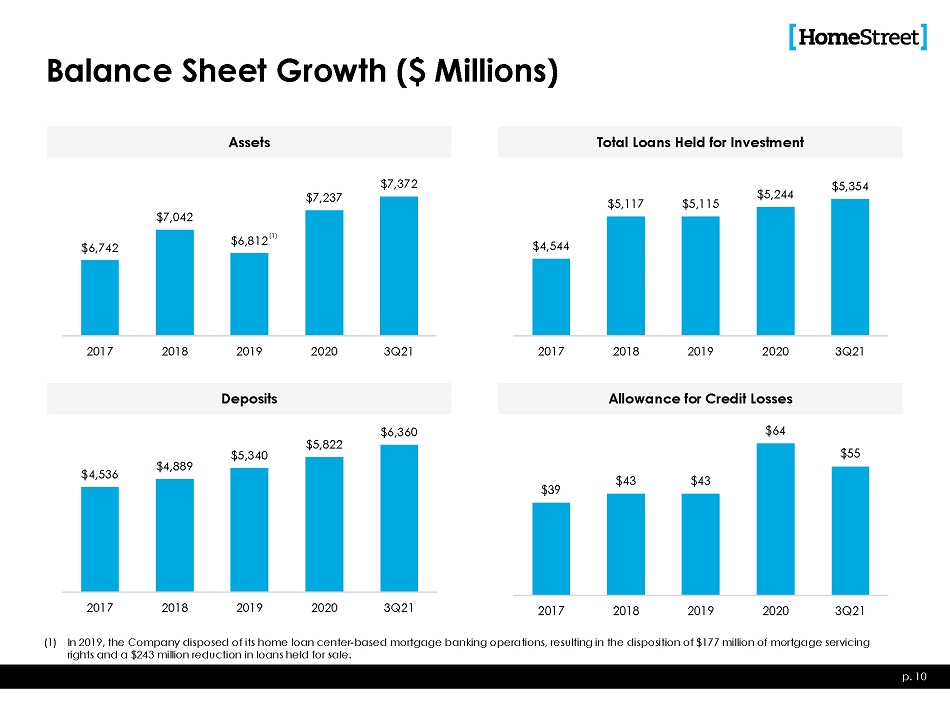

Balance Sheet Growth ($ Millions) $6 , 742 $7 , 042 $7 , 237 $6 , 81 2 ( 1 ) $7 , 372 2 0 17 2 0 18 2 0 19 2 0 20 3 Q 21 Assets Total Loans Held for Investment $4 , 544 $5 , 117 $5 , 115 $5 , 244 $5 , 354 2 0 17 2 0 18 2 0 19 2 0 20 3 Q 21 Deposits $4 , 536 $4 , 889 $5 , 340 $5 , 822 $6 , 360 2 0 1 7 2 0 1 8 2 0 1 9 2 0 2 0 3 Q 21 Allowance for Credit Losses $39 p. 10 $43 $43 $64 $55 2 0 1 7 2 0 1 8 2 0 1 9 2 0 2 0 3 Q 21 (1) In 2019, the Company disposed of its home loan center - based mortgage banking operations, resulting in the disposition of $177 million of mortgage servicing rights and a $243 million reduction in loans held for sale.

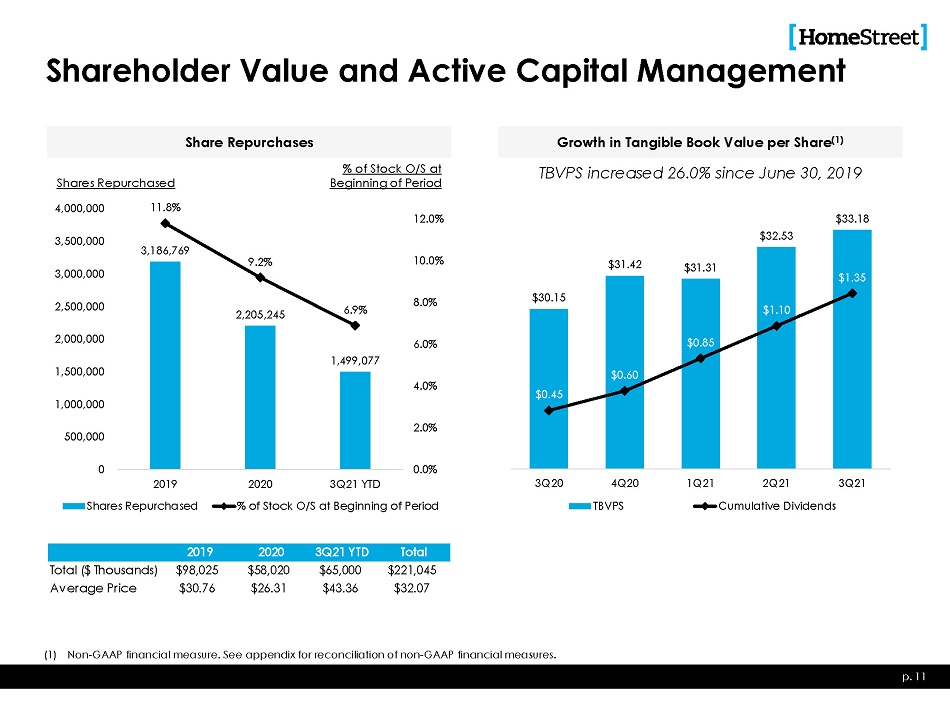

Shareholder Value and Active Capital Management TBVPS increased 26.0% since June 30, 2019 2019 2020 3 Q 2 1 YT D Total Total ($ Thousands) $98,025 $58,020 $65,000 $221,045 Average Price $30.76 $26.31 $43.36 $32.07 Share Repurchases Growth in Tangible Book Value per Share (1) 3,186,769 2,205,245 1,499,077 Shares Repurchased 4,0 0 0,00 0 11 . 8% 9 . 2% 6 . 9% 0.0% 2.0% 4.0% 6.0% 8.0% 10. 0 % 12. 0 % 0 500,000 1,0 0 0,000 1,5 0 0,000 2,0 0 0,000 2,5 0 0,000 3,0 0 0,000 3,5 0 0,000 20 1 9 2020 3Q21 YTD % of Stock O/S at Beginning of Period Shares Repurchased $30.15 $31.42 $31.31 $32.53 $33.18 $0 . 45 $0 . 60 $0 . 85 $1 . 10 $1 . 35 3 Q 20 4 Q 20 TBVPS 1 Q 21 3 Q 21 2Q21 Cumulative Dividends % of Stock O/S at B e g i nn i ng o f P e r i o d (1) Non - GAAP financial measure. See appendix for reconciliation of non - GAAP financial measures. p. 11

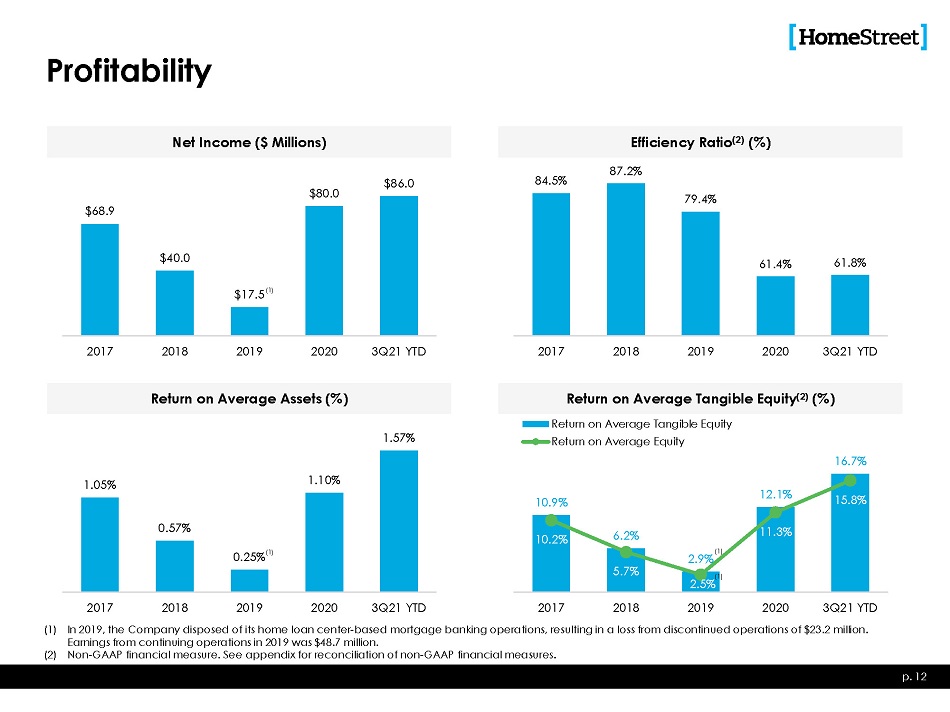

Profitability $68 . 9 $40 . 0 $80 . 0 $17.5 (1) $86 . 0 2 0 17 2 0 18 2 0 19 2 0 20 3Q21 YTD Net Income ($ Millions) Efficiency Ratio (2) (%) 84 . 5% 87 . 2% 79 . 4% 61 . 4% 61 . 8% 2 0 17 2 0 18 2 0 19 2 0 20 3Q21 YTD Return on Average Assets (%) 1 . 05% 0 . 57% 1 . 10% 0.25% (1) 1 . 57% 2017 2018 2019 2020 3Q21 YTD 2017 2018 2019 2020 3Q21 YTD (1) In 2019, the Company disposed of its home loan center - based mortgage banking operations, resulting in a loss from discontinued operations of $23.2 million. Earnings from continuing operations in 2019 was $48.7 million. Return on Average Tangible Equity (2) (%) 10 . 9% 6 . 2% 12 . 1% 16 . 7% 10 . 2% 5 . 7% 11 . 3% 15 . 8% (1) 2.9% (1) 2.5% Return on Average Tangible Equity Return on Average Equity (2) Non - GAAP financial measure. See appendix for reconciliation of non - GAAP financial measures. p. 12

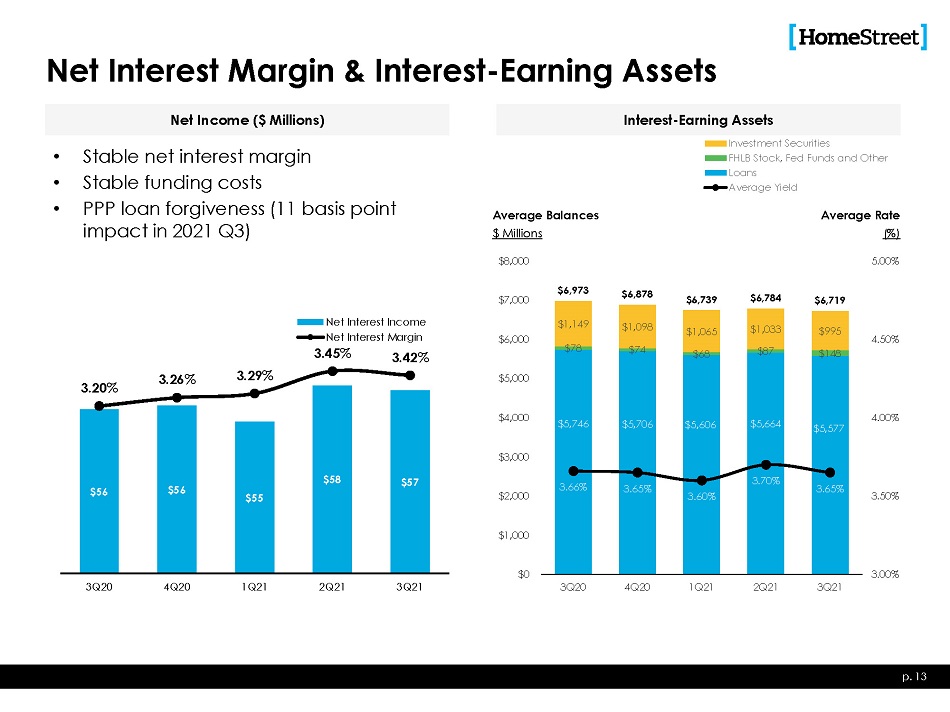

$5,746 $5,706 $5,606 $5,664 $5,577 $78 $1,149 $1,098 $74 $1,065 $68 $1,033 $87 $995 $148 $6,973 $6,878 $6,739 $6,784 $6,719 3.66% 3.65% 3.60% 3.70% 3.65% 3.00% 3.50% 4.00% 4.50% 5.00% $0 $ 1 ,0 00 $ 2 ,0 00 $ 3 ,0 00 $ 4 ,0 00 $ 5 ,0 00 $ 6 ,0 00 $ 7 ,0 00 $ 8 ,0 00 3Q20 4Q20 1Q21 2Q21 3Q21 Total Interest - Earning Assets Investment Securities FHLB Stock, Fed Funds and Other Loans Average Yield Net Interest Margin & Interest - Earning Assets • Stable net interest margin • Stable funding costs • PPP loan forgiveness (11 basis point impact in 2021 Q3) $56 $56 $55 $58 $57 3 . 20% 3 . 26% 3 . 29% 3 . 45% 3 . 42% 3Q20 4Q20 1Q21 2Q21 3Q21 Net Interest Income Net Interest Margin Net Income ($ Millions) p. 13 Interest - Earning Assets Average Balances $ Millions A ver ag e Ra t e (%)

$4,526 $158 $5,188 $5,088 $4,919 $4,883 $861 $597 $329 $305 $4,327 $4,491 $4,589 $4,578 $4,684 0.62% 0.52% 0.42% 0.35% 0.33% 0.36% 0.29% 0.21% 0.16% 0.15% 0 . 0 0 % 0 . 5 0 % 1 . 0 0 % 1 . 5 0 % 2 . 0 0 % 2 . 5 0 % $0 $ 1 , 0 00 $ 2 , 0 00 $ 3 , 0 00 $ 4 , 0 00 $ 5 , 0 00 $ 6 , 0 00 3Q20 4Q20 1Q21 2Q21 3Q21 Total Borrowings Interest Bearing Deposits Average Rate Period End Cost of Deposits Interest - Bearing Liabilities p. 14 Average Balances $ Millions Average Rate (%)

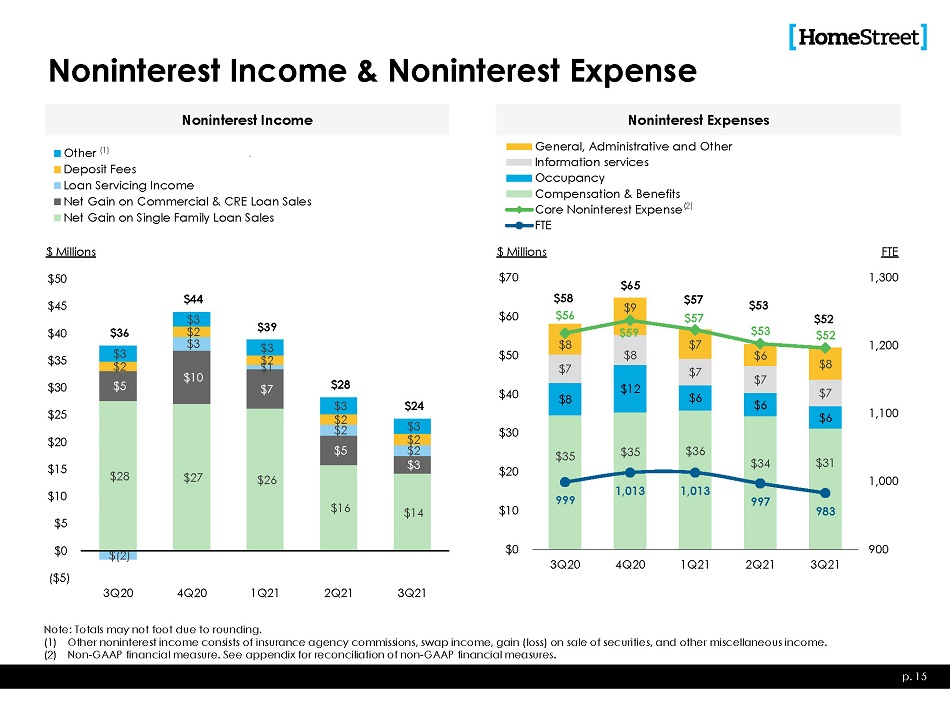

$28 $27 $26 $16 $14 $5 $10 $7 $5 $3 $ ( 2) $3 $2 $2 $2 $2 $2 $2 $2 $3 $3 $3 $3 $3 $36 $44 $39 $28 $24 $0 ( $ 5 ) $ 15 $ 10 $5 $ 25 $ 20 $ 30 $ 40 $ 35 $ 50 $ 45 3 Q 20 4 Q 20 1 Q 21 2 Q 21 3 Q 21 Other (1) Deposit Fees Loan Servicing Income Net Gain on Commercial & CRE Loan Sales Net Gain on Single Family Loan Sales Noninterest Income & Noninterest Expense Noninterest Income Noninterest Expenses $35 $35 $36 $34 $31 $8 $12 $6 $6 $6 $7 $8 $7 $7 $7 $8 $7 $6 $8 $58 $65 $57 $56 $9 $59 $57 $53 $53 $52 $52 999 1,013 1,013 997 983 9 00 1 , 000 1 , 100 1 , 200 F T E 1 , 300 $0 $ 10 $ 20 $ 30 $ 40 $ 50 $ 60 $ 70 3 Q 20 4 Q 20 1 Q 21 2 Q 21 3 Q 21 General, Administrative and Other Information services Occupancy Compensation & Benefits Core Noninterest Expense (2) FTE $ Millions p. 15 Note: Totals may not foot due to rounding. (1) Other noninterest income consists of insurance agency commissions, swap income, gain (loss) on sale of securities, and other miscellaneous income. (2) Non - GAAP financial measure. See appendix for reconciliation of non - GAAP financial measures. $ Millions

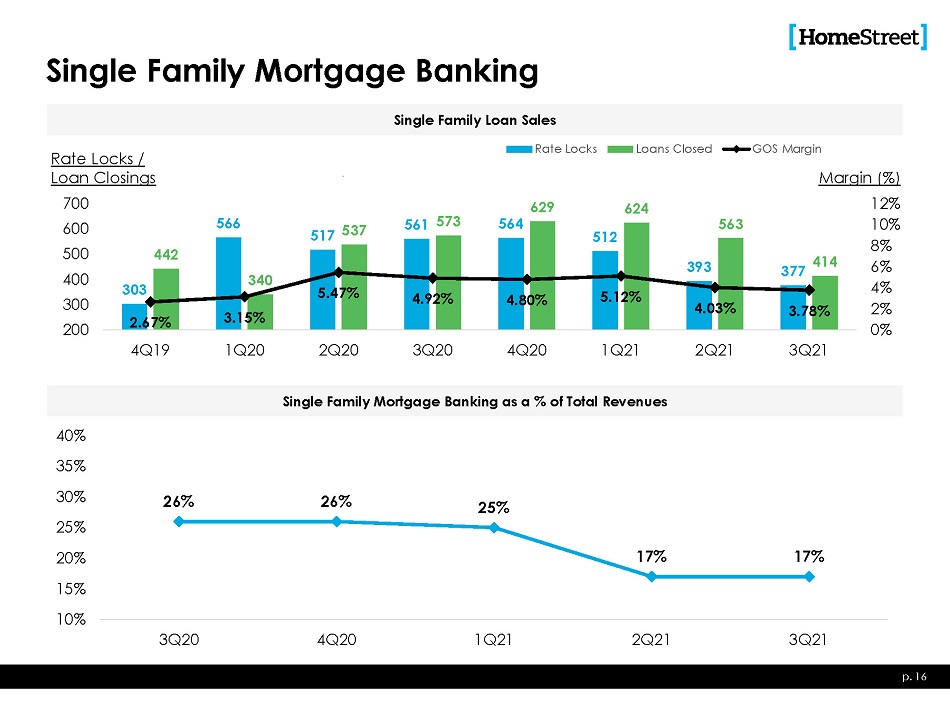

303 566 517 537 561 573 564 512 393 377 442 340 629 624 563 414 2 . 67% 3 . 15% 5 . 47% 4 . 92% 4 . 80% 5 . 12% 4 . 03% 3 . 78% 6% 4% 2% 0% GOS Margin Margin (%) 12% 10% 8% 4 0 0 3 0 0 2 0 0 5 0 0 Rate Locks / Loan Closings 700 600 4Q1 9 1Q2 0 2Q2 0 3Q2 0 4Q2 0 1Q2 1 2Q2 1 3Q21 Rate Locks Loans Closed Single Family Mortgage Banking 26% p. 16 26% 25% 17% 17% 4 0 % 3 5 % 3 0 % 2 5 % 2 0 % 1 5 % 1 0 % 3Q20 4Q20 1Q21 2Q21 3Q21 Single Family Loan Sales Single Family Mortgage Banking as a % of Total Revenues

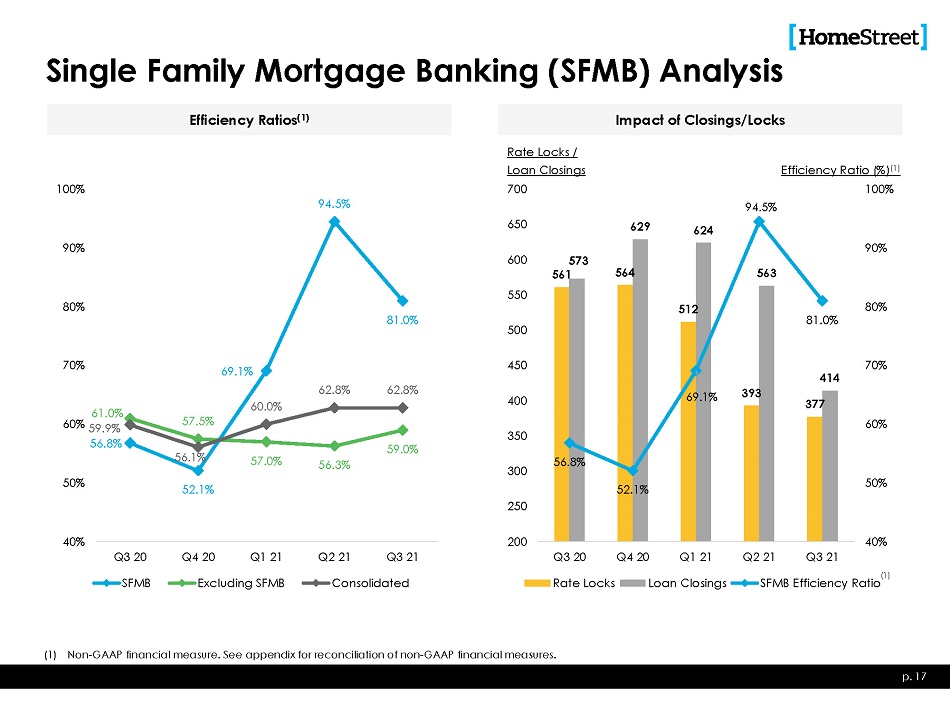

561 564 512 393 377 573 629 624 563 414 56 . 8% 52 . 1% 69 . 1% 94 . 5% 81 . 0% 4 0% 5 0% 6 0% 7 0% 8 0% 9 0% 1 0 0% 2 00 2 50 3 00 3 50 4 00 4 50 5 00 5 50 6 00 6 50 Rate Locks / L oa n C los i n g s 700 R ati o Q3 20 Q4 20 Q1 21 Q2 21 Q3 21 Q3 20 Q4 20 Q1 21 Q2 21 Q3 21 SFMB Excluding SFMB C o n so lidated Rate Locks Loan Closings S F MB Efficiency Single Family Mortgage Banking (SFMB) Analysis 52 . 1% 69 . 1% 94 . 5% 81 . 0% 57 . 5% 57 . 0% 56 . 3% 59 . 0% 56 . 1% 60 . 0% 62 . 8% 62 . 8% 61.0% 6 0 % 59 . 9% 56.8% 4 0% 5 0% 7 0% 8 0% 9 0% 1 0 0% (1) Non - GAAP financial measure. See appendix for reconciliation of non - GAAP financial measures. Efficiency Ratios (1) Impact of Closings/Locks Efficiency Ratio (%) (1) p. 17 ( 1)

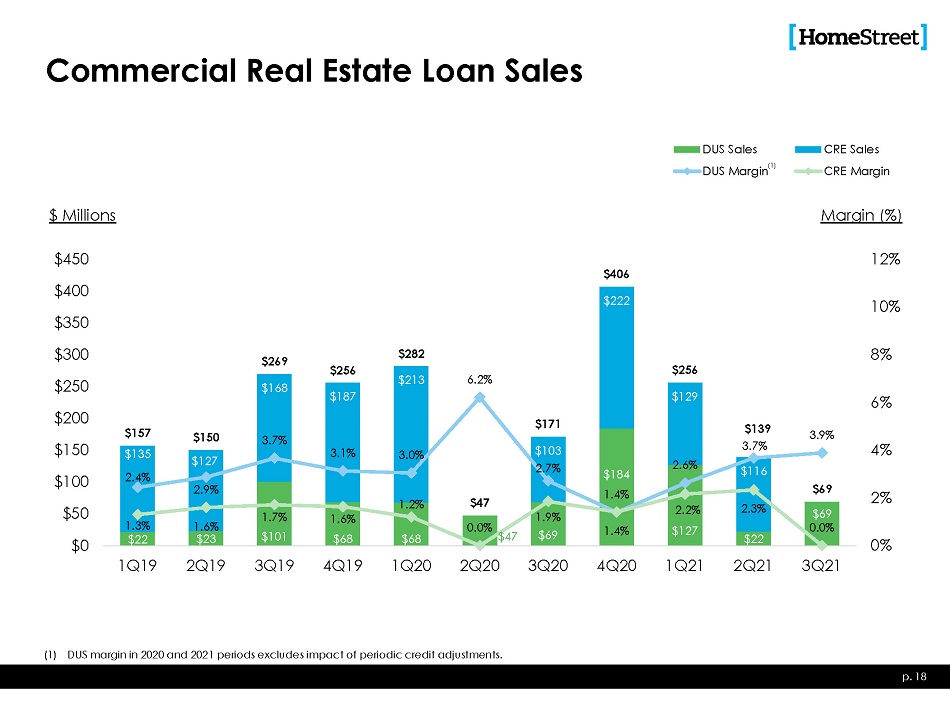

$22 $23 $68 $47 $22 $168 $187 $213 $222 $129 $157 $150 $269 $256 $282 $47 $171 $406 $256 $69 $135 2 . 4% 3 . 7% 3 . 1% 3 . 0% $103 2 . 7% 6 . 2% 2 . 6% $139 3.7% 3 . 9% 1 . 3% $127 2.9% 1.6% 1.7% $101 1 . 6% $68 1 . 2% 0 . 0% 1.9% $69 $184 1 . 4% 1.4% 2 . 2% $127 $116 2.3% $69 0 . 0% 0% 2% 4% 6% 8% 1 0 % 1 2 % $ 3 00 $ 2 50 $ 2 00 $ 1 50 $ 1 00 $50 $0 $ 4 50 $ 4 00 $ 3 50 1Q19 2Q19 3Q19 4Q19 1Q20 2Q20 3Q20 4Q20 1Q21 2Q21 3Q21 CRE Sales C R E M a r g i n DUS Sales D U S M a r g i n ( 1 ) Commercial Real Estate Loan Sales (1) DUS margin in 2020 and 2021 periods excludes impact of periodic credit adjustments. p. 18 $ Millions Margin (%)

Loan Portfolio and Asset Quality

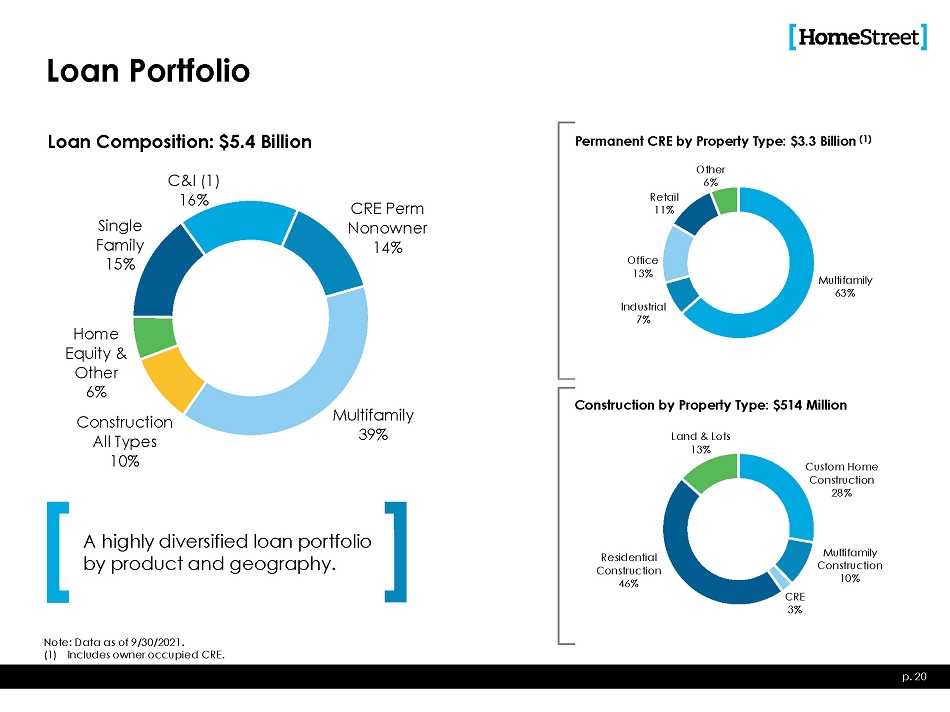

CRE Perm N o n o w ner 14% M u l t ifa m i l y 39% Home Equity & Other 6% C o ns t r uc t i o n All Types 10% Loan Composition: $5.4 Billion C&I (1) 16% Single F a m i l y 15% Loan Portfolio A highly diversified loan portfolio by product and geography. M u l t i f a m ily 63% I ndu s t r i a l 7% Off i c e 13% Permanent CRE by Property Type: $3.3 Billion (1) O t h e r 6% R e ta i l 11% C u s t om Home Construction 28% Multifamily C ons t r u c t i on 10% C RE 3% Residential C ons t r u c t i on 46% Land & Lots 13% Construction by Property Type: $514 Million Note: Data as of 9/30/2021. (1) Includes owner occupied CRE. p. 20

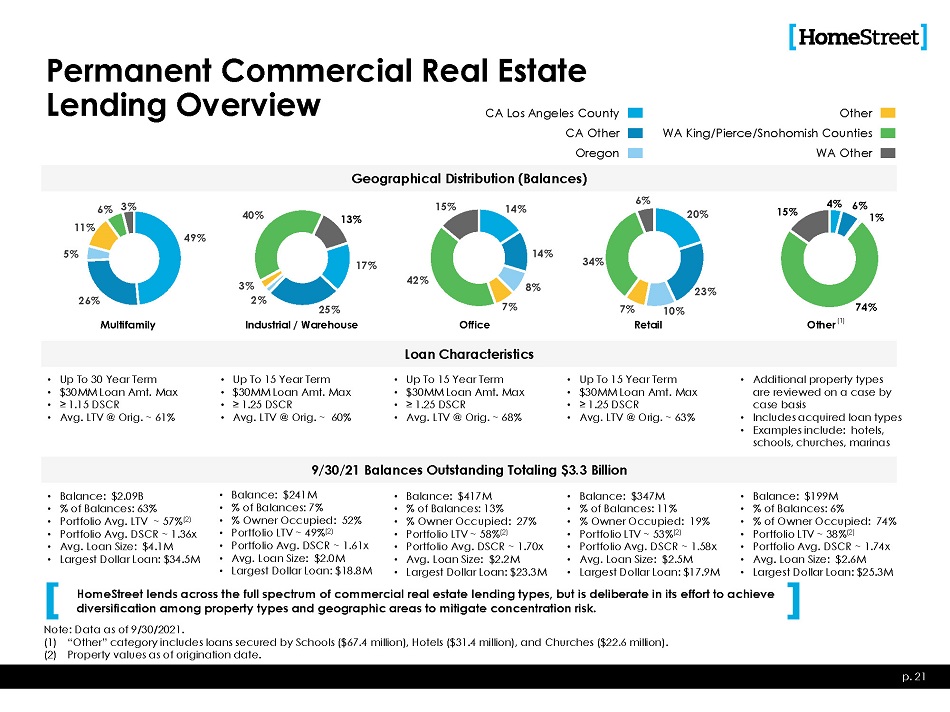

Permanent Commercial Real Estate Lending Overview • Up To 30 Year Term • $30MM Loan Amt. Max • ≥ 1.15 DSCR • Avg. LTV @ Orig. ~ 61% Loan Characteristics • Up To 15 Year Term • $30MM Loan Amt. Max • ≥ 1.25 DSCR • Avg. LTV @ Orig. ~ 60% • Up To 15 Year Term • $30MM Loan Amt. Max • ≥ 1.25 DSCR • Avg. LTV @ Orig. ~ 68% • Up To 15 Year Term • $30MM Loan Amt. Max • ≥ 1.25 DSCR • Avg. LTV @ Orig. ~ 63% • Additional property types are reviewed on a case by case basis • Includes acquired loan types • Examples include: hotels, schools, churches, marinas • Balance: $2.09B • % of Balances: 63% • Portfolio Avg. LTV ~ 57% (2) • Portfolio Avg. DSCR ~ 1.36x • Avg. Loan Size: $4.1M • La rg e s t Do ll ar Loan: $34 . 5M 9/30/21 Balances Outstanding Totaling $3.3 Billion • Balance: $241M • % of Balances: 7% • % Owner Occupied: 52% • Portfolio LTV ~ 49% (2) • Portfolio Avg. DSCR ~ 1.61x • Avg. Loan Size: $2.0M • La rg e s t Do ll ar Loan: $18 . 8M • Balance: $417M • % of Balances: 13% • % Owner Occupied: 27% • Portfolio LTV ~ 58% (2) • Portfolio Avg. DSCR ~ 1.70x • Avg. Loan Size: $2.2M • La rg e s t Do ll ar Loan: $23 . 3M • Balance: $347M • % of Balances: 11% • % Owner Occupied: 19% • Portfolio LTV ~ 53% (2) • Portfolio Avg. DSCR ~ 1.58x • Avg. Loan Size: $2.5M • La rg e s t Do ll ar Loan: $17 . 9M • Balance: $199M • % of Balances: 6% • % of Owner Occupied: 74% • Portfolio LTV ~ 38% (2) • Portfolio Avg. DSCR ~ 1.74x • Avg. Loan Size: $2.6M • La rg e s t Do ll ar Loan: $25 . 3M 49% 26% 5% 11% Geographical Distribution (Balances) 17% 25% 3% 2% 40% 13% 6% 3% 15% 14% 8% 7% 42% 14% Multi f a m il y I ndu s t r ia l / Wa r e h o u s e O ff i ce 20% 23% 10% 34% 6% 4% 6% 1% 74% 15% 7% Re tai l Oth er ( 1 ) CA Los Angeles County CA Ot her O r e g o n Ot her WA King/Pierce/Snohomish Counties W A Ot her HomeStreet lends across the full spectrum of commercial real estate lending types, but is deliberate in its effort to achieve diversification among property types and geographic areas to mitigate concentration risk. Note: Data as of 9/30/2021. (1) “Other” category includes loans secured by Schools ($67.4 million), Hotels ($31.4 million), and Churches ($22.6 million). (2) Property values as of origination date. p. 21

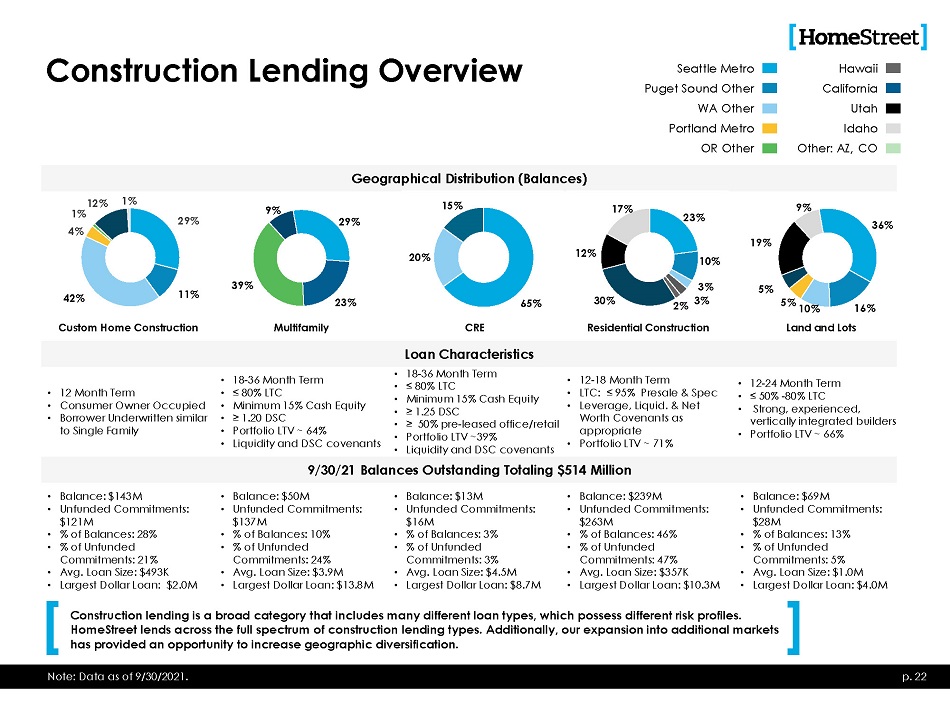

Construction Lending Overview • 12 Month Term • C onsum e r O w n e r Occ up i e d • Borrower Underwritten similar to Single Family p. 22 Loan Characteristics • 18 - 36 Month Term • ≤ 80% LTC • Minimum 15% Cash Equity • ≥ 1.20 DSC • Portfolio LTV ~ 64% • Liquidity and DSC covenants • 18 - 36 Month Term • ≤ 80% LTC • Minimum 15% Cash Equity • ≥ 1.25 DSC • ≥ 50% pre - leased office/retail • Portfolio LTV ~39% • Liquidity and DSC covenants • 12 - 18 Month Term • LTC: ≤ 95% Presale & Spec • Leverage, Liquid. & Net Worth Covenants as appropriate • Portfolio LTV ~ 71% • 12 - 24 Month Term • ≤ 50% - 80% LTC • Strong, experienced, vertically integrated builders • Portfolio LTV ~ 66% • Balance: $143M • Unfunded Commitments: $121M • % of Balances: 28% • % of Unfunded C omm i t m e n t s : 21 % • Avg. Loan Size: $493K • La rg e s t Do ll ar Loan: $2 . 0M 9/30/21 Balances Outstanding Totaling $514 Million • Balance: $50M • Unfunded Commitments: $137M • % of Balances: 10% • % of Unfunded C omm i t m e n t s : 24 % • Avg. Loan Size: $3.9M • La rg e s t Do ll ar Loan: $13 . 8M • Balance: $13M • Unfunded Commitments: $16M • % of Balances: 3% • % of Unfunded C omm i t m e n t s : 3 % • Avg. Loan Size: $4.5M • La rg e s t Do ll ar Loan: $8 . 7M • Balance: $239M • Unfunded Commitments: $263M • % of Balances: 46% • % of Unfunded C omm i t m e n t s : 47 % • Avg. Loan Size: $357K • La rg e s t Do ll ar Loan: $10 . 3M • Balance: $69M • Unfunded Commitments: $28M • % of Balances: 13% • % of Unfunded C omm i t m e n t s : 5 % • Avg. Loan Size: $1.0M • La rg e s t Do ll ar Loan: $4 . 0M 29% 11% 42% 12% 1% 4% 1% Geographical Distribution (Balances) Custom Home Construction Multifamily CRE Residential Construction Land and Lots 29% 23% 39% 9% 65% 20% 15% 23% 10% 3% 2% 3% 30% 12% 17% 36% 16% 5 % 10% 5% 19% 9% S e attl e Me t r o Puget Sound Other W A Ot her Po r tla nd Me t r o O R O t her Hawa i i C al i f o r n i a Uta h I da ho Other: AZ, CO Construction lending is a broad category that includes many different loan types, which possess different risk profiles. HomeStreet lends across the full spectrum of construction lending types. Additionally, our expansion into additional markets has provided an opportunity to increase geographic diversification. Note: Data as of 9/30/2021.

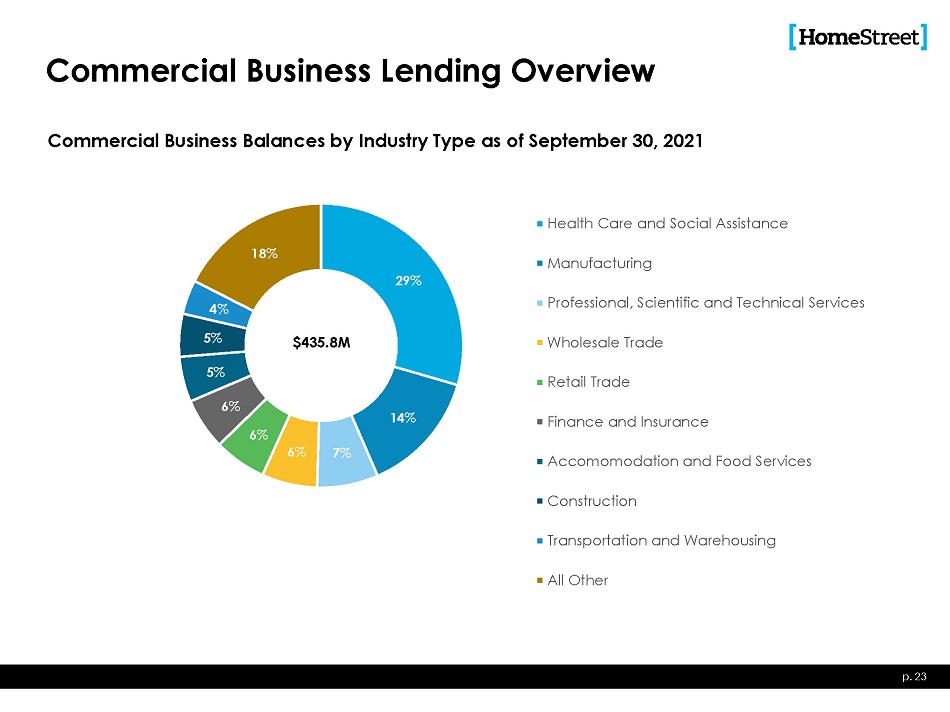

Commercial Business Lending Overview Commercial Business Balances by Industry Type as of September 30, 2021 29% 14% 7% 6% 6% 6% 5% 5% 4% 18% Health Care and Social Assistance Manufacturing Professional, Scientific and Technical Services Wholesale Trade Retail Trade Finance and Insurance Accomomodation and Food Services Construction Transportation and Warehousing All Other $43 5 . 8 M p. 23

COVID - 19 Response p. 24 Paycheck Protection Program (PPP) Loans • $77 million of outstanding PPP loans as of 9/30/2021 • Funded 1,384 loans during 2021 with balances of $159 million under the PPP for the nine months ended 9/30/2021 • $368 million cumulative PPP loans forgiven through 9/30/2021 Loan Modifications • HMST approved forbearance for certain borrowers » Forbearances approved for commercial and industrial loans and CRE nonowner occupied loans were generally for a period of three months » Forbearances approved for single family, HELOCs and consumer loans were generally for a period of three to six months • Forbearance periods for the majority of single family and consumer loans that were not complete as of 9/30/2021 are scheduled to be completed in 4Q21 • 99% of commercial and CRE loans approved for forbearance have completed their forbearance period and have resumed payments as of 9/30/2021 • Approximately $43 million in loans still on forbearance as of 9/30/2021

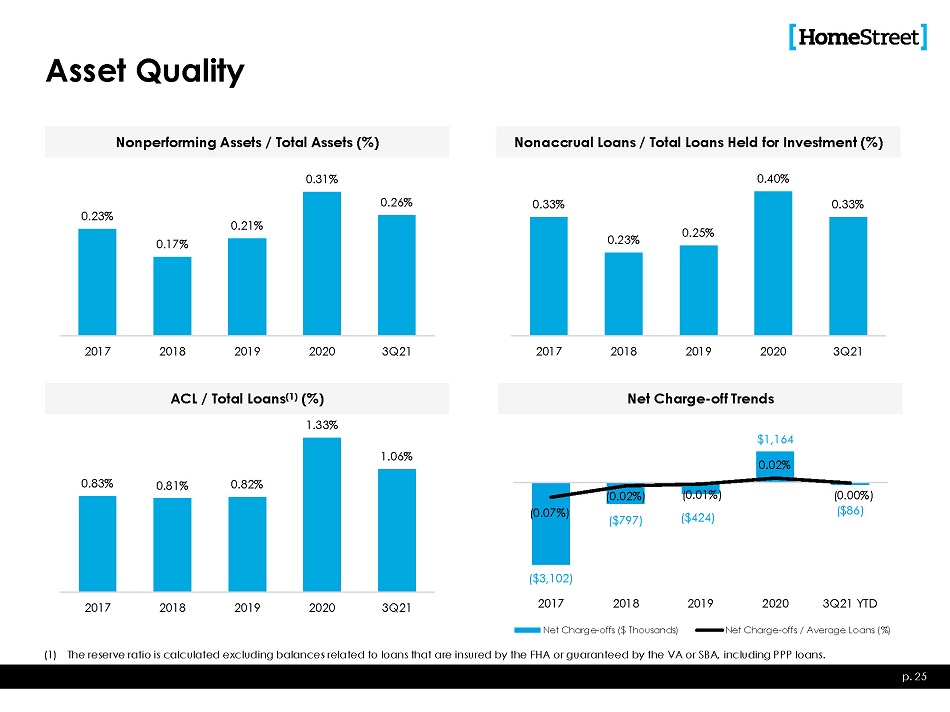

Asset Quality Nonperforming Assets / Total Assets (%) 0 . 23% 0 . 17% 0 . 21% 0 . 31% 0 . 26% 2 0 17 2 0 18 2 0 19 2 0 20 3 Q 21 Nonaccrual Loans / Total Loans Held for Investment (%) 0 . 33% 0 . 23% 0 . 25% 0 . 40% 0 . 33% 2 0 17 2 0 18 2 0 19 2 0 20 3 Q 21 ACL / Total Loans (1) (%) 0 . 83% 0 . 81% 0 . 82% 1 . 33% 1 . 06% 2 0 17 2 0 18 2 0 19 2 0 20 3 Q 21 Net Charge - off Trends ( $797) ( $424) $1 , 164 (0.07%) (0.02%) (0.01%) 0.02% ( 0 . 00 %) ($86) 2 0 19 2020 3Q21 YTD Net Charge - offs / Average Loans (%) ($3,102) 2017 2018 Net Charge - offs ($ Thousands) (1) The reserve ratio is calculated excluding balances related to loans that are insured by the FHA or guaranteed by the VA or SBA, including PPP loans. p. 25

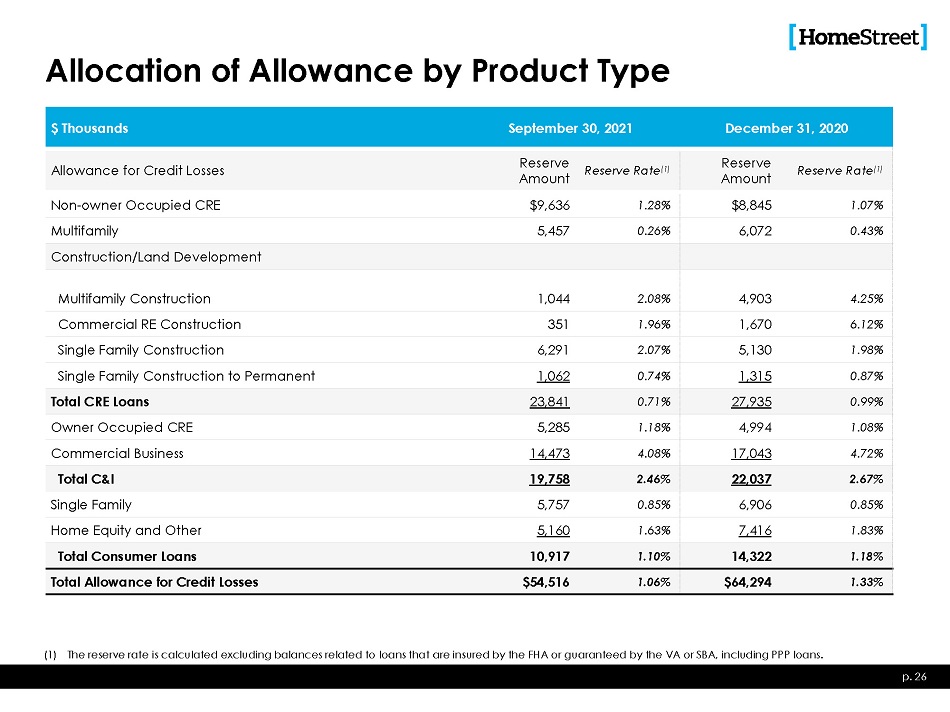

Allocation of Allowance by Product Type (1) The reserve rate is calculated excluding balances related to loans that are insured by the FHA or guaranteed by the VA or SBA, including PPP loans. p. 26 $ Thousands September 30, 2021 December 31, 2020 Allowance for Credit Losses R e s erve A m o u nt Reserve Rate (1) R e s erve A m o u nt Reserve Rate (1) Non - owner Occupied CRE $9,636 1.28% $8,845 1.07% Multifamily 5,457 0.26% 6,072 0.43% Construction/Land Development Multifamily Construction 1,044 2.08% 4,903 4.25% Commercial RE Construction 351 1.96% 1,670 6.12% Single Family Construction 6,291 2.07% 5,130 1.98% Single Family Construction to Permanent 1,062 0.74% 1,315 0.87% Total CRE Loans 23,841 0.71% 27,935 0.99% Owner Occupied CRE 5,285 1.18% 4,994 1.08% Commercial Business 14,473 4.08% 17,043 4.72% Total C&I 19,758 2.46% 22,037 2.67% Single Family 5,757 0.85% 6,906 0.85% Home Equity and Other 5,160 1.63% 7,416 1.83% Total Consumer Loans 10,917 1.10% 14,322 1.18% Total Allowance for Credit Losses $54,516 1.06% $64,294 1.33%

Deposits, Capital, Asset - Liability Management, Interest Rate Management and Liquidity

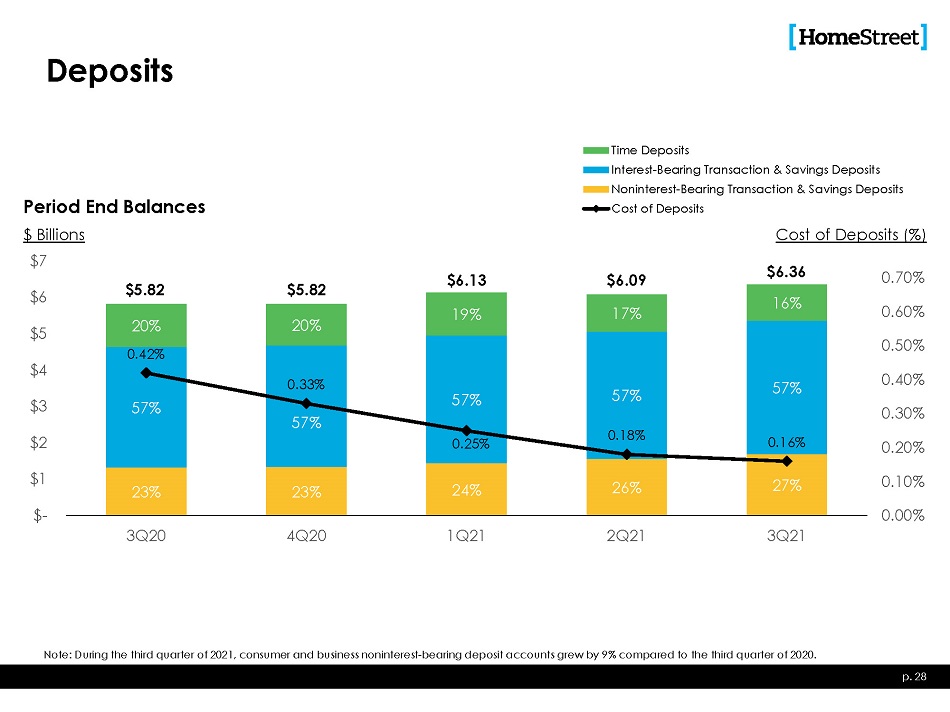

23% 23% 24% 26% 27% 57% 57% 57% 57% 57% 20% 20% 19% 17% 16% 0 . 42% 0 . 33% 0 . 25% 0 . 18% 0 . 16% 0 . 7 0% 0 . 6 0% 0 . 5 0% 0 . 4 0% 0 . 3 0% 0 . 2 0% 0 . 1 0% 0 . 0 0% $ - $1 $2 $3 $4 $5 $6 Period End Balances $ Billions $7 3Q20 4Q20 1Q21 2Q21 3Q21 Time Deposits Interest - Bearing Transaction & Savings Deposits Noninterest - Bearing Transaction & Savings Deposits Cost of Deposits Cost of Deposits (%) Deposits p. 28 $5.82 $5.82 $6.13 $6.09 $6.36 Note: During the third quarter of 2021, consumer and business noninterest - bearing deposit accounts grew by 9% compared to the third quarter of 2020.

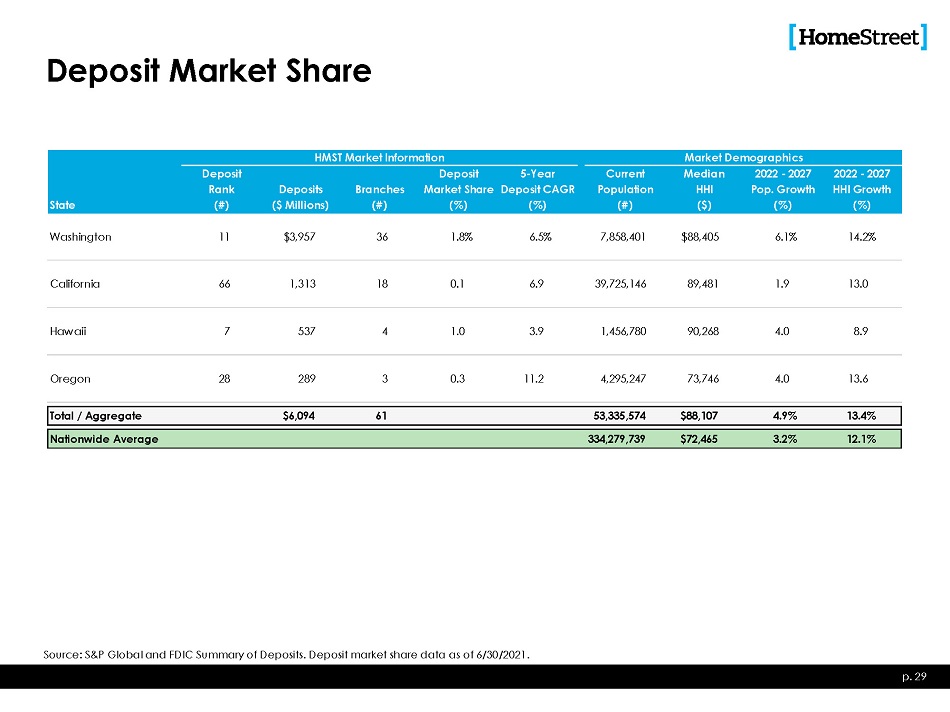

Deposit Market Share Source: S&P Global and FDIC Summary of Deposits. Deposit market share data as of 6/30/2021. HMST Market Information M a r k e t D em ographics Deposit Deposit 5 - Year Current Median 202 2 - 2027 202 2 - 2027 Rank Deposits Branches Market Share Deposit CAGR Population HHI Pop. Growth HH I G r o w t h State (#) ( $ M illio n s ) (#) (%) (%) (#) ($) (%) (%) Washington 11 $3,957 36 1.8% 6.5% 7,858,401 $88,405 6.1% 14.2% California 66 1,313 18 0.1 6.9 39,725,146 89,481 1.9 13.0 Ha w a i i 7 537 4 1.0 3.9 1,456,780 90,268 4.0 8.9 Oregon 28 289 3 0.3 11.2 4,295,247 73,746 4.0 13.6 Total / Aggregate $6,094 61 53,335,574 $88,107 4.9% 13.4% Nationwide Average 334,279,739 $72,465 3.2% 12.1% p. 29

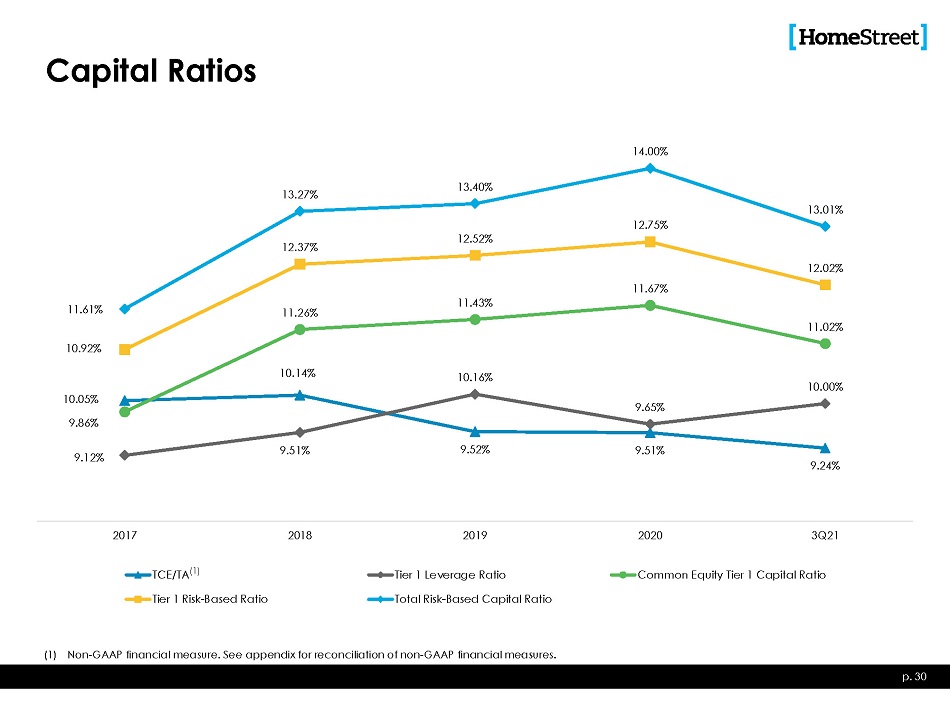

Capital Ratios (1) Non - GAAP financial measure. See appendix for reconciliation of non - GAAP financial measures. 10.05% 9.86% 10.14% 9 . 52% 9 . 51% 9 . 24% 9 . 12% 9 . 51% 10.16% 9 . 65% 10.00% 11.26% 11.43% 11.67% 11.02% 10.92% 12.37% 12.52% 12.75% 12.02% 11.61% 13.27% 13.40% 14.00% 13.01% 2 0 17 2 0 18 2 0 19 2 0 20 3 Q 21 Tier 1 Leverage Ratio Total Risk - Based Capital Ratio Common Equity Tier 1 Capital Ratio TCE/TA (1) Tier 1 Risk - Based Ratio p. 30

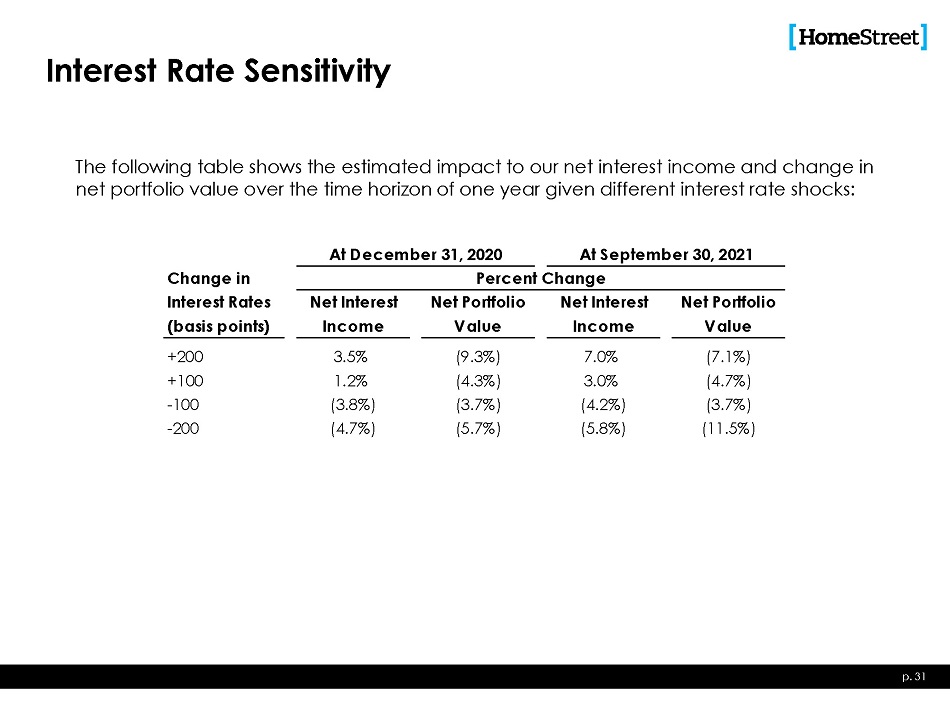

Interest Rate Sensitivity At December 31, 2020 At September 30, 2021 Percent Change Change in I n t e r e s t R a t e s ( ba s i s p oi n t s) N e t I n t e r e s t Income Net Portfolio Value N e t I n t e r e s t Income Net Portfolio Value +200 3.5% (9.3%) 7.0% (7.1%) +100 1.2% (4.3%) 3.0% (4.7%) - 100 (3.8%) (3.7%) (4.2%) (3.7%) - 200 (4.7%) (5.7%) (5.8%) (11.5%) The following table shows the estimated impact to our net interest income and change in net portfolio value over the time horizon of one year given different interest rate shocks: p. 31

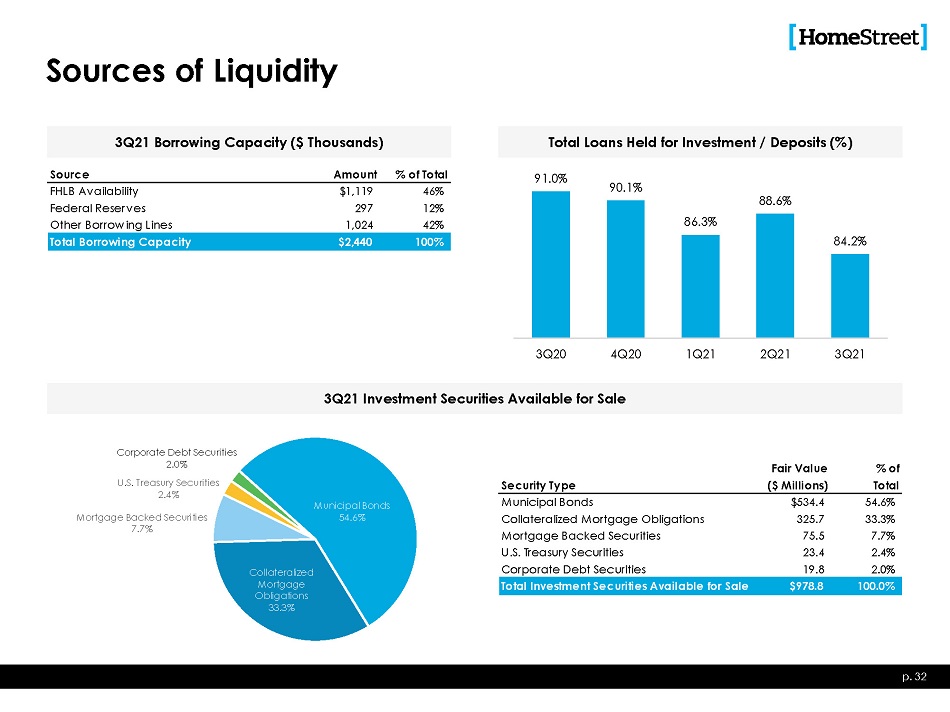

Sources of Liquidity Source Amount % of Total FHLB Availability $1,119 46% Federal Reserves Other Borrowing Lines 297 1 , 024 12% 42% Total Borrowing Capacity $2 , 440 100% 3Q21 Borrowing Capacity ($ Thousands) 3Q21 Investment Securities Available for Sale Total Loans Held for Investment / Deposits (%) M un i c i p al B onds 54.6% C o ll at e r a l iz ed Mortgage Obligations 33.3% Corporate Debt Securities 2.0% U.S. Treasury Securities 2.4% Mortgage Backed Securities 7.7% 91 . 0% 90 . 1% 86 . 3% 88 . 6% 84 . 2% 3 Q 2 0 4 Q 2 0 1 Q 2 1 2 Q 2 1 3 Q 21 Security Type F a i r V a l ue ( $ M illio n s ) % o f T o t a l Municipal Bonds Collateralized Mortgage Obligations Mortgage Backed Securities U.S. Treasury Securities Corporate Debt Securities $534 . 4 325 . 7 75 . 5 23 . 4 19 . 8 54 . 6% 33 . 3% 7 . 7% 2 . 4% 2 . 0% Total Investment Securities Available for Sale $978.8 100.0% p. 32

Appendix

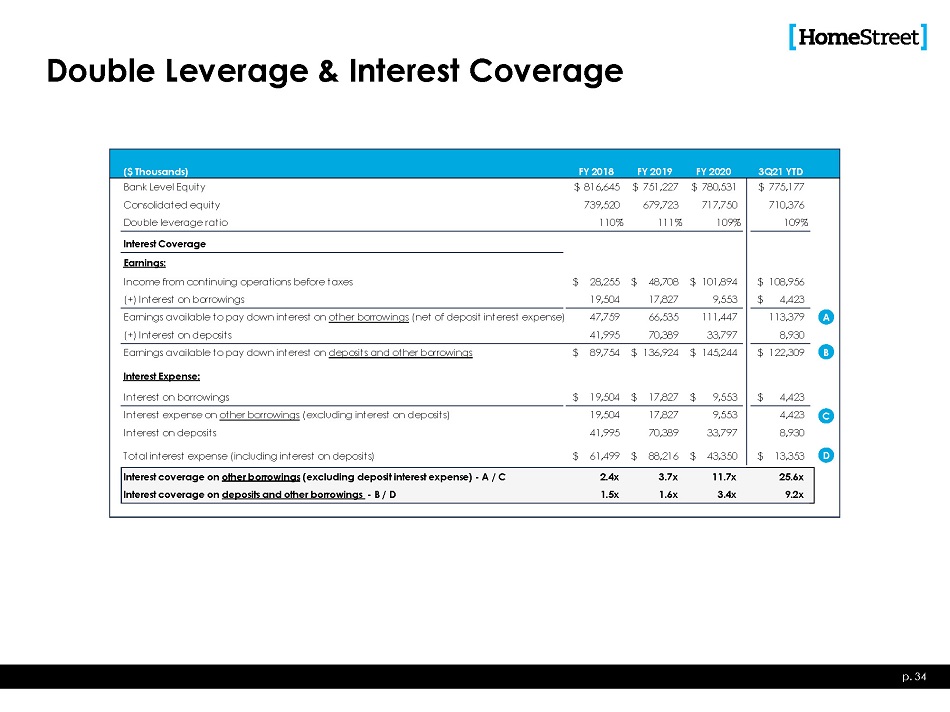

Double Leverage & Interest Coverage ( $ T h o u s a n d s ) F Y 2018 F Y 2019 F Y 2020 3 Q 21 Y T D B a n k Le v e l E q u i t y $ 816,645 $ 751,227 $ 780,531 $ 775,177 C o n s o li dat e d e q u i t y 739,520 679,723 717,750 710,376 D o u b l e l e v e r a g e r a t i o 110% 111% 109% 109% I n t e r e s t C o v e r ag e Earnings : Income from cont inuing operat ions before taxes $ 28,255 $ 48,708 $ 101,894 $ 108,956 ( + ) I n t e r e s t o n b o rr o w i ng s 19,504 17,827 9,553 $ 4,423 Earnings available to pay down interest on other borrowings (net of deposit int erest expense) 47,759 66,535 111,447 113,379 A ( + ) I n t e r e s t o n d e p o si t s 41,995 70,389 33,797 8,930 Earnings available to pay down interest on deposits and other borrowings $ 89,754 $ 136,924 $ 145,244 $ 122,309 B I n t e r e s t E x p e n s e : I n t e r e s t o n b o rr o w i ng s $ 19,504 $ 17,827 $ 9,553 $ 4,423 Int erest expense on other borrowings (excluding int erest on deposit s) 19,504 17,827 9,553 4,423 C I n t e r e s t o n d e p o si t s 41,995 70,389 33,797 8,930 Total int erest expense (including interest on deposit s) $ 61,499 $ 88,216 $ 43,350 $ 13,353 D Interest coverage on other borrowings (excluding deposit interest expense) - A / C Interest coverage on deposits and other borrowings - B / D 2.4x 1.5x 3.7x 1.6x 11.7x 3.4x 25.6x 9.2x p. 34

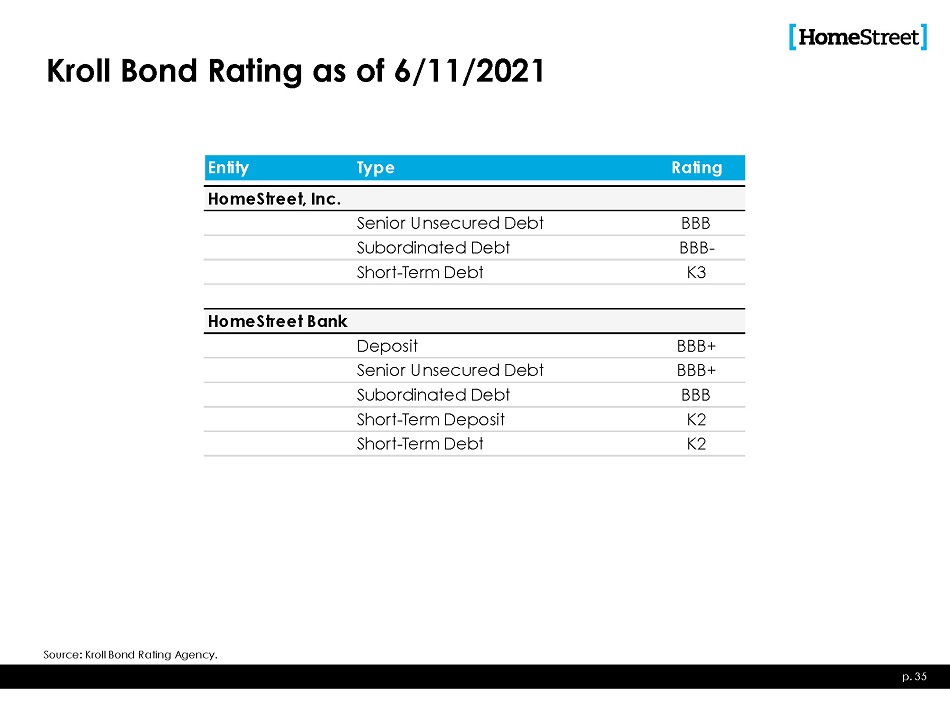

Kroll Bond Rating as of 6/11/2021 p. 35 Source: Kroll Bond Rating Agency. Entity Type Rating HomeStreet, Inc. Senior Unsecured Debt BBB Subordinated Debt BBB - S h o r t - T e r m D e b t K3 HomeStreet Bank Deposit BBB+ Senior Unsecured Debt BBB+ Subordinated Debt BBB S h o r t - T e r m D e p os it K2 S h o r t - T e r m D e b t K2

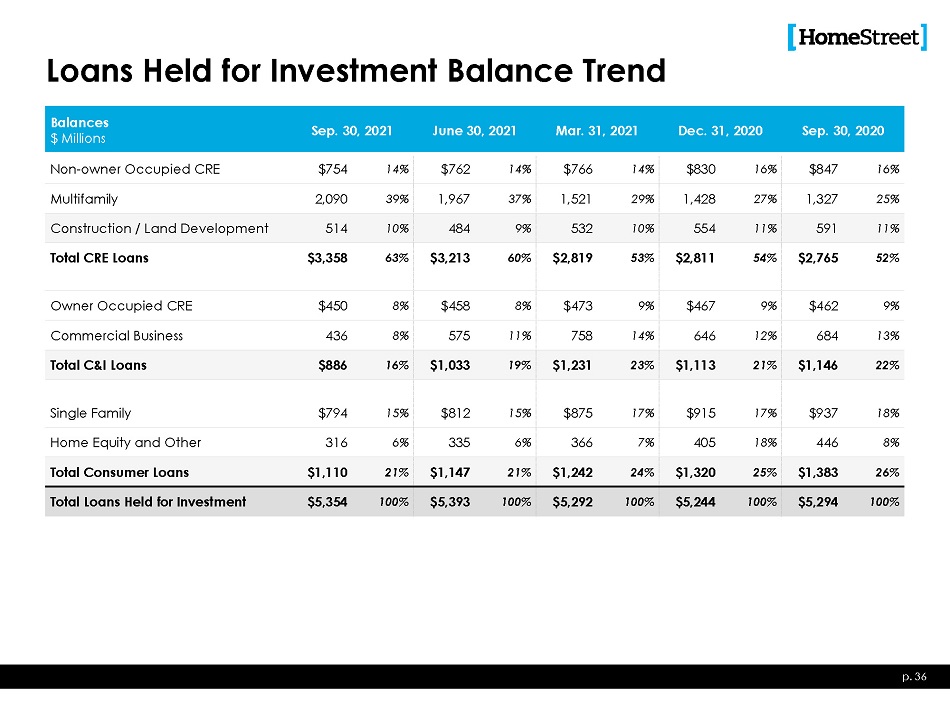

Loans Held for Investment Balance Trend p. 36 Balances $ Millions Sep. 30, 2021 June 30, 2021 Mar. 31, 2021 Dec. 31, 2020 Sep. 30, 2020 Non - owner Occupied CRE $754 14% $762 14% $766 14% $830 16% $847 16% Multifamily 2,090 39% 1,967 37% 1,521 29% 1,428 27% 1,327 25% Construction / Land Development 514 10% 484 9% 532 10% 554 11% 591 11% Total CRE Loans $3,358 63% $3,213 60% $2,819 53% $2,811 54% $2,765 52% Owner Occupied CRE $450 8% $458 8% $473 9% $467 9% $462 9% Commercial Business 436 8% 575 11% 758 14% 646 12% 684 13% Total C&I Loans $886 16% $1,033 19% $1,231 23% $1,113 21% $1,146 22% Single Family $794 15% $812 15% $875 17% $915 17% $937 18% Home Equity and Other 316 6% 335 6% 366 7% 405 18% 446 8% Total Consumer Loans $1,110 21% $1,147 21% $1,242 24% $1,320 25% $1,383 26% Total Loans Held for Investment $5,354 100% $5,393 100% $5,292 100% $5,244 100% $5,294 100%

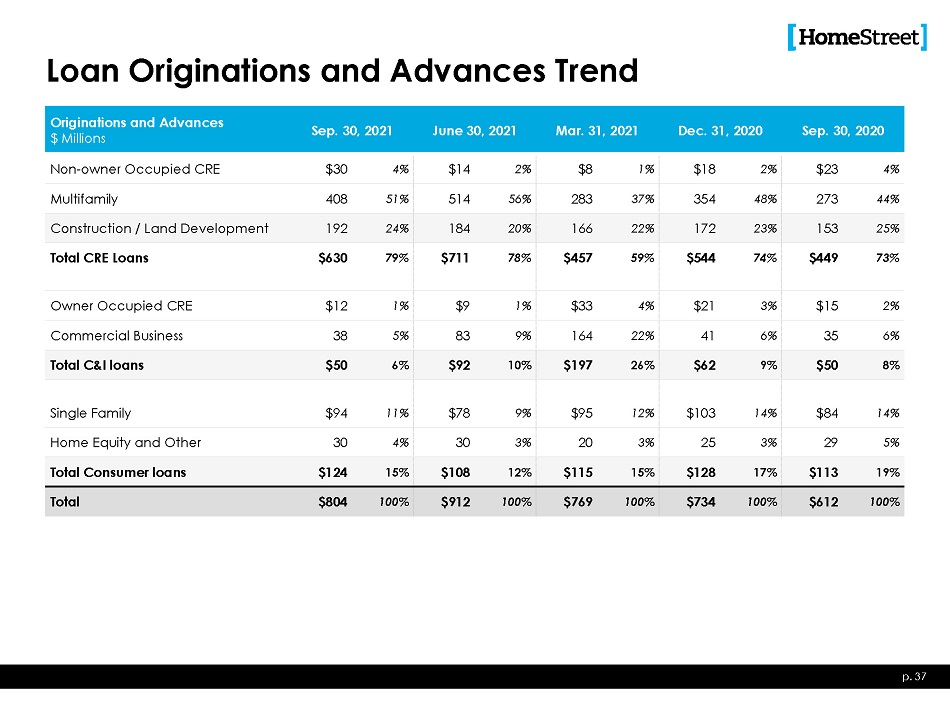

Loan Originations and Advances Trend p. 37 Originations and Advances $ Millions Sep. 30, 2021 June 30, 2021 Mar. 31, 2021 Dec. 31, 2020 Sep. 30, 2020 Non - owner Occupied CRE $30 4% $14 2% $8 1% $18 2% $23 4% Multifamily 408 51% 514 56% 283 37% 354 48% 273 44% Construction / Land Development 192 24% 184 20% 166 22% 172 23% 153 25% Total CRE Loans $630 79% $711 78% $457 59% $544 74% $449 73% Owner Occupied CRE $12 1% $9 1% $33 4% $21 3% $15 2% Commercial Business 38 5% 83 9% 164 22% 41 6% 35 6% Total C&I loans $50 6% $92 10% $197 26% $62 9% $50 8% Single Family $94 11% $78 9% $95 12% $103 14% $84 14% Home Equity and Other 30 4% 30 3% 20 3% 25 3% 29 5% Total Consumer loans $124 15% $108 12% $115 15% $128 17% $113 19% Total $804 100 % $912 100 % $769 100 % $734 100 % $612 100 %

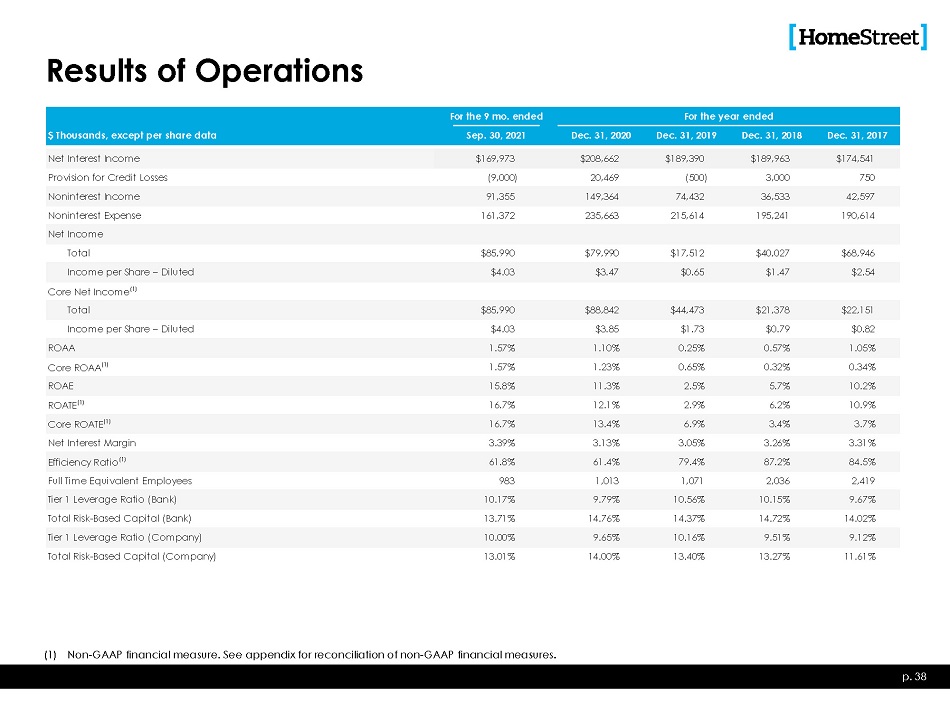

Results of Operations p. 38 For the 9 mo. ended For the year ended $ Thousands, except per share data Sep. 30, 2021 Dec. 31, 2020 Dec. 31, 2019 Dec. 31, 2018 Dec. 31, 2017 Net Interest Income $169,973 $208,662 $189,390 $189,963 $174,541 Provision for Credit Losses (9,000) 20,469 (500) 3,000 750 Noninterest Income 91,355 149,364 74,432 36,533 42,597 Noninterest Expense 161,372 235,663 215,614 195,241 190,614 Net Income Total $85,990 $79,990 $17,512 $40,027 $68,946 Income per Share – Diluted $4.03 $3.47 $0.65 $1.47 $2.54 C o re N e t In c o m e ( 1) Total $85,990 $88,842 $44,473 $21,378 $22,151 Income per Share – Diluted $4.03 $3.85 $1.73 $0.79 $0.82 ROAA 1.57% 1.10% 0.25% 0.57% 1.05% C o r e R O AA ( 1) 1.57% 1.23% 0.65% 0.32% 0.34% ROAE 15.8% 11.3% 2.5% 5.7% 10.2% R O A T E ( 1) 16.7% 12.1% 2.9% 6.2% 10.9% C o r e R O A T E ( 1) 16.7% 13.4% 6.9% 3.4% 3.7% Net Interest Margin 3.39% 3.13% 3.05% 3.26% 3.31% E ff i c i e n c y Ra t i o ( 1) 61.8% 61.4% 79.4% 87.2% 84.5% Full Time Equivalent Employees 983 1,013 1,071 2,036 2,419 Tier 1 Leverage Ratio (Bank) 10.17% 9.79% 10.56% 10.15% 9.67% Total Risk - Based Capital (Bank) 13.71% 14.76% 14.37% 14.72% 14.02% Tier 1 Leverage Ratio (Company) 10.00% 9.65% 10.16% 9.51% 9.12% Total Risk - Based Capital (Company) 13.01% 14.00% 13.40% 13.27% 11.61% (1) Non - GAAP financial measure. See appendix for reconciliation of non - GAAP financial measures.

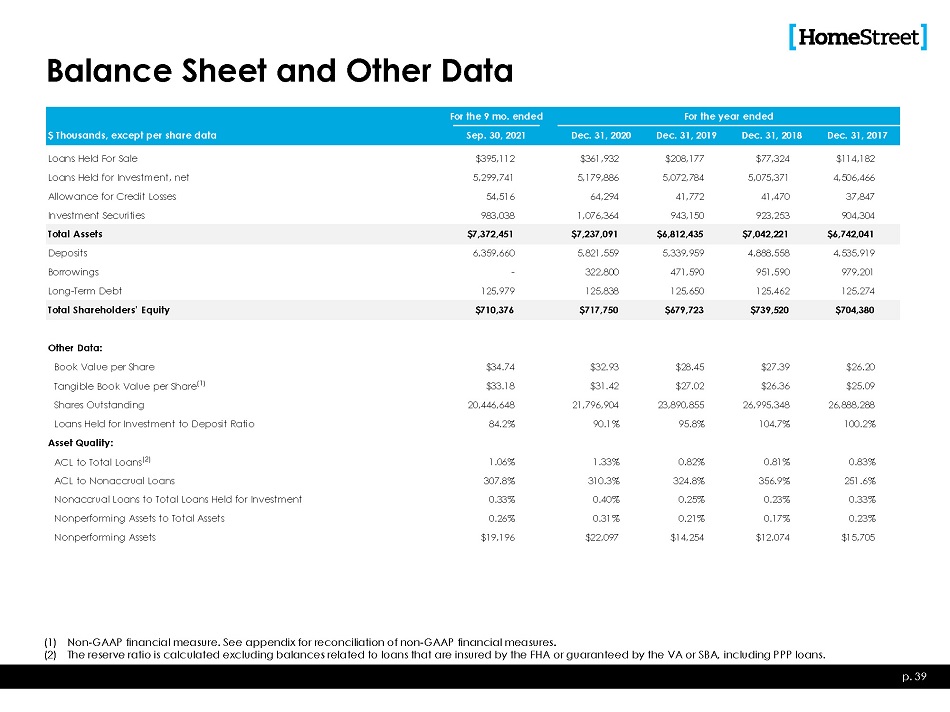

Balance Sheet and Other Data p. 39 (1) Non - GAAP financial measure. See appendix for reconciliation of non - GAAP financial measures. (2) The reserve ratio is calculated excluding balances related to loans that are insured by the FHA or guaranteed by the VA or SBA, including PPP loans. For the 9 mo. ended For the year ended $ Thousands, except per share data Sep. 30, 2021 Dec. 31, 2020 Dec. 31, 2019 Dec. 31, 2018 Dec. 31, 2017 Loans Held For Sale $395,112 $361,932 $208,177 $77,324 $114,182 Loans Held for Investment, net 5,299,741 5,179,886 5,072,784 5,075,371 4,506,466 Allowance for Credit Losses 54,516 64,294 41,772 41,470 37,847 Investment Securities 983,038 1,076,364 943,150 923,253 904,304 Total Assets $7,372,451 $7,237,091 $6,812,435 $7,042,221 $6,742,041 Deposits 6,359,660 5,821,559 5,339,959 4,888,558 4,535,919 Borrowings - 322,800 471,590 951,590 979,201 Long - Term Debt 125,979 125,838 125,650 125,462 125,274 Total Shareholders’ Equity $710,376 $717,750 $679,723 $739,520 $704,380 Other Data: Book Value per Share $34.74 $32.93 $28.45 $27.39 $26.20 Tangible Book Value per Share (1) $33.18 $31.42 $27.02 $26.36 $25.09 Shares Outstanding 20,446,648 21,796,904 23,890,855 26,995,348 26,888,288 Loans Held for Investment to Deposit Ratio Asset Quality: 84.2% 90.1% 95.8% 104.7% 100.2% ACL to Total Loans (2) 1.06% 1.33% 0.82% 0.81% 0.83% ACL to Nonaccrual Loans 307.8% 310.3% 324.8% 356.9% 251.6% Nonaccrual Loans to Total Loans Held for Investment 0.33% 0.40% 0.25% 0.23% 0.33% Nonperforming Assets to Total Assets 0.26% 0.31% 0.21% 0.17% 0.23% Nonperforming Assets $19,196 $22,097 $14,254 $12,074 $15,705

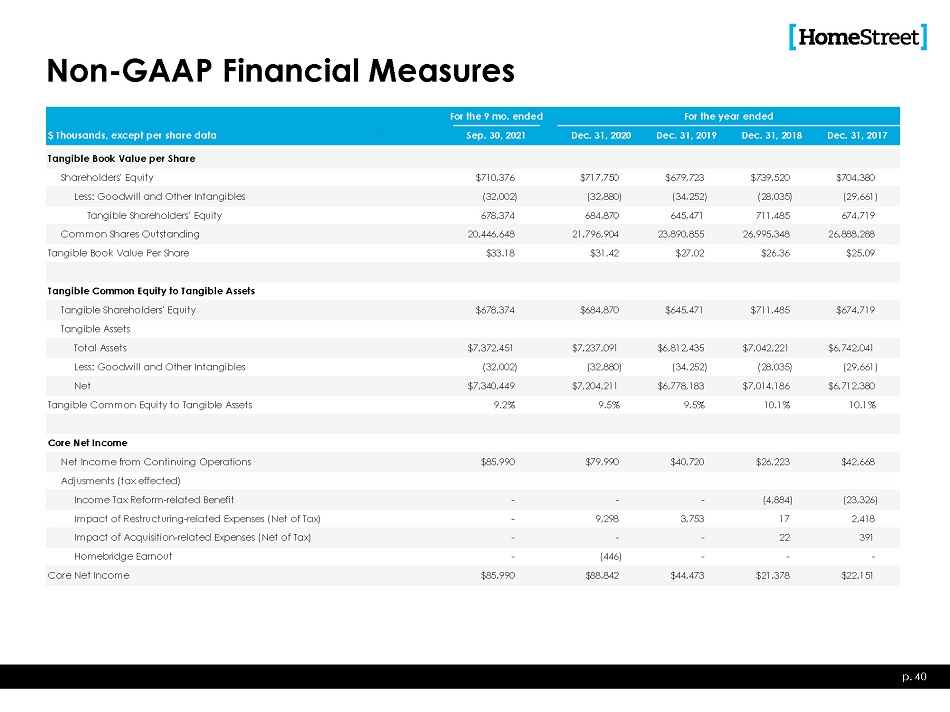

Non - GAAP Financial Measures p. 40 For the 9 mo. ended For the year ended $ Thousands, except per share data Sep. 30, 2021 Dec. 31, 2020 Dec. 31, 2019 Dec. 31, 2018 Dec. 31, 2017 Tangible Book Value per Share Shareholders' Equity $710,376 $717,750 $679,723 $739,520 $704,380 Less: Goodwill and Other Intangibles (32,002) (32,880) (34,252) (28,035) (29,661) Tangible Shareholders' Equity 678,374 684,870 645,471 711,485 674,719 Common Shares Outstanding 20,446,648 21,796,904 23,890,855 26,995,348 26,888,288 Tangible Book Value Per Share $33.18 $31.42 $27.02 $26.36 $25.09 Tangible Common Equity to Tangible Assets Tangible Shareholders' Equity $678,374 $684,870 $645,471 $711,485 $674,719 Tangible Assets Total Assets $7,372,451 $7,237,091 $6,812,435 $7,042,221 $6,742,041 Less: Goodwill and Other Intangibles (32,002) (32,880) (34,252) (28,035) (29,661) Net $7,340,449 $7,204,211 $6,778,183 $7,014,186 $6,712,380 Tangible Common Equity to Tangible Assets 9.2% 9.5% 9.5% 10.1% 10.1% Core Net Income Net Income from Continuing Operations $85,990 $79,990 $40,720 $26,223 $42,668 Adjusments (tax effected) Income Tax Reform - related Benefit - - - (4,884) (23,326) Impact of Restructuring - related Expenses (Net of Tax) - 9,298 3,753 17 2,418 Impact of Acquisition - related Expenses (Net of Tax) - - - 22 391 Homebridge Earnout - (446) - - - Core Net Income $85,990 $88,842 $44,473 $21,378 $22,151

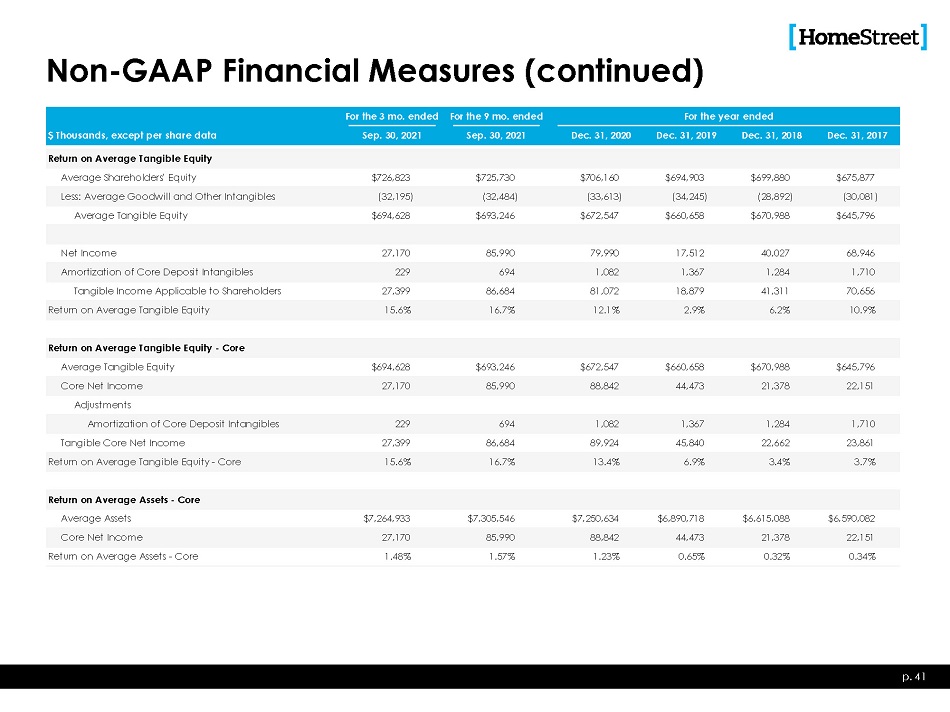

Non - GAAP Financial Measures (continued) p. 41 For the 3 mo. ended For the 9 mo. ended For the year ended $ Thousands, except per share data Sep. 30, 2021 Sep. 30, 2021 Dec. 31, 2020 Dec. 31, 2019 Dec. 31, 2018 Dec. 31, 2017 Return on Average Tangible Equity Average Shareholders' Equity $726,823 $725,730 $706,160 $694,903 $699,880 $675,877 Less: Average Goodwill and Other Intangibles (32,195) (32,484) (33,613) (34,245) (28,892) (30,081) Average Tangible Equity $694,628 $693,246 $672,547 $660,658 $670,988 $645,796 Net Income 27,170 85,990 79,990 17,512 40,027 68,946 Amortization of Core Deposit Intangibles 229 694 1,082 1,367 1,284 1,710 Tangible Income Applicable to Shareholders 27,399 86,684 81,072 18,879 41,311 70,656 Return on Average Tangible Equity 15.6% 16.7% 12.1% 2.9% 6.2% 10.9% Return on Average Tangible Equity - Core Average Tangible Equity $694,628 $693,246 $672,547 $660,658 $670,988 $645,796 Core Net Income 27,170 85,990 88,842 44,473 21,378 22,151 Adjustments Amortization of Core Deposit Intangibles 229 694 1,082 1,367 1,284 1,710 Tangible Core Net Income 27,399 86,684 89,924 45,840 22,662 23,861 Return on Average Tangible Equity - Core 15.6% 16.7% 13.4% 6.9% 3.4% 3.7% Return on Average Assets - Core Average Assets $7,264,933 $7,305,546 $7,250,634 $6,890,718 $6,615,088 $6,590,082 Core Net Income 27,170 85,990 88,842 44,473 21,378 22,151 Return on Average Assets - Core 1.48% 1.57% 1.23% 0.65% 0.32% 0.34%

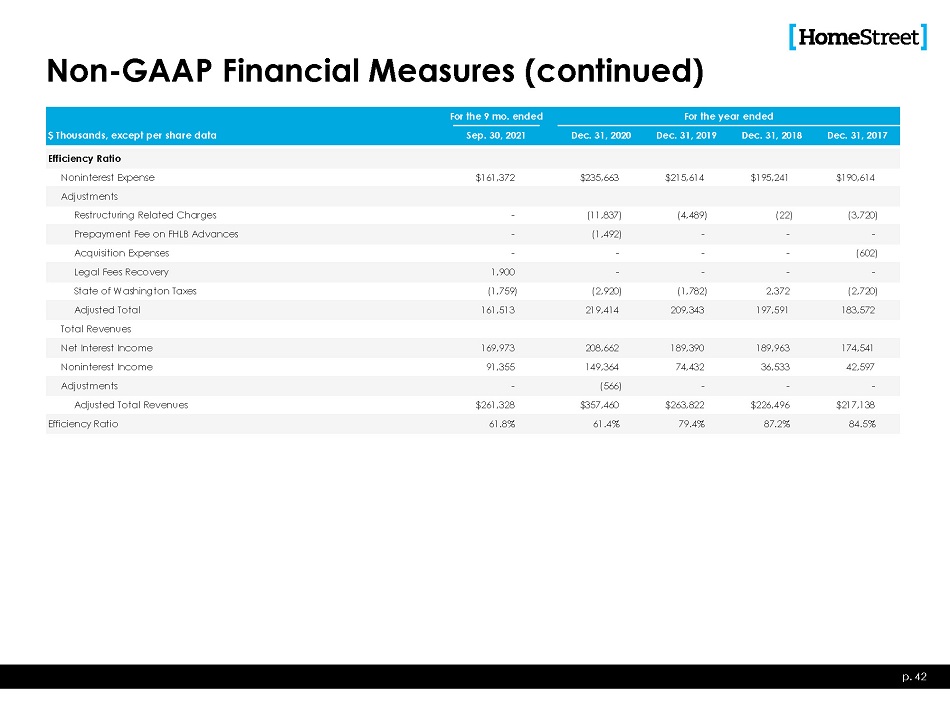

For the 9 mo. ended For the year ended $ Thousands, except per share data Sep. 30, 2021 Dec. 31, 2020 Dec. 31, 2019 Dec. 31, 2018 Dec. 31, 2017 Efficiency Ratio Noninterest Expense $161,372 $235,663 $215,614 $195,241 $190,614 Adjustments Restructuring Related Charges - (11,837) (4,489) (22) (3,720) Prepayment Fee on FHLB Advances - (1,492) - - - Acquisition Expenses - - - - (602) Legal Fees Recovery 1,900 - - - - State of Washington Taxes (1,759) (2,920) (1,782) 2,372 (2,720) Adjusted Total 161,513 219,414 209,343 197,591 183,572 Total Revenues Net Interest Income 169,973 208,662 189,390 189,963 174,541 Noninterest Income 91,355 149,364 74,432 36,533 42,597 Adjustments - (566) - - - Adjusted Total Revenues $261,328 $357,460 $263,822 $226,496 $217,138 E ff i c i e n c y Ra t io 61.8% 61.4% 79.4% 87.2% 84.5% Non - GAAP Financial Measures (continued) p. 42

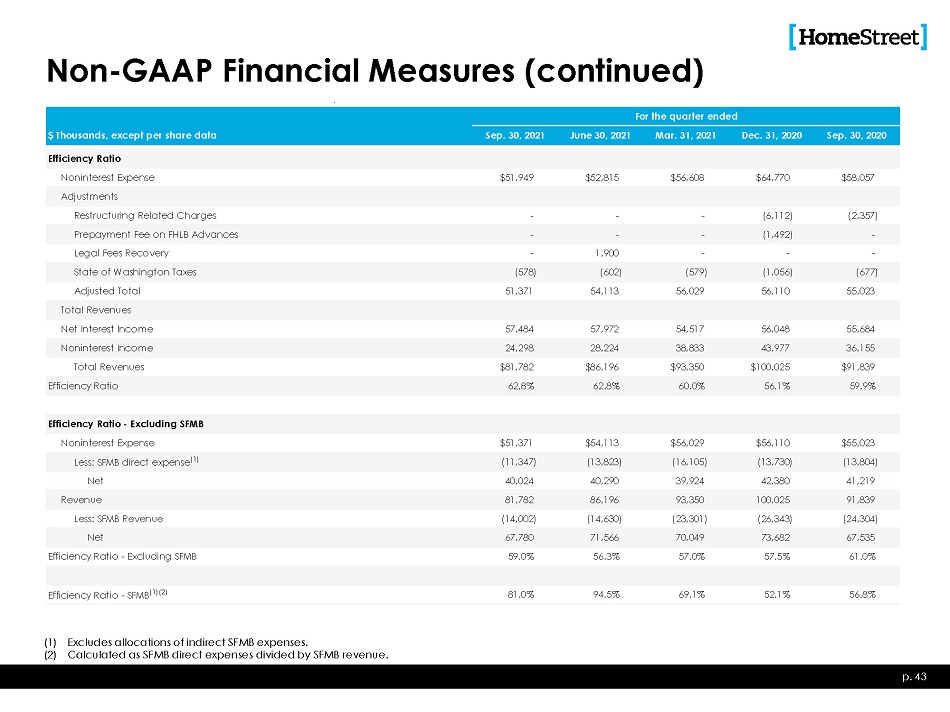

Non - GAAP Financial Measures (continued) p. 43 ( ( Noninterest Expense $51,949 $52,815 $56,608 $64,770 $58,057 Adjustments Restructuring Related Charges - - - (6,112) (2,357) Prepayment Fee on FHLB Advances - - - (1,492) - Legal Fees Recovery - 1,900 - - - State of Washington Taxes (578) (602) (579) (1,056) (677) Adjusted Total 51,371 54,113 56,029 56,110 55,023 Total Revenues Net Interest Income 57,484 57,972 54,517 56,048 55,684 Noninterest Income 24,298 28,224 38,833 43,977 36,155 Total Revenues $81,782 $86,196 $93,350 $100,025 $91,839 E ff i c i e n c y Ra t io 62.8% 62.8% 60.0% 56.1% 59.9% Efficiency Ratio - Excluding SFMB Noninterest Expense $51,371 $54,113 $56,029 $56,110 $55,023 Less: SFMB direct expense (1) (11,347) (13,823) (16,105) (13,730) (13,804) Net 40,024 40,290 39,924 42,380 41,219 Revenue 81,782 86,196 93,350 100,025 91,839 Less: SFMB Revenue (14,002) (14,630) (23,301) (26,343) (24,304) Net 67,780 71,566 70,049 73,682 67,535 Efficiency Ratio - Excluding SFMB 59.0% 56.3% 57.0% 57.5% 61.0% Efficiency Ratio - SFMB (1)(2) 81.0% 94.5% 69.1% 52.1% 56.8% 1) Excludes allocations of indirect SFMB expenses. 2) Calculated as SFMB direct expenses divided by SFMB revenue. $ Thousands, except per share data For the quarter ended Sep. 30, 2021 June 30, 2021 Mar. 31, 2021 Dec. 31, 2020 Sep. 30, 2020 Efficiency Ratio

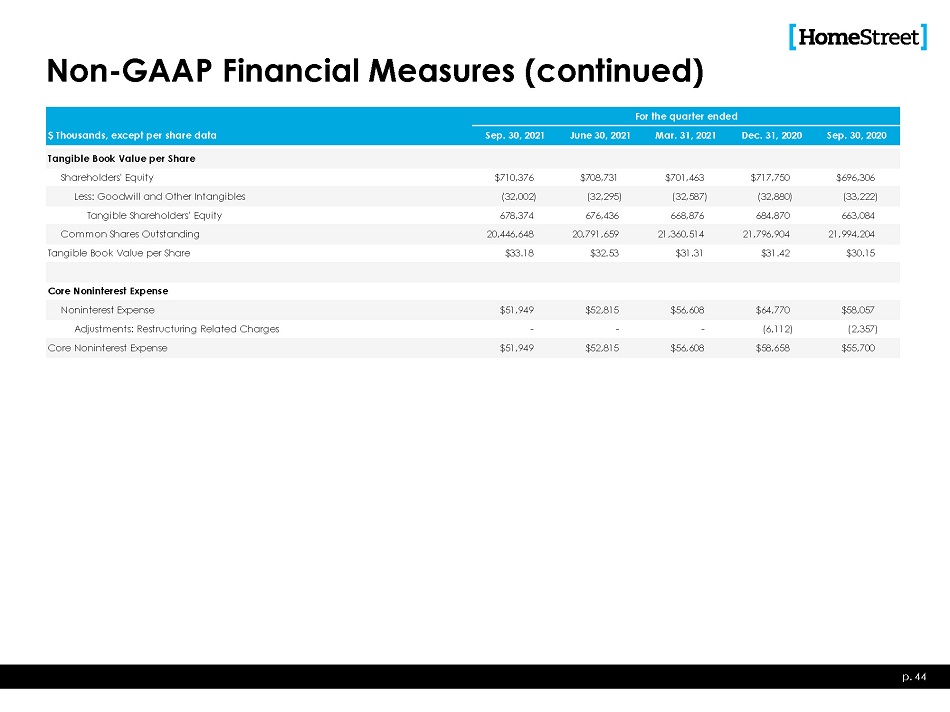

Non - GAAP Financial Measures (continued) p. 44 $ Thousands, except per share data For the quarter ended Sep. 30, 2021 June 30, 2021 Mar. 31, 2021 Dec. 31, 2020 Sep. 30, 2020 Tangible Book Value per Share Shareholders' Equity $710,376 $708,731 $701,463 $717,750 $696,306 Less: Goodwill and Other Intangibles (32,002) (32,295) (32,587) (32,880) (33,222) Tangible Shareholders' Equity 678,374 676,436 668,876 684,870 663,084 Common Shares Outstanding 20,446,648 20,791,659 21,360,514 21,796,904 21,994,204 Tangible Book Value per Share $33.18 $32.53 $31.31 $31.42 $30.15 Core Noninterest Expense Noninterest Expense $51,949 $52,815 $56,608 $64,770 $58,057 Adjustments: Restructuring Related Charges - - - (6,112) (2,357) Core Noninterest Expense $51,949 $52,815 $56,608 $58,658 $55,700

Non - GAAP Financial Measures (continued) p. 45 To supplement our audited and unaudited condensed consolidated financial statements presented in accordance with GAAP, we use certain non - GAAP measures of financial performance. These supplemental performance measures may vary from, and may not be comparable to, similarly titled measures provided by other companies in our industry. Non - GAAP financial measures are not in accordance with, or an alternative for, GAAP. Generally, a non - GAAP financial measure is a numerical measure of a company’s performance that either excludes or includes amounts that are not normally excluded or included in the most directly comparable measure calculated and presented in accordance with GAAP. A non - GAAP financial measure may also be a financial metric that is not required by GAAP or other applicable requirement. We believe that these non - GAAP financial measures, when taken together with the corresponding GAAP financial measures, provide meaningful supplemental information regarding our performance by providing additional information used by management that is not otherwise required by GAAP or other applicable requirements. Our management uses, and believes that investors benefit from referring to, these non - GAAP financial measures in assessing our operating results and when planning, forecasting and analyzing future periods. These non - GAAP financial measures also facilitate a comparison of our performance to prior periods. We believe these measures are frequently used by securities analysts, investors and other interested parties in the evaluation of companies in our industry. However, these non - GAAP financial measures should be considered in addition to, not as a substitute for or superior to, financial measures prepared in accordance with GAAP. In the information above, we have provided a reconciliation of, where applicable, the most comparable GAAP financial measures to the non - GAAP measures used in this press release, or a reconciliation of the non - GAAP calculation of the financial measure. In this presentation, we use the following non - GAAP measures: (i) tangible common equity and tangible assets as we believe this information is consistent with the treatment by bank regulatory agencies, which exclude intangible assets from the calculation of capital ratios; (ii) core earnings and core noninterest expense which exclude certain charges primarily related to our discontinued operations and restructuring activities as we believe this measure is a better comparison to be used for projecting future results; and (iii) an efficiency ratio which is the ratio of noninterest expenses to the sum of net interest income and noninterest income, excluding certain items of income or expense and excluding taxes incurred and payable to the state of Washington as such taxes are not classified as income taxes and we believe including them in noninterest expenses impacts the comparability of our results to those companies whose operations are in states where assessed taxes on business are classified as income taxes.