UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

(Mark one)

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2012.

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

for the transition period from __________ to ___________

Commission file number 001-35273

Cogo Group, Inc.

(Exact name of the Registrant as specified in its charter)

Cayman Islands

(Jurisdiction of incorporation or organization)

Room 1001, Tower C, Skyworth Building,

High-Tech Industrial Park,

Nanshan, Shenzhen 518057, PRC

Telephone: +86 (755) 2674-3210

(Address of principal executive offices)

Mr. Jeffrey Kang, Chief Executive Officer

Room 1001, Tower C, Skyworth Building

High-Tech Industrial Park

Nanshan, Shenzhen 518057, PRC

Telephone: +86 (755) 2674-3210

Facsimile: +86 (755) 2674-3522

(Name, Telephone, E-mail and/or Facsimile Number and Address of Company Contact Person)

Copies to:

Mitchell Nussbaum

Loeb & Loeb LLP

345 Park Avenue

New York, New York 10154

Telephone: (212) 407-4000

Fax: (212) 407-4990

Securities registered or to be registered pursuant to Section 12(b) of the Act:

ORDINARY SHARES, PAR VALUE $0.01

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None.

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None.

On December 31, 2012, the issuer had 31,110,922 ordinary shares outstanding.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act.

| ¨ Large Accelerated filer | ¨ Accelerated filer | x Non-accelerated filer |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| x US GAAP | ¨ | International Financial Reporting Standards as

issued by the International Accounting Standards

Board | ¨ Other |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Table of Contents

| | | | Page |

| | | | |

| PART I. | | | |

| ITEM 1. | | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS | 2 |

| ITEM 2. | | OFFER STATISTICS AND EXPECTED TIMETABLE | 2 |

| ITEM 3. | | KEY INFORMATION | 2 |

| A. | | Selected financial data | 2 |

| B. | | Capitalization and Indebtedness | 4 |

| C. | | Reasons for the Offer and Use of Proceeds | 4 |

| D. | | Risk Factors | 4 |

| ITEM 4. | | INFORMATION ON THE COMPANY | 22 |

| ITEM 4A. | | UNRESOLVED STAFF COMMENTS | 32 |

| ITEM 5. | | OPERATING AND FINANCIAL REVIEW AND PROSPECTS | 33 |

| ITEM 6. | | DIRECTORS, SENIOR MANAGEMENT AND EMPLOYEES | 51 |

| A. | | Directors and senior management | 51 |

| B. | | Compensation | 52 |

| C. | | Board Practices | 55 |

| D. | | Employees | 57 |

| E. | | Share Ownership | 57 |

| ITEM 7. | | MAJOR SHAREHOLDERS AND RELATED PARTY TRANSACTIONS | 58 |

| A. | | Major shareholders | 58 |

| B. | | Related Party Transactions | 59 |

| C. | | Interests of Experts and Counsel | 60 |

| ITEM 8. | | FINANCIAL INFORMATION | 60 |

| A. | | Consolidated Statements and Other Financial Information | 60 |

| B. | | Significant Changes | 60 |

| ITEM 9. | | THE OFFER AND LISTING | 60 |

| A. | | Offer and Listing Details | 60 |

| B. | | Plan of Distribution | 60 |

| C. | | Markets | 61 |

| D. | | Dilution | 61 |

| E. | | Expenses of the Issue | 61 |

| ITEM 10. | | ADDITIONAL INFORMATION | 61 |

| A. | | Share Capital | 61 |

| B. | | Memorandum and Articles of Association | 61 |

| C. | | Material Contracts | 62 |

| D. | | Exchange controls | 62 |

| E. | | Taxation | 63 |

| F. | | Dividends and paying agents | 67 |

| G. | | Statement by experts | 67 |

| H. | | Documents on display | 67 |

| I. | | Subsidiary Information | 68 |

| ITEM 11. | | QUANTITATIVE AND QUALITATIVE DISCLOSURE ABOUT MARKET RISK | 68 |

| ITEM 12. | | DESCRIPTION OF SECURITIES OTHER THAN EQUITY SECURITIES | 69 |

| | | | |

| PART II. | | | |

| ITEM 13. | | DEFAULTS, DIVIDEND ARREARAGES AND DELINQUENCIES | 69 |

| ITEM 14. | | MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS | 69 |

| ITEM 15. | | CONTROLS AND PROCEDURES | 70 |

| ITEM 16. | | [RESERVED] | 71 |

| ITEM 16A. | | AUDIT COMMITTEE FINANCIAL EXPERT | 71 |

| ITEM 16B. | | CODE OF ETHICS. | 71 |

| ITEM 16C. | | PRINCIPAL ACCOUNTANT FEES AND SERVICES. | 72 |

| ITEM 16D. | | EXEMPTIONS FROM THE LISTING STANDARDS FOR AUDIT COMMITTEES. | 72 |

| ITEM 16E. | | PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS. | 72 |

Table of Contents continued

| | | | Page |

| | | | |

| ITEM 16F. | | CHANGES IN REGISTRANT’S CERTIFYING ACCOUNTANT. | 73 |

| ITEM 16G. | | CORPORATE GOVERNANCE | 73 |

| | | | |

| PART III. | | | |

| ITEM 19. | | FINANCIAL STATEMENTS | 73 |

| ITEM 20. | | FINANCIAL STATEMENTS | 73 |

| ITEM 21. | | EXHIBITS | 73 |

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 20-F (this “Annual Report”) contains “forward-looking statements” that represent our beliefs, projections and predictions about future events. All statements other than statements of historical fact are “forward-looking statements” including any projections of earnings, revenue or other financial items, any statements of the plans, strategies and objectives of management for future operations, any statements concerning proposed new projects or other developments, any statements regarding future economic conditions or performance, any statements of management’s beliefs, goals, strategies, intentions and objectives, and any statements of assumptions underlying any of the foregoing. Words such as “may”, “will”, “should”, “could”, “would”, “predicts”, “potential”, “continue”, “expects”, “anticipates”, “future”, “intends”, “plans”, “believes”, “estimates” and similar expressions, as well as statements in the future tense, identify forward-looking statements.

These statements are necessarily subjective and involve known and unknown risks, uncertainties and other important factors that could cause our actual results, performance or achievements, or industry results, to differ materially from any future results, performance or achievements described in or implied by such statements. Actual results may differ materially from expected results described in our forward-looking statements, including with respect to correct measurement and identification of factors affecting our business or the extent of their likely impact, the accuracy and completeness of the publicly available information with respect to the factors upon which our business strategy is based on the success of our business.

A variety of factors, some of which are outside our control, may cause our operating results to fluctuate significantly. They include:

| · | the availability and cost of products from our suppliers incorporated into our customized module design solutions; |

| · | changes in end-user demand for the products manufactured and sold by our customers; |

| · | general and cyclical economic and business conditions, domestic or foreign, and, in particular, those in China’s mobile handset, telecommunications equipment and digital media industries; |

| · | the rate of introduction of new products by our customers; |

| · | the rate of introduction of enabling technologies by our suppliers; |

| · | changes in our pricing policies or the pricing policies of our competitors or suppliers; |

| · | our ability to compete effectively with our current and future competitors; |

| · | our ability to manage our growth effectively, including possible growth through acquisitions; |

| · | our ability to enter into and renew key corporate and strategic relationships with our customers and suppliers; |

| · | changes in our relationship with any of our key customers; |

| · | changes in the favorable tax incentives enjoyed by our People’s Republic of China (“PRC”) operating companies; |

| · | foreign currency exchange rates fluctuations; |

| · | adverse changes in the securities markets; and |

| · | legislative or regulatory changes in the PRC. |

Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Our expectations are as of the date this Annual Report is filed, and we do not intend to update any of the forward-looking statements after the filing date to conform these statements to actual results, unless required by law.

Forward-looking statements should not be read as a guarantee of future performance or results, and will not necessarily be accurate indications of whether, or the times by which, our performance or results may be achieved. Forward-looking statements are based on information available at the time those statements are made and management’s belief as of that time with respect to future events, and are subject to risks and uncertainties that could cause actual performance or results to differ materially from those expressed in or suggested by the forward-looking statements. Important factors that could cause such differences include, but are not limited to, those factors discussed under the headings “Item 3. Key Information – Risk Factors”, “Item 5. Operating and Financial Review and Prospects”, “Item 4. Information on the Company” and elsewhere in this Annual Report.

This Annual Report should be read in conjunction with the audited financial statements of Cogo Group, Inc. (“we,” “Cogo” or the “Company”) and the accompanying notes thereto, which are included in Item 19 of this Annual Report.

PART I.

| ITEM 1. | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS |

Not required.

| ITEM 2. | OFFER STATISTICS AND EXPECTED TIMETABLE |

Not required.

| A. | Selected financial data |

The following selected consolidated statement of comprehensive income/(loss) data for each of the years in the five-year period ended December 31, 2012 and selected consolidated balance sheet data as of December 31, 2012, 2011, 2010, 2009, and 2008, presented below are derived from our audited consolidated financial statements, which have been prepared in accordance with U.S. generally accepted accounting principles (“U.S. GAAP”) and have been audited by KPMG, an independent registered public accounting firm. The selected consolidated statement of comprehensive income/(loss) data for the years ended December 31, 2009 and 2008 and the selected consolidated balance sheet data as of December 31, 2010, 2009 and 2008 were derived from our audited financial statements which are not included in this Annual Report.

The selected consolidated financial statement data should be read in conjunction with our “Management’s discussion and analysis of financial condition and results of operations” and our audited consolidated financial statements and the related notes included elsewhere in this Annual Report.

The selected consolidated financial statement data are expressed in Renminbi (“RMB”), the national currency of the PRC. Solely for the convenience of the reader, the December 31, 2012 amounts have been translated into United States dollars (“USD”) at the closing rate in New York City on December 31, 2012 for cable transfers in RMB as certified for customers purposes by the Federal Reserve Bank of New York of USD1.0000 = RMB6.2301. No representation is made that the RMB could have been, or could be, converted into USD at that rate or at any other rate on December 31, 2012, or at any other date.

Selected Consolidated Statement of Comprehensive Income/(Loss) Data

| | | Year Ended December 31, | |

| | | 2012 USD | | | 2012 RMB | | | 2011 RMB | | | 2010 RMB | | | 2009 RMB | | | 2008 RMB | |

| | | (in thousands, except share and per share amounts) | |

| Net revenue | | | | | | | | | | | | | | | | | | | | | | | | |

| Product sales | | | 785,003 | | | | 4,890,649 | | | | 3,554,401 | | | | 2,554,991 | | | | 2,066,815 | | | | 1,931,845 | |

| Service revenue | | | — | | | | — | | | | — | | | | 34,527 | | | | 29,401 | | | | 27,695 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | 785,003 | | | | 4,890,649 | | | | 3,554,401 | | | | 2,589,518 | | | | 2,096,216 | | | | 1,959,540 | |

| Cost of sales | | | | | | | | | | | | | | | | | | | | | | | | |

| Cost of goods sold | | | (733,036 | ) | | | (4,566,886 | ) | | | (3,157,009 | ) | | | (2,194,901 | ) | | | (1,771,166 | ) | | | (1,624,101 | ) |

| Cost of services | | | — | | | | — | | | | — | | | | (27,971 | ) | | | (23,716 | ) | | | (18,664 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | (733,036 | ) | | | (4,566,886 | ) | | | (3,157,009 | ) | | | (2,222,872 | ) | | | (1,794,882 | ) | | | (1,642,765 | ) |

| Gross profit | | | 51,967 | | | | 323,763 | | | | 397,392 | | | | 366,646 | | | | 301,334 | | | | 316,775 | |

| Selling, general and administrative expenses | | | (25,421 | ) | | | (158,377 | ) | | | (188,083 | ) | | | (191,855 | ) | | | (124,842 | ) | | | (152,898 | ) |

| Research and development expenses | | | (16,457 | ) | | | (102,531 | ) | | | (101,639 | ) | | | (77,888 | ) | | | (67,504 | ) | | | (50,947 | ) |

| Provision for doubtful accounts | | | — | | | | — | | | | (2,325 | ) | | | (2 | ) | | | (35,992 | ) | | | (6,847 | ) |

| Net gain on settlement relating to the acquisition of Long Rise before goodwill impairment | | | — | | | | — | | | | — | | | | 43,676 | | | | — | | | | — | |

| Impairment loss of goodwill and intangible assets | | | — | | | | — | | | | (236,945 | ) | | | (21,422 | ) | | | — | | | | (33,759 | ) |

| Other operating income / (loss), net | | | 569 | | | | 3,546 | | | | (842 | ) | | | 463 | | | | 116 | | | | 214 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Income / (loss) from operations | | | 10,658 | | | | 66,401 | | | | (132,442 | ) | | | 119,618 | | | | 73,112 | | | | 72,538 | |

| Gain on disposal of subsidiaries | | | 90 | | | | 558 | | | | — | | | | — | | | | — | | | | — | |

| Interest expense | | | (4,186 | ) | | | (26,081 | ) | | | (20,152 | ) | | | (9,407 | ) | | | (1,963 | ) | | | (1,056 | ) |

| Interest income | | | 2,194 | | | | 13,668 | | | | 14,928 | | | | 14,693 | | | | 14,490 | | | | 27,895 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Earnings / (loss) before income taxes and extraordinary item | | | 8,756 | | | | 54,546 | | | | (137,666 | ) | | | 124,904 | | | | 85,639 | | | | 99,377 | |

| Income tax expense(1) | | | (937 | ) | | | (5,839 | ) | | | (11,553 | ) | | | (11,849 | ) | | | (9,207 | ) | | | (2,215 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Income / (loss) before extraordinary item | | | 7,819 | | | | 48,707 | | | | (149,219 | ) | | | 113,055 | | | | 76,432 | | | | 97,162 | |

| Extraordinary item, net of nil tax | | | — | | | | — | | | | — | | | | — | | | | 6,737 | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Net income / (loss) | | | 7,819 | | | | 48,707 | | | | (149,219 | ) | | | 113,055 | | | | 83,169 | | | | 97,162 | |

| Less net income attributable to noncontrolling interests | | | (3,945 | ) | | | (24,577 | ) | | | (7,386 | ) | | | (680 | ) | | | (2,945 | ) | | | (1,255 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Net income / (loss) attributable to Cogo Group, Inc. | | | 3,874 | | | | 24,130 | | | | (156,605 | ) | | | 112,375 | | | | 80,224 | | | | 95,907 | |

| Earnings / (loss) per share attributable to Cogo Group, Inc. | | | | | | | | | | | | | | | | | | | | | | | | |

| Income / (loss) before extraordinary item | | | 0.11 | | | | 0.66 | | | | (4.22 | ) | | | 3.01 | | | | 2.01 | | | | 2.49 | |

| Extraordinary item | | | — | | | | — | | | | — | | | | — | | | | 0.19 | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Basic | | | 0.11 | | | | 0.66 | | | | (4.22 | ) | | | 3.01 | | | | 2.20 | | | | 2.49 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Income / (loss) before extraordinary item | | | 0.11 | | | | 0.66 | | | | (4.22 | ) | | | 2.94 | | | | 1.95 | | | | 2.42 | |

| Extraordinary item | | | — | | | | — | | | | — | | | | — | | | | 0.18 | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Diluted | | | 0.11 | | | | 0.66 | | | | (4.22 | ) | | | 2.94 | | | | 2.13 | | | | 2.42 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Weighted average number of common shares outstanding | | | | | | | | | | | | | | | | | | | | | | | | |

| Basic | | | | | | | 36,355,124 | | | | 37,094,995 | | | | 37,275,427 | | | | 36,541,037 | | | | 38,488,861 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Diluted | | | | | | | 36,488,041 | | | | 37,094,995 | | | | 38,188,814 | | | | 37,673,351 | | | | 39,585,921 | |

| Selected Consolidated Balance Sheet Data | | As of December 31, | |

| | | 2012 USD | | | 2012 RMB | | | 2011 RMB | | | 2010 RMB | | | 2009 RMB | | | 2008 RMB | |

| | | (in thousands) | |

| Cash | | | 52,140 | | | | 324,839 | | | | 572,364 | | | | 699,650 | | | | 667,320 | | | | 686,379 | |

| Accounts receivable, net | | | 113,155 | | | | 704,968 | | | | 941,798 | | | | 681,911 | | | | 617,613 | | | | 497,992 | |

| Property and equipment, net | | | 2,811 | | | | 17,515 | | | | 17,891 | | | | 14,613 | | | | 14,406 | | | | 17,993 | |

| Total assets | | | 380,693 | | | | 2,371,758 | | | | 2,559,988 | | | | 2,322,017 | | | | 1,921,527 | | | | 1,686,810 | |

| Total current liabilities | | | 121,957 | | | | 759,812 | | | | 1,014,411 | | | | 600,905 | | | | 350,397 | | | | 257,662 | |

| Total liabilities | | | 125,369 | | | | 781,066 | | | | 1,039,838 | | | | 614,682 | | | | 369,505 | | | | 277,355 | |

| Total equity | | | 255,324 | | | | 1,590,692 | | | | 1,520,150 | | | | 1,707,335 | | | | 1,552,022 | | | | 1,409,455 | |

| (1) | Certain of our operating subsidiaries were entitled to tax holidays. The effect of the tax holiday increased our net income for 2012, 2011, 2010, 2009 and 2008 by RMB29.1 million (USD4.7 million), RMB33.9 million, RMB26.5 million, RMB29.5 million and RMB28.2 million, respectively (equivalent to basic earnings per share amount of RMB0.80 (USD0.13), RMB0.92, RMB0.71, RMB0.81 and RMB0.73 and a diluted earnings per share amount of RMB0.80 (USD0.13), RMB0.92, RMB0.69, RMB0.78 and RMB0.71 for the years ended December 31, 2012, 2011, 2010, 2009 and 2008, respectively. |

The following table sets forth information concerning exchange rates between the RMB and the U.S. dollar for the periods indicated. On April 12, 2013, the buying rate announced by Federal Reserve Statistical Release was RMB6.1914 to $1.00.

| | | Spot Exchange Rate | |

| Period | | Period Ended | | | Average (1) | | | Low | | | High | |

| | | (RMB per US$1.00) | |

| 2008 | | | 6.8225 | | | | 6.9477 | | | | 7.2946 | | | | 6.7800 | |

| 2009 | | | 6.8259 | | | | 6.8295 | | | | 6.8180 | | | | 6.8395 | |

| 2010 | | | 6.6000 | | | | 6.7603 | | | | 6.6000 | | | | 6.8305 | |

| 2011 | | | 6.2939 | | | | 6.4633 | | | | 6.2939 | | | | 6.6364 | |

| 2012 | | | 6.2301 | | | | 6.2990 | | | | 6.2265 | | | | 6.3684 | |

| September | | | 6.2848 | | | | 6.3200 | | | | 6.2848 | | | | 6.3489 | |

| October | | | 6.2372 | | | | 6.2627 | | | | 6.2372 | | | | 6.2877 | |

| November | | | 6.2265 | | | | 6.2221 | | | | 6.2221 | | | | 6.2454 | |

| December | | | 6.2301 | | | | 6.2328 | | | | 6.2251 | | | | 6.2502 | |

| 2013 (through April 12) | | | 6.1914 | | | | 6.2105 | | | | 6.1914 | | | | 6.2213 | |

| January | | | 6.2186 | | | | 6.2215 | | | | 6.2134 | | | | 6.2303 | |

| February | | | 6.2213 | | | | 6.2323 | | | | 6.2213 | | | | 6.2438 | |

| March | | | 6.2108 | | | | 6.2157 | | | | 6.2105 | | | | 6.2246 | |

| Source: | Federal Reserve Statistical Release |

| (1) | Annual averages, lows, and highs are calculated from month-end rates. Monthly averages, lows, and highs are calculated using the daily rates during the relevant period. |

| B. | Capitalization and Indebtedness |

Not required.

| C. | Reasons for the Offer and Use of Proceeds |

Not required.

You should carefully consider the following risk factors, together with all of the other information included in this annual report.

Risks Related to Our Business

Our operating results fluctuate from quarter to quarter.

Our quarterly revenue, income and other operating results have fluctuated in the past and may fluctuate significantly in the future due to a number of factors, including the following:

| · | the ability of our suppliers to meet our supply requirements; |

| · | the cancellation of large orders; |

| · | the time required for research and development; |

| · | changing design requirements resulting from rapid technology shifts; and |

| · | industry trends impacting the overall market for our customers’ end-products. |

As a result of these and other factors, our results of operations may vary on a quarterly basis and net revenue may be adversely affected from period to period. Our results of operations for a particular quarter may not be indicative of our future performance. If our operating results in a quarter fall below our expectations or the expectations of market analysts or investors, the price of our ordinary shares is likely to decrease.

Our operating results are substantially dependent on development of new customized module design solutions.

We may be unable to develop new customized module design solutions in a timely or cost-efficient manner, and these new solutions may fail to meet the requirements of our customers’ end-markets. If we fail to develop new solutions that help our customers respond to competitive pressures, achieve shorter time-to-market or broaden and improve their product offerings, we will lose business and our results of operations will be materially and adversely affected.

If our customers do not accept our proposed customized module design solutions or do not purchase from us the specified components contained in the proposed module reference design, our net revenue will be adversely affected.

While many of our proposed customized module design solutions are accepted by our customers, there is no obligation for customers to accept our proposed solutions. We dedicate personnel, management and financial resources to research and development and technical support in developing new customized module design solutions for our customers. The time frames for most research and development projects typically range from two to eighteen months. For product sales, because we do not charge a design fee, but rather generate revenue through the resale of specified components contained in our proposed reference designs, if our customers do not accept our proposed designs, we will fail to capitalize on the invested resources, time and effort that we expended on a project. Furthermore, our customers typically make purchases on a purchase order basis. Prior to submission of a purchase order, our customers are not obligated to purchase from us any quantity of specific components that we propose to sell in our proposed module reference design. Our customers may cancel or defer their purchase orders on short notice without significant penalty. Even if a customer accepts our proposed module reference design, the customer could bypass us and contract with our competitors or possibly our suppliers directly for the purchase of the specific components we otherwise had proposed to sell. The failure to accept our proposed module reference design, the loss of ongoing business from our customers or the transition away from us in favor of direct purchases from our competitors or suppliers could each result in our failure to realize potentially significant net revenue.

Reliance on our suppliers, with whom we often do not have long-term supply agreements, makes us vulnerable to the loss of one or more key suppliers or the delivery capabilities of our suppliers.

We typically rely on a limited number of key suppliers, and many customized module design solutions that we develop are designed around technology components provided by our suppliers. We typically do not have long-term supply agreements or other forms of exclusive arrangements with our suppliers. In 2012, for example, Broadcom, Sandisk, Freescale Semiconductor and Atmel accounted for approximately 45.7%, 9.6%, 6.9% and 5.8%, respectively, of our cost of sales. If we lose a key supplier or a supplier reduces the quantity of products it sells to us, does not maintain a sufficient inventory level of products required by us or is otherwise unable to meet our demand for its components, we may have to expend significant time, effort and other resources to locate a suitable alternative supplier and secure replacement components. For example, on one prior occasion, one of our key suppliers experienced an interruption in its production capacity due to a relocation of its production facilities, which resulted in its inability to meet our quarterly supply requirements. If suitable replacement components are unavailable, we may be forced to redevelop certain of our solutions, which ultimately may not be accepted by our customers.

Also, if our suppliers fail to introduce new products that keep up with new technologies, they may be surpassed by other suppliers entering the market with whom we may not have existing relationships. The costs and delays related to finding new suppliers or redeveloping solutions could significantly harm our business.

If we fail to attract and retain key personnel, particularly our chief executive officer, our business will be materially impaired and our financial condition and results of operations will suffer.

Our business greatly relies on the continued services of Jeffrey Kang, our principal shareholder and chief executive officer. Many relationships with our key suppliers and key customers have been developed by and continue to be maintained by Mr. Kang. Our future success will depend to a significant degree upon the performance and contribution of Mr. Kang and other members of our senior management team in areas including sales, research and development, information technology and finance. Therefore, our business and results of operations may be materially and adversely affected if Mr. Kang or another member of our senior management team leaves us, which they may do at any time. In addition, we will incur additional expenses to recruit and develop senior management members if one or more of our key employees are unwilling or unable to continue his or her employment with us. We do not maintain any life insurance covering our senior management or any of our key employees.

Our future success also depends on our ability to identify, attract, hire, train, retain and motivate highly-skilled personnel. If we cannot attract and retain the personnel we require at a reasonable cost, our cost of goods sold will increase and the profitability of our business could be negatively affected. Our business is especially dependent on sales, marketing, research and development, and services personnel. Competition in the PRC for executive-level and skilled technical and sales and marketing personnel is strong, and recruiting, training, and retaining qualified key personnel are important factors affecting our ability to meet our growth objectives. Should key employees leave our company, we may lose both an important internal asset and net revenue from customer projects in which those employees were involved.

Loss of key customers may adversely impact our net revenue.

We generate the majority of our net revenue from a small number of key customers, and we anticipate that a relatively small number of key customers will continue to account for a significant portion of our net revenue in the foreseeable future, particularly in the telecommunications equipment market. In 2012, our sales to ZTE, T&W Electronics, Yulong and Wuhan Research Institute of Post & Telecommunications accounted for approximately 16.1%, 9.7%, 5.6% and 4.2%, respectively, of our net revenue. Sales to our top 10 customers represented approximately 51.3% of our net revenue in 2012. Should we lose, receive reduced orders from, or experience any adverse change in our relationship with any of our key customers, or should they decide to use solutions provided by other companies, we will suffer a substantial loss in net revenue.

The end-markets in which we operate are highly competitive and fragmented. Competition may intensify in the future, and if we fail to compete effectively, our business will be harmed.

Pressures from current or future competitors could cause our solutions to lose market acceptance or require us to significantly reduce our sales prices to keep and attract customers. Our competitors often have longer operating histories, stronger customer and supplier relationships, larger technical staffs and sales forces, and/or greater financial, technical and marketing resources than we do. Although we believe that there are no direct competitors of any meaningful size who operate using the same business model as ours, we face indirect competition from:

| · | Other technology component suppliers. For each project, we work with one enabling technology component supplier to compete against other enabling technology component suppliers. Consequently, we indirectly compete against our suppliers’ competitors. For example, by working with JDS Uniphase, we compete against companies such as Avanex Corp. and Bookham Inc. in supplying optical transmission module design solutions. |

| · | Component manufacturers and distributors. We compete indirectly with component manufacturers such as Epcos AG, and component distributors such as Arrow Electronics, Inc. and Avnet Inc., which may seek to expand their product/service offerings to include customized module design solutions. |

We may also face indirect competition from customers and suppliers. Currently many of our customers and suppliers do not focus on customized module design. If our customers or suppliers decide to devote more time and resources to in-house module design, the demand for our solutions may decline. In addition, our customers may change their procurement strategy or decide to rely on us primarily for component delivery and not for integration or design work. Similarly, component suppliers may also seek to offer their component products or modules incorporating key components from our solutions directly to our customers. The loss of customers for our customized module design solutions as a result of these competitive factors would have a material adverse effect on our business, financial condition and results of operations.

As we expand our business, we intend to develop new customized module design solutions and technological capabilities in end-markets where we do not currently have extensive experience or technological capability. Failure to develop or execute this growth strategy will have a material adverse effect on our net revenue.

Prior to 2005, we derived substantially all of our net revenue from our customized module design solutions provided to customers in the mobile handset and telecommunications equipment end-markets. In 2005, we began targeting the digital media end-market. In 2006 and 2007, we began our own business of providing engineering service and software design, respectively. In 2008, we also started targeting the industrial business end-market. Our success in the digital media end-market will depend, in significant part, on our ability to continue to develop the necessary technological capability and to leverage our existing customer base that has expanded into this end-market. If we are unable to quickly develop technological expertise, increase our research and development capabilities and leverage our customer base as anticipated, our return on our investment with respect to these efforts may be lower than anticipated and our operating results may suffer. Finally, our customer base may not respond to our efforts to expand our proprietary capabilities and may be unwilling to utilize these enhanced capabilities.

We may be unable to manage rapid growth and a changing operating environment, which could adversely affect our ability to serve our customers and harm our business.

We have experienced rapid growth over the last five years, with our net revenue increasing from RMB1,960 million in 2008 to RMB4,891 million (USD785 million) in 2012. Our number of employees has increased from approximately 30 in 2001 to 540 as of December 31, 2012. We have limited operational, administrative and financial resources, which may be inadequate to sustain our current growth rate. If we are unable to manage our growth effectively, the quality of our solutions could deteriorate and our business may suffer. As our customer base increases and we enter new end-markets, we will need to:

| · | increase our investments in personnel, research and development capabilities, facilities and other operational areas; |

| · | continue training, motivating and retaining our existing employees, and attract and integrate new qualified employees; |

| · | develop and improve our operational, financial, accounting and other internal systems and controls; and |

| · | take enhanced measures to protect any proprietary technology or technological capability we develop. |

Any failure to manage our growth successfully could distract management’s attention and result in our failure to serve our customers and harm our business.

We face risks associated with future investments or acquisitions.

An important component of our growth strategy is to invest in or acquire businesses complementary to ours that will enable us to expand the solutions we offer to our existing target customer base, and that will provide opportunities to expand into new markets. We may be unable to identify suitable investment or acquisition candidates or to make these investments or acquisitions on a commercially reasonable basis, if at all. If we complete an investment or acquisition, we may not realize the anticipated benefits from the transaction.

Integrating an acquired company or technology is complex, distracting and time consuming, as well as a potentially expensive process. The successful integration of an acquisition would require us to:

| · | integrate and retain key management, sales, research and development, and other personnel; |

| · | incorporate the acquired products or capabilities into our offerings both from an engineering and sales and marketing perspective; |

| · | coordinate research and development efforts; |

| · | integrate and support pre-existing supplier, distribution and customer relationships; and |

| · | consolidate duplicate facilities and functions and combine back office accounting, order processing and support functions. |

The geographic distance between the companies, the complexity of the technologies and operations being integrated and the disparate corporate cultures being combined may increase the difficulties of combining an acquired company or technology. Acquired businesses are likely to have different standards, controls, contracts, procedures and policies, making it more difficult to implement and harmonize company-wide financial, accounting, billing, information and other systems. Management’s focus on integrating operations may distract attention from our day-to-day business and may disrupt key research and development, marketing or sales efforts.

Our acquisition strategy also depends on our ability to obtain necessary government approvals that may be required, as described under “—Risks Related to Doing Business in the PRC—Our acquisition strategy may be subject to SDRC approval under legislation enacted in 2004.”

Our competitive position could decline if we are unable to obtain additional financing to acquire businesses or technologies that are strategic for our success, or otherwise execute our business strategy.

We believe that our current cash will be sufficient to fund our working capital and capital expenditure requirements for at least the next twelve months. However, we may need to raise additional funds to support more rapid expansion, respond to competitive pressures, acquire complementary businesses or technologies or respond to unanticipated requirements. We cannot assure you that additional funding will be available to us in amounts or on terms acceptable to us. If sufficient funds are not available or are not available on acceptable terms, our ability to fund our expansion, take advantage of acquisition opportunities, develop or enhance our services or products, or otherwise respond to competitive pressures would be significantly limited.

If appropriate opportunities arise, we intend to acquire businesses, technologies, services or products that we believe are strategic for our success. Our competitive position could decline if we are unable to identify and acquire businesses or technologies that are strategic for our success in this market.

The unauthorized use of our intellectual property could have a material adverse impact on our net revenue.

Our in-house design engineering teams develop our customized module design solutions. We typically do not have patent or other intellectual property protection for our solutions, nor do we typically have non-disclosure or confidentiality agreements with most of our suppliers or customers to keep our design specifications confidential. Suppliers or other competitors may attempt to circumvent us by selling products or providing module design solutions directly to our customers. The unauthorized use by our suppliers or other competitors of our module design solution specifications or other intellectual property in the future would result in a substantial decrease in our net revenue. The validity, enforceability and scope of protection of intellectual property in the PRC is uncertain and still evolving, and PRC laws may not protect intellectual property rights to the same extent as the laws of some other jurisdictions, such as the United States. Moreover, litigation may be necessary in the future to enforce any intellectual property rights we may establish or acquire in the future, which could result in substantial costs and diversion of our resources, and have a material adverse effect on our business, financial condition and results of operations.

We became a public company through a share exchange with a non-operating public shell company, where we were the accounting acquirer and assumed all known and unknown potential liabilities of our predecessor entity.

Our July 2004 share exchange with Trident Rowan Group, Inc. (“Trident”) was accounted for as a reverse merger in which Comtech Group, a Cayman Islands company (“Comtech Cayman”) was deemed the accounting acquirer and Trident, which was originally incorporated in 1917, was the legal acquirer. We have retained all the known and unknown liabilities of Trident. There may be other potential liabilities about which we are not yet aware.

We continue to act as the guarantors of certain subsidiaries (the “Disposal Group”) that we sold to Envision Global Group (“Envision”), including Comtech Communication Technology (Shenzhen) Company Limited (“Comtech Communication”), Comtech International (Hong Kong) Limited (“Comtech Hong Kong”), Comtech Software Technology (Shenzhen) Company Limited (“Comtech Software”) and Epcot Multimedia Technology (SZ) Co. Ltd. (“Epcot”), for existing credit facilities granted to the Disposal Group and for certain suppliers and customers of the Disposal Group. If any of the Disposal Group entities fail to meet their repayment obligations, our operating results would be adversely affected by any amounts we could become liable to cover on their behalf.

Pursuant to a Sale and Purchase Agreement dated October 23, 2012 with Envision (the “Envision Agreement”), we sold certain subsidiaries, including Comtech Communication, Comtech Hong Kong, Comtech Software and Epcot, to Envision for a total consideration of USD78 million. The transactions contemplated by the Envision Agreement closed and the entire purchase price was fully received on November 15, 2012 (“Date of Sale”). In connection with the disposal, we agreed to continue to provide certain transitional guarantee services (the “Transitional Guarantee Services”), whereby we act as the guarantors of the Disposal Group and continue to provide and honor, from the Date of Sale until December 31, 2014 (unless earlier terminated by mutual consent): (i) guarantees given by us and our subsidiaries in favor of banks and financial institutions in respect of all existing credit facilities granted to the Disposal Group; and (ii) guarantees given by us and our subsidiaries in favor of the Disposal Group’s suppliers and customers subject to a maximum cap of USD60 million. In consideration of the Transitional Guarantee Services provided by us, Envision agreed to pay a guarantee service fee of USD250,000 (or pro-rated if terminated earlier) each 3 month-period following the Date of Sale.

If the Disposal Group or Envision fails to repay the banks or its suppliers or customers, we will become liable for the amounts owed by the Disposal Group under the terms of its agreements with such creditors, which could materially and adversely affect our operating results and financial condition.

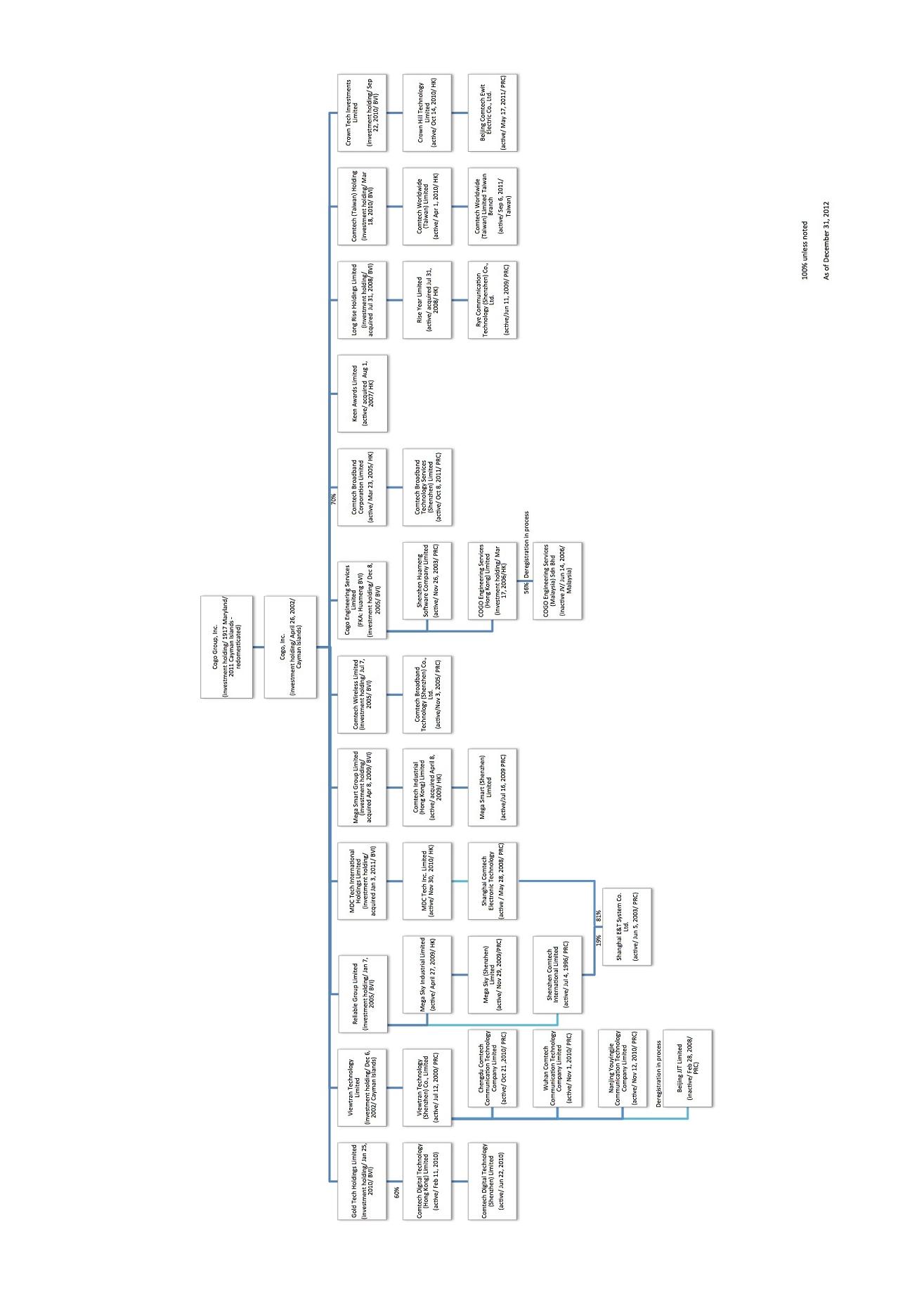

We depend upon contractual agreements with the legal shareholders of Shenzhen Comtech International Limited (“Shenzhen Comtech”) and Shanghai Comtech Electronic Technology Company Limited (“Shanghai Comtech”) to conduct our business and receive payments through Shenzhen Comtech, Shanghai Comtech and Shanghai E&T System Company Limited (“Shanghai E&T”). Such contractual arrangements may not be as effective in providing operational control as direct ownership and may be difficult to enforce. Further, if the PRC government finds these contractual agreements violate or conflict with PRC governmental regulations, our business would be materially adversely affected.

At the time of its incorporation, foreign shareholding in a trading business such as Shenzhen Comtech could not exceed 65%. With subsequent PRC deregulation, foreign ownership of such a trading business can now reach 100%, and approval of foreign ownership of companies in the PRC engaged in commodity trading businesses—which includes agency trade, wholesale, retail and franchise operations is now delegated to local government agencies of the PRC Ministry of Commerce.

In order to exercise control over Shenzhen Comtech (a PRC operating company legally permitted to engage in a commodity trading business), without direct shareholding by us (a U.S.-listed company and therefore a foreign-invested entity), Honghui Li, our vice president, and Huimo Chen, the mother of our principal shareholder and chief executive officer, Jeffrey Kang, hold 99% and 1%, respectively, of the equity interests of Shenzhen Comtech, and through contractual agreements with us hold such equity interests exclusively for the benefit of our 100% directly owned subsidiary. Shenzhen Comtech, in turn owns a 19% equity interest in another of our PRC operating companies, Shanghai E&T, and Shanghai Comtech owns the remaining 81%. While we do not have any equity interest in either Shenzhen Comtech, or Shanghai Comtech or Shanghai E&T, through these contractual agreements, we enjoy voting control and are entitled to the economic interests associated with the equity interest in these three entities. These contractual agreements may not be as effective as direct ownership in providing us with control over Shenzhen Comtech, Shanghai Comtech and Shanghai E&T because we rely on the performance of legal shareholders under the agreements. If these shareholders fail to perform their respective obligations under the agreements, we may have to incur substantial costs and resources to enforce such agreements and may not be able to do so in any case. Further, the profits of Shenzhen Comtech, Shanghai Comtech and Shanghai E&T may not be able to be remitted outside the PRC due to foreign exchange controls. Also, we must rely on legal remedies under applicable law, which may not be as effective as those in the United States. Because we rely on Shenzhen Comtech, Shanghai Comtech and Shanghai E&T in conducting our business operations in the PRC, the realization of any of these risks relating to our corporate structure could result in a material disruption of our business, diversion of our resources and the incurrence of substantial costs, any of which could materially and adversely affect our operating results and financial condition.

Pursuant to the Envision Agreement, we sold certain subsidiaries, including Comtech Communication, Comtech Hong Kong, Comtech Software and Epcot, to Envision for a total consideration of USD78 million. The entire purchase price was received and the transactions contemplated by the Envision Agreement closed on November 15, 2012. One of our indirectly controlled subsidiaries, Shanghai Comtech, did not form part of the Disposal Group, but its 100% equity interest is held by one of entities in the Disposal Group. In order to retain control over Shanghai Comtech, we, through one of our 100% wholly-owned subsidiaries, entered into legal arrangements with the Disposal Group pursuant to which the Disposal Group agreed to hold the equity interest in Shanghai Comtech on behalf of our wholly-owned subsidiary and waive all rights and risks of ownership of the equity interests in favour of our wholly-owned subsidiary. Accordingly, we retain our control over Shanghai Comtech through such legal arrangements.

In the opinion of our PRC counsel, the ownership structure of Shenzhen Comtech and Shanghai Comtech and the contractual agreements among our 100% directly owned subsidiaries and legal shareholders do not violate existing PRC laws, rules and regulations. There are, however, substantial uncertainties regarding the interpretation and application of current or future PRC laws and regulations, including but not limited to the laws and regulations governing the validity and enforcement of these contractual agreements. Accordingly, we cannot assure you that PRC regulatory authorities will not determine that these contractual agreements violate or conflict with PRC laws or regulations.

If we or our PRC operating companies, Shenzhen Comtech, Shanghai Comtech and Shanghai E&T, are found to violate any existing or future PRC laws or regulations, the relevant regulatory authorities will have broad discretion in dealing with such violation, which would cause significant disruptions to our business operations or render us unable to conduct our business operations and may materially adversely affect our business, financial condition and results of operations.

Risks Related to Our Industry

Our inability to respond quickly and effectively to rapid technological advances and market demands would adversely impact our competitive position and our results of operations.

Historically, we have focused on the digital media and telecommunications equipment end-markets in the PRC. The digital media and telecommunications equipment end-markets are characterized by rapid technological advances, intense competition, frequent introduction of new products and services and consumer demand for greater functionality, lower costs, smaller products and better performance. We must constantly seek out new products and develop new solutions to maintain in our portfolio. We have experienced and will continue to experience some solution design obsolescence. We expect our customers’ demands for improvements in product performance to increase, which means that we must continue to improve our design solutions and develop new solutions to remain competitive and grow our business. Our failure to compete successfully for customers will result in price reductions, reduced margins or loss of market share, any of which would harm our business, results of operations and financial condition.

A large portion of our net revenue currently comes from sales to manufacturers in the cyclical digital media and telecommunications equipment end-markets and cyclical downturns could harm our operating results.

The digital media and telecommunications equipment end-markets in particular are highly cyclical and have experienced severe and prolonged downturns, often in connection with maturing product cycles and declines in general economic conditions. These downturns have been characterized by diminished product demand, production overcapacity, high inventory levels and accelerated erosion of average selling prices. The impact of slowing end-customer demand may be compounded by higher than normal levels of equipment and inventories among our customers and our customers’ adjustments in their order levels, resulting in increased pricing pressure.

In addition, our recent and significant growth in net revenue resulted, in large part, from the high growth in sales of industrial applications products in the PRC. These domestic manufacturers may not continue to grow their sales at historical levels, if at all. The stagnation or reduction in overall demand for industrial applications products would materially affect our results of operations and financial condition.

The digital media end-market is characterized by a short product lifecycle, making time-to-market and sensitivity to customer needs critical to our success and our failure to respond will harm our business.

Mobile handsets in the digital media end-market typically have a lifecycle of approximately six to twelve months before the technology becomes obsolete. Time-to-market, both with respect to our customers’ ability to supply consumers with timely and marketable products and our ability to provide our customers with a wide array of latest generation customized module design solutions, is critical to our success. As design cycles in the industry shorten, we face logistical challenges in providing our solutions in an increasingly shorter timeframe. If we are unable to respond to the shortened lifecycles and time-to-market, our business will suffer.

The global financial crisis could harm our product demands and adversely affect our results of operations.

Due to difficult market conditions, the level of consumer and information technology spending has declined and the demand for our mobile handsets business since the third quarter of 2008 has decreased. Furthermore, we may need to strategically lower our pricing in order to grow our business in a slowing economic environment.

Risks Related to Doing Business in the PRC

There are substantial risks associated with doing business in the PRC, including those set forth in the following risk factors.

Our operations may be adversely affected by the PRC’s economic, political and social conditions.

Substantially all of our operations and assets are located in the PRC and substantially all of our net revenue are derived from our operations in the PRC. Accordingly, our results of operations and future prospects are subject to economic, political and social developments in the PRC. In particular, our results of operations may be adversely affected by:

| · | changes in the PRC’s political, economic and social conditions; |

| · | changes in policies of the government or changes in laws and regulations, or the interpretation of laws and regulations; |

| · | changes in foreign exchange regulations; |

| · | measures that may be introduced to control inflation, such as interest rate increases; and |

| · | changes in the rate or method of taxation. |

The PRC economy has historically been a planned economy. The majority of productive assets in the PRC are still owned by various levels of the PRC government. In recent years the government has implemented economic reform measures emphasizing decentralization, utilization of market forces in the development of the economy and a high level of management autonomy. Such economic reform measures may be inconsistent or ineffectual, and we may not benefit from all such reforms. Furthermore, these measures may be adjusted or modified, possibly resulting in such economic liberalization measures being applied inconsistently from industry to industry, or across different regions of the country.

In the past twenty years, the PRC has been one of the world’s fastest growing economies in terms of gross domestic product, or GDP. This growth may not be sustainable. Moreover, a slowdown in the economies of the United States, the European Union and certain Asian countries may adversely affect economic growth in the PRC which depends on exports to those countries. Our financial condition and results of operations, as well as our future prospects, would be materially and adversely affected by an economic downturn in the PRC.

Our financial results benefit from tax concessions granted by the PRC government, the change to or expiration of which would materially change our results of operations.

Our results of operation may be adversely affected by changes to or expiration of tax holiday and preferential tax concessions that some of our PRC operating companies currently enjoy or expect to enjoy in the future. As a result of tax holiday and preferential tax rate incentives, our operations have been subject to relatively low tax liabilities. Tax that would otherwise have been payable without tax holiday treatment amounted to approximately RMB29.1 million (USD4.7 million) in 2012. For additional details regarding these tax incentives, please see “Item 5. Operating and Financial Review and Prospects—Taxation.”

Tax laws in the PRC are subject to interpretations by relevant tax authorities. The tax holiday treatment may not remain in effect or may change, in which case we may be required to pay the higher income tax rate generally applicable to Chinese companies, or such other rate as is required by the laws of the PRC.

On March 16, 2007, the National People’s Congress passed the Corporate Income Tax law (the “CIT law”), which revised the PRC statutory income tax rate to 25%. The CIT law was effective on January 1, 2008. Accordingly, our PRC subsidiaries are subject to income tax at 25% effective from January 1, 2008 unless otherwise specified. The CIT law and its relevant regulations provide a five-year transition period from January 1, 2008 for those companies which were established before March 16, 2007 and were entitled to preferential lower tax rates under the then effective tax regulations, as well as grandfathering certain tax holidays. The transitional tax rates are 20%, 22%, 24% and 25% for 2009, 2010, 2011 and 2012 onwards, respectively. For our subsidiaries located in Shenzhen Special Economic Zone, the PRC that were each entitled to a tax holiday of two-year tax exemption followed by three-year 50% tax reduction starting from the first profit making year from the PRC tax perspective, they are entitled to enjoy the transitional rates and continue their tax holidays until they expire. For the entities which had not commenced their respective tax holidays as of December 31, 2007, the CIT law and its relevant regulations require their tax holidays to begin on January 1, 2008.

The telecommunications equipment market is extensively regulated in the PRC.

The telecommunications equipment end-market accounted for 44.2% of our net revenue in 2012. PRC’s telecommunications industry is heavily regulated. Changes in regulations affecting sales of these customers could negatively affect the telecommunications equipment end-market for our solutions, which will materially harm our business.

PRC government control of currency conversion may affect our ability to meet foreign currency obligations.

Because the majority of our net revenue are denominated in Renminbi, any restrictions on currency exchange may limit our ability to use revenue generated in Renminbi to meet our foreign currency obligations, such as settling the purchase of materials which may be denominated in U.S. dollars. The principal regulation governing foreign currency exchange in the PRC is the Foreign Currency Administration Rules (1996), or the Rules, as amended. Under the Rules, once certain procedural requirements are met, Renminbi is convertible for current account transactions, including trade and service-related foreign exchange transactions and dividend payments, but not for capital account transactions, including direct investment, loans or investments in securities outside the PRC, without prior approval of the PRC State Administration of Foreign Exchange (“SAFE”), or its local counter-parts. Since a significant amount of our future revenues will continue to be denominated in Renminbi, any existing and future restrictions on currency exchange may limit our ability to utilize revenue generated in the PRC to fund our business activities outside of the PRC, if any, or expenditures denominated in foreign currencies, or our ability to meet our foreign currency obligations, which could have a material adverse effect on our business, financial condition and results of operations. We cannot be certain that the PRC regulatory authorities will not impose more stringent restrictions on the convertibility of Renminbi with respect to foreign exchange transactions.

PRC regulations relating to offshore investment activities by PRC residents may increase the administrative burden we face and create regulatory uncertainties that could restrict our overseas and cross-border investment activity, and a failure by our shareholders who are PRC residents to make any required applications and filings pursuant to such regulations may prevent us from being able to distribute profits and could expose us and our PRC resident shareholders to liability under PRC law.

In October 2005, SAFE promulgated regulations that require PRC residents and PRC corporate entities to register with and obtain approvals from relevant PRC government authorities in connection with their direct or indirect offshore investment activities. These regulations apply to our shareholders who are PRC residents in connection with our prior and any future offshore acquisitions.

The SAFE regulation required registration by March 31, 2006 of direct or indirect investments previously made by PRC residents in offshore companies prior to the implementation of the Notice on Issues Relating to the Administration of Foreign Exchange in Fund-Raising and Reverse Investment Activities of Domestic Residents Conducted via Offshore Special Purpose Companies on November 1, 2005. If a PRC shareholder with a direct or indirect stake in an offshore parent company fails to make the required SAFE registration, the PRC subsidiaries of such offshore parent company may be prohibited from making distributions of profit to the offshore parent and from paying the offshore parent proceeds from any reduction in capital, share transfer or liquidation in respect of the PRC subsidiaries, and may be prohibited from receiving capital contributions, shareholder loan or other payments from our offshore parent company, and may be further prohibited from making payments to or receiving payments from other overseas entities. Furthermore, failure to comply with the various SAFE registration requirements described above could result in liability under PRC law for foreign exchange evasion.

Some of our PRC resident shareholders may not have completed their registration with SAFE under the SAFE regulation, in part, due to confusion over the application of the SAFE regulation to our company. For example, in mid-2006, some of our PRC resident shareholders attempted to register with SAFE in Shenzhen under predecessor regulations to the SAFE regulation, but were informed by Shenzhen SAFE that the regulation did not apply to them. These PRC resident shareholders did not realize they might be required to register under the new SAFE regulations. Further, even if our PRC resident shareholders do apply for SAFE registration, they may not be able to obtain such registration at the discretion of SAFE due to various reasons including their failure to comply with the retroactive SAFE registration requirement prior to March 31, 2006, the statutorily prescribed deadline for compliance. The failure or inability of our PRC resident shareholders to obtain any required approvals or make any required registrations may subject us to fines and legal sanctions, prevent us from being able to make distributions or pay dividends or to receive capital contribution or shareholder loans, as a result of which our business operations and our ability to distribute profits to you or capitalize our operation in the PRC could be materially and adversely affected.

In December 2006, the People’s Bank of China promulgated the Administrative Measures of Foreign Exchange Matters for Individuals, or the PBOC Regulation, setting forth the respective requirements for foreign exchange transactions by PRC individuals under either the current account or the capital account. In January 2007, SAFE issued implementing rules for the PBOC Regulation, which, among other things, specified approval requirements for certain capital account transactions such as a PRC citizen’s participation in the employee stock ownership plans or stock option plans of an overseas publicly-listed company. On March 28, 2007, SAFE promulgated the Application Procedure of Foreign Exchange Administration for Domestic Individuals Participating in Employee Stock Holding Plan or Stock Option Plan of Overseas-Listed Company, or the Stock Option Rule. Under the Stock Option Rule, PRC citizens who are granted stock options by an overseas publicly-listed company are required, through a PRC agent or PRC subsidiary of such overseas publicly-listed company, to register with SAFE and complete certain other procedures. We and our PRC employees who have been granted stock options will be subject to the Stock Option Rule when our company becomes an overseas publicly-listed company. If we or our PRC optionees fail to comply with these regulations, we or our PRC optionees may be subject to fines and legal sanctions.

Our acquisition strategy may be subject to SDRC approval under legislation enacted in 2004.

The State Development and Reform Commission, or SDRC, promulgated a regulation in 2004 that requires SDRC approval in connection with direct or indirect offshore investment activities by individuals who are PRC residents and PRC corporate entities. This regulation may apply to our future offshore or cross-border acquisitions, as well as to the equity interests in offshore companies held by our PRC shareholders who are considered PRC residents. We intend to make all required application and filings, and will require the shareholders of the offshore entities in our corporate group who are considered PRC residents to make the application and filings, as required under the regulation and under any implementing rules or approval practices that may be established under this regulation. However, because this regulation lacks implementing rules, approval precedents or reconciliation with other approval requirements, it remains uncertain how this regulation, and any future legislation concerning offshore or cross-border transactions, will be interpreted and implemented by the relevant government authorities. The approval criteria by SDRC agencies for outbound investment by PRC residents are not provided under this regulation or other SDRC regulations. Accordingly, we cannot provide any assurances that we will be able to comply with, qualify under or obtain any approval as required by this regulation or other related legislations. Our failure or the failure of our PRC resident shareholders to obtain SDRC approvals may restrict our ability to acquire a company outside of the PRC or use our entities outside of the PRC to acquire or establish companies inside of the PRC, which could negatively affect our business and future prospects.

PRC laws and our corporate structure may restrict our ability to receive dividends and payments from, and transfer funds to, our PRC operating companies, which may negatively affect our results of operations and restrict our ability to act in response to changing market conditions.

Substantially all of our operations are conducted through our PRC operating companies. The ability of our PRC operating companies to make dividends and other payments to us may be restricted by factors such as changes in applicable foreign exchange and other laws and regulations. For example, under the regulations discussed above, the foreign exchange activities of our present or prospective PRC subsidiaries are conditioned upon the compliance with the SAFE registration requirements by the shareholders of our offshore entities who are PRC residents. Failure to comply with these SAFE registration requirements may substantially restrict or prohibit the foreign exchange inflow to and outflow from our PRC subsidiaries, namely Shenzhen Comtech, Shanghai Comtech, Shanghai E&T and Viewtran Technology (Shenzhen) Co. Ltd. (“Viewtran PRC”), including, remittance of dividends and foreign-currency-denominated borrowings by these PRC subsidiaries. In addition, our PRC operating companies are required, where applicable, to allocate a portion of their net profit to certain funds before distributing dividends, including at least 10% of their net profit to certain reserve funds until the balance of such fund has reached 50% of their registered capital. These reserves can only be used for specific purposes, including making-up cumulative losses of previous years, conversion to equity capital, and application to business expansion, and are not distributable as dividends. Our PRC operating companies are also required, where applicable, to allocate an additional 5% to 10% of their net profits to the common welfare fund. The net profit available for distribution from our PRC operating companies is determined in accordance with generally accepted accounting principles in the PRC, which may materially differ from a determination performed in accordance with U.S. GAAP. As a result, we may not receive sufficient distributions or other payments from these entities to enable us to make dividend distributions to our shareholders in the future, even if our U.S. GAAP financial statements indicate that our operations have been profitable. For additional details regarding the taxation risk of dividend distributions from our PRC operating companies, please see “Item 3. Key Information – Risk Factors – Our global income and your capital gain may be subject to PRC tax under the new PRC tax law, which may have an effect on our results of operations and your investments, respectively.”

We do not directly own the equity interests in: (i) Shenzhen Comtech, which accounted for approximately 0.6% of our net revenue in 2012; or (ii) Shanghai Comtech, which accounted for approximately 1.7% of our net revenue in 2012. Shenzhen Comtech and Shanghai Comtech own 19% and 81% equity interest in Shanghai E&T, respectively, which accounted for 2.2% of our net revenue in 2012. Honghui Li and Huimo Chen, the shareholders of Shenzhen Comtech, and the Disposal Group, the shareholder of Shanghai Comtech, have contractually agreed, among others things, to apply all dividends or other payments they receive from Shenzhen Comtech and Shanghai Comtech to payments to our 100% wholly-owned subsidiaries, or their designated entities, for valid and valuable consideration and to the extent permitted by applicable PRC law, including PRC foreign exchange law. PRC law and regulatory requirements would currently restrict the ability of the shareholders of Shenzhen Comtech and Shanghai Comtech, based solely upon the contractual agreements, to directly apply the dividends or other payments they receive from Shenzhen Comtech and Shanghai Comtech in U.S. dollars to payments to our 100% wholly-owned subsidiaries or in Renminbi to their designated entities in the PRC. For example, the PRC foreign exchange authorities would have discretion to review the adequacy of the consideration given in exchange for the application of any dividends or payments from Shenzhen Comtech and Shanghai Comtech to our 100% wholly-owned subsidiaries. If the legal shareholders fail to apply such dividends or other payments received from Shenzhen Comtech and Shanghai Comtech, which might include profit distributions from Shanghai E&T, to payments to our 100% wholly-owned subsidiaries or their designated entities, our financial condition would be negatively affected. Apart from the dividend distribution from our PRC subsidiaries to us, the transfer of funds from our company to our PRC operating companies, either as a shareholder loan or as an increase in registered capital or otherwise, is subject to registration or approval with or by PRC governmental authorities, including the relevant administration of foreign exchange and/or other relevant examining and approval authorities. These limitations on the free flow of funds between us and our PRC operating companies may restrict our ability to act in response to changing market conditions.

Fluctuations in exchange rates could adversely affect our business.

Because a substantial majority of our earnings and cash assets are denominated in Renminbi, fluctuations in the exchange rate between the U.S. dollar and the Renminbi will affect the relative purchasing power of any proceeds from financing and our balance sheet and earnings per share in U.S. dollars following such transaction. In addition, appreciation or depreciation in the value of the Renminbi relative to the U.S. dollar would affect our financial results reported in U.S. dollar terms without giving effect to any underlying change in our business or results of operations. Fluctuations in the exchange rate will also affect the relative value any dividend we may issue that will be exchanged into U.S. dollars and earnings from and the value of any U.S. dollar-denominated investments we make in the future. In addition, a depreciation of the Renminbi relative to the U.S. dollar would have the effect of reducing our U.S. dollar-translated net revenue and increasing the debt servicing requirements for our U.S. dollar-denominated debt. On the other hand, the appreciation of the Renminbi would make our customers’ products more expensive to purchase outside of the PRC because many of our customers are involved in the export of goods, which could adversely affect their sales, thereby eroding our customer base and adversely affecting our results of operations.

Since July 2005, the Renminbi has no longer been pegged to the U.S. dollar. Although currently the Renminbi exchange rate versus the U.S. dollar is restricted to a rise or fall of no more than 1.0% per day and the People’s Bank of China regularly intervenes in the foreign exchange market to prevent significant short-term fluctuations in the exchange rate, the Renminbi may appreciate or depreciate significantly in value against the U.S. dollar in the medium to long term. Moreover, it is possible that in the future, the PRC authorities may lift restrictions on fluctuations in the Renminbi exchange rate and lessen intervention in the foreign exchange market.

Very limited hedging transactions are available in the PRC to reduce our exposure to exchange rate fluctuations. To date, we have not entered into any hedging transactions in an effort to reduce our exposure to foreign currency exchange risk. While we may enter into hedging transactions in the future, the availability and effectiveness of these transactions may be limited and we may not be able to successfully hedge our exposure at all. In addition, our foreign currency exchange losses may be magnified by PRC exchange control regulations that restrict our ability to convert Renminbi into foreign currencies.

The legal system in the PRC has inherent uncertainties that may limit the legal protections available to you as an investor or to us in the event of any claims or disputes with third parties.

The legal system in the PRC is based on written statutes. Prior court decisions may be cited for reference but have limited precedential value. Since 1979, the central government has promulgated laws and regulations dealing with economic matters such as foreign investment, corporate organization and governance, commerce, taxation and trade. As PRC’s foreign investment laws and regulations are relatively new and the legal system is still evolving, the interpretation of many laws, regulations and rules is not always uniform and enforcement of these laws, regulations and rules involve uncertainties, which may limit the remedies available to you as an investor and to us in the event of any claims or disputes with third parties. In addition, any litigation in the PRC may be protracted and result in substantial costs and diversion of resources and management attention.

On August 8, 2006, six PRC regulatory agencies, including the Chinese Securities Regulatory Commission, or CSRC, promulgated the Regulation on Mergers and Acquisitions of Domestic Companies by Foreign Investors, which became effective on September 8, 2006. This new regulation, among other things, requires offshore special purpose vehicles, or SPVs, formed for overseas listing purposes through acquisitions of PRC domestic companies and controlled by PRC individuals, to obtain the approval of the CSRC prior to publicly listing their securities on an overseas stock exchange. We believe, based on the advice of our PRC counsel, that this regulation does not apply to us or any of our prior transactions or offerings and that CSRC approval is not required because such acquisition was completed long before September 8, 2006 when the new regulation became effective. On September 21, 2006, the CSRC published a notice specifying the documents and materials that are required to be submitted for obtaining CSRC approval. In the opinion of our PRC counsel, the new notice does not contradict its interpretation of the new regulation, nor does it add greater clarity to the applicability of the new regulation to us. Based on the advice we have received from our PRC counsel, we do not intend to seek CSRC approval in connection with any of our prior transactions, offerings, or the listing of our shares on NASDAQ.

There may be some uncertainty as to how this regulation will be interpreted or implemented. If the CSRC or other PRC regulatory body subsequently determines that the CSRC’s approval was required for any prior transactions or offerings, we may face sanctions by the CSRC or other PRC regulatory agencies. These regulatory agencies may impose fines and penalties on our operations in the PRC, limit our operation privileges in the PRC, delay or restrict the repatriation of the proceeds from any offerings into the PRC, restrict or prohibit payment or remittance of dividends by Comtech China, or take other actions that could have a material adverse effect on our business, financial condition, results of operations, reputation and prospects, as well as the trading price of our ordinary shares.

You may experience difficulties in effecting service of legal process and enforcing judgments against us and our management.

Substantially all of our operations and assets are located in the PRC. In addition, most of our directors, executive officers and some of the experts named in this document reside within the PRC, and many of the assets of these persons are also located within the PRC. As a result, it may not be possible to effect service of process within the United States or elsewhere outside the PRC upon these directors or executive officers or some of the experts named in this document, including with respect to matters arising under U.S. federal securities laws. Moreover, our PRC legal counsel has advised us that the PRC does not have treaties with the United States or many other countries providing for the reciprocal recognition and enforcement of court judgments. As a result, recognition and enforcement in the PRC of judgments of a court of the United States or any other jurisdiction, including judgments against us or our directors, executive officers, or the named experts, may be difficult or impossible.

The enforcement of civil liabilities against us may be more difficult than if we were a U.S. company.