Fortune Brands Home and Security Investor Presentation September 2011 Exhibit 99.1 |

2 Disclaimer Please note that the information included in this presentation contains statements relating to future results, which are forward-looking statements. We caution you that these forward-looking statements speak only as of the date hereof, and we have no obligation to update them. Actual results may differ materially from those projected as a result of certain risks and uncertainties, including the risks described in our Registration Statement on Form 10, as amended. There can be no assurance that the spin-off of Fortune Brands Home & Security, Inc. will be completed as anticipated or at all. |

3 Distribution Date Distributing Company Transaction Overview Distributed Company Distributed Securities Dividend Policy Fortune Brands, Inc. (NYSE: FO), to be renamed Beam Inc. (NYSE: BEAM) after distribution Fortune Brands Home & Security, Inc. (NYSE: FBHS) 100% of outstanding shares of Fortune Brands Home & Security common stock Distribution Ratio One share of Fortune Brands Home & Security common stock for one share of Fortune Brands common stock Recapitalization of FBHS / Dividend to FO Initially, Fortune Brands Home & Security does not intend to pay a dividend on its common stock Fortune Brands Home & Security has entered into a $1.0 billion of credit facility and will dividend $500 million to Fortune Brands prior to spin-off Fortune Brands Home & Security is expected to have approximately $520 million of debt immediately following spin-off Record Date September 20, 2011 October 3, 2011 |

4 Today’s Presenters Chris Klein Chief Executive Officer Lee Wyatt Chief Financial Officer |

5 FBHS has multiple brands that appeal to consumers and the trade focused in home products, security and storage. Our Partners Our Brands |

6 Our Mission At Fortune Brands Home & Security, our Mission is to create products and services that help fulfill the dreams of homeowners and help people feel more secure |

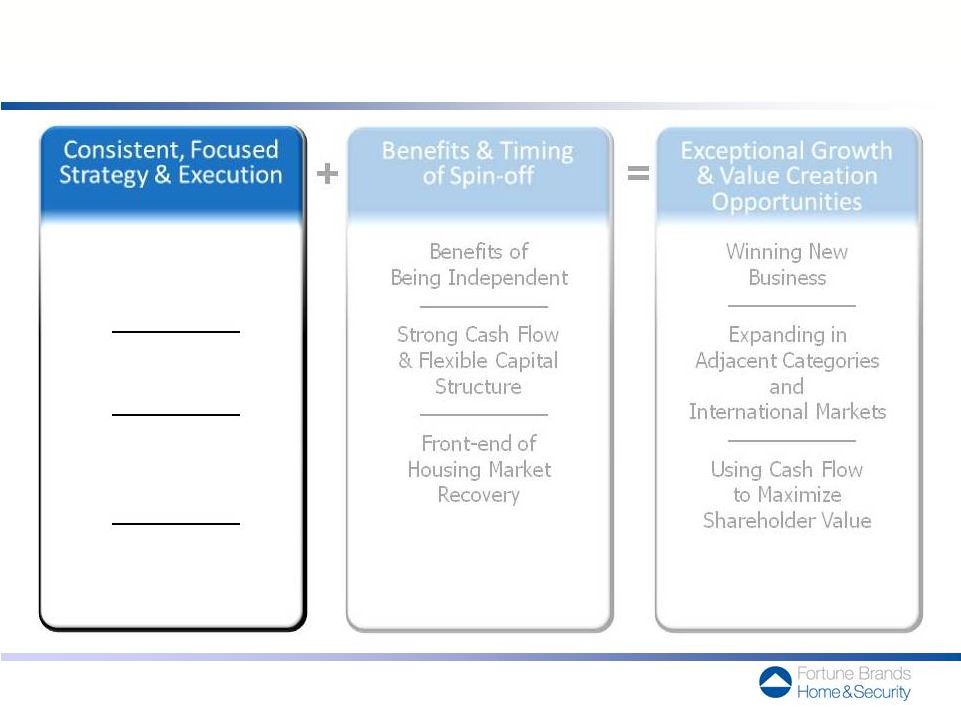

7 Winning New Business Expanding in Adjacent Categories and International Markets Using Cash Flow to Maximize Shareholder Value An Outperforming Industry Leader Well-Positioned to Accelerate Growth and Create Value Attractive Home & Security Product Categories & Positions Consumer & Customer Focus Operational & Management Excellence Demonstrated Ability to Outperform the Market Benefits of Being Independent Strong Cash Flow & Flexible Capital Structure Front-end of Housing Market Recovery Consistent, Focused Strategy & Execution Benefits & Timing of Spin-off Exceptional Growth & Value Creation Opportunities |

8 An Outperforming Industry Leader Well-Positioned to Accelerate Growth and Create Value Attractive Home & Security Product Categories & Positions Consumer & Customer Focus Operational & Management Excellence Demonstrated Ability to Outperform the Market |

9 FBHS has a strong foundation built on systematic innovation, strong brands, excellent customer service and balanced channels of distribution. We believe this foundation can be leveraged to create attractive growth and returns. Solid Business Foundation Strong branding opportunities – To consumer and/or to trade – Underpins channel strength Strong innovation opportunities – Functionality – Fashion/finish – Material conversion Excellent customer service Balance across end markets – New Construction and Repair & Remodel – Retail and Wholesale … and Opportunities for Leveraged Returns Operating leverage — Scale efficiencies and global supply chains Complexity — Ability to add value and/or service Strong channel mix — Ability to deliver products/services across a balance of channels Growth opportunities — Share gains, substantial adjacency opportunities and potential add-on acquisitions |

10 Brand Leadership Position Leading Brands and Differentiated Positions in Each Category Fully integrated platform, poised to leverage scale across multiple brands, channels and price points Powerful engine for consistent growth and profitability Leaders poised to leverage the market recovery Exceptional brand with growth potential well beyond padlocks; more stable market not tied to housing cycle Kitchen & bath cabinet manufacturer in North America Faucet brand in North America Fiberglass residential entry door brand in U.S. Padlock brand in North America #1 #1 #1 #1 Winner of two consumer and five builder awards from JD Power Kitchen & Bath Cabinetry Plumbing & Accessories Advanced Material Windows & Door Systems Security & Storage |

11 Channel Positioning Deep and Broad Channel Strength Specialized distribution for specific channel/customer needs Broad channel presence across price points and demographics Provides distinct value to retail chains Deep builder relationships Halo effect on wholesale channel Global momentum in key international markets Exclusive arrangements with strong two-step distributors Strong trade brand fosters loyal distributor/customer relationships Considerable strength in locksmith channel Widespread distribution across retail channels Commercial market / Channel momentum Home centers Dealers & Showrooms Wholesale 2-Step Other Retail Builders Kitchen & Bath Cabinetry Plumbing & Accessories Advanced Material Windows & Door Systems Security & Storage |

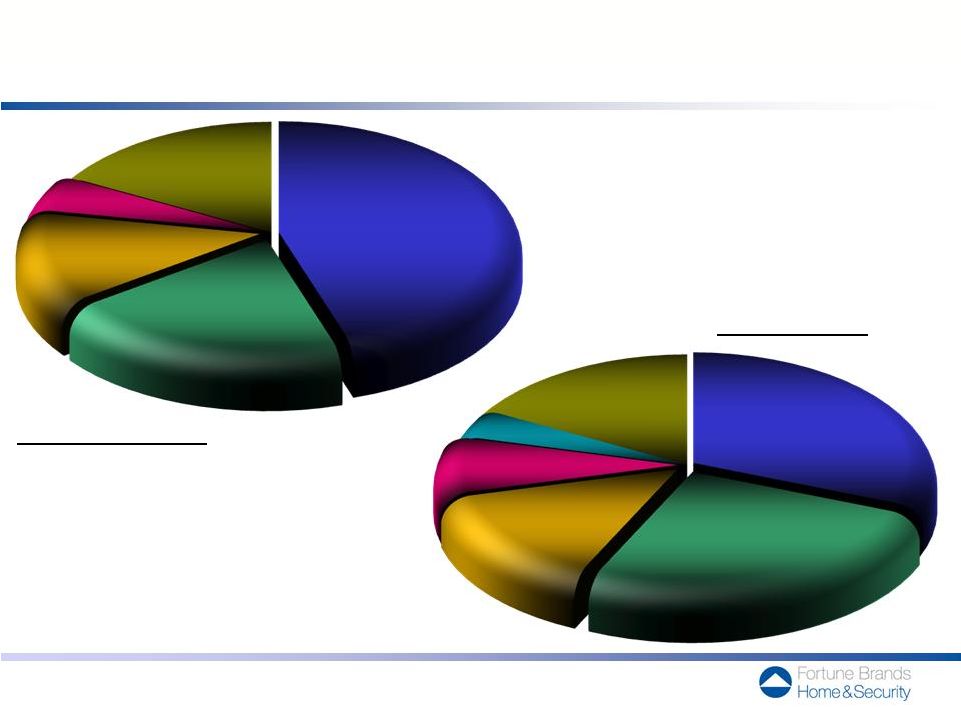

12 Well-Balanced Business Mix by End Market* by Channel* * Source: Company internal estimates for year ended December 31, 2010 Repair & Remodel 45% New Construction 20% Security & Storage 13% Commercial 5% International 17% Wholesale 31% Home Centers 26% Dealer 14% Other Retail 8% International 17% Builder Direct 4% |

13 Consumer Driven Innovation has led to Consistently Winning Profitable New Business Track Record of Leading New Product Launches across all Business Segments Vented Sidelites New Glass Styles Electronics Storage Speed Dial Padlocks Adding value for customers and winning new business Martha Stewart Living cabinetry introduced at all US and Canadian Home Depot stores in 2010 In-stock cabinetry at Lowe’s rolling out in 2011 Moen expanding in home centers and mass retail with new products Waterloo rolling out Husky Garage Organization at all US Home Depot stores in 2011 23% of 2010 sales came from products introduced in the last three years Kitchen & Bath Cabinetry Plumbing & Accessories Advanced Material Windows & Door Systems Security & Storage |

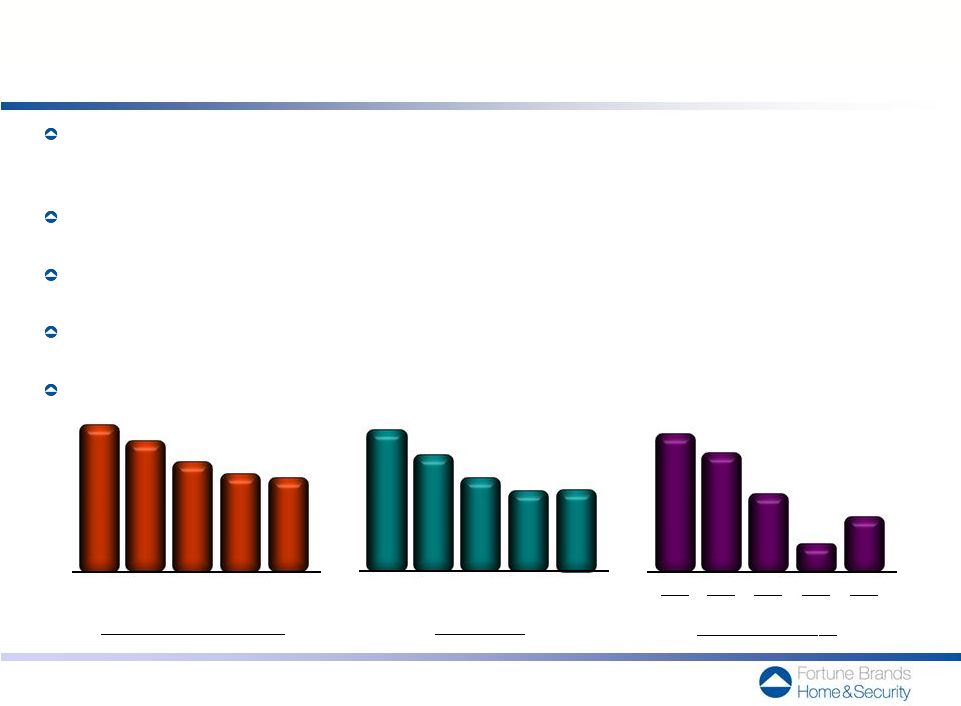

14 Efficient and Scalable Supply Chain / Infrastructure Substantially improved cost structures by proactively reducing footprint nearly 40% between 2006 – 2009 and creating more flexible supply chains Increased productivity through continuous improvement investments Maintaining capacity to ramp up with industry-leading service levels and lead times Well-positioned to accelerate earnings growth as volumes grow Can support revenue of up to $5B without capital spending above normal levels Headcount (000’s) Operating Margin Manufacturing Facilities Sales: 1 - Adjusted Pro Forma: before Charges / Gains, including incremental standalone corporate expenses. 2006 2007 2008 2009 2010 2006 2007 2008 2009 2010 2006 2007 2008 2009 2010 $4.7B $4.6B $3.8B $3.0B $3.2B 27.7 64 56 47 41 40 22.8 18.4 15.8 16.1 14.2% 12.1% 8.0% 2.7% 5.6% 1 |

15 Proven Management Team Driving Continued Growth – Powerful Combination of Operational & Strategic Leadership Corporate, Stategic & Financial Leadership Operating Management Chris Klein CEO Lee Wyatt CFO 8 years with Fortune Brands including ~ 3 years with FBHS and 5+ years leading Strategy & Corporate Development at Fortune Brands; previously a Partner at McKinsey & Co. and EVP at Bank One Recruited as CFO of FBHS; previously CFO of Hanesbrands and led spin-off from Sara Lee, CFO at $7B Sonic Automotive and CFO of Sealy Greg Stoner President – MBCI 7 years with FBHS; previously 11 years with Newell Rubbermaid and 9 years with GE; drove rationalization efforts through the downturn in 2009; managed MBCI as it became the #1 cabinet manufacturer in North America in 2011 David Lingafelter President – Moen 21 years with FBHS; managed transition from engineering-driven to consumer-driven organization, leading marketing, brand investments and new product development processes David Randich President – Therma-Tru Mark Savan President – Simonton 4 years with FBHS; previously 24 years with Armstrong; repositioned business during downturn through channel diversification and restructuring of global supply chain 11 years with FBHS; previously 6 years with Booz Allen; led Simonton’s transition from a building products-focused to a consumer-focused organization John Heppner President – Master Lock & CEO – FOSS 18 years with FBHS; grew Master Lock market share while repositioning Waterloo Kitchen & Bath Cabinetry Plumbing & Accessories Advanced Material Windows & Door Systems Security & Storage |

16 Demonstrated growth that has exceeded the market over extended period of time and through multiple cycles. Sales performance reflects both organic growth and acquisitions includes housing recessions of ‘90-’91, ‘94-’96, ‘00-’01, ‘06-’11 Sales Growth Rate 1989 2011 Projected FBHS Organic Sales* U.S. Home Products Market New Construction and Replace & Remodel FBHS GAAP Sales * Excludes impact from acquisitions and divestitures 4% 9% ~2% |

17 An Outperforming Industry Leader Well-Positioned to Accelerate Growth and Create Value Attractive Home & Security Product Categories & Positions Consumer & Customer Focus Operational & Management Excellence Demonstrated Ability to Outperform the Market Benefits of Being Independent Strong Cash Flow & Flexible Capital Structure Front-end of Housing Market Recovery + |

18 Benefits of Being Independent Clearer focus and alignment on Home & Security priorities enables more nimble response to growth and capital investment opportunities Strong balance sheet and flexible capital structure aligned to the needs of a growth company Business unit performance and management incentive structure more tightly linked to overall company performance “Pure play” equity may be more attractive to investors who want to participate in the home market recovery |

19 Opportune Timing of the Spin-off Ahead of Expected Housing Market Recovery Long-Term Home Market Drivers Factors that Enable Recovery Positive population and immigration growth Increased levels of household formation driven by demographics Favorable housing affordability Aging housing stock (average of 40 years), particularly homes >12 years Increasing existing home sales New Construction Repair & Remodel Improvements in the broader economy and employment – at the local market level Credit availability Stability in home prices Improving consumer confidence |

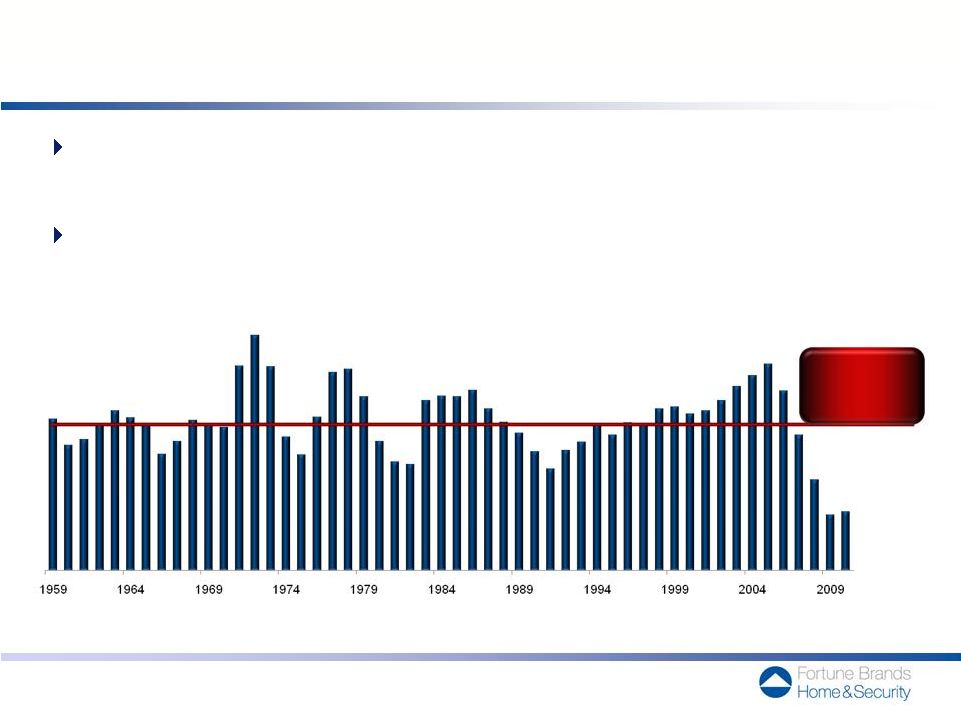

20 1959 – 2010 average: 1,497,000 starts Long-Term Market Trends Point Towards an Eventual Recovery in New Housing Starts New housing starts are at a historically low level, with just 587,000 starts in 2010 The long-term average, as well as demographic trends, suggest a recovery is likely Annual New Housing Starts Source: US Census Bureau. Data reflects single and multi-family housing starts. |

21 Winning New Business Expanding in Adjacent Categories and International Markets Using Cash Flow to Maximize Shareholder Value An Outperforming Industry Leader Well-Positioned to Accelerate Growth and Create Value Attractive Home & Security Product Categories & Positions Consumer & Customer Focus Operational & Management Excellence Demonstrated Ability to Outperform the Market Benefits of Being Independent Strong Cash Flow & Flexible Capital Structure Front-end of Housing Market Recovery Consistent, Focused Strategy & Execution Benefits & Timing of Spin-off Exceptional Growth & Value Creation Opportunities |

22 Consumers have a latent need to maximize functional storage space MBCI has launched hundreds of practical functional solutions fitting many different consumer needs Physical challenges Organomics / Ergonomics Occupying the valuable toe-kick space High density storage of "Super Cab" Differentiation is an aspiration for consumers By engaging advanced technology and High-Tech Materials, we are able to bring fashionable color to consumers at an affordable price Started with the key insight that Consumers want faucets that are easier to clean and don’t show water spots or fingerprints Moen developed an innovative new finish that virtually eliminates water spotting and finger printing Moen activated the market using a broad range of traditional media, on-line techniques and strong in-store point of purchase support from our partners The new finish increased sell through by 10% - 25% generating significant increases for Moen and our key partners Our Systematic, Consumer Driven Innovation Processes Result in New Products Consumers Love Purestyle Technologies Logix Storage & Organization |

23 International Markets In Addition to Winning New Business, Potential for Expansion in Adjacent Categories and International Markets (Examples) Commercial China India Europe Automotive Latin America Bath Accessories Sinks Commercial Safety Electronic Security Storage Security Bath Vanities China $25B $25B $7B China Market Opportunity Adjacent Categories 1 2 3 1 – N. America & China Residential & Commercial Fashion Plumbing Market includes fixtures (bathtub/shower, toilets, sinks, other) and fittings (lavatory, bathtub/shower, kitchen/other sink, other) ; source – Freedonia, company analysis 2 – North American Security Products (mechanical & electronic access control) and Services; source – Freedonia, company analysis 3 – US Residential Wood Kitchen and Bath Cabinet Market; source – Freedonia, company analysis |

24 We will use Cash Flow to Maximize Shareholder Value in Multiple Ways Continue to invest in current businesses – products, markets, brands, supply chains Pay down debt Pursue accretive acquisitions or return cash to shareholders – share buybacks or dividends |

25 Target Criteria Illustrative Past Acquisitions Fit within our market Primary focus Ability to leverage existing Good companies to be made New home & security Truly differentiated leader with a capable management team Clear path for organic growth Acquisition Opportunities Can Accelerate Growth in Both Home and Security Markets What We Acquired: Strong commercial brand Heavy-duty commercial products What We Did: Leveraged combined strengths to Maintained market facing teams Fully integrated supply chain What We Acquired: Position in higher-end of dealer channel Custom kitchen products and capabilities What We Did: Leveraged brand across broader dealer channel Maintained market facing teams Fully integrated supply chain & back office What We Acquired: Strong trade brand #1 position in U.S. fiberglass What We Did: Grew in R&R market Streamlined supply chain Increased productivity solidify #1 padlock share in N.A. & back office residential entry doors attractiveness criteria on core categories capabilities, market positions and structure great, not turnarounds categories under two conditions: |

26 Security Market Offers Attractive Opportunities for Growth Growing ~$25B North American Security market Historically stable demand in core padlock market segment Technology is an enabler to solve security issues that customers value Exploring opportunities in Electronic Access control and monitoring Unparalleled brand and channel strength, particularly with distributors and locksmiths Existing commercial channel market position Solution focused innovation to meet unmet security needs Master Lock has Strong Assets to Leverage The Security Market is Attractive |

27 FBHS Corporate Governance Structure is consistent with Fortune Brands but supplemented with additional defenses to protect new company Board of Directors • Initially 7 members (6 independent from Fortune Brands plus Chris Klein) • David Thomas – non-executive chairman Auditors • External auditors – PriceWaterhouseCoopers • Internal audit function and people transferring from Fortune Brands Structural Defenses • Shareholder rights plan – one year plan with a 15% trigger • Other appropriate protections such as classified board, no cumulative voting, no shareholder right to call for special meetings or remove directors other than for cause and advance notice of director nominations |

28 Confidence in the Fortune Brands Home & Security Opportunity Strong belief in our strong brands and attractive categories Well positioned, having restructured early and made substantial strategic investments in long-term growth Strong historical performance versus market and demonstrated operating leverage in 2010, off the 2009 low Long-term demographics in place to drive eventual housing market recovery |

29 While the housing market slump has significantly reduced sales and profit, we believe the business is positioned to return to previous levels when the housing market recovers $ millions * Adjusted Pro Forma: before Charges / Gains, including incremental standalone corporate expenses. Net Sales $4,694 $4,551 $3,759 $3,007 $3,234 % Growth 13% (3%) (17%) (20%) 8% Operating Income* $668 $553 $301 $81 $180 % Operating Margin* 14% 12% 8% 3% 6% EBITDA* $816 $703 $435 $195 $288 % EBITDA Margin* 17% 15% 12% 6% 9% Unlevered Free Cash Flow* $464 $393 $325 $280 $146 Fiscal Year ending December 31 2006 2007 2008 2009 2010 adjusted Pro Forma |

30 2011 First-half results reflect overall market decline, negative impact of 2010 home buyers credit and commodity inflation, but FBHS continued to invest in the business and out-perform the market. Second-half expectations assume a flat market and negative impact of 2010 energy credit, but FBHS expects to continue to benefit from price increases, invest in the business and out-perform the market *Assumes second half improvement in consumer confidence and overall employment. Market Market declined - Assuming Market flat* - FBHS Sales FBHS grew 2% We believe FBHS could grow mid-single digits Prior Year New home buyer credit Energy credit benefited 2010 benefited 2010 Commodity Inflation Higher costs; Higher costs; price increases initiated price increases in place Investment in Business FBHS continued to invest FBHS continues to invest Competitive Promotions Heavy in cabinets On-going Operating Costs Continued cost reductions Continuing cost reductions 1 Half 2011 Observations 2 Half 2011 Expectations st nd |

31 Flexible capital structure following spin-off with strong balance sheet and cash flow to fuel growth opportunities. Bank financing in place with strong bank leadership group. 1. Peer leverage metrics per Moody’s. 2. Peers include Armstrong, Lennox, Masco, Mohawk, Owens Corning, Stanley Black & Decker and Whirlpool. 3. Adjusted Pro Forma: before Charges/ Gains, including incremental standalone corporate expenses. 4. As disclosed in Form 10 $ millions ~3.9x 1.8x Peer Average 2 Debt-to-Capita Barclays Citibank Credit Suisse Wells Fargo JPMorgan Bank of America Spin-off Capital Structure: Term Loans $350 Revolver ($650 facility) 150 Subsidiary Debt 20 Total Long-Term Debt $520 Total Debt 520 Liabilities 1,083 Equity 2,107 2010 EBITDA 3 288 2010 Unlevered Free Cash Flow³ 146 Assets $3,710 Balance Sheet Statistics: (12/31/10 pro forma 4 ) Peer Debt/EBITDA Benchmarking 1 Strong Bank Leadership Group 3 3 20% ~ |

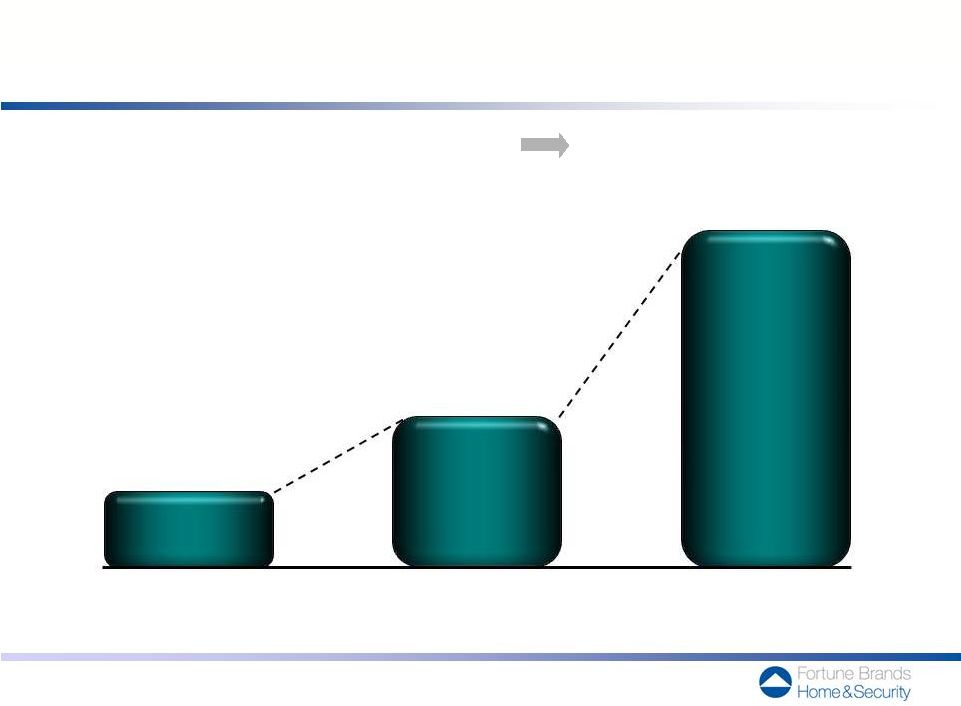

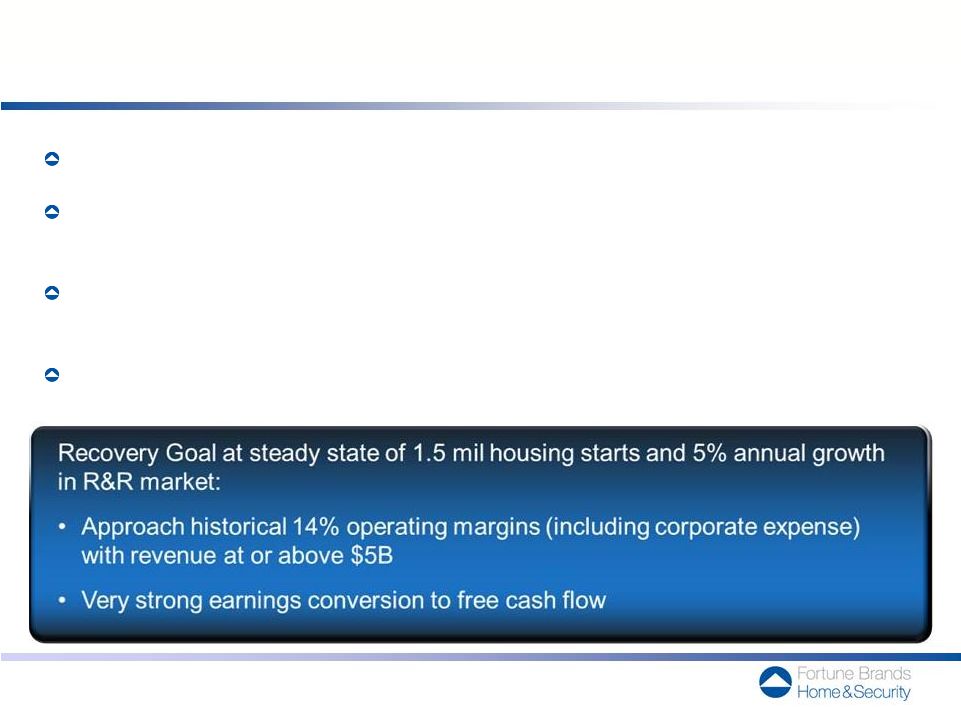

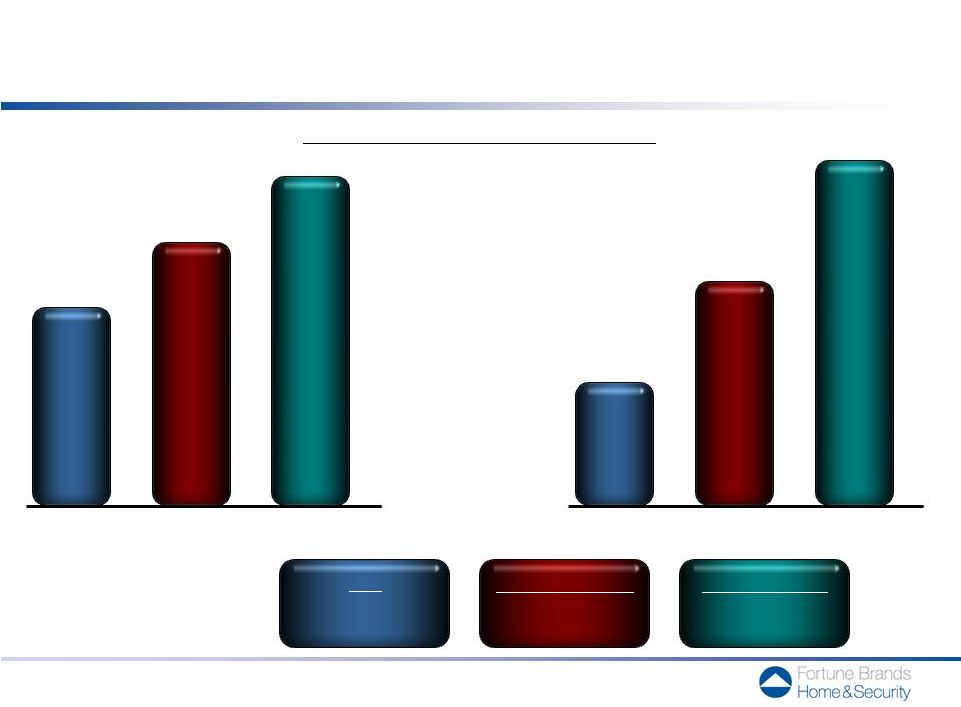

32 Our success is not dependent on rapid market recovery for solid returns and cash flow, although returning to “steady state” is very attractive Market Recovery Scenarios Operating Income $200 $450 $750 Sales annual $ in B $3 $4 $5 EBITDA annual $ in M $300 $550 $850 flat ~600,000 ~0% mid-recovery ~1,000,000 ~2 – 3% steady state ~1,500,000 ~4 – 6% Housing Starts R&R Growth 1 1. Adjusted Pro Forma: before Charges/ Gains, including incremental standalone corporate expenses. |

33 Ability to Leverage Our Business Model as the Market Recovers Efficient supply chains allow us to profitably serve a wide range of price points Operations that support up to $5B in sales without capital spending above normal levels Industry leading brands can be leveraged for both organic and acquisition growth Leadership market positions to introduce new products Proven management team can drive additional growth Acquisition and integration experience Invest in business growth Fund acquisitions or return cash to shareholders Brands / Market Position Supply Chains Management Capital Structure and Cash Flow |

Thank You Any Questions? |

Appendix |

36 $1,189 Kitchen & Bath Cabinetry – Fully Integrated Business, Scalable and Poised to Leverage Across Multiple Brands, Channels and Price Points Key Brands Market Position Summary Why We Win $ millions Notes: Market size includes residential wood cabinets sold in US in 2010 Source: Freedonia Differentiated brands across multiple channels and price points Broad participation across channels Leading design and finish innovation Leverage global supply chain with local assembly model 2010 Sales Market Size |

37 Plumbing & Accessories – The Engine that Provides Consistent Growth and Profitability Notes: Market size reflects global faucets and accessories as of Dec. 2010 Source: Freedonia $ millions Key Brands Market Position Summary Why We Win Strong consumer and trade brand Leading market position Sustainable and flexible supply chain Large installed base helps replace / repair Consistent ability to innovate $924 2010 Sales Market Size |

Advanced Material Windows & Door Systems – Ready to Leverage the Market Recovery Notes: Market size - US residential windows and doors in all materials as of Dec. 2010 Source: Freedonia, Ducker, FBHS analysis $ millions Key Brands Market Position Summary Why We Win Strong market positions Trusted trade brands Restructured to profitably lever with market recovery 2010 Sales Market Size $601 38 |

39 Security & Storage – Strong Brand with Growth Potential Well Beyond Padlocks; More Stable Market not Tied to Housing Cycle $ millions Key Brands Market Position Summary Why We Win Large market size and room for growth Strong brand Ability to extend across broader security categories Strong channel position across retail and commercial segments Solution focused innovation $520 2010 Sales Market Size Notes: Market size reflects North American security market as of Dec. 2010 Source: Freedonia |

40 Supply Chain Characteristics Differentiated and Focused Supply Chains to Best Serve Our Customers Customizable designs and cabinet configurations Flexible manufacturing facilities Distributive assembly model Competitive Advantage Global supply base / standard platforms Variable cost model Reacts quickly to change in demand & product mix Vertically integrated / standard platforms Scale manufacturing drives high efficiency for doors Consistent rapid delivery model for windows Global supply base Variable cost model Rapid response customer packaging and keying capabilities Reacts quickly to change in demand & product mix Serve multiple channels and brands Can achieve value price points profitably when winning new business Significant leverage as market grows Offer stylish solutions at affordable prices Ramp-up innovation quickly Significant leverage as market grows Can meet unique customer requirement for retail and commercial Rapid cycle to get new product to market Kitchen & Bath Cabinetry Plumbing & Accessories Advanced Material Windows & Door Systems Security & Storage |

Appendix

Reconciliation of Non-GAAP Measures to GAAP

FBHS Net Sales Growth Rate to FBHS Organic Sales Growth | Page 42 | |||

Adjusted Pro Forma Operating Income to GAAP Operating Income | Page 43 | |||

Adjusted Pro Forma Operating Margin to GAAP Operating Margin | Page 44 | |||

Adjusted Pro Forma EBITDA to GAAP Net Income | Page 45 | |||

Adjusted Pro Forma EBITDA margin to GAAP Net Income margin | Page 46 | |||

Adjusted Pro Forma Unlevered Free Cash Flow to GAAP Cash flow from Operations | Page 47 | |||

Reconciliation of FBHS Net Sales Growth Rate to FBHS Organic Sales Growth

| Home & Security 1989-2011 Projected CAGR* | ||||

Net sales growth (GAAP) | 9 | % | ||

Net impact from acquisitions/divestitures | (5 | )% | ||

|

| |||

Organic sales growth | 4 | % | ||

|

| |||

| * | Compounded annual growth rate |

Organic sales growth is the rate of compounded annual net sales growth from 1989 through 2011 projected, excluding the impact of acquisitions and divestitures. Organic sales growth is not a measure derived in accordance with GAAP. Management believes this measure provides useful supplemental information regarding the underlying level of sales growth. This measure may be inconsistent with similar measures presented by other companies.

Page 42

Reconciliation of Adjusted Pro Forma Operating Income to GAAP Operating Income

(in millions)

| 2006 | 2007 | 2008 | 2009 | 2010 | ||||||||||||||||

Adjusted pro forma operating income | $ | 668 | $ | 553 | $ | 301 | $ | 81 | $ | 180 | ||||||||||

Standalone corporate expenses(1) | 20 | 20 | 20 | 20 | 20 | |||||||||||||||

Restructuring and other charges(2) | (26 | ) | (93 | ) | (56 | ) | (52 | ) | (12 | ) | ||||||||||

Asset impairment charges | — | — | (848 | ) | — | — | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

GAAP operating income | $ | 662 | $ | 480 | $ | (583 | ) | $ | 49 | $ | 188 | |||||||||

Adjusted pro forma operating income is operating income derived in accordance with GAAP including estimated incremental standalone corporate expenses and excluding restructuring and other charges, and asset impairment charges.

Adjusted pro forma operating income is a measure not derived in accordance with GAAP. Management uses this measure to determine the returns generated by FBHS and to evaluate and identify cost-reduction initiatives. Management believes this measure provides investors with helpful supplemental information regarding the underlying performance of the company from year to year. This measure may be inconsistent with similar measures presented by other companies.

| (1) | After the separation, the Company estimates it will incur higher expenses of approximately $20 million annually associated with the incremental costs of functioning as an independent standalone public company. |

| (2) | Restructuring charges are costs incurred to implement significant cost reduction initiatives and include workforce reduction costs and asset write-downs; “other charges” represent charges directly related to restructuring initiatives that cannot be reported as restructuring under U.S. GAAP. Such costs may include losses on disposal of inventories, trade receivables allowances from exiting product lines and accelerated depreciation resulting from the closure of facilities. |

Page 43

Reconciliation of Adjusted Pro Forma Operating Margin to GAAP Operating Margin

| 2006 | 2007 | 2008 | 2009 | 2010 | ||||||||||||||||

Adjusted pro forma operating margin | 14.2 | % | 12.1 | % | 8.0 | % | 2.7 | % | 5.6 | % | ||||||||||

Standalone corporate expenses(1) | 0.4 | % | 0.4 | % | 0.5 | % | 0.6 | % | 0.6 | % | ||||||||||

Restructuring and other charges(2) | (0.5 | )% | (2.0 | )% | (1.5 | )% | (1.7 | )% | (0.4 | )% | ||||||||||

Asset impairment charges | — | — | (22.5 | )% | — | — | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

GAAP Operating Margin | 14.1 | % | 10.5 | % | (15.5 | )% | 1.6 | % | 5.8 | % | ||||||||||

Adjusted pro forma operating margin is operating margin derived in accordance with GAAP including estimated incremental standalone corporate expenses and excluding restructuring and other charges, and asset impairment charges divided by GAAP net sales.

Adjusted pro forma operating margin is a measure not derived in accordance with GAAP. Management uses this measure to determine the returns generated by FBHS and to evaluate and identify cost-reduction initiatives. Management believes this measure provides investors with helpful supplemental information regarding the underlying performance of the company from year to year. This measure may be inconsistent with similar measures presented by other companies.

| (1) | After the separation, the Company estimates it will incur higher expenses of approximately $20 million annually associated with the incremental costs of functioning as an independent standalone public company. |

| (2) | Restructuring charges are costs incurred to implement significant cost reduction initiatives and include workforce reduction costs and asset write-downs; “other charges” represent charges directly related to restructuring initiatives that cannot be reported as restructuring under U.S. GAAP. Such costs may include losses on disposal of inventories, trade receivables allowances from exiting product lines and accelerated depreciation resulting from the closure of facilities. |

Page 44

Reconciliation of Adjusted Pro Forma EBITDA to GAAP Net Income

(in millions)

| 2006 | 2007 | 2008 | 2009 | 2010 | ||||||||||||||||

Adjusted pro forma EBITDA | $ | 816 | $ | 703 | $ | 435 | $ | 195 | $ | 288 | ||||||||||

Depreciation(1) | (105 | ) | (116 | ) | (108 | ) | (97 | ) | (92 | ) | ||||||||||

Amortization of intangible assets | (30 | ) | (35 | ) | (33 | ) | (16 | ) | (16 | ) | ||||||||||

Restructuring and other charges(2) | (26 | ) | (93 | ) | (56 | ) | (52 | ) | (12 | ) | ||||||||||

Asset impairment charges | — | — | (848 | ) | — | — | ||||||||||||||

Related party interest expense, net | (169 | ) | (188 | ) | (127 | ) | (85 | ) | (116 | ) | ||||||||||

External interest expense | (1 | ) | (0 | ) | (1 | ) | (0 | ) | (0 | ) | ||||||||||

Standalone corporate expenses(3) | 20 | 20 | 20 | 20 | 20 | |||||||||||||||

Income tax (provision) benefit | (176 | ) | (137 | ) | 77 | (6 | ) | (14 | ) | |||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net income (loss) | $ | 329 | $ | 154 | $ | (641 | ) | $ | (41 | ) | $ | 58 | ||||||||

Noncontrolling interests | (1 | ) | (1 | ) | (1 | ) | (1 | ) | (1 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net income (loss) attributable to Home & Security | $ | 328 | $ | 153 | $ | (642 | ) | $ | (42 | ) | $ | 57 | ||||||||

Adjusted pro forma EBITDA is net income (loss) derived in accordance with GAAP including estimated incremental standalone corporate expenses and excluding restructuring and other charges, asset impairment charges, depreciation, amortization of intangible assets, related party interest expense, net, external interest expense, and income taxes.

Adjusted pro forma EBITDA is a measure not derived in accordance with GAAP. Management uses this measure to assess returns generated by FBHS. Management believes this measure provides investors with helpful supplemental information regarding the underlying performance of the company from year to year. This measure may be inconsistent with similar measures presented by other companies.

| (1) | Depreciation excludes accelerated depreciation included in restructuring and other charges. |

| (2) | Restructuring charges are costs incurred to implement significant cost reduction initiatives and include workforce reduction costs and asset write-downs; “other charges” represent charges directly related to restructuring initiatives that cannot be reported as restructuring under U.S. GAAP. Such costs may include losses on disposal of inventories, trade receivables allowances from exiting product lines and accelerated depreciation resulting from the closure of facilities. |

| (3) | After the separation, the Company estimates it will incur higher expenses of approximately $20 million annually associated with the incremental costs of functioning as an independent standalone public company. |

Page 45

Reconciliation of Adjusted Pro Forma EBITDA margin to GAAP Net Income margin

| 2006 | 2007 | 2008 | 2009 | 2010 | ||||||||||||||||

Adjusted pro forma EBITDA margin | 17 | % | 15 | % | 12 | % | 6 | % | 9 | % | ||||||||||

Depreciation(1) | (2 | )% | (3 | )% | (3 | )% | (3 | )% | (3 | )% | ||||||||||

Amortization of intangible assets | (1 | )% | (1 | )% | (1 | )% | (0 | )% | (0 | )% | ||||||||||

Restructuring and other charges (2) | (0 | )% | (2 | )% | (1 | )% | (2 | )% | (0 | )% | ||||||||||

Asset impairment charges | — | — | (23 | )% | 0 | % | 0 | % | ||||||||||||

Related party interest expense, net | (3 | )% | (4 | )% | (3 | )% | (3 | )% | (4 | )% | ||||||||||

External interest expense | (0 | )% | (0 | )% | (0 | )% | (0 | )% | (0 | )% | ||||||||||

Standalone corporate expenses(3) | 0 | % | 1 | % | 0 | % | 1 | % | 0 | % | ||||||||||

Income tax (provision) benefit | (4 | )% | (3 | )% | 2 | % | (0 | )% | (0 | )% | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

GAAP Net income (loss) margin | 7 | % | 3 | % | (17 | )% | (1 | )% | 2 | % | ||||||||||

Adjusted pro forma EBITDA margin is net income (loss) derived in accordance with GAAP including estimated incremental standalone corporate expenses and excluding restructuring and other charges, asset impairment charges, depreciation, amortization of intangible assets, related party interest expense, net, external interest expense, and income taxes divided by GAAP net sales.

Adjusted pro forma EBITDA is a measure not derived in accordance with GAAP. Management uses this measure to assess returns generated by FBHS. Management believes this measure provides investors with helpful supplemental information regarding the underlying performance of the company from year to year. This measure may be inconsistent with similar measures presented by other companies.

| (1) | Depreciation excludes accelerated depreciation included in restructuring and other charges. |

| (2) | Restructuring charges are costs incurred to implement significant cost reduction initiatives and include workforce reduction costs and asset write-downs; “other charges” represent charges directly related to restructuring initiatives that cannot be reported as restructuring under U.S. GAAP. Such costs may include losses on disposal of inventories, trade receivables allowances from exiting product lines and accelerated depreciation resulting from the closure of facilities. |

| (3) | After the separation, the Company estimates it will incur higher expenses of approximately $20 million annually associated with the incremental costs of functioning as an independent standalone public company. |

Page 46

Reconciliation of Adjusted Pro Forma Unlevered Free Cash Flow to GAAP Cash flow from Operations

(in millions)

| 2006 | 2007 | 2008 | 2009 | 2010 | ||||||||||||||||

Adjusted pro forma unlevered free cash flow | $ | 464 | $ | 393 | $ | 325 | $ | 280 | $ | 146 | ||||||||||

Add: | ||||||||||||||||||||

Capital Expenditures | 128 | 75 | 57 | 43 | 58 | |||||||||||||||

Standalone corporate expenses, net of tax | 13 | 13 | 13 | 13 | 13 | |||||||||||||||

Less: | ||||||||||||||||||||

Proceeds from the disposition of assets | 11 | 20 | 14 | 11 | 3 | |||||||||||||||

Related party interest expense, net of tax | 110 | 122 | 84 | 56 | 75 | |||||||||||||||

External interest expense, net of tax | 0 | 0 | 0 | 0 | 0 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Cash flow from operations | $ | 484 | $ | 339 | $ | 297 | $ | 269 | $ | 139 | ||||||||||

Adjusted pro forma unlevered free cash flow is Cash Flow from Operations (i) less net capital expenditures (capital expenditures less proceeds from the sale of assets including property, plant and equipment) and estimated incremental standalone corporate expenses, net of tax, (ii) plus related party interest expense, net of tax, and external interest expense, net of tax. In computing unlevered free cash flow, net of tax reconciling items assume an income tax rate of 35%. Unlevered free cash flow is a measure not derived in accordance with GAAP. Management believes that Free Cash Flow provides investors with helpful supplemental information about the company's ability to fund internal growth, make acquisitions, repay debt and related interest, pay dividends, and repurchase common stock. This measure may be inconsistent with similar measures presented by other companies.

Page 47