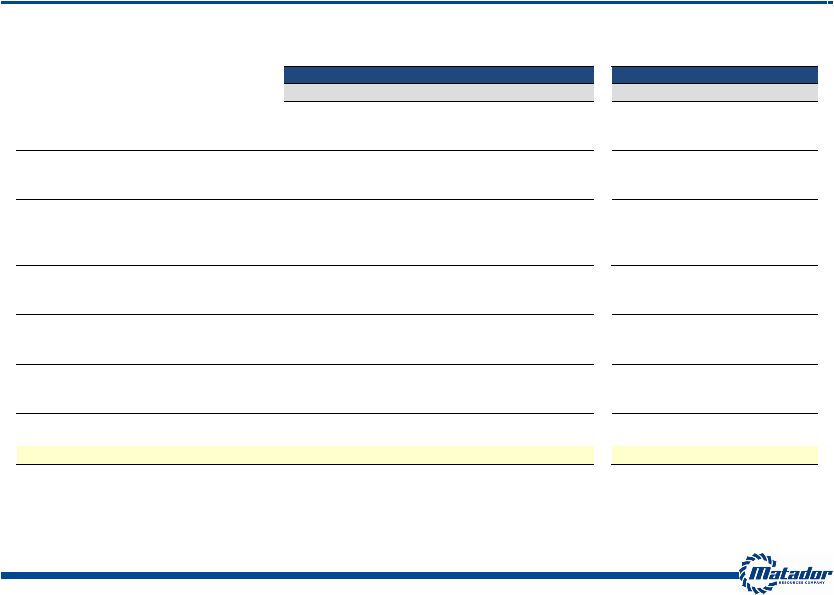

19 Adjusted EBITDA Reconciliation The following table presents our calculation of Adjusted EBITDA and reconciliation of Adjusted EBITDA to the GAAP financial measures of net income (loss) and net cash provided by operating activities, respectively. We believe Adjusted EBITDA helps us evaluate our operating performance and compare our results of operation from period to period without regard to our financing methods or capital structure. We define Adjusted EBITDA as earnings before interest expense, income taxes, depletion, depreciation and amortization, accretion of asset retirement obligations, property impairments, unrealized derivative gains and losses, non-recurring income and expenses and non-cash stock-based compensation expense, including stock option and grant expense and restricted stock expense. Adjusted EBITDA is not a measure of net income (loss) or cash flows as determined by GAAP. Adjusted EBITDA should not be considered an alternative to, or more meaningful than, net income or cash flows from operating activities as determined in accordance with GAAP or as an indicator of our operating performance or liquidity. Year Ended December 31, (In thousands) 2008 2009 2010 2011 2010 2011 2012 Unaudited Adjusted EBITDA reconciliation to Net Income (Loss): Net income (loss) $103,878 ($14,425) $6,377 ($10,309) $5,676 ($27,596) $3,801 Interest expense - - 3 683 - 106 308 Total income tax provision (benefit) 20,023 (9,925) 3,521 (5,521) 2,975 (6,906) 3,064 Depletion, depreciation and amortization 12,127 10,743 15,596 31,754 3,362 7,111 11,205 Accretion of asset retirement obligations 92 137 155 209 38 39 53 Full-cost ceiling impairment 22,195 25,244 - 35,673 - 35,673 - Unrealized (gain) loss on derivatives (3,592) 2,375 (3,139) (5,138) (6,093) 1,668 3,270 Stock option and grant expense 605 622 824 2,362 180 42 (374) Restricted stock grants 60 34 74 44 6 11 11 Net (gain) loss on asset sales and inventory impairment (136,977) 379 224 154 - - - Adjusted EBITDA $18,411 $15,184 $23,635 $49,911 $6,142 $10,148 $21,338 Year Ended December 31, (In thousands) 2008 2009 2010 2011 2010 2011 2012 Unaudited Adjusted EBITDA reconciliation to Net Cash Provided by Operating Activities: Net cash provided by operating activities $25,851 $1,791 $27,273 $61,868 $9,101 $12,732 $5,110 Net change in operating assets and liabilities (17,888) 15,717 (2,230) (12,594) (2,959) (2,690) 15,920 Interest expense - - 3 683 - 106 308 Current income tax provision (benefit) 10,448 (2,324) (1,411) (46) - - - Adjusted EBITDA $18,411 $15,184 $23,635 $49,911 $6,142 $10,148 $21,338 Three Months Ended March 31, Three Months Ended March 31, |