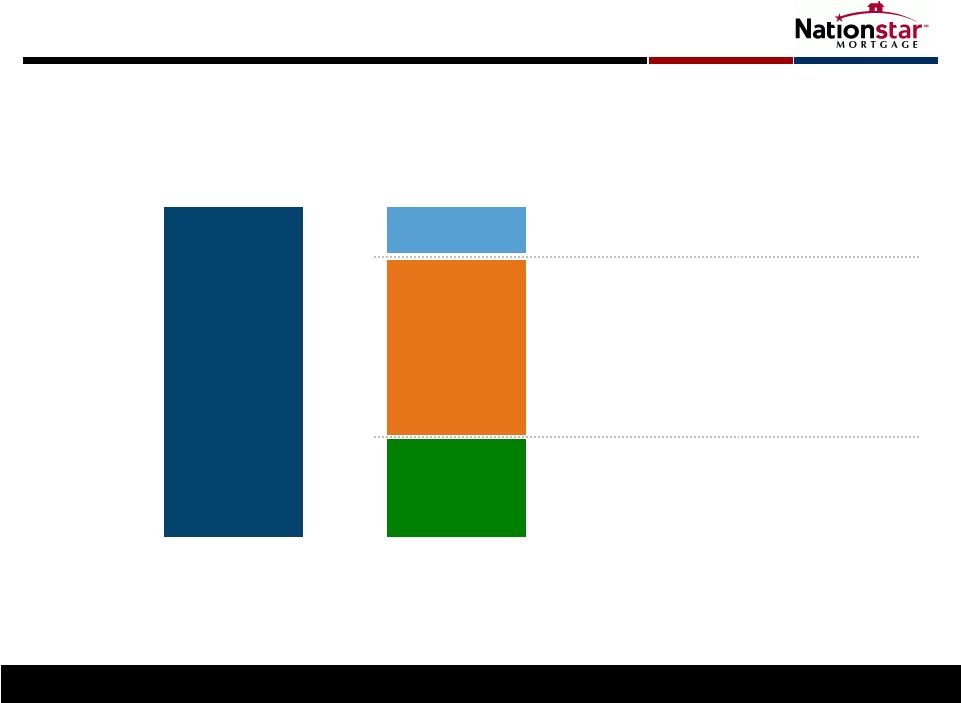

(bps, except %) (2) Prior Structure Initial New Structure Target Advances as a % of UPB 5.5% 4.0% Servicing fee 22) 2 Performance fee ---) 5 Ancillary, Solutionstar, excess spread 19) 19 Advance interest expense (3) (15) --- Net servicing fee revenue before MTM/amortization (4) 26) 26 Rights to MSR Net Servicing Fee Impact 1 1) Each MSR pool may have different pricing, but average to these fee amounts in the aggregate. 2) For illustrative purposes; may not meet actual results. 3) Assumes Nationstar’s interest rate of 3.0%; NRZ’s interest rate of 2.4%. 4) Revenue net of servicing advance facility interest expense. 5) For comparison purposes, Aurora non-Agency advances, on a relative basis, have had a similar reduction over the last twelve months. 6) $362MM expected to close in initial transactions by mid-January; NRZ has the right but not the obligation to close on remaining advances at substantially the same terms. NSM retains all ancillary fees, Solutionstar fee income, originations income and share of existing excess MSR No advance interest expense to NSM Servicing compensation structure for the RMSR (22 bps total) (1) (5) + Up to an additional $681MM in equity to redeploy (6) + up to nearly 8 bps of retained fee – Servicing fee of 2 basis points (bps) to NSM – paid regardless of New Residential and investor (“NRZ”) return – Performance fee of up to 5 bps to NSM; subject to achieving servicer performance objectives – Retained fee of 15 bps to NRZ to meet target return; fees in excess of target return split 50/ 50 Exhibit 99.2 |

Rights to MSR Servicing Fee Details Current Structure New RMSR Structure Basic Fee 22 bps Servicing Fee 2 bps Performance Fee 5 bps Retained Fee 15 bps Paid to NSM If NRZ target return is met, 100% of fee to NSM If NRZ target return is not met, portion of fee required for target return to NRZ, with remaining to NSM Paid to NSM 2 + all ancillary fees, Solutionstar fee income, originations income and share of existing excess MSR to NSM + no future advance funding requirements for NSM Retained by NRZ to meet target return on investment If target return is met, excess above target return split 50/50 to NSM / NRZ up to nearly 8 bps paid to NSM ; |