As filed with the U.S. Securities and Exchange Commission on March 11, 2021

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

811-22562

Investment Company Act file number

Barings Global Short Duration High Yield Fund

(Exact name of registrant as specified in charter)

300 South Tryon Street, Suite 2500, Charlotte, NC 28202

(Address of principal executive offices) (Zip code)

Corporation Service Company (CSC)

251 Little Falls Drive

Wilmington DE 19808

United States

(Name and address of agent for service)

704-805-7200

Registrant’s telephone number, including area code

Date of fiscal year end: December 31, 2020

Date of reporting period: December 31, 2020

Item 1. Reports to Stockholders.

(a)

(b) Not Applicable for this Registrant

Item 1. Reports to Stockholders.

Barings Global Short Duration High Yield Fund

c/o Barings LLC

300 S Tryon St.

Suite 2500

Charlotte, NC 28202

704.805.7200

http://www.Barings.com/bgh

ADVISER

Barings LLC

300 S Tryon St.

Suite 2500

Charlotte, NC 28202

SUB-ADVISOR

Baring International Investment Limited

20 Old Bailey

London EC4M 78F UK

COUNSEL TO THE FUND

Ropes & Gray LLP

Prudential Tower

800 Boylston Street

Boston, Massachusetts 02110

INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

Deloitte & Touche LLP

30 Rockefeller Plaza

New York, NY 10112

CUSTODIAN

US Bank

MK-WI-S302

1555 N. River Center Drive

Milwaukee, WI 53212

TRANSFER AGENT & REGISTRAR

U.S. Bancorp Fund Services, LLC, d/b/a

U.S. Bank Global Fund Services

615 E. Michigan St.

Milwaukee, WI 53202

FUND ADMINISTRATION/ACCOUNTING

U.S. Bancorp Fund Services, LLC, d/b/a

U.S. Bank Global Fund Services

615 E. Michigan St.

Milwaukee, WI 53202

PROXY VOTING POLICIES & PROCEDURES

The Trustees of Barings Global Short Duration High Yield Fund (the “Fund”) have delegated proxy voting responsibilities relating to the voting of securities held by the Fund to Barings LLC (“Barings”). A description of Barings’ proxy voting policies and procedures is available (1) without charge, upon request, by calling, toll-free 1-866-399-1516; (2) on the Fund’s website at http://www.barings.com/bgh; and (3) on the U.S. Securities and Exchange Commission’s (“SEC”) website at http://www.sec.gov.

FORM N-Q

The Fund will file its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q or Part F of Form N-PORT (beginning with filings after March 31, 2019). This information is available (1) on the SEC’s website at http://www.sec.gov; and (2) at the SEC’s Public Reference Room in Washington, DC (which information on their operation may be obtained by calling 1-800-SEC-0330). A complete schedule of portfolio holdings as of each quarter-end is available on the Fund’s website at http://www.barings.com/bgh or upon request by calling, toll-free, 1-866-399-1516.

CERTIFICATIONS

The Fund’s President has submitted to the NYSE the annual CEO Certification as required by Section 303A.12(a) of the NYSE Listed Company Manual.

LEGAL MATTERS

The Fund has entered into contractual arrangements with an investment adviser, transfer agent and custodian (collectively “service providers”) who each provide services to the Fund. Shareholders are not parties to, or intended beneficiaries of, these contractual arrangements, and these contractual arrangements are not intended to create any shareholder right to enforce them against the service providers or to seek any remedy under them against the service providers, either directly or on behalf of the Fund.

Under the Fund’s Bylaws, any claims asserted against or on behalf of the Fund, including claims against Trustees and officers must be brought in courts located within the Commonwealth of Massachusetts.

The Fund’s registration statement and this shareholder report are not contracts between the Fund and its shareholders and do not give rise to any contractual rights or obligations or any shareholder rights other than any rights conferred explicitly by federal or state securities laws that may not be waived.

Barings Global Short Duration High Yield Fund 2020 Annual Report

OFFICERS OF THE FUND

Sean Feeley

President

Carlene Pollock

Chief Financial Officer

Elizabeth Murray

Treasurer

Michael Freno

Vice President

Scott Roth

Vice President

Michael Cowart

Chief Compliance Officer

Jill Dinerman

Secretary/Chief Legal Officer

Alexandra Pacini

Assistant Secretary

Barings Global Short Duration High Yield Fund is a closed-end investment company, first offered to the public in 2012, whose shares are traded on the New York Stock Exchange.

INVESTMENT OBJECTIVE & POLICY

Barings Global Short Duration High Yield Fund (the “Fund”) was organized as a business trust under the laws of the Commonwealth of Massachusetts. The Fund is registered under the Investment Company Act of 1940, as amended, as a de facto diversified, closed-end management investment company with its own investment objective. The Fund’s common shares are listed on the New York Stock Exchange under the symbol “BGH”.

The Fund’s primary investment objective is to seek as high a level of current income as the Adviser (as defined herein) determines is consistent with capital preservation. The Fund seeks capital appreciation as a secondary investment objective when consistent with its primary investment objective. There can be no assurance that the Fund will achieve its investment objectives.

The Fund seeks to take advantage of inefficiencies between geographies, primarily the North American and Western European high yield bond and loan markets and within capital structures between bonds and loans. For example, the Fund seeks to take advantage of differences in pricing between bonds and loans of an issuer denominated in U.S. dollars and substantially similar bonds and loans of the same issuer denominated in Euros, potentially allowing the Fund to achieve a higher relative return for the same credit risk exposure.

1

Barings Global Short Duration High Yield Fund 2020 Annual Report

Dear Fellow Shareholders,

We present the 2020 Annual Report for the Barings Global Short Duration High Yield Fund (the “Fund”) to recap portfolio performance and positioning. We believe our Global High Yield Investments Group is one of the largest teams in the market primarily focused on North American and Western European credit. Utilizing the Group’s unparalleled expertise, deep resources and time-tested process, we believe we can provide investors with an attractive level of current income while navigating the challenging times that may still lie ahead and continuing to uncover compelling opportunities across the global high yield market.

The Fund’s strategy focuses primarily on North American and Western European high yield companies, with the flexibility to dynamically shift the geographic weighting in order to capture, in our opinion, the best risk-adjusted investment opportunities. In the coming months and quarters, as the economic road to recovery may vary across different countries and regions, Barings’ global capabilities on the ground in major markets allow for us to be nimble in these times and take advantage of unique opportunities as they arise. In addition, the strategy focuses closely on limiting the duration of the Fund, while maintaining what we consider to be a reasonable amount of leverage.

Market Review

During the full year 2020, the market saw historic volatility, from a dramatic sell-off in the first quarter to a rebound in the second quarter and then into a risk rally that led global markets to end the year in positive territory. In the final six months of the year, markets were provided stability through global stimulus measures and continued Fed support in the U.S. in the form of corporate bond and exchange-traded fund (ETF) purchases. This, along with a move by investors into the below-investment grade market in the search for yield, led to historic new issuance levels in the global high yield bond market. Generally speaking, high yield issuers had ample access to capital, taking the opportunity to extend their liquidity into 2021 which helped to provide a more secure fundamental picture going into the New Year. This was all further supported by the Covid-19 vaccine roll-out and sustained consumer spending strength during the year.

The U.S. high yield bond market ended 2020 with a positive return despite the historic volatility across global markets in the first quarter. Performance was positive across all industry sectors following a strong rebound in the latter three quarters of the year with the exception of the energy sector. Many energy credits remained in negative territory following swings in the price of crude oil, which entered negative territory before rebounding back to near $40 per barrel. Double-Bs largely outperformed during the year followed by single-Bs and triple-Cs. The yield-to-worst finished the year 118 bps tighter from year-end 2019 at 4.30% while the option adjusted spread ended 24 bps wider at 391 bps. Gross high yield new issuance hit record highs with over $441 billion pricing across 664 bonds. Issuance net of refinancing activity was also elevated at $149 billion. The strong new issuance trends were absorbed by U.S. high yield bond fund net inflows of $44.3 billion over the year, despite notable outflows in the first quarter. Defaults increased to 6.17% as measured by the 12-month par weighted default rate and were largely driven by the energy sector. Similarly, the European high yield bond market posted positive performance over the year 2020 despite the market volatility. The European high yield bond market recorded its second worst month on record in terms of performance in March 2020, with the option adjusted spread widening significantly to 907 bps. However, as central banks and governments provided unprecedented stimulus following the initial onset of Covid-19, European high yield bonds experienced a strong resurgence for the rest of the year. While higher-rated bonds were the first to recover after the drawdown in March, the triple-C rated segment outperformed the rest of the market over the course of the year followed by double-Bs, while single-Bs were relatively flat. The option adjusted spread and yield-to-worst finished the year 45 bps and 0.18% wider, respectively, than the levels at which they started the year, to end at 368 bps and 3.05%. With the exception of the services sector, annual performance across industries was positive with two notable outperformers, energy and media. Despite the new issuance market being effectively closed during March and April, for the full year of 2020, issuance remained strong and totaled €85 billion, up 15% compared to last year.

Barings Global Short Duration High Yield Fund Overview and Performance

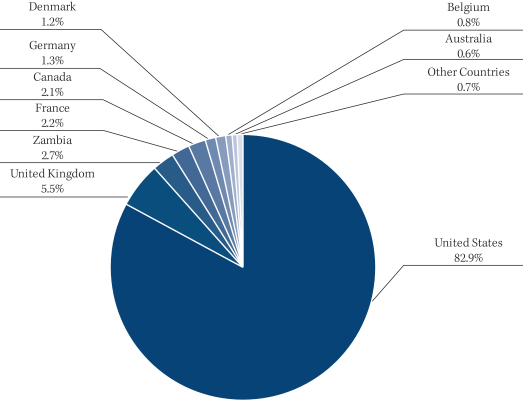

The Fund ended December 2020 with a portfolio of 148 issuers, up from 127 issuers at the beginning of the year. A majority of the issuers are domiciled in the United States at 82.9%, followed by the United Kingdom at 5.5%. (See Country Composition chart below). From a geographic standpoint, exposure to North American issuers was mostly in-line with year-end 2019, while issuers in Europe were down modestly. The Fund’s exposure to Rest of World issuers whose country of risk is outside of the U.S. and Europe but fit within the Fund’s developed market focus was modestly higher than from the

2

Barings Global Short Duration High Yield Fund 2020 Annual Report

previous year-end. The Fund’s primary exposure continues to be in the U.S. market, where the opportunity set was substantial given fallen angel activity and heavy new issue supply in the form of higher quality double-Bs and senior secured issues.

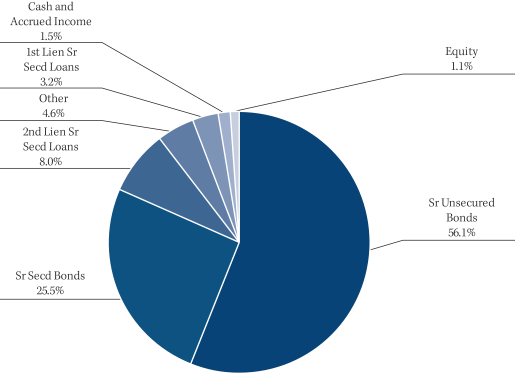

As of December 31, 2020, the Fund’s positioning across the credit quality spectrum was as follows: 20.2% BB rated and above, 41.0% single-B rated, and 35.0% triple-C rated and below, with approximately 32% of the portfolio consisting of secured obligations. The Fund decreased single-B rated credits, while triple-C and below rated credits increased during the period to take advantage of yield opportunities within the category but also through ratings downgrades. Non-publicly rated securities, and cash and accrued interest represented 3.7% and 3.2%, respectively.1

The Fund paid 3 consecutive monthly dividend payments of $0.1408 from January to March and subsequent payments of $0.1056 per share from April to December following a dividend payment reduction. The subsequent payments of $0.1056 per share represent a 25% reduction from previous dividend payments and were based on an assessment of market conditions by Barings at the time. The Fund’s share price and net asset value (“NAV”) ended the reporting period at $15.09 and $16.68, respectively, or at a 10.5% discount to NAV. Based on the Fund’s share price and NAV on December 31, 2020, the Fund’s market price and NAV distribution rates – using the most recent monthly dividend, on an annualized basis – were 8.40% and 7.60%, respectively. Assets acquired through leverage, which represented 28.7% of the Fund’s total assets at the end of December, were accretive to net investment income and benefited shareholders.

On a year-to-date (“YTD”) basis through December 31, 2020, the NAV total return was 0.79%, underperforming the global high yield bond market, as measured by the Bank of America / Merrill Lynch Non-Financial Developed Markets High Yield Constrained Index (HNDC), which returned 5.56% on a USD hedged basis. From a market value perspective, the total return year-to-date through December 31, 2020 was -4.65%.2 During the first six months of 2020, the Fund saw considerable weakness, returning -18.81% as a result of the Covid-19 pandemic with much of the negative returns stemming from the metals and mining and energy sectors, where the Fund maintained larger positions. Other Covid-centric sectors also weighed heavily on performance such as credits in the travel, leisure, and services sectors given the abrupt enactment of global lockdowns. The risk-off sentiment drove outflows from the asset class with lower-quality single-Bs and triple-Cs seeing the most weakness in trading levels and, as such, weighing most heavily on Fund performance. During the second half of the year, however, the Fund made substantial headway in gaining back performance lost during the unprecedented market volatility earlier in the year, returning 24.14%, from an NAV perspective, for the final six months of the year. While still detracting from performance for the full year, the energy sector rebounded strongly in the last six months, up over 20% on a total return basis. Similarly, the financial and manufacturing sectors returned approximately 19% and 16%, respectively. By year-end, the metals and mining sector continued to be the largest detractor, given earlier losses, though the Fund was still able to regain a portion of the negative performance in the sector, returning 29% for the semi-annual period ended December 31, 2020. The majority of all other sectors ended the year either in positive territory or negative to a modest degree. Lower-quality credit across the market and within the Fund outperformed in the second half of the year led by triple-Cs and followed by single-Bs. While still positively contributing to Fund performance, double-Bs lagged the broader market. From an asset class perspective, positive total returns in the latter half of the year were led by CLOs, followed by senior secured loans and high yield bonds.

On November 9, 2020, Thomas M. Finke submitted his resignation from the Board of Directors (the “Board”) of Barings Global Short Duration High Yield Fund (the “Fund”), effective as of the close of business on November 30, 2020. Mr. Finke, former Chief Executive Officer of Barings LLC (“Barings”), the Fund’s external investment adviser, decided to retire from Barings. Mr. Finke’s resignation was not the result of a disagreement with the Fund on any matter relating to its operations, policies or practices. The Board, upon recommendation from its Nominating and Corporate Governance Committee, appointed David Mihalick to fill the vacant seat created by Mr. Finke’s resignation, effective as of the close of business on November 30, 2020, to serve as a Class I member of the Board for the remainder of the full term of such Class I directorship.

Market Outlook

We believe high yield credit markets have a number of supportive tailwinds heading into 2021, from a more manageable default environment compared to 2020 to the continued search for yield by investors globally. These are in addition to the potential for further improvements in local economies as the cadence of vaccine distribution and implementation increases,

3

Barings Global Short Duration High Yield Fund 2020 Annual Report

although varying by region. While we believe defaults are likely to remain elevated going into 2021, we believe they will remain much lower than peak-Covid forecasts, largely due to markets being open as has been the case over recent months. Investors have been willing to capitalize businesses and central bank support has been a critical component of that. However, there remains an element of uncertainty in the markets and therefore we believe credit selection will remain critical in the high yield credit markets focused on issuers that can withstand short-term market volatility and potentially offer attractive risk-adjusted returns as the global economy continues to recover.

At Barings, we remain committed to focusing on corporate fundamentals as market sentiment can change quickly and unexpectedly. Our focused and disciplined approach emphasizes our fundamental bottom-up research, with the goal of preserving investor capital while seeking to capture attractive capital appreciation opportunities that may exist through market and economic cycles. On behalf of the Barings team, we continue to take a long-term view of investing despite the recent economic challenges, and look forward to helping you achieve your investment goals.

Sincerely,

Sean Feeley

| 1. | Ratings are based on Moody’s, S&P and Fitch. If securities are rated differently by the rating agencies, the higher rating is applied and all ratings are converted to the equivalent Moody’s major rating category for purposes of the category shown. Credit ratings are based largely on the rating agency’s investment analysis at the time of rating and the rating assigned to any particular security is not necessarily a reflection of the issuer’s current financial condition. The rating assigned to a security by a rating agency does not necessarily reflect its assessment of the volatility of the security’s market value or of the liquidity of an investment in the security. Ratings of Baa3 or higher by Moody’s and BBB- or higher by S&P and Fitch are considered to be investment grade quality. |

| 2. | Past performance is not necessarily indicative of future results. Current performance may be lower or higher. All performance is net of fees, which is inclusive of advisory fees, administrator fees and interest expense. |

4

Barings Global Short Duration High Yield Fund 2020 Annual Report

PORTFOLIO COMPOSITION (% OF ASSETS*)

COUNTRY COMPOSITION (% OF ASSETS*)

| * | The percentages shown above represent a percentage of the assets as of December 31, 2020. |

5

Barings Global Short Duration High Yield Fund 2020 Annual Report

FINANCIAL REPORT

6

Barings Global Short Duration High Yield Fund 2020 Annual Report

STATEMENT OF ASSETS AND LIABILITIES

| | | | |

| | | DECEMBER 31, 2020 | |

| |

| Assets | | | | |

| Investments, at fair value (cost $478,817,979) | | $ | 458,897,234 | |

| Cash | | | 2,053,651 | |

| Foreign currency, at fair value (cost $68,731) | | | 69,158 | |

| Receivable for investments sold | | | 1,500,798 | |

| Interest receivable | | | 10,062,979 | |

| Prepaid expenses and other assets | | | 8,151 | |

| | | | |

Total assets | | | 472,591,971 | |

| | | | |

| |

| Liabilities | | | | |

| Note payable | | | 135,950,000 | |

| Dividend payable | | | 70,332 | |

| Payable for investments purchased | | | 580,121 | |

| Payable to adviser | | | 328,102 | |

| Unrealized depreciation on forward foreign exchange contracts | | | 493,952 | |

| Accrued expenses and other liabilities | | | 593,360 | |

| | | | |

Total liabilities | | | 138,015,867 | |

| | | | |

Total net assets | | $ | 334,576,104 | |

| | | | |

| |

| Net Assets: | | | | |

| Common shares, $0.00001 par value | | $ | 201 | |

| Additional paid-in capital | | | 468,435,225 | |

| Accumulated losses | | | (133,859,322 | ) |

| | | | |

Total net assets | | $ | 334,576,104 | |

| | | | |

| |

| Common shares issued and outstanding (unlimited shares authorized) | | | 20,064,313 | |

| | | | |

| |

Net asset value per share | | $ | 16.68 | |

| | | | |

See accompanying Notes to the Financial Statements.

7

Barings Global Short Duration High Yield Fund 2020 Annual Report

STATEMENT OF OPERATIONS

| | | | |

| | | YEAR ENDED

DECEMBER 31, 2020 | |

| |

| Investment Income | | | | |

Interest income | | $ | 38,378,651 | |

Dividends from common stock (net of foreign taxes withheld of $54,730) | | | 187,467 | |

Other income | | | 191,491 | |

| | | | |

Total investment income | | | 38,757,609 | |

| | | | |

| |

| Operating Expenses | | | | |

Advisory fees | | | 4,204,530 | |

Interest expense | | | 1,646,178 | |

Administrator fees | | | 349,842 | |

Taxes paid on undistributed income | | | 390,061 | |

Professional fees | | | 236,654 | |

Trustees fees | | | 91,121 | |

Printing and mailing expense | | | 65,030 | |

Pricing expense | | | 21,500 | |

Other operating expenses | | | 32,359 | |

| | | | |

Total operating expenses | | | 7,037,275 | |

| | | | |

Less fees waived by Adviser | | | (257,838 | ) |

| | | | |

Net Expenses | | | 6,779,437 | |

| | | | |

Net investment income | | | 31,978,172 | |

| | | | |

| |

| Realized and Unrealized Gains (Losses) on Investments | | | | |

Net realized loss on investments | | | (43,366,843 | ) |

Net realized gain on forward foreign exchange contracts | | | 277,051 | |

Net realized loss on foreign currency related transactions | | | (1,945,512 | ) |

| | | | |

Net realized loss on investments, forward foreign exchange contracts and foreign currency related transactions | | | (45,035,304 | ) |

| | | | |

Net change in unrealized appreciation on investments | | | 7,648,517 | |

Net change in unrealized depreciation on forward foreign exchange contracts | | | (122,813 | ) |

Net change in unrealized appreciation on foreign currency translation | | | 3,016 | |

| | | | |

Net change in unrealized appreciation on investments, forward foreign exchange contracts and foreign currency translation | | | 7,528,720 | |

| | | | |

Net realized and unrealized losses | | | (37,506,584 | ) |

| | | | |

Net decrease in net assets resulting from operations | | $ | (5,528,412 | ) |

| | | | |

See accompanying Notes to the Financial Statements.

8

Barings Global Short Duration High Yield Fund 2020 Annual Report

STATEMENT OF CASH FLOWS

| | | | |

| | | YEAR ENDED

DECEMBER 31, 2020 | |

| |

Reconciliation of net decrease in net assets resulting from

operations to net cash provided by operating activities | | | | |

| Net decrease in net assets applicable to common shareholders resulting from operations | | $ | (5,528,412 | ) |

| Adjustments to reconcile net decrease in net assets applicable to common shareholders resulting from operations to net cash provided by operating activities: | | | | |

Purchases of long-term investments | | | (173,524,718 | ) |

Proceeds from sales of long-term investments | | | 184,586,929 | |

Proceeds from sales of foreign currency, net | | | 161,848 | |

Forward currency exchange contracts, net | | | 122,813 | |

Net change in unrealized appreciation on investments | | | (7,648,517 | ) |

Net realized loss on investments | | | 43,366,843 | |

Amortization and accretion | | | (1,389,069 | ) |

Changes in operating assets and liabilities: | | | | |

Decrease in interest receivable | | | 706,633 | |

Increase in prepaid expenses and other assets | | | (8,151 | ) |

Increase in receivable for investments sold | | | (1,500,798 | ) |

Increase in payable for investments purchased | | | 217,983 | |

Decrease in payable to Adviser | | | (104,424 | ) |

Decrease in accrued expenses and other liabilities | | | (263,779 | ) |

| | | | |

Net cash provided by operating activities | | | 39,195,181 | |

| | | | |

| Cash flows from financing activities | | | | |

Advances from credit facility | | | 69,500,000 | |

Repayments on credit facility | | | (80,750,000 | ) |

Distributions paid to common shareholders | | | (30,447,485 | ) |

| | | | |

Net cash used in financing activities | | | (41,697,485 | ) |

| | | | |

Net change in cash | | | (2,502,304 | ) |

Cash beginning of year | | | 4,555,955 | |

| | | | |

Cash end of year | | $ | 2,053,651 | |

| | | | |

| |

| Supplemental disclosure of cash flow information | | | | |

Income taxes paid | | $ | 123,794 | |

Interest paid | | | 1,824,574 | |

See accompanying Notes to the Financial Statements.

9

Barings Global Short Duration High Yield Fund 2020 Annual Report

STATEMENTS OF CHANGES IN NET ASSETS

| | | | | | | | |

| | | YEAR ENDED

DECEMBER 31, 2020 | | | YEAR ENDED

DECEMBER 31, 2019 | |

| | |

| Operations | | | | | | | | |

Net investment income | | $ | 31,978,172 | | | $ | 37,994,028 | |

Net realized loss on investments, forward foreign exchange contracts and foreign currency related transactions | | | (45,035,304 | ) | | | (15,486,954 | ) |

Net change in unrealized appreciation on investments, forward foreign exchange contracts and foreign currency translation | | | 7,528,720 | | | | 14,010,346 | |

| | | | | | | | |

Net increase (decrease) in net assets resulting from operations | | | (5,528,412 | ) | | | 36,517,420 | |

| | | | | | | | |

| | |

| Dividends to Common Shareholders | | | | | | | | |

From distributable earnings | | | (27,544,286 | ) | | | (35,672,794 | ) |

| | | | | | | | |

Total dividends to common shareholders | | | (27,544,286 | ) | | | (35,672,794 | ) |

| | | | | | | | |

| | |

| Capital Stock Transactions | | | | | | | | |

Issuance from common shares issued on reinvestment | | | — | | | | 112,799 | |

| | | | | | | | |

Net increase in net assets from capital stock transactions | | | — | | | | 112,799 | |

| | | | | | | | |

Total increase (decrease) in net assets | | | (33,072,698 | ) | | | 957,425 | |

| | | | | | | | |

| | |

| Net Assets | | | | | | | | |

Beginning of year | | | 367,648,802 | | | | 366,691,377 | |

| | | | | | | | |

End of year | | $ | 334,576,104 | | | $ | 367,648,802 | |

| | | | | | | | |

See accompanying Notes to the Financial Statements.

10

Barings Global Short Duration High Yield Fund 2020 Annual Report

FINANCIAL HIGHLIGHTS

| | | | | | | | | | | | | | | | | | | | |

| | | YEAR ENDED

DECEMBER 31,

2020 | | | YEAR ENDED

DECEMBER 31,

2019 | | | YEAR ENDED

DECEMBER 31,

2018 | | | YEAR ENDED

DECEMBER 31,

2017 | | | YEAR ENDED

DECEMBER 31,

2016 | |

| | | | | |

| Per Common Share Data | | | | | | | | | | | | | | | | | | | | |

Net asset value, beginning of year | | $ | 18.32 | | | $ | 18.28 | | | $ | 20.84 | | | $ | 20.87 | | | $ | 18.47 | |

Income from investment operations: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | 1.59 | | | | 1.87 | | | | 1.89 | | | | 1.77 | | | | 1.57 | |

Net realized and unrealized gains (losses) on investments | | | (1.86 | ) | | | (0.05 | ) | | | (2.67 | ) | | | 0.04 | | | | 2.68 | |

| | | | | | | | | | | | | | | | | | | | |

Total increase (decrease) from investment operations | | | (0.27 | ) | | | 1.82 | | | | (0.78 | ) | | | 1.81 | | | | 4.25 | |

| | | | | | | | | | | | | | | | | | | | |

Less dividends to common stockholders: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | (1.37 | ) | | | (1.78 | ) | | | (1.78 | ) | | | (1.63 | ) | | | (1.60 | ) |

Net realized gain | | | – | | | | – | | | | – | | | | – | | | | – | |

Return of capital | | | – | | | | – | | | | – | | | | (0.21 | ) | | | (0.25 | ) |

| | | | | | | | | | | | | | | | | | | | |

Total dividends to common stockholders | | | (1.37 | ) | | | (1.78 | ) | | | (1.78 | ) | | | (1.84 | ) | | | (1.85 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net asset value, end of year | | $ | 16.68 | | | $ | 18.32 | | | $ | 18.28 | | | $ | 20.84 | | | $ | 20.87 | |

| | | | | | | | | | | | | | | | | | | | |

Per common share market value, end of year | | $ | 15.09 | | | $ | 17.53 | | | $ | 15.95 | | | $ | 19.38 | | | $ | 19.23 | |

| | | | | | | | | | | | | | | | | | | | |

Total investment return based on net asset value (1) | | | 0.79 | % | | | 10.77 | | | | (3.42 | )% | | | 9.40 | % | | | 25.42 | % |

| | | | | | | | | | | | | | | | | | | | |

Total investment return based on market value (1) | | | (4.65 | )% | | | 21.45 | | | | (9.38 | )% | | | 10.41 | % | | | 29.44 | % |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

| Supplemental Data and Ratios | | | | | | | | | | | | | | | | | | | | |

Net assets, end of period (000’s) | | $ | 334,576 | | | $ | 367,649 | | | $ | 366,691 | | | $ | 417,924 | | | $ | 418,613 | |

Ratio of expenses (before reductions and reimbursements) to average net assets | | | 2.32 | %(2) | | | 3.00 | % | | | 2.93 | % | | | 2.33 | % | | | 2.05 | %(2) |

Ratio of expenses (after reductions and reimbursements) to average net assets | | | 2.23 | % | | | 3.00 | % | | | 2.93 | % | | | 2.33 | % | | | 1.78 | % |

Ratio of net investment income (before reductions and reimbursements) to average net assets | | | 10.61 | %(2) | | | 10.22 | % | | | 9.34 | % | | | 9.20 | % | | | 10.68 | %(2) |

Ratio of net investment income (after reductions and reimbursements) to average net assets | | | 10.53 | % | | | 10.22 | % | | | 9.34 | % | | | 9.20 | % | | | 10.41 | % |

Portfolio turnover rate | | | 42.21 | % | | | 52.25 | % | | | 48.92 | % | | | 36.59 | % | | | 44.81 | % |

| (1) | | Total investment return calculation assumes reinvestment of dividends at actual prices pursuant to the Fund’s dividend reinvestment plan. Total investment return does not reflect brokerage commissions. |

| (2) | | The Adviser contractually waived a portion of its management and other fees equal to an annual rate of 0.275% of the Fund’s managed assets for a period of one year ended December 31, 2016. Effective August 6, 2020 the Adviser began waiving a portion of it’s management and other fees equal to an annual rate of 0.150% of the Fund’s managed assets. |

See accompanying Notes to the Financial Statements.

11

Barings Global Short Duration High Yield Fund 2020 Annual Report

SCHEDULE OF INVESTMENTS

December 31, 2020

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | SHARES | | | COST | | | FAIR

VALUE | |

Equities — 1.50%*: | |

|

Common Stocks — 1.42%*: | |

Boomerang Tube Holdings, Inc.¤ | | | | | | | | | | | 36,149 | | | | $3,510,832 | | | | $0 | |

Fieldwood Energy LLC¤ | | | | | | | | | | | 167,574 | | | | 4,057,567 | | | | 0 | |

Jupiter Resources Inc.¤+& | | | | | | | | | | | 1,171,624 | | | | 5,662,542 | | | | 3,749,197 | |

Sabine Oil & Gas LLC¤ | | | | | | | | | | | 4,342 | | | | 248,858 | | | | 56,446 | |

KCA Deutag Ordinary A Shares¤+ | | | | | | | | | | | 23,585 | | | | 990,570 | | | | 955,193 | |

Travelex Private Equity¤+ | | | | | | | | | | | 16,120 | | | | 0 | | | | 0 | |

| | | | | | | | | | | | | | | | | | | | |

Total Common Stocks | | | | | | | | | | | 1,419,394 | | | | 14,470,369 | | | | 4,760,836 | |

| | | | | | | | | | | | | | | | | | | | |

|

Warrants — 0.08%*: | |

Travelex Topco Limited Warrant¤+ | | | | | | | | | | | 2,218 | | | | 0 | | | | 250,232 | |

| | | | | | | | | | | | | | | | | | | | |

Total Warrants | | | | | | | | | | | 2,218 | | | | 0 | | | | 250,232 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

Total Equities | | | | | | | | | | | 1,421,612 | | | | 14,470,369 | | | | 5,011,068 | |

| | | | | | | | | | | | | | | | | | | | |

| | | EFFECTIVE

INTEREST RATE ‡ | | | DUE DATE | | | PRINCIPAL | | | COST | | | FAIR

VALUE | |

Fixed Income — 135.66%*: | |

|

Asset-Backed Securities — 11.34%*: | |

|

CDO/CLO — 11.34%*: | |

Anchorage Capital CLO LTD 2015-6A, 3M LIBOR + 6.350%^~ | | | 6.59 | % | | | 7/15/2030 | | | | 600,000 | | | | $608,442 | | | | $573,109 | |

Anchorage Capital CLO LTD 2016-9A ER, 3M LIBOR + 6.410%^~ | | | 6.65 | | | | 7/15/2032 | | | | 1,500,000 | | | | 1,455,000 | | | | 1,494,992 | |

Anchorage Capital CLO LTD 2013-1R, 3M LIBOR + 6.800%^~ | | | 7.02 | | | | 10/15/2030 | | | | 1,000,000 | | | | 977,213 | | | | 1,000,078 | |

Bain Capital Credit CLO 2020-2 E, 3M LIBOR + 6.830%^~ | | | 7.05 | | | | 7/29/2031 | | | | 1,000,000 | | | | 926,357 | | | | 1,001,627 | |

Ballyrock CLO LTD 2019-2A, 3M LIBOR + 7.740%^~ | | | 7.96 | | | | 11/20/2030 | | | | 2,000,000 | | | | 1,960,000 | | | | 2,001,464 | |

BlueMountain CLO LTD 2018-23A, 3M LIBOR + 5.650%^~ | | | 5.87 | | | | 10/20/2031 | | | | 1,000,000 | | | | 1,000,000 | | | | 936,141 | |

Canyon CLO LTD 2019-2A, 3M LIBOR + 7.150%^~ | | | 7.39 | | | | 10/15/2032 | | | | 1,000,000 | | | | 1,000,000 | | | | 1,001,340 | |

Carbone CLO, LTD 2017-1A, 3M LIBOR + 5.900%^~ | | | 6.12 | | | | 1/21/2031 | | | | 750,000 | | | | 750,000 | | | | 702,061 | |

Carlyle Global Market Strategies 2013-3A, 3M LIBOR + 7.750%^~ | | | 7.99 | | | | 10/15/2030 | | | | 1,000,000 | | | | 1,000,000 | | | | 715,936 | |

Carlyle Global Market Strategies 2017-5A, 3M LIBOR + 5.300%^~ | | | 5.52 | | | | 1/22/2030 | | | | 700,000 | | | | 700,000 | | | | 616,791 | |

Carlyle Global Market Strategies 2019-3 LTD, 3M LIBOR + 7.030%^~ | | | 7.25 | | | | 10/20/2032 | | | | 1,000,000 | | | | 975,000 | | | | 1,000,412 | |

Cedar Funding LTD 2016-6A, 3M LIBOR + 5.900%^~ | | | 6.12 | | | | 10/20/2028 | | | | 2,500,000 | | | | 2,500,000 | | | | 2,399,155 | |

CIFC Funding 2020-1 LTD^~ | | | 7.32 | | | | 7/15/2032 | | | | 1,900,000 | | | | 1,881,000 | | | | 1,907,484 | |

See accompanying Notes to the Financial Statements.

12

Barings Global Short Duration High Yield Fund 2020 Annual Report

SCHEDULE OF INVESTMENTS (CONTINUED)

December 31, 2020

| | | | | | | | | | | | | | | | | | | | |

| | | EFFECTIVE

INTEREST RATE ‡ | | | DUE DATE | | | PRINCIPAL | | | COST | | | FAIR

VALUE | |

Fixed Income (Continued) | |

|

Asset-Backed Securities (Continued) | |

|

CDO/CLO (Continued) | |

Galaxy CLO LTD 2017-24A, 3M LIBOR + 5.500%^~ | | | 5.74 | % | | | 1/15/2031 | | | | 1,000,000 | | | | $1,000,000 | | | | $938,032 | |

GoldenTree Loan Management 2018-3A, 3M LIBOR + 6.500%^~ | | | 6.72 | | | | 4/22/2030 | | | | 1,500,000 | | | | 1,439,376 | | | | 1,226,774 | |

GoldenTree Loan Opportunities XI LTD 2015-11A, 3M LIBOR + 5.400%^~ | | | 5.62 | | | | 1/18/2031 | | | | 500,000 | | | | 500,000 | | | | 471,166 | |

KKR Financial CLO LTD 2017-20, 3M LIBOR + 5.500%^~ | | | 5.73 | | | | 10/16/2030 | | | | 1,500,000 | | | | 1,500,000 | | | | 1,368,239 | |

LCM LTD 2019-30, 3M LIBOR + 6.950%^~ | | | 7.17 | | | | 4/21/2031 | | | | 1,100,000 | | | | 1,100,000 | | | | 1,099,232 | |

Madison Park Funding LTD 2015-19A, 3M LIBOR + 4.350%^~ | | | 4.57 | | | | 1/24/2028 | | | | 1,000,000 | | | | 1,000,000 | | | | 912,674 | |

Madison Park Funding LTD 2018-29A, 3M LIBOR + 7.570%^~# | | | 7.79 | | | | 10/18/2030 | | | | 2,000,000 | | | | 1,960,000 | | | | 1,702,548 | |

Madison Park Funding LTD 2019-32E, 3M LIBOR + 7.100%^~ | | | 7.32 | | | | 1/22/2031 | | | | 1,000,000 | | | | 997,800 | | | | 1,000,325 | |

Magnetite CLO LTD 2016-18A, 3M LIBOR + 7.600%^~ | | | 7.82 | | | | 11/15/2028 | | | | 1,400,000 | | | | 1,386,000 | | | | 1,238,364 | |

Neuberger Berman Loan Advisers CLO LTD, 3M LIBOR + 7.050% ^~ | | | 7.27 | | | | 7/21/2031 | | | | 800,000 | | | | 792,000 | | | | 804,538 | |

OCP CLO LTD 2020-19, 3M LIBOR + 6.110% ^~ | | | 6.43 | | | | 7/21/2031 | | | | 800,000 | | | | 713,203 | | | | 796,039 | |

OHA Credit Partners LTD 2015-11A, 3M LIBOR + 7.900%^~ | | | 8.12 | | | | 1/20/2032 | | | | 2,000,000 | | | | 1,970,323 | | | | 1,731,160 | |

OHA Loan Funding LTD 2013-1A, 3M LIBOR + 7.900%^~ | | | 8.11 | | | | 7/23/2031 | | | | 1,500,000 | | | | 1,477,500 | | | | 1,307,006 | |

Sound Point CLO XVIII 2018-18D, 3M LIBOR + 5.500%^~ | | | 5.72 | | | | 1/21/2031 | | | | 2,000,000 | | | | 2,000,000 | | | | 1,762,796 | |

Sound Point CLO Ltd Series 2020-1A Class E, 3M LIBOR + 7.080%^~ | | | 7.39 | | | | 7/22/2030 | | | | 1,600,000 | | | | 1,471,120 | | | | 1,602,810 | |

TICP CLO LTD 2018-10A, 3M LIBOR + 5.500%^~ | | | 5.72 | | | | 4/20/2031 | | | | 1,000,000 | | | | 933,145 | | | | 948,026 | |

Voya CLO LTD 2019-4A, 3M LIBOR + 7.480%^~ | | | 7.72 | | | | 1/18/2033 | | | | 1,400,000 | | | | 1,358,585 | | | | 1,401,628 | |

Wellfleet CLO LTD 2017-3A, 3M LIBOR + 5.550%^~ | | | 5.77 | | | | 1/17/2031 | | | | 1,500,000 | | | | 1,500,000 | | | | 1,354,500 | |

Wind River CLO LTD 2017-4A, 3M LIBOR + 5.800%^~ | | | 6.02 | | | | 11/20/2030 | | | | 1,000,000 | | | | 1,000,000 | | | | 926,511 | |

| | | | | | | | | | | | | | | | | | | | |

Total CDO/CLO | | | | | | | | | | | 40,550,000 | | | | 39,832,064 | | | | 37,942,958 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

Total Asset-Backed Securities | | | | | | | | | | | 40,550,000 | | | | 39,832,064 | | | | 37,942,958 | |

| | | | | | | | | | | | | | | | | | | | |

See accompanying Notes to the Financial Statements.

13

Barings Global Short Duration High Yield Fund 2020 Annual Report

SCHEDULE OF INVESTMENTS (CONTINUED)

December 31, 2020

| | | | | | | | | | | | | | | | | | | | |

| | | EFFECTIVE

INTEREST RATE ‡ | | | DUE DATE | | | PRINCIPAL | | | COST | | | FAIR

VALUE | |

Fixed Income (Continued) | |

| | | | | |

Bank Loans§ — 8.62%*: | | | | | | | | | | | | | | | | | | | | |

|

Automotive — 0.59%*: | |

Dexko Global Inc, 3M LIBOR + 8.250%~ | | | 9.25 | % | | | 7/24/2025 | | | | 2,000,000 | | | | $2,000,000 | | | | $1,982,500 | |

| | | | | | | | | | | | | | | | | | | | |

Total Automotive | | | | | | | | | | | 2,000,000 | | | | 2,000,000 | | | | 1,982,500 | |

| | | | | | | | | | | | | | | | | | | | |

|

Chemicals, Plastics and Rubber — 0.46%*: | |

Colouroz Investment 2 LLC, 3M LIBOR + 7.250%+~ | | | 5.50 | | | | 9/21/2024 | | | | 2,050,737 | | | | 2,042,988 | | | | 1,544,472 | |

| | | | | | | | | | | | | | | | | | | | |

Total Chemicals, Plastics and Rubber | | | | | | | | | | | 2,050,737 | | | | 2,042,988 | | | | 1,544,472 | |

| | | | | | | | | | | | | | | | | | | | |

|

Diversified/Conglomerate Manufacturing — 0.89%*: | |

Averys, 3M LIBOR + 8.250%+~ | | | 8.25 | | | | 9/25/2026 | | | | 500,000 | | | | 571,943 | | | | 531,036 | |

Commercial Vehicle Group Inc., 1M LIBOR + 6.000%~ | | | 5.75 | | | | 4/12/2023 | | | | 544,580 | | | | 538,913 | | | | 522,797 | |

SunSource, Inc., 1M LIBOR + 8.000%~ | | | 9.00 | | | | 4/30/2026 | | | | 2,500,000 | | | | 2,515,048 | | | | 1,926,575 | |

| | | | | | | | | | | | | | | | | | | | |

Total Diversified/Conglomerate Manufacturing | | | | | | | | | | | 3,544,580 | | | | 3,625,904 | | | | 2,980,408 | |

| | | | | | | | | | | | | | | | | | | | |

|

Diversified/Conglomerate Service — 4.67%*: | |

Misys (Finastra), 3M LIBOR + 7.250%~ | | | 8.25 | | | | 6/16/2025 | | | | 15,630,136 | | | | 15,505,118 | | | | 15,635,763 | |

| | | | | | | | | | | | | | | | | | | | |

Total Diversified/Conglomerate Service | | | | | | | | | | | 15,630,136 | | | | 15,505,118 | | | | 15,635,763 | |

| | | | | | | | | | | | | | | | | | | | |

|

Healthcare, Education and Childcare — 1.92%*: | |

Advanz Pharma Corp., 1M LIBOR + 5.500%+~ | | | 6.50 | | | | 9/6/2024 | | | | 3,820,000 | | | | 3,766,565 | | | | 3,726,410 | |

Envision Healtcare, 1M LIBOR + 3.750%~ | | | 3.90 | | | | 10/10/2025 | | | | 3,228,439 | | | | 2,321,862 | | | | 2,683,253 | |

| | | | | | | | | | | | | | | | | | | | |

Total Healthcare, Education and Childcare | | | | | | | | | | | 7,048,439 | | | | 6,088,427 | | | | 6,409,663 | |

| | | | | | | | | | | | | | | | | | | | |

|

Mining, Steel, Iron and Non-Precious Metals — 0.03%*: | |

Boomerang Tube, LLC, 3M LIBOR + 6.500%¤~ | | | 5.15 | | | | 6/30/2022 | | | | 2,608,648 | | | | 2,608,648 | | | | 104,346 | |

| | | | | | | | | | | | | | | | | | | | |

Total Mining, Steel, Iron and Non-Precious Metals | | | | | | | | | | | 2,608,648 | | | | 2,608,648 | | | | 104,346 | |

| | | | | | | | | | | | | | | | | | | | |

|

Oil and Gas — 0.00%*: | |

Fieldwood Energy LLC, 1M LIBOR + 7.250%~ | | | 0.00 | | | | 4/11/2023 | | | | 7,481,592 | | | | 2,720,500 | | | | 1,721 | |

| | | | | | | | | | | | | | | | | | | | |

Total Oil and Gas | | | | | | | | | | | 7,481,592 | | | | 2,720,500 | | | | 1,721 | |

| | | | | | | | | | | | | | | | | | | | |

|

Personal Transportation — 0.06%*: | |

Naviera Armas Bridge, 1M LIBOR + 2.500%¤+~ | | | 5.00 | | | | 4/30/2021 | | | | 106,472 | | | | 128,305 | | | | 127,521 | |

Naviera Armas Bridge, 1M LIBOR + 2.500%¤+~ | | | 0.00 | | | | 4/30/2021 | | | | 60,543 | | | | 69,174 | | | | 68,751 | |

| | | | | | | | | | | | | | | | | | | | |

Total Personal Transportation | | | | | | | | | | | 167,015 | | | | 197,479 | | | | 196,272 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | |

Total Bank Loans | | | | | | | | | | | 40,531,148 | | | | 34,789,064 | | | | 28,855,145 | |

| | | | | | | | | | | | | | | | | | | | |

Corporate Bonds — 115.70%*: | | | | | | | | | | | | | | | | | | | | |

|

Aerospace and Defense — 4.29%*: | |

Rolls Royce^+ | | | 5.75 | | | | 10/15/2027 | | | | 250,000 | | | | 325,750 | | | | 377,773 | |

TransDigm Group, Inc.# | | | 7.50 | | | | 3/15/2027 | | | | 6,000,000 | | | | 6,023,714 | | | | 6,405,000 | |

See accompanying Notes to the Financial Statements.

14

Barings Global Short Duration High Yield Fund 2020 Annual Report

SCHEDULE OF INVESTMENTS (CONTINUED)

December 31, 2020

| | | | | | | | | | | | | | | | | | | | |

| | | EFFECTIVE

INTEREST RATE ‡ | | | DUE DATE | | | PRINCIPAL | | | COST | | | FAIR

VALUE | |

Fixed Income (Continued) | |

| | | | | |

Corporate Bonds (Continued) | | | | | | | | | | | | | | | | | | | | |

|

Aerospace and Defense (Continued) | |

Triumph Group, Inc.# | | | 7.75 | % | | | 8/15/2025 | | | | 8,289,000 | | | | $8,293,067 | | | | $7,574,074 | |

| | | | | | | | | | | | | | | | | | | | |

Total Aerospace and Defense | | | | | | | | | | | 14,539,000 | | | | 14,642,531 | | | | 14,356,847 | |

| | | | | | | | | | | | | | | | | | | | |

|

Automotive — 6.46%*: | |

Ford Motor Company# | | | 9.63 | | | | 4/22/2030 | | | | 2,000,000 | | | | 2,603,393 | | | | 2,822,500 | |

Ford Motor Company# | | | 7.45 | | | | 7/16/2031 | | | | 2,000,000 | | | | 2,327,377 | | | | 2,565,000 | |

Power Solutions^# | | | 8.50 | | | | 5/15/2027 | | | | 8,965,000 | | | | 9,059,575 | | | | 9,739,660 | |

Truck Hero Inc.^# | | | 8.50 | | | | 4/21/2024 | | | | 6,118,000 | | | | 6,140,149 | | | | 6,492,728 | |

| | | | | | | | | | | | | | | | | | | | |

Total Automotive | | | | | | | | | | | 19,083,000 | | | | 20,130,494 | | | | 21,619,888 | |

| | | | | | | | | | | | | | | | | | | | |

|

Beverage, Food and Tobacco — 1.99%*: | |

Kehe Distributors, LLC^# | | | 8.63 | | | | 10/15/2026 | | | | 1,287,000 | | | | 1,287,000 | | | | 1,444,658 | |

Manitowoc Foodservice# | | | 9.50 | | | | 2/15/2024 | | | | 3,074,000 | | | | 3,195,099 | | | | 3,177,102 | |

Refresco Group N.V.+^# | | | 6.50 | | | | 5/15/2026 | | | | 1,600,000 | | | | 1,931,881 | | | | 2,026,949 | |

| | | | | | | | | | | | | | | | | | | | |

Total Beverage, Food and Tobacco | | | | | | | | | | | 5,961,000 | | | | 6,413,980 | | | | 6,648,709 | |

| | | | | | | | | | | | | | | | | | | | |

|

Broadcasting and Entertainment — 5.29%*: | |

Arqiva Broadcast+^# | | | 6.75 | | | | 9/30/2023 | | | | 2,400,000 | | | | 3,038,647 | | | | 3,383,585 | |

Banijay+^# | | | 6.50 | | | | 3/1/2026 | | | | 2,500,000 | | | | 2,761,119 | | | | 3,060,215 | |

Clear Channel Worldwide Holdings Inc.# | | | 9.25 | | | | 2/15/2024 | | | | 5,469,000 | | | | 5,769,360 | | | | 5,537,363 | |

Cox Media Group^# | | | 8.88 | | | | 12/15/2027 | | | | 1,837,000 | | | | 1,853,762 | | | | 2,025,293 | |

Dish DBS Corp.# | | | 7.75 | | | | 7/1/2026 | | | | 673,000 | | | | 611,892 | | | | 753,767 | |

Townsquare Media Inc.^ | | | 6.50 | | | | 4/1/2023 | | | | 430,000 | | | | 402,498 | | | | 437,568 | |

Univision Communications Inc.^# | | | 9.50 | | | | 5/1/2025 | | | | 2,234,000 | | | | 2,481,405 | | | | 2,485,325 | |

| | | | | | | | | | | | | | | | | | | | |

Total Broadcasting and Entertainment | | | | | | | | | | | 15,543,000 | | | | 16,918,683 | | | | 17,683,116 | |

| | | | | | | | | | | | | | | | | | | | |

|

Buildings and Real Estate — 3.16%*: | |

Cemex S.A.B. de C.V.^# | | | 7.38 | | | | 6/5/2027 | | | | 698,000 | | | | 698,000 | | | | 794,324 | |

New Enterprise Stone & Lime Co.^# | | | 9.75 | | | | 7/15/2028 | | | | 665,000 | | | | 665,000 | | | | 728,175 | |

Realogy Group^# | | | 9.38 | | | | 4/1/2027 | | | | 3,763,000 | | | | 3,586,302 | | | | 4,167,523 | |

Realogy Group^ | | | 7.63 | | | | 6/15/2025 | | | | 329,000 | | | | 329,000 | | | | 357,202 | |

Service Properties Trust | | | 4.38 | | | | 2/15/2030 | | | | 400,000 | | | | 347,926 | | | | 390,000 | |

Stl Hldg Co LLC^# | | | 7.50 | | | | 2/15/2026 | | | | 4,000,000 | | | | 4,000,000 | | | | 4,150,000 | |

| | | | | | | | | | | | | | | | | | | | |

Total Buildings and Real Estate | | | | | | | | | | | 9,855,000 | | | | 9,626,228 | | | | 10,587,224 | |

| | | | | | | | | | | | | | | | | | | | |

|

Cargo Transport — 2.99%*: | |

Kenan Advantage^# | | | 7.88 | | | | 7/31/2023 | | | | 10,000,000 | | | | 10,033,211 | | | | 10,000,000 | |

| | | | | | | | | | | | | | | | | | | | |

Total Cargo Transport | | | | | | | | | | | 10,000,000 | | | | 10,033,211 | | | | 10,000,000 | |

| | | | | | | | | | | | | | | | | | | | |

|

Chemicals, Plastics and Rubber — 4.62%*: | |

Carlyle Group^# | | | 8.75 | | | | 6/1/2023 | | | | 2,600,118 | | | | 2,574,377 | | | | 2,619,619 | |

Consolidated Energy Finance S.A.^# | | | 6.88 | | | | 6/15/2025 | | | | 3,560,000 | | | | 3,426,913 | | | | 3,608,950 | |

Consolidated Energy Finance S.A.^ | | | 6.50 | | | | 5/15/2026 | | | | 2,799,000 | | | | 2,034,626 | | | | 2,799,000 | |

CVR Partners LP^# | | | 9.25 | | | | 6/15/2023 | | | | 4,576,000 | | | | 4,543,382 | | | | 4,580,759 | |

Diversey^# | | | 5.63 | | | | 8/15/2025 | | | | 1,500,000 | | | | 1,627,880 | | | | 1,853,171 | |

| | | | | | | | | | | | | | | | | | | | |

Total Chemicals, Plastics and Rubber | | | | | | | | | | | 15,035,118 | | | | 14,207,178 | | | | 15,461,499 | |

| | | | | | | | | | | | | | | | | | | | |

See accompanying Notes to the Financial Statements.

15

Barings Global Short Duration High Yield Fund 2020 Annual Report

SCHEDULE OF INVESTMENTS (CONTINUED)

December 31, 2020

| | | | | | | | | | | | | | | | | | | | |

| | | EFFECTIVE

INTEREST RATE ‡ | | | DUE DATE | | | PRINCIPAL | | | COST | | | FAIR

VALUE | |

Fixed Income (Continued) | |

| | | | | |

Corporate Bonds (Continued) | | | | | | | | | | | | | | | | | | | | |

|

Containers, Packaging, and Glass — 3.32%*: | |

Mauser Packaging Solutions^# | | | 7.25 | % | | | 4/15/2025 | | | | 2,575,000 | | | | $2,456,803 | | | | $2,600,750 | |

Tekni-Plex^# | | | 9.25 | | | | 8/1/2024 | | | | 8,000,000 | | | | 7,905,687 | | | | 8,520,000 | |

| | | | | | | | | | | | | | | | | | | | |

Total Containers, Packaging, and Glass | | | | | | | | | | | 10,575,000 | | | | 10,362,490 | | | | 11,120,750 | |

| | | | | | | | | | | | | | | | | | | | |

|

Diversified/Conglomerate Manufacturing — 1.66%*: | |

Heat Exchangers+^ | | | 7.78 | | | | 10/9/2025 | | | | 625,000 | | | | 657,723 | | | | 653,579 | |

Manitowoc Cranes^# | | | 9.00 | | | | 4/1/2026 | | | | 4,538,000 | | | | 4,545,995 | | | | 4,901,040 | |

| | | | | | | | | | | | | | | | | | | | |

Total Diversified/Conglomerate Manufacturing | | | | | | | | | | | 5,163,000 | | | | 5,203,718 | | | | 5,554,619 | |

| | | | | | | | | | | | | | | | | | | | |

|

Diversified/Conglomerate Service — 3.39%*: | |

Algeco Scotsman+^# | | | 6.50 | | | | 2/15/2023 | | | | 1,750,000 | | | | 2,142,120 | | | | 2,164,513 | |

Carlson Travel Holdings Inc.^# | | | 11.50 | | | | 12/15/2026 | | | | 6,078,253 | | | | 6,086,402 | | | | 3,297,452 | |

Endurance International Group LLC# | | | 10.88 | | | | 2/1/2024 | | | | 1,324,000 | | | | 1,372,902 | | | | 1,369,678 | |

Powerteam Services LLC^# | | | 9.03 | | | | 12/4/2025 | | | | 2,750,000 | | | | 2,988,790 | | | | 3,059,678 | |

Summer BC Holdco+^ | | | 9.25 | | | | 10/31/2027 | | | | 1,126,301 | | | | 1,353,596 | | | | 1,451,338 | |

| | | | | | | | | | | | | | | | | | | | |

Total Diversified/Conglomerate Service | | | | | | | | | | | 13,028,554 | | | | 13,943,810 | | | | 11,342,659 | |

| | | | | | | | | | | | | | | | | | | | |

|

Diversified Natural Resources, Precious Metals and Minerals — 0.03%*: | |

Northwest Acquisitions ULC+^ | | | 7.13 | | | | 11/1/2022 | | | | 16,122,000 | | | | 12,416,503 | | | | 108,824 | |

| | | | | | | | | | | | | | | | | | | | |

Total Diversified/Conglomerate Service | | | | | | | | | | | 16,122,000 | | | | 12,416,503 | | | | 108,824 | |

| | | | | | | | | | | | | | | | | | | | |

|

Electronics — 6.53%*: | |

Solera LLC# | | | 10.50 | | | | 3/1/2024 | | | | 1,000,000 | | | | 1,050,224 | | | | 1,036,250 | |

Wesco Distribution Inc.^ | | | 7.13 | | | | 6/15/2025 | | | | 460,000 | | | | 460,000 | | | | 505,922 | |

Wesco Distribution Inc.^ | | | 7.25 | | | | 6/15/2028 | | | | 475,000 | | | | 471,409 | | | | 540,213 | |

Veritas Bermuda Ltd.^# | | | 10.50 | | | | 2/1/2024 | | | | 16,957,000 | | | | 15,176,123 | | | | 17,211,355 | |

Veritas Bermuda Ltd.^# | | | 7.50 | | | | 9/1/2025 | | | | 2,024,000 | | | | 2,024,000 | | | | 2,077,130 | |

Presidio Inc.^# | | | 8.25 | | | | 2/1/2028 | | | | 430,000 | | | | 430,000 | | | | 474,075 | |

| | | | | | | | | | | | | | | | | | | | |

Total Electronics | | | | | | | | | | | 21,346,000 | | | | 19,611,756 | | | | 21,844,945 | |

| | | | | | | | | | | | | | | | | | | | |

|

Finance — 5.26%*: | |

Alliance Data Systems Corp.^# | | | 7.00 | | | | 1/15/2026 | | | | 2,000,000 | | | | 1,992,500 | | | | 2,115,600 | |

Avolon Holdings^# | | | 6.50 | | | | 9/15/2024 | | | | 8,214,611 | | | | 6,396,566 | | | | 7,331,541 | |

Galaxy Bidco Ltd.+^# | | | 6.50 | | | | 7/31/2026 | | | | 1,850,000 | | | | 2,352,475 | | | | 2,638,968 | |

Garfunkelux Holdco+^ | | | 6.75 | | | | 11/1/2025 | | | | 450,000 | | | | 533,833 | | | | 563,483 | |

Travelex¤+^ | | | 12.50 | | | | 8/5/2025 | | | | 2,015,000 | | | | 2,275,272 | | | | 4,959,932 | |

Travelex¤+^# | | | 8.00 | | | | 5/15/2022 | | | | 4,600,000 | | | | 5,097,344 | | | | 0 | |

| | | | | | | | | | | | | | | | | | | | |

Total Finance | | | | | | | | | | | 19,129,611 | | | | 18,647,990 | | | | 17,609,524 | |

| | | | | | | | | | | | | | | | | | | | |

|

Healthcare, Education and Childcare — 7.20%*: | |

Advanz Pharma Corp.+ | | | 8.00 | | | | 9/6/2024 | | | | 3,743,000 | | | | 3,681,160 | | | | 3,780,430 | |

Bausch Health Companies Inc.^# | | | 9.00 | | | | 12/15/2025 | | | | 11,045,000 | | | | 11,260,894 | | | | 12,193,128 | |

Endo International^# | | | 7.50 | | | | 4/1/2027 | | | | 1,890,000 | | | | 1,890,000 | | | | 2,050,650 | |

Radiology Partners Inc.^# | | | 9.25 | | | | 2/1/2028 | | | | 2,586,000 | | | | 2,779,811 | | | | 2,902,785 | |

See accompanying Notes to the Financial Statements.

16

Barings Global Short Duration High Yield Fund 2020 Annual Report

SCHEDULE OF INVESTMENTS (CONTINUED)

December 31, 2020

| | | | | | | | | | | | | | | | | | | | |

| | | EFFECTIVE

INTEREST RATE ‡ | | | DUE DATE | | | PRINCIPAL | | | COST | | | FAIR

VALUE | |

Fixed Income (Continued) | |

| | | | | |

Corporate Bonds (Continued) | | | | | | | | | | | | | | | | | | | | |

|

Healthcare, Education and Childcare (Continued) | |

Verscend Technologies, Inc.^# | | | 9.75 | % | | | 8/15/2026 | | | | 2,915,000 | | | | $3,071,507 | | | | $3,159,131 | |

| | | | | | | | | | | | | | | | | | | | |

Total Healthcare, Education and Childcare | | | | | | | | | | | 22,179,000 | | | | 22,683,372 | | | | 24,086,124 | |

| | | | | | | | | | | | | | | | | | | | |

|

Home and Office Furnishings, Housewares, and Durable Consumer Products — 0.50%*: | |

Balta+^# | | | 7.75 | | | | 9/15/2022 | | | | 1,449,900 | | | | 1,607,043 | | | | 1,675,675 | |

| | | | | | | | | | | | | | | | | | | | |

Total Home and Office Furnishings, Housewares, and Durable Consumer Products | | | | | | | | | | | 1,449,900 | | | | 1,607,043 | | | | 1,675,675 | |

| | | | | | | | | | | | | | | | | | | | |

|

Hotels, Motels, Inns and Gaming — 1.71%*: | |

Boyne USA, Inc.^# | | | 7.25 | | | | 5/1/2025 | | | | 950,000 | | | | 950,000 | | | | 996,313 | |

Scientific Games International Inc.^# | | | 8.63 | | | | 7/1/2025 | | | | 4,325,000 | | | | 4,416,076 | | | | 4,735,875 | |

| | | | | | | | | | | | | | | | | | | | |

Total Hotels, Motels, Inns and Gaming | | | | | | | | | | | 5,275,000 | | | | 5,366,076 | | | | 5,732,188 | |

| | | | | | | | | | | | | | | | | | | | |

|

Insurance — 4.73%*: | |

Acrisure LLC^# | | | 10.13 | | | | 8/1/2026 | | | | 9,575,000 | | | | 9,751,551 | | | | 10,987,313 | |

Acrisure LLC^# | | | 8.13 | | | | 2/15/2024 | | | | 4,564,000 | | | | 4,666,248 | | | | 4,831,975 | |

| | | | | | | | | | | | | | | | | | | | |

Total Insurance | | | | | | | | | | | 14,139,000 | | | | 14,417,799 | | | | 15,819,288 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Leisure, Amusement, Entertainment — 2.77%*: | | | | | | | | | | | | | | | | | | | | |

Carnival Corp.^ | | | 7.63 | | | | 3/1/2026 | | | | 1,000,000 | | | | 1,185,944 | | | | 1,292,376 | |

Center Parcs+^ | | | 6.50 | | | | 8/28/2026 | | | | 900,000 | | | | 1,253,715 | | | | 1,278,407 | |

Eldorado Resorts^# | | | 8.13 | | | | 7/1/2027 | | | | 4,000,000 | | | | 3,894,336 | | | | 4,428,090 | |

Motion Finco+^ | | | 7.00 | | | | 5/15/2025 | | | | 1,750,000 | | | | 1,932,647 | | | | 2,250,113 | |

| | | | | | | | | | | | | | | | | | | | |

Total Leisure, Amusement, Entertainment | | | | | | | | | | | 7,650,000 | | | | 8,266,642 | | | | 9,248,986 | |

| | | | | | | | | | | | | | | | | | | | |

|

Machinery (Non-Agriculture, Non-Construct, Non-Electronic) — 4.38%*: | |

Apex Tool Group LLC^# | | | 9.00 | | | | 2/15/2023 | | | | 5,627,000 | | | | 5,480,980 | | | | 5,514,460 | |

Diebold Nixdorf Inc.^# | | | 9.38 | | | | 7/15/2025 | | | | 5,577,000 | | | | 5,945,474 | | | | 6,246,240 | |

Diebold Nixdorf Inc.^ | | | 9.00 | | | | 7/15/2025 | | | | 815,000 | | | | 959,187 | | | | 1,080,268 | |

Sarens+^# | | | 5.75 | | | | 2/21/2027 | | | | 1,625,000 | | | | 1,783,930 | | | | 1,826,395 | |

| | | | | | | | | | | | | | | | | | | | |

Total Machinery (Non-Agriculture, Non-Construct, Non-Electronic) | | | | | | | | | | | 13,644,000 | | | | 14,169,571 | | | | 14,667,363 | |

| | | | | | | | | | | | | | | | | | | | |

|

Mining, Steel, Iron and Non-Precious Metals — 14.58%*: | |

Cleveland-Cliffs Inc.^# | | | 9.88 | | | | 10/17/2025 | | | | 6,000,000 | | | | 6,571,847 | | | | 7,057,500 | |

Consol Energy Inc.^# | | | 11.00 | | | | 11/15/2025 | | | | 10,316,000 | | | | 10,684,566 | | | | 7,633,840 | |

First Quantum Minerals+^# | | | 7.25 | | | | 4/1/2023 | | | | 2,000,000 | | | | 1,945,342 | | | | 2,061,350 | |

First Quantum Minerals+^# | | | 7.50 | | | | 4/1/2025 | | | | 9,775,000 | | | | 9,426,389 | | | | 10,178,219 | |

First Quantum Minerals+^ | | | 6.88 | | | | 10/15/2027 | | | | 200,000 | | | | 200,000 | | | | 217,000 | |

Hecla Mining Company# | | | 7.25 | | | | 2/15/2028 | | | | 2,099,000 | | | | 2,277,548 | | | | 2,293,158 | |

International Wire Group Inc.^# | | | 10.75 | | | | 8/1/2021 | | | | 7,389,000 | | | | 7,299,397 | | | | 7,389,000 | |

Perenti Finance Pty Ltd+^# | | | 6.50 | | | | 10/7/2025 | | | | 2,500,000 | | | | 2,500,000 | | | | 2,659,454 | |

SunCoke Energy Inc.^# | | | 7.50 | | | | 6/15/2025 | | | | 5,743,000 | | | | 5,721,235 | | | | 5,701,076 | |

See accompanying Notes to the Financial Statements.

17

Barings Global Short Duration High Yield Fund 2020 Annual Report

SCHEDULE OF INVESTMENTS (CONTINUED)

December 31, 2020

| | | | | | | | | | | | | | | | | | | | |

| | | EFFECTIVE

INTEREST RATE ‡ | | | DUE DATE | | | PRINCIPAL | | | COST | | | FAIR

VALUE | |

Fixed Income (Continued) | |

| | | | | |

Corporate Bonds (Continued) | | | | | | | | | | | | | | | | | | | | |

|

Mining, Steel, Iron and Non-Precious Metals (Continued) | |

Warrior Met Coal Inc.^# | | | 8.00 | % | | | 11/1/2024 | | | | 3,513,000 | | | | $3,587,677 | | | | $3,592,043 | |

| | | | | | | | | | | | | | | | | | | | |

Total Mining, Steel, Iron and Non-Precious Metals | | | | | | | | | | | 49,535,000 | | | | 50,214,001 | | | | 48,782,640 | |

| | | | | | | | | | | | | | | | | | | | |

|

Oil and Gas — 16.05%*: | |

Antero Resources Corp.^ | | | 8.38 | | | | 7/15/2026 | | | | 451,000 | | | | 452,600 | | | | 460,331 | |

Blue Racer Midstream LLC^ | | | 7.63 | | | | 12/15/2025 | | | | 361,000 | | | | 361,000 | | | | 384,465 | |

Calumet Specialty Products^# | | | 11.00 | | | | 4/15/2025 | | | | 1,030,000 | | | | 1,062,129 | | | | 1,040,300 | |

Calumet Specialty Products^# | | | 9.25 | | | | 7/15/2024 | | | | 2,850,000 | | | | 2,747,985 | | | | 3,163,500 | |

CVR Energy Inc.^ | | | 5.75 | | | | 2/15/2028 | | | | 3,850,000 | | | | 3,304,616 | | | | 3,647,875 | |

Enlink Midstream Partners LP | | | 4.85 | | | | 7/15/2026 | | | | 200,000 | | | | 174,647 | | | | 195,268 | |

Enlink Midstream Partners LP | | | 4.40 | | | | 4/1/2024 | | | | 239,000 | | | | 218,459 | | | | 235,838 | |

Enlink Midstream Partners LP | | | 5.60 | | | | 4/1/2044 | | | | 5,413,000 | | | | 3,551,651 | | | | 4,343,923 | |

Genesis Energy LP# | | | 7.75 | | | | 2/1/2028 | | | | 3,408,000 | | | | 3,111,766 | | | | 3,263,160 | |

Harvest Midstream I L P^ | | | 7.50 | | | | 9/1/2028 | | | | 458,000 | | | | 458,000 | | | | 487,198 | |

Hilcorp Energy I L P^# | | | 6.25 | | | | 11/1/2028 | | | | 3,202,000 | | | | 2,779,140 | | | | 3,270,043 | |

KCA Deutag¤+^ | | | 9.88 | | | | 12/1/2025 | | | | 1,179,286 | | | | 1,179,286 | | | | 1,223,509 | |

Laredo Petroleum Inc. | | | 10.13 | | | | 1/15/2028 | | | | 3,765,000 | | | | 3,668,171 | | | | 3,200,250 | |

MEG Energy Corp.+^# | | | 7.13 | | | | 2/1/2027 | | | | 2,698,000 | | | | 2,522,071 | | | | 2,785,685 | |

Neptune Energy Bondco PLC^# | | | 6.63 | | | | 5/15/2025 | | | | 4,306,000 | | | | 3,908,745 | | | | 4,259,797 | |

Occidental Pete Corp.# | | | 8.50 | | | | 7/15/2027 | | | | 4,523,000 | | | | 4,573,184 | | | | 5,219,768 | |

Occidental Pete Corp.# | | | 7.88 | | | | 9/15/2031 | | | | 2,500,000 | | | | 2,659,015 | | | | 2,787,500 | |

Occidental Pete Corp. | | | 4.50 | | | | 7/15/2044 | | | | 586,000 | | | | 435,873 | | | | 496,635 | |

Ovintiv Inc. | | | 6.50 | | | | 8/15/2034 | | | | 500,000 | | | | 477,756 | | | | 579,020 | |

Ovintiv Inc.# | | | 6.50 | | | | 2/1/2038 | | | | 2,000,000 | | | | 1,836,522 | | | | 2,233,311 | |

PBF Holding Co LLC^ | | | 9.25 | | | | 5/15/2025 | | | | 1,196,000 | | | | 1,187,673 | | | | 1,179,136 | |

PBF Holding Co LLC | | | 6.00 | | | | 2/15/2028 | | | | 6,000,000 | | | | 4,937,032 | | | | 3,427,500 | |

Southwestern Energy Co. | | | 8.38 | | | | 9/15/2028 | | | | 449,000 | | | | 449,000 | | | | 487,165 | |

Welltec A/S+^# | | | 9.50 | | | | 12/1/2022 | | | | 5,713,000 | | | | 5,681,766 | | | | 5,313,090 | |

| | | | | | | | | | | | | | | | | | | | |

Total Oil and Gas | | | | | | | | | | | 56,877,286 | | | | 51,738,087 | | | | 53,684,267 | |

| | | | | | | | | | | | | | | | | | | | |

|

Personal Transportation — 1.15%*: | |

American Airlines^# | | | 11.75 | | | | 7/15/2025 | | | | 3,000,000 | | | | 2,970,000 | | | | 3,459,750 | |

Naviera Armas, 3M EURIBOR + 4.250%+^~ | | | 4.25 | | | | 11/15/2024 | | | | 150,000 | | | | 127,479 | | | | 81,893 | |

Naviera Armas, 3M EURIBOR + 6.500%+^~ | | | 6.50 | | | | 7/31/2023 | | | | 525,000 | | | | 608,346 | | | | 298,431 | |

| | | | | | | | | | | | | | | | | | | | |

Total Personal Transportation | | | | | | | | | | | 3,675,000 | | | | 3,705,825 | | | | 3,840,074 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Printing and Publishing — 1.79%*: | | | | | | | | | | | | | | | | | | | | |

Cimpress N.V.^# | | | 7.00 | | | | 6/15/2026 | | | | 2,069,000 | | | | 2,069,000 | | | | 2,175,036 | |

Houghton Mifflin Harcourt Publishers Inc.^# | | | 9.00 | | | | 2/15/2025 | | | | 3,000,000 | | | | 2,949,793 | | | | 3,052,500 | |

IPD 3 BV+^ | | | 5.50 | | | | 12/1/2025 | | | | 600,000 | | | | 712,682 | | | | 754,975 | |

| | | | | | | | | | | | | | | | | | | | |

Total Printing and Publishing | | | | | | | | | | | 5,669,000 | | | | 5,731,475 | | | | 5,982,511 | |

| | | | | | | | | | | | | | | | | | | | |

See accompanying Notes to the Financial Statements.

18

Barings Global Short Duration High Yield Fund 2020 Annual Report

SCHEDULE OF INVESTMENTS (CONTINUED)

December 31, 2020

| | | | | | | | | | | | | | | | | | | | |

| | | EFFECTIVE

INTEREST RATE ‡ | | | DUE DATE | | | PRINCIPAL | | | COST | | | FAIR

VALUE | |

Fixed Income (Continued) | |

| | | | | |

Corporate Bonds (Continued) | | | | | | | | | | | | | | | | | | | | |

|

Retail Store — 1.68%*: | |

At Home Holding III INC^# | | | 8.75 | % | | | 9/1/2025 | | | | 2,000,000 | | | | $2,102,700 | | | | $2,165,000 | |

Casino Guichard Perracho+^ | | | 6.63 | | | | 1/15/2026 | | | | 1,050,000 | | | | 1,279,474 | | | | 1,292,345 | |

Michaels Stores Inc.^# | | | 8.00 | | | | 7/15/2027 | | | | 2,000,000 | | | | 2,104,204 | | | | 2,150,000 | |

| | | | | | | | | | | | | | | | | | | | |

Total Retail Store | | | | | | | | | | | 5,050,000 | | | | 5,486,378 | | | | 5,607,345 | |

| | | | | | | | | | | | | | | | | | | | |

|

Telecommunications — 8.83%*: | |

Altice France Holding S.A.^# | | | 10.50 | | | | 5/15/2027 | | | | 2,000,000 | | | | 2,250,655 | | | | 2,245,000 | |

BMC Software^# | | | 9.75 | | | | 9/1/2026 | | | | 9,682,000 | | | | 9,553,038 | | | | 10,458,012 | |

Commscope Inc.^# | | | 8.25 | | | | 3/1/2027 | | | | 11,673,000 | | | | 11,690,192 | | | | 12,460,928 | |

Consolidated Communications^# | | | 6.50 | | | | 10/1/2028 | | | | 832,000 | | | | 832,000 | | | | 890,240 | |

Digicel Limited ¤+^# | | | 8.25 | | | | 9/30/2020 | | | | 2,500,000 | | | | 2,491,364 | | | | 0 | |

Northwest Fiber LLC^# | | | 10.75 | | | | 6/1/2028 | | | | 1,206,000 | | | | 1,332,158 | | | | 1,374,840 | |

Viasat^# | | | 6.50 | | | | 7/15/2028 | | | | 790,000 | | | | 790,000 | | | | 854,946 | |

Windstream Escrow LLC^# | | | 7.75 | | | | 8/15/2028 | | | | 1,251,000 | | | | 1,246,000 | | | | 1,259,757 | |

| | | | | | | | | | | | | | | | | | | | |

Total Telecommunications | | | | | | | | | | | 29,934,000 | | | | 30,185,407 | | | | 29,543,723 | |

| | | | | | | | | | | | | | | | | | | | |

|

Utilities — 1.34%*: | |

Techem+^# | | | 6.00 | | | | 7/30/2026 | | | | 3,500,000 | | | | 3,996,234 | | | | 4,479,275 | |

| | | | | | | | | | | | | | | | | | | | |

Total Utilities | | | | | | | | | | | 3,500,000 | | | | 3,996,234 | | | | 4,479,275 | |

| | | | | | | | | | | | | | | | | | | | |

Total Corporate Bonds | | | | | | | | | | | 393,957,469 | | | | 389,726,482 | | | | 387,088,063 | |

| | | | | | | | | | | | | | | | | | | | |

Total Fixed Income | | | | | | | | | | | 475,038,617 | | | | 464,347,610 | | | | 453,886,166 | |

| | | | | | | | | | | | | | | | | | | | |

Total Investments | | | | | | | | | | | 476,460,229 | | | | 478,817,979 | | | | 458,897,234 | |

| | | | | | | | | | | | | | | | | | | | |

| |

Other assets and liabilities — (37.16)% | | | | (124,321,130 | ) |

| | | | | | | | | | | | | | | | | | | | |

| |

Net Assets — 100% | | | | $334,576,104 | |

| | | | | | | | | | | | | | | | | | | | |

| ‡ | The effective interest rates are based on settled commitment amount. |

| * | Calculated as a percentage of net assets applicable to common shareholders. |

| ¤ | Value determined using significant unobservable inputs, security is categorized as Level 3. |

| ^ | Security exempt from registration under Rule 144a of the Securities Act of 1933. These securities may only be resold in transactions exempt from registration, normally to qualified institutional buyers. |

| ~ | Variable rate security. The interest rate shown is the rate in effect at December 31, 2020. |

| # | All or a portion of the security is segregated as collateral for the credit facility. |

| § | Bank loans are exempt from registration under the Securities Act of 1933, as amended, but contain certain restrictions on resale and cannot be sold publicly. These loans pay interest at rates which adjust periodically. The interest rates shown for bank loans are the current interest rates at December 31, 2020. Bank loans are also subject to mandatory and/or optional prepayment which cannot be predicted. As a result, the remaining maturity may be substantially less than the stated maturity shown. |

| & | Jupiter Resources Inc. common stock restructured into 276,778 shares of Tourmaline Oil Corp. common stock. The restructure was completed in February 2021. |

See accompanying Notes to the Financial Statements.

19

Barings Global Short Duration High Yield Fund 2020 Annual Report

SCHEDULE OF INVESTMENTS (CONTINUED)

December 31, 2020

Distributions of investments by country of risk. Percentage of assets are expressed by market value excluding cash and accrued income as of December 31, 2020.

| | | | | | |

| | United States | | | 82.9% | |

| | United Kingdom | | | 5.5% | |

| | Canada | | | 2.1% | |

| | Zambia | | | 2.7% | |

| | Germany | | | 1.3% | |

| | Denmark | | | 1.2% | |

| | France | | | 2.2% | |

| | Belgium | | | 0.8% | |

| | Australia | | | 0.6% | |

| | (Individually less than 1%) | | | 0.7% | |

| | | | | | |

| | | | | 100.0% | |

| | | | | | |

A summary of outstanding derivatives at December 31, 2020 is as follows:

Schedule of Open Forward Currency Contracts

December 31, 2020

| | | | | | | | | | | | | | | | | | | | | | | | |

CURRENCY TO BE

RECEIVED | | | | | CURRENCY TO BE

DELIVERED(1) | | | | | | COUNTERPARTY OF

CONTRACT | | | FORWARD

SETTLEMENT

DATE | | | UNREALIZED

APPRECIATION /

(DEPRECIATION) | |

| | 27,951,072 | | | USD | | | (23,011,893 | ) | | | EUR | | | | Morgan Stanley | | | | 1/14/2021 | | | $ | (171,678 | ) |

| | 11,755,825 | | | USD | | | (8,820,221 | ) | | | GBP | | | | Morgan Stanley | | | | 1/14/2021 | | | | (307,360 | ) |

| | 794,747 | | | USD | | | (591,998 | ) | | | GBP | | | | JP Morgan Chase | | | | 1/14/2021 | | | | (14,914 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | $ | (493,952 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

| (1) | Values are listed in U.S. dollars. |

See accompanying Notes to the Financial Statements.

20

Barings Global Short Duration High Yield Fund 2020 Annual Report

NOTES TO THE FINANCIAL STATEMENTS

December 31, 2020

Barings Global Short Duration High Yield Fund (the “Fund”) was organized as a business trust under the laws of the Commonwealth of Massachusetts on May 20, 2011, and commenced operations on October 26, 2012. The Fund is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as a de facto diversified, closed-end management investment company.

Barings LLC (the “Adviser”), a wholly-owned indirect subsidiary of Massachusetts Mutual Life Insurance Company, is a registered investment adviser under the Investment Advisers Act of 1940, as amended, and serves as investment adviser to the Fund.

Baring International Investment Limited (the “Sub-Adviser”), an indirect wholly-owned subsidiary of the Adviser, serves as sub-adviser with respect to the Fund’s European investments.

The Fund’s primary investment objective is to seek as high a level of current income as the Adviser determines is consistent with capital preservation. The Fund seeks capital appreciation as a secondary investment objective when consistent with its primary investment objective. There can be no assurance that the Fund will achieve its investment objectives. The Fund seeks to take advantage of inefficiencies between geographies, primarily the North American and Western European high yield bond and loan markets and within capital structures between bonds and loans. Under normal market conditions, the Fund will invest at least 80% of its Managed Assets in bonds, loans and other income-producing instruments that are, at the time of purchase, rated below investment grade (below Baa3 by Moody’s Investors Service, Inc. (“Moody’s”) or below BBB- by either Standard & Poor’s Global Ratings, a division of the McGraw-Hill Company, Inc. (“S&P”) or Fitch Ratings, Inc. (Fitch), or unrated but judged by the Adviser or Sub-Adviser to be of comparable quality).

| 2. | Significant Accounting Policies |

The Fund is an investment company and follows accounting and reporting guidance in Financial Accounting Standards Board (“FASB”) Accounting Standards Codification Topic 946. The following is a summary of significant accounting policies followed consistently by the Fund in the preparation of its financial statements in conformity with accounting principles generally accepted in the United States of America (“U.S. GAAP”).

| | A. | Valuation of Investments |

The Fund’s investments in fixed income securities are generally valued using the prices provided directly by independent third party services or provided directly from one or more broker dealers or market makers, each in accordance with the valuation policies and procedures approved by the Fund’s Board of Trustees (the “Board”).

The pricing services may use valuation models or matrix pricing, which consider yield or prices with respect to comparable bond quotations from bond dealers or by reference to other securities that are considered comparable in such characteristics as credit rating, interest rates and maturity date, to determine the current value. The closing prices of domestic or foreign securities may not reflect their market values at the time the Fund calculates its NAV if an event that materially affects the value of those securities has occurred since the closing prices were established on the domestic or foreign exchange market, but before the Fund’s NAV calculation. Under certain conditions, the Board has approved an independent pricing service to fair value foreign securities. This is generally accomplished by adjusting the closing price for movements in correlated indices, securities or derivatives. Fair value pricing may cause the value of the security on the books of the Fund to be different from the closing value on the non-U.S. exchange and may affect the calculation of the Fund’s NAV. The Fund may fair value securities in other situations, for example, when a particular foreign market is closed but the Fund is pricing their shares.

The Fund’s investments in bank loans are normally valued at the bid quotation obtained from dealers in loans by an independent pricing service in accordance with the Fund’s valuation policies and procedures approved by the Board.

Forward foreign exchange contracts are normally valued on the basis of independent pricing service providers.

A Valuation Committee, made up of officers of the Fund and employees of the Adviser, is responsible for determining, in accordance with the Fund’s valuation policies and procedures approved by the Board: (1) whether market quotations are readily available for investments held by the Fund; and (2) the fair value of investments held by the Fund for which market quotations are not readily available or are deemed not reliable by the Adviser. In certain cases, authorized pricing service vendors may not provide prices for a security held by the Fund, or the price provided by such

21

Barings Global Short Duration High Yield Fund 2020 Annual Report

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

December 31, 2020

pricing service vendor is deemed unreliable by the Adviser. In such cases, the Fund may use market maker quotations provided by an established market maker for that security (i.e. broker quotes) to value the security if the Adviser has experience obtaining quotations from the market maker and the Adviser determines that quotations obtained from the market maker in the past have generally been reliable (or, if the Adviser has no such experience with respect to a market maker, it determines based on other information available to it that quotations obtained by it from the market maker are reasonably likely to be reliable). In any such case, the Adviser will review any market quotations so obtained in light of other information in its possession for their general reliability.

Bank loans in which the Fund may invest have similar risks to lower-rated fixed income securities. Changes in the financial condition of the borrower or economic conditions or other circumstances may reduce the capacity of the borrower to make principal and interest payments on such instruments and may lead to defaults. Senior secured bank loans are supported by collateral; however, the value of the collateral may be insufficient to cover the amount owed to the Fund. By relying on a third party to administer a loan, the Fund is subject to the risk that the third party will fail to perform it obligations. The loans in which the Fund will invest are largely floating rate instruments; therefore, the interest rate risk generally is lower than for fixed-rate debt obligations. However, from the perspective of the borrower, an increase in interest rates may adversely affect the borrower’s financial condition. Due to the unique and customized nature of loan agreements evidencing loans and the private syndication thereof, loans are not as easily purchased or sold as publicly traded securities. Although the range of investors in loans has broadened in recent years, there can be no assurance that future levels of supply and demand in loan trading will provide the degree of liquidity which currently exists in the market. In addition, the terms of the loans may restrict their transferability without borrower consent. These factors may have an adverse effect on the market price and the Fund’s ability to dispose of particular portfolio investments. A less liquid secondary market also may make it more difficult for the Fund to obtain precise valuations of the high yield loans in its portfolio.

The Fund may invest in collateralized debt obligations (“CDOs”), which include collateralized bond obligations (“CBOs”) and collateralized loan obligations (“CLOs”).