Exhibit 99.10

May 20, 2013

Mr. Drew Cozby

Memorial Production Partners LP

1301 McKinney Street, Suite 2100

Houston, TX 77010

| | Re: | Memorial Production Partners LP |

Estimate of Reserves and Revenues

May 1, 2013 SEC Pricing Case

“As of” May 1, 2013

Dear Mr. Cozby:

At your request, we have estimated the future reserves and projected net revenues for certain property interests owned by Memorial Production Partners LP (MEMP). This report was prepared utilizing provided May 1, 2013 SEC pricing. The subject properties are located in Crockett, Loving, and Winkler Counties, Texas.

Our conclusions, as of May 1, 2013, are as follows:

| | | | | | | | | | | | | | | | | | | | |

| May 1, 2013 SEC Pricing Case | | Net to Memorial Production Partners LP | |

| | Proved Developed | | | Proved Undeveloped | | | Total Proved | | | Total Probable | |

| | Producing | | | Non-Producing | | | | |

Reserve Estimates | | | | | | | | | | | | | | | | | | | | |

Oil/Cond., Mobl | | | 1,112.9 | | | | 188.4 | | | | 2,418.1 | | | | 3,719.5 | | | | 3,518.1 | |

Gas, MMcf | | | 1,833.4 | | | | 177.8 | | | | 1,627.1 | | | | 3,638.3 | | | | 6,355.2 | |

Oil Equivalent, MBOE | | | 1,418.5 | | | | 218.0 | | | | 2,689.3 | | | | 4,325.9 | | | | 4,577.3 | |

| | | | | | |

Revenues | | | | | | | | | | | | | | | | | | | | |

Oil, $ (93.2) % | | | 94,514,080 | | | | 16,016,510 | | | | 204,933,250 | | | | 315,463,840 | | | | 298,045,770 | |

Gas, $ (4.4) % | | | 7,267,020 | | | | 674,430 | | | �� | 6,885,780 | | | | 14,827,230 | | | | 22,390,700 | |

Other, $ (2.4) % | | | 8,120,000 | | | | 0 | | | | 0 | | | | 8,120,000 | | | | 0 | |

Total, $ | | | 109,901,100 | | | | 16,690,940 | | | | 211,819,030 | | | | 338,411,070 | | | | 320,436,470 | |

| | | | | | |

Expenditures | | | | | | | | | | | | | | | | | | | | |

Ad Valorem Tax, $ | | | 2,900,210 | | | | 478,470 | | | | 6,121,290 | | | | 9,499,960 | | | | 9,560,140 | |

Severance Tax, $ | | | 4,671,900 | | | | 787,340 | | | | 9,943,360 | | | | 15,402,600 | | | | 15,389,410 | |

Direct Operating Expense, $ | | | 59,751,760 | | | | 5,964,070 | | | | 84,178,950 | | | | 149,894,780 | | | | 61,938,630 | |

Total, $ | | | 67,323,870 | | | | 7,229,880 | | | | 100,243,600 | | | | 174,797,340 | | | | 86,888,180 | |

| | | | | | |

Investments incl. Abandonment | | | | | | | | | | | | | | | | | | | | |

Abandonment, $ | | | 0 | | | | 0 | | | | 0 | | | | 0 | | | | 0 | |

Other, $ | | | 0 | | | | 1,841,040 | | | | 31,091,960 | | | | 32,933,000 | | | | 122,037,000 | |

Total, $ | | | 0 | | | | 1,841,040 | | | | 31,091,960 | | | | 32,933,000 | | | | 122,037,000 | |

| | | | | | |

Estimated Future Net Revenues (FNR) | | | | | | | | | | | | | | | | | | | | |

Undiscounted FNR, $ | | | 42,577,230 | | | | 7,620,020 | | | | 80,483,460 | | | | 130,680,710 | | | | 111,511,290 | |

FNR Disc. @ 10%, $ | | | 29,879,310 | | | | 4,457,780 | | | | 32,564,970 | | | | 66,902,060 | | | | 13,134,760 | |

| | | | | | |

Allocation Percentage by Classification | | | | | | | | | | | | | | | | | | | | |

FNR Disc. @ 10% | | | 44.7% | | | | 6.7% | | | | 48.7% | | | | 100.0% | | | | | |

*Due to computer rounding, numbers in the above table may not sum exactly.

Report Preparation

Purpose of Report – The purpose of this report is to provide MEMP with an estimate of future reserves and revenues attributable to certain interests owned by MEMP. These properties are located in Crockett, Loving, and Winkler counties of Texas.

Scope of Work – W.D. Von Gonten & Co. was engaged by MEMP to estimate the future reserves and revenues associated with the properties included in this report.

Reporting Requirements – The Society of Petroleum Engineers (SPE) requires Proved reserves to be economically recoverable with prices and costs in effect on the “as of” date of the report. In conjunction with the World Petroleum Council (WPC), American Association of Petroleum Geologists (AAPG), and the Society of Petroleum Evaluation Engineers (SPEE), the SPE has issuedPetroleum Resources Management System(2007 ed.), which sets forth the definitions and requirements associated with the classification of both reserves and resources. In addition, the SPE has issuedStandards Pertaining to the Estimating and Auditing of Oil and Gas Reserve Information,which sets requirements for the qualifications and independence of reserve estimators and auditors.

The estimated Proved reserves herein have been prepared in conformance with all SPE, WPC, AAPG and SPEE definitions and requirements.

Projections – The attached reserve and revenue projections are on a calendar year basis with the first time period being May 1, 2013 through December 31, 2013.

Property Discussion

The Dimmit field, located in Loving County, Texas, comprises approximately 44% of the producing value. MEMP currently operates approximately 36 wells which are completed in the Ramsey and Cherry Canyon Sands within the Delaware Consolidated reservoir. The current gross rates are approximately 190 barrels of oil and 800 Mcf of gas per day from the 10 leases.

The assets with the second highest value are the Ida Hendrick and Hendrick M leases located in Winkler County, Texas. They comprise 38% of the producing value. MEMP operates eleven wells which produce from the Yates and Seven Rivers reservoirs. The eleven wells produce approximately 420 barrels of oil per day and 160 Mcf of gas per day on a gross basis.

The remaining producing value is comprised of properties found in the Shannon lease which is located in the Elkhorn field in Crockett County, Texas. The current production from the 11 producing wells comes from the Canyon, Ellenburger, and Wolfcamp formations. The current gross volumes are approximately 200 barrels of oil and 300 Mcf of gas per day.

The Probable Undeveloped reserves consist of 2 Ramsey locations in Dimmit field and 16 locations on the Shannon lease in Elkhorn field. The Shannon wells are horizontally targeting the Wolfcamp A bench with the first location scheduled to begin production in early 2016.

Reserve Estimates

Proved Developed Producing - Reserve estimates for the producing properties were based on decline curve analysis, volumetric calculations and/or analogy to nearby production.

Proved Behind Pipe & Undeveloped - The Proved Behind Pipe and Proved Undeveloped reserves were necessarily estimated using volumetric calculations, and/or analogy to nearby production.

Probable Undeveloped - The Probable Undeveloped reserves were necessarily estimated using volumetric calculations, log analysis, core analysis, geophysical interpretation and reservoir simulation. In addition, W.D. Von Gonten & Co. has performed a field study of the Wolfcamp shale play independent of this report. Our conclusions from that field study have fortified our confidence in the undeveloped reserves included herein. W.D. Von Gonten & Co. has developed a methodology for

MEMP Energy, LLC – May 20, 2013 – Page 2

evaluating the resource and reserve potential for shale plays which is unique to the industry. The ultimate goal of the evaluation is to assess reserves volumetrically and with numerical reservoir simulation. The results are then verified using decline curve analysis of historical production data. This methodology is a common practice with conventional reservoirs, but mostly non-existent in the realm of unconventional reservoirs, including the Wolfcamp shale.

Reserves and schedules of production included in this report are only estimates. The amount of available data, reservoir and geological complexity, reservoir drive mechanism, and mechanical aspects can have a material effect on the accuracy of these reserve estimates. Due to inherent uncertainties in future production rates, commodity prices, and geologic conditions, it should be realized that the reserve estimates, the reserves actually recovered, the revenue derived therefrom and the actual cost incurred could be more or less than the estimated amounts.

We consider the assumptions, data, methods, and procedures used in this report appropriate hereof, and we have used all such methods and procedures that we consider necessary and appropriate to prepare the estimates of reserves and future net revenues.

Product Prices

The estimated revenues shown herein were based on SEC May 1, 2013 pricing guidelines. SEC pricing is determined by averaging the first day of each month’s closing price for the previous calendar year using published benchmark oil and gas prices. This method renders a price of $92.13 per barrel of oil and $3.12 per MMBtu of gas.

Pricing differentials were applied to all properties on an individual property basis in order to reflect prices actually received at the wellhead. Pricing differentials are normally utilized to account for transportation charges, geographical differentials, quality adjustments, and any marketing bonus or deduction. The differentials utilized herein were determined from lease operating data provided by MEMP covering a period of March 2012 through February 2013.

Operating and Capital Cost

Monthly operating expenses for each well were derived from the average historical costs derived from the profit and loss statements provided by MEMP.

The average historical costs were calculated using the 12 month period of March 1, 2012 through February 28, 2013.

Operating costs were adjusted for nonrecurring costs where applicable.

Capital costs related to drilling, completion, and recompletion operations were supplied by MEMP. These costs were estimated from recent work in the areas of interest or any current AFEs made available. W.D. Von Gonten & Co. only reviewed the provided estimates for reasonableness.

At the request of MEMP, revenues associated with income from the Dimmitt Field Salt Water Disposal System have been included in the report as “Other Revenues.” The projection was provided from MEMP and based upon recent income from the system. W.D. Von Gonten & Co. expresses no warranties as to the accuracy or reasonableness of this assumption.

Operating and capital costs were held flat for the life of the properties.

Other Considerations

Abandonment Costs – Cost estimates regarding future plugging and abandonment procedures associated with these properties were NOT supplied by MEMP for the purposes of this report. At MEMP’s request, we have assumed the “rule of thumb” that the costs necessary to abandon the properties are equal to the salvage value of the surface and subsurface equipment. As we have not

MEMP Energy, LLC – May 20, 2013 – Page 3

inspected the properties personally, W.D. Von Gonten & Co. expresses no warranties as to the accuracy or reasonableness of this assumption. A third party study would be necessary in order to accurately estimate all future abandonment liabilities.

Additional Costs – Costs were not deducted for general and administrative expenses, depletion, depreciation and/or amortization (a non-cash item), or federal income tax.

Data Sources – Data furnished by MEMP included basic well information, operating costs, ownership, and production information on certain leases. The remaining production histories were taken from Dwight’s Energy data archives.

Context – We specifically advise that any particular reserve estimate for a specific property not be used out of context with the overall report.The revenues and present worth of future net revenues are not represented to be market value either for individual properties or on a total property basis. The estimation of fair market value for oil and gas properties requires additional analysis other than evaluating undiscounted and discounted future net revenues.

While the oil and gas industry may be subject to regulatory changes from time to time that could affect an industry participant’s ability to recover its oil and gas reserves, we are not aware of any such governmental actions which would restrict the recovery of the May 1, 2013 estimated oil and gas volumes. The reserves in this report can be produced under current regulatory guidelines. Actual future commodity prices may differ substantially from the utilized pricing scenario which may or may not extend or limit the estimated reserve and revenue quantities presented in this report.

We have not inspected the properties included in this report, nor have we conducted independent well tests. W.D. Von Gonten & Co. and our employees have no direct ownership in any of the properties included in this report. Our fees are based on hourly expenses and are not related to the reserve and revenue estimates produced in this report.

Thank you for the opportunity to assist Memorial Production Partners LP with this project.

| | | | |

| |  | | Respectfully submitted,

Phillip R. Hunter, P.E. TX# 96590

Jason P. Warren |

| | |

| | |

| | |

| | |

MEMP Energy, LLC – May 20, 2013 – Page 4

PETROLEUM RESERVES AND RESOURCES CLASSIFICATION AND DEFINITIONS

This document contains information excerpted from definitions and guidelines prepared by the Oil and Gas Reserves Committee of the Society of Petroleum Engineers (SPE) and reviewed and jointly sponsored by the World Petroleum Council (WPC), the American Association of Petroleum Geologists (AAPG), and the Society of Petroleum Evaluation Engineers (SPEE).

Preamble

Petroleum resources are the estimated quantities of hydrocarbons naturally occurring on or within the Earth’s crust. Resource assessments estimate total quantities in known and yet-to-be discovered accumulations; resources evaluations are focused on those quantities that can potentially be recovered and marketed by commercial projects. A petroleum resources management system provides a consistent approach to estimating petroleum quantities, evaluating development projects, and presenting results within a comprehensive classification framework.

These definitions and guidelines are designed to provide a common reference for the international petroleum industry, including national reporting and regulatory disclosure agencies, and to support petroleum project and portfolio management requirements. They are intended to improve clarity in global communications regarding petroleum resources. It is expected that this document will be supplemented with industry education programs and application guides addressing their implementation in a wide spectrum of technical and/or commercial settings.

It is understood that these definitions and guidelines allow flexibility for users and agencies to tailor application for their particular needs; however, any modifications to the guidance contained herein should be clearly identified. The definitions and guidelines contained in this document must not be construed as modifying the interpretation or application of any existing regulatory reporting requirements.

1.0 Basic Principles and Definitions

The estimation of petroleum resource quantities involves the interpretation of volumes and values that have an inherent degree of uncertainty. These quantities are associated with development projects at various stages of design and implementation. Use of a consistent classification system enhances comparisons between projects, groups of projects, and total company portfolios according to forecast production profiles and recoveries. Such a system must consider both technical and commercial factors that impact the project’s economic feasibility, its productive life, and its related cash flows.

1.1 Petroleum Resources Classification Framework

Petroleum is defined as a naturally occurring mixture consisting of hydrocarbons in the gaseous, liquid, or solid phase. Petroleum may also contain non-hydrocarbons, common examples of which are carbon dioxide, nitrogen, hydrogen sulfide and sulfur. In rare cases, non-hydrocarbon content could be greater than 50%.

The term “resources” as used herein is intended to encompass all quantities of petroleum naturally occurring on or within the Earth’s crust, discovered and undiscovered (recoverable and unrecoverable), plus those quantities already produced. Further, it includes all types of petroleum whether currently considered “conventional” or “unconventional.”

Excerpted from the Petroleum Resources Management System Approved by the

Society of Petroleum Engineers (SPE) Board of Directors, March 2007

Page 1

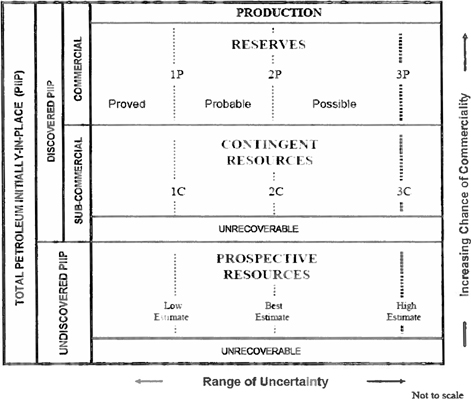

Figure 1-1 is a graphical representation of the SPE/WPC/AAPG/SPEE resources classification system. The system defines the major recoverable resources classes: Production, Reserves, Contingent Resources, and Prospective Resources, as well as Unrecoverable petroleum.

Figure 1-1: Resources Classification Framework.

The “Range of Uncertainty” reflects a range of estimated quantities potentially recoverable from an accumulation by a project, while the vertical axis represents the “Chance of Commerciality, that is, the chance that the project that will be developed and reach commercial producing status.

The following pages contain the definitions in Tables 1, 2, and 3 that display the major classes and sub-classes of petroleum reserves and resources as defined by the SPE:

Excerpted from the Petroleum Resources Management System Approved by the

Society of Petroleum Engineers (SPE) Board of Directors, March 2007

Page 2

Table 1: Recoverable Resources Classes and Sub-Classes

| | | | |

Class/Sub-Class | | Definition | | Guidelines |

| Reserves | | Reserves are those quantities of petroleum anticipated to be commercially recoverable by application of development projects to known accumulations from a given date forward under defined conditions. | | Reserves must satisfy four criteria: they must be discovered, recoverable, commercial, and remaining based on the development project(s) applied. Reserves are further subdivided in accordance with the level of certainty associated with the estimates and may be sub-classified based on project maturity and/or characterized by their development and production status. To be included in the Reserves class, a project must be sufficiently defined to establish its commercial viability. There must be a reasonable expectation that all required internal and external approvals will be forthcoming, and there is evidence of firm intention to proceed with development within a reasonable time frame. A reasonable time frame for the initiation of development depends on the specific circumstances and varies according to the scope of the project. While 5 years is recommended as a benchmark, a longer time frame could be applied where, for example, development of economic projects are deferred at the option of the producer for, among other things, market-related reasons, or to meet contractual or strategic objectives. In all cases, the justification for classification as Reserves should be clearly documented. To be included in the Reserves class, there must be a high confidence in the commercial producibility of the reservoir as supported by actual production or formation tests. In certain cases, Reserves may be assigned on the basis of well logs and/or core analysis that indicate that the subject reservoir is hydrocarbon-bearing and is analogous to reservoirs in the same area that are producing or have demonstrated the ability to produce on formation tests. |

| On Production | | The development project is currently producing and selling petroleum to market. | | The key criterion is that the project is receiving income from sales, rather than the approved development project necessarily being complete. This is the point at which the project “chance of commerciality” can be said to be 100%. The project “decision gate” is the decision to initiate commercial production from the project. |

| Approved for Development | | All necessary approvals have been obtained, capital funds have been committed, and implementation of the development project is under way. | | At this point, it must be certain that the development project is going ahead. The project must not be subject to any contingencies such as outstanding regulatory approvals or sales contracts. Forecast capital expenditures should be included in the reporting entity’s current or following year’s approved budget. The project “decision gate” is the decision to start investing capital in the construction of production facilities and/or drilling development wells. |

Excerpted from the Petroleum Resources Management System Approved by the

Society of Petroleum Engineers (SPE) Board of Directors, March 2007

Page 3

| | | | |

Class/Sub-Class | | Definition | | Guidelines |

| Justified for Development | | Implementation of the development project is justified on the basis of reasonable forecast commercial conditions at the time of reporting, and there are reasonable expectations that all necessary approvals/contracts will be obtained. | | In order to move to this level of project maturity, and hence have reserves associated with it, the development project must be commercially viable at the time of reporting, based on the reporting entity’s assumptions of future prices, costs, etc. (“forecast case”) and the specific circumstances of the project. Evidence of a firm intention to proceed with development within a reasonable time frame will be sufficient to demonstrate commerciality. There should be a development plan in sufficient detail to support the assessment of commerciality and a reasonable expectation that any regulatory approvals or sales contracts required prior to project implementation will be forthcoming. Other than such approvals/contracts, there should be no known contingencies that could preclude the development from proceeding within a reasonable timeframe (see Reserves class). The project “decision gate” is the decision by the reporting entity and its partners, if any, that the project has reached a level of technical and commercial maturity sufficient to justify proceeding with development at that point in time. |

| Contingent Resources | | Those quantities of petroleum estimated, as of a given date, to be potentially recoverable from known accumulations by application of development projects, but which are not currently considered to be commercially recoverable due to one or more contingencies. | | Contingent Resources may include, for example, projects for which there are currently no viable markets, or where commercial recovery is dependent on technology under development, or where evaluation of the accumulation is insufficient to clearly assess commerciality. Contingent Resources are further categorized in accordance with the level of certainty associated with the estimates and may be sub-classified based on project maturity and/or characterized by their economic status. |

| Development Pending | | A discovered accumulation where project activities are ongoing to justify commercial development in the foreseeable future. | | The project is seen to have reasonable potential for eventual commercial development, to the extent that further data acquisition (e.g. drilling, seismic data) and/or evaluations are currently ongoing with a view to confirming that the project is commercially viable and providing the basis for selection of an appropriate development plan. The critical contingencies have been identified and are reasonably expected to be resolved within a reasonable time frame. Note that disappointing appraisal/evaluation results could lead to a re-classification of the project to “On Hold” or “Not Viable” status. The project “decision gate” is the decision to undertake further data acquisition and/or studies designed to move the project to a level of technical and commercial maturity at which a decision can be made to proceed with development and production. |

Excerpted from the Petroleum Resources Management System Approved by the

Society of Petroleum Engineers (SPE) Board of Directors, March 2007

Page 4

| | | | |

Class/Sub-Class | | Definition | | Guidelines |

| | | | | |

| Development Unclarified or on Hold | | A discovered accumulation where project activities are on hold and/or where justification as a commercial development may be subject to significant delay. | | The project is seen to have potential for eventual commercial development, but further appraisal/evaluation activities are on hold pending the removal of significant contingencies external to the project, or substantial further appraisal/evaluation activities are required to clarify the potential for eventual commercial development. Development may be subject to a significant time delay. Note that a change in circumstances, such that there is no longer a reasonable expectation that a critical contingency can be removed in the foreseeable future, for example, could lead to a re-classification of the project to “Not Viable” status. The project “decision gate” is the decision to either proceed with additional evaluation designed to clarify the potential for eventual commercial development or to temporarily suspend or delay further activities pending resolution of external contingencies. |

| Development Not Viable | | A discovered accumulation for which there are no current plans to develop or to acquire additional data at the time due to limited production potential. | | The project is not seen to have potential for eventual commercial development at the time of reporting, but the theoretically recoverable quantities are recorded so that the potential opportunity will be recognized in the event of a major change in technology or commercial conditions. The project “decision gate” is the decision not to undertake any further data acquisition or studies on the project for the foreseeable future. |

| Prospective Resources | | Those quantities of petroleum which are estimated, as of a given date, to be potentially recoverable from undiscovered accumulations. | | Potential accumulations are evaluated according to their chance of discovery and, assuming a discovery, the estimated quantities that would be recoverable under defined development projects. It is recognized that the development programs will be of significantly less detail and depend more heavily on analog developments in the earlier phases of exploration. |

| Prospect | | A project associated with a potential accumulation that is sufficiently well defined to represent a viable drilling target. | | Project activities are focused on assessing the chance of discovery and, assuming discovery, the range of potential recoverable quantities under a commercial development program. |

| Lead | | A project associated with a potential accumulation that is currently poorly defined and requires more data acquisition and/or evaluation in order to be classified as a prospect. | | Project activities are focused on acquiring additional data and/or undertaking further evaluation designed to confirm whether or not the lead can be matured into a prospect. Such evaluation includes the assessment of the chance of discovery and, assuming discovery, the range of potential recovery under feasible development scenarios. |

| Play | | A project associated with a prospective trend of potential prospects, but which requires more data acquisition and/or evaluation in order to define specific leads or prospects. | | Project activities are focused on acquiring additional data and/or undertaking further evaluation designed to define specific leads or prospects for more detailed analysis of their chance of discovery and, assuming discovery, the range of potential recovery under hypothetical development scenarios. |

Excerpted from the Petroleum Resources Management System Approved by the

Society of Petroleum Engineers (SPE) Board of Directors, March 2007

Page 5

Table 2: Reserves Status Definitions and Guidelines

| | | | |

Status | | Definition | | Guidelines |

| Developed Reserves | | Developed Reserves are expected quantities to be recovered from existing wells and facilities. | | Reserves are considered developed only after the necessary equipment has been installed, or when the costs to do so are relatively minor compared to the cost of a well. Where required facilities become unavailable, it may be necessary to reclassify Developed Reserves as Undeveloped. Developed Reserves may be further sub-classified as Producing or Non-Producing. |

| Developed Producing Reserves | | Developed Producing Reserves are expected to be recovered from completion intervals that are open and producing at the time of the estimate. | | Improved recovery reserves are considered producing only after the improved recovery project is in operation. |

| Developed Non-Producing Reserves | | Developed Non-Producing Reserves include shut-in and behind-pipe Reserves. | | Shut-in Reserves are expected to be recovered from (1) completion intervals which are open at the time of the estimate but which have not yet started producing, (2) wells which were shut-in for market conditions or pipeline connections, or (3) wells not capable of production for mechanical reasons. Behind-pipe Reserves are expected to be recovered from zones in existing wells which will require additional completion work or future re-completion prior to start of production. In all cases, production can be initiated or restored with relatively low expenditure compared to the cost of drilling a new well. |

| Undeveloped Reserves | | Undeveloped Reserves are quantities expected to be recovered through future investments: | | (1) from new wells on undrilled acreage in known accumulations, (2) from deepening existing wells to a different (but known) reservoir, (3) from infill wells that will increase recovery, or (4) where a relatively large expenditure (e.g. when compared to the cost of drilling a new well) is required to (a) recomplete an existing well or (b) install production or transportation facilities for primary or improved recovery projects. |

Excerpted from the Petroleum Resources Management System Approved by the

Society of Petroleum Engineers (SPE) Board of Directors, March 2007

Page 6

Table 3: Reserves Category Definitions and Guidelines

| | | | |

Category | | Definition | | Guidelines |

Proved Reserves | | Proved Reserves are those quantities of petroleum, which by analysis of geoscience and engineering data, can be estimated with reasonable certainty to be commercially recoverable, from a given date forward, from known reservoirs and under defined economic conditions, operating methods, and government regulations. | | If deterministic methods are used, the term reasonable certainty is intended to express a high degree of confidence that the quantities will be recovered. If probabilistic methods are used, there should be at least a 90% probability that the quantities actually recovered will equal or exceed the estimate. The area of the reservoir considered as Proved includes (1) the area delineated by drilling and defined by fluid contacts, if any, and (2) adjacent undrilled portions of the reservoir that can reasonably be judged as continuous with it and commercially productive on the basis of available geoscience and engineering data. In the absence of data on fluid contacts, Proved quantities in a reservoir are limited by the lowest known hydrocarbon (LKH) as seen in a well penetration unless otherwise indicated by definitive geoscience, engineering, or performance data. Such definitive information may include pressure gradient analysis and seismic indicators. Seismic data alone may not be sufficient to define fluid contacts for Proved reserves (see “2001 Supplemental Guidelines,” Chapter 8). Reserves in undeveloped locations may be classified as Proved provided that: •The locations are in undrilled areas of the reservoir that can be judged with reasonable certainty to be commercially productive. • Interpretations of available geoscience and engineering data indicate with reasonable certainty that the objective formation is laterally continuous with drilled Proved locations. For Proved Reserves, the recovery efficiency applied to these reservoirs should be defined based on a range of possibilities supported by analogs and sound engineering judgment considering the characteristics of the Proved area and the applied development program. |

| Probable Reserves | | Probable Reserves are those additional Reserves which analysis of geoscience and engineering data indicate are less likely to be recovered than Proved Reserves but more certain to be recovered than Possible Reserves. | | It is equally likely that actual remaining quantities recovered will be greater than or less than the sum of the estimated Proved plus Probable Reserves (2P). In this context, when probabilistic methods are used, there should be at least a 50% probability that the actual quantities recovered will equal or exceed the 2P estimate. Probable Reserves may be assigned to areas of a reservoir adjacent to Proved where data control or interpretations of available data are less certain. The interpreted reservoir continuity may not meet the reasonable certainty criteria. Probable estimates also include incremental recoveries associated with project recovery efficiencies beyond that assumed for Proved. |

Excerpted from the Petroleum Resources Management System Approved by the

Society of Petroleum Engineers (SPE) Board of Directors, March 2007

Page 7

| | | | |

Category | | Definition | | Guidelines |

Possible Reserves | | Possible Reserves are those additional reserves which analysis of geoscience and engineering data indicate are less likely to be recoverable than Probable Reserves. | | The total quantities ultimately recovered from the project have a low probability to exceed the sum of Proved plus Probable plus Possible (3P), which is equivalent to the high estimate scenario. When probabilistic methods are used, there should be at least a 10% probability that the actual quantities recovered will equal or exceed the 3P estimate. Possible Reserves may be assigned to areas of a reservoir adjacent to Probable where data control and interpretations of available data are progressively less certain. Frequently, this may be in areas where geoscience and engineering data are unable to clearly define the area and vertical reservoir limits of commercial production from the reservoir by a defined project. Possible estimates also include incremental quantities associated with project recovery efficiencies beyond that assumed for Probable. |

Probable and Possible Reserves | | (See above for separate criteria for Probable Reserves and Possible Reserves.) | | The 2P and 3P estimates may be based on reasonable alternative technical and commercial interpretations within the reservoir and/or subject project that are clearly documented, including comparisons to results in successful similar projects. In conventional accumulations, Probable and/or Possible Reserves may be assigned where geoscience and engineering data identify directly adjacent portions of a reservoir within the same accumulation that may be separated from Proved areas by minor faulting or other geological discontinuities and have not been penetrated by a wellbore but are interpreted to be in communication with the known (Proved) reservoir. Probable or Possible Reserves may be assigned to areas that are structurally higher than the Proved area. Possible (and in some cases, Probable) Reserves may be assigned to areas that are structurally lower than the adjacent Proved or 2P area. Caution should be exercised in assigning Reserves to adjacent reservoirs isolated by major, potentially sealing, faults until this reservoir is penetrated and evaluated as commercially productive. Justification for assigning Reserves in such cases should be clearly documented. Reserves should not be assigned to areas that are clearly separated from a known accumulation by non-productive reservoir (i.e., absence of reservoir, structurally low reservoir, or negative test results); such areas may contain Prospective Resources. In conventional accumulations, where drilling has defined a highest known oil (HKO) elevation and there exists the potential for an associated gas cap, Proved oil Reserves should only be assigned in the structurally higher portions of the reservoir if there is reasonable certainty that such portions are initially above bubble point pressure based on documented engineering analyses. Reservoir portions that do not meet this certainty may be assigned as Probable and Possible oil and/or gas based on reservoir fluid properties and pressure gradient interpretations. |

Excerpted from the Petroleum Resources Management System Approved by the

Society of Petroleum Engineers (SPE) Board of Directors, March 2007

Page 8