Filed Pursuant to Rule 424(b)(3)

Securities Act File No. 333-274497

File No. 814-00908

Prospectus

Prospect Floating Rate and Alternative Income Fund, Inc.

Class S, Class D and Class I Shares of Common Stock

Maximum Offering of $300,000,000

Prospect Floating Rate and Alternative Income Fund, Inc. (“we,” “us,” “our,” the “Fund” or the “Company”) is an externally managed, non-diversified, closed-end management investment company, organized as a Maryland corporation, that has elected to be regulated as a business development company (“BDC”) under the Investment Company Act of 1940, as amended (the “1940 Act“). We have elected, and intend to qualify annually, to be taxed for U.S. federal income tax purposes as a regulated investment company (“RIC”) under Subchapter M of the Internal Revenue Code of 1986, as amended (the “Code”).

Our investment objective is to generate current income and, as a secondary objective, capital appreciation by targeting investment opportunities with favorable risk-adjusted returns. Under normal market conditions, we will invest at least 80% of our net assets (plus any borrowings for investment purposes) in floating rate loans and other income producing investments. We intend to meet our investment objective by primarily lending to and investing in the debt of privately-owned U.S. middle market companies, which we define as companies with annual revenue between $50 million and $2.5 billion. We may on occasion invest in smaller or larger companies if an attractive opportunity presents itself, especially when there are dislocations in the capital markets. We expect that at least 70% of our portfolio of investments will consist primarily of directly originated or syndicated senior secured first lien loans, directly originated or syndicated senior secured second lien loans, and to a lesser extent, subordinated debt of middle market companies in a broad range of industries. Syndicated secured loans refer to commercial loans provided by a group of lenders that are structured, arranged, and administered by one or several commercial or investment banks, known as arrangers. These loans are then sold (or syndicated) to other banks or institutional investors. Syndicated secured loans may have a first priority lien on a borrower’s assets (i.e., senior secured first lien loans), a second priority lien on a borrower’s assets (i.e., senior secured second lien loans), or a lower lien or unsecured position on the borrower’s assets (i.e., subordinated debt). We expect that up to 30% of our portfolio of investments will consist of other securities, including private equity (both common and preferred), dividend-paying equity, royalties, and the equity and junior debt tranches of a type of pools of broadly syndicated loans known as collateralized loan obligations, or CLOs, which we referred to as “Subordinated Structured Notes” or “SSNs”. The senior secured loans underlying our SSN investments are expected typically to be BB or B rated (non-investment grade, which is often referred to as “high yield” or “junk”) and in limited circumstances, unrated, senior secured loans. Our investment portfolio is expected to consist primarily of debt securities. Our target credit investments are expected to typically have initial maturities between three and ten years and generally range in size between $1 million and $100 million, although the investment size may vary with the size of our capital base. We expect that the majority of our debt investments will bear interest at floating interest rates, but our portfolio may also include fixed-rate investments. We expect to make our investments directly through the primary issuance by the borrower or in the secondary market. “Risk-adjusted returns” refers to a measure of investment return per unit of risk and provides a framework to compare and evaluate investment opportunities with differing risk/return profiles. The term “risk-adjusted returns” does not imply that we employ low-risk strategies or that an investment should be considered a low-risk or no risk investment.

We are offering on a continuous basis up to $300,000,000 in any combination of amount of shares of Class S, Class D and Class I common stock (collectively, the “Common Stock”). The share classes have different ongoing shareholder servicing and/or distribution fees. The purchase price per share for each class of Common Stock sold in this offering will equal our net asset value (“NAV”) per share, as of the effective date of the monthly share purchase

date. This is a “best efforts” offering, which means that Preferred Capital Securities, LLC (the “Dealer Manager”), will use its best efforts to sell Common Stock in this offering, but is not obligated to purchase or sell any specific amount of shares in this offering.

Investing in our Common Stock may be considered speculative and involves a high degree of risk. You should purchase our Common Stock only if you can afford the complete loss of your investment. See “Risk Factors” beginning on page 31 of this prospectus. Also consider the following:

•Our shares are not listed on any exchange and you should not expect to be able to resell your shares. See "Risk Factors-Risks Related to this Offering and Our Common Stock" and "Non-Exchange Traded BDC."

•If you are able to sell your shares, you likely will receive less than your purchase price.

•We do not intend to list our shares on any securities exchange and we do not expect a secondary market in our shares to develop.

•Because you will be unable to sell your shares, you will be unable to reduce your exposure in any market downturn.

•We have not identified any specific investments that we will make with the proceeds of this offering and you will not have the opportunity to evaluate our future investments prior to purchasing shares of our Common Stock. As a result, our offering may be considered a “blind pool” offering.

•An investment in our shares is not suitable for all investors, particularly investors who require short or medium-term liquidity.

•We have implemented a share repurchase program, but only a limited number of shares, if any, will be eligible for repurchase. In addition, any such repurchases will be at the NAV per share of the Company, except that the Company deducts 2.00% from such NAV for shares that have not been outstanding for at least one year. Such share repurchase prices may be lower than the price you paid for your shares in this offering. Our board of directors may amend, suspend or terminate the share repurchase program at any time and there can be no assurance that any shares will be repurchased under the share repurchase program. For more information regarding the limitations in respect of the proposed share repurchase program, see “Share Repurchase Program.”

•A substantial portion of our distributions, if any, may result from expense waivers from our Adviser, which are subject to repayment by us, and may also consist, in whole or in part, of a return of capital. In addition, we may fund our cash distributions to stockholders from any sources of funds legally available to us, including offering proceeds and borrowings. If we borrow money to fund distributions, the costs of such borrowings will be borne by us and, indirectly, by our stockholders. You should understand that any such distributions are not based on our investment performance, and can only be sustained if we achieve positive investment performance in future periods and/or our Adviser continues to make such expense waivers. You should also understand that our future repayments may reduce the distributions that you would otherwise receive.

•The Senior Secured Revolving Credit Facility (as defined below) exposes us to certain risks, including market risk, liquidity risk and other risks similar to those associated with the use of leverage. See "Prospectus Summary-Credit Facility" and "Risks Related to Debt Financing."

•We expect to use leverage, including through the Senior Secured Revolving Credit Facility, which will magnify the potential for loss on amounts invested in us. See "Prospectus Summary-Credit Facility" and "Risks Related to Debt Financing."

•Investors in our Class S and Class D shares will be subject to ongoing shareholder servicing and/or distribution fees of 0.85% and 0.25%, respectively. See “Description of Our Securities" and "Plan of Distribution."

•An investment in our Common Stock is not suitable for you if you need access to the money you invest. See “Suitability Standards” and “Share Repurchase Program.”

•An investment in our Common Stock is suitable only for investors with the financial ability and willingness to accept the high risks and lack of liquidity inherent in an investment in our Common Stock.

•We expect to invest in securities that are rated below investment grade by rating agencies or that would be rated below investment grade if they were rated. Below investment grade securities, which are often referred to as “high yield” or “junk,” have predominantly speculative characteristics with respect to the issuer’s capacity to pay interest and repay principal. They may also be illiquid and difficult to value. See “Prospectus Summary-Who We Are," "Risks Related to Our Investments" and Risks Related to Our Investments in CLOs."

Neither the Securities and Exchange Commission nor any state securities regulator has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense. Securities regulators have also not passed upon whether this offering can be sold in compliance with existing or future suitability or conduct standards including the ‘Regulation Best Interest’ standard to any or all purchasers.

The use of forecasts in this offering is prohibited. Any oral or written predictions about the amount or certainty of any cash benefits or tax consequences that may result from an investment in our Common Stock is prohibited. No one is authorized to make any statements about this offering different from those that appear in this prospectus.

Price to the Public(1) | Sales Load(2) | Proceeds to Us, Before Expenses(3) | ||||||||||||||||||

Maximum Offering(4) | $ | 300,000,000 | Up to $300,000,000 | |||||||||||||||||

| Class S Shares, per Share | $ | 5.12 | None | $ | 100,000,000 | |||||||||||||||

| Class D Shares, per Share | $ | 5.12 | None | $ | 100,000,000 | |||||||||||||||

| Class I Shares, per Share | $ | 5.12 | None | $ | 100,000,000 | |||||||||||||||

(1)Shares of each class of our Common Stock will be offered on a monthly basis at a price per share equal to the NAV per share for such class. As of December 31, 2023, the NAV per share of our Class A shares was $5.12. Our Class S, Class D and Class I shares have not been issued yet and the NAV per share of the new classes will be based off the NAV per share of our Class A shares.

(2)The Fund will not charge investors an upfront sales load with respect to Class S shares, Class D shares or Class I shares. However, if you buy Class S shares or Class D shares through certain participating brokers, they may directly charge you transaction or other fees, including upfront placement fees or brokerage commissions, in such amounts as they may determine, provided that participating brokers limit such charges to a 3.5% cap on NAV for Class S shares and a 1.5% cap on NAV for Class D shares. Participating brokers will not charge brokerage commissions on Class I shares.

(3)We and, ultimately, holders of certain classes of our Common Stock, will also pay the following shareholder servicing and/or distribution fees to the Dealer Manager, subject to Financial Industry Regulatory Authority, Inc. (“FINRA”) limitations on underwriting compensation: (a) for Class S shares, a shareholder servicing and/or distribution fee equal to 0.85% per annum of the aggregate NAV as of the beginning of the first calendar day of the month for the Class S shares; and (b) for Class D shares, a shareholder servicing and/or distribution fee equal to 0.25% per annum of the aggregate NAV as of the beginning of the first calendar day of the month for the Class D shares, in each case, payable monthly. No shareholder servicing and/or distribution fee will be paid with respect to Class I shares. The total amount that will be paid over time depends on the average length of time for which shares remain outstanding, the term over which such amount is measured and the performance of our investments. We and, ultimately, our common shareholders, will also pay or reimburse organization and initial offering expenses and, subject to FINRA limitations on underwriting compensation, certain wholesaling expenses. FINRA defines “underwriting compensation” as any payment, right, interest, or benefit received or to be received by a participating member from any source for underwriting, allocation, distribution, advisory and other investment banking services in connection with a public offering. The total underwriting compensation and total organization and offering expenses will not exceed 10% and 15%, respectively, of the gross proceeds from this offering. See “Plan of Distribution” and “Estimated Use of Proceeds.” We and, ultimately, our common shareholders will also pay certain ongoing offering expenses associated with our continuous offering of Common Stock if such ongoing offering costs are paid by us.

(4)Assumes that all shares are sold in the primary offering, with 1/3 of the gross offering proceeds from the sale of Class S shares, 1/3 from the sale of Class D shares, and 1/3 from the sale of Class I shares. The number of shares of each class sold and the relative proportions in which the classes of Common Stock are sold are uncertain and may differ significantly from this assumption. The proceeds may differ from that shown if the then-current NAV at which Common Stock is sold varies from that shown and/or additional Common Stock is registered.

This prospectus contains important information about us that a prospective investor should know before investing in our Common Stock. Please read this prospectus before investing and keep it for future reference. We will file annual, quarterly and current reports, proxy statements and other information about us with the SEC, and additional information about the Registrant will be filed with the Commission and will be available upon written or oral request and without charge. This information will be available free of charge by contacting Prospect Floating Rate and Alternative Income Fund, Inc., 10 East 40th Street, 42nd Floor, New York, NY 10016, or by telephone at (212) 448-0702 or on our website at www.pfloat.com. Any future annual or quarterly reports will be available on our website free of charge. Information contained on our website is not incorporated by reference into this prospectus, and you should not consider that information to be part of this prospectus. The SEC also maintains a website at www.sec.gov, which contains such information.

The date of this prospectus is May 10, 2024

SUITABILITY STANDARDS

Common Stock offered through this prospectus are suitable only as a long-term investment for persons of adequate financial means such that they do not have a need for liquidity in this investment. We have established financial suitability standards for initial shareholders in this offering which require that a purchaser of shares have either:

| ● | a gross annual income of at least $70,000 and a net worth of at least $70,000; or | ||||

| ● | a net worth of at least $250,000. | ||||

For purposes of determining the suitability of an investor, net worth in all cases should be calculated excluding the value of an investor’s home, home furnishings and automobiles. In the case of sales to fiduciary accounts, these minimum standards must be met by the beneficiary, the fiduciary account or the donor or grantor who directly or indirectly supplies the funds to purchase the shares if the donor or grantor is the fiduciary.

Certain states have established suitability standards in addition to the minimum income and net worth standards described above. Common Stock will be sold to investors in these states only if they meet the additional suitability standards set forth below.

Alabama Investors. Investors residing in Alabama may not invest more than 10% of their liquid net worth in us and our affiliates.

California Investors. California residents may not invest more than 10% of their liquid net worth in us and must have either (a) a liquid net worth of $350,000 and annual gross income of $65,000 or (b) a liquid net worth of $500,000.

Idaho Investors. Purchasers residing in Idaho must have either (a) a net worth of $85,000 and annual income of $85,000 or (b) a liquid net worth of $300,000. Additionally, the total investment in us shall not exceed 10% of their liquid net worth.

Iowa Investors. Investors residing in Iowa must have either (a) an annual gross income of at least $100,000 and a net worth of at least $100,000, or (b) a net worth of at least $350,000. In addition, investors residing in Iowa who are not “accredited investors” as defined in Regulation D under the Securities Act may not invest more than 10% of their net worth in our Common Stock and the common stock of other non-traded BDCs.

Kansas Investors. It is recommended by the Office of the Kansas Securities Commissioner that Kansas investors limit their aggregate investment in our securities and other similar investments to not more than 10% of their liquid net worth. Liquid net worth shall be defined as that portion of the purchaser’s total net worth that is comprised of cash, cash equivalents, and readily marketable securities, as determined in conformity with U.S. generally accepted accounting principles (“GAAP”).

Kentucky Investors. A Kentucky investor may not invest more than 10% of its liquid net worth in us or our affiliates. “Liquid net worth” is defined as that portion of net worth that is comprised of cash, cash equivalents and readily marketable securities.

Maine Investors. The Maine Office of Securities recommends that an investor’s aggregate investment in this offering and similar direct participation investments not exceed 10% of the investor’s liquid net worth. For this purpose, “liquid net worth” is defined as that portion of net worth that consists of cash, cash equivalents and readily marketable securities.

Massachusetts Investors. In addition to the suitability standards set forth above, Massachusetts residents may not invest more than 10% of their liquid net worth in us and in other illiquid direct participation programs.

Michigan Investors. No more than 10% of any one Michigan investor’s liquid net worth shall be invested in us and our affiliates.

Mississippi Investors. In addition to the suitability standards set forth above, investors residing in Mississippi may not invest more than 10% of their liquid net worth.

Missouri Investors. In addition to the suitability standards set forth above, no more than ten percent (10%) of any one (1) Missouri investor’s liquid net worth shall be invested in the securities being registered in this offering.

Nebraska Investors. In addition to the suitability standards set forth above, Nebraska investors must limit their aggregate investment in this offering and the securities of other business development companies to 10% of such investor’s net worth. Investors who are accredited investors as defined in Regulation D under the Securities Act are not subject to the foregoing investment concentration limit.

i

New Jersey Investors. New Jersey investors must have either (a) a minimum liquid net worth of at least $100,000 and a minimum annual gross income of not less than $85,000, or (b) a minimum liquid net worth of $350,000. For these purposes, “liquid net worth” is defined as that portion of net worth (total assets exclusive of home, home furnishings, and automobiles, minus total liability) that consists of cash, cash equivalent and readily marketable securities. In addition, a New Jersey investor’s investment in us, our affiliates, and other non-publicly traded direct investment programs (including real estate investment trusts, business development companies, oil and gas programs, equipment leasing programs and commodity pools, but excluding unregistered, federally and state exempt private offerings) may not exceed ten percent (10%) of their liquid net worth.

New Mexico Investors. In addition to the general suitability standards listed above, a New Mexico investor may not invest, and we may not accept from an investor more than ten percent (10%) of that investor’s liquid net worth in shares of us, our affiliates and in other non-traded business development companies. Liquid net worth is defined as that portion of net worth which consists of cash, cash equivalents and readily marketable securities.

North Dakota Investors. Investors residing in North Dakota who are not “accredited investors” as defined in Regulation D under the Securities Act must have a net worth of at least ten times their investment in our Common Stock.

Ohio Investors. Purchasers residing in Ohio may not invest more than 10% of their liquid net worth in us, our affiliates, and other non-traded business development companies. For purposes of Ohio's suitability standard, "liquid net worth” is defined as that portion of net worth (total assets exclusive of home, home furnishings, and automobiles minus total liabilities) that is comprised of cash, cash equivalents, and readily marketable securities. This condition does not apply, directly or indirectly, to federally covered securities.

Oklahoma Investors. Purchasers residing in Oklahoma may not invest more than 10% of their liquid net worth in us.

Oregon Investors. In addition to the suitability standards set forth above, Oregon investors may not invest more than 10% of their liquid net worth. Liquid net worth is defined as net worth excluding the value of the investor’s home, home furnishings and automobile.

Pennsylvania Investors. Investors residing in Pennsylvania may not invest more than 10% of their net worth in our Common Stock.

Puerto Rico Investors. Purchasers residing in Puerto Rico may not invest more than 10% of their liquid net worth in us, our affiliates and other non-traded business development companies. For these purposes, “liquid net worth” is defined as that portion of net worth (total assets exclusive of primary residence, home furnishings and automobiles minus total liabilities) consisting of cash, cash equivalents and readily marketable securities.

Tennessee Investors. Investors residing in Tennessee who are not “accredited investors” as defined in Regulation D under the Securities Act may not invest more than 10% of their net worth in our Common Stock.

Vermont Investors. Accredited investors in Vermont, as defined in 17 C.F.R. § 230.501, may invest freely in this offering. In addition to the suitability standards described above, non-accredited Vermont investors may not purchase an amount in this offering that exceeds 10% of the investor’s liquid net worth. For these purposes, “liquid net worth” is defined as an investor’s total assets (not including home, home furnishings, or automobiles) minus total liabilities.

Our investment adviser, those selling shares on our behalf and participating brokers and registered investment advisers recommending the purchase of shares in this offering are required to make every reasonable effort to determine that the purchase of shares in this offering is a suitable and appropriate investment for each investor based on information provided by the investor regarding the investor’s financial situation and investment objective and must maintain records for at least six years after the information is used to determine that an investment in our Common Stock is suitable and appropriate for each investor. Relevant information for this purpose includes, at the minimum, the age, investment objectives, investment experience, income, net worth, financial situation, and other investments of the prospective investor, as well as any other pertinent factors. In making this determination, our investment adviser, the participating broker, registered investment adviser, authorized representative or other person selling shares will, based on a review of the information provided by the investor, consider whether the investor:

ii

| ● | meets the minimum income and net worth standards established in the investor’s state; | ||||

| ● | can reasonably benefit from an investment in our Common Stock based on the investor’s overall investment objective and portfolio structure; | ||||

| ● | is able to bear the economic risk of the investment based on the investor’s overall financial situation; and | ||||

| ● | has an apparent understanding of the following: | ||||

| ● | the fundamental risks of the investment; | ||||

| ● | the risk that the investor may lose its entire investment; | ||||

| ● | the lack of liquidity of our Common Stock; | ||||

| ● | the restrictions on transferability of the Common Stock; | ||||

| ● | the background and qualifications of our investment adviser; and | ||||

| ● | the tax consequences of the investment. | ||||

In addition to investors who meet the minimum income and net worth requirements set forth above, our Common Stock may be sold to financial institutions that qualify as “institutional investors” under the state securities laws of the state in which they reside. “Institutional investor” is generally defined to include banks, insurance companies, investment companies as defined in the 1940 Act, pension or profit sharing trusts and certain other financial institutions. A financial institution that desires to purchase shares will be required to confirm that it is an “institutional investor” under applicable state securities laws.

In addition to the suitability standards established herein, (i) a participating broker may impose additional suitability requirements and investment concentration limits to which an investor could be subject and (ii) various states may impose additional suitability standards, investment amount limits and alternative investment limitations.

Brokers must comply with Regulation Best Interest, which, among other requirements, enhances the existing standard of conduct for brokers and establishes a “best interest” obligation for brokers and their associated persons when making recommendations of any securities transaction or investment strategy involving securities to a retail customer. The obligations of Regulation Best Interest are in addition to, and may be more restrictive than, the suitability requirements listed above. When making such a recommendation to a retail customer, a broker must, among other things, act in the best interest of the retail customer at the time a recommendation is made, without placing its interests ahead of its retail customer’s interests. Reasonable alternatives to the Fund, such as listed entities, exist and may have lower expenses, less complexity, and/or lower investment risk than the Fund. Certain investments in listed entities may involve lower or no commissions at the time of initial purchase. Under Regulation Best Interest, high cost, high risk and complex products may require greater scrutiny by broker-dealers and their salespersons before they recommend such products. A participating broker may satisfy the best interest standard imposed by Regulation Best Interest by meeting disclosure, care, conflict of interest and compliance obligations. In addition, brokers are required to provide retail investors a brief relationship summary, or Form CRS, that summarizes for the retail investor key information about the broker. Form CRS is different from this prospectus, which contains regarding this offering and the Fund. Investors should refer to the prospectus for detailed information about this offering before deciding to purchase Common Stock. Currently, there is limited administrative or case law interpreting Regulation Best Interest and the full scope of its applicability on brokers participating in our offering cannot be determined at this time.

iii

ABOUT THIS PROSPECTUS

Please carefully read the information in this prospectus and any accompanying prospectus supplements, which we refer to collectively as the “prospectus.” You should rely only on the information contained in this prospectus. We have not authorized anyone to provide you with different information. This prospectus may only be used where it is legal to sell these securities. You should not assume that the information contained in this prospectus is accurate as of any date later than the date hereof or such other dates as are stated herein or as of the respective dates of any documents or other information incorporated herein by reference.

We will disclose the NAV per share of each class of our Common Stock for each month when available on our website at https://www.pfloat.com. Information contained on our website is not incorporated by reference into this prospectus, and you should not consider that information to be part of this prospectus. The words “we,” “us,” “our” and the “Fund” refer to Prospect Floating Rate and Alternative Income Fund, Inc., together with its consolidated subsidiaries.

Unless otherwise noted, numerical information relating to the Fund is approximate as of December 31, 2023.

Citations included herein to industry sources are used only to demonstrate third-party support for certain statements made herein to which such citations relate. Information included in such industry sources that do not relate to supporting the related statements made herein are not part of this prospectus and should not be relied upon.

iv

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Some of the statements included in this prospectus and any accompanying prospectus supplement, constitute forward-looking statements, which relate to future events or our future performance or financial condition. The forward-looking statements contained in this prospectus, any accompanying prospectus supplement and other information incorporated herein by reference involve a number of risks and uncertainties, including statements concerning:

•our, or our portfolio companies’, future operating results;

•our business prospects and the prospects of potential investments;

•the return or impact of current or future the investments we expect to make;

•the financial condition and ability of our current and prospective portfolio companies to achieve their objectives;

•difficulty in obtaining financing or raising capital, especially in the current credit and equity environment, and the impact of a protracted decline in the liquidity of credit markets on our and our portfolio companies’ business;

•the adequacy of our cash resources and working capital; and

•the timing of cash flows, if any, from operations of our portfolio companies.

In addition, words such as “anticipate,” “believe,” “expect,” “intend,” “seeks,” “would” and “should” indicate a forward-looking statement, although not all forward-looking statements include these words. The forward-looking statements in this prospectus are not guarantees of future performance and involve risks, uncertainties and other factors, many of which will be beyond our control and difficult to predict. Our actual results could differ materially from those implied or expressed in the forward-looking statements for any reason, including the factors set forth in “Risk Factors” and elsewhere in this prospectus. Other factors that could cause actual results to differ materially include:

•the dependence of our future success on the general economy and its impact on the industries in which we invest;

•the impact of global health epidemics, wars and civil disorder and other events outside our control, including, but not limited to, the renewed hostilities in the Middle East and the conflict between Russia and Ukraine, on our and our portfolio companies’ businesses and the global economy;

•uncertainty surrounding inflation and the financial stability of the United States, Europe, and China;

•the impact of changes in laws or regulations governing our operations or the operations of our portfolio companies; and

•the ability of our Adviser to locate suitable investments for us and to monitor and administer our investments.

Although we believe that the assumptions on which the forward-looking statements in this prospectus are based are reasonable, any of those assumptions could prove to be inaccurate. As a result, the statements based on those assumptions could be inaccurate. Accordingly, the inclusion of forward-looking statements in this prospectus should not be regarded as a representation that our plans and objectives will be achieved and you should not place undue reliance on those statements.

We have based the forward-looking statements included in this prospectus on information available to us on the date of this prospectus, and, except as required by the federal securities laws, we undertake no obligation to revise or update any forward-looking statements, whether as a result of new information, future events or otherwise. You are advised to review any additional disclosures that we may make directly to you or through reports that we in the future may file with the SEC, including annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K. The forward-looking statements and projections contained in this prospectus are excluded from the safe harbor protection provided by Section 27A of the Securities Act.

v

TABLE OF CONTENTS

| Page | |||||

| RESTRICTIONS ON SHARE OWNERSHIP | |||||

| CUSTODIAN, TRANSFER AND DISTRIBUTION PAYING AGENT AND REGISTRAR | |||||

| BROKERAGE ALLOCATION AND OTHER PRACTICES | |||||

| INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM | |||||

| LEGAL MATTERS | |||||

| AVAILABLE INFORMATION | |||||

| A-1 | |||||

vi

PROSPECTUS SUMMARY

This summary highlights some of the information in this prospectus. It is not complete and may not contain all of the information that you may want to consider. To understand this offering fully, you should read the entire prospectus carefully, including the section entitled “Risk Factors” before making a decision to invest in our common stock.

Unless otherwise noted, the terms “we”, “us”, “our,” “the Fund” and the “Company” refer to Prospect Floating Rate and Alternative Income Fund, Inc., a Maryland corporation. Certain other entities having a role in our offering or in our management are referred to as follows and are further described in this prospectus:

“Adviser,” “Investment Adviser,” “Prospect Capital Management,” and “PCM” refer to Prospect Capital Management L.P., a Delaware limited partnership and our investment adviser.

“Administrator” and “Prospect Administration” refers to Prospect Administration LLC, a Delaware limited liability company and our administrator.

Also, the terms “1940 Act” and “Advisers Act” refer to the Investment Company Act of 1940, as amended, and the Investment Advisers Act of 1940, as amended, respectively, and the term “Code” refers to the Internal Revenue Code of 1986, as amended.

Who We Are

We were formed as a Maryland corporation on April 29, 2011. We are an externally managed, closed-end, non-diversified management investment company that has elected to be regulated as a business development company, or BDC, under the 1940 Act. We are therefore required to comply with certain regulatory requirements. We have elected to be taxed for U.S. federal income tax purposes, and intend to qualify annually, as a regulated investment company, or RIC, under Subchapter M of the Code. Our Adviser is registered as an investment adviser with the Securities and Exchange Commission, or SEC, under the Advisers Act. Our Adviser manages our portfolio and makes all investment decisions for us, subject to supervision by our board of directors. On June 25, 2014, we satisfied our minimum offering requirement of selling at least $2.5 million in common stock and on October 1, 2014, we commenced our investment operations.

Our investment objective is to generate current income and, as a secondary objective, capital appreciation by targeting investment opportunities with favorable risk-adjusted returns. Under normal market conditions, we will invest at least 80% of our net assets (plus any borrowings for investment purposes) in floating rate loans and other income producing investments. We intend to meet our investment objective by primarily lending to and investing in the debt of privately-owned U.S. middle market companies, which we define as companies with annual revenue between $50 million and $2.5 billion. We may on occasion invest in smaller or larger companies if an attractive opportunity presents itself, especially when there are dislocations in the capital markets. We expect to focus primarily on directly originating senior secured first lien loans and senior secured second lien loans and making investments in syndicated senior secured first lien loans, syndicated senior secured second lien loans, and to a lesser extent, subordinated debt, of middle market companies in a broad range of industries. Syndicated secured loans refer to commercial loans provided by a group of lenders that are structured, arranged, and administered by one or several commercial or investment banks, known as arrangers. These loans are then sold (or syndicated) to other banks or institutional investors. Syndicated secured loans may have a first priority lien on a borrower’s assets (i.e., senior secured first lien loans), a second priority lien on a borrower’s assets (i.e., senior secured second lien loans), or a lower lien or unsecured position on the borrower’s assets (i.e., subordinated debt). Our target credit investments are expected to typically have initial maturities between three and ten years and generally range in size between $1 million and $100 million, although the investment size may vary with the size of our capital base. We expect that the majority of our debt investments will bear interest at floating interest rates, but our portfolio may also include fixed-rate investments. We expect to make our investments directly through the primary issuance by the borrower or in the secondary market. “Risk-adjusted returns” refers to a measure of investment return per unit of risk and provides a framework to compare and evaluate investment opportunities with differing risk/return profiles. The term “risk-adjusted returns” does not imply that we employ low-risk strategies or that an investment should be considered a low-risk or no risk investment.

We expect that at least 70% of our portfolio of investments will consist primarily of directly originated or syndicated senior secured first lien loans, directly originated or syndicated senior secured second lien loans, and to a lesser extent, subordinated debt, and up to 30% of our portfolio of investments will consist of other securities, including private equity (both common and preferred), dividend-paying equity, royalties, and the equity and junior debt tranches of a type of pools of broadly syndicated loans known as collateralized loan obligations, or CLOs, which we referred to as “Subordinated Structured Notes” or “SSNs”. The senior secured loans underlying our SSN investments are expected typically to be BB or B rated (non-investment grade, which is often referred to as “high yield” or “junk”) and in limited circumstances, unrated, senior secured loans. The SSN investments are entitled to recurring distributions which are generally equal to the excess cash flow generated

1

from the underlying investments after payment of the contractual payments to debt holders and fund expenses. The current estimated yield, calculated using amortized cost, is based on the current projections of this excess cash flow taking into account assumptions which have been made regarding expected prepayments, losses and future reinvestment rates. These assumptions are periodically reviewed and adjusted. Ultimately, the actual yield may be higher or lower than the estimated yield if actual results differ from those used for the assumptions.

As part of our strategy, we intend to dynamically allocate our assets in varying types of investments based on our analysis of the credit markets. These investments include senior secured first lien loans, senior secured second lien loans, subordinated debt, equity and equity-related securities, non-U.S. securities, subordinated structured notes and other securities.

We will be subject to certain regulatory restrictions in making our investments. On January 13, 2020 (amended on August 2, 2022), we received a co-investment exemptive order from the SEC (the “Order”) granting us the ability to negotiate terms other than price and quantity of co-investment transactions with other funds managed or owned by our Adviser or certain affiliates, including Prospect Capital Corporation and Priority Income Fund, Inc., where co-investing would otherwise be prohibited under the 1940 Act, subject to the conditions included therein. Under the terms of the Order, a majority of our independent directors who have no financial interest in the transaction must make certain conclusions in connection with a co-investment transaction, including that (1) the terms of the proposed transaction, including the consideration to be paid, are reasonable and fair to us and our stockholders and do not involve overreaching of us or our stockholders on the part of any person concerned and (2) the transaction is consistent with the interests of our stockholders and is consistent with our investment objective and strategies. The Order also imposes reporting and record keeping requirements and limitations on transactional fees. We may only co-invest with other funds managed or owned by our Adviser or certain affiliates in accordance with such Order and existing regulatory guidance. See “Additional Relationships and Related Party Transactions—Allocation of Investments.” These co-investment transactions may give rise to conflicts of interest or perceived conflicts of interest among us and the other participating accounts. To mitigate these conflicts, our Adviser and its affiliates will seek to allocate portfolio transactions for all of the participating investment accounts, including us, on a fair and equitable basis, taking into account such factors as the relative amounts of capital available for new investments, the applicable investment programs and portfolio positions, the clients for which participation is appropriate and any other factors deemed appropriate. We intend to make all of our investments in compliance with the 1940 Act and in a manner that will not jeopardize our status as a BDC or RIC.

As a BDC, we are permitted under the 1940 Act to borrow funds to finance portfolio investments. To enhance our opportunity for gain, we intend to employ leverage as market conditions permit. The use of leverage, although it may increase returns, may also increase the risk of loss to our investors, particularly if the level of our leverage is high and the value of our investments declines. For a discussion of the risks of leverage, see “Risk Factors – Risks Relating to Our Business and Structure.”

Merger and Accounting Survivor

On March 31, 2019, Pathway Capital Opportunity Fund, Inc. (“PWAY”) merged with and into us (the “Merger”). As the combined surviving company, we were renamed as TP Flexible Income Fund, Inc. (we were formerly known as Triton Pacific Investment Corporation, Inc. (“TPIC”)). Effective September 16, 2022, we changed our name to Prospect Floating Rate and Alternative Income Fund, Inc. Although PWAY merged with and into us, PWAY is considered the accounting survivor of the Merger and its historical financial statements are included and discussed in this prospectus and in the reports that we file with the Securities and Exchange Commission (the “SEC”).

Status of Our Prior Public Offering

The Company previously conducted an offering of its “Class A” common stock. This offering was terminated on February 19, 2021. As of that date, the Company had sold $24,195,384 in shares pursuant to the public offering registration statement, excluding $2,619,663 in shares issued pursuant to the Company’s distribution reinvestment plan. In connection with the termination of the public continuous offering of shares, the Company deregistered the remaining $275,804,616 in shares, which remained unsold as of that date. The Class A shares are not being offered as a part of this prospectus and are only expected to be issued in the future in connection with the reinvestment of distributions.

About Our Adviser

On April 20, 2021, we entered into a new investment advisory agreement (the “Advisory Agreement”) with Prospect Capital Management L.P., our current investment adviser. The Advisory Agreement was unanimously approved by our board of directors, including by all of our directors who are not “interested persons” (as defined in the 1940 Act). Our stockholders approved the Advisory Agreement at a Special Meeting of Stockholders held on March 31, 2021 (the “Special Meeting”). On November 5, 2021, the Advisory Agreement was amended and restated to reduce the base management fee and eliminate the incentive fee, effective as of January 1, 2022 and until the one year anniversary of the listing of our common stock on a national

2

securities exchange as discussed herein (the “Amended and Restated Advisory Agreement”). The Amended and Restated Advisory Agreement was most recently approved by our board of directors, including all of our directors who are not “interested persons” (as defined in the 1940 Act), on June 15, 2023.

Our Adviser is registered as an investment adviser under the Advisers Act and provides services to us pursuant to the terms of the Advisory Agreement, including as amended and restated. Our Adviser’s investment professionals have significant experience and an extensive track record of investing in companies, managing high-yielding debt and equity investments in infrastructure companies and have developed an expertise in using all levels of a firm’s capital structure to produce income-generating investments, while focusing on risk management. Such parties also have extensive knowledge of the managerial, operational and regulatory requirements of publicly traded investment companies. Most of the finance professionals of our Adviser are involved in the operation, management and regulatory compliance of two affiliated funds, Prospect Capital Corporation, a BDC that is listed for trading on the Nasdaq Stock Market that had total assets of approximately $7.9 billion as of June 30, 2023, and Priority Income Fund, Inc., an externally managed, non-diversified, closed-end management investment company that invests primarily in senior secured loans, including via SSN investments, of companies whose debt is rated below investment grade or, in limited circumstances, unrated.

Prospect Capital Management L.P. is led by John F. Barry III and M. Grier Eliasek, two senior executives with significant investment advisory and business experience. Both Messrs. Barry and Eliasek spend a significant amount of their time in their roles at Prospect Capital Management working on our behalf. The principal executive offices of Prospect Capital Management are 700 S Rosemary Ave, Suite 204, West Palm Beach, FL 33401. We depend on the due diligence, skill and network of business contacts of the senior management of our Adviser. We also depend, to a significant extent, on the Adviser’s investment professionals and the information and deal flow generated by those investment professionals in the course of their investment and portfolio management activities. Our Adviser’s senior management team evaluates, negotiates, structures, closes, monitors and services our investments. Our future success depends to a significant extent on the continued service of the senior management team, particularly John F. Barry III and M. Grier Eliasek. The departure of any of the senior managers of our Adviser could have a materially adverse effect on our ability to achieve our investment objective. In addition, we can offer no assurance that Prospect Capital Management will remain our investment adviser or that we will continue to have access to its investment professionals or its information and deal flow. Under the Advisory Agreement, we pay Prospect Capital Management investment advisory fees, which consist of an annual base management fee based on our average total assets as well as a two-part incentive fee based on our performance. Upon effectiveness of the Amended and Restated Advisory Agreement on January 1, 2022, we began paying Prospect Capital Management a reduced annual base management of 1.20% of our average total assets and no incentive fee until the one-year anniversary of the listing of our common stock on a national securities exchange. Mr. Barry currently controls Prospect Capital Management.

Our board of directors includes a majority of independent directors and oversees and monitors the activities of our Adviser as well as our investment portfolio and performance, and annually reviews the compensation paid to our Adviser. See “Advisory Agreement” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” below. In addition to managing our portfolio, our Adviser provides on our behalf managerial assistance to those of our portfolio companies to which we are required to provide such assistance. We have the right to terminate the Advisory Agreement, including the Amended and Restated Advisory Agreement, upon 60 days’ written notice to our Adviser, and our Adviser has the right to terminate the Advisory Agreement, including the Amended and Restated Advisory Agreement, upon 120 days’ written notice to us.

Risk Factors

An investment in shares of our common stock involves a high degree of risk and may be considered speculative. You should carefully consider the information found in “Risk Factors” before deciding whether to invest in shares of our common stock. The following are some of the risks an investment in us involves:

Risks Relating to Our Business and Structure

•Except for the investments described in this prospectus, we have not identified specific investments that we will make with the proceeds of this offering, and you will not have the opportunity to evaluate our future investments prior to purchasing shares of our common stock.

•We have not established any limit on the amount of funds we may use from available sources, such as borrowings, if any, or proceeds from this offering, to fund distributions (which may reduce the amount of capital we ultimately invest in assets).

•A failure on our part to maintain our qualification as a business development company would significantly reduce our operating flexibility.

3

•Regulations governing our operation as a business development company and RIC will affect our ability to raise, and the way in which we raise, additional capital or borrow for investment purposes, which may have a negative effect on our growth.

•A significant portion of our investment portfolio will be recorded at fair value as determined in good faith by our board of directors for quarter-end periods and by our Valuation Designee (discussed below) for intra-quarter periods and, as a result, there could be uncertainty as to the actual market value of our portfolio investments.

•Because our business model depends to a significant extent upon the business relationships of our Adviser, the inability of our Adviser to maintain or develop these relationships, or the failure of these relationships to generate investment opportunities, could adversely affect our business.

•The amount and timing of distributions are uncertain and distributions may be funded from the proceeds of this offering and may represent a return of capital.

•We will be subject to U.S. federal income tax if we are unable to qualify as a RIC under Subchapter M of the Code or do not satisfy the annual distribution requirement.

•Our board of directors may change our operating policies and strategies without prior notice or stockholder approval, the effects of which may be adverse.

•Our board of directors has discretion over the use of the proceeds of this offering.

•If we borrow money, the potential for gain or loss on amounts invested in us will be magnified and may increase the risk of investing in us.

•Because we intend to distribute substantially all of our income to our stockholders in connection with our election to be treated as a RIC, we will continue to need additional capital to finance our growth. If additional funds are unavailable or not available on favorable terms, our ability to grow will be impaired.

•In selecting and structuring investments appropriate for us, our Adviser will consider the investment and tax objectives of the Company and our stockholders as a whole, not the investment, tax or other objectives of any stockholder individually.

•We may pursue strategic acquisitions.

•If we are unable to consummate or successfully integrate development opportunities, acquisitions or joint ventures, we may not be able to implement our growth strategy successfully.

•We entered into a non-exclusive, royalty-free license to use the “Prospect” name, which may be terminated if our Adviser or another affiliate of the Adviser is no longer our investment adviser.

•Compliance with the SEC’s Regulation Best Interest may negatively impact our ability to raise capital in this offering, which would harm our ability to achieve our investment objectives.

Risks Related to our Adviser and Its Affiliates

•We will rely on our Adviser and its investment personnel for the selection of our assets and the monitoring of our investments.

•There are significant potential conflicts of interest which could adversely impact our investment returns.

•The involvement of our Adviser’s investment professionals in our valuation process may create conflicts of interest.

•Our fee structure may induce our Adviser to cause us to borrow and make speculative investments.

Risks Relating to Our Investments

•Our investments in prospective portfolio companies may be risky, and we could lose all or part of our investment.

•Investing in small and mid-sized companies involves a number of significant risks.

•An investment strategy focused primarily on privately-held companies presents certain challenges, including the lack of available information about these companies.

•Defaults by our portfolio companies will harm our operating results.

•Our portfolio companies may incur debt that ranks equally with, or senior to, our debt investments in such companies.

•If we make unsecured investments, those investments might not generate sufficient cash flow to service their debt obligations to us.

• If we invest in the securities and obligations of distressed and bankrupt issuers, we might not receive interest or other payments.

4

•There may be circumstances where our debt investments could be subordinated to claims of other creditors or we could be subject to lender liability claims.

•We generally will not control the portfolio companies in which we make debt investments.

•To the extent original issue discount (“OID”) constitutes a portion of our income, we will be exposed to risks associated with the deferred receipt of cash representing such income.

•The lack of liquidity in our investments may adversely affect our business.

•We may not have the funds or ability to make additional investments in the companies in which we invest.

•The companies in which we invest may incur debt that ranks equally with, or senior to, our investments in such companies.

•The disposition of our investments may result in contingent liabilities.

•Second priority liens on collateral securing loans that we make to a company may be subject to control by senior creditors with first priority liens. If there is a default, the value of the collateral may not be sufficient to repay in full both the first priority creditors and us.

•We generally will not control companies to which we provide debt.

•We may incur lender liability as a result of our lending activities.

•We may not realize gains from our private equity investments.

•We may focus our investments in companies in a particular industry or industries.

•Our portfolio companies may be highly leveraged.

•Rising interest rates may adversely affect the value of our portfolio investments which could have an adverse effect on our business, financial condition and results of operations.

•The discontinuation of LIBOR may adversely affect the value of floating-rate debt securities in our portfolio.

Risks Relating to our Investments in CLOs

•Our investments in CLOs may be riskier and less transparent to us and our stockholders than direct investments in the underlying companies.

•Our financial results may be affected adversely if one or more of our significant equity or junior debt investments in a CLO vehicle defaults on our payment obligations or fails to perform as we expect.

•CLOs typically will have no significant assets other than their underlying senior secured loans; payments on CLO investments are and will be payable solely from the cash flows from such senior secured loans.

•Our CLO investments will be exposed to leveraged credit risk.

•There is the potential for interruption and deferral of cash flow from CLO investments.

•Investments in foreign securities may involve significant risks in addition to the risks inherent in U.S. investments.

•The payment of underlying portfolio manager fees and other charges on CLO investments could adversely impact our return on our CLO investments.

•The inability of a CLO collateral manager to reinvest the proceeds of the prepayment of senior secured loans may adversely affect us.

•Our CLO investments are subject to prepayments and calls, increasing re-investment risk.

•We will have limited control of the administration and amendment of senior secured loans owned by the CLOs in which we invest.

•We will have limited control of the administration and amendment of any CLO in which we invest.

•Non-investment grade debt involves a greater risk of default and higher price volatility than investment grade debt.

•We will have no influence on management of underlying investments managed by non-affiliated third-party CLO collateral managers.

•Certain collateral quality test failures in our CLO investments may result in diversion of CLO payments and harm our operating results.

•The application of the risk retention rules under U.S. and EU law to CLOs may have broader effects on the CLO and loan markets in general, potentially resulting in fewer or less desirable investment opportunities for us.

Risks Relating to Economic Conditions

•Adverse economic conditions or increased competition for investment opportunities could delay deployment of our capital, reduce returns and result in losses.

•Economic recessions or downturns could impair a company in which we invest and harm our operating results.

•Changes in interest rates may adversely affect our cost of capital, net investment income and ability to borrow money.

•Future changes in laws or regulations governing our operations may adversely affect our business or cause us to alter our business strategy.

5

•Terrorist attacks, acts of war or natural disasters may affect any market for our common stock, impact the businesses in which we invest and harm our business, operating results and financial condition.

Risks Relating to this Offering and Our Common Stock

•Delays in the application of offering proceeds to our investment program may adversely affect our results.

•If we are unable to raise substantial funds, we will be limited in the number and type of investments we may make, and the value of your investment in us may be reduced in the event our assets under-perform.

•The shares sold in this offering will not be listed on an exchange or quoted through a quotation system for the foreseeable future, if ever. Therefore, if you purchase shares in this offering, you will have limited liquidity.

•Although we plan to offer to repurchase your shares on a quarterly basis through our share repurchase program, the terms of any such repurchases will be limited. As a result, you will have limited opportunities to sell your shares.

•The timing of our share repurchase offers pursuant to our share repurchase program may be at a time that is disadvantageous to our stockholders.

•We may be unable to invest a significant portion of the net proceeds of this offering on acceptable terms in the timeframe contemplated by this prospectus.

•Your interest in us will be diluted if we issue additional shares, which could reduce the overall value of your investment.

•Our Distribution Reinvestment Plan will dilute the interest of those who do not opt-in.

•We may issue preferred stock as a means to access additional capital, which could adversely affect common stockholders and subject us to specific regulation under the 1940 Act.

•Certain provisions of our charter and bylaws as well as provisions of the Maryland General Corporation Law could deter takeover attempts and have an adverse impact on the value of our common stock.

•Special considerations for certain benefit plan investors.

Risks Related to Debt Financing

•Our use of borrowed money will magnify the potential for gain or loss on amounts invested in our common stock and may increase the risk of investing in our common stock.

•Our use of borrowed funds to make investments will expose us to risks typically associated with leverage.

•If we default under our Senior Secured Revolving Credit Facility or any subsequent credit facility or are unable to amend, repay or refinance any such facility on commercially reasonable terms, or at all, we may suffer material adverse effects on our business, financial condition, results of operations and cash flows.

•Incurring leverage creates conflicts of interests for our investment adviser.

Risks Related to Business Development Companies

•The requirement that we invest a sufficient portion of our assets in qualifying assets could preclude us from investing in accordance with our current business strategy; conversely, the failure to invest a sufficient portion of our assets in qualifying assets could result in our failure to maintain our status as a BDC.

•We may incur additional leverage.

U.S. Federal Income Tax Risks

•Legislative or other actions relating to taxes could have a negative effect on us.

•We may be subject to U.S. federal income tax if we fail to qualify as a RIC.

•We may have difficulty paying our required distributions if we recognize income before or without receiving cash representing such income.

•You may receive shares of our common stock as distributions, which could result in adverse tax consequences to you.

•You may have current tax liability on distributions you elect to reinvest in our common stock but would not receive cash from such distributions to pay such tax liability.

•If we do not qualify as a “publicly offered regulated investment company,” as defined in the Code, you will be taxed as though you received a distribution of some of our expenses.

•Our investments in CLO vehicles may be subject to special anti-deferral provisions that could result in us incurring tax or recognizing income prior to receiving cash distributions related to such income.

General Risk Factors

•We will experience fluctuations in our quarterly operating results.

•Global economic, political and market conditions may adversely affect our business, results of operations and financial condition, including our revenue growth and profitability.

•We are dependent on information systems and systems failures could significantly disrupt our business, which may, in turn, negatively affect our liquidity, financial condition or results of operations.

•Cybersecurity risks and cyber incidents may adversely affect our business or the business of our portfolio companies by causing a disruption to our operations or the operations of our portfolio companies, a

6

compromise or corruption of our confidential information or the confidential information of our portfolio companies and/or damage to our business relationships or the business relationships of our portfolio companies, all of which could negatively impact the business, financial condition and operating results of us or our portfolio companies.

•Inflation can adversely impact our cost of capital and the value of our portfolio investments.

•The prolonged Russian invasion of Ukraine and the resulting international response may have a material adverse impact on us and our portfolio companies.

Prospective investors should realize that factors other than those set forth in this prospectus may ultimately affect the investment offered pursuant to this prospectus in a manner and to a degree which cannot be foreseen at this time.

Credit Facility

On May 16, 2019, the Company established a $50 million senior secured revolving credit facility (the “Credit Facility”) with Royal Bank of Canada, a Canadian chartered bank, acting as administrative agent. On May 16, 2019, we also formed a wholly-owned subsidiary Prospect Flexible Funding, LLC (f/k/a TP Flexible Funding, LLC) (the “SPV”), a Delaware limited liability company and a bankruptcy remote special purpose entity, which holds certain of our portfolio loan investments that were used as collateral for the Credit Facility at the SPV. This subsidiary has been consolidated since operations commenced. In connection with the Credit Facility, the SPV, as borrower, and each of the other parties thereto entered into a Revolving Loan Agreement, dated as of May 16, 2019 (the “Loan Agreement”).

The Credit Facility had a maturity of May 21, 2029 and, initially, bore interest at a rate of three-month LIBOR plus 1.55%. On May 11, 2020, in connection with an extension of the ramp period for the Credit Facility from May 15, 2020 to November 15, 2020, the Company agreed to the increased interest rate of three-month LIBOR plus 2.20% on the Credit Facility for the period from May 16, 2020 through November 15, 2020. Effective November 10, 2020, the end date of the ramp period of the Credit Facility was extended again, from November 15, 2020 to May 14, 2021. As a result, the interest rate on borrowings under the Credit Facility of the three-month LIBOR plus 2.20% was extended through May 14, 2021. On May 11, 2021, the end date of the ramp period of the Credit Facility was further extended from May 14, 2021 to November 15, 2021. As a result, the interest rate on borrowings under the Credit Facility of the three-month LIBOR plus 2.20% was extended through November 15, 2021. On August 26, 2021, the end date of the ramp period of the Credit Facility was further extended from November 15, 2021 to August 25, 2022. In exchange, the interest rate on borrowings under the Credit Facility of the three-month LIBOR plus 2.20% was extended permanently. On July 6, 2022, the end date of the ramp period of the Credit Facility was further extended from August 25, 2022 to August 25, 2023. In connection with such extension, the interest rate on borrowings under the Credit Facility was amended from three-month LIBOR plus 2.20% to Secured Overnight Financing Rate (“SOFR”) plus 2.20%. On March 24, 2023, (i) the end date of the ramp period of the Credit Facility was further extended from August 25, 2023 to October 25, 2023 and (ii) the Loan Agreement was amended to require sales of collateral and/or receipt of capital contributions in a combined amount to have generated proceeds (on a trade date basis) (x) during the period from March 24, 2023 through April 30, 2023, in the Initial Amount (the "Initial Amount") of $4,000,000, and (y) during each month thereafter in an amount equal to $2,000,000 (the "Required Amount") with any amount in excess of the total Required Amount plus the Initial Amount contributing to the Required Amount for the next month. In connection with such extension and amendment, the interest rate on borrowings under the Credit Facility was reduced from SOFR plus 2.20% to SOFR plus 1.55%. The Credit Facility was secured by substantially all of the SPV’s properties and assets. Under the Loan Agreement, the SPV made certain customary representations and warranties and was required to comply with various covenants, including reporting requirements and other customary requirements for similar credit facilities. The Loan Agreement included usual and customary events of default for credit facilities of this nature. On November 7, 2022, Royal Bank of Canada granted a waiver of any non-compliance with certain waterfall provisions in the Loan Agreement that may have occurred prior to November 7, 2022. Further non-compliance with certain waterfall provisions was permitted through January 31, 2023.

On September 21, 2023, the Company entered into a senior secured revolving credit agreement (the "Senior Secured Revolving Credit Facility"), by and among the Company, as borrower, the lenders party thereto, and Sumitomo Mitsui Banking Corporation, as administrative agent. In conjunction with the closing of the Senior Secured Revolving Credit Facility, we terminated the Credit Facility.

The Senior Secured Revolving Credit Facility provides for borrowings in U.S. dollars and certain agreed upon foreign currencies in an initial aggregate amount of up to $20,000,000 with an option for the Company to request, at one or more times, that existing and/or new lenders, at their election, provide up to $150,000,000 in aggregate. The Senior Secured Revolving Credit Facility provides for swingline loans in an aggregate principal amount at any time outstanding that will not exceed $5,000,000. On January 30, 2024, the Company entered into the first amendment (the "First Amendment") to the Senior

Secured Revolving Credit Agreement. Among other changes, the First Amendment amends the original Senior Secured

Revolving Credit Agreement to provide for an increase in the aggregate commitment from $20,000,000 to $65,000,000. On

7

February 1, 2024, there was an Automatic Commitment Increase which increased the aggregate commitment from $65,000,000

to $75,000,000. Availability under the Senior Secured Revolving Credit Facility will terminate on the earlier of the Commitment Termination Date of September 19, 2025 or the date of termination of the revolving commitments thereunder, and the outstanding loans under the Senior Secured Revolving Credit Facility will mature on September 21, 2026. The Senior Secured Revolving Credit Facility also requires mandatory prepayment of interest and principal upon certain events, including after the date of termination of the revolving commitments thereunder from asset sales, extraordinary receipts, returns of capital, equity issuances, and incurrence of indebtedness, with certain exceptions and minimum amount thresholds.

Borrowings under the Senior Secured Revolving Credit Facility are subject to compliance with a borrowing base test. Amounts drawn under the Senior Secured Revolving Credit Facility in U.S. dollars will bear interest at either term SOFR plus a credit spread adjustment of 0.10% plus 2.5%, or the prime rate plus 1.5%. The Company may elect either the term SOFR or prime rate at the time of drawdown, and loans denominated in U.S. dollars may be converted from one rate to another at any time at the Company’s option, subject to certain conditions. Amounts drawn under the Senior Secured Revolving Credit Facility in other permitted currencies will bear interest at the relevant rate specified therein plus 2.5%.

During the period commencing on September 21, 2023 and ending on the earlier of the Commitment Termination Date or the date of termination of the revolving commitments under the Senior Secured Revolving Credit Facility, the Company will pay a commitment fee of 0.375% per annum (based on the immediately preceding quarter’s average usage) on the daily unused amount of the commitments then available thereunder.

In connection with the Senior Secured Revolving Credit Facility, the Company has made certain representations and warranties and must comply with various covenants and reporting requirements customary for facilities of this type. In addition, the Company must comply with the following financial covenants with respect to the Company and its consolidated subsidiaries: (a) the Company must maintain a minimum shareholders’ equity, measured as of each fiscal quarter end; and (b) the Company must maintain at all times an asset coverage ratio not less than 150%.

The Senior Secured Revolving Credit Facility contains events of default customary for facilities of this type. Upon the occurrence of an event of default, the Administrative Agent, at the request of the required lenders, may terminate the commitments and declare the outstanding advances and all other obligations under the Senior Secured Revolving Credit Facility immediately due and payable.

The Company’s obligations under the Senior Secured Revolving Credit Facility are guaranteed by Prospect Flexible Funding, LLC, a subsidiary of the Company, and will be guaranteed by certain domestic subsidiaries of the Company that are formed or acquired by the Company in the future. The Company’s obligations under the Senior Secured Revolving Credit Facility are secured by a first priority security interest in substantially all of the Company’s assets and certain of the Company’s subsidiaries thereunder.

As of December 31, 2023, there was a $4,200,000 balance on the Senior Secured Revolving Credit Facility.

Potential Market Opportunity

We believe that there are and will continue to be significant investment opportunities in the senior secured first lien loan and senior secured second lien loan asset classes, as well as investments in debt and equity securities of middle market companies.

Potential Opportunity in Middle Market Private Companies

We believe the middle market lending environment provides opportunities for us to meet our objective of making investments that generate attractive risk-adjusted returns as a result of a combination of the following factors:

Large Addressable Market. According to Leveraged Commentary & Data, institutional leveraged loan issuance (senior secured loans and second lien secured loans) is attracting inflows due to the Federal Reserve’s indication of rising interest rates over 2022 and beyond. We believe that there exists a large number of prospective lending opportunities for lenders, which should allow us to generate substantial investment opportunities and build an attractive portfolio of investments.

Strong Demand for Debt Capital. We expect that private equity firms will continue to be active investors in middle market companies. These private equity funds generally seek to leverage their investments by combining their capital with loans provided by other sources, and we believe that our investment strategy positions us well to invest alongside such private equity investors. In addition, we believe the large amount of uninvested capital held by private equity buyout firms in North America, estimated by Preqin Ltd., an alternative assets industry data and research company, to be $541 billion as of August 2022, will continue to drive deal activity.

8

Attractive Market Segment. We believe that the underserved nature of such a large segment of the market can at times create a significant opportunity for investment. In many environments, we believe that middle market companies are more likely to offer attractive economics in terms of transaction pricing, up-front and ongoing fees, prepayment penalties and security features in the form of stricter covenants and quality collateral than loans to larger companies. In addition, as compared to larger companies, middle market companies often have simpler capital structures and carry less leverage, thus aiding the structuring and negotiation process and allowing us greater flexibility in structuring favorable transactions.

Attractive Deal Structure and Terms

We believe senior secured debt provides strong defensive characteristics. Because this debt has priority in payment among an issuer’s security holders (i.e., holders are due to receive payment before junior creditors and equity holders), they carry less potential risk than other investments in the issuer’s capital structure. Further, these investments are secured by the issuer’s assets, which may be seized in the event of a default, if necessary. They generally also carry restrictive covenants aimed at ensuring repayment before junior creditors, such as most types of unsecured bondholders, and other security holders and preserving collateral to protect against credit deterioration.

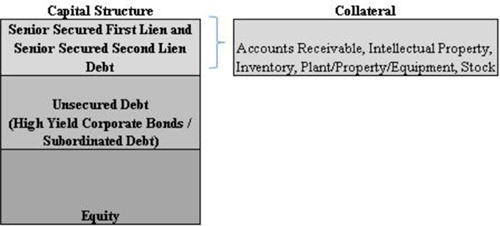

The chart below illustrates examples of the collateral used to secure senior secured first lien debt and senior secured second lien debt.

Investments in Floating Rate Debt

A large portion of the investments we expect to make in middle market companies are expected to be in the form of floating rate debt instruments. These floating rate debt instruments are expected to be below investment grade rated (which are often referred to as “high yield” or “junk”). Floating rate loans have a base rate that adjusts periodically plus a spread over the base rate. The base rate typically resets every 30-90 days. As the reference rate increases, the income stream from these floating rate instruments will also increase. Syndicated floating rate debt offers certain benefits: