Exhibit 99.1

Dear Shareholders and Friends of First Business,

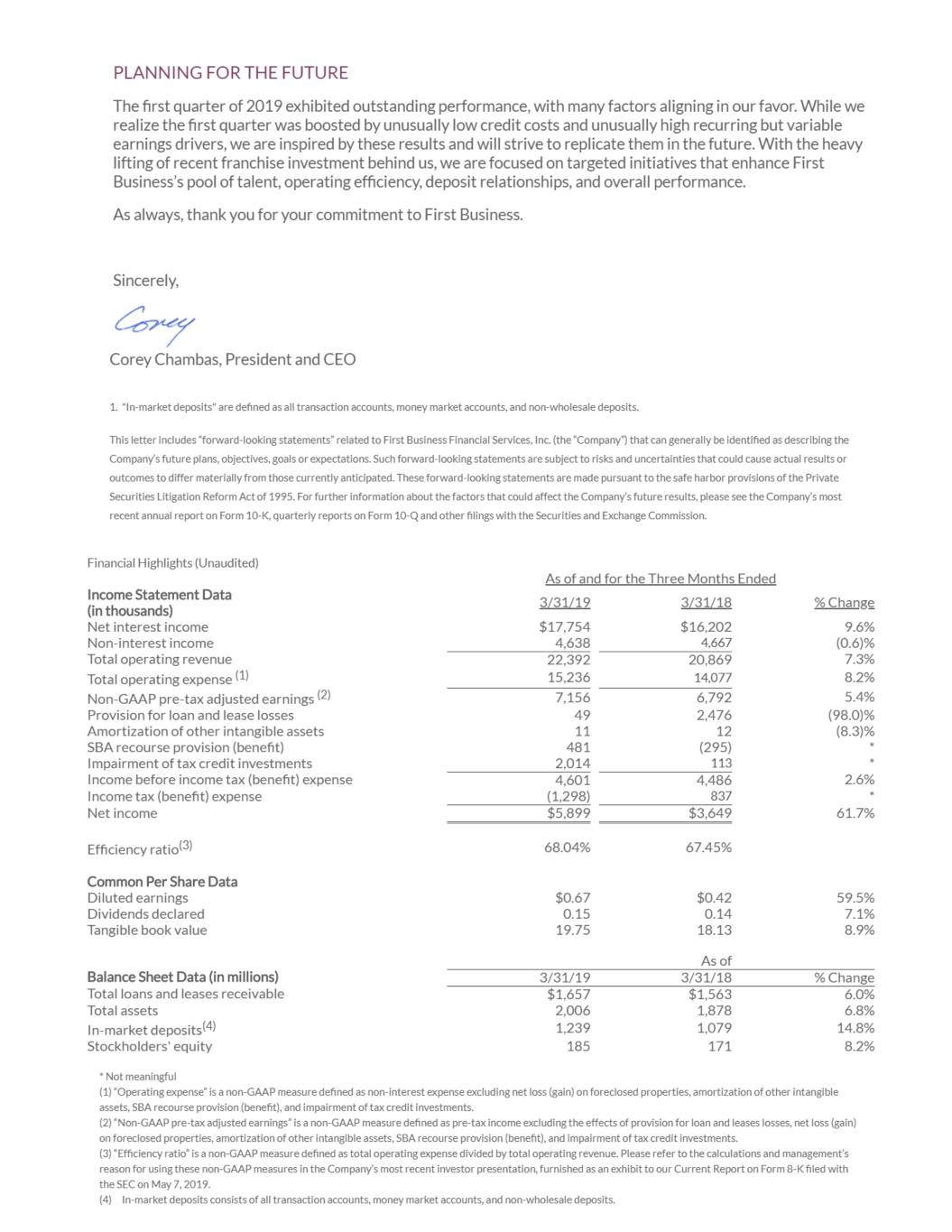

Exceptional first quarter 2019 results reinforced our team’s commitment to the momentum we are building at First Business. Net income, top line revenue, loans, deposits, and trust assets under administration all reached record quarterly levels. First Business produced a return on average assets of 1.20% and a return on average equity of 13.67%, both high water marks in recent quarters.

The fundamentals supporting our record performance are a direct result of our strategic investments in infrastructure and talent. These include our ongoing efforts to increase private wealth management relationships, SBA lending production, and commercial banking market share by prudently and opportunistically investing in production talent. To that end, producers were added across multiple business lines, particularly in our markets outside of Madison.

We believe attracting, developing, and retaining high-performing employees enhances our long-term relationships with clients, and ultimately our shareholder returns. The high-caliber talent we attract is a competitive advantage that we believe will produce quality, sustainable growth.

CONSISTENT EXECUTION DELIVERS QUALITY GROWTH

During the first quarter of 2019, First Business surpassed $2 billion in assets for the first time ever. The milestone was achieved just over 10 years after reaching $1 billion in assets in the fourth quarter of 2008. In the interim 10 years, we steadily executed our entrepreneurial, niche-market business banking strategy as the company evolved with the addition of new businesses and markets.

Over the same 10-year period, we delivered compound average annual growth in: assets of 7%, loans of 7%, and revenues of 10%. As a growth-oriented and entrepreneurial bank, we have continually prioritized investment for growth. The merit of that approach is evident in our bottom line expansion: diluted earnings per share grew approximately 12% per year over the last decade, on a compound average annual basis. Over the same time frame, our stock price expanded at a compound annual rate of nearly 12%. These results demonstrate the power of persistence. By staying true to our model, we have been able to consistently add talent, attract new quality client relationships, and develop new business lines. All of these things have allowed us to provide long-term shareholder value despite periods of short-term variability.

STRONG CORE FUNDAMENTALS DRIVE PERFORMANCE

We are very excited about our results for the first quarter of 2019 — not only because they are outstanding on headline, but because they demonstrate robust strength and momentum across the core fundamentals of our company’s profitability and multiple aspects of our business.

In the second half of 2018, we launched deposit campaigns designed for high net worth clients as part of our private wealth management growth initiative. Certificate of deposit and money market promotions in our less mature markets contributed to in-market deposit growth of $60.0 million, or 20.4%, annualized, during the first quarter, helping to expand our ratio of in-market deposits to total bank funding to 70.9% as of March 31, 20191. The successful promotions complemented solid deposit generation from commercial banking relationships, driving in-market deposit balances to a record $1.239 billion.

In-market, relationship deposit expansion is a key area of focus for First Business. Robust deposit generation over the past year supported record loan balances and a solid net interest margin during the first quarter. Business development efforts enabled us to fully fund our above-average loan growth with local in-market deposits priced at or below the alternative cost of wholesale funding. We continue to prioritize in-market deposit generation and believe this will also generate new private wealth client opportunities for our trust and investment area.

Solid production drove period-end gross loans and leases receivable up 9.6% annualized during the first quarter to $1.657 billion at March 31, 2019, in what is historically our slowest quarter for loan growth due to seasonal factors. This marked our sixth consecutive quarter of record loan balances, and we are pleased to report growth occurred across essentially all of our lending portfolios and geographies.

Although our markets remain very competitive, we were able to show exceptional loan and deposit growth and still maintain a strong net interest margin. We expect our strategies will continue to allow the company to maintain a net interest margin at or above our target of 3.50%, providing robust net interest income growth to support our long-term revenue growth objectives.

Diverse fee income sources, representing 20.7% of total revenue in the first quarter, are also integral to First Business’s core earnings power, and trust fee income, service charge income, and other fee income each brought reliable strength to first quarter results. We expect continued growth in trust fee income after the addition of a wealth advisor in Kansas City expands our private wealth presence to all of our markets.

RECURRING VARIABLE REVENUE SOURCES BOOST CORE PERFORMANCE

First quarter results also demonstrated the importance of those drivers of performance that are recurring but can fluctuate from period to period. The timing of each is driven to a meaningful degree by factors outside First Business’s control. Nonetheless, they are a recurring, core part of our business and serve a critical role in diversifying and boosting our income stream.

Net interest income can experience spikes due to fees collected in lieu of interest, which are the result of loan prepayments and non-accrual interest recoveries. Such fees totaled an unusually high $2.2 million in the first quarter of 2019. This impact, which is primarily driven by our asset-based lending business, helped grow net interest margin to 3.79% — meaningfully above our target 3.50% level.

Fee income similarly benefited from robust client swap fee activity, with swap fee income totaling $473,000 in the first quarter of 2019. While this is a strong earnings driver, the amount can vary on a quarterly basis as activity level and fee income associated with this product are dependent on client demand and interest rate expectations.

Another key catalyst for our earnings power is SBA lending, which we believe is primed for profitable growth following significant investments in our platform and new producers. We see strong pipelines, however, loan sale gains are largely dependent on the timing of loan sales. We believe our differentiated SBA client acquisition strategy has the potential to produce quarterly revenues at a multiple of the first quarter’s $242,000.

We are pleased with the progress of our improving credit profile and expect headwinds related to our legacy SBA portfolio to diminish over time as it rolls off. While we continue to anticipate volatility in credit outcomes from this portfolio, we are encouraged by the first quarter’s low overall net charge-off levels, improved ratio of non-performing loans to total loans, significant reduction in criticized assets, and strong coverage ratio. Our outlook on asset quality improvement in the coming quarters remains positive.

Finally, historic tax credit investments, while not occurring every quarter, can provide a net benefit to our earnings, with variable timing based on project completion and building occupancy. Our active in-market historic tax credit investing program contributed $846,000, or $0.10 per share, to first quarter 2019 results, already in excess of the total recognized in all of 2018. We intend to continue actively pursuing in-market historic tax credit opportunities throughout 2019 and beyond.

PLANNING FOR THE FUTURE

The first quarter of 2019 exhibited outstanding performance, with many factors aligning in our favor. While we realize the first quarter was boosted by unusually low credit costs and unusually high recurring but variable earnings drivers, we are inspired by these results and will strive to replicate them in the future. With the heavy lifting of recent franchise investment behind us, we are focused on targeted initiatives that enhance First Business’s pool of talent, operating efficiency, deposit relationships, and overall performance.

As always, thank you for your commitment to First Business.

Sincerely,

Corey Chambas, President and CEO

| |

| 1. | "In-market deposits" are defined as all transaction accounts, money market accounts, and non-wholesale deposits. |

This letter includes “forward-looking statements” related to First Business Financial Services, Inc. (the “Company”) that can generally be identified as describing the Company’s future plans, objectives, goals or expectations. Such forward-looking statements are subject to risks and uncertainties that could cause actual results or outcomes to differ materially from those currently anticipated. These forward-looking statements are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. For further information about the factors that could affect the Company’s future results, please see the Company’s most recent annual report on Form 10-K, quarterly reports on Form 10-Q and other filings with the Securities and Exchange Commission.