FILED PURSUANT TO RULE 424(b)(2)

Registration No. 333-171055-01

333-171055-02

333-171055-03

PROSPECTUS SUPPLEMENT DATED MARCH 17, 2014

(to Prospectus dated February 26, 2014 )

Citibank Credit Card Issuance Trust

Issuing Entity

$350,000,000 Floating Rate Class 2013-A7 Notes of September 2018

(Legal Maturity Date September 2020)

Citibank, N.A.

Sponsor and Depositor

| | |

| The issuance trust will issue and sell | | Class 2013-A7 Notes

|

Principal amount | | $350,000,000 |

Interest rate | | one-month LIBOR plus 0.43% per annum |

Interest payment dates | | 10thday of each month, beginning April 2014 |

Expected principal payment date | | September 10, 2018 |

Legal maturity date | | September 10, 2020 |

Expected issuance date | | March 24, 2014 |

Price to public | | $350,943,250 (or 100.2695%) |

Underwriting discount | | $ 962,500 (or 0.2750%) |

Proceeds to the issuance trust | | $349,980,750 (or 99.9945%) |

The price to public and proceeds to the issuance trust set forth above do not include accrued interest on these Class A notes which must be paid by the purchasers. Interest on these Class A notes will accrue from March 10, 2014 to the date of delivery.

These Class A notes form a part of the same subclass and have the same terms as, and are fungible with, the issuance trust’s outstanding $1,575,000,000 Floating Rate Class 2013-A7 notes of September 2018 (legal maturity date September 2020) issued on September 23, 2013 in the principal amount of $650,000,000, on November 21, 2013 in the principal amount of $525,000,000 and on December 17, 2013 in the principal amount of $400,000,000. Upon completion of this offering, the aggregate outstanding dollar principal amount of Class 2013-A7 notes will be $1,925,000,000.

The Class 2013-A7 notes will be paid from the issuance trust’s assets consisting primarily of an interest in credit card receivables arising in a portfolio of revolving credit card accounts.

The Class 2013-A7 notes are a subclass of Class A notes of the Citiseries. Principal payments on Class B notes of the Citiseries are subordinated to payments on Class A notes of that series. Principal payments on Class C notes of the Citiseries are subordinated to payments on Class A and Class B notes of that series.

See page S-4 for a description of how LIBOR is determined

You should review and consider the discussion under “Risk Factors” beginning on page 17 of the accompanying prospectus before you purchase any notes.

Neither the Securities and Exchange Commission nor any state securities commission has approved the notes or determined that this prospectus supplement or the prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The notes are obligations of Citibank Credit Card Issuance Trust only and are not obligations of or interests in any other person. Each class of notes is secured by only some of the assets of Citibank Credit Card Issuance Trust. Noteholders will have no recourse to any other assets of Citibank Credit Card Issuance Trust for the payment of the notes. The notes are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency or instrumentality.

Underwriters

| | | | | | |

| Citigroup | | | | | | |

| | | BofA Merrill Lynch | | |

| | | | | | | RBS |

TABLE OF CONTENTS

Prospectus Supplement

The table of contents for the prospectus begins on page (i) of that document.

Information about these Class A notes is in two separate documents: a prospectus and a prospectus supplement. The prospectus provides general information about each series of notes issued by Citibank Credit Card Issuance Trust, some of which may not apply to the Citiseries. The prospectus supplement provides the specific terms of these Class A notes. You should carefully read both the prospectus and the prospectus supplement before you purchase any of these Class A notes.

This prospectus supplement may supplement disclosure in the accompanying prospectus.

In deciding whether to purchase these Class A notes, you should rely solely on the information in this prospectus supplement and the accompanying prospectus. We have not authorized anyone to give you different information about these Class A notes.

This prospectus supplement may be used to offer and sell these Class A notes only if accompanied by the prospectus.

These Class A notes are offered subject to receipt and acceptance by the underwriters and to their right to reject any order in whole or in part and to withdraw, cancel or modify the offer without notice.

S-2

SUMMARY OF TERMS

Because this is a summary, it does not contain all the information you may need to make an informed investment decision. You should read the entire prospectus supplement and prospectus before you purchase any of these Class A notes.

There is a glossary beginning on page 137 of the prospectus where you will find the definitions of some terms used in this prospectus supplement.

Securities Offered | $350,000,000 Floating Rate Class 2013-A7 notes of September 2018 (legal maturity date September 2020). |

| | These Class A notes form a part of the same subclass and have the same terms—other than the issuance date—as, and are fungible with, the issuance trust’s outstanding $1,575,000,000 Floating Rate Class 2013-A7 notes of September 2018 (legal maturity date September 2020) issued on September 23, 2013 in the principal amount of $650,000,000, on November 21, 2013 in the principal amount of $525,000,000 and on December 17, 2013 in the principal amount of $400,000,000. These Class A notes have the same CUSIP Number as, and upon closing will trade interchangeably with, the other outstanding Class 2013-A7 notes. Upon completion of this offering, the aggregate outstanding dollar principal amount of Class 2013-A7 notes will be $1,925,000,000. |

| | These Class A notes are part of a multiple issuance series of notes called the Citiseries. The Citiseries consists of Class A notes, Class B notes and Class C notes. These Class A notes are a subclass of Class A notes of the Citiseries. |

| | These Class A notes are issued by, and are obligations of, Citibank Credit Card Issuance Trust. The issuance trust has issued and expects to issue other classes and subclasses of notes of the Citiseries with different interest rates, payment dates, legal maturity dates and other characteristics. The issuance trust may also issue additional Class 2013-A7 notes in the future. Holders of these Class A notes will not receive notice of, or have the right to consent to, any subsequent issuance of notes, including any issuance of additional Class 2013-A7 notes. See “The Notes—Issuances of New Series, Classes and Subclasses of Notes” in the prospectus. |

S-3

Multiple Issuance Series | A multiple issuance series is a series of notes consisting of three classes: Class A, Class B and Class C. Each class may consist of multiple subclasses. Notes of any subclass can be issued on any date so long as there are enough outstanding subordinated notes to provide the necessary subordination protection for outstanding and newly issued senior notes. The expected principal payment dates and legal maturity dates of the senior and subordinated classes of a multiple issuance series may be different, and subordinated notes may have expected principal payment dates and legal maturity dates earlier than some or all senior notes of the same series. Subordinated notes will generally not be paid before their legal maturity date, unless, after payment, the remaining subordinated notes provide the required amount of subordination protection for the senior notes of that series. |

| | All of the subordinated notes of a multiple issuance series provide subordination protection to the senior notes of the same series to the extent of the required subordinated amount, regardless of whether the subordinated notes are issued before, at the same time as, or after the senior notes of that series. |

Interest | These Class A notes will accrue interest at a per annum rate equal to the one-month LIBOR rate for U.S. dollar deposits for the applicable interest periodplusa margin of 0.43%. The interest rate for the interest period beginning March 10, 2014 will be 0.58440%. |

| Interest on these Class A notes will accrue from March 10, 2014 and will be calculated on the basis of the actual number of days in the year divided by a 360-day year. |

| The LIBOR rate for each interest period will be determined by the issuance trust two business days before the beginning of that interest period. For purposes of determining LIBOR, a business day is any day on which dealings in deposits in U.S. dollars are transacted in the London interbank market. The applicable LIBOR rate will be the rate for deposits in U.S. dollars for the applicable interest period which appears on the Reuters Screen LIBOR01 Page (successor to Telerate Page 3750)—or any |

S-4

| | other page as may replace that page on that service or any successor service for the purpose of displaying comparable rates or prices—as of 11:00 a.m., London time, on that date. |

| If the LIBOR rate does not appear on the Reuters Screen LIBOR01 Page (successor to Telerate Page 3750)—or any other page as may replace that page on that service or any successor service for the purpose of displaying comparable rates or prices—the LIBOR rate for the applicable interest period will be determined on the basis of the rate at which deposits in U.S. dollars are offered by four major banks in the London interbank market, selected by the issuance trust, at approximately 11:00 a.m., London time, on that day to prime banks in the London interbank market for the applicable interest period. |

| The issuance trust will request the principal London office of each reference bank to provide a quotation of its LIBOR rate for the applicable interest period. If at least two quotations are provided as requested, the applicable LIBOR rate will be the arithmetic mean of the quotations. If fewer than two quotations are provided as requested, the applicable LIBOR rate will be the arithmetic mean of the rates quoted by major banks in New York City, selected by the issuance trust, at approximately 11:00 a.m., New York City time, on that day for loans in U.S. dollars to leading European banks for the applicable interest period. |

| The payment of accrued interest on a class of notes of the Citiseries from finance charge collections is not senior to or subordinated to payment of interest on any other class of notes of the Citiseries. |

| The issuance trust will make interest payments on these Class A notes on the 10th day of each month, beginning April 2014. Interest payments due on a day that is not a business day in New York and South Dakota will be made on the following business day. |

| As a result of concerns in recent years regarding the accuracy of LIBOR, changes have been made to the administration and process for determining LIBOR, including increasing the number of banks surveyed to set |

S-5

| | LIBOR, streamlining the number of LIBOR currencies and maturities and generally strengthening the oversight of the process, including by providing for U.K. regulatory oversight of LIBOR. In early 2014, Intercontinental Exchange (ICE) took over the administration of LIBOR from the British Banker’s Association (BBA). |

| It is uncertain whether or to what extent any further changes in the administration or method for determining LIBOR could have on the value of any LIBOR-linked notes issued by the issuance trust, including these Class A notes, or any loans, derivatives and other financial obligations or extensions of credit for which the issuance trust or Citibank, N.A. is an obligor. It is also not certain whether or to what extent any such changes would have an adverse impact on the value of any LIBOR-linked securities, loans, derivatives and other financial obligations or extensions of credit held by or due to the issuance trust or Citibank, N.A. or on the issuance trust or Citibank, N.A.’s overall financial condition or results of operations. |

Principal | The issuance trust expects to pay the stated principal amount of these Class A notes in one payment on September 10, 2018, which is the expected principal payment date, and is obligated to do so if funds are available for that purpose. However, if the stated principal amount of these Class A notes is not paid in full on the expected principal payment date, noteholders will not have any remedies against the issuance trust until September 10, 2020, the legal maturity date of these Class A notes. |

| | If the stated principal amount of these Class A notes is not paid in full on the expected principal payment date, then subject to the principal payment rules described below principal and interest payments on these Class A notes will be made monthly until they are paid in full or the legal maturity date occurs, whichever is earlier. However, if the nominal liquidation amount of these Class A notes has been reduced, the amount of principal collections and finance charge collections available to pay principal of and interest on these Class A notes will be reduced. The nominal liquidation amount of a class of notes corresponds to the portion of the invested amount of the collateral certificate that is allocable to support that class of notes. |

S-6

| | The initial nominal liquidation amount of these Class A notes is $350,000,000. If this amount is reduced as a result of charge-offs to the principal receivables in the master trust, and not reimbursed as described in the prospectus, not all of the principal of these Class A notes will be repaid. For a more detailed discussion of nominal liquidation amount, see “The Notes—Stated Principal Amount, Outstanding Dollar Principal Amount and Nominal Liquidation Amount of Notes” in the prospectus. |

| | Principal of these Class A notes may be paid earlier than the expected principal payment date if an early redemption event or an event of default occurs with respect to these notes. See “Covenants, Events of Default and Early Redemption Events—Early Redemption Events” and “—Events of Default” in the prospectus. |

| | If principal payments on these Class A notes are made earlier or later than the expected principal payment date, the monthly principal date for principal payments will be the 10th day of each month, or if that day is not a business day, the following business day. |

Monthly Accumulation Amount | $29,166,666.67. This amount is one-twelfth of the initial dollar principal amount of these Class A notes, and is targeted to be deposited in the principal funding subaccount for these Class A notes each month beginning with the twelfth month before the expected principal payment date of these Class A notes. This amount will be increased if the date for beginning the budgeted deposits is postponed, as described under “Deposit and Application of Funds—Targeted Deposits of Principal Collections to the Principal Funding Account—Budgeted Deposits” in the prospectus. |

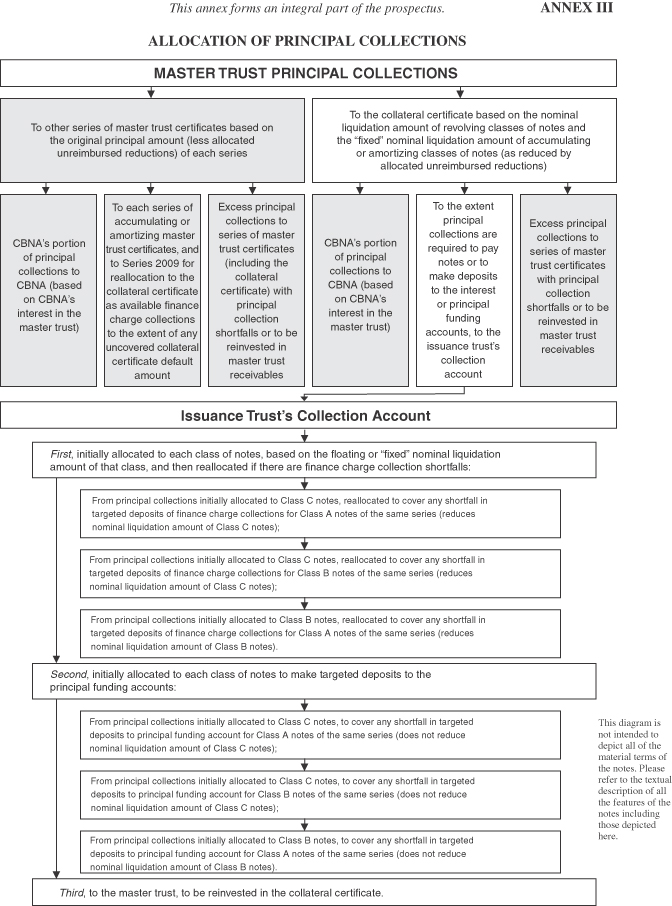

Subordination; Credit Enhancement | No payment of principal will be made on any Class B note of the Citiseries unless, following the payment, the remaining available subordinated amount of Class B notes of this series is at least equal to the required subordinated amount for the outstanding Class A notes of this series. |

| | Similarly, no payment of principal will be made on any Class C note of the Citiseries unless, following the payment, the remaining available subordinated amount of |

S-7

| | Class C notes of this series is at least equal to the required subordinated amounts for the outstanding Class A notes and Class B notes of this series. However, there are some exceptions to this rule. See “The Notes—Subordination of Principal” and “Deposit and Application of Funds—Limit on Repayments of Subordinated Classes of Multiple Issuance Series” in the prospectus. |

| | The maximum amount of principal of Class B notes of the Citiseries that may be applied to provide subordination protection to these Class A notes is $20,940,185 (5.98291% of the initial principal amount of these Class A notes). The maximum amount of principal of Class C notes of the Citiseries that may be applied to provide subordination protection to these Class A notes is $27,920,235 (7.97721% of the initial principal amount of these Class A notes). This amount of principal of Class C notes may also be applied to provide subordination protection to the Class B notes of the Citiseries. |

| | The issuance trust may at any time change the amount of subordination required or available for any class of notes of the Citiseries, including these Class A notes, or the method of computing the amounts of that subordination without the consent of any noteholders so long as the issuance trust has received confirmation from the rating agencies that have rated any outstanding notes of the Citiseries that the change will not result in the rating assigned to any outstanding notes of the Citiseries to be withdrawn or reduced, and the issuance trust has received the tax opinions described in “The Notes—Required Subordinated Amount” in the prospectus. |

| | See “Deposit and Application of Funds” in the prospectus for a description of the subordination protection of these Class A notes. |

Optional Redemption by the Issuance Trust | The issuance trust has the right, but not the obligation, to redeem these Class A notes in whole but not in part on any |

| | day on or after the day on which the aggregate nominal liquidation amount of these Class A notes is reduced to less than 5% of its initial dollar principal amount. This repurchase option is referred to as a clean-up call. |

S-8

| | If the issuance trust elects to redeem these Class A notes, it will notify the registered holders of the redemption at least 30 days prior to the redemption date. The redemption price of a note so redeemed will equal 100% of the outstanding dollar principal amount of that note, plus accrued but unpaid interest on the note to but excluding the date of redemption. |

| | If the issuance trust is unable to pay the redemption price in full on the redemption date, monthly payments on these Class A notes will thereafter be made until the outstanding dollar principal amount of these Class A notes, plus all accrued and unpaid interest, is paid in full or the legal maturity date occurs, whichever is earlier. Any funds in the principal funding subaccount and interest funding subaccount for these Class A notes will be applied to make the principal and interest payments on these Class A notes on the redemption date. |

Security for the Notes | These Class A notes are secured by a shared security interest in the collateral certificate and the collection account, but are entitled to the benefits of only that portion of those assets allocated to them under the indenture. These Class A notes are also secured by a security interest in the applicable principal funding subaccount and the applicable interest funding subaccount. See “Sources of Funds to Pay the Notes—The Collateral Certificate” and “—The Trust Accounts” in the prospectus. |

Limited Recourse to the Issuance Trust | The sole source of payment for principal of or interest on these Class A notes is provided by: |

| | Ÿ | | the portion of the principal collections and finance charge collections received by the issuance trust under the collateral certificate and available to these Class A notes after giving effect to all allocations and reallocations; and |

| | Ÿ | | funds in the applicable trust accounts for these Class A notes; |

| | Class A noteholders will have no recourse to any other assets of the issuance trust or any other person or entity for the payment of principal of or interest on these Class A notes. |

S-9

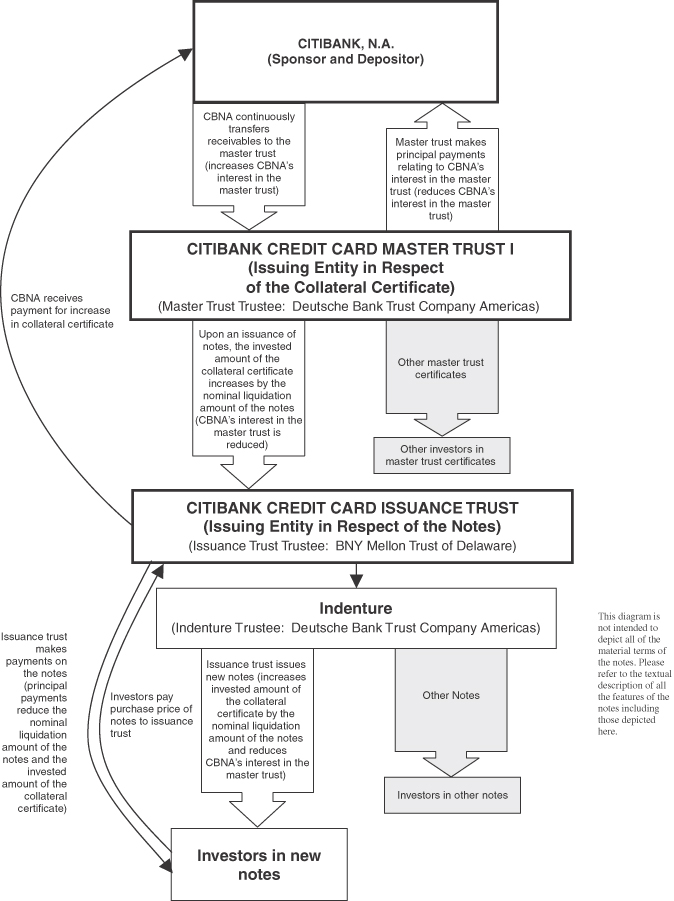

Master Trust Assets and Receivables | The collateral certificate, which is the issuance trust’s primary source of funds for the payment of principal of and interest on these Class A notes, is an investor certificate issued by Citibank Credit Card Master Trust I. The collateral certificate represents an undivided interest in the assets of the master trust. The master trust assets include credit card receivables from selected MasterCard, VISA and American Express revolving credit card accounts that meet the eligibility criteria for inclusion in the master trust. These eligibility criteria are discussed in the prospectus under “The Master Trust—Master Trust Assets.” |

| | The credit card receivables in the master trust consist of principal receivables and finance charge receivables. Principal receivables include amounts charged by cardholders for merchandise and services and amounts advanced to cardholders as cash advances. Finance charge receivables include periodic finance charges, annual membership fees, cash advance fees, late charges and some other fees billed to cardholders, as well as amounts representing a discount from the face amount of principal receivables. |

| | The aggregate amount of credit card receivables in the master trust as of January 26, 2014 was $50,163,694,075, of which $49,588,496,084 were principal receivables and $575,197,991 were finance charge receivables. Citibank may from time to time execute substantial lump removals of credit card receivables in excess of the required seller’s interest (as determined by the pooling and servicing agreement and the rating agencies). See “The Master Trust Receivables and Accounts” in Annex I of this prospectus supplement for more detailed financial information on the receivables and the accounts. |

| | On or about March 22, 2014, Citibank intends to designate a random selection of additional eligible credit card accounts to the master trust, the receivables in which will be sold and assigned to the master trust in a lump addition in the amount of approximately $2 billion. Citibank believes these additional accounts and the related receivables are substantially similar to the accounts currently designated to the master trust and their related receivables. Therefore, Citibank believes the lump addition will not have a material adverse impact on the financial performance of the master trust. |

S-10

In addition:

| | Ÿ | | Citibank may at its option designate additional credit card accounts to the master trust, and the receivables arising in those accounts will then be transferred daily to the master trust. |

| | Ÿ | | If the amount of receivables in the master trust falls below a required minimum amount, Citibank is required to designate additional accounts to the master trust. |

| | Ÿ | | Citibank may also designate newly originated accounts to the master trust. The number of newly originated accounts that may be designated to the master trust is limited to quarterly and yearly maximums. |

| | Ÿ | | Citibank may remove receivables from the master trust by ending the designation of the related account to the master trust. |

| | All additions and removals of accounts are subject to additional conditions. See “The Master Trust–Master Trust Assets” in the prospectus for a fuller description. |

The Citiseries | As of March 17, 2014, there were 50 subclasses of notes of the Citiseries outstanding, with an aggregate outstanding dollar principal amount of $35,346,931,344, consisting of: |

| | Class A notes $30,890,931,344 |

Class B notes $1,908,000,000

Class C notes $2,548,000,000

| | As of March 17, 2014, the weighted average interest rate payable by the issuance trust in respect of the outstanding subclasses of notes of the Citiseries was 1.57% per annum, consisting of: |

| | Class A notes 1.68% per annum |

Class B notes 0.66% per annum

Class C notes 1.03% per annum

The weighted average interest rate calculation takes into account:

| | Ÿ | | the actual rate of interest in effect on floating rate notes at the time of calculation; and |

| | Ÿ | | all net payments to be made or received under performing derivative agreements. |

S-11

| | No series of issuance trust notes other than the Citiseries is currently outstanding. |

| | For a list and description of each outstanding subclass of notes of the Citiseries, see the issuance trust’s monthly reports filed with the Securities and Exchange Commission on Form 10-D. |

Other Master Trust Series | The collateral certificate is a certificate of beneficial ownership issued by the master trust. Pursuant to an amended and restated supplement to the pooling and servicing agreement dated May 1, 2009, as amended and restated as of August 9, 2011, as further amended as of July 10, 2012, the master trust issued a new certificate of beneficial interest—the Series 2009 certificate—to the seller in order to provide credit enhancement to the collateral certificate and the notes. The Series 2009 certificate has a fluctuating principal amount which will generally equal 7.66865% of the invested amount of the collateral certificate (which equals the aggregate nominal liquidation amount of all of the issuance trust’s notes). For a description of the Series 2009 certificate, see “The Master Trust—The Series 2009 Certificate” in the prospectus. |

| | In addition to the collateral certificate and the Series 2009 certificate, other master trust certificates may be issued from time to time. See “The Master Trust—Allocation of Collections, Losses and Fees” in the prospectus. |

| | No master trust certificates other than the collateral certificate and the Series 2009 certificate are currently outstanding. |

Participation with Other Classes of Notes | Each class of notes of the Citiseries will be included in “Group 1.” In addition to the Citiseries, the issuance trust may issue other series of notes that are included in Group 1. |

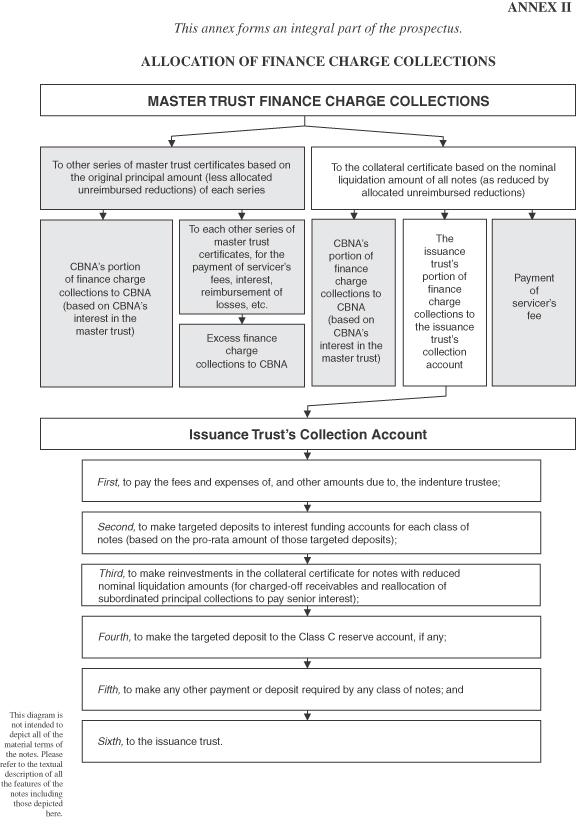

| | Collections of finance charge receivables allocable to each class of notes in Group 1 will be aggregated and shared by each class of notes in Group 1 pro rata based on the applicable interest rate of each class. See “Deposit and Application of Funds—Allocation to Interest Funding Subaccounts” in the prospectus. Under this system, classes of notes in Group 1 with high interest rates take a larger |

S-12

| | proportion of the collections of finance charge receivables allocated to Group 1 than classes of notes with low interest rates. Consequently, the issuance of later classes of notes with high interest rates can have the effect of reducing the finance charge collections available to pay interest on your notes, or available to reimburse reductions in the nominal liquidation amount of your notes. |

No Listing | The Class A notes will not be listed on any stock exchange. |

Denominations | These Class A notes will be issued in minimum denominations of $100,000 and multiples of $1,000 in excess of that amount. |

Ratings | The issuance trust will issue these Class A notes only if they are rated “AAA” or its equivalent by at least one nationally recognized rating agency. See “Risk Factors—If the ratings of the notes are lowered or withdrawn, or if an unsolicited rating is issued, the market value of the notes could decrease” in the prospectus. Citibank expects at least one nationally recognized rating agency to monitor these Class A notes as long as they are outstanding. |

S-13

UNDERWRITING

Subject to the terms and conditions of the underwriting agreement for these Class A notes, the issuance trust has agreed to sell to each of the underwriters named below, and each of those underwriters has severally agreed to purchase, the principal amount of these Class A notes set forth opposite its name:

| | | | |

Underwriters

| | Principal Amount

| |

Citigroup Global Markets Inc. | | $ | 118,000,000 | |

BofA Merrill Lynch | | | 116,000,000 | |

RBS Securities Inc. | | | 116,000,000 | |

| | |

|

|

|

Total | | $ | 350,000,000 | |

| | |

|

|

|

The several underwriters have agreed, subject to the terms and conditions of the underwriting agreement, to purchase all $350,000,000 aggregate principal amount of these Class A notes if any of these Class A notes are purchased.

The underwriters have advised the issuance trust that the several underwriters propose initially to offer these Class A notes to the public at the public offering price set forth on the cover page of this prospectus supplement, and to certain dealers at that public offering price less a concession not in excess of 0.165% of the principal amount of these Class A notes. The underwriters may allow, and those dealers may reallow to other dealers, a concession not in excess of 0.099% of the principal amount.

After the public offering, the public offering price and other selling terms may be changed by the underwriters.

Each underwriter of these Class A notes has agreed that:

| | • | | it has complied and will comply with all applicable provisions of the Financial Services and Markets Act 2000 (the “FSMA”) with respect to anything done by it in relation to these Class A notes in, from or otherwise involving the United Kingdom; and |

| | • | | it has only communicated or caused to be communicated or will only communicate or cause to be communicated any invitation or inducement to engage in investment activities (within the meaning of Section 21 of the FSMA) received by it in connection with the issue or sale of any of these Class A notes in circumstances in which Section 21(1) of the FSMA does not apply to the issuance trust. |

In connection with the sale of these Class A notes, the underwriters may engage in:

| | • | | over-allotments, in which members of the syndicate selling these Class A notes sell more notes than the issuance trust actually sold to the syndicate, creating a syndicate short position; |

S-14

| | • | | stabilizing transactions, in which purchases and sales of these Class A notes may be made by the members of the selling syndicate at prices that do not exceed a specified maximum; |

| | • | | syndicate covering transactions, in which members of the selling syndicate purchase these Class A notes in the open market after the distribution has been completed in order to cover syndicate short positions; and |

| | • | | penalty bids, by which underwriters reclaim a selling concession from a syndicate member when any of these Class A notes originally sold by that syndicate member are purchased in a syndicate covering transaction to cover syndicate short positions. |

These stabilizing transactions, syndicate covering transactions and penalty bids may cause the price of these Class A notes to be higher than it would otherwise be. These transactions, if commenced, may be discontinued at any time.

The issuance trust and Citibank will, jointly and severally, indemnify the underwriters against certain liabilities, including liabilities under applicable securities laws, or contribute to payments the underwriters may be required to make in respect of those liabilities. The issuance trust’s obligation to indemnify the underwriters will be limited to finance charge collections from the collateral certificate received by the issuance trust after making all required payments and required deposits under the indenture.

Citigroup Global Markets Inc. is an affiliate of the issuance trust and Citibank.

The proceeds to the issuance trust from the sale of these Class A notes and the underwriting discount are set forth on the cover page of this prospectus supplement. The proceeds to the issuance trust will be paid to Citibank. See “Use of Proceeds” in the prospectus. Additional offering expenses are estimated to be $175,000.

REVIEW OF DISCLOSURE REGARDING MASTER TRUST ASSETS

Citibank has performed a review of the master trust receivables and accounts and the disclosure regarding those assets as required by Rule 193 under the Securities Act of 1933, as amended. The purpose of this review was to provide Citibank with reasonable assurance that the disclosure regarding the master trust assets in this prospectus supplement and the accompanying prospectus is accurate in all material respects.

As part of the review, Citibank identified the information concerning the master trust assets to be covered and determined the review procedures for each portion of that information. Factual information was reviewed by those officers and employees of Citibank and its affiliates who are knowledgeable about that information. Counsel to Citibank reviewed the portions of the descriptions of the transaction documents regarding the master trust assets and compared those descriptions to the related transaction documents to ensure that the descriptions were accurate in all material respects. Officers and employees of Citibank and its affiliates also consulted with counsel with respect to the description of the legal and regulatory

S-15

provisions that may materially and adversely affect the performance of the credit card receivables or payments on the notes.

Employees of Citibank and its affiliates reviewed the statistical information with respect to the master trust receivables and accounts contained in “The Master Trust Receivables and Accounts” in Annex I of this prospectus supplement. As part of the review, such employees sampled 5,000 credit card accounts randomly selected from the consumer credit card accounts and 5,000 credit card accounts randomly selected from Citibank/American Airlines AAdvantage commercial accounts designated to the master trust and compared the stratification results of certain information relating to those accounts—including obligor address, obligor FICO score, account balance, payment status, age of account, and whether the account is subject to a loan modification—to the related statistical information contained in “The Master Trust Receivables and Accounts.” The stratification results of the selected accounts were found to be materially consistent with the related statistical information. Citibank also engaged a third party to assist in its review of such statistical information. In accordance with Citibank’s instructions, the third party compared information derived from Citibank’s computer systems regarding the attributes of the master trust receivables and accounts to such statistical information. The results of these reviews, together with Citibank’s control processes used in the operation of its credit card business as described below, provided reasonable assurance that the statistical information relating to the master trust receivables and accounts contained in “The Master Trust Receivables and Accounts” is accurate in all material respects.

Employees of Citibank and its affiliates, with the assistance of a third party engaged by Citibank, also perform certain other reviews of the master trust assets on a periodic basis. Annually, the third party engaged by Citibank, in accordance with Citibank’s instructions, sends confirmation requests to credit card customers asking them to confirm their name, address, account number, date of their last statement, account balance, annual percentage rate for purchases and credit limit. These confirmation requests are sent to more than 900 customers selected randomly in accordance with a procedure designed by the third party using data supplied by Citibank. The third party randomly selects 10% of the confirmations requests and compares the specified customer name, address, account number, date of the last statement, account balance, annual percentage rate for purchases and credit limit as of such statement date to information derived from Citibank’s computer systems. No material discrepancies were noted as a result of the most recent annual review.

Before making lump additions of accounts to the master trust, Citibank identifies accounts that meet the eligibility criteria for addition to the master trust by screening the inventory of accounts owned by Citibank that are not yet designated to the master trust for the applicable characteristics. On an annual basis for each year in which there are lump additions of accounts to the master trust, employees of Citibank and its affiliates, with the assistance of a third party engaged by Citibank, perform additional procedures to assure that the screen properly excluded ineligible accounts.

S-16

With respect to the disclosure in “The Credit Card Business of Citibank—Acquisition of Accounts and Use of Credit Cards” in Annex I of the prospectus, Citibank regularly engages in activities that are designed to monitor and measure compliance with its credit policy. These activities include a Risk Management Control and Oversight program designed to ensure that new credit card account acquisitions and assigned credit limits meet approved Citibank policy. Ongoing performance of the accounts is routinely reviewed by senior management of Citibank’s cards business as well as senior officers in Citigroup’s Global Risk Management department.

Underwriting decisions made using Citibank’s automated approval system are reviewed and affirmed using two primary methods. First, on a quarterly basis, acquisition models are reviewed in a Quarterly Model Validation program to ensure that they are meeting stated performance objectives. Based on the results, adjustments may be made to the score cutoffs or a redevelopment of the score may be required. Additionally, on a monthly basis, new credit card accounts are reviewed as part of the Risk Management Control and Oversight program. This program consists of three parts—exception reports, account monitoring, and interactive reviews such as call monitoring—to ensure that the accounts are within the stated Citibank policy. Citibank considers the decision to approve a new account or a credit limit increase to be an exception to the underwriting criteria only if such decision is a result of an error in processing within the automated approval system. Accounts identified in the exception reports are promptly remediated. All recent results from both the Quarterly Model Validation program and the Risk Management Control and Oversight program have been satisfactory and have verified that the exception rate for new accounts isde minimis.

In accordance with Citibank’s credit policy, some applications are routed for a manual review by the Credit Operations team to make a final credit decision. These decisions are also monitored on a monthly basis by the Risk Management Control and Oversight team using the methods outlined above. Additionally, performance monitoring reports and, if necessary, remedial efforts, for this population of accounts are used to ensure that these accounts adhere to Citibank’s stated policy.

Portions of the review of the legal, regulatory and statistical information were performed with the assistance of third parties engaged by Citibank. Citibank determined the nature, extent and timing of the review and the sufficiency of the assistance provided by the third parties for purposes of Citibank’s review. Citibank had ultimate authority and control over, and assumes all responsibility for, the review and the findings and conclusions of the review. Citibank attributes all findings and conclusions of the review to itself.

Citibank’s review of the master trust accounts and receivables is supported by Citibank’s extensive control processes used in the day-to-day operation of its credit card business. These controls include financial reporting controls, regular internal audits of key business functions, including account origination, servicing and systems processing, controls to verify compliance with procedures and quality assurance reviews for credit decisions and securitization processes. In addition, Citibank has an integrated network of computer applications to make certain that information about the master trust accounts and receivables is accurately entered,

S-17

captured and maintained in its computer systems. These computer systems are subject to change control processes, automated controls testing and control review programs to determine whether systems controls are operating effectively and accurately. All of these controls and procedures ensure the integrity of Citibank’s information systems and the accuracy of disclosures in all material respects.

After completing the review described above, Citibank has concluded that it has reasonable assurance that the disclosure regarding the master trust assets in this prospectus supplement and the accompanying prospectus is accurate in all material respects.

DEMANDS FOR REPURCHASES OF RECEIVABLES

The pooling and servicing agreement contains covenants requiring the repurchase of receivables from the master trust for the breach of a related representation or warranty. No credit card receivables securitized by Citibank were the subject of a demand to repurchase for a breach of the representations and warranties during the three year period ending February 25, 2014. Citibank, as securitizer, discloses all fulfilled and unfulfilled repurchase requests for receivables that were the subject of a demand to repurchase on SEC FormABS-15G. The most recent Form ABS-15G filed by Citibank was filed with the SEC on February 14, 2014 under CIK number 0001541816. Citibank also discloses all such demands for repurchase with respect to the master trust assets in its monthly reports on Form 10-D under CIK number 0001522616. For more information on obtaining a copy of the monthly reports orForm ABS-15G, see “Where You Can Find Additional Information” in the accompanying prospectus.

S-18

ANNEX I

This annex forms an integral part of the prospectus supplement.

THE MASTER TRUST RECEIVABLES AND ACCOUNTS

The following information relates to the credit card receivables owned by Citibank Credit Card Master Trust I and the related credit card accounts.

Reporting System Enhancements

As disclosed in the issuance trust’s quarterly Form 8-K for the second quarter of 2013, filed with the SEC on July 26, 2013 (the “2Q 2013 Form 8-K”), starting with the trust monthly reporting period beginning on April 26, 2013 and ended May 28, 2013, system enhancements have provided management with improved financial reporting for the issuance trust, the master trust’s assets and the collateral certificate.

Implementation of the system enhancements was fully completed during July 2013. As a result, the characterization and recordation of certain cardholder payments, fees, adjustments, returns and reversals (collectively “payments”) were improved for financial reporting purposes for all periods beginning after June 25, 2013. The improved characterization and recording of these payments resulted in a marginal decrease in the reported finance charge payments, interchange and recoveries, and a marginal increase in the reported net credit losses, as compared with the financial reporting if these system enhancements had not been implemented. As a result, Gross Charge-Offs, Recoveries, Finance Charges and Fees Paid, and Revenue Yield as a percentage of total Principal Receivables will each be marginally lower, and Net Losses and Net Losses as a percentage of Gross Charge-Offs will each be marginally higher, for all periods beginning after June 25, 2013, as compared with the information that would have been reported for such items in this Form 8-K reporting period and future reporting periods if the system enhancements had not been implemented.

Financial reporting for all periods beginning after June 25, 2013 is not fully comparable to financial reporting for prior periods. Further, system limitations prevent management from producing data that would have been reported in past periods had the system enhancements been implemented prior to June 25, 2013, other than certain estimates shown in the 2Q 2013 Form 8-K, and also prevent the production of data that would have been reported in this and future periods had the system enhancements not been implemented. Therefore, the variances in the financial reporting for this Annex I and future Form 8-K reporting periods between the reported data and the data that would have been reported had the system enhancements not been implemented will not be available.

Only the financial reporting was impacted by these changes. The master trust’s assets and the servicing of those assets were not impacted. Other than those items discussed above or as previously disclosed, no additional significant impacts to the information reported in this Annex I have been identified as a result of the system enhancements, and management does not currently expect any additional significant impacts to the information reported in this Annex I in the future.

AI-1

Refer to the 2Q 2013 Form 8-K for additional information regarding the system enhancements. In addition, the issuance trust’s Form 10-D’s filed with the SEC on July 15, 2013 and August 15, 2013 described certain impacts to the financial reporting on Form 10-D also as a result of the system enhancements.

Loss and Delinquency Experience

The following table sets forth the loss experience for cardholder payments on the credit card accounts for each of the periods shown on a cash basis. The Net Loss percentage calculated for each period below is obtained by dividing Net Losses by the Average Principal Receivables Outstanding multiplied by a fraction, the numerator of which is the total number of days in the applicable calendar year and the denominator of which is the total number of days in the trust monthly reporting periods for the applicable period (365/33 for the one month ended January 28, 2014, 365/365 for the year ended December 26, 2013, 366/365 for the year ended December 26, 2012, and 365/364 for the year ended December 27, 2011).

If accrued finance charge receivables that have been written off were included in losses, Net Losses would be higher as an absolute number and as a percentage of the average of principal and finance charge receivables outstanding during the periods indicated. Average Principal Receivables Outstanding is the average of principal receivables outstanding during the periods indicated. There can be no assurance that the loss experience for the receivables in the future will be similar to the historical experience set forth below. There could be future increases in net losses, and such increases could be significant.

Loss Experience for the Accounts

(Dollars in Thousands)

| | | | | | | | | | | | | | | | |

| | | One Month

Ended

January 28, 2014

| | | Year Ended

December 26,

2013

| | | Year Ended

December 26,

2012

| | | Year Ended

December 27,

2011

| |

Average Principal Receivables Outstanding | | $ | 43,153,134 | | | $ | 39,660,646 | | | $ | 53,779,354 | | | $ | 60,924,613 | |

Gross Charge-Offs | | $ | 121,437 | | | $ | 1,797,828 | | | $ | 3,191,647 | | | $ | 4,886,666 | |

Recoveries | | $ | 31,872 | | | $ | 591,651 | | | $ | 759,252 | | | $ | 698,723 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Net Losses | | $ | 89,565 | | | $ | 1,206,177 | | | $ | 2,432,395 | | | $ | 4,187,943 | |

Net Losses as a Percentage of Average Principal Receivables Outstanding | | | 2.30 | % | | | 3.04 | % | | | 4.54 | % | | | 6.89 | % |

Net losses as a percentage of gross charge-offs for the one month ended January 28, 2014 were 73.75% and for each of the years ended December 26, 2013, December 26, 2012, and December 27, 2011, were 67.09%, 76.21% and 85.70%, respectively. Gross charge-offs are charge-offs before recoveries and do not include the amount of any reductions in Average Principal Receivables Outstanding due to fraud, returned goods, customer disputes or various other miscellaneous write-offs. During the 37 trust monthly reporting periods from January 2011 through January 2014, such reductions ranged from 0.01% to 0.98% of the outstanding principal receivables as of the end of the related trust monthly reporting period. The reduction of receivables in this manner reduces only the seller’s interest in the master trust. Recoveries

AI-2

are collections received in respect of principal receivables previously charged off as uncollectible. Net losses are gross charge-offs minus recoveries.

The following table sets forth the delinquency experience for cardholder payments on the credit card accounts as of each of the dates shown. The Delinquent Amount includes both principal receivables and finance charge receivables. Each percentage is the result of dividing the corresponding delinquent amount as of the end of the period indicated by the sum of the average principal receivables and average finance receivables outstanding during the one month ended January 26, 2014 and the years ended December 29, 2013, December 30, 2012, and December 25, 2011. There can be no assurance that the delinquency experience for the receivables in the future will be similar to the historical experience set forth below. There could be future increases in delinquencies, and such increases could be significant.

Delinquency Experience for the Accounts

(Dollars in Thousands)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | As of

January 26, 2014

| | | As of

December 29, 2013

| | | As of

December 30, 2012

| | | As of

December 25, 2011

| |

Number of Days

Delinquent

| | Delinquent

Amount

| | | Percentage

| | | Delinquent

Amount

| | | Percentage

| | | Delinquent

Amount

| | | Percentage

| | | Delinquent

Amount

| | | Percentage

| |

| | | | | | | | |

Up to 34 days | | $ | 975,415 | | | | 1.94 | % | | $ | 777,989 | | | | 1.83 | % | | $ | 976,601 | | | | 1.81 | % | | $ | 1,281,238 | | | | 2.08 | % |

| | | | | | | | |

35 to 64 days | | | 222,248 | | | | 0.44 | | | | 210,171 | | | | 0.50 | | | | 316,108 | | | | 0.58 | | | | 525,245 | | | | 0.85 | |

| | | | | | | | |

65 to 94 days | | | 164,269 | | | | 0.33 | | | | 162,883 | | | | 0.38 | | | | 271,656 | | | | 0.50 | | | | 423,006 | | | | 0.69 | |

| | | | | | | | |

95 to 124 days | | | 141,817 | | | | 0.28 | | | | 142,924 | | | | 0.34 | | | | 246,651 | | | | 0.46 | | | | 351,324 | | | | 0.57 | |

| | | | | | | | |

125 to 154 days | | | 121,475 | | | | 0.24 | | | | 112,870 | | | | 0.27 | | | | 184,600 | | | | 0.34 | | | | 289,044 | | | | 0.47 | |

| | | | | | | | |

155 to 184 days | | | 107,776 | | | | 0.21 | | | | 101,753 | | | | 0.24 | | | | 174,820 | | | | 0.32 | | | | 268,674 | | | | 0.44 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

| | | | | | | | |

Total | | $ | 1,733,000 | | | | 3.44 | % | | $ | 1,508,590 | | | | 3.56 | % | | $ | 2,170,436 | | | | 4.01 | % | | $ | 3,138,531 | | | | 5.10 | % |

Citibank, as servicer, may enter into arrangements to extend or otherwise change payment schedules for cardholders who are experiencing financial hardship. This includes reducing interest rates, ceasing the accrual of interest entirely or making other accommodations to a cardholder. The following table presents the number of accounts and the receivables outstanding of portfolios designated to the master trust subject to such arrangements as of the dates noted, and as percentages of the total number of accounts and total outstanding receivables in the master trust as of January 26, 2014:

| | | | | | | | | | | | | | | | |

| | | Number of

Accounts

| | | Percentage of

Total Number

of Accounts

| | | Receivables

Outstanding

| | | Percentage of Total

Receivables

Outstanding

| |

Loan Modifications - as of 01/26/2014 | | | 198,890 | | | | 0.93 | % | | $ | 847,886,424 | | | | 1.69 | % |

Total as of 1/26/2014 | | | 21,453,708 | | | | | | | $ | 50,163,694,075 | | | | | |

AI-3

Revenue Experience

The revenues for the credit card accounts from finance charges, fees paid by cardholders and interchange for the one month ended January 28, 2014 and for each of the years December 26, 2013, December 26, 2012, and December 27, 2011 are set forth in the following table. The revenue experience in this table is presented on a cash basis before deduction for charge-offs. Average Revenue Yield calculated for each period below is obtained by dividing Finance Charges and Fees Paid by Average Principal Receivables Outstanding multiplied by a fraction, the numerator of which is the total number of days in the applicable calendar year and the denominator of which is the total number of days in the trust monthly reporting periods for the applicable period (365/33 for the month ended January 28, 2014, 365/365 for the year ended December 26, 2013, 366/365 for the year ended December 26, 2012, and 365/364 for the year ended December 27, 2011).

Revenues from finance charges, fees and interchange will be affected by numerous factors, including the periodic finance charge on the credit card receivables, the amount of any annual membership fee, other fees paid by cardholders, the amount, if any, of principal receivables that is discounted and treated as finance charge receivables, the percentage of cardholders who pay off their balances in full each month and do not incur periodic finance charges on purchases, the percentage of credit card accounts bearing finance charges at promotional rates and changes in the level of delinquencies on the receivables.

Revenue Experience for the Accounts

(Dollars in Thousands)

| | | | | | | | | | | | | | | | |

| | | One Month

Ended

January 28, 2014

| | | Year Ended

December 26,

2013

| | | Year Ended

December 26,

2012

| | | Year Ended

December 27,

2011

| |

Finance Charges and Fees Paid | | $ | 633,092 | | | $ | 6,998,325 | | | $ | 8,923,604 | | | $ | 10,335,132 | |

Average Revenue Yield | | | 16.23 | % | | | 17.65 | % | | | 16.64 | % | | | 17.01 | % |

The revenues from periodic finance charges and fees—other than annual fees—depend in part upon the collective preference of cardholders to use their credit cards as revolving debt instruments for purchases and cash advances and to pay account balances over several months—as opposed to convenience use, where cardholders pay off their entire balance each month, thereby avoiding periodic finance charges on their purchases—and upon other card-related services for which the cardholder pays a fee. Revenues from periodic finance charges and fees also depend on the types of charges and fees assessed on the credit card accounts. Accordingly, revenues will be affected by future changes in the types of charges and fees assessed on the accounts and in the types of additional accounts added from time to time. These revenues could be adversely affected by future changes in fees and charges assessed on the accounts and other factors.

From March 2009 to March 2011, a 1% discount percentage was applied to the principal receivables in the credit card accounts designated to the master trust. The impact of this discounting—by recharacterizing 1% of principal collections as finance charge collections—

AI-4

was to increase the reported revenue yield on the accounts by an amount ranging from 1.97% to 2.39%, with an average increase of 2.17%, during the 25 trust monthly reporting periods that discounting was in effect. This discounting was discontinued in accordance with the operative documents in April 2011 because the 3-month average excess spread was above 7% for each of the three preceding trust monthly reporting periods.

Cardholder Monthly Payment Rates

The following table sets forth the highest and lowest cardholder monthly payment rates for the credit card accounts during any month in the periods shown and the average of the cardholder monthly payment rates for all months during the periods shown, in each case calculated as a percentage of the total beginning account balances for that month.

Monthly payment rates on the credit card receivables may vary because, among other things, a cardholder may fail to make a required payment or may only make the minimum required payment or may pay the entire outstanding balance. Monthly payment rates on the receivables may also vary due to seasonal purchasing and payment habits of cardholders. Monthly payment rates include amounts that are treated as payments of principal receivables and finance charge receivables with respect to the accounts under the pooling and servicing agreement. In addition, the amount of outstanding receivables and the rates of payments, delinquencies, charge-offs and new borrowings on the accounts depend on a variety of factors including seasonal variations, the availability of other sources of credit, general economic conditions, tax laws, consumer spending and borrowing patterns and the terms of the accounts, which may change. Cardholder monthly payment rates are calculated on the balances of those cardholder accounts that have an amount due. Cardholder accounts with a zero balance or a credit balance are excluded from these calculations.

As of the most recent related billing date prior to January 26, 2014, 38.78% of the accounts had a credit balance or otherwise had no payment due, 25.94% of the cardholders paid their entire outstanding balance, 5.69% of the cardholders made only the minimum payment due, 3.68% of the cardholders paid an amount less than the minimum due (including no payment) and the remaining 25.91% of the cardholders paid an amount greater than the minimum due, but less than the entire outstanding balance.

Cardholder Monthly Payment Rates for the Accounts

| | | | | | | | | | | | | | | | |

| | | One Month Ended

January 28, 2014

| | | Year Ended

December 26,

2013

| | | Year Ended

December 26,

2012

| | | Year Ended

December 27,

2011

| |

| | | | |

Lowest Month | | | 26.32 | % | | | 20.00 | % | | | 19.74 | % | | | 18.44 | % |

Highest Month | | | 26.32 | % | | | 26.00 | % | | | 22.63 | % | | | 22.11 | % |

Average of the Months in the Period | | | 26.32 | % | | | 23.49 | % | | | 21.56 | % | | | 20.48 | % |

AI-5

Interchange

Credit card-issuing banks participating in the MasterCard International, VISA and American Express systems receive interchange or similar fee income—referred to herein as interchange—as compensation for performing issuer functions, including taking credit risk, absorbing certain fraud losses and funding receivables for a limited period before initial billing. Under the MasterCard International, VISA and American Express systems, interchange in connection with cardholder charges for merchandise and services is passed from banks or other entities which clear the transactions for merchants to credit card-issuing banks. Interchange generally ranges from approximately 1% to 2% of the transaction amount, but may be higher for some card products or transactions. Citibank is required to transfer to the master trust interchange attributed to cardholder charges for merchandise and services in the accounts. In general, interchange is allocated to the master trust on the basis of the ratio that the amount of cardholder charges for merchandise and services in the accounts bears to the total amount of cardholder charges for merchandise and services in the portfolio of credit card accounts maintained by Citibank. MasterCard International, VISA and American Express may change the amount of interchange reimbursed to banks issuing their credit cards.

The Credit Card Receivables

The receivables in the credit card accounts designated to the master trust as of January 26, 2014 included $575,197,991 of finance charge receivables and $49,588,496,084 of principal receivables—which amounts include overdue finance charge receivables and overdue principal receivables. As of January 26, 2014, there were 21,453,708 accounts. For financial reporting purposes, included within the accounts are inactive, zero balance accounts other than those categorized as converted or lost or stolen accounts. The accounts had an average principal receivable balance of $2,311 and an average credit limit of $13,182. The average principal receivable balance in the accounts as a percentage of the average credit limit with respect to the accounts was approximately 17.53%. 92.89% of the accounts were opened before January 2012.

As of January 26, 2014, 99.86% of the credit card receivables in the master trust represented obligations of cardholders with billing addresses in the United States. Of the accounts, as of January 26, 2014, the following percentages related to cardholders with billing addresses in the following states:

| | | | | | | | |

| | | Percentage of Total

Number of Accounts

| | | Percentage of Total

Outstanding Receivables

| |

California | | | 14.66 | % | | | 14.03 | % |

New York | | | 11.78 | % | | | 10.03 | % |

Texas | | | 7.80 | % | | | 9.52 | % |

Florida | | | 6.64 | % | | | 6.14 | % |

Illinois | | | 5.55 | % | | | 6.04 | % |

Since the largest number of cardholders’ billing addresses were in California, New York, Texas, Florida and Illinois, adverse changes in the business or economic conditions in these states could have an adverse effect on the performance of the receivables. No other state represents more than 5% of the number of accounts or outstanding receivables.

AI-6

As of January 26, 2014, 2.28% of the credit card receivables in the master trust related to small business revolving credit card accounts originated by Citibank. The receivables in the 203,031 small business credit card accounts designated to the master trust as of January 26, 2014 included $10,078,921 of finance charge receivables and $1,137,611,855 of principal receivables—which amounts include overdue finance charge receivables and overdue principal receivables.

Citibank issues its small business credit cards to business owners who agree to use the cards for business purposes. With respect to substantially all accounts, both the individual business owner and the business are jointly and severally liable for all charges and balances on the account. For the remainder of the accounts, only the individual business owner is liable. The small business credit card accounts generally have higher receivables balances, credit limits and monthly payment rates than the other accounts designated to the master trust, taken as a whole. In addition, interchange generated on the receivables in these accounts is generally higher than the interchange generated on the receivables in the other accounts designated to the master trust.

As of January 26, 2014, the small business credit card accounts designated to the master trust had an average principal receivable balance of $5,603 and an average credit limit of $32,220. The average principal receivable balance in the accounts as a percentage of the average credit limit with respect to the accounts was approximately 17.39%. 98.86% of the accounts were opened before January 2012. Of the accounts, as of January 26, 2014, 24.77% of the receivables related to obligors with billing addresses in California and 17.69% in Texas. No other state represents more than 10% of the outstanding receivables. As of January 26, 2014, 94.20% of the receivables in the accounts related to obligors with a FICO score greater than 660, and 97.20% of the receivables had a “current” payment status as of the most recent related billing date.

As of the most recent related billing date prior to January 26, 2014, 28.93% of the small business credit card accounts had a credit balance or otherwise had no payment due, 49.21% of the obligors paid their entire outstanding balance, 2.35% of the obligors made only the minimum payment due, 3.46% of the obligors paid an amount less than the minimum due (including no payment) and the remaining 16.05% of the obligors paid an amount greater than the minimum due, but less than the entire outstanding balance.

As of January 29, 2014, approximately 23.94% of the credit card receivables in the master trust are related to credit cards issued under the Citibank/American Airlines AAdvantage co-brand program. Cardholders in the AAdvantage program receive benefits for the amounts charged on their AAdvantage cards, including frequent flyer miles in American Airlines’ frequent flyer program. Conditions that adversely affect the airline industry or American Airlines could adversely affect the usage and payment patterns of the AAdvantage cards. In addition, any future termination of the AAdvantage program could have an adverse effect on the payment rates and excess spread reported by the master trust.

AI-7

The credit card accounts include receivables which, in accordance with the servicer’s normal servicing policies, were charged-off as uncollectible. However, for purposes of calculation of the amount of principal receivables and finance charge receivables in the master trust for any date, the balance of the charged-off receivables is zero and the master trust owns only the right to receive recoveries on these receivables.

The following tables summarize the credit card accounts designated to the master trust as of January 26, 2014 by various criteria. References to “Receivables Outstanding” in these tables include both finance charge receivables and principal receivables. Because the composition of the accounts will change in the future, these tables are not necessarily indicative of the future composition of the accounts.

Credit balances presented in the following table are a result of cardholder payments and credit adjustments applied in excess of a credit card account’s unpaid balance. Accounts which have a credit balance are included because receivables may be generated in these accounts in the future. Credit card accounts which have no balance are included because receivables may be generated in these accounts in the future.

Composition of Accounts by Account Balance

| | | | | | | | | | | | | | | | |

Account Balance

| | Number of

Accounts

| | | Percentage

of Total

Number of

Accounts

| | | Receivables

Outstanding

| | | Percentage

of Total

Receivables

Outstanding

| |

Credit Balance | | | 177,259 | | | | 0.83 | % | | $ | (43,021,722 | ) | | | (0.09 | )% |

No Balance | | | 8,450,008 | | | | 39.39 | | | | 0 | | | | 0.00 | |

Less than or equal to $500.00 | | | 3,498,255 | | | | 16.31 | | | | 653,321,619 | | | | 1.30 | |

$500.01 to $1,000.00 | | | 1,498,016 | | | | 6.98 | | | | 1,104,853,892 | | | | 2.20 | |

$1,000.01 to $2,000.00 | | | 1,888,878 | | | | 8.80 | | | | 2,777,608,874 | | | | 5.54 | |

$2,000.01 to $3,000.00 | | | 1,220,861 | | | | 5.69 | | | | 3,028,053,011 | | | | 6.04 | |

$3,000.01 to $4,000.00 | | | 888,717 | | | | 4.14 | | | | 3,096,009,426 | | | | 6.17 | |

$4,000.01 to $5,000.00 | | | 698,007 | | | | 3.25 | | | | 3,132,584,622 | | | | 6.24 | |

$5,000.01 to $6,000.00 | | | 514,867 | | | | 2.40 | | | | 2,824,548,957 | | | | 5.63 | |

$6,000.01 to $7,000.00 | | | 417,666 | | | | 1.95 | | | | 2,709,957,526 | | | | 5.40 | |

$7,000.01 to $8,000.00 | | | 336,876 | | | | 1.57 | | | | 2,521,390,117 | | | | 5.03 | |

$8,000.01 to $9,000.00 | | | 282,890 | | | | 1.32 | | | | 2,401,612,574 | | | | 4.79 | |

$9,000.01 to $10,000.00 | | | 232,950 | | | | 1.09 | | | | 2,211,742,922 | | | | 4.41 | |

$10,000.01 to $15,000.00 | | | 670,121 | | | | 3.12 | | | | 8,133,388,319 | | | | 16.21 | |

$15,000.01 to $20,000.00 | | | 316,097 | | | | 1.47 | | | | 5,458,490,403 | | | | 10.88 | |

Over $20,000.00 | | | 362,240 | | | | 1.69 | | | | 10,153,153,535 | | | | 20.25 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Total | | | 21,453,708 | | | | 100.00 | % | | $ | 50,163,694,075 | | | | 100.00 | % |

AI-8

Composition of Accounts by Credit Limit

| | | | | | | | | | | | | | | | |

Credit Limit

| | Number of

Accounts

| | | Percentage

of Total

Number of

Accounts

| | | Receivables

Outstanding

| | | Percentage

of Total

Receivables

Outstanding

| |

Less than or equal to $500.00 | | | 515,972 | | | | 2.41 | % | | | 45,073,737 | | | | 0.09 | % |

$500.01 to $1,000.00 | | | 483,175 | | | | 2.25 | | | | 145,883,854 | | | | 0.29 | |

$1,000.01 to $2,000.00 | | | 1,078,497 | | | | 5.03 | | | | 664,764,825 | | | | 1.33 | |

$2,000.01 to $3,000.00 | | | 952,667 | | | | 4.44 | | | | 916,773,431 | | | | 1.83 | |

$3,000.01 to $4,000.00 | | | 870,076 | | | | 4.06 | | | | 1,058,992,385 | | | | 2.11 | |

$4,000.01 to $5,000.00 | | | 1,113,557 | | | | 5.19 | | | | 1,615,390,200 | | | | 3.22 | |

$5,000.01 to $6,000.00 | | | 891,849 | | | | 4.16 | | | | 1,293,694,907 | | | | 2.58 | |

$6,000.01 to $7,000.00 | | | 935,675 | | | | 4.36 | | | | 1,566,832,578 | | | | 3.12 | |

$7,000.01 to $8,000.00 | | | 960,211 | | | | 4.48 | | | | 1,577,733,703 | | | | 3.15 | |

$8,000.01 to $9,000.00 | | | 975,740 | | | | 4.55 | | | | 1,767,269,197 | | | | 3.52 | |

$9,000.01 to $10,000.00 | | | 1,063,307 | | | | 4.96 | | | | 1,868,990,569 | | | | 3.73 | |

$10,000.01 to $15,000.00 | | | 4,214,794 | | | | 19.65 | | | | 8,459,054,497 | | | | 16.86 | |

$15,000.01 to $20,000.00 | | | 2,253,203 | | | | 10.50 | | | | 5,973,521,255 | | | | 11.90 | |

Over $20,000.00 | | | 5,144,985 | | | | 23.96 | | | | 23,209,718,937 | | | | 46.27 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Total | | | 21,453,708 | | | | 100.00 | % | | $ | 50,163,694,075 | | | | 100.00 | % |

Accounts presented in the table below as “Current” include accounts on which the minimum payment has not been received before the next billing date following the issuance of the related bill.

Composition of Accounts by Payment Status

| | | | | | | | | | | | | | | | |

Payment Status

| | Number of

Accounts

| | | Percentage

of Total

Number of

Accounts

| | | Receivables

Outstanding

| | | Percentage

of Total

Receivables

Outstanding

| |

Current | | | 21,135,839 | | | | 98.51 | % | | $ | 48,430,693,232 | | | | 96.56 | % |

Up to 34 days delinquent | | | 213,218 | | | | 0.99 | | | | 975,415,205 | | | | 1.94 | |

35 to 64 days delinquent | | | 38,004 | | | | 0.18 | | | | 222,248,376 | | | | 0.44 | |

65 to 94 days delinquent | | | 22,851 | | | | 0.11 | | | | 164,268,835 | | | | 0.33 | |

95 to 124 days delinquent | | | 17,769 | | | | 0.08 | | | | 141,816,985 | | | | 0.28 | |

125 to 154 days delinquent | | | 14,115 | | | | 0.07 | | | | 121,475,238 | | | | 0.24 | |

155 to 184 days delinquent | | | 11,912 | | | | 0.06 | | | | 107,776,204 | | | | 0.21 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Total | | | 21,453,708 | | | | 100.00 | % | | $ | 50,163,694,075 | | | | 100.00 | % |

Composition of Accounts by Age

| | | | | | | | | | | | | | | | |

Age

| | Number of

Accounts

| | | Percentage

of Total

Number of

Accounts

| | | Receivables

Outstanding

| | | Percentage

of Total

Receivables

Outstanding

| |

Less than or equal to 6 months | | | 61,120 | | | | 0.28 | % | | $ | 163,513,700 | | | | 0.33 | % |

Over 6 months to 12 months | | | 483,849 | | | | 2.26 | | | | 1,297,699,044 | | | | 2.59 | |

Over 12 months to 24 months | | | 981,780 | | | | 4.58 | | | | 2,510,789,179 | | | | 5.01 | |

Over 24 months to 36 months | | | 829,218 | | | | 3.87 | | | | 2,902,788,205 | | | | 5.79 | |

Over 36 months to 48 months | | | 503,100 | | | | 2.35 | | | | 1,824,765,120 | | | | 3.64 | |

Over 48 months to 60 months | | | 738,706 | | | | 3.44 | | | | 1,432,475,282 | | | | 2.86 | |

Over 60 months | | | 17,855,935 | | | | 83.22 | | | | 40,031,663,545 | | | | 79.78 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Total | | | 21,453,708 | | | | 100.00 | % | | $ | 50,163,694,075 | | | | 100.00 | % |

AI-9

The following table sets forth the composition of accounts by FICO®* score as of January 26, 2014. A FICO score is a measurement determined by Fair, Isaac & Company using information collected by major credit bureaus to assess credit risk. A credit report is generally obtained from one or more credit bureaus for each application for a new account. Once a customer has been issued a card, Citibank refreshes the FICO score on most accounts on a monthly basis. Citibank generally does not refresh the FICO scores of closed accounts that have no balance and certain other categories of accounts. A FICO score of zero indicates that the FICO score of an account has not been refreshed for one of these reasons or that the customer did not have enough credit history for a FICO score to be calculated.

As of January 26, 2014, 90.76% of the receivables in the master trust related to obligors whose FICO score is greater than 660.

Composition of Accounts by FICO Score

| | | | | | | | | | | | | | | | |

FICO Score

| | Number of

Accounts

| | | Percentage

of Total

Number of

Accounts

| | | Receivables

Outstanding

| | | Percentage

of Total

Receivables

Outstanding

| |

0 | | | 6,067,033 | | | | 28.28 | % | | $ | 239,303,964 | | | | 0.47 | % |

001 to 599 | | | 227,924 | | | | 1.06 | | | | 1,187,621,502 | | | | 2.37 | |

600 to 639 | | | 279,263 | | | | 1.30 | | | | 1,442,463,877 | | | | 2.88 | |

640 to 660 | | | 314,171 | | | | 1.46 | | | | 1,767,768,063 | | | | 3.52 | |

661 to 679 | | | 694,845 | | | | 3.24 | | | | 3,905,516,123 | | | | 7.79 | |

680 to 699 | | | 961,768 | | | | 4.48 | | | | 5,852,771,362 | | | | 11.67 | |

700 to 719 | | | 1,132,651 | | | | 5.28 | | | | 6,830,875,516 | | | | 13.62 | |

720 to 739 | | | 1,169,449 | | | | 5.45 | | | | 6,292,217,752 | | | | 12.54 | |

740 to 759 | | | 1,237,509 | | | | 5.77 | | | | 5,628,039,937 | | | | 11.22 | |

760 to 800 | | | 2,856,830 | | | | 13.32 | | | | 8,348,127,760 | | | | 16.64 | |

801 and above | | | 6,512,265 | | | | 30.36 | | | | 8,668,988,219 | | | | 17.27 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Total | | | 21,453,708 | | | | 100.00 | % | | $ | 50,163,694,075 | | | | 100.00 | % |

| * | FICO® is a registered trademark of Fair, Isaac & Company. |

Billing and Payments

The credit card accounts have different billing and payment structures, including different periodic finance charges and fees. The following information reflects the current billing and payment characteristics of the accounts.

In general, each month billing statements are sent to cardholders. To the extent a cardholder has a balance due, the cardholder must make a minimum payment equal to the sum of any amount which is past due plus any amount which is in excess of the credit limit and, for most accounts, the greatest of the following:

| | Ÿ | | the new balance on the billing statement if it is less than $20, or $20, if the new balance is at least $20; |

AI-10

| | Ÿ | | 1% of the new balance plus the amount of any billed finance charges and any billed late fee; and |

| | Ÿ | | 1.5% of the new balance. |

A periodic finance charge is imposed on the credit card accounts. The periodic finance charge imposed on balances for purchases and cash advances for a majority of the accounts is calculated by multiplying (1) the daily balances for each day during the billing cycle by (2) the applicable daily periodic finance charge rate, and summing the results for each day in the billing period. The daily balance is calculated by taking the previous day’s balance, adding any new purchases or cash advances and fees, adding the daily finance charge on the previous day’s balance, and subtracting any payments or credits. Cash advances are included in the daily balance from the date the advances are made. Purchases are included in the daily balance generally from the date of purchase. Periodic finance charges are not imposed in most circumstances on purchase amounts if all balances shown in the previous billing statement are paid in full by the due date indicated on the statement.

As of the date of this prospectus supplement:

| | Ÿ | | the periodic finance charge imposed on balances in most credit card accounts for purchases is the Prime Rate, as published in The Wall Street Journal, plus a percentage ranging from 10.74% to 21.74%. A small portion of the credit card accounts have a non-variable periodic finance charge imposed on purchase balances ranging from 13.99% to 24.99%; |

| | Ÿ | | the periodic finance charge imposed on balances in most credit card accounts for cash advances is the sum of the Prime Rate and 21.99%; and |

| | Ÿ | | if a cardholder fails to make a payment by the due date under their credit card agreement, the periodic finance charge assessed on new transactions can be increased up to the sum of the Prime Rate and 26.74%, with 45 days advance notice. If a cardholder fails to make a payment for more than 60 days after the due date under their credit card agreement, the periodic finance charge assessed on existing balances in their account can be increased up to the sum of the Prime Rate and 26.74%, with 45 days advance notice. |

Promotional rates are offered from time to time to attract new cardholders and to promote balance transfers from other credit card issuers and the periodic finance charge on a limited number of accounts may be greater or less than those generally assessed on the accounts.

Most of the accounts are subject to additional fees, including: