UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-Q

☒QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended March 31, 2019

or

☐TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES ACT OF 1934

For the transition period from _________ to ________

Commission File Number: 001-36615

GWG HOLDINGS, INC.

(Exact name of registrant as specified in its charter)

| Delaware | | 26-2222607 |

(State or other jurisdiction of

incorporation or organization) | | (I.R.S. Employer

Identification No.) |

220 South Sixth Street, Suite 1200

Minneapolis, MN 55402

(Address of principal executive offices, including zip code)

(612) 746-1944

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | | Trading Symbol(s) | | Name of each exchange

on which registered |

| Common Stock | | GWGH | | NASDAQ Capital Market |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☐ Yes ☒ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). ☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☐ | Smaller reporting company | ☒ |

| | | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes ☒ No

As of July 31, 2019, GWG Holdings, Inc. had 33,033,420 shares of common stock outstanding.

GWG HOLDINGS, INC.

Index to Form 10-Q

for the Quarter Ended March 31, 2019

PART I — FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

GWG HOLDINGS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

| | | March 31,

2019

(unaudited) | | | December 31,

2018 | |

| ASSETS | | | | | | |

| Cash and cash equivalents | | $ | 154,384,426 | | | $ | 114,587,084 | |

| Restricted cash | | | 20,311,646 | | | | 10,849,126 | |

| Investment in life insurance policies, at fair value | | | 782,184,731 | | | | 747,922,465 | |

| Life insurance policy benefits receivable, net | | | 9,200,000 | | | | 16,460,687 | |

| Financing receivable from affiliate | | | 186,738,243 | | | | 184,768,874 | |

| Equity method investment | | | 359,096,434 | | | | 360,841,651 | |

| Other assets | | | 50,116,768 | | | | 45,437,164 | |

| TOTAL ASSETS | | $ | 1,562,032,248 | | | $ | 1,480,867,051 | |

| | | | | | | | | |

| LIABILITIES & STOCKHOLDERS’ EQUITY | | | | | | | | |

| LIABILITIES | | | | | | | | |

| Senior credit facility with LNV Corporation | | $ | 146,868,215 | | | $ | 148,977,596 | |

| L Bonds | | | 756,397,420 | | | | 651,402,663 | |

| Seller Trust L Bonds | | | 366,891,940 | | | | 366,891,940 | |

| Accounts payable | | | 6,079,306 | | | | 9,276,507 | |

| Interest and dividends payable | | | 18,506,588 | | | | 18,555,293 | |

| Other accrued expenses | | | 6,030,841 | | | | 4,705,170 | |

| TOTAL LIABILITIES | | | 1,300,774,310 | | | | 1,199,809,169 | |

| | | | | | | | | |

| STOCKHOLDERS’ EQUITY | | | | | | | | |

| | | | | | | | | |

| REDEEMABLE PREFERRED STOCK | | | | | | | | |

| (par value $0.001; shares authorized 100,000; shares outstanding 96,954 and 97,524; liquidation preference of $97,520,000 and $98,093,000 as of March 31, 2019 and December 31, 2018, respectively) | | | 86,340,335 | | | | 86,910,335 | |

| SERIES 2 REDEEMABLE PREFERRED STOCK | | | | | | | | |

| (par value $0.001; shares authorized 150,000; shares outstanding 148,110 and 148,359; liquidation preference of $148,974,000 and $149,225,000 as of March 31, 2019 and December 31, 2018, respectively) | | | 128,813,787 | | | | 129,062,704 | |

| COMMON STOCK | | | | | | | | |

| (par value $0.001; shares authorized 210,000,000; shares issued and outstanding 32,992,606 as of March 31, 2019 and 33,018,161 as of December 31, 2018) | | | 32,993 | | | | 33,018 | |

| Additional paid-in capital | | | 245,294,858 | | | | 249,662,168 | |

| Accumulated deficit | | | (199,224,035 | ) | | | (184,610,343 | ) |

| TOTAL STOCKHOLDERS’ EQUITY | | | 261,257,938 | | | | 281,057,882 | |

| | | | | | | | | |

| TOTAL LIABILITIES & EQUITY | | $ | 1,562,032,248 | | | $ | 1,480,867,051 | |

The accompanying notes are an integral part of these Condensed Consolidated Financial Statements.

GWG HOLDINGS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(unaudited)

| | | Three Months Ended | |

| | | March 31,

2019 | | | March 31,

2018 | |

| REVENUE | | | | | | |

| Gain (loss) on life insurance policies, net | | $ | 21,496,390 | | | $ | 13,868,745 | |

| Interest and other income | | | 3,720,550 | | | | 672,927 | |

| TOTAL REVENUE | | | 25,216,940 | | | | 14,541,672 | |

| | | | | | | | | |

| EXPENSES | | | | | | | | |

| Interest expense | | | 26,974,988 | | | | 16,063,337 | |

| Employee compensation and benefits | | | 5,153,984 | | | | 3,742,669 | |

| Legal and professional fees | | | 2,947,196 | | | | 1,173,629 | |

| Other expenses | | | 2,827,721 | | | | 2,740,577 | |

| TOTAL EXPENSES | | | 37,903,889 | | | | 23,720,212 | |

| | | | | | | | | |

| INCOME (LOSS) BEFORE INCOME TAXES | | | (12,686,949 | ) | | | (9,178,540 | ) |

| INCOME TAX EXPENSE (BENEFIT) | | | - | | | | - | |

| | | | | | | | | |

| NET INCOME (LOSS) BEFORE EARNINGS (LOSS) FROM EQUITY METHOD INVESTMENT | | | (12,686,949 | ) | | | (9,178,540 | ) |

| | | | | | | | | |

| Earnings (loss) from equity method investment | | | (1,926,743 | ) | | | - | |

| | | | | | | | | |

| NET INCOME (LOSS) | | | (14,613,692 | ) | | | (9,178,540 | ) |

| | | | | | | | | |

| Preferred stock dividends | | | 4,296,314 | | | | 3,704,484 | |

| NET INCOME (LOSS) ATTRIBUTABLE TO COMMON SHAREHOLDERS | | $ | (18,910,006 | ) | | $ | (12,883,024 | ) |

| NET INCOME (LOSS) PER COMMON SHARE | | | | | | | | |

| Basic | | $ | (0.57 | ) | | $ | (2.22 | ) |

| Diluted | | $ | (0.57 | ) | | $ | (2.22 | ) |

| | | | | | | | | |

| WEIGHTED AVERAGE COMMON SHARES OUTSTANDING | | | | | | | | |

| Basic | | | 32,984,741 | | | | 5,813,555 | |

| Diluted | | | 32,984,741 | | | | 5,813,555 | |

The accompanying notes are an integral part of these Condensed Consolidated Financial Statements.

GWG HOLDINGS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(unaudited)

| | | Three Months Ended | |

| | | March 31,

2019 | | | March 31,

2018* | |

| CASH FLOWS FROM OPERATING ACTIVITIES | | | | | | |

| Net income (loss) | | $ | (14,613,692 | ) | | $ | (9,178,540 | ) |

| Adjustments to reconcile net income (loss) to net cash flows from operating activities: | | | | | | | | |

| Change in fair value of life insurance policies | | | (15,570,805 | ) | | | (16,645,594 | ) |

| Amortization of deferred financing and issuance costs | | | 3,099,989 | | | | 2,263,188 | |

| Accretion of discount on financing receivable from affiliate | | | (418,611 | ) | | | - | |

| Loss from equity method investment | | | 1,926,743 | | | | - | |

| Stock-based compensation | | | 833,809 | | | | 212,924 | |

| (Increase) decrease in operating assets: | | | | | | | | |

| Life insurance policy benefits receivable | | | 7,260,687 | | | | 4,356,031 | |

| Accrued interest on financing receivable | | | (1,550,758 | ) | | | - | |

| Other assets | | | (3,941,937 | ) | | | (76,441 | ) |

| Increase (decrease) in operating liabilities: | | | | | | | | |

| Accounts payable and other accrued expenses | | | (3,327,959 | ) | | | (1,758,132 | ) |

| NET CASH FLOWS USED IN OPERATING ACTIVITIES | | | (26,302,534 | ) | | | (20,826,564 | ) |

| | | | | | | | | |

| CASH FLOWS FROM INVESTING ACTIVITIES | | | | | | | | |

| Investment in life insurance policies | | | (27,392,631 | ) | | | (25,299,825 | ) |

| Carrying value of matured life insurance policies | | | 8,701,168 | | | | 5,083,294 | |

| NET CASH FLOWS USED IN INVESTING ACTIVITIES | | | (18,691,463 | ) | | | (20,216,531 | ) |

| | | | | | | | | |

| CASH FLOWS FROM FINANCING ACTIVITIES | | | | | | | | |

| Borrowings on senior debt | | | - | | | | 9,636,945 | |

| Repayments of senior debt | | | (2,373,135 | ) | | | (12,691,280 | ) |

| Proceeds from issuance of L Bonds | | | 125,984,692 | | | | 36,661,099 | |

| Payments for issuance and redemption of L Bonds | | | (23,973,679 | ) | | | (12,245,448 | ) |

| Issuance (repurchase) of common stock | | | (268,788 | ) | | | - | |

| Proceeds from issuance of preferred stock | | | - | | | | 41,865,169 | |

| Payments for issuance of preferred stock | | | - | | | | (3,157,695 | ) |

| Payments for redemption of preferred stock | | | (818,917 | ) | | | (327,224 | ) |

| Preferred stock dividends | | | (4,296,314 | ) | | | (3,704,484 | ) |

| NET CASH FLOWS PROVIDED BY FINANCING ACTIVITIES | | | 94,253,859 | | | | 56,037,082 | |

| | | | | | | | | |

| NET INCREASE (DECREASE) IN CASH, CASH EQUIVALENTS AND RESTRICTED CASH | | | 49,259,862 | | | | 14,993,987 | |

| | | | | | | | | |

| CASH, CASH EQUIVALENTS AND RESTRICTED CASH | | | | | | | | |

| BEGINNING OF PERIOD | | | 125,436,210 | | | | 142,771,176 | |

| END OF PERIOD | | $ | 174,696,072 | | | $ | 157,765,163 | |

| | * | The line items Borrowings on senior debt and Repayments of senior debt for the three months ended March 31, 2018 have been revised to present gross activity that was previously reported net as discussed in Note 2 Correction of an Immaterial Error. |

The accompanying notes are an integral part of these Condensed Consolidated Financial Statements.

GWG HOLDINGS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS — CONTINUED

(unaudited)

| | | Three Months Ended | |

| | | March 31,

2019 | | | March 31,

2018 | |

| SUPPLEMENTAL DISCLOSURES OF CASH FLOW INFORMATION | | | | | | |

| Interest paid | | $ | 23,604,000 | | | $ | 13,475,000 | |

| Premiums paid, including prepaid | | $ | 19,113,000 | | | $ | 11,833,000 | |

| Payments for exercised stock options | | $ | - | | | $ | 37,000 | |

| | | | | | | | | |

| NON-CASH INVESTING AND FINANCING ACTIVITIES | | | | | | | | |

| L Bonds: | | | | | | | | |

| Conversion of accrued interest and commissions payable to principal | | $ | 634,000 | | | $ | 342,000 | |

| Conversion of L Bonds to redeemable preferred stock | | $ | - | | | $ | 4,421,000 | |

| Investment in life insurance policies included in accounts payable | | $ | 2,914,000 | | | $ | 1,350,000 | |

The accompanying notes are an integral part of these Condensed Consolidated Financial Statements.

GWG HOLDINGS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS’ EQUITY

(unaudited)

| | | Preferred

Stock

Shares | | | Preferred

Stock | | | Common

Shares | | | Common

Stock

(par) | | | Additional

Paid-in

Capital | | | Accumulated

Deficit | | | Total

Equity | |

| Balance, December 31, 2017 (audited) | | | 187,319 | | | $ | 173,115,447 | | | | 5,813,555 | | | $ | 5,813 | | | $ | — | | | $ | (39,449,517 | ) | | $ | 133,671,743 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Net income (loss) | | | — | | | | — | | | | — | | | | — | | | | — | | | | (9,178,540 | ) | | | (9,178,540 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Issuance of redeemable preferred stock | | | 46,317 | | | | 43,159,571 | | | | — | | | | — | | | | — | | | | — | | | | 43,159,571 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Redemption of redeemable preferred stock | | | (327 | ) | | | (327,224 | ) | | | — | | | | — | | | | — | | | | — | | | | (327,224 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Preferred stock dividends | | | — | | | | (3,704,484 | ) | | | — | | | | — | | | | — | | | | — | | | | (3,704,484 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Stock-based compensation | | | — | | | | 125,921 | | | | — | | | | — | | | | — | | | | — | | | | 125,921 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Balance, March 31, 2018 | | | 233,309 | | | $ | 212,369,231 | | | | 5,813,555 | | | $ | 5,813 | | | $ | — | | | $ | (48,628,057 | ) | | $ | 163,746,987 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Balance, December 31, 2018 (audited) | | | 245,883 | | | $ | 215,973,039 | | | | 33,018,161 | | | $ | 33,018 | | | $ | 249,662,168 | | | $ | (184,610,343 | ) | | $ | 281,057,882 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Net income (loss) | | | — | | | | — | | | | — | | | | — | | | | — | | | | (14,613,692 | ) | | | (14,613,692 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Issuance of common stock | | | — | | | | — | | | | 17,135 | | | | 17 | | | | 92,688 | | | | — | | | | 92,705 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Repurchase of common stock | | | — | | | | — | | | | (42,690 | ) | | | (42 | ) | | | (361,451 | ) | | | — | | | | (361,493 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Redemption of redeemable preferred stock | | | (819 | ) | | | (818,917 | ) | | | — | | | | — | | | | — | | | | — | | | | (818,917 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Preferred stock dividends | | | — | | | | — | | | | — | | | | — | | | | (4,296,314 | ) | | | — | | | | (4,296,314 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Stock-based compensation | | | — | | | | — | | | | — | | | | — | | | | 197,767 | | | | — | | | | 197,767 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Balance, March 31, 2019 | | | 245,064 | | | $ | 215,154,122 | | | | 32,992,606 | | | $ | 32,993 | | | $ | 245,294,858 | | | $ | (199,224,035 | ) | | $ | 261,257,938 | |

The accompanying notes are an integral part of these Condensed Consolidated Financial Statements.

GWG HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

(1) Nature of Business and Summary of Significant Accounting Policies

Nature of Business — GWG Holdings, Inc. (“GWG Holdings”) conducts its life insurance secondary market business through a wholly owned subsidiary, GWG Life, LLC (“GWG Life”), and GWG Life’s wholly owned subsidiaries, GWG Life Trust and GWG DLP Funding IV, LLC. GWG Holdings’ owns a significant equity interest in The Beneficient Company Group, L.P. (“BEN LP,” including all of the subsidiaries it may have from time to time — “Beneficient”). Beneficient is a financial services firm based in Dallas, Texas, that provides liquidity solutions for mid-to-high net worth (“MHNW”) individuals and small-to-mid (“STM”) size institutions, which previously had few options to obtain early liquidity for their alternative assets holdings. Beneficient has closed a limited number of these transactions to date, and intends to significantly expand its operations. All of these entities are legally organized in Delaware, other than GWG Life Trust, which is governed by the laws of the state of Utah. GWG Holdings’ wholly owned subsidiary, Life Epigenetics Inc. (formerly named Actüa Life & Annuity Ltd.) (“Life Epigenetics”) was formed to engage in various life insurance related businesses and activities related to its development of epigenetic technology. Through its wholly owned subsidiary, youSurance General Agency, LLC (“youSurance”), GWG Holdings offers life insurance directly to customers from a variety of life insurance carriers. Unless the context otherwise requires or we specifically so indicate, all references in this report to “we,” “us,” “our,” “our Company,” “GWG,” or the “Company” refer to these entities collectively. Our headquarters are currently in Minneapolis, Minnesota.

Beneficient was formed in 2003 but began its alternative asset business in September 2017. Beneficient operates primarily through its subsidiaries, which provide Beneficient’s products and services. These subsidiaries include: (i) Beneficient Capital Company, L.L.C. (“BCC”), through which Beneficient offers loans and liquidity products; (ii) Beneficient Administrative and Clearing Company, L.L.C. (“BACC”), through which Beneficient provides services for fund and trust administration and plans to provide custody services; (iii) PEN Indemnity Insurance Company, LTD (“PEN”), through which Beneficient plans to offer insurance services; and (iv) ACE Portal, L.L.C. (“ACE”), through which Beneficient plans to provide an online portal for direct access to Beneficient’s financial services and products.

In 2018 and early 2019, we consummated a series of transactions (as more fully described below) with Beneficient that has resulted in a significant reorientation of our business and capital allocation strategy in addition to a change in our Board of Directors and executive management team.

The Exchange Transaction

On August 10, 2018 (the “Initial Transfer Date”), we completed the first of two closings (the “Initial Transfer”) contemplated by a Master Exchange Agreement with BEN LP and certain other parties (the “Seller Trusts”), which governs the strategic exchange of assets among the parties (the “Exchange Transaction”). On the Initial Transfer Date:

| ● | GWG issued to the Seller Trust L Bonds due 2023 (the “Seller Trust L Bonds”) in an aggregate principal amount of $403,234,866, as more fully described below; |

| ● | Beneficient purchased 5,000,000 shares of GWG’s Series B Convertible Preferred Stock, par value $0.001 per share and having a stated value of $10 per share (“Series B”), for cash consideration of $50,000,000, which shares were subsequently transferred to the Seller Trusts, as more fully described below; |

| ● | in consideration for GWG and GWG Life entering into the Master Exchange Agreement and consummating the transactions contemplated thereby, BEN LP, as borrower, entered into a commercial loan agreement (the “Commercial Loan Agreement”) with GWG Life, as lender, providing for a loan in a principal amount of $200,000,000 (the “Commercial Loan”); |

| ● | BEN LP delivered to GWG a promissory note (the “Exchangeable Note”) in the principal amount of $162,911,379; and |

| ● | the Seller Trusts delivered to GWG 4,032,349 common units of BEN LP at an assumed value of $10 per common unit. |

On December 28, 2018, the final closing of the transaction occurred and the following actions took place (the “Final Closing” and the date upon which the Final Closing occurs, the “Final Closing Date”):

| ● | in accordance with the Master Exchange Agreement, and based on the net asset value of alternative asset financings as of the Final Closing Date, effective as of the Initial Transfer Date, (i) the principal amount of the Commercial Loan was reduced to $181,974,314, (ii) the principal amount of the Exchangeable Note was reduced to $148,228,432, and (iii) the principal amount of the Seller Trust L Bonds was reduced to $366,892,000; |

GWG HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

| ● | the Seller Trusts refunded to GWG $840,430 in interest paid on the Seller Trust L Bonds related to the Seller Trust L Bonds that were issued as of the Initial Transfer Date but cancelled, effective as of the Initial Transfer Date; |

| ● | the accrued interest on the Commercial Loan and the Exchangeable Note was added to the principal amount of the Commercial Loan, as a result of which the principal amount of the Commercial Loan as of the Final Closing Date was $192,507,946; |

| ● | the Seller Trusts transferred to GWG an aggregate of 21,650,087 common units of BEN LP and GWG received 14,822,843 common units of BEN LP in exchange for the Exchangeable Note, upon completion of which GWG owned (including the 4,032,349 common units received by GWG on the Initial Transfer Date) 40,505,279 common units of BEN LP; |

| ● | BEN LP issued to GWG an option (the “Option Agreement”) to acquire the number of common units of BEN LP, interests or other property that would be received by a holder of the NPC-A Prime limited partnership interests of Beneficient Company Holdings, L.P., an affiliate of BEN LP (“Beneficient Holdings”); and |

| ● | GWG issued to the Seller Trusts 27,013,516 shares of GWG common stock (including 5,000,000 shares issued upon conversion of the Convertible Preferred Stock). |

A summary of the Exchange Transaction is set forth in our Current Report onForm 8-K, filed with the Securities and Exchange Commission (“SEC”) on August 14, 2018, and amended in our Current Report onForm 8-K/A filed with the SEC on November 9, 2018, as well as theForm 8-K filed with the SEC on January 4, 2019.

Description of the Assets Exchanged

Seller Trust L Bonds

On August 10, 2018, in connection with the Initial Transfer, GWG Holdings, GWG Life and Bank of Utah, as trustee, entered into a Supplemental Indenture (the “Supplemental Indenture”) to the Amended and Restated Indenture dated as of October 23, 2017 (the “Amended and Restated Indenture”). GWG Holdings entered into the Supplemental Indenture to add and modify certain provisions of the Amended and Restated Indenture necessary to provide for the issuance of the Seller Trust L Bonds. The maturity date of the Seller Trust L Bonds is August 9, 2023. The Seller Trust L Bonds bear interest at 7.5% per year. Interest is payable monthly in cash.

After the second anniversary of the Final Closing Date, the holders of the Seller Trust L Bonds will have the right to cause GWG to repurchase, in whole but not in part, the Seller Trust L Bonds held by such holder. The repurchase may be paid, at GWG’s option, in the form of cash, a pro rata portion of (i) the outstanding principal amount and accrued and unpaid interest under the Commercial Loan and (ii) BEN LP common units, or a combination of cash and such property.

The Seller Trust L Bonds (see Note 10) are senior secured obligations of GWG, ranking junior only to all senior debt of GWG (see Note 8), pari passu in right of payment and in respect of collateral with all “L Bonds” of GWG (see Note 9), and senior in right of payment to all subordinated indebtedness of GWG. Payments under the Seller Trust L Bonds are guaranteed by GWG Life (see Note 22).

Series B Convertible Preferred Stock

The Series B converted into 5,000,000 shares of our common stock at a conversion price of $10 per share upon the Final Closing.

Commercial Loan

The $192,508,000 principal amount under the Commercial Loan is due on August 9, 2023; however, is extendable for two five-year terms. See Note 6 for a full description of the terms of the Commercial Loan. BEN LP’s obligations under the Commercial Loan are unsecured.

The principal amount of the Commercial Loan bears interest at 5.0% per year. From and after the Final Closing Date, one-half of the interest, or 2.5% per year, is due and payable monthly in cash, and (ii) one-half of the interest, or 2.5% per year, accrues and compounds annually on each anniversary date of the Final Closing Date and become due and payable in full in cash on the maturity date.

GWG HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

In accordance with the Supplemental Indenture issuing the Seller Trust L Bonds, upon a redemption event or at the maturity date of the Seller Trust L Bonds, the Company, at its option, may use the outstanding principal amount of the Commercial Loan, and accrued and unpaid interest thereon, as repayment consideration of the Seller Trust L Bonds.

Exchangeable Note

The Exchangeable Note accrued interest at a rate of 12.4% per year, compounded annually. Interest was payable in cash on the earlier to occur of the maturity date or the Final Closing Date; provided that Beneficient had the option to add to the outstanding principal balance under the Commercial Loan the accrued interest in lieu of payment in cash of such accrued interest thereon at the Final Closing Date. At the Final Closing date, the principal amount of the Exchangeable Note was exchanged for 14,822,843 common units of BEN LP, and the accrued interest on the Exchangeable Note was added to the principal balance of the Commercial Loan.

Option Agreement

In connection with the Final Closing, the Company entered into the Option Agreement with BEN LP. The Option Agreement gives us the option to acquire the number of common units in BEN LP that would be received by the holder of NPC-A Prime limited partnership interests of Beneficient Holdings, if such holder were converting on that date. There is no exercise price and the Company may exercise the option at any time until December 27, 2028, at which time the option will automatically settle.

Common Units of BEN LP

In connection with the Initial Transfer and Final Closing, the Seller Trusts and Beneficient delivered to us 40,505,279 common units of BEN LP. This represented an approximate 89.9% interest in the common units of BEN LP as of the Final Closing Date.

Basis of Presentation —The accompanying unaudited condensed consolidated financial statements have been prepared in accordance with the SEC requirements for interim reporting, which allows certain footnotes and other financial information normally required by Generally Accepted Accounting Principles in the United States of America (GAAP) to be condensed or omitted. In our opinion, the condensed consolidated financial statements contain all adjustments (consisting of only normal recurring adjustments) necessary for the fair presentation of our financial position and results of operations. These statements should be read in conjunction with the consolidated financial statements and notes included in our Annual Report onForm 10-K for the year ended December 31, 2018. The results of operations for interim periods are not necessarily indicative of the results to be expected for the full year.

Principles of Consolidation —The condensed consolidated financial statements include the accounts of GWG Holdings, Inc. and all its wholly owned subsidiaries. All material intercompany balances and transactions have been eliminated upon consolidation.

The Company has interests in various entities including corporations and limited partnerships. For each such entity, the Company evaluates its ownership interest to determine whether the entity is a variable interest entity (“VIE”) and, if so, whether it is the primary beneficiary of the VIE. The Company would consolidate any entity for which it was the primary beneficiary, regardless of its ownership or voting interests. Upon inception of a variable interest or the occurrence of a reconsideration event, the Company makes judgments in determining whether entities in which it invests are VIEs. If so, the Company makes judgments to determine whether it is the primary beneficiary and is thus required to consolidate the entity.

If it is concluded that an entity is not a VIE, then the Company considers its proportional voting interests in the entity. The Company consolidates majority-owned subsidiaries in which a controlling financial interest is maintained. A controlling financial interest is determined by majority ownership and the absence of significant third-party participating rights. Ownership interests in entities for which the Company has significant influence that are not consolidated under the Company’s consolidation policy are accounted for as equity method investments. SEC Staff Announcement: Accounting for Limited Partnership Investments (codified in Accounting Standards Codification (“ASC”) 323-30-S99-1) guidance requires the use of the equity method unless the investor’s interest “is so minor that the limited partner may have virtually no influence over partnership operating and financial policies.” The SEC staff’s position is that investments in limited partnerships of greater than 3% to 5% are considered more than minor and, therefore, should be accounted for using the equity method.

Related party transactions between the Company and its equity method investee have not been eliminated.

GWG HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

Use of Estimates —The preparation of our condensed consolidated financial statements in conformity with GAAP requires management to make significant estimates and assumptions affecting the reported amounts of assets and liabilities at the date of the condensed consolidated financial statements, as well as the reported amounts of revenue during the reporting period. We regularly evaluate estimates and assumptions, which are based on current facts, historical experience, management’s judgment, and various other factors that we believe to be reasonable under the circumstances. Our actual results may differ materially and adversely from our estimates. The most significant estimates with regard to these condensed consolidated financial statements relate to (1) the determination of the assumptions used in estimating the fair value of our investments in life insurance policies, (2) the assessment of potential impairment of our equity method investment and our equity security investment and determination of the allowance for credit losses on our financing receivable, and (3) the value of our deferred tax assets and liabilities. Periodically, we make significant estimates in assessing the fair value of assets acquired and consideration given in return for those assets, which are used to establish the initial recorded values of such assets in accordance with ASC 805,Business Combinations. Under ASC 805, the consideration paid in an asset acquisition is allocated among the assets acquired based on their relative fair values at acquisition date. In relation to the Exchange Transaction, relative fair values obtained from a third-party valuation firm were used to calculate the amounts recorded for the Commercial Loan, the Exchangeable Note, the equity method investment and the option agreement at their acquisition dates.

Cash and Cash Equivalents —We consider cash in demand deposit accounts and temporary investments purchased with an original maturity of three months or less to be cash equivalents. We maintain our cash and cash equivalents with highly rated financial institutions. The balances in our bank accounts may exceed Federal Deposit Insurance Corporation limits. We periodically evaluate the risk of exceeding insured levels and may transfer funds as we deem appropriate.

Cash, cash equivalents and restricted cash on our condensed consolidated statements of cash flows include cash and cash equivalents of $154.4 million and restricted cash of $20.3 million as of March 31, 2019, and $141.2 million and $16.6 million, respectively, as of March 31, 2018.

Life Insurance Policies — ASC 325-30,Investments in Insurance Contracts,permits a reporting entity to account for its investments in life insurance policies using either the investment method or the fair value method. We elected to use the fair value method to account for our life insurance policies. We initially record our purchase of life insurance policies at the purchase price, which is the amount paid for the policy, inclusive of all external fees and costs associated with the purchase. At each subsequent reporting period, we re-measure the investment at fair value in its entirety and recognize the change in fair value as unrealized gain or loss in the current period, net of premiums paid, within gain (loss) on life insurance policies, net in our condensed consolidated statements of operations.

In a case where our acquisition of a policy is not complete as of a reporting date, but we have nonetheless advanced direct costs and deposits for the acquisition, those costs and deposits are recorded as other assets on our condensed consolidated balance sheets until the acquisition is complete and we have secured title to the policy. On both March 31, 2019 and December 31, 2018, none of our other assets comprised direct costs and deposits that we had advanced for life insurance policy acquisitions.

We also recognize realized gain (or loss) from a life insurance policy upon one of the two following events: (1) our receipt of notice or verified mortality of the insured; or (2) our sale of the policy (upon filing of change-of-ownership forms and receipt of payment). In the case of mortality, the gain (or loss) we recognize is the difference between the policy benefits and the carrying value of the policy once we determine that collection of the policy benefits is realizable and reasonably assured. In the case of a policy sale, the gain (or loss) we recognize is the difference between the sale price and the carrying value of the policy on the date we receive sale proceeds.

Life Insurance Policy Benefits Receivable, Net— Our policy benefit receivables represent amounts due from insurance carriers for claims submitted on matured life insurance policies. Policy benefit receivables are recorded at the policy benefit amounts less reserves for estimated uncollectible amounts. Uncollectible policy benefits can result from challenges by the insurance carrier to the legal validity of the policy, typically related to the concept of insurable interest, or from liquidity or solvency problems at the insurance carrier (although policy benefits are senior to any other obligations of a carrier).

We reserve for policy benefits when it becomes probable that we will not collect the full amount of the policy benefit. The reserve requirements are based on the best facts available to us and are reevaluated and adjusted as additional information becomes available. Uncollectible policy benefits are written off against the reserves when it is deemed that a policy amount is uncollectible. As of March 31, 2019, the balance of the allowance for uncollectible receivables was $4.3 million, relating to a single life insurance policy claim where collection is doubtful.

GWG HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

Other Assets — Included in other assets at March 31, 2019 are $38.6 million of equity security investment (see below), $5.1 million of prepaid expenses, $1.4 million of net fixed assets, $0.6 million of security deposits with states for life settlement provider licenses, $0.3 million net secured merchant cash advances and $4.1 million of other miscellaneous assets — including Life Epigenetics’ exclusive license for the “DNA Methylation Based Predictor of Mortality” technology for the life insurance industry. At December 31, 2018, other assets included $38.6 million of equity security investment, $1.2 million of prepaid expenses, $1.5 million of net fixed assets, $0.6 million of security deposits with states for life settlement provider licenses, $0.5 million net secured merchant cash advances and $3.1 million of other miscellaneous assets.

In December 2018, in connection with the Final Closing of the Exchange Transaction, the Company entered into an Option Agreement with Beneficient. The agreement gives GWG the option to acquire the number of common units in BEN LP that would be received by the holder of NPC-A Prime limited partnership interests of Beneficient Holdings. There is no exercise price and the Company may exercise the option at any time until December 27, 2028, at which time the option will automatically settle. The Option Agreement is recorded in other assets at a value of $38.6 million at both March 31, 2019 and December 31, 2018. The Option Agreement is considered an equity security investment and the Company has elected the measurement alternative for equity securities without a readily determinable fair value. Under this measurement alternative, we record the Option Agreement at its cost, less any impairment, plus or minus changes resulting from observable price changes in orderly transactions for the identical or similar investments of Beneficient. As at March 31, 2019, there were no indications of impairment.The instrument earns a preferred return which we accrue to the investment balance and record in interest and other income in the condensed consolidated statement of operations.

Financing Receivable — ASC 310,Receivables, provides guidance for receivables and notes that arise from credit sales, loans or other transactions. Financing receivable includes loans and notes receivable. Originated loans we hold for which we have the intent and ability to hold for the foreseeable future or to maturity (or payoff) are classified as held for investment. Financing receivables held for investment are reported in our condensed consolidated balance sheets at the outstanding principal balance adjusted for any write-offs, allowance for loan losses, deferred fees or costs, and any unamortized premiums or discounts. Interest income is accrued on outstanding principal as earned. Unamortized discounts and premiums are amortized using the interest method with the amortization recognized as part of interest income in the condensed consolidated statements of operations.

Losses on financing receivables are recognized when they are incurred, which requires us to make our best estimate of probable losses. Specific allowances are recorded for individually impaired loans to the extent we have determined that it is probable that we will be unable to collect all amounts due according to original contractual terms of the loan agreement. Certain loans classified as impaired may not require an allowance for loan loss because we believe that we will ultimately collect the unpaid balance (through collection or collateral repossession). The method for calculating the best estimate of losses depends on the type and risk characteristics of the related financing receivable. Such an estimate requires consideration of historical loss experience, adjusted for current conditions, and judgments about the probable effects of relevant observable data, including present economic conditions such as delinquency rates, financial health of market sectors, and the present and expected future levels of interest rates. The underlying assumptions, estimates and assessments we use to provide for losses are updated periodically to reflect our view of current conditions. Changes in such estimates can significantly affect the allowance and provision for losses. It is possible that we will experience credit losses that are different from our current estimates. We have no allowance for losses at March 31, 2019 or December 31, 2018. Write-offs are deducted from the allowance for losses when we judge the principal to be uncollectible and subsequent recoveries are added to the allowance at the time cash is received on a written-off account.

Equity Method Investment — We account for investments in common stock or in-substance common stock in which we have the ability to exercise significant influence, but do not own a controlling financial interest, under the equity method of accounting. Investments within the scope of the equity method of accounting are initially measured at cost, including the cost of the investment itself and direct transaction costs incurred to acquire the investment. After the initial recognition of the investment at cost, we recognize income and losses from our investment by adjusting upward or downward the balance of our equity method investment on our condensed consolidated balance sheet with such adjustments, if any, flowing through earnings (loss) from equity method investment on our condensed consolidated statement of operations, in all cases adjusted to reflect amortization of basis differences, if any, and the elimination of intercompany gains and losses, if any. Cash distributions received from equity method investees are recorded as reductions to the investment balance and classified on the statement of cash flows using the cumulative earnings approach.

Our equity method investment is reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of the investment might not be recoverable. These circumstances can include, but are not limited to: evidence that we do not have the ability to recover the carrying amount, the inability of the investee to sustain earnings, a current fair value of the investment that is less than the carrying amount, and other investors ceasing to provide support or reduce their financial commitment to the investee. If the fair value of the investment is less than the carrying amount, and the investment will not recover in the near term, then an other-than-temporary impairment may exist. We recognize a loss in value of an investment deemed other-than-temporary in the period the conclusion is made.

GWG HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

The Company reports its share of the income or loss of the equity method partner companies on a one-quarter lag where we do not expect financial information to be consistently available on a timely basis.

For more information on equity method investments, see Note 7.

Leases –The Company currently has one significant lease relating to office space that is classified as an operating lease. We assess whether an arrangement is a lease at inception. Leases with an initial term of twelve months or less are not recorded on the balance sheet. We have elected the practical expedient to not separate lease and non-lease components for all assets. Operating lease assets and operating lease liabilities are calculated based on the present value of the future minimum lease payments over the lease term at the lease start date. As our leases do not provide an implicit rate, we use our incremental borrowing rate based on the information available at the lease start date in determining the present value of future payments. The operating lease asset is increased by any lease payments made at or before the lease start date and reduced by lease incentives and initial direct costs incurred. The lease term includes options to renew or terminate the lease when it is reasonably certain that we will exercise that option. The exercise of lease renewal options is at our sole discretion. The depreciable life of lease assets and leasehold improvements are limited by the lease term, unless there is a transfer of title or purchase option reasonably certain of exercise. Lease expense for operating leases is recognized on a straight-line basis over the lease term.

Stock-Based Compensation — We measure and recognize compensation expense for all stock-based payments at fair value on the grant date over the requisite service period. We use the Black-Scholes option pricing model to determine the weighted-average fair value of stock options and stock appreciation rights. For restricted stock grants (including restricted stock units), fair value is determined as of the closing price of our common stock on the date of grant. Stock-based compensation expense is recorded in general and administrative expenses based on the classification of the employee or vendor. The determination of fair value of stock-based payment awards on the date of grant is affected by our stock price and a number of subjective variables. These variables include, but are not limited to, the expected stock price volatility over the term of the awards and the expected duration of the awards. We account for the effects of forfeitures as they occur.

The risk-free interest rate is based on the U.S. Treasury rates at the date of grant with maturity dates approximately equal to the expected life at grant date. Volatility is based on the standard deviation of the average continuously compounded rate of return of five selected companies.

Deferred Financing and Issuance Costs— Loans advanced to us under our amended and restated senior credit facility with LNV Corporation, as described in Note 8, are reported net of financing costs, including issuance costs, sales commissions and other direct expenses, which are amortized using the straight-line method over the term of the facility. The L Bonds, as described in Note 9, are reported net of financing costs, which are amortized using the interest method over the term of those borrowings. Selling and issuance costs of Redeemable Preferred Stock (“RPS”) and Series 2 Redeemable Preferred Stock (“RPS 2”), described in Notes 11 and 12, are netted against additional paid-in-capital, until depleted, and then against the outstanding balance of the preferred stock are netted against additional paid-in-capital, until depleted, and then against the outstanding balance of the preferred stock. The offerings of our RPS and RPS 2 closed in March 2017 and April 2018, respectively. There were no issuance costs associated with August 2018 issuance of the Series B Convertible Preferred Stock (“Series B”), described in Note 13.

Earnings (Loss) per Share —Basic earnings (loss) per share attributable to common shareholders are calculated using the weighted-average number of shares outstanding during the reported period. Diluted earnings (loss) per share are calculated based on the potential dilutive impact of our RPS, RPS 2, restricted stock units, warrants and stock options. Due to our net loss attributable to common shareholders for the three months ended March 31, 2019 and 2018, there are no dilutive securities.

Reclassification — Certain prior year amounts have been reclassified for consistency with the current year presentation. These reclassifications had no effect on the reported results of operations. See Note 22 for an explanation of certain reclassifications we recorded in comparative periods on the guarantor financial statements.

Newly Adopted Accounting Pronouncements — On January 1, 2019, we adopted Accounting Standards Update (“ASU”) No. 2016-02,Leases (Topic 842). ASU 2016-02 requires lessees to recognize right-of-use assets and lease liabilities on the balance sheet for all leases with a term greater than twelve months. We elected to adopt the standard using the modified retrospective method, without restatement of prior periods’ financial information. The impact to the balance sheet was the addition of approximately $0.9 million in right-of-use assets, a reduction to deferred rent of $0.7 million, and a net increase to lease liabilities of $1.6 million for our operating lease. The adoption of the new standard did not materially affect our condensed consolidated statements of operations, condensed consolidated statements of cash flows or condensed consolidated statements of changes in stockholders’ equity.

GWG HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

Recently Issued Accounting Pronouncements— In June 2016, the FASB issued ASU No. 2016-13,Financial Instruments — Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments,which changes the impairment model for most financial assets and certain other instruments, including trade and other receivables, held-to-maturity debt securities and loans. The standard requires entities to use a new, forward-looking “expected loss” model that is expected to generally result in the earlier recognition of allowances for losses. The guidance is effective for annual periods beginning after December 15, 2019, including interim periods within those years, but early adoption is permitted. The Company is evaluating the potential impact of this guidance on our condensed consolidated financial statements.

In August 2018, the FASB issued ASU No. 2018-13, Fair Value Measurement (Topic 820): Disclosure Framework — Changes to the Disclosure Requirements for Fair Value Measurement, which eliminates, adds and modifies certain disclosure requirements for fair value measurements. The guidance is effective for fiscal years and interim periods beginning after December 15, 2019. Certain of the amendments require prospective application, while the remainder require retrospective application. Early adoption is allowed either for the entire standard or only the provisions that eliminate or modify the requirements. The Company is currently evaluating the potential impact of this guidance on our condensed consolidated financial statements.

(2) Correction of an Immaterial Error

In the condensed consolidated statement of cash flows for the three months ended March 31, 2018, we have separated the gross borrowings and repayments on our senior credit facility that were previously erroneously reported on a net basis in cash flows from financing activities.

For the three months ended March 31, 2018, we previously reported net repayments of senior debt of $3.1 million. We have revised the comparative information for the three months ended March 31, 2018 to report gross borrowings on senior debt of $9.6 million and gross repayments of senior debt of $12.7 million in the condensed consolidated statement of cash flows. This revision had no effect on the total cash flows from financing activities.

(3) Restrictions on Cash

Under the terms of our amended and restated senior credit facility with LNV Corporation (discussed in Note 8), we are required to maintain collection and payment accounts that are used to collect policy benefits from pledged policies, pay annual policy premiums, interest and other charges under the facility, and distribute funds to pay down the facility.

The agents for the lender authorize the disbursements from these accounts. At March 31, 2019 and December 31, 2018, there was a balance of $17,724,000 and $4,164,000, respectively, in these collection and payment accounts.

To fund the Company’s acquisition of life insurance policies, we are required to maintain escrow accounts. Distributions from these accounts are made according to life insurance policy purchase contracts. At March 31, 2019 and December 31, 2018, there was a balance of $2,587,000 and $6,685,000, respectively, in the Company’s escrow accounts.

(4) Investment in Life Insurance Policies

Our investments in life insurance policies are valued based on unobservable inputs that are significant to their overall fair value. Changes in the fair value of these policies, net of premiums paid, are recorded in gain (loss) on life insurance policies, net in our condensed consolidated statements of operations. Fair value is determined on a discounted cash flow basis that incorporates life expectancy assumptions generally derived from reports obtained from widely accepted life expectancy providers (other than insured lives covered under small face amount policies — those with $1 million in face value benefits or less — which utilize either a single fully underwritten, or simplified report based on self-reported medical interview), assumptions relating to cost-of-insurance (premium) rates and other assumptions. The discount rate we apply incorporates current information about the discount rates observed in the life insurance secondary market, fixed income market interest rates, the estimated credit exposure to the insurance companies that issued the life insurance policies and management’s estimate of the operational risk premium a purchaser would require to receive the future cash flows derived from our portfolio as a whole. Management has significant discretion regarding the combination of these and other factors when determining the discount rate. As a result of management’s analysis, a discount rate of 8.25% was applied to our portfolio as of both March 31, 2019 and December 31, 2018.

GWG HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

Portfolio Information

Our portfolio of life insurance policies, owned by our subsidiaries as of March 31, 2019, is summarized below:

Life Insurance Portfolio Summary

| Total life insurance portfolio face value of policy benefits | | $ | 2,098,428,000 | |

| Average face value per policy | | $ | 1,757,000 | |

| Average face value per insured life | | $ | 1,885,000 | |

| Average age of insured (years)* | | | 81.7 | |

| Average life expectancy estimate (years)* | | | 7.6 | |

| Total number of policies | | | 1,194 | |

| Number of unique lives | | | 1,113 | |

| Demographics | | | 78% Males; 22% Females | |

| Number of smokers | | | 53 | |

| Largest policy as % of total portfolio face value | | | 0.6 | % |

| Average policy as % of total portfolio | | | 0.1 | % |

| Average annual premium as % of face value | | | 3.0 | % |

| * | Averages presented in the table are weighted averages. |

A summary of our policies, organized according to their estimated life expectancy dates as of the reporting date, is as follows:

| | | As of March 31, 2019 | | | As of December 31, 2018 | |

| Years Ending December 31, | | Number of

Policies | | | Estimated

Fair Value | | | Face Value | | | Number of

Policies | | | Estimated

Fair Value | | | Face Value | |

| 2019 | | | 6 | | | $ | 4,118,000 | | | $ | 4,445,000 | | | | 9 | | | $ | 6,380,000 | | | $ | 7,305,000 | |

| 2020 | | | 33 | | | | 34,924,000 | | | | 43,429,000 | | | | 41 | | | | 46,338,000 | | | | 59,939,000 | |

| 2021 | | | 76 | | | | 66,708,000 | | | | 97,989,000 | | | | 81 | | | | 68,836,000 | | | | 108,191,000 | |

| 2022 | | | 109 | | | | 99,532,000 | | | | 175,228,000 | | | | 104 | | | | 97,231,000 | | | | 177,980,000 | |

| 2023 | | | 115 | | | | 105,957,000 | | | | 206,536,000 | | | | 109 | | | | 93,196,000 | | | | 185,575,000 | |

| 2024 | | | 120 | | | | 97,732,000 | | | | 228,427,000 | | | | 107 | | | | 84,150,000 | | | | 211,241,000 | |

| Thereafter | | | 735 | | | | 373,214,000 | | | | 1,342,374,000 | | | | 703 | | | | 351,791,000 | | | | 1,297,761,000 | |

| Totals | | | 1,194 | | | $ | 782,185,000 | | | $ | 2,098,428,000 | | | | 1,154 | | | $ | 747,922,000 | | | $ | 2,047,992,000 | |

We recognized life insurance benefits of $30,459,000 and $14,504,000 during the three months ended March 31, 2019 and 2018, respectively, related to policies with a carrying value of $8,701,000 and $5,083,000, respectively, and as a result recorded realized gains of $21,758,000 and $9,421,000.

A reconciliation of gain (loss) on life insurance policies is as follows:

| | | Three Months Ended

March 31, | |

| | | 2019 | | | 2018 | |

| Change in estimated probabilistic cash flows(1) | | $ | 17,131,000 | | | $ | 19,005,000 | |

| Unrealized gain on acquisitions(2) | | | 4,459,000 | | | | 6,974,000 | |

| Premiums and other annual fees | | | (15,832,000 | ) | | | (12,197,000 | ) |

| Change in discount rates(3) | | | - | | | | - | |

| Change in life expectancy evaluation(4) | | | - | | | | (4,868,000 | ) |

| Face value of matured policies | | | 30,459,000 | | | | 14,504,000 | |

| Fair value of matured policies | | | (14,721,000 | ) | | | (9,549,000 | ) |

| Gain (loss) on life insurance policies, net | | $ | 21,496,000 | | | $ | 13,869,000 | |

| (1) | Change in fair value of expected future cash flows relating to our investment in life insurance policies that are not specifically attributable to changes in life expectancy, discount rate changes or policy maturity events. |

| (2) | Gain resulting from fair value in excess of the purchase price for life insurance policies acquired during the reporting period. |

| (3) | The discount rate applied to estimate the fair value of the portfolio of life insurance policies we own was 8.25% at both March 31, 2019 and December 31, 2018, and 10.45% at both March 31, 2018 and December 31, 2017. |

| (4) | The change in fair value due to updating life expectancy estimates on certain life insurance policies in our portfolio. |

GWG HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

Estimated premium payments and servicing fees required to maintain our current portfolio of life insurance policies in force for the next five years, assuming no mortalities, are as follows:

| Years Ending December 31, | | Premiums | | | Servicing | | | Premiums and

Servicing Fees | |

| Nine months ending December 31, 2019 | | $ | 50,753,000 | | | $ | 1,413,000 | | | $ | 52,166,000 | |

| 2020 | | | 78,314,000 | | | | 1,413,000 | | | | 79,727,000 | |

| 2021 | | | 90,938,000 | | | | 1,413,000 | | | | 92,351,000 | |

| 2022 | | | 104,170,000 | | | | 1,413,000 | | | | 105,583,000 | |

| 2023 | | | 116,608,000 | | | | 1,413,000 | | | | 118,021,000 | |

| 2024 | | | 126,999,000 | | | | 1,413,000 | | | | 128,412,000 | |

| | | $ | 567,782,000 | | | $ | 8,478,000 | | | $ | 576,260,000 | |

Management anticipates funding the majority of the premium payments and servicing fees estimated above from cash flows realized from life insurance policy benefits, and to the extent necessary, with additional borrowing capacity created as the premiums and servicing costs of pledged life insurance policies become due, under the amended and restated senior credit facility with LNV Corporation as described in Note 8, and the net proceeds from our offering of L Bonds as described in Note 9. Management anticipates funding premiums and servicing costs of non-pledged life insurance policies with cash flows realized from life insurance policy benefits from our portfolio of life insurance policies and net proceeds from our offering of L Bonds. The proceeds of these capital sources may also be used for the purchase, policy premiums and servicing costs of additional life insurance policies, working capital and financing expenditures including paying principal, interest and dividends.

(5) Fair Value Definition and Hierarchy

ASC 820,Fair Value Measurements and Disclosures,establishes a hierarchical disclosure framework that prioritizes and ranks the level of market price observability used in measuring assets and liabilities at fair value. Market price observability is affected by a number of factors, including the type of investment, the characteristics specific to the investment and the state of the marketplace, including the existence and transparency of transactions between market participants. Assets and liabilities with readily available and actively quoted prices, or for which fair value can be measured from actively quoted prices in an orderly market, generally will have a higher degree of market price observability and a lesser degree of judgment used in measuring fair value.

ASC 820 maximizes the use of observable inputs and minimizes the use of unobservable inputs by requiring the use of observable inputs whenever available. Observable inputs are inputs that market participants would use in pricing the asset or liability developed based on market data obtained from independent sources. Unobservable inputs are inputs that reflect assumptions about how market participants price an asset or liability based on the best available information. Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability (i.e., the “exit price”) in an orderly transaction between market participants at the measurement date (a non-distressed transaction in which neither seller nor buyer is compelled to engage in the transaction). A sale of the portfolio or a portion of the portfolio in an other than orderly transaction would likely occur at less than the fair value of the respective life insurance policies.

The hierarchy is broken down into three levels based on the observability of inputs as follows:

| Level 1 — | Valuations based on quoted prices in active markets for identical assets or liabilities that the Company has the ability to access. Valuations are based on quoted prices that are readily and regularly available in an active market. |

| Level 2 — | Valuations based on one or more quoted prices in markets that are not active or for which all significant inputs are observable, either directly or indirectly. |

| Level 3 — | Valuations based on inputs that are unobservable and significant to the overall fair value measurement. |

The availability of observable inputs can vary by types of assets and liabilities and is affected by a wide variety of factors, including, for example, whether an instrument is established in the marketplace, the liquidity of markets and other characteristics particular to the transaction. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised by management in determining fair value is greatest for assets and liabilities categorized in Level 3.

GWG HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

Level 3 Valuation Process

The estimated fair value of our portfolio of life insurance policies is determined on a quarterly basis by management taking into consideration a number of factors, including changes in discount rate assumptions, estimated premium payments and life expectancy estimate assumptions, as well as any changes in economic and other relevant conditions. The discount rate incorporates current information about discount rates observed in the life insurance secondary market, fixed income market interest rates, the estimated credit exposure to the insurance company that issued the life insurance policy and management’s estimate of the operational risk premium a purchaser would require to receive the future cash flows derived from our portfolio as a whole. Management has significant discretion regarding the combination of these and other factors when determining the discount rate.

These inputs are then used to estimate the discounted cash flows from the portfolio using the ClariNet LS probabilistic and stochastic portfolio pricing model from ClearLife Limited, which estimates the expected cash flows using various mortality probabilities and scenarios. The valuation process includes a review by senior management as of each quarterly valuation date. We also engage ClearLife Limited to prepare a net present value calculation of our life insurance portfolio using the inputs we provide on a quarterly basis. A copy of a letter documenting the ClariNet LS calculation as of March 31, 2019 is filed as Exhibit 99.1 to this report.

The following table reconciles the beginning and ending fair value of our Level 3 investments in our portfolio of life insurance policies for the periods ended March 31, as follows:

| | | Three Months Ended

March 31, | |

| | | 2019 | | | 2018 | |

| Beginning balance | | $ | 747,922,000 | | | $ | 650,527,000 | |

| Purchases | | | 27,393,000 | | | | 25,300,000 | |

| Maturities (initial cost basis) | | | (8,701,000 | ) | | | (5,083,000 | ) |

| Net change in fair value | | | 15,571,000 | | | | 16,645,000 | |

| Ending balance | | $ | 782,185,000 | | | $ | 687,389,000 | |

Historically, for life insurance policies with face amounts greater than $1 million and that are not pledged as collateral under our amended and restated senior credit facility with LNV Corporation (approximately 25.5% of our portfolio by face amount of policy benefits), we attempted to obtain updated life expectancy reports on a continuous rotating three year cycle. For life insurance policies that are pledged under our amended and restated senior credit facility with LNV Corporation (approximately 62.6% of our portfolio by face amount of policy benefits), we are presently required to begin to update the life expectancy estimates every two years beginning from the closing date of the amended and restated senior credit facility with LNV Corporation. For the remaining small face insurance policies (i.e., a policy with $1 million in face value benefits or less), we historically employed other methods and timeframes to update life expectancy estimates.

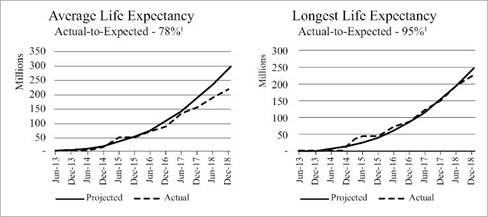

With the adoption of the Longest Life Expectancy method in the fourth quarter of 2018 (as described under “Fair Value Components — Life Expectancies” within the Management Discussion and Analysis section), we discontinued the practice of obtaining updated life expectancy reports (or updating specific life expectancies in any manner) except as may be required by lenders to comply with existing and future covenants within credit facilities. This change was accounted for as a change in accounting estimate and affects current and future periods. To the extent such updated life expectancy reports are available, we do not expect to incorporate these life expectancy reports into our revised valuation methodology; however, we will monitor this data to determine over time if there exists any additive predictive value in relation to the basis of its mortality projections.

The following table summarizes the inputs utilized in estimating the fair value of our portfolio of life insurance policies:

| | | As of

March 31,

2019 | | | As of

December 31,

2018 | |

| Weighted-average age of insured, years* | | | 81.7 | | | | 82.1 | |

| Weighted-average life expectancy, months* | | | 91.7 | | | | 93.2 | |

| Average face amount per policy | | $ | 1,757,000 | | | $ | 1,775,000 | |

| Discount rate | | | 8.25 | % | | | 8.25 | % |

| (*) | Weighted-average by face amount of policy benefits |

GWG HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

Life expectancy estimates and market discount rates for a portfolio of life insurance policies are inherently uncertain and the effect of changes in estimates may be significant. For example, if the life expectancy estimates were increased or decreased by four and eight months on each outstanding policy, and the discount rates were increased or decreased by 1% and 2%, with all other variables held constant, the fair value of our investment in life insurance policies would increase or decrease as summarized below:

Change in Fair Value of the Investment in Life Insurance Policies

| | | Change in Life Expectancy Estimates | |

| | | minus

8 months | | | minus

4 months | | | plus

4 months | | | plus

8 months | |

| March 31, 2019 | | $ | 116,407,000 | | | $ | 59,103,000 | | | $ | (56,941,000 | ) | | $ | (113,465,000 | ) |

| December 31, 2018 | | $ | 113,410,000 | | | $ | 57,661,000 | | | $ | (55,470,000 | ) | | $ | (110,473,000 | ) |

| | | Change in Discount Rate | |

| | | minus 2% | | | minus 1% | | | plus 1% | | | plus 2% | |

| March 31, 2019 | | $ | 97,636,000 | | | $ | 46,366,000 | | | $ | (42,069,000 | ) | | $ | (80,359,000 | ) |

| December 31, 2018 | | $ | 95,747,000 | | | $ | 45,440,000 | | | $ | (41,179,000 | ) | | $ | (78,615,000 | ) |

Other Fair Value Considerations

The carrying value of policy benefit receivables, prepaid expenses, accounts payable and accrued expenses approximate fair value due to their short-term maturities and low credit risk. Using the income-based valuation approach, the estimated fair value of our L Bonds and Seller Trust L Bonds, largely containing the same terms, having an aggregate face value of $1,136,199,000 as of March 31, 2019, is approximately $1,164,650,000 based on a weighted-average market interest rate of 7.02%.

The Commercial Loan receivable from BEN LP has a below-market interest rate of 5.0% per year; provided that the accrued interest from the date of the Initial Transfer to the Final Closing Date of the Exchange Transaction was added to the principal balance of the Commercial Loan. From and after the Final Closing Date, one-half of the interest, or 2.5% per year, is due and payable monthly in cash, and (ii) one-half of the interest, or 2.5% per year, accrues and compounds annually on each anniversary date of the Final Closing Date and becomes due and payable in full in cash on the maturity date. Utilizing an implied yield of 6.75%, we estimate the fair value of the Commercial Loan to be approximately $185,222,000 as of March 31, 2019 based on a market yield analysis for similar instruments with similar credit profiles.

The carrying value of the amended and restated senior credit facility with LNV Corporation reflects interest charged at 12-month LIBOR plus an applicable margin. The margin represents our credit risk, and the strength of the portfolio of life insurance policies collateralizing the debt. The overall rate reflects the current interest rate market, and the carrying value of the facility approximates fair value.

GWG MCA Capital, Inc. (“GWG MCA”) participated in the merchant cash advance industry by directly advancing sums to merchants and lending money, on a secured basis, to companies that advance sums to merchants. Each quarter, we review the carrying value of these cash advances, determine if an impairment exists and establish or adjust an allowance for loan loss as necessary. At March 31, 2019, one of our secured cash advances was impaired. Specifically, the secured loan to Nulook Capital LLC had an outstanding balance of $1,879,000 and an allowance for loan loss of $1,879,000 at March 31, 2019. We deem fair value to be the estimated collectible value on each loan or advance made from GWG MCA. Secured merchant cash advances, net of allowance for loan loss, of $258,000 and $547,000 are included within other assets on our condensed consolidated balance sheets as of March 31, 2019 and December 31, 2018, respectively. Where we estimate the collectible amount to be less than the outstanding balance, we record an allowance for the difference. Provision for merchant cash advances are recorded within other expenses on our condensed consolidated statements of operations (see Note 17).

GWG HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

Certain assets are subject to periodic impairment testing by comparing the respective carrying value of the asset to its estimated fair value. In the event we determine these assets to be impaired, we would recognize an impairment loss equal to the amount by which the carrying value of the impaired asset exceeds its estimated fair value. These periodic impairment tests utilize company-specific assumptions involving significant unobservable inputs, or Level 3, in the fair value hierarchy.

The following table summarizes outstanding common stock warrants (discussed in Note 15) as of March 31, 2019:

| Month issued | | Warrants issued | | | Fair value

per share | | | Risk free rate | | | Volatility | | | Term |

| September 2014 | | | 16,000 | | | $ | 1.26 | | | | 1.85 | % | | | 17.03 | % | | 5 years |

| | | | 16,000 | | | | | | | | | | | | | | | |

(6) Financing Receivable from Affiliate

Commercial Loan

On August 10, 2018, in connection with the Initial Transfer of the Exchange Transaction, GWG Life, as lender, and BEN LP, as borrower, entered into the Commercial Loan Agreement. On December 28, 2018, the Final Closing Date of the Exchange Transaction, the agreement was amended to adjust the principal to $192,508,000. The principal amount under the Commercial Loan is due on August 9, 2023, but is extendable for two five-year terms under certain circumstances. The extensions are available to the borrower provided that (a) in the event BEN LP completes at least one public offering of its common units raising at least $50,000,000, which on its own or together with any other public offering of BEN LP’s common units results in Beneficient raising at least $100,000,000, then the maturity date will be extended to August 9, 2028; and (b) in the event that BEN LP (i) completes at least one public offering of its common units raising at least $50,000,000, which on its own or together with any other public offering of BEN LP’s common units results in Beneficient raising at least $100,000,000 and (ii) at least 75% of Beneficient Holding’s total outstanding NPC-B limited partnership interests, if any, have been converted to shares of BEN LP’s common units, then the maturity date will be extended to August 9, 2033.

Repayment of the Commercial Loan is subordinated in right of payment to other Beneficient obligations, including (i) Beneficient’s exiting senior debt obligations, (ii) any of Beneficient’s commercial bank debt and (iii) any Beneficient obligations that may arise in connection with the issuance of Preferred Series B Unit Accounts of Beneficient Holdings. BEN LP’s obligations under the Commercial Loan Agreement are unsecured.

The Commercial Loan Agreement contains negative covenants that limit or restrict, subject to certain exceptions, the incurrence of liens and indebtedness by Beneficient, fundamental changes to its business and transactions with affiliates. The Commercial Loan Agreement also contains customary affirmative covenants, including, but not limited to, preservation of corporate existence, compliance with applicable law, payment of taxes, notice of material events, financial reporting and keeping of proper books of record and account.

The Commercial Loan Agreement includes customary events of default, including, but not limited to, non-payment of principal or interest, failure to comply with covenants, failure to pay other indebtedness when due, cross-acceleration to other debt, material adverse effects, events of bankruptcy and insolvency, and unsatisfied judgments. The borrower was in violation of certain of its financial reporting covenants in the Commercial Loan Agreement as of March 31, 2019. GWG Life has agreed to a forbearance of its rights and remedies under the Commercial Loan Agreement relating to such noncompliance until July 31, 2019. As of the date of this filing, the borrower is current on its financial reporting covenants.

The principal amount of the Commercial Loan bears interest at 5.00% per year from the Final Closing Date. One-half of the interest, or 2.50% per year, is due and payable monthly in cash, and (ii) one-half of the interest, or 2.50% per year, accrues and compounds annually on each anniversary date of the Final Closing Date and becomes due and payable in full in cash on the maturity date. The accrued interest from the Initial Transfer to the Final Closing Date was added to the principal amount of the Commercial Loan. The Commercial Loan was recorded at a discount as a result of the relative fair value allocations for the assets received in the Initial Transfer of the Exchange Transaction. Under ASC 805,Business Combinations, the consideration paid in an asset acquisition is allocated among the assets acquired based on their relative fair values at acquisition date. The discount is being amortized to interest income over the term of the loan.

In accordance with the Supplemental Indenture issuing the Seller Trust L Bonds, upon a redemption event or at the maturity date of the Seller Trust L Bonds, the Company, at its option, may use the outstanding principal amount of the Commercial Loan, and accrued and unpaid interest thereon, as repayment consideration of the Seller Trust L Bonds (see Note 10).

GWG HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

The following table summarizes outstanding principal, discount and accrued interest balances of the Commercial Loan receivable:

| | | As of

March 31,

2019 | | | As of

December 31,

2018 | |

| Commercial Loan receivable – principal | | $ | 192,508,000 | | | $ | 192,508,000 | |

| Discount on Commercial Loan receivable | | | (7,427,000 | ) | | | (7,846,000 | ) |

| Accrued interest receivable on Commercial Loan | | | 1,657,000 | | | | 107,000 | |

| Financing receivable from affiliate | | $ | 186,738,000 | | | $ | 184,769,000 | |

(7) Equity Method Investment

During 2018, in connection with the Initial Transfer and Final Closing of the Exchange Transaction, we acquired 40.5 million common units of BEN LP for a total limited partnership interest in the common units of BEN LP of approximately 89.9% as of December 31, 2018. The common units of BEN LP are not publicly traded on a stock exchange.

In accordance with ASC 810,Consolidation, the Company assesses whether it has a variable interest in legal entities in which it has a financial relationship and, if so, whether or not those entities are variable interest entities (“VIEs”). For those entities that qualify as VIEs, ASC 810 requires the Company to determine if the Company is the primary beneficiary of the VIE, and if so, to consolidate the VIE.