As filed with the Securities and Exchange Commission on October 24, 2012

Registration No. 333-174764

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form S-1

PRE-EFFECTIVE AMENDMENT NO. 8 TO

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Nuveen Long/Short Commodity Total Return Fund

(Exact name of Registrant as specified in its charter)

| | | | |

| Delaware | | 6799 | | 45-2470177 |

(State or other jurisdiction of incorporation or organization) | | (Primary Standard Industrial Classification Code Number) | | (I.R.S. Employer Identification No.) |

333 West Wacker Drive, Suite 3300

Chicago, Illinois 60606

(877) 827-5920

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

William Adams IV

Nuveen Commodities Asset Management, LLC

President

333 West Wacker Drive, Suite 3300

Chicago, Illinois 60606

(877) 827-5920

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| | |

Donald S. Weiss, Esq. J. Craig Walker, Esq. K&L Gates LLP 70 West Madison Street Chicago, Illinois 60602 (312) 372-1121 | | Leonard B. Mackey, Jr., Esq. David Yeres, Esq. Clifford R. Cone, Esq. Clifford Chance US LLP 31 West 52nd Street New York, New York 10019 (212) 878-8000 |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act of 1933, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act of 1933, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act of 1933, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| | |

Large accelerated filer ¨ | | Accelerated filer ¨ |

| | |

| Non-accelerated filer (Do not check if a smaller reporting company) x | | Smaller reporting company ¨ |

CALCULATION OF REGISTRATION FEE

| | | | | | | | |

|

Title of Each Class of Securities to be Registered | | Amount

to be

Registered | | Proposed

Maximum

Offering Price

per Unit(1) | | Proposed

Maximum

Aggregate

Offering Price(1) | | Amount of

Registration

Fee(2) |

Common Units of Beneficial Interest (“Shares”) of Nuveen Long/Short Commodity Total Return Fund | | 21,600,000 Shares | | $25.00 | | $540,000,000 | | $73,656.00 |

|

| (1) | Estimated solely for the purpose of calculating the registration fee. |

| (2) | $22,920.00 of this amount has been previously paid. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any jurisdiction where the offer or sale is not permitted.

| | | | | | |

| PROSPECTUS | | Subject to Completion Preliminary Prospectus dated October 24, 2012 | | |  | |

8,000,000 Shares

Nuveen Long/Short Commodity Total Return Fund

$25.00 per Share

The Nuveen Long/Short Commodity Total Return Fund (the “Fund”) is a commodity pool. The Fund issues shares, which represent units of fractional undivided beneficial interest in and ownership of the Fund. The Fund’s investment objective is to generate attractive total returns. The Fund is actively managed and seeks to outperform its benchmark, the Morningstar® Long/Short Commodity IndexSM. In pursuing its investment objective, the Fund will invest directly in a diverse portfolio of exchange-traded commodity futures contracts that represent the main commodity sectors and are among the most actively traded futures contracts in the global commodity markets. Generally, individual commodity futures positions may be either long or short (or flat in the special case of energy futures contracts, as described in the Prospectus Summary under “Investment Strategy”) depending upon market conditions. The Fund is unleveraged, and the Fund’s commodity futures contracts will be fully collateralized with cash equivalents, U.S. government securities and other short-term, high grade debt securities. Depending on market conditions, the Fund anticipates that it will make regular monthly distributions to shareholders commencing approximately 60 days after this initial offering. Nuveen Commodities Asset Management, LLC will be the manager of the Fund. Gresham Investment Management LLC, an affiliate of the manager, through one of its divisions, will be responsible for the Fund’s commodity investments. Nuveen Asset Management, LLC, an affiliate of the manager, will be responsible for the Fund’s collateral investments.

Investing in the Fund involves significant risks. See “Risk Factors” starting on page 22.

| | • | | Because the Fund has not commenced business, its shares have no history of public trading, and the Fund does not have any performance history. |

| | • | | Shares of the Fund may trade at a discount from their net asset value, which could be significant. |

| | • | | Fund shares are subject to investment risk, including the possible loss of the entire amount of your investment. |

| | • | | Investments in commodities have a high degree of price variability and are subject to rapid and substantial price changes. |

| | • | | The Fund is not a complete investment program and is designed as a long-term investment and not as a short-term trading vehicle. |

| | • | | The Fund may not be able to achieve its investment objective. |

It is anticipated that the Fund’s shares will be approved for listing on the NYSE MKT, subject to notice of issuance, under the trading or “ticker” symbol “CTF.”

The Fund qualifies as an “emerging growth company” as defined under the Jumpstart Our Business Startups Act. “Emerging growth company” does not mean that the Fund is a “growth” type of investment vehicle or that it will utilize a “growth” investment strategy. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Emerging Growth Company Status.”

THE FUND IS NOT A MUTUAL FUND, A CLOSED-END FUND, OR ANY OTHER TYPE OF “INVESTMENT COMPANY” WITHIN THE MEANING OF THE INVESTMENT COMPANY ACT OF 1940, AS AMENDED, AND IS NOT SUBJECT TO REGULATION NOR AFFORDED THE PROTECTIONS THEREUNDER.

THE COMMODITY FUTURES TRADING COMMISSION HAS NOT PASSED UPON THE MERITS OF PARTICIPATING IN THIS POOL NOR HAS THE COMMISSION PASSED ON THE ADEQUACY OR ACCURACY OF THIS DISCLOSURE DOCUMENT.

This prospectus is in two parts: a disclosure document and a statement of additional information. These parts are bound together and both contain important information.

| | | | | | |

| | | Per Share

| | | Total(3) |

Public offering price | | | $25.000 | | | $ |

Underwriting commissions(1) | | | $1.125 | | | $ |

Estimated offering expenses(2) | | | $.050 | | | $ |

Proceeds, after expenses, to the Fund(2)(3) | | | $23.825 | | | $ |

| | (1) | Nuveen Commodities Asset Management, LLC (and not the Fund) has agreed to pay from its own assets a structuring fee to Merrill Lynch, Pierce, Fenner & Smith Incorporated, Citigroup Global Markets Inc., Morgan Stanley & Co. LLC and UBS Securities LLC and may also pay certain qualifying underwriters a structuring fee, a sales incentive fee or additional compensation in connection with the offering. See “Underwriting.” |

| | (2) | After payment of expenses relating to issuance and distribution (other than underwriting commissions), proceeds to the Fund will be $23.825 per share. Nuveen Securities, LLC has agreed to (i) reimburse all organization expenses of the Fund and (ii) pay the amount by which the Fund’s offering costs (other than commissions) exceed $.05 per common share. |

| | (3) | The Fund has granted the underwriters an option to purchase up to additional shares at the public offering price less the underwriting commissions within 30 days from the date of this prospectus. If such option is exercised in full, the total public offering price, underwriting commissions, offering expenses (payable by the Fund) and proceeds to the Fund will be $ , $ , $ , and $ , respectively. See “Underwriting.” |

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the securities offered in this prospectus, or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares to purchasers on or about , 2012.

| | | | | | | | | | |

| BofA Merrill Lynch | | | | | | | | |

| | | Citigroup | | | | |

| | | Morgan Stanley | | | | |

| | | | | UBS Investment Bank |

| | | | | | | | | Nuveen Securities |

| | | | |

| Barclays | | Oppenheimer & Co. | | RBC Capital Markets |

| BB&T Capital Markets | | Deutsche Bank Securities | | Ladenburg Thalmann & Co. Inc. |

| Maxim Group LLC | | Southwest Securities | | Wunderlich Securities |

The date of this prospectus is , 2012.

COMMODITY FUTURES TRADING COMMISSION

RISK DISCLOSURE STATEMENT

YOU SHOULD CAREFULLY CONSIDER WHETHER YOUR FINANCIAL CONDITION PERMITS YOU TO PARTICIPATE IN A COMMODITY POOL. IN SO DOING, YOU SHOULD BE AWARE THAT COMMODITY INTEREST TRADING CAN QUICKLY LEAD TO LARGE LOSSES AS WELL AS GAINS. SUCH TRADING LOSSES CAN SHARPLY REDUCE THE NET ASSET VALUE OF THE POOL AND CONSEQUENTLY THE VALUE OF YOUR INTEREST IN THE POOL. IN ADDITION, RESTRICTIONS ON REDEMPTIONS MAY AFFECT YOUR ABILITY TO WITHDRAW YOUR PARTICIPATION IN THE POOL.

FURTHER, COMMODITY POOLS MAY BE SUBJECT TO SUBSTANTIAL CHARGES FOR MANAGEMENT, AND ADVISORY AND BROKERAGE FEES. IT MAY BE NECESSARY FOR THOSE POOLS THAT ARE SUBJECT TO THESE CHARGES TO MAKE SUBSTANTIAL TRADING PROFITS TO AVOID DEPLETION OR EXHAUSTION OF THEIR ASSETS. THIS DISCLOSURE DOCUMENT CONTAINS A COMPLETE DESCRIPTION OF EACH EXPENSE TO BE CHARGED THIS POOL AT PAGES 20-21 AND A STATEMENT OF THE PERCENTAGE RETURN NECESSARY TO BREAK EVEN, THAT IS, TO RECOVER THE AMOUNT OF YOUR INITIAL INVESTMENT, AT PAGES 18-19.

THIS BRIEF STATEMENT CANNOT DISCLOSE ALL THE RISKS AND OTHER FACTORS NECESSARY TO EVALUATE YOUR PARTICIPATION IN THIS COMMODITY POOL. THEREFORE, BEFORE YOU DECIDE TO PARTICIPATE IN THIS COMMODITY POOL, YOU SHOULD CAREFULLY STUDY THIS DISCLOSURE DOCUMENT, INCLUDING A DESCRIPTION OF THE PRINCIPAL RISK FACTORS OF THIS INVESTMENT, AT PAGES 22-36.

YOU SHOULD ALSO BE AWARE THAT THIS COMMODITY POOL MAY TRADE FOREIGN FUTURES OR OPTIONS CONTRACTS. TRANSACTIONS ON MARKETS LOCATED OUTSIDE THE UNITED STATES, INCLUDING MARKETS FORMALLY LINKED TO A UNITED STATES MARKET, MAY BE SUBJECT TO REGULATIONS WHICH OFFER DIFFERENT OR DIMINISHED PROTECTION TO THE POOL AND ITS PARTICIPANTS. FURTHER, UNITED STATES REGULATORY AUTHORITIES MAY BE UNABLE TO COMPEL THE ENFORCEMENT OF THE RULES OF REGULATORY AUTHORITIES OR MARKETS IN NON-UNITED STATES JURISDICTIONS WHERE TRANSACTIONS FOR THE POOL MAY BE EFFECTED.

OTHER REGULATORY NOTICES

THE BOOKS AND RECORDS OF THE FUND WILL BE MAINTAINED AT THE OFFICES OF NUVEEN COMMODITIES ASSET MANAGEMENT, LLC, OR ITS ADMINISTRATIVE AGENT AND WILL OTHERWISE BE MAINTAINED IN ACCORDANCE WITH THE RULES OF THE COMMODITY FUTURES TRADING COMMISSION.

THIS POOL HAS NOT COMMENCED TRADING AND DOES NOT HAVE ANY PERFORMANCE HISTORY.

YOU SHOULD RELY ONLY ON THE INFORMATION CONTAINED OR INCORPORATED BY REFERENCE IN THIS PROSPECTUS. THE FUND HAS NOT, AND THE UNDERWRITERS HAVE NOT, AUTHORIZED ANYONE TO PROVIDE YOU WITH DIFFERENT INFORMATION. IF ANYONE PROVIDES YOU WITH DIFFERENT OR INCONSISTENT INFORMATION, YOU SHOULD NOT RELY UPON IT. THE FUND IS NOT, AND THE UNDERWRITERS ARE NOT, MAKING AN OFFER OF THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER IS NOT PERMITTED. YOU SHOULD NOT ASSUME THAT THE INFORMATION CONTAINED IN THIS PROSPECTUS IS ACCURATE AS OF ANY DATE OTHER THAN THE DATE ON THE FRONT OF THIS PROSPECTUS.

YOU SHOULD BE AWARE THAT YOU WILL RECEIVE A SCHEDULE K-1 (NOT A FORM 1099) REPORTING YOUR ALLOCABLE PORTION OF TAX ITEMS OF THE FUND.

THE NUVEEN LONG/SHORT COMMODITY TOTAL RETURN FUND IS NOT SPONSORED, ENDORSED, SOLD OR PROMOTED BY MORNINGSTAR, INC. MORNINGSTAR MAKES NO REPRESENTATION OR WARRANTY, EXPRESS OR IMPLIED, TO THE OWNERS OF THE NUVEEN LONG/SHORT COMMODITY TOTAL RETURN FUND OR ANY MEMBER OF THE PUBLIC REGARDING THE ADVISABILITY OF INVESTING IN COMMODITY FUTURES OR OPTION CONTRACTS GENERALLY OR IN THE NUVEEN LONG/SHORT COMMODITY TOTAL RETURN FUND IN PARTICULAR OR THE ABILITY OF THE MORNINGSTAR® LONG/SHORT COMMODITYINDEXSM TO TRACK GENERAL COMMODITY MARKET PERFORMANCE.

MORNINGSTAR, INC. DOES NOT GUARANTEE THE ACCURACY AND/OR THE COMPLETENESS OF THE MORNINGSTAR® LONG/SHORT COMMODITY INDEXSM OR ANY DATA INCLUDED THEREIN, AND MORNINGSTAR SHALL HAVE NO LIABILITY FOR ANY ERRORS, OMISSIONS, OR INTERRUPTIONS THEREIN.

TABLE OF CONTENTS

i

ii

This prospectus contains information you should consider when making an investment decision about the shares. You should rely only on the information contained or incorporated by reference in this prospectus. None of the Fund, the manager nor the underwriters have authorized any person to provide you with different information and, if anyone provides you with different or inconsistent information, you should not rely on it. The Fund is not, the manager is not, and the underwriters are not making an offer to sell the shares in any jurisdiction where the offer or sale of the shares is not permitted. You should not assume that the information in this prospectus is current as of any date other than the date on the front page of this prospectus.

The current prospectus for the Fund, which may be updated from time to time pursuant to Securities and Exchange Commission and Commodity Futures Trading Commission requirements, is available at the Fund’s website (www.nuveen.com/ctfipo) as well as at the Securities and Exchange Commission’s website (http://www.sec.gov).

iii

PART ONE: DISCLOSURE DOCUMENT

PROSPECTUS SUMMARY

This is only a summary. You should review the more detailed information contained elsewhere in this prospectus, including the Glossary appearing at the end of “Part Two: Statement of Additional Information,” which contains explanations of capitalized or other frequently used terms, to understand the offering fully.

The Fund | Nuveen Long/Short Commodity Total Return Fund (the “Fund”) is a commodity pool. The Fund was organized as a statutory trust under Delaware law on May 25, 2011. The Fund will be operated pursuant to an Amended and Restated Trust Agreement (“Trust Agreement”), which is described under “Trust Agreement.” The Fund will be managed by Nuveen Commodities Asset Management, LLC (“NCAM” or the “manager”), a limited liability company which is registered as a commodity pool operator (“CPO”) and commodity trading advisor (“CTA”) with the Commodity Futures Trading Commission (the “CFTC”). Gresham Investment Management LLC (“Gresham LLC”), acting through its Near Term Active division (“Gresham NTA”), will be the Fund’s commodity subadvisor and is referred to in this prospectus in that capacity as “Gresham” or the “commodity subadvisor.” Nuveen Asset Management, LLC (“Nuveen Asset Management” or the “collateral subadvisor”) will be the Fund’s collateral subadvisor. The Fund issues shares, which represent units of fractional undivided beneficial interest in, and ownership of, the Fund. After the initial offering, it is anticipated that the shares may be purchased and sold on the NYSE MKT. The principal offices of the Fund and the manager are each located at 333 West Wacker Drive, Suite 3300, Chicago, Illinois 60606. The main telephone number of the Fund and the manager is (312) 917-7700. Information about the Fund also can be obtained by calling (877) 827-5920. |

Listing | It is anticipated that the Fund’s shares will be approved for listing on the NYSE MKT, subject to notice of issuance, under the trading or “ticker” symbol “CTF.” Secondary market purchases and sales of shares will be subject to ordinary brokerage commissions and charges. |

The Offering | The Fund is offering 8,000,000 shares at $25.00 per share through a group of underwriters led by Merrill Lynch, Pierce, Fenner & Smith Incorporated, Citigroup Global Markets Inc., Morgan Stanley & Co. LLC, UBS Securities LLC and Nuveen Securities, LLC (“Nuveen”). Certain underwriters, their affiliates or employees, including Merrill Lynch, Pierce, Fenner & Smith Incorporated, Citigroup Global Markets Inc., Morgan Stanley & Co. LLC and UBS Securities LLC, have, and other underwriters participating in this offering or their affiliates may have, a minority ownership interest in Nuveen Investments, Inc. (“Nuveen Investments”), the parent company of Nuveen, NCAM, Nuveen Asset Management and Gresham LLC. See “Management of the Fund.” Until the completion of this offering, no Fund shares will be outstanding (other than 840 shares owned by the manager). The offering |

1

| | price of $25.00 per share was determined on an arbitrary basis by the manager. You must purchase at least 100 shares ($2,500) in this offering. The Fund has given the underwriters an option to purchase up to additional shares to cover orders in excess of 8,000,000 shares. See “Underwriting.” |

Use of Net Proceeds | The Fund will invest the net proceeds of the offering in accordance with the Fund’s investment objective as stated in this prospectus. Upon receipt, the Fund will use all of the net proceeds to invest in commodity futures contracts and options on commodity futures contracts, and cash equivalents, U.S. government securities and other short-term, high grade debt securities constituting collateral assets. It is presently anticipated that the Fund will be able to invest substantially all of its net proceeds in accordance with its investment objective within approximately 30 business days after the completion of this offering. |

Who May Want to Invest | You should consider your investment goals, time horizons and risk tolerance before investing in the Fund. An investment in the Fund is not appropriate for all investors and is not intended to be a complete investment program. The Fund is designed as a long-term investment and not as a trading vehicle. This is the first actively managed long/short commodity fund to be listed on any of the exchanges owned by NYSE Euronext. |

| | The Fund may be an appropriate investment for you if you are seeking the potential for: |

| | • | | an actively managed long/short commodity futures strategy that seeks to capitalize on opportunities in both up and down commodity markets; |

| | • | | regular monthly distributions; |

| | • | | attractive total returns; |

| | • | | reduced risk relative to equity and commodity market benchmarks; |

| | • | | an investment strategy that seeks to benefit from trading on commodity price momentum; |

| | • | | a fully-collateralized and unleveraged commodity investment strategy; |

| | • | | access to tax-advantaged investments in commodity futures and options on commodity futures which generate gains (losses) that are characterized as 60% long-term capital gains (losses) and 40% short-term capital gains (losses); |

| | • | | diversification from a portfolio with little long-term historical correlation to U.S. equities and U.S. bonds; |

| | • | | access to the commodity investing and trading experience of Gresham; and |

| | • | | daily liquidity afforded by listing on the NYSE MKT. |

2

| | However, keep in mind that you will need to assume the risks associated with an investment in the Fund. See “Risk Factors.” |

Investment Objective | The Fund’s investment objective is to generate attractive total returns. The Fund is actively managed and seeks to outperform its benchmark, the Morningstar® Long/Short Commodity IndexSM (the “Index”). There can be no assurance that the Fund will achieve its investment objective. |

In pursuing its investment objective, the Fund will invest directly in a diverse portfolio of exchange-traded commodity futures contracts that represent the main commodity sectors and are among the most actively traded futures contracts in the global commodity markets. Generally, individual commodity futures positions may be either long or short (or flat in the case of energy futures) depending upon market conditions. The Fund’s options strategy seeks to produce option premiums for the purpose of enhancing the Fund’s risk-adjusted total return over time. Option premiums generated by this strategy may also enable the Fund to more efficiently implement its distribution policy. The Fund’s integrated options strategy relies upon the judgment of the commodity subadvisor in its implementation and may not be successful in achieving the goal of enhancing risk-adjusted returns. The Fund’s total returns over any particular period may be positive or negative. In this prospectus, risk-adjusted total return refers to the total return generated by a portfolio per unit of risk taken, with such risk measured by the volatility of the portfolio’s total returns over a specific period of time. See “Glossary of Defined Terms” for the definition of total return and risk-adjusted total return. See also “The Fund’s Investments” for a discussion of risk-adjusted total return. See also “Risk Factors.”

Investment Strategy | Commodity Investments. The manager has selected Gresham to manage the Fund’s commodity futures investment strategy and options strategy. The Fund’s investment strategy utilizes the commodity subadvisor’s proprietary long/short commodity investment program, which has three principal elements: |

| | • | | an actively managed long/short portfolio of exchange-traded commodity futures contracts; |

| | • | | a portfolio of exchange-traded commodity option contracts; and |

| | • | | a collateral portfolio of cash equivalents, U.S. government securities and other short-term, high grade debt securities. |

| | The Fund’s long/short commodity investment program is an actively managed, fully collateralized, rules-based commodity investment strategy. The Fund will invest in a diverse portfolio of exchange-traded commodity futures contracts with an aggregate notional value substantially equal to the net assets of the Fund. To provide diversification, the Fund will invest initially in approximately 20 commodities, and the program rules limit weights for any individual commodity futures contract. The Fund expects to make investments in the |

3

| | most actively traded commodity futures contracts in the four main commodity sectors in the global commodities markets: |

| | See “The Fund’s Investments—Commodity Investments—Eligible Contracts” for a list of individual commodity futures contracts that the Fund may invest in and the exchanges on which they currently trade. See also “Glossary of Defined Terms” for the definition of notional value. During temporary defensive periods or during adverse market circumstances, the Fund may deviate from its investment objective and policies. |

| | Generally, the program rules are used to determine the specific commodity futures contracts in which the Fund will invest, the relative weighting for each commodity and whether a position is either long or short (or flat in the case of energy futures contracts). |

| | The relative balance of the Fund’s long/short exposure may vary significantly over time, and at certain times, the Fund’s aggregate exposure may be all long, all short and flat or may consist of various combinations (long, short and flat) thereof. Gresham will manage its overall strategy so that the notional amount of the Fund’s combined long, short and flat commodity futures positions will not exceed 100% of the Fund’s net assets. |

| | The Fund will not short energy futures contracts, because the prices of energy futures contracts are generally more sensitive to geopolitical events than to economic factors and, as a result, significant price variations are often driven by factors other than supply-demand imbalances. References to a flat position mean that instead of shorting an energy futures contract when market signals dictate, the Fund will not have a futures contract position for that energy commodity, and will instead move that position to cash. See “The Fund’s Investments—Commodity Investments—Long/Short Commodity Investment Program” for more information concerning the Fund’s energy positions, including flat positions. |

| | The specific commodities, the total number of futures contracts in which the Fund will invest, and the relative weighting of those contracts, will be determined annually by the commodity subadvisor based upon the composition of the Index at that time. The selected commodity futures contracts are expected to remain unchanged until the next annual reconstitution each December. Upon annual reconstitution, the target weight of any individual commodity futures contract will be set and will be limited to 10% of the Fund’s net assets to provide for diversification. The commodity subadvisor expects the actual portfolio weights to vary during the year due to market movements. If price movements cause an individual commodity contract to represent more |

4

| | than 10% of the Index at any time between monthly rebalancing, the Fund would seek to match the target weighting at the time of the monthly rebalancing. Generally, the Fund expects to invest in short-term commodity futures contracts with terms of one to three months but may invest in commodity futures contracts with terms of up to six months. The commodity markets are dynamic and as such the long/short commodity investment program may require frequent adjustments in the Fund’s commodity positions. The commodity subadvisor expects to trade each position no less frequently than once per month. See “The Fund’s Investments—Long/Short Portfolio of Commodity Futures.” |

| | The Fund’s commodity investments will, at all times, be fully collateralized and will be unleveraged. Approximately 15% to 25% of the Fund’s net assets will be placed in one or more accounts at Barclays Capital Inc. (“BCI”), the Fund’s clearing broker, and will be held in high quality instruments permitted under CFTC regulations. The remaining collateral (approximately 75% to 85% of the Fund’s net assets) will be managed by Nuveen Asset Management, the Fund’s collateral subadvisor. See “The Fund’s Investments—Collateral Portfolio.” |

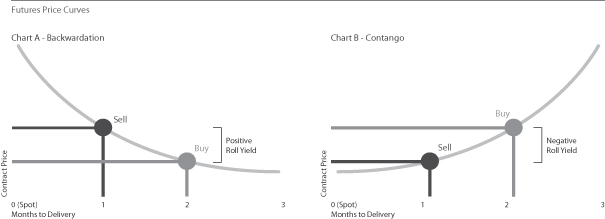

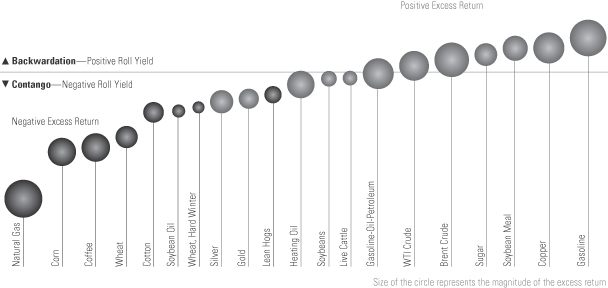

| | Long/Short Portfolio of Commodity Futures. The Fund will invest directly in a diverse portfolio of exchange-traded commodity futures contracts that provide long/short exposure to the global commodity markets. By investing long/short, the Fund seeks to generate attractive total returns from positive or negative commodity price changes and positive or negative roll yield (as described below). Like most commodity futures investors, the Fund will replace expiring futures contracts with more distant contracts to avoid taking physical delivery of a commodity. This replacement of expiring contracts with more distant contracts is referred to as “roll.” To maintain exposure to commodity futures over an extended period, before contracts expire, the commodity subadvisor will roll the futures contracts throughout the year into new contracts so as to maintain a fully invested position. “Roll yield” refers to the return generated from the difference in price between an expiring futures contract and the more distant futures contract that replaces it. See also “Glossary of Defined Terms” for definitions of roll and roll yield. |

| | Gresham employs a proprietary methodology in assessing commodity market movements and in determining the Fund’s long/short commodity futures positions. Generally, the commodity subadvisor employs momentum-based modeling (quantitative formulas that evaluate trend relationships between the changes in prices of futures contracts and trading volumes for a specific commodity) to estimate forward-looking prices and to evaluate the return impact of futures contract rolls. To determine the direction of the commodity futures position, either long or short (or flat in the case of energy futures contracts), the commodity subadvisor calculates a roll-adjusted price that accounts for the current spot price and the impact of roll yield. The futures price for a commodity that has positive roll yield (described as “backwardation”) is adjusted up and the price for a commodity that has negative roll yield (described as “contango”) is adjusted down. |

5

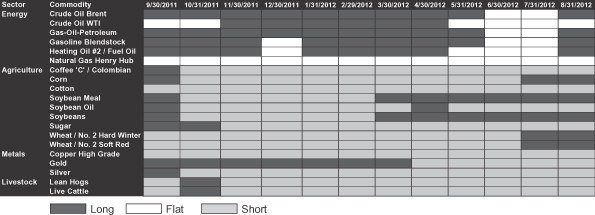

| | Gresham’s long/short commodity investment program rules are proprietary, were developed by its senior management team, and expand upon the rules governing the Index. Upon completing the initial investment of the net proceeds of the offering, the Fund expects that the commodity futures contracts, their relative weights and long/short direction will substantially replicate the constituent holdings and weights of the Index. Although Gresham may exercise discretion in deciding which commodities to invest in, typically the Fund expects to follow certain rules pertaining to eligible commodity futures contracts, weights, diversification, rebalancing, and annual reconstitution that are the same as those for the Index in order to minimize the divergence between the price behavior of the Fund’s commodity futures portfolio and the price behavior of the Index (such divergence is referred to as “tracking error”). See page 8 for a description of the Index and also page 39 for actual weightings of the Index as of August 31, 2012. Over time, the Fund’s commodity investments managed pursuant to Gresham’s long/short commodity investment program may differ from those of the Index. The manager has entered into a license agreement with Morningstar, Inc. relating to the Index, which is described under “The Funds Investments—Commodity Investments.” |

In actively managing the Fund’s long/short portfolio of commodity futures contracts, Gresham seeks to add value compared with the Index by implementing the following proprietary investment methods: (i) trading contracts in advance of monthly index rolls; (ii) individual commodity futures contract selection; and (iii) active implementation. As a result, the roll dates, terms, underlying contracts and contract prices selected by Gresham may vary significantly from the Index based upon Gresham’s implementation of the long/short commodity investment program in light of the relative value of different contract terms. Gresham’s active management approach is market-driven and opportunistic and is intended to minimize market impact and avoid market congestion during certain days of the trading month.

| | Integrated Options Strategy. The Fund will employ a commodity option writing strategy that seeks to produce option premiums for the purpose of enhancing the Fund’s risk-adjusted total return over time. Option premiums generated by this strategy may also enable the Fund to more efficiently implement its distribution policy. There can be no assurance that the Fund’s options strategy will be successful. |

| | Pursuant to the options strategy, the Fund may sell exchange-traded commodity call or put options on a continual basis on up to approximately 25% of the notional value of each of its commodity futures contracts that, in Gresham’s determination, have sufficient option trading volume and liquidity. Initially, the Fund expects to sell commodity options on approximately 15% of the notional value of each of its commodity futures contracts. If Gresham buys the commodity futures contract, they will sell a call option on the same underlying commodity futures contract. If Gresham shorts the commodity futures |

6

| | contract, they will sell a put option on the same underlying commodity futures contract (except in the case of energy futures contracts). Gresham may exercise discretion with respect to commodity futures contract selection. Due to trading and liquidity considerations, Gresham may determine that it is in the best interest of Fund shareholders to sell options on like commodities (for example, gas oil and heating oil are like commodities) and not matched commodity futures contracts. |

| | Because the Fund’s option overwrite is initially expected to represent 15% of the notional value of each of its commodity futures contract positions, the Fund retains the ability to benefit from the full capital appreciation potential beyond the strike price on the majority (85% or more) of its long and/or short commodity futures contracts. An important objective of the Fund’s long/short commodity investment strategy is to retain capital appreciation potential with respect to the major portion of the Fund’s portfolio. |

| | When initiating new trades, the Fund expects to sell covered in-the-money options and will not sell uncovered options. Because the Fund will hold options until expiration, the Fund may have uncovered out-of-the-money options in its portfolio depending on price movements of the underlying futures contracts. This element of the Fund’s options strategy increases the Fund’s gap risk, which is the risk that a commodity price will change from one level to another with no trading in between. In the event of an extreme market change or gap move in the price of a single commodity, the Fund’s options strategy may result in increased exposure to that commodity from any uncovered options. See “ Risk Factors—Options Strategy Risks.” |

| | Generally, the Fund expects to sell short-term commodity options with terms of one to three months. Subject to the foregoing limitations, the implementation of the options strategy will be within Gresham’s discretion. Over extended periods of time, the “moneyness” of the commodity options may vary significantly. Upon sale, the commodity options may be “in-the-money,” “at-the-money” or “out-of-the-money.” A call option is said to be “in-the-money” if the exercise price is below current market levels, “out-of-the-money” if the exercise price is above current market levels, and “at-the-money” if the exercise price is at current market levels. Conversely, a put option is said to be “in-the-money” if the exercise price is above the current market levels and “out-of-the-money” if the exercise price is below current market levels. See also “Glossary of Defined Terms” for definitions. |

| | Collateral Portfolio. The Fund’s commodity investments will, at all times, be fully collateralized. The notional value of the Fund’s commodity exposure is expected to be approximately equal to the market value of the collateral. The Fund’s commodity investments generally will not require significant outlays of principal. Approximately 15% to 25% of the Fund’s net assets will be initially committed as “initial” and “variation” margin to secure the futures contracts and |

7

| | additional assets may be committed as margin upon call by BCI. These assets will be placed in one or more commodity futures accounts maintained by the Fund at BCI and will be invested by BCI in high-quality instruments permitted under CFTC regulations. |

| | The remaining collateral (approximately 75% to 85% of the Fund’s net assets) will be held in a separate collateral investment account managed by Nuveen Asset Management. The Fund’s assets held in this separate collateral account will be invested in cash equivalents, U.S. government securities and other short-term, high grade debt securities with final terms not exceeding one year at the time of investment. These collateral investments will consist primarily of direct and guaranteed obligations of the U.S. government and senior obligations of U.S. government agencies (referred to herein as “U.S. government securities”) and may also include, among others, money market funds and bank money market accounts invested in U.S. government securities, as well as repurchase agreements collateralized with U.S. government securities. The Fund’s investments in cash equivalents and other short-term debt securities (other than U.S. government securities) shall be rated at all times at the applicable highest short-term or long-term debt or deposit rating or money market fund rating as determined by at least one nationally recognized statistical rating organization (“NRSRO”). |

| | Leverage. The Fund has no current intention to utilize leverage (except for borrowings for temporary or emergency purposes, as explained in more detail under “The Funds Investments” and “Investment Policies of the Fund—Borrowings”). The Fund may not borrow in excess of 5% of its net assets. Borrowings by the Fund could cause tax-exempt investors to recognize unrelated business taxable income with respect to a portion of their income from the Fund. See “Federal Income Tax Considerations—Tax-Exempt Organizations.” |

Fund Benchmark | For comparative purposes, the Fund uses the Morningstar® Long/Short Commodity IndexSM as its primary benchmark. The Index tracks the historical total return performance of a diverse portfolio of commodity futures, which may be invested long, short or flat, and is currently comprised of 20 different commodities as of August 31, 2012 (listed on page 39). The Index uses a momentum rule to determine if each commodity futures position is long, short or flat. The Index is fully collateralized with short-term U.S. Treasury bills. To qualify for inclusion in the Index, a commodity must have futures contracts traded on one of the U.S. exchanges and rank in the top 95% of total dollar value of open interest (measured by the 12-month average). The Index was launched August 1, 2007. Return data is available from December 21, 1979 to the present and is constructed using the same futures price data and index rules that the Index has employed since its launch. The Index is reconstituted and rebalanced once annually, on the third Friday of December after the day’s closing Index values have been determined. The Index commodity membership and constituent commodity weights are reset at that time. The direction of the long or short positions are adjusted monthly on the |

8

| | third Friday of every month and are effective on the first trading day after the third Friday. The Index construction rules and other information about the Index can be found on Morningstar’s website at http://indexes.morningstar.com, which is publicly available at no charge. |

Special Risk Considerations | An investment in the Fund involves special risk considerations, which are summarized below. The Fund may not be able to achieve its investment objective. A more extensive discussion of these risks appears beginning on page 22. |

| | • | | THIS POOL HAS NOT COMMENCED TRADING AND DOES NOT HAVE ANY PERFORMANCE HISTORY. The Fund has no history of operations. Therefore, there is no performance history for the Fund to serve as a basis for you to evaluate an investment in the Fund. The commodity subadvisor has not previously managed client accounts utilizing the long/short commodity investment program. |

| | • | | An investment in the Fund’s shares is subject to investment risk, including the possible loss of the entire amount that you invest. |

| | • | | Investments in commodity futures contracts and options on commodity futures contracts have a high degree of price variability and are subject to rapid and substantial price changes.These price changes may be magnified by computer-driven algorithmic trading, which is becoming more prevalent in the commodities markets. |

| | • | | The net asset value of each share will change as fluctuations occur in the market value of the Fund’s portfolio. Investors should be aware that the public trading price of a share may be different from the net asset value of a share and that shares may trade at a discount from their net asset value (which could be significant). This price difference may be due to the fact that supply and demand forces at work in the secondary trading market for shares are not necessarily the same as the forces influencing the prices of the Fund’s investments at any point in time. |

| | • | | If the Fund experiences greater losses than gains during the period you hold shares, you will experience a loss for the period even if the Fund’s historical performance is positive. The Fund’s risk-adjusted returns over any particular period may be positive or negative. |

| | • | | In managing and directing the Fund’s activities and affairs, the manager will rely heavily on Gresham, which has a relatively small number of personnel. If any of Jonathan S. Spencer or Douglas J. Hepworth, President and Chief Investment Officer, and Director of Research, respectively, of Gresham LLC, or Susan Wager and Randy Migdal, the Fund’s portfolio managers, were to leave Gresham LLC or be unable to carry out their present responsibilities, it may have an adverse effect on the Fund’s management. In addition, should market conditions deteriorate or |

9

| | for other reasons, Nuveen Investments, NCAM, Nuveen Asset Management and Gresham may need to implement cost reductions in the future which could make the retention of qualified and experienced personnel more difficult and could lead to personnel turnover. |

| | • | | The Fund’slong/short commodity investment program is not designed to provide the return of any single commodity or to replicate the performance of long-only commodity market benchmarks. In any given period, the net asset value returns of the Fund may differ substantially from any single commodity or long-only commodity market benchmarks. The relative balance of the Fund’s long/short exposure may vary significantly over time and at certain times the Fund’s aggregate exposure may be all long, all short and flat, or may consist of various combinations (long, short and flat) thereof. The Fund is not expected to provide a hedge against inflation in market environments when the Fund’s aggregate exposure is predominantly short and flat. |

| | • | | Because the Fund expects to invest in short commodity futures positions, it will face the risk of an unlimited loss on a short position, as the price at which the Fund would need to cover a short position could theoretically increase without limit. |

| | • | | There can be no assurance that the Fund’s options strategy will be successful. Because of the volatile nature of the commodities markets, the writing (selling) of commodity options involves a high degree of risk. |

| | • | | As the writer of options for which a premium is received, the Fund will forego the right to up to 25% of any capital appreciation in the value of each commodity futures contract in its portfolio that effectively underlies an option. The extent of foregone capital appreciation depends on the value of the commodity futures contract relative to the exercise price of such option and option premium realized. |

| | • | | The Fund is subject to gap risk, which is the risk that a commodity price will change from one level to another with no trading in between. The Fund’s options strategy increases the Fund’s gap risk. Gap risk could adversely affect the Fund’s performance in the event that the price of an individual commodity futures contract drops or increases substantially, and may negatively impact the trading price of the Fund’s shares. |

| | • | | The Fund may invest a substantial portion of its net assets in long positions in the energy sector. A downturn in the energy sector could have a larger impact on the Fund than on a fund that does not concentrate in the sector. |

| | • | | Shares may be adversely affected if Gresham makes changes to the Fund in response to changes in the composition and/or valuation of the Index. The composition of the Index may change over time as commodity futures contracts in the Index are added or replaced. In |

10

| | addition, Index positions, and, therefore, positions taken by the Fund, may change quickly and frequently in response to changes in the commodities markets, which would result in greater trading expenses being incurred by the Fund. Furthermore, the Index sponsor may modify the method for determining the composition and weightings of the Index and for calculating its value in order to ensure that the Index represents a measure of the performance over time of the markets for the underlying commodities. Because the Index is serving as a benchmark measure for the Fund, the composition and weighting of their respective portfolios, while not identical, are likely to largely resemble each other. If the method for determining the Index composition and/or weighting were to change over time, any such changes could adversely impact the ability of the Fund to continue to track the Index. |

| | • | | The investment decisions of the commodity subadvisor may be modified, and commodity futures contracts held by the Fund may have to be liquidated at disadvantageous times or prices, to avoid exceeding regulatory “position limits,” potentially subjecting the Fund to substantial losses. The CFTC has recently adopted final regulations that would replace existing position limit rules and impose position limits and limit formulas on 28 physical commodity futures and options contracts, including energy and metals contracts, and on swaps that are economically equivalent to such contracts. Given their application to unleveraged, exchange-traded commodity funds, such position limits could detract from the Fund’s ability to implement its investment strategy. The U.S. District Court for the District of Columbia recently vacated the CFTC’s new position limit regulations and remanded the matter to the CFTC for further consideration consistent with the court’s opinion. See “Risk Factors—Commodity Investment Strategy Risks—Regulatory and exchange position limits may adversely affect the Fund.” |

| | • | | Gresham NTA makes all trading decisions independently from Gresham LLC’s other division. If the CFTC’s new position limit regulations or any reproposed or other similar position limit regulations become effective, or if Gresham LLC’s positions were to exceed currently applicable position limits, then Gresham NTA would operate under the CFTC’s independent account controller exemption such that Gresham NTA would not be required to aggregate its positions with Gresham LLC’s other division. If the CFTC were to terminate, suspend or revoke or not renew the independent account controller exemption, or that exemption were otherwise unavailable, Gresham NTA would be required to aggregate its positions with Gresham LLC’s other division for purposes of the CFTC’s position limits. In that case, it is possible that investment decisions of the commodity subadvisor would be modified and that positions held by the Fund would have to be liquidated to avoid exceeding such position limits, potentially resulting in substantial losses to the Fund and the value of your investment. |

11

| | • | | The Fund is a new investment product and the value of the Fund’s shares could decrease if unanticipated operational or trading problems occur. Certain new mechanisms and operational procedures involving the trading and composition of the Fund’s portfolio have been developed specifically for this Fund. Accordingly, there may be unanticipated problems or issues with respect to the trading and operational procedures of the Fund that could have a material adverse effect on an investment in the shares. |

| | • | | The Fund is subject to numerous conflicts of interest, including those that arise because: |

| | — | the Fund’s commodity subadvisor, commodity brokers and their principals and affiliates may execute trades in commodity futures contracts and options on commodity futures contracts for their own account and accounts of other customers that may compete with orders placed for the Fund; |

| | — | commodity futures contracts established for the benefit of the Fund may be aggregated with the positions held by the commodity subadvisor, its principals or affiliates for their own account and the accounts of other customers for the purposes of determining “position limits,” and there can be no assurance that the commodity subadvisor will choose to liquidate the Fund’s positions in a proportionate manner in the event of mandatory liquidation of positions held by the commodity subadvisor (or its principals or affiliates) to comply with position limits or for other reasons; |

| | — | the manager has less of an incentive to replace either the commodity subadvisor or the collateral subadvisor because each is an affiliate of the manager; and |

| | — | each of the manager and the subadvisors (as defined below) resolve conflicts of interest as they arise based on its judgment and analysis of the particular conflict. While there are no formal procedures to resolve conflicts of interest, the manager and the subadvisors seek to resolve all potential conflicts in a manner that is fair and equitable to the Fund and its shareholders over time. However, there may be instances in which the manager and/or the subadvisors could resolve a potential conflict in a manner that is not in the best interest of the Fund or its shareholders. |

| | • | | Regardless of its investment performance, the Fund will incur fees and expenses, including brokerage commissions and management fees. A management fee will be paid by the Fund even if the Fund experiences a net loss for the full year. To break even from a purchase made in the initial offering, and assuming the Fund’s estimated net proceeds from the offering generate interest income at an annual rate of .074%, the Fund must earn profits other than from interest income at an annual rate of 7.01% during its first year. |

| | • | | The failure of a clearing broker to comply with financial responsibility and customer segregation rules and/or the |

12

| | bankruptcy of a clearing broker could result in a substantial loss of Fund assets. Under current CFTC regulations, a clearing broker maintains customers’ assets in a bulk segregated account. If a clearing broker fails to do so, or is unable to satisfy a substantial deficit in a customer account, its other customers may be subject to risk of loss of their funds in the event of that clearing broker’s bankruptcy. In that event, the clearing broker’s customers, such as the Fund, are entitled to recover, even in respect of property specifically traceable to them, only a pro rata share of all property available for distribution to all of that clearing broker’s customers. |

| | • | | The Fund may need to liquidate some of its investments in order to make distributions, and such liquidation could be at times or on terms different than those the Fund would otherwise select, which could have an adverse effect on the Fund’s results. |

| | • | | Unlike other Nuveen Investments-sponsored funds, the Fund is not a mutual fund, a closed-end fund, or any other type of “investment company” within the meaning of the Investment Company Act of 1940, as amended (the “1940 Act”), and is not subject to regulation thereunder nor afforded the protections of the 1940 Act. As such, the Fund does not have a board with the scope of authority mandated to a board under the 1940 Act. Based on the Fund’s investment strategy, its (i) potential for the realization of the greatest gains and (ii) exposure to the largest risk of loss will always be from its commodity investments and options strategy. |

| | • | | Shareholders will have no rights to participate in the Fund’s management other than the right in certain circumstances to remove or replace the manager. The manager has established a committee (referred to herein as the “independent committee”), comprised entirely of members who are independent of the manager, which will have certain limited powers with respect to the Fund (specifically, to serve the audit and nominating committee functions for the Fund). The Fund will not have a board with the ability to control the management and operation of the Fund that would be typical of the board of directors of a corporation. Therefore, Fund shareholders will have to rely on the judgment of the manager and the subadvisors to manage the Fund. |

| | • | | There have been and likely will continue to be proposals for various amendments to U.S. federal income tax laws that could, if enacted, have adverse effects on the Fund, its investments, or its shareholders. In addition, previously enacted changes to the U.S. federal income tax law that were deferred and are scheduled to take effect in the future could either independently or in conjunction with new tax legislation materially affect the tax treatment of the Fund, its investments, or its shareholders. |

| | • | | The Fund will be considered to have terminated for U.S. federal income tax purposes if there is a sale or exchange of 50% or more of the total Fund shares within a 12-month period. A constructive termination results in the closing of the Fund’s taxable year for the |

13

| | Fund for all holders of shares. Among other things, constructive termination could result in the imposition of substantial penalties on the Fund if the Fund were unable to determine that the termination had occurred. See “Federal Income Tax Considerations—U.S. Shareholders—Constructive Termination.” |

| | • | | The Fund’s shares do not represent a deposit or obligation of, and are not guaranteed or endorsed by, any bank or other insured depository institution, and are not federally insured by the Federal Deposit Insurance Corporation, the Federal Reserve Board or any other governmental agency. |

| | For additional risks, see “Risk Factors.” |

Trustee; Independent Committee Functions | Wilmington Trust Company, a Delaware trust company, is the resident Delaware trustee of the Fund (the “Trustee”), and as such will have very limited duties with respect to the Fund. The independent committee consisting of four individuals, all of whom are unaffiliated with the manager, will fulfill those functions required under the NYSE MKT listing standards and certain other functions as set forth in the Trust Agreement. The Trust Agreement vests in the manager all authority (other than the limited duties of the independent committee) to operate the business of the Fund and to be responsible for the conduct of the Fund’s commodity affairs. |

Manager and Subadvisors | Manager. Nuveen Commodities Asset Management, LLC, a Delaware limited liability company organized on October 31, 2005, is a wholly-owned subsidiary of Nuveen Investments and is the manager and CPO of the Fund and will be responsible for determining the Fund’s overall investment strategy and its implementation, including: |

| | • | | the selection and ongoing monitoring of the subadvisors; |

| | • | | the assessment of performance and potential needs to modify strategy or change subadvisors; |

| | • | | the determination of the Fund’s administrative policies; |

| | • | | the management of the Fund’s business affairs; and |

| | • | | the provision of certain clerical, bookkeeping and other administrative services. |

| | The manager is registered with the CFTC as a CTA and a CPO and is a member of the National Futures Association (“NFA”). The manager, commodity subadvisor, and collateral subadvisor act in similar capacities for the Nuveen Diversified Commodity Fund (“CFD”), which is a Nuveen Investments-sponsored commodity pool traded on the NYSE MKT that completed its initial public offering on September 30, 2010. As required by the CFTC, NCAM’s historical performance record is disclosed under the caption “NCAM Performance Record” and reflects the performance of CFD. Neither the Fund nor the manager has established formal procedures to resolve |

14

| | potential conflicts of interest related to managing the investments and operations of the Fund. Shares of other commodity pools are not offered pursuant to this prospectus. |

| | As permitted under Delaware law, the Trust Agreement provides that the manager does not owe any duties (including fiduciary duties) to the Fund, other than the implied contractual covenant of good faith and fair dealing. In their dealings with the Fund, the commodity subadvisor and collateral subadvisor will be subject to the fiduciary duties imposed on them by the Commodity Exchange Act, as amended (“CEA”), and the Investment Advisers Act of 1940, as amended (the “Investment Advisers Act”), respectively. |

| | The address of NCAM is 333 West Wacker Drive, Suite 3300, Chicago, Illinois 60606. Its telephone number is (312) 917-7700. Information about the Fund also can be obtained by calling (877) 827-5920. |

| | The commodity subadvisor and the collateral subadvisor are sometimes together referred to herein as the “subadvisors.” |

| | Commodity Subadvisor. Gresham, the commodity subadvisor, will manage the Fund’s commodity futures investment strategy and options strategy. Gresham LLC is a Delaware limited liability company, the successor to Gresham Investment Management, Inc., formed in July 1992 by Dr. Henry Jarecki, who serves as the Chairman. Gresham LLC is registered with the CFTC as a CTA and a CPO and is a member of the NFA. Gresham LLC also is registered with the Securities and Exchange Commission (“SEC”) as an investment adviser. As of August 31, 2012, Gresham LLC had approximately $15 billion of client assets under management, including approximately $7.8 billion under management by Gresham NTA and approximately $7.3 billion under management by Gresham LLC’s other division. Gresham LLC’s senior management team has extensive experience in overall supervision of commodities portfolio management and trading operations. |

| | On December 31, 2011, Nuveen Investments completed its acquisition of a 60% stake in Gresham LLC. As part of the acquisition, Gresham LLC’s management and investment teams maintained a significant minority ownership stake in the firm, and will operate independently while leveraging the strengths of certain shared resources of Nuveen Investments. |

| | Beginning in 1987, Dr. Henry Jarecki, the founder of Gresham LLC, and Mr. Jonathan Spencer began managing commodity futures in a proprietary family account. Gresham’s actively managed commodity futures strategies were first offered to outside clients beginning in September 2004. As required by the CFTC, Gresham’s historical performance record is disclosed on page 60 under the caption “Gresham Performance Record” and reflects the performance of Tangible Asset Program® (“TAP®”) and TAP PLUSSM, not the long/short commodity investment program. Gresham has not previously employed the long/short commodity investment program for client accounts. |

15

| | Collateral Subadvisor. Nuveen Asset Management, the collateral subadvisor, an affiliate of the manager and an indirect wholly-owned subsidiary of Nuveen Investments, will manage the Fund’s collateral. The collateral subadvisor is registered with the SEC as an investment adviser. As of June 30, 2012, Nuveen Asset Management had approximately $112 billion of assets under management. Founded in 1898, Nuveen Investments and its affiliates had approximately $212 billion of assets under management as of June 30, 2012. |

| | Fees. The Fund has agreed to pay the manager an annual fee, payable monthly, in a maximum amount equal to 1.25% of the Fund’s average daily net assets, with lower fee levels for assets that exceed $500 million. The manager has agreed to pay, out of the fee it receives from the Fund, a fee to each of the commodity subadvisor and the collateral subadvisor for subadvisory services. For more information on fees and expenses, see “Management of the Fund—Management Fees.” |

Distributions | Commencing with the Fund’s first distribution, the Fund intends to make regular monthly distributions to its shareholders (stated in terms of a fixed cents per share distribution rate) based on the past and projected performance of the Fund. Among other factors, the Fund will seek to establish a distribution rate that roughly corresponds to NCAM’s projections of the total return that could reasonably be expected to be generated by the Fund over an extended period of time. Each monthly distribution will not be solely dependent on the amount of income earned or capital gains realized by the Fund, and such distributions may from time to time represent a return of capital and may require that the Fund liquidate investments. As market conditions and portfolio performance may change, the rate of distributions on the shares and the Fund’s distribution policy could change. The Fund reserves the right to change its distribution policy and the basis for establishing the rate of its monthly distributions, or may temporarily suspend or reduce distributions without a change in policy, at any time and may do so without prior notice to shareholders. Any suspension or reduction of distributions will increase the Fund’s assets under management upon which NCAM earns management fees. |

| | Because the Fund expects to be classified as a partnership for U.S. federal income tax purposes, shareholders will be allocated their pro-rata share of the Fund’s income, gains, losses, deductions and credits for purposes of computing their U.S. federal income tax liability. Depending on market conditions, the Fund anticipates it will make regular monthly distributions intended in part to provide shareholders with cash with which to fund potential U.S. federal income tax liabilities on their proportionate share of income and gains earned by the Fund, although there can be no assurance that distributions for any period will correspond to such potential U.S. federal income tax liabilities or share of income and gains for such period. |

16

| | The Fund expects to receive substantially all of its current income and gains from the following sources: |

| | • | | realized and unrealized net capital gains (both short-term and long-term) from commodity futures contracts; |

| | • | | realized and unrealized net capital gains (both short-term and long-term) from the options strategy; and |

| | • | | interest income and/or capital gains received on collateral invested in cash equivalents, U.S. government securities and other short-term, high grade debt securities. |

| | The Fund expects to declare its initial distribution within 45 days, and to pay that distribution approximately 60 days, after the completion of this offering, depending on market conditions. For more information, see “Distributions.” |

Transfer Agent, Registrar and Custodian | State Street Bank and Trust Company (“State Street”) will serve as transfer agent and registrar for the Fund’s shares and custodian for the assets of the Fund. BCI, the Fund’s clearing broker, also may serve as custodian for all or a portion of the Fund’s assets. |

Break-Even Threshold | Assuming the Fund’s estimated gross offering size is $200,000,000, and assuming the Fund’s estimated net proceeds ($190,600,000) generate interest income at an annual rate of .074%, an investment of $2,500 must earn profits other than from interest income of $175.22 or at an annual rate of 7.01% in order to “break-even” during the first year of the Fund’s operations. See “Break-Even Analysis.” |

U.S. Federal Income Tax Aspects | Subject to the discussion below in “Federal Income Tax Considerations,” the Fund expects to be classified as a partnership for U.S. federal income tax purposes. Accordingly, the Fund will not incur U.S. federal income tax liability; rather, each owner of the Fund’s shares will be required to take into account his or her allocable share of the Fund’s income, gain, loss, deduction and other items for the Fund’s taxable year ending with or within its taxable year. Fund shareholders will receive an Internal Revenue Service (“IRS”) Form 1065, Schedule K-1 (not a Form 1099), which reports their allocable portion of such tax items. Shareholders who seek advice from tax advisors with respect to the Schedule K-1 may incur additional costs. The Fund anticipates that shareholders will have access to their Schedule K-1 by the end of the first week of March in the following year. Please refer to the “Tax Risk” section on pages 34 to 36 for additional information. |

| | The Fund will invest primarily in exchange-listed futures and options that are tax-advantaged and generally qualify as Section 1256 Contracts which generate gains (losses) that are characterized as 60% long-term capital gains (losses) and 40% short-term capital gains (losses). |

| | Please refer to the “Federal Income Tax Considerations” section below for information on the potential U.S. federal income tax consequences of the purchase, ownership and disposition of shares. |

17

BREAK-EVEN ANALYSIS

The following “break-even” table indicates the approximate dollar amount and percentage the Fund must earn after one year for investors who purchase shares in the initial offering to offset the costs applicable to an investment of $2,500 (the minimum investment for purchases in the initial offering). In the table below, expenses are based on estimated amounts for the Fund’s first year of operations, and assume the Fund’s estimated gross offering size is $200,000,000 (assuming an offering of 8,000,000 shares at a $25.00 offering price) with net proceeds of the offering (after Underwriting Commissions and Offering Expenses borne by the Fund) totaling $190,600,000. Expenses also assume the Fund’s leverage is equal to 0% of net assets. To break even from a purchase made in this offering, and assuming the Fund’s portfolio generates interest income at an annual rate of .074%, the Fund must earn profits other than from interest at an annual rate of 7.01% during the first year of the Fund’s operations.

| | | | | | | | |

| | | Initial Offering Purchases(1)

| |

| | | Dollar

Amount

| | | Percentage

| |

Underwriting Commissions | | | $9,000,000 | | | | 4.50 | % |

Manager’s Management Fee(2) | | | $2,382,500 | | | | 1.19 | % |

Brokerage Commissions and Fees(3) | | | $1,467,620 | | | | .73 | % |

Transaction Fees(4) | | | $57,180 | | | | .03 | % |

Offering Expenses(5) | | | $400,000 | | | | .20 | % |

Operating Expenses(6) | | | $851,206 | | | | .43 | % |

| | |

|

|

| |

|

|

|

Total Fees | | | $14,158,506 | | | | 7.08 | % |

Interest Income(7) | | | ($141,044 | ) | | | (.07 | )% |

| | |

|

|

| |

|

|

|

12-Month Break-Even Value on Estimated Fund Gross Offering Size of $200,000,000 | | | $14,017,462 | | | | 7.01 | % |

| | |

|

|

| |

|

|

|

12-Month Break-Even Value on a $2,500 Investment | | | $175.22 | | | | | |

| | |

|

|

| | | | |

| (1) | The expenses in connection with a minimum purchase of the Fund in the initial offering are calculated based on the estimated net proceeds of the offering ($190,600,000), with the exception of Underwriting Commissions and Offering Expenses, which are calculated based on the estimated gross offering of $200,000,000. The percentages presented are calculated based on the gross offering size. If the estimated gross offering size was $100 million or $500 million, the 12-Month Break-Even Value on a $2,500 purchase made in the initial offering expressed as a percentage of the gross offering size would be, respectively, 7.31% and 6.82%. Thus, the amount of profits the Fund must earn in order for investors to break even in the first year of operations is reduced as the assets of the Fund increase. |

| (2) | The Fund will pay the manager an annual fee, payable monthly, in a maximum amount equal to 1.25% of the Fund’s average daily net assets. The percentage shown in the table above is calculated based on the Fund’s gross offering size, before deduction of underwriting commissions and offering expenses. |

| (3) | Brokerage commissions and transaction fees on the Fund’s commodity investments are estimated at .77% of the net proceeds of the offering based on expected trading activity. Brokerage commissions and transaction fees include rebalancing costs, markups and markdowns on fixed income trades, floor brokerage and NFA, exchange, clearing and give-up fees. The total amount will vary based upon the actual trading activity in the Fund’s commodity portfolio, the specific commodity futures and option contracts purchased (or sold), and the volatility of the commodity futures and options markets. |

| (4) | Transaction fees on the Fund’s collateral investments are estimated at .03% of the net proceeds of the offering but may vary based upon the trading activity in the Fund’s collateral portfolio, the specific investments made, and the volatility of the fixed income markets. |

18

| (5) | Nuveen has agreed to pay Offering Expenses of the Fund (other than Underwriting Commissions) that exceed $.05 per share and to reimburse all organization expenses of the Fund. Based on an estimated gross offering size of $200,000,000 (8,000,000 shares at a $25 share price), the Fund would pay a maximum of $400,000 of offering expenses and Nuveen would pay all offering expenses in excess of $400,000, which are currently estimated to be $1,610,000. |

| (6) | The Fund will pay all of its Operating Expenses, including, but not limited to, index licensing fees, transfer agent fees, custodial fees, fees and expenses of the independent committee and the Trustee, legal and accounting fees and expenses, tax preparation expenses, filing fees and printing, mailing and duplication costs. |

| (7) | Interest income for purposes of the break-even analysis is estimated to be earned at an annual rate of .074% based on the three-month U.S. Treasury bill yield as of August 31, 2012. The interest earned on the Fund’s collateral portfolio may differ from the quoted Treasury bill rate. |

| | For more information, see “Fees and Expenses.” |

19

FEES AND EXPENSES

The Fund will pay fees and expenses that must be offset by investment gains and interest income in order to avoid depletion of the Fund’s net assets. See “Management of the Fund—Management Fees.”

| | |

Type of Fee or Expense

| | Amount

|

Manager’s Management Fees | | The Fund will pay the manager a maximum amount equal to 1.25% of the Fund’s average daily net assets, payable on a monthly basis. The fees paid by the Fund to the manager are subject to various breakpoints, as set forth on page 56. A break point means that if the value of investments held by the Fund achieves a specified level, the Fund will be eligible to pay the manager a reduced fee on the portion of the assets above that level (the “break point”). |

| |

Brokerage Commissions and Transaction Fees | | Brokerage commissions and transaction fees charged in connection with the Fund’s investment activity are estimated at .80% of the net proceeds of the offering based on expected trading activity of the commodity and collateral portfolios. Brokerage commissions and transaction fees include rebalancing costs, markups and markdowns on fixed income trades, floor brokerage and NFA, exchange, clearing and give-up fees. |

| |

Offering Expenses | | The Fund will pay its offering expenses, up to $.05 per share, which include but are not limited to legal and accounting fees and expenses, printing fees, and various exchange and regulatory registration fees and expenses. Nuveen has agreed to pay offering expenses of the Fund (other than underwriting commissions) that exceed $.05 per share and to pay all organizational expenses of the Fund. The manager currently estimates that the amount of such offering expenses to be paid by Nuveen will be approximately $1,610,000. |

| |

Operating Expenses | | The Fund will pay all of its routine operating, administrative and other ordinary expenses, including, but not limited to, index licensing fees, transfer agent fees, custodial fees, fees and expenses of the independent committee and the Trustee, legal and accounting fees and expenses, tax preparation expenses, filing fees and printing, mailing and duplication costs. The manager currently estimates that the Fund’s routine ongoing expenses will be approximately .43% of net assets per year based on the Fund’s estimated gross offering size of $200,000,000. |

20

| | |

Type of Fee or Expense

| | Amount

|

Extraordinary Fees and Expenses | | The Fund will pay all of its extraordinary fees and expenses, if any. Such extraordinary fees and expenses, by their nature, are unpredictable in terms of timing and amount. |

REPORTS TO SHAREHOLDERS

The manager will furnish you with annual reports as required by the rules and regulations of the SEC as well as with those reports required by the CFTC and the NFA, including, but not limited to, annual financial statements audited by an independent registered public accounting firm and any other reports required by any other governmental authority that has jurisdiction over the activities of the Fund. The Fund’s monthly account statement and its portfolio holdings will be disclosed on its website at www.nuveen.com/ctfipo on each business day that the NYSE MKT is open for trading. The Fund’s website is publicly available at no charge. This website disclosure of portfolio holdings and the Fund’s net asset value (as of the previous day’s close) will be made daily and will include, as applicable, the name and total value of each commodity investment and the total value of the collateral held in the Fund’s portfolio. The values of the Fund’s portfolio holdings will, in each case, be determined in accordance with the Fund’s valuation policies. Fund shareholders will be provided with information to permit them to file U.S. federal and state income tax returns with respect to their shares. The Fund will file a partnership return with the IRS and will transmit a Schedule K-1 to each shareholder reporting the shareholder’s allocable portion of relevant tax items of the Fund. The Fund anticipates that shareholders will have access to their Schedule K-1 by the end of the first week of March in the following year. See “Federal Income Tax Considerations—U.S. Shareholders—Tax Reporting by the Fund.”

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus includes forward-looking statements that generally relate to future events or future performance. In some cases, you can identify forward-looking statements by terminology such as “may,” “will,” “should,” “expect,” “plan,” “anticipate,” “believe,” “estimate,” “predict,” “potential” or the negative of these terms or other comparable terminology. These forward-looking statements are based on information currently available to the manager and subadvisors and are subject to a number of risks, uncertainties and other factors, both known, such as those described in “Risk Factors” and elsewhere in this prospectus, and unknown, that could cause the actual results, performance, prospects or opportunities of the Fund to differ materially from those expressed in, or implied by, these forward-looking statements.

You should not place undue reliance on any forward-looking statements. Except as expressly required by the federal securities laws or otherwise, the manager and the subadvisors undertake no obligation to publicly update or revise any forward-looking statements or the risks, uncertainties or other factors described in this prospectus, as a result of new information, future events or changed circumstances or for any other reason after the date of this prospectus.

21

RISK FACTORS

Investing in the Fund’s shares involves a number of significant risks. Before you invest in the Fund’s shares, you should be aware of the various risks, including those described below. You should consider carefully the risks described below before making an investment decision. You should also refer to the other information included in this prospectus, including the Fund’s financial statements and the related notes. Additional risks and uncertainties not presently known by the Fund or not presently deemed material by the Fund may also impair the Fund’s operations and performance. If any of the following events occur, the Fund’s performance could be materially and adversely affected. In such case, the Fund’s net asset value and the trading price of the Fund’s shares may decline and you may lose all or part of your investment.

An investment in the Fund involves a high degree of risk. You should not invest in shares unless you can afford to lose all of your investment.

Commodity Investment Strategy Risks