Table of Contents

As filed pursuant to Rule 424(b)(3)

File No. 333-176592

PRETIUM PACKAGING, L.L.C.

PRETIUM FINANCE, INC.

$150,000,000

OFFER TO EXCHANGE

$150,000,000 in Aggregate Principal Amount of 11.50% Senior Secured Notes due 2016, Series B and related guarantees for all outstanding

$150,000,000 in Aggregate Principal Amount of 11.50% Senior Secured Notes due 2016, Series A and related guarantees

The exchange offer will expire at 5:00 p.m., New York City time,

on December 12, 2011, which is 21 business days after the commencement of the exchange offer, unless extended.

The Offering:

Offered Securities: The securities offered by this prospectus are 11.50% Senior Secured Notes due 2016, Series B (the “New Notes”) and related guarantees, which are being issued in exchange for 11.50% Senior Secured Notes due 2016, Series A (the “Original Notes” and, together with the New Notes, the “Notes”) and related guarantees, sold by us in our private placement that we consummated on March 31, 2011. The New Notes and related guarantees are substantially identical to the Original Notes and are governed by the same indenture. There is no public market for the Original Notes and we do not intend to apply for the New Notes to be listed on any national securities exchange.

Expiration of Offering: The exchange offer expires at 5:00 p.m., New York City time, on December 12, 2011, which is 21 business days after the commencement of the exchange offer, unless extended.

We will exchange all Original Notes that are validly tendered and not withdrawn prior to the expiration of the exchange offer.

We will not receive any proceeds from the exchange.

Each broker-dealer that receives New Notes pursuant to the exchange offer must acknowledge that it will deliver a prospectus in connection with any resale of the New Notes. If the broker-dealer acquired the Original Notes as a result of market-making or other trading activities, such broker-dealer must use the prospectus for the exchange offer, as supplemented or amended, in connection with resales of the New Notes. Broker-dealers who acquired the Original Notes directly from us through an exemption from registration must, in the absence of an exemption, comply with the registration and prospectus delivery requirements of the Securities Act of 1933 (the “Securities Act”) in connection with secondary resales and cannot rely on the position of the Securities and Exchange Commission (“SEC”) or SEC staff enunciated in the Exxon Capital Holding Corp. no-action letter (available May 13, 1988).

The New Notes:

Maturity: The New Notes will mature on April 1, 2016.

Interest Payment Dates: Interest payment dates for the New Notes are April 1 and October 1, beginning on April 1, 2012.

See “Risk Factors,” beginning on page 15, for a discussion of some factors that should be considered by holders in connection with a decision to tender Original Notes in the exchange offer.

These securities have not been approved or disapproved by the SEC or any state securities commission nor has the SEC or any state securities commission passed on the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is November 10, 2011.

Table of Contents

| Page | ||||

| 1 | ||||

| 15 | ||||

| 34 | ||||

| 35 | ||||

| 35 | ||||

| 36 | ||||

| 37 | ||||

| 38 | ||||

| 45 | ||||

| 47 | ||||

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 48 | |||

| 65 | ||||

| 74 | ||||

| 85 | ||||

| 89 | ||||

| 96 | ||||

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT | 97 | |||

| 99 | ||||

| 100 | ||||

| 103 | ||||

| 160 | ||||

| 164 | ||||

| 165 | ||||

| 165 | ||||

| 165 | ||||

| F-1 | ||||

i

Table of Contents

INFORMATION ABOUT THE TRANSACTION

THIS PROSPECTUS INCORPORATES IMPORTANT INFORMATION ABOUT US THAT IS NOT INCLUDED IN OR DELIVERED WITH THIS PROSPECTUS. SUCH INFORMATION IS AVAILABLE WITHOUT CHARGE TO THE HOLDERS OF OUR ORIGINAL NOTES BY CONTACTING US AT OUR ADDRESS, WHICH IS 15450 SOUTH OUTER FORTY DRIVE, SUITE 120, CHESTERFIELD, MISSOURI, OR BY CALLING US AT (314) 727-8200. TO OBTAIN TIMELY DELIVERY OF THIS INFORMATION, YOU MUST REQUEST THIS INFORMATION NO LATER THAN FIVE BUSINESS DAYS BEFORE DECEMBER 12, 2011, WHICH IS 21 BUSINESS DAYS AFTER THE COMMENCEMENT OF THE EXCHANGE OFFER, UNLESS EXTENDED. ALSO SEE “AVAILABLE INFORMATION.”

ii

Table of Contents

The following summary contains basic information about us and this exchange offer. It is not complete and likely does not contain all the information that is important to you. The following summary is qualified in its entirety by the more detailed information and financial statements and notes thereto included elsewhere in this prospectus. You should carefully read this entire prospectus and should consider, among other things, the matters set forth in “Risk Factors”. Unless otherwise noted, references to the terms “Pretium”, “we,” “us” and “our” refer to Pretium Packaging, L.L.C. and its consolidated subsidiaries. “Pretium Finance” refers to Pretium Finance, Inc., the co-issuer of the Notes. “Novapak” refers to PVC Container Corporation. “Robb” refers to Robb Container Corporation. “Pretium Holding” and “our parent” refer to Pretium Holding, LLC, an entity controlled by Castle Harlan and its affiliates. “Castle Harlan” refers to Castle Harlan, Inc. “CHPV” refers to Castle Harlan Partners V, L.P. The “Novapak Acquisition” refers to Pretium’s acquisition of Novapak on February 16, 2010. The “Acquisition” refers collectively to Pretium Holding’s acquisition of Pretium, the Novapak Acquisition and the restructuring of Pretium’s equity and debt on February 16, 2010. The “Refinancing” means, collectively, (1) the issuance of the Original Notes and the application of the net proceeds therefrom and (2) the closing of our ABL Facility and the initial borrowings thereunder. Whenever information relating to outstanding indebtedness is presented in this prospectus on an as adjusted basis to give effect to the Refinancing, such information excludes the indebtedness represented by a term loan and revolving credit facilities and our senior subordinated notes existing prior to issuance of the Original Notes, as a portion of the proceeds of the offering of the Original Notes and the initial borrowings under the ABL Facility were applied to repay these obligations. Our financial reporting is based on the twelve months ended on September 30 (i.e. “FY 2010” refers to the fiscal year ended September 30, 2010). As used in this prospectus, the term “ABL Facility” means our new asset backed revolving credit facility, which closed concurrently with the offering of the Original Notes and was amended and restated on April 20, 2011 to increase the borrowing capacity thereunder, among other things.

Our Company

Overview

Founded in 1992 and based in Chesterfield, Missouri, we are one of the nation’s largest manufacturers of customized, high performance rigid plastic bottles and containers primarily made from polyethylene terephthalate (“PET”) and high density polyethylene (“HDPE”) resins. We market our products largely into the food, personal care, household products, healthcare and pharmaceutical end markets. We sell our products to a diversified customer base of over 750 accounts, ranging from Fortune 500 companies to smaller privately-owned businesses with a focus on customers with small-to-medium annual volume requirements. We currently operate 11 manufacturing facilities, nine in the United States and two in Canada, generating approximately 84% of net sales domestically and 16% from Canada in FY 2010. On February 16, 2010, Pretium and Novapak were combined and today operate under the name “Pretium Packaging.” We believe this combination will enable us to take advantage of numerous cost synergies and increased revenue generation opportunities.

Products

We design, manufacture and sell a broad range of customized bottles and containers, representing over 1.2 billion units and utilizing over 110 million pounds of resin across 1,600 different bottle types and over 2,600 stock-keeping units (“SKUs”) in FY 2010. The majority of our products are manufactured for a specific customer on an exclusive basis. Our highly flexible manufacturing capabilities include an extensive library of proprietary custom and stock molds. Our wide breadth of capabilities allows us to target customers with small-to-medium annual volume requirements (between 1 million and 25 million units per year for specific products). Our extensive product offering targets a wide variety of customers and end markets, which results in low customer concentration, with our largest customer representing approximately 5% of net sales and no product or SKU accounting for more than 2% of net sales for FY 2010. We utilize all major blow molding technologies in the

1

Table of Contents

manufacturing of plastic bottles and containers, including one and two-step stretch blow molding (“SBM”), extrusion blow molding (“EBM”) and injection blow molding (“IBM”). In addition, we utilize injection molding (“IM”) to produce preforms, which are utilized primarily for internal manufacturing. Preforms are an injection molded part which appear very similar to a test tube, in various sizes. These preforms are used as the raw material in the second step of the two-step process and are subsequently blown into bottles on other production lines. The principal resins used in our production processes are PET and HDPE, although we use other resins based on customer requirements.

Our Competitive Strengths

We believe we are well-positioned in the plastics packaging market because of the following competitive strengths:

| • | Favorable industry dynamics; |

| • | Recession resistant end markets; |

| • | 100% resin pass through; |

| • | Extensive product offering; |

| • | Stable, long term customer relationships; |

| • | A defensible market position; |

| • | Strong cash flow generation; and |

| • | Experienced management team. |

See “Business—Our Competitive Strengths” for a more detailed discussion of our competitive strengths.

Our Strategy

We intend to enhance our position as a leading manufacturer of customized, high-performance rigid plastic packaging products by leveraging our core manufacturing competencies, expanding our relationships with existing customers, actively targeting new accounts, rationalizing our cost structure, and selectively pursuing highly synergistic acquisition opportunities. The key elements of our strategy include the following factors:

| • | Continue to increase free cash flow generation by leveraging our core manufacturing competencies; |

| • | Capitalize on continued industry conversion to plastic containers; |

| • | Increase sales to our existing customers and pursue new customers; |

| • | Enhance profitability through productivity improvements and cost reductions; and |

| • | Selectively pursue strategic acquisitions. |

See “Business—Our Strategy” for a more detailed discussion of our business strategy.

2

Table of Contents

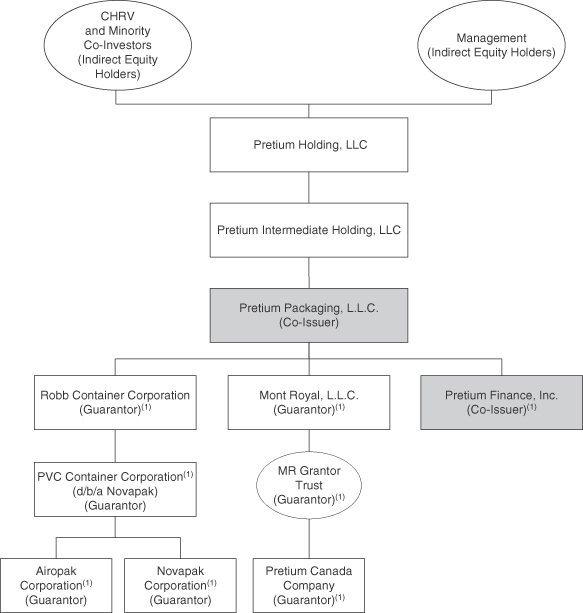

Corporate Structure

| (1) | Obligations in respect of the Notes will be guaranteed on a joint and several basis by each of our current subsidiaries and future domestic subsidiaries other than the Co-issuer. |

Our Sponsor

Castle Harlan is a New York-based private equity investment firm founded in 1987 by John K. Castle, former President and Chief Executive Officer of Donaldson, Lufkin & Jenrette, formerly one of the leading U.S. investment banking firms, and by Leonard M. Harlan, founder and former President of The Harlan Company, a

3

Table of Contents

real estate investment and advisory firm. Castle Harlan invests in controlling interests in the buyout and development of middle-market companies principally in North America and Europe, as well as in Australia and Southeast Asia through Castle Harlan Australian Mezzanine Partners (CHAMP Private Equity). Its team of 18 investment professionals has completed over 50 platform acquisitions since its inception with a total value of over $10 billion. Castle Harlan currently manages investment funds globally with equity commitments of approximately $3.5 billion. Examples of some of the over 50 platform investments completed by Castle Harlan include Securus Technologies, Inc., IDQ Holdings, Inc., United Malt Holdings LP, Americast Technologies, Inc., Bravo Brio Restaurant Group, Inc. and Ames True Temper, Inc.

Additional Information

We are a Delaware limited liability company and our headquarters are located at 15450 South Outer Forty Drive, Suite 120, Chesterfield, Missouri 63017. Our telephone number is (314) 727-8200 and our website is located at http://www.pretiumpkg.com.Our website and the information contained thereon are not part of this prospectus and should not be relied upon by holders of Original Notes in connection with any decision to tender the Original Notes in this exchange offer.

The Exchange Offer

Exchange and Registration Rights | In a registration rights agreement dated March 31, 2011 (the “Registration Rights Agreement”), the holders of our Original Notes were granted exchange and registration rights. This exchange offer is intended to satisfy these rights. You have the right to exchange the Original Notes that you hold for our registered New Notes with substantially identical terms. Once the exchange offer is complete, you will no longer be entitled to any exchange or registration rights with respect to your Original Notes. |

Expiration Date | 5:00 p.m., New York City time, on December 12, 2011, which is 21 business days after the commencement of the exchange offer, unless we extend the exchange offer. |

Interest on the New Notes | The New Notes will bear interest from October 1, 2011. Holders of Original Notes that are accepted for exchange will be deemed to have waived the right to receive any payment in respect of interest on those Original Notes accrued to the date of issuance of the New Notes. |

Conditions to the Exchange Offer | The exchange offer is conditioned upon some customary conditions, which we may waive. All conditions to which the exchange offer is subject must be satisfied or waived on or before the expiration of this offer. |

Procedures for Tendering Original Notes | Each holder of Original Notes wishing to accept the exchange offer must: |

| • | Complete, sign and date the letter of transmittal, or a facsimile of the letter of transmittal; or |

| • | Arrange for the Depository Trust Company (“DTC”) to transmit required information in accordance with DTC’s procedures for transfer to the exchange agent in connection with a book-entry transfer. |

4

Table of Contents

| You must mail or otherwise deliver this documentation together with the Original Notes to the exchange agent. Original Notes tendered in the exchange offer must be in denominations of principal amount of $2,000 and integral multiples of $1,000 in excess of $2,000. |

Special Procedures for Beneficial Holders | If you beneficially own Original Notes registered in the name of a broker, dealer, commercial bank, trust company or other nominee and you wish to tender your Original Notes in the exchange offer, you should contact the registered holder promptly and instruct them to tender on your behalf. If you wish to tender on your own behalf, you must, before completing and executing the letter of transmittal for the exchange offer and delivering your Original Notes, either arrange to have your Original Notes registered in your name or obtain a properly completed bond power from the registered holder. The transfer of registered ownership may take considerable time. |

Guaranteed Delivery Procedures | You must comply with the applicable guaranteed delivery procedures for tendering if you wish to tender your Original Notes and: |

| • | Time will not permit your required documents to reach the exchange agent by the expiration date of the exchange offer; or |

| • | You cannot complete the procedure for book-entry transfer on time; or |

| • | Your Original Notes are not immediately available. |

Withdrawal Rights | You may withdraw your tender of Original Notes at any time on or prior to 5:00 p.m., New York City time, on the expiration date. |

Failure to Exchange will Affect You Adversely | If you are eligible to participate in the exchange offer and you do not tender your Original Notes, you will not have further exchange or registration rights and you will continue to be restricted from transferring your Original Notes. Accordingly, the liquidity of the Original Notes will be adversely affected. |

Federal Tax Considerations | We believe that the exchange of the Original Notes for New Notes pursuant to the exchange offer will not be a taxable event for United States federal income tax purposes. A holder’s holding period for New Notes will include the holding period for Original Notes, and the adjusted tax basis of the New Notes will be the same as the adjusted tax basis of the Original Notes exchanged. See “Material U.S. Federal Income Tax Consequences.” |

Exchange Agent | The Bank of New York Mellon Trust Company, N.A., trustee under the indenture under which the New Notes will be issued, is serving as exchange agent. |

Use of Proceeds | We will not receive any proceeds from the exchange offer. |

5

Table of Contents

Summary Terms of the New Notes

The summary below describes the principal terms of the New Notes. Certain of the terms and conditions described below are subject to important limitations and exceptions. The following is not intended to be complete. You should carefully review the “Description of the New Notes” section of this prospectus, which contains a more detailed description of the terms and conditions of the New Notes. The summary below describes the principal terms of the New Notes. The New Notes will evidence the same debt as the Original Notes. They will be entitled to the benefits of the indenture governing the Original Notes and will be treated under the indenture as a single series with the Original Notes.

Issuers | Pretium Packaging, L.L.C. and Pretium Finance, Inc. |

Notes Offered | The form and terms of the New Notes will be the same as the form and terms of the Original Notes except that: |

| • | the New Notes will bear a different CUSIP number from the Original Notes; |

| • | the New Notes will have been registered under the Securities Act, and, therefore, will not bear legends restricting their transfer; and |

| • | you will not be entitled to any exchange or registration rights with respect to the New Notes. |

Maturity Date | The New Notes will mature on April 1, 2016. |

Interest | The New Notes will bear interest at a rate of 11.50% per annum. |

Interest Payment Dates | April 1 and October 1 of each year, commencing April 1, 2012. |

Guarantees | The Issuers’ obligations under the New Notes will be fully and unconditionally guaranteed by Pretium’s existing subsidiaries and its future domestic subsidiaries (other than Pretium Finance, which is a co-issuer of the New Notes) on a joint and several basis. Each guarantor’s guarantee is a senior secured obligation of that guarantor and ranks pari passu in right of payment with all existing and future senior indebtedness of that guarantor that is not subordinated, including such guarantor’s guarantee of indebtedness under the ABL Facility.If the Issuers cannot make payments on the New Notes when they are due, the guarantors must make the payments instead. |

| As of June 30, 2011: |

| • | the Issuers and guarantors had $150.0 million of senior secured indebtedness outstanding in respect of the Original Notes. |

| • | the Issuers and guarantors had borrowings and related guarantees of approximately $3.0 million under the ABL Facility which would rank equally with the New Notes and the Issuers would have an additional $25.0 million of borrowing capacity under the ABL Facility which would rank equally with the New Notes and related guarantees, or senior to the extent the value of the Collateral securing such obligations is on a first-priority basis. |

| • | the Issuers and the guarantors had approximately $0.4 million of other secured indebtedness. |

Security | The New Notes and the guarantees will be secured, subject to permitted liens and except for certain excluded assets on a second priority basis by substantially all of the Issuers’ and the guarantors’ current and future property and assets, including the capital stock of |

6

Table of Contents

each current subsidiary of Pretium (the “collateral”). The pledge of equity interests may be released in certain instances as described under “Description of the New Notes—Security for the Notes—Limitations on Collateral in the Form of Securities.” |

Intercreditor Agreement | An intercreditor agreement with PNC Bank, National Association, as agent under the ABL Facility, governs the relationship of holders of the New Notes and the lenders under the ABL Facility with respect to the collateral and certain other matters. See “Description of the New Notes—Intercreditor Agreement.” |

Ranking | The New Notes and the guarantees will be the Issuers’ and the guarantors’ senior secured obligations secured to the extent described above. The New Notes and the guarantees will rank: |

| • | pari passu in right of payment with any of the Issuers’ and the guarantors’ senior indebtedness, including indebtedness under the ABL Facility; |

| • | effectively senior to the Issuers’ and guarantors’ unsecured senior indebtedness to the extent of the value of the assets securing the New Notes; |

| • | senior in right of payment to any existing and future indebtedness of the Issuers and the guarantors that is expressly subordinated to the New Notes and the guarantees; |

| • | effectively junior to the Issuers’ and the guarantors’ obligations under the ABL Facility and to any of the Issuers’ and the guarantors’ secured indebtedness which is either secured by assets that are not collateral for the New Notes and the guarantees or secured by a prior lien on the collateral for the New Notes and the guarantees, in each case, to the extent of the value of the assets securing such indebtedness; and |

| • | structurally subordinated to existing and future indebtedness, preferred stock and other liabilities of any of the Issuers’ subsidiaries that are not guarantors of the New Notes. |

| As of June 30, 2011: |

| • | the Issuers and guarantors had $150.0 million of senior secured indebtedness outstanding in respect of the Original Notes. |

| • | the Issuers and guarantors had borrowings and related guarantees of approximately $3.0 million under the ABL Facility which would rank equally with the New Notes and the Issuers would have an additional $25.0 million of borrowing capacity under the ABL Facility which would rank equally with the New Notes and related guarantees, or senior to the extent the value of the Collateral securing such obligations is on a first-priority basis. |

| • | the Issuers and the guarantors had approximately $0.4 million of other secured indebtedness. |

7

Table of Contents

Optional Redemption | On or after April 1, 2014, the Issuers may, on one or more than one occasions, redeem some or all of the New Notes at any time at a redemption price set forth under “Description of the New Notes—Optional Redemption,” plus accrued and unpaid interest and special interest, if any, to the date of redemption. |

| In addition, at any time prior to April 1, 2014, the Issuers may redeem up to 35% of the original aggregate principal amount of the Notes, using the net cash proceeds from certain equity offerings, at a redemption price of 100% of the principal amount thereof plus the coupon, plus accrued and unpaid interest and special interest, if any, to the date of redemption; provided that at least 65% of the aggregate principal amount of the Notes issued under the indenture governing the Notes remains outstanding after such redemption. See “Description of the New Notes—Optional Redemption.” |

Mandatory Redemption | None. |

Change of Control Offer | If certain changes of control occur, the Issuers must give holders of the New Notes an opportunity to sell to the Issuers their New Notes at a purchase price of 101% of the principal amount of such New Notes, plus accrued and unpaid interest, to the applicable repurchase date. The term “Change of Control” is defined under “Description of the New Notes—Repurchase at the Option of Holders—Change of Control.” |

Asset Sale Offer | If the Issuers or Pretium’s restricted subsidiaries sell assets under certain circumstances and do not apply the proceeds as provided in “Description of the New Notes,” the Issuers must offer to repurchase the New Notes at a repurchase price equal to 100% of the principal amount of the New Notes repurchased, plus accrued and unpaid interest, to the applicable repurchase date. See “Description of the New Notes—Repurchase at the Option of Holders—Asset Sales.” |

Certain Covenants | The indenture governing the New Notes contains covenants that, among other things, limit the Issuers’ ability and the ability of Pretium’s restricted subsidiaries to: |

| • | incur additional indebtedness; |

| • | pay dividends on, repurchase or make distributions in respect of our capital stock or make other restricted payments; |

| • | make certain investments; |

| • | sell, transfer or otherwise convey certain assets; |

| • | create liens; |

| • | designate our future subsidiaries as unrestricted subsidiaries; |

| • | consolidate, merge, sell or otherwise dispose of all or substantially all of our assets; and |

| • | enter into certain transactions with our affiliates. |

8

Table of Contents

| These covenants are subject to a number of important limitations and exceptions as described under “Description of the New Notes—Certain Covenants.” |

Exchange Offer; Registration Rights | You have the right to exchange the Original Notes for New Notes with substantially identical terms. This exchange offer is intended to satisfy that right. The New Notes will not provide you with any further exchange or registration rights. |

Resale Without Further Registration | We believe that the New Notes issued in the exchange offer in exchange for Original Notes may be offered for resale, resold and otherwise transferred by you without compliance with the registration and prospectus delivery provisions of the Securities Act, if: |

| • | you are acquiring the New Notes issued in the exchange offer in the ordinary course of business; |

| • | you have not engaged in, do not intend to engage in and have no arrangement or understanding with any person to participate in the distribution of the New Notes issued to you in the exchange offer; and |

| • | you are not our “affiliate,” as defined under Rule 405 of the Securities Act. |

| Each of the participating broker-dealers that receives the New Notes for its own account in exchange for Original Notes that were acquired by it as a result of market-making or other activities must acknowledge that it will deliver a prospectus in connection with the resale of the New Notes. We do not intend to list the New Notes on any securities exchange. |

9

Table of Contents

Summary Consolidated Historical and Pro Forma Financial Information

The following tables set forth our summary consolidated historical and pro forma financial information for the periods ended and at the dates indicated below. The summary consolidated historical financial information for the fiscal years ended September 30, 2008 and 2009 has been derived from the audited consolidated financial statement of our predecessor included elsewhere in this prospectus. The summary consolidated financial information for the period from October 1, 2009 to February 16, 2010 (the date of the Acquisition and the Predecessor period) and the period from February 17, 2010 to September 30, 2010 (the Successor period) have been derived from our audited consolidated financial statements for each of those respective periods included elsewhere in this prospectus. The summary consolidated financial information for the nine months ended June 30, 2011 have been derived from our unaudited financial statements included elsewhere in this prospectus which, in the opinion of management, include all adjustments, including usual recurring adjustments, necessary for the fair presentation of that information for such periods. The financial information presented for the interim periods is not necessarily indicative of the results for the full year.

As part of the Acquisition, all of our operations were acquired by Pretium Holding. This transaction was accounted for as a business combination. As a result of this transaction, the consolidated financial statements for the period subsequent to the Acquisition are referred to as “Successor” and the consolidated financial statements for the period prior to the Acquisition are referred to as “Predecessor”. Accordingly, our consolidated financial statements presented for periods prior to February 17, 2010 are not comparable to our consolidated financial statements presented on or after February 17, 2010.

The pro forma consolidated financial information set forth in the table below is derived from our audited and unaudited consolidated financial information included elsewhere in this prospectus, adjusted to illustrate the pro forma effect of the Acquisition. The unaudited pro forma statement of operations for FY 2010 gives pro forma effect to the Acquisition as if it had occurred on October 1, 2009.

Such pro forma information does not purport to represent what our actual financial position or results of operations would have been had the Acquisition actually been completed on the date or for the periods indicated and is not necessarily indicative of our financial position or results of operations as of the specified date or in the future.

The summary historical and pro forma financial information should be read in conjunction with the sections entitled “Capitalization,” “Selected Consolidated Historical Financial Information,” “Unaudited Pro Forma Combined Financial Information,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and the notes thereto included elsewhere in this prospectus.

10

Table of Contents

| Predecessor | Successor | Pro Forma (1) | Successor | |||||||||||||||||||||||

Fiscal Year Ended September 30, | Period from October 1, 2009 through February 16, 2010 | Period from February 17, 2010 through September 30, 2010 | Fiscal Year Ended September 30, 2010 | Nine Months Ended June 30, 2011 | ||||||||||||||||||||||

| 2008 | 2009 | |||||||||||||||||||||||||

Statement of Operations (in thousands): | ||||||||||||||||||||||||||

Net sales | $ | 186,126 | $ | 164,674 | $ | 58,621 | $ | 148,991 | $ | 234,118 | $ | 178,432 | ||||||||||||||

Cost of sales | 162,174 | 137,317 | 49,125 | 129,149 | 200,243 | 153,150 | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Gross profit | 23,952 | 27,357 | 9,496 | 19,842 | 33,875 | 25,282 | ||||||||||||||||||||

Selling, general and administrative expenses | 13,537 | 14,060 | 5,439 | 12,726 | 22,778 | 13,685 | ||||||||||||||||||||

Restructuring expenses | — | 790 | — | 6,684 | 6,684 | 2,328 | ||||||||||||||||||||

Transaction-related fees and expenses | — | — | — | — | — | 1,237 | ||||||||||||||||||||

(Gain) loss of foreign currency exchange | 948 | 342 | (576 | ) | (197 | ) | (773 | ) | (341 | ) | ||||||||||||||||

Depreciation and amortization expense | 108 | 116 | 52 | 241 | 386 | 278 | ||||||||||||||||||||

Amortization of intangibles | — | — | — | 887 | 1,371 | 978 | ||||||||||||||||||||

Bank related fees | 440 | 2,159 | 917 | — | 917 | — | ||||||||||||||||||||

Acquisition fees and expense | — | — | 1,184 | 10,770 | 847 | — | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Income (loss) from operations | 8,919 | 9,890 | 2,480 | (11,269 | ) | 1,665 | 7,117 | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Interest expense | (15,006 | ) | (15,990 | ) | (7,007 | ) | (8,200 | ) | (15,609 | ) | (11,455 | ) | ||||||||||||||

Loss on extinguishment of debt | — | — | — | — | — | (5,470 | ) | |||||||||||||||||||

Other | — | — | — | — | (135 | ) | — | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Loss before income tax (benefit) provision | (6,087 | ) | (6,100 | ) | (4,527 | ) | (19,469 | ) | (14,079 | ) | (9,808 | ) | ||||||||||||||

Income tax (benefit) provision | (339 | ) | (948 | ) | (365 | ) | 164 | 229 | 1,892 | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Net loss | $ | (5,748 | ) | $ | (5,152 | ) | $ | (4,162 | ) | $ | (19,633 | ) | $ | (14,308 | ) | $ | (11,700 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

| Predecessor | Successor | |||||||||||||||||||||

Fiscal Year Ended September 30, | Period from February 17, 2010 through September 30, 2010 | Nine Months Ended June 30, 2011 | ||||||||||||||||||||

| 2008 | 2009 | Period from October 1, 2009 through February 16, 2010 | ||||||||||||||||||||

Other Financial Data (in thousands): | ||||||||||||||||||||||

EBITDA | $ | 17,960 | $ | 18,541 | $ | 5,595 | $ | (2,923 | ) | $ | 12,212 | |||||||||||

Adjusted EBITDA(2)(3) | 19,348 | 21,832 | 7,250 | 21,726 | 26,088 | |||||||||||||||||

Depreciation | 9,041 | 8,651 | 3,115 | 7,459 | 9,587 | |||||||||||||||||

Amortization of intangibles | — | — | — | 887 | 978 | |||||||||||||||||

Capital expenditures | 8,833 | 5,235 | 2,379 | 6,028 | 6,930 | |||||||||||||||||

11

Table of Contents

| Predecessor | Successor | |||||||||||||||||

| As of September 30, 2008 | As of September 30, 2009 | As of September 30, 2010 | As of June 30, 2011 | |||||||||||||||

Balance Sheet Data (in thousands): | ||||||||||||||||||

Cash and cash equivalents | $ | 514 | $ | 318 | $ | 1,278 | $ | 2,990 | ||||||||||

Property and equipment, net | 37,772 | 33,597 | 82,697 | 80,168 | ||||||||||||||

Total assets | 114,330 | 101,876 | 216,197 | 225,694 | ||||||||||||||

Total debt | 119,918 | 115,437 | 106,459 | 153,393 | ||||||||||||||

Total members equity | (32,281 | ) | (37,647 | ) | 68,088 | 28,038 | ||||||||||||

| (1) | Results for FY 2010 have been adjusted to give pro forma effect to the Acquisition. |

| (2) | We define EBITDA as net income (loss) plus interest expense, tax expense (benefit), and depreciation and amortization, and Adjusted EBITDA as EBITDA further adjusted to eliminate the impact of certain noteworthy items that we do not consider indicative of our ongoing operating performance. Those items are itemized in footnote 3 below. |

| (3) | The following table presents a reconciliation of net income (loss) to Adjusted EBITDA for the periods indicated below |

| Predecessor | Successor | |||||||||||||||||||||

Fiscal Year Ended September 30, | Period from October 1, 2009 through February 16, 2010 | Period from February 17, 2010 through September 30, 2010 | Nine Months Ended June 30, 2011 | |||||||||||||||||||

| 2008 | 2009 | |||||||||||||||||||||

Net Loss to Adjusted EBITDA Reconciliation: | ||||||||||||||||||||||

Net loss | $ | (5,748 | ) | $ | (5,152 | ) | $ | (4,162 | ) | $ | (19,633 | ) | $ | (11,700 | ) | |||||||

Interest expense, net | 15,006 | 15,990 | 7,007 | 8,200 | 11,455 | |||||||||||||||||

Tax expense | (339 | ) | (948 | ) | (365 | ) | 164 | 1,892 | ||||||||||||||

Depreciation and amortization of intangibles | 9,041 | 8,651 | 3,115 | 8,346 | 10,565 | |||||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||

EBITDA | 17,960 | 18,541 | 5,595 | (2,923 | ) | 12,212 | ||||||||||||||||

Management fees(a) | — | — | — | 2,237 | 1,690 | |||||||||||||||||

Consulting fees(b) | — | — | — | 1,047 | 795 | |||||||||||||||||

Restructuring expenses(c) | — | 790 | — | 6,684 | 2,328 | |||||||||||||||||

Bank related fees(d) | 440 | 2,159 | 917 | — | — | |||||||||||||||||

Acquisition fees and expenses(e) | — | — | 1,184 | 10,770 | — | |||||||||||||||||

Fair value inventory step up(f) | — | — | — | 2,782 | — | |||||||||||||||||

Transaction related fees and expenses(g) | — | — | — | — | 1,237 | |||||||||||||||||

Non-cash foreign exchange (gain) loss(h) | 948 | 342 | (446 | ) | — | — | ||||||||||||||||

Integration-related manufacturing variances(i) | — | — | — | 1,129 | 2,356 | |||||||||||||||||

Loss of extinguishment of debt(j) | — | — | — | — | 5,470 | |||||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||

Adjusted EBITDA | $ | 19,348 | $ | 21,832 | $ | 7,250 | $ | 21,726 | $ | 26,088 | ||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||

| (a) | In connection with the Acquisition, we entered into a management services agreement with Castle Harlan to provide business and organizational strategy, financial and investment management, advisory, and merchant and investment banking services. See “Certain Relationships and Related Transactions—Management Agreement.” |

| (b) | In connection with the Acquisition, we entered into a consulting agreement with Keith S. Harbison, the controlling equity holder of Pretium prior to the Acquisition and an equity co-investor in Pretium Holding. See “Certain Relationships and Related Transactions—Consulting Agreement.” |

12

Table of Contents

| (c) | Represents the implementation of several initiatives to restructure and realign manufacturing and administrative resources. These costs incurred in connection with these initiatives consisted of severance, facility consolidation costs, and other exit costs. Restructuring expenses were incurred as part of the integration plan initiated subsequent to the Acquisition. |

| (d) | Represents deferred financing fees as included in bank related loan costs in the consolidated statement of operations. |

| (e) | Represents transaction related costs as included in acquisition fees and expenses in the consolidated statement of operations. For the period October 1, 2009 to February 16, 2010, approximately $0.6 million of these costs were deferred acquisition related costs that were previously capitalized under FASB Statement No. 141, Business Combinations, (now part of ASC Topic 805 Business Combinations). |

| (f) | Represents the increase in inventories to fair value in the purchase accounting adjustments recorded as a result of the Acquisition. The amount was charged to costs of goods during the period February 17, 2010 to September 30, 2010. |

| (g) | Represents professional fees associated with our exploration of acquisition opportunities which we consider noteworthy to the period presented. |

| (h) | Represents the foreign currency transaction impact on debt previously held by our Canadian subsidiary. Concurrent with the Acquisition, the debt held at the Canadian subsidiary was repaid in full. |

| (i) | As a result of the Acquisition and related operational integration plans, we consolidated the Nashua, New Hampshire operation into the Philmont, New York plant and we consolidated Novapak’s Hazelton, Pennsylvania operation into our Hazelton, Pennsylvania plant. Beginning in July 2010, we experienced certain material and labor variances to our standard operating costs reflected in our historical results. We consider these material and labor variances to be noteworthy as we incurred incremental costs to manufacture our products. Variances in the amount of $1.1 million, $0.8 million and $0.4 million were incurred during the three month period ended December 31, 2010, March 31, 2011 and June 30, 2011, respectively. These material and labor variances associated with the integration plans ceased in the period ended June 30, 2011. |

| (j) | We recorded a loss on the extinguishment of debt related to the Refinancing on March 31, 2011. The amount represents the write off of net deferred financing costs from previously outstanding costs, original issue discount, prepayment penalties and other related costs from the Refinancing. |

EBITDA and Adjusted EBITDA are supplemental measures to assess our operating performance that are not required by, or presented in accordance with, generally accepted accounting principles in the United States (“GAAP”). EBITDA and Adjusted EBITDA are not measures of our financial performance under GAAP and should not be considered as alternatives to net income or any other performance measures derived in accordance with GAAP or as an alternative to cash flow from operating activities as measures of our liquidity. When evaluating EBITDA and Adjusted EBITDA, investors should consider, among other factors, (i) increasing or decreasing trends in EBITDA and Adjusted EBITDA, (ii) whether EBITDA and Adjusted EBITDA have remained at positive levels historically, and (iii) how EBITDA and Adjusted EBITDA compares to our outstanding debt.

Our measurements of EBITDA and Adjusted EBITDA and the ratios related thereto may not be comparable to similarly titled measures of other companies. We have included information concerning EBITDA and Adjusted EBITDA in this prospectus because they are bases upon which our management assesses our operating performance, are components of certain covenants in our ABL Facility and we believe that such information is used by certain investors as measures of evaluating our operating performance. Furthermore, we believe these measures are frequently used by securities analysts, investors and other interested parties in the evaluation of high yield issuers, many of which present EBITDA and Adjusted EBITDA when reporting their results. Our presentation of EBITDA and Adjusted EBITDA should not be construed as an inference that our future results will be unaffected by other noteworthy items.

13

Table of Contents

EBITDA and Adjusted EBITDA have limitations as analytical tools, and you should not consider them in isolation, or as substitutes for analysis of our operating results or cash flows as reported under GAAP. Some of these limitations are:

| • | EBITDA and Adjusted EBITDA do not reflect our cash expenditures, or future requirements, for capital expenditures or contractual commitments; |

| • | EBITDA and Adjusted EBITDA do not reflect changes in, or cash requirements for, our working capital needs; |

| • | EBITDA and Adjusted EBITDA do not reflect the significant interest expense or the cash requirements necessary to service interest or principal payments, on our debt; |

| • | although depreciation and amortization are non-cash charges, the assets being depreciated or amortized may have to be replaced in the future, EBITDA and Adjusted EBITDA do not reflect any cash requirements for such replacements; |

| • | EBITDA and Adjusted EBITDA are adjusted for certain noteworthy and non-cash income or expense items that are reflected in our statements of cash flows; and |

| • | other companies in our industry will calculate the measures differently than we do, limiting their usefulness as comparative measures. |

Because of these limitations, EBITDA and Adjusted EBITDA should not be considered as measures of discretionary cash available to us to invest in the growth of our business. We compensate for these limitations by relying primarily on our GAAP results and using EBITDA and Adjusted EBITDA only for supplemental purposes. Please see our audited consolidated financial statements included elsewhere in this prospectus.

14

Table of Contents

You should carefully consider the following risk factors discussed below, as well as the other information presented in this prospectus, before deciding whether to tender the Original Notes in exchange for the New Notes. As a result of any of the following risks, our business, financial and other condition, results of operations, prospects and ability to service our debt could be materially adversely affected, the trading price of the New Notes could decline and you may lose all or part of your investment in the New Notes. See “Forward-Looking Statements.”

Risks Relating to the New Notes and our Indebtedness

We have a substantial amount of indebtedness, which may adversely affect our cash flow, our ability to operate our business and our ability to satisfy our obligations under the Notes.

We have a significant amount of indebtedness. As of June 30, 2011, we had approximately $153.4 million of indebtedness outstanding, all of which is secured and, based on our borrowing base, we had approximately $25.0 million available for borrowings under the ABL Facility, subject to meeting customary borrowing conditions. Our substantial amount of indebtedness could have important consequences for you. For example, it could:

| • | increase our vulnerability to adverse economic, industry or competitive developments; |

| • | result in an event of default if we fail to satisfy our obligations with respect to the Notes or other debt or fail to comply with the financial and other restrictive covenants contained in the ABL Facility and the indenture or agreements governing our other indebtedness, which event of default could result in all of our debt becoming immediately due and payable and could permit our lenders to foreclose on our assets securing such debt; |

| • | require a substantial portion of cash flow from operations to be dedicated to the payment of principal and interest on our indebtedness, therefore reducing our ability to use our cash flow to fund our operations, capital expenditures and future business opportunities; |

| • | make it more difficult for us to satisfy our obligations with respect to the Notes; |

| • | increase our cost of borrowing; |

| • | restrict us from making strategic acquisitions or causing us to make non-strategic divestitures; |

| • | limit our ability to service our indebtedness, including the Notes; |

| • | limit our ability to obtain additional financing for working capital, capital expenditures, debt service requirements, acquisitions and general corporate or other purposes; |

| • | limit our flexibility in planning for, or reacting to, changes in our business or the industry in which we operate, placing us at a competitive disadvantage compared to our competitors who are less highly leveraged and who therefore may be able to take advantage of opportunities that our leverage prevents us from exploiting; and |

| • | prevent us from raising the funds necessary to repurchase all Notes tendered to us upon the occurrence of certain changes of control, which failure to repurchase would constitute a default under the indenture. |

The occurrence of any one of these events could have a material adverse effect on our business, financial condition, results of operations, prospects or ability to satisfy our obligations under the Notes.

Borrowings under the ABL Facility bear interest at variable rates. If we were to borrow funds under the ABL Facility and these rates were to increase significantly, our ability to borrow additional funds may be reduced and

15

Table of Contents

the risks related to our substantial indebtedness would intensify. While we may enter into agreements limiting our exposure to higher interest rates, any such agreements may not offer complete protection for this risk.

Despite our substantial indebtedness level, we and our subsidiaries will still be able to incur substantial additional amounts of debt, which could further exacerbate the risks associated with our indebtedness.

We and our subsidiaries may be able to incur substantial additional indebtedness in the future, including additional secured debt. Our ABL Facility provides for borrowings up to $30 million, and includes an uncommitted incremental facility that, if committed, would increase borrowing capacity, subject to borrowing base capacity. All of the borrowings under the ABL Facility are secured by liens that rank senior to the liens of the holders of the Notes on the collateral. Although the credit agreement governing the ABL Facility and the indenture contain restrictions on the incurrence of additional indebtedness, these restrictions are subject to a number of qualifications and exceptions, and under certain circumstances, the amount of indebtedness that could be incurred in compliance with these restrictions could be substantial. Moreover, if we incur any additional indebtedness secured by liens that rank equally with those securing the Notes, the holders of such indebtedness will be entitled to share ratably with you in any proceeds distributed in connection with any insolvency, liquidation, reorganization, dissolution or other winding-up of us and we cannot assure you any collateral would be sufficient to cover all obligations. In addition, the indenture and the agreement governing the ABL Facility do not prevent us from incurring obligations that do not constitute indebtedness thereunder. If new debt is added to our and our subsidiaries’ existing debt levels, the risks associated with our substantial indebtedness described above, including our possible inability to secure our debt, will increase.

We may not be able to generate sufficient cash to service the Notes or our other indebtedness, and may be forced to take other actions to satisfy our obligations under our indebtedness, which may not be successful.

Our ability to make scheduled payments on our indebtedness, including the Notes, and to fund our operations will depend on our ability to generate cash in the future. We may not be able to maintain a level of cash flows from operating activities sufficient to permit us to pay the principal and interest on the Notes or our other indebtedness.

If our cash flows and capital resources are insufficient to meet our debt service obligations or to fund our other liquidity needs, we may need to refinance all or a portion of our debt, including the Notes, before maturity, seek additional equity capital, reduce or delay scheduled expansions and capital expenditures or sell material assets or operations. We cannot assure you that we would be able to refinance or restructure our indebtedness, obtain equity capital or sell assets or operations on commercially reasonable terms or at all. In addition, the terms of existing or future debt instruments, including the indenture, may limit or prevent us from taking any of these actions. Our inability to take these actions and to generate sufficient cash flow to satisfy our debt service and other obligations could have a material adverse effect on our business, results of operation and financial condition, as well as on our ability to satisfy our obligations in respect of the Notes.

If for any reason we are unable to meet our debt service obligations, we would be in default under the terms of the agreements governing such outstanding indebtedness. If such a default were to occur, the lenders under such indebtedness could elect to declare all amounts outstanding under it immediately due and payable, and in the case of the ABL Facility, the lenders would not be obligated to continue to advance funds under the ABL Facility. If the amounts outstanding under our debt were accelerated, it could cause an event of default under other indebtedness or allow other indebtedness to be accelerated. We cannot assure you that our assets will be sufficient to repay in full the money owed to the banks or to holders of Notes if any indebtedness were accelerated.

16

Table of Contents

The indenture and the credit agreement governing the ABL Facility contain various covenants limiting the discretion of our management in operating our business and could prevent us from capitalizing on business opportunities and taking some corporate actions.

The indenture and the credit agreement governing the ABL Facility impose significant operating and financial restrictions on us. These restrictions will limit or restrict, among other things, our ability and the ability of our subsidiaries to:

| • | incur additional indebtedness or guarantee obligations; |

| • | issue certain preferred stock or redeemable stock; |

| • | pay dividends on, repurchase or make distributions in respect of our capital stock or make other restricted payments; |

| • | make certain investments or acquisitions; |

| • | sell, transfer or otherwise convey certain assets; |

| • | create or incur liens or other encumbrances; |

| • | prepay, redeem or repurchase debt (including the Notes) prior to stated maturities; |

| • | designate our subsidiaries as unrestricted subsidiaries; |

| • | consolidate, merge, sell or otherwise dispose of all or substantially all of our assets; |

| • | enter into a new or different line of business; and |

| • | enter into certain transactions with our affiliates. |

In addition, any debt agreements we enter into in the future may further limit our ability to enter into certain types of transactions.

The covenants described above are subject to important exceptions and qualifications and, with respect to the Notes, are described under the heading “Description of the New Notes—Covenants” and, with respect to the ABL Facility, are described under the heading “Description of Certain Indebtedness—ABL Facility” in this prospectus. Our ability to comply with these covenants may be affected by events beyond our control, including those described in this “Risk Factors” section. As a result, we cannot assure you that we will be able to comply with these covenants. A breach of any of the covenants contained in the indenture or in the credit agreement governing the ABL Facility, including our inability to comply with any financial covenants, could result in an event of default, which would allow the holders of the Notes or the lenders under the ABL Facility, as the case may be, to declare all borrowings outstanding to be due and payable under such indebtedness, which would in turn trigger an event of default under other indebtedness. At maturity or in the event of an acceleration of payment obligations, we would likely be unable to pay our outstanding indebtedness with our cash and cash equivalents then on hand. We would, therefore, be required to seek alternative sources of funding, which may not be available on commercially reasonable terms, terms as favorable as our current agreements or at all, or face bankruptcy. If we are unable to refinance our indebtedness or find alternative means of funding, we may be required to curtail our operations or take other actions that are inconsistent with our current business practices or strategy. Further, if we are unable to repay, refinance or restructure our indebtedness, the holder of such debt could proceed against the collateral securing that indebtedness.

Certain of our assets will be subject to senior priority security interests on collateral that will secure the Notes on a junior basis. Therefore, your ability to receive payments on the Notes will be subject to the prior satisfaction of all such obligations, to the extent of the value of such collateral.

Obligations under the ABL Facility are secured by a first priority lien on substantially all of our and the guarantors’ assets, subject to certain permitted liens. The Notes and the guarantees will be secured by a second priority lien on the same assets. See “Description of the New Notes—Security for the Notes.” Any rights to

17

Table of Contents

payment and claims by the holders of the Notes will, therefore, be subject to the rights to payment or claims by our lenders under the ABL Facility with respect to distributions of such collateral. Only when our obligations under the ABL Facility are satisfied in full will the proceeds of certain assets be available to repay the Notes. As a result, the Notes will be effectively subordinated in right of payment to indebtedness under the ABL Facility and any other indebtedness secured by a first priority lien on such assets, to the extent of the realizable value of such assets. Furthermore, the collateral securing the Notes and the guarantees will be subject to liens permitted under the terms of the indenture, whether arising before or after the date the Notes are issued. The existence of any permitted liens could adversely affect the value of the collateral securing the Notes and the guarantees, as well as the ability of the collateral agent to realize or foreclose on such collateral.

The Notes will be effectively subordinated to the debt of our non-guarantor subsidiaries, if any.

Although the Notes will be fully and unconditionally guaranteed on a senior secured basis by each of our existing subsidiaries (other than the Co-Issuer) and our future domestic subsidiaries, they will not be guaranteed by any future foreign subsidiaries. As a result of this structure, the Notes will be effectively subordinated to all other indebtedness and other liabilities, including trade payables, of our non-guarantor subsidiaries. The effect of this subordination is that, in the event of a bankruptcy, liquidation, dissolution, reorganization or similar proceeding involving a non-guarantor subsidiary, the assets of that subsidiary cannot be used to pay you until all other claims against that subsidiary, including trade payables, have been fully guaranteed.

The intercreditor agreement in connection with the indenture may limit the rights of the holders of the Notes and their control with respect to the collateral securing the Notes.

The rights of the holders of the Notes with respect to the collateral securing the ABL Facility on a first priority basis are substantially limited pursuant to the terms of the intercreditor agreement. Under the intercreditor agreement, if amounts or commitments remain outstanding under the ABL Facility, actions taken in respect of collateral securing our obligations under the ABL Facility on a first priority basis, including the ability to cause the commencement of enforcement proceedings against such collateral and to control the conduct of these proceedings, will be at the sole direction of the holders of the obligations secured by the first priority liens, subject to certain limitations. As a result, the collateral agent, on behalf of the holders of the Notes, may not have the ability to control or direct these actions, even if the rights of the holders of the Notes are adversely affected. The intercreditor agreement also contains certain provisions that restrict the collateral agent, on behalf of the holders of the Notes, from objecting to a number of important matters involving certain of the collateral following a bankruptcy filing by us. After such a filing, the value of the collateral could materially deteriorate. Additionally, the agent for the lenders under the ABL Facility generally has a right to access and use the collateral following any notice to the collateral agent from the agent for the lenders under the ABL Facility that an enforcement action is taking place. See “Description of the New Notes—Intercreditor Agreement.”

The waiver in the intercreditor agreement of rights of marshalling may adversely affect the recovery rates of holders of the Notes in a bankruptcy or foreclosure scenario.

The intercreditor agreement provides that, prior to the discharge of first priority liens securing obligations under the ABL Facility and any pari passu indebtedness sharing in the first priority liens with lenders under the ABL Facility, the holders of the Notes and the trustee under the indenture may not assert or enforce any right of marshalling accorded to a junior lien holder, as against the holders of first priority liens securing obligations under the ABL Facility and such pari passu debt. Without this waiver of the right of marshalling, in the event of an enforcement action by the lenders under the ABL Facility on the collateral in which they hold a first priority lien, the holders of first priority liens securing obligations under the ABL Facility and such pari passu debt would likely be required to liquidate collateral on which the Notes did not have a lien, prior to liquidating collateral on which the Notes have a second priority lien, thereby maximizing the proceeds of the collateral that would be available to repay our obligations under the Notes. As a result of this waiver, the proceeds of sales of the collateral securing the Notes on a second priority basis could be applied to repay obligations under the ABL

18

Table of Contents

Facility and such pari passu debt before applying proceeds of other collateral securing such obligations, and the holders of the Notes may recover less than they would have if such proceeds were applied in the order most favorable to the holders of the Notes.

There may not be sufficient collateral to pay all or any of the Notes.

The Notes and the guarantees will be secured on a second priority basis by security interests in substantially all of the collateral from time to time owned by us or the guarantors. See “Description of the New Notes—Security for the Notes.”

In the event of a foreclosure on the collateral (or a distribution in respect thereof in a bankruptcy or insolvency proceeding), the proceeds from such collateral on which the Notes have a second priority lien may not be sufficient to satisfy the Notes because such proceeds would, under the intercreditor agreement, first be applied to satisfy our obligations under the ABL Facility and any other pari passu indebtedness sharing in the first priority liens with lenders under the ABL Facility. Only after all of our obligations under the ABL Facility and any other pari passu indebtedness sharing in the first priority liens with lenders under the ABL Facility have been satisfied will proceeds from the collateral on which the Notes have a second priority lien be applied to satisfy our obligations under the Notes. To prevent foreclosure, we may be motivated to commence voluntary bankruptcy proceedings, or the holders of the Notes and/or various other interested persons may be motivated to institute bankruptcy proceedings against us. The commencement of such bankruptcy proceedings would expose the holders of the Notes to additional risks, including additional restrictions on exercising rights against collateral. See “—In the event of our bankruptcy, the ability of the holders of the Notes to realize upon the collateral will be subject to certain bankruptcy law limitations.”

Furthermore, the collateral securing the Notes is subject to liens permitted under the terms of the credit agreement governing the ABL Facility and the indenture. The existence of any permitted liens (whether senior to or on parity with the liens securing the Notes) could adversely affect the value of the collateral securing the Notes, as well as the ability of the collateral agent to realize or foreclose on such collateral.

In addition, not all of our and the guarantors’ assets secure the Notes. See “Description of the New Notes—Security for the Notes.” To the extent that the claims of the holders of the Notes exceed the value of the assets securing those Notes and other liabilities, those claims will rank equally with the claims of the holders of our outstanding unsecured indebtedness and other obligations ranking pari passu with the Notes. As a result, if the value of the assets pledged as security for the Notes and other liabilities is less than the value of the claims of the holders of the Notes and other liabilities, those claims may not be satisfied in full.

The collateral may be subject to exceptions, defects, encumbrances, liens and other imperfections. Further, we have not conducted appraisals of all of our or the guarantors’ assets constituting collateral securing the Notes to determine if the value of such collateral upon foreclosure or liquidation equals or exceeds the amount of the Notes or such other obligations secured by such collateral. Accordingly, we cannot assure you that the remaining proceeds from the sale of the collateral would be sufficient to repay holders of Notes all amounts owed under the Notes. The fair market value of the collateral is subject to fluctuations based on factors that include, among others, the condition of our industry, the ability to sell the collateral in an orderly sale, general economic conditions, the availability of buyers, our failure to implement our business strategy and similar factors. The amount received upon a sale of the collateral would be dependent on numerous factors, including but not limited to the actual fair market value of the collateral at such time and the timing and the manner of the sale. By its nature, portions of the collateral may be illiquid and may have no readily ascertainable market value. In the event of a foreclosure, liquidation, bankruptcy or similar proceeding, we cannot assure you that the proceeds from any sale or liquidation of the collateral securing our obligations under the ABL Facility on a first priority basis will be sufficient to pay our obligations under the Notes, in full or at all, after first satisfying our obligations in full under the ABL Facility. In such an event, we cannot assure that the collateral securing our obligations with respect to the Notes on a first priority basis, either alone or with any remaining collateral securing our obligations

19

Table of Contents

under the ABL Facility after satisfying the obligations thereunder, will be sufficient to pay our obligations under the Notes in full. There also can be no assurance that the collateral will be saleable, and, even if saleable, the timing of its liquidation would be uncertain.

In addition, we may not have perfected liens on all of the collateral securing the Notes prior to the consummation of this exchange offer or, in some cases, at all. The security documents contain certain exclusions from perfection requirements and therefore we will not make any attempt to perfect the security interests in that excluded collateral. To the extent certain security interests were not granted, filed and/or perfected on the issuance date of the Original Notes, covenants in the indenture and the security documents for the Notes require us to do or cause to be done all things that may be reasonably required, or that the collateral agent from time to time may reasonably request, to assure and confirm that an enforceable security interest is granted to the collateral agent in such collateral and to take certain actions, if required under the security documents, in order to perfect such security interest (in certain cases within specified time periods following the issue date of the Original Notes, which have not yet expired). We cannot assure you that we will be able to perfect the security interests on a timely basis, and our failure to do so may result in a default under the indenture, the credit agreement governing the ABL Facility and the related security documents. To the extent the certain security interests have been or will be perfected following the issuance date of the Original Notes that security interest would remain at risk of having been granted within 90 days of a bankruptcy filing (in which case it might be avoided as a preferential transfer by a trustee in bankruptcy) even after the security interests perfected on the closing date were no longer subject to such risk. See “—The Notes could be wholly or partially voided as a preferential transfer.”

Accordingly, there may not be sufficient collateral to pay all or any of the amounts due on the Notes. Any claim for the difference between the amount, if any, realized by holders of the Notes from the sale of the collateral securing the Notes and the obligations under the Notes will rank equally in right of payment with all of our other unsecured unsubordinated indebtedness and other obligations, including trade payables.

With respect to some of the collateral, the collateral agent’s security interest and ability to foreclose will also be limited by the need to meet certain requirements, such as obtaining third-party consents and making additional filings. If we are unable to obtain these consents or make these filings, the security interests may be invalid and the holders will not be entitled to the collateral or any recovery with respect thereto. We cannot assure you that any such required consents can be obtained on a timely basis or at all. These requirements may limit the number of potential bidders for certain collateral in any foreclosure and may delay any sale, either of which events may have an adverse effect on the sale price of the collateral. Therefore, the practical value of realizing on the collateral may, without the appropriate consents and filings, be limited.

The rights of holders of the Notes in the collateral may be adversely affected by the failure to perfect security interests in the collateral and other issues generally associated with the realization of security interests in the collateral.

Applicable law provides that a security interest in certain tangible and intangible assets can only be properly perfected and its priority retained through certain actions undertaken by the secured party. The liens on the collateral securing the Notes may not be perfected with respect to the Notes and the guarantees if the collateral agent has not taken the actions necessary to perfect any of those liens. The inability or failure of the collateral agent to take all actions necessary to create properly perfected security interests in the collateral may result in the loss of the priority of the security interest for the benefit of the holders of the Notes to which they would have been entitled.

In addition, applicable law provides that certain property and rights acquired after the grant of a general security interest can only be perfected at the time such property and rights are acquired and identified. We cannot assure you that the collateral agent for the Notes or the agent under the ABL Facility will monitor, or that we or the guarantors will inform such collateral agent or agent of, the future acquisition of property and rights that constitute collateral, and that the necessary action will be taken to properly perfect the security interest in such

20

Table of Contents

after-acquired collateral. The collateral agent and the agent under the ABL Facility have no obligation to monitor the acquisition of additional property or rights that constitute collateral or the perfection of any security interest. Such failure may result in the loss of the security interest in the collateral or the priority of the security interest in favor of the Notes and the guarantees against third parties.

The security interest of the collateral agent will be subject to practical challenges generally associated with the realization of security interests in the collateral. For example, the collateral agent may need to obtain the consent of a third party to obtain or enforce a security interest in an asset. We cannot assure you that the collateral agent will be able to obtain any such consent or that the consents of any third parties will be given when required to facilitate a foreclosure on such assets. As a result, the collateral agent may not have the ability to foreclose upon those assets and the value of the collateral may significantly decrease.

The collateral is subject to casualty risks.

The indenture, the credit agreement governing the ABL Facility and the related security documents require us and the guarantors to maintain adequate insurance or otherwise insure against risks to the extent customary with companies in the same or similar business operating in the same or similar locations. There are, however, certain losses, including losses resulting from terrorist acts, that may be either uninsurable or not economically insurable, in whole or in part. As a result, we cannot assure you that the insurance proceeds will compensate us fully for our losses. If there is a total or partial loss of any of the collateral securing the Notes we cannot assure you that any insurance proceeds received by us will be sufficient to satisfy all the secured obligations, including the Notes.

In the event of a total or partial loss to any of the mortgaged facilities, certain items of equipment and inventory may not be easily replaced. Accordingly, even though there may be insurance coverage, the extended period needed to manufacture replacement units or inventory could cause significant delays.

The collateral is subject to condemnation risks, which may limit your ability to recover as a secured creditor for losses to the collateral consisting of mortgaged properties, and which may have an adverse impact on our operations and results.

It is possible that all or a portion of the mortgaged facilities securing the Notes may become subject to a condemnation proceeding. In such event, we may be compensated for any total or partial loss of property but it is possible that such compensation will be insufficient to fully compensate us for our losses. In addition, a total or partial condemnation may interfere with our ability to use and operate all or a portion of the affected facility, which may have an adverse impact on our operations and results.

We may be unable to repay or repurchase the Notes at maturity.

At maturity, the entire principal amount of the Notes, together with accrued and unpaid interest, will become due and payable. We may not have the ability to repay or refinance these obligations. If the maturity date occurs at a time when other arrangements prohibit us from repaying the Notes, we would try to obtain waivers of such prohibitions from the lenders and holders under those arrangements, or we could attempt to refinance the borrowings that contain the restrictions. If we could not obtain the waivers or refinance these borrowings, we would be unable to repay the Notes.

In the event of our bankruptcy, the ability of the holders of the Notes to realize upon the collateral will be subject to certain bankruptcy law limitations.

Bankruptcy law could prevent the collateral agent (or the rights of the lenders under the ABL Facility provided for in the intercreditor agreement) from repossessing and disposing of, or otherwise exercising remedies in respect of, the collateral upon the occurrence of an event of default if a bankruptcy proceeding were to be commenced by or against us prior to the collateral agent having repossessed and disposed of, or otherwise

21

Table of Contents

exercised remedies in respect of, the collateral. Under the U.S. bankruptcy code, a secured creditor such as the collateral agent is prohibited from repossessing its security from a debtor in a bankruptcy case, or from disposing of security repossessed from such debtor, without bankruptcy court approval. Moreover, the bankruptcy code permits the debtor to continue to retain and to use collateral even though the debtor is in default under the applicable debt instrument; provided that the secured creditor is given “adequate protection.” The meaning of the term “adequate protection” may vary according to the circumstances, but it is intended in general to protect the value of the secured creditor’s interest in the collateral. The court may find “adequate protection” if the debtor pays cash or grants additional security, if and at such times as the court in its discretion determines, for any diminution in the value of the collateral during the pendency of the bankruptcy case.

In view of the lack of a precise definition of the term “adequate protection” and the broad discretionary powers of a bankruptcy court, it is impossible to predict how long payments with respect to the Notes could be delayed following commencement of a bankruptcy case, whether or when the trustee could repossess or dispose of the collateral or whether or to what extent holders would be compensated for any delay in payment or loss of value of the collateral through the requirement of “adequate protection.” Furthermore, in the event the bankruptcy court determines that the value of the collateral is not sufficient to repay all amounts due on the Notes, the holders of the Notes would have “undersecured claims” as to the difference. Federal bankruptcy laws do not permit the payment or accrual of interest, costs and attorneys’ fees for “undersecured claims” during the debtor’s bankruptcy case.