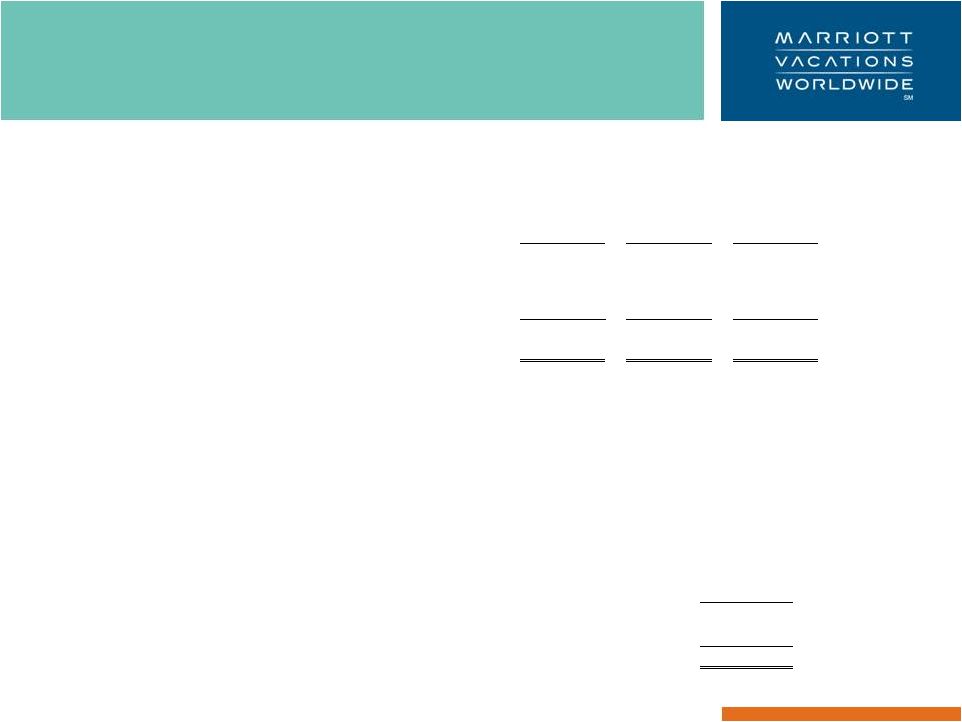

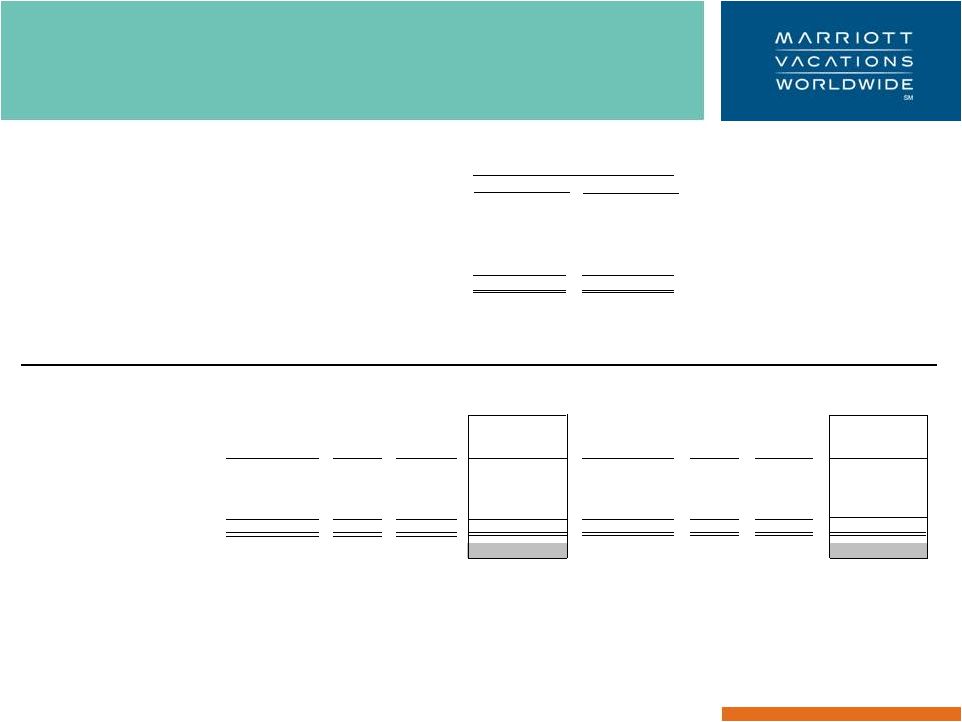

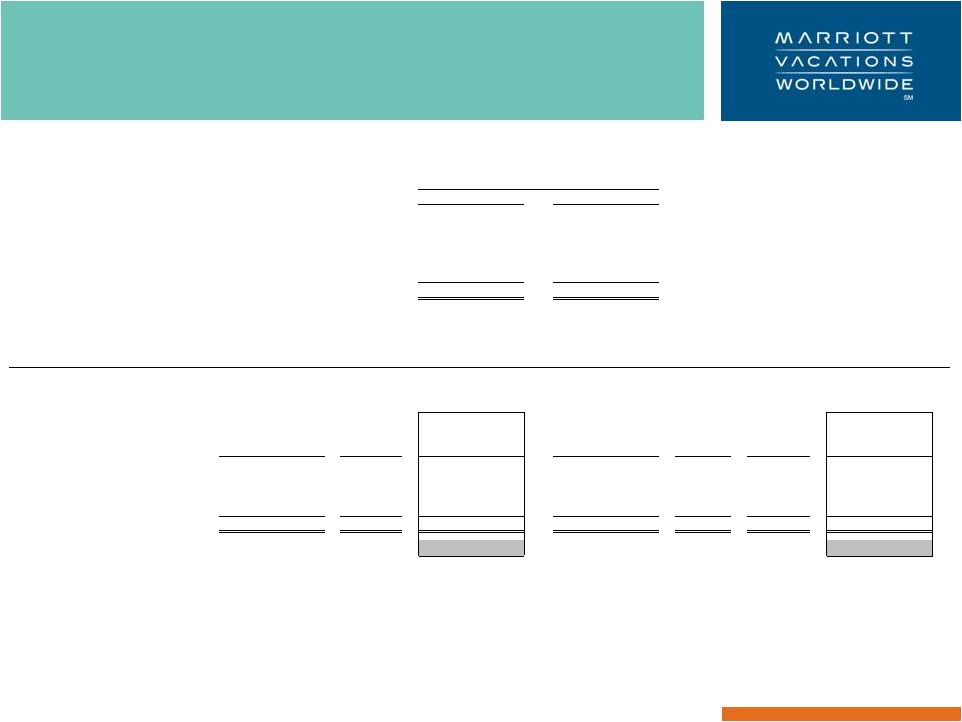

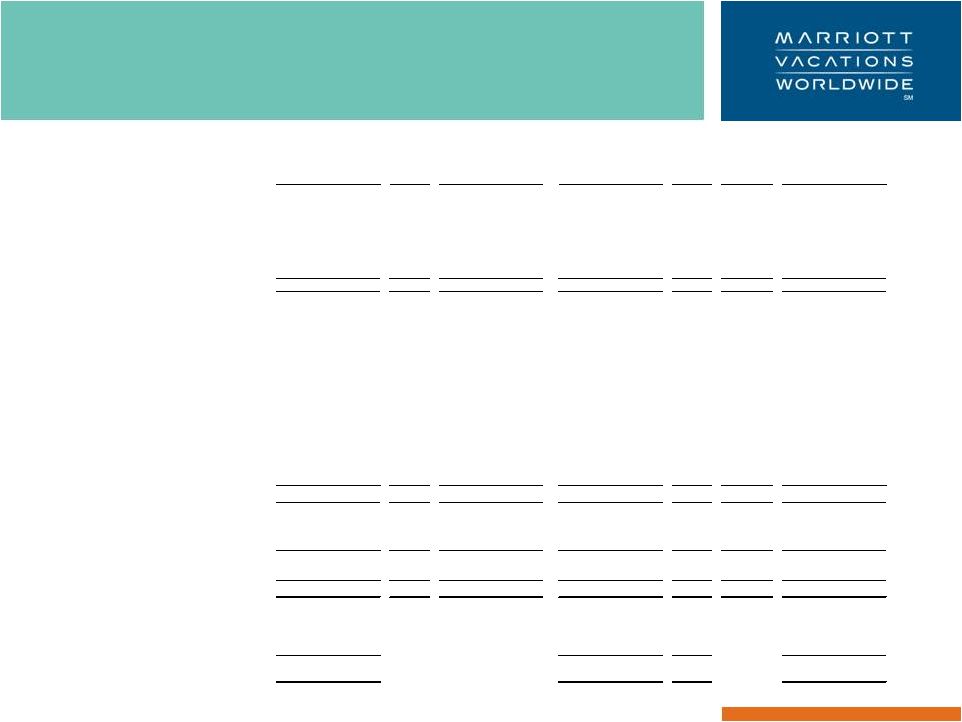

MARRIOTT VACATIONS WORLDWIDE CONFIDENTIAL AND PROPRIETARY INFORMATION 20 Non-GAAP Financial Measures Adjusted Net Income and Adjusted Pro Forma Net Income (continued) Operations, we recorded $10 million of pre-tax charges comprised of $4 million of spin-off related charges under the "General and administrative" caption, $3 million of severance costs ($1 million under the "Marketing and sales" caption and $2 million under the "General and administrative" caption), and $3 million of legal related charges under the "Marketing and sales" caption. In our 52 weeks ended December 30, 2011 Statements of Operations, we recorded $18 million of pre-tax charges comprised of $5 million of severance costs ($3 million under the "Marketing and sales" caption and $2 million under the "General and administrative" caption), $4 million of spin-off related charges under the "General and administrative" caption, $3 million of costs related to ADA compliance and Hurricane Irene damage at a resort in the Bahamas under the "Cost of vacation ownership products" caption, $3 million for a legal settlement related to a project in our Luxury segment under the "Litigation settlement" caption, and $3 million of legal related charges under the "Marketing and sales" caption. 2012 Statements of Operations, we did not record any non-cash impairment charges. In our 52 weeks ended December 28, 2012 Statements of Operations, we reversed $2 million related to our previously recorded impairment of an equity investment in a Luxury segment vacation ownership joint venture project, because the actual costs incurred to suspend the marketing and sales operations were lower than previously estimated, under the "Impairment reversals on equity investment" caption. 2011 Statements of Operations, we did not record any non-cash impairment charges. In preparation for the spin-off from Marriott International, management assessed the intended use of excess undeveloped land and built inventory and the current market conditions for those assets. During 2011, management approved a plan to accelerate cash flow through the monetization of certain excess undeveloped land in the United States, Mexico, and the Bahamas and to accelerate sales of excess built Luxury fractional and residential inventory. As a result, in accordance with the guidance for accounting for the impairment or disposal of long-lived assets, because the nominal cash flows from the planned land sales and the estimated fair values of the land and excess built Luxury inventory were less than their respective carrying values, we recorded a pre-tax non-cash impairment charge of $324 million in our 36 weeks ended September 9, 2011 Statements of Operations under the “Impairment” caption. Additionally, in our 36 weeks ended September 9, 2011 Statements of Operations, under the "Impairment reversals on equity investment" caption, we reversed nearly $4 million of a more than $16 million funding liability we originally recorded in 2009 related to a Luxury segment vacation ownership joint venture project, based on facts and circumstances surrounding the project, including favorable resolution of certain construction related claims and contingent obligations to refund certain deposits relating to sales that have subsequently closed. Other Charges - 16 weeks and 52 weeks ended December 30, 2011. In our 16 weeks ended December 30, 2011 Statements of Non-cash Impairment Charges - 16 weeks and 52 weeks ended December 28, 2012. In our 16 weeks ended December 28, Non-cash Impairment Charges - 16 weeks and 52 weeks ended December 30, 2011. In our 16 weeks ended December 30, |