Exhibit 99.1

| Equity Roadshow October/November 2011 |

| Forward-Looking Statement Safe Harbor Statement under the Private Securities Litigation Reform Act of 1995 (the "Act"): Certain material presented herein includes forward-looking statements intended to qualify for the safe harbor from liability established by the Private Securities Litigation Reform Act of 1995. These forward-looking statements include, but are not limited to, statements about the separation of Exelis Inc. (the "Company") from ITT Corporation, the terms and the effect of the separation, the nature and impact of such a separation, capitalization of the Company, future strategic plans and other statements that describe the Company's business strategy, outlook, objectives, plans, intentions or goals, and any discussion of future operating or financial performance. Whenever used, words such as "anticipate," "estimate," "expect," "project," "intend," "plan," "believe," "target" and other terms of similar meaning are intended to identify such forward-looking statements. Forward-looking statements are uncertain and to some extent unpredictable, and involve known and unknown risks, uncertainties and other important factors that could cause actual results to differ materially from those expressed or implied in, or reasonably inferred from, such forward-looking statements. Factors that could cause results to differ materially from those anticipated include, but are not limited to: The Company undertakes no obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise. Economic, political and social conditions in the countries in which we conduct our businesses; Changes in U.S. or International government defense budgets; Decline in consumer spending; Sales and revenues mix and pricing levels; Availability of adequate labor, commodities, supplies and raw materials; Interest and foreign currency exchange rate fluctuations and changes in local government regulations; Competition, industry capacity & production rates; Ability of third parties, including our commercial partners, counterparties, financial institutions and insurers, to comply with their commitments to us; Our ability to borrow or to refinance our existing indebtedness and availability of liquidity sufficient to meet our needs; Changes in the value of goodwill or intangible assets; Our ability to achieve stated synergies or cost savings from acquisitions or divestitures; The number of personal injury claims filed against or the Company or degree of liability; Our ability to effect restructuring and cost reduction programs and realize savings from such actions; Government regulations and compliance therewith, including Dodd-Frank legislation; Changes in technology; Intellectual property matters; Governmental investigations; Potential future employee benefit plan contributions and other employment and pension matters; Contingencies related to actual or alleged environmental contamination, claims and concerns; Changes in generally accepted accounting principles; and Other factors set forth in our Registration Statement on Form 10 and our other filings with the Securities and Exchange Commission. In addition, there are risks and uncertainties relating to the separation including whether those transactions will result in any tax liability, the operational and financial profile of the Company or any of its businesses after giving effect to the separation, and the ability of the Company to operate as an independent entity. 2 |

| Transaction Overview Ticker XLS Exchange NYSE Exchange ratio 1:1 Expected number of shares 185 million October 13, 2011 First day of trading on a "when-issued" basis (Bloomberg ticker: XLS-W) October 17, 2011 Record date (at close of business) October 31, 2011 Distribution of Exelis stock to ITT shareholders (after market close) November 1, 2011 First day of Regular way trading for Exelis stock on the NYSE 3 In January 2011, ITT announced its intended separation into 3 publicly traded entities, including two tax-free spin-offs for its Water- and Defense-related businesses ITT Exelis is the new ITT Defense business The IRS has approved the tax-free nature of the transaction Form 10 registration statement for ITT Exelis common stock has been declared effective by the SEC |

| Exelis - Investment Highlights Diversified portfolio with attractive positions in enduring market segments Leader in electronic warfare, ISR, navigation and information exploitation Strong contract positions in essential government services Growing non-DoD positions: air traffic management, aerostructures and international Mission-critical and affordable ready-now solutions Leveraging agility, customer intimacy and deep technology expertise Cost-efficient products and services Proven record of solid program performance and operational excellence Large fielded base and platform-agnostic solutions drive sustainable revenue Strong cash generation to complement well-capitalized balance sheet Experienced management team 4 |

| Electronic Warfare Force Protection Networked Communications Radar Composite Structures Reconnaissance & Surveillance Undersea Acoustics Global Base Operations Support Range Operations, Sustainment, Upgrade & Modernization Battlefield Network Communications Support Worldwide Logistics & Deployment Support Ground Vehicle & Equipment Maintenance Airborne Situational Awareness Information Exploitation Space-Based Satellite Imaging Weather & Climate Monitoring GPS Night Vision Large-scale Network Architecture & Integration Cyber Security Air Traffic and Airport Solutions Space Communications Network Services Data Fusion Engineering and Professional Services CBRNE Technologies C4ISR Electronics & Systems Information & Technical Services (I&TS) A Diversified Business Responding to Global Security Needs... Electronic Systems Geospatial Systems Mission Systems Information Systems 5 |

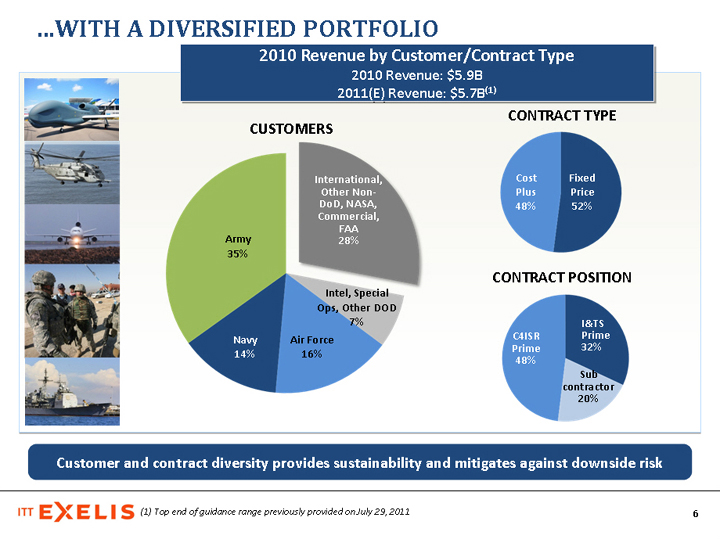

| ....with A Diversified Portfolio (CHART) (CHART) Cost Plus 48% Fixed Price 52% Army 35% Intel, Special Ops, Other DOD 7% Navy 14% Air Force 16% International, Other Non- DoD, NASA, Commercial, FAA 28% Customers Contract Type Contract Position 2010 Revenue by Customer/Contract Type 2010 Revenue: $5.9B 2011(E) Revenue: $5.7B(1) Customer and contract diversity provides sustainability and mitigates against downside risk Sub contractor 20% C4ISR Prime 48% I&TS Prime 32% 6 (1) Top end of guidance range previously provided on July 29, 2011 |

| .... Expanding in International Markets International Revenue by Region - 2010 Focus business development on Middle East, Asia-Pacific, India, Brazil Growth driven by expanding product sales and solutions in high-growth markets International revenue 11% of total; 17% of Exelis product businesses Europe 41% Middle East 28% Asia-Pacific 25% Americas 6% Traditional Markets 41% High-Growth Markets 59% 20% CAGR international growth 2008-2010 7 |

| Needs We enable smarter, faster decisions and efficient, targeted responses Electronic Warfare / Electronic Protection Autonomy Data to Decisions Cyber Science & Technology Protection of systems and extension of capabilities across the electromagnetic spectrum Next Gen EW Jammer Networked IED Protection Electromagnetic pulse protection Autonomous completion of complex tasks in a reliable and safe manner Sense & Avoid Radar Tagging, Tracking & Locating Faster and more efficient analysis and use of large data sets Efficient and effective cyber capabilities across the joint operations spectrum Multi-level Secure Cloud Cyber Mission Assurance Communications and network solutions EchoStorm Gorgon Stare Large-Data-WAN Investments Aligned with DoD Priorities (1) As stated by Secretary of Defense; 4/19/2011 memorandum; Science and Technology Priorities for Fiscal Years 2013-17 Planning Priorities1 Exelis Solutions 8 |

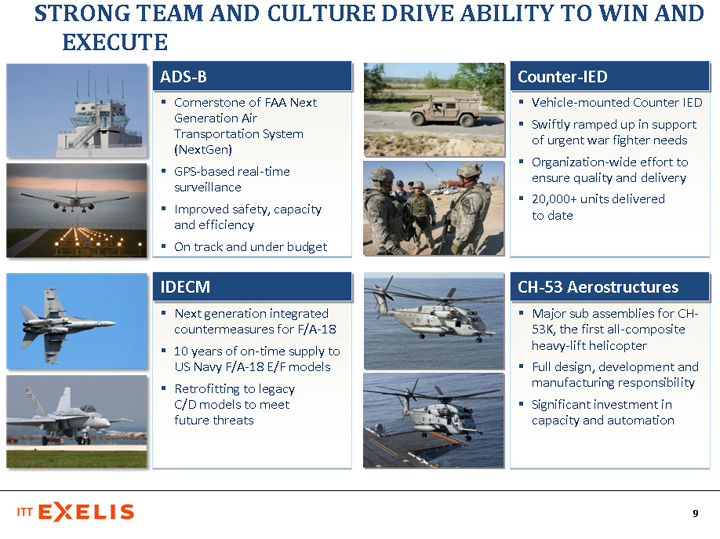

| Strong Team and Culture Drive Ability to Win and Execute Cornerstone of FAA Next Generation Air Transportation System (NextGen) GPS-based real-time surveillance Improved safety, capacity and efficiency On track and under budget Next generation integrated countermeasures for F/A-18 10 years of on-time supply to US Navy F/A-18 E/F models Retrofitting to legacy C/D models to meet future threats ADS-B IDECM Major sub assemblies for CH- 53K, the first all-composite heavy-lift helicopter Full design, development and manufacturing responsibility Significant investment in capacity and automation CH-53 Aerostructures Vehicle-mounted Counter IED Swiftly ramped up in support of urgent war fighter needs Organization-wide effort to ensure quality and delivery 20,000+ units delivered to date Counter-IED 9 |

| C4ISR Electronics and Systems Overview Cost Plus 39% Fixed Price 61% Subcontractor 35% Prime 65% Army 24% Other 20% Navy 2% Air Force 14% International, Other Non-DoD, NASA, Commercial 39% Full-Spectrum Imaging and Positioning Solutions 10 Geospatial Systems 2010 REVENUE = $1.2b YTD 6/30/2011 REVENUE = $0.6b Fixed Price 80% Subcontractor 15% Prime 85% Army 23% Classified 13% Navy 23% Air Force 11% International, Other Non-DoD, Commercial 30% Cost Plus 20% 2010 REVENUE = $2.4b YTD 6/30/2011 REVENUE = $0.8b Customers Contract Type Contract Position Customers Contract Type Contract Position Integrated C4ISR Product & EW Solutions Electronics Systems |

| Information & Technical Services (I&TS) Cost Plus 91% Fixed Price 9% Subcontractor 14% Prime 86% Army 13% Other DoD 6% Navy 14% Other US Gov 35% NASA and FAA 32% Customers Contract Type Contract Position 11 Cost Plus 83% Fixed Price 17% Subcontractor 14% Prime 86% Army 60% Navy 4% Air Force 31% International, Other Non-DoD, NASA, Commercial, FAA 5% Customers Contract Type Contract Position Information Systems Mission Systems 2010 Revenue: $0.8b YTD 6/30/2011 Revenue: $0.4b 2010 Revenue: $1.5b YTD 6/30/2011 Revenue: $1.1b Delivering Mission Critical Services Designing and Operating Complex Networks |

| Core Positions: Extend Leadership Portfolio Management to Align with Enduring Needs Create value through complementary C4ISR capabilities and positions ISR 12 Focused Growth: Invest in Capabilities & Scale Information & Cyber Air Traffic Solutions Aerostructures Electronic Warfare Networked Communications Core Positions: Extend Leadership Focused Growth: Invest in Capabilities & Scale |

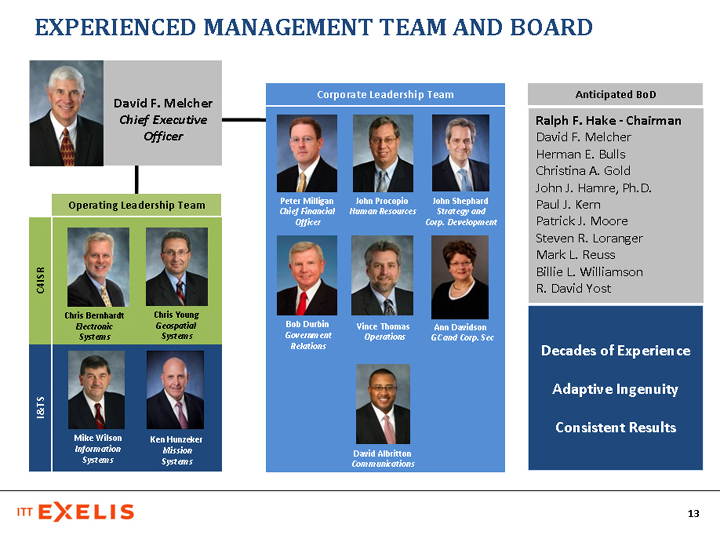

| Experienced Management Team and Board Ralph F. Hake - Chairman David F. Melcher Herman E. Bulls Christina A. Gold John J. Hamre, Ph.D. Paul J. Kern Patrick J. Moore Steven R. Loranger Mark L. Reuss Billie L. Williamson R. David Yost David F. Melcher Chief Executive Officer Mike Wilson Information Systems Chris Young Geospatial Systems Chris Bernhardt Electronic Systems Operating Leadership Team Ken Hunzeker Mission Systems Vince Thomas Operations Peter Milligan Chief Financial Officer John Procopio Human Resources Ann Davidson GC and Corp. Sec David Albritton Communications John Shephard Strategy and Corp. Development Bob Durbin Government Relations Corporate Leadership Team Anticipated BoD Decades of Experience Adaptive Ingenuity Consistent Results C4ISR I&TS 13 |

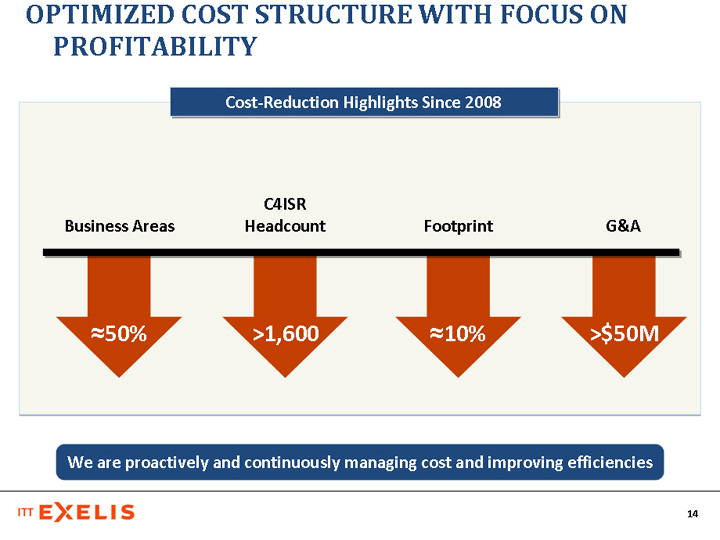

| Optimized Cost Structure with Focus On Profitability We are proactively and continuously managing cost and improving efficiencies Cost-Reduction Highlights Since 2008 ^50% Footprint >1,600 C4ISR Headcount ^10% Business Areas >$50M G&A 14 |

| Financial Highlights October 2011 15 |

| Exelis Revenue Overview ($B) $6.1 $6.1 $5.9 $5.7 (1) Top end of guidance range previously provided on July 29, 2011 (1) Significant revenue mix shift between C4ISR and I&TS in 2011 I&TS ^51% C4ISR ^49% I&TS 39% C4ISR 61% I&TS 38% C4ISR 62% I&TS 36% C4ISR 64% 2011 coming in strong due to large service task orders 2012 pressure in line with overall industry Longer term, well positioned to gain share in an uncertain market 16 |

| Evolving Revenue Mix-Balance of Products and Services $B 60 / 40 50 / 50 (2) Product and service revenues serve as a close proxy for fixed price (product) and cost plus (service) revenues $1.7B $0.6B $4.4B $5.1B CAGR -28.2% CAGR 5.0% $B $- US SINCGARS, IED Jammers and Night Vision All Other Service mix anticipated to remain in the ratio seen in 2011 Services Products "All other" represents 90% of 2011 revenue and is well positioned for continued market-share growth (1) 2011E Guidance as previously provided on July 29, 2011 (1) (2) (2) (1) 17 |

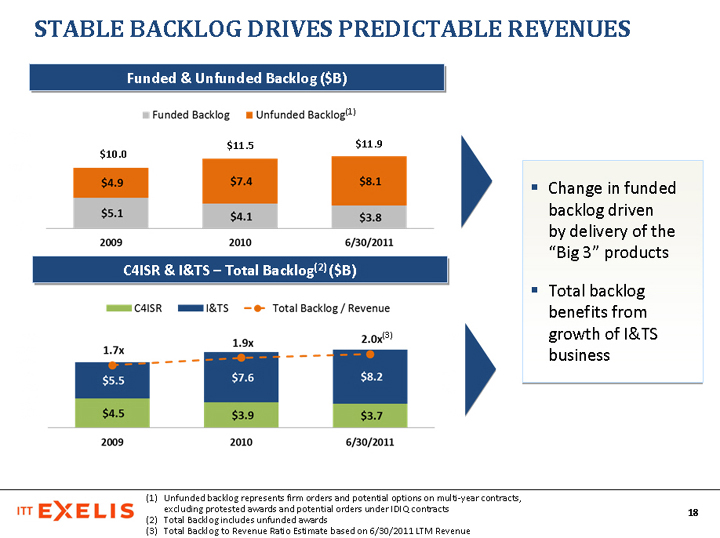

| Stable Backlog Drives Predictable Revenues C4ISR & I&TS - Total Backlog(2) ($B) Unfunded backlog represents firm orders and potential options on multi-year contracts, excluding protested awards and potential orders under IDIQ contracts Total Backlog includes unfunded awards Total Backlog to Revenue Ratio Estimate based on 6/30/2011 LTM Revenue $10.0 $11.5 $11.9 Funded & Unfunded Backlog ($B) (3) Change in funded backlog driven by delivery of the "Big 3" products Total backlog benefits from growth of I&TS business (1) 18 |

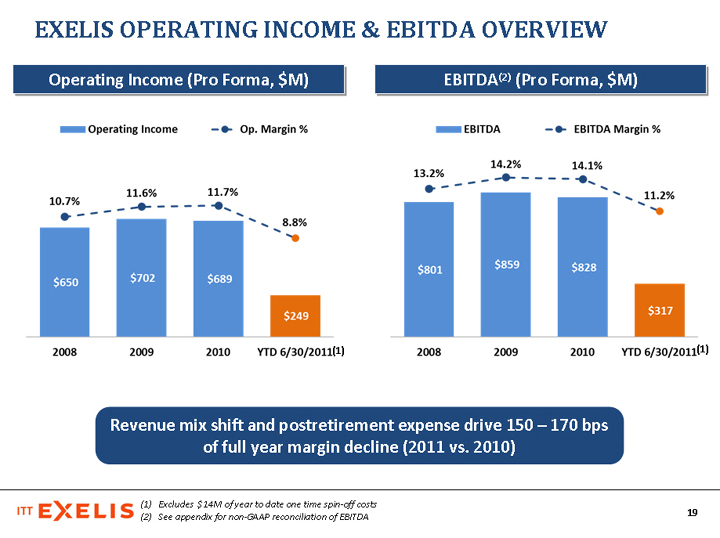

| Exelis Operating Income & EBITDA Overview Operating Income (Pro Forma, $M) EBITDA(2) (Pro Forma, $M) Excludes $14M of year to date one time spin-off costs See appendix for non-GAAP reconciliation of EBITDA (1) (1) Revenue mix shift and postretirement expense drive 150 - 170 bps of full year margin decline (2011 vs. 2010) 19 |

| Flexible & Controllable Cost Structure Cost Structure 2011E Substantial portion of overall cost structure is variable Monitoring direct labor utilization drives ongoing optimization of workforce Material purchased when contracts are placed-results in minimal inventory risk Other direct costs largely relates to contract labor within the I&TS business ~50% of overhead is fringe costs driven by headcount Drivers 20 |

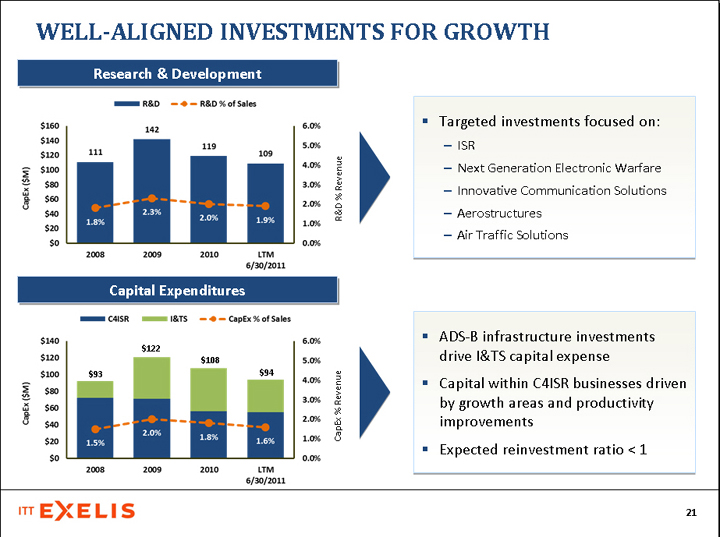

| Well-Aligned Investments for Growth Targeted investments focused on: ISR Next Generation Electronic Warfare Innovative Communication Solutions Aerostructures Air Traffic Solutions ADS-B infrastructure investments drive I&TS capital expense Capital within C4ISR businesses driven by growth areas and productivity improvements Expected reinvestment ratio < 1 R&D % Revenue CapEx % Revenue $93 $122 $108 $94 Research & Development Capital Expenditures 21 |

| Exelis Strong Cash Flow Generation and Actively Managed Cash Flow Requirements Free cash flow conversion ^100% of net income excluding pension contributions Pension funding profile(1) characterized by: Unfunded liability of ^$1B expected to be funded over the next four years(2) Plan expected to be fully funded in 2015 with average contributions of $0.2B-$0.3B per year (before tax benefit) Current P&L non-cash pension expense ^$0.1B Annual dividend anticipated to be $76M Expected tax rate in 36% - 38% range Unfunded liability based on postretirement valuation as of 12/31/10; as outlined in Form 10 See slide 29 in appendix for pension asset/liability and expense sensitivities 22 |

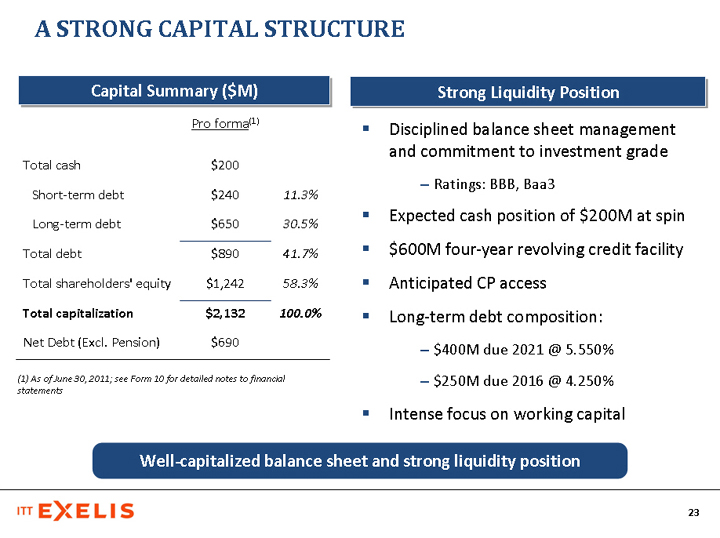

| Pro forma(1) Total cash $200 Short-term debt $240 11.3% Long-term debt $650 30.5% Total debt $890 41.7% Total shareholders' equity $1,242 58.3% Total capitalization $2,132 100.0% Net Debt (Excl. Pension) $690 (1) As of June 30, 2011; see Form 10 for detailed notes to financial statements Capital Summary ($M) Strong Liquidity Position Disciplined balance sheet management and commitment to investment grade Ratings: BBB, Baa3 Expected cash position of $200M at spin $600M four-year revolving credit facility Anticipated CP access Long-term debt composition: $400M due 2021 @ 5.550% $250M due 2016 @ 4.250% Intense focus on working capital Well-capitalized balance sheet and strong liquidity position A Strong Capital Structure 23 |

| Exelis Financial Highlights Diversified revenue base with balanced outlook given budget uncertainty Highly variable and controllable cost structure Conservative pension funding assumptions Attractive dividend Strong cash flow available for incremental growth and return to shareholders 24 |

| Exelis - Investment Highlights Diversified portfolio with attractive positions in enduring market segments Leader in electronic warfare, ISR, navigation and information exploitation Strong contract positions in essential government services Growing non-DoD positions: air traffic management, aerostructures and international Mission-critical and affordable ready-now solutions Leveraging agility, customer intimacy and deep technology expertise Cost-efficient products and services Proven record of solid program performance and operational excellence Large fielded base and platform-agnostic solutions drive sustainable revenue Strong cash generation to complement well-capitalized balance sheet Experienced management team 25 |

| Appendix 26 |

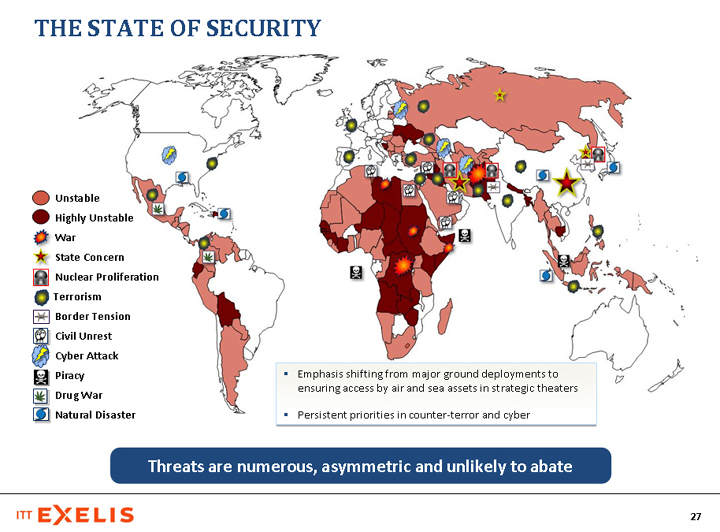

| The State of Security Threats are numerous, asymmetric and unlikely to abate War State Concern Civil Unrest Piracy Drug War Natural Disaster Unstable Highly Unstable Nuclear Proliferation Terrorism Border Tension Cyber Attack Emphasis shifting from major ground deployments to ensuring access by air and sea assets in strategic theaters Persistent priorities in counter-terror and cyber 27 |

| Build Off Large Fielded Base & Platform-Agnostic Solutions Space Space Fixed Wing & UAVs Fixed Wing & UAVs Fixed Wing & UAVs Fixed Wing & UAVs Fixed Wing & UAVs Fixed Wing & UAVs Fixed Wing & UAVs Fixed Wing & UAVs Fixed Wing & UAVs Com'l Aircraft Rotary Wing Rotary Wing Rotary Wing Rotary Wing Rotary Wing Rotary Wing Naval Naval Ground Vehicles Soldier Systems ISR GPS B-1B C-130 F-15 F-16 E/F-18 (G) F-22 F-35 P-8 UAVs Com'l Aircraft AH-64 MH-47 CH/MH-53 MH-60 CV-22 UH-60 Surface Subs Ground Vehicles Soldier Systems Electronic Warfare ? ? ? ? ? ? ? ? ? ? ? ? ? 25,000 counter-IED systems; 2,500 airborne jammers Communications ? ? ? ? 600,000 radio systems Radar & Acoustics ? ? ? ? ? ? 1,200 radars; 1,000 ESM systems Night Vision & Imaging ? ? ? ? ? ? ? ? ? ? ? ? ? ? 860,000+ goggles Navigation ? ? ? ? 43 GPS payloads Integrated Structures ? ? ? ? ? ? ? ? ? 18,000 weapon release racks Platform diversification, modernization and aftermarket drive revenue sustainability ? Exelis Position Capabilities Examples Broadly positioned on enduring platforms 28 |

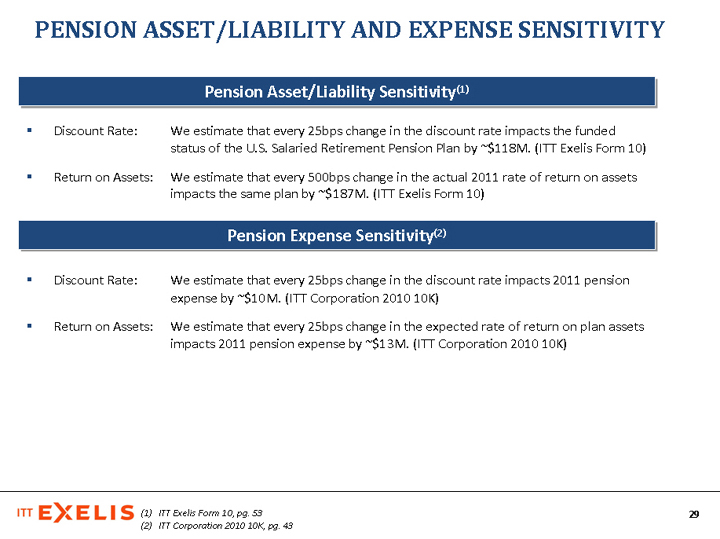

| Pension Asset/Liability and Expense Sensitivity 29 Pension Asset/Liability Sensitivity(1) Pension Expense Sensitivity(2) Discount Rate: We estimate that every 25bps change in the discount rate impacts the funded status of the U.S. Salaried Retirement Pension Plan by ~$118M. (ITT Exelis Form 10) Return on Assets: We estimate that every 500bps change in the actual 2011 rate of return on assets impacts the same plan by ~$187M. (ITT Exelis Form 10) Discount Rate: We estimate that every 25bps change in the discount rate impacts 2011 pension expense by ~$10M. (ITT Corporation 2010 10K) Return on Assets: We estimate that every 25bps change in the expected rate of return on plan assets impacts 2011 pension expense by ~$13M. (ITT Corporation 2010 10K) ITT Exelis Form 10, pg. 53 ITT Corporation 2010 10K, pg. 43 |

| Operating Income and EPS 30 Op. Income: Pro Forma vs. ITT 10K/Q $715 $761 $752 $278 Earnings Per Share - Pro Forma (1) Reflects adjustment for removal of one-time spin costs; see Form 10 for detailed notes to financial statements (1) |

| Non-GAAP EBITDA Reconciliation 31 Year Ended December 31, (except YTD) $ in Millions 2008 2009 2010 YTD 6/30/2011 ITT Exelis Operating Income $650 $702 $689 $249 Plus: Depreciation & Amortization $151 $157 $139 $68 EBITDA $801 $859 $828 $317 |