Filed by FS Investment Corporation II

pursuant to Rule 425 under the Securities Act of 1933

and deemed filed underRule 14a-12 of the Securities Exchange Act of 1934

Subject Companies: FS Investment Corporation III

FS Investment Corporation IV

Corporate Capital Trust II

CommissionFile No. 814-00926

FS/KKR announces mergers and liquidity plan for FSIC II,

FSIC III, FSIC IV and CCT II

Overview

| 1. | What are the details of the announced merger and liquidity plan? |

| • | FS Investment Corporation II (FSIC II), FS Investment Corporation III (FSIC III), FS Investment Corporation IV (FSIC IV) and Corporate Capital Trust II (CCT II) entered into an agreement and plan of merger (the “Merger Agreement”) to create the second-largest business development company (BDC), with over $9 billion in total assets on a pro forma basis as of March 31, 2019. |

| • | The mergers are part of a proposedthree-step process to create a liquidity event for all shareholders. |

| – | Merger:FSIC II will serve as the surviving entity in net asset value (NAV)-for-NAV mergers with FSIC III, FSIC IV and CCT II (the “Acquired Funds”). |

| – | Recapitalization:Following the completion of the mergers and subject to board approval, the combined company intends to issue approximately $1 billion of 5.5% perpetual preferred equity pro rate to holders of the combined company’s common equity prior to any public listing of the common equity, subject to final board approval. |

The preferred shares will provide current income for investors (5.5%) and help align the dividend yield and return on equity of the combined company’s common stock to a competitive level with some of the largest publicly traded business development companies (BDCs).

Following the recapitalization, an investor’s total value will consist of the following (assuming the value of the common shares is the NAV per share and the value of the preferred shares is the liquidation preference):

| • | Common shares of the combined company representing approximately 80% of total shareholder value |

| • | Preferred shares of the combined company representing approximately 20% of total shareholder value |

| – | Listing:After the mergers and recapitalization, the combined company intends to list its common equity on the New York Stock Exchange, subject to market conditions and board approval. |

| 2. | What is the purpose of the staged liquidity plan? |

| • | We believe the staged liquidity plan provides FS/KKR Advisor, LLC (the “Adviser”) and the board with the flexibility to pursue the optimal liquidity event for shareholders following the closing of the mergers and the recapitalization based on, among other considerations, market conditions, public BDC valuations and the combined company’s performance. |

| • | The liquidity plan is intended to maximize shareholder value, diversify the combined company’s portfolio, align the dividend of the combined company’s common stock to be competitive in the public market, and manage the key risks of a public listing. The strategic rationale for each stage of the liquidity plan is as follows. |

MERGERS

| – | Create significant scale and visibility for public marketsas the combined company will rank as the second-largest BDC, with over $9 billion in assets on a pro forma basis as of March 31, 2019. |

| – | Ensure shareholders receive equal value |

| • | Shareholders of the Acquired Funds will be entitled to receive equal value of shares of FSIC II’s common stock based on the NAV of FSIC II and the NAV of the respective Acquired Fund, less merger-related expenses, special distributions and other adjustments. |

| • | The number of FSIC II common shares to be issued to shareholders of the Acquired Funds will be based on an exchange ratio, equal to the NAV per share of the respective Acquired Fund’s common stock divided by the NAV per share of FSIC II’s common stock. |

| • | The exchange ratio will be calculated within 48 hours (excluding Sundays and holidays) of the closing date of the mergers. |

| – | Enhance portfolio diversification |

| • | The pro forma portfolio will be composed of 208 portfolio companies across 20 industries as of March 31, 2019. |

| • | The pro forma portfolio reduces the percentage of fair value represented by the top 10 portfolio companies from as high as 35.7% for FSIC III to 28.2% on a pro forma basis as of March 31, 2019. |

| • | In addition, the mergers are expected to reduce single issuer concentration, which would help limit the impact of a single investment’s performance on the total portfolio. |

| • | The combined company’s investment objectives and strategy will be consistent with the existing strategy of the Acquired Funds, which seek to generate income and, to a lesser extent, capital appreciation by investing in floating rate, senior secured debt of private U.S. middle market companies. |

| – | Reduce expenses: |

| • | The mergers are expected to create operational synergies as the combined company’s fixed costs will be spread across a larger asset base, and duplicative fixed costs (e.g., administrative, regulatory, and other professional services expenses) will be eliminated. |

| • | As a result, although certain one-time costs will be borne by the funds in connection with the mergers, the annual operating expense borne by the shareholders of the funds as a percentage of assets is expected to be reduced in part due to the reduction in general and administrative expenses. |

2

| • | The mergers are expected to result in approximately $11 million in annual cost savings for the combined entity. |

| • | In addition, the mergers are expected to help reduce the combined company’s cost of borrowing by consolidating existing facilities, leveraging scale to reduce borrowing costs and by potentially accessing debt capital markets as a publicly traded company. |

RECAPITALIZATION

| – | Assuming the board of the combined company approves the recapitalization, shareholders of the funds would hold approximately 80% of their premerger value in common shares of the combined company and approximately 20% in preferred shares (assuming the value of the common shares is the NAV per share and the value of the preferred shares is the liquidation preference). |

| – | The recapitalization is intended to achieve the following: |

| • | Provide current income:The preferred shares are expected to carry an annual preferred dividend of 5.5% and are paid ahead of dividends on common shares. |

| • | Align the combined company’s distribution yield with the public markets:The combined company is expected to be able to sustain up to a 9%–10% annualized dividend yield on NAV for its common shares, which is highly competitive with some of the largest publicly traded BDCs with a track record of consistently covering their distribution.1 |

| • | Ensure sustainable, competitive distribution: At a 9-10% dividend yield, the combined company’s projected annualized net investment income is estimated to represent 105%–110% of its dividend compared to approximately 90%–100% without the recapitalization. |

| – | Publicly traded BDCs that have a track record of consistently funding their distributions through net investment income typically trade at a higher valuation(price-to-book) than their peers. |

| • | Help mitigate selling pressure at listing:The preferred shares are not expected to have an active secondary market at issuance. We expect the illiquid nature of the preferred shares will help reduce the float of the common stock at listing and, therefore, help preserve shareholder value. |

1. Assumes 20% of shareholder value is in preferred shares following the recapitalization, the preferred shares have a 5.5% dividend and the combined company pays aggregate annualized distributions on its common shares that are equal to 80% of FSIC II’s aggregate annualized distributions on common shares as of March 31, 2019. Based on FSIC II’s Q1 2019 distribution and yield on common shares based on NAV as of March 31, 2019.

3

Indicative terms of the preferred shares:

| Preferred dividend | 5.5%; cumulative (must be paid prior to common stock dividends) | |

| Issuance | Following the mergers and prior to the listing of the combined company’s common stock | |

| Amount | 40M shares ($1 billion in liquidation preference) | |

| Listing | Subject to market conditions after the listing of the combined company’s common stock | |

| Maturity | Perpetual | |

| Liquidation preference | $25.00 per share | |

LISTING

| – | Flexibility to select optimal path to liquidity:We expect to list the combined company’s common stock on the New York Stock Exchange following the closing of the mergers and the recapitalization. Prior to a listing, the Adviser and the board will take into account, among other considerations, the combined company’s performance, market conditions and the valuations of publicly traded BDC peers. |

| • | If the Adviser and board determine that a listing would not be in the best interests of shareholders at such time due to any of the aforementioned factors or any other factors, the staged liquidity plan ensures that the combined company is not “forced” to list the combined company’s common stock into potentially unfavorable market conditions. |

| • | Furthermore, the timing of a liquidity event will not impact the expected benefits of the mergers, including enhanced portfolio diversification and the reduction of expenses of the combined company. |

| – | A single transaction, consisting of allnon-traded BDCsmanaged by the Adviser, eliminates the uncertainty of the timing and impact of future mergers on shareholder value. |

3. As an investor, what do I need to do next?

| • | There is no immediate action necessary. Investors are urged to review documents that the funds will file with the Securities and Exchange Commission, including a registration statement on FormN-14, which will include a joint proxy statement of the funds that will also be posted atwww.fsinvestments.com. |

4

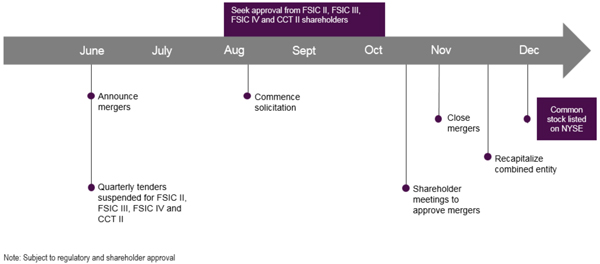

| 4. | What is the expected timeline for the proposed staged liquidity plan? |

| 5. | Will FSIC II, FSIC III, FSIC IV and CCT II conduct quarterly tender offers prior to the mergers? |

| • | In connection with the announced agreement and plan of merger, and in accordance with federal securities laws and regulatory guidance, the quarterly tender offers of FSIC II, FSIC III, FSIC IV and CCT II will be suspended effective immediately. |

Merger Q&A

| 6. | Why is FSIC II the surviving entity? |

| • | With over $4.8 billion in assets based on fair value as of March 31, 2019, FSIC II is the largest of the non-traded funds managed by the Adviser. |

| • | FSIC II launched in June 2012 and, therefore, has the longest performance track record among the non-traded funds. We believe a long track record will help garner attention from new potential institutional investors upon a listing. |

| 7. | Why not merge FSIC II, FSIC III, FSIC IV and CCT II into FS KKR Capital Corp. (“FSK”)? |

| • | We do not believe a merger into FSK would maximize shareholder value for the non-traded shareholders as FSK’s common stock currently trades at a discount to book value. |

| • | In addition, the merger of the non-traded funds into FSK could create technical pressure on the price of FSK’s common stock upon a merger, which could further reduce the value of FSK shares to non-traded shareholders. |

| 8. | Will the Acquired Funds shareholders receive special distributions in connection with the mergers? |

| • | Upon or prior to closing the mergers, each of the Acquired Funds will declare a distribution to its shareholders representing any undistributed net investment income and net realized capital gains. |

5

| 9. | Are the mergers expected to be taxable to FSIC II shareholders? |

| • | No. The mergers are not expected to be a taxable event for FSIC II shareholders. |

| 10. | Are the mergers expected to be taxable to FSIC III, FSIC IV or CCT II shareholders? |

| • | No. Each merger is intended to qualify as tax-free for U.S. federal income tax purposes, and it is a condition to the funds’ respective obligations to complete the applicable merger that each of them receives a legal opinion to that effect. |

| • | Shareholders of the Acquired Funds are not expected to recognize any gain or loss for U.S. federal income tax purposes on the exchange of their shares of FSIC III, FSIC IV or CCT II for shares of FSIC II pursuant to the mergers. |

| • | Tax matters can be complicated, and the tax consequences of the mergers to an FSIC II, FSIC III, FSIC IV or CCT II shareholder will depend on the particular tax situation of such shareholder. Shareholders should review carefully the joint proxy statement of the funds when it becomes available for more information and details as to the tax consequences of the mergers to FSIC II, FSIC III, FSIC IV and CCT II and their shareholders. Shareholders should consult with their own tax advisors to determine the tax consequences of the merger. |

| 11. | Will any other BDCs managed by FS Investments or KKR be a party to the merger? |

| • | No. The merger proposal is for only the non-traded BDCs managed by the Adviser. |

Recapitalization Q&A

| 12. | Will investors be able to redeem their preferred shares? |

| • | We expect to list the combined company’s preferred shares on the New York Stock Exchange at a future point following the listing of the combined company’s common stock. Timing is subject to market conditions and other considerations. |

| • | We do not expect an active secondary market will exist for the combined company’s preferred shares prior to a listing. |

| 13. | Will investors be able to transfer ownership of their preferred shares? |

| • | The preferred shares will not be registered at the time of issuance. Therefore, the preferred shares may only be resold pursuant to registration under the Securities Act of 1933, as amended, or a valid exemption from registration. |

| 14 | How frequently will the preferred shares pay dividends? |

| • | Dividends will generally be payable quarterly on January 31, April 30, July 31 and October 31 as declared by the combined company’s board. |

| • | The combined company cannot declare or pay distributions on its common shares unless the distributions have been declared and paid on the preferred shares. |

6

| 15. | What is the expected tax treatment of the dividend on the preferred shares? |

| • | We expect the dividends on the preferred shares will be reported as ordinary income on Form1099-DIV. |

| 16. | How will the combined company account for the preferred shares on its balance sheet? |

| • | The combined company will hold the preferred shares at its liquidation preference of $25 per share. |

| 17. | How was the anticipated distribution rate for the preferred shares determined? |

| • | Together with the Adviser, the funds’ boards and their financial advisor conducted a comprehensive competitor and market review. |

| • | While there are limited comparables in the BDC sector, there is awell-developed and liquid market for $25 par preferred stock securities, including in the property REIT and mortgage REIT sectors. The analysis covered a broad range of issuers as well as structures, including fixed and floating rate securities, and issuance sizes. |

| • | The combined company’s expected distribution rate takes into account the results of the competitor analysis as well as the preferred dividend required to achieve the objective of aligning the dividend yield on the combined company’s common shares to a competitive level with “Tier 1” publicly traded BDCs. |

| 18. | When does the Adviser anticipate listing the preferred equity? |

| • | The board and Adviser intend to list the preferred shares following the listing of the combined company’s common equity as soon as the Adviser and board believe market conditions support a listing. |

| • | Among other considerations in determining the timing of the listing, the Adviser and the board will take into account the performance of the combined company’s stock price with the goal to mitigate technical pressure on the stock. |

Listing Q&A

| 19. | Once listed, how will the combined company differ from FSK? |

| • | While FSK and the combined company share a common investment adviser and investment strategy focused on investing in the floating rate, senior secured debt of private upper middle market U.S. companies, the portfolios today differ in the following ways: |

– Portfolio allocations:

| • | The combined company’s combined portfolio is expected to have a higher allocation to first lien debt (74%) compared to FSK (54%). Senior secured debt will represent 81% of the combined portfolio compared to 72% for FSK based on fair value as of March 31, 2019. |

| • | In addition, given the merger of FS Investment Corporation (FSIC) and Corporate Capital Trust (CCT) in December 2018 to create FS KKR Capital Corp., FSK’s portfolio has a |

7

| higher concentration ofKKR-originated investments compared to the combined company, representing 59% and 25% of the portfolios, respectively, based on fair market value as of March 31, 2019. (Note: CCT wassub-advised by KKR Credit since its inception in 2011 until April 2018.) |

– Issuer sizing:

| • | While the estimated overlap between FSK and the combined company is approximately 80% based on fair market value as of March 31, 2019, the position sizes may differ significantly between the funds. |

| • | Therefore, the performance of any single overlapping investment can have a varying impact on the portfolios. |

– Capital structure:

| • | As a publicly traded stock, FSK has greater access to the debt capital markets. As of March 31, 2019, FSK had $1.3 billion in unsecured, fixed rate debt outstanding. |

| • | Approximately 39% of FSK’s borrowings are fixed rate based on principal outstanding as of March 31, 2019. The combined company’s borrowings are 100% floating rate term facilities. |

| • | In addition, the combined company’s preferred share issuance will be differentiated in the public BDC market. |

| 20. | Is thelong-term plan to merge FSK and the combined company? |

| • | We believe having two separate publicly traded vehicles is in the best interest of both sets of shareholders at this time. |

| • | While we would expect the portfolios and capital structures of FSK and the combined company to converge over time, our focus is on executing the merger and staged liquidity plan of the non-traded funds. |

| • | The Adviser and board may evaluate a future potential merger if they believe it is in the best interest of shareholders. |

| • | Any merger of FSK and the combined company would be subject to board and shareholder approval. |

| 21. | Will FSK and the combined company have separate boards? |

| • | The boards of FSK, FSIC II, FSIC III and FSIC IV are currently composed of the same members. The boards of FSK and the combined company will continue to be composed of the same members. |

8

Proxy Q&A

| 22. | Will there be a meeting for shareholders to vote on the proposals related to mergers? |

| • | Shareholders will be asked to approve proposals related to the mergers at the respective fund’s annual meeting, which we expect to occur in the third or fourth quarter of 2019. |

| 23. | What vote is required by shareholders to approve the mergers? |

| • | For each fund, the approval of the merger and related proposals will require the affirmative vote of shareholders owning more than 50% of each fund’s outstanding common stock. |

| 24. | Will the funds incur expenses in soliciting proxies? |

| • | The expenses of the solicitation of proxies for the annual meetings of FSIC II, FSIC III, FSIC IV and CCT II, including the cost of preparing, printing and mailing the joint proxy statement/prospectus, the applicable accompanying notice of the annual meeting of shareholders and the proxy card, will be borne pro rata based on assets under management. |

| • | FSIC II, FSIC III, FSIC IV and CCT II have each retained Broadridge Investor Communication Solutions, Inc. to assist in the solicitation of proxies. |

Distributions Q&A

| 25. | What is the expected quarterly distribution of the combined company? |

| • | Subject to the closing of the merger, we expect the board to declare distributions for the combined company. |

| • | Assuming the closing of the merger and recapitalization, we expect that the annualized blended distribution amount of the common shares and preferred shares may be lower than the current annualized distribution amount for FSIC II and FSIC III shareholders. |

| • | However, we anticipate that the issuance of the preferred shares will help improve the combined entity’s distribution coverage to a competitive level with some of the largest BDCs in the market. |

| • | Since public markets generally assign a higher valuation to BDCs with strong distribution coverage, we view the issuance of the preferred shares as a critical step toward preparing the common shares for a public listing. |

| • | Finally, we expect that the annualized blended distribution amount of the common shares and preferred shares will be higher than the annualized distribution rate for FSIC IV and CCT II investors. |

| 26. | Will the funds continue to pay monthly distributions until the closing of the merger? |

| • | We currently expect each fund will continue to pay monthly distributions. |

9

Fees & expenses Q&A

| 27. | What will be the investment advisory fees of the combined company? |

| • | In connection with the approval of the mergers, the board of FSIC II approved an amended investment advisory agreement, which will be submitted to shareholders for approval. |

| • | Base management fee:Under the current investment advisory agreement, the base management fee is calculated at an annual rate of 1.5% of the average weekly value of FSIC II’s gross assets. Under the amended investment advisory agreement, cash and cash equivalents will be excluded from the gross assets on which the base management fee is calculated, and the base management fee will be reduced from 1.5% to 1.0% on all assets financed using leverage over 1.0xdebt-to-equity. |

| • | Subordinated incentive fee on income:Under the current investment advisory agreement, the subordinated incentive fee on income is subject to a quarterly hurdle rate expressed as a rate of return on adjusted capital as of the most recently completed calendar quarter of 1.75% (7.0% annualized), subject to a “catch-up” equal to the amount of FSIC II’s pre-incentive fee net investment income in excess of the hurdle rate until FSIC II’s pre-incentive fee net investment income for such quarter equals 2.1875% (or 8.75% annually) (the “Hurdle Rate”). Under the amended investment advisory agreement, the Hurdle Rate will be calculated on net assets rather than adjusted capital. In addition, under the amended investment advisory agreement, the definition of pre-incentive fee net investment income will exclude any interest expense or dividends paid on any issued and outstanding shares of preferred stock created through a reclassification of common stock or due to a distribution in kind to holders of common stock. |

| • | New cap on subordinated incentive fee on income:Under the current investment advisory agreement, there is no“look-back” or cap feature on the subordinated incentive fee on income. Under the amended investment advisory agreement, commencing with the ninth full fiscal quarter following the closing of the mergers, the subordinated incentive fee on income will be subject to a cap equal to (a) (i) 20% of the per share pre-incentive fee return for the current fiscal quarter and the 11 fiscal quarters (or fewer number of fiscal quarters) preceding the current fiscal quarter (commencing with the first full fiscal quarter following the mergers) less (ii) the cumulative per share incentive fees accrued and/or payable for the 11 fiscal quarters (or fewer number of fiscal quarters) preceding the current fiscal quarter (commencing with the first full fiscal quarter following the mergers) multiplied by (b) the weighted average number of outstanding shares of common stock of the combined company during the applicable fiscal quarter. |

| • | Incentive fee on capital gains:The current investment advisory agreement does not expressly provide for taking into account the historical net realized losses and unrealized depreciation of any merging entity, essentially forgiving them. The amended investment advisory agreement will ensure that aggregate historical net realized losses and unrealized depreciation of each of FSIC III, FSIC IV and CCT II are offset by capital gains before the Adviser will receive payment of incentive fees on capital gains. |

10

| 28. | Who can I contact with any additional questions? |

ADVISORS AND RETAIL INVESTORS

877-628-8575

MEDIA (FS INVESTMENTS)

Melanie Hemmert,media@fsinvestments.com,215-309-6843

MEDIA (KKR)

Kristi Huller or Cara Kleiman Major,media@kkr.com,212-750-8300

Forward-Looking Statements

Statements included herein may constitute “forward-looking” statements as that term is defined in Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended by the Private Securities Litigation Reform Act of 1995, including statements with regard to future events or the future performance or operations of FS Investment Corporation II, FS Investment Corporation III, FS Investment Corporation IV and Corporate Capital Trust II (collectively, the “Funds”). Words such as “believes,” “expects,” “projects,” and “future” or similar expressions are intended to identify forward-looking statements. These forward-looking statements are subject to the inherent uncertainties in predicting future results and conditions. Certain factors could cause actual results to differ materially from those projected in these forward-looking statements. Factors that could cause actual results to differ materially include changes in the economy, risks associated with possible disruption to a Fund’s operations or the economy generally due to terrorism or natural disasters, future changes in laws or regulations and conditions in a Fund’s operating area, failure to obtain requisite shareholder approval for the Proposals (as defined below) set forth in the Proxy Statement (as defined below), failure to consummate the business combination transaction involving the Funds, uncertainties as to the timing of the consummation of the business combination transaction involving the Funds, unexpected costs, charges or expenses resulting from the business combination transaction involving the Funds, failure to realize the anticipated benefits of the business combination transaction involving the Funds, failure to consummate the recapitalization transaction and failure to list the common stock of the combined entity on a national securities exchange. Some of these factors are enumerated in the filings the Funds made with the Securities and Exchange Commission (the “SEC”) and will also be contained in the Proxy Statement when such document becomes available. The inclusion of forward-looking statements should not be regarded as a representation that any plans, estimates or expectations will be achieved. Any forward-looking statements speak only as of the date of this communication. Except as required by federal securities laws, the Funds undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. Readers are cautioned not to place undue reliance on any of these forward-looking statements.

Additional Information and Where to Find It

This communication relates to a proposed business combination involving the Funds, along with related proposals for which shareholder approval will be sought (collectively, the “Proposals”). In connection with the Proposals, the Funds intend to file relevant materials with the SEC, including a registration statement on FormN-14, which will include a joint proxy statement of the Funds and a

11

prospectus of FSIC II (the “Proxy Statement”). This communication does not constitute an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote or approval. No offer of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act. SHAREHOLDERS OF THE FUNDS ARE URGED TO READ ALL RELEVANT DOCUMENTS FILED WITH THE SEC, INCLUDING THE PROXY STATEMENT WHEN IT BECOMES AVAILABLE, AS WELL AS ANY AMENDMENTS OR SUPPLEMENTS THERETO, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT THE FUNDS, THE BUSINESS COMBINATION TRANSACTION INVOLVING THE FUNDS AND THE PROPOSALS. Investors and security holders will be able to obtain the documents filed with the SEC free of charge at the SEC’s website,www.sec.gov, or from the Funds’ website atwww.fsinvestments.com.

Participants in the Solicitation

The Funds and their respective directors and trustees, executive officers and certain other members of management and employees, including employees of FS/KKR Advisor, LLC, Franklin Square Holdings, L.P. (which does business as FS Investments), KKR Credit Advisors (US) LLC and their respective affiliates, may be deemed to be participants in the solicitation of proxies from the stockholders of the Funds in connection with the Proposals. Information regarding the persons who may, under the rules of the SEC, be considered participants in the solicitation of the Funds’ stockholders in connection with the Proposals will be contained in the Proxy Statement when such document becomes available. This document may be obtained free of charge from the sources indicated above.

12