UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-23146

Natixis ETF Trust

(Exact name of Registrant as specified in charter)

888 Boylston Street, Suite 800 Boston, Massachusetts 02199-8197

(Address of principal executive offices) (Zip code)

Susan McWhan Tobin, Esq.

Natixis Distribution, LLC

888 Boylston Street, Suite 800

Boston, Massachusetts 02199-8197

(Name and address of agent for service)

Registrant’s telephone number, including area code: (617) 449-2139

Date of fiscal year end: December 31

Date of reporting period: December 31, 2023

Item 1. Reports to Stockholders.

| (a) | The Registrant’s annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 is as follows: |

Annual Report

December 31, 2023

Natixis Gateway Quality Income ETF |

Natixis Loomis Sayles Focused Growth ETF |

Natixis Loomis Sayles Short Duration Income ETF |

Natixis Vaughan Nelson Mid Cap ETF |

Natixis Vaughan Nelson Select ETF |

IMPORTANT NOTICE TO SHAREHOLDERS

The Securities and Exchange Commission (SEC) has adopted new regulations that will result in changes to the design and delivery of annual and semiannual shareholder reports. Beginning in July 2024, Funds will be required by the SEC to send shareholders a paper copy of a new tailored shareholder report in place of the full shareholder report that is currently being provided. If you would like to receive shareholder reports and other communications from the Funds electronically, instead of by mail, you may make that request at www.icsdelivery.com/natixisfunds. If you have already elected to receive shareholder reports electronically, you will not be affected by this change, and you need not take any action.

Natixis Gateway Quality Income ETF

|

|

|

|

|

Gateway Investment Advisers, LLC

|

Investment GoalThe Fund seeks to deliver current income while maintaining prospects for capital appreciation.

Market Conditions

The S&P 500® Index returned 7.50%, 8.74%, -3.27%, and 11.69% in the first, second, third, and fourth quarters of 2023, respectively. Despite significant turmoil and growing global conflict, the year was all about the US Federal Reserve (Fed) and expectations surrounding the path of monetary policy. Investors attempted to predict the direction of Fed decisions and, most importantly, the level and pace of interest rate increases. After record inflation and negative equity markets in 2022, signs of softening inflation in January 2023 helped the S&P 500® Index climb 8.98% from January 1 to February 2, 2023. Sudden tumult from a regional bank crisis contributed to a 7.53% decline in the S&P 500® Index from February 2 to March 13. As confidence in the financial system showed signs of deterioration, the Fed enacted emergency measures which relieved investor concerns and fueled a 19.72% rally in the S&P 500® Index from March 13 to July 31. Last-minute US debt ceiling negotiations triggered a surprise credit downgrade by Fitch Ratings and a second wave of regional bank downgrades. The burst of uncertainty contributed to a 9.94% equity market decline from the end of July to October 27. As inflation continued to ease, a less-hawkish tone from the Fed kicked off a 16.23% market advance from October 27 through year-end.

With a significant equity market advance during 2023, implied volatility drifted lower, as expected. Implied volatility, as measured by the Cboe® Volatility Index (the VIX®), ended 2022 at 21.67 and averaged 16.85 during 2023. Consistent with its typical relationship, average implied volatility exceeded realized volatility, as measured by the standard deviation of daily returns for the S&P 500® Index, which was 13.10% for the year. The Volatility Risk Premium, or the difference between the two volatility measures, was positive throughout the year and averaged 4.19% in 2023, above its average of 4.08% since 1990. The VIX® spent most of 2023 ranging from the mid-teens to the mid-20s, closing above its long-term average of 19.58 for more than 20% of the year. The VIX® reached an intra-year high of 26.52 on March 13 at the height of the banking crisis before settling into a quiet summer supported by a rapid equity market advance and growing investor optimism surrounding the direction of monetary policy. The selloff from July 31 through October 27 drove the measure above summer lows, reaching a fourth quarter high of 21.71 on October 20. Implied volatility through the end of 2023 was stifled as hopes grew for an extended pause, or even a cut, in interest rates. The VIX® reached an intra-year low of 12.07 on December 12 and ended 2023 at 12.45.

Performance Results

Since the December 13, 2023 inception through December 31, 2023, the Natixis Gateway Quality Income ETF returned 1.97% at net asset value. The Fund underperformed its benchmark, the S&P 500® Index, which returned 2.79% for the same period.

Explanation of Fund Performance

The Fund invests in a diversified portfolio of high-quality US common stocks and combines it with the characteristics of an options selling overlay program designed to provide consistent cash flow to support a monthly distribution, enhance return, and reduce downside risk. High-quality companies offer the potential to benefit from rising equity markets while also providing protection during times of uncertainty. Over the long-term, a quality focus can provide a robust risk and return profile relative to other factors and lead to outperformance relative to the broad market. The Fund’s equity portfolio is driven by a focus on key fundamental variables and invests in firms exhibiting consistent quality factors. The Fund uses equity-linked notes (ELNs) to replicate the performance of selling index covered call options on a portion of the underlying equity portfolio. This combination helps drive monthly income, enhances yield, and reduces volatility. The options overlay covers 50% of the equity portfolio to provide investors with consistent income and monthly payouts. The remaining 50% of the equity portfolio is uncovered to provide unhedged market exposure. This approach balances long-term growth with monthly income.

The cash flow generated by the strategy is a factor of the level of participation the strategy has in a rising equity market and how much protection is provided in a falling market. The amount of cash flow available to the strategy varies with the amount of implied

Natixis Gateway Quality Income ETF

volatility priced into the index options market, with higher volatility generally resulting in more cash flow while lower implied volatility generally results in less cash flow.

The Fund underperformed its benchmark since its inception on December 13, 2023 through year-end. The Fund’s equity portfolio returned 2.28% during this period, a performance differential of negative 0.51% versus the S&P 500® Index. With no maturities during the reporting period, the ELN portion of the Fund performed as expected. The measured risk of the Fund, as measured by the standard deviation of daily returns for this period, was 8.49% versus 11.08% for the S&P 500® Index.

Outlook

The Federal Funds Effective Rate (Fed Funds Rate) was increased seven times during 2022, ratcheting from 0.07% to 4.33%. With a significant departure from the quantitative easing approach of the prior decade or more, the consensus was that the Fed had been too aggressive and risked pushing the US economy into recession. Amidst progress against inflation paired with an impressively resilient economy and labor market, the Fed’s tone turned less hawkish as the year progressed and led to a pause in the rate hiking cycle. Ultimately, the Fed Funds Rate climbed to 5.33% in July 2023 and was held steady through year-end. Bond yields are higher than prior to the Global Financial Crisis but only time will tell if current yields will be overwhelmed by lower-but-persistent inflation or be sufficient compensation for the potential loss of principle if the Fed’s tightening cycle resumes.

There are growing expectations of interest rate cuts in 2024 and some market participants may view such a reversal as a potentially bullish development. The historical record is not so sanguine as the effects of monetary policy tend to lag policy action and create significant uncertainty. On average, the equity market advanced 5.1% in the one-year period following an interest rate cut, although investors had to withstand significant drawdowns and increased volatility along the way.

While it’s impossible to predict market performance in 2024, a review of the last 25 years shows that the equity market has climbed more than 20% in eight of those years. In the year following those advances, average returns were just 3.8%. Positive, but hardly as exciting as 2023’s results. With ample drivers of volatility on the horizon – such as the US presidential election, geopolitical uncertainty, and ongoing wars – risk management may be prudent.

If current levels of volatility and interest rates persist, or move higher, option writing premiums may continue to be an effective source of cash flow. Whether the Fed resumes rate hikes, holds steady, or even cuts rates, investment strategies that combine high-quality equity market exposure with cash flow from writing index options may benefit from relatively higher levels of interest rates and implied volatility. Quality investing paired with robust cash flow from option writing seeks to provide attractive return potential during market advances and attractive downside protection potential in market declines.

Top Ten Holdings as of December 31, 2023 |

| |

| |

| |

3 Alphabet, Inc., Class A | |

| |

5 Canadian Imperial Bank of Commerce, (S&P 500 Index) | |

6 Morgan Stanley Finance LLC, (S&P 500 Index) | |

7 BNP Paribas Issuance BV, (S&P 500 Index) | |

8 UBS AG, (S&P 500 Index) | |

| |

10 Mastercard, Inc., Class A | |

The portfolio is actively managed and holdings are subject to change. There is no guarantee the Fund continues to invest in the securities referenced. The holdings listed exclude any temporary cash investments, are presented on an individual security basis and do not represent holdings of the issuer. |

Natixis Gateway Quality Income ETF

Total Returns —December 31, 20231 |

| Life of Fund (Inception 12/13/23) | |

| | |

| | | |

| | | |

| | | |

| | | |

Performance data shown represents past performance and is no guarantee of, and not necessarily indicative of, future results. Total return and value will vary, and you may have a gain or loss when shares are sold. Current performance may be lower or higher than quoted. For most recent month-end performance, visit im.natixis.com/performance. You may not invest directly in an index. Performance for periods less than one year is cumulative, not annualized. Returns reflect changes in share price and reinvestment of dividends and capital gains, if any. The table(s) do not reflect taxes shareholders might owe on any fund distributions or when they redeem their shares.

| Fund performance has been increased by fee waivers and/or expense reimbursements, if any, without which performance would have been lower. |

| Expense ratios are as shown in the Fund’s prospectus in effect as of the date of this report. The expense ratios for the current reporting period can be found in the Financial Highlights section of this report under Ratios to Average Net Assets. Net expenses reflect contractual expense limitations set to expire on 4/30/26. When a Fund’s expenses are below the limitation, gross and net expense ratios will be the same. See Note 6 of the Notes to Financial Statements for more information about the Fund’s expense limitations. |

| The NAV return is based on the NAV of the Fund, and the market return is based on the market price per share of the Fund, which is determined by using the midpoint between the highest bid and the lowest offer on the primary stock exchange on which shares of the Fund are listed for trading, as of the time that the Fund’s NAV is calculated. 12/13/23 represents the date trading of Fund shares commenced on the secondary market. 12/12/23 represents commencement of operations for accounting and financial reporting purposes only. NAV is used as a proxy for the opening market price on 12/13/23. Market and NAV returns assume that dividends and capital gain distributions have been reinvested in the Fund at market price and NAV, respectively. |

| S&P 500® Index is a widely recognized measure of U.S. stock market performance. It is an unmanaged index of 500 common stocks chosen for market size, liquidity, and industry group representation, among other factors. It also measures the performance of the large cap segment of the U.S. equities market. |

Natixis Loomis Sayles Focused Growth ETF

|

|

Loomis, Sayles & Company, L.P.

|

Investment GoalThe Fund's investment objective is long-term growth of capital.

Market Conditions

The US equity market overcame a number of potential headwinds to post a robust total return in 2023. The interest-rate outlook was a key driver of volatility throughout the year, as the US Federal Reserve (Fed) continued to raise rates—albeit at a slower pace than in 2022—to combat inflation. This issue became more prominent in late summer and early autumn, when rising energy prices fueled concerns that persistent inflation could compel the Fed to keep rates “higher for longer.” The backdrop changed considerably in the fourth quarter, however, thanks to a series of cooler-than-expected inflation reports. In addition, Fed Chairman Jerome Powell surprised the markets in December by indicating that the central bank was likely finished raising rates and possibly on track to begin enacting rate cuts in 2024. Not least, it appeared that GDP growth would remain in positive territory and allow the Fed to achieve the ideal outcome of a “soft landing” for the economy. Stocks surged in response, bringing most major large-cap indexes to near all-time highs by year-end.

The late rally was broad-based, with strong participation from market segments—including the value style, small caps, and mid caps—that had underperformed for most of 2023. Despite this shift, growth stocks were the key source of market leadership over the full year. Mega-cap technology-related companies produced particularly impressive gains that were fueled, in part, by excitement about the long-term prospects for artificial intelligence. On the other hand, the more traditionally defensive segments of the market lagged.

Performance Results

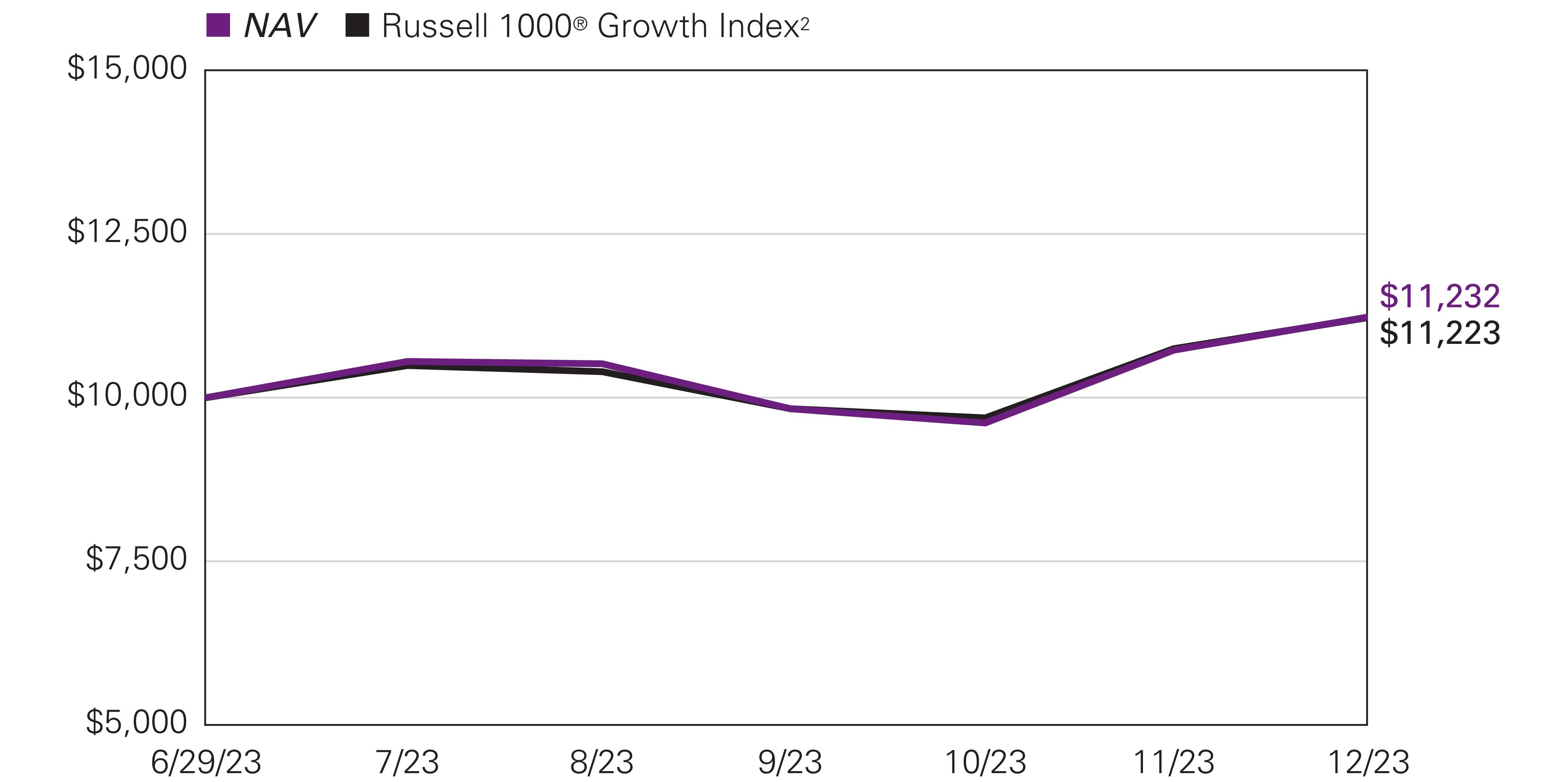

The Natixis Loomis Sayles Focused Growth ETF was launched on June 29, 2023. For the period ended December 31, 2023, shares of the Fund returned 12.31% at net asset value. The Fund outperformed its benchmark, the Russell 1000® Growth Index, which returned 12.23%.

Explanation of Fund Performance

We are an active manager with a long-term, private equity approach to investing. Through our proprietary bottom-up research framework, we look to invest in those few high-quality businesses with sustainable competitive advantages and profitable growth when they trade at a significant discount to intrinsic value. Given the rare confluence of quality, growth, and valuation, we may study dozens of companies but may only invest in a select few businesses each year. We believe identifying those few businesses with such characteristics is an art, not a science. As a result of this rigorous approach, ours is a selective, high-conviction portfolio of typically 20–30 stocks.

The Fund’s positions in Meta Platforms, Nvidia, and Amazon contributed the most to performance. Stock selection in the industrials, information technology, and financials sectors, along with our allocation in the communication services sector, contributed positively to relative performance.

Meta Platforms operates online social networking platforms that allow people to connect, share, and interact with friends and communities. With 3.9 billion monthly users, 200 million businesses, and 10 million advertisers worldwide using its family of apps – Facebook, Messenger, WhatsApp, and Instagram – we believe the scale and reach of Meta’s network is unrivaled. A Fund holding since inception, Meta’s shares rebounded substantially in 2023 after being under pressure throughout most of 2022 due to a perceived lack of discipline in the company’s capital expenditures – especially with respect to the metaverse – that coincided with what we believed was temporary fundamental weakness arising from the company’s transition to a new advertising format and maneuvering around privacy changes imposed by Apple in 2021. Our analysis suggested that Meta was being priced as if a high-quality, high-returning, growth company – whose returns on capital were many times larger than its cost of capital – would become a low-quality business that both ceased to grow and would also see its margins and returns on invested capital deteriorate. Despite ongoing macroeconomic pressure on advertising spending, during the reporting period Meta, posted consecutive quarters of better-than-expected financial results, including accelerating revenue growth as it made further progress in navigating Apple’s privacy changes and saw improved monetization of its newest Reels video format. Earlier in the year, Meta announced a set of efficiency measures that have already led to significant improvements in margins and lower capital expenditure plans, and shares responded positively to the company’s increased focus on productivity and cost management. We believe founder and CEO Mark Zuckerberg has always managed

Natixis Loomis Sayles Focused Growth ETF

the company with a long-term focus and strong strategic vision. Over the past ten years, Meta has spent over $125 billion on research and development and $110 billion on capital expenditures – a level of investment that few firms can match, and which creates high barriers to entry for competitors that are further buttressed by the growth of cumulative knowledge over time. The successful development of a metaverse is not an explicit part of our investment thesis for Meta. However, given the potential size of the opportunity, which we estimate could impact over $1 trillion of spending over the long term, and Meta’s positioning with billions of users and hundreds of millions of businesses, we believe Meta’s current balanced approach to its forward-looking investments make sense. We expect that corporations will continue to allocate an increasing proportion of their advertising spending online, and Meta remains one of very few platforms where advertisers can reach consumers at such scale in such a targeted and effective fashion. We believe Meta’s brands, network, and targeting advantage position the company to take increasing share of the industry’s profit pool and grow its market share from approximately 6% currently to approximately 10% of the total global advertising market over our investment time horizon. On the basis of its core business alone, we believe the company is substantially undervalued and trades at a significant discount to our estimate of intrinsic value.

Nvidia is the world leader in artificial intelligence (AI) computing, which enables computers to mimic human-like intelligence for problem solving and decision-making capabilities. We believe the company’s competitive advantages include its intellectual property, brands, and a large and growing ecosystem of developers and applications utilizing its GPU (graphics processing unit) technology. A Fund holding since inception, Nvidia reported record financial results during the period that were well above consensus expectations, as AI applications, including generative AI, are driving strong demand for GPUs by companies looking to leverage these capabilities and drive competitive differentiation. Revenue in the company’s gaming segment had been depressed, which we believe reflected global demand for PCs returning to pre-pandemic levels after a period of excess and the impact of Covid restrictions on China consumer spending. However, we believe the company has worked expeditiously in clearing existing inventory in its retail channels, which contributed to the gaming business returning to growth in the most recent two quarters. In its data center business, we believe Nvidia’s decades of focused investment, cumulative know-how, and robust software platform and architecture that has attracted millions of developers position the company to benefit from several secular long-term growth drivers, including continued growth in use cases for artificial intelligence. To further drive adoption by enterprises, Nvidia is also partnering with cloud service providers including Oracle, Microsoft, and Google to offer AI services via the cloud. We believe Nvidia remains strongly positioned to benefit from secular growth in PC gaming and is still in the early stages of growth in its data center business, which has the potential to be much larger in the long term. We believe Nvidia’s strong growth prospects are not currently reflected in its share price. As a result, we believe the company’s shares are trading at a significant discount to our estimate of intrinsic value, offering a compelling reward-to-risk opportunity.

Online retailer Amazon offers millions of products – sold by Amazon or by third parties – with the value proposition to consumers of selection, price, and convenience. Amazon’s enterprise IT business, Amazon Web Services (AWS), offers a suite of secure, on-demand cloud-computing services, with a value proposition to clients of speed, agility, and savings. In both of its core markets, we believe Amazon possesses strong and sustainable competitive advantages that would be difficult for competitors to replicate. A Fund holding since inception, Amazon reported fundamentally solid low-double-digit revenue growth and much higher growth in operating profits that were both above management’s guidance and consensus expectations during the period. Earlier in the year, the company saw a deceleration in growth in AWS as businesses continue to optimize their cloud spending following a period of economic weakness; the trend was also apparent at both Microsoft and Alphabet. During the reporting period, the optimization activity began to stabilize, and Amazon observed companies once again focusing on innovation rather than cost reduction and bringing increasing workloads to the cloud. Over the past few years, Amazon made substantial investments to ensure that its fulfillment and transportation network remained unconstrained during the pandemic. As a result, the company doubled its fulfillment footprint – which took 25 years to build – and built out a transportation network to support last-mile delivery. Given the company’s long-tailed secular growth opportunities, over time we believe it will realize greater productivity and fixed cost leverage from these investments in labor, fulfillment, and distribution. The company showed efficiency gains during the year due in part to its decision to transition away from a national network and towards several smaller regional networks. This resulted in faster and less expensive deliveries and contributed to operating margins expanding by over 400 basis points in each of the past two quarters. However, expense pressures are expected to persist as the company progresses towards full utilization of its new investments. We believe Amazon is one of the best-positioned companies in e-commerce and enterprise IT – in each case addressing large, underpenetrated markets experiencing secular growth that is still in its early stages. We also expect Amazon’s strong position in the e-commerce market to support an emerging advertising business, which has already reached a $44 billion annual revenue run rate. We believe the current share price shows a lack of appreciation for Amazon’s significant long-term growth opportunities and the sustainability of its business model. As a result, we believe the company is selling at a significant discount to our estimate of intrinsic value and offers a compelling reward-to-risk opportunity.

The Fund’s positions in Illumina, Oracle, and Tesla detracted the most from performance. Stock selection in the consumer discretionary, healthcare, information technology, and consumer staples sectors, as well as our allocations in the consumer discretionary and information technology sectors, also detracted from relative performance.

Natixis Loomis Sayles Focused Growth ETF

Founded in 1998, Illumina is the industry leader in the fast-growing field of sequencing for genetic and genomic analysis, supporting research, clinical, and consumer genetics applications. A Fund holding since inception, Illumina’s shares have been under pressure due to lower-than-expected results in its core business, uncertainty regarding its acquisition of GRAIL, and near-term management uncertainty following an activist investor campaign that succeeded in ousting the Chairman of the Board in May and later prompted the resignation of CEO Francis deSouza in June. While orders for its newest sequencing platform, NovaSeq X, had been solid, they slowed in the most recently reported quarter as the company observed a lengthening sales cycle among customers facing macroeconomic pressure – which has similarly impacted peers as well. Still, Illumina’s recent results and guidance are below our long-term expectations as we believe GRAIL has detracted from near-term focus and returns. Illumina acquired GRAIL in August 2021 but closed the transaction prior to receiving approval from the EU, which has since ordered that the business be divested. In December 2023, Illumina announced it will divest GRAIL and aims to have the terms finalized by June 2024. GRAIL is an early leader in asymptomatic cancer screening through liquid biopsies that use Illumina’s sequencing technology to detect tumor DNA in the bloodstream before it could otherwise be sampled via a traditional biopsy. While we believed that there was potential upside in GRAIL, our structural investment thesis for Illumina was not premised on a successful completion of the acquisition, and GRAIL will remain an important customer for the company. We believe the core Illumina business remains highly attractive on a reward-to-risk basis and remains substantially discounted relative to intrinsic value. Illumina is in the early stages of a major platform launch while simultaneously facing more competition than in recent years. Over the last two years, Illumina’s share of industry revenue has dropped from an estimated 80% to 77%. These share losses have been most pronounced in China and in the lower-value, mid- and low- throughput portions of the sequencing market. We anticipate Illumina will retain its dominant share in the high-value, high-throughput ends of the market on the strength of its product ecosystem and continue to capture approximately 75% of the sequencing market. In September, the company named Jacob Thaysen, Ph.D. as its new CEO. Thaysen previously served as President of the Life Sciences and Applied Markets Group at Agilent, and brings a background in research and development (R&D) as well as experience operating in genetics and clinical end market. We met with Thaysen and our interactions have been positive as we believe he has the requisite skills and vision to reinvigorate the core Illumina franchise. We are encouraged that new management seems committed to redoubling its focus on the significant opportunity in Illumina’s core markets and reinvigorating operational execution – which appeared to have diminished over the last several quarters under deSouza. In addition to the activist-sponsored candidate, Illumina also added two new board members with significant experience at innovative, market-expanding healthcare businesses that we believe should contribute positively to Illumina’s return to growth. Despite the near-term uncertainty, we believe Illumina remains advantageously positioned in a high-quality industry benefiting from long-term, secular growth. We believe Illumina is at the forefront of a multi-decade transformation that will see genetic analysis incorporated into multiple facets of our lives. While demand today is still predominantly from large life sciences research facilities, over the next decade we believe democratization of gene sequencing technology and greater practical application will result in the equipment becoming ubiquitous in clinical settings as well, with oncology offering the largest market opportunity. We believe Illumina is a dominant competitor whose sequencing technology represents the critical enabling technology that ideally positions it to capitalize on an approximately $100 billion market opportunity. We believe Illumina’s shares embed expectations for key revenue and cash flow growth drivers that are well below our long-term assumptions. As a result, we believe the company is selling at a significant discount to our estimate of its intrinsic value and offers a compelling reward-to-risk opportunity.

Oracle is a leader in the enterprise software market with a strong market position in database, infrastructure and application software, and cloud-based software and services. We believe the company’s competitive advantages include its large and experienced direct sales force, a founder-driven management team that reinvests relentlessly to maintain a leading intellectual property portfolio and differentiated product suite, and a large installed base of clients with high switching costs where it consistently achieves renewal and retention rates in the mid-90% range. We believe Oracle is well positioned to benefit from the continuing growth in data storage and enterprise application software, as well as the shift to cloud-based solutions. A Fund holding since inception, Oracle reported fundamentally solid financial results that were generally in line with or better than consensus expectations. However, shares may have responded negatively to a deceleration in cloud revenue growth, due in part to capacity constraints in its data centers. Oracle is a leading global provider of enterprise infrastructure software, which includes its database technology, Oracle Cloud Infrastructure (OCI), and enterprise applications software. Oracle is transitioning its entire software business from a traditional, on-premise, up-front software licensing and maintenance revenue model to a cloud computing subscription-based model where software revenue is recognized over the life of the client’s contract. The purchase of both database and applications software is typically a long-term decision for an enterprise (usually 7-10 years) due to the mission-critical nature of these products and the high switching costs involved for customers deciding to go with a new vendor. This contributes to high client retention. While there has been near-term pressure on year-over-year overall revenue comparisons during this transition as up-front license revenue shifts to subscription revenue, we expected this to lead to faster growth over time due to a higher customer lifetime value as the transition progresses. The cloud model also allows Oracle to monetize its services and technology more efficiently and yield savings to the customer. During the period, Oracle grew its cloud revenues, which now represent almost 40% of total corporate revenues, in excess of 25% and has seen total revenue growth inflect upward towards the high single digits, consistent with our long-term expectations. There are no changes to

Natixis Loomis Sayles Focused Growth ETF

our view of Oracle as a structurally attractive business trading substantially below our estimate of intrinsic value. Oracle has a strong financial model that now has higher financial leverage due to its increased allocation of capital to share repurchases and more recently its $28 billion acquisition of healthcare IT provider Cerner in 2022. However, the company consistently generates high operating cash flow margins in the low-to-mid 30% range, and cash flow returns on invested capital that are well above its cost of capital, and we believe cash flow will be focused on debt reduction over the near to immediate term. As the subscription-based, cloud-computing services model matures and increases in sales mix, we believe Oracle will realize stronger revenue, operating margins, and free cash flow growth. We believe Oracle’s stock price embeds free cash flow growth assumptions that are well below our long-term forecast. As a result, we believe its shares are selling at a significant discount to our estimate of intrinsic value and offer a compelling reward-to-risk opportunity.

Founded in 2003, Tesla is a global leader in the design, manufacturing, and sales of high-performance fully electric (battery) vehicles (EVs). We believe Tesla’s strong and sustainable competitive advantages include its brand, focus and business model, scale, and entrepreneurial culture. With a mission that includes accelerating the world’s transition to sustainable energy, no other brand is more closely associated with EVs, and the company has become the dominant global battery EV manufacturer with over 20% global market share. Tesla’s focus and business model have enabled it to substantially disrupt the automotive industry, maintain a first-mover advantage, and capture structural cost advantages. A Fund holding since inception, Tesla reported financial results during the period that were mixed with respect to consensus expectations, due in part to pricing cuts aimed at sustaining affordability of its vehicles in the face of elevated interest rates and economic uncertainty, as well as lingering materials and logistics cost inflation, both of which lowered profitability. However, we believe the company continues to execute well, as reflected by record quarterly revenue growth, record production and deliveries in its second quarter, and growing market share as a percentage of total light vehicle sales, despite an automotive industry slowdown. Given that affordability in the EV industry is being impacted by multi-decade-high interest rates and lingering materials and logistics cost inflation, we believe Tesla has been prudently managing the business. Despite working to lower the price of its vehicles to increase affordability, higher interest rates have impacted the core mass market customer Tesla ultimately seeks to win over. With respect to price reductions, Tesla has a pricing strategy where they price their vehicles to maximize overall profit dollars. Historically the company has reduced prices annually as they leveraged their growing scale to lower the total cost of ownership for potential buyers and drive EV adoption. The company is focused on penetrating mass-market buyers, where pricing sensitivity is a greater factor, and rising rates effectively increased the price of Tesla’s cars by 10% over the last two years. Tesla’s long-term strategy remains lowering the total cost of ownership for its vehicles. We believe this is the correct strategy because Tesla manufacturing factories have high fixed costs that benefit from scale, so increasing EV sales from current levels would improve production utilization and generate higher profit per vehicle. We believe that increased volumes will offset near-term margin pressure over time. Further, unlike other manufacturers, Tesla has the ability to sell software to car owners after the initial sale, providing incentive to grow an installed base that can later be monetized through software sales. Despite a substantial year-over-year decline in operating margins, due to lower average selling prices, new factories that are not yet operating at full efficiency, higher raw materials and logistics costs, and strong investments in research and development to support the Cybertruck and its AI robot, Tesla’s operating margin trails only Ferrari, and exceeds other scaled auto manufacturers. We believe these impacts are temporary and that over the long term, Tesla can achieve operating margins in the mid-20% range. We believe the secular growth driver for Tesla is increasing penetration of electric vehicles as a share of global automotive sales. Around the world, EVs accounted for a high-single digit percentage of new light vehicle sales in 2022, with penetration rates ranging from mid-single digits in North America to low double digits in Western Europe and almost 20% in China. We believe the pace of EV adoption will accelerate, driven by advances in battery technology that will drive cost parity, lower ongoing cost of ownership for consumers, government incentives, and numerous global initiatives to phase out internal combustion engine sales over the next two decades. Tesla is the global leader in battery EV sales, with approximately 20% unit share, 25% revenue share, and a much higher share of industry profitability. While we expect competition to increase substantially, we believe Tesla’s superior brand, focus, technology leadership, and strong ongoing consumer demand will enable the company to maintain its leading global market share in the low-20% range. As a result of a rapidly expanding global EV market, we expect Tesla’s unit sales to grow by approximately 30% on a compounded annual basis, which will translate to automotive revenue growth in the high-20% range as Tesla addresses the lower-priced segment of the market with a more affordable offering. As a function of lower battery cost and greater leverage of fixed manufacturing expenses, we expect Tesla to generate higher automotive gross margins as the company gains scale. We also believe the company will benefit from operating leverage, as well as growth in its higher-margin software business, led by FSD (full self-driving) software which we believe can increase from 0% of profits today to approximately 25% by the end of the forecast period. As a result, we believe the company can expand its operating margins, contributing to operating profits and free cash flow growing faster than revenues over our long-term investment horizon. We believe the assumptions embedded in Tesla’s share price underestimate the company’s significant long-term growth opportunities and the sustainability of its global market share. We believe the company’s shares currently sell at a significant discount to our estimate of intrinsic value and thereby offer a compelling reward-to-risk opportunity.

Natixis Loomis Sayles Focused Growth ETF

All aspects of our quality-growth-valuation investment thesis must be present simultaneously for us to make an investment. Often our research is completed well in advance of the opportunity to invest. We are patient investors and maintain coverage of high-quality businesses in order to take advantage of meaningful price dislocations if and when they occur. During the period there was no investment activity.

Outlook

Our investment process is characterized by bottom-up fundamental research and a long-term investment time horizon. The nature of the process leads to a lower-turnover portfolio in which sector positioning is the result of stock selection. The Fund ended the year with overweight positions in the communication services, consumer discretionary, financials, and healthcare sectors and was underweight in the information technology, industrials, and consumer staples sectors. We had no exposure to stocks in the materials, energy, utilities, or real estate sectors.

Top Ten Holdings as of December 31, 2023 |

| |

| |

| |

3 Meta Platforms, Inc., Class A | |

| |

5 Alphabet, Inc., Class A | |

| |

| |

8 Vertex Pharmaceuticals, Inc. | |

| |

| |

The portfolio is actively managed and holdings are subject to change. There is no guarantee the Fund continues to invest in the securities referenced. The holdings listed exclude any temporary cash investments, are presented on an individual security basis and do not represent holdings of the issuer. |

Natixis Loomis Sayles Focused Growth ETF

Hypothetical Growth of $10,000 Investment1 |

June 29, 2023 (inception) through December 31, 2023 |

Total Returns —December 31, 20231 |

| Life of Fund (Inception 6/29/23) | |

| | |

| | | |

| | | |

| | | |

Russell 1000® Growth Index2 | | | |

Performance data shown represents past performance and is no guarantee of, and not necessarily indicative of, future results. Total return and value will vary, and you may have a gain or loss when shares are sold. Current performance may be lower or higher than quoted. For most recent month-end performance, visit im.natixis.com/performance. You may not invest directly in an index. Performance for periods less than one year is cumulative, not annualized. Returns reflect changes in share price and reinvestment of dividends and capital gains, if any. The table(s) do not reflect taxes shareholders might owe on any fund distributions or when they redeem their shares.

| Fund performance has been increased by fee waivers and/or expense reimbursements, if any, without which performance would have been lower. |

| Russell 1000® Growth Index is an unmanaged index that measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000® Index companies with higher price-to-book ratios and higher forecasted growth values. |

| Expense ratios are as shown in the Fund’s prospectus in effect as of the date of this report. The expense ratios for the current reporting period can be found in the Financial Highlights section of this report under Ratios to Average Net Assets. Net expenses reflect contractual expense limitations set to expire on 4/30/26. When a Fund’s expenses are below the limitation, gross and net expense ratios will be the same. See Note 6 of the Notes to Financial Statements for more information about the Fund’s expense limitations. |

| The NAV return is based on the NAV of the Fund, and the market return is based on the market price per share of the Fund, which is determined by using the midpoint between the highest bid and the lowest offer on the primary stock exchange on which shares of the Fund are listed for trading, as of the time that the Fund’s NAV is calculated. 6/29/23 represents the date trading of Fund shares commenced on the secondary market. 6/28/23 represents commencement of operations for accounting and financial reporting purposes only. NAV is used as a proxy for the opening market price on 6/29/23. Market and NAV returns assume that dividends and capital gain distributions have been reinvested in the Fund at market price and NAV, respectively. |

Natixis Loomis Sayles Short Duration Income ETF

|

|

|

|

Loomis, Sayles & Company, L.P.

|

Investment GoalThe Fund’s investment objective is current income consistent with preservation of capital.

Market Conditions

The bond market finished 2023 with positive total returns, but the favorable end result obscures the elevated volatility that occurred along the way. For most of the year, bonds were under pressure from concerns about persistent inflation and the US Federal Reserve’s (Fed) continued interest rate increases. As late as October, the headline US investment grade bond indexes were in negative territory on a year-to-date basis amid worries that the Fed would have to keep interest rates “higher for longer.”

This backdrop changed considerably in November and December, as the concerns that had weighed on the market throughout 2023 dissipated rapidly. Inflation continued to decline unabated, despite concerns about rising oil prices in the third quarter. In November, the headline Consumer Price Index came in at inflation rates not seen since early 2021. With inflation receding, the markets grew comfortable with the idea that the Fed was finished raising rates. In December, Fed Chairman Jerome Powell added to the upbeat tone with comments suggesting that rate cuts could begin as early as the first half of 2024. Bond prices took another leg higher in response, erasing all previous losses and helping the fixed income market close with solid gains for the full year. Income also made a meaningful contribution to total returns thanks to the increase in yields over the past two years.

US Treasuries registered gains for the year, albeit with unusually high volatility brought about by the shifting interest rate outlook. The yield on the two-year note, which came into 2023 at 4.41%, rose as high as 5.19% in mid-October before falling sharply to finish December at 4.23%. The ten-year issue took a similar path, moving from 3.88% at the end of 2022 to 4.99% in October and ultimately closing at the same 3.88% level where it began. The yield curve remained inverted for all of 2023, meaning that short-term debt offered higher yields than longer-term issues – an unusual condition that is often seen as a precursor to a recession. However, the extent of the inversion gradually receded from its July high during the remainder of the year.

Corporate bonds delivered a robust gain and outperformed US Treasuries. In addition to benefiting from the drop in Treasury yields in the fourth quarter, the asset class was boosted by the environment of positive economic growth, continued strength in corporate earnings, and investors’ hearty appetite for risk. Corporates’ above-average yield was an additional factor in their positive relative performance.

Securitized assets produced largely positive total returns in 2023. Collateralized loan obligations and commercial asset-backed securities delivered particularly strong gains. Portions of the residential mortgage-backed securities market also outperformed. Headwinds facing the commercial real estate sector emerged in the first half of 2023, negatively impacting non-agency commercial mortgage-backed securities’ performance for the full year. Generally, the higher-yielding securitized credit sectors performed best. A challenging supply-and-demand backdrop negatively impacted agency mortgage-backed securities (MBS) as elevated levels of interest-rate volatility continued and historically large buyers of agency MBS (banks and the US Federal Reserve) pulled back from the market. Still, agency MBS outperformed US Treasuries for the year.

Performance Results

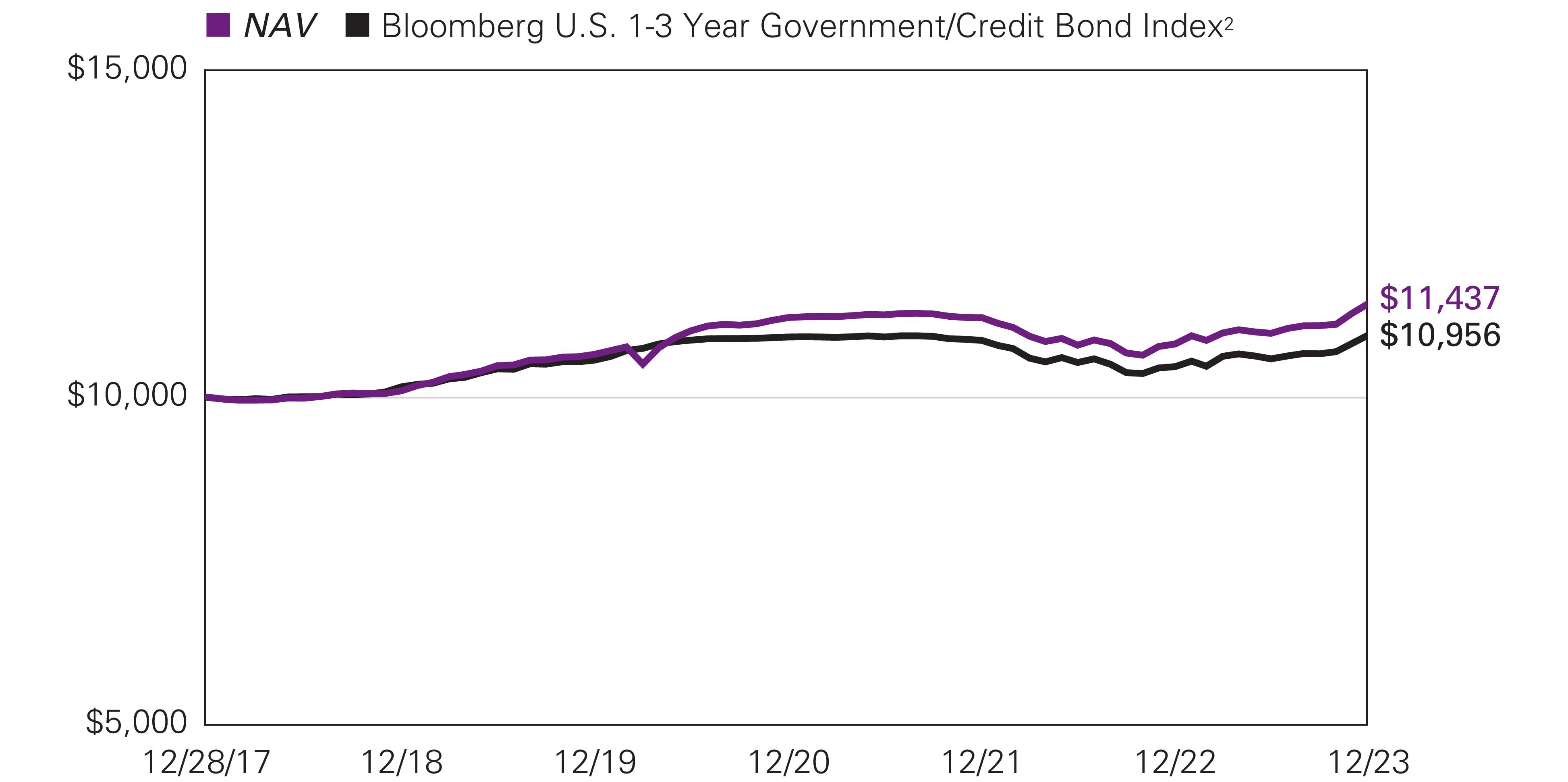

For the 12 months ended December 31, 2023, the Natixis Loomis Sayles Short Duration Income ETF returned 5.74%. The Fund outperformed its benchmark, the Bloomberg U.S. 1-3 Year Government/Credit Bond Index, which returned 4.61%.

Explanation of Fund Performance

Sector allocation and security selection effects provided a large contribution for the year. In sector allocation, positioning with respect to investment grade corporate bonds provided the largest benefit to relative performance. Securitized credit, particularly exposure to asset-backed securities, was also positive for the year. While the Fund’s positioning with respect to duration (and corresponding interest rate sensitivity) continues to be managed in line with the benchmark, tactical positioning along the yield curve (which depicts

Natixis Loomis Sayles Short Duration Income ETF

the relationship among bond yields across the maturity spectrum) resulted in a negative contribution to performance. The underweight allocation to US Treasuries hindered performance and exposure to US Agency securities was also negative for the period.

Outlook

The Fed elected to hold the fed funds rates steady at 5.25% throughout the fourth quarter. Forward guidance shifted from a hawkish to a dovish tone, as inflation surprised to the downside and softer economic data increased the odds of achieving the elusive "soft landing". In our view, the shift in tone caused market sentiment to dramatically reverse course; yields fell sharply while spreads tightened. Yields on the 10-year Treasury peaked at just over 5% in late-October before falling over 110 bps to 3.88% by year-end. Market expectations for any additional hikes disappeared, while expectations for easing monetary policy rose and were pulled forward into early 2024. Current pricing reflects 150 bps of anticipated cuts in the next 12 months, equivalent to three additional hikes on top of what is reflected in the Fed's Summary of Economic Projections. The yield curve steepened but remained inverted during the fourth quarter, with higher yields on shorter maturity Treasuries relative to longer-dated notes and bonds.

We continue to hold the view that we are in the late expansion phase of the credit cycle, with a significant probability of either a softer landing or more meaningful slowdown (i.e. downturn) sometime over the next 6-9 months. Corporate balance sheets have deteriorated, but from a very strong starting point; profit margins could continue to be pressured amid higher input costs, tighter credit conditions, and a slowdown in de-leveraging trends. We believe a relatively healthy middle class consumer and resilient labor market should prevent the economy from entering into a severe recession in this cycle.

We remain concerned about the lagged effects of significant monetary tightening, globally. This has come through traditional monetary policy tightening, including some central bank asset sales and/or balance sheet run-off, and covers many developed and emerging economies across the globe. Notable exceptions on the policy tightening side include the Bank of Japan, where policy remains very accommodative, and the Bank of China, where weakness in the Chinese property sector remains a concern. We also remain concerned about potential exogenous shocks to growth, possibly emanating from the ongoing conflict in the Middle East.

We continue to favor spread sectors, such as corporate bonds and securitized assets

Corporate bond risk relative to benchmark is currently below median, and sized to be approximately one-third of budget. The team continues to hold a small number of non-investment grade issuers we believe offer value.

We believe asset backed securities (ABS) continue to be a favorable alternative in the front end of the curve. We currently favor consumer related collateral and prefer the top of the capital stack, but are not limited to the highest quality band of the structure. The strategy’s ABS risk relative to benchmark remains around two-thirds of risk budget.

While the strategy continues to hold commercial mortgage-backed securities (CMBS), the exposure is typically on the low end of our risk range relative to benchmark. When opportunities arise within CMBS we tend to favor senior parts of the capital stack.

We continue to follow our process of seeking to build diversified exposures by asset class, industry and issuers.

Natixis Loomis Sayles Short Duration Income ETF

Hypothetical Growth of $10,000 Investment1 |

December 28, 2017 (inception) through December 31, 2023 |

Average Annual Total Returns —December 31, 20231 |

| | | Life of Fund (Inception 12/28/17) | |

| | |

| | | | | |

| | | | | |

| | | | | |

Bloomberg U.S. 1-3 Year Government/Credit Bond Index2 | | | | | |

Performance data shown represents past performance and is no guarantee of, and not necessarily indicative of, future results. Total return and value will vary, and you may have a gain or loss when shares are sold. Current performance may be lower or higher than quoted. For most recent month-end performance, visit im.natixis.com/performance. You may not invest directly in an index. Performance for periods less than one year is cumulative, not annualized. Returns reflect changes in share price and reinvestment of dividends and capital gains, if any. The table(s) do not reflect taxes shareholders might owe on any fund distributions or when they redeem their shares.

| Fund performance has been increased by fee waivers and/or expense reimbursements, if any, without which performance would have been lower. |

| Bloomberg U.S. 1-3 Year Government/Credit Bond Index is an unmanaged index which is a component of the U.S. Government/Credit Bond Index, which includes Treasury and agency securities (U.S. Government Bond Index) and publicly issued US corporate and foreign debentures and secured notes (U.S. Credit Bond Index). The bonds in the index are investment grade with a maturity between one and three years. |

| Expense ratios are as shown in the Fund’s prospectus in effect as of the date of this report. The expense ratios for the current reporting period can be found in the Financial Highlights section of this report under Ratios to Average Net Assets. Net expenses reflect contractual expense limitations set to expire on 4/30/26. When a Fund’s expenses are below the limitation, gross and net expense ratios will be the same. See Note 6 of the Notes to Financial Statements for more information about the Fund’s expense limitations. |

| The NAV return is based on the NAV of the Fund, and the market return is based on the market price per share of the Fund, which is determined by using the midpoint between the highest bid and the lowest offer on the primary stock exchange on which shares of the Fund are listed for trading, as of the time that the Fund’s NAV is calculated. 12/28/17 represents the date trading of Fund shares commenced on the secondary market. 12/27/17 represents commencement of operations for accounting and financial reporting purposes only. NAV is used as a proxy for the opening market price on 12/28/17. Market and NAV returns assume that dividends and capital gain distributions have been reinvested in the Fund at market price and NAV, respectively. |

Natixis Vaughan Nelson Mid Cap ETF

|

|

|

Chris D. Wallis, CFA®, CPA |

Vaughan Nelson Investment Management, L.P.

|

Investment GoalThe Fund seeks long-term capital appreciation.

Market Conditions

During the fiscal year ending December 31, 2023, the market began with sequential growth slowing in both the first and second quarters. Typically, banking stress develops once we are well into a recession as the ability for borrowers to service debt becomes impaired. Given the rapid increase in interest rates, regional banks fell under tremendous pressure.

As we moved through the summer months, global growth continued to deteriorate as the impact of aggressive rate increases affected economic fundamentals. In the U.S., the manufacturing and transportation sectors recessed and the service sector slowed further. Offsetting the deteriorating economic environment were continued liquidity injections by the major non-U.S. central banks and the U.S. Federal Reserve’s (Fed) reverse repo facility, which became the primary source of liquidity for rebuilding the U.S. Treasury’s general account. This flood of liquidity boosted equity markets and dampened fixed income volatility, compressing fixed income spreads (the difference in yield between bonds with similar maturity but different credit quality).

Inflation peaked in the fourth quarter of 2022 and economic growth bottomed, which set the stage for the move higher in U.S. equity markets during the first seven months of 2023. The reacceleration in growth coupled with declining inflation allowed the market to begin pricing in a “soft landing” for the U.S. economy despite aggressive monetary policy tightening, the emergence of a banking crisis, and rising U.S. Treasury yields as the U.S. Treasury struggled to fund rising deficit spending. The Fed added fuel to the rally by aggressively pumping liquidity into the banking system to offset the material losses on bank balance sheets.

During the fourth quarter, improving supply chains, rising employment participation rates, and the lagging influence of stabilized home prices and rental inflation continued to promote disinflationary conditions. Declining inflationary pressures, combined with stable economic growth, produced a material improvement in financial conditions as the market discounted future Fed rate cuts without any corresponding decrease in earnings expectations or economic weakness. The resulting decline in interest rates led to a powerful fourth quarter rally in equity and fixed income markets.

Performance Results

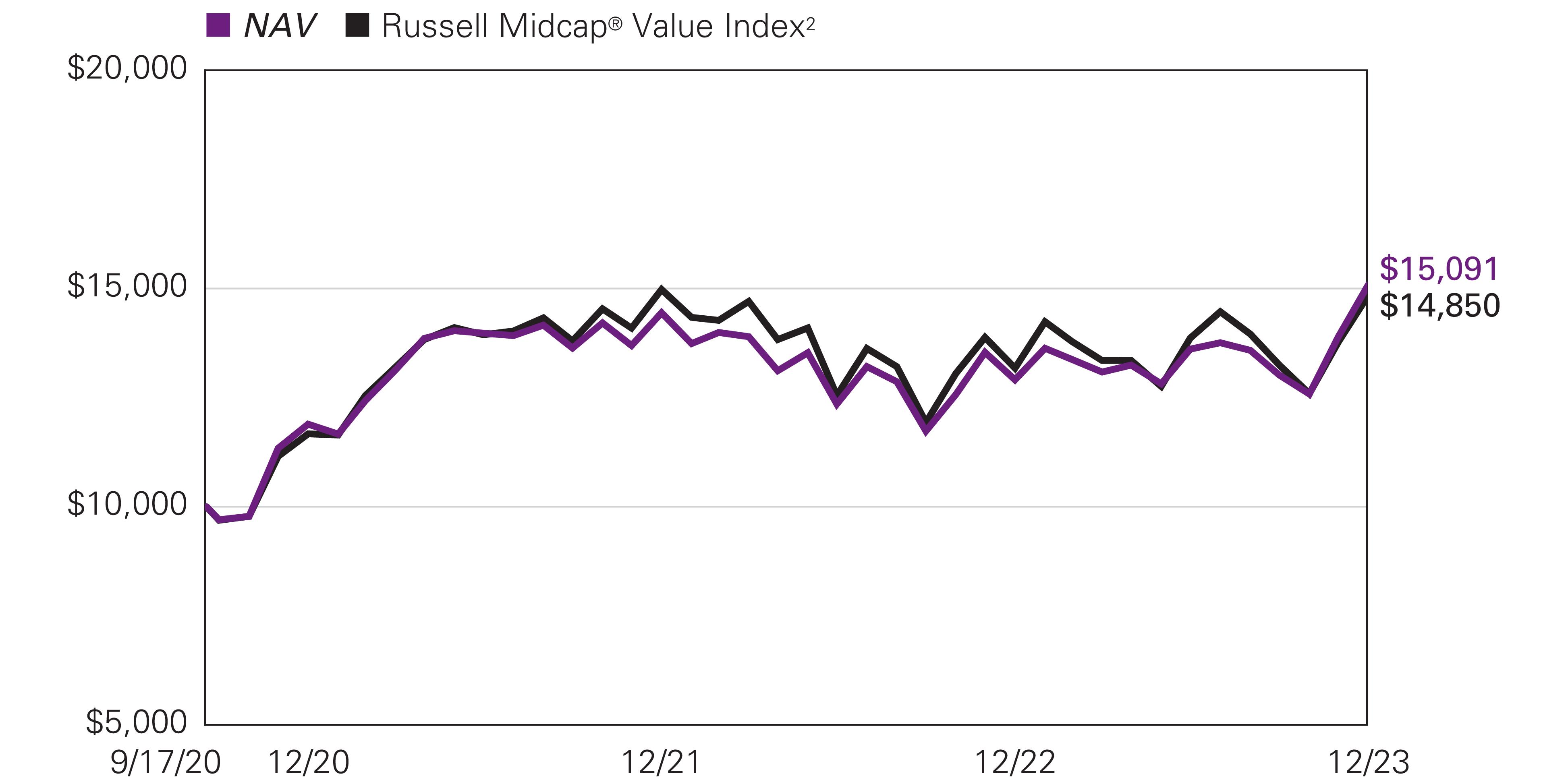

For the 12 months ended December 31, 2023, the Vaughan Nelson Mid Cap ETF returned 16.91% at net asset value. The Fund outperformed its benchmark, the Russell Mid Cap Value® Index, which returned 12.71%.

Explanation of Fund Performance

The Fund outperformed on a relative basis during the period.

Health care was the top performing sector with Cencora, Inc. leading the way. Cencora benefited from both multiple expansion and positive earnings revisions. The company’s consistent top-line and bottom-line growth combined with strong cash flow generation and return of capital were rewarded.

Materials outperformed driven by selection. Constellium SE Class A outperformed on a cycle of positive earnings revisions, as demand remained robust, and the company spoke to the end of destocking in packaging.

Overweight and selection within information technology aided performance. The strongest name was Motorola Solutions, Inc. Motorola’s public end markets continued to prove strong and consistent, as the company was able to beat and raise earnings expectations throughout the year.

Financials outperformed via selection with Comerica Incorporated leading the way. Comerica benefited with the rest of the regional banks as valuations had gotten too punitive for what may turn out to be a shallow recession.

Consumer staples’ outperformance was led by Church & Dwight Co., Inc. After a year of disappointing investors in 2022, Church & Dwight regained its credibility in 2023 by putting an end to the downward revision cycle, while recent acquisitions performed better

Natixis Vaughan Nelson Mid Cap ETF

than expectations. Additionally, with GLP1 headlines hurting packaged food and beverage stocks, Church & Dwight benefited on a relative basis as it is not impacted by GLP1s.

Further assisting in outperformance was Extra Space Storage Inc. within real estate. REITs outperformed in the fourth quarter as interest rates peaked, and Extra Space Storage outperformed REITs on solid fundamentals.

Selection within utilities assisted performance with Vistra Corp. as the top name. Vistra continued to show a strong recovery in earnings power as the company benefited from pricing during a very hot summer in Texas. The company outperformed regulated utilities which are dealing with ROE (return on equity) pressures.

An underweight to energy, an underperforming sector, added to relative performance.

Last, selection within consumer discretionary positively impacted performance. Floor & Decor Holdings, Inc. Class A outperformed as strong numbers and a desirable long-term algorithm led to the stock rising with other highly shorted names in the fourth quarter.

Selection within communication services hurt on a relative basis. Nexstar Media Group, Inc. detracted the most as softness in advertising markets coupled with worries about distribution held down the stock.

The Fund experienced negative attribution within industrials with WillScot Mobile Mini Holdings Corp. Class A being the largest drag. WillScot lagged due to slowing volumes coupled with an uncertain macro environment, especially in non-residential end markets.

Outlook

As we enter 2024, we expect modest economic weakness in the first half of the year followed by economic stability and an improvement in growth heading into the 2024 election cycle. Inflation will likely remain above the Fed’s 2% target, and with the recent dramatic easing in financial conditions, inflation may begin increasing in the fourth quarter of 2024. Should inflation expectations begin firming, we would expect some modest downward pressure on equity valuations.

Top Ten Holdings as of December 31, 2023 |

| |

1 Extra Space Storage, Inc. | |

2 EastGroup Properties, Inc. | |

3 Monolithic Power Systems, Inc. | |

| |

| |

6 Diamondback Energy, Inc. | |

| |

8 Marvell Technology, Inc. | |

9 Skechers USA, Inc., Class A | |

| |

The portfolio is actively managed and holdings are subject to change. There is no guarantee the Fund continues to invest in the securities referenced. The holdings listed exclude any temporary cash investments, are presented on an individual security basis and do not represent holdings of the issuer. |

Natixis Vaughan Nelson Mid Cap ETF

Hypothetical Growth of $10,000 Investment1 |

September 17, 2020 (inception) through December 31, 2023 |

Average Annual Total Returns —December 31, 20231 |

| | Life of Fund (Inception 9/17/20) | |

| | |

| | | | |

| | | | |

| | | | |

Russell Midcap® Value Index2 | | | | |

Performance data shown represents past performance and is no guarantee of, and not necessarily indicative of, future results. Total return and value will vary, and you may have a gain or loss when shares are sold. Current performance may be lower or higher than quoted. For most recent month-end performance, visit im.natixis.com/performance. You may not invest directly in an index. Performance for periods less than one year is cumulative, not annualized. Returns reflect changes in share price and reinvestment of dividends and capital gains, if any. The table(s) do not reflect taxes shareholders might owe on any fund distributions or when they redeem their shares.

| Fund performance has been increased by fee waivers and/or expense reimbursements, if any, without which performance would have been lower. |

| Russell Midcap® Value Index is an unmanaged index that measures the performance of the mid-cap value segment of the U.S. equity universe. It includes those Russell Midcap® Index companies with lower price-to-book ratios and lower forecasted growth values. |

| Expense ratios are as shown in the Fund’s prospectus in effect as of the date of this report. The expense ratios for the current reporting period can be found in the Financial Highlights section of this report under Ratios to Average Net Assets. Net expenses reflect contractual expense limitations set to expire on 4/30/26. When a Fund’s expenses are below the limitation, gross and net expense ratios will be the same. See Note 6 of the Notes to Financial Statements for more information about the Fund’s expense limitations. |

| The NAV return is based on the NAV of the Fund, and the market return is based on the market price per share of the Fund, which is determined by using the midpoint between the highest bid and the lowest offer on the primary stock exchange on which shares of the Fund are listed for trading, as of the time that the Fund’s NAV is calculated. 9/17/20 represents the date trading of Fund shares commenced on the secondary market. 9/16/20 represents commencement of operations for accounting and financial reporting purposes only. NAV is used as a proxy for the opening market price on 9/17/20. Market and NAV returns assume that dividends and capital gain distributions have been reinvested in the Fund at market price and NAV, respectively. |

Natixis Vaughan Nelson Select ETF

|

Chris D. Wallis, CFA®, CPA |

|

Vaughan Nelson Investment Management, L.P.

|

Investment GoalThe Fund seeks long-term capital appreciation.

Market Conditions

During the fiscal year ending December 31, 2023, the market began with sequential growth slowing in both the first and second quarters. Typically, banking stress develops once we are well into a recession as the ability for borrowers to service debt becomes impaired. Given the rapid increase in interest rates, regional banks fell under tremendous pressure.

As we moved through the summer months, global growth continued to deteriorate as the impact of aggressive rate increases affected economic fundamentals. In the U.S., the manufacturing and transportation sectors recessed and the service sector slowed further. Offsetting the deteriorating economic environment were continued liquidity injections by the major non-U.S. central banks and the U.S. Federal Reserve’s (Fed) reverse repo facility, which became the primary source of liquidity for rebuilding the U.S. Treasury’s general account. This flood of liquidity boosted equity markets and dampened fixed income volatility, compressing fixed income spreads (the difference in yield between bonds with similar maturity but different credit quality).

Inflation peaked in the fourth quarter of 2022 and economic growth bottomed, which set the stage for the move higher in U.S. equity markets during the first seven months of 2023. The reacceleration in growth coupled with declining inflation allowed the market to begin pricing in a “soft landing” for the U.S. economy despite aggressive monetary policy tightening, the emergence of a banking crisis, and rising U.S. Treasury yields as the U.S. Treasury struggled to fund rising deficit spending. The Fed added fuel to the rally by aggressively pumping liquidity into the banking system to offset the material losses on bank balance sheets.

During the fourth quarter, improving supply chains, rising employment participation rates, and the lagging influence of stabilized home prices and rental inflation continued to promote disinflationary conditions. Declining inflationary pressures, combined with stable economic growth, produced a material improvement in financial conditions as the market discounted future Fed rate cuts without any corresponding decrease in earnings expectations or economic weakness. The resulting decline in interest rates led to a powerful fourth quarter rally in equity and fixed income markets.

Performance Results

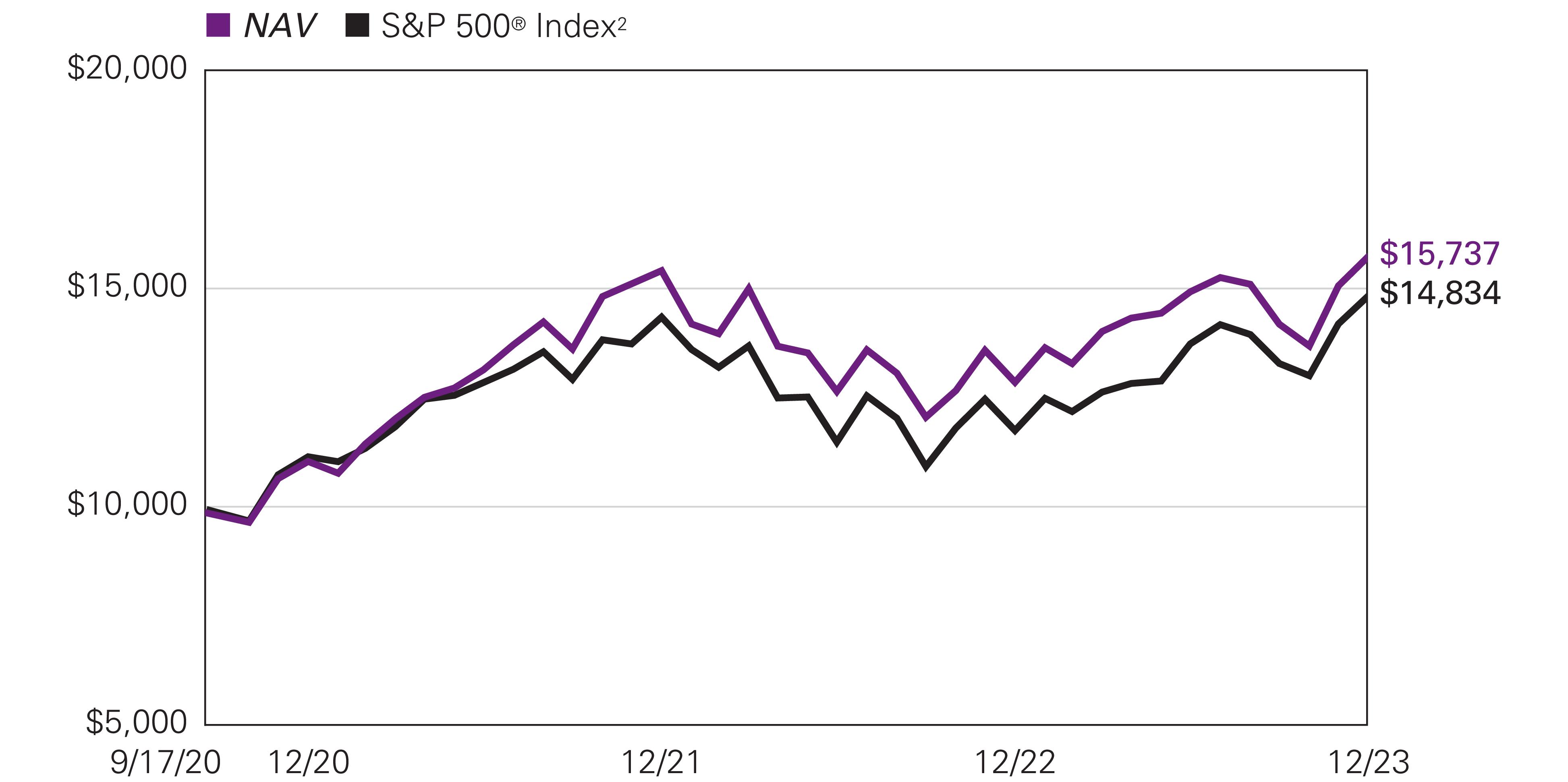

For the 12 months ended December 31, 2023, the Vaughan Nelson Select ETF returned 22.48% at net asset value. The Fund underperformed its benchmark, the S&P 500® Index, which returned 26.29%.

Explanation of Fund Performance

The Fund underperformed on a relative basis during the period.

The largest detractor was in consumer staples, driven by security selection, with Dollar General being the worst-performing name. Dollar General struggled with declining same-store sales due to lower-margin product mix shift, store safety and organization issues, and the lack of trade-down in consumer spend. While we expect management will be able to reverse these issues over time, the stock was sold to allocate capital into names with a better return opportunity.

An overweight to and selection within utilities impaired relative performance. NextEra Energy, Inc. was the most challenged name. NextEra Energy’s share price suffered from higher costs of capital threatening the growth rate for renewable energy projects. We expect the unregulated portion of the business will still be able to achieve outsized returns as capital costs stabilize.

An underweight to both communication services and information technology, which were top performing sectors, also detracted.

The Fund experienced positive attribution within industrials, with Saia, Inc. leading the way. Saia is gaining share as a best-in-class operator as it invests to add terminal capacity while over-levered competitors struggle to maintain operations.

An underweight to health care, an underperforming sector, and selection within it aided relative performance with DexCom, Inc. being the best name in the space. As the technology leader in continuous glucose monitoring (CGM), we expect that with increased insurance coverage and more data showing CGM use alongside semaglutide, Dexcom will achieve higher growth and profitability

Natixis Vaughan Nelson Select ETF

Sherwin-Wiliams Company assisted in materials outperformance. The company’s value proposition for its clients allows it the ability to maintain prices. As inflationary cost pressures abate, this strategic positioning has led to stronger margins.

An underweight to energy, an underperforming sector, contributed to performance.

Selection within real estate assisted, with the contribution led by Crown Castle Inc. (CCI). We believed that CCI’s small cell business was undervalued as higher data consumption would drive the need for densified coverage. Activist attention brought forward potential realization of that value in the form of a multiple re-rating.

Selection within consumer discretionary helped on a relative basis. Amazon.com was the best performer due to investment in higher-margin business products such as AWS, subscriptions, and advertising.

An underweight to and selection within financials aided relative performance. JPMorgan Chase & Co. was the top contributor. The company’s size and the balance sheet de-risking it instituted after the Global Financial Crisis has allowed it to gain share and protect against macroeconomic headwinds.

Outlook

As we enter 2024, we expect modest economic weakness in the first half of the year followed by economic stability and an improvement in growth heading into the 2024 election cycle. Inflationary pressures will likely remain above the Fed’s 2% target, and with the recent dramatic easing in financial conditions, inflation may begin increasing in the fourth quarter of 2024. Should inflation expectations begin firming, we would expect some modest downward pressure on equity valuations.

Top Ten Holdings as of December 31, 2023 |

| |

| |

| |

3 Intercontinental Exchange, Inc. | |

4 Alphabet, Inc., Class A | |

| |

| |

7 Monolithic Power Systems, Inc. | |

| |

9 O'Reilly Automotive, Inc. | |

| |

The portfolio is actively managed and holdings are subject to change. There is no guarantee the Fund continues to invest in the securities referenced. The holdings listed exclude any temporary cash investments, are presented on an individual security basis and do not represent holdings of the issuer. |

Natixis Vaughan Nelson Select ETF

Hypothetical Growth of $10,000 Investment1 |

September 17, 2020 (inception) through December 31, 2023 |

Average Annual Total Returns —December 31, 20231 |

| | Life of Fund (Inception 9/17/20) | |

| | |

| | | | |

| | | | |

| | | | |

| | | | |

Performance data shown represents past performance and is no guarantee of, and not necessarily indicative of, future results. Total return and value will vary, and you may have a gain or loss when shares are sold. Current performance may be lower or higher than quoted. For most recent month-end performance, visit im.natixis.com/performance. You may not invest directly in an index. Performance for periods less than one year is cumulative, not annualized. Returns reflect changes in share price and reinvestment of dividends and capital gains, if any. The table(s) do not reflect taxes shareholders might owe on any fund distributions or when they redeem their shares.

| Fund performance has been increased by fee waivers and/or expense reimbursements, if any, without which performance would have been lower. |

| S&P 500® Index is a widely recognized measure of U.S. stock market performance. It is an unmanaged index of 500 common stocks chosen for market size, liquidity, and industry group representation, among other factors. It also measures the performance of the large cap segment of the U.S. equities market. |

| Expense ratios are as shown in the Fund’s prospectus in effect as of the date of this report. The expense ratios for the current reporting period can be found in the Financial Highlights section of this report under Ratios to Average Net Assets. Net expenses reflect contractual expense limitations set to expire on 4/30/26. When a Fund’s expenses are below the limitation, gross and net expense ratios will be the same. See Note 6 of the Notes to Financial Statements for more information about the Fund’s expense limitations. |

| The NAV return is based on the NAV of the Fund, and the market return is based on the market price per share of the Fund, which is determined by using the midpoint between the highest bid and the lowest offer on the primary stock exchange on which shares of the Fund are listed for trading, as of the time that the Fund’s NAV is calculated. 9/17/20 represents the date trading of Fund shares commenced on the secondary market. 9/16/20 represents commencement of operations for accounting and financial reporting purposes only. NAV is used as a proxy for the opening market price on 9/17/20. Market and NAV returns assume that dividends and capital gain distributions have been reinvested in the Fund at market price and NAV, respectively. |

ADDITIONAL INFORMATION

The views expressed in this report reflect those of the portfolio managers as of the dates indicated. The managers’ views are subject to change at any time without notice based on changes in market or other conditions. References to specific securities or industries should not be regarded as investment advice. Because the Funds are actively managed, there is no assurance that they will continue to invest in the securities or industries mentioned.

All investing involves risk, including the risk of loss. There is no assurance that any investment will meet its performance objectives or that losses will be avoided.

ADDITIONAL INDEX INFORMATION

This document may contain references to third party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with Natixis Investment Managers or any of its related or affiliated companies (collectively “Natixis Affiliates”) and does not sponsor, endorse or participate in the provision of any Natixis Affiliates services, funds or other financial products.

The index information contained herein is derived from third parties and is provided on an “as is” basis. The user of this information assumes the entire risk of use of this information. Each of the third party entities involved in compiling, computing or creating index information disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to such information.

PROXY VOTING INFORMATION

A description of the Natixis Funds' proxy voting policies and procedures is available without charge, upon request, by calling Natixis Funds at 800-225-5478; on the Natixis Funds’ website at im.natixis.com, and on the Securities and Exchange Commission (“SEC”) website at www.sec.gov. Information about how the Natixis Funds voted proxies relating to portfolio securities during the most recent 12-month period ended June 30 is available through the Natixis Funds’ website and the SEC website.

QUARTERLY PORTFOLIO SCHEDULES

The Natixis Funds file a complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year as an exhibit to its reports on Form N-PORT. The Funds’ Form N-PORT reports are available on the SEC website at www.sec.gov. First and third quarter schedules of portfolio holdings are also available at im.natixis.com/funddocuments. A hard copy may be requested from the Fund at no charge by calling 800-225-5478.

TAILORED SHAREHOLDER REPORTS FOR MUTUAL FUNDS AND EXCHANGE-TRADED FUNDS

In October 2022, the SEC adopted rule and form amendments requiring mutual funds and exchange-traded funds to transmit concise and visually engaging streamlined annual and semiannual reports that highlight key information to shareholders. Other information, including financial statements, will no longer appear in the funds’ shareholder reports but will be available online, delivered free of charge upon request, and filed with the SEC on a semiannual basis on Form N-CSR. The rule and form amendments have a compliance date of July 24, 2024.

CFA® and Chartered Financial Analyst® are registered trademarks owned by the CFA Institute.

Understanding Fund Expenses

As a shareholder, you incur two types of costs: (1) transaction costs, which may include creation and redemption fees and brokerage charges, and (2) ongoing costs, including management fees and other fund expenses. These ongoing costs are described in more detail in the Fund’s prospectus. The following examples are intended to help you understand the ongoing costs of investing in the Fund and help you compare these with the ongoing costs of investing in other funds.

The first line in the table shows the actual account values and actual Fund expenses you would have paid on a $1,000 investment in the Fund from July 1, 2023, 2023 through December 31, 2023. To estimate the expenses you paid over the period, simply divide your account value by $1,000 (for example $8,600 account value divided by $1,000 = 8.60) and multiply the result by the number in the Expenses Paid During Period column as shown below for your class.

The second line in the table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The

hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid on your investment for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. Please note that the expenses shown reflect ongoing costs only, and do not include any transaction costs, such as brokerage commissions on purchases and sales of Fund shares. Therefore, the second line in the table is useful in comparing ongoing costs only, and will not help you determine the relative costs of owning different funds. If transaction costs were included, total costs would be higher.

Natixis Gateway Quality Income ETF | Beginning

Account Value

7/1/2023 | Ending

Account Value

12/31/2023 | Expenses Paid

During Period

|

| | | |

Hypothetical (5% return before expenses) | | | |