UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

____________

Form 6-K

____________

REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16 UNDER THE SECURITIES EXCHANGE ACT OF 1934

November 12, 2019

Commission File Number: 333-177693

Reynolds Group Holdings Limited

(Translation of registrant’s name into English)

Reynolds Group Holdings Limited

Level Nine

148 Quay Street

Auckland 1010 New Zealand

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

Form 20-F x Form 40-F ¨

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1): ¨

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7): ¨

QUARTERLY REPORT

For the three and nine month periods ended September 30, 2019

REYNOLDS GROUP HOLDINGS LIMITED

New Zealand

(Jurisdiction of incorporation or organization)

Reynolds Group Holdings Limited

Level Nine

148 Quay Street

Auckland 1010 New Zealand

Attention: Joseph Doyle

Tel: +1 847 482 2409

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

|

| | |

| | Reynolds Group Holdings Limited |

| | (Registrant) |

| | |

| | By: | /s/ ALLEN HUGLI |

| | Allen Hugli |

| | Chief Financial Officer |

| | November 12, 2019 |

Table of Contents

|

| | | | | | | |

| PART I - FINANCIAL INFORMATION | |

| | ITEM 1. FINANCIAL STATEMENTS | |

| | ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | |

| | | Overview | |

| | | Key Factors Influencing Our Financial Condition and Results of Operations | |

| | | Results of Operations | |

| | | Differences Between the RGHL Group and the BP I Group Results of Operations | |

| | | Liquidity and Capital Resources | |

| | | Accounting Principles | |

| | | Critical Accounting Policies | |

| | | Recently Issued Accounting Pronouncements | |

| | | Recent Developments | |

| | ITEM 3. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | |

| | ITEM 4. CONTROLS AND PROCEDURES | |

| PART II - OTHER INFORMATION | |

| | ITEM 1. LEGAL PROCEEDINGS | |

| | ITEM 1A. RISK FACTORS | |

| | ITEM 2. UNREGISTERED SALES OF EQUITY SECURITIES AND USE OF PROCEEDS | |

| | ITEM 3. DEFAULTS UPON SENIOR SECURITIES | |

| | ITEM 4. MINE SAFETY DISCLOSURE | |

| | ITEM 5. OTHER INFORMATION | |

| | ITEM 6. EXHIBITS | |

Introductory Note

In this quarterly report, references to “we,” “us,” “our” or the “RGHL Group” are to Reynolds Group Holdings Limited (“RGHL”) and its consolidated subsidiaries, unless otherwise indicated.

Certain financial information that is normally included in annual financial statements, including certain financial statement notes, is not required for interim reporting purposes and has been condensed or omitted in this quarterly report. Our annual report on Form 20-F for the year ended December 31, 2018 filed with the U.S. Securities and Exchange Commission (the “SEC”) on February 14, 2019 (the “Annual Report”) also includes certain other information about our business, including risk factors and more detailed descriptions of our businesses, which is not included in this quarterly report. This quarterly report should be read in conjunction with the Annual Report, including the consolidated financial statements and notes thereto included therein. The SEC maintains an internet site at https://www.sec.gov, from which interested persons can electronically access the Annual Report including the exhibits thereto. The Annual Report can also be found at www.reynoldsgroupholdings.com, or a copy will be provided free of charge upon written request to Mr. Joseph Doyle, RGHL Group Legal Counsel, 1900 West Field Court, Lake Forest, Illinois, 60045.

We have prepared this quarterly report pursuant to (i) the requirements of the indentures that govern our senior secured notes and our senior notes, excluding the Pactiv Notes (as defined below), and (ii) the credit agreement with our lenders governing our senior secured credit facilities (the “Credit Agreement”). Our outstanding notes include:

| |

| • | Notes covered by an effective registration statement filed with the SEC, comprised of: |

| |

| • | the 5.750% Senior Secured Notes due 2020; and |

| |

| • | the 6.875% Senior Secured Notes due 2021; |

| |

| • | Notes not covered by an effective registration statement filed with the SEC, comprised of: |

| |

| • | the Floating Rate Senior Secured Notes due 2021; |

| |

| • | the 5.125% Senior Secured Notes due 2023; |

| |

| • | the 7.000% Senior Notes due 2024; and |

| |

| • | the 7.950% Debentures due 2025 and the 8.375% Debentures due 2027 (collectively, the “Pactiv Notes”). |

The senior secured notes are referred to as the “Reynolds Senior Secured Notes.” The senior notes are referred to as the “Reynolds Senior Notes.” The Reynolds Senior Secured Notes and the Reynolds Senior Notes are collectively referred to as the “Reynolds Notes.”

The indentures governing these notes, as well as our Credit Agreement, are described more fully in our Annual Report. Additionally, refer to note 12 of the RGHL Group’s interim unaudited condensed consolidated financial statements included elsewhere in this quarterly report for more information.

Non-GAAP Financial Measures

In this quarterly report, we utilize certain non-GAAP financial measures and ratios, including earnings before interest, tax, depreciation and amortization (“EBITDA”) and Adjusted EBITDA. Adjusted EBITDA, a measure used by our management to measure operating performance, is defined as EBITDA, adjusted to exclude certain items of a significant or unusual nature, including but not limited to acquisition costs, non-cash pension income or expense, restructuring costs, related party management fees, unrealized gains or losses on derivatives, gains or losses on the sale of non-strategic assets, asset impairments and write-downs, strategic review costs and equity method profit not distributed in cash. These measures are presented because we believe that they and similar measures are widely used in the markets in which we operate as a means of evaluating a company’s operating performance and financing structure and, in certain cases, because those measures are used to determine compliance with covenants in our debt agreements and compensation of certain management. They may not be comparable to other similarly titled measures of other companies and are not measurements under International Financial Reporting Standards (“IFRS”), as issued by the International Accounting Standards Board (“IASB”), generally accepted accounting principles in the United States of America (“U.S. GAAP”), or other generally accepted accounting principles, are not measures of financial condition, liquidity or profitability and should not be considered as an alternative to profit from operations for the period or operating cash flows determined in accordance with IFRS, nor should they be considered as substitutes for the information contained in our financial statements prepared in accordance with IFRS included in this quarterly report. Additionally, EBITDA and Adjusted EBITDA are not intended to be measures of free cash flow, as they do not take into account certain items such as interest and principal payments on our indebtedness, working capital needs, tax payments and capital expenditures. We believe that the inclusion of EBITDA and Adjusted EBITDA in this quarterly report is appropriate to provide additional information to investors about our operating performance and to provide a measure of operating results unaffected by differences in capital structures, capital investment cycles and ages of related assets among otherwise comparable companies. We believe that issuers of high yield debt securities present EBITDA and Adjusted EBITDA because investors, analysts and rating agencies consider these measures useful. For additional information regarding the non-GAAP financial measures used by management, refer to note 4 of the RGHL Group’s interim unaudited condensed consolidated financial statements included elsewhere in this quarterly report.

Forward-Looking Statements

This quarterly report includes forward-looking statements. Forward-looking statements include statements regarding our goals, beliefs, plans or current expectations, taking into account the information currently available to our management. Forward-looking statements are not statements of historical fact. For example, when we use words such as “believe,” “anticipate,” “expect,” “estimate,” “plan,” “intend,” “should,” “would,” “could,” “may,” “might,” “will” or other words that convey uncertainty of future events or outcomes, we are making forward-looking statements. We have based these forward-looking statements on our management’s current view with respect to future events and financial performance and future

business and economic conditions more generally. These views reflect the best judgment of our management, but involve a number of risks and uncertainties which could cause actual results to differ materially from those predicted in our forward-looking statements and from past results, performance or achievements. Although we believe that the estimates and the projections reflected in the forward-looking statements are reasonable, such estimates and projections may prove to be incorrect, and our actual results may differ from those described in our forward-looking statements as a result of the following risks, uncertainties and assumptions, among others:

| |

| • | risks related to future costs of raw materials, energy and freight, including the impact of tariffs, trade sanctions and similar matters affecting our importation of certain raw materials; |

| |

| • | risks related to economic downturns in our target markets; |

| |

| • | risks related to changes in consumer lifestyle, eating habits, nutritional preferences and health-related and environmental concerns that may harm our business and financial performance; |

| |

| • | risks related to complying with environmental, health and safety laws or as a result of satisfying any liability or obligation imposed under such laws; |

| |

| • | risks related to the impact of a loss of any of our key manufacturing facilities; |

| |

| • | risks related to our dependence on key management and other highly skilled personnel; |

| |

| • | risks related to the consolidation of our customer bases, loss of a significant customer, competition and pricing pressure; |

| |

| • | risks related to any potential supply of faulty or contaminated products; |

| |

| • | risks related to exchange rate fluctuations; |

| |

| • | risks related to dependence on the protection of our intellectual property and the development of new products; |

| |

| • | risks related to pension plans sponsored by us and others in our control group; |

| |

| • | risks related to strategic transactions, including completed and future acquisitions or dispositions; |

| |

| • | risks related to our hedging activities which may result in significant losses and in period-to-period earnings volatility; |

| |

| • | risks related to our suppliers of raw materials and any interruption in our supply of raw materials; |

| |

| • | risks related to information security, including a cybersecurity breach or a failure of one or more of our information technology systems, networks, processes or service providers; |

| |

| • | risks related to our substantial indebtedness and our ability to service our current and future indebtedness; |

| |

| • | risks related to restrictive covenants in certain of our outstanding notes and our other indebtedness which could adversely affect our business by limiting our operating and strategic flexibility; and |

| |

| • | risks related to increases in interest rates which would increase the cost of servicing our variable rate debt instruments. |

The risks described above and the risks disclosed in or referred to in “Part II - Other Information — Item 1A. Risk Factors” in this quarterly report and in “Part I — Item 3. Key Information — Risk Factors” of our Annual Report are not exhaustive. Other sections of this quarterly report describe additional factors that could adversely affect our business, financial condition or results of operations. Moreover, we operate in a very competitive and rapidly changing environment. New risk factors emerge from time to time and it is not possible for us to predict all such risk factors, nor can we assess the impact of all such risk factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. Given these risks and uncertainties, you are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. Except as required by law, we undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise. All subsequent written and oral forward-looking statements attributable to us or to persons acting on our behalf are expressly qualified in their entirety by the cautionary statements referred to above and included elsewhere in this quarterly report.

PART I - FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS.

Refer to the attached F pages of this quarterly report for our interim unaudited condensed consolidated financial statements and notes thereto for the three and nine month periods ended September 30, 2019 and September 30, 2018.

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS.

Overview

RGHL was incorporated on May 30, 2006 under the Companies Act 1993 of New Zealand. We are a leading global manufacturer and supplier of consumer food, beverage and foodservice packaging products. We are one of the largest consumer food, beverage and foodservice packaging companies in the United States, as measured by revenue, with leading market positions in many of our product lines based on management’s analysis of industry data. We sell our products to customers globally, including to a diversified mix of leading multinational companies, large national and regional companies, and small local businesses. We primarily serve the consumer, food, beverage and foodservice market segments. We operate through four segments: Reynolds Consumer Products, Pactiv Foodservice, Graham Packaging and Evergreen.

In addition to our four segments, our Other/Unallocated category includes operations which do not meet the quantitative threshold for reportable segments. It also includes holding companies and certain debt issuer companies which support the entire RGHL Group and which are not part of a specific segment, as well as eliminations of transactions between segments.

Our Segments

Reynolds Consumer Products

Reynolds Consumer Products is a leading manufacturer of branded and store branded consumer products such as aluminum foil, wraps, trash bags, food storage bags and disposable tableware and cookware. These products are typically used by consumers in their homes and are sold through a variety of retailers. Reynolds Consumer Products sells many of its products under well known brands such as Reynolds® and Hefty®, and also offers store branded products. Reynolds Consumer Products has a large customer base and operates primarily in North America. Substantially all revenue for Reynolds Consumer Products comes from the U.S. and Canada.

Pactiv Foodservice

Pactiv Foodservice is a leading manufacturer of various foodservice and food packaging products serving the foodservice industry, which includes food processors, restaurants and supermarkets. Pactiv Foodservice offers a comprehensive range of products including tableware items, clear plastic containers, foam containers, paperboard containers, aluminum containers, microwaveable containers, clear rigid-display packaging, molded fiber and plastic egg cartons, foam and rigid trays, absorbent tray pads and plastic film. Pactiv Foodservice has a large customer base and operates primarily in North America.

Graham Packaging

Graham Packaging is a leading designer and manufacturer of value-added, custom blow-molded plastic containers for branded consumer products. Graham Packaging focuses on product categories where customers and end-users value the technology and innovation that Graham Packaging's custom plastic containers offer as an alternative to traditional packaging materials such as glass, metal and paperboard. Graham Packaging has a large global customer base with its largest presence in North America.

Evergreen

Evergreen is a vertically integrated, leading manufacturer of fresh carton packaging for beverage products, primarily serving the juice and milk markets. Fresh carton packaging, most predominant in North America, is primarily used for beverages that require a cold-chain distribution system. Evergreen supplies integrated fresh carton packaging systems, which can include fresh cartons, spouts and filling machines. Evergreen produces liquid packaging board for its internal requirements and to sell to other fresh beverage carton manufacturers. Evergreen also produces paper products, including coated groundwood primarily for catalogs, inserts, magazine and commercial printing, and uncoated freesheet primarily for envelope, specialty and offset printing paper. Evergreen has a large customer base and operates primarily in North America.

Strategic Reviews and Discontinued Operations

Closures

Closures manufactures plastic and aluminum beverage caps, closures and high speed rotary capping equipment. In our 2018 annual report, we announced that we had commenced a strategic review of our Closures business. As a result of the status of the strategic review process, the North American and Japanese closures businesses were classified as held for sale as of September 30, 2019 and the results presented as discontinued operations for the three and nine month periods ended September 30, 2019 and 2018.

On October 11, 2019, we entered into an agreement pursuant to which we will sell our North American and Japanese closures businesses, to an affiliate of Cerberus Capital Management, L.P. The purchase price is $615 million, subject to certain adjustments based upon closing date cash, indebtedness and working capital. These operations represent substantially all of our Closures segment.

We will retain and continue to operate our remaining closures businesses in Europe, the Middle East, Egypt (collectively, “EMEA”) and South America.

The results and financial position for all periods of our remaining closures businesses have been presented within the Other/Unallocated category, as they do not meet the quantitative threshold for a reportable segment. For additional information, refer to notes 2.2 and 7 of the RGHL Group’s interim unaudited condensed consolidated financial statements included elsewhere in this quarterly report.

Reynolds Consumer Products

We are currently undertaking a strategic review of our Reynolds Consumer Products business. This review may result in an initial public offering of common stock or a sale of that business, though no decision has been made at this time.

Key Factors Influencing Our Financial Condition and Results of Operations

The following discussion should be read in conjunction with “Key Factors Influencing Our Financial Condition and Results of Operations” in “Part I — Item 5. Operating and Financial Review and Prospects” of our Annual Report, which discusses further key factors influencing our financial condition and results of operations.

Substantial Leverage

The four segments in which we operate have all been acquired through a series of transactions. Our results of operations, financial position and cash flows are significantly impacted by the effects of these acquisitions, which were financed primarily through borrowings, including recurring interest costs and transaction-related debt commitment fees. In addition, from time to time, we refinance our borrowings which also can have a significant impact on our results of operations.

As of September 30, 2019, our total indebtedness of $11,032 million was comprised of the outstanding principal amounts of our borrowings. As reflected in our consolidated statement of financial position, we had total borrowings of $10,985 million, consisting of total indebtedness net of unamortized transaction costs, original issue discounts and embedded derivatives. For more information regarding our external borrowings, refer to note 12 of the RGHL Group’s interim unaudited condensed consolidated financial statements included elsewhere in this quarterly report. Our future results of operations, including our net financial expenses, will be significantly affected by our substantial indebtedness. The servicing of this indebtedness has had and will continue to have an impact on our cash flows and cash balance. For more information, refer to “— Liquidity and Capital Resources.”

Raw Materials and Energy Prices

Our results of operations, and the gross margins corresponding to each of our segments, are impacted by changes in the costs of our raw materials and energy prices. The primary raw materials used to manufacture our products are plastic resins, aluminum, fiber (principally raw wood and wood chips) and paperboard (principally cartonboard and cupstock). We also use commodity chemicals, steel and energy, including fuel oil, electricity, natural gas and coal, to manufacture our products.

Principal raw materials used by each of our segments are as follows (in order of cost significance):

| |

| • | Reynolds Consumer Products — resin, aluminum |

| |

| • | Pactiv Foodservice — resin, paperboard, aluminum |

| |

| • | Graham Packaging — resin |

| |

| • | Evergreen — fiber, resin |

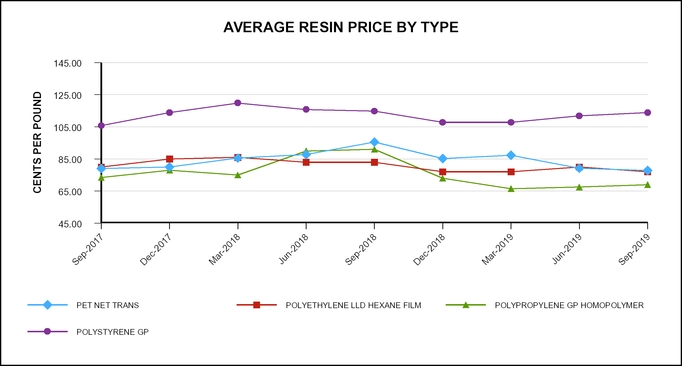

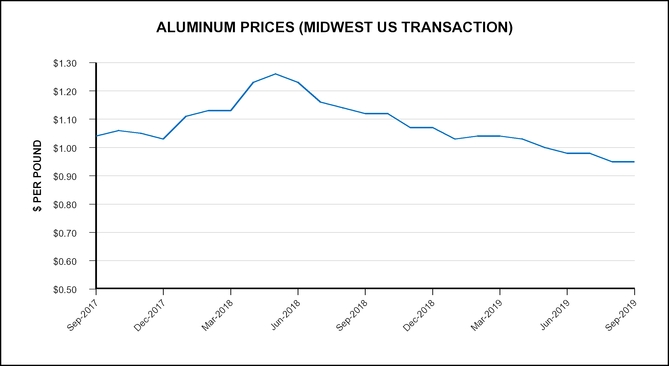

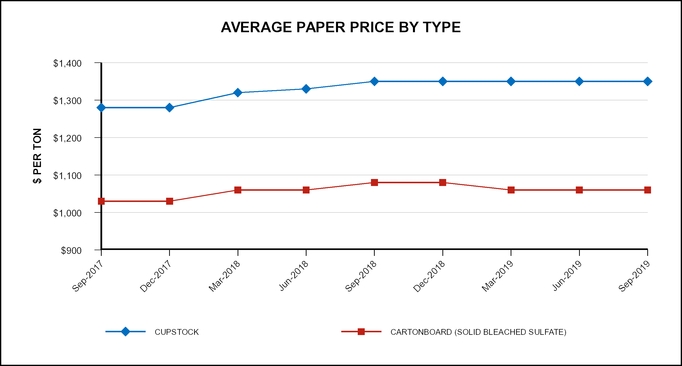

Historical index prices of resin, aluminum and paperboard for the past two years are shown in the charts below. These charts present index prices and do not represent the prices at which we purchased these raw materials.

Source: IHS Inc.

Resin prices can fluctuate significantly with fluctuations in crude oil and natural gas prices, as well as changes in refining capacity and the demand for other petroleum-based products.

Source: Platts Metals Weekly

Aluminum prices can fluctuate significantly as aluminum is a cyclical commodity with prices subject to global market factors. These factors include speculative activities by market participants, production capacity, strength or weakness in key end-markets such as housing and transportation, political and economic conditions and production costs in major production regions.

Source: RISI, Inc.

The prices of cupstock and cartonboard may fluctuate due to external conditions such as weather, product scarcity, currency and commodity market fluctuations and changes in governmental policies and regulations.

Results of Operations

The following discussion should be read in conjunction with the RGHL Group’s interim unaudited condensed consolidated financial statements included elsewhere in this quarterly report. Detailed comparisons of revenue and results of operations are presented in the discussions of the operating segments, which follow the RGHL Group results discussion.

Three month period ended September 30, 2019 compared to the three month period ended September 30, 2018

RGHL Group

|

| | | | | | | | | | | | | | | | | | |

| | | For the three month period ended September 30, | | | | |

| (In $ million, except for %) | | 2019 | | % of revenue | | 2018(2) | | % of revenue | | Change | | % change |

| Revenue | | 2,408 |

| | 100 | % | | 2,536 |

| | 100 | % | | (128 | ) | | (5 | )% |

| Cost of sales | | (1,924 | ) | | (80 | )% | | (2,019 | ) | | (80 | )% | | 95 |

| | 5 | % |

| Gross profit | | 484 |

| | 20 | % | | 517 |

| | 20 | % | | (33 | ) | | (6 | )% |

| Selling, marketing and distribution expenses/General and administration expenses | | (257 | ) | | (11 | )% | | (217 | ) | | (9 | )% | | (40 | ) | | (18 | )% |

| Net other income (expenses) | | (98 | ) | | (4 | )% | | (12 | ) | | — | % | | (86 | ) | | NM |

|

| Profit from operating activities | | 129 |

| | 5 | % | | 288 |

| | 11 | % | | (159 | ) | | (55 | )% |

| Financial income | | 98 |

| | 4 | % | | 132 |

| | 5 | % | | (34 | ) | | (26 | )% |

| Financial expenses | | (163 | ) | | (7 | )% | | (156 | ) | | (6 | )% | | (7 | ) | | (4 | )% |

| Net financial income (expenses) | | (65 | ) | | (3 | )% | | (24 | ) | | (1 | )% | | (41 | ) | | NM |

|

| Profit (loss) from continuing operations before income tax | | 64 |

| | 3 | % | | 264 |

| | 10 | % | | (200 | ) | | (76 | )% |

| Income tax (expense) benefit | | 7 |

| | — | % | | (82 | ) | | (3 | )% | | 89 |

| | NM |

|

| Profit (loss) from continuing operations | | 71 |

| | 3 | % | | 182 |

| | 7 | % | | (111 | ) | | (61 | )% |

| Profit (loss) from discontinued operations, net of income tax | | (31 | ) | | NM |

| | 17 |

| | NM |

| | (48 | ) | | NM |

|

| Profit (loss) for the period | | 40 |

| | NM |

| | 199 |

| | NM |

| | (159 | ) | | (80 | )% |

| Depreciation and amortization from continuing operations | | 174 |

| | 7 | % | | 145 |

| | 6 | % | | (29 | ) | | (20 | )% |

RGHL Group Adjusted EBITDA(1) from continuing operations | | 455 |

| | 19 | % | | 473 |

| | 19 | % | | (18 | ) | | (4 | )% |

| RGHL Group Adjusted EBITDA from discontinued operations | | 31 |

| | NM |

| | 26 |

| | NM |

| | 5 |

| | 19 | % |

| Total Adjusted EBITDA | | 486 |

| | NM |

| | 499 |

| | NM |

| | (13 | ) | | (3 | )% |

| |

| (1) | Refer to page 2 under the heading “Non-GAAP Financial Measures” for additional information related to this financial measure. |

| |

| (2) | The information presented has been revised to reflect the North American and Japanese closures businesses as discontinued operations. Refer to notes 2.2 and 7 of the RGHL Group’s interim unaudited condensed consolidated financial statements included elsewhere in this quarterly report for additional information. |

Revenue. Revenue decreased by $128 million, or 5%.The decrease was primarily due to lower sales volume, lower pricing and the impact of business divestitures.

Cost of Sales. Cost of sales decreased by $95 million, or 5%. The decrease was primarily due to lower raw material costs, lower sales volume and the impact of business divestitures, partially offset by higher manufacturing costs. The adoption of the new lease accounting standard, IFRS 16 “Leases,” resulted in a portion of operating lease expense now being classified as depreciation expense (refer to note 2 of the RGHL Group’s interim unaudited condensed consolidated financial statements included elsewhere in this quarterly report).

Selling, Marketing and Distribution Expenses/General and Administration Expenses. Selling, marketing and distribution expenses and general and administration expenses increased by $40 million, or 18%. The increase was primarily due to higher employee-related costs, as well as higher strategic review costs of $19 million, which has been included in the RGHL Group’s Adjusted EBITDA calculation.

Net Other. Net other expenses increased by $86 million to $98 million. The increase was primarily due to higher asset impairment charges, which included $67 million at the remaining EMEA and South American closures businesses as a result of dissynergies associated with the pending sale of the North American and Japanese closures businesses, as well as an unfavorable change in gains and losses on sale of businesses. These items have been included in the RGHL Group’s Adjusted EBITDA calculation.

Net Financial Income (Expenses). Net financial expenses increased by $41 million to $65 million. The increase was primarily due to an unfavorable change of $74 million in the fair value of derivatives, partially offset by a $36 million favorable foreign currency impact. For more information regarding financial income (expenses), refer to note 8 of the RGHL Group’s interim unaudited condensed consolidated financial statements included elsewhere in this quarterly report.

Income Tax. We recognized income tax benefit of $7 million on income before income tax of $64 million (an effective tax rate of (11)%) in the three month period ended September 30, 2019 as compared to income tax expense of $82 million on income before income tax of $264 million (an effective tax rate of 31%) for the three month period ended September 30, 2018. Factors that have contributed to the effective tax rate include (i) a tax benefit for refunds associated with foreign tax credits, (ii) no tax benefit for certain impairment charges and (iii) the mix of book income and

losses taxed at varying rates among the jurisdictions in which the RGHL Group operates. For further information, including a reconciliation of income tax expense, refer to note 9 of the RGHL Group’s interim unaudited condensed consolidated financial statements included elsewhere in this quarterly report.

Profit (Loss) from Discontinued Operations, Net of Income Tax. Profit (loss) from discontinued operations, net of income tax, which represents the results of the North American and Japanese closures businesses, changed by $48 million, resulting in loss from discontinued operations of $31 million. The change was primarily due to a $33 million goodwill impairment charge, higher strategic review costs and lower pricing primarily due to lower costs passed through to customers, partially offset by lower raw material costs. For more information regarding discontinued operations, refer to notes 2.2 and 7 of the RGHL Group’s interim unaudited condensed consolidated financial statements included elsewhere in this quarterly report.

Depreciation and Amortization. Depreciation and amortization increased by $29 million. The increase was primarily due to the impact of the new lease accounting standard.

Impact of IFRS 16. The adoption of the new lease accounting standard, IFRS 16, has resulted in a portion of operating lease expense being classified as depreciation and interest expense. Under the transition method chosen by the RGHL Group, the comparative information has not been restated. For further information, refer to note 2 of the RGHL Group’s interim unaudited condensed consolidated financial statements included elsewhere in this quarterly report. The following table sets out the benefit to Adjusted EBITDA by segment for the three month period ended September 30, 2019:

|

| | | |

| (In $ million) | | For the three month period ended September 30, 2019 |

| Reynolds Consumer Products | | 4 |

|

| Pactiv Foodservice | | 9 |

|

| Graham Packaging | | 8 |

|

| Evergreen | | 2 |

|

| Other/Unallocated | | 2 |

|

| Total impact of IFRS 16 on RGHL Group Adjusted EBITDA from continuing operations | | 25 |

|

| Total impact of IFRS 16 on RGHL Group Adjusted EBITDA from discontinued operations | | 1 |

|

| Total impact of IFRS 16 on RGHL Group Adjusted EBITDA | | 26 |

|

EBITDA/Adjusted EBITDA Reconciliation

The reconciliation of profit from operating activities to EBITDA and Adjusted EBITDA for the RGHL Group is as follows:

|

| | | | | | |

| | | For the three month period ended September 30, |

| (In $ million) | | 2019 | | 2018(2) |

| Profit from operating activities | | 129 |

| | 288 |

|

| Depreciation and amortization from continuing operations | | 174 |

| | 145 |

|

RGHL Group EBITDA(1) from continuing operations | | 303 |

| | 433 |

|

| Included in the RGHL Group EBITDA: | | | | |

| Asset impairment charges, net of reversals | | 77 |

| | 6 |

|

| (Gain) loss on sale of businesses and non-current assets | | 18 |

| | 1 |

|

| Non-cash pension expense | | 19 |

| | 15 |

|

| Operational process engineering-related consultancy costs | | 6 |

| | 3 |

|

| Related party management fee | | 7 |

| | 7 |

|

| Restructuring costs, net of reversals | | 5 |

| | 5 |

|

| Strategic review costs | | 19 |

| | — |

|

| Other | | 1 |

| | 3 |

|

| RGHL Group Adjusted EBITDA from continuing operations | | 455 |

| | 473 |

|

| | | | | |

| Segment detail of Adjusted EBITDA: | | | | |

| Reynolds Consumer Products | | 164 |

| | 163 |

|

| Pactiv Foodservice | | 158 |

| | 162 |

|

| Graham Packaging | | 92 |

| | 92 |

|

| Evergreen | | 47 |

| | 63 |

|

| Other/Unallocated | | (6 | ) | | (7 | ) |

RGHL Group Adjusted EBITDA from continuing operations | | 455 |

| | 473 |

|

| RGHL Group Adjusted EBITDA from discontinued operations | | 31 |

| | 26 |

|

| Total Adjusted EBITDA | | 486 |

| | 499 |

|

(1) Refer to page 2 under the heading “Non-GAAP Financial Measures” for additional information related to these financial measures.

| |

| (2) | The information presented has been revised to reflect the North American and Japanese closures businesses as discontinued operations. Refer to notes 2.2 and 7 of the RGHL Group’s interim unaudited condensed consolidated financial statements included elsewhere in this quarterly report for additional information. |

Reynolds Consumer Products Segment

|

| | | | | | | | | | | | | | | | | | |

| | | For the three month period ended September 30, | | | | |

| (In $ million, except for %) | | 2019 | | % of segment revenue | | 2018 | | % of segment revenue | | Change | | % change |

| External revenue | | 699 |

| | 95 | % | | 731 |

| | 94 | % | | (32 | ) | | (4 | )% |

| Inter-segment revenue | | 38 |

| | 5 | % | | 44 |

| | 6 | % | | (6 | ) | | (14 | )% |

| Total segment revenue | | 737 |

| | 100 | % | | 775 |

| | 100 | % | | (38 | ) | | (5 | )% |

| Cost of sales | | (525 | ) | | (71 | )% | | (567 | ) | | (73 | )% | | 42 |

| | 7 | % |

| Gross profit | | 212 |

| | 29 | % | | 208 |

| | 27 | % | | 4 |

| | 2 | % |

| Selling, marketing and distribution expenses/ General and administration expenses | | (74 | ) | | (10 | )% | | (67 | ) | | (9 | )% | | (7 | ) | | (10 | )% |

| Net other income (expenses) | | 1 |

| | — | % | | — |

| | — | % | | 1 |

| | NM |

|

| Profit from operating activities | | 139 |

| | 19 | % | | 141 |

| | 18 | % | | (2 | ) | | (1 | )% |

| Reynolds Consumer Products segment Adjusted EBITDA | | 164 |

| | 22 | % | | 163 |

| | 21 | % | | 1 |

| | 1 | % |

Revenue. Total segment revenue decreased by $38 million, or 5%. The decrease was primarily due to lower pricing, mainly due to higher trade spend, and decreased sales volume.

Cost of Sales. Cost of sales decreased by $42 million, or 7%. The decrease was primarily due to lower raw material costs and decreased sales volume, partially offset by higher manufacturing costs. For the three month periods ended September 30, 2019 and September 30, 2018, raw material costs accounted for 60% and 64% of Reynolds Consumer Products’ cost of sales, respectively.

Selling, Marketing and Distribution Expenses/General and Administration Expenses. Selling, marketing and distribution expenses and general and administration expenses increased by $7 million, or 10%, primarily due to higher employee-related costs.

Net Other. Net other income increased to $1 million.

EBITDA/Adjusted EBITDA Reconciliation

The reconciliation of profit from operating activities to EBITDA and Adjusted EBITDA for our Reynolds Consumer Products segment is as follows:

|

| | | | | | |

| | | For the three month period ended September 30, |

| (In $ million) | | 2019 | | 2018 |

| Profit from operating activities | | 139 |

| | 141 |

|

| Depreciation and amortization | | 23 |

| | 20 |

|

| EBITDA | | 162 |

| | 161 |

|

| Included in Reynolds Consumer Products segment EBITDA: | | | | |

| Other | | 2 |

| | 2 |

|

| Reynolds Consumer Products segment Adjusted EBITDA | | 164 |

| | 163 |

|

Pactiv Foodservice Segment

|

| | | | | | | | | | | | | | | | | | |

| | | For the three month period ended September 30, | | | | |

| (In $ million, except for %) | | 2019 | | % of segment revenue | | 2018 | | % of segment revenue | | Change | | % change |

| External revenue | | 824 |

| | 87 | % | | 837 |

| | 86 | % | | (13 | ) | | (2 | )% |

| Inter-segment revenue | | 119 |

| | 13 | % | | 134 |

| | 14 | % | | (15 | ) | | (11 | )% |

| Total segment revenue | | 943 |

| | 100 | % | | 971 |

| | 100 | % | | (28 | ) | | (3 | )% |

| Cost of sales | | (782 | ) | | (83 | )% | | (798 | ) | | (82 | )% | | 16 |

| | 2 | % |

| Gross profit | | 161 |

| | 17 | % | | 173 |

| | 18 | % | | (12 | ) | | (7 | )% |

| Selling, marketing and distribution expenses/ General and administration expenses | | (68 | ) | | (7 | )% | | (60 | ) | | (6 | )% | | (8 | ) | | (13 | )% |

| Net other income (expenses) | | (2 | ) | | — | % | | (1 | ) | | — | % | | (1 | ) | | (100 | )% |

| Profit from operating activities | | 91 |

| | 10 | % | | 112 |

| | 12 | % | | (21 | ) | | (19 | )% |

| Pactiv Foodservice segment Adjusted EBITDA | | 158 |

| | 17 | % | | 162 |

| | 17 | % | | (4 | ) | | (2 | )% |

Revenue. Total segment revenue decreased by $28 million, or 3%. The decrease was primarily due to lower pricing primarily due to lower costs passed through to customers, lower inter-segment revenues and the impact of business divestitures, partially offset by higher sales volume with external customers.

Cost of Sales. Cost of sales decreased by $16 million, or 2%. The decrease was primarily due to lower raw material costs and the impact of business divestitures, partially offset by higher volume and higher manufacturing and logistics costs. For the three month periods ended September 30, 2019 and September 30, 2018, raw material costs accounted for 55% and 62% of Pactiv Foodservice’s cost of sales, respectively.

Selling, Marketing and Distribution Expenses/General and Administration Expenses. Selling, marketing and distribution expenses and general and administration expenses increased by $8 million, or 13%. The increase was primarily due to higher employee-related costs.

Net Other. Net other expenses increased by $1 million to $2 million.

EBITDA/Adjusted EBITDA Reconciliation

The reconciliation of profit from operating activities to EBITDA and Adjusted EBITDA for our Pactiv Foodservice segment is as follows:

|

| | | | | | |

| | | For the three month period ended September 30, |

| (In $ million) | | 2019 | | 2018 |

| Profit from operating activities | | 91 |

| | 112 |

|

| Depreciation and amortization | | 62 |

| | 47 |

|

| EBITDA | | 153 |

| | 159 |

|

| Included in Pactiv Foodservice segment EBITDA: | | | | |

| Operational process engineering-related consultancy costs | | 4 |

| | 3 |

|

| Other | | 1 |

| | — |

|

| Pactiv Foodservice segment Adjusted EBITDA | | 158 |

| | 162 |

|

Graham Packaging Segment

|

| | | | | | | | | | | | | | | | | | |

| | | For the three month period ended September 30, | | | | |

| (In $ million, except for %) | | 2019 | | % of segment revenue | | 2018 | | % of segment revenue | | Change | | % change |

| External revenue | | 475 |

| | 100 | % | | 532 |

| | 100 | % | | (57 | ) | | (11 | )% |

| Inter-segment revenue | | — |

| | — | % | | — |

| | — | % | | — |

| | — | % |

| Total segment revenue | | 475 |

| | 100 | % | | 532 |

| | 100 | % | | (57 | ) | | (11 | )% |

| Cost of sales | | (411 | ) | | (87 | )% | | (461 | ) | | (87 | )% | | 50 |

| | 11 | % |

| Gross profit | | 64 |

| | 13 | % | | 71 |

| | 13 | % | | (7 | ) | | (10 | )% |

| Selling, marketing and distribution expenses/General and administration expenses | | (45 | ) | | (9 | )% | | (43 | ) | | (8 | )% | | (2 | ) | | (5 | )% |

| Net other income (expenses) | | (13 | ) | | (3 | )% | | (5 | ) | | (1 | )% | | (8 | ) | | NM |

|

| Profit from operating activities | | 6 |

| | 1 | % | | 23 |

| | 4 | % | | (17 | ) | | (74 | )% |

| Graham Packaging segment Adjusted EBITDA | | 92 |

| | 19 | % | | 92 |

| | 17 | % | | — |

| | — | % |

Revenue. Total segment revenue decreased by $57 million, or 11%. The decrease was primarily due to lower sales volume and lower pricing primarily due to lower costs passed through to customers.

Cost of Sales. Cost of sales decreased by $50 million, or 11%. The decrease was primarily due to lower raw material costs and lower sales volume. For the three month periods ended September 30, 2019 and September 30, 2018, raw material costs accounted for 50% and 53% of Graham Packaging’s cost of sales, respectively.

Selling, Marketing and Distribution Expenses/General and Administration Expenses. Selling, marketing and distribution expenses and general and administration expenses increased by $2 million, or 5%.

Net Other. Net other expenses increased by $8 million to $13 million. The increase was primarily due to a net loss on sale of businesses and non-current assets in the current year and higher asset impairment charges related to plant rationalizations. These items have been included in the segment’s Adjusted EBITDA calculation.

EBITDA/Adjusted EBITDA Reconciliation

The reconciliation of profit from operating activities to EBITDA and Adjusted EBITDA for our Graham Packaging segment is as follows:

|

| | | | | | |

| | | For the three month period ended September 30, |

| (In $ million) | | 2019 | | 2018 |

| Profit from operating activities | | 6 |

| | 23 |

|

| Depreciation and amortization | | 69 |

| | 61 |

|

| EBITDA | | 75 |

| | 84 |

|

| Included in Graham Packaging segment EBITDA: | | | | |

| Asset impairment charges, net of reversals | | 9 |

| | 5 |

|

| (Gain) loss on sale of businesses and non-current assets | | 5 |

| | — |

|

| Other | | 3 |

| | 3 |

|

| Graham Packaging segment Adjusted EBITDA | | 92 |

| | 92 |

|

Evergreen Segment

|

| | | | | | | | | | | | | | | | | | |

| | | For the three month period ended September 30, | | | | |

| (In $ million, except for %) | | 2019 | | % of segment revenue | | 2018 | | % of segment revenue | | Change | | % change |

| External revenue | | 372 |

| | 93 | % | | 382 |

| | 93 | % | | (10 | ) | | (3 | )% |

| Inter-segment revenue | | 29 |

| | 7 | % | | 27 |

| | 7 | % | | 2 |

| | 7 | % |

| Total segment revenue | | 401 |

| | 100 | % | | 409 |

| | 100 | % | | (8 | ) | | (2 | )% |

| Cost of sales | | (358 | ) | | (89 | )% | | (347 | ) | | (85 | )% | | (11 | ) | | (3 | )% |

| Gross profit | | 43 |

| | 11 | % | | 62 |

| | 15 | % | | (19 | ) | | (31 | )% |

| Selling, marketing and distribution expenses/ General and administration expenses | | (19 | ) | | (5 | )% | | (15 | ) | | (4 | )% | | (4 | ) | | (27 | )% |

| Net other income (expenses) | | 1 |

| | — | % | | — |

| | — | % | | 1 |

| | NM |

|

| Profit from operating activities | | 25 |

| | 6 | % | | 47 |

| | 11 | % | | (22 | ) | | (47 | )% |

| Evergreen segment Adjusted EBITDA | | 47 |

| | 12 | % | | 63 |

| | 15 | % | | (16 | ) | | (25 | )% |

Revenue. Total segment revenue decreased by $8 million, or 2%. The decrease was primarily due to lower sales volume, partially offset by higher pricing.

Cost of Sales. Cost of sales increased by $11 million, or 3%. The increase was primarily due to higher manufacturing costs and higher raw material costs, primarily fiber, partially offset by lower sales volume. For the three month periods ended September 30, 2019 and September 30, 2018, raw material costs accounted for 38% and 39% of Evergreen’s cost of sales, respectively.

Selling, Marketing and Distribution Expenses/General and Administration Expenses. Selling, marketing and distribution expenses and general and administration expenses increased by $4 million, or 27%, primarily due to higher employee-related costs.

Net Other. Net other income increased to $1 million.

EBITDA/Adjusted EBITDA Reconciliation

The reconciliation of profit from operating activities to EBITDA and Adjusted EBITDA for our Evergreen segment is as follows:

|

| | | | | | |

| | | For the three month period ended September 30, |

| (In $ million) | | 2019 | | 2018 |

| Profit from operating activities | | 25 |

| | 47 |

|

| Depreciation and amortization | | 18 |

| | 15 |

|

| EBITDA | | 43 |

| | 62 |

|

| Included in Evergreen segment EBITDA: | | | | |

| Other | | 4 |

| | 1 |

|

| Evergreen segment Adjusted EBITDA | | 47 |

| | 63 |

|

Other/Unallocated

|

| | | | | | | | | | | | |

| | | For the three month period ended September 30, | | | | |

| (In $ million, except for %) | | 2019 | | 2018(1) | | Change | | % change |

| External revenue | | 38 |

| | 54 |

| | (16 | ) | | (30 | )% |

| Inter-segment revenue/eliminations | | (186 | ) | | (205 | ) | | 19 |

| | 9 | % |

| Total revenue | | (148 | ) | | (151 | ) | | 3 |

| | 2 | % |

| Cost of sales | | 152 |

| | 154 |

| | (2 | ) | | (1 | )% |

| Gross profit | | 4 |

| | 3 |

| | 1 |

| | 33 | % |

| Selling, marketing and distribution expenses/General and administration expenses | | (51 | ) | | (32 | ) | | (19 | ) | | (59 | )% |

| Net other income (expenses) | | (85 | ) | | (6 | ) | | (79 | ) | | NM |

|

| Loss from operating activities | | (132 | ) | | (35 | ) | | (97 | ) | | NM |

|

| Other/Unallocated Adjusted EBITDA | | (6 | ) | | (7 | ) | | 1 |

| | 14 | % |

| |

| (1) | The information presented has been revised to include the results of our remaining closures businesses. Refer to note 2.2 of the RGHL Group’s interim unaudited condensed consolidated financial statements included elsewhere in this quarterly report for additional information. |

Revenue. External revenue decreased by $16 million, or 30%. The decrease was primarily due to the impact of business divestitures and lower sales volume.

Cost of Sales. Cost of sales decreased by $2 million, or 1%.

Selling, Marketing and Distribution Expenses/General and Administration Expenses. Selling, marketing and distribution expenses and general and administration expenses increased by $19 million, or 59%. The increase was primarily due to $18 million of higher strategic review costs. This item has been included in the Adjusted EBITDA calculation.

Net Other. Net other expenses increased by $79 million to $85 million. The increase was primarily due to higher asset impairment charges of $67 million at the remaining closures businesses as a result of dis-synergies associated with the pending sale of the North American and Japanese closures businesses and an unfavorable change in gains and losses on sale of businesses and non-current assets. These items have been included in the Adjusted EBITDA calculation.

EBITDA/Adjusted EBITDA Reconciliation

The reconciliation of loss from operating activities to EBITDA and Adjusted EBITDA for Other/Unallocated is as follows:

|

| | | | | | |

| | | For the three month period ended September 30, |

| (In $ million) | | 2019 | | 2018(1) |

| Loss from operating activities | | (132 | ) | | (35 | ) |

| Depreciation and amortization | | 2 |

| | 2 |

|

| EBITDA | | (130 | ) | | (33 | ) |

| Included in Other/Unallocated EBITDA: | | | | |

| Asset impairment charges, net of reversals | | 67 |

| | — |

|

| (Gain) loss on sale of businesses and non-current assets | | 13 |

| | 1 |

|

| Non-cash pension expense | | 19 |

| | 15 |

|

| Related party management fee | | 7 |

| | 7 |

|

| Strategic review costs | | 18 |

| | — |

|

| Other | | — |

| | 3 |

|

| Other/Unallocated Adjusted EBITDA | | (6 | ) | | (7 | ) |

| |

| (1) | The information presented has been revised to include the results of our remaining closures businesses. Refer to note 2.2 of the RGHL Group’s interim unaudited condensed consolidated financial statements included elsewhere in this quarterly report for additional information. |

Results of Operations

Nine month period ended September 30, 2019 compared to the nine month period ended September 30, 2018

RGHL Group

|

| | | | | | | | | | | | | | | | | | |

| | | For the nine month period ended September 30, | | | | |

| (In $ million, except for %) | | 2019 | | % of revenue | | 2018(2) | | % of revenue | | Change | | % change |

| Revenue | | 7,243 |

| | 100 | % | | 7,464 |

| | 100 | % | | (221 | ) | | (3 | )% |

| Cost of sales | | (5,793 | ) | | (80 | )% | | (6,010 | ) | | (81 | )% | | 217 |

| | 4 | % |

| Gross profit | | 1,450 |

| | 20 | % | | 1,454 |

| | 19 | % | | (4 | ) | | — | % |

| Selling, marketing and distribution expenses/General and administration expenses | | (764 | ) | | (11 | )% | | (683 | ) | | (9 | )% | | (81 | ) | | (12 | )% |

| Net other income (expenses) | | (122 | ) | | (2 | )% | | (39 | ) | | (1 | )% | | (83 | ) | | NM |

|

| Profit from operating activities | | 564 |

| | 8 | % | | 732 |

| | 10 | % | | (168 | ) | | (23 | )% |

| Financial income | | 185 |

| | 3 | % | | 37 |

| | — | % | | 148 |

| | NM |

|

| Financial expenses | | (491 | ) | | (7 | )% | | (489 | ) | | (7 | )% | | (2 | ) | | — | % |

| Net financial income (expenses) | | (306 | ) | | (4 | )% | | (452 | ) | | (6 | )% | | 146 |

| | 32 | % |

| Profit (loss) from continuing operations before income tax | | 258 |

| | 4 | % | | 280 |

| | 4 | % | | (22 | ) | | (8 | )% |

| Income tax (expense) benefit | | (71 | ) | | (1 | )% | | (78 | ) | | (1 | )% | | 7 |

| | 9 | % |

| Profit (loss) from continuing operations | | 187 |

| | 3 | % | | 202 |

| | 3 | % | | (15 | ) | | (7 | )% |

| Profit (loss) from discontinued operations, net of income tax | | (2 | ) | | NM |

| | 29 |

| | NM |

| | (31 | ) | | NM |

|

| Profit (loss) for the period | | 185 |

| | NM |

| | 231 |

| | NM |

| | (46 | ) | | (20 | )% |

| Depreciation and amortization from continuing operations | | 514 |

| | 7 | % | | 457 |

| | 6 | % | | (57 | ) | | (12 | )% |

RGHL Group Adjusted EBITDA(1) from continuing operations | | 1,325 |

| | 18 | % | | 1,295 |

| | 17 | % | | 30 |

| | 2 | % |

| RGHL Group Adjusted EBITDA from discontinued operations | | 87 |

| | NM |

| | 81 |

| | NM |

| | 6 |

| | 7 | % |

| Total Adjusted EBITDA | | 1,412 |

| | NM |

| | 1,376 |

| | NM |

| | 36 |

| | 3 | % |

| |

| (1) | Refer to page 2 under the heading “Non-GAAP Financial Measures” for additional information related to this financial measure. |

| |

| (2) | The information presented has been revised to reflect the North American and Japanese closures businesses as discontinued operations. Refer to notes 2.2 and 7 of the RGHL Group’s interim unaudited condensed consolidated financial statements included elsewhere in this quarterly report for additional information. |

Revenue. Revenue decreased by $221 million, or 3%. The decrease was primarily due to lower sales volume, the impact of business divestitures and an unfavorable foreign currency impact, partially offset by higher pricing.

Cost of Sales. Cost of sales decreased by $217 million, or 4%. The decrease was primarily due to lower raw material costs, lower sales volume and the impact of business divestitures, partially offset by higher manufacturing costs. The adoption of the new lease accounting standard, IFRS 16 “Leases,” resulted in a portion of operating lease expense now being classified as depreciation expense (refer to note 2 of the RGHL Group’s interim unaudited condensed consolidated financial statements included elsewhere in this quarterly report).

Selling, Marketing and Distribution Expenses/General and Administration Expenses. Selling, marketing and distribution expenses and general and administration expenses increased by $81 million, or 12%. The increase was primarily due to higher employee-related costs, including $14 million of additional pension expense associated with the Pactiv Retirement Plan, as well as $20 million of higher strategic review costs. The expense associated with the Pactiv Retirement plan and the strategic review costs have been included in the RGHL Group’s Adjusted EBITDA calculation.

Net Other. Net other expenses increased by $83 million to $122 million. The increase was primarily due to higher asset impairment charges, which included $67 million at the remaining EMEA and South American closures businesses as a result of dis-synergies associated with the pending sale of the North American and Japanese closures businesses and a $37 million unfavorable change in gains (losses) on the sale of businesses and non-current assets, partially offset by a favorable change in unrealized gains and losses on derivatives. These items have been included in the RGHL Group’s Adjusted EBITDA calculation.

Net Financial Income (Expenses). Net financial expenses decreased by $146 million to $306 million. The decrease was primarily due to a favorable change of $146 million in the fair value of derivatives and a $20 million favorable foreign currency impact, partially offset by a $30 million increase in interest expense. For more information regarding financial income (expenses) and borrowings, refer to notes 8 and 12, respectively, of the RGHL Group’s interim unaudited condensed consolidated financial statements included elsewhere in this quarterly report.

Income Tax. We recognized income tax expense of $71 million on income before income tax of $258 million (an effective tax rate of 28%) in the nine month period ended September 30, 2019 as compared to income tax expense of $78 million on income before income tax of $280 million (an effective tax rate of 28%) for the nine month period ended September 30, 2018. Factors that have contributed to the effective tax rate include (i) a tax benefit for refunds associated with foreign tax credits, (ii) no tax benefit for certain impairment charges and (iii) the mix of book income and losses taxed at varying rates among the jurisdictions in which the RGHL Group operates. For further information, including a reconciliation of income

tax expense, refer to note 9 of the RGHL Group’s interim unaudited condensed consolidated financial statements included elsewhere in this quarterly report.

Profit (Loss) from Discontinued Operations, Net of Income Tax. Profit (loss) from discontinued operations, net of income tax, which represents the results of the North American and Japanese closures businesses, changed by $31 million, resulting in loss from discontinued operations of $2 million. The change was primarily due to a $33 million goodwill impairment charge, higher strategic review costs and lower pricing primarily due to lower costs passed through to customers, partially offset by lower raw material costs. For more information regarding discontinued operations, refer to notes 2.2 and 7 of the RGHL Group’s interim unaudited condensed consolidated financial statements included elsewhere in this quarterly report.

Depreciation and Amortization. Depreciation and amortization increased by $57 million. The increase was primarily due to the impact of the new lease accounting standard.

Impact of IFRS 16. The adoption of the new lease accounting standard, IFRS 16, has resulted in a portion of operating lease expense being classified as depreciation and interest expense. Under the transition method chosen by the RGHL Group, the comparative information has not been restated. For further information, refer to note 2 of the RGHL Group’s interim unaudited condensed consolidated financial statements included elsewhere in this quarterly report. The following table sets out the benefit to Adjusted EBITDA by segment for the nine month period ended September 30, 2019:

|

| | | |

| (In $ million) | | For the nine month period ended September 30, 2019 |

| Reynolds Consumer Products | | 10 |

|

| Pactiv Foodservice | | 28 |

|

| Graham Packaging | | 24 |

|

| Evergreen | | 6 |

|

| Other/Unallocated | | 3 |

|

| Total impact of IFRS 16 on RGHL Group Adjusted EBITDA from continuing operations | | 71 |

|

| Total impact of IFRS 16 on RGHL Group Adjusted EBITDA from discontinued operations | | 4 |

|

| Total impact of IFRS 16 on RGHL Group Adjusted EBITDA | | 75 |

|

EBITDA/Adjusted EBITDA Reconciliation

The reconciliation of profit from operating activities to EBITDA and Adjusted EBITDA for the RGHL Group is as follows:

|

| | | | | | |

| | | For the nine month period ended September 30, |

| (In $ million) | | 2019 | | 2018(2) |

| Profit from operating activities | | 564 |

| | 732 |

|

| Depreciation and amortization from continuing operations | | 514 |

| | 457 |

|

RGHL Group EBITDA(1) from continuing operations | | 1,078 |

| | 1,189 |

|

| Included in the RGHL Group EBITDA: | | | | |

| Asset impairment charges, net of reversals | | 94 |

| | 20 |

|

| (Gain) loss on sale of businesses and non-current assets | | 32 |

| | (5 | ) |

| Non-cash pension expense | | 56 |

| | 42 |

|

| Operational process engineering-related consultancy costs | | 19 |

| | 10 |

|

| Related party management fee | | 19 |

| | 19 |

|

| Restructuring costs, net of reversals | | 13 |

| | 11 |

|

| Strategic review costs | | 20 |

| | — |

|

| Unrealized (gain) loss on derivatives | | (15 | ) | | 7 |

|

| Other | | 9 |

| | 2 |

|

| RGHL Group Adjusted EBITDA from continuing operations | | 1,325 |

| | 1,295 |

|

| | | | | |

| Segment detail of Adjusted EBITDA: | | | | |

| Reynolds Consumer Products | | 458 |

| | 427 |

|

| Pactiv Foodservice | | 466 |

| | 438 |

|

| Graham Packaging | | 282 |

| | 284 |

|

| Evergreen | | 147 |

| | 167 |

|

| Other/Unallocated | | (28 | ) | | (21 | ) |

| RGHL Group Adjusted EBITDA from continuing operations | | 1,325 |

| | 1,295 |

|

| RGHL Group Adjusted EBITDA from discontinued operations | | 87 |

| | 81 |

|

| Total Adjusted EBITDA | | 1,412 |

| | 1,376 |

|

| |

| (1) | Refer to page 2 under the heading “Non-GAAP Financial Measures” for additional information related to these financial measures. |

| |

| (2) | The information presented has been revised to reflect the North American and Japanese closures businesses as discontinued operations. Refer to notes 2.2 and 7 of the RGHL Group’s interim unaudited condensed consolidated financial statements included elsewhere in this quarterly report for additional information. |

Reynolds Consumer Products Segment

|

| | | | | | | | | | | | | | | | | | |

| | | For the nine month period ended September 30, | | | | |

| (In $ million, except for %) | | 2019 | | % of segment revenue | | 2018 | | % of segment revenue | | Change | | % change |

| External revenue | | 2,081 |

| | 95 | % | | 2,110 |

| | 94 | % | | (29 | ) | | (1 | )% |

| Inter-segment revenue | | 117 |

| | 5 | % | | 126 |

| | 6 | % | | (9 | ) | | (7 | )% |

| Total segment revenue | | 2,198 |

| | 100 | % | | 2,236 |

| | 100 | % | | (38 | ) | | (2 | )% |

| Cost of sales | | (1,593 | ) | | (72 | )% | | (1,666 | ) | | (75 | )% | | 73 |

| | 4 | % |

| Gross profit | | 605 |

| | 28 | % | | 570 |

| | 25 | % | | 35 |

| | 6 | % |

| Selling, marketing and distribution expenses/ General and administration expenses | | (220 | ) | | (10 | )% | | (209 | ) | | (9 | )% | | (11 | ) | | (5 | )% |

| Net other income (expenses) | | 10 |

| | — | % | | (6 | ) | | — | % | | 16 |

| | NM |

|

| Profit from operating activities | | 395 |

| | 18 | % | | 355 |

| | 16 | % | | 40 |

| | 11 | % |

| Reynolds Consumer Products segment Adjusted EBITDA | | 458 |

| | 21 | % | | 427 |

| | 19 | % | | 31 |

| | 7 | % |

Revenue. Total segment revenue decreased by $38 million, or 2%. The decrease was primarily due to lower sales volume, partially offset by higher pricing.

Cost of Sales. Cost of sales decreased by $73 million, or 4%. The decrease was primarily due to lower raw material costs and lower sales volume, partially offset by increased manufacturing costs. For the nine month periods ended September 30, 2019 and September 30, 2018, raw material costs accounted for 61% and 64% of Reynolds Consumer Products’ cost of sales, respectively.

Selling, Marketing and Distribution Expenses/General and Administration Expenses. Selling, marketing and distribution expenses and general and administration expenses increased by $11 million, or 5%, primarily due to higher employee-related costs.

Net Other. Net other changed by $16 million, resulting in net other income of $10 million. The change was primarily due to a favorable change in unrealized gains and losses on derivatives. This item has been included in the segment’s Adjusted EBITDA calculation.

EBITDA/Adjusted EBITDA Reconciliation

The reconciliation of profit from operating activities to EBITDA and Adjusted EBITDA for our Reynolds Consumer Products segment is as follows:

|

| | | | | | |

| | | For the nine month period ended September 30, |

| (In $ million) | | 2019 | | 2018 |

| Profit from operating activities | | 395 |

| | 355 |

|

| Depreciation and amortization | | 69 |

| | 63 |

|

| EBITDA | | 464 |

| | 418 |

|

| Included in Reynolds Consumer Products segment EBITDA: | | | | |

| Unrealized (gain) loss on derivatives | | (9 | ) | | 8 |

|

| Other | | 3 |

| | 1 |

|

| Reynolds Consumer Products segment Adjusted EBITDA | | 458 |

| | 427 |

|

Pactiv Foodservice Segment

|

| | | | | | | | | | | | | | | | | | |

| | | For the nine month period ended September 30, | | | | |

| (In $ million, except for %) | | 2019 | | % of segment revenue | | 2018 | | % of segment revenue | | Change | | % change |

| External revenue | | 2,460 |

| | 87 | % | | 2,445 |

| | 86 | % | | 15 |

| | 1 | % |

| Inter-segment revenue | | 353 |

| | 13 | % | | 398 |

| | 14 | % | | (45 | ) | | (11 | )% |

| Total segment revenue | | 2,813 |

| | 100 | % | | 2,843 |

| | 100 | % | | (30 | ) | | (1 | )% |

| Cost of sales | | (2,328 | ) | | (83 | )% | | (2,370 | ) | | (83 | )% | | 42 |

| | 2 | % |

| Gross profit | | 485 |

| | 17 | % | | 473 |

| | 17 | % | | 12 |

| | 3 | % |

| Selling, marketing and distribution expenses/ General and administration expenses | | (216 | ) | | (8 | )% | | (198 | ) | | (7 | )% | | (18 | ) | | (9 | )% |

| Net other income (expenses) | | (20 | ) | | (1 | )% | | (30 | ) | | (1 | )% | | 10 |

| | 33 | % |

| Profit from operating activities | | 249 |

| | 9 | % | | 245 |

| | 9 | % | | 4 |

| | 2 | % |

| Pactiv Foodservice segment Adjusted EBITDA | | 466 |

| | 17 | % | | 438 |

| | 15 | % | | 28 |

| | 6 | % |

Revenue. Total segment revenue decreased by $30 million, or 1%. The decrease was primarily due to lower inter-segment revenue, the impact of business divestitures and an unfavorable impact from foreign currencies, partially offset by higher sales volume with external customers and higher pricing as a result of increased costs passed through to customers.

Cost of Sales. Cost of sales decreased by $42 million, or 2%. The decrease was primarily due to lower raw material costs, partially offset by higher manufacturing and logistics costs. For the nine month periods ended September 30, 2019 and September 30, 2018, raw material costs accounted for 56% and 59% of Pactiv Foodservice’s cost of sales, respectively.

Selling, Marketing and Distribution Expenses/General and Administration Expenses. Selling, marketing and distribution expenses and general and administration expenses increased by $18 million, or 9%. The increase was primarily due to higher employee-related costs, as well as higher operational process engineering-related consultancy costs, which has been included in the segment’s Adjusted EBITDA calculation.

Net Other. Net other expenses decreased by $10 million to $20 million. The decrease was primarily due to a favorable change in unrealized gains and losses on derivatives and lower asset impairment charges. These items have been included in the segment’s Adjusted EBITDA calculation.

EBITDA/Adjusted EBITDA Reconciliation

The reconciliation of profit from operating activities to EBITDA and Adjusted EBITDA for our Pactiv Foodservice segment is as follows:

|

| | | | | | |

| | | For the nine month period ended September 30, |

| (In $ million) | | 2019 | | 2018 |

| Profit from operating activities | | 249 |

| | 245 |

|

| Depreciation and amortization | | 179 |

| | 152 |

|

| EBITDA | | 428 |

| | 397 |

|

| Included in Pactiv Foodservice segment EBITDA: | | | | |

| Asset impairment charges, net of reversals | | 2 |

| | 6 |

|

| (Gain) loss on sale of businesses and non-current assets | | 22 |

| | 23 |

|

| Operational process engineering-related consultancy costs | | 17 |

| | 10 |

|

| Unrealized (gain) loss on derivatives | | (7 | ) | | — |

|

| Other | | 4 |

| | 2 |

|

| Pactiv Foodservice segment Adjusted EBITDA | | 466 |

| | 438 |

|

Graham Packaging Segment

|

| | | | | | | | | | | | | | | | | | |

| | | For the nine month period ended September 30, | | | | |

| (In $ million, except for %) | | 2019 | | % of segment revenue | | 2018 | | % of segment revenue | | Change | | % change |

| External revenue | | 1,487 |

| | 100 | % | | 1,610 |

| | 100 | % | | (123 | ) | | (8 | )% |

| Inter-segment revenue | | — |

| | — | % | | — |

| | — | % | | — |

| | — | % |

| Total segment revenue | | 1,487 |

| | 100 | % | | 1,610 |

| | 100 | % | | (123 | ) | | (8 | )% |

| Cost of sales | | (1,283 | ) | | (86 | )% | | (1,389 | ) | | (86 | )% | | 106 |

| | 8 | % |

| Gross profit | | 204 |

| | 14 | % | | 221 |

| | 14 | % | | (17 | ) | | (8 | )% |

| Selling, marketing and distribution expenses/General and administration expenses | | (136 | ) | | (9 | )% | | (132 | ) | | (8 | )% | | (4 | ) | | (3 | )% |

| Net other income (expenses) | | (24 | ) | | (2 | )% | | (13 | ) | | (1 | )% | | (11 | ) | | (85 | )% |

| Profit from operating activities | | 44 |

| | 3 | % | | 76 |

| | 5 | % | | (32 | ) | | (42 | )% |

| Graham Packaging segment Adjusted EBITDA | | 282 |

| | 19 | % | | 284 |

| | 18 | % | | (2 | ) | | (1 | )% |

Revenue. Total segment revenue decreased by $123 million, or 8%. The decrease was primarily due to lower sales volume, lower pricing, an unfavorable foreign currency impact and the impact of business divestitures.

Cost of Sales. Cost of sales decreased by $106 million, or 8%. The decrease was primarily due to lower sales volume, lower raw material costs, the impact of business divestitures and a favorable foreign currency impact, partially offset by higher manufacturing costs. For the nine month periods ended September 30, 2019 and September 30, 2018, raw material costs accounted for 51% and 53% of Graham Packaging’s cost of sales, respectively.

Selling, Marketing and Distribution Expenses/General and Administration Expenses. Selling, marketing and distribution expenses and general and administration expenses increased by $4 million, or 3%.

Net Other. Net other expenses increased by $11 million to $24 million. The increase was primarily due to higher asset impairment charges related to plant rationalizations, partially offset by a favorable change in gains and losses on sale of businesses and non-current assets. These items have been included in the segment’s Adjusted EBITDA calculation.

EBITDA/Adjusted EBITDA Reconciliation

The reconciliation of profit from operating activities to EBITDA and Adjusted EBITDA for our Graham Packaging segment is as follows:

|

| | | | | | |

| | | For the nine month period ended September 30, |

| (In $ million) | | 2019 | | 2018 |

| Profit from operating activities | | 44 |

| | 76 |

|

| Depreciation and amortization | | 204 |

| | 189 |

|

| EBITDA | | 248 |

| | 265 |

|

| Included in Graham Packaging segment EBITDA: | | | | |

| Asset impairment charges, net of reversals | | 25 |

| | 10 |

|

| (Gain) loss on sale of businesses and non-current assets | | — |

| | 3 |

|

| Restructuring costs, net of reversals | | 9 |

| | 6 |

|

| Graham Packaging segment Adjusted EBITDA | | 282 |

| | 284 |

|

Evergreen Segment

|

| | | | | | | | | | | | | | | | | | |

| | | For the nine month period ended September 30, | | | | |

| (In $ million, except for %) | | 2019 | | % of segment revenue | | 2018 | | % of segment revenue | | Change | | % change |

| External revenue | | 1,094 |

| | 92 | % | | 1,125 |

| | 94 | % | | (31 | ) | | (3 | )% |

| Inter-segment revenue | | 94 |

| | 8 | % | | 75 |

| | 6 | % | | 19 |

| | 25 | % |

| Total segment revenue | | 1,188 |

| | 100 | % | | 1,200 |

| | 100 | % | | (12 | ) | | (1 | )% |

| Cost of sales | | (1,041 | ) | | (88 | )% | | (1,027 | ) | | (86 | )% | | (14 | ) | | (1 | )% |

| Gross profit | | 147 |

| | 12 | % | | 173 |

| | 14 | % | | (26 | ) | | (15 | )% |

| Selling, marketing and distribution expenses/ General and administration expenses | | (64 | ) | | (5 | )% | | (52 | ) | | (4 | )% | | (12 | ) | | (23 | )% |

| Net other income (expenses) | | 3 |

| | — | % | | 4 |

| | — | % | | (1 | ) | | (25 | )% |

| Profit from operating activities | | 86 |

| | 7 | % | | 125 |

| | 10 | % | | (39 | ) | | (31 | )% |

| Evergreen segment Adjusted EBITDA | | 147 |

| | 12 | % | | 167 |

| | 14 | % | | (20 | ) | | (12 | )% |

Revenue. Total segment revenue decreased by $12 million, or 1%. The decrease was primarily due to lower sales volume, partially offset by higher pricing.

Cost of Sales. Cost of sales increased by $14 million, or 1%. The increase was primarily due to higher manufacturing and raw material costs, primarily fiber, partially offset by lower sales volume. For the nine month periods ended September 30, 2019 and September 30, 2018, raw material costs accounted for 41% and 40% of Evergreen’s cost of sales, respectively.

Selling, Marketing and Distribution Expenses/General and Administration Expenses. Selling, marketing and distribution expenses and general and administration expenses increased by $12 million, or 23%, primarily due to higher employee-related costs.

Net Other. Net other income decreased by $1 million to $3 million.

EBITDA/Adjusted EBITDA Reconciliation

The reconciliation of profit from operating activities to EBITDA and Adjusted EBITDA for our Evergreen segment is as follows:

|

| | | | | | |

| | | For the nine month period ended September 30, |

| (In $ million) | | 2019 | | 2018 |

| Profit from operating activities | | 86 |

| | 125 |

|

| Depreciation and amortization | | 54 |

| | 45 |

|

| EBITDA | | 140 |

| | 170 |

|

| Included in Evergreen segment EBITDA: | | | | |

| Non-cash change in multi-employer pension plan withdrawal liability | | 6 |

| | (2 | ) |

| Other | | 1 |

| | (1 | ) |

| Evergreen segment Adjusted EBITDA | | 147 |

| | 167 |

|

Other/Unallocated

|

| | | | | | | | | | | | |

| | | For the nine month period ended September 30, | | | | |

| (In $ million, except for %) | | 2019 | | 2018(1) | | Change | | % change |

| External revenue | | 121 |

| | 174 |

| | (53 | ) | | (30 | )% |

| Inter-segment revenue/eliminations | | (564 | ) | | (599 | ) | | 35 |

| | 6 | % |

| Total revenue | | (443 | ) | | (425 | ) | | (18 | ) | | (4 | )% |

| Cost of sales | | 452 |

| | 442 |

| | 10 |

| | 2 | % |

| Gross profit | | 9 |

| | 17 |

| | (8 | ) | | NM |

|

| Selling, marketing and distribution expenses/General and administration expenses | | (128 | ) | | (92 | ) | | (36 | ) | | (39 | )% |

| Net other income (expenses) | | (91 | ) | | 6 |

| | (97 | ) | | NM |

|

| Loss from operating activities | | (210 | ) | | (69 | ) | | (141 | ) | | NM |

|

| Other/Unallocated Adjusted EBITDA | | (28 | ) | | (21 | ) | | (7 | ) | | (33 | )% |

| |

| (1) | The information presented has been revised to include the results of our remaining closures businesses. Refer to note 2.2 of the RGHL Group’s interim unaudited condensed consolidated financial statements included elsewhere in this quarterly report for additional information. |

Revenue. External revenue decreased by $53 million, or 30%. The decrease was primarily due to the impact of business divestitures and lower sales volume.

Cost of Sales. Cost of sales decreased by $10 million, or 2%.The decrease was primarily due to the impact of business divestitures and lower sales volume.

Selling, Marketing and Distribution Expenses/General and Administration Expenses. Selling, marketing and distribution expenses and general and administration expenses increased by $36 million, or 39%. The increase was primarily due to $19 million of higher strategic review costs and higher pension expense. These items have been included in the Adjusted EBITDA calculation.

Net Other. Net other expenses changed by $97 million to $91 million. The change was primarily due to higher asset impairment charges of $63 million at the remaining closures businesses primarily as a result of dis-synergies associated with the pending sale of the North American and Japanese closures businesses and a $41 million unfavorable change in gains and losses on sale of businesses and non-current assets. These items have been included in the Adjusted EBITDA calculation.

EBITDA/Adjusted EBITDA Reconciliation

The reconciliation of loss from operating activities to EBITDA and Adjusted EBITDA for Other/Unallocated is as follows:

|

| | | | | | |

| | | For the nine month period ended September 30, |

| (In $ million) | | 2019 | | 2018(1) |

| Loss from operating activities | | (210 | ) | | (69 | ) |

| Depreciation and amortization | | 8 |

| | 8 |

|

| EBITDA | | (202 | ) | | (61 | ) |

| Included in Other/Unallocated EBITDA: | | | | |

| Asset impairment charges, net of reversals | | 67 |

| | 4 |

|

| (Gain) loss on sale of businesses and non-current assets | | 10 |

| | (31 | ) |

| Non-cash pension expense | | 56 |

| | 42 |

|

| Related party management fee | | 19 |

| | 19 |

|

| Strategic review costs | | 19 |

| | — |

|

| Other | | 3 |

| | 6 |

|

| Other/Unallocated Adjusted EBITDA | | (28 | ) | | (21 | ) |

| |

| (1) | The information presented has been revised to include the results of our remaining closures businesses in EMEA and South America. Refer to note 2.2 of the RGHL Group’s interim unaudited condensed consolidated financial statements included elsewhere in this quarterly report for additional information. |

Differences Between the RGHL Group and the BP I Group Results of Operations