ZAZA ENERGY CORPORATION

| | | | |

TABLE OF CONTENTS |

| | | | |

| | | | Page |

PART I | | | | |

| | | | |

Items 1 and 2 | | Business and Properties | | 2 |

Item 1A | | Risk Factors | | 15 |

Item 1B | | Unresolved Staff Comments | | 34 |

Item 2 | | Properties (see Items 1 and 2. Business and Properties) | | 34 |

Item 3 | | Legal Proceedings | | 34 |

Item 4 | | Mine Safety Disclosure | | 37 |

| | | | |

PART II | | | | |

| | | | |

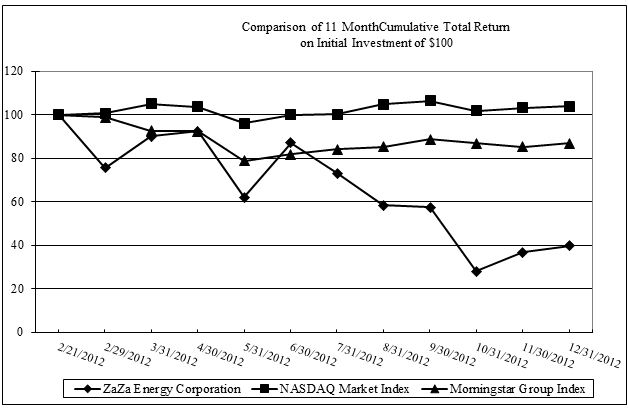

Item 5 | | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | | 38 |

Item 6 | | Selected Financial Data | | 40 |

Item 7 | | Management's Discussion and Analysis of Financial Condition and Results of Operations | | 41 |

Item 7A | | Quantitative and Qualitative Disclosures About Market Risk | | 67 |

Item 8 | | Financial Statements and Supplementary Data | | 68 |

Item 9 | | Changes In And Disagreements With Accountants On Accounting And Financial Disclosure | | 68 |

Item 9A | | Controls and Procedures | | 68 |

Item 9B | | Other Information | | 69 |

| | | | |

PART III | | | | |

| | | | |

Item 10 | | Directors, Executive Officers and Corporate Governance | | 71 |

Item 11 | | Executive Compensation | | 71 |

Item 12 | | Security Ownership Of Certain Beneficial Owners And Management And Related Stockholder Matters | | 71 |

Item 13 | | Certain Relationships and Related Transactions, and Director Independence | | 71 |

Item 14 | | Principal Accountant Fees And Services | | 71 |

| | | | |

PART IV | | | | |

| | | | |

Item 15 | | Exhibits and Financial Statement Schedules | | 72 |

| | | | |

SIGNATURES | | | | 79 |

| | | | |

PART I

ITEM 1 AND 2. BUSINESS AND PROPERTIES

See the "Glossary of Selected Oil and Natural Gas Terms" at the end of Item 1 for the definition of certain terms in this annual report.

ZaZa Energy Corporation (“ZaZa”) is an independent exploration and production company focused on unconventional oil and gas resources, particularly tight oil plays. ZaZa has grown its existing property base by developing and exploring its acreage, purchasing new undeveloped leases, and acquiring oil and gas producing properties and drilling prospects. According to our external engineering firm, Ryder Scott, as of December 31, 2012, ZaZa LLC's proved reserves were 3,348 MBOE.

ZaZa is a Delaware corporation formed for the purpose of being a holding company of both Toreador Resources Corporation, a Delaware corporation (“Toreador”), and ZaZa Energy, LLC, a Texas limited liability company (“ZaZa LLC”), from and after completion of the Combination, as described below. Prior to the Combination on February 21, 2012, ZaZa had no assets and had not conducted any material activities other than those incident to its formation. However, upon the consummation of the Combination, ZaZa became the parent company of ZaZa LLC and Toreador. In this Annual Report on Form 10-K, unless the context provides otherwise, “we”, “our”, “us” and like references refer to ZaZa and its subsidiaries.

ZaZa's principal executive office is located at, 1301 McKinney Street, Suite 2850, Houston, Texas 77010 (telephone number: (713) 595-1900).

On February 22, 2012 our common stock began trading on the NASDAQ Capital Market under the trading symbol "ZAZA".

Creation of ZaZa Energy Corporation

On February 21, 2012, we consummated the combination (the “Combination”) of ZaZa LLC and Toreador, on the terms set forth in the Agreement and Plan of Merger and Contribution, dated August 9, 2011, and as subsequently amended (as amended, the “Merger Agreement”).

Pursuant to the Merger Agreement, (i) a wholly-owned subsidiary of ZaZa merged with and into Toreador (the “Merger”), with Toreador continuing as a surviving entity, (ii) the three former members of ZaZa LLC (the “ZaZa LLC Members”), holding 100% of the limited liability company interests in ZaZa LLC, directly and indirectly contributed all of such interests to ZaZa (the “Contribution”), and (iii) the holders of certain profits interests in ZaZa LLC contributed 100% of such interests to ZaZa (the “Profits Interests Contribution”). Upon the consummation of the Combination, Toreador and ZaZa LLC became our wholly-owned subsidiaries.

The Combination was treated as a reverse merger under the purchase method of accounting in accordance with GAAP. For accounting purposes, ZaZa LLC is considered to have acquired Toreador in the Combination. Under the purchase method of accounting, the assets and liabilities of Toreador were recorded at their respective fair values and added to those of ZaZa LLC in our financial statements.

At the effective time of the Merger, each share of common stock of Toreador issued and outstanding immediately prior to the effective time of the Merger was converted into the right to receive one share of ZaZa common stock, par value $0.01 per share (the “Common Stock”), which in the aggregate represented 25% of the issued and outstanding shares of Common Stock immediately after the consummation of the Combination (but without giving effect to the shares of Common Stock issuable upon exercise of the Warrants as discussed below).

Simultaneously with the consummation of the Merger, and pursuant to the Contribution Agreement dated August 9, 2011, among the ZaZa LLC Members and ZaZa (the “Contribution Agreement”), the ZaZa LLC Members contributed all of the direct or indirect limited liability company interests in ZaZa LLC to ZaZa in exchange for (i) a number of shares of Common Stock that, in the aggregate, represented 75% of the issued and outstanding shares of Common Stock immediately after the consummation of the Combination (but without giving effect to the shares of Common Stock issuable upon exercise of the Warrants as discussed below), and (ii) subordinated notes in an aggregate amount of $38.25 million issued to the ZaZa LLC Members as partial consideration for the Combination

(the “Seller Notes”). In addition, as required under the terms of the Merger Agreement and the Contribution Agreement, we issued subordinated notes in an aggregate amount of $9.08 million to the individuals that own and control the ZaZa LLC Members, Todd Alan Brooks, Gaston L. Kearby and John E. Hearn Jr. (together, the “ZaZa Founders”), in respect of certain unpaid compensation amounts owing to the ZaZa Founders by ZaZa LLC (the “Compensation Notes”).

Immediately after the consummation of the Merger and Contribution, and pursuant to the Net Profits Interest Contribution Agreement, dated August 9, 2011, among ZaZa, ZaZa LLC and the holders of net profits interests in ZaZa LLC, the parties completed the Profits Interests Contribution pursuant to which ZaZa acquired their net profits interests from such holders in exchange for $4.8 million in cash.

Additionally, in connection with the Combination, we issued senior secured notes with a principal amount of $100 million maturing in 2017 (the “Senior Secured Notes”) in a private placement to a group of investors led by MSD Energy Partners, L.P. and Senator Investment Group LP. As a result of prepayments in connection with the dissolution of our Hess joint venture and certain asset sales, discussed in more detail elsewhere, we had reduced the outstanding principal amount of the Senior Secured Notes to $33.2 million as of December 31, 2012. In connection with the issuance of the Senior Secured Notes, ZaZa also issued to the investors warrants to purchase an aggregate of approximately 26.3 million shares of our common stock at $3.15 per share (the “Warrants”) representing 20.6% of the outstanding shares of our common stock at the closing of the Combination, on a fully diluted and on an as-converted basis. The Warrants expire in five years and are exercisable at any time after August 21, 2012. As a result of anti-dilution adjustments in connection with our issuance of $40 million of Convertible Senior Notes due 2017 in October 2012, the number of outstanding shares of our common stock represented by the Warrants was increased from 26,315,789 to 27,226,223 and the exercise price per share was reduced to $3.04 per share. In connection with our recent amendment to the terms of the Senior Secured Notes discussed elsewhere, we agreed to reduce the exercise price of the Warrants to $2.00 per share.

ZaZa Energy, LLC

ZaZa LLC was formed in March 2009 primarily to acquire and develop unconventional oil and gas resources and was a privately-held company until February 21, 2012 when it was contributed to ZaZa as part of the Combination. ZaZa LLC was previously controlled by the ZaZa Founders who each beneficially owned one-third of the outstanding limited liability company interests of ZaZa LLC. ZaZa LLC's operations have been concentrated in south Texas, including its exploration area in the core area of the Eagle Ford shale formation and in the eastern extension of the Eagle Ford/Woodbine formation, which we refer to as the "Eaglebine."

ZaZa LLC’s initial exploration and production activities were undertaken primarily through a joint venture with Hess Corporation, which accumulated approximately 121,000 gross acres (approximately 11,500 net acres to ZaZa LLC). ZaZa LLC operated the Hess joint venture properties during the first year of drilling, after which Hess had an election to take over operatorship. This provision enabled ZaZa LLC to build an operating track record during this first year of drilling. As operator of the Hess joint venture, ZaZa LLC successfully drilled and completed 18 Eagle Ford wells. Hess then elected to take over operatorship, and the transition from ZaZa LLC to Hess commenced in November 2011 and was expected to be completed in July 2012. In conjunction with the operatorship transition, Hess also made public announcements in the first quarter of 2012 indicating that Hess intended to pursue a drilling program in 2012-2013 that was slower than ZaZa LLC had anticipated. The combination of Hess taking over operatorship and the expectation that Hess would slow the drilling program led ZaZa LLC to negotiate an exit from the Hess joint venture in July 2012. As a result of this exit, ZaZa LLC relinquished the Cotulla Area and regained operational control of approximately 60% of the venture’s former acreage (totaling 72,000 net acres). As described below, Toreador also exited its joint venture with Hess in France, which had stalled due to French governmental regulations on the development of unconventional resources. This resulted in ZaZa converting its 50% working interest in the French exploration licenses to a 5% non-cost bearing revenue interest for up to $130 million in cash receipts. In addition to the aforementioned land transitions in connection with the dissolution of the joint venture, ZaZa also received an aggregate of $84 million in cash from Hess. For a complete description of the transactions in connection with the dissolution of the Hess Joint Venture, see Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations - 2012 Developments - Hess Joint Venture Dissolution Agreement.”

ZaZa LLC also had accumulated approximately 82,000 gross acres (approximately 60,000 net acres) in the Eaglebine formation, which acreage was not part of its joint venture with Hess. On March 29, 2012, ZaZa LLC entered into a transaction with Range Texas Production, LLC (“Range”), a subsidiary of Range Resources

Corporation, to expand ZaZa’s position in the Eaglebine to a total holding of approximately 143,400 gross acres (98,520 net acres). Under the terms of the transaction, ZaZa LLC: obtained a 75% working interest in the acquired acreage; was designated as operator; committed to drill one well; was obligated and satisfied its obligation to commence operations on the commitment well on or before August 1, 2012; and committed to and made two cash payments to Range. After a casing collar failure on the commitment well, Range granted ZaZa LLC an extension to drill a substitute well, which is scheduled for the third quarter of 2013. For a complete description of the transactions in connection with the Range joint venture, see Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations -- 2012 Developments -- Range Transaction.”

Toreador Resources Corporation

Prior to the Combination, Toreador was a publicly held independent energy company engaged in the exploration and production of crude oil with interests in developed and undeveloped oil properties in the Paris Basin, France. At the time of the Combination, Toreador operated solely in the Paris Basin and its operations consisted of (i) a joint venture with Hess Corporation in the Paris Basin focused on unconventional resources and (ii) conventional Paris Basin assets held by ZaZa Energy France SAS.

The unconventional resource joint venture with Hess stalled due to French governmental regulations. ZaZa ended the Hess Paris venture in July 2012 by exchanging its 50% working interest in the Paris Basin exploration licenses it held together with Hess for a 5% cost-free revenue interest in such licenses, in which the total proceeds relating thereto to ZaZa are capped at $130 million. Following ZaZa’s exit from the unconventional resource play in France, ZaZa divested its Paris Basin conventional assets in December 2012 through the sale of 100% of the shares in ZaZa Energy France SAS to Vermillion REP SAS, a wholly-owned subsidiary of Vermillion Energy Inc., for a net sales price of approximately $76 million. At the end of 2012, ZaZa’s only exploration and production asset in France was the Hess royalty interest, which is held by ZaZa.

Recent Development in Business Relationships

After the termination of the Hess joint venture and the disposition of its French oil and gas properties, ZaZa’s principal assets were approximately 66,000 net acres in the Eagle Ford core and approximately 89,000 net acres in the Eaglebine. The Company's strategic objectives since then have focused on executing drilling operations to further appraise its acreage and evaluating joint venture opportunities to realize its development. Since the dissolution of the Hess joint ventures, ZaZa has drilled two wells in the Eaglebine and one well in the Eagle Ford and has entered into the joint venture with EOG Resources, Inc. described below.

Eaglebine Joint Venture with EOG

On March 21, 2013, we entered into a Joint Exploration and Development Agreement with EOG Resources, Inc., (“our counterparty”), for the joint development of certain of our Eaglebine properties located in Walker, Grimes, Madison, Trinity, and Montgomery Counties, Texas. Under this agreement, we and our counterparty will jointly develop up to approximately 100,000 gross acres (approximately 73,000 net acres) that ZaZa currently owns in the Eaglebine trend in these counties. Our counterparty will act as the operator and will pay us certain cash amounts, the drilling and completion costs of certain specified wells, and a portion of our share of any additional seismic or well costs in order to earn their interest in these properties. Generally, ZaZa will retain a 25% working interest, our counterparty will earn a 75% working interest in the acreage, subject to the agreement, that is currently 100% owned by ZaZa. ZaZa will retain a 25% working interest, our counterparty will earn a 50% working interest, and Range will retain a 25% working interest in the acreage that is currently owned 75% by ZaZa and 25% by Range, subject to the terms of our agreement with Range. This joint development will be divided into three phases.

In the first phase, we will transfer 20,000 net acres, approximately 15,000 of which will come from our joint venture with Range, to our counterparty in exchange for a cash payment by our counterparty to us of $10 million and an obligation of our counterparty to drill and pay 100% of the drilling and completion costs of three wells. The second of these three wells to be drilled will be the substitute well that we are required to drill pursuant to our agreement with Range described above. Drilling operations on the third well in the first phase of joint development with our counterparty must be commenced by our counterparty before December 31, 2013.

Within 60 days of completion of the third well under the first phase, our counterparty will have the option to elect to go forward with the second phase of the joint development. If they so elect, we will transfer an additional

20,000 net acres to our counterparty in exchange for a cash payment of $20 million, an obligation of our counterparty to drill and pay 100% of the drilling and completions costs of an additional three wells, and an obligation of our counterparty to pay for up to $1.25 million of ZaZa’s share of additional costs for seismic or well costs.

Within 60 days of completion of the second phase, our counterparty will have the option to elect to go forward with the third phase of the joint development. If they so elect, we will transfer an additional 15,000 net acres to our counterparty in exchange for a cash payment of $20 million, an obligation of our counterparty to drill and pay 100% of the drilling and completion costs of an additional three wells, and an obligation of our counterparty to pay for up to $1.25 million of ZaZa’s share of additional costs for seismic or well costs.

Sale of Moulton acreage

On March 5, 2013 the Company entered into a purchase and sale agreement to sell its remaining Moulton prospect for approximately $9.2 million. This transaction is expected to close on or before April 5, 2013 and is subject to normal closing conditions.

On March 22, 2013, we entered into an agreement to sell approximately 10,000 net acres of our properties in the Eagle Ford trend located in Fayette, Gonzalez and Lavaca Counties, Texas, which we refer to as our Moulton properties, including seven producing wells located on the Moulton properties, for approximately $43.3 million in cash. The closing of the sale of the Moulton properties is expected to occur during the second quarter of 2013, and net proceeds from the sale, after closing purchase price adjustments and expenses, are expected to be approximately $42 million. The closing is subject to normal closing conditions, and the amendment of ZaZa’s securities purchase agreement for its senior secured notes, and there can be no assurance that this transaction will be consummated. We intend to use these net proceeds to fund a portion of capital expenditures for exploration on our other properties and/or to repay indebtedness.

Strategy

ZaZa’s strategy is to identify prospective unconventional acreage, appraise such acreage and then realize the development of high-graded units through a combination of self-funded development and joint ventures. To this end, ZaZa maintains a team of technical and commercial personnel with experience in unconventional resources. ZaZa���s operations in the Hess venture demonstrated a track record of identifying prospective unconventional acreage, acquiring material land positions, and appraising and developing such acreage as its operator. As ZaZa evaluates additional joint venture opportunities with other companies, ZaZa will evaluate whether a transition of operatorship to the joint venture partner is appropriate. When transition occurs, ZaZa can then redeploy its personnel to the evaluation and acquisition of new acreage, the development of its self-funded acreage and/or the delineation of other areas that it is considering for joint ventures.

Areas of Operations

ZaZa owns producing and non-producing oil and gas properties in proven or prospective basins that are primarily located in South Texas. ZaZa’s producing areas are in the Eagle Ford shale located in Gonzales, Fayette, Dewitt, and Lavaca counties. ZaZa also owns prospective acreage in the Eaglebine formation located in Madison, Grimes, and Walker counties. All of ZaZa's assets (other than the overriding royalty interest in certain French production licenses obtained in connection with the dissolution of the Hess joint venture), including long-lived assets, are located within the United States. The following is a summary of its major operating areas.

Eagle Ford Shale

For the year ending December 31, 2012, ZaZa drilled or participated in 13 gross wells and 1.23 net wells all successful in the Eagle Ford shale. ZaZa also operated 100% of the Boening A-1H well, which began initial flow back in February 2013. ZaZa also installed a pumping unit on its Crabb Ranch well in Gonzales county sustaining production rates over 200 Bbls per day. In 2012, ZaZa's Eagle Ford operations were conducted as 100% ZaZa operations on the Boening A-1H and non-operated participation with GeoResources (Halcon) on the Ring Unit 1 through 5 wells.

As of December 31, 2012, ZaZa owns operating interest in four Eagle Ford producing wells and non-

operating working interests in ten Eagle Ford producing wells located in South Texas. Our management intends to continue to acquire non-operating working interests in both prospective and producing wells when the opportunity arises and to acquire such properties at attractive valuations. Such interests may be in wells that are considered either conventional or unconventional.

Eaglebine Shale

The Eaglebine is an expansion area of the Eagle Ford shale, but is also prospective for the Woodbine shale as well as the Lower Cretaceous comingled conventional section, hence the industry term "Eaglebine." ZaZa was in the process of drilling 2 gross, 1.75 net wells in the Eaglebine Shale area across the December 31, 2012 timeline one horizontal well targeting the Lower Eaglebine Shale (Stingray A-1H) and one vertical well targeting the Lower Cretaceous (Commodore A1-V). ZaZa’s operations on the Stingray A-1H successfully drilled a vertical pilot hole through the Lower Eaglebine section obtaining critical open hole logs and core data. ZaZa then plugged back and successfully drilled a +4000’ lateral targeting the Lower Eaglebine section, ran production casing and fracked 15 of 16 stages. At that point the wellbore suffered a casing collar failure in the 5½’ casing. ZaZa has re-entered the wellbore to drill vertically to the Lower Cretaceous. ZaZa also commenced drilling the Commodore A-1V, a vertical well designed to test the Lower Cretaceous section. This well reached total depth and production casing was run on February 10, 2013. ZaZa plans to continue drilling vertical and horizontal wells to demonstrate the commercial viability of the play. Once demonstrated, ZaZa plans to move into the development phase, where it may drill up to one well per month, subject to availability of capital resources to do so. The Company continues to exercise options and extensions maintaining the Eaglebine leases.

On March 29, 2012, ZaZa LLC announced that it had entered into a farm-in transaction with Range to increase its position in the Eaglebine. Currently, ZaZa holds approximately 135,000 gross acres (89,000 net acres) in the Eaglebine. ZaZa’s Eaglebine operations are wholly-owned, but ZaZa intends to explore ways to accelerate the drilling program on its Eaglebine acreage by selectively partnering with others. The first such joint venture is the EOG JV. ZaZa also expects to finance a portion of its Eaglebine program with cash flow from operations. If cash flow from operations is not sufficient to fund this program, ZaZa would be required to seek additional financing to maintain and expand this program.

Title to Properties

ZaZa believes it has satisfactory title to all of its producing properties in accordance with standards generally accepted in the oil and gas industry. As is customary in the oil and gas industry, ZaZa makes title investigations and receives title opinions of local counsel not on acquisition but only before it commences drilling operations. ZaZa believes that it has satisfactory title to all of its other assets. ZaZa's properties are subject to customary royalty interests, liens incident to operating agreements, liens for current taxes and other burdens, including other mineral encumbrances and restrictions. Although title to its properties is subject to encumbrances in certain cases, ZaZa believes that none of these burdens will materially detract from the value of ZaZa's properties or from its interest therein or will materially interfere with its use of the properties in the operation of its business.

Oil and Gas Continuing Operations

The following tables present our production data for the referenced geographic areas for the periods indicated:

| | | | | | |

| | For the Year Ended December 31, 2012 |

| | Gas | | Oil | | Equivalent |

| | (Mcf) | | (Bbls) | | (BOE) |

Eagle Ford: | | | | | | |

Cotulla | | 48,492 | | 50,780 | | 58,862 |

Moulton | | 10,268 | | 34,106 | | 35,817 |

Sweet Home | | - | | - | | - |

Hackberry | | 101,335 | | 8,189 | | 25,078 |

Eaglebine | | - | | - | | - |

Other Onshore | | 2,118 | | 4,523 | | 4,876 |

Total | | 162,213 | | 97,598 | | 124,634 |

| | | | | | |

| | For the Year Ended December 31, 2011 |

| | Gas | | Oil | | Equivalent |

| | (Mcf) | | (Bbls) | | (BOE) |

Eagle Ford: | | | | | | |

Cotulla | | 9,551 | | 24,829 | | 26,421 |

Moulton | | - | | - | | - |

Sweet Home | | - | | - | | - |

Hackberry | | - | | - | | - |

Eaglebine | | - | | - | | - |

Other Onshore | | 2,095 | | 2,955 | | 3,304 |

Total | | 11,646 | | 27,784 | | 29,725 |

| | | | | | |

| | For the Year Ended December 31, 2010 |

| | Gas | | Oil | | Equivalent |

| | (Mcf) | | (Bbls) | | (BOE) |

Eagle Ford: | | | | | | |

Cotulla | | - | | - | | - |

Moulton | | - | | - | | - |

Sweet Home | | - | | - | | - |

Hackberry | | - | | - | | - |

Eaglebine | | - | | - | | - |

Other Onshore | | 4,247 | | 4,331 | | 5,038 |

Total | | 4,247 | | 4,331 | | 5,038 |

Capital Expenditures

The following table summarizes information regarding ZaZa's development and exploration capital expenditures for the periods indicated:

| | | | | | | | |

| For the Year Ended December 31, |

| 2012 | | 2011 | | 2010 |

| (In thousands) |

Additions to oil and gas properties | $ | 53,789 | | $ | 10,667 | | $ | 6,436 |

Additions to furniture and fixtures | | 291 | | | 1,975 | | | 831 |

Total capital expenditures | $ | 54,080 | | $ | 12,642 | | $ | 7,267 |

Productive Wells and Acreage

The following table sets forth our interest in undeveloped acreage, developed acreage and productive wells in which we own a working interest as of December 31, 2012. "Gross" represents the total number of acres or wells in which we own a working interest. "Net" represents our proportionate working interest resulting from our ownership in the gross acres or wells. Productive wells are wells in which we have a working interest and that are capable of producing oil or gas.

| | | | | | | | | | | | | | | |

| Acres | | Productive Wells |

| Undeveloped | | Developed | | Gross | | Net |

| Gross | | Net | | Gross | | Net | | Gas | | Oil | | Gas | | Oil |

Eagle Ford | | | | | | | | | | | | | | | |

Cotulla | 2,270 | | 1,973 | | - | | - | | - | | - | | - | | - |

Moulton | 10,989 | | 10,543 | | 824 | | 824 | | - | | 7 | | - | | 1.6 |

Sweet Home | 35,405 | | 34,076 | | - | | - | | - | | - | | - | | - |

Hackberry | 22,086 | | 19,537 | | 1,325 | | 1,325 | | 2 | | - | | 2 | | - |

Eaglebine | 134,711 | | 89,034 | | - | | - | | - | | - | | - | | - |

Other Onshore U.S. | 640 | | 426 | | 2,424 | | 59 | | - | | 4 | | - | | 0.1 |

The following table sets forth our interest in undeveloped acreage as of December 31, 2012 that is subject to expiration in 2013, 2014, 2015 and thereafter:

| | | | | | | | | | | | | | |

2013 | | 2014 | | 2015 | | Thereafter |

Gross | | Net | | Gross | | Net | | Gross | | Net | | Gross | | Net |

| | | | | | | | | | | | | | |

| 104,875 | | 77,937 | | 67,309 | | 51,108 | | 31,884 | | 25,025 | | 2,033 | | 1,519 |

Drilling Activity

The following table sets forth the number of gross exploratory and development wells ZaZa drilled or in which it participated during 2012, 2011and 2010. Productive wells are either producing wells or wells capable of production.

| | | | | | | | | | | | |

| | Gross Wells |

| | Exploratory | | Development |

| | Productive | | Dry | | Total | | Productive | | Dry | | Total |

Year ended December 31, 2012 | | - | | - | | - | | 13 | | - | | 13 |

Year ended December 31, 2011 | | - | | - | | - | | 20 | | - | | 20 |

Year ended December 31, 2010 | | - | | - | | - | | 5 | | - | | 5 |

The following table sets forth the number of net exploratory and net development wells drilled by ZaZa during 2012, 2011and 2010 based on its proportionate working interest in such wells.

| | | | | | | | | | | | |

| | Net Wells |

| | Exploratory | | Development |

| | Productive | | Dry | | Total | | Productive | | Dry | | Total |

Year ended December 31, 2012 | | - | | - | | - | | 1.23 | | - | | 1.23 |

Year ended December 31, 2011 | | - | | - | | - | | 2.00 | | - | | 2.00 |

Year ended December 31, 2010 | | - | | - | | - | | 0.20 | | - | | 0.20 |

As of December 31, 2012, ZaZa had an additional two exploratory wells being drilled, the Stingray and Boening, that are currently being completed and are pending final results. We have determined the horizontal portion of the Stingray to be dry due to the casing restriction and have recorded $12.9 million in exploration

expense. These wells are located in our Eaglebine area. Additionally, 8 of the gross wells, (0.8 net), drilled in 2012, were in the Cotulla area which was divested in the Hess joint venture dissolution.

Marketing and Customers

Prior to the dissolution of the Hess joint venture, ZaZa Energy, LLC was dependent upon Hess for all of its oil sales revenue, which had been primarily delivered from two purchasers, Shell Oil and Superior Oil Company. With the dissolution of the joint venture, ZaZa retained production from three operated producing Eagle Ford Shale wells. Sales revenue from these wells is delivered from GulfMark Energy (“GulfMark”); however, multiple purchaser options exist for this production. All existing purchaser contracts are on monthly or “evergreen” terms. Our financial condition and results of operations could be materially adversely affected if this purchaser fails to pay or ceases to acquire its production on terms that are favorable to us, or if the purchaser decreases demand. Should this occur, we are confident we can obtain new contracts that are similar in terms and conditions, and we do not anticipate a significant fluctuation in operations or sales.

We currently receive favorable pricing for crude oil produced from our operated Eagle Ford Shale properties due to the high quality content of the crude and the geographic location of the production. The crude is considered “sweet” because of its low sulfur content and light because it has API gravity between 40 to 45 degrees. Since the production exists in relatively close proximity to refineries in Corpus Christi and Houston, we are able to acquire favorable end-market optionality. Crude oil can be transported via truck or pipeline to these markets, or to barge terminals which give us access to several refineries along the Texas and Louisiana Gulf Coast. These options allow us to take advantage of favorable price differentials between West Texas Intermediate (WTI) and Louisiana Light Sweet (LLS) markets. We currently receive an average net price in excess of $8.00 per barrel above WTI.

Since the third quarter of 2011, ZaZa has contracted Texla Energy Management, Inc. (“Texla”) to serve as its agent for the marketing and sale of natural gas production. We receive revenue from natural gas sales and natural gas liquid sales from our three producing Eagle Ford Shale wells. With current market conditions, we do not receive significant revenue from these sales; however, the high natural gas liquid content of the gas stream and high recovery percentage of these liquids translates into a net price that is well above the NYMEX settlement price. One hundred percent (100%) of revenue derived from gas sales is attributable to domestic customers and not foreign customers. Limited gas production that is not sold to Texla is flared.

In addition to our Eagle Ford Shale contracts, ZaZa Energy, LLC has also received bids from multiple buyers for both crude oil and natural gas production from its Eaglebine properties. With multiple buyer options, we believe we can assure competitive pricing, reduce buyer credit exposure and market production quickly if needed. Given the similar quality content of the crude oil and the same geographic location advantage as our existing production, we expect to receive a premium price for our crude oil that is as favorable as our Eagle Ford Shale production. Gas gathering and processing options are limited for our Eaglebine properties and will be addressed on a well-by-well basis. We are in the process of negotiating central gas gathering and processing options for all future Eaglebine production.

Competition

The oil and gas industry is highly competitive, and we compete with a substantial number of other companies that have greater resources than us. Many of these companies explore for, produce and market oil and gas, carry on refining operations and market the resulting products on a worldwide basis. The primary areas in which we encounter substantial competition are in locating and acquiring desirable leasehold acreage for development operations, locating and acquiring attractive producing oil and gas properties, and obtaining purchasers and transporters of the oil and gas it produces. There is also competition between producers of oil and gas and other industries producing alternative energy and fuel.

Furthermore, competitive conditions may be substantially affected by various forms of energy legislation and/or regulation considered from time to time by the federal, state and local government. It is not possible to predict the nature of any such legislation or regulation that may ultimately be adopted or its effects upon its future operations. Such legislation and regulations may, however, substantially increase the costs of exploring for, or the development, production or marketing of oil and gas and may prevent or delay the commencement or continuation of a given operation. The effect of these risks cannot be accurately predicted.

Summary of Oil and Natural Gas Reserves as of December 31, 2012 and 2011

The following table sets forth information about ZaZa's estimated net proved reserves at December 31, 2012 and 2011 for our properties in the Eagle Ford. Ryder Scott Company, L.P. (“Ryder Scott”), independent petroleum consultants, prepared our proved reserves as of December 31, 2012. Rex Morris, an independent petroleum reservoir engineer, audited our proved reserves as of December 31, 2011.We prepared the estimate of standardized measure of proved reserves in accordance with FASB ASC 932, "Extractive Activities-Oil and Gas." No reserve reports have been provided to any governmental agencies.

| | | | �� | | | | | | | |

| At December 31, 2012 | | At December 31, 2011 |

| Gas | | Oil | | Equivalent | | Gas | | Oil | | Equivalent |

| (MMcf) | | (MBbls) | | (MBOE) | | (MMcf) | | (MBbls) | | (MBOE) |

Proved developed | 303 | | 248 | | 299 | | 1,433 | | 443 | | 682 |

Proved undeveloped | 1,410 | | 2,815 | | 3,049 | | 2,696 | | 502 | | 951 |

Total proved | 1,713 | | 3,063 | | 3,348 | | 4,129 | | 945 | | 1,633 |

Our proved reserves at December 31, 2012 and 2011 were located in the Eagle Ford Shale in South Texas.

Internal Controls Over Reserves Estimates

Our policies regarding internal controls over the recording of reserves estimates require reserves to be in compliance with the SEC definitions and guidance and prepared in accordance with generally accepted petroleum engineering principles. Responsibility for compliance in reserves bookings is delegated to a qualified petroleum engineer in our Houston office. The petroleum engineer prepares all reserves estimates for our producing assets. Data used in these integrated assessments include information obtained directly from the subsurface via wellbores such as well logs, reservoir cores, fluid samples, static and dynamic information, production test data and production history. Other types of data used include 2D seismic recently reprocessed and calibrated to available well control. The tools used to interpret the data included reservoir modeling and simulation, Decline Curve Analyses and data analysis packages. We engage a third-party petroleum consulting firm to prepare all of our proved reserves. See "Third-Party Reserves Preparation" below.

Third-Party Reserves Preparation

The reserves preparation of ZaZa LLC as of December 31, 2012 was performed by Ryder Scott Company, L.P. (Ryder Scott). Ryder Scott evaluate oil and gas properties and independently certify petroleum reserve quantities in the U.S. and internationally. Founded in 1937, Ryder Scott is one of the largest, oldest and most respected reservoir-evaluation consulting firms in the industry. For the last 10 years, Ryder Scott has been the most widely used consulting firm for preparing annual petroleum reserves certifications for filers with the SEC, according to research firm John S. Herold, Ryder Scott also serves clients listed on the London, Ontario, Toronto, Hong Kong, Australian and other stock exchanges.

Ryder Scott determined that the estimates of reserves for ZaZa LLC conform to the guidelines of the SEC, including the criteria of "reasonable certainty," as it pertains to expectations about the recoverability of reserves in future years, under existing economic and operating conditions, consistent with the definition in the recently amended Rule 4-10(a) of Regulation S-X. Ryder Scott prepared our proved reserves as at December 31, 2012, based upon their evaluation. The report is attached to this Annual Report on Form 10-K as Exhibit 99.1.

The reserves audit of ZaZa LLC as of December 31, 2011 was performed by Rex Morris a Consulting Reservoir Engineer. Mr. Morris has over 30 years' experience as a practicing petroleum engineer specializing in reservoir modeling and economics. He earned a Bachelor's of Science in Natural Gas Engineering from Texas A&I University and is a member in good standing in the Society of Petroleum Engineers.

Rex Morris determined that our estimates of reserves for ZaZa LLC conform to the guidelines of the SEC, including the criteria of "reasonable certainty," as it pertains to expectations about the recoverability of reserves in future years, under existing economic and operating conditions, consistent with the definition in the recently amended Rule 4-10(a) of Regulation S-X. Rex Morris issued an unqualified audit opinion on our proved reserves at December 31, 2011, based upon his evaluation. The opinion concluded that our estimates of proved reserves were, in aggregate, reasonable and have been prepared in accordance with generally accepted petroleum engineering and

evaluation principles.

Proved Undeveloped Reserves

As of December 31, 2012, our proved undeveloped reserves ("PUDs") totaled 2,815 Mbbl of crude oil and 1,410 Mmcf of natural gas, all of which were associated with the Eagle Ford field. As of December 31, 2012, PUDs represented approximately 91% of our total proved reserves. We currently estimate that future development costs relating to the development of these PUDs are projected to be approximately $21.0 million in 2013, $37.6 million in 2014, $41.0 million in 2015 and $11.6 million in 2016

As of December 31, 2011, our proved undeveloped reserves ("PUDs") totaled 502 Mbbl of crude oil and 2,696 Mmcf of natural gas, all of which were associated with the Eagle Ford field. As of December 31, 2011, PUDs represented approximately 58% of our total proved reserves. We currently estimate that future development costs relating to the development of these PUDs are projected to be approximately $2.3 million, $1.8 million and $3.3 million in 2012, 2013 and 2014, respectively.

Insurance Matters

As is common in the oil and gas industry, we do not insure fully against all risks associated with our business either because such insurance is unavailable or because premium costs are considered prohibitive. A material loss not fully covered by insurance could have material adverse effect on our financial position, results of operations or cash flows. We maintain insurance at levels we believe to be customary in the industry to limit our financial exposure in the event of a substantial environmental claim resulting from sudden, unanticipated and accidental discharges of certain prohibited substances into the environment. Such insurance might not cover the complete amount of such a claim and would not cover fines or penalties for a violation of an environmental law.

Office Leases

We occupy 46,121 square feet of office space at 1301 McKinney St, Houston, Texas 77010; 6,376 square feet of office space at 600 Leopard St., Corpus Christi, Texas 78401; 374 square feet of office space at 13760 Noel Rd., Dallas, Texas 75240; and 2,000 square feet of office at 176 Hwy 19, Huntsville, Texas 77340. The total rental expense for 2012 was approximately $1.2 million.

Employees

ZaZa had 39 full-time employees, none of whom are represented by unions or are covered by collective bargaining agreements. To date, ZaZa has not experienced any strikes or work stoppages due to labor problems, and believes that it has good relations with its employees. In addition, ZaZa directly engages approximately 31 independent contractors.

Seasonal Nature of Business

Generally, but not always, the demand for gas decreases during the summer months and increases during the winter months. Seasonal anomalies such as mild winters or abnormally hot summers sometimes lessen this fluctuation. In addition, certain gas users utilize natural gas storage facilities and purchase some of their anticipated winter requirements during the summer. This can also lessen seasonal demand fluctuations. Seasonal weather conditions and lease stipulations can limit drilling and production activities and other oil and gas operations in certain areas. These seasonal anomalies can increase competition for equipment, supplies and personnel.

Internet Address/Availability of Reports

Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (the "Exchange Act"), are made available free of charge on our website at http://www.zazaenergy.com as soon as reasonably practicable after we electronically file such material with, or otherwise furnish it to, the SEC. Corporate governance materials, guidelines, charter and code of conduct are also available on the website. A copy of corporate governance materials is available upon written request to the

Company. The Company will disclose any changes or amendments to the Company’s code of ethics as well as waivers to the code of ethics by posting such changes or waivers on the Company’s website.

GLOSSARY OF OIL AND GAS TERMS

The terms defined in this section are used throughout this annual report on Form 10-K:

"3D" or "3D SEISMIC"—An exploration method of sending energy waves or sound waves into the earth and recording the wave reflections to indicate the type, size, shape, and depth of subsurface rock formations. 3D seismic lines are shot very close together. This allows for the ability for computers to generate seismic profiles in any direction and form 3D surfaces. 3D surveys are measured in square kilometers or square miles.

"Basin"—A large natural depression on the earth's surface in which sediments generally brought by water accumulate.

"Bbl"—One stock tank barrel, of 42 U.S. gallons liquid volume, used herein in reference to crude oil, condensate or natural gas liquids.

"Bcf"—One billion cubic feet of natural gas.

"BOE"—Barrel of oil equivalent. Oil equivalents are determined herein using the relative energy content method, with a ratio of 1.0 Bbl of oil or natural gas liquid to 6.0 Mcf of gas.

"Btu"—British thermal unit.

"Completion"—The process of treating a drilled well followed by the installation of permanent equipment for the production of oil or natural gas, or in the case of a dry hole, the reporting of abandonment to the appropriate agency.

"DD&A"—Depreciation, depletion, amortization and accretion.

"Developed acreage"—The number of acres that are allocated or assignable to productive wells or wells capable of production.

"Development well"—A well drilled within the proved area of an oil or natural gas reservoir to the depth of a stratigraphic horizon known to be productive.

"Exploratory well"—A well drilled to find and produce oil or natural gas reserves not classified as proved, to find a new reservoir in a field previously found to be productive of oil or natural gas in another reservoir or to extend a known reservoir.

"Field"—An area consisting of a single reservoir or multiple reservoirs all grouped on, or related to, the same individual geological structural feature or stratigraphic condition. The field name refers to the surface area, although it may refer to both the surface and the underground productive formations.

"Formation"—A layer of rock which has distinct characteristics that differs from nearby rock.

"Gross acres" or "gross wells"—The total acres or wells, as the case may be, in which a working interest is owned.

"Horizontal drilling"—A drilling technique used in certain formations where a well is drilled vertically to a certain depth and then drilled at a right angle within a specified interval.

"Horizontal well"—A well drilled using horizontal drilling techniques.

"Hydraulic fracturing"—A stimulation treatment routinely performed on oil and gas wells in low-permeability reservoirs. Specially engineered fluids are pumped at high pressure and rate into the reservoir interval to be treated, causing a vertical fracture to open. Commonly referred to as "fracking."

"Identified drilling locations"—Locations specifically identified by management as an estimation of our multi-year

drilling activities based on evaluation of applicable geologic, seismic, engineering, production and reserves data on contiguous acreage and geologic formations. The availability of local infrastructure, drilling support assets and other factors as management may deem relevant, such as spacing requirements, easement restrictions and state and local regulations, are considered in determining such locations. The drilling locations on which we actually drill wells will ultimately depend upon the availability of capital, regulatory approvals, seasonal restrictions, oil and natural gas prices, costs, actual drilling results and other factors.

"Liquids"—Describes oil, condensate and natural gas liquids.

"KM"—One kilometer.

"MBbls"—One thousand barrels of crude oil, condensate or natural gas liquids.

"MBOE"—One thousand barrels of oil equivalent.

"Mcf"—One thousand cubic feet of natural gas.

"MMBbl"—One million barrels of crude oil, condensate or natural gas liquids.

"MMBOE"—One million barrels of oil equivalent.

"MMBtu"—One million British thermal units.

"MMcf"—One million cubic feet of natural gas.

"Natural gas liquid"—Components of natural gas that are separated from the gas state in the form of liquids, which include propane, butanes and ethane, among others.

"Net acres"—The percentage of total acres an owner has out of a particular number of acres, or a specified tract. An owner who has 50% interest in 100 acres owns 50 net acres.

"NYMEX"—The New York Mercantile Exchange.

"Productive well"—A well that is found to be capable of producing hydrocarbons in sufficient quantities such that proceeds from the sale of the production exceed production expenses and taxes.

"Proved developed reserves ("PDP") —Reserves that can be expected to be recovered through existing wells with existing equipment and operating methods.

"Proved reserves"—The estimated quantities of oil, gas and natural gas liquids which geological and engineering data demonstrate with reasonable certainty to be commercially recoverable in future years from known reservoirs under existing economic and operating conditions.

"Proved undeveloped reserves ("PUD") —Proved reserves that are expected to be recovered from new wells on undrilled acreage or from existing wells where a relatively major expenditure is required for recompletion.

"Reservoir"—A porous and permeable underground formation containing a natural accumulation of producible oil and/or natural gas that is confined by impermeable rock or water barriers and is separate from other reservoirs.

"Spacing"—The distance between wells producing from the same reservoir. Spacing is often expressed in terms of acres, e.g., 40-acre spacing, and is often established by regulatory agencies.

"Standardized measure"—Discounted future net cash flows estimated by applying year-end prices to the estimated future production of year-end proved reserves. Future cash inflows are reduced by estimated future production and development costs based on period end costs to determine pre-tax cash inflows. Future income taxes, if applicable, are computed by applying the statutory tax rate to the excess of pre-tax cash inflows over our tax basis in the oil and gas properties. Future net cash inflows after income taxes are discounted using a 10% annual discount rate.

"Undeveloped acreage"—Lease acreage on which wells have not been drilled or completed to a point that would

permit the production of commercial quantities of oil and gas regardless of whether such acreage contains proved reserves.

"Unit"—The joining of all or substantially all interests in a reservoir or field, rather than a single tract, to provide for development and operation without regard to separate property interests. Also, the area covered by a unitization agreement.

"Working interest"—The right granted to the lessee of a property to explore for and to produce and own natural gas or other minerals. The working interest owners bear the exploration, development, and operating costs on either a cash, penalty, or carried basis.

ITEM 1A. RISK FACTORS

Risks Related to Our Company

Our independent registered public accounting firm expressed substantial doubt regarding our ability to continue as a going concern in their audit opinion for our December 31, 2012 financial statements.

Our audited financial statements for the year ended December 31, 2012 have been prepared under the assumption that we will continue as a going concern. Our independent registered public accounting firm has issued their report dated April 1, 2013, in connection with the audit of our financial statements for the year ended December 31, 2012 that included an explanatory paragraph describing the existence of conditions that raise substantial doubt about our ability to continue as a going concern due to our liquidity. The fact that we have received this “going concern qualification” from our independent registered public accounting firm will likely make it more difficult for us to raise capital on favorable terms and could hinder, to some extent, our operations. Additionally, if we are not able to continue as a going concern, it is possible stockholders may lose part or all of their investment. Our financial statements do not include any adjustments that might result from the outcome of this uncertainty.

Our development and exploration operations require substantial capital and we may be unable to obtain needed capital or financing on satisfactory terms or at all, which could lead to a loss of properties and a decline in our oil and gas reserves.

The oil and gas exploration and development industry is capital intensive. We expect to continue making substantial capital expenditures in our business and operations for the purpose of exploration, development, production and acquisition of, oil and gas reserves. Historically, we financed capital expenditures in part from contributions, bonus payments and cost reimbursements by Hess under our joint venture with them. As a result of the termination of our joint venture with Hess in 2012, we have sold assets and incurred indebtedness in order to provide capital to carry out our activities. To maintain our oil and gas leases and pursue our planned drilling program, we will need to raise additional capital. Our cash flow from operations and access to capital are subject to a number of variables that may or may not be within our control, including:

· | the level of oil and gas we are able to produce from existing wells; |

· | the prices at which our oil and gas production is sold; |

· | the results of our development programs associated with proved and unproved reserves; |

· | our ability to acquire, locate and produce new economically recoverable reserves; |

· | global credit and securities markets; and |

· | the ability and willingness of lenders and investors to provide capital and the cost of that capital. |

We will need to raise capital to maintain our oil and gas leases and finance our drilling operations. We intend to pursue various strategies to raise capital, including asset sales, debt or equity financing, and joint ventures. However, our existing indebtedness contains covenants that restrict our ability to pursue these strategies. If we are unable to sell assets or if financing and joint venture partnerships are not available on acceptable terms or at all, we may have limited ability to obtain the capital necessary to sustain our operations at current levels or to implement our strategy, including executing on our portfolio of drilling opportunities or expanding our existing portfolio. There can be no assurance as to our ability to sell assets or as to the availability or terms of any joint ventures or other financing.

The failure to obtain additional capital could result in an inability to implement our strategy to pursue our drilling program and a curtailment of our operations relating to exploration and development of our prospects, which in turn could lead to possible write-downs in the carrying value of our properties, a material decline in our oil and gas reserves as well as our revenues and results of operations. The failure to obtain additional capital could also materially adversely affect our operations and prospects, including potentially resulting in the reversion of certain portions of our acreage to the lessors.

If we are unable to find a joint venture partner or partners in the Eagle Ford to finance development costs or to complete the joint development of our Eaglebine acreage with EOG Resources, we may need to find alternative sources of capital, which may not be available on favorable terms, or at all.

We are currently planning to have discussions with potential joint venture partners to develop our properties in the Eagle Ford trend, evaluating asset sale options for our properties in the Eagle Ford trend, and have recently entered into a joint development arrangement with EOG Resources for certain of our Eaglebine acreage. ZaZa holds approximately 89,000 net acres in the Eaglebine (before giving effect to any transfers of interests therein to EOG Resources), and approximately 66,000 net acres in the Eagle Ford (before giving effect to our sale of our Moulton properties). There can be no assurances that we will identify a joint venture partner or partners for our Eagle Ford acreage or that such partner(s) will provide funding on acceptable terms to develop the existing properties or acquire new properties. There can be no assurances that we will be able to sell assets in the Eagle Ford trend at valuations we deem acceptable. There can also be no assurances that EOG Resources will elect to proceed with subsequent phases of the joint development of our Eaglebine acreage. If we cannot identify a joint venture partner or partners for our Eagle Ford acreage, sell assets at acceptable valuations or are unable to complete the joint development of our Eaglebine acreage, we will need to utilize cash flow from other operations or will need to find alternative sources of capital to finance operations, which may slow the development of our properties and have a material adverse effect on our operations and prospects.

Joint venture agreements that we may enter into could present a number of challenges that could have a material adverse effect on our business, financial condition and results of operations.

We are seeking joint venture partners to develop our properties in the Eagle Ford trend and have recently entered into a joint development arrangement with EOG Resources for certain of our Eaglebine acreage. Joint venture and joint development arrangements typically present financial, managerial and operational challenges, including potential disputes, liabilities or contingencies and may involve risks not otherwise present when exploring and developing properties directly, including, for example:

· | the joint venture partners may share certain approval rights over major decisions, including the acquisition of oil and gas properties; |

· | the joint venture partners may not pay their share of the joint venture’s obligations, potentially leaving us liable for their share of such obligations; |

· | the joint venture partners may have options to assume the operation of the properties acquired by the joint venture; |

· | the joint venture partners may terminate the agreements under certain circumstances; |

· | we may incur liabilities or losses as a result of an action taken by the joint venture partners; and |

· | disputes between us and the joint venture partners may result in delays, litigation or operational impasses. |

The risks described above or the failure to continue any joint venture or joint development arrangement or to resolve disagreements with the joint venture partners could materially adversely affect our ability to transact the business that is the subject of such joint venture, which would in turn negatively affect our financial condition and results of operations.

Our indebtedness and near term obligations could materially adversely affect our financial health, limit our ability to finance capital expenditures and future acquisitions and prevent us from executing our business strategy.

We have approximately $33 million outstanding in aggregate principal under our Senior Secured Notes due 2017 (the “Senior Secured Notes”) and $40 million outstanding in aggregate principal under our 9% Convertible Senior Notes due 2017 (the “Convertible Notes”) and we may incur additional indebtedness in the future. In addition, we have approximately $47 million outstanding in aggregate principal amount under our Subordinated Notes. Our level of indebtedness has, or could have, important consequences to our business, because:

· | a substantial portion of our cash flows from operations will have to be dedicated to interest and principal payments and may not be available for operations, working capital, capital expenditures, expansion, acquisitions or general corporate or other purposes; |

· | it may impair our ability to obtain additional financing in the future for acquisitions, capital expenditures or general corporate purposes; |

· | it may limit our flexibility in planning for, or reacting to, changes in our business and industry; and |

· | we may be substantially more leveraged than some of our competitors, which may place us at a relative competitive disadvantage and make us more vulnerable to downturns in our business, our industry or the economy in general. |

In addition, the terms of our Senior Secured Notes and our Convertible Notes restrict, and the terms of any future indebtedness, including any future credit facility, may restrict our ability to incur additional indebtedness and grant liens because of debt or financial covenants we are, or may be, required to meet. Thus, we may not be able to obtain sufficient capital to grow our business or implement our business strategy and may lose opportunities to acquire interests in oil properties or related businesses because of our inability to fund such growth.

Our ability to comply with restrictions and covenants, including those in our Senior Secured Notes, Convertible Notes or in any future debt agreement, is uncertain and will be affected by the levels of cash flow from our operations and events or circumstances beyond our control. Our Senior Secured Notes also contain restrictions on the operation of our business, such as limitations on the sale and acquisition of assets, limitations on entering into joint ventures, limitations on restricted payments, limitations on mergers and consolidations, limitations on loans and investments, and limitations on the lines of business in which we may engage, which may limit our activities. Our Convertible Notes contain certain of the foregoing restrictions as well. We must obtain consent from the holders of a majority of the Senior Secured Notes for all transactions involving oil and gas properties, with certain carveouts and requirements to apply a portion of net sales proceeds to pay down the Senior Secured Notes and with certain carveouts to enter into our joint venture with EOG and to sell our Moulton acreage. Thus, we may not be able to manage our cash flow in a manner that maximizes our business opportunities. Our failure to comply with any of the restrictions and covenants could result in a default, which could permit the holders of our Senior Secured Notes and our Convertible Notes to accelerate repayments and foreclose on the collateral securing the indebtedness.

We may not have the ability to raise the funds necessary to purchase the Senior Secured Notes and the Convertible Notes upon a fundamental change, and our future debt may contain limitations on our ability to purchase the Senior Secured Notes and the Convertible Notes.

Holders of the Senior Secured Notes and the Convertible Notes will have the right to require us to purchase the notes upon the occurrence of a fundamental change at 101% and 100%, respectively, of their principal amount plus accrued and unpaid interest. However, we may not have enough available cash or be able to obtain financing at the time we are required to make purchases of tendered Senior Secured Notes and Convertible Notes. In addition, our ability to purchase the Senior Secured Notes and Convertible Notes may be limited by law, by regulatory authority or by the agreements governing our then current and future indebtedness. Our failure to purchase tendered Senior Secured Notes and Convertible Notes at a time when the purchase is required by the terms of the Senior Secured Notes or Convertible Notes would constitute a default under those notes. A default under those notes or the fundamental change itself could also lead to a default or require a prepayment under, or result in the acceleration of the maturity or purchase of, our existing or future other indebtedness. The requirement that we offer to purchase the Senior Secured Notes and Convertible Notes upon a fundamental change is limited to the transactions specified in the definition of a “fundamental change,” which definition may differ from the definition of a “fundamental change” or “change of control” in the agreements governing our existing or future other indebtedness. If the repayment of the related indebtedness were to be accelerated after any applicable notice or grace periods, we may not have sufficient funds to repay the indebtedness and purchase the Senior Secured Notes and the Convertible Notes.

If we do not satisfy our drilling obligations under our agreement with Range, we could lose a portion of our acreage and revenue stream in the Eaglebine, which could adversely affect our expected revenues.

On March 28, 2012, the Company entered into a Participation Agreement (the “Range Agreement”), and associated Joint Operating Agreement, with Range Texas Production, LLC (“Range”), a subsidiary of Range Resources Corporation, under which the Company agreed to acquire a 75% working interest from Range in certain leases located in Grimes Country, Texas (the “Leases”). Pursuant to the terms of the Range Agreement, Range retained a 25% working interest in the Leases and the Company committed to drill a well (the “Commitment Well”). The Company recently ceased completion operations at the Commitment Well, and effective January 16, 2013, the Company and Range entered into an Amendment No. 5 to the Range Agreement (the “Amendment”). Under the terms of the Amendment, if the Company fails to commence re-completion operations at the Commitment Well (the “Re-entry Well”) in a bona fide attempt to complete the Re-entry Well as a vertical well within 60 days of January 16, 2013 (the Company has timely commenced such operations) or fails to commence drilling of a substitute well for the Commitment Well within 180 days of January 16, 2013, the Company will be required to assign a 25% working interest in the Leases to Range, resulting in the Company retaining a 50% working interest in the Leases,

and transfer operatorship in the Leases to Range. If the Company fails to meet either of these deadlines, the foregoing remedies will have an impact on our expected revenues in the Eaglebine.

Our ability to use net operating loss carryforwards to offset future taxable income may be limited or such net operating loss carryforwards may expire before utilization.

As of December 31, 2012, we had U.S. federal tax net operating loss carryforwards (“NOLs”) of approximately $45.2 million, which expire at various dates from fiscal year 2026 through fiscal year 2032. These net operating loss carryforwards, subject to certain requirements and restrictions, including limitations on their use as a result of an “ownership change”, may be used to offset future taxable income and thereby reduce our U.S. federal income taxes otherwise payable. We are required to evaluate the likelihood of utilizing the NOLs according to a “more likely than not” standard in accordance with GAAP and, if as a result of such evaluation we determine we may not be able to meet such standard, we may be required to recognize a valuation allowance for this deferred tax asset. The recognition of a valuation allowance would reduce earnings and would also result in a corresponding reduction of stockholders’ equity. Recognition of a valuation allowance is a non-cash charge to earnings and it does not preclude us from using the NOLs to reduce future taxable income otherwise payable. Section 382 of the Internal Revenue Code of 1986, as amended (the “Code”), imposes an annual limit on the ability of a corporation that undergoes an “ownership change” to use its net operating loss carry forwards to reduce its tax liability. The amount of taxable income in each tax year after the ownership change that may be offset by pre-change NOLs and certain other pre-change tax attributes is generally equal to the product of (a) the fair market value of the corporation’s outstanding stock immediately prior to the ownership change and (b) the long-term tax exempt rate (i.e., a rate of interest established by the Internal Revenue Service that fluctuates from month to month). An “ownership change” would occur if stockholders, deemed under Section 382 to own 5% or more of our capital stock by value, increase their collective ownership of the aggregate amount of our capital stock to more than 50 percentage points over a defined period of time. In the event of certain changes in our stockholder base, we may at some point in the future experience an “ownership change” as defined in Section 382 of the Code. Accordingly, our use of the net operating loss carryforwards and credit carryforwards may be limited at some point in the future by the annual limitations described in Sections 382 and 383 of the Code.

We have disclosed a material weakness in our internal disclosure controls and procedures which could erode investor confidence, jeopardize our ability to obtain insurance, and limit our ability to attract qualified persons to serve at ZaZa.

As of December 31, 2012, an evaluation was conducted by ZaZa management, including our Chief Executive Officer and Chief Financial Officer, as to the effectiveness of the design and operation of our disclosure controls and procedures pursuant to Rules 13a-15(e) and 15d-15(e) of the Exchange Act. Based on that evaluation, our management concluded that our disclosure controls and procedures were not effective as of December 31, 2012 because of material weaknesses in our internal controls over financial reporting resulting from the write off of exploration costs associated with a failed lateral portion of an exploratory well, and an error in the calculation of certain deferred income tax losses.

Our management believes that this error was a result of the failure of coordination between our personnel that make our determinations of well outcomes and our personnel that prepare our financial statements. This evaluation is more fully described elsewhere in this Annual Report on form 10-K for the fiscal year ended December 31, 2012. Failure to comply with rules regarding internal controls and procedures may make it more difficult for us to obtain certain types of insurance, including director and officer liability insurance. We may be forced to accept reduced policy limits and coverage and/or incur substantially higher costs to obtain the same or similar coverage. The impact of these events could also make it more difficult for us to attract and retain qualified persons to serve on our Board of Directors, on committees of our Board of Directors, or as executive officers.

Our management identified an error in the calculation of certain deferred tax liabilities for the period ended March 31, 2012. This error was corrected prior to our filing of the financial statements for such period with the SEC. Accordingly, management believes that the financial statements included in this report fairly present in all material respects our financial condition, results of operations and cash flows for the periods presented. Notwithstanding the correct presentation in our financial statements, our management believes that this error was a result of the failure of coordination between our personnel that calculate our tax liabilities and our personnel that prepare the financial statements.

Management is reviewing remediation steps necessary to address the material weaknesses and to improve our internal control over financial reporting. We intend to correct the material weaknesses promptly.

Title to the properties in which ZaZa has an interest may be impaired by title defects.

ZaZa generally obtains title opinions on significant properties that it drills or acquires. Additionally, undeveloped acreage has greater risk of title defects than developed acreage. Generally, under the terms of the operating agreements affecting its properties, any monetary loss is to be borne by all parties to any such agreement in proportion to their interests in such property. If there are any title defects or defects in assignment of leasehold rights in properties in which ZaZa holds an interest, we could suffer a material financial loss.

The unavailability or high cost of drilling rigs, equipment, raw materials, supplies, personnel and oil field services could materially adversely affect our ability to execute our exploration and development plans on a timely basis and within its budget.

Our industry is cyclical and, from time to time, there is a shortage of drilling rigs, equipment, raw materials (particularly sand, cement and other proppants), supplies or qualified personnel. During these periods, the costs and delivery times of rigs, equipment, raw materials and supplies are substantially greater. In addition, the demand for, and wage rates of, qualified drilling rig crews rise as the number of active rigs in service increases. If oil and gas prices increase in the future, increasing levels of exploration, development and production could result in response to these stronger prices, and as a result, the demand and the costs of oilfield services, drilling rigs, raw materials, supplies and equipment could increase, while the quality of these services and supplies may suffer. In addition, our exploration, development and production operations also require local access to large quantities of water supplies and disposal services for produced water in connection with our hydraulic fracture stimulations due to prohibitive transportation costs. Existing shortages of drilling rig service providers for pressure pumping and other services required for well completion in the Eagle Ford shale have delayed our development and production operations and caused us to incur additional expenditures that were in excess of those provided for in its capital budget. We cannot determine the magnitude or length of these shortages or future shortages or price increases, which could have a material adverse effect on its business, cash flows, financial condition or results of operations. In addition, shortages and price increases could restrict our ability to drill wells and conduct ordinary operations.

Drilling for and producing oil and gas are high-risk activities with many uncertainties that could materially adversely affect our financial condition and results of operations.

Our success will depend on the results of our exploration, development and production activities. Oil and gas exploration, development and production activities are subject to numerous risks beyond our control, including the risk that drilling will not result in commercially viable oil or gas production. Decisions to purchase, explore, develop or otherwise exploit prospects or properties will depend in part on the evaluation of data obtained through geophysical and geological analyses, production data, and engineering studies, the results of which are often inconclusive or inaccurate or subject to varying interpretations or uncertainty. Costs of drilling, completing and operating wells are often uncertain before drilling commences. Overruns in budgeted expenditures are common risks that can make a particular project uneconomical. Furthermore, many factors may curtail, delay or cancel drilling, and such work stoppage may not be covered by our insurance, including:

· | shortages of or delays in obtaining equipment and qualified personnel; |

· | pressure or irregularities in geological formations; |

· | equipment failures or accidents; |

· | the joint venture partners may not pay their share of the joint venture’s obligations, potentially leaving us liable for their share of such obligations; |

· | the joint venture partners may have options to assume the operation of the properties acquired by the joint venture; |

· | the joint venture partners may terminate the agreements under certain circumstances; |

· | we may incur liabilities or losses as a result of an action taken by the joint venture partners; and |

· | disputes between us and the joint venture partners may result in delays, litigation or operational impasses. |

The risks described above or the failure to continue any joint venture or to resolve disagreements with the joint venture partners could materially adversely affect our ability to transact the business that is the subject of such joint venture, which would in turn negatively affect our financial condition and results of operations.

Numerous uncertainties will be inherent in our estimates of oil and gas reserves and estimated reserve quantities, and the present value calculations presented in the future relating to such reserves may not be accurate. Any material inaccuracies in reserve estimates or underlying assumptions will affect materially the estimated quantities and present value of our reserves.

There are numerous uncertainties inherent in estimating quantities of proved oil and gas reserves and cash flows attributable to such reserves, including factors beyond our engineers’ control (or the third party preparing the reserve report). Reserve engineering is a subjective process of estimating underground accumulations of oil and gas that cannot be measured in an exact manner. The accuracy of an estimate of quantities of reserves, or of cash flows attributable to such reserves, is a function of the available data, assumptions regarding future oil and gas prices, expenditures for future development and exploration activities, engineering and geological interpretation and judgment. In addition, accurately estimating reserves in shale formations such as ours can be even more difficult than estimating reserves in more traditional hydrocarbon bearing formations given the complexities of the projected decline curves and economics of shale gas wells. Additionally, “probable” and “possible” reserve estimates are estimates of unproved reserves and may be misunderstood or seen as misleading to investors that are not experts in the oil or natural gas industry. As such, investors should not place undue reliance on these estimates. Reserves and future cash flows may be subject to material downward or upward revisions, based upon production history, development and exploration activities and prices of oil and gas. In addition, different reserve engineers may make different estimates of reserves and cash flows based on the same available data.

The present value of future net revenues from our proved reserves referred to in any reserve report will not necessarily be the actual current market value of our estimated oil and gas reserves at such time. In accordance with SEC requirements, we base the estimated discounted future net cash flows from its proved reserves using the un-weighted arithmetic average of the first day of the month for each month within a twelve month period.

Unless we replace our reserves, our reserves and production will decline, which would adversely affect our financial condition, results of operations and cash flows.