Table of Contents

Index to Financial Statements

As filed with the Securities and Exchange Commission on October 25, 2011

Registration No. 333-176753

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1

to

Form S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

FTS International, LLC

to be converted as described herein into a corporation named

FTS International, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 1389 | 45-1610731 | ||

(State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) |

777 Main Street, Suite 3000

Fort Worth, Texas 76102

(817) 862-2000

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Marcus C. Rowland

Chief Executive Officer

FTS International, LLC

777 Main Street, Suite 3000

Fort Worth, Texas 76102

(817) 862-2000

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Michael S. Telle Bracewell & Giuliani LLP 711 Louisiana Street, Suite 2300 Houston, Texas 77002 (713) 221-1327 | David J. Beveridge Shearman & Sterling LLP 599 Lexington Avenue New York, New York 10022 (212) 848-4000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | þ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission acting pursuant to said Section 8(a), may determine.

Table of Contents

Index to Financial Statements

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion

Preliminary Prospectus dated October 25, 2011

PROSPECTUS

Shares

FTS International, Inc.

Common Stock

This is FTS International’s initial public offering. We are selling shares of our common stock and the selling stockholder is selling shares of our common stock. We will not receive any proceeds from the sale of shares to be offered by the selling stockholder.

We expect the public offering price to be between $ and $ per share. Currently, no public market exists for the shares. After pricing of the offering, we expect that the shares will trade on the New York Stock Exchange under the symbol “ .”

Investing in our common stock involves risks that are described in the “Risk Factors” section beginning on page 18 of this prospectus.

Per Share | Total | |||||||

Public offering price | $ | $ | ||||||

Underwriting discount | $ | $ | ||||||

Proceeds, before expenses, to us | $ | $ | ||||||

Proceeds, before expenses, to the selling stockholder | $ | $ | ||||||

The underwriters may also exercise their option to purchase up to an additional shares from us, and up to an additional shares from the selling stockholder, at the public offering price, less the underwriting discount, for 30 days after the date of this prospectus to cover over-allotments, if any.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The shares will be ready for delivery on or about , 2011.

| BofA Merrill Lynch | Goldman, Sachs & Co. |

| Citigroup | Credit Suisse |

The date of this prospectus is , 2011.

Table of Contents

Index to Financial Statements

Table of Contents

Index to Financial Statements

| 1 | ||||

| 18 | ||||

| 32 | ||||

| 33 | ||||

| 33 | ||||

| 34 | ||||

| 35 | ||||

| 36 | ||||

MANAGEMENT’S DISCUSSIONAND ANALYSISOF FINANCIAL CONDITIONAND RESULTSOF OPERATIONS | 38 | |||

| 57 | ||||

| 81 | ||||

| 88 | ||||

| 100 | ||||

| 104 | ||||

| 106 | ||||

| 108 | ||||

| 112 | ||||

| 114 | ||||

MATERIAL U.S. FEDERAL INCOME TAX CONSIDERATIONSTO NON-U.S. HOLDERS | 117 | |||

| 121 | ||||

| 128 | ||||

| 128 | ||||

| 129 | ||||

| F-1 |

We are responsible for the information contained in this prospectus and in any free writing prospectus we may authorize to be delivered to you. Neither we nor the underwriters have authorized anyone to provide you with additional or different information. We and the underwriters are offering to sell, and seeking offers to buy, these securities only in jurisdictions where offers and sales are permitted. The information in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or any sale of these securities.

Industry and Market Data

The market data and certain other statistical information used throughout this prospectus are based on independent industry publications, government publications or other published independent sources. Some data is also based on our good faith estimates. Although we believe these third-party sources are reliable and that the information is accurate and complete, we have not independently verified the information.

i

Table of Contents

Index to Financial Statements

This summary provides a brief overview of information contained elsewhere in this prospectus. This summary does not contain all the information that you should consider before investing in our common stock. You should read the entire prospectus carefully before making an investment decision, including the information presented under the headings “Risk Factors,” “Cautionary Note Regarding Forward-Looking Statements” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the historical consolidated financial statements and related notes thereto included elsewhere in this prospectus.

The historical financial information presented in this prospectus for periods and as of dates prior to May 6, 2011 is the historical consolidated financial information of Frac Tech Holdings, LLC, which we refer to as our “predecessor.” The historical financial information presented in this prospectus for periods and as of dates on or after May 6, 2011 is the historical consolidated financial information of FTS International, LLC, which we will convert into a Delaware corporation named FTS International, Inc. prior to the consummation of this offering. In this prospectus, unless the context otherwise requires, the terms “we,” “us,” “our” or “ours” refer to Frac Tech Holdings, LLC and its subsidiaries and predecessor entities before May 6, 2011, to FTS International, LLC and its subsidiaries on or after May 6, 2011 until the time of its conversion into a Delaware corporation and to FTS International, Inc. and its subsidiaries from and after such conversion. See “History and Conversion.”

Our Company

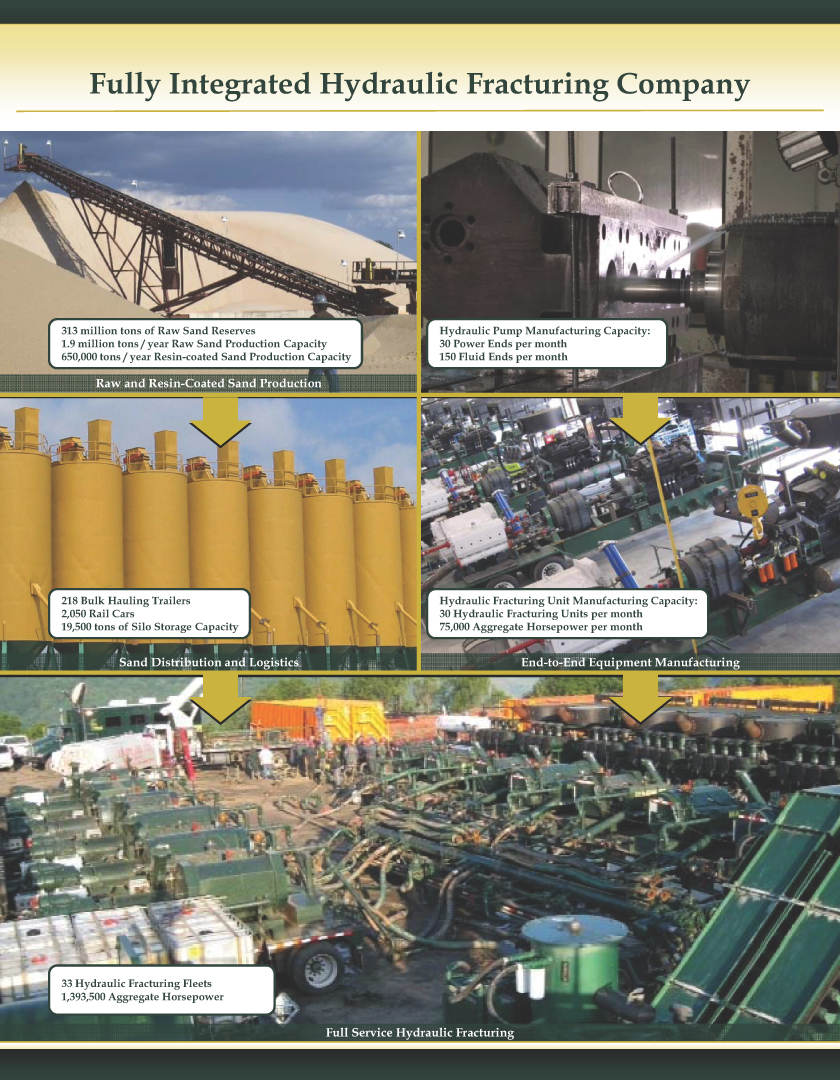

We are a leading independent provider of oil and natural gas well stimulation services with expertise in high-pressure hydraulic fracturing. We currently operate 33 hydraulic fracturing fleets with 1,393,500 horsepower in the aggregate. We have leading positions in the primary U.S. shale plays and are actively exploring international expansion into areas where the geology is similar to the U.S. unconventional basins in which we currently operate. We are vertically integrated unlike the majority of our competitors. We manufacture many of the components of our hydraulic fracturing units, mine, process and transport a majority of our proppant requirements and formulate and blend a portion of the chemicals we use in our operations.

We believe the vertical integration of our operations reduces our operating costs, increases our asset utilization, improves our supply chain flexibility and responsiveness and ultimately enhances our financial performance and ability to provide high-quality customer service. We manufacture durable equipment based on proprietary designs that we believe provides superior performance in the most demanding applications while extending the useful life of our equipment. Unlike manufacturers without service operations, we are able to incorporate the knowledge acquired in our hydraulic fracturing operations to improve our equipment designs. We also have significant maintenance and repair capabilities, and we manufacture replacement parts to support our operations and enhance our asset utilization. Our raw sand reserves and processing operations provide us with ready access to the two principal proppants we use in our operations, raw sand and resin-coated sand, which can often be in short supply in the required specifications. Additionally, we formulate and blend a portion of the chemical compounds we use in our operations, which allows us to provide tailored solutions to our customers. Our chemical offerings include some of the most environmentally friendly products in the industry, most of which produce no harmful by-products and require no auxiliary chemicals. Our technical staff of engineers, chemists, technicians and a geologist support our operations by optimizing the design and delivery of our equipment, products and services and by continually seeking to improve the quality, durability and effectiveness of the solutions we provide to our customers.

Our revenues have grown from $214.4 million in 2006 to $1,286.6 million in 2010, a compound annual growth rate of 56.5%. For the six months ended June 30, 2011 our revenues were $1,096.4 million and our Adjusted EBITDA was $453.5 million, representing increases of 143% and 178%, respectively, compared to the

1

Table of Contents

Index to Financial Statements

six months ended June 30, 2010. We are benefitting from a number of positive industry developments, including a dramatic increase in the amount and efficiency of horizontal drilling activity, an increase in the number of hydraulic fracturing stages per well and an increase in drilling activity in oil- and liquids-rich shale formations. These trends have led to increased asset utilization in our industry and a tight supply of fracturing fleets, proppants and other fracturing-related services and products. We also believe there is growing international interest in horizontal drilling and fracturing methods.

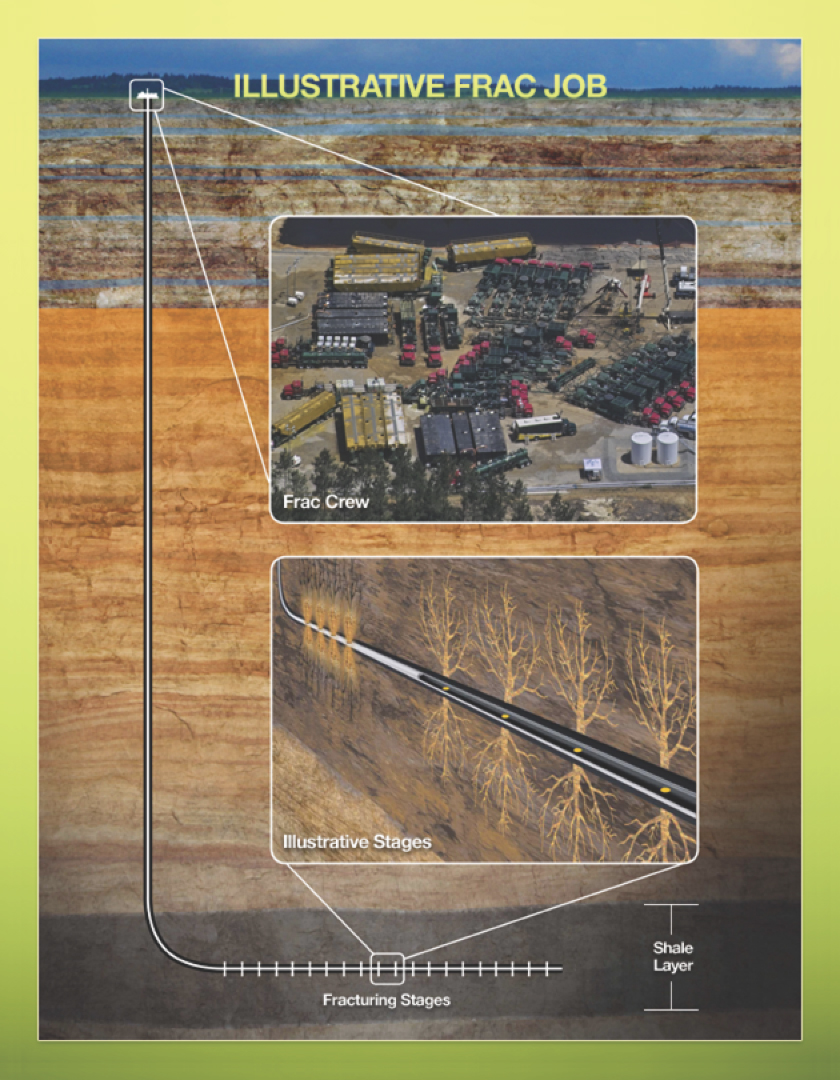

Our fleets consist of mobile hydraulic fracturing units and other auxiliary heavy equipment to perform fracturing services. Our hydraulic fracturing units consist primarily of a high-pressure hydraulic pump, a diesel engine, a transmission and various hoses, valves, tanks and other supporting equipment that are typically mounted on a flat-bed trailer. The group of hydraulic fracturing units, other equipment and vehicles necessary to perform a typical fracturing job is referred to as a “fleet” and the personnel assigned to each fleet are commonly referred to as a “crew.” In areas where we operate on a 24-hour-per-day basis, we typically staff two crews per fleet. The following table summarizes the amount of horsepower and the number of hydraulic fracturing fleets that we operate as of August 31, 2011:

Formation | Location | Total Horsepower | Fleets | |||||||

Haynesville Shale | Louisiana, East Texas | 396,750 | 7 | |||||||

Eagle Ford Shale | South Texas | 281,000 | 6 | |||||||

Marcellus Shale | Pennsylvania, West Virginia | 242,750 | 6 | |||||||

Permian Basin | West Texas, New Mexico | 201,550 | 7 | |||||||

Bakken Shale | North Dakota, Montana | 106,750 | 3 | |||||||

Granite Wash | Oklahoma, North Texas | 97,500 | 2 | |||||||

Barnett Shale | North Texas | 45,000 | 1 | |||||||

Rockies | Utah | 22,200 | 1 | |||||||

|

|

|

| |||||||

Total | 1,393,500 | 33 | ||||||||

Exploration and production (“E&P”) companies operating in the United States use our services primarily to enhance their recovery rates from wells drilled in shale and other unconventional reservoirs. Our operations are focused primarily in unconventional oil and natural gas formations in the Haynesville Shale, the Eagle Ford Shale, the Marcellus Shale, the Permian Basin and the Bakken Shale. We believe we have one of the largest market shares of any hydraulic fracturing service provider in the Haynesville Shale, the Eagle Ford Shale and the Marcellus Shale, based on number of fleets. In recent months, we have obtained an increasing number of engagements in connection with oil-directed drilling, particularly in the Eagle Ford Shale and the Permian Basin. In 2011, we began serving customers in the Bakken Shale and the Granite Wash formation. Our engagements in these areas primarily relate to horizontal drilling for oil and other hydrocarbon liquids. We expect to continue to deploy new fleets in additional regions with significant oil- and liquids-directed drilling activity through the end of 2011. The customers we currently serve are primarily large E&P companies such as Chesapeake Energy Corporation (“Chesapeake”), Anadarko Petroleum Corporation, El Paso Corporation, Marathon Oil Corporation, Petrohawk Energy (owned by BHP Billiton Ltd.), Range Resources Corporation and XTO Energy (owned by Exxon Mobil Corporation).

We currently manufacture many of the components of our hydraulic fracturing units, including all of the hydraulic pumps, and we assemble all of the hydraulic fracturing units in our fleets. At full capacity, we are capable of producing up to 30 hydraulic fracturing units, with an aggregate of approximately 75,000 horsepower, per month. To increase the durability, reliability and utilization of our hydraulic fracturing units, we manufacture a proprietary hydraulic pump consisting of two key assemblies, a power end and a fluid end. Although the power end of our pumps generally lasts several years, the fluid end, which is the part of the pump through which the fracturing fluid is expelled under high pressure, is a shorter-lasting consumable, often lasting less than one year. We currently have the capacity to manufacture up to 30 power ends and 150 fluid ends per month to equip new

2

Table of Contents

Index to Financial Statements

hydraulic fracturing units and to replace the fluid ends on our existing units. Because we build and service our own fluid ends, they are designed to provide high performance at low cost and to have greater longevity than those manufactured by third parties.

We own and operate sand mines, related processing facilities, resin-coating facilities and a distribution network that provide us with a reliable and low cost supply of raw and resin-coated sand. Our raw sand operations supplied approximately 65.1% and 76.5% of the raw sand we used as proppants in our hydraulic fracturing operations during 2010 and the six months ended June 30, 2011, respectively. Our resin-coating operations supplied approximately 49.3% and 57.6% of the resin-coated sand we used as proppants during 2010 and the six months ended June 30, 2011, respectively. We have processing plants at our two sand mines in Texas and Missouri and also obtain and process sand from agricultural sources in Wisconsin. We are currently capable of processing approximately 1.9 million tons per year of raw sand, which is the most common type of proppant we use in our hydraulic fracturing operations. As of June 30, 2011, we had an estimated 313 million tons of probable sand reserves. See “Business—Sand Production and Distribution—Sand Reserves.” Our resin-coating facilities currently have the capacity to produce approximately 650,000 tons of resin-coated sand annually. Resin-coated sand is raw sand that has been processed and coated with resin and has a greater resistance to crushing forces compared to raw sand. We use resin-coated sand as a proppant in the more geologically challenging formations that require fracturing at higher pressures. We intend to expand our raw sand and resin-coated sand production capacity over the next 12 months. See “Business—Sand Production and Distribution—Sand Production.” In addition to our mines and processing plants, we have eight operating sand distribution facilities in Texas, Louisiana and Pennsylvania, 218 bulk hauling trailers for highway transportation and approximately 2,050 rail cars, which enable us to deliver proppants to our fracturing jobs quickly and on short notice.

In addition, we formulate and blend a portion of the chemical compounds that we use in fracturing fluids at our chemical manufacturing facility and research and development laboratories.

Industry Overview

The pressure pumping industry provides hydraulic fracturing and other well stimulation services to E&P companies. Hydraulic fracturing involves pumping a fluid down a well casing or tubing under high pressure to cause the underground formation to crack, allowing the oil or natural gas to flow more freely. A propping agent, or “proppant,” is suspended in the fracturing fluid and props open the cracks created by the hydraulic fracturing process in the underground formation. Proppants generally consist of sand, resin-coated sand or ceramic particles. The total size of the hydraulic fracturing market, based on revenue, was estimated to be approximately $10.5 billion in 2009, $18.0 billion in 2010 and is estimated to be $22.5 billion in 2011 based on data from a 2011 report by Spears & Associates.

When drilling a horizontal well, the E&P company directs drillers to drill vertically into the formation, and steer the drill string to create a horizontal section of the wellbore inside the target formation, which is referred to as a “lateral.” This lateral is divided into “stages” which are isolated zones that focus the high-pressure fluid and proppant from the hydraulic fracturing fleet into distinct portions of the wellbore and surrounding formation. Customers typically compensate hydraulic fracturing service providers based on the number of stages fractured.

The main factors influencing demand for hydraulic fracturing services in North America are the level of horizontal drilling activity by E&P companies and the fracturing requirements, including the number of fracturing stages and the volume of fluids, chemicals and proppant pumped per stage, in the respective resource plays. The hydraulic fracturing market is cyclical and is largely influenced by drilling and completion expenditures by our customers. Since late 2009, there has been a significant increase in both horizontal drilling activity and related hydraulic fracturing requirements, which has increased the demand for our services.

3

Table of Contents

Index to Financial Statements

Industry Trends Impacting Our Business

Industry revenues are generally impacted by the following trends and have recently been growing significantly in excess of rig count.

Increase in Fracturing Stages Resulting from Horizontal Drilling Activity

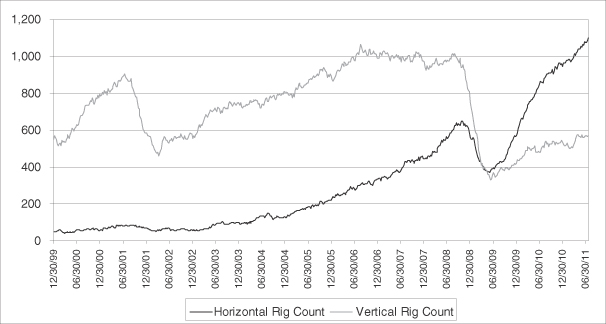

Advances in drilling and completion technologies including horizontal drilling and hydraulic fracturing have made the development of many unconventional resources, such as oil and natural gas shale formations, economically attractive. This has led to a dramatic increase in the development of oil- and natural gas-producing shale formations, or “plays,” in the United States. According to Baker Hughes, the U.S. horizontal rig count has risen from 337 at the beginning of 2007 to 1,136 at September 2, 2011, increasing from 20% to 58% of total rig count. As E&P companies have become more experienced at developing shale plays, the time required to drill wells has decreased, thus increasing the number of wells drilled per year and hence the number of fracturing stages demanded for a given rig count.At the same time, the length of well laterals is increasing, and fracturing stages are being performed at closer intervals. As a result, the number of fracturing stages is growing at a faster rate than the horizontal rig count, leading to a significant increase in the demand for hydraulic fracturing services.

Increased Service Intensity and Activity in More Demanding Shale Reservoirs

Many of the new shales that have been discovered, such as the Haynesville and Eagle Ford Shales, are high-pressure reservoirs that require more durable equipment, a greater amount of horsepower and more technically sophisticated forms of proppant, such as resin-coated sand and ceramic proppants. The additional horizontal drilling activity, coupled with the demanding characteristics of unconventional reservoirs, has put increasing demands on hydraulic fracturing equipment. We focus on the most demanding reservoirs where per stage revenues are higher and where we believe we have a competitive advantage due to the high performance and durability of our equipment.

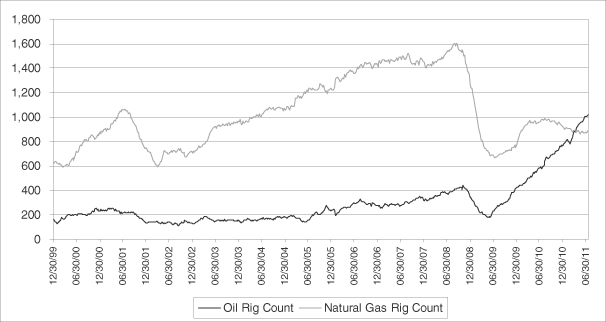

Increased Drilling in Oil- and Liquids-Rich Formations

There is increasing drilling activity in oil- and liquids-rich formations in the United States, such as the Eagle Ford, Bakken, Niobrara and Utica Shales and various plays in Oklahoma, including the Granite Wash formation. Additionally, hydraulic fracturing services are increasingly being deployed in traditionally oil-focused basins like the Permian Basin. Although the E&P industry is cyclical and oil prices have historically been volatile, we believe that many of the oil- and liquids-rich plays are economically attractive at oil prices substantially below the current prevailing oil price. We believe this should provide continued and growing opportunities for our services in the near term.

Tight Supply of Hydraulic Fracturing Fleets, Proppants and Other Products

Due to increased drilling in unconventional formations, hydraulic fracturing fleets, proppants, replacement and repair parts and other products became increasingly scarce since 2010, as demand increased for hydraulic fracturing services. Moreover, individual fracturing stages have become more intensive, requiring more fluids, chemicals and proppant per stage. Based on current market conditions, we expect this trend to continue throughout 2011 and into 2012. We are well positioned to take advantage of the market scarcity due to our vertical integration strategy because we supply our own hydraulic pumps and the majority of our proppant requirements, and we manufacture many of the components of and repair our hydraulic fracturing units in-house.

4

Table of Contents

Index to Financial Statements

Growing International Interest in Hydraulic Fracturing

There is growing international interest in the development of unconventional resources such as oil and natural gas shales. This interest has resulted in a number of recently completed joint ventures between major U.S. and international E&P companies related to shale plays in the United States. We believe that these joint ventures, which generally require the international partner to commit to significant future capital expenditures, will provide additional demand for hydraulic fracturing services in the coming years. Additionally, we believe such joint ventures will continue to stimulate the development of other oil and natural gas shales outside the United States. The technological advances seen in the United States over the last five years can be applied to unconventional basins internationally, allowing foreign countries to reach the level of drilling and fracturing efficiency currently being achieved in the United States. We believe rapid development of cost-effective oil and natural gas reserves has the potential to provide an attractive source of energy for rapidly developing emerging economies.

Competitive Strengths

We believe that we have the following competitive strengths:

Vertically Integrated Business

Our vertical integration provides us with a number of competitive advantages. For example, the amount of time required to fabricate and assemble a hydraulic fracturing unit is significantly reduced as a result of our in-house capabilities. Moreover, once our units are deployed, they are able to continue to operate with minimal delays for our customers, because our ability to quickly provide replacement fluid ends and other consumables reduces our maintenance turnaround time. Similarly, our raw sand and resin-coating operations provide a reliable source of proppant for our operations. Our sand distribution centers and our transportation infrastructure reduce the logistical challenges inherent in our business by allowing us to transport and deliver proppant and equipment quickly to our fracturing jobs on short notice.

Because we produce most of the key equipment and products necessary for our operations, we are able to provide prompt service while controlling costs. We estimate that our manufacturing costs per fracturing unit are approximately 30% less than we would pay to purchase a similar fracturing unit from outside suppliers and that our manufacturing cost per fluid end is approximately 50% less than we would pay to purchase a similar fluid end from outside suppliers. Similarly, we are able to produce proppants such as raw sand and resin-coated sand and to blend chemicals at lower cost than we would typically pay for such products from outside suppliers. As a result, our vertically integrated business improves our margins, reduces our maintenance capital expenditures and improves our equipment utilization. These factors enable us to provide superior service at competitive prices, thereby increasing customer satisfaction, strengthening our existing customer relationships and helping us to expand our customer base.

High-Quality Fleet

We maintain high-quality fleets of hydraulic fracturing units and related equipment. Our 33 fleets have 1,393,500 horsepower in the aggregate, are strategically located throughout our principal markets and have an average age of less than four years. We believe our fleets are among the most reliable and highest performing in the industry with the capability of meeting the most demanding pressure and flow rate requirements in the field. Our equipment’s durability minimizes delays and reduces maintenance costs. Moreover, we maintain our high-quality fleets through our manufacturing and repair facilities and our maintenance and repair personnel who work out of our district offices, which allow us to service, repair and rebuild our equipment quickly and efficiently without incurring excessive costs. These factors increase utilization of our fleets and enhance customer satisfaction because of reduced down time and delays.

5

Table of Contents

Index to Financial Statements

Advanced Equipment and Products

Our engineering team has enabled us to create what we believe to be one of the most technologically advanced and durable fleets of hydraulic pumps in the industry. We believe that, within the industry, we manufacture and deploy one of the most durable fluid ends, which is the part of the high-pressure pump that requires replacement most frequently. We also have chemical blending and research and development facilities where our technical staff designs and improves upon the composition of the chemicals we add to hydraulic fracturing fluids based on specific customer needs and geological factors. For example, we have filed a U.S. patent application for a new additive that uses nano particles to enhance the recovery of hydrocarbons from significantly depleted hydrocarbon formations. In addition, our technical staff has developed innovative techniques for completing and stimulating wells in unconventional formations that have helped establish us as a market leader in our industry.

Highly Active, High-Quality Customer Base

We have long-standing relationships with many of the leading oil and natural gas producers operating in the United States. Our largest customers include Chesapeake, El Paso Corporation, Petrohawk Energy (owned by BHP Billiton Ltd.), Range Resources Corporation and XTO Energy (owned by Exxon Mobil Corporation). Since 2002, we have broadened our customer base as a result of our technical expertise, high-quality hydraulic fracturing fleets and reputation for quality and customer service. We currently have more than 170 customers. Our strong customer relationships provide us with significant revenue visibility in the near to intermediate term and facilitate our ability to opportunistically expand our business to provide services to our customers in multiple areas in which they have operations. In addition, we have dedicated a larger portion of our fleets to some of our largest customers.

Leading Market Share in Key Unconventional Resource Plays

As a result of our focus on superior service and strong customer relationships, we believe we have one of the largest market shares of any hydraulic fracturing company in the Haynesville Shale, the Eagle Ford Shale and the Marcellus Shale, based on number of fleets. In addition to our current leading positions, we have recently begun serving customers in the Bakken Shale and the Granite Wash formation, and we have plans to expand into other prolific unconventional resource plays where significant demand exists for high-quality hydraulic fracturing services. Our leading market positions in the most demanding shale plays create economies of scale that allow us to more efficiently deploy our crews and to increase our productivity, efficiency and performance.

Incentivized Work Force

The managers of our hydraulic fracturing crews are eligible to receive incentive pay per fracturing stage based on customer and senior management satisfaction and subject to satisfying quality and safety standards. In addition, all of our field employees are eligible for incentive pay based on customer and management satisfaction and satisfying safety standards. We believe these incentive programs enable us to achieve higher utilization, attract the most competent work force and motivate our employees to continually maintain quality and safety. The discretionary incentive pay available under these programs has the potential to significantly supplement the earnings of our fleet managers and field employees.

Experienced Management Team

We have an experienced management team that includes Marcus C. Rowland, our chief executive officer, James Coy Randle, Jr., our president and chief operating officer, Charles Veazey, our senior vice president of operations, Robert Pike, our senior vice president of sales, Chris Cummins, our senior vice president

6

Table of Contents

Index to Financial Statements

of proppants, and Brad Holms, our senior vice president—global business development and technology, who collectively have over 190 years of oilfield business experience. The remainder of our management team is comprised of seasoned operating, marketing, financial and administrative executives, many of whom have prior experience at prominent oilfield service companies such as BJ Services Company, Halliburton Corporation and Schlumberger Limited. Our management team’s extensive experience in, and knowledge of, the oilfield services industry strengthens our ability to compete and manage our business through industry cycles.

Strategy

We intend to build upon our competitive strengths to grow our business and increase our revenues and operating income. Our strategy to achieve these goals consists of (1) expanding our geographic footprint in the United States and internationally, (2) increasing our proppant production and distribution and our equipment manufacturing capabilities, (3) continuing to enhance our contract terms, (4) further increasing asset utilization and (5) evaluating opportunities for complementary services.

Expand Geographic Footprint in the United States and Internationally

We will continue to expand our operations to regions containing unconventional formations that are likely to require multi-stage high-pressure hydraulic fracturing efforts. For example, we deployed six fleets with approximately 281,000 aggregate horsepower to serve customers in the Eagle Ford Shale since June 30, 2010. In the first half of 2011, we deployed five new fleets with approximately 177,500 aggregate horsepower to serve customers in the Granite Wash formation and the Bakken Shale.

We are exploring international expansion into areas where the geology is similar to the U.S. unconventional basins in which we currently operate. By applying our technologies to these new areas we believe we can help producers achieve levels of drilling and completion efficiencies comparable to those in the United States in less time than it took in the U.S. market. Based on a report from the Energy Information Administration, international shale gas recoverable reserves are 6.7 times those in the United States. We are actively working to establish relationships with local reserve holders and to provide them stimulation services at the appropriate time in their development plans. We currently believe the most attractive international markets for our services are China, the Middle East and South America.

Increase Proppant Production and Distribution and Equipment Manufacturing Capabilities

We intend to increase our raw sand production capacity by expanding our existing processing plants in Texas and opening an additional sand processing plant in Texas. In addition, we plan to continue to increase our resin-coated sand production capacity over the next few years, and are constructing a new resin-coating plant in Texas that we expect to complete later in 2011. We are enlarging our distribution network to support the expansion of our sand operations. We also intend to increase our hydraulic pump manufacturing capacity and enhance our manufacturing capabilities by expanding our existing plants and adding new plants.

Continue to Enhance Contract Terms

We intend to continue to enhance our contract terms with our customers to increase the predictability of our future revenues, improve our ability to deploy fleets efficiently and enhance our customer relationships. In response to increased demand and tight supply of fracturing fleets in some of our key markets, we have agreed with some of our customers to dedicate one or more of our fleets to their operations at agreed prices. These arrangements typically have 12- to 24-month terms and require customers to pay us an established rate per fracturing stage or a minimum amount per month or quarter. Beginning in late 2010, several of our largest customers entered into such arrangements with us to operate one or more fleets in the Haynesville, Eagle Ford,

7

Table of Contents

Index to Financial Statements

Marcellus and Bakken Shales and the Permian Basin. Revenues generated from these types of arrangements represented 55% of our revenues for the six months ended June 30, 2011. The remainder of our revenues is derived from providing our services on a “call-out” basis for one or a discrete series of hydraulic fracturing jobs.

Further Increase Asset Utilization

We will continue to focus on increasing asset utilization, particularly in the most demanding reservoirs. We are generally compensated based on the number of fracturing stages we complete. Each of our fleets historically completed one fracturing stage per day, but our fleets now typically complete multiple stages per day, usually on the same well. We have the ability to operate our fleets on a 24-hour-per-day, seven-day-per-week basis with two crews rotating to increase asset efficiency. Increases in the number of stages per well allow us to increase revenues for a given crew by reducing travel and mobilization time between jobs. In addition, we seek to increase asset utilization by scheduling fracturing jobs that are geographically close to one another.

Evaluate Opportunities for Complementary Services

We will continue to seek opportunities to further grow our business by adding complementary service offerings. We expect that any new services that we may add will be focused primarily on improving the quality, reliability and deliverability of our existing service offerings.

History and Conversion

We were originally formed as a Texas limited partnership in August 2000 and began providing hydraulic fracturing services to E&P companies in 2002.

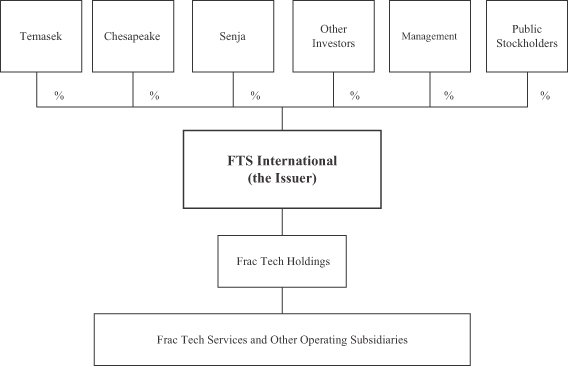

On May 6, 2011, our prior majority owners sold their 74.2% interest in Frac Tech Holdings, LLC to Frac Tech International, LLC, a newly-formed Delaware limited liability company controlled by an investor group comprised of Maju Investments (Mauritius) Pte Ltd, an indirect wholly owned investment holding company of Temasek Holdings (Private) Limited (“Temasek”), Senja Capital Ltd (“Senja”) and other investors. In connection with the transaction, which we refer to as the “Acquisition Transaction,” Chesapeake contributed its 25.8% interest in Frac Tech Holdings, LLC to Frac Tech International, LLC in exchange for cash and limited liability company units representing 30% of Frac Tech International, LLC’s outstanding limited liability company units.

On October 3, 2011, we changed our name from Frac Tech International, LLC to FTS International, LLC.

8

Table of Contents

Index to Financial Statements

The chart below depicts our organizational structure after giving effect to our conversion into a Delaware corporation named FTS International, Inc., which we refer to as our “Conversion,” and our initial public offering. For more information, see “Principal and Selling Stockholders.”

Company Information

Our principal executive offices are located at 777 Main Street, Suite 3000, Fort Worth, Texas 76102, and our telephone number at that address is (817) 862-2000. Our website address ishttp://www.fractech.net. However, information contained on our website is not incorporated by reference into this prospectus, and you should not consider the information contained on our website to be part of this prospectus.

9

Table of Contents

Index to Financial Statements

The Offering

Common stock offered by us | shares |

Common stock offered by selling stockholder | shares |

Common stock outstanding after the offering | shares |

Over-allotment option | We and the selling stockholder have granted the underwriters an option, exercisable for 30 days, to purchase up to an aggregate of additional shares of our common stock to cover over-allotments, if any. |

Use of proceeds | We expect to receive approximately $ million of net proceeds from the sale of the common stock offered by us, based upon the assumed initial public offering price of $ per share (the midpoint of the price range set forth on the cover page of this prospectus), after deducting underwriting discounts and estimated offering expenses. Each $1.00 increase (decrease) in the public offering price would increase (decrease) our net proceeds by approximately $ million. |

| We are required under the terms of our senior secured term loan to use all of the net proceeds we receive from this offering to repay outstanding borrowings under the term loan. As of October 25, 2011, the outstanding principal balance of our senior secured term loan was $1.4 billion. We do not currently anticipate that our net proceeds from this offering will be greater than the outstanding principal balance of our senior secured term loan. See “Use of Proceeds.” |

| We will not receive any of the net proceeds from the sale of the common stock offered by the selling stockholder. |

Dividend policy | After this offering, we do not anticipate paying cash dividends on our common stock in the foreseeable future. See “Dividend Policy.” |

Proposed NYSE symbol | “ ” |

Unless otherwise indicated, all share information contained in this prospectus:

| • | assumes the consummation of our Conversion, as described under “History and Conversion;” |

| • | assumes that the underwriters’ over-allotment option granted by us and the selling stockholder will not be exercised; and |

| • | does not include shares of common stock reserved for issuance under our 2011 Long-Term Incentive Plan to be approved by our board of directors and stockholders immediately prior to the completion of this offering. |

10

Table of Contents

Index to Financial Statements

Risk Factors

An investment in our common stock involves significant risks. Before investing in our common stock, you should carefully consider all the information contained in this prospectus, including the information under the headings “Risk Factors” and “Cautionary Note Regarding Forward-Looking Statements.” Our business, financial condition and results of operations could be materially and adversely affected by many factors, including the following factors and the factors discussed in “Risk Factors” and elsewhere in this prospectus:

| • | the cyclical nature of demand for hydraulic fracturing and other stimulation services; |

| • | volatility in market prices for oil and natural gas and in the level of E&P activity in the United States, and the effect of this volatility on the demand for oilfield services generally; |

| • | changes in legislation and the regulatory environment; |

| • | liabilities and risks, including environmental liabilities and risks, inherent in oil and natural gas operations; |

| • | the loss of any of our key executives; |

| • | continuing or increased competition; |

| • | our inability to fully protect our intellectual property rights; |

| • | delays by our customers or by us in obtaining permits necessary for the conduct of our operations; and |

| • | dependence on a limited number of major customers. |

11

Table of Contents

Index to Financial Statements

Summary Consolidated Financial Information

The following summary consolidated financial information for each of the years in the three-year period ended December 31, 2010 is based on the audited consolidated financial statements of our predecessor included elsewhere in this prospectus. The summary consolidated financial information for the six months ended June 30, 2010 and the partial periods from January 1, 2011 through May 5, 2011 and May 6, 2011 through June 30, 2011 is based on our unaudited consolidated financial statements included elsewhere in this prospectus. The summary consolidated financial information for the year ended December 31, 2007 is based on the audited consolidated financial statements of our predecessor not included in this prospectus. The summary consolidated financial information for the year ended December 31, 2006 is based on the unaudited consolidated financial statements of our predecessor not included in this prospectus. In the opinion of our management, the interim financial information includes all adjustments, consisting only of normal recurring adjustments, necessary for a fair presentation of our financial condition, results of operations and cash flows. The results for interim periods set forth below are not necessarily indicative of the results to be expected for the full year.

We recorded the Acquisition Transaction using the acquisition accounting method, under which the assets acquired and liabilities assumed were recorded at their estimated fair values as of May 6, 2011. The selected financial data below is presented on a “predecessor” basis for periods prior to May 6, 2011 and “successor” basis for periods beginning on or after May 6, 2011 to indicate the application of two bases of accounting and on a combined basis for the six month period ended June 30, 2011. Even though our operations did not change significantly due to the Acquisition Transaction, the expenses related to these changes in our basis of accounting affect certain expenses recognized in the successor period, thereby impacting the comparability of successor period and predecessor period financial information.

The information set forth below should be read together with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the historical consolidated financial statements and related notes thereto included elsewhere in this prospectus.

| Predecessor | Successor | Combined | ||||||||||||||||||||||||||||||||||||

| Year Ended December 31, | Six Months Ended June 30, 2010 | January 1 through May 5, 2011 | May 6 through June 30, 2011 | Six Months Ended June 30, 2011 | ||||||||||||||||||||||||||||||||||

| 2006 | 2007 | 2008 | 2009 | 2010 | ||||||||||||||||||||||||||||||||||

| (Unaudited) | (Unaudited) | (Unaudited) | (Unaudited) | (Unaudited) | ||||||||||||||||||||||||||||||||||

| (In thousands) | ||||||||||||||||||||||||||||||||||||||

Income Statement Information: | ||||||||||||||||||||||||||||||||||||||

Revenues | $ | 214,426 | $ | 362,462 | $ | 573,543 | $ | 389,230 | $ | 1,286,599 | $ | 451,874 | $ | 729,365 | $ | 366,997 | $ | 1,096,362 | ||||||||||||||||||||

Costs of revenues, excluding depreciation, depletion and amortization | 88,246 | 202,620 | 343,301 | 255,977 | 641,783 | 245,482 | 365,480 | 245,763 | 611,243 | |||||||||||||||||||||||||||||

Selling and administrative costs | 20,731 | 35,006 | 81,940 | 68,386 | 136,299 | 49,091 | 88,695 | 30,001 | 118,696 | |||||||||||||||||||||||||||||

Depreciation, depletion and amortization | 15,646 | 38,938 | 69,200 | 91,149 | 117,976 | 52,959 | 52,553 | 49,134 | 101,687 | |||||||||||||||||||||||||||||

Goodwill impairment | — | — | 5,971 | — | — | — | — | — | — | |||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

Income (loss) from operations | 89,803 | 85,898 | 73,131 | (26,282 | ) | 390,541 | 104,342 | 222,637 | 42,099 | �� | 264,736 | |||||||||||||||||||||||||||

Interest expense, net | (4,963 | ) | (13,467 | ) | (29,040 | ) | (15,945 | ) | (19,476 | ) | (11,529 | ) | (13,935 | ) | (22,829 | ) | (36,764 | ) | ||||||||||||||||||||

Other income (expense), excluding interest | 53 | 568 | 1,262 | 2,335 | 865 | (66 | ) | (1,347 | ) | 296 | (1,051 | ) | ||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

Income (loss) before income taxes | 84,893 | 72,999 | 45,353 | (39,892 | ) | 371,930 | 92,747 | 207,355 | 19,566 | 226,921 | ||||||||||||||||||||||||||||

Income taxes(1) | 2,421 | 1,248 | 1,994 | 347 | 3,254 | 1,685 | 2,051 | 730 | 2,781 | |||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

Net income (loss) | $ | 82,472 | $ | 71,751 | $ | 43,359 | $ | (40,239 | ) | $ | 368,676 | $ | 91,062 | $ | 205,304 | $ | 18,836 | $ | 224,140 | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

Other Financial Information: | ||||||||||||||||||||||||||||||||||||||

Adjusted EBITDA(2) (unaudited) | $ | 105,449 | $ | 124,836 | $ | 148,302 | $ | 64,868 | $ | 518,844 | $ | 162,952 | $ | 309,556 | $ | 143,956 | $ | 453,512 | ||||||||||||||||||||

Capital expenditures | $ | 195,727 | $ | 292,469 | $ | 163,040 | $ | 61,777 | $ | 266,050 | $ | 47,689 | $ | 188,880 | $ | 90,236 | $ | 279,116 | ||||||||||||||||||||

12

Table of Contents

Index to Financial Statements

| Predecessor | Successor | Combined | ||||||||||||||||||||||||||||||||||||

| Year Ended December 31, | Six Months Ended June 30, 2010 | January 1 through May 5, 2011 | May 6 through June 30, 2011 | Six Months Ended June 30, 2011 | ||||||||||||||||||||||||||||||||||

| 2006 | 2007 | 2008 | 2009 | 2010 | ||||||||||||||||||||||||||||||||||

| Operating Data—Unaudited: | ||||||||||||||||||||||||||||||||||||||

Number of wells fractured | 398 | 750 | 839 | 675 | 1,374 | 665 | 583 | 278 | 861 | |||||||||||||||||||||||||||||

Total fracturing stages | * | * | * | 4,786 | 9,916 | 4,253 | 5,086 | 2,506 | 7,592 | |||||||||||||||||||||||||||||

Average revenue per stage | * | * | * | $ | 81,327 | $ | 129,750 | $ | 105,155 | $ | 142,951 | $ | 140,754 | $ | 142,226 | |||||||||||||||||||||||

Horsepower (end of period) | 213,750 | 678,250 | 779,500 | 802,000 | 996,250 | 802,000 | 1,194,000 | 1,312,750 | 1,312,750 | |||||||||||||||||||||||||||||

Number of fleets deployed (end of period) | 11 | 16 | 19 | 20 | 23 | 20 | 27 | 31 | 31 | |||||||||||||||||||||||||||||

| * | Unavailable |

| June 30, 2011 | ||||||||

| Actual | As Adjusted(3) | |||||||

| (Unaudited) | ||||||||

| (In thousands) | ||||||||

Balance Sheet Information: | ||||||||

Cash and cash equivalents | $ | 216,979 | $ | |||||

Fixed assets, net | $ | 1,378,227 | $ | |||||

Total assets | $ | 5,869,648 | $ | |||||

Long-term debt (including current portion) | $ | 2,063,106 | $ | |||||

Owners’ equity | $ | 3,573,837 | $ | |||||

| (1) | Consists primarily of State of Texas margin tax treated as income taxes for accounting purposes. Prior to our Conversion, we have been treated as a partnership for federal income tax purposes and therefore have not directly paid federal or state income taxes on our income. |

| (2) | “Adjusted EBITDA” is a non-GAAP financial measure that we define as net income before interest, taxes, depreciation, depletion, amortization, gain or loss on sale of assets, ownership-based compensation and Acquisition Transaction costs, as further adjusted to add back amounts charged to income for goodwill impairment related to the discontinuance of the operations of a subsidiary in fiscal year 2008 and impairment of service equipment in fiscal year 2010. “Adjusted EBITDA,” as used and defined by us, may not be comparable to similarly titled measures employed by other companies and is not a measure of performance calculated in accordance with GAAP. Adjusted EBITDA should not be considered in isolation or as a substitute for operating income, net income or loss, cash flows provided by operating, investing and financing activities, or other income or cash flow statement data prepared in accordance with GAAP. However, our management believes Adjusted EBITDA may be useful to an investor in evaluating our operating performance because this measure: |

| • | is widely used by investors in the oilfield services industry to measure a company’s operating performance without regard to items excluded from the calculation of such measure, which can vary substantially from company to company depending upon accounting methods, book value of assets, capital structure and the method by which assets were acquired, among other factors; |

| • | helps investors to more meaningfully evaluate and compare the results of our operations from period to period by removing the effect of our capital structure and asset base from our operating structure; and |

| • | is used by our management for various purposes, including as a measure of performance of our operating entities, in presentations to our board of directors and as a basis for strategic planning and forecasting. |

There are significant limitations to using Adjusted EBITDA as a measure of performance, including the inability to analyze the effect of certain recurring and non-recurring items that materially affect our net income or loss, and the lack of comparability of results of operations of different companies.

13

Table of Contents

Index to Financial Statements

The following table reconciles our net income, the most directly comparable GAAP financial measure, to Adjusted EBITDA:

| Predecessor | Successor | Combined | ||||||||||||||||||||||||||||||||||||

| Year Ended December 31, | Six Months Ended June 30, 2010 | January 1 through May 5, 2011 | May 6 through June 30, 2011 | Six Months Ended June 30, 2011 | ||||||||||||||||||||||||||||||||||

| 2006 | 2007 | 2008 | 2009 | 2010 | ||||||||||||||||||||||||||||||||||

(In thousands) | ||||||||||||||||||||||||||||||||||||||

Net income (loss) | $ | 82,472 | $ | 71,751 | $ | 43,359 | $ | (40,239 | ) | $ | 368,676 | $ | 91,062 | $ | 205,304 | $ | 18,836 | $ | 224,140 | |||||||||||||||||||

Interest expense, net | 4,963 | 13,467 | 29,040 | 15,945 | 19,476 | 11,529 | 13,935 | 22,829 | 36,764 | |||||||||||||||||||||||||||||

Income taxes | 2,421 | 1,248 | 1,994 | 347 | 3,254 | 1,685 | 2,051 | 730 | 2,781 | |||||||||||||||||||||||||||||

Depreciation, depletion and amortization | 15,646 | 38,938 | 69,200 | 91,149 | 117,976 | 52,959 | 52,553 | 49,134 | 101,687 | |||||||||||||||||||||||||||||

Goodwill impairment | — | — | 5,971 | — | — | — | — | — | — | |||||||||||||||||||||||||||||

Impairment of service equipment(a) | — | — | — | — | 9,352 | 5,651 | — | — | — | |||||||||||||||||||||||||||||

Loss (gain) on sale of assets | (47 | ) | (73 | ) | (442 | ) | (50 | ) | 390 | 338 | 2,244 | (541 | ) | 1,703 | ||||||||||||||||||||||||

Ownership-based compensation | — | — | — | — | 975 | — | 18,165 | — | 18,165 | |||||||||||||||||||||||||||||

Acquisition Transaction costs | — | — | — | — | — | — | 16,201 | 52,723 | 68,924 | |||||||||||||||||||||||||||||

Miscellaneous revenue(b) | (6 | ) | (495 | ) | (820 | ) | (2,284 | ) | (1,255 | ) | (272 | ) | (897 | ) | 245 | (652 | ) | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

Adjusted EBITDA | $ | 105,449 | $ | 124,836 | $ | 148,302 | $ | 64,868 | $ | 518,844 | $ | 162,952 | $ | 309,556 | $ | 143,956 | $ | 453,512 | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

| (a) | The amount shown in the table above for impairment of service equipment relates to a charge taken during fiscal year 2010 resulting from increased use of our equipment in demanding shale reservoirs, which required us to replace the equipment earlier than its originally estimated useful life. |

| (b) | Miscellaneous revenue consisted principally of the following: rebates and commissions, for fiscal years 2006 and 2007; settlement of discounts and warranty claims, for fiscal year 2008; amortization of deferred gain, for fiscal year 2009; and rental income and amortization of deferred gain, for fiscal year 2010. |

| (3) | As adjusted to give effect to the closing of this offering and application of the estimated net proceeds of this offering to repay borrowings under our senior secured term loan as described in “Use of Proceeds.” |

14

Table of Contents

Index to Financial Statements

Summary Unaudited Pro Forma Financial Information

The following tables present our unaudited pro forma condensed consolidated statements of operations for the year ended December 31, 2010 and for the six months ended June 30, 2011, and our unaudited pro forma condensed consolidated balance sheet as of June 30, 2011.

Our unaudited pro forma condensed consolidated financial statements have been developed by applying pro forma adjustments to our historical consolidated financial statements appearing elsewhere in this prospectus. The unaudited pro forma condensed consolidated statements of operations data for the periods presented give effect to our Conversion from a limited liability company to a corporation and the Acquisition Transaction as if they had been completed on January 1, 2010. The unaudited pro forma condensed consolidated balance sheet data gives effect to the Conversion as if it had occurred on June 30, 2011. The Acquisition Transaction occurred on May 6, 2011 and is reflected in our historical consolidated balance sheet as of June 30, 2011 included elsewhere in this prospectus. As a result, no pro forma adjustments to the June 30, 2011 balance sheet were necessary to reflect the Acquisition Transaction. We describe the assumptions underlying the pro forma adjustments in the accompanying notes and the notes to the unaudited pro forma condensed consolidated financial statements included elsewhere in this prospectus, which should be read in conjunction with this summary pro forma condensed consolidated financial information.

The pro forma adjustments related to the purchase price allocation of the Acquisition Transaction are preliminary and are subject to revision as additional information becomes available. Revisions to the preliminary purchase price allocation may have a significant impact on the pro forma amounts of total assets, total liabilities and owners’ equity and on depreciation, depletion and amortization expense. The pro forma adjustments related to the Acquisition Transaction reflect the fair values allocated to our assets as of May 6, 2011 and do not necessarily reflect the fair values that would have been recorded if the Acquisition Transaction had occurred on January 1, 2010.

The unaudited pro forma condensed consolidated financial statements should be read in conjunction with the information contained in “Selected Consolidated Financial Data,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and related notes thereto, included elsewhere in this prospectus.

The unaudited pro forma condensed consolidated financial statements are included for informational purposes only and do not purport to reflect our results of operations or financial position that would have occurred had the Acquisition Transaction and Conversion occurred on the dates assumed, and they therefore should not be relied upon as being indicative of our results of operations or financial position had the Conversion or the Acquisition Transaction occurred on the dates assumed. The unaudited condensed consolidated pro forma financial statements are also not a projection of our results of operations or financial position for any future period or date.

15

Table of Contents

Index to Financial Statements

Unaudited Pro Forma Condensed Consolidated Statements of Operations

| Year Ended December 31, 2010 | ||||||||||||||||

| Predecessor | Conversion Adjustments | Acquisition Transaction Adjustments(a) | Pro Forma | |||||||||||||

| (In thousands, except per share information) | ||||||||||||||||

Revenues | $1,286,599 | $— | $— | $1,286,599 | ||||||||||||

Costs of revenues, excluding depreciation, depletion and amortization | 641,783 | — | — | 641,783 | ||||||||||||

Selling and administrative costs | 136,299 | — | — | 136,299 | ||||||||||||

Depreciation, depletion and amortization | 117,976 | — | 161,765(b) | 279,741 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Income from operations | 390,541 | — | (161,765) | 228,776 | ||||||||||||

Interest expense, net, and other income (expense) | (18,611) | — | (97,585)(c) | (116,196) | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Income before income taxes | 371,930 | — | (259,350) | 112,580 | ||||||||||||

Income taxes | 3,254 | 137,550(d) | (98,136)(d) | 42,668 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Net income | $368,676 | $(137,550) | $(161,214) | $69,912 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Basic and diluted net income per share | ||||||||||||||||

Weighted average number of shares outstanding: | ||||||||||||||||

Basic | ||||||||||||||||

Diluted | ||||||||||||||||

See footnotes below | ||||||||||||||||

| Six Months Ended June 30, 2011 | ||||||||||||||||||||||

| Historical | ||||||||||||||||||||||

| Predecessor (January 1 through May 5, 2011) | Successor (May 6 through June 30, 2011) | Conversion Adjustments | Acquisition Transaction Adjustments(a) | Pro Forma | ||||||||||||||||||

| (In thousands, except per share information) | ||||||||||||||||||||||

Revenues | $ | 729,365 | $ | 366,997 | $ | — | $ | — | $ | 1,096,362 | ||||||||||||

Costs of revenues, excluding depreciation, depletion and amortization | 365,480 | 245,763 | — | (52,723 | )(e) | 558,520 | ||||||||||||||||

Selling and administrative costs | 88,695 | 30,001 | — | (34,366 | )(f) | 84,330 | ||||||||||||||||

Depreciation, depletion and amortization | 52,553 | 49,134 | — | 46,294 | (b) | 147,981 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||

Income from operations | 222,637 | 42,099 | — | 40,795 | 305,531 | |||||||||||||||||

Interest expense, net, and other income (expense) | (15,282 | ) | (22,533 | ) | — | (33,339 | )(c) | (71,154 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||

Income before income taxes | 207,355 | 19,566 | — | 7,456 | 234,377 | |||||||||||||||||

Income taxes | 2,051 | 730 | 83,354 | (d) | 2,928 | (d) | 89,063 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||

Net income | $ | 205,304 | $ | 18,836 | $ | (83,354 | ) | $ | 4,528 | $ | 145,314 | |||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||||

| Basic and diluted net income per share | ||||||||||||||||||||||

Weighted average number of shares outstanding: | ||||||||||||||||||||||

Basic | ||||||||||||||||||||||

Diluted | ||||||||||||||||||||||

See footnotes below | ||||||||||||||||||||||

16

Table of Contents

Index to Financial Statements

Unaudited Pro Forma Condensed Consolidated Balance Sheet

| June 30, 2011 | ||||||||||||

| Historical Successor | Conversion Adjustments | Pro Forma | ||||||||||

| (In thousands) | ||||||||||||

Total current assets | $ | 719,291 | $ | 6,463 | (d) | $ | 725,754 | |||||

Total non-current assets | 5,150,357 | — | 5,150,357 | |||||||||

|

|

|

|

|

| |||||||

Total assets | $ | 5,869,648 | $ | 6,463 | $ | 5,876,111 | ||||||

|

|

|

|

|

| |||||||

Total current liabilities | $ | 257,570 | $ | 10,471 | (d) | $ | 268,041 | |||||

Deferred tax liabilities, net | — | 226,059 | (d) | 226,059 | ||||||||

Long-term notes, net of current portion | 2,038,241 | — | 2,038,241 | |||||||||

|

|

|

|

|

| |||||||

Total liabilities | 2,295,811 | 236,530 | 2,532,341 | |||||||||

Owners’ equity | 3,573,837 | (230,067 | ) | 3,343,770 | ||||||||

|

|

|

|

|

| |||||||

Total liabilities and owners’ equity | $ | 5,869,648 | $ | 6,463 | $ | 5,876,111 | ||||||

|

|

|

|

|

| |||||||

| (a) | Reflects the Acquisition Transaction which was accounted for as a business combination and is reflected in the pro forma financial statements as if the Acquisition Transaction had occurred on January 1, 2010. These pro forma adjustments reflect the estimated allocation of the purchase price to the pro rata fair value of tangible and intangible assets and liabilities as of the acquisition date. In calculating these pro forma adjustments, the purchase consideration has been allocated on a preliminary basis and therefore, may be subject to adjustment. We will finalize the amounts recognized as information necessary to complete the analysis is obtained. See Note 3 to our unaudited interim consolidated financial statements included elsewhere in this prospectus. |

| (b) | Reflects the increased depreciation, depletion and amortization expense as if we had recorded the acquisition date fair values of our fixed assets and intangible assets as of January 1, 2010. |

| (c) | Reflects the increased interest expense as a result of (i) the entry into our $1.5 billion senior secured term loan to finance a portion of the purchase price in the Acquisition Transaction and (ii) amortization of a $39.2 million premium recorded in accordance with acquisition accounting requirements associated with a fair market value adjustment on our senior notes which yielded above market interest rates at the closing of the Acquisition Transaction. The senior secured term loan bears interest at a rate per annum equal to LIBOR, plus an applicable margin based on our leverage, for which the effective interest rate used in calculating pro forma interest expense was 6.9%. |

| (d) | Reflects adjustments to give effect to the Conversion for the periods presented. Prior to the Conversion, we have been treated as a partnership for federal income tax purposes and therefore have not directly paid income taxes on our income nor have we benefitted from losses. Instead, our income and other tax attributes have been passed through to our owners for federal and, where applicable, state income tax purposes. Following the Conversion, we will be treated as a corporation for tax purposes and will be required to pay federal and state income taxes. The unaudited pro forma condensed consolidated statements of operations reflect: (1) the tax expense we would have incurred had we been subject to tax as a corporation in the historical periods presented (those pro forma adjustments being presented in the Conversion column), and (2) the tax effect of the acquisition accounting adjustments (those pro forma adjustments being presented in the Acquisition Transaction column). The pro forma balance sheet reflects deferred taxes related to the differences in the book and tax carrying values of our assets and liabilities as of June 30, 2011. As required under GAAP, upon completion of our Conversion, the impact of recognizing deferred tax assets and liabilities will be recorded as a charge to income in the fiscal quarter in which the Conversion occurs. As of June 30, 2011, the amount of the charge would have been $230 million. The impact of recognizing deferred tax assets and liabilities has been excluded from our unaudited pro forma condensed consolidated statements of operations because it is not expected to have a continuing impact. |

| (e) | Reflects the removal of non-recurring additional costs of revenues that we recorded in May and June 2011 resulting from the allocation of fair value to our inventories as of the date of the Acquisition Transaction. |

| (f) | Reflects the removal of transaction costs (such as legal and other professional fees) and employee benefit costs directly related to the Acquisition Transaction that were incurred by our predecessor. These employee benefit costs were the result of accelerated vesting of employee ownership-based compensation and bonus awards due to pre-existing change of control provisions triggered by the Acquisition Transaction. |

17

Table of Contents

Index to Financial Statements

An investment in our common stock involves risks. You should carefully consider the risks described below before making an investment decision. Our business, financial condition or results of operations could be materially adversely affected by any of these risks. The trading price of our common stock could decline due to any of these risks, and you may lose all or part of your investment.

Risks Relating to Our Business

Our business is cyclical and depends on spending and drilling activity by the onshore oil and natural gas industry in the United States, and the level of such activity is volatile. Our business has been, and may continue to be, adversely affected by industry conditions that are beyond our control.

Our business is cyclical, and we depend on our customers’ willingness to make expenditures to explore for, develop and produce oil and natural gas in the United States. Our customers’ willingness to undertake these activities depends largely upon prevailing industry conditions that are influenced by numerous factors over which we have no control, including:

| • | prices, and expectations about future prices, of oil and natural gas; |

| • | domestic and foreign supply of and demand for oil and natural gas; |

| • | the cost of exploring for, developing, producing and delivering oil and natural gas; |

| • | available pipeline, storage and other transportation capacity; |

| • | lead times associated with acquiring equipment and products and availability of qualified personnel; |

| • | the expected rates of decline in production from existing and prospective wells; |

| • | the discovery rates of new oil and natural gas reserves; |

| • | federal, state and local regulation of hydraulic fracturing and other oilfield service activities, E&P activities and mining activities, including public pressure on governmental bodies and regulatory agencies to regulate our industry; |

| • | the availability, capacity and cost of disposal and recycling services for used hydraulic fracturing fluids; |

| • | the availability of water resources and suitable proppants in sufficient quantities for use in hydraulic fracturing operations; |

| • | political instability in oil and natural gas producing countries; |

| • | advances in exploration, development and production technologies or in technologies affecting energy consumption; |

| • | the price and availability of alternative fuels and energy sources; and |

| • | uncertainty in capital and commodities markets and the ability of oil and natural gas producers to raise equity capital and debt financing. |

18

Table of Contents

Index to Financial Statements

The level of E&P activity in the United States is volatile. Changes in current or anticipated future prices for crude oil and natural gas are a primary factor affecting capital spending and drilling activity by E&P companies, and decreases in capital spending and drilling activity can cause rapid and material declines in demand for fracturing services. A reduction in the activity levels of our customers would cause a decline in the demand for our services and could adversely affect the prices that we can charge or collect for our services. In addition, any prolonged substantial reduction in oil and natural gas prices would likely affect oil and natural gas production levels and, therefore, would affect demand for the services we provide. A material decline in oil and natural gas prices or drilling activity levels or sustained lower prices or activity levels could have a material adverse effect on our business, financial condition, results of operations and cash flow.

A substantial portion of our revenues in 2010 and the first six months of 2011 was derived from our activities in the Haynesville Shale. Drilling activity in the Haynesville Shale has been, and may be further, reduced due to lower natural gas prices. If natural gas prices remain low and drilling activity in the Haynesville Shale continues to decline, our revenues could be adversely affected if we are unable to redeploy our equipment to other regions where drilling activity levels are higher. While drilling activity in liquids-rich plays is currently strong, a decrease in oil and natural gas liquids prices could cause drilling activity in those plays to decrease causing us to be unable to redeploy our equipment.

In 2009, declines in prices for oil and natural gas, together with adverse changes in the capital and credit markets, caused many E&P companies to sharply reduce capital expenditure budgets and drilling activity. This trend resulted in a significant decline in demand for our services, had a material negative impact on the prices we were able to charge our customers and adversely affected our equipment utilization and results of operations. We were in default with respect to certain covenants under our prior revolving credit facility as of December 31, 2009, which we resolved by entering into an amendment and forbearance agreement in January 2010 and an amended and restated facility in May 2010. This facility was terminated in November 2010. Future cuts in spending levels or drilling activity could have similar adverse effects on our results of operations and financial condition, and such effects could be material.

Any future decreases in the rate at which oil or natural gas reserves are discovered or developed, or any increase in in-house fracturing capabilities by E&P companies, could decrease the demand for our services.

Reduced discovery rates of new oil and natural gas reserves, or a decrease in the development rate of reserves, in our market areas, whether due to increased governmental regulation, limitations on exploration and drilling activity or other factors, could have a material adverse impact on our business even in a stronger oil and natural gas price environment. In addition, some E&P companies have begun performing hydraulic fracturing on their wells using their own equipment and personnel. Any increase in the development and utilization of in-house fracturing capabilities by E&P companies could decrease the demand for our services and have a material adverse impact on our business.

We are subject to federal, state and local laws and regulations regarding issues of health, safety and protection of the environment. Under these laws and regulations, we may become liable for penalties, damages or costs of remediation or other corrective measures. Any changes in laws or government regulations could increase our costs of doing business.

Our operations are subject to stringent federal, state and local laws and regulations relating to, among other things, protection of natural resources, wetlands, endangered species, the environment, health and safety, waste management, waste disposal and transportation of waste and other materials. Our operations pose risks of environmental liability, including leakage from our operations to surface or subsurface soils, surface water or groundwater. Some environmental laws and regulations may impose strict liability, joint and several liability, or both. Therefore, in some situations, we could be exposed to liability as a result of our conduct that was lawful at the time it occurred or the conduct of, or conditions caused by, third parties without regard to whether we caused or contributed to the conditions. Actions arising under these laws and regulations could result in the shutdown of

19

Table of Contents

Index to Financial Statements

our operations, fines and penalties, expenditures for remediation or other corrective measures, and claims for liability for property damage, exposure to hazardous materials, exposure to hazardous waste or personal injuries. Sanctions for noncompliance with applicable environmental laws and regulations also may include the assessment of administrative, civil or criminal penalties, revocation of permits, temporary or permanent cessation of operations in a particular location and issuance of corrective action orders. Such claims or sanctions and related costs could cause us to incur substantial costs or losses and could have a material adverse effect on our business, financial condition and results of operations. Additionally, an increase in regulatory requirements on oil and gas exploration and completion activities could significantly delay or interrupt our operations.

If we do not perform in accordance with government, industry or our own safety standards, we could lose business from our customers, many of whom have an increased focus on safety issues as a result of recent incidents, such as the Macondo Well event in the Gulf of Mexico, and governmental initiatives on safety and environmental issues related to E&P activities. The EPA has announced that the energy extraction sector is one of the sectors designated for increased enforcement over the next three to five years.

Additionally, the EPA regulates air emissions from certain off-road diesel engines that are used by us to power equipment in the field. Under these Tier IV regulations, we are required to retrofit or retire certain engines, and we are limited in the number of non-compliant off-road diesel engines we can purchase. Tier IV engines are costlier and are not yet widely available. Until Tier IV-compliant engines that meet our needs are available, these regulations could limit our ability to acquire a sufficient number of diesel engines to expand our fleet and to replace existing engines as they are taken out of service. Further, the Tier IV regulations may result in increased costs as we continue to grow.