May 26, 2023

William Schroder

Michael Volley

U.S. Securities and Exchange Commission

Division of Corporation Finance

Office of Finance

100 F Street, N.E.

Washington, D.C. 20549

Re: | Enova International, Inc. |

| Form 10-K for Fiscal Year Ended December 31, 2022 |

| Filed February 24, 2023 |

| File No. 001-35503 |

Dear Mr. Schroder and Mr. Volley:

This correspondence is being furnished by Enova International, Inc. (“Enova” or the “Company”) in response to comments contained in the letter dated April 28, 2023 (the “Letter”) from the Staff (the “Staff”) of the Securities and Exchange Commission (the “Commission”) with respect to the Company’s Form 10-K for the fiscal year ended December 31, 2022 (the “2022 Form 10-K”).

The responses set forth below have been organized in the same manner in which the Commission’s comments were organized and all page references in the Company’s response are to those referenced in any headings or Staff comments. Set forth in italicized print below are the Staff’s comments followed by the Company’s responses.

Form 10-K filed February 24, 2023

Bank Programs, page 2

1. Please tell us and revise future filings, here or in MD&A, to discuss the number of and any significant reliance on a particular bank partner and quantify the amount of revenue earned and loans purchased through your bank partner program for each period presented and discuss any trends. Please refer to Item 303(a) of Regulation S-K and SEC Release No. 33-8350 for guidance.

Enova response: We currently have programs with three separate banks in the United States. In aggregate, purchases under these programs represented 22% of our consolidated originations and purchases for the year ended December 31, 2022, with no individual partner representing more than 12%. In aggregate, revenue earned on loans under these programs represented 23% of our consolidated revenue for the year ended December 31, 2022, with no individual partner representing more than 17%. We do not believe that we have significant reliance on any of our bank partners. Additionally, if there were to be an issue with any one of our current banking partners that disrupted purchases, there would be multiple alternatives to replace any potential reduction in purchases, such as seeking a different banking partner, as there are numerous other banks that have similar relationships with other non-bank lenders. In addition, each of the written agreements with our existing partners requires, in most cases outside of

United States Securities and Exchange Commission

Division of Corporation Finance

May 26, 2023

Page 2

bankruptcy or regulatory demand, significant advance notice of intention to terminate and wind down the respective program, which would allow ample time for us to identify and secure alternatives. Another option would be to refocus our capital and marketing efforts on other products and services that do not involve the banking partner. We believe our existing loan portfolio represents less than 1% of what we have identified as the total addressable market in the U.S., and so the bank partnerships are only one way that we can offer diversified products.

In response to the Staff’s comment, we will supplement our disclosures in our future 10-K filings to disclose the percentage of purchases from our bank partner programs and will note any material known trends to the extent relevant. For example, the following indented section represents the original text included in Part I, Item 1. Business, Overview, Bank Programs in our 2022 Form 10-K with marked changes (underlines) to address the Staff’s comment.

Bank programs. Certain subsidiaries operate programs with certain banks to provide marketing services and loan servicing for near-prime unsecured consumer installment loans and, beginning in January 2021, line of credit accounts. Under the programs, those subsidiaries receive marketing and servicing fees. The bank has the ability to sell, and the participating subsidiaries have the option, but not the requirement, to purchase the loans or a participating interest in receivables the bank originates. We do not guarantee the performance of the loans and line of credit accounts originated by the bank. As part of the OnDeck business both prior and subsequent to Enova’s acquisition, OnDeck operates a program with a separate bank to provide marketing services and loan servicing for small business installment loans and line of credit accounts. Under the OnDeck program, we receive marketing fees while the bank receives origination fees and certain program fees. The bank has the ability to sell and we have the option, but not the requirement, to purchase the installment loans the bank originates and, in the case of line of credit accounts, extensions under those line of credit accounts. We do not guarantee the performance of the loans or line of credit accounts originated by the bank.

As of December 31, 2022, we operate programs with three separate bank partners. Purchases under these programs represented 22% of our consolidated originations and purchases for the year ended December 31, 2022. Management does not deem there to be significant reliance on any of our banking partners.

The Company respectfully advises the Staff that it will revise its disclosures to include the above information in future 10-K filings.

Our Markets, page 2

2. Please tell us and revise future filings, here or in MD&A, to disclose any concentration of originations by state.

Enova response: We have reviewed the Staff’s disclosure guidance as well as relevant accounting guidance, which includes, but is not limited to, ASC 275-10-50-16, the Financial Reporting Manual of the Division of Corporation Finance, and 825-10-50-22. We do not deem state concentration risk or

United States Securities and Exchange Commission

Division of Corporation Finance

May 26, 2023

Page 3

disclosure of originations by state to be material to an understanding of our business or financial results. From a credit perspective, the borrower’s state is not a substantial variable in the underwriting process. From a regulatory perspective, as we note in Item 1A, Risk Factors, in our 2022 Form 10-K, state governments may seek to impose new laws, regulatory restrictions or licensing requirements that affect the products or services we offer. We are a diversified company with multiple products and jurisdictions in which we operate. As we have demonstrated in the past, if a particular state in which we currently provide products and services were to impose new laws, regulatory restrictions or licensing requirements that would have an adverse impact on the products or services that we offer in that state, we would shift our efforts, resources, and marketing spend to other jurisdictions to serve our customers, which based on our historical experience would ultimately be expected to have an immaterial net impact to our financial results. For the year ended December 31, 2022, the largest concentration of originations of a product in a single state was 7%. As we do not deem state origination concentration or state concentration risk to be material to the users of our financial statements, we believe omission of state origination disclosure to be consistent with U.S. GAAP as well as the Commission’s principles-based disclosure approach.

Products and Services, page 2

3. Please tell us and revise future filings to provide additional information for each significant loan product to allow an investor to understand the nature of your loan products. At a minimum, discuss the estimated average contractual term, the typical payment structure (e.g. - regular payments that amortize the loan to zero at maturity, interest-only payments, a single payment at maturity, etc.), the typical of fees or interest charged (e.g. – fixed interest rates, variable interest rates, one-time fee based on the principal amount, etc.), and the estimated annual percentage rate, average yield earned or average interest rate charged per loan. Please clarify if any significant loan product includes a single-pay structure and provide the key terms of this loan product. Please refer to Item 303(a) of Regulation S-K and SEC Release No. 33-8350 for guidance.

Enova response: In response to the Staff’s comment, the Company will include additional information for each significant loan product to allow investors to better understand the nature of such loan products. For example, the following represents the original text included in Part I, Item 1. Business, Overview, Products and Services in our 2022 Form 10-K with marked changes (strikethroughs and underlines) to address the Staff’s comment. Note that the description of receivables purchase agreements (“RPA”) section will be removed as we have redirected applicants to our other small business offerings and ceased originations of RPAs.

Installment loans. Certain subsidiaries (i) directly offer installment loans, (ii) as part of our Bank Programs, purchase or purchase a participating interest in, installment loans or (iii) as part of our CSO program, arrange and guarantee installment loans, as discussed below. Certain subsidiaries offer, or arrange through our Bank Programs and CSO program, unsecured consumer installment loan products in 37 states in the United States and small business installment loans in 47 states and in Washington D.C. Internationally, we also offer or arrange unsecured consumer installment loan products in Brazil. Effective in the third quarter of 2022, Enova no longer offers any single-pay products. Terms for our consumer installment loan products range between threetwo and 60 months with regular payments that amortize principal. Loan sizes for these products range

United States Securities and Exchange Commission

Division of Corporation Finance

May 26, 2023

Page 4

between $300 and $10,500. The majority of these loans accrue interest daily at a fixed rate for the life of the loan and have no fees. The average annualized yield for these loans was 72% for the year ended December 31, 2022. Loans may be repaid early at any time with no additional prepayment charges.

Certain subsidiaries offer, or arrange through our Bank Programs, small business installment loans in 47 states and in Washington D.C. Terms for these products range between three and 24 months with regular payments that amortize principal. Loan sizes for these products range between $5,000 and $250,000. There is generally a fee paid upon origination, and total interest is typically calculated at a fixed rate for the life of the loan. A portion of the interest is forgivable if prepaid early, although we also offer a full prepayment forgiveness option at a higher interest rate. The average annualized yield for these products was 46% for the year ended December 31, 2022.

Line of credit accounts. Certain subsidiaries directly offer, or purchase a participation interest in receivables through our Bank Programs, new consumer line of credit accounts in 31 states (and continue to service existing line of credit accounts in two additional states) in the United States. and business line of credit accounts in 47 states and in Washington D.C. in the United States, which Line of credit accounts allow customers to draw on their unsecured line of credit in increments of their choosing up to their credit limit, which ranges between $100 and $7,000. Customers may pay off their account balance in full at any time or make required minimum payments in accordance with the terms of the line of credit account. The repayment period varies depending upon certain factors, which may include outstanding principal and differences in minimum payment calculations by product. As long as the customer’s account is in good standing and has credit available, customers may continue to borrow on their line of credit. Customers are charged a fee when funds are drawn and subsequently incur fee- or interest-based charges at a fixed rate, depending upon the product and the state in which the customer resides. The average annualized yield for these products was 212% for the year ended December 31, 2022.

Certain subsidiaries offer, or arrange through our Bank Programs, new small business line of credit accounts in 47 states and in Washington D.C. in the United States. Terms for these products range between 12 and 24 months with regular payments that amortize principal. Loan sizes for these products range between $5,000 and $100,000. Interest is calculated at a fixed rate based on the outstanding balance. There is generally no fee paid upon origination with the exception of one of our small business line of credit products, which has an origination fee when allowed by state law. Certain small business line of credit accounts also charge a monthly maintenance fee. The average annualized yield for these products was 48% for the year ended December 31, 2022.

The Company respectfully advises the Staff that it will enhance its disclosures along the lines of the above in future 10-K and 10-Q filings.

Marketing, page 8

United States Securities and Exchange Commission

Division of Corporation Finance

May 26, 2023

Page 5

4. We note your disclosure that you have increased the percentage of loans sourced through direct marketing to 41% in 2022 and your disclosure on page 22 that the success of your business depends substantially on the willingness and ability of lead providers or marketing affiliates to provide you with customer leads at acceptable prices. Please tell us and revise future filings, here or in MD&A, to:

• disclose the percentage of loans sourced through each of your marketing channels for each period presented and discuss any trends, and

• discuss the number of and any significant reliance on a particular marketing partner. Please refer to Item 303(a) of Regulation S-K and SEC Release No. 33-8350 for guidance.

Enova response: Enova views its utilization of various marketing channels as a competitive advantage in a highly competitive environment. We believe that more granular disclosure on the channels we are using, specifically the percentage of loans sourced through each channel for each fiscal period, could be analyzed and used by our competitors to influence the manner in which they market. This could cause competitive harm to us, which would likely have a negative impact on our financial results. Further, we have reviewed the financial fillings of our competitors, noting that most do not disclose this level of detail. Moreover, we do not believe that disclosure of the percentage of loans sourced through each of our marketing channels would be material information for investors or measurably enhance an understanding of our business and financial results.

In regards to the second bullet in the Staff’s comment, we interact with hundreds of different vendors as it relates to our marketing spend. For the year ended December 31, 2022, we made payments to over 600 vendors. Due to the large number of vendors (and other potential vendors that we do not currently partner with, but could do so in the future) as well as the versatility of our marketing approach and various channels we can use, we do not have a significant reliance on any particular marketing partner and do not believe discussion of the number of and other information about specific marketing vendors would be material information for investors or measurably enhance an understanding of our business and financial results.

CFPB, page 13

5. We note your disclosure that you remain subject to restrictions and obligations, including a prohibition from engaging in certain conduct, related to a January 25, 2019 Consent Order with the CFPB. Please tell us and revise future filings to disclose each significant provision under the terms of the Consent Order, the actions you have taken or you plan to take to comply with each provision and the current status of your compliance. Additionally, please discuss how your actions will impact future financial results and

trends including credit quality trends and discuss what the steps needed for the CFPB to terminate the Consent Order.

Enova response: The Company respectfully advises the Staff that it will augment its disclosures related to the CFPB Consent Order in future filings, for so long as it remains in effect. For example, the following represents the original text included in Part I, Item 1. Business, Regulation, CFPB, in our 2022 Form 10-K with marked changes (strikethroughs and underlines) to address the Staff’s comment.

United States Securities and Exchange Commission

Division of Corporation Finance

May 26, 2023

Page 6

On January 25, 2019, we consented to the issuance of a Consent Order by the CFPB pursuant to which we agreed, without admitting or denying any of the facts or conclusions, to pay a civil money penalty of $3.2 million. The Consent Order relates to issues self-disclosed to the CFPB in 2014, including failure to provide loan extensions to 308 consumers and debiting approximately 5,500 consumers from the wrong bank account. We remain subject to the restrictions and obligations of the Consent Order, including a prohibition from engaging in certain conduct.

The Consent Order requires Enova to honor loan extensions granted to consumers and not debit the full payment instead of a loan extension fee to consumers granted a loan extension.

In addition, the Consent Order requires that Enova not: 1) debit or attempt to debit any consumer’s bank account without having obtained the consumer’s express informed consent; or 2) make or initiate electronic fund transfers from a consumer’s bank account on a recurring basis without obtaining a valid authorization signed or similarly authenticated from the consumer for preauthorized electronic fund transfers from that particular bank account.

As a result of the issues that we self-identified, Enova implemented enhanced policies and procedures designed to prevent the prohibited actions. Additionally, Enova continues to enhance its compliance management system and internal controls, as well as its technology platform to address these issues noted above.

Enova continues to monitor and optimize its compliance programs with respect to the Consent Order requirements, leveraging monitoring, testing and audit of its compliance program and payment processes. The Consent Order will terminate five years from January 25, 2019. The aforementioned changes have not had a material impact on our financial results, nor do we expect them to have a material impact on future financial results.

Results of Operations, page 43

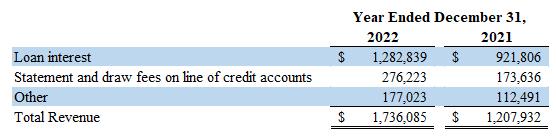

6. We note your disclosure on page 73 that revenue includes: interest income, finance charges, fees for services provided through the Company’s CSO programs, revenue on RPAs, service charges, draw fees, minimum billing fees, purchase fees, origination fees, late fees and non-sufficient funds fees. Noting the different nature the sources of revenue, please tell us and revise future filings to separately disclose each significant revenue amount for each period presented and discuss any trends. Please refer to Item 303(a) of Regulation S-K and SEC Release No. 33-8350 for guidance.

Enova response: In response to the Staff’s comment, the Company will include an additional table with all material revenue categories in our MD&A substantially in the form below, which is subject to change based on the materiality of individual components, and will note any material known trends to the extent relevant. There are no subcategories included in “Other” that exceed 5% of total revenue. Amounts have been included for the year ended December 31, 2022 and 2021 to give the Staff a sense of materiality for the categories presented.

Revenue generated from the Company’s loans and finance receivables for the years ended December 31, 2022 and 2021 was as follows (in thousands):

United States Securities and Exchange Commission

Division of Corporation Finance

May 26, 2023

Page 7

Furthermore, in response to the Staff’s comment, the Company expects to clarify the wording in the “Revenue Recognition” section of Note 1 to the financial statements to better align with the new table and would address, at a minimum, all revenue streams that are material to the financial statements. The following represents the original text included in the first paragraph of the “Revenue Recognition” section in Note 1 in our 2022 Form 10-K filing with marked changes (strikethroughs and underlines) to address the Staff’s comment.

The Company recognizes revenue based on the financing products and services it offers and on loans it acquires. “Revenue” in the consolidated statements of income primarily includes interest income, statement and draw fees on line of credit accounts finance charges, fees for services provided through the Company’s CSO programs (“CSO fees”), revenue on RPAs, service charges, draw fees, minimum billing fees, purchase fees, origination fees, and other late fees and non-sufficient funds fees as permitted by applicable laws and pursuant to the agreement with the customer. Interest is generally recognized on an effective yield basis over the contractual term of the loan on installment loans, the estimated outstanding period of the draw on line of credit accounts, or the projected delivery term on RPAs. CSO fees are recognized over the term of the loan. Late and nonsufficient funds fees are recognized when assessed to the customer. Interest income is generally recognized on an effective yield basis over the contractual term of the loan on installment loans or the estimated outstanding period of the draw on line of credit accounts. Statement fees on line of credit accounts are similar to interest charges and are generally recognized similarly to interest income. Draw fees on line of credit accounts are generally recognized at the time of draw. Revenue on RPAs is recognized over the projected delivery term of the agreement. CSO fees are recognized over the term of the loan. Origination fees are charged to customers on certain installment loan products and are recognized upon origination.

Loan and Finance Receivable Balances, page 48

7. Please tell us and revise future filings to explain the relationship between the average loan and finance receivable origination amount in the table at the bottom of page 49 and the average amount outstanding per loan and finance receivable amount in the table at the top of page 49. Specifically describe why the origination amount is significantly smaller than the amount outstanding.

Enova response: The average loan origination amount is smaller than the average amount outstanding per loan and finance receivable as the former measure includes incremental draws on our line of credit accounts whereas the latter measure includes the entire outstanding receivable on our line of credit

United States Securities and Exchange Commission

Division of Corporation Finance

May 26, 2023

Page 8

accounts. We will include this clarification in future filings, likely in the “Average Loan and Finance Receivable Origination” section of the MD&A.

Consumer Loans and Finance Receivables, page 51

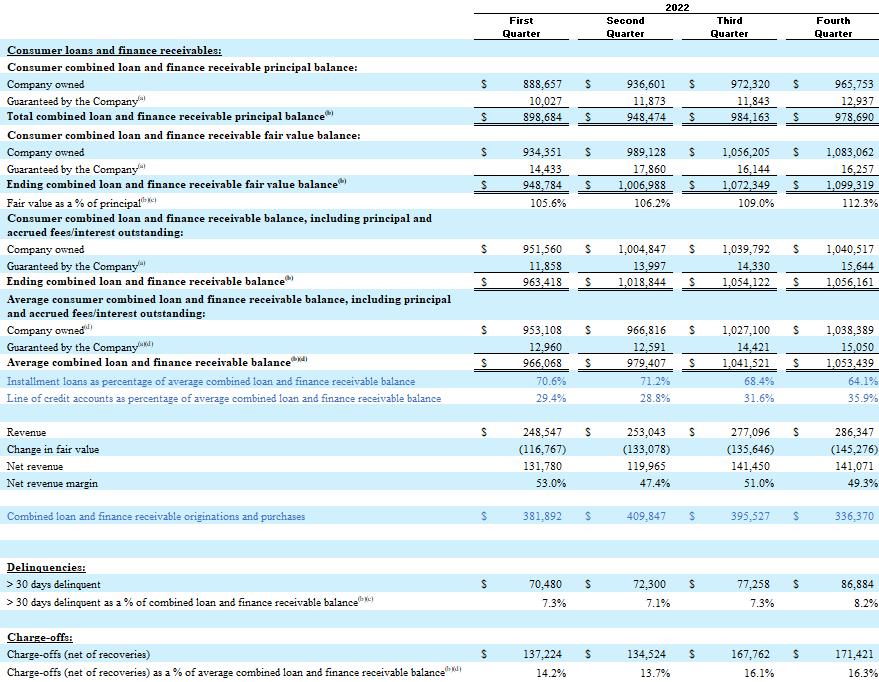

8. We note your discussion of the different revenue and credit characteristics of line of credit products here and in the small business loans section on page 54. Please tell us and revise future filings to disclose the information presented in the tables on pages 51 -54 separately for installment loans, lines of credit, and any other material loan product. Please refer to Item 303(a) of Regulation S-K and SEC Release No. 33-8350 for guidance.

Enova response: Enova manages its products at the portfolio level and does so on a dynamic basis, adapting to evolving market conditions to deliver strong returns at the portfolio level. Among other things, we believe that the disaggregation of all results to the individual product level would be potentially misleading to the users of our financial statements as it would be too granular. We believe that the sheer volume of data would be overwhelming to the reader and obfuscate their understanding of our results. The following is an excerpt from Item 303(a) of Regulation S-K that discusses part of the objective of the MD&A section:

The discussion and analysis must be of the financial statements and other statistical data that the registrant believes will enhance a reader's understanding of the registrant's financial condition, cash flows and other changes in financial condition and results of operations. A discussion and analysis that meets the requirements of this paragraph (a) is expected to better allow investors to view the registrant from management's perspective

In response to the Staff’s comments, we have included below the current year presentation of the results of our consumer loan and finance receivable portfolio referenced in the Staff’s comments, as updated with additional disclosure in blue text that we will add to future filings that we believe is responsive to Staff comments #8 and 9 (we will also add this information to the prior year table for the consumer portfolio as well as the current and prior year tables that present the results of our small business portfolio). We will also add discussion in the narrative analysis that follows the tables of any material known trends as it relates to the additional disclosures, to the extent relevant. If we determine that further disaggregation disclosure is material to the understanding of Enova’s results, we will discuss that in the narrative analysis that follows the tables along with any material known trends. We believe that the proposed disclosure is optimal and is consistent with Regulation S-K and the objective of the MD&A section as it better allows investors to view Enova’s results from management’s perspective.

United States Securities and Exchange Commission

Division of Corporation Finance

May 26, 2023

Page 9

Consumer Loans and Finance Receivables, page 51

9. We note your discussion related to the impact that the amount of originations has on your profitability and credit trends. Please tell us and revise future filings to include the amount of originations in the tables on pages 51-54 by loan product and discuss any trends. Please refer to Item 303(a) of Regulation S-K and SEC Release No. 33-8350 for guidance.

Enova response: Refer to our response to Staff comment #8, which includes our response to comment #9.

Consumer Loans and Finance Receivables, page 51

United States Securities and Exchange Commission

Division of Corporation Finance

May 26, 2023

Page 10

10. We note your discussion during your 2022 fourth quarter earnings conference call that originations from new customers during the quarter was 42% of total originations and your disclosure on page 52 that new customers typically have a higher default rate than returning customers. Please tell us and revise future filings to quantify, for each period presented, the dollar amount and percentage of originations by new customer and returning customers. To the extent there is a significant difference, please clarify if returning customers typically represent renewals of existing loans or new loans.

Enova response: There is no clear and consistent legal or industry definition for what comprises new or returning customers. We utilize the terms internally for a variety of reasons, and the definitions can differ across our various brands and products. We do not believe that disclosure of dollar amounts and percentages by new and returning customer is appropriate as it could be misleading to users of our financial statements. Furthermore, we do not believe there to be a comparability issue as very few of our competitors disclose dollar amounts and percentages of originations by new and returning customers. To the extent we determine that it would meaningfully help a reader understand our financial results, including known material trends, we will continue to include discussion of new customer mix in the narrative analysis of the MD&A.

Consumer Loans and Finance Receivables, page 51

11. We note your discussion on page 6 that if a loan is renewed or refinanced, it is considered a new loan. Please tell us and revise your disclosure of significant accounting policies in your financial statements in future filings to discuss how you determine whether a renewal is accounted for as a new loan or as a modification. Please tell us the guidance you considered in making your determination.

Enova response: We generally follow the guidance in ASC 310 for loan modifications. However, since we carry all loans and finance receivables under the fair value option as allowed under ASC 825-10-15-4, much of the loan modification guidance is not applicable since, under the fair value option, we do not defer any nonrefundable fees or origination costs and are not subject to an allowance for credit losses. In the “Significant Accounting Policies” section of the notes to consolidated financial statements, we will add in future applicable filings the following language: “If a loan is renewed or refinanced, the renewal or refinanced loan is considered a new loan. We generally do not consider modifications that do not necessitate the customer to sign a new loan agreement to be new loans.”

Current and Delinquent Loans and Finance Receivables, page 74

12. To the extent material, please tell us and revise future filings, here or in MD&A, to disclose the amount of payment deferrals in each period presented and the impact on financial results and trends.

Enova response: The Company offers certain forbearance options on its loan products with features such as payment deferrals without the incurrence of additional finance charges or late fees. Although options can vary between products, our customers’ ability to utilize deferrals is generally limited in number and available only to those customers who are not delinquent. We note that payment deferrals as a

United States Securities and Exchange Commission

Division of Corporation Finance

May 26, 2023

Page 11

percentage of overall payment obligations are de minimus. For the year ended December 31, 2022, this percentage was approximately 1%. Furthermore, when compared to disclosures provided by similar publicly-traded non-bank lenders, we generally cease the accrual of revenue and charge off loans fairly early in the delinquency cycle, which further decreases the impact of deferrals on financial results and trends. As we do not believe deferrals to be material to our financial results, we believe disclosure of the amount of payment deferrals is unnecessary.

Note 3. Loans and Finance Receivables, page 80

13. Please tell us and revise future filings to disclose the amount of accrued interest and fees included in the principal balances in the table on the bottom of page 80.

Enova response: In future filings, the Company will add a line below “Total principal balance” in the table indicated in the Staff’s comment to show accrued interest and fees.

Note 3. Loans and Finance Receivables, page 80

14. Please tell us and revise future filings to clarify if “Originations and acquisitions” in the rollforward on page 81 is presented on a cost basis or a fair value basis.

Enova response: In future filings, the Company will add a footnote explanation to the table that specifies that originations and acquisitions are presented on a cost basis.

******************************************************************************************

Please do not hesitate to contact me at (312) 517-7425 or scunningham@enova.com with any questions you may have with respect to the foregoing.

Very truly yours,

\s\ Steven E. Cunningham |

Steven E. Cunningham Enova International, Inc Chief Financial Officer

|

|

|