Filed Pursuant to Rule 424(b)(3)

SEC File No. 333-212848

PROSPECTUS

BioSig Technologies, Inc.

Up to 3,003,016 Shares of Common Stock and up to 1,501,513 Shares of Common Stock Underlying Warrants

This prospectus relates to the resale of up to (i) 3,003,016 shares of our common stock to be offered by the selling stockholders and (ii) 1,501,513 shares of our common stock to be offered by the selling stockholders upon the exercise of outstanding common stock purchase warrants.

Our common stock trades in the over-the-counter market and is quoted on the OTCQB tier of the OTC Markets Group, Inc. under the symbol “BSGM.” Only a limited public market currently exists for our common stock. On August 1, 2016, the last reported sale price of our shares of common stock on the OTCQB was $1.30 per share.

We will not receive any of the proceeds from the sale of common stock by the selling stockholders. However, we will receive proceeds from the exercise of the warrants if the warrants are exercised for cash. We intend to use those proceeds, if any, for general corporate purposes. All expenses of registration incurred in connection with this offering are being borne by us, but all selling and other expenses incurred by the selling stockholders will be borne by the selling stockholders.

We qualify as an “emerging growth company” as defined in the Jumpstart our Business Startups Act of 2012, or JOBS Act. Please read the related disclosure beginning on page 15 of this prospectus.

Investing in our common stock is highly speculative and involves a high degree of risk. You should carefully consider the risks and uncertainties in the section entitled “Risk Factors” beginning on page 3 of this prospectus before making a decision to purchase our stock.

We may amend or supplement this prospectus from time to time by filing amendments or supplements as required. You should read the entire prospectus and any amendments or supplements carefully before you make your investment decision.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is August 9, 2016

TABLE OF CONTENTS

You should rely only on the information contained in this prospectus. We have not authorized any other person to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. We are not making an offer to sell these securities in any jurisdiction where offer or sale is not permitted. You should assume that the information appearing in this prospectus is accurate only as of the date on the front cover of this prospectus. Our business, financial condition, results of operations and prospects may have changed since that date.

Information contained on our website is not part of this prospectus.

The following summary highlights information contained elsewhere in this prospectus. It may not contain all the information that may be important to you. You should read this entire prospectus carefully, including the sections entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and our historical financial statements and related notes included elsewhere in this prospectus or any accompanying prospectus supplement before making an investment decision. In this prospectus, unless the context requires otherwise, all references to “we,” “our,” “us” and the “Company” refer to BioSig Technologies, Inc.

Overview

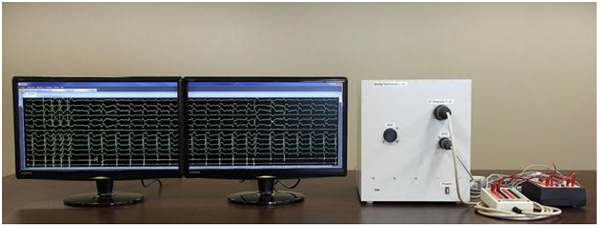

We are a development stage medical device company that is developing a proprietary technology platform to minimize noise and artifacts from cardiac recordings during electrophysiology studies, where signals that measure electrical activity of the heart, such as electrocardiograms and electrograms, are measured. These signals are also evaluated during ablation, a procedure that involves delivery of energy through the tip of a catheter that scars or destroys heart tissue in order to correct heart rhythm disturbances. Our product under development, the PURE (Precise Uninterrupted Real-time evaluation of Electrograms) EP System, is a surface electrocardiogram and intracardiac multichannel recording and analysis system that acquires, processes and displays electrocardiogram and electrograms required during electrophysiology studies and ablation procedures. The PURE EP System is intended to be used in addition to existing electrophysiology recorders. We believe that data provided by the PURE EP System will increase the workload ability and enhance the capabilities of the typical electrophysiology laboratory.

We were formed as BioSig Technologies, Inc., a Nevada corporation, in February 2009. In April 2011, we merged with our wholly-owned subsidiary, BioSig Technologies Inc., a Delaware corporation, with the Delaware corporation continuing as the surviving entity. We have not generated any revenue to date and consequently our operations are subject to all risks inherent in the establishment of a new business enterprise.

Our principal executive offices are located at 8441 Wayzata Blvd., Suite 240, Minneapolis, Minnesota 55426, telephone number (763) 999-7330. Our website address is www.biosigtech.com. Information accessed through our website is not incorporated into this prospectus and is not a part of this prospectus.

The Offering

| Common stock offered by the selling stockholders: | Up to 3,003,016 shares of our common stock to be offered by the selling stockholders and up to 1,501,513 shares of our common stock to be offered by the selling stockholders upon the exercise of outstanding common stock purchase warrants. | |||

| Common stock outstanding prior to the offering: | 20,476,522 | |||

| Common stock outstanding after this offering: | 21,978,035 (1) | |||

| Use of proceeds: | We will not receive any proceeds from the sale of the common stock offered by the selling stockholders. However, we will receive proceeds from the exercise price of the warrants if the warrants are exercised for cash. We intend to use those proceeds, if any, for general corporate purposes. | |||

| The OTCQB trading symbol: | “BSGM” | |||

| Risk factors: | You should carefully consider the information set forth in this prospectus and, in particular, the specific factors set forth in the “Risk Factors” section beginning on page 3 of this prospectus before deciding whether or not to invest in shares of our common stock. | |||

| (1) | The number of shares of common stock outstanding after the offering is based upon 20,476,522 shares outstanding as of August 1, 2016, and assumes the exercise of all warrants with respect to those shares being registered for resale pursuant to the registration statement of which this prospectus forms a part. |

The number of shares of common stock outstanding after this offering excludes:

| ● | 8,450,190 shares of common stock issuable upon the exercise of currently outstanding options at a weighted average exercise price of $2.26 per share; |

| ● | 130,933 shares of common stock available for future issuance under the BioSig Technologies, Inc. 2012 Equity Incentive Plan; | |

| ● | 230,582 shares of common stock issuable for accrued dividends on our Series C Preferred Stock as of June 30, 2016; | |

| ● | 726,679 shares of common stock issuable upon the conversion of our Series C Preferred Stock; and |

| ● | 6,644,208 shares of common stock issuable upon exercise of warrants at a weighted average exercise price of $2.01 per share. |

Investing in our common stock involves a high degree of risk. You should carefully consider the following factors and other information in this prospectus or any accompanying prospectus supplement before making a decision to invest in our common stock. If any of the risks actually occur, our business, financial conditions and operating results may be materially and adversely affected. In that event, the trading price of our common stock may decline, and you could lose all or part of your investment.

Risks Related to Our Business and Industry

Because our condition as a going concern is in doubt, we will be forced to cease our business operations unless we can raise sufficient funds to satisfy our working capital needs.

As shown in the accompanying financial statements during years ended December 31, 2015 and 2014, we incurred net losses attributable to common stockholders of $9,812,974 and $8,773,399, respectively and used $4,523,751 in cash for operating activities for the year ended December 31, 2015. As of August 1, 2016, we had cash on hand of approximately $700,000. These factors, among others, raise substantial doubt that we will be able to continue as a going concern for a reasonable period of time.

Our existence is dependent upon management’s ability to develop profitable operations. We are devoting substantially all of our efforts to developing product candidates and there can be no assurance that our efforts will be successful. There is no assurance that can be given that our actions will result in profitable operations or the resolution of our liquidity problems.

Because we are an early development stage company with no products near commercialization, we expect to incur significant additional operating losses.

We are an early development stage company and we expect to incur substantial additional operating expenses over the next several years as our research, development, pre-clinical testing, regulatory approval and clinical trial activities increase. The amount of our future losses and when, if ever, we will achieve profitability are uncertain. We have no products that have generated any commercial revenue and do not expect to generate revenues from the commercial sale of our products in the near future, if ever. Our ability to generate revenue and achieve profitability will depend on, among other things, the following:

| ● | successful completion of the pre-clinical and clinical development of our products; |

| ● | obtaining necessary regulatory approvals from the U.S. Food and Drug Administration or other regulatory authorities; |

| ● | establishing manufacturing, sales, and marketing arrangements, either alone or with third parties; and |

| ● | raising sufficient funds to finance our activities. |

We might not succeed at all, or at any, of these undertakings. If we are unsuccessful at some or all of these undertakings, our business, prospects, and results of operations may be materially adversely affected.

Our product candidates are at an early stage of development and may not be successfully developed or commercialized.

Our main product candidate, the PURE EP System, is in the early stage of development and will require substantial further capital expenditures, development, testing, and regulatory clearances prior to commercialization, especially given that we have not yet completed pre-clinical testing on this product. The development and regulatory approval process takes several years and it is not likely that the PURE EP System, even if successfully developed and approved by the U.S. Food and Drug Administration, may not be commercially available for a number of years. In addition, due to budgetary constraints, we have not been able to devote the level of resources that we desired to our research and development efforts. The continued development of our product candidates is dependent upon our ability to obtain sufficient financing. However, even if we are able to obtain the requisite financing to fund our development program, we cannot assure you that our product candidates will be successfully developed or commercialized. Our failure to develop, manufacture or receive regulatory approval for or successfully commercialize any of our product candidates could result in the failure of our business and a loss of all of your investment in our company.

We expect to derive our revenue from sales of our PURE EP System and other products we may develop. If we fail to generate revenue from these sources, our results of operations and the value of our business will be materially and adversely affected.

We expect our revenue to be generated from sales of our PURE EP System and other products we may develop. Future sales of these products, if any, will be subject to, among other things, the receipt of regulatory approvals and commercial and market uncertainties that may be outside our control. If we fail to generate our intended revenues from these products, our results of operations and the value of our business and securities would be materially and adversely affected.

We may need to finance our future cash needs through public or private equity offerings, debt financings or corporate collaboration and licensing arrangements. Any additional funds that we obtain may not be on terms favorable to us or our stockholders and may require us to relinquish valuable rights.

Until and unless we receive approval from the U.S. Food and Drug Administration and other regulatory authorities for our products, we will not generate revenues from our products. Therefore, for the foreseeable future, we will have to fund all of our operations and capital expenditures from cash on hand, public or private equity offerings, debt financings, bank credit facilities or corporate collaboration and licensing arrangements. We believe that our existing cash on hand will be sufficient to enable us to fund our projected operating requirements for approximately the next two and half months. However, we may need to raise additional funds more quickly if one or more of our assumptions prove to be incorrect or if we choose to expand our product development efforts more rapidly than we presently anticipate. We also may decide to raise additional funds before we require them if we are presented with favorable terms for raising capital.

If we seek to sell additional equity or debt securities, obtain a bank credit facility or enter into a corporate collaboration or licensing arrangement, we may not obtain favorable terms for us and/or our stockholders or be able to raise any capital at all, all of which could result in a material adverse effect on our business and results of operations. The sale of additional equity or debt securities, if convertible, could result in dilution to our stockholders. The incurrence of indebtedness would result in increased fixed obligations and could also result in covenants that would restrict our operations. Raising additional funds through collaboration or licensing arrangements with third parties may require us to relinquish valuable rights to our technologies, future revenue streams, research programs or product candidates, or to grant licenses on terms that may not be favorable to us or our stockholders. In addition, we could be forced to discontinue product development, reduce or forego sales and marketing efforts and forego attractive business opportunities, all of which could have an adverse impact on our business and results of operations.

We may be unable to develop our existing or future technology.

Our product, the PURE EP System, may not deliver the levels of accuracy and reliability needed to make it a successful product in the marketplace, and the development of such accuracy and reliability may be indefinitely delayed or may never be achieved. In addition, we may experience delays in the development of our technology for other reasons, including failure to obtain necessary funding and failure to obtain regulatory approvals. Failure to develop this or other technology could have an adverse material effect on our business, financial condition, results of operations and future prospects.

The results of clinical studies may not support the usefulness of our technology.

Conducting clinical trials is a long, expensive and uncertain process that is subject to delays and failure at any stage. Clinical trials can take months or years. The commencement or completion of any of our clinical trials may be delayed or halted for numerous reasons, including:

| ● | the U.S. Food and Drug Administration may not approve a clinical trial protocol or a clinical trial, or may place a clinical trial on hold; |

| ● | subjects may not enroll in clinical trials at the rate we expect or we may not follow up on subjects at the rate we expect; |

| ● | subjects may experience events unrelated to our products; |

| ● | third-party clinical investigators may not perform our clinical trials consistent with our anticipated schedule or the clinical trial protocol and good clinical practices, or other third-party organizations may not perform data collection and analysis in a timely or accurate manner; |

| ● | interim results of any of our clinical trials may be inconclusive or negative; |

| ● | regulatory inspections of our clinical trials may require us to undertake corrective action or suspend or terminate the clinical trials if investigators find us not to be in compliance with regulatory requirements; or |

| ● | governmental regulations or administrative actions may change and impose new requirements, particularly with respect to reimbursement. |

Results of pre-clinical studies do not necessarily predict future clinical trial results and previous clinical trial results may not be repeated in subsequent medical trials. We may experience delays, cost overruns and project terminations despite achieving promising results in pre-clinical testing or early clinical testing. In addition, the data obtained from clinical trials may be inadequate to support approval or clearance of a submission. The U.S. Food and Drug Administration may disagree with our interpretation of the data from our clinical trials, or may find the clinical trial design, conduct or results inadequate to demonstrate the safety and effectiveness of the product candidate. The U.S. Food and Drug Administration may also require us to conduct additional pre-clinical studies or clinical trials that could further delay approval of our products. If we are unsuccessful in receiving U.S. Food and Drug Administration approval of a product, we would not be able to commercialize the product in the U.S., which could seriously harm our business. Moreover, we face similar risks in other jurisdictions in which we may sell or propose to sell our products.

The medical device industry is subject to stringent regulation and failure to obtain regulatory approval will prevent commercialization of our products.

Medical devices are subject to extensive and rigorous regulation by the U.S. Food and Drug Administration pursuant to the Federal Food, Drug, and Cosmetic Act, by comparable agencies in foreign countries and by other regulatory agencies and governing bodies. Under the Federal Food, Drug, and Cosmetic Act and associated regulations, manufacturers of medical devices must comply with certain regulations that cover the composition, labeling, testing, clinical study, manufacturing, packaging and distribution of medical devices. In addition, medical devices must receive U.S. Food and Drug Administration clearance or approval before they can be commercially marketed in the U.S., and the U.S. Food and Drug Administration may require testing and surveillance programs to monitor the effects of approved products that have been commercialized and can prevent or limit further marketing of a product based on the results of these post-market evaluation programs. The process of obtaining marketing clearance from the U.S. Food and Drug Administration for new products could take a significant period of time, require the expenditure of substantial resources, involve rigorous pre-clinical and clinical testing, require changes to the products and result in limitations on the indicated uses of the product. In addition, if we seek regulatory approval in non-U.S. markets, we will be subject to further regulatory approvals that may require additional costs and resources. There is no assurance that we will obtain necessary regulatory approvals in a timely manner, or at all.

Our product, the PURE EP System, will need to receive 510(k) marketing clearance from the U.S. Food and Drug Administration in order permit us to market this product in the U.S. In addition, if we intend to market our product for additional medical uses or indications, we will need to submit additional 510(k) applications to the U.S. Food and Drug Administration that are supported by satisfactory clinical trial results specifically for the additional indication. The results of our initial clinical trials may not provide sufficient evidence to allow the U.S. Food and Drug Administration to grant us such additional marketing clearances and even additional trials requested by the U.S. Food and Drug Administration may not result in our obtaining 510(k) marketing clearance for our product. The failure to obtain U.S. Food and Drug Administration marketing clearance for the PURE EP System, any additional indications for the PURE EP System or any other of our future products would have a material adverse effect on our business.

Even if regulatory approval is obtained, our products will be subject to extensive post-approval regulation.

Once a product is approved by the relevant regulatory body for our targeted commercialization market, numerous post-approval requirements apply, including but not limited to requirements relating to manufacturing, labeling, packaging, advertising and record keeping. Even if regulatory approval of a product is obtained, the approval may be subject to limitations on the uses for which the product may be marketed, or contain requirements for costly post-marketing testing and surveillance to monitor the safety or efficacy of the product. Any such post-approval requirement could reduce our revenues, increase our expenses and render the approved product candidate not commercially viable. If we fail to comply with the regulatory requirements of the applicable regulatory authorities, or if previously unknown problems with any approved commercial products, manufacturers or manufacturing processes are discovered, we could be subject to administrative or judicially imposed sanctions or other negative consequences, including:

| ● | restrictions on our products, manufacturers or manufacturing processes; |

| ● | warning letters and untitled letters; |

| ● | civil penalties and criminal prosecutions and penalties; |

| ● | fines; |

| ● | injunctions; |

| ● | product seizures or detentions; |

| ● | import or export bans or restrictions; |

| ● | voluntary or mandatory product recalls and related publicity requirements; |

| ● | suspension or withdrawal of regulatory approvals; |

| ● | total or partial suspension of production; and |

| ● | refusal to approve pending applications for marketing approval of new products or of supplements to approved applications. |

Regulations are constantly changing, and in the future our business may be subject to additional regulations that increase our compliance costs.

We believe we understand the current laws and regulations to which our products will be subject in the future. However, federal, state and foreign laws and regulations relating to the sale of our products are subject to future changes, as are administrative interpretations of regulatory agencies. If we fail to comply with such federal, state or foreign laws or regulations, we may fail to obtain regulatory approval for our products and, if we have already obtained regulatory approval, we could be subject to enforcement actions, including injunctions preventing us from conducting our business, withdrawal of clearances or approvals and civil and criminal penalties. In the event that federal, state, and foreign laws and regulations change, we may incur additional costs to seek government approvals, in addition to the clearance we intend to seek from the U.S. Food and Drug Administration in order to sell or market our products. If we are slow or unable to adapt to changes in existing regulatory requirements or the promulgation of new regulatory requirements or policies, we or our licensees may, following approval, lose marketing approval for our products which will impact our ability to conduct business in the future.

The market for our technology and revenue generation avenues for our products may be slow to develop, if at all.

The market for our products may be slower to develop or smaller than estimated or it may be more difficult to build the market than anticipated. The medical community may resist our products or be slower to accept them than we anticipate. Revenues from our products may be delayed or costs may be higher than anticipated which may result in our need for additional funding. We anticipate that our principal route to market will be through commercial distribution partners. These arrangements are generally non-exclusive and have no guaranteed sales volumes or commitments. The partners may be slower to sell our products than anticipated. Any financial, operational or regulatory risks that affect our partners could also affect the sales of our products. In the current economic environment, hospitals and clinical purchasing budgets may exercise greater restraint with respect to purchases, which may result in purchasing decisions being delayed or denied. If any of these situations were to occur this could have a material adverse effect on our business, financial condition, results of operations and future prospects.

If we seek to market our products in foreign jurisdictions, we may need to obtain regulatory approval in these jurisdictions.

In order to market our products in the European Union and many other foreign jurisdictions, we may need to obtain separate regulatory approvals and comply with numerous and varying regulatory requirements. Approval procedures vary among countries (except with respect to the countries that are part of the European Economic Area) and can involve additional clinical testing. The time required to obtain approval may differ from that required to obtain U.S. Food and Drug Administration approval. Should we decide to market our products abroad, we may fail to obtain foreign regulatory approvals on a timely basis, if at all. Approval by the U.S. Food and Drug Administration does not ensure approval by regulatory authorities in other countries, and approval by one foreign regulatory authority, including obtaining CE Mark approval, does not ensure approval by regulatory authorities in other foreign countries or by the U.S. Food and Drug Administration. We may be unable to file for, and may not receive, necessary regulatory approvals to commercialize our products in any foreign market, which could adversely affect our business prospects.

The electrophysiology market is highly competitive.

There are a number of groups and organizations, such as healthcare, medical device and software companies in the electrophysiology market that may develop a competitive offering to our products. The largest companies in the electrophysiology market are GE, Johnson & Johnson, Boston Scientific, Siemens and St. Jude Medical. All of these companies have significantly greater resources, experience and name recognition than we possess. There is no assurance that they will not attempt to develop similar or superior products, that they will not be successful in developing such products or that any products they may develop will not have a competitive advantage over our products. If we experience delayed regulatory approvals or disputed clinical claims, we may not have a commercial or clinical advantage over competitors’ products that we believe we currently possess. Should a superior offering come to market, this could have a material adverse effect on our business, financial condition, results of operations and future prospects.

We rely on key officers, consultants and scientific and medical advisors, and their knowledge of our business and technical expertise would be difficult to replace.

We are highly dependent on our officers, consultants and scientific and medical advisors because of their expertise and experience in medical device development. We do not have “key person” life insurance policies for any of our officers. Moreover, if we are unable to obtain additional funding, we will be unable to meet our current and future compensation obligations to such employees and consultants. In light of the foregoing, we are at risk that one or more of our consultants or employees may leave our company for other opportunities where there is no concern about such employers fulfilling their compensation obligations, or for other reasons. The loss of the technical knowledge and management and industry expertise of any of our key personnel could result in delays in product development, loss of customers and sales and diversion of management resources, which could adversely affect our results of operations.

We may fail to attract and retain qualified personnel.

We expect to rapidly expand our operations and grow our sales, research and development and administrative operations. This expansion is expected to place a significant strain on our management and will require hiring a significant number of qualified personnel. Accordingly, recruiting and retaining such personnel in the future will be critical to our success. There is intense competition from other companies, research and academic institutions, government entities and other organizations for qualified personnel in the areas of our activities. Many of these companies, institutions and organizations have greater resources than we do, along with more prestige associated with their names. If we fail to identify, attract, retain and motivate these highly skilled personnel, we may be unable to continue our marketing and development activities, and this could have a material adverse effect on our business, financial condition, results of operations and future prospects.

If we do not effectively manage changes in our business, these changes could place a significant strain on our management and operations.

Our ability to grow successfully requires an effective planning and management process. The expansion and growth of our business could place a significant strain on our management systems, infrastructure and other resources. To manage our growth successfully, we must continue to improve and expand our systems and infrastructure in a timely and efficient manner. Our controls, systems, procedures and resources may not be adequate to support a changing and growing company. If our management fails to respond effectively to changes and growth in our business, including acquisitions, there could be a material adverse effect on our business, financial condition, results of operations and future prospects.

Our strategic business plan may not produce the intended growth in revenue and operating income.

Our strategies ultimately include making significant investments in sales and marketing programs to achieve revenue growth and margin improvement targets. If we do not achieve the expected benefits from these investments or otherwise fail to execute on our strategic initiatives, we may not achieve the growth improvement we are targeting and our results of operations may be adversely affected. We may also fail to secure the capital necessary to make these investments, which will hinder our growth.

In addition, as part of our strategy for growth, we may make acquisitions and enter into strategic alliances such as joint ventures and joint development agreements. However, we may not be able to identify suitable acquisition candidates, complete acquisitions or integrate acquisitions successfully, and our strategic alliances may not prove to be successful. In this regard, acquisitions involve numerous risks, including difficulties in the integration of the operations, technologies, services and products of the acquired companies and the diversion of management’s attention from other business concerns. Although we will endeavor to evaluate the risks inherent in any particular transaction, there can be no assurance that we will properly ascertain all such risks. In addition, acquisitions could result in the incurrence of substantial additional indebtedness and other expenses or in potentially dilutive issuances of equity securities. There can be no assurance that difficulties encountered with acquisitions will not have a material adverse effect on our business, financial condition and results of operations.

We currently have no sales, marketing or distribution operations and will need to expand our expertise in these areas.

We currently have no sales, marketing or distribution operations and, in connection with the expected commercialization of our planned products, will need to expand our expertise in these areas. To increase internal sales, distribution and marketing expertise and be able to conduct these operations, we would have to invest significant amounts of financial and management resources. In developing these functions ourselves, we could face a number of risks, including:

| ● | we may not be able to attract and build an effective marketing or sales force; |

| ● | the cost of establishing, training and providing regulatory oversight for a marketing or sales force may be substantial; and |

| ● | there are significant legal and regulatory risks in medical device marketing and sales that we have never faced, and any failure to comply with applicable legal and regulatory requirements for sales, marketing and distribution could result in an enforcement action by the U.S. Food and Drug Administration, European regulators or other authorities that could jeopardize our ability to market our planned products or could subject us to substantial liability. |

The liability of our directors and officers is limited.

The applicable provisions of the Delaware General Corporation Law and our Amended and Restated Certificate of Incorporation and By-laws limit the liability of our directors to us and our stockholders for monetary damages for breaches of their fiduciary duties, with certain exceptions, and for other specified acts or omissions of such persons. In addition, the applicable provisions of the Delaware General Corporation Law and of our Amended and Restated Certificate of Incorporation and By-laws provide for indemnification of such persons under certain circumstances. In the event we are required to indemnify any of our directors or any other person, our financial strength may be harmed.

Our product development program depends upon third-party researchers who are outside our control and whose negative performance could materially hinder or delay our pre-clinical testing or clinical trials.

We do not have the ability to conduct all aspects of pre-clinical testing or clinical trials ourselves. We depend upon independent investigators and collaborators, such as commercial third-parties, government, universities and medical institutions, to conduct our pre-clinical and clinical trials under agreements with us. These collaborators are not our employees and we cannot control the amount or timing of resources that they devote to our programs. These investigators may not assign as great a priority to our programs or pursue them as diligently as we would if we were undertaking such programs ourselves. The failure of any of these outside collaborators to perform in an acceptable and timely manner in the future, including in accordance with any applicable regulatory requirements, such as good clinical and laboratory practices, or pre-clinical testing or clinical trial protocols, could cause a delay or otherwise adversely affect our pre-clinical testing or clinical trials, our success in obtaining regulatory approvals and, ultimately, the timely advancement of our development programs. In addition, these collaborators may also have relationships with other commercial entities, some of whom may compete with us. If our collaborators assist our competitors at our expense, our competitive position would be harmed.

Negative publicity or unfavorable media coverage could damage our reputation and harm our operations.

In the event that the marketplace perceives our products as not offering the benefits which we believe they offer, we may receive negative publicity. This publicity may result in litigation and increased regulation and governmental review. If we were to receive such negative publicity or unfavorable media attention, whether warranted or unwarranted, our ability to market our products would be adversely affected. We may be required to change our products and services and become subject to increased regulatory burdens, and we may be required to pay large judgments or fines and incur significant legal expenses. Any combination of these factors could further increase our cost of doing business and adversely affect our financial position, results of operations and cash flows.

We may face risks associated with future litigation and claims.

We may, in the future, be involved in one or more lawsuits, claims or other proceedings. These suits could concern issues including contract disputes, employment actions, employee benefits, taxes, environmental, health and safety, personal injury and product liability matters. Due to the uncertainties of litigation, we can give no assurance that we will prevail on any claims made against us in any such lawsuit. Also, we can give no assurance that any other lawsuits or claims brought in the future will not have an adverse effect on our financial condition, liquidity or operating results.

Specifically, we believe we will be subject to product liability claims or product recalls, particularly in the event of false positive or false negative reports, because we plan to develop and manufacture medical diagnostic products. We intend to obtain appropriate insurance coverage once we reach a manufacturing stage. A product recall or a successful product liability claim or claims that exceed our planned insurance coverage could have a material adverse effect on us. In addition, product liability insurance is expensive. In the future we may not be able to obtain coverage on acceptable terms, if at all. Moreover, our insurance coverage may not adequately protect us from liability that we incur in connection with clinical trials or sales of our products. In the event of an award against us during a time when we have no available insurance or insufficient insurance, we may sustain significant losses of our operating capital. In addition, any products liability litigation, regardless of outcome or strength of claims, may divert time and resources away from the day-to-day operation of our business and product development efforts. Any of these outcomes could adversely impact our business and results of operations, as well as impair our reputation in the medical and investment communities.

We may be subject, directly or indirectly, to U.S. federal and state health care fraud and abuse and false claims laws and regulations. Prosecutions under such laws have increased in recent years and we may become subject to such litigation. If we are unable to, or have not fully complied with such laws, we could face substantial penalties.

If we are successful in achieving regulatory approval to market our PURE EP System, our operations will be directly, or indirectly through our customers and health care professionals, subject to various U.S. federal and state fraud and abuse laws, including, without limitation, the federal Anti-Kickback Statute, federal False Claims Act, and federal Foreign Corrupt Practices Act. These laws may impact, among other things, our proposed sales, and marketing and education programs.

The federal Anti-Kickback Statute prohibits persons from knowingly and willfully soliciting, offering, receiving or providing remuneration, directly or indirectly, in exchange for or to induce either the referral of an individual, or the furnishing or arranging for a good or service, for which payment may be made under a federal health care program such as the Medicare and Medicaid programs. Several courts have interpreted the statute’s intent requirement to mean that if any one purpose of an arrangement involving remuneration is to induce referrals of federal health care covered business, the statute has been violated. The federal Anti-Kickback Statute is broad and, despite a series of narrow safe harbors, prohibits many arrangements and practices that are lawful in businesses outside of the health care industry. Penalties for violations of the federal Anti-Kickback Statute include criminal penalties and civil and administrative sanctions such as fines, imprisonment and possible exclusion from Medicare, Medicaid and other federal health care programs. An alleged violation of the federal Anti-Kickback Statute may be used as a predicate offense to establish liability pursuant to other federal laws and regulations such as the federal False Claims Act. Many states have also adopted laws similar to the federal Anti-Kickback Statute, some of which apply to the referral of patients for health care items or services reimbursed by any source, not only the Medicare and Medicaid programs.

The federal False Claims Act prohibits persons from knowingly filing, or causing to be filed, a false claim to, or the knowing use of false statements to obtain payment from, the federal government. Suits filed under the federal False Claims Act, known as “qui tam” actions, can be brought by any individual on behalf of the government and such individuals, commonly known as “relators” or “whistleblowers,” may share in any amounts paid by the entity to the government in fines or settlement. The frequency of filing qui tam actions has increased significantly in recent years, causing greater numbers of medical device and health care companies to have to defend a federal False Claim Act action. The federal Patient Protection and Affordable Care Act includes provisions expanding the ability of certain relators to bring actions that would have been previously dismissed under prior law. When an entity is determined to have violated the federal False Claims Act, it may be required to pay up to three times the actual damages sustained by the government, plus civil penalties for each separate false claim. The Deficit Reduction Act of 2005 encouraged states to enact or modify their state false claims act to be at least as effective as the federal False Claims Act by granting states a portion of any federal Medicaid funds recovered through Medicaid-related actions. Most states have enacted state false claims laws, and many of those states included laws including qui tam provisions.

The federal Patient Protection and Affordable Care Act includes provisions known as the Physician Payments Sunshine Act, which requires manufacturers of drugs, biologics, devices and medical supplies covered under Medicare and Medicaid starting in 2012 to record any transfers of value to physicians and teaching hospitals and to report this data beginning in 2013 to the Centers for Medicare and Medicaid Services for subsequent public disclosure. Manufacturers must also disclose investment interests held by physicians and their family members. Failure to submit the required information may result in civil monetary penalties of up to $1 million per year for knowing violations and may result in liability under other federal laws or regulations. Similar reporting requirements have also been enacted on the state level in the U.S., and an increasing number of countries worldwide either have adopted or are considering similar laws requiring transparency of interactions with health care professionals. In addition, some states such as Massachusetts and Vermont impose an outright ban on certain gifts to physicians. If we receive U.S. Food and Drug Administration clearance to market our system in the U.S., these laws could affect our promotional activities by limiting the kinds of interactions we could have with hospitals, physicians or other potential purchasers or users of our system. Both the disclosure laws and gift bans will impose administrative, cost and compliance burdens on us.

We are unable to predict whether we could be subject to actions under any of these laws, or the impact of such actions. If we are found to be in violation of any of the laws described above and other applicable state and federal fraud and abuse laws, we may be subject to penalties, including civil and criminal penalties, damages, fines, or an administrative action of suspension or exclusion from government health care reimbursement programs and the curtailment or restructuring of our operations.

In addition, to the extent we commence commercial operations overseas, we will be subject to the federal Foreign Corrupt Practices Act and other countries’ anti-corruption/anti-bribery regimes, such as the U.K. Bribery Act. The federal Foreign Corrupt Practices Act prohibits improper payments or offers of payments to foreign governments and their officials for the purpose of obtaining or retaining business. Safeguards we implement to discourage improper payments or offers of payments by our employees, consultants, sales agents or distributors may be ineffective, and violations of the federal Foreign Corrupt Practices Act and similar laws may result in severe criminal or civil sanctions, or other liabilities or proceedings against us, any of which would likely harm our reputation, business, financial condition and results of operations.

Risks Related to Our Intellectual Property

If we do not obtain protection for our intellectual property rights, our competitors may be able to take advantage of our research and development efforts to develop competing products.

We intend to rely on a combination of patents, trade secrets, and nondisclosure and non-competition agreements to protect our proprietary intellectual property. We have filed a patent application with the U.S. Patent and Trademark Office, and we have filed this patent application under the Patent Cooperation Treaty (PCT) with the U.S. Receiving Office. We plan to file additional patent applications in the U.S. and in other countries as we deem appropriate for our products. Our applications have and will include claims intended to provide market exclusivity for certain commercial aspects of the products, including the methods of production, the methods of usage and the commercial packaging of the products. However, we cannot predict:

| ● | the degree and range of protection any patents will afford us against competitors, including whether third parties will find ways to invalidate or otherwise circumvent our patents; |

| ● | if and when such patents will be issued, and, if granted, whether patents will be challenged and held invalid or unenforceable; |

| ● | whether or not others will obtain patents claiming aspects similar to those covered by our patents and patent applications; or |

| ● | whether we will need to initiate litigation or administrative proceedings which may be costly regardless of outcome. |

Our success also depends upon the skills, knowledge and experience of our scientific and technical personnel, our consultants and advisors as well as our licensors and contractors. To help protect our proprietary know-how and our inventions for which patents may be unobtainable or difficult to obtain, we rely on trade secret protection and confidentiality agreements. To this end, it is our policy to require all of our employees, consultants, advisors and contractors to enter into agreements which prohibit the disclosure of confidential information and, where applicable, require disclosure and assignment to us of the ideas, developments, discoveries and inventions important to our business. These agreements may not provide adequate protection for our trade secrets, know-how or other proprietary information in the event of any unauthorized use or disclosure or the lawful development by others of such information. If any of our trade secrets, know-how or other proprietary information is disclosed, the value of our trade secrets, know-how and other proprietary rights would be significantly impaired and our business and competitive position would suffer.

Given the fact that we may pose a competitive threat, competitors, especially large and well-capitalized companies that own or control patents relating to electrophysiology recording systems, may successfully challenge our current and planned patent applications, produce similar products or products that do not infringe our future patents, or produce products in countries where we have not applied for patent protection or that do not respect our patents.

If any of these events occurs, or we otherwise lose protection for our trade secrets or proprietary know-how, the value of our intellectual property may be greatly reduced. Patent protection and other intellectual property protection are important to the success of our business and prospects, and there is a substantial risk that such protections will prove inadequate.

If we infringe upon the rights of third parties, we could be prevented from selling products and forced to pay damages and defend against litigation.

If our products, methods, processes and other technologies infringe the proprietary rights of other parties, we could incur substantial costs and we may be required to:

| ● | obtain licenses, which may not be available on commercially reasonable terms, if at all; |

| ● | abandon an infringing product candidate; |

| ● | redesign our product candidates or processes to avoid infringement; |

| ● | cease usage of the subject matter claimed in the patents held by others; |

| ● | pay damages; and/or |

| ● | defend litigation or administrative proceedings which may be costly regardless of outcome, and which could result in a substantial diversion of our financial and management resources. |

Any of these events could substantially harm our earnings, financial condition and operations.

Risks Related to our Common Stock

The public trading market for our common stock is volatile and may result in higher spreads in stock prices, which may limit the ability of our investors to sell their shares of our common stock at a profit, if at all.

Our common stock trades in the over-the-counter market and is quoted on the OTCQB tier of the OTC Markets Group, Inc. The over-the-counter market for securities has historically experienced extreme price and volume fluctuations during certain periods. These broad market fluctuations may adversely affect the market price of our common stock and result in substantial losses to our investors. In addition, the spreads on stock traded through the over-the-counter market are generally unregulated and higher than on national stock exchanges, which means that the difference between the price at which shares could be purchased by investors in the over-the-counter market compared to the price at which they could be subsequently sold would be greater than on these exchanges. Significant spreads between the bid and asked prices of the stock could continue during any period in which a sufficient volume of trading is unavailable or if the stock is quoted by an insignificant number of market makers. Historically, our trading volume has been insufficient to significantly reduce this spread and we have had a limited number of market makers insufficient to affect this spread. These higher spreads could adversely affect investors who purchase the shares at the higher price at which the shares are sold, but subsequently sell the shares at the lower bid prices quoted by the brokers. Unless the bid price for the stock exceeds the price paid for the shares by the investor, plus brokerage commissions or charges, the investor could lose money on the sale. For higher spreads such as those on over-the-counter stocks, this is likely a much greater percentage of the price of the stock than for exchange listed stocks. There is no assurance that at the time an investor in our common stock wishes to sell the shares, the bid price will have sufficiently increased to create a profit on the sale.

We do not know whether a market for our common stock will be sustained or what the market price of our common stock will be and as a result it may be difficult for you to sell your shares of our common stock.

Although our common stock now trades on the OTCQB, an active trading market for our shares may not be sustained. It may be difficult for our stockholders to sell their shares without depressing the market price for our shares or at all. As a result of these and other factors, our stockholders may not be able to sell their shares. Further, an inactive market may also impair our ability to raise capital by selling shares of our common stock and may impair our ability to enter into strategic partnerships or acquire companies or products by using our shares of common stock as consideration. If an active market for our common stock does not develop or is not sustained, it may be difficult for our stockholders to sell shares of our common stock.

The market price for our common stock may fluctuate significantly, which could result in substantial losses by our investors.

The market price of our common stock may fluctuate significantly in response to numerous factors, some of which are beyond our control, such as:

| ● | the outcomes of potential future patent litigation; |

| ● | our ability to monetize our future patents; |

| ● | changes in our industry; |

| ● | announcements of technological innovations, new products or product enhancements by us or others; |

| ● | announcements by us of significant strategic partnerships, out-licensing, in-licensing, joint ventures, acquisitions or capital commitments; |

| ● | changes in earnings estimates or recommendations by security analysts, if our common stock is covered by analysts; | |

| ● | investors’ general perception of us; | |

| ● | future issuances of common stock; | |

| ● | the addition or departure of key personnel; | |

| ● | general market conditions, including the volatility of market prices for shares of technology companies, generally, and other factors, including factors unrelated to our operating performance; and | |

| ● | the other factors described in this “Risk Factors” section. |

These factors and any corresponding price fluctuations may materially and adversely affect the market price of our common stock and result in substantial losses by our investors.

Further, the stock market in general, and the market for technology companies in particular, has experienced extreme price and volume fluctuations in the past. Continued market fluctuations could result in extreme volatility in the price of our common stock, which could cause a decline in the value of our common stock.

Price volatility of our common stock might be worse if the trading volume of our common stock is low. In the past, following periods of market volatility, stockholders have often instituted securities class action litigation. If we were involved in securities litigation, it could have a substantial cost and divert resources and attention of management from our business, even if we are successful. Future sales of our common stock could also reduce the market price of such stock.

Moreover, the liquidity of our common stock is limited, not only in terms of the number of shares that can be bought and sold at a given price, but by delays in the timing of transactions and reduction in security analysts’ and the media’s coverage of us, if any. These factors may result in lower prices for our common stock than might otherwise be obtained and could also result in a larger spread between the bid and ask prices for our common stock. In addition, without a large float, our common stock is less liquid than the stock of companies with broader public ownership and, as a result, the trading prices of our common stock may be more volatile. In the absence of an active public trading market, an investor may be unable to liquidate its investment in our common stock. Trading of a relatively small volume of our common stock may have a greater impact on the trading price of our stock than would be the case if our public float were larger. We cannot predict the prices at which our common stock will trade in the future.

Our common stock is a “penny stock,” which makes it more difficult for our investors to sell their shares.

Our common stock is subject to the “penny stock” rules adopted under Section 15(g) of the Securities Exchange Act of 1934, as amended. The penny stock rules generally apply to companies whose common stock is not listed on The NASDAQ Stock Market or other national securities exchange and trades at less than $5.00 per share, other than companies that have had average revenue of at least $6,000,000 for the last three years or that have tangible net worth of at least $5,000,000 ($2,000,000 if the company has been operating for three or more years). These rules require, among other things, that brokers who trade penny stock to persons other than “established customers” complete certain documentation, make suitability inquiries of investors and provide investors with certain information concerning trading in the security, including a risk disclosure document and quote information under certain circumstances. Many brokers have decided not to trade penny stocks because of the requirements of the penny stock rules and, as a result, the number of broker-dealers willing to act as market makers in such securities is limited. If we remain subject to the penny stock rules for any significant period, it could have an adverse effect on the market, if any, for our securities. If our securities are subject to the penny stock rules, investors will find it more difficult to dispose of our securities.

Offers or availability for sale of a substantial number of shares of our common stock may cause the price of our common stock to decline.

If our stockholders sell substantial amounts of our common stock in the public market, it could create a circumstance commonly referred to as an “overhang,” in anticipation of which the market price of our common stock could fall. The existence of an overhang, whether or not sales have occurred or are occurring, also could make more difficult our ability to raise additional financing through the sale of equity or equity-related securities in the future at a time and price that we deem reasonable or appropriate.

Our stockholders may experience substantial dilution as a result of the conversion of outstanding convertible preferred stock or the exercise of options and warrants to purchase shares of our common stock.

As of August 1, 2016, we have granted options to purchase 8,450,190 shares of common stock and have reserved 130,933 shares of our common stock for further issuances pursuant to our 2012 Equity Incentive Plan. In addition, as of August 1, 2016, we may be required to issue 957,261 shares of our common stock for issuance upon conversion of outstanding convertible preferred stock plus accrued dividends as of June 30, 2016 and 8,145,721 shares of our common stock for issuance upon exercise of outstanding warrants. Should all of these shares be issued, you would experience dilution in ownership of our common stock and the price of our common stock will decrease unless the value of our company increases by a corresponding amount.

The interests of our controlling stockholders may not coincide with yours and such controlling stockholders may make decisions with which you may disagree.

As of August 1, 2016, two of our stockholders beneficially owned over 40.05% of our common stock. As a result, these stockholders may be able to influence the outcome of matters requiring stockholder approval, including the election of directors and approval of significant corporate transactions. In addition, this concentration of ownership may delay or prevent a change in control of our company and make some future transactions more difficult or impossible without the support of our controlling stockholders. The interests of our controlling stockholders may not coincide with our interests or the interests of other stockholders.

If securities or industry analysts do not publish research or publish inaccurate or unfavorable research about our business, our stock price and trading volume could decline.

The trading market for our common stock will depend in part on the research and reports that securities or industry analysts publish about us or our business. We currently have new research coverage by securities and industry analysts. If one or more of the analysts who covers us downgrades our stock or publishes inaccurate or unfavorable research about our business, our stock price would likely decline. If one or more of these analysts cease coverage of us or fails to publish reports on us regularly, demand for our stock could decrease, which could cause our stock price and trading volume to decline.

We are subject to financial reporting and other requirements that place significant demands on our resources.

We are subject to reporting and other obligations under the Securities Exchange Act of 1934, as amended, including the requirements of Section 404 of the Sarbanes-Oxley Act of 2002. Section 404 requires us to conduct an annual management assessment of the effectiveness of our internal controls over financial reporting. These reporting and other obligations place significant demands on our management, administrative, operational, internal audit and accounting resources. Any failure to maintain effective internal controls could have a material adverse effect on our business, operating results and stock price. Moreover, effective internal control is necessary for us to provide reliable financial reports and prevent fraud. If we cannot provide reliable financial reports or prevent fraud, we may not be able to manage our business as effectively as we would if an effective control environment existed, and our business and reputation with investors may be harmed.

We are an “emerging growth company” and we cannot be certain that the reduced disclosure requirements applicable to emerging growth companies will not make our common stock less attractive to investors.

The JOBS Act permits “emerging growth companies” like us to rely on some of the reduced disclosure requirements that are already available to smaller reporting companies. As long as we qualify as an emerging growth company or a smaller reporting company, we would be permitted to omit the auditor’s attestation on internal control over financial reporting that would otherwise be required by the Sarbanes-Oxley Act, as described above, and are also exempt from the requirement to submit “say-on-pay”, “say-on-pay frequency” and “say-on-parachute” votes to our stockholders and may avail ourselves of reduced executive compensation disclosure that is already available to smaller reporting companies.

In addition, Section 107 of the JOBS Act also provides that an emerging growth company can take advantage of the exemption from complying with new or revised accounting standards provided in Section 7(a)(2)(B) of the Securities Act of 1933, as amended, as long as we are an emerging growth company. An emerging growth company can therefore delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. We intend to take advantage of the benefits of this until we are no longer an emerging growth company or until we affirmatively and irrevocably opt out of this exemption. Our financial statements may therefore not be comparable to those of companies that comply with such new or revised accounting standards.

We will cease to be an emerging growth company upon the earliest to occur of (i) the last day of the fiscal year during which we had total annual gross revenues of $1 billion (as indexed for inflation); (ii) the last day of the fiscal year following the fifth anniversary of the date of the first sale of common stock under our registration statement on Form S-1 that became effective on June 23, 2014; (iii) the date on which we have, during the previous 3-year period, issued more than $1 billion in non-convertible debt; or (iv) the date on which we are deemed to be a “large accelerated filer,” as defined by the Securities and Exchange Commission, which would generally occur upon our attaining a public float of at least $700 million. Once we lose emerging growth company status, we expect the costs and demands placed upon our management to increase, as we would have to comply with additional disclosure and accounting requirements, particularly if we would also not qualify as a smaller reporting company. In addition, until such time, we cannot predict if investors will find our common stock less attractive because we may rely on these exemptions. If some investors find our common stock less attractive as a result, there may be a less active trading market for our common stock and our stock price may be more volatile and could cause our stock price to decline.

Delaware law and our Amended and Restated Certificate of Incorporation and By-laws contain anti-takeover provisions that could delay or discourage takeover attempts that stockholders may consider favorable.

Our board of directors is authorized to issue shares of preferred stock in one or more series and to fix the voting powers, preferences and other rights and limitations of the preferred stock. Accordingly, we may issue shares of preferred stock with a preference over our common stock with respect to dividends or distributions on liquidation or dissolution, or that may otherwise adversely affect the voting or other rights of the holders of common stock. Issuances of preferred stock, depending upon the rights, preferences and designations of the preferred stock, may have the effect of delaying, deterring or preventing a change of control, even if that change of control might benefit our stockholders. In addition, we are subject to Section 203 of the Delaware General Corporation Law. Section 203 generally prohibits a public Delaware corporation from engaging in a “business combination” with an “interested stockholder” for a period of three years after the date of the transaction in which the person became an interested stockholder, unless (i) prior to the date of the transaction, the board of directors of the corporation approved either the business combination or the transaction which resulted in the stockholder becoming an interested stockholder; (ii) the interested stockholder owned at least 85% of the voting stock of the corporation outstanding at the time the transaction commenced, excluding for purposes of determining the number of shares outstanding (a) shares owned by persons who are directors and also officers and (b) shares owned by employee stock plans in which employee participants do not have the right to determine confidentially whether shares held subject to the plan will be tendered in a tender or exchange offer; or (iii) on or subsequent to the date of the transaction, the business combination is approved by the board and authorized at an annual or special meeting of stockholders, and not by written consent, by the affirmative vote of at least 66 2/3% of the outstanding voting stock which is not owned by the interested stockholder.

Section 203 could delay or prohibit mergers or other takeover or change in control attempts with respect to us and, accordingly, may discourage attempts to acquire us even though such a transaction may offer our stockholders the opportunity to sell their stock at a price above the prevailing market price.

The terms of our Series C Preferred Stock prohibit us from paying dividends in the future on our common stock. As a result, any return on investment may be limited to the value of our common stock.

The terms of our Series C Preferred Stock prohibit us from paying dividends in the future on our common stock, absent consent from the holders representing a super-majority of the outstanding shares of our Series C Preferred Stock and a certain investor. Because we will likely not pay dividends, our common stock may be less valuable because a return on an investment in our common stock will only occur if our stock price appreciates.

Risks Related to our Series C Preferred Stock

Our Series C Preferred Stock contains covenants that could limit our financing options and liquidity position, which would limit our ability to grow our business.

Covenants in the certificate of designation for our Series C Preferred Stock impose operating and financial restrictions on us. These restrictions prohibit or limit our ability to, among other things:

| ● | incur additional indebtedness; |

| ● | permit liens on assets; |

| ● | repay, repurchase or otherwise acquire more than a de minimis number of shares of capital stock; |

| ● | pay cash dividends to our stockholders; and |

| ● | engage in transactions with affiliates. |

These restrictions may limit our ability to obtain financing, withstand downturns in our business or take advantage of business opportunities. Moreover, debt financing we may seek may contain terms that include more restrictive covenants, may require repayment on an accelerated schedule or may impose other obligations that limit our ability to grow our business, acquire needed assets, or take other actions we might otherwise consider appropriate or desirable.

In addition, the certificate of designation for our Series C Preferred Stock requires us to redeem shares of our Series C Preferred Stock, at each holder’s option and for an amount greater than their stated value, upon the occurrence of certain events, including our being subject to a judgment of greater than $100,000 or our initiation of bankruptcy proceedings.

The holders of our Series C Preferred Stock are entitled to receive a dividend, which may be increased if we do not comply with certain covenants.

The holders of the Series C Preferred Stock are entitled to a 9% annual dividend on the $1,000 per share stated value of our Series C Preferred Stock, which is payable in cash or, subject to the satisfaction of certain conditions, in pay-in-kind shares. The dividend may be increased to a 18% annual dividend if we fail to comply with certain covenants, including our being subject to a judgment of greater than $100,000 or our initiation of bankruptcy proceedings. As a result of the payment of dividends related to our Series C Preferred Stock, we may be obligated to pay significant sums of money or issue a significant number of shares of our common stock, which could negatively affect our operations or result in the dilution of the holders of our common stock, respectively.

Our Series C Preferred Stock and certain of our warrants contain anti-dilution provisions that may result in the reduction of their conversion prices or exercise prices in the future.

Our Series C Preferred Stock and certain of our warrants contain anti-dilution provisions, which provisions require the lowering of the conversion price or exercise price, as applicable, to the purchase price of future offerings. Furthermore, with respect to such warrants, if we complete an offering below the exercise price of such warrants, the number of shares issuable under such warrants will be proportionately increased such that the aggregate exercise price payable after taking into account the decrease in the exercise price, shall be equal to the aggregate exercise price prior to such adjustment. If in the future we issue securities for less than the conversion or exercise price of our Series C Preferred Stock and such warrants, respectively, we will be required to further reduce the relevant conversion or exercise prices, and the number of shares underlying such warrants will be increased. We may find it more difficult to raise additional equity capital while our Series C Preferred Stock and such warrants are outstanding.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains “forward-looking statements,” which include information relating to future events, future financial performance, strategies, expectations, competitive environment and regulation. Words such as “may,” “should,” “could,” “would,” “predict,” “potential,” “continue,” “expect,” “anticipate,” “future,” “intend,” “plan,” “believe,” “estimate,” and similar expressions, as well as statements in future tense, identify forward-looking statements. Forward-looking statements should not be read as a guarantee of the occurrence or the expected timing of future performance or results. Forward-looking statements are based on information we have when those statements are made or our management’s good faith belief as of that time with respect to future events, and are subject to risks and uncertainties that could cause actual performance or results to differ materially from those expressed in or suggested by the forward-looking statements. Important factors that could cause such differences include, but are not limited to:

| ● | inability to manufacture our product candidates on a commercial scale on our own, or in collaboration with third parties; |

| ● | difficulties in obtaining financing on commercially reasonable terms; |

| ● | changes in the size and nature of our competition; |

| ● | loss of one or more key executives or scientists; and |

| ● | difficulties in securing regulatory approval to market our product candidates. |

You should review carefully the section entitled “Risk Factors” beginning on page 3 of this prospectus for a discussion of these and other risks that relate to our business and investing in shares of our common stock. We undertake no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise.

All shares of our common stock offered by this prospectus are being registered for the accounts of the selling stockholders and we will not receive any proceeds from the sale of these shares. However, we will receive proceeds from the exercise price of the warrants if the warrants are exercised for cash. We intend to use those proceeds, if any, for general corporate purposes.

MARKET FOR COMMON EQUITY AND RELATED STOCKHOLDER MATTERS

Market Information

On October 29, 2014, our common stock commenced trading on OTCQB under the symbol “BSGM.” Prior to October 29, 2014, there was no established trading price for our common stock. The following table sets forth, for the periods indicated, the high and low sales prices per share of our common stock as reported by the OTCQB. The quotations reflect inter-dealer prices, without retail markup, markdown or commissions, and may not represent actual transactions.

| Fiscal Year 2016 | ||||||||

| High | Low | |||||||

| Second Quarter | $ | 2.15 | $ | 1.33 | ||||

| First Quarter | $ | 1.59 | $ | 0.90 | ||||

| Fiscal Year 2015 | ||||||||

| High | Low | |||||||

| Fourth Quarter | $ | 1.90 | $ | 1.08 | ||||

| Third Quarter | $ | 2.30 | $ | 1.13 | ||||

| Second Quarter | $ | 4.80 | $ | 2.00 | ||||

| First Quarter | $ | 2.85 | $ | 1.31 | ||||

| Fiscal Year 2014 | ||||||||

| High | Low | |||||||

| Fourth Quarter | $ | 3.50 | $ | 2.56 | ||||

| Third Quarter | $ | — | $ | — | ||||

| Second Quarter | $ | — | $ | — | ||||

| First Quarter | $ | — | $ | — | ||||

We have never paid cash dividends on our common stock and do not anticipate paying any cash dividends in the foreseeable future, but intend to retain our capital resources for reinvestment in our business. In addition, the terms of our Series C Preferred Stock prohibit us from paying dividends in the future on our common stock, absent consent from the holders representing a super-majority of the outstanding shares of our Series C Preferred Stock and a certain investor.

MANAGEMENT’S DISCUSSION AND ANALYSIS OF

FINANCIAL CONDITION AND RESULTS OF OPERATIONS

You should read the following discussion and analysis of our financial condition and results of operations in conjunction with our financial statements and the related notes thereto that are included in this prospectus. In addition to historical information, the following discussion and analysis includes forward-looking statements that reflect our plans, estimates and beliefs. Our actual results could differ materially from those discussed in the forward-looking statements. Factors that could cause or contribute to these differences include those discussed below and elsewhere in this prospectus, particularly in the section entitled “Risk Factors.” See “Special Note Regarding Forward-Looking Statements.”

Our Business

We are a development stage medical device company that is developing a proprietary technology platform to minimize noise and artifacts from cardiac recordings during electrophysiology studies and ablation. Our product under development, the PURE EP System, is a surface electrocardiogram and intracardiac multichannel recording and analysis system that acquires, processes and displays electrocardiogram and electrograms required during electrophysiology studies and ablation procedures.

We have not generated any revenue to date and consequently our operations are subject to all risks inherent in the establishment of a new business enterprise.

Critical Accounting Policies and Estimates

The following discussion and analysis of our financial condition and results of operations are based upon our financial statements, which have been prepared in accordance with generally accepted accounting principles in the U.S. The preparation of financial statements in accordance with generally accepted accounting principles in the U.S. requires us to make estimates and assumptions that affect the amounts reported in our financial statements. The financial statements include estimates based on currently available information and our judgment as to the outcome of future conditions and circumstances. Significant estimates in these financial statements include allowance for doubtful accounts and accruals for inventory claims. Changes in the status of certain facts or circumstances could result in material changes to the estimates used in the preparation of the financial statements and actual results could differ from the estimates and assumptions.