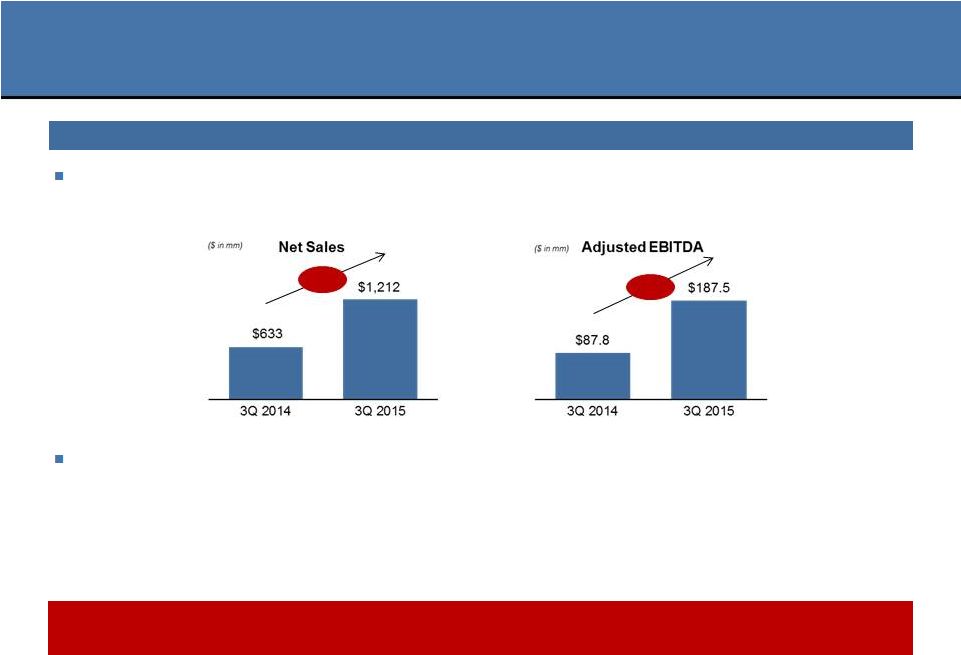

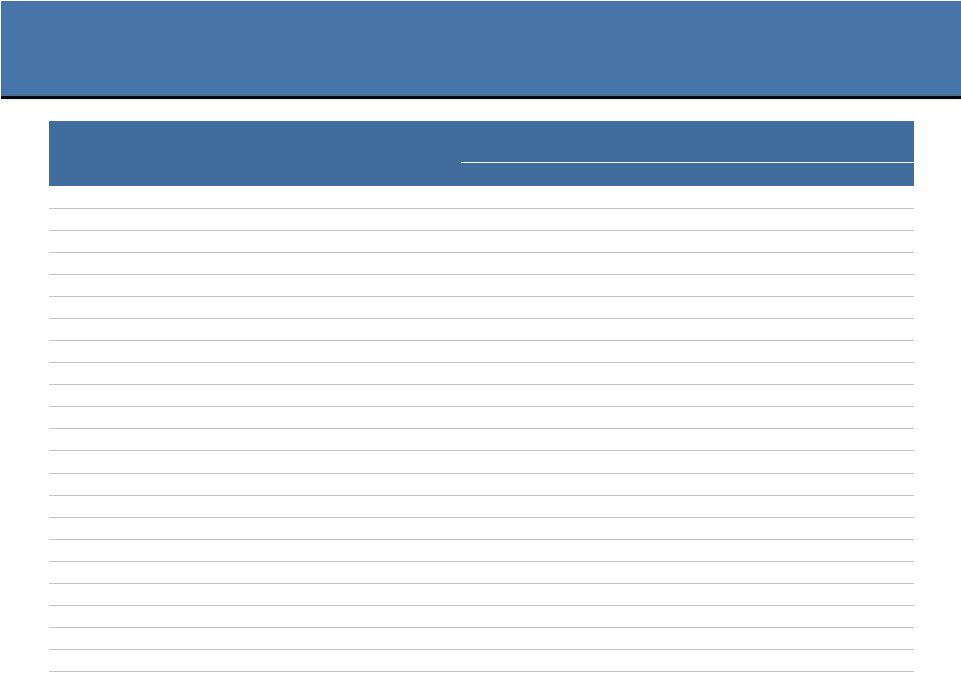

Key Cash Flow Characteristics 1 2 3 4 Recurring revenue stream supported by strong or growing market positions or attractive category trends Attractive Adjusted EBITDA margins Limited capex needs Modest working capital requirements M&A tax efficiency where possible (1) Please see the Appendix for a full reconciliation. (2) Adjustment gives effect to the acquisition of ABC, which was consummated effective November 1, 2014, as if such acquisition had occurred on July 1, 2014, by including management’s estimate of the Adjusted EBITDA of ABC for the period from July 1, 2014 through October 31, 2014. (3) Adjustment gives effect to the acquisition of MOM Brands, which was consummated effective May 4, 2015, as if such acquisition had occurred on July 1, 2014, by including management’s estimate of the Adjusted EBITDA of MOM Brands for the period from June 29, 2014 through May 3, 2015. (4) In connection with the acquisition of MOM Brands, the Company expects to recognize $50mm in run-rate synergies by the second full fiscal year following the closing of the acquisition (excluding one-time costs to achieve). (5) Pro Forma for expected interest on debt issued in the Transaction. (6) Based on current Post shares outstanding of 54.9mm plus $275mm of common equity expected to be issued in conjunction with the Transaction. Assumes new common equity issued to the public is based on a share price as of August 7, 2015, for illustrative purposes. Illustrative Free Cash Flow (“FCF”) Calculation 5 Bank cash balance as of 7/31/2015: ~$385mm Post LTM 6/30/2015 Adjusted EBITDA $602 Acquired American Blanching Adjusted EBITDA 6 Acquired MOM Brands Adjusted EBITDA 96 Run-rate MOM Brands Synergies 50 PF LTM 6/30/2015 Adjusted EBITDA $754 Less: Cash Interest (302) Less: Maintenance Capital Expenditures (100) Less: Cash Taxes (90) FCF to All Shareholders $262 Less: Dividends on Convertible Preferred Securities (17) FCF to Common Shareholders $245 FCF to Common Shareholders per Share $4.11 ($ in mm) (1) (3) (2) (4) (5) (6) Business Model Focused on Strong Cash Generation |