Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

SCHEDULE 14A

(Rule 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

Filed by the Registrant x Filed by a Party other than the Registrant ¨

Check the appropriate box:

x PreliminaryProxy Statement | ||

¨ Confidential,For Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | ||

¨ DefinitiveProxy Statement | ||

| ¨ Definitive Additional Materials | ||

| ¨ Soliciting Material Pursuant to § 240.14a-12 | ||

ROI ACQUISITION CORP.

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if Other Than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| ¨ | No fee required. |

| x | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

| (1) | Title of each class of securities to which transaction applies: |

| Not applicable. |

| (2) | Aggregate number of securities to which transaction applies: |

| Not applicable. |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

| Not applicable. |

| (4) | Proposed maximum aggregate value of transaction: |

| $249,460,000(1) |

| (5) | Total fee paid: |

| $34,026.34(2) |

| ¨ | Fee paid previously with preliminary materials. |

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the form or schedule and the date of its filing. |

| (1) | Amount previously paid: |

| (2) | Form, Schedule or Registration Statement No.: |

| (3) | Filing Party: |

| (4) | Date Filed: |

| 1 | Our estimate of the transaction value is based on the following estimated values: (i) $107.5 million in cash, (ii) 13,940,000 shares of ROI common stock valued at $10 per share and (iii) options to purchase shares of ROI common stock with an estimated intrinsic value of $2,560,000. |

| 2 | The amount is the product of $249,460,000 multiplied by the SEC’s filing fee of $136.40 per million. |

Table of Contents

ROI ACQUISITION CORP.

601 Lexington Avenue, 51st Fl.

New York, NY 10022

Dear ROI Acquisition Corp. Stockholders and Public Warrantholders:

You are cordially invited to attend the special meeting in lieu of the 2013 annual meeting of stockholders and/or the special meeting of public warrantholders of ROI Acquisition Corp., which we refer to as “we,” “us,” “our,” “ROI” or the “Company,” on [·], 2013, at 10:00 a.m., Eastern time, and 10:30 a.m., Eastern time, respectively, at the offices of McDermott Will & Emery LLP, 340 Madison Avenue, New York, New York.

At the special meeting of stockholders, our stockholders will be asked to consider and vote upon a proposal, which we refer to as the “Business Combination Proposal,” to approve a business combination agreement and plan of merger (the “Merger Agreement”) providing for the acquisition by us of EveryWare Global, Inc., which we refer to as “EveryWare,” and which acquisition we refer to as the “EveryWare Merger” or the “Business Combination.” Pursuant to the Merger Agreement, the aggregate consideration to be paid to EveryWare stockholders will consist of (i) $107.5 million in cash (the “Cash Merger Consideration”) and (ii) 10,440,000 shares of ROI Common Stock (“Stock Merger Consideration”), subject to adjustment in accordance with the terms of the Merger Agreement if the aggregate amount of cash available to pay the Cash Merger Consideration is less than $107.5 million. If the amount of the Cash Merger Consideration is less than $107.5 million but at least $90.0 million, ROI may issue additional shares of ROI Common Stock in an amount equal to the cash shortfall, with each share of ROI Common Stock valued at $10.00. If the amount of the Cash Merger Consideration is less than $90.0 million, EveryWare may terminate the Merger Agreement or, at its option, if the Cash Merger Consideration is at least $55.0 million, elect to receive additional shares of ROI Common Stock in an amount equal to the cash shortfall from $107.5 million, with each share of ROI Common Stock valued at $10.00. In addition, EveryWare’s existing stockholders will receive an aggregate of 3,500,000 additional shares of ROI Common Stock (the “Earnout Shares”) that will be subject to forfeiture in the event that the trading price of ROI’s Common Stock does not exceed certain price targets subsequent to the closing of the Business Combination. A copy of the Merger Agreement is attached to the accompanying proxy statement as Annex A.

It is anticipated that, upon completion of the Business Combination, ROI’s existing stockholders, including our Sponsor, will retain an ownership interest of approximately 39.7% of the post-merger company, which we refer to as “EveryWare Global, Inc.,” and the former equity holders of EveryWare will own approximately 60.3% of the outstanding common stock of the post-merger company. These percentages are calculated based on a number of assumptions and are subject to adjustment in accordance with the terms of the merger agreement. These relative percentages assume that: (a) the aggregate amount of cash available to pay the Cash Merger Consideration is $107.5 million and ROI receives $250.0 million in cash proceeds from the proposed issuance of senior secured notes in order to fund the Cash Merger Consideration and refinance EveryWare’s existing debt; and (b) that no more than 26.3% of the ROI stockholders exercise their redemption rights. If the actual facts are different than these assumptions, the percentage ownership retained by ROI’s existing stockholders will be different. These percentages also do not take into account (i) the 3,500,000 Earnout Shares and 551,471 shares of outstanding ROI common stock currently held by our Sponsor, that in each case are subject to forfeiture if certain performance conditions relating to the trading price of ROI’s Common Stock are not met following the Business Combination, (ii) options to purchase shares of ROI common stock that will be issued to former holders of EveryWare stock options in connection with the Business Combination and (iii) warrants to purchase ROI’s common stock that will remain outstanding following the Business Combination. You should read “Summary—ROIShares to be Issued in the Business Combination” and “Unaudited Pro Forma Condensed Combined Financial Information” for further information.

Table of Contents

Our stockholders will also be asked to consider and vote upon proposals (a) to approve and adopt our third amended and restated certificate of incorporation, a copy of which is attached as Annex B to the accompanying proxy statement, which we refer to as the “Certificate Proposal,” (b) to elect three directors to serve on our board of directors, subject to the closing of the Business Combination, which we refer to as the “Director Election Proposal,” and (c) to approve and adopt the EveryWare Global, Inc. 2013 Omnibus Incentive Plan (an equity-based incentive plan), a copy of which is attached to the accompanying proxy statement as Annex C, which we refer to as the “Incentive Plan Proposal.”

At the special meeting of public warrantholders, our public warrantholders will be asked to consider and vote on a proposal, which we refer to as the “Warrant Amendment Proposal,” to approve and consent to an amendment to the terms of the warrant agreement governing ROI’s outstanding warrants to remove a provision that provides for a reduction of the warrant exercise price upon the occurrence of certain transactions following the Business Combination in which the consideration to be received by our stockholders includes equity securities that are not listed for trading on a national securities exchange or on the OTC Bulletin Board, or are not to be so listed for trading immediately following such event.

Each of these proposals is more fully described in the accompanying proxy statement.

Our common stock, units and warrants are currently listed on The NASDAQ Stock Market under the symbols “ROIQ,” “ROIQU” and “ROIQW,” respectively. We have applied to continue the listing of our common stock on The NASDAQ Stock Market under the symbol “EVRY” upon the closing of the Business Combination. Following the closing, we expect that our warrants will trade on the OTC market under the symbol “EVRYW.” At the closing, our units will separate into their component shares of common stock and warrants to purchase one share of our common stock.

Pursuant to our second amended and restated certificate of incorporation, we are providing our public stockholders with the opportunity to redeem their shares of our common stock for cash equal to their pro rata share of the aggregate amount on deposit in the trust account which holds the proceeds of our initial public offering as of two business days prior to the consummation of the Business Combination, less franchise and income taxes payable, upon the consummation of the Business Combination. For illustrative purposes, based on funds in the trust account of approximately $75.1 million on December 31, 2012, the estimated per share redemption price would have been approximately $10.00.Public stockholders may elect to redeem their shares even if they vote for the Business Combination Proposal. A public stockholder, together with any of his, her or its affiliates or any other person with whom it is acting in concert or as a “group” (as defined under Section 13 of the Securities Exchange Act of 1934, as amended), will be restricted from redeeming his, her or its shares with respect to more than an aggregate of 10% of the public shares. Holders of our outstanding public warrants do not have redemption rights in connection with the Business Combination. The holders of ROI shares issued prior to our initial public offering, which we refer to as “founder shares,” have agreed to waive their redemption rights with respect to their founder shares and any other shares they may hold in connection with the consummation of the Business Combination, and the founder shares will be excluded from the pro rata calculation used to determine the per-share redemption price. Currently, Clinton Magnolia Master Fund, Ltd., which we refer to as our “Sponsor,” owns approximately 20.0% of our issued and outstanding shares of common stock, consisting of all of the founder shares.

We are providing this proxy statement and accompanying proxy card to our stockholders and public warrantholders in connection with the solicitation of proxies to be voted at the special meetings and at any adjournments or postponements of the special meetings.Whether or not you plan to attend the applicable special meeting(s), we urge you to read this proxy statement (and any documents incorporated into this proxy statement by reference) carefully. Please pay particular attention to the section entitled “Risk Factors.”

Table of Contents

Our board of directors has unanimously approved and adopted the Merger Agreement and unanimously recommends that (i) our stockholders vote FOR all of the proposals presented to our stockholders and (ii) our public warrantholders vote FOR all of the proposals presented to our public warrantholders. When you consider the board recommendation of these proposals, you should keep in mind that our directors and officers have interests in the Business Combination that may conflict with your interests as a stockholder or public warrantholder, as applicable. See the section entitled“Proposal No. 1—Approval of the Business Combination—Certain Benefits of ROI’s Directors and Officers and Others in the Business Combination.”

Approval of the Business Combination Proposal and Incentive Plan Proposal requires the affirmative vote of holders of a majority of the shares of our common stock that are voted at the special meeting of stockholders. Approval of the Certificate Proposal requires the affirmative vote of holders of a majority of our outstanding shares of common stock. Approval of the Director Election Proposal requires the affirmative vote of the holders of a plurality of the shares of our common stock represented in person or by proxy and entitled to vote thereon at the special meeting of stockholders. Approval of the Adjournment Proposal requires the affirmative vote of the holders of a majority of the shares of our common stock represented in person or by proxy and entitled to vote thereon at the special meeting of stockholders. The board of directors and shareholders of EveryWare have already approved the EveryWare Merger.

Approval of the Warrant Amendment Proposal requires approval by registered public warrantholders holding at least 65% of the outstanding public warrants. Regardless of whether the Business Combination is consummated, the amendment to the warrant agreement will become effective if warrantholders have approved the Warrant Amendment Proposal. Approval of the Warrantholder Adjournment Proposal requires the affirmative vote of a majority of the public warrants as of the record date represented in person or by proxy at the special meeting of warrantholders, and entitled to vote thereon.

We have no specified maximum redemption threshold under our charter. It is a condition to closing under the Merger Agreement, however, that we provide Cash Merger Consideration of at least $90.0 million to EveryWare’s stockholders. Each redemption of public shares by our public stockholders will decrease the amount in our trust account and increase the number of additional shares of ROI Common Stock we would need to issue as a result of the cash shortfall or the amount of cash we would need to obtain through acquisition financing. Therefore, in order to satisfy the condition to closing, the maximum redemption threshold is the amount that would allow us to maintain, in the aggregate, at least $90.0 million of available cash to pay the Cash Merger Consideration when aggregated with the proceeds of our acquisition financing. If, however, redemptions by our public stockholders cause us to be unable to provide EveryWare’s stockholders with at least $90.0 million in Cash Merger Consideration at the closing of the Business Combination when aggregated with the proceeds of our acquisition financing, then EveryWare may terminate the Merger Agreement or, at its option, if the Cash Merger Consideration is at least $55 million, elect to receive additional shares of ROI Common Stock in an amount equal to the cash shortfall from $107.5 million. In no event, however, will we redeem public shares in an amount that would cause our net tangible assets to be less than $5,000,001.

Clinton Magnolia Master Fund, Ltd., managed by Clinton Group, Inc., is our Sponsor and owner of our founder shares. Founded in 1991, Clinton Group, Inc. is a SEC registered investment advisor that serves as investment manager for private investment funds and hedge fund products that are invested globally across multiple alternative investment strategies. Clinton Magnolia Master Fund, Ltd. has agreed to vote the founder shares and any shares of common stock acquired during or after our initial public offering in favor of the Business Combination Proposal. In addition, I have agreed to vote my shares in favor of the Business Combination Proposal. Pursuant to the terms of the warrant agreement, our Sponsor is not permitted to vote the sponsor warrants in favor of the Warrant Amendment Proposal unless the

Table of Contents

registered holders of 65% of the public warrants vote in favor of the Warrant Amendment Proposal. Although permitted under our second amended and restated certificate of incorporation, we will not, prior to consummation of the Business Combination, release amounts from the trust account to purchase in the open market shares of common stock sold in our initial public offering.

Your vote is very important. If you are a registered stockholder or public warrantholder, please vote your shares or warrants, as applicable, as soon as possible using one of the following methods to ensure that your vote is counted, regardless of whether you expect to attend the applicable special meeting(s) in person: (1) call the toll-free number specified on the enclosed proxy card and follow the instructions when prompted, (2) access the Internet website specified on the enclosed proxy card and follow the instructions provided to you, or (3) complete, sign, date and return the enclosed proxy card in the postage-paid envelope provided. If you hold your shares or warrants in “street name” through a bank, broker or other nominee, you will need to follow the instructions provided to you by your bank, broker or other nominee to ensure that your shares or warrants, as applicable, are represented and voted at the applicable special meeting(s). A failure to vote your shares is the equivalent of a vote “AGAINST” the Certificate Proposal but will have no effect on the other proposals for the special meeting of stockholders. A failure to vote your warrants is the equivalent of a vote “AGAINST” the Warrant Amendment Proposal.

If you sign, date and return your proxy card without indicating how you wish to vote, your proxy will be voted in favor of each of the proposals presented at the special meetings. With respect to the proposals for the special meeting of stockholders, if you fail to return your proxy card or fail to submit your proxy by telephone or over the Internet, or fail to instruct your bank, broker or other nominee how to vote, and do not attend the special meeting in person, the effect will be that your shares will not be counted for purposes of determining whether a quorum is present at the special meeting of stockholders and, if a quorum is present, will have the same effect as a vote against the Certificate Proposal but will have no effect on the other proposals. With respect to the proposals for the special meeting of public warrantholders, if you fail to return your proxy card or fail to submit your proxy by telephone or over the Internet, or fail to instruct your bank, broker or other nominee how to vote, and do not attend the special meeting in person, the effect will be that your warrants will have the same effect as a vote against the Warrant Amendment Proposal. If you are a stockholder or public warrantholder of record and you attend the applicable special meeting(s) and wish to vote in person, you may withdraw your proxy and vote in person.

On behalf of our board of directors, I thank you for your support and look forward to the successful completion of the Business Combination.

| [·], 2013 | Sincerely, | |

Thomas J. Baldwin Chairman and Chief Executive Officer | ||

This proxy statement is dated [·], 2013, and is first being mailed to stockholders and public warrantholders of the Company on or about [·], 2013.

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES REGULATORY AGENCY HAS APPROVED OR DISAPPROVED THE TRANSACTIONS DESCRIBED IN THIS PROXY STATEMENT OR ANY OF THE SECURITIES TO BE ISSUED IN THE BUSINESS COMBINATION, PASSED UPON THE MERITS OR FAIRNESS OF THE BUSINESS COMBINATION OR RELATED TRANSACTIONS OR PASSED UPON THE ADEQUACY OR ACCURACY OF THE DISCLOSURE IN THIS PROXY STATEMENT. ANY REPRESENTATION TO THE CONTRARY CONSTITUTES A CRIMINAL OFFENSE.

Table of Contents

ROI ACQUISITION CORP.

601 Lexington Avenue, 51st Fl.

New York, NY 10022

NOTICE OF SPECIAL MEETING IN LIEU OF 2013 ANNUAL MEETING

OF STOCKHOLDERS OF ROI ACQUISITION CORP.

To Be Held On [·], 2013

To the Stockholders of ROI Acquisition Corp.:

NOTICE IS HEREBY GIVEN that a special meeting in lieu of the 2013 annual meeting of stockholders (the “special meeting”) of ROI Acquisition Corp., a Delaware corporation (“ROI” or the “Company”), will be held at 10:00 a.m., Eastern time, on [·], 2013, at the offices of McDermott Will & Emery LLP, 340 Madison Avenue, New York, New York. You are cordially invited to attend the special meeting for the following purposes:

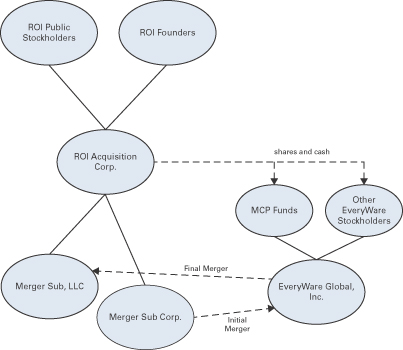

(1)The Business Combination Proposal—to consider and vote upon a proposal (i) to approve and adopt the Business Combination Agreement and Plan of Merger, dated as of January 31, 2013, as it may be amended (the “Merger Agreement”), by and among the Company, ROI Merger Sub Corp., a Delaware corporation (“Merger Sub Corp.”), ROI Merger Sub LLC, a Delaware limited liability company (“Merger Sub LLC” and, together with Merger Sub Corp., the “Merger Subs” and each, a “Merger Sub”), and EveryWare Global, Inc., a Delaware corporation (“EveryWare”), and the transactions contemplated thereby (the “Business Combination Proposal”);

(2)The Certificate Proposal—to consider and vote upon a proposal to approve our third amended and restated certificate of incorporation to, among other things:

| • | change our name to EveryWare Global, Inc.; |

| • | remove certain provisions related to our status as a blank check company; and |

| • | make certain other changes that our board of directors deems appropriate for a public operating company (this proposal is referred to herein as the “Certificate Proposal”). |

(3)The Director Election Proposal—to consider and vote upon a proposal to elect three directors to serve on ROI’s board of directors upon consummation of the Business Combination (the “Director Election Proposal”);

(4)The Incentive Plan Proposal—to consider and vote upon a proposal to approve and adopt the EveryWare Global, Inc. 2013 Omnibus Incentive Plan (the “Incentive Plan Proposal”);

(5)The Adjournment Proposal—to consider and vote upon a proposal to adjourn the special meeting to a later date or dates, if necessary, to permit further solicitation and vote of proxies if, based upon the tabulated vote at the time of the special meeting, there are not sufficient votes to approve one or more proposals presented to stockholders for vote (the “Adjournment Proposal”); and

(6) to consider and transact such other procedural matters as may properly come before the special meeting or any adjournment or postponement thereof.

Only holders of record of our common stock at the close of business on [·], 2013 are entitled to notice of the special meeting of stockholders and to vote at the special meeting and any adjournments or postponements of the special meeting. A complete list of our stockholders of record entitled to vote at the special meeting will be available for ten days before the special meeting at our principal executive offices for inspection by stockholders during ordinary business hours for any purpose germane to the special meeting.

Table of Contents

ROI is also holding a special meeting of its public warrantholders where our public warrantholders will be asked to consider and vote on a proposal, which we refer to as the “Warrant Amendment Proposal,” to approve and consent to an amendment to the terms of the warrant agreement governing ROI’s outstanding warrants to remove a provision which provides for a reduction of the warrant exercise price upon the occurrence of certain transactions following the Business Combination in which the consideration to be received by our stockholders includes equity securities which are not listed for trading on a national securities exchange or on the OTC Bulletin Board, or are not to be so listed for trading immediately following such event.

Pursuant to our second amended and restated certificate of incorporation, we will provide our public stockholders with the opportunity to redeem their shares of our common stock for cash equal to their pro rata share of the aggregate amount on deposit in the trust account which holds the proceeds of our initial public offering as of two business days prior to the consummation of the transactions contemplated by the Merger Agreement, less franchise and income taxes payable, upon the closing of the transactions contemplated by the Merger Agreement. For illustrative purposes, based on funds in the trust account of approximately $75.1 million on December 31, 2012, the estimated per share redemption price would have been approximately $10.00.Public stockholders may elect to redeem their shares even if they vote for the Business Combination Proposal. A public stockholder, together with any of his, her or its affiliates or any other person with whom it is acting in concert or as a “group” (as defined under Section 13 of the Securities Exchange Act of 1934, as amended), will be restricted from redeeming his, her or its shares with respect to more than an aggregate of 10% of the public shares. The holders of our shares issued prior to our initial public offering (“founder shares”) have agreed to waive their redemption rights with respect to their founder shares and any other shares they may hold in connection with the consummation of the Business Combination, and the founder shares will be excluded from the pro rata calculation used to determine the per-share redemption price. Currently, Clinton Magnolia Master Fund, Ltd., our Sponsor, owns approximately 20.0% of our issued and outstanding shares of common stock, consisting of all of the founder shares.

The transactions contemplated by the Merger Agreement will be consummated only if a majority of the outstanding shares of common stock of the Company that are voted at the special meeting of the stockholders are voted in favor of the Business Combination Proposal and the Certificate Proposal and the Director Election Proposal are approved. We have no specified maximum redemption threshold under our charter. It is a condition to closing under the Merger Agreement, however, that we provide cash consideration of at least $90.0 million to EveryWare’s stockholders. Each redemption of public shares by our public stockholders will decrease the amount in our trust account and increase the number of additional shares of ROI Common Stock we would need to issue as a result of the cash shortfall or the amount of cash we would need to obtain through acquisition financing. Therefore, in order to satisfy the condition to closing, the maximum redemption threshold is the amount that would allow us to maintain, in the aggregate, at least $90.0 million of available cash to pay the Cash Merger Consideration when aggregated with the proceeds of our acquisition financing. If, however, redemptions by our public stockholders cause us to be unable to provide EveryWare’s stockholders with at least $90.0 million in cash consideration at the closing of the Business Combination when aggregated with the proceeds of our acquisition financing, then EveryWare, may terminate the Merger Agreement or, at its option, if the Cash Merger Consideration is at least $55.0 million, elect to receive additional shares of ROI Common Stock equal to the cash shortfall from $107.5 million. In no event, however, will we redeem public shares in an amount that would cause our net tangible assets to be less than $5,000,001.

Table of Contents

Your attention is directed to the proxy statement accompanying this notice (including the annexes thereto) for a more complete description of the proposed Business Combination and related transactions and each of our proposals. We encourage you to read this proxy statement carefully. If you have any questions or need assistance voting your shares, please call our proxy solicitor, Okapi Partners LLC, at (877) 274-8654 (toll free) or (212) 297-0720.

| By Order of the Board of Directors, | ||

| [·], 2013 | ||

| Daniel A. Strauss | ||

| Secretary | ||

Table of Contents

ROI ACQUISITION CORP.

601 Lexington Avenue, 51st Fl.

New York, NY 10022

NOTICE OF SPECIAL MEETING OF WARRANTHOLDERS

OF ROI ACQUISITION CORP.

To Be Held On [·], 2013

To the Public Warrantholders of ROI Acquisition Corp.:

NOTICE IS HEREBY GIVEN that a special meeting of public warrantholders (the “special meeting”) of ROI Acquisition Corp., a Delaware corporation (“ROI” or the “Company”), owning warrants originally issued in the Company’s initial public offering, will be held at 10:30 a.m., Eastern time, on [·], 2013, at the offices of McDermott Will & Emery LLP, 340 Madison Avenue, New York, New York. You are cordially invited to attend the special meeting for the following purposes:

(1)The Warrant Amendment Proposal—to consider and vote upon an amendment (the “Warrant Amendment”) to the warrant agreement (the “Warrant Agreement”) that governs all of the ROI warrants to remove a provision that provides for a reduction of the warrant exercise price upon the occurrence of certain transactions following the Business Combination in which the consideration to be received by our stockholders includes equity securities that are not listed for trading on a national securities exchange or on the OTC Bulletin Board, or are not to be so listed for trading immediately following such event.

(2)The Warrantholder Adjournment Proposal—to consider and vote upon a proposal to adjourn the special meeting of public warrantholders to a later date or dates, if necessary, to permit further solicitation and vote of proxies if, based upon the tabulated vote at the time of the special meeting of public warrantholders, there are not sufficient votes to approve the Warrant Amendment Proposal (the “Warrantholder Adjournment Proposal”); and

(3) to consider and transact such other procedural matters as may properly come before the special meeting of public warrantholders or any adjournment or postponement thereof.

Only holders of record of our public warrants at the close of business on [·], 2013 are entitled to notice of the special meeting of public warrantholders and to vote at the special meeting of public warrantholders and any adjournments or postponements of the special meeting of public warrantholders. A complete list of our public warrantholders of record entitled to vote at the special meeting of public warrantholders will be available for ten days before the special meeting of public warrantholders at our principal executive offices for inspection by warrantholders during ordinary business hours for any purpose germane to the special meeting.

ROI is also holding a special meeting of stockholders to consider and vote upon proposals (a) to approve a business combination agreement and plan of merger providing for the acquisition by us of EveryWare Global, Inc., which we refer to as the Business Combination Proposal, (b) to approve and adopt our third amended and restated certificate of incorporation, a copy of which is attached as Annex B to the accompanying proxy statement, which we refer to as the “Certificate Proposal,” (c) to elect three directors to serve on our board of directors, subject to the closing of the Business Combination, which we refer to as the “Director Election Proposal,” and (d) to approve and adopt the EveryWare Global, Inc. 2013 Omnibus Incentive Plan (an equity-based incentive plan), a copy of which is attached to the accompanying proxy statement as Annex C, which we refer to as the “Incentive Plan Proposal.”

The transactions contemplated by the Merger Agreement will be consummated only if a majority of the outstanding shares of common stock of the Company voted at the Special

Table of Contents

Meeting are voted in favor of the Business Combination Proposal and if the Certificate Proposal and the Director Election Proposal are approved.

Your vote is very important. If you are a public warrantholder, please vote as soon as possible using one of the following methods to ensure that your vote is counted, regardless of whether you expect to attend the special meeting of public warrantholders in person: (1) call the toll-free number specified on the enclosed proxy card and follow the instructions when prompted, (2) access the Internet website specified on the enclosed proxy card and follow the instructions provided to you, or (3) complete, sign, date and return the enclosed proxy card in the postage-paid envelope provided. If you hold your public warrants in “street name” through a bank, broker or other nominee, you will need to follow the instructions provided to you by your bank, broker or other nominee to ensure that your warrants are represented and voted at the special meeting of public warrantholders.

If you sign, date and return your proxy card without indicating how you wish to vote, your proxy will be voted in favor of each of the proposals presented at the special meeting of public warrantholders. If you fail to return your proxy card or fail to submit your proxy by telephone or over the Internet, or fail to instruct your bank, broker or other nominee how to vote, and do not attend the special meeting of public warrantholders in person, the effect will be that your warrants will have the same effect as a vote against the Warrant Amendment Proposal. If you are a public warrantholder of record and you attend the special meeting of public warrantholders and wish to vote in person, you may withdraw your proxy and vote in person.

On behalf of our board of directors, I thank you for your participation and look forward to your continued support.

| Sincerely, | ||

| [·], 2013 | ||

| Thomas J. Baldwin | ||

| Chairman and Chief Executive Officer | ||

Table of Contents

Table of Contents

| 144 | ||||

| 144 | ||||

| 144 | ||||

| 144 | ||||

| 145 | ||||

| 145 | ||||

Certain Effects of the Approval of the Warrant Amendment Proposal | 145 | |||

| 145 | ||||

| 145 | ||||

| 146 | ||||

Consequences if the Warrantholder Adjournment Proposal is Not Approved | 146 | |||

| 146 | ||||

| 146 | ||||

| 147 | ||||

ROI MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 157 | |||

| 161 | ||||

| 175 | ||||

EVERYWARE MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 187 | |||

| 208 | ||||

| 215 | ||||

| 226 | ||||

| 229 | ||||

| 233 | ||||

| 235 | ||||

| 235 | ||||

| 235 | ||||

| 235 | ||||

| 235 | ||||

| 236 | ||||

| 236 | ||||

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS | 238 | |||

ANNEXES | ||||

| A-1 | ||||

Annex B—Third Amended and Restated Certificate of Incorporation of EveryWare Global, Inc. | B-1 | |||

| C-1 | ||||

| D-1 |

| * | The schedules and exhibits to the Business Combination Agreement and Plan of Merger have been omitted pursuant to Item 601(b)(2) of Regulation S-K. ROI hereby agrees to furnish supplementally a copy of any omitted schedules or exhibits to the staff of the SEC upon request. |

Table of Contents

This Summary Term Sheet, together with the sections entitled “Questions and Answers About the Proposals for Stockholdersand Public Warrantholders” and “Summary of the Proxy Statement,” summarize certain information contained in this proxy statement, but do not contain all of the information that is important to you. You should read carefully this entire proxy statement, including the attached Annexes, for a more complete understanding of the matters to be considered at the special meeting.

| • | ROI is a special purpose acquisition company formed for the purpose of effecting a merger, capital stock exchange, asset acquisition, stock purchase, reorganization or similar business combination with one or more businesses. There currently are 9,385,000 shares of ROI’s common stock issued and outstanding, consisting of 7,500,000 shares originally sold as part of units in ROI’s initial public offering, 1,875,000 founder shares that were issued to an affiliate of our Sponsor prior to ROI’s initial public offering (which founder shares were subsequently transferred to Clinton Magnolia Master Fund, Ltd. (our “Sponsor”)) and 10,000 shares originally sold as part of units issued simultaneously with our initial public offering to Mr. Baldwin. In addition, there currently are 11,676,667 warrants of ROI outstanding, consisting of 7,500,000 warrants originally sold as part of units in ROI’s initial public offering, 4,166,667 sponsor warrants that were sold by ROI to an affiliate of our Sponsor in a private sale simultaneously with ROI’s initial public offering (which sponsor warrants were subsequently transferred to our Sponsor) and 10,000 sponsor warrants originally sold as part of units issued simultaneously with our initial public offering to Mr. Baldwin. Each warrant entitles its holder to purchase one share of ROI’s common stock at an exercise price of $12.00 per share. The warrants will become exercisable 30 days after the completion of ROI’s initial Business Combination, and expire at 5:00 p.m., New York time, five years after the completion of ROI’s initial Business Combination or earlier upon redemption or liquidation. Once the warrants become exercisable, ROI may redeem the outstanding warrants at a price of $0.01 per warrant, if the last sale price of ROI’s common stock equals or exceeds $18.00 per share for any 20 trading days within a 30 trading day period. The sponsor warrants, however, are non-redeemable so long as they are held by our Sponsor or its permitted transferees. For more information about ROI and its securities, see the sections entitled “Information About ROI,” “ROI Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Description of Securities” beginning on pages 147, 157 and 215, respectively. |

| • | EveryWare is a leading global marketer of tabletop and food preparation products for the consumer and foodservice markets. EveryWare offers a comprehensive line of tabletop and food preparation products, such as bakeware, beverageware, serveware, storageware, flatware, dinnerware, crystal, buffetware and hollowware; premium spirit bottles; cookware; gadgets; candle and floral glass containers; and other kitchen products. EveryWare markets its products globally under the Anchor Hocking®, Anchor®, AnchorHome®, FireKing®, ONEIDA®, OneidaCraft®, Buffalo China®, Delco® and Sant’ Andrea® brands; in Europe and Australia under the Viners® brand; and in Latin America under the W.A. Rogers® brand. EveryWare’s customers range from Fortune 500 companies to medium and small-sized companies in the consumer, foodservice, business-to-business and e-commerce channels. EveryWare operates two glass manufacturing plants in the U.S. and sources a variety of tableware products from third parties, primarily in Asia and Europe. EveryWare was formed through the combination of Anchor and Oneida in March of 2012. For more information about EveryWare, see the sections entitled “Information About EveryWare,” “EveryWare Management’s Discussion and Analysis ofFinancial Condition and Results of Operations” and “Management After the Business Combination” beginning on pages 161, 187 and 208, respectively. |

1

Table of Contents

| • | Pursuant to a Business Combination Agreement and Plan of Merger, dated as of January 31, 2013, by and among ROI, ROI Merger Sub Corp., ROI Merger Sub LLC and EveryWare (the “Merger Agreement”), the Company proposes to acquire EveryWare through two consecutive mergers between wholly owned subsidiaries of the Company and EveryWare. A wholly owned subsidiary of the Company, which is a corporation, will merge with and into EveryWare, with EveryWare surviving the initial merger, which we refer to as the “Initial EveryWare Merger,” immediately followed by the merger of the surviving corporation with and into another wholly owned subsidiary of the Company, which is a limited liability company, with the wholly owned subsidiary of the Company as the surviving company of the final merger, which we refer to as the “Final EveryWare Merger.” All references to the “EveryWare Merger” or the “Business Combination” in this proxy statement include the Initial EveryWare Merger and the Final EveryWare Merger. For more information about the transactions contemplated by the Merger Agreement, which is referred to herein as the “Business Combination,” see the section entitled “Proposal No. 1—Approval of the Business Combination” beginning on page 85 and the copy of the Merger Agreement attached to this proxy statement as Annex A. |

| • | Pursuant to the Merger Agreement, upon the effectiveness of the Initial EveryWare Merger, each share of common stock of EveryWare will be exchanged for cash and validly issued shares of the Company’s common stock (the “Shares”). The aggregate consideration to EveryWare stockholders will consist of (i) $107.5 million in cash (the “Cash Merger Consideration”) and (ii) 10,440,000 shares of ROI Common Stock (“Stock Merger Consideration”), subject to adjustment in accordance with the terms of the Merger Agreement if the aggregate amount of cash available to pay the Cash Merger Consideration is less than $107.5 million. If the amount of the Cash Merger Consideration is less than $107.5 million but at least $90.0 million, ROI may issue additional shares of ROI Common Stock in an amount equal to the cash shortfall, with each share of ROI Common Stock valued at $10.00. If the amount of the Cash Merger Consideration is less than $90.0 million, EveryWare may terminate the Merger Agreement or, at its option, if the Cash Merger Consideration is at least $55.0 million, elect to receive additional shares of ROI Common Stock in an amount equal to the cash shortfall from the $107.5 million, with each share of ROI Common Stock valued at $10.00. In addition, EveryWare’s existing stockholders will receive an aggregate of 3,500,000 additional shares of ROI Common Stock (the “Earnout Shares”) that will be subject to forfeiture in the event that the trading price of ROI’s Common Stock does not exceed certain price targets subsequent to the closing of the Business Combination. For more information on the Shares, see the section entitled “Proposal No. 1—Approval of the Business Combination—Total ROI Shares to be Issued in the Business Combination” beginning on page 110. For more information about the Merger Agreement and related transaction agreements, see the section entitled “Proposal No. 1—Approval of the Business Combination—The Merger Agreement” beginning on page 85. |

| • | In connection with the stockholder vote to approve the proposed Business Combination, we may privately negotiate transactions to purchase shares after the closing of the Business Combination from stockholders who would have otherwise elected to have their shares redeemed in conjunction with a proxy solicitation pursuant to the proxy rules for a per-share pro rata portion of the trust account. The Sponsor, our directors, officers, or advisors or their respective affiliates may also purchase shares in privately negotiated transactions. Neither we nor our directors, officers or advisors or our or their respective affiliates will make any such purchases when we or they are in possession of any material non-public information not disclosed to the seller. Such a purchase would include a contractual acknowledgement that such stockholder, although still the record holder of our shares, is no longer the beneficial owner thereof and therefore agrees not |

2

Table of Contents

to exercise its redemption rights. In the event that we, the Sponsor, our directors, officers or advisors or our or their affiliates purchase shares in privately negotiated transactions from public stockholders who have already elected to exercise their redemption rights, such selling stockholders would be required to revoke their prior elections to redeem their shares. Any such privately negotiated purchases may be effected at purchase prices that are in excess of the per-share pro rata portion of the trust account. In the event that we are the buyer in such privately negotiated purchases, we could elect to use trust account proceeds to pay the purchase price in such transactions after the closing of the Business Combination. The purpose of such purchases would be to increase the likelihood of obtaining stockholder approval of the Business Combination. |

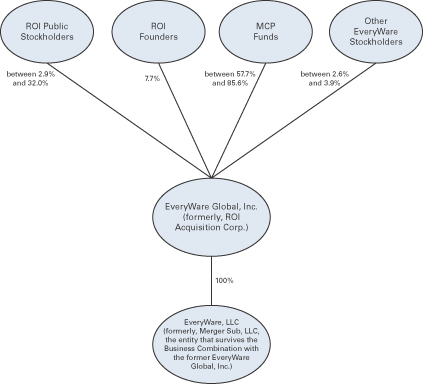

| • | It is anticipated that, upon effectiveness of the Initial EveryWare Merger, ROI’s existing stockholders will retain an ownership interest of between 10.5% and 39.7% of the post-merger company and the former equity holders of EveryWare will own between 89.5% and 60.3% of the post-merger company. These percentages are calculated based on a number of assumptions and are subject to adjustment in accordance with the terms of the Merger Agreement. These relative percentages assume that ROI receives $250.0 million in cash proceeds from the proposed issuance of senior secured notes in order to fund the Cash Merger Consideration and refinance EveryWare’s existing debt and are based upon net debt of EveryWare at December 31, 2012. If the actual facts are different than these assumptions, the percentage ownership retained by ROI’s existing stockholders will be different. These percentages also do not take into account (i) the additional 3,500,000 Earnout Shares and 551,471 shares of outstanding ROI common stock currently held by our Sponsor, that could in each case be subject to forfeiture in the future if certain performance conditions relating to the trading price of ROI’s Common Stock are not met following the Business Combination, (ii) options to purchase shares of ROI common stock that will be issued to former holders of EveryWare stock options in connection with the Business Combination and (iii) warrants to purchase ROI’s common stock that will remain outstanding following the Business Combination. |

The following table illustrates several hypothetical scenarios based on the assumptions described above but assuming varying levels of redemptions by ROI stockholders:

| Assumed % of ROI Shares Redeemed | ||||||||||||||||

| 0-26.3% | 50% | 75% | Maximum | |||||||||||||

ROI public stockholders | 32.0 | % | 21.7 | % | 10.9 | % | 2.9 | % | ||||||||

ROI founders | 7.7 | % | 7.7 | % | 7.7 | % | 7.7 | % | ||||||||

MCP Funds | 57.7 | % | 67.6 | % | 77.9 | % | 85.6 | % | ||||||||

Former EveryWare stockholders (other than the MCP Funds) | 2.6 | % | 3.1 | % | 3.6 | % | 3.9 | % | ||||||||

See “Summary—ROI Shares to be Issued in the Business Combination” and “Unaudited Pro Forma Condensed Combined Financial Information” for further information.

| • | Our management and board of directors considered various factors in determining whether to approve the Merger Agreement and the transactions contemplated thereby, and that the value of the Business Combination is equal to at least 80% of the balance in the trust account (excluding deferred underwriting discounts and commissions). They did not seek or receive any third party valuation of EveryWare. For more information about our decision-making process, see the section entitled “Proposal No. 1—Approval of the Business Combination—ROI’s Board of Directors’ Reasons for the Approval of the Business Combination” beginning on page 103. |

3

Table of Contents

| • | Pursuant to our second amended and restated certificate of incorporation, in connection with the Business Combination holders of our public shares may elect to have their shares redeemed for cash at the applicable redemption price per share calculated in accordance with our second amended and restated certificate of incorporation. As of December 31, 2012 this would have amounted to approximately $10.00 per share. If a holder exercises its redemption rights, then such holder will be exchanging its shares of our common stock for cash and will no longer own shares of the Company. Such a holder will be entitled to receive cash for its public shares only if it properly demands redemption and delivers its shares (either physically or electronically) to our transfer agent at least two business days prior to the special meeting of stockholders. See the section entitled “Special Meeting in Lieu of 2013 Annual Meeting of ROI Stockholders and Special Meeting of ROI Public Warrantholders—Redemption Rights” beginning on page 111 for the procedures to be followed if you wish to redeem your shares for cash. |

| • | In addition to voting on the proposal to approve and adopt the Merger Agreement at the special meeting of stockholders, the stockholders of ROI will be asked to vote on proposals to approve a third amended and restated certificate of incorporation for ROI, to elect three directors to the board of ROI, subject to the closing of the Business Combination, to adopt an equity incentive plan, and to adjourn the special meeting, if necessary, to permit further solicitation of proxies in the event that there are insufficient votes for, or otherwise in connection with, the approval of the Business Combination. See the sections entitled “Proposal No. 2—Approval of the Third Amended and Restated Certificate of Incorporation,” beginning on page 117, “Proposal No. 3—Election of Directors to the Board,” beginning on page 130, “Proposal No. 4—Approval and Adoption of the EveryWare Global, Inc. 2013 Omnibus Incentive Plan,” beginning on page 134, “Proposal No. 5—The Adjournment Proposal” beginning on page 144, and “Special Meeting in Lieu of 2013 Annual Meeting of ROI Stockholdersand Special Meeting of ROI Public Warrantholders” beginning on page 78. |

| • | In addition to the proposals to be voted upon by ROI stockholders at the special meeting of stockholders, ROI Warrantholders will be asked at the special meeting of warrantholders to vote on proposals to approve an amendment to the warrant agreement to remove a provision which provides for a reduction of the warrant exercise price upon the occurrence of certain transactions following the Business Combination in which the consideration to be received by our stockholders includes equity securities which are not listed for trading on a national securities exchange or on the OTC Bulletin Board, or are not to be so listed for trading immediately following such event, and to adjourn the special meeting, if necessary, to permit further solicitation of proxies in the event that there are insufficient votes for, or otherwise in connection with, the approval of the Warrant Amendment Proposal. See the sections entitled “The Warrant Amendment Proposal,” beginning on page 145, “The Warrantholder Adjournment Proposal” beginning on page 146 and“Special Meeting in Lieu of 2013 Annual Meeting of ROI Stockholders and Special Meeting of ROI Public Warrantholders” beginning on page 78. |

| • | Upon the closing of the Business Combination, our board of directors will consist of nine directors, three of whom will be voted upon by our stockholders at the special meeting. If all director nominees are elected and the Business Combination is consummated, our board will consist of five (5) directors designated by the MCP Funds, three (3) of our existing board members and one director who is the Chief Executive Officer and President of EveryWare. See the sections entitled “Proposal No. 3—Election ofDirectorsto the Board” and “Management After the Business Combination” on pages 130 and 208, respectively. |

4

Table of Contents

| • | The closing of the Business Combination is subject to a number of conditions set forth in the Merger Agreement including, among others, receipt of the requisite stockholder approval contemplated by this proxy statement. For more information about the closing conditions to the Business Combination, see the section entitled “Proposal No. 1—Approval of the Business Combination—The Merger Agreement” beginning on page 85. |

| • | The Merger Agreement may be terminated at any time prior to the consummation of the Business Combination in specified circumstances. For more information about the termination rights under the Merger Agreement, see the section entitled “Proposal No. 1—Approval of the Business Combination—The Merger Agreement” beginning on page 85. |

| • | The proposed Business Combination involves numerous risks. For more information about these risks, see the section entitled “Risk Factors” beginning on page 40. |

| • | In considering the recommendation of ROI’s board of directors to vote for the proposals presented at the special meeting of stockholders, you should be aware that our executive officers and members of our board of directors have interests in the Business Combination that are different from, or in addition to, the interests of our stockholders generally. The members of our board of directors were aware of these differing interests and considered them, among other matters, in evaluating and negotiating the transaction agreements and in recommending to our stockholders that they vote in favor of the proposals presented at the special meeting. These interests include, among other things: |

| • | the continued right of our Sponsor and our Chief Executive Officer to hold our common stock following the Business Combination, subject to the lock-up agreements; |

| • | the continued right of our Sponsor and our Chief Executive Officer to hold sponsor warrants to purchase shares of our common stock; |

| • | the continuation of certain of our officers and directors as directors (but not officers) of the Company; and |

| • | the continued indemnification of current directors and officers of the Company and the continuation of directors’ and officers’ liability insurance after the Business Combination. |

5

Table of Contents

Unless otherwise stated or unless the context otherwise requires, the terms “we,” “us,” “our,” the “Company” and “ROI” refer to ROI, and the terms “combined company” and “post-merger company” refer to ROI and EveryWare together following the consummation of the Business Combination.

In this document:

“Anchor” means Anchor Hocking, LLC and Anchor Hocking Canada, Inc.

“Anchor Holdings” means Anchor Holdings, Inc.

“Anchor Merger” means the merger of Anchor Holdings into EveryWare on March 23, 2012.

“Business Combination” and “EveryWare Merger” each mean the Initial EveryWare Merger and the Final EveryWare Merger pursuant to the Merger Agreement.

“Cash Merger Consideration” means $107.5 million in cash, subject to adjustment in accordance with the terms of the Merger Agreement.

“Earnout Shares” means the 3,500,000 additional shares of ROI Common Stock to be issued to EveryWare stockholders in connection with the closing of the Business Combination, which will be subject to forfeiture in the event that the trading price of the ROI Common Stock does not exceed certain price targets subsequent to the closing of the Business Combination. The Earnout Shares will have the same rights as other outstanding shares of ROI Common Stock but will not be transferrable prior to the time the shares cease to be subject to forfeiture.

“EveryWare” means EveryWare Global, Inc.

“Final EveryWare Merger” means the merger of EveryWare with and into Merger Sub LLC immediately following the Initial EveryWare Merger, with Merger Sub LLC surviving the merger as a wholly-owned subsidiary of ROI, at which time Merger Sub LLC will be renamed “EveryWare, LLC.”

“founder shares” means the shares of ROI Common Stock issued prior to ROI’s initial public offering.

“founders” means holders of the founder shares.

“Initial EveryWare Merger” means the merger of Merger Sub Corp. with and into EveryWare, with EveryWare surviving the merger as a wholly-owned subsidiary of ROI.

“Lampert” means Lampert Debt Advisors.

“MCP Funds” means Monomoy Capital Partners, L.P., MCP Supplemental Fund, L.P., Monomoy Executive Co-Investment Fund, L.P., Monomoy Capital Partners II, L.P. and MCP Supplemental Fund II, L.P.

“Merger Agreement” means the Business Combination Agreement and Plan of Merger, dated as of January 31, 2013, as it may be amended, by and among the Company, ROI Merger Sub Corp., ROI Merger Sub LLC and EveryWare.

6

Table of Contents

“Merger Sub Corp.” means ROI Merger Sub Corp., a Delaware corporation.

“Merger Sub LLC” means ROI Merger Sub LLC, a Delaware limited liability company.

“Monomoy” means Monomoy Capital Management, LLC.

“Oneida” means Oneida Ltd.

“Oneida Merger” means the acquisition of Oneida, Ltd. by EveryWare on November 1, 2011.

“public shares” means shares of ROI Common Stock issued in ROI’s initial public offering.

“public warrants” means the warrants issued in ROI’s initial public offering, each of which is exercisable for one share of ROI Common Stock, in accordance with its terms.

“ROI” means ROI Acquisition Corp.

“ROI Common Stock” means common stock, par value $0.0001 per share, of ROI.

“Sponsor” means Clinton Magnolia Master Fund, Ltd.

“Stock Merger Consideration” means 10,440,000 shares of ROI Common Stock, subject to adjustment in accordance with the terms of the Merger Agreement.

7

Table of Contents

QUESTIONS AND ANSWERS ABOUT THE PROPOSALS

FOR STOCKHOLDERS AND PUBLIC WARRANTHOLDERS

The following questions and answers briefly address some commonly asked questions about the proposals to be presented at the special meetings of stockholders and public warrantholders, including with respect to the proposed Business Combination. The following questions and answers may not include all the information that is important to our stockholders and public warrantholders. We urge stockholders and public warrantholders to read carefully this entire proxy statement, including the annexes and the other documents referred to herein.

| Q: | Why am I receiving this proxy statement? |

| A: | We have entered into the Merger Agreement pursuant to which ROI Merger Sub Corp., a wholly owned subsidiary of the Company, will merge with and into EveryWare, immediately followed by the merger of EveryWare with and into ROI Merger Sub, LLC, another wholly owned subsidiary of the Company, with ROI Merger Sub, LLC surviving the merger. The aggregate consideration to EveryWare equityholders will consist of (i) $107.5 million in cash (the “Cash Merger Consideration”) and (ii) 10,440,000 shares of ROI Common Stock (“Stock Merger Consideration”), subject to adjustment in accordance with the terms of the Merger Agreement if the aggregate amount of cash available to pay the Cash Merger Consideration is less than $107.5 million. If the amount of the Cash Merger Consideration is less than $107.5 million but at least $90.0 million, ROI may issue additional shares of ROI Common Stock in an amount equal to the cash shortfall, with each share of ROI Common Stock valued at $10.00. If the amount of the Cash Merger Consideration is less than $90.0 million, EveryWare may terminate the Merger Agreement or, at its option, if the Cash Merger Consideration is at least $55.0 million, elect to receive additional shares of ROI Common Stock in an amount equal to the cash shortfall from $107.5 million, with each share of ROI Common Stock valued at $10.00. In addition, EveryWare’s existing stockholders will receive an aggregate of 3,500,000 Earnout Shares. This agreement, as it may be amended, is referred to as the Merger Agreement, and the transactions contemplated by this agreement are referred to as the EveryWare Merger and the Business Combination. A copy of the Merger Agreement is attached to this proxy statement as Annex A. |

Our stockholders are being asked to consider and vote upon a proposal to approve and adopt the Merger Agreement, among other proposals, and our warrantholders are being asked to consider and vote upon a proposal to approve and adopt the Warrant Amendment.

Our common stock, units and warrants are currently listed on The NASDAQ Stock Market, or NASDAQ, under the symbols “ROIQ,” “ROIQU” and “ROIQW,” respectively. We have applied to continue the listing of our common stock on NASDAQ under the symbol “EVRY” upon the closing of the Business Combination. Prior to the closing, our units will separate into their component share of common stock and warrant to purchase one share of our common stock. Following the closing, we expect that our warrants will trade on the OTC market under the symbol “EVRYW.”

This proxy statement and its annexes contain important information about the proposed Business Combination and the other matters to be acted upon at the special meetings. You should read this proxy statement and its annexes carefully and in their entirety.

Your vote is important. You are encouraged to submit your proxy as soon as possible after carefully reviewing this proxy statement and its annexes.

| Q: | What is being voted on at the special meetings? |

| A: | Below are proposals on which our stockholders and public warrantholders are being asked to vote. |

8

Table of Contents

Proposals for the Special Meeting of Stockholders

| 1. | To approve and adopt the Merger Agreement (this proposal is referred to herein as the “Business Combination Proposal”); |

| 2. | To consider and vote upon a proposal to approve a third amended and restated certificate of incorporation of the Company, or the proposed certificate, to, among other things: |

| • | change our name to EveryWare Global, Inc.; |

| • | remove certain provisions related to our status as a blank check company; and |

| • | make certain other changes that our board of directors deems appropriate for a public operating company (this proposal is referred to herein as the “Certificate Proposal”); |

| 3. | To elect three directors to our board of directors, subject to the consummation of the Business Combination (this proposal is referred to herein as the “Director Election Proposal”); |

| 4. | To approve and adopt the EveryWare Global, Inc. 2013 Omnibus Incentive Plan (this proposal is referred to herein as the “Incentive Plan Proposal”); and |

| 5. | To approve the adjournment of the special meeting of stockholders to a later date or dates, if necessary, to permit further solicitation and vote of proxies in the event that, based upon the tabulated vote at the time of the special meeting, there are not sufficient votes to approve one or more proposals presented at the special meeting of stockholders (this proposal is referred to herein as the “Adjournment Proposal”). This proposal will only be presented at the special meeting if there are not sufficient votes to approve one or more proposals presented to stockholders for vote. |

Proposals for the Special Meeting of Warrantholders

| 1. | To consider and vote upon a proposal to approve an amendment to the warrant agreement to remove a provision that provides for a reduction of the warrant exercise price upon the occurrence of certain transactions following the Business Combination in which the consideration to be received by our stockholders includes equity securities that are not listed for trading on a national securities exchange or on the OTC Bulletin Board, or are not to be so listed for trading immediately following such event (this proposal is referred to herein as the “Warrant Amendment Proposal”); |

| 2. | To consider and vote upon a proposal to approve a proposal to approve the adjournment of the special meeting of public warrantholders to a later date or dates, if necessary, to permit further solicitation and vote of proxies (this proposal is referred to herein as the “Warrantholder Adjournment Proposal”) in the event that, based upon the tabulated vote at the time of the special meeting, there are not sufficient votes to approve the Warrant Amendment Proposal. |

| Q: | Are the proposals conditioned on one another? |

| A: | The Business Combination Proposal is conditioned on the Certificate Proposal and the Director Election Proposal, and the Certificate Proposal and the Director Election Proposal are each conditioned on the Business Combination Proposal. The Equity Incentive Plan Proposal is conditioned on the Business Combination Proposal. The Warrant Amendment Proposal does not require the approval of any other proposal to be effective. The Adjournment Proposal and Warrantholder Adjournment Proposal (which we collectively refer to as the “Adjournment Proposals”) do not require the approval of any other proposal to be effective. It is important for you to note that in the event that any of the Business |

9

Table of Contents

Combination Proposal, the Certificate Proposal or the Director Election Proposal does not receive the requisite vote for approval, then we will not consummate the Business Combination. If we do not consummate the Business Combination and fail to complete an initial business combination by November 29, 2013, we will be required to dissolve and liquidate our trust account. |

| Q: | Why is ROI proposing the Business Combination Proposal? |

| A: | We were organized for the purpose of effecting a merger, capital stock exchange, asset acquisition, stock purchase, reorganization or similar business combination with one or more businesses. In particular, we have sought to focus on the consumer, restaurant or food sectors, though we are not limited to any particular industry or sector. |

We consummated our initial public offering on February 29, 2012. Approximately $75.1 million of the proceeds of our initial public offering and the private placement of the sponsor warrants and units was placed in a trust account immediately following the initial public offering and, in accordance with our second amended and restated certificate of incorporation, will be released upon the consummation of the Business Combination. See the question entitled “What happens to the funds held in the trust account upon consummation of the Business Combination?”

There currently are 9,385,000 shares of our common stock issued and outstanding, consisting of 7,500,000 shares originally sold as part of units in our initial public offering, 1,875,000 shares that were issued prior to our initial public offering to an affiliate of our Sponsor (which were subsequently transferred to Clinton Magnolia Master Fund, Ltd. (our “Sponsor”)) and 10,000 shares originally sold as part of units issued simultaneously with our initial public offering to Mr. Baldwin. In addition, there currently are 11,676,667 warrants outstanding, consisting of 7,500,000 warrants originally sold as part of units in our initial public offering, 4,166,667 sponsor warrants that were sold by us to an affiliate of our Sponsor in a private sale simultaneously with our initial public offering (which were subsequently transferred to our Sponsor) and 10,000 sponsor warrants originally sold as part of units issued simultaneously with our initial public offering to Mr. Baldwin.

Under our second amended and restated certificate of incorporation, we must provide all holders of public shares with the opportunity to have their public shares redeemed upon the consummation of our initial Business Combination either in conjunction with a tender offer or in conjunction with a stockholder vote.

NASDAQ Listing Rule 5635(a) requires shareholder approval where, among other things, the issuance of securities in a transaction exceeds 20% of the number of shares of common stock or the voting power outstanding before the transaction, and NASDAQ Listing Rule 5635(b) requires shareholder approval where the issuance of securities will result in a change of control. We intend to issue approximately 13,940,000 shares of our common stock (including 3,500,000 Earnout Shares), or approximately 149% of our 9,385,000 currently outstanding shares of common stock, in the Business Combination (assuming no redemptions of our public shares and no additional issuances of our common stock). Therefore, we are required to obtain the approval of our stockholders under both NASDAQ Listing Rules 5635(a) and 5635(b).

| Q: | Why is ROI holding a special meeting of public warrantholders? |

| A: | At a special meeting of public warrantholders, ROI will ask its public warrantholders to approve and consent to an amendment to the terms of the warrant agreement, governing ROI’s outstanding warrants, to remove a provision that provides for a reduction of the |

10

Table of Contents

warrant exercise price upon the occurrence of certain transactions following a business combination in which the consideration to be received by our stockholders includes equity securities that are not listed for trading on a national securities exchange or on the OTC Bulletin Board, or are not to be so listed for trading immediately following such event (the “Warrant Amendment Proposal”). Even if the Business Combination is not consummated, the Warrant Amendment will become effective if warrantholders have approved the Warrant Amendment. The holders of the sponsor warrants are not permitted to vote on the Warrant Amendment Proposal unless the registered holders of 65% of the public warrants vote in favor of the Warrant Amendment Proposal. |

In addition, at the special meeting of public warrantholders, holders of public warrants will also be asked to approve a proposal to approve the adjournment of the special meeting of public warrantholders to a later date or dates, if necessary, to permit further solicitation and vote of proxies in the event that, based upon the tabulated vote at the time of the special meeting, there are not sufficient votes to approve the Warrant Amendment Proposal. This is referred to herein as the Warrantholder Adjournment Proposal. This proposal will only be presented at the special meeting of public warrantholders if there are not sufficient votes to approve the Warrant Amendment Proposal.

| Q: | Why is ROI proposing the Warrant Amendment Proposal? |

| A: | ROI and our Sponsor have agreed to effect the Warrant Amendment in connection with the consummation of the Business Combination in order for the warrants to classify as permanent equity. Even if the Business Combination is not consummated, the Warrant Amendment will become effective if warrantholders have approved the Warrant Amendment. Approval of the Warrant Amendment Proposal requires the affirmative vote of the holders of at least 65% of the outstanding public warrants as of the record date. |

| Q: | What will happen in the Business Combination? |

| A: | At the closing of the EveryWare Merger, ROI Merger Sub Corp., a wholly owned subsidiary of the Company, will merge with and into EveryWare, with EveryWare surviving the merger as a wholly owned subsidiary of the Company, immediately followed by the merger of EveryWare with and into ROI Merger Sub LLC, another wholly owned subsidiary of the Company, with ROI Merger Sub LLC surviving the merger. As a result of the EveryWare Merger, former stockholders of EveryWare will become stockholders of the Company. |

| Q: | What equity stake will current ROI stockholders and former EveryWare stockholders hold in the Company after the closing? |

| A: | It is anticipated that, upon effectiveness of the Initial EveryWare Merger, ROI’s existing stockholders will retain an ownership interest of between 10.5% and 39.7% of the post-merger company and the former equity holders of EveryWare will own between 89.5% and 60.3% of the post-merger company. These percentages are calculated based on a number of assumptions and are subject to adjustment in accordance with the terms of the Merger Agreement. These relative percentages assume that ROI receives $250.0 million in cash proceeds from the proposed issuance of senior secured notes in order to fund the Cash Merger Consideration and refinance EveryWare’s existing debt and are based upon net debt of EveryWare at December 31, 2012. If the actual facts are different than these assumptions, the percentage ownership retained by ROI’s existing stockholders will be different. These percentages also do not take into account (i) the additional 3,500,000 Earnout Shares and 551,471 shares of outstanding ROI common stock currently held by our Sponsor, that could in each case be subject to forfeiture in the future if certain performance conditions relating |

11

Table of Contents

to the trading price of ROI’s Common Stock are not met following the Business Combination, (ii) options to purchase shares of ROI common stock that will issued to former holders of EveryWare stock options in connection with the Business Combination and (iii) warrants to purchase ROI’s common stock that will remain outstanding following the Business Combination. |

The following table illustrates several hypothetical scenarios based on the assumptions described above but assuming varying levels of redemptions by ROI stockholders:

| Assumed % of ROI Shares Redeemed | ||||||||||||||||

| 0-26.3% | 50% | 75% | Maximum | |||||||||||||

ROI public stockholders | 32.0 | % | 21.7 | % | 10.9 | % | 2.9 | % | ||||||||

ROI founders | 7.7 | % | 7.7 | % | 7.7 | % | 7.7 | % | ||||||||

MCP Funds | 57.7 | % | 67.6 | % | 77.9 | % | 85.6 | % | ||||||||

Former EveryWare stockholders (other than the MCP Funds) | 2.6 | % | 3.1 | % | 3.6 | % | 3.9 | % | ||||||||

See “Summary—ROI Shares to be Issued in the Business Combination” and “Unaudited Pro Forma Condensed Combined Financial Information” for further information.

| Q: | Is the EveryWare Merger the first step in a “going-private” transaction? |

| A: | The Company does not intend for the EveryWare Merger to be the first step in a “going-private” transaction. Indeed, one of the primary purposes of the Business Combination is to provide a platform for EveryWare to access the U.S. public markets. |

| Q: | What conditions must be satisfied to complete the Business Combination? |

| A: | There are a number of closing conditions in the Merger Agreement, including that our stockholders have approved and adopted the Merger Agreement. For a summary of the conditions that must be satisfied or waived prior to completion of the Business Combination, see the section entitled“Proposal No. 1—Approval of the Business Combination—The Merger Agreement.” |

| Q: | Why is ROI proposing the Certificate Proposal? |

| A: | The proposed certificate that we are asking our stockholders to approve in connection with the Business Combination provides for the change of our name to EveryWare Global, Inc., the removal of provisions related to our status as a blank check company and other changes that our board of directors deem appropriate for a public operating company. |

| Q: | Why is ROI proposing the Director Election Proposal? |

| A: | The Merger Agreement provides that effective immediately after the closing of the EveryWare Merger, the board of directors of the Company will consist of nine members, divided into three classes, with each class having a term of three years. If all director nominees are elected, our board will consist of five (5) directors designated by the MCP Funds, three (3) of our existing board members and one director who is the Chief Executive Officer and President of EveryWare. See the sections entitled “Proposal No. 3—Election of Directors to the Board of Directors” and “Management After the Business Combination” for additional information. |

| Q: | Why is ROI proposing the Incentive Plan Proposal? |

| A: | The purpose of the 2013 Omnibus Incentive Plan is to provide incentives that will attract, retain and motivate high-performing officers, directors, employees (generally, all classes of our employees and those of our subsidiaries) and consultants by providing them a |

12

Table of Contents

proprietary interest in our long-term success or compensation based on their performance in fulfilling their responsibilities to the combined company thereby strengthening their commitment to the welfare of the combined company and its affiliates and aligning their interests with those of our stockholders. |

| Q: | What happens if I sell my shares of ROI common stock before the special meeting of stockholders? |

| A: | The record date for the special meeting of stockholders is earlier than the date that the Business Combination is expected to be completed. If you transfer your shares of ROI common stock after the record date, but before the special meeting of stockholders, unless the transferee obtains from you a proxy to vote those shares, you will retain your right to vote at the special meeting of stockholders. |

| Q: | What vote is required to approve the proposals presented at the special meeting of stockholders? |

| A: | The approval of the Business Combination Proposal and the Incentive Plan Proposal requires the affirmative vote of holders of a majority of the shares of our common stock that are voted at the special meeting of stockholders. Accordingly, an ROI stockholder’s failure to vote by proxy or to vote in person at the special meeting of stockholders, an abstention from voting, or the failure of an ROI stockholder who holds his or her shares in “street name” through a broker or other nominee to give voting instructions to such broker or other nominee (a “broker non-vote”) will have no effect on the outcome of any vote on the Business Combination Proposal or the Incentive Plan Proposal. |

The approval of the Certificate Proposal requires the affirmative vote of the holders of a majority of the outstanding shares of our common stock. Accordingly, an ROI stockholder’s failure to vote by proxy or to vote in person at the special meeting of stockholders, an abstention from voting or a broker non-vote will have the same effect as a vote “AGAINST” the Certificate Proposal.

Directors are elected by a plurality of all of the votes cast by holders of shares of our common stock represented in person or by proxy and entitled to vote thereon at the special meeting of stockholders. This means that the three nominees will be elected if they receive more affirmative votes than any other nominee for the same position. Stockholders may not cumulate their votes with respect to the election of directors. Abstentions and broker non-votes will have no effect on the election of directors.

The approval of the Adjournment Proposal requires the affirmative vote of the holders of a majority of the shares of our common stock represented in person or by proxy and entitled to vote thereon at the special meeting of stockholders. Accordingly, abstentions will have the same effect as a vote “AGAINST” the Adjournment Proposal, while a broker non-vote and shares not in attendance at the special meeting will have no effect on the outcome of any vote on the Adjournment Proposal.