File No. 333-______

AS FILED WITH THE SECURITIES AND EXCHANGE COMMISSION ON JANUARY 16, 2015

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-14

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 [X]

Pre-Effective Amendment No. [ ]

Post-Effective Amendment No. [ ]

Curian Variable Series Trust

(Exact Name of Registrant as Specified in Charter)

7601 Technology Way, Denver, Colorado 80237

(Address of Principal Executive Offices)

(877) 847-4143

(Registrant’s Area Code and Telephone Number)

7601 Technology Way

Denver, Colorado 80237

(Mailing Address)

With copies to:

SUSAN S. RHEE, ESQ. Curian Variable Series Trust Vice President, Chief Legal Officer, & Secretary 1 Corporate Way Lansing, Michigan 48951 | ALAN GOLDBERG, ESQ. K&L Gates LLP 70 West Madison Street Suite 3100 Chicago, Illinois 60602 |

Approximate Date of Proposed Public Offering:

As soon as practicable after this Registration Statement becomes effective.

It is proposed that this Registration Statement will become effective on February 19, 2015 pursuant to Rule 488 under the Securities Act of 1933, as amended.

Title of securities being registered: shares of beneficial interest in the series of the registrant designated as the Curian Guidance – Conservative Fund.

No filing fee is required because the registrant is relying on Section 24(f) of the Investment Company Act of 1940, as amended, pursuant to which it has previously registered an indefinite number of shares (File Nos. 333-177369 and 811-22613).

CURIAN VARIABLE SERIES TRUST

CONTENTS OF REGISTRATION STATEMENT

This Registration Statement contains the following papers and documents:

Cover Sheet

Contents of Registration Statement

Letter to Shareholders

Notice of Special Meeting

Information Statement

Part A - Proxy Statement/Prospectus

Part B - Statement of Additional Information

Part C - Other Information

Signature Page

Exhibits

JACKSON NATIONAL LIFE INSURANCE COMPANY

JACKSON NATIONAL LIFE INSURANCE COMPANY OF NEW YORK

1 Corporate Way

Lansing, Michigan 48951

February 19, 2015

Dear Contract Owner:

Enclosed is a notice of a Special Meeting of Shareholders of the Curian Guidance – International Conservative Fund (the “International Conservative Fund” or the “Acquired Fund”), a series of Curian Variable Series Trust (the “Trust”). The Special Meeting of Shareholders of the Acquired Fund is scheduled to be held at the offices of Jackson National Life Insurance Company, 1 Corporate Way, Lansing, Michigan, 48951, on April 2, 2015 at 10:30 a.m., Eastern Time (the “Meeting”). At the Meeting, the shareholders of the Acquired Fund will be asked to approve the proposal described below.

The Trust’s Board of Trustees (the “Board”) called the Meeting to request shareholder approval of the reorganization (the “Reorganization”) of the Acquired Fund into the Curian Guidance – Conservative Fund, a series of the Trust (the “Acquiring Fund”).

The Board has approved this proposal.

Both the Acquired Fund and the Acquiring Fund are managed by Curian Capital, LLC (“Curian Capital”). If the Reorganization is approved and implemented, each person that invests indirectly in an Acquired Fund will automatically become an investor indirectly in the Acquiring Fund.

An owner of an annuity contract or certificate that participates in the Acquired Fund through the investment divisions of separate accounts established by Jackson National Life Insurance Company or Jackson National Life Insurance Company of New York (each, an “Insurance Company”), is entitled to instruct the applicable Insurance Company how to vote the Acquired Fund shares related to the ownership interest in those accounts as of the close of business on February 6, 2015. The attached Notice of Special Meeting of Shareholders and Proxy Statement and Prospectus concerning the Meeting describe the matters to be considered at the Meeting.

You are cordially invited to attend the Meeting. Because it is important that your vote be represented whether or not you are able to attend, you are urged to consider these matters and to exercise your voting instructions by completing, dating, signing, and returning the enclosed voting instruction card in the accompanying return envelope at your earliest convenience or by relaying your voting instructions via telephone or the Internet by following the enclosed instructions. Of course, we hope that you will be able to attend the Meeting, and if you wish, you may vote your shares in person, even though you may have already returned a voting instruction card or submitted your voting instructions via telephone or the Internet. Please respond promptly in order to save additional costs of proxy solicitation and in order to make sure you are represented.

| | |

| Very truly yours, | |

| | |

| Mark D. Nerud | |

| President and Chief Executive Officer |

| Curian Variable Series Trust |

CURIAN VARIABLE SERIES TRUST

Curian Guidance – International Conservative Fund

7601 Technology Way

Denver, Colorado 80237

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

TO BE HELD ON APRIL 2, 2015

To the Shareholders:

NOTICE IS HEREBY GIVEN that a Special Meeting of Shareholders of the Curian Guidance – International Conservative Fund (the “International Conservative Fund” or the “Acquired Fund”) will be held on April 2, 2015, at 10:30 a.m., Eastern Time, at the offices of Jackson National Life Insurance Company, 1 Corporate Way, Lansing, Michigan 48951 (the “Meeting”).

The Meeting will be held to act on the following proposals:

| 1. | To approve the Plan of Reorganization, adopted by the Trust’s Board of Trustees, which provides for the reorganization of the International Conservative Fund into the Curian Guidance – Conservative Fund, also a series of the Trust. |

| 2. | To transact other business that may properly come before the Meeting or any adjournments thereof. |

Please note that owners of variable life insurance policies or variable annuity contracts or certificates (the “Contract Owners”) issued by Jackson National Life Insurance Company or Jackson National Life Insurance Company of New York (each, an “Insurance Company”) who have invested in shares of the Acquired Fund through the investment divisions of a separate account or accounts of an Insurance Company (“Separate Account”) will be given the opportunity, to the extent required by law, to provide the applicable Insurance Company with voting instructions on the above proposals.

You should read the Proxy Statement and Prospectus attached to this notice prior to completing your proxy or voting instruction card. The record date for determining the number of shares outstanding, the shareholders entitled to vote and the Contract Owners entitled to provide voting instructions at the Meeting and any adjournments thereof has been fixed as the close of business on February 6, 2015. If you attend the Meeting, you may vote or give your voting instructions in person.

YOUR VOTE IS IMPORTANT

PLEASE RETURN YOUR PROXY CARD OR VOTING INSTRUCTION CARD PROMPTLY

Regardless of whether you plan to attend the Meeting, you should vote or give voting instructions by promptly completing, dating, signing, and returning the enclosed proxy or voting instruction card for the Acquired Fund in the enclosed postage-paid envelope. You also can vote or provide voting instructions through the Internet or by telephone using the 14-digit control number that appears on the enclosed proxy or voting instruction card and following the simple instructions. If you are present at the Meeting, you may change your vote or voting instructions, if desired, at that time. The Board recommends that you vote or provide voting instructions to vote FOR the proposals.

| By order of the Board, | |

| | |

| Mark D. Nerud | |

| President & Chief Executive Officer |

February 19, 2015

Denver, Colorado

JACKSON NATIONAL LIFE INSURANCE COMPANY

JACKSON NATIONAL LIFE INSURANCE COMPANY OF NEW YORK

INFORMATION STATEMENT

REGARDING A SPECIAL MEETING OF SHAREHOLDERS OF

CURIAN GUIDANCE – INTERNATIONAL CONSERVATIVE FUND

A SERIES OF THE CURIAN VARIABLE SERIES TRUST

TO BE HELD ON APRIL 2, 2015

DATED: FEBRUARY 19, 2015

GENERAL

This Information Statement is being furnished by Jackson National Life Insurance Company (“Jackson National”), or Jackson National Life Insurance Company of New York (each, an “Insurance Company” and, together, the “Insurance Companies”), each of which is a stock life insurance company, to owners of their variable life insurance policies or variable annuity contracts or certificates (the “Contracts”) (the “Contract Owners”) who, as of February 6, 2015 (the “Record Date”), had net premiums or contributions allocated to the investment divisions of their separate accounts (the “Separate Accounts”) that are invested in shares of the Curian Guidance – International Conservative Fund (the “International Conservative Fund” or “Acquired Fund”), a series of Curian Variable Series Trust (the “Trust”).

The Trust is a Massachusetts business trust registered with the Securities and Exchange Commission (the “SEC”) as an open-end management investment company.

Each Insurance Company is required to offer Contract Owners the opportunity to instruct it, as the record owner of all of the shares of beneficial interest in the Acquired Fund (the “Shares”) held by its Separate Accounts, as to how it should vote on the reorganization proposal (the “Proposal”) to be considered at the Special Meeting of Shareholders of the Acquired Fund referred to in the preceding Notice and at any adjournments (the “Meeting”). The enclosed Proxy Statement and Prospectus, which you should retain for future reference, concisely sets forth information about the proposed reorganization involving the Acquired Fund and a corresponding series of the Trust that a Contract Owner should know before completing the enclosed voting instruction card.

This Information Statement and the accompanying voting instruction card are being mailed to Contract Owners on or about February 19, 2015.

HOW TO INSTRUCT AN INSURANCE COMPANY

To instruct an Insurance Company as to how to vote the Shares held in the investment divisions of its Separate Accounts, Contract Owners are asked to promptly complete their voting instructions on the enclosed voting instruction card(s); and sign, date and mail the voting instruction card(s) in the accompanying postage-paid envelope. Contract Owners also may provide voting instructions by phone at 1-866-298-8476 or by Internet at our website at www.proxy-direct.com.

If a voting instruction card is not marked to indicate voting instructions but is signed, dated and returned, it will be treated as an instruction to vote the Shares in favor of the Proposal.

The number of Shares held in the investment division of a Separate Account corresponding to the Acquired Fund for which a Contract Owner may provide voting instructions was determined as of the Record Date by dividing (i) a Contract’s account value (minus any Contract indebtedness) allocable to that investment division by (ii) the net asset value of one Share of the Acquired Fund. At any time prior to an Insurance Company’s voting at the Meeting, a Contract Owner may revoke his or her voting instructions with respect to that investment division by providing the Insurance Company with a properly executed written revocation of such voting instructions, properly executing

later-dated voting instructions by a voting instruction card, telephone or the Internet, or appearing and voting in person at the Meeting.

HOW AN INSURANCE COMPANY WILL VOTE

An Insurance Company will vote the Shares for which it receives timely voting instructions from Contract Owners in accordance with those instructions. An Insurance Company will vote Shares attributable to Contracts for which the Insurance Company is the Contract Owner “FOR” the Proposal. Shares in each investment division of a Separate Account for which an Insurance Company receives a voting instruction card that is signed, dated and timely returned but is not marked to indicate voting instructions will be treated as an instruction to vote the Shares in favor of the Proposal. Shares in each investment division of a Separate Account for which an Insurance Company receives no timely voting instructions from a Contract Owner, or that are attributable to amounts retained by an Insurance Company or its affiliate as surplus or seed money, will be voted by the applicable Insurance Company either for or against approval of the Proposal, or as an abstention, in the same proportion as the Shares for which Contract Owners (other than the Insurance Company) have provided voting instructions to the Insurance Company.

OTHER MATTERS

The Insurance Companies are not aware of any matters, other than the Proposal, to be acted on at the Meeting. If any other matters come before the Meeting, an Insurance Company will vote the Shares upon such matters in its discretion. Voting instruction cards may be solicited by employees of Jackson National or its affiliates as well as officers and agents of the Trust. The principal solicitation will be by mail, but voting instructions may also be solicited by telephone, fax, personal interview, the Internet or other permissible means.

If the necessary quorum to transact business is not established or the vote required to approve or reject the Proposal is not obtained at the Meeting, the persons named as proxies may propose one or more adjournments of the Meeting in accordance with applicable law to permit further solicitation of voting instructions. The persons named as proxies will vote in favor of such adjournment with respect to those Shares for which they received voting instructions in favor of the Proposal and will vote against any such adjournment those Shares for which they received voting instructions against the Proposal.

It is important that your Contract be represented. Please promptly mark your voting instructions on the enclosed voting instruction card; then sign, date and mail the voting instruction card in the accompanying postage-paid envelope. You may also provide your voting instructions by telephone at 1-866-298-8476 or by Internet at our website at www.proxy-direct.com.

PROXY STATEMENT

for

Curian Guidance – International Conservative Fund, a series of Curian Variable Series Trust

and

PROSPECTUS

for

Curian Guidance – Conservative Fund, a series of Curian Variable Series Trust

Dated

February 19, 2015

7601 Technology Way

Denver, Colorado 80237

(877) 847-4143

This Proxy Statement and Prospectus (the “Proxy Statement/Prospectus”) is being furnished to owners of variable life insurance policies or variable annuity contracts or certificates (the “Contracts”) (the “Contract Owners”) issued by Jackson National Life Insurance Company (“Jackson National”) or Jackson National Life Insurance Company of New York (each, an “Insurance Company” and together, the “Insurance Companies”) who, as of February 6, 2015, had net premiums or contributions allocated to the investment divisions of an Insurance Company’s separate accounts (the “Separate Accounts”) that are invested in shares of beneficial interest in the Curian Guidance – International Conservative Fund (the “International Conservative Fund” or the “Acquired Fund”), a series of Curian Variable Series Trust (the “Trust”), an open-end management investment company registered with the Securities and Exchange Commission (“SEC”).

This Proxy Statement/Prospectus also is being furnished to the Insurance Companies as the record owners of shares and to other shareholders that were invested in the Acquired Fund as of February 6, 2015. Contract Owners are being provided the opportunity to instruct the applicable Insurance Company to approve or disapprove the proposal contained in this Proxy Statement/Prospectus in connection with the solicitation by the Board of Trustees of the Trust (the “Board”) of proxies to be used at the Special Meeting of Shareholders of the Acquired Fund to be held at 1 Corporate Way, Lansing, Michigan 48951, on April 2, 2015, at 10:30 a.m., Eastern Time, or any adjournment or adjournments thereof (the “Meeting”).

| THE SEC HAS NOT APPROVED OR DISAPPROVED THE SECURITIES DESCRIBED IN THIS PROXY STATEMENT/PROSPECTUS OR DETERMINED IF THIS PROXY STATEMENT/PROSPECTUS IS TRUTHFUL OR COMPLETE. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE. |

The proposal described in this Proxy Statement/Prospectus is as follows:

| Proposal | Shareholders Entitled to Vote on

the Proposal |

| 1. To approve the Plan of Reorganization, adopted by the Trust’s Board of Trustees, which provides for the reorganization of the International Conservative Fund into the Curian Guidance – Conservative Fund (the “Conservative Fund”), also a series of the Trust. | Shareholders of the International Conservative Fund |

The reorganization referred to in the above proposal is referred to herein as the “Reorganization.” The Conservative Fund is herein referred to as the “Acquiring Fund.”

This Proxy Statement/Prospectus, which you should retain for future reference, contains important information regarding the proposal that you should know before voting or providing voting instructions. Additional information about the Trust has been filed with the SEC and is available upon oral or written request without charge. This Proxy Statement/Prospectus is being provided to the Insurance Companies and mailed to Contract Owners on or about February 19, 2015. It is expected that one or more representatives of each Insurance Company will attend the Meeting in person or by proxy and will vote shares held by the Insurance Company in accordance with voting instructions received from its Contract Owners and in accordance with voting procedures established by the Trust.

The following documents have been filed with the SEC and are incorporated by reference into this Proxy Statement/Prospectus:

| 1. | The Prospectus and Statement of Additional Information of the Trust, each dated April 28, 2014, as supplemented, with respect to the International Conservative Fund and the Conservative Fund (File Nos. 333-177369 and 811-22613); |

| 2. | The Annual Report to Shareholders of the Trust with respect to the International Conservative Fund and the Conservative Fund for the fiscal year ended December 31, 2013 (File Nos. 333-177369 and 811-22613); |

| 3. | The Semi-Annual Report to Shareholders of the Trust with respect to the International Conservative Fund and the Conservative Fund for the period ended June 30, 2014 (File Nos. 333-177369 and 811-22613); |

| 4. | The Statement of Additional Information dated [_________], 2015, relating to the Reorganization (File No. 333-_____). |

For a free copy of any of the above documents, please call or write to the phone numbers or address below.

Contract Owners can learn more about the Acquired Fund in the Trust’s Annual Report listed above, which has been furnished to Contract Owners. Contract Owners may request another copy thereof, without charge, by calling 1-800-644-4565 (Annuity and Life Service Center), 1-800-599-5651 (NY Annuity and Life Service Center), 1-800-777-7779 (for contracts purchased through a bank or financial institution) or 1-888-464-7779 (for NY contracts purchased through a bank or financial institution), or by writing the Curian Variable Series Trust, P.O. Box 30314, Lansing, Michigan 48909-7814 or by visiting www.jackson.com.

The Trust is subject to the informational requirements of the Securities Exchange Act of 1934, as amended. Accordingly, it must file certain reports and other information with the SEC. You can copy and review information about the Trust at the SEC’s Public Reference Room in Washington, DC, and at certain of the following SEC Regional Offices: New York Regional Office, Brookfield Place, 200 Vesey Street, Suite 400, New York, New York 10281; Miami Regional Office, 801 Brickell Avenue, Suite 1800, Miami, Florida 33131; Chicago Regional Office, 175 W. Jackson Boulevard, Suite 900, Chicago, Illinois 60604; Denver Regional Office, 1961 Stout Street, Suite 1700, Denver, Colorado 80294; Los Angeles Regional Office, 444 South Flower Street, Suite 900, Los Angeles,

California 90071; Boston Regional Office, 33 Arch Street, 23rd Floor, Boston, MA 02110; Philadelphia Regional Office, One Penn Center, 1617 JFK Boulevard, Suite 520, Philadelphia, PA 19103; Atlanta Regional Office, 950 East Paces Ferry, N.E., Suite 900, Atlanta, GA 30326; Fort Worth Regional Office, Burnett Plaza, Suite 1900, 801 Cherry Street, Unit 18, Fort Worth, TX 76102; Salt Lake Regional Office, 351 S. West Temple Street, Suite 6100, Salt Lake City, UT 84101; San Francisco Regional Office, 44 Montgomery Street, Suite 2800, San Francisco, CA 94104. You may obtain information on the operation of the Public Reference Room by calling the SEC at (202) 551-8090. Reports and other information about the Trust are available on the SEC’s Internet site at http://www.sec.gov. You may obtain copies of this information from the SEC’s Public Reference Branch, Office of Consumer Affairs and Information Services, Washington, DC 20549, at prescribed rates.

TABLE OF CONTENTS

| | |

| | 1 |

| | 1 |

| | 2 |

| | 3 |

| | 4 |

| | 4 |

| | 4 |

| | 5 |

| | 7 |

| | 8 |

| | 9 |

| | 10 |

| | 11 |

| | 11 |

| | 12 |

| | 12 |

| | 14 |

| | 14 |

| | 15 |

| | 15 |

| | 15 |

| | 15 |

| | 15 |

| | 17 |

| | 17 |

| | 17 |

| | 17 |

| | 18 |

| | 19 |

| | 19 |

| | 20 |

| | 20 |

| | 22 |

| | 22 |

| | 22 |

| | 22 |

| | 23 |

| | 23 |

| | 23 |

| | 24 |

| | 24 |

| | A-1 |

| | B-1 |

| | C-1 |

You should read this entire Proxy Statement/Prospectus carefully. For additional information, you should consult the Plan of Reorganization, a copy of which is attached hereto as Appendix A.

This Proxy Statement/Prospectus is soliciting shareholders with amounts invested in the Acquired Fund as of February 6, 2015 to approve the Plan of Reorganization, whereby the Acquired Fund will be reorganized into the Acquiring Fund. (The Acquired Fund and Acquiring Fund are each sometimes referred to herein as a “Fund” and collectively, the “Funds.”)

The Acquired Fund has one share class (“Acquired Fund Shares”). The Acquiring Fund also only has one share class (the “Acquiring Fund Shares”). The rights and preferences of the Acquiring Fund Shares are identical to the Acquired Fund Shares.

The Plan of Reorganization provides for:

| ● | the transfer of all of the assets of the Acquired Fund to the Acquiring Fund in exchange for Acquiring Fund Shares having an aggregate net asset value equal to the Acquired Fund’s net assets; |

| ● | the Acquiring Fund’s assumption of all the liabilities of the Acquired Fund; |

| ● | the distribution to the shareholders (for the benefit of the Separate Accounts, as applicable, and thus the Contract Owners) of those Acquiring Fund Shares; and |

| ● | the complete termination of the Acquired Fund. |

A comparison of the investment objective(s), investment policies, strategies and principal risks of the Acquired Fund and the Acquiring Fund is included in “Comparison of Investment Objectives, Policies and Strategies” and “Comparison of Principal Risk Factors” below. The Funds have identical distribution procedures, purchase procedures, exchange rights and redemption procedures, which are discussed in “Additional Information about the Acquiring Fund” below. Each Fund offers its shares to Separate Accounts and certain other eligible investors. Shares of each Fund are offered and redeemed at their net asset value without any sales load. You will not incur any sales loads or similar transaction charges as a result of the Reorganization.

The Reorganization is expected to be effective as of the close of business on April 24, 2015, or on a later date the Trust decides upon (the “Closing Date”). As a result of the Reorganization, a shareholder invested in shares of the Acquired Fund would become an owner of shares of the Acquiring Fund. Such shareholder would hold, immediately after the Closing Date, shares of the Acquiring Fund having an aggregate value equal to the aggregate value of the Acquired Fund shares that were held by the shareholder as of the Closing Date. Similarly, each Contract Owner whose Contract values are invested in shares of the Acquired Fund would become an indirect owner of shares of the Acquiring Fund. Each such Contract Owner would indirectly hold, immediately after the Closing Date, shares of the Acquiring Fund having an aggregate value equal to the aggregate value of the Acquired Fund shares that were indirectly held by the Contract Owner as of the Closing Date. The Trust believes that there will be no adverse tax consequences to Contract Owners as a result of the Reorganization. Please see “Additional Information about the Reorganization – Federal Income Tax Consequences of the Reorganization” below for further information.

The Trust’s Board of Trustees (the “Board”) unanimously approved the Plan of Reorganization with respect to the International Conservative Fund. Accordingly, the Board is submitting the Plan of Reorganization for approval by the Acquired Fund’s shareholders. In considering whether to approve the proposal (“Proposal”), you should review the Proposal for the Acquired Fund in which you were a direct or indirect holder on the Record Date (as defined under “Voting Information”). In addition, you should review the information in this Proxy Statement/Prospectus

that relates to the Proposal and the Plan of Reorganization generally. The Board recommends that you vote “FOR” the Proposal to approve the Plan of Reorganization.

| APPROVAL OF THE PLAN OF REORGANIZATION WITH RESPECT TO THE REORGANIZATION OF THE INTERNATIONAL CONSERVATIVE FUND INTO THE CONSERVATIVE FUND. |

Proposal 1 requests the approval of International Conservative Fund shareholders of the Plan of Reorganization pursuant to which the International Conservative Fund will be reorganized into the Conservative Fund.

In considering whether you should approve this Proposal, you should note that:

| ● | The Funds have different investment objectives. The International Conservative Fund seeks total return, consistent with preservation of capital, through a predominant allocation in international bonds, stocks and other asset classes and strategies through investment in other funds (the “Underlying Funds”), while the Conservative Fund seeks the generation of income through investment in Underlying Funds. However, the Funds have similar investment goals. Each Fund allocates the majority of its assets to Underlying Funds that invest in bonds and equity securities of issuers in the U.S. and foreign countries, including emerging markets. There are, however, differences in the Funds’ primary investment policies and strategies of which you should be aware, including that the International Conservative Fund allocates a large portion its assets to Underlying Funds that invest either primarily in international bonds or international equity securities and that the Conservative Fund allocates a large portion its assets to Underlying Funds that invest in U.S. bonds. The Funds have the same fundamental policies and restrictions, see “Comparison of Fundamental Policies” below. For a detailed comparison of each Fund’s investment policies and strategies, see “Comparison of Investment Objectives, Policies and Strategies” below. |

| ● | The Funds also have similar investment policies. Each Fund is structured as a fund-of-funds and invests in shares of Underlying Funds. The International Conservative Fund seeks to achieve its objective by allocating its assets to Underlying Funds that invest in international equity and fixed income asset classes, as well as non-traditional and emerging markets equity asset classes. The Conservative Fund seeks to achieve its objective by allocating its assets to Underlying Funds that invest in global and domestic fixed income asset classes as well as non-traditional asset classes. For a detailed comparison of each Fund’s investment policies and strategies, see “Comparison of Investment Objectives, Policies and Strategies” below. |

| ● | The Funds also have some similarities in their risk profiles, although there are differences of which you should be aware. Each Fund’s principal risks include allocation risk, commodity risk, counterparty risk, credit risk, currency risk, derivatives risk, emerging markets risk, equity securities risk, fixed income risk, foreign regulatory risk, foreign securities risk, interest rate risk, liquidity risk, managed portfolio risk, market risk, non-diversification risk, real estate investment risk, sovereign debt risk, and Underlying Funds risk. The International Conservative Fund, however, also is subject to bonds risk, while the Conservative Fund generally is not. In addition, the principal risks of investing in the Conservative Fund also include frontier market countries risk, micro-cap company risk, precious metal related securities risk, and short sales risk, which are not principal risks of investing in the International Conservative Fund. For a detailed comparison of each Fund’s risks, see “Comparison of Principal Risk Factors” below. |

| ● | Curian Capital, LLC (“Curian Capital” or the “Adviser”) currently serves as the investment adviser and administrator for each Fund. However, if a proposal to change investment advisers from Curian Capital to Jackson National Asset Management, LLC (“JNAM”) is approved by shareholders via a separate proxy, then JNAM will manage and administer the Conservative Fund after the Reorganization. Curian Capital and JNAM have both received separate exemptive orders from the SEC that generally permit Curian Capital, JNAM, and the Trust’s Board of Trustees to appoint, dismiss and replace each Fund’s sub-adviser(s) and to amend the advisory agreements between Curian Capital or JNAM, as the case may be, and the sub-adviser(s), without obtaining shareholder approval. However, any amendment to an advisory agreement between |

| | Curian Capital or JNAM, as the case may be, and the Trust that would result in an increase in the management fee rate specified in that agreement (i.e., the aggregate management fee) charged to a Fund will be submitted to shareholders for approval. Currently, neither Fund employs a sub-adviser. For a detailed description of the Adviser, please see “Additional Information about the Acquiring Funds - The Adviser” below. |

| ● | The International Conservative Fund and Conservative Fund had net assets of approximately $3.5 million and $76.8 million, respectively, as of June 30, 2014. Thus, if the Reorganization had been in effect on that date, the combined Fund (“Combined Fund”) would have had net assets of approximately $80.3 million. |

| ● | Shareholders of the International Conservative Fund will receive shares of the Conservative Fund pursuant to the Reorganization. Shareholders will not pay any sales charges in connection with the Reorganization. Please see “Comparative Fee and Expense Tables,” “Additional Information about the Reorganization” and “Additional Information about the Acquiring Fund” below for more information. |

| ● | It is estimated that the annual operating expense ratios for the Conservative Fund’s shares, following the Reorganization, will be lower than those of the International Conservative Fund’s shares. For a more detailed comparison of the fees and expenses of the Funds, please see “Comparative Fee and Expense Tables” and “Additional Information about the Acquiring Fund” below. |

| ● | The maximum management fee for the International Conservative Fund and the Conservative Fund are both equal to an annual rate of 0.15% of their average daily net assets. The administrative fee payable to the administrator is also the same for both Funds. For a more detailed description of the fees and expenses of the Funds, please see “Comparative Fee and Expense Tables” and “Additional Information about the Acquiring Fund” below. |

| ● | Following the Reorganization, the Combined Fund will be managed in accordance with the investment objective, policies and strategies of the Conservative Fund. It is not expected that the Conservative Fund will revise any of its investment policies following the Reorganization to reflect those of the International Conservative Fund. |

| ● | The costs and expenses associated with the Reorganization relating to preparing, filing, printing and mailing of material, disclosure documents and related legal fees, including the legal fees incurred in connection with the analysis under the Internal Revenue Code of 1986 (the “Code”) of the taxability of this transaction and the preparation of the tax opinion, and obtaining a consent of independent registered public accounting firm will be borne by JNAM. No sales or other charges will be imposed on Contract Owners in connection with the Reorganization. Please see “Additional Information about the Reorganization” below for more information. |

The following tables show the fees and expenses of each Fund and the estimated pro forma fees and expenses of the Acquiring Fund after giving effect to the proposed Reorganization. Fees and expenses for each Fund are based on those incurred for the fiscal year ended December 31, 2013. The pro forma fees and expenses of the Acquiring Fund Shares assume that the Reorganization had been in effect for the year ended December 31, 2013. The tables below do not reflect any fees and expenses related to the Contracts, which would increase overall fees and expenses. See a Contract prospectus for a description of those fees and expenses.

Annual Operating Expenses

(expenses that you pay each year as a percentage of the value of your investment)

| | International Conservative Fund | Conservative Fund | Pro Forma Conservative Fund (assuming expected operating expenses if the Reorganization is approved) |

| Management Fee | 0.15% | 0.15% | 0.15% |

Other Expenses2 | 0.12% | 0.12% | 0.07%4 |

Acquired Fund Fees and Expenses3 | 1.13% | 1.07% | 1.07% |

| Total Annual Fund Operating Expenses | 1.40% | 1.34% | 1.29% |

1 Management Fees and Administrative Fees have been restated to reflect a change in the management fee rate and administrative fee rate effective January 2, 2014.

2 "Other Expenses" for the International Conservative Fund and the Conservative Fund includes an Administrative Fee of 0.10% which is payable to Curian Capital.

3 Acquired fund fees and expenses are the indirect expenses of investing in other investment companies. The Total Annual Fund Operating Expenses disclosed above do not correlate to the Ratio of Total Expenses to Average Net Assets of the Fund stated in the Financial Highlights because the Ratio of Total Expenses to Average Net Assets does not include Acquired Fund Fees and Expenses.

4 In conjunction with the separate proposal to change investment advisers, the Board approved a reduction of 5 basis points in the Administrative Fee at its January 8, 2015 Special Board Meeting.

This example is intended to help you compare the costs of investing in the Funds with the cost of investing in other mutual funds. This example does not reflect fees and expenses related to the Contracts, and the total expenses would be higher if they were included. The example assumes that:

| ● | You invest $10,000 in a Fund; |

| ● | Your investment has a 5% annual return; |

| ● | Each Fund’s operating expenses remain the same as they were as of December 31, 2013; and |

| ● | You redeem your investment at the end of each time period. |

Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| | 1 Year | 3 Years | 5 Years | 10 Years |

| International Conservative Fund | $143 | $443 | $766 | $1,680 |

| Conservative Fund | $136 | $425 | $734 | $1,613 |

Pro Forma Conservative Fund (assuming expected operating expenses if the Reorganization is approved) | $131 | $409 | $708 | $1,556 |

Each Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs. These costs, which are not reflected in annual fund operating expenses or in the example, affect a Fund’s performance. For the six-months ended June 30, 2014, the portfolio turnover rates for the International Conservative Fund and Conservative Fund were 11% and 12%, respectively, of the average value of the respective Fund.

The following table compares the investment adviser of the Conservative Fund with that of the International Conservative Fund.

| Acquiring Fund | Acquired Fund |

| Conservative Fund | International Conservative Fund |

Investment Adviser Curian Capital, LLC* | Investment Adviser Curian Capital, LLC* |

*Although it is proposed that Jackson National Asset Management, LLC become investment adviser to the Funds, subject to approval of the Trust’s shareholders, with such change to become effective on April 27, 2015.

The following table compares the investment objectives and principal investment policies and strategies of the Conservative Fund with those of the International Conservative Fund. The Board may change the investment objective of a Fund without a vote of the Fund’s shareholders. For more detailed information about each Fund’s investment strategies and risks, see Appendix B.

| Acquiring Fund | Acquired Fund |

| Conservative Fund | International Conservative Fund |

Investment Objective The investment objective of the Fund is to seek the generation of income through investment in other funds. | Investment Objective The investment objective of the Fund is to seek total return, consistent with preservation of capital, through a predominant allocation in international bonds, stocks and other asset classes and strategies through investment in other funds. |

Principal Investment Strategies The Fund seeks to achieve its objective by investing in shares of the Underlying Funds. The Fund allocates its assets to Underlying Funds that invest primarily in fixed income and other income-oriented securities of issuers in the U.S. and foreign countries, including emerging markets. The Underlying Funds in which the Fund may invest each are a separate series of the Curian Variable Series Trust, JNL Series Trust, JNL Variable Fund LLC, or JNL Investors Series Trust. Not all Funds of the Curian Variable Series Trust, JNL Series Trust, JNL Variable Fund LLC, or JNL Investors Series Trust are available as Underlying Funds. Please refer to Appendix B for a list of available Underlying Funds. | Principal Investment Strategies The Fund seeks to achieve its objective by investing in shares of the Underlying Funds. The Fund allocates the majority of its assets to Underlying Funds that invest either primarily in international bonds or international equity securities of issuers in the U.S. and foreign countries, including emerging markets, as well as in Underlying Funds that invest in currencies. The Underlying Funds in which the Fund may invest each are a separate series of the Curian Variable Series Trust, JNL Series Trust, JNL Variable Fund LLC, or JNL Investors Series. Not all Funds of the Curian Variable Series Trust, JNL Series Trust, JNL Variable Fund LLC, or JNL Investors Series are available as Underlying Funds. Please refer to Appendix B for a list of available Underlying Funds. |

| The Fund allocates its assets among Underlying Funds categorized by the Adviser as Alternative Assets, Alternative Strategies, Domestic/Global Equity, Domestic/Global Fixed Income, International, | The Fund allocates its assets among Underlying Funds categorized by the Adviser as Alternative Assets, Alternative Strategies, Domestic/Global Equity, Domestic/Global Fixed Income, International, |

| Acquiring Fund | Acquired Fund |

| Conservative Fund | International Conservative Fund |

| International Fixed Income, Risk Management, Sector, Specialty, and Tactical Management. | International Fixed Income, Risk Management, Sector, Specialty, and Tactical Management. |

| The Fund considers the Underlying Funds in the Domestic/Global Fixed Income and International Fixed Income investment categories to be funds that invest primarily in fixed income securities, and the Underlying Funds in the Domestic/Global Equity, International, Sector, and Specialty investment categories to be funds that invest primarily in equity securities. The Underlying Funds in the Risk Management and Tactical Management investment categories include funds that can invest in a variety of asset classes in various proportions, may take measures to manage risk and/or adapt to prevailing market conditions and may have significant exposure to both fixed income and equity securities. To the extent the Fund invests in one of these Underlying Funds, the Fund’s exposure to fixed income securities and equity securities will be allocated according to the Underlying Fund’s relative exposure to these asset classes. The Fund considers the Underlying Funds in the Alternative Assets and Alternative Strategies investment categories to be funds that invest primarily in alternative assets and employ alternative strategies. | The Fund considers the Underlying Funds in the Domestic/Global Fixed Income and International Fixed Income investment categories to be funds that invest primarily in fixed income securities, and the Underlying Funds in the Domestic/Global Equity, International, Sector, and Specialty investment categories to be funds that invest primarily in equity securities. The Underlying Funds in the Risk Management and Tactical Management investment categories include funds that can invest in a variety of asset classes in various proportions, may take measures to manage risk and/or adapt to prevailing market conditions and may have significant exposure to both fixed income and equity securities. To the extent the Fund invests in one of these Underlying Funds, the Fund’s exposure to fixed income securities and equity securities will be allocated according to the Underlying Fund’s relative exposure to these asset classes. The Fund considers the Underlying Funds in the Alternative Assets and Alternative Strategies investment categories to be funds that invest primarily in alternative assets and employ alternative strategies. |

| In determining allocations to any particular Underlying Fund, the Adviser considers, among other things, long-term market and economic conditions, historical performance of each Underlying Fund, and expected long-term performance of each Underlying Fund, as well as diversification to control overall portfolio risk exposure. | In determining allocations to any particular Underlying Fund, the Adviser considers, among other things, long-term market and economic conditions, historical performance of each Underlying Fund, and expected long-term performance of each Underlying Fund, as well as diversification to control overall portfolio risk exposure. |

| The Underlying Funds in which the Fund may invest may be changed from time to time at the discretion of the Adviser without notice or shareholder approval. Therefore, the Fund may invest in Underlying Funds that are not listed in Appendix B. | The Underlying Funds in which the Fund may invest may be changed from time to time at the discretion of the Adviser without notice or shareholder approval. Therefore, the Fund may invest in Underlying Funds that are not listed in Appendix B. |

| The Fund is “non-diversified” under the Investment Company Act of 1940, as amended (the “1940 Act”), and may invest more of its assets in fewer issuers than “diversified” mutual funds. | The Fund is “non-diversified” under the 1940 Act, and may invest more of its assets in fewer issuers than “diversified” mutual funds. |

An investment in a Fund is not guaranteed. As with any mutual fund, the value of a Fund’s shares will change, and an investor could lose money by investing in a Fund. The following table compares the principal risks of an investment in each Fund. For an explanation of each such risk, see “Additional Information about the Reorganizations – Description of Risk Factors” below.

| Risks | Conservative Fund | International Conservative Fund |

| Allocation risk | X | X |

| Bonds risk | | X |

| Commodity risk | X | X |

| Counterparty risk | X | X |

| Credit risk | X | X |

| Currency risk | X | X |

| Derivatives risk | X | X |

| Emerging markets risk | X | X |

| Equity securities risk | X | X |

| Fixed income risk | X | X |

| Foreign regulatory risk | X | X |

| Foreign securities risk | X | X |

| Frontier market countries risk | X | |

| Interest rate risk | X | X |

| Liquidity risk | X | X |

| Managed portfolio risk | X | X |

| Market risk | X | X |

| Micro-cap company risk | X | |

| Non-diversification risk | X | X |

| Precious metal related securities risk | X | |

| Risks | Conservative Fund | International Conservative Fund |

| Real estate investment risk | X | X |

| Short sales risk | X | |

| Sovereign debt risk | X | X |

| Underlying Funds risk | X | X |

Each Fund is subject to certain fundamental policies and restrictions that may not be changed without shareholder approval. The following table compares the fundamental policies of the Conservative Fund with those of the International Conservative Fund.

| Acquiring Fund | Acquired Fund |

| Conservative Fund | International Conservative Fund |

| (1) The Fund is “non-diversified.” | Same. |

| (2) The Fund may not invest more than 25% of the value of its respective assets in any particular industry (other than U.S. government securities and/or foreign sovereign debt securities). | Same. |

| (3) The Fund may not invest directly in real estate or interests in real estate; however, the Fund may own debt or equity securities issued by companies engaged in those businesses. | Same. |

| (4) The Fund may not purchase or sell physical commodities other than foreign currencies unless acquired as a result of ownership of securities (but this limitation shall not prevent the Fund from purchasing or selling options, futures, swaps and forward contracts or from investing in securities or other instruments backed by physical commodities). | Same. |

| (5) The Fund may not lend any security or make any other loan, except to the extent permitted by the 1940 Act, the rules and regulations thereunder, and any applicable exemptive relief. | Same. |

| Acquiring Fund | Acquired Fund |

| Conservative Fund | International Conservative Fund |

| (6) The Fund may not act as an underwriter of securities issued by others, except to the extent that the Fund may be deemed an underwriter in connection with the disposition of portfolio securities. | Same. |

| (7) The Fund may not issue senior securities, except to the extent permitted by the 1940 Act, the rules and regulations thereunder, and any applicable exemptive relief. | Same. |

| (8) The Fund may not borrow money, except to the extent permitted by the 1940 Act, the rules and regulations thereunder, and any applicable exemptive relief. | Same. |

The performance information shown below provides some indication of the risks of investing in each Fund by showing changes in the Funds’ performance from year to year and by showing how each Fund’s average annual returns compared with those of a broad measure of market performance. Past performance is not an indication of future performance.

The returns shown in the bar chart and table do not include charges imposed under the Contracts. If these amounts were reflected, returns would be less than those shown.

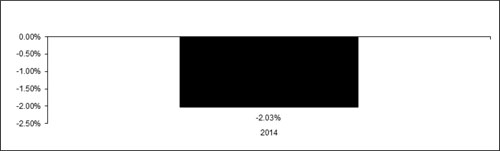

International Conservative Fund – Calendar Year Total Returns |

|

Best Quarter (ended 6/30/2014): 4.33%; Worst Quarter (ended 9/30/2014): -4.64% |

Conservative Fund – Calendar Year Total Returns |

|

Best Quarter (ended 6/30/2014): 2.95%; Worst Quarter (ended 6/30/2013): -3.23% |

| International Conservative Fund – Average Annual Total Returns as of December 31, 2014 |

| | 1 year | Life of Fund (April 29, 2013) |

| International Conservative Fund | -2.03% | 2.34% |

| Dow Jones Moderately Conservative Index | 4.78% | 5.31% |

| 20% MSCI All Country World Index ex-US (Net), 80% Citigroup Non-U.S. Dollar World Government Bond Index | -2.87% | -1.28% |

| Citigroup Non-U.S. Dollar World Government Bond Index | -2.68% | -2.32% |

| MSCI All Country World Index ex-US (Net) | -3.87% | 2.70% |

| Conservative Fund – Average Annual Total Returns as of December 31, 2014 |

| | 1 year | Life of Fund (February 6, 2012) |

| Conservative Fund | 3.71% | 3.69% |

| Barclays U.S. Aggregate Bond Index | 5.97% | 2.51% |

The following table shows the capitalization of each Fund as of June 30, 2014 and of the Conservative Fund on a pro forma combined basis as of June 30, 2014 after giving effect to the proposed Reorganization. The actual net assets of the International Conservative Fund and the Conservative Fund on the Closing Date will differ due to fluctuations in net asset values, subsequent purchases, and redemptions of shares. No assurance can be given as to how many shares of the Conservative Fund will be received by shareholders of International Conservative Fund on the Closing Date, and the following table should not be relied upon to reflect the number of shares of Conservative Fund that will actually be received.

| | Net Assets | Net Asset Value Per Share | Shares Outstanding |

| International Conservative Fund | $3,457,091 | $10.35 | 334,163 |

| Conservative Fund | $76,826,647 | $11.15 | 6,892,548 |

| Adjustments | $0 (a) | | (24,110) (b) |

Pro forma Conservative Fund (assuming the Reorganization is approved) | $80,283,738 | $11.15 | 7,202,601 |

(a) The costs and expenses associated with the Reorganization relating to preparing, filing, printing and mailing of material, disclosure documents and related legal fees, including the legal fees incurred in connection with the analysis under the Code of the taxability of this transaction and the preparation of the tax opinion, and obtaining a consent of independent registered public accounting firm will be borne by JNAM. No sales or other charges will be imposed on Contract Owners in connection with the Reorganization.

(b) The adjustment to the pro forma shares outstanding number represents a decrease in shares outstanding of the International Conservative Fund to reflect the exchange of shares of the Conservative Fund.

The Reorganization provides for the acquisition of all the assets and all the liabilities of the International Conservative Fund by the shareholders of the Conservative Fund. If the Reorganization had taken place on June 30, 2014, the shareholders of the International Conservative Fund would have received 310,053 shares of the Conservative Fund.

After careful consideration, the Trust’s Board of Trustees unanimously approved the Plan of Reorganization with respect to the International Conservative Fund. Accordingly, the Board has submitted the Plan of Reorganization for approval by the International Conservative Fund’s shareholders. The Board recommends that you vote “FOR” this Proposal.

* * * * *

The terms of the Plan of Reorganization are summarized below. The summary is qualified in its entirety by reference to the Plan, a copy of which is attached as Appendix A.

If shareholders of the Acquired Fund approve the Plan of Reorganization, then the assets of the Acquired Fund will be acquired by, and in exchange for, shares of the Acquiring Fund and the liabilities of the Acquired Fund will be assumed by the Acquiring Fund. The Acquired Fund will then be terminated by the Trust, and the shares of the Acquiring Fund distributed to the shareholders of the Acquired Fund in the redemption of the Acquired Fund shares. Immediately after completion of the Reorganization, the number of shares of the Acquiring Fund then held by former shareholders of the Acquired Fund may be different than the number of shares of the Acquired Fund that had been held immediately before completion of the Reorganization, but the total investment will remain the same (i.e., the total value of the Acquiring Fund shares held immediately after the completion of the Reorganization will be the same as the total value of the Acquired Fund shares formerly held immediately before completion of the Reorganization).

It is anticipated that the Reorganization will be consummated as of the close of business on April 24, 2015, or on a later date the Trust decides upon (the “Closing Date”), subject to the satisfaction of all conditions precedent to the closing. It is not anticipated that the Acquired Fund will hold any investment that the Acquiring Fund would not be permitted to hold (“non-permitted investments”).

The shareholders of each Acquired Fund will receive shares of the Acquiring Fund in accordance with the procedures provided for in the Plan of Reorganization. Each such share will be fully paid and non-assessable by the Trust when issued and will have no preemptive or conversion rights.

The Trust may issue an unlimited number of full and fractional shares of beneficial interest of the Fund and divide or combine such shares into a greater or lesser number of shares without thereby changing the proportionate beneficial interests in the Trust. Each share of the Fund represents an equal proportionate interest in the Fund with each other share. The Trust reserves the right to create and issue any number of Fund shares. In that case, the shares of the Fund would participate equally in the earnings, dividends, and assets of the Fund. Upon liquidation of the Fund, shareholders are entitled to share pro rata in the net assets of the Fund available for distribution to shareholders. The Acquiring Fund is a series of the Trust.

The Trust currently offers one class of shares. The Trust has adopted, in the manner prescribed under Rule 12b-1 under the 1940 Act, a plan of distribution pertaining to shares of the Acquiring Fund. The maximum distribution and/or service (12b-1) fee for the Acquiring Fund’s shares is currently equal to an annual rate of 0.25% of the average daily net assets attributable to those shares. Because these distribution/service fees are paid out of the Acquiring Fund’s assets on an ongoing basis, over time these fees will increase your cost of investing and may cost more than paying other types of charges.

At meetings of the Trust's Board of Trustees held on January 4 and January 8, 2015, the Trustees, all of whom are not "interested persons" (as that term is defined in the 1940 Act) of the Trust ("Independent Trustees"), considered materials and discussed the potential benefits to the shareholders of the Acquired Fund under the proposed Reorganization. The Reorganization is part of an overall rationalization of the Trust's offerings and service providers, and is designed to eliminate inefficiencies arising from offering overlapping funds with similar investment objectives and investment strategies that serve as investment options for the Contracts issued by the Insurance Companies and certain qualified and nonqualified plans. The Reorganization also seeks to increase assets under management in the Acquiring Fund and seeks to achieve additional economies of scale. In addition, the Acquiring Fund has generally performed better when compared to its benchmark than has the Acquired Fund. The objective of the Reorganization is to seek to ensure that a consolidated family of investments offers a streamlined, complete, and competitive set of underlying investment options to serve the interests of shareholders and Contract Owners. Approval of the Reorganization requires the affirmative vote of a majority of the outstanding voting securities of the Acquired Fund. In determining whether to recommend approval of the Reorganization, the Board considered many factors, including:

| · | Investment Objectives and Investment Strategies. The Board noted that the Reorganization will permit the Contract Owners with beneficial interest in the Acquired Fund to continue to invest in a professionally managed fund with similar investment goals to that of the Acquired Fund, noting that the Acquired Fund seeks total return, consistent with preservation of capital, through a predominant allocation in international bonds, stocks and other asset classes and strategies through investment in Underlying Funds, and the Acquiring Fund seeks the generation of income through investment in Underlying Funds. The Board noted that while the Acquiring Fund does not invest exclusively in international Underlying Funds, the Acquiring Fund is globally diverse and maintains exposure to international equities and bonds. The Board also discussed that the Funds have the same fundamental policies. For a full description of the investment objectives and investment strategies of the Acquired Fund and Acquiring Fund, see "Comparison of Investment Objectives, Policies and Strategies." |

The Board considered management's desire to streamline the Curian fund lineup. It discussed that since the Acquired Fund has not attracted an appropriate amount of assets, the Acquiring Fund, which offers a more diversified global exposure, will be a suitable alternative to the Acquired Fund's shareholders. The Board discussed how the risk profile of the Combined Fund will compare to that of the Acquired Fund and that the Combined Fund will have lower risk volatility.

| · | Operating Expenses. The Board noted that the Reorganization will result in a gross expense ratio that is lower than that of the Acquired Fund currently and a net expense ratio that is the same as that of the Acquired Fund currently. The Board discussed how acquired fund fees and expenses affect the Funds' expense ratios and took into account management's assertion that the Acquiring Fund is expected to continue to invest in the same Underlying Funds after the Reorganization as it does currently. The Board considered that, as of the fiscal year ended December 31, 2013, the Acquired Fund had a total expense ratio that was higher than the total expense ratio of the Acquiring Fund. See "Comparative Fee and Expense Tables." The Board noted that the Funds have the same management fee schedule. |

| · | Larger Asset Base. The Board noted that the Reorganization may benefit Contract Owners and others with beneficial interests in the Acquired Fund by allowing them to invest in the Combined Fund with a larger asset base than that of the Acquired Fund currently. As of October 31, 2014, the Acquired Fund had assets of $4.7 million, as compared to assets of $99.3 million for the Acquiring Fund. The Board considered management's belief that because the Acquired Fund has lower prospects for growth, reorganizing the Acquired Fund into the Acquiring Fund is the best way to offer Contract Owners and other investors the ability to achieve economies of scale. |

| · | Performance. The Board noted that the Acquiring Fund has better historical risk-adjusted performance than the Acquired Fund. The Board considered each Fund's performance compared to its benchmark, noting that the Acquired Fund underperformed its benchmark and the Acquiring Fund during the year-to-date and one-year periods ended October 31, 2014. The Board also noted the Acquired Fund has a relatively short track record, as its inception was in April 2013. The Board also noted that the same portfolio management team currently managing the Acquiring Fund is expected to continue to manage the Combined Fund after the Reorganization. |

| · | Investment Adviser and Other Service Providers. The Funds currently have the same investment adviser and administrator, Curian Capital, and other service providers. After the Reorganization, it is proposed that the Combined Fund will have a different investment adviser, JNAM. This change of investment adviser is being considered by shareholders of the Trust via a separate proxy statement. See "Comparison of Investment Adviser." The custodian for the Acquiring Fund, JPMorgan Chase Bank, N.A., is the same as for the Acquired Fund and will remain the same after the Reorganization. The transfer agent for the Acquiring Fund, JNAM, is the same as for the Acquired Fund and will remain the same after the Reorganization. The distributor for shares of the Acquiring Fund, Jackson National Life Distributors LLC, is the same as for the Acquired Fund and will remain the same after the Reorganization. |

| · | Tax-Free Reorganization. The Reorganization will have no tax effect on Contract Owners or others with beneficial interests in the Acquired Fund. |

| · | Costs of Reorganization. The expenses of the Reorganization will be borne by JNAM, and no sales or other charges will be imposed on Contract Owners in connection with the Reorganization. |

In summary, in determining whether to recommend approval of the Reorganization, the Board considered factors including (1) the terms and conditions of the Reorganization and whether the Reorganization would result in dilution of the Funds' shareholders', Contract Owners' and plan participants' interests; (2) the compatibility of the Funds' investment objectives, investment strategies and investment restrictions, as well as shareholder services offered by the Fund; (3) the expense ratios and information regarding the fees and expenses of the Funds; (4) the advantages and disadvantages to the Funds' shareholders, Contract Owners and plan participants of having a larger asset base in the Combined Fund; (5) the relative historical performance of the Funds; (6) the management of the Funds; (7) the federal tax consequences of the Reorganization; and (8) the costs of the Reorganization. The Board also considered alternative options available for the Acquired Fund.

For the reasons described above, the Board, comprised solely of Independent Trustees, determined that the Reorganization would be in the best interests of the Acquired Fund and the Acquiring Fund and that the interests of the Acquired Fund's and Acquiring Fund's Contract Owners and other investors would not be diluted as a result of effecting the Reorganization. At the Board meeting held on January 8, 2015, the Board voted unanimously to approve the Reorganization and recommended its approval by Contract Owners and others with beneficial interests in the Acquired Fund.

A Fund’s performance may be affected by one or more risk factors. For a detailed description of a Fund’s risk factors, please see Appendix B “More Information on Strategies and Risk Factors.”

The Reorganization is intended to qualify for federal income tax purposes as a tax-free reorganization under Section 368(a) of the Code.

As a condition to consummation of the Reorganization, the Trust will receive an opinion from K&L Gates LLP (“Counsel”), with respect to the Reorganization and the Funds participating therein and their shareholders, substantially to the effect that, based on the facts and assumptions stated therein as well as certain representations of the Trust and conditioned on the Reorganization being completed in accordance with the Plan of Reorganization, for federal income tax purposes: (1) the Reorganization will qualify as a “reorganization” (as defined in Section 368(a)(1) of the Code), and each Fund will be a “party to a reorganization” (within the meaning of Section 368(b) of the Code); (2) neither Fund will recognize any gain or loss on the Reorganization; (3) the Acquired Fund shareholders will not recognize any gain or loss on the exchange of their Acquired Fund Shares for Acquiring Fund Shares; (4) the holding period for and tax basis in the Acquiring Fund Shares that the Acquired Fund shareholder receives pursuant to the Reorganization will include the holding period for, and will be the same as the aggregate tax basis in, the Acquired Fund Shares that the shareholder holds immediately before the Reorganization (provided, with respect to inclusion of the holding period, the shareholder holds the shares as capital assets on the applicable Closing Date); and (5) the Acquiring Fund’s tax basis in each asset the Acquired Fund transfers to it will be the same as the Acquired Fund’s tax basis therein immediately before the Reorganization, and the Acquiring Fund’s holding period for each such asset will include the Acquired Fund’s holding period therefore (except where the Acquiring Fund’s investment activities have the effect of reducing or eliminating an asset’s holding period). Notwithstanding clauses (2) and (5), such opinion may state that no opinion is expressed as to the effect of a Reorganization on the Funds or the Acquired Fund shareholders with respect to any transferred asset as to which any unrealized gain or loss is required to be recognized for federal income tax purposes at the end of a taxable year (or on the termination or transfer thereof) under a mark-to-market system of accounting.

Contract Owners who had premiums or contributions allocated to the investment divisions of the Separate Accounts as well as others that are invested in Acquired Fund Shares generally will not recognize any gain or loss as a result of the Reorganization. If the Acquired Fund sells securities before its Reorganization, it may recognize net gains or losses. Any net gains recognized on those sales would increase the amount of any distribution that the Acquired Fund must make to its shareholders before consummating its Reorganization.

As a result of the Reorganization, the Acquiring Fund will succeed to certain tax attributes of the Acquired Fund, except that the amount of the Acquired Fund’s accumulated capital loss carryforwards (plus any net capital loss that Acquired Fund sustains during its taxable year ending on the applicable Closing Date and any net unrealized built-in loss it has on that date) that the Acquiring Fund may use to offset capital gains it recognizes after its Reorganization may be subject to an annual limitation under Sections 382 and 383 of the Code.

If a Reorganization fails to meet the requirements of Code Section 368(a)(1), a Separate Account that is invested in shares of the Acquired Fund involved therein could realize a gain or loss on the transaction equal to the difference between its tax basis in those shares and the fair market value of the Acquiring Fund Shares it receives.

The Trust has not sought a tax ruling from the Internal Revenue Service (“IRS”) but instead is acting in reliance on the opinion of Counsel discussed above. That opinion is not binding on the IRS or the courts and does not preclude the IRS from adopting a contrary position. Contract Owners and other investors are urged to consult their tax advisers as to the specific consequences to them of the Reorganization, including the applicability and effect of state, local, foreign and other taxes.

If the Reorganization is not approved by shareholders, the Board will consider what actions are appropriate until there is adequate time to take further action.

This section provides information about the Trust and the Adviser for the Acquiring Fund.

The Trust is organized as a Massachusetts business trust and is registered with the SEC as an open-end management investment company. Under Massachusetts law and the Trust’s Declaration of Trust and By-Laws, the management of the business and affairs of the Trust is the responsibility of the Board of Trustees. The Acquiring Fund is a series of the Trust.

Curian Capital, LLC, 7601 Technology Way, Denver, Colorado 80237, is the current investment adviser to the Trust and provides the Trust with professional investment supervision and management. The Adviser is a wholly owned subsidiary of Jackson National, which is in turn a wholly owned subsidiary of Prudential plc, a publicly traded company incorporated in the United Kingdom. Prudential plc is not affiliated in any manner with Prudential Financial Inc., a company whose principal place of business is in the United States of America. Prudential plc is also the ultimate parent of Jackson National Asset Management, LLC, the sponsor of investment companies that are in the same group of investment companies as the Trust, M&G Investment Management Limited, PPM America, Inc. and Eastspring Investments (Singapore) Limited.

Curian Capital acts as investment adviser to the Trust pursuant to an Investment Advisory and Management Agreement. The Investment Advisory and Management Agreement continues in effect for each Fund from year to year after its initial two-year term so long as its continuation is approved at least annually before December 31 by (i) a majority of the Trustees who are not parties to such agreement or interested persons of any such party except in their capacity as Trustees of the Trust, and (ii) the shareholders of the affected Fund or the Board of Trustees. It may be terminated at any time upon 60 days notice by the Adviser, the Trust, or by a majority vote of the outstanding shares of a Fund with respect to that Fund, and will terminate automatically upon assignment. Additional Funds may be subject to a different agreement. The Investment Advisory and Management Agreement provides that the Adviser shall not be liable for any error of judgment, or for any loss suffered by any Fund in connection with the matters to which the agreement relates, except a loss resulting from willful misfeasance, bad faith or gross negligence on the part of the Adviser in the performance of its obligations and duties, or by reason of its reckless disregard of its obligations and duties under the agreement. As compensation for its services, the Trust pays the Adviser a fee in respect of each Fund as described in that Fund’s Prospectus.

There is a shareholder proposal in a separate proxy statement that has been sent out to all shareholders of the Trust that is asking for approval of a new investment advisory agreement with respect to each fund of the Trust. If this proposal is approved by shareholders, the new investment adviser of the Acquiring Fund will be an affiliate of Curian Capital, JNAM, effective as of April 27, 2015. The terms of the Investment Advisory and Management Agreement with JNAM will be identical to the terms of the current Curian Capital Investment Advisory and Management Agreement.

The Acquiring Fund’s investments are selected by the Adviser. The following table describes the Acquiring Fund’s portfolio managers and the portfolio managers’ business experience. Information about the portfolio managers’ compensation, other accounts they manage, and their ownership of securities of the Acquiring Fund is available in the Trust’s Statement of Additional Information dated April 28, 2014, as supplemented.

| Acquiring Fund | Portfolio Managers | Business Experience |

| Conservative Fund | Curian Capital, LLC 7601 Technology Way Denver, Colorado 80237 James W. Gilmore, CFA William Harding, CFA Jonathan Shiffer, MBA | James W. Gilmore, CFA, Vice President and Portfolio Manager is responsible for portfolio construction and asset allocation of the Funds. Mr. Gilmore brings over 30 years of investment experience in all aspects of the investment process, including due diligence, manager selection, performance measurement, portfolio optimization and portfolio management. Mr. Gilmore has been actively involved in the Asset Management Group since his arrival at Curian in 2011. Mr. Gilmore’s past experience includes Senior Consultant with NEPC, LLC from January 2008 through November 2011. In this role, he led public pension, corporate pension, labor union pension and defined contribution clients in the portfolio allocation and management process. He counseled over $12 billion in assets utilizing traditional and alternative asset classes in the process. Prior to NEPC, LLC, he was employed at Stonebridge Investment Partners from September 2005 through January 2008. Additional experience was acquired during assignments with New York Life Investment Management, Columbia Management Company and Morley Capital Management. William Harding, Vice President of Curian Capital and Vice President and Head of Investment Management for JNAM, is a dual employee of Curian Capital and JNAM. Mr. Harding leads the Investment Management function at JNAM is responsible for oversight of sub-adviser performance and risk, due diligence, and manager research. Mr. Harding was previously the Head of Manager Research for Morningstar Inc.’s Investment Management division and has over 13 years of investment experience including asset allocation, manager research, portfolio management, and performance evaluation. Mr. Harding graduated from the University of Colorado, Boulder with a Bachelor of Science degree in Business. He holds an MBA from Loyola University Chicago and he is a Chartered Financial Analyst. Jonathan Shiffer, MBA, Vice President and Portfolio Manager for Curian Capital, is responsible for overseeing the firm’s activities related to Curian Capital’s proprietary investment strategies. Mr. Shiffer has over 15 years of experience in the investment management industry. Prior to joining Curian Capital in 2012, Mr. Shiffer served as Chief Investment Officer for Rushmore Investment Advisors Inc., an institutional money management firm, where he supervised portfolio management, research, trading, and portfolio operations staff. Mr. Shiffer joined Rushmore from First Union Securities where he worked as a client portfolio manager responsible for equity & debt research, manager due diligence, and portfolio allocation. Mr. Shiffer received his Bachelor of Science in business and Masters of Business Administration from the University of Texas at Dallas. |

As compensation for its services, the Adviser receives a fee from the Trust computed separately for the Acquiring Fund, accrued daily and payable monthly. The fee the Adviser receives from the Acquiring Fund is set forth below as an annual percentage of the net assets of the Acquiring Fund.

| Acquiring Fund | Assets | Advisory Fee (Annual Rate Based on Average Net Assets) |

| Conservative Fund | $0 to $500 million Over $500 million | 0.15% 0.10% |

In addition to the investment advisory fee, the Acquiring Fund pays to Curian Capital (“Administrator”) an Administrative Fee as an annual percentage of the average daily net assets of the Fund as set forth below.

| Acquiring Fund | Assets | Administrative Fee (Annual Rate

Based on Average Net Assets) |

| Conservative Fund | All Assets | 0.10% |

In return for the Administrative Fee, the Administrator provides or procures all necessary administrative functions and services for the operation of the Funds. In addition, the Administrator, at its own expense, arranges and pays for routine legal, audit, fund accounting, custody (except overdraft and interest expense), printing and mailing, a portion of the Chief Compliance Officer costs and all other services necessary for the operation of each Fund. Each Fund is responsible for trading expenses, including brokerage commissions, interest and taxes, and other non-operating expenses. Each Fund is also responsible for nonrecurring and extraordinary legal fees, registration fees, licensing costs, a portion of the Chief Compliance Officer costs, directors and officers insurance, the fees and expenses of the Independent Trustees and of independent legal counsel to the Independent Trustees.

The Trust has adopted, in accord with the provisions of Rule 12b-1 under the 1940 Act, a Distribution Plan (“Plan”). The Board of Trustees, including all of the Independent Trustees, must approve, at least annually, the continuation of the Plan. Under the Plan, certain Funds will pay a Rule 12b-1 fee at an annual rate of up to 0.25% of the Fund’s average daily net assets attributed to interests, to be used to pay or reimburse distribution and administrative or other service expenses with respect to interests. Jackson National Life Distributors LLC (the “Distributor”), as principal underwriter, to the extent consistent with existing law and the Plan, may use the Rule 12b-1 fee to reimburse fees or to compensate broker-dealers, administrators, or others for providing distribution, administrative or other services. Under the Plan, the Acquired Fund and the Acquiring Fund do not pay a Rule 12b-1 fee.

The Distributor receives payments from certain of the sub-advisers to assist in defraying the costs of certain promotional and marketing meetings in which they participate. The amounts paid depend on the nature of the meetings, the number of meetings attended, the costs expected to be incurred, and the level of the sub-adviser’s participation. A brokerage affiliate of the Distributor participates in the sales of shares of retail mutual funds advised by certain of the sub-advisers and receives selling and other compensation from them in connection with those activities, as described in the prospectus or statement of additional information for those funds. In addition, the Distributor acts as distributor of the Contracts issued by the Insurance Companies.

Only Separate Accounts, registered investment companies, and qualified and certain non-qualified plans of the Insurance Companies may purchase shares of the Acquiring Fund. If an investor invests in the Fund under a

Contract or a plan that offers a Contract as a plan option through a broker-dealer or other financial intermediary (such as a bank), the Fund and its related companies may pay the intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and the salesperson to recommend the Fund over another investment.