Exhibit 99.5

Information related to Worldpay, Inc.’s business and operations

and information related to certain material regulatory matters related to Worldpay, Inc.’s business

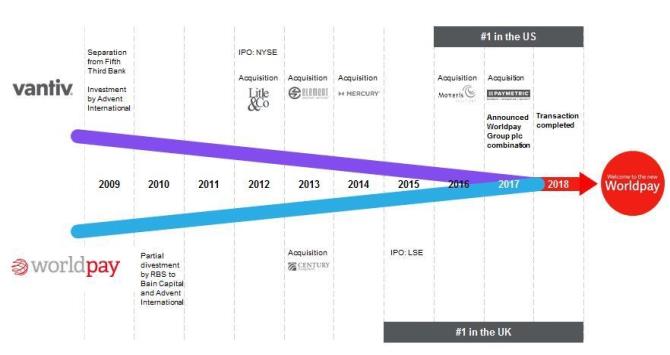

Worldpay, Inc., formerly Vantiv, Inc., a Delaware corporation, is a holding company that conducts its operations through its majority-owned subsidiary, Worldpay Holding, LLC (“Worldpay Holding”). On January 16, 2018, we completed the previously announced acquisition of all of the outstanding shares of Worldpay Group Limited, formerly Worldpay Group plc, a public limited company and changed our name to Worldpay, Inc. Worldpay, Inc., Worldpay Holding and their subsidiaries are referred to collectively as the “Company,” “Worldpay,” “we,” “us” or “our,” unless the context requires otherwise.

Business and Client Description

Worldpay, Inc. is a leading payments technology company. We process over 40 billion transactions annually, supporting more than 300 payment types across 146 countries and 126 currencies. According to the Nilson Report, we are the largest merchant acquirer globally by number of transactions, and the largest PIN debit acquirer by number of transactions in the United States.

We are a payments innovator, differentiated by our global reach, innovative technology and tailored solutions. Our leading competitive position and differentiated solutions have enabled us to achieve unique advantages in fast-growing and strategically-important segments of the payments market, including capabilities in global eCommerce, a first-mover advantage in U.S. Integrated Payments, and Enterprise payments and data security solutions inbusiness-to-business (B2B) payments.

Our solutions bring together advanced payments technologies at each stage of the transaction life cycle. We enable acceptance by integrating software and delivering omni-channel solutions that allow merchants to transact online, via mobile andin-store. Our innovative and proprietary suite of payments technology enables our clients to increase their revenue by improving authorization rates while simultaneously lowering transaction costs. We offer numerous dynamic funding options and enable real-time payouts at settlement. We use advanced data analytics and machine learning to continuously evolve our capabilities, and we offer additional value-added services, including prepaid services and gift card solutions, to help our clients operate and manage their businesses more profitably. We also provide security solutions, such aspoint-to-point encryption, tokenization, and fraud prevention services, at each stage of the transaction lifecycle, in order to help our clients protect their revenue.

Our global reach, innovative technology and tailored solutions create our client value proposition. Our global reach makes it easy for our clients to expand into new markets and to simplify the back-office operations. We employ the most advanced payments technologies to help our clients increase their revenue while minimizing costs. Our flexible and client-centered technology platforms enable ourin-country vertical-specific and technical experts to develop tailored solutions that solve our clients’ most complex needs.

Our Segments

Our business is organized into three segments, Technology Solutions, Merchant Solutions and Issuer Solutions. Our Technology Solutions and Merchant Solutions segments provide merchant acquiring, payment processing and related services to a diverse set of merchants worldwide, while our Issuer Solutions segment primarily serves financial institutions, including regional banks, community banks, credit unions and regional personal identification number (“PIN”) networks.

Within our Technology Solutions and Merchant Solutions segments, we enable merchants of all sizes to accept electronic payments, including credit, debit and prepaid payments originated at the physicalpoint-ofsale-as well as incard-not-present (CNP) eCommerce and mobile environments. Per the chart below, our services include all aspects of payment processing, including authorization and settlement, customer service, chargeback and retrieval processing, reporting for electronic payment transactions and network fee and interchange management. We also provide our merchants with value-added services, such as security and fraud prevention solutions, advanced data analytics and information management solutions, foreign currency management and numerous funding options.

Within our Issuer Solutions segment, we supply payment services to financial institutions, including card issuer processing, payment network processing, fraud protection, card production, prepaid program management, ATM driving, and network gateway and switching services that utilize our proprietary Jeanie PIN debit payment network.

Technology Solutions

Our Technology Solutions segment serves a diverse set of merchants that primarily accept payments through advanced technology-enabled solutions, typically encompassingcard-not-present (CNP) eCommerce and mobile solutions, integrated payments, or electronicbusiness-to-business payments solutions. Within this segment, we enable payments to merchants primarily by integrating into their global eCommerce environments or through their enterprise software.

Our Technology Solutions client base is highly diversified with low client concentration and includes global enterprises as well as small to medium sized businesses. Our Technology Solutions segment utilizes broad and varied distribution channels, including direct sales forces as well as multiple referral partner relationships that provide us with a growing and diverse client base.

Merchant Solutions

Our Merchant Solutions segment serves a diverse set of merchants that primarily accept paymentsin-store within the U.S. and U.K., including complex multi-lane retail environments. Within this segment, we enable payments to merchants primarily through integration into technology environments that include physical terminals.

Our Merchant Solutions client base has low client concentration and is heavily weighted innon-discretionary everyday spend categories, such as grocery and pharmacy, and includes thirteen of the United States’ top 25 national retailers by revenue in 2018. Our Merchant Solutions segment utilizes broad and varied distribution channels, including direct sales forces and multiple referral partners.

Issuer Solutions

Our Issuer Solutions segment provides card issuer processing, payment network processing, fraud protection and card production to a diverse set of financial institutions, including regional banks, community banks, credit unions and regional personal identification number (“PIN”) networks. We process and service a wide range of credit, debit, ATM and prepaid transactions for our clients, and also provide card and statement production, collections and inbound/outbound call centers. Other services we provide include ATM driving, portfolio optimization, data analytics and card program marketing. We also provide network gateway and switching services that utilize our Jeanie PIN network, which offers real-time electronic payment, network bill payment, single point settlement, shared deposit taking and customer select PINs.

- 2 -

Our Issuer Solutions segment generally focuses on small tomid-sized financial institutions with less than $15 billion in assets. Smaller financial institutions generally do not have the scale or infrastructure typical of large institutions and are more likely to outsource their payment processing needs. Our Issuer Solutions segment utilizes broad and varied distributions channels, including direct sales forces and multiple referral partners.

Sales and Marketing

We distribute our services through multiple sales channels that enable us to efficiently and effectively target a growing and diverse client base of merchants and financial institutions. All three segments’ sales channels include direct sales forces and referral partners that sell our solutions. In addition, all three segments offer certain services on a white-label basis which enables them to be marketed under our partners’ brands. We select referral partners that enhance our distribution and augment our services with complementary offerings. We believe our sales structure provides us with broad geographic coverage and access to various industries and verticals.

Our sales teams in all three segments are paid a combination of base salary and commission. As of December 31, 2018, we had approximately 1,900 full-time employees participating in sales and marketing, including sales support personnel. Commissions paid to our sales force are based upon a portion of revenue from new business and cross-selling to existing clients. Residual payments to our referral partners are based upon a portion of revenues earned from referred business. For the year ended December 31, 2018, combined sales force commissions and residual payments represent approximately 63% of total sales and marketing expenses, or $715.7 million.

Our History

Worldpay, Inc. was formed on January 16, 2018 through Vantiv, Inc.’s acquisition of Worldpay Group plc. The strategic rationale for the acquisition included creating a leader in global eCommerce as well as to leverage the predecessor companies’ core strengths to continue to expand across high-growth segments of the payments market. The heritage companies’ technology assets provide a strong, integrated foundation for innovation and growth, enabled by an agile and scalable U.S. platform as well as a flexible, highly advanced global platform. The companies’ leading international eCommerce and U.S. eCommerce capabilities combined to establish a leading global eCommerce player. At the same time, the companies’ Integrated Payments technologicalknow-how and capabilities in the U.S. combined with Legacy Worldpay’s global merchant base enabled the combined company to expand its capabilities into new and high-growth emerging markets.

As a result of the combination, Worldpay is a leader in global eCommerce and serves a diverse set of merchants across a variety ofend-markets, sizes and geographies. It has become the leading global payment solutions provider, powering integrated omni-commerce in the U.S. and Europe, the two largest cross-border payments markets. We are one of the few global businesses able to address merchant’s global complexities, providing payments capabilitiesin-store, online or on a mobile device, and granting merchants access to a global payments network through an agile, integrated, secure, reliable and highly scalable proprietary global payments platform.

- 3 -

We have a history of successfully integrating the technology platforms of acquired companies, including winding down legacy environments and consolidating platforms from other acquisitions onto our core processing architecture. Our skills in technology integration represented a unique and significant competitive advantage, enabling quicker product delivery as well as providing scale, resiliency, and an improved customer experience. As a result, Worldpay’s technology capabilities are differentiated from our competitors’, and enable us to efficiently provide a comprehensive suite of services to merchants and financial institutions of all sizes as well as to innovate, develop and deploy new services, while providing us with significant economies of scale.

Competition

We are a leading payments technology company; we compete with financial institutions and well-established payment processing companies, including Chase Paymentech Solutions, Bank of America Merchant Services, First Data Corporation, Global Payments, Inc., Citi Merchant Services, Barclays, Wells Fargo, Elavon Inc. (a subsidiary of U.S. Bancorp), Total System Services, Inc., Adyen, PayPal, Square, and Stripe in our Technology Solutions and Merchant Solutions segments. The most significant competitive factors in this segment are brand, breadth of features and functionality, data security, price, scalability, service capability and system performance.

In our Issuer Solutions segment, competitors include Fidelity National Information Services, Inc., First Data Corporation, Fiserv, Inc., Jack Henry & Associates, Inc., Mastercard, Inc., Total System Services, Inc. and Visa Debit Processing Service. In addition to competition with direct competitors, we also compete with the capabilities of many larger potential clients to conduct their key payment processing applicationsin-house. The most significant competitive factors in this segment are breadth of services and functionality, data security, flexibility of infrastructure and servicing capability, price, scalability and system performance.

Our Strategy

We are a payments innovator. We develop tailored solutions to solve our client’s most complex problems, and our global reach and innovative technology enable us to create value for our clients across the transaction lifecycle. Together, these create a powerful client value proposition that we will use to grow our business and win market share. We will build on our core strengths to further expand into attractive segments of the market that will have strong secular growth in electronic payments, such as global eCommerce, integrated payments, andbusiness-to-business (B2B) payments.

Following the Worldpay acquisition, we continue to maintain our focus on completing the integration of the two businesses while delivering on our synergy targets. As part of the integration we are now executing a technology strategy, leveraging modular cloud-based technology solutions that provide ease of client connectivity and more quickly enable value-added services. This will allow us to deliver online and offline transactions at significant scale. We are also continuing to invest in our enterprise data capabilities, adding advanced analytics and machine learning, along with other value-added services to drive improved authorization and acceptance for our customers while minimizing fraud.

- 4 -

Industry Background

Electronic Payments

Electronic payments have evolved globally into a large and growing market with favorable secular trends that continue to increase the adoption and use of card-based payment services, such as those for credit, debit and prepaid cards.

This growth is driven by the shift from cash and checks towards card-based and other electronic forms of payment due to their greater convenience, security, enhanced services and rewards and loyalty features. We believe emerging trends, such as the adoption of new technologies and business models, including the growth ofcard-not-present (CNP) transactions in eCommerce and mobile commerce and prepaid services, will also continue to drive growth in electronic payments.

Payment Processing Industry

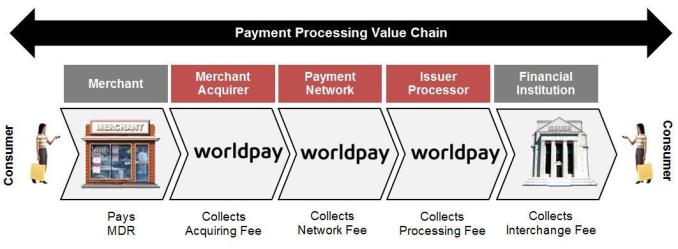

The payment processing industry is comprised of various processors that create and manage the technology infrastructure that enables electronic payments. Payment processors help merchants and financial institutions develop and offer electronic payment solutions to their customers, facilitate the routing and processing of electronic payment transactions and manage a range of supporting security, value-added and back office services. In addition, many large banks manage and process their card accountsin-house. This is collectively referred to as the payment processing value chain.

Many payment processors specialize in providing services in discrete areas of the payment processing value chain, which can result in merchants and financial institutions using payment processing services from multiple providers. A limited number of payment processors have capabilities or offer services in multiple parts of the payment processing value chain. We provide solutions across the payment processing value chain as a merchant acquirer, payment network, and as an issuer processor, primarily by utilizing our innovative technology to enable our clients to easily access a broad range of payment processing services as illustrated below:

The payment processing value chain encompasses three key types of processing:

| • | Merchant Acquiring Processing. Merchant acquiring processors sell electronic payment acceptance, processing and supporting services to merchants and third-party resellers. These processors route transactions originated by consumer transactions with the merchant, including in omni-channel environments that spanpoint-of-sale, eCommerce and mobile devices, to the appropriate payment networks for authorization, known as“front-end” processing, and then ensure that each transaction is appropriately cleared and settled into the merchant’s bank account, known as“back-end” processing. Many of these processors also provide specialized reporting, back office support, risk management and other value-added services, such as fraud prevention, to merchants. Merchant acquirers charge merchants based on a percentage of the transaction value, a specified fee per transaction or a fixed fee, or a combination. Merchant acquirers pay the payment network processors a routing fee per transaction and pass through interchange fees to the issuing financial institution. |

- 5 -

| • | Payment Network Processing. Payment network processors, such as Visa, Mastercard and PIN debit payment networks, sell electronic payment network routing and support services to financial institutions that issue cards and merchant acquirers that provide transaction processing. Depending on their market position and network capabilities, these providers route credit, debit and prepaid card transactions from merchant acquiring processors to the financial institution that issued the card, and they ensure that the financial institution’s authorization approvals are routed back to the merchant acquiring processor and that transactions are appropriately settled between the merchant’s bank and the card-issuing financial institution. These providers also provide specialized risk management and other value-added services to financial institutions. Payment networks charge merchant acquiring processors and issuing financial institutions routing fees per transaction and monthly or annual maintenance fees and assessments. |

| • | Issuer Card Processing. Issuer card processors sell electronic payment issuing, processing and supporting services to financial institutions. These providers authorize transactions received from the payment networks and ensure that each transaction is appropriately cleared and settled from the originating card account. These companies also provide specialized program management, reporting, outsourced customer service, back office support, risk management and other value-added services to financial institutions. Card processors charge issuing financial institutions fees based on the number of transactions processed and the number of cards that are managed. |

Emerging Trends and Opportunities in the Payment Processing Industry

The payment processing industry is adopting new technologies, developing new products and services, evolving new business models and experiencing new market entrants and an evolving regulatory environment. As merchants and financial institutions respond to these changes by seeking services to help them enhance their own offerings to consumers, including the ability to acceptcard-not-present (CNP) payments in eCommerce and mobile environments as well as contactless cards and mobile wallets at thepoint-of-sale, we believe that payment processors will seek to develop additional capabilities in order to capture additional revenue streams by offering additional value added services as well as by expanding across the payment processing value chain. In order to facilitate this expansion, we believe that payment processors will need to enhance their technology platforms so that they can deliver these capabilities and differentiate their offerings from other providers.

We believe that payment processors, like Worldpay, that have scalable, integrated business models, provide solutions across the payment processing value chain and utilize broad distribution capabilities will be best positioned to successfully partner with new market entrants by providing processing services for emerging alternative electronic payment technologies. Further, we believe that Worldpay’s depth of capabilities and breadth of distribution will further enhance its competitive position as emerging payment technologies are adopted by merchants and other businesses. Worldpay’s ability to partner withnon-financial institution enterprises, such as mobile payment providers, internet, retail and social media companies, could create attractive growth opportunities as these new entrants seek to become more active participants in the development of alternative electronic payment technologies and to facilitate the convergence of retail, online, mobile and social commerce applications.

Regulation

The financial services regulatory regime affects our operations and costs. The financial services industry is highly regulated under U.S. and foreign law. Federal, state, local and foreign statutes, regulations, policies and guidance are continually under review by governmental authorities. Changes in the regulatory regime, including changes in how they are interpreted, implemented or enforced, could have a material adverse effect on our business. Violations or perceived weaknesses in compliance or internal controls may result in civil or criminal enforcement action; suspension or revocation of licenses or registrations; limitation, suspension or termination of services; civil or criminal penalties, such as fines; and reputational harm. In addition to governmental regulation, certain of our services are subject to rules set by various payment networks, such as Visa and Mastercard. Many of these aspects of the regulatory regime are described in more detail below.

Licensing and Registration in Multiple Jurisdictions

Our regulatory environment varies from jurisdiction to jurisdiction. In some U.S. and foreign jurisdictions, we are required to obtain and maintain various licenses and registrations to conduct our business. For example, in the United States, we are authorized in multiple U.S. states to engage in debt administration and debt collection activities on behalf of some of our card issuing financial institution clients through calls and letters to the debtors in those states. Our international operations and subsidiaries are subject to a range of licensing, registration and regulatory requirements under U.K., Dutch, European Union (“E.U.”) and other foreign regulatory regimes. We may seek, or be required to obtain, licenses or registrations in other jurisdictions based on changes in our business or the applicable regulatory regime.

- 6 -

As a licensed or registered provider of financial services, we are subject to the exercise of potentiallyfar-reaching discretionary supervisory, regulatory and enforcement powers by numerous U.S. and foreign regulatory authorities. Licensing and regulatory authorities can require, among other things, the provision of detailed information covering our management, business plan, products and services, compliance, internal controls, ownership structure and financial performance. Regulators and other governmental authorities have a range of enforcement powers in the event that we fail to comply with applicable laws and regulations or do not meet their guidance or supervisory expectations.

Dodd-Frank Act

The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (Dodd-Frank Act) made significant structural and other changes to the regulation of the U.S. financial services industry. Those changes included important provisions affecting credit card and debit transactions. For example, the Dodd-Frank Act allows merchants to set minimum dollar amounts (not to exceed $10) for the acceptance of a credit card (and allows federal governmental entities and institutions of higher education to set maximum amounts for the acceptance of credit cards) and to provide discounts or incentives to entice consumers to pay with cash, checks, debit cards or credit cards, as the merchant prefers.

In addition, the “Durbin Amendment” to the Dodd-Frank Act provided that interchange fees that a card issuer or payment network receives or charges for debit transactions are now regulated by the Federal Reserve and must be “reasonable and proportional” to the cost incurred by the card issuer in authorizing, clearing and settling the transaction. The Durbin Amendment also contains prohibitions on network exclusivity and merchant routing restrictions.

Consumer Protection Laws and the Consumer Financial Protection Bureau

Our business is subject to a wide range of consumer protection laws. For example, we are also subject to the Fair Debt Collection Practices Act and similar state laws in connection with our credit card processing business. In addition, the Dodd-Frank Act established the Consumer Financial Protection Bureau (CFPB) to regulate consumer financial services, including many of the types of services offered by our clients. We are subject to regulation and enforcement by the CFPB because we are a service provider to insured depository institutions with assets of $10 billion or more in connection with their consumer financial products and to entities that are larger participants in markets for consumer financial products and services such as prepaid cards. CFPB rules, examinations and enforcement actions may require us to adjust our activities and may increase our compliance costs. In addition to rule making authority over several enumerated federal consumer financial protection laws, the CFPB is authorized to issue rules prohibiting unfair, deceptive or abusive acts or practices by persons offering consumer financial products or services and those, such as us, who are service providers to such persons, and has authority to enforce these consumer financial protection laws and CFPB rules.

Banking and Payment Services Regulation

United States

Although we are not a bank, the U.S. bank regulatory regime affects our business because we provide services to banks. Banking regulators are authorized to examine, supervise and bring enforcement action againstnon-bank companies that perform services for U.S. banks. Because we provide data processing and other services to U.S. banks and financial institutions, we are subject to regular oversight and examination by the Federal Financial Institutions Examination Council (FFIEC). The FFIEC is an inter-agency body of the Federal Deposit Insurance Corporation, the Office of the Comptroller of the Currency, the Board of Governors of the Federal Reserve (Federal Reserve), the National Credit Union Administration and the CFPB. We are also subject to review under state laws and rules governing the provision of services to U.S. banks and other financial institutions, including electronic data processing, back-office services, and use of consumer information. In addition, independent auditors annually review several of our operations to provide reports on internal controls for our clients’ auditors and regulators. Our failure to comply with applicable laws and regulations, or to meet supervisory expectations, may result in adverse action against us by regulators or by the financial institutions to which we provide services.

Our business may also be affected by banking regulation because of Fifth Third Bank’s equity ownership in our Company. Fifth Third Bank is a state-chartered bank and a member of the Federal Reserve System. Fifth Third Bank is regulated, examined and supervised by the Ohio Division of Financial Institutions (ODFI) and the Federal Reserve. Fifth Third Bank is an indirect subsidiary of Fifth Third Bancorp, which is a bank holding company regulated, examined and supervised by the Federal Reserve under the Bank Holding Company Act of 1956 (BHC Act). Depending on the facts and circumstances, a company in which a bank or bank holding company owns equity securities may be subject to banking regulation, supervision, examination and enforcement.

- 7 -

Fifth Third Bank is presumed not to “control” us under the statutory terms of the BHC Act based on its current ownership level. Nevertheless, in the future or in connection with other initiatives, the ODFI or Federal Reserve could assert that our relationship with Fifth Third Bank imposes limitations, conditions or approval requirements under banking laws that affect our activities, investments or acquisitions. The imposition of such limitations, conditions or approval requirements could have an adverse impact on our business, such as by preventing us from pursuing an otherwise attractive acquisition or business opportunity.

The framework by which we would address such circumstances is set forth in the Second Amended and Restated Limited Liability Company Agreement of Worldpay Holding, LLC, as amended by that certain Transaction Agreement, dated August 7, 2017, by and among the Company, Worldpay Holding, Fifth Third Bank and Fifth Third Bancorp (the Worldpay Holding LLC Agreement). Among other things, we must notify Fifth Third Bank before we engage in any business activity (by acquisition, investment or organic growth that may reasonably require Fifth Third Bank or an affiliate of Fifth Third Bank to obtain regulatory approval, so that Fifth Third Bank can consider the legal permissibility of the activity and any required regulatory approvals, and we and Fifth Third Bank must use our respective reasonable best efforts to obtain any such regulatory approvals if we determine to pursue the business activity. The Worldpay Holding LLC Agreement also includes provisions to address circumstances where any such required regulatory approval is not obtained.

The United Kingdom

In the U.K., the Payment Services Regulations 2017 requirenon-bank payment service providers, such as Worldpay, to be authorized as Payment Institutions upon which these regulations impose anon-going system of regulation and control. To comply with these regulations, we have licensed three entities, Worldpay (UK) Limited (WPUKL), Worldpay Limited (WPL) and Worldpay AP Ltd (WPAP), as “Authorized Payment Institutions” and we are authorized to provide certain payment services across the European Economic Area. The FCA has the power to take a range of enforcement actions, including the ability to sanction firms and individuals carrying out functions within the firm. Additionally, WPUKL has a regulated consumer hire business, for which it currently holds the necessary permission under the U.K. Financial Conduct Authority and WPAP is registered with Her Majesty’s Revenue and Customs for the purposes of the Money Laundering, Terrorist Financing and Transfer of Funds (Information on the Payer) Regulations 2017. We are also subject to the Regulation of the European Parliament and the Council on interchange fees for card-based payment transactions (IFR). These interchange fees are a major part of the charges paid by merchants to payment service providers. The Payment Systems Regulator is the competent authority for the monitoring and enforcement of compliance with the IFR in the U.K.

The Netherlands

Worldpay BV (WPBV) is incorporated and registered in the Netherlands and holds a license from the Dutch Central Bank (De Nederlandsche Bank or DNB) for providing payment services. The regulatory system in the Netherlands is a comprehensive system based on the Dutch Financial Supervision Act, which sets out rules regarding the conduct of business supervision (exercised by the Netherlands Authority of Financial Markets (Autoriteit Financiële Markten or AFM)) and prudential supervision exercised by DNB on payment services providers. As WPBV provides payment services in the Netherlands, it is both subject to the supervision of the DNB and the AFM, both of which are empowered to intervene in cases ofnon-compliance with the regulations.

Association and Network Rules

We are subject to the network rules of Visa, Mastercard and other payment networks. The payment networks routinely update and modify their requirements. On occasion, we have received notices ofnon-compliance and fines, which have typically related to excessive chargebacks by a merchant or data security failures. Although these network rules are not government regulations, our failure to comply with the networks’ requirements or to pay the fines they impose could cause the termination of our registration and require us to stop providing payment processing services.

Privacy and Information Security Regulations

We provide services that may be subject to privacy laws and regulations of a variety of U.S. and foreign jurisdictions, including the European Union General Data Protection Regulation (“GDPR”). These laws and regulations restrict the collection, processing, storage, use and disclosure of personal information, require notice to individuals of privacy practices and provide individuals with certain rights to prevent the use and disclosure of protected information. These laws also impose requirements for safeguarding and proper destruction of personal information through the issuance of data security standards or guidelines. For example, relevant U.S. federal privacy laws include the Gramm-Leach-Bliley Act of 1999, which applies directly to a broad range of financial institutions and indirectly, or in some instances directly, to companies that provide services to financial institutions. In addition, there are state laws restricting the ability to collect and utilize certain types of information such as Social Security and driver’s license numbers. U.S. federal and state and foreign laws also impose privacy and data security requirements, which can include obligations to provide notification of security breaches of computer databases that contain personal information to affected individuals, officers and consumer reporting agencies and businesses and governmental agencies that own data. In addition, we are subject to the GDPR, which is the expanded E.U. regime applicable to all foreign companies processing personal data of E.U. residents. GDPR requires companies to maintain a comprehensive data protection and privacy program to protect the personal and sensitive data of European citizens and residents, and failure to comply with GDPR, including country-specific legislation interpreting GDPR, carries significant penalties.

- 8 -

Anti-Corruption, Anti-Money Laundering, Counter Terrorism and Economic Sanctions

We are subject to anti-corruption laws and regulations, including the U.S. Foreign Corrupt Practices Act (FCPA), the UK Bribery Act, and other laws that generally prohibit the making or offering of improper payments to foreign government officials and political figures for the purpose of obtaining or retaining business or to gain an unfair business advantage. We are also subject to anti-money laundering and counter-terrorism financing laws and regulations, including the U.S. Bank Secrecy Act, as amended by the USA PATRIOT Act and EU AML Directives. In addition, we are obligated to comply with economic and trade sanctions programs administered by the U.S Department of Treasury’s Office of Foreign Assets Control (OFAC). As a result, we do not do business to, from, in or with countries or territories subject to comprehensive OFAC trade sanctions (currently, Cuba, Iran, North Korea, Syria and the region of Crimea). In addition, we do not permit as customers nor otherwise do business with any person or entity that is included on OFAC’s list of Specially Designated Nationals and Blocked Persons.

Our regulatory compliance programs and policies are designed to support our compliance with a vast range of laws and regulations. We continually review and enhance our compliance programs to address new and evolving regulations. However, we cannot ensure that our practices will be determined to be compliant by every applicable regulatory authority. In the event our controls fail or we are found to be out of compliance, we could be subject to monetary damages, civil and criminal penalties, litigation, investigations and regulatory proceedings, and damage to our brand and reputation. Furthermore, the evolving and increased regulatory focus on the payments industry could negatively impact or reduce the services we offer and the types of customers who can obtain our services, which could harm our business.

Federal Trade Commission Act and Other Laws Impacting Our and our Customers’ Business

All persons engaged in commerce, including, but not limited to, us and our merchant and financial institution customers are subject to Section 5 of the Federal Trade Commission Act prohibiting unfair or deceptive acts or practices, or UDAP. In addition, there are other laws, rules and or regulations, including the Telemarketing Sales Act and the Unlawful Internet Gambling Enforcement Act of 2006, that may directly impact the activities of our merchant customers and in some cases may subject us, as the merchant’s payment processor, to litigation, investigations, fees, fines and disgorgement of funds in the event we are deemed to have aided and abetted or otherwise provided the means and instrumentalities to facilitate the illegal activities of the merchant through our payment processing services. Various federal and state regulatory enforcement agencies including the Federal Trade Commission, or FTC, and the states’ attorneys general have authority to take action againstnon-banks that engage in UDAP or violate other laws, rules and regulations.

Prepaid Services

Prepaid card programs managed by us are subject to various federal and state laws and regulations, which may include laws and regulations related to consumer and data protection, licensing, consumer disclosures, escheat, anti-money laundering, banking, trade practices and competition and wage and employment. Furthermore, the Credit Card Accountability Responsibility and Disclosure Act of 2009 and the Federal Reserve’s Regulation E impose requirements ongeneral-use prepaid cards, store gift cards and electronic gift certificates. These laws and regulations are sometimes inconsistent and subject to judicial and regulatory challenge and interpretation, and therefore the extent to which these laws and rules have application to, and their impact on, us, financial institutions, merchants or others could change. Prepaid services may also be subject to the rules and regulations of Visa, Mastercard and other payment networks with which we and the card issuers do business. The programs in place to process these products generally may be modified by the payment networks in their discretion and such modifications could also impact us, financial institutions, merchants and others. We are also registered with the Financial Crimes Enforcement Network of the U.S. Department of the Treasury, or FinCEN, as a “money services business-provider of prepaid access.”

Other

We are subject to the Housing Assistance Tax Act of 2008, which requires information returns to be made for each calendar year by merchant acquiring entities. In addition, we are subject to U.S. federal and state unclaimed or abandoned property (escheat) laws which require us to turn over to certain government authorities the property of others we hold that has been unclaimed for a specified period of time such as account balances that are due to a merchant following discontinuation of its relationship with us.

The foregoing list of laws and regulations to which we are subject is not exhaustive, and the regulatory framework governing our operations changes continuously. The enactment of new laws and regulations may increasingly affect the operation of our business, directly and indirectly, which could result in substantial regulatory compliance costs, litigation expense, adverse publicity, the loss of revenue and decreased profitability.

- 9 -

Intellectual Property

Intellectual property is a component of our ability to be a leading payment services provider. We rely on a combination of intellectual property laws, confidentiality procedures and contractual provisions to protect our proprietary technology and our brand. We have registered, or applied for the registration of, U.S., U.K. and other international trademarks, service marks, and domain names and will continue to seek such protection. Additionally, we own issued patents in the U.S., and have filed patent applications in several countries, including the U.S. and U.K., that cover certain of our proprietary technologies related to payment solutions, transaction processing and other products and services. Over time, we have assembled and continue to assemble a portfolio of patents, trademarks, service marks, copyrights, domain names and trade secrets covering our products and services. We do not believe our technology position is dependent on any single patent. We also believe that the life of our patent portfolio is adequate to cover the expected lives of our products and services. Successful third-party claims of intellectual property infringement, including patent infringement, may limit or disrupt our ability to sell our products and services. As such, we defend third party claims of infringement as necessary.

Employees

As of December 31, 2018, we had 8,186 employees globally, of whom 4,331 were located in the U.S. As of December 31, 2018, total employees included 754 in Technology Solutions employees 1,057 Merchant Solutions employees, 85 Issuer Solutions employees, 4,953 IT and Operations employees, and 1,337 general and administrative employees.

- 10 -