Table of Contents

Filed Pursuant to Rule 424 (b) (3)

Registration No. 333- 162821

The information in this preliminary prospectus supplement relates to an effective registration statement under the Securities Act of 1933, as amended, and is not complete and may be changed. This preliminary prospectus supplement and the accompanying prospectus are not an offer to sell nor do they seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION DATED FEBRUARY 2, 2012

PRELIMINARY PROSPECTUS SUPPLEMENT

(To Prospectus dated November 2, 2009)

Copano Energy, L.L.C.

Copano Energy Finance Corporation

$150,000,000

7.125% Senior Notes due 2021

Interest payable April 1 and October 1.

We are offering $150,000,000 of our 7.125% Senior Notes due 2021. The notes will mature on April 1, 2021. Interest on the notes offered hereby will accrue from October 1, 2011 at 7.125% per year, and we will pay interest twice a year, beginning on April 1, 2012.

The notes offered hereby are an additional issue of our outstanding 7.125% Senior Notes due 2021 issued in an aggregate principal amount of $360,000,000 on April 5, 2011. The notes offered hereby will be issued under the same indenture as the outstanding notes and are part of the same series of debt securities. The notes offered hereby will be fungible with the outstanding notes for trading purposes and will trade under the same CUSIP number.

We may redeem some or all of the notes at any time on or after April 1, 2016 at the redemption prices listed in this prospectus supplement, together with accrued and unpaid interest, if any, to the date of redemption, and we may redeem all of the notes at any time prior to April 1, 2016 at the make-whole redemption price specified in this prospectus supplement, together with accrued and unpaid interest, if any, to the date of redemption. In addition, prior to April 1, 2014, we may redeem up to 35% of the aggregate principal amount of the notes with the proceeds of certain equity offerings at the redemption price specified in this prospectus supplement under “Description of Notes – Optional Redemption.” If we sell certain of our assets or experience specific kinds of changes of control, we must offer to repurchase the notes.

The notes are the senior unsecured obligations of Copano Energy, L.L.C. and Copano Energy Finance Corporation, a wholly owned subsidiary of ours that has no material assets and was formed for the sole purpose of being a co-issuer of some of our debt, including the notes. The notes rank equally in right of payment with all of our existing and future senior debt, senior in right of payment to all of our future subordinated debt, effectively junior in right of payment to all of our existing and future secured debt to the extent of the value of the collateral securing such debt and structurally junior in right of payment to all liabilities of our future subsidiaries that do not guarantee the notes. The notes are guaranteed on a senior unsecured basis by each of our existing wholly owned subsidiaries (other than the co-issuer) and certain of our future subsidiaries.

See “Risk Factors” beginning on page S-14 of this prospectus supplement for a discussion of certain risks that you should consider in connection with an investment in the notes.

| Per note | Total | |||||

Public offering price(1) | % | $ | ||||

Underwriting discount | % | $ | ||||

Proceeds to Copano Energy, L.L.C. (before expenses)(1) | % | $ | ||||

| (1) | Plus accrued interest from October 1, 2011. |

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus supplement or the accompanying prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The notes will not be listed on any national securities exchange or quoted on any automated quotation system.

We expect that delivery of the notes will be made to investors in book-entry form through the facilities of The Depository Trust Company on or about , 2012.

Joint book-running managers

| Wells Fargo Securities | BofA Merrill Lynch | Citigroup | ||

J.P. Morgan | RBC Capital Markets | |||

The date of this prospectus supplement is , 2012.

Table of Contents

You should not assume that the information contained in this prospectus supplement, the accompanying prospectus or any free writing prospectus is accurate as of any date other than the date on the front of those documents or that any information that we have incorporated by reference is accurate as of any date other than the date of the document incorporated by reference. Our business, financial condition, results of operations and prospects may have changed since those dates.

We are not making an offer to sell or soliciting offers to buy securities in any jurisdiction where the offer or sale is not permitted.

You should not consider any information contained in or incorporated by reference into this prospectus supplement or the accompanying prospectus to be legal, business or tax advice. You should consult your own attorney, business advisor and tax advisor for legal, business and tax advice regarding an investment in our securities.

Prospectus supplement

| Page | ||||

About this Prospectus Supplement and the Accompanying Prospectus | ii | |||

| iii | ||||

| S-1 | ||||

| S-7 | ||||

| S-10 | ||||

| S-14 | ||||

| S-18 | ||||

| S-19 | ||||

| S-20 | ||||

| S-21 | ||||

| S-62 | ||||

| S-65 | ||||

| S-68 | ||||

| S-73 | ||||

| S-75 | ||||

| S-77 | ||||

| S-77 | ||||

| S-78 | ||||

Prospectus dated November 2, 2009

| 1 | ||||

| 1 | ||||

| 2 | ||||

| 3 | ||||

| 3 | ||||

| 4 | ||||

| 27 | ||||

| 28 | ||||

| 28 | ||||

| 30 | ||||

| 39 | ||||

| 40 | ||||

| 55 | ||||

| 55 |

i

Table of Contents

ABOUT THIS PROSPECTUS SUPPLEMENT AND THE ACCOMPANYING PROSPECTUS

This document is in two parts. The first part is the prospectus supplement, which describes our business and the specific terms of this offering of the notes and also adds to and updates information contained in the accompanying prospectus and the documents incorporated by reference into this prospectus supplement and the accompanying prospectus. The second part, the accompanying prospectus dated November 2, 2009, gives more general information about securities we may offer from time to time, some of which may not apply to this offering.

We are not making an offer to sell securities in any jurisdiction where the offer or sale is not permitted.

Before investing in the notes, you should read both this prospectus supplement and the accompanying prospectus together with the additional information described under the heading “Where You Can Find More Information.”

In making your investment decision, you should rely only on the information contained in or incorporated by reference in this prospectus supplement and the accompanying prospectus and any free writing prospectus prepared by or on behalf of us. To the extent that there is a conflict between the information contained in this prospectus supplement and the information contained in the accompanying prospectus or any earlier-dated document incorporated by reference, you should rely on the information in this prospectus supplement. Neither we nor the underwriters have authorized anyone to provide you with any other information. If anyone provides you with additional, different or inconsistent information, you should not rely on it.

ii

Table of Contents

INFORMATION REGARDING FORWARD-LOOKING STATEMENTS

This prospectus supplement, the accompanying prospectus and the documents we incorporate by reference contain certain “forward-looking statements” within the meaning of the federal securities laws. Statements included in this prospectus supplement, the accompanying prospectus and the documents we incorporate by reference that are not historical facts, but that address activities, events or developments that we expect or anticipate will or may occur in the future, including references to future goals or intentions or other such references, are forward-looking statements. These statements can be identified by the use of forward-looking terminology, including “may,” “believe,” “expect,” “anticipate,” “estimate,” “continue” or similar words. These statements include assertions related to plans for growth of our business, future capital expenditures and competitive strengths and goals. We make these statements based on our past experience and our perception of historical trends, current conditions and expected future developments, as well as other considerations we believe are appropriate under the circumstances. Whether actual results and developments in the future will conform to our expectations is subject to numerous risks and uncertainties, many of which are beyond our control. Therefore, actual outcomes and results could materially differ from what is expressed, implied or forecasted in these statements. Any differences could be caused by a number of factors, including, but not limited to:

| • | the volatility of prices and market demand for natural gas, crude oil and natural gas liquids (“NGLs”), and for products derived from these commodities; |

| • | our ability to continue to connect new sources of natural gas supply and the NGL content of new supplies; |

| • | the ability of key producers to continue to drill and successfully complete and attach new natural gas and NGL supplies; |

| • | our ability to attract and retain key customers and contract with new customers; |

| • | our ability to access or construct new gas processing, NGL fractionation and transportation capacity; |

| • | the availability of local, intrastate and interstate transportation systems and other facilities and services for natural gas and NGLs; |

| • | our ability to meet in-service dates and cost expectations for construction projects; |

| • | our ability to successfully integrate any acquired asset or operations; |

| • | our ability to access our revolving credit facility and to obtain additional financing on acceptable terms; |

| • | the effectiveness of our hedging program; |

| • | general economic conditions; |

| • | force majeure situations such as the loss of a market or facility downtime; |

| • | the effects of government regulations and policies; and |

| • | other financial, operational and legal risks and uncertainties detailed from time to time in our filings with the Securities and Exchange Commission (“SEC”). |

This prospectus supplement, the accompanying prospectus and the documents incorporated by reference include cautionary statements identifying important factors that could cause actual results to materially differ from our expectations, including in conjunction with the forward-looking statements referred to above. When considering forward-looking statements, you should keep in mind the risk factors and other cautionary statements in this prospectus supplement, the accompanying prospectus and the documents we incorporate by reference. All forward-looking statements included in those documents and all subsequent written or oral forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by these cautionary statements. The forward-looking statements speak only as of the date made, and we undertake no obligation to publicly update or revise any forward-looking statements, other than as required by law, whether as a result of new information, future events or otherwise.

iii

Table of Contents

This summary highlights information contained elsewhere or incorporated by reference in this prospectus supplement and the accompanying prospectus. It does not contain all of the information you should consider before making an investment decision. You should read the entire prospectus supplement, the accompanying prospectus, the documents incorporated by reference and any other documents to which we refer for a more complete understanding of this offering and our business. Please read the section entitled “Risk Factors” beginning on page S-14 of this prospectus supplement and contained in our Annual Report on Form 10-K for the year ended December 31, 2010 and our Quarterly Report on Form 10-Q for the quarterly period ended June 30, 2011 for more information about important risks that you should consider before buying the notes in this offering. Throughout this prospectus supplement and the accompanying prospectus, when we use the terms “we,” “us,” “our” or like terms, we are referring either to Copano Energy, L.L.C. or to Copano Energy, L.L.C. and its consolidated subsidiaries collectively, unless otherwise indicated or the context otherwise requires.

Copano Energy, L.L.C.

Overview

We are an energy company engaged in the business of providing midstream services to natural gas producers, including gathering and transportation of natural gas and related services such as compression, dehydration, treating, processing, nitrogen rejection and marketing services. We also provide transportation and fractionation services for natural gas liquids, or NGLs. We were formed in August 2001 as a Delaware limited liability company to acquire entities operating under the Copano name since 1992, and to serve as a holding company for our operating subsidiaries.

Our Operations

Our natural gas pipelines collect natural gas from wellheads or designated points near producing wells. We treat and process natural gas as needed to remove contaminants and to extract mixed NGLs, and we deliver the resulting residue gas to third-party pipelines, local distribution companies, power generation facilities and industrial customers. We sell extracted NGLs as a mixture or as fractionated purity products and deliver them through our plant interconnects or NGL pipelines. We process natural gas from our own gathering systems and from third-party pipelines, and in some cases we deliver natural gas and mixed NGLs to third parties who provide us with transportation, processing or fractionation services.

Our Operating Segments

Through our subsidiaries and equity investments, we own and operate natural gas gathering and intrastate transportation pipeline assets, natural gas processing and fractionation facilities and NGL pipelines. We operate in Texas, Oklahoma, Wyoming and Louisiana. We manage our business and analyze and report our results of operations on a segment basis. Our operations are divided into three operating segments: Texas, Oklahoma and Rocky Mountains.

| • | Texas. Our Texas segment provides midstream natural gas services in south and north Texas, including gathering and transportation of natural gas, and related services such as compression, dehydration, treating, processing and marketing. Our Texas segment also provides NGL fractionation and transportation services. This segment includes our 62.5% interest in Webb/Duval Gatherers, 50% interest in Eagle Ford Gathering LLC (“Eagle Ford Gathering”), 50% interest in Liberty Pipeline Group, LLC (“Liberty Pipeline Group”) and 50% interest in Double Eagle Pipeline LLC (“Double Eagle Pipeline”), as well as a processing plant located in Southwest Louisiana. |

| • | Oklahoma. Our Oklahoma segment provides midstream natural gas services in central and east Oklahoma, including gathering of natural gas and related services such as compression, |

S-1

Table of Contents

dehydration, treating, processing and nitrogen rejection. This segment includes our majority interest in Southern Dome, LLC (“Southern Dome”). |

| • | Rocky Mountains. Our Rocky Mountains segment provides midstream natural gas services in the Powder River Basin of Wyoming, including gathering and treating of natural gas and compressor rental services. This segment includes our 51% interest in Bighorn Gas Gathering, L.L.C. (“Bighorn”) and our 37.04% interest in Fort Union Gas Gathering, L.L.C. (“Fort Union”). |

Our operating segments are summarized in the following table:

Segment | Assets | Pipeline Miles / Number of Processing Plants | Pipeline Throughput/Plant Inlet Capacity(1)(2) | |||||||

Texas | Natural Gas Pipelines(3) | 2,260 | 1,900,400 | |||||||

| Processing Plants | 3 | 1,000,000 | ||||||||

| NGL Pipelines(4) | 370 | 117,000 | ||||||||

Oklahoma | Natural Gas Pipelines | 3,820 | 350,000 | |||||||

| Processing Plants(5) | 7 | 236,000 | ||||||||

Rocky Mountains | Natural Gas Pipelines(6) | 600 | 1,550,000 | |||||||

| (1) | Capacity values generally are based on current operating configurations and could be increased or decreased through addition or removal of compression, delivery meter capacity or other facility modifications. |

| (2) | Natural gas pipeline throughputs and plant inlet capacity are presented in Mcf/d. NGL pipeline throughputs and capacity are presented in Bbls/d. |

| (3) | Includes the 188-mile gathering system owned by Eagle Ford Gathering, an unconsolidated company in which we own a 50% interest, and the 153-mile gathering system owned by Webb/Duval Gatherers, an unconsolidated partnership in which we own a 62.5% interest. |

| (4) | Includes the 87-mile NGL pipeline owned by Liberty Pipeline Group, an unconsolidated company in which we own a 50% interest. |

| (5) | Includes the Southern Dome plant owned by Southern Dome, an unconsolidated company in which we own a majority interest. |

| (6) | Owned by Bighorn and Fort Union, unconsolidated companies in which we own 51.0% and 37.04% interests, respectively. We do not operate Fort Union. |

Our Business Strategy

Our management team is committed to our mission of building a diversified midstream company with scale, stability of cash flows, above-average returns on invested capital and providing secure and growing distributions to our unitholders. Key elements of our strategy include:

| • | Executing on organic growth opportunities and bolt-on acquisitions. We pursue capital projects and complementary acquisitions that we believe will enhance our ability to increase cash flows from our existing assets by capitalizing on our existing infrastructure, personnel and customer relationships. For example, we have completed significant expansions of our assets to capitalize on significant activity in the Eagle Ford Shale, near our Houston Central complex in Texas, in the North Barnett Shale Combo, near our Saint Jo processing plant in Texas, and in the Woodford Shale, near our Mountains gathering systems in Oklahoma, and we have undertaken further expansion in Texas to meet continued demand from Eagle Ford Shale producers. In addition, where our pipelines and processing or fractionation facilities have excess capacity, we have opportunities to increase throughput volume and cash flow with minimal incremental costs. We seek to increase volumes and utilization of capacity by aggressively marketing our services to producers to connect new supplies of natural gas. |

S-2

Table of Contents

| • | Reducing sensitivity to commodity prices. The volatility of natural gas and NGL prices is a key consideration as we enter into new contracts and review opportunities for growth. Our goal is to position ourselves to achieve stable cash flows in a variety of market conditions. Generally, we pursue contracts under which the compensation for our services is not directly dependent on commodity prices. For example, we have focused on replacing commodity-sensitive contracts with fee-based contracts in executing our strategy to increase volumes from the Eagle Ford Shale, the north Barnett Shale Combo play and the Woodford Shale. In addition, we pursue opportunities to increase the fee-based component of our contract portfolio through acquisitions or other growth projects. To the extent that our contracts are commodity sensitive, we use derivative instruments to hedge our exposure to commodity price risk. We have established a product-specific, option-focused portfolio designed to allow us to meet our debt service, maintenance capital expenditure and similar requirements, along with our distribution objectives, despite fluctuations in commodity prices. |

| • | Expanding through greenfield opportunities and strategic acquisitions. We pursue significant greenfield projects that leverage our strengths through alignment with producers and downstream customers. We also pursue potential acquisitions in new regions that we believe will enhance the scale and diversity of our assets or otherwise offer cash flow and operational growth opportunities that are attractive to us. |

| • | Pursuing growth judiciously. We believe that a disciplined approach in selecting new projects will better enable us to choose opportunities that deliver value for our company and our unitholders. In analyzing a particular acquisition, expansion or greenfield project, we consider the operational, financial and strategic benefits of the transaction. Our analysis includes location of the assets or projects, strategic fit in relation to our existing business, expertise and management personnel required, capital required to integrate and maintain the assets involved, and the surrounding competitive environment. From a financial perspective, we analyze the rate of return the assets are expected to generate relative to our cost of capital under various commodity price scenarios, comparative market parameters and the anticipated earnings and cash flow capabilities of the assets. |

| • | Developing and exploiting flexibility in our operations. Flexibility is a fundamental consideration underlying our approach to developing, expanding or acquiring assets. We can modify the operation of our assets to maximize our cash flows. For example, we can operate several of our processing plants in ethane-rejection mode as commodity price environments or operating conditions warrant. In 2010 and 2011, we focused on developing our ability to offer Eagle Ford Shale producers access to multiple natural gas and NGL markets. Multiple residue markets are available at the tailgate of our Houston Central complex, and in 2010 and 2011 we secured alternatives for NGL handling through initiatives such as the startup and expansion of our Houston Central fractionator, our Liberty pipeline project and our execution of third-party fractionation or purchase arrangements for NGLs or purity products, including agreements with petrochemical customers along the Texas Gulf Coast. |

| • | Maintaining a strong balance sheet and access to liquidity. We are committed to pursuing growth in a way that allows us to maintain the strength of our balance sheet and a liquidity position that allows us to execute our business strategy in various commodity price environments. For example, we financed a substantial portion of our Eagle Ford Shale capital expenditures though a private placement of preferred equity with an affiliate of TPG Capital, L.P., which included a paid-in-kind distribution feature that allowed us the flexibility to maintain a strong balance sheet and liquidity position during construction and expansion of our assets and prior to generating cash flow from these projects. |

S-3

Table of Contents

| • | Maintaining an approach to business founded on a culture of integrity, service and creativity. We believe that the dedication of our employees is a critical component of our success. We seek to maintain a company culture that fosters integrity and encourages innovation and teamwork, which we believe will allow us to deliver the superior service required to establish and maintain valued long-term commercial relationships. |

Recent Developments

Recent Eagle Ford Shale projects. We have undertaken various expansion capital projects in Texas to accommodate volume growth from the Eagle Ford Shale play.

| • | Condensate gathering joint venture with Magellan Midstream Partners, L.P. Effective December 15, 2011, we entered into agreements to form Double Eagle Pipeline, a 50/50 joint venture with Magellan Midstream Partners, L.P. (“Magellan”), to provide condensate gathering and product terminalling services to Eagle Ford Shale producers. The joint venture intends to construct a 182-mile pipeline system extending from Gardendale, Texas, in LaSalle County to Three Rivers, Texas, in Live Oak County, Texas then extending north into central DeWitt County, Texas. We will convert to condensate service and dedicate to the joint venture an existing natural gas pipeline that extends from near Three Rivers, Texas to Nueces Bay, Texas, near Corpus Christi. Magellan will dedicate to the joint venture storage assets, as well as marine vessel loading facilities at the Port of Corpus Christi. The pipeline from Three Rivers to Corpus Christi may begin service as early as the fourth quarter of 2012, while the remaining joint venture assets are expected to begin service in the second quarter of 2013. Our 50% share of estimated construction costs associated with the joint venture and our costs to convert our existing pipeline are expected to total approximately $110 million. The joint venture project is supported by long-term customer commitments from two major producers with significant acreage in the rich gas window of the Eagle Ford Shale. |

| • | DK pipeline expansion placed in service in December 2011. In December 2011, we placed into service 58 miles of newly constructed pipeline through Lavaca and Colorado Counties, Texas that directly connect our existing 38-mile DK pipeline in DeWitt and Karnes Counties, Texas to our Houston Central complex. The pipeline extension has increased the DK pipeline’s capacity from 225,000 MMBtu per day to 350,000 MMBtu per day. We have secured firm producer volume commitments for aggregate production of approximately 120,000 MMBtu per day through contracts with an average term of six years, as well as an additional commitment for production from approximately 135,000 gross acres in the Eagle Ford Shale. |

| • | Eagle Ford Gathering pipeline placed in full service in December 2011. Eagle Ford Gathering, our joint venture with Kinder Morgan Energy Partners LP (“Kinder Morgan”), completed construction of a 117-mile pipeline and began limited service in August 2011. Eagle Ford Gathering then placed the pipeline into full service on December 1, 2011. The joint venture has secured fee-based contracts with several producers, which have an average term of 10 years and provide volume commitments of 637,500 MMBtu per day. |

| • | Eagle Ford Gathering crossover pipeline placed in service in October 2011. Eagle Ford Gathering recently completed construction of a 54-mile crossover pipeline between existing Kinder Morgan pipelines, a 5,000 horsepower compressor station and additional lateral pipelines, enabling Eagle Ford Gathering to deliver natural gas from the crossover pipeline to Williams Field Services’ Markham processing plant and Formosa Hydrocarbon Company’s (“Formosa”) Point Comfort facility for processing and associated fractionation services under long-term agreements. Eagle Ford Gathering began deliveries to Williams Field Services via the crossover pipeline in October, and we anticipate that it will begin deliveries to Formosa in early 2012. |

| • | Liberty pipeline placed in service in September 2011. Our Liberty Pipeline Group joint venture with Energy Transfer Partners completed construction of an NGL pipeline that extends |

S-4

Table of Contents

approximately 87 miles, from our Houston Central complex in Colorado County, Texas, first to an NGL product storage facility in Matagorda County, Texas, and then to Formosa’s Point Comfort facility. We have 37,500 barrels per day of firm capacity on the Liberty pipeline, which enables us to transport mixed NGLs for delivery to Formosa under a long-term fractionation and product purchase agreement. Our agreement with Formosa initially provides us access to 5,000 to 7,000 barrels per day of fractionation and NGL product sales, and the agreement will provide us with up to 37,500 barrels per day of fractionation and product sales beginning in early 2013, after Formosa completes an expansion of its facilities. |

| • | Houston Central NGL fractionator expansion completed in October 2011. In October 2011, we completed the expansion of the fractionator at our Houston Central complex from 22,000 to 44,000 barrels per day. We expect to be able to utilize the full expanded fractionation capacity in early 2012, after we complete an upgrade to our purity ethane takeaway facilities. We also expect to complete a related upgrade of the cryogenic facility at our Houston Central complex in early 2012, which will increase the plant’s ability to process NGL-rich natural gas from the Eagle Ford Shale. |

| • | Houston Central processing expansion. In April 2011, we announced plans to expand our Houston Central complex with the addition of a new 400,000 Mcf per day cryogenic processing plant, for total processing capacity of 1.1 Bcf per day. We have obtained the necessary permits and procured long-lead equipment for the project. We have begun site construction and expect to complete the expansion late in the first quarter of 2013. |

2012 capital projects. Our estimated 2012 expansion capital expenditures for board-approved projects total approximately $395 million, which includes expenditures for our joint venture with Magellan, our Houston Central processing expansion and additional gathering infrastructure in the Eagle Ford Shale.

Declaration of distribution. On January 11, 2012, our Board of Directors declared a cash distribution for the three months ended December 31, 2011 of $0.575 per common unit. The distribution will be paid on February 9, 2012 to all common unitholders of record at the close of business on January 26, 2012. Based on our common units outstanding at December 31, 2011, and the common units sold in our recent equity offering, the distribution would total approximately $42.1 million.

Registered common unit offering. On January 19, 2012, we completed a registered underwritten offering of 5,750,000 common units (including 750,000 common units issued pursuant to the underwriters’ exercise of their option to purchase additional common units) at $34.03 per unit. We received net proceeds from that offering of approximately $187.5 million, after deducting estimated underwriting discounts and offering expenses. We used the net proceeds from that offering to repay a portion of the outstanding indebtedness under our senior secured revolving credit facility.

Principal Executive Offices and Internet Address

Our principal executive offices are located at 2727 Allen Parkway, Suite 1200, Houston, Texas 77019. Our telephone number at our principal executive offices is (713) 621-9547. We maintain a website at www.copano.com. The information on our website is not part of this prospectus supplement, and you should rely only on information contained in or incorporated by reference herein and any free writing prospectus filed in connection with this offering when making an investment decision.

S-5

Table of Contents

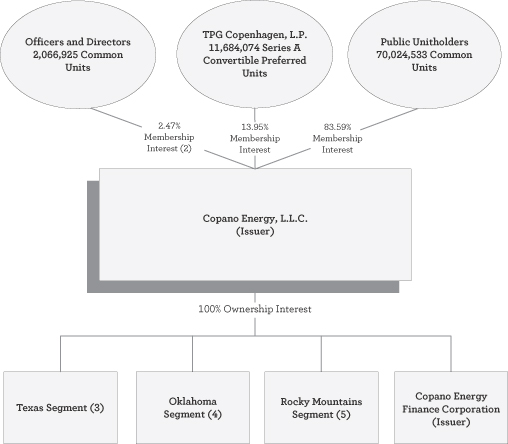

Our Organizational Structure

The following chart depicts our abridged organizational and ownership structure. Copano Energy Finance Corporation, the co-issuer of the notes, is a direct wholly owned subsidiary of Copano Energy, L.L.C. and carries on no independent business other than acting as a co-issuer of the notes and our other senior notes.

Structure of Copano Energy, L.L.C.(1)

| (1) | Based on units outstanding as of December 31, 2011, assuming conversion of all Series A convertible preferred units into common units and as adjusted to include 5,750,000 common units we issued on January 19, 2012. |

| (2) | Reflects outstanding common units over which management has voting and/or dispositive control or in which management has a pecuniary interest. |

��

| (3) | Our Texas segment includes our 62.5% partnership interest in Webb/Duval Gatherers, our 50% limited liability company interest in Eagle Ford Gathering, our 50% limited liability company interest in Liberty Pipeline Group and our 50% limited liability company interest in Double Eagle Pipeline. None of these entities will guarantee the notes offered hereby. |

| (4) | Our Oklahoma segment includes our majority limited liability company interest in Southern Dome, which will not guarantee the notes offered hereby. |

| (5) | Our Rocky Mountains segment includes our 51% limited liability company interest in Bighorn and our 37.04% limited liability company interest in Fort Union. Neither of these entities will guarantee the notes offered hereby. |

S-6

Table of Contents

The following summary contains basic information about the notes offered hereby and is not complete. For a more complete understanding of the notes offered hereby, please refer to the section entitled “Description of Notes” in this prospectus supplement and “Description of Our Debt Securities” in the accompanying prospectus.

Issuers | Copano Energy, L.L.C. and Copano Energy Finance Corporation |

Securities | $150,000,000 aggregate principal amount of 7.125% Senior Notes due 2021. The notes offered hereby are an additional issue of our outstanding 7.125% Senior Notes due 2021 issued in an aggregate principal amount of $360,000,000 on April 5, 2011. The notes offered hereby will be issued under the same indenture as the outstanding notes and are part of the same series of debt securities. The notes offered hereby will be fungible with the outstanding notes for trading purposes and will trade under the same CUSIP number. The notes will be issued in denominations of $2,000 and integral multiples of $1,000 in excess thereof. |

Maturity | The notes will mature on April 1, 2021. |

Interest | Interest will accrue on the notes offered hereby from October 1, 2011 until maturity at 7.125% per year. |

Interest payment dates | April 1 and October 1 of each year, beginning on April 1, 2012. |

Use of proceeds | We expect the net proceeds from this offering to be approximately $146.5 million, after deducting estimated fees and expenses payable by us (including underwriting discounts and commissions). We intend to use the net proceeds from this offering to repay a portion of the outstanding indebtedness under our senior secured revolving credit facility. Affiliates of the underwriters are lenders under our senior secured revolving credit facility and, accordingly, will receive a portion of the proceeds of this offering. Please read “Use of Proceeds” on page S-18 of this prospectus supplement. |

Optional redemption | We may redeem some or all of the notes at any time on or after April 1, 2016 at the redemption prices listed in this prospectus supplement, together with accrued and unpaid interest, if any, to the date of redemption, and we may redeem all of the notes at any time prior to April 1, 2016 at a make-whole redemption price described in this prospectus supplement, together with accrued and unpaid interest, if any, to the date of redemption. In addition, prior to April 1, 2014, we may redeem up to 35% of the aggregate principal amount of the notes with the proceeds of certain equity offerings at the redemption price specified in this prospectus supplement together with accrued and unpaid interest, if any, to the date of redemption. |

Mandatory offers to repurchase | If we sell certain assets and do not reinvest the proceeds or repay senior indebtedness, or if we experience specific kinds of changes of control, we must offer to repurchase the notes at the prices, in the amounts and subject to the conditions described in the section “Description of Notes — Repurchase at the Option of Holders.” |

S-7

Table of Contents

Subsidiary guarantees | Each of our wholly owned existing subsidiaries, other than Copano Energy Finance Corporation, has guaranteed the notes initially and will continue to do so as long as such subsidiary guarantees any other debt of ours or any other subsidiary guarantor. Not all of our future subsidiaries will have to become guarantors. If we cannot make payments on the notes when they are due, the subsidiary guarantors, if any, must make them instead. Please read “Description of Notes—Subsidiary Guarantees.” |

Ranking | The notes are: |

| • | our senior unsecured obligations; |

| • | equal in right of payment with all of our existing and future senior debt; |

| • | senior in right of payment to all of our future subordinated debt; |

| • | effectively junior in right to payment to our existing and future secured debt to the extent of the value of the assets securing the debt, including our obligations in respect of our Second Amended and Restated Credit Agreement; and |

| • | structurally junior to all liabilities of our future subsidiaries that do not guarantee the notes. |

| Upon the closing of this offering and the application of the net proceeds as indicated in “Use of Proceeds,” we anticipate that we and the subsidiary guarantors will have approximately $ million of indebtedness ranking equally in right of payment with the notes. |

| As of September 30, 2011, on an as further adjusted basis after giving effect to this offering, our recent registered common unit offering and our use of proceeds therefrom, we and our subsidiaries would have had approximately $759.5 million of senior indebtedness outstanding (including the notes), none of which would have been secured, with $435.9 million of available borrowing capacity under our senior secured revolving credit facility. After giving effect to this offering and application of the net proceeds, we would have had $75.5 million of outstanding borrowings under our revolving credit facility at January 31, 2012. |

Covenants | We will issue the notes offered hereby under an indenture with U.S. Bank National Association, as trustee. The indenture, among other things, limits our ability and the ability of our restricted subsidiaries to: |

| • | borrow money; |

| • | pay distributions or dividends on equity or purchase, redeem or otherwise acquire equity; |

| • | make investments; |

| • | use assets as collateral in other transactions; |

| • | engage in sale and leaseback transactions; |

| • | sell certain assets or merge with or into other companies; |

S-8

Table of Contents

| • | engage in transactions with affiliates; and |

| • | engage in unrelated businesses. |

| For more details, please read “Description of Notes—Certain Covenants.” |

Covenant termination | If at any time the notes are rated investment grade by both Moody’s Investors Service and Standard & Poor’s Ratings Services and no default has occurred and is continuing under the indenture, certain of the foregoing covenants will terminate and will no longer apply to us or our subsidiaries. Please read “Description of Notes — Certain Covenants — Covenant Termination.” |

Listing for trading | We do not intend to list the notes for trading on any securities exchange. We can provide no assurance as to the liquidity of, or development of any trading market for, the notes. |

Further issuances | We may from time to time create and issue additional notes having the same terms as the notes originally issued on April 5, 2011 and the notes being issued in this offering, so that such additional notes shall be consolidated and form a single series with the previously issued notes. |

Form | The notes offered hereby will be represented by one or more global notes registered in the name of The Depository Trust Company, referred to as DTC, or its nominee. Beneficial interests in the notes will be evidenced by, and transfers thereof will be effected only through, records maintained by participants in DTC. |

Trustee | U.S. Bank National Association. |

Delivery and clearance | We will deposit the global notes representing the notes offered hereby with the trustee as custodian for DTC. You may hold an interest in the notes through DTC, Clearstream Banking S.A. or Euroclear Bank S.A./N.V., as operator of the Euroclear System, directly as a participant of any such system or indirectly through organizations that are participants in such systems. |

Governing law | The notes offered hereby will be, and the indenture relating to the notes is, governed by New York law. |

Risk factors | Investing in the notes involves risks. Please read “Risk Factors” beginning on page S-14 of this prospectus supplement and in the documents incorporated by reference, as well as the other cautionary statements throughout this prospectus supplement, for a discussion of factors you should carefully consider before deciding to invest in the notes. |

S-9

Table of Contents

SUMMARY HISTORICAL FINANCIAL INFORMATION

The following tables show our summary historical financial information as of and for the periods indicated. We derived the information in the following tables from, and that information should be read together with and is qualified in its entirety by reference to, our historical consolidated financial statements and the accompanying notes incorporated herein by reference. The tables should be read together with “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” included in our Annual Report on Form 10-K for the year ended December 31, 2010 and our Quarterly Reports on Form 10-Q for the quarterly periods ended March 31, 2011, June 30, 2011 and September 30, 2011, which are incorporated herein by reference.

| Nine Months ended September 30, | Year ended December 31, | |||||||||||||||||||

| 2011 | 2010 | 2010 | 2009 | 2008 | ||||||||||||||||

| (in thousands, except per unit information) | ||||||||||||||||||||

Statement of Operations: | ||||||||||||||||||||

Revenue: | ||||||||||||||||||||

Natural gas sales | $ | 348,538 | $ | 292,559 | $ | 381,453 | $ | 316,686 | $ | 747,258 | ||||||||||

Natural gas liquids sales | 521,129 | 353,119 | 490,980 | 406,662 | 597,986 | |||||||||||||||

Transportation, compression and processing fees | 82,706 | 47,539 | 68,398 | 55,983 | 59,006 | |||||||||||||||

Condensate and other | 37,299 | 41,204 | 54,333 | 40,715 | 50,169 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total revenue | 989,672 | 734,421 | 995,164 | 820,046 | 1,454,419 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Costs and expenses: | ||||||||||||||||||||

Cost of natural gas and natural gas liquids(1) | 779,986 | 551,939 | 745,074 | 576,448 | $ | 1,178,304 | ||||||||||||||

Transportation(1) | 19,202 | 16,619 | 22,701 | 24,148 | 21,971 | |||||||||||||||

Operations and maintenance | 46,953 | 38,337 | 53,487 | 51,477 | 53,824 | |||||||||||||||

Depreciation, amortization and impairment | 56,143 | 46,002 | 62,572 | 56,975 | 52,916 | |||||||||||||||

General and administrative | 34,530 | 31,311 | 40,347 | 39,511 | 45,571 | |||||||||||||||

Taxes other than income | 4,029 | 3,658 | 4,726 | 3,732 | 3,019 | |||||||||||||||

Equity in loss (earnings) from unconsolidated affiliates | 158,581 | 19,788 | 20,480 | (4,600 | ) | (6,889 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total costs and expenses | 1,099,424 | 707,654 | 949,387 | 747,691 | 1,348,716 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Operating income | (109,752 | ) | 26,767 | 45,777 | 72,355 | 105,703 | ||||||||||||||

Other income (expense): | ||||||||||||||||||||

Interest and other income | 31 | 59 | 78 | 1,202 | 1,174 | |||||||||||||||

Gain (loss) on retirement of unsecured debt | (18,233 | ) | — | — | 3,939 | 15,272 | ||||||||||||||

Interest and other financing costs | (34,450 | ) | (41,239 | ) | (53,605 | ) | (55,836 | ) | (64,978 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

(Loss) income before income taxes and discontinued operations | (162,404 | ) | (14,413 | ) | (7,750 | ) | 21,660 | 57,171 | ||||||||||||

Provision for income taxes | (1,161 | ) | (660 | ) | (931 | ) | (794 | ) | (1,249 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

(Loss) income from continuing operations | — | — | (8,681 | ) | 20,866 | 55,922 | ||||||||||||||

Discontinued operations, net of tax(2) | — | — | — | 2,292 | 2,291 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net (loss) income | (163,565 | ) | (15,073 | ) | (8,681 | ) | 23,158 | 58,213 | ||||||||||||

Preferred unit distributions | (24,235 | ) | (7,500 | ) | (15,188 | ) | — | — | ||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net (loss) income to common units | $ | (187,800 | ) | $ | (22,573 | ) | $ | (23,869 | ) | $ | 23,158 | $ | 58,213 | |||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Basic net (loss) income per common unit: | ||||||||||||||||||||

(Loss) income per common unit from continuing operations | $ | (2.84 | ) | $ | (0.36 | ) | $ | (0.37 | ) | $ | 0.39 | $ | 1.15 | |||||||

Income per common unit from discontinued operations | — | — | — | 0.04 | 0.05 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net (loss) income per common unit | $ | (2.84 | ) | $ | (0.36 | ) | $ | (0.37 | ) | $ | 0.43 | $ | 1.20 | |||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Weighted average number of common units | 66,125 | 63,193 | 63,854 | 54,395 | 48,513 | |||||||||||||||

Diluted net (loss) income per common unit: | ||||||||||||||||||||

(Loss) income per common unit from continuing operations | $ | (2.84 | ) | $ | (0.36 | ) | $ | (0.37 | ) | $ | 0.36 | $ | 0.97 | |||||||

Income per common unit from discontinued operations | — | — | — | 0.04 | 0.04 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net (loss) income per common unit | $ | (2.84 | ) | $ | (0.36 | ) | $ | (0.37 | ) | $ | 0.40 | $ | 1.01 | |||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Weighted average number of common units | 66,125 | 63,193 | 63,854 | 58,038 | 57,856 | |||||||||||||||

S-10

Table of Contents

| Nine Months ended September 30, | Year ended December 31, | |||||||||||||||||||

| 2011 | 2010 | 2010 | 2009 | 2008 | ||||||||||||||||

| (in thousands) | ||||||||||||||||||||

Balance Sheet Data (at period end): | ||||||||||||||||||||

Total assets | $ | 2,017,900 | $ | 1,927,145 | $ | 1,906,993 | $ | 1,867,412 | $ | 2,013,665 | ||||||||||

Long term debt (includes $0 and $567 as of September 30, 2011 and 2010, respectively and $546, $628 and $704 bond premium as of December 31, 2010, 2009 and 2008, respectively) | 904,525 | 582,757 | 592,736 | 852,818 | 821,119 | |||||||||||||||

Total members’ capital | 906,228 | 1,196,850 | 1,154,757 | 860,026 | 1,037,958 | |||||||||||||||

Cash Flow Data: | ||||||||||||||||||||

Net cash provided by operating activities | $ | 122,789 | $ | 94,489 | $ | 123,598 | $ | 141,318 | $ | 89,924 | ||||||||||

Net cash used in investing activities | (299,114 | ) | (111,596 | ) | (156,730 | ) | (70,967 | ) | (198,855 | ) | ||||||||||

Net cash provided by (used in) financing activities | 169,929 | 74,196 | 48,370 | (89,343 | ) | 99,950 | ||||||||||||||

Other Financial Data: | ||||||||||||||||||||

Total segment gross margin(3)(4) | $ | 190,484 | $ | 165,683 | $ | 227,389 | $ | 219,450 | $ | 254,144 | ||||||||||

EBITDA(5) | (76,811 | ) | 72,828 | 108,427 | 137,327 | 174,752 | ||||||||||||||

Adjusted EBITDA(5) | 153,618 | 146,313 | 199,528 | 201,095 | 242,009 | |||||||||||||||

Maintenance capital expenditures | $ | 11,111 | $ | 6,370 | $ | 9,563 | $ | 9,728 | $ | 11,769 | ||||||||||

Expansion Capital Expenditures | 203,576 | 101,232 | 120,941 | 61,424 | 169,056 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total Capital Expenditures | $ | 214,687 | $ | 107,602 | $ | 130,504 | $ | 71,152 | $ | 180,825 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

| (1) | Exclusive of operations and maintenance and depreciation, amortization and impairment shown separately. |

| (2) | For more information, please read Note 13, “Discontinued Operations,” in our consolidated financial statements included in our Annual Report on Form 10-K for the year ended December 31, 2010. |

| (3) | Excludes results attributable to our crude oil pipeline and related assets for the year ended December 31, 2009; which are classified as discontinued operations, as discussed in Note 13, “Discontinued Operations,” in our consolidated financial statements included in our Annual Report on Form 10-K for the year ended December 31, 2010. |

| (4) | To measure the overall financial impact of our contract portfolio, we use total segment gross margin, which is the sum of our operating segments’ gross margins and the results of our risk management activities, which are included in corporate and other. Our total segment gross margin is determined primarily by five interrelated variables: (i) the volume of natural gas gathered or transported through our pipelines, (ii) the volume of natural gas processed, conditioned, fractionated or treated at our processing plants or on our behalf at third-party processing plants, (iii) natural gas, oil and NGL prices and the relative price differential between NGLs and natural gas, (iv) our contract portfolio and (v) the results of our risk management activities. The results of our risk management activities consist of (i) net cash settlements paid or received on expired commodity derivative instruments, (ii) amortization expense relating to the option component of our commodity derivative instruments and (iii) unrealized mark-to-market gain or loss on our commodity derivative instruments that have not been designated as cash flow hedges. Total segment gross margin does not have any standardized definition and therefore is unlikely to be comparable to similar measures presented by other reporting companies. Our use of total gross margin, and the underlying methodology in |

S-11

Table of Contents

| excluding certain charges, is not necessarily an indication of the results of operations that may be expected in the future, or that we will not, in fact, incur such charges in future periods. The following table reconciles total gross margin to operating income, which is the most directly comparable GAAP financial performance measure: |

| Nine Months ended September 30, | Year ended December 31, | |||||||||||||||||||

| 2011 | 2010 | 2010 | 2009 | 2008 | ||||||||||||||||

| (in thousands) | ||||||||||||||||||||

Reconciliation of total segment gross margin to operating income: | ||||||||||||||||||||

Operating income | $ | (109,752 | ) | $ | 26,767 | $ | 45,777 | $ | 72,355 | $ | 105,703 | |||||||||

Add: | ||||||||||||||||||||

Operations and maintenance expenses | 46,953 | 38,337 | 53,487 | 51,477 | 53,824 | |||||||||||||||

Depreciation, amortization and impairment | 56,143 | 46,002 | 62,572 | 56,975 | 52,916 | |||||||||||||||

General and administrative expenses | 34,530 | 31,311 | 40,347 | 39,511 | 45,571 | |||||||||||||||

Taxes other than income | 4,029 | 3,658 | 4,726 | 3,732 | 3,019 | |||||||||||||||

Equity in (earnings) loss from unconsolidated affiliates | 158,581 | 19,788 | 20,480 | (4,600 | ) | (6,889 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total segment gross margin | $ | 190,484 | $ | 165,863 | $ | 227,389 | $ | 219,450 | $ | 254,144 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

| (5) | We define EBITDA as net income (loss) plus interest and other financing costs, provision for income taxes and depreciation and amortization expense. We determine adjusted EBITDA by adding to EBITDA (i) the amortization expenses attributable to commodity derivative options, (ii) distributions from unconsolidated affiliates, (iii) any loss on refinancing of unsecured debt, (iv) equity-based compensation expenses, (v) equity in loss or subtracting equity in earnings from unconsolidated affiliates, (vi) unrealized loss or subtracting unrealized gain from commodity risk management activities, (vii) impairment expenses and (viii) other non-cash operating items. We revised our calculation of adjusted EBITDA commencing in the second quarter of 2011 to the formula above in order to more closely resemble that of many of our peers in terms of measuring our ability to generate cash. Subsequent to the third quarter of 2011, we revised our presentation of EBITDA to exclude impairment expenses and instead add back impairment expenses in Adjusted EBITDA. |

External users of our financial statements such as investors, commercial banks and research analysts use EBITDA or adjusted EBITDA, and our management uses adjusted EBITDA, as a supplemental financial measure to assess:

| • | the financial performance of our assets without regard to financing methods, capital structure or historical cost basis; |

| • | the ability of our assets to generate cash sufficient to pay interest costs and support our indebtedness; |

| • | our operating performance and return on capital as compared to those of other companies in the midstream energy sector, without regard to financing or capital structure; and |

| • | the viability of acquisitions and capital expenditure projects and the overall rates of return on alternative investment opportunities. |

EBITDA is also a financial measure that, with certain negotiated adjustments, is reported to our lenders and used to compute financial covenants under our senior secured revolving credit facility. Neither EBITDA nor adjusted

S-12

Table of Contents

EBITDA should be considered an alternative to net income, operating income, cash flows from operating activities or any other measure of liquidity or financial performance presented in accordance with GAAP. The following table reconciles EBITDA and Adjusted EBITDA to net income (loss), which is the most directly comparable GAAP financial performance measure:

| Nine Months ended September 30, | Year ended December 31, | |||||||||||||||||||

| 2011 | 2010 | 2010 | 2009 | 2008 | ||||||||||||||||

| (in thousands) | ||||||||||||||||||||

Reconciliation of EBITDA and adjusted EBITDA to net income (loss): | ||||||||||||||||||||

Net (loss) income | $ | (163,565 | ) | $ | (15,073 | ) | $ | (8,681 | ) | $ | 23,158 | $ | 58,213 | |||||||

Add: | ||||||||||||||||||||

Depreciation and amortization(6) | 51,143 | 46,002 | 62,572 | 57,539 | 50,312 | |||||||||||||||

Interest and other financing costs | 34,450 | 41,239 | 53,605 | 55,836 | 64,978 | |||||||||||||||

Provisions for income taxes | 1,161 | 660 | 931 | 794 | 1,249 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

EBITDA | (76,811 | ) | 72,828 | 108,427 | 137,327 | 174,752 | ||||||||||||||

Add: | ||||||||||||||||||||

Amortization of commodity derivative options | 22,069 | 24,211 | 32,378 | 36,950 | 32,842 | |||||||||||||||

Distributions from unconsolidated affiliates | 20,329 | 19,554 | 25,955 | 29,684 | 25,830 | |||||||||||||||

Loss on refinancing of unsecured debt | 18,233 | — | — | — | — | |||||||||||||||

Equity-based compensation | 9,184 | 7,849 | 10,388 | 8,252 | 7,789 | |||||||||||||||

Equity in loss (earnings) from unconsolidated affiliates | 158,581 | 19,788 | 20,480 | (4,600 | ) | (6,889 | ) | |||||||||||||

Unrealized loss (gain) from commodity risk management activities | (2,695 | ) | 150 | 584 | (4,131 | ) | 2,759 | |||||||||||||

Impairment | 5,000 | — | — | — | 2,842 | |||||||||||||||

Other non-cash operating items | (272 | ) | 1,933 | 1,316 | (2,387 | ) | 2,084 | |||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Adjusted EBITDA | $ | 153,618 | $ | 146,313 | $ | 199,528 | $ | 201,095 | $ | 242,009 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

| (6) | Includes activity related to the discontinued operations of the crude oil pipeline and related assets discussed in Note 13, “Discontinued Operations,” in our consolidated financial statements included in our Annual Report on Form 10-K for the year ended December 31, 2010. |

S-13

Table of Contents

An investment in the notes is subject to a number of risks. You should carefully consider the risk factors included below and those in Item 1A. “Risk Factors” in our annual report on Form 10-K for the year ended December 31, 2010, and our Quarterly Report on Form 10-Q for the quarterly period ended June 30, 2011, together with all of the other information included or incorporated by reference in this prospectus supplement. You should consider the following risk factors in evaluating this investment. If any of these risks materialize into actual events, our business, financial condition or results of operations could be adversely affected.

Risks Related to the Notes

We have a holding company structure in which our subsidiaries conduct our operations and own our operating assets.

We are a holding company, and our subsidiaries conduct all of our operations and own all of our operating assets. We have no significant assets other than the limited liability company interests and other equity interests in our subsidiaries. As a result, our ability to make required payments on the notes depends on the performance of our subsidiaries and the other entities in which we own interests and their ability to distribute funds to us. The ability of our subsidiaries to make distributions to us may be restricted by, among other things, our Second Amended and Restated Credit Agreement and applicable state and other laws and regulations or, in the case of other entities in which we own an interest, debt that they may incur, which could be governed by agreements restricting their ability to distribute cash to us. If we are unable to obtain the funds necessary to pay the principal amount at maturity of the notes, or to repurchase the notes upon the occurrence of a change of control, we may be required to adopt one or more alternatives, such as a refinancing of the notes. We cannot assure you that we would be able to refinance the notes or obtain the funds to pay principal or interest on the notes.

Payment of principal and interest on the notes is effectively subordinated to our senior secured debt to the extent of the value of the assets securing that debt and structurally subordinated to the liabilities of any of our subsidiaries that do not guarantee the notes.

The notes are effectively subordinated to claims of our secured creditors, and the subsidiary guarantees are effectively subordinated to the claims of our secured creditors as well as the secured creditors of our subsidiary guarantors. As of September 30, 2011, on an as further adjusted basis as described under “Capitalization,” we and our subsidiary guarantors would have had no secured indebtedness outstanding. After giving effect to this offering and application of the net proceeds, we would have had $75.5 million of outstanding borrowings under our revolving credit facility at January 31, 2012. Holders of our secured obligations, including obligations under our Second Amended and Restated Credit Agreement, will have claims that are prior to claims of the holders of the notes with respect to the assets securing those obligations. In the event of a liquidation, dissolution, reorganization, bankruptcy or any similar proceeding, our assets and those of our subsidiaries will be available to pay obligations on the notes and the guarantees only after holders of our senior secured debt have been paid the value of the assets securing such debt. Although all of our wholly owned subsidiaries, other than Copano Energy Finance Corporation, the co-issuer of the notes, currently guarantee the notes, in the future, under certain circumstances, these guarantees are subject to release, and our less than wholly owned subsidiaries are not guarantors. As a result, the notes are structurally subordinated to the claims of all creditors, including trade creditors and tort claimants, of our subsidiaries that are not guarantors. In the event of the liquidation, dissolution, reorganization, bankruptcy or similar proceeding of the business of a subsidiary that is not a guarantor, creditors of that subsidiary would generally have the right to be paid in full before any distribution is made to us or the holders of the notes. Accordingly, there may not be sufficient funds remaining to pay amounts due on all or any of the notes.

S-14

Table of Contents

We require a significant amount of cash to service our indebtedness. Our ability to generate cash depends on many factors beyond our control.

Our ability to make payments on and to refinance our indebtedness, including the notes, and to fund planned capital expenditures depends on our ability to generate cash in the future. This, to a certain extent, is subject to general economic, financial, competitive, legislative, regulatory and other factors that are beyond our control.

We cannot assure you that we will generate sufficient cash flow from operations or that future borrowings will be available to us under our Second Amended and Restated Credit Agreement or otherwise in an amount sufficient to enable us to pay our indebtedness, including the notes, or to fund our other liquidity needs. We may need to refinance all or a portion of our indebtedness, including the notes, on or before maturity. We cannot assure you that we will be able to refinance any of our indebtedness, including outstanding indebtedness pursuant to our Second Amended and Restated Credit Agreement and the notes, on commercially reasonable terms or at all.

We do not have the same flexibility as other types of organizations to accumulate cash, which may limit cash available to service the notes or to repay them at maturity.

Subject to the limitations on restricted payments contained in the indentures governing the notes and our other outstanding series of senior notes and in our Second Amended and Restated Credit Agreement and any other indebtedness, we distribute all of our “available cash” each quarter to our unitholders. “Available cash” is defined in our limited liability company agreement, and it generally means, for each fiscal quarter:

| • | all cash on hand at the end of the quarter; |

| • | plus, all cash on hand on the date of determination of available cash for the quarter resulting from working capital borrowings made after the end of the quarter. Our credit agreement does not provide for the type of working capital borrowing that would be eligible, pursuant to our limited liability company agreement, to be considered available cash; |

| • | less, the amount of cash reserves that our Board of Directors determines in its reasonable discretion is necessary or appropriate to: |

| • | provide for the proper conduct of our business (including reserves for future capital expenditures and for our future credit needs); |

| • | comply with applicable law, any of our debt instruments or other agreements or obligations; or |

| • | provide funds for distributions to our unitholders for any one or more of the next four quarters. |

As a result, we may not accumulate significant amounts of cash. If our Board of Directors fails to establish sufficient reserves, these distributions could significantly reduce the cash available to us in subsequent periods to make payments on the notes.

We may not be able to fund a change of control offer.

In the event of a change of control, we will be required, subject to certain conditions, to offer to purchase all outstanding notes at a price equal to 101% of the principal amount thereof, plus accrued and unpaid interest thereon to the date of purchase. The holders of our other outstanding series of senior notes have substantially the same rights. If a change of control were to occur today, we would not have sufficient funds available to purchase all of the outstanding notes were they to be tendered in response to an offer made as a result of a change of control. We cannot assure you that we will have sufficient funds available or that we will be permitted by our other debt instruments to fulfill these obligations upon a change of control in the future. Furthermore, certain change of control events would constitute an event of default under our Second Amended and Restated Credit Agreement. Please read “Description of Notes — Repurchase at the Option of Holders — Change of Control.”

S-15

Table of Contents

The Chancery Court of Delaware has raised the possibility in a published decision that a change of control put right occurring as a result of a failure to have “continuing directors” comprising a majority of a board of directors may be unenforceable on public policy grounds. Therefore, you may not be entitled to receive this protection under the indenture.

The term “change of control” is limited to certain specified transactions and may not include other events that might adversely affect our financial condition. Our obligation to repurchase the notes upon a change of control would not necessarily afford holders of the notes protection in the event of a highly leveraged transaction, reorganization, merger or similar transaction involving us.

Many of the covenants contained in the indenture will terminate if the notes are rated investment grade by both Standard & Poor’s Ratings Services and Moody’s Investors Service and no default has occurred and is continuing.

Many of the covenants in the indenture governing the notes will terminate if the notes are rated investment grade by both Standard & Poor’s Ratings Services and Moody’s Investors Service, provided at such time no default or event of default has occurred and is continuing. The covenants restrict, among other things, our ability to pay dividends, incur debt and to enter into certain other transactions. There can be no assurance that the notes will ever be rated investment grade. However, termination of these covenants would allow us to engage in certain transactions that would not be permitted while these covenants are in force, and the effects of any such transactions will be permitted to remain in place even if the notes are subsequently downgraded below investment grade. Please read “Description of Notes—Certain Covenants—Covenant Termination.”

The guarantees by certain of our subsidiaries of the notes could be deemed fraudulent conveyances under certain circumstances, and a court may try to subordinate or void these subsidiary guarantees.

Under U.S. bankruptcy law and comparable provisions of state fraudulent transfer laws, a guarantee can be voided, or claims under a guarantee may be subordinated to all other debts of that guarantor if, among other things, the guarantor, at the time it incurred the indebtedness evidenced by its guarantee:

| • | intended to hinder, delay or defraud any present or future creditor or received less than reasonably equivalent value or fair consideration for the incurrence of the guarantee; |

| • | was insolvent or rendered insolvent by reason of such incurrence; |

| • | was engaged in a business or transaction for which the guarantor’s remaining assets constituted unreasonably small capital; or |

| • | intended to incur, or believed that it would incur, debts beyond its ability to pay those debts as they mature. |

In addition, any payment by that guarantor under a guarantee could be voided and required to be returned to the guarantor or to a fund for the benefit of the creditors of the guarantor. The measures of insolvency for purposes of these fraudulent transfer laws will vary depending upon the law applied in any proceeding to determine whether a fraudulent transfer has occurred. Generally, however, a subsidiary guarantor would be considered insolvent if:

| • | the sum of its debts, including contingent liabilities, was greater than the fair saleable value of all of its assets; |

| • | the present saleable value of its assets was less than the amount that would be required to pay its probable liability, including contingent liabilities, on its existing debts as they become absolute and mature; or |

| • | it could not pay its debts as they became due. |

S-16

Table of Contents

Your ability to sell the notes may be limited by the absence of an established trading market.

Although the underwriters have informed us that they currently intend to continue to make a market in the notes, they are not obligated to do so. In addition, they may discontinue any such market making at any time without notice. The liquidity of any market for the notes depends on the number of holders of the notes, the interest of securities dealers in making a market in the notes and other factors. Accordingly, we cannot assure you as to the continuance or liquidity of any market for the notes. Historically, the market for noninvestment grade debt has been subject to disruptions that have caused substantial volatility in the prices of securities similar to the notes. We cannot assure you that any market for the notes will be free from similar disruptions. Any such disruption may adversely affect the noteholders’ ability to sell the notes.

Risks Related to Our Structure

Our tax treatment depends on our status as a partnership for U.S. federal income tax purposes as well as our not being subject to a material amount of entity-level taxation by individual states. If the Internal Revenue Service were to treat us as a corporation for U.S. federal income tax purposes or we were to become subject to a material amount of entity-level taxation for state purposes, then our cash available for payment of principal and interest on the notes would be substantially reduced.

Despite the fact that we are a limited liability company under Delaware law, it is possible in certain circumstances for a publicly traded limited liability company such as ours to be treated as a corporation rather than a partnership for U.S. federal income tax purposes. Although we do not believe based upon our current operations that we should be so treated, a change in our business (or a change in current law) could cause us to be treated as a corporation for U.S. federal income tax purposes or otherwise subject us to taxation as an entity.

If we were treated as a corporation for U.S. federal income tax purposes, we would pay U.S. federal income tax on our taxable income at the corporate tax rates, currently at a maximum rate of 35%, and would likely pay state income tax at varying rates. Because a tax would be imposed on us as a corporation, our cash available for payment of principal and interest on the notes and other debt obligations would be substantially reduced.

Current law may change so as to cause us to be treated as a corporation for U.S. federal income tax purposes or otherwise subject us to entity-level taxation. At the federal level, legislation has recently been considered by members of Congress that would have eliminated partnership tax treatment for certain publicly traded limited liability companies. Although it does not appear that the legislation considered would have affected our tax treatment, we are unable to predict whether any of these changes, or other proposals, will be reconsidered or will ultimately be enacted. Any such changes could negatively impact the amount of cash available for payment on the notes and on our other debt obligations. At the state level, because of widespread state budget deficits and other reasons, several states are evaluating ways to subject limited liability companies to entity-level taxation through the imposition of state income, franchise and other forms of taxation. For example, we are required to pay an entity-level tax on the portion of our gross income apportioned to Texas. Imposition of such a tax on us by any other state will reduce the cash available for payments on the notes and on our other debt obligations.

S-17

Table of Contents

We expect the net proceeds from this offering to be approximately $146.5 million, after deducting estimated fees and expenses payable by us (including underwriting discounts and commissions). We intend to use the net proceeds from this offering to repay a portion of the outstanding indebtedness under our senior secured revolving credit facility.

At January 31, 2012, an aggregate of approximately $222.0 million of borrowings was outstanding under our senior secured revolving credit facility and the weighted average interest rate on borrowings under our senior secured revolving credit facility was 5.60%. Our senior secured revolving credit facility matures on June 10, 2016. We use borrowings under our senior secured revolving credit facility for capital projects, acquisitions, hedging, working capital and general corporate purposes, and we anticipate that we will use increased borrowing availability under our senior secured revolving credit facility after this offering for such purposes. Affiliates of the underwriters are lenders under our senior secured revolving credit facility and, accordingly, will receive a portion of the proceeds of this offering. See “Underwriting—Conflicts of Interest.”

S-18

Table of Contents

The following table sets forth our consolidated cash and cash equivalents and our consolidated capitalization as of September 30, 2011 on:

| • | an actual basis; |

| • | on an as adjusted basis to give effect to the completion of our offering of 5,750,000 common units on January 19, 2012 and the application of net proceeds from that offering to repay a portion of the outstanding indebtedness under our senior secured revolving credit facility, as further described under “Summary — Recent Developments — Registered common unit offering”; and |

| • | an as further adjusted basis to give effect to the issuance of the notes in this offering and the application of the net proceeds of this offering in the manner described under “Use of Proceeds.” |

This table is derived from, should be read together with and is qualified in its entirety by reference to our audited consolidated financial statements and the accompanying notes incorporated by reference into this prospectus supplement. Please read “Where You Can Find More Information.”

| As of September 30, 2011 | ||||||||||||

| Actual | As adjusted | As further adjusted | ||||||||||

| (In thousands) | ||||||||||||

Cash and cash equivalents | $ | 53,534 | $ | 53,534 | $ | 92,490 | ||||||

|

|

|

|

|

| |||||||

Long-term debt: | ||||||||||||

Revolving credit facility(1) | $ | 295,000 | $ | 107,499 | $ | — | (1) | |||||

Senior notes: | ||||||||||||

7.125% senior notes due 2021 | 360,000 | 360,000 | 510,000 | (2) | ||||||||

7.75% senior notes due 2018 | 249,525 | 249,525 | 249,525 | |||||||||

|

|

|

|

|

| |||||||

Total senior notes | 609,525 | 609,525 | 759,525 | |||||||||

|

|

|

|

|

| |||||||

Total long-term debt | 904,525 | 717,024 | 759,525 | |||||||||

Members’ capital | ||||||||||||

Series A convertible preferred units | 285,168 | 285,168 | 285,168 | |||||||||

Common units | 1,164,399 | 1,351,900 | 1,351,900 | |||||||||

Paid in capital | 59,250 | 59,250 | 59,250 | |||||||||

Accumulated deficit | (592,676 | ) | (592,676 | ) | (592,676 | ) | ||||||

Accumulated other comprehensive loss | (9,913 | ) | (9,913 | ) | (9,913 | ) | ||||||

|

|

|

|

|

| |||||||

Total members’ capital | 906,228 | 1,093,729 | 1,093,729 | |||||||||

|

|

|

|

|

| |||||||

Total capitalization | $ | 1,810,753 | $1,810,753 | $ | 1,853,254 | |||||||

|

|

|

|

|

| |||||||

| (1) | At January 31, 2012, approximately $222.0 million of borrowings were outstanding under our senior secured revolving credit facility. After giving effect to this offering and application of the net proceeds, we would have had $75.5 million of outstanding borrowings under our revolving credit facility at January 31, 2012. |

| (2) | Assumes that the notes offered hereby will be issued at par. |

S-19

Table of Contents

RATIO OF EARNINGS TO FIXED CHARGES

The table below sets forth the ratios of earnings to fixed charges for us for the periods indicated.

| Nine Months ended September 30, 2011 | Year ended December 31, | |||||||||||||||||||||||

| 2010 | 2009 | 2008 | 2007 | 2006 | ||||||||||||||||||||

Earnings: | ||||||||||||||||||||||||

Net income (loss) | $ | (163,565 | ) | $ | (8,681 | ) | $ | 23,158 | $ | 58,213 | $ | 63,175 | $ | 65,114 | ||||||||||

Income taxes | 1,161 | 931 | 794 | 1,249 | 1,714 | — | ||||||||||||||||||

Equity in losses (earnings) from unconsolidated affiliates | 158,581 | 20,480 | (4,600 | ) | (6,889 | ) | (2,850 | ) | (1,297 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Pre-tax income from continuing operations | (3,823 | ) | 12,730 | 19,352 | 52,573 | 62,039 | 63,817 | |||||||||||||||||

Fixed charges | 42,233 | 57,423 | 60,069 | 69,339 | 30,753 | 34,011 | ||||||||||||||||||