| OMB APPROVAL | ||

| OMB Number: 3235-0570 Expires: January 31, 2017 Estimated average burden hours per response. . . . . . .20.6 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number 811-22647

PRIVATE ADVISORS ALTERNATIVE STRATEGIES FUND

(Exact name of Registrant as specified in charter)

51 Madison Avenue, New York, NY 10010

(Address of principal executive offices) (Zip code)

J. Kevin Gao, Esq.

30 Hudson Street

Jersey City, New Jersey 07302

(Name and address of agent for service)

Registrant’s telephone number, including area code: (212) 576-7000

Date of fiscal year end: March 31

Date of reporting period: March 31, 2016

| Item 1. | Reports to Stockholders. |

Private Advisors

Alternative Strategies Fund

Message from the President and Annual Report

March 31, 2016

This Page Intentionally Left Blank

Message from the President

The U.S. economy continued to expand, but the pace moderated during the 12-month reporting period ended March 31, 2016. Looking back, the U.S. Department of Commerce reported that second quarter 2015 U.S. gross domestic product (“GDP”) growth was 3.9%. GDP growth then decelerated to 2.0% and 1.4% during the third and fourth quarters of 2015, respectively. Based on the U.S. Department of Commerce’s initial estimate, first quarter 2016 GDP growth was a modest 0.5%. The tepid reading was driven by several factors, including a decrease in nonresidential fixed investment, a deceleration in personal consumption expenditures, and a downturn in federal government spending.

Despite slowing growth, in December 2015 the U.S. Federal Reserve (the “Fed”) raised interest rates for the first time in nearly a decade. More specifically, the Fed raised the federal funds target rate from a range between 0.0% to 0.25% to a range between 0.25% and 0.50%. In its statement after the December 2015 meeting, the Fed said, “The stance of monetary policy remains accommodative after this increase, thereby supporting further improvement in labor market conditions and a return to 2 percent inflation.”1 During its meetings that concluded in January and March 2016, the Fed kept rates on hold. Against this backdrop, the U.S. stock market, as measured by the S&P 500® Index,2 gained 1.78% for the 12 months ended March 31, 2016. Over the same period, the U.S. bond market, as measured by the Barclays U.S. Aggregate Bond Index,2 returned 1.96%.

On the following pages we present the annual report for Private Advisors Alternative Strategies Fund. The report contains information about the markets, hedge funds and activity that affected the Fund during the reporting period.

On a final note, on November 2, 2015, the Fund’s Board of Trustees, upon the recommendation of the Fund’s investment manager, New York Life Investment Management LLC, and upon careful consideration, approved a proposal to liquidate the Fund pursuant to the terms of a plan of liquidation.

Sincerely,

Stephen P. Fisher

President

| 1. | Source: December 16, 2015, Federal Reserve Press Release. |

| 2. | See page 5 for more information on this index. |

Not part of the Annual Report

Certain material in this report may include statements that constitute “forward-looking” statements under the U.S. securities laws. Forward looking statements include, among other things, projections, estimates and information about possible future results or events related to the Funds, market or regulatory developments. The views expressed herein are not guarantees of future performance or economic results and involve certain risks, uncertainties and assumptions that could cause the actual outcomes and results to differ materially from the views expressed herein. The views expressed herein are subject to change at any time based upon economic, market, or other conditions and the Funds undertake no obligation to update the views expressed herein.

Performance data quoted represents past performance. Past performance is no guarantee of future results. Because of market volatility, current performance may be lower or higher than the figures shown. Investment return and principal value will fluctuate, and as a result, when shares are redeemed, they may be worth more or less than their original cost. For performance information current to the most recent month-end, please call 1-888-207-6176.

Average Annual Total Returns for the Period Ended March 31, 2016

| Fund | Sales Charge | One Year | Since Inception | Gross Expense Ratio2 | ||||||||||||

| Private Advisors Alternative Strategies Fund | Maximum 3% Initial Sales Charge | With sales charges Excluding sales charges |

| –10.23 –7.45 | %

|

| 0.64 1.43 | %

|

| 8.41 8.41 | %

| |||||

| Private Advisors Alternative Strategies Master Fund | No Sales Charge | –6.76 | 2.15 | 5.80 | ||||||||||||

| Benchmark Performance | One Year | Since Inception | ||||||||

HFRI Fund of Funds Diversified Index3 | –3.53 | % | 2.76 | % | ||||||

S&P 500® Index4 | 1.78 | 12.81 | ||||||||

Barclays U.S. Aggregate Bond Index5 | 1.96 | 2.59 | ||||||||

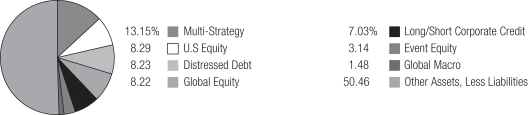

Strategy Allocations as of March 31, 2016 (Unaudited)

Top Ten Holdings as of March 31, 2016 (Unaudited)

| 1. | HBK Multi-Strategy Offshore Fund, Ltd. |

| 2. | Fir Tree International Value Fund II, Ltd. |

| 3. | Aurelius Capital International, Ltd. |

| 4. | Sheffield International Partners, Ltd. |

| 5. | Archer Capital Offshore Fund, Ltd. |

| 6. | SRS Partners, Ltd. |

| 7. | Redwood Offshore Fund, Ltd. |

| 8. | Marble Arch Offshore Partners, Ltd. |

| 9. | Empyrean Capital Overseas Fund, Ltd. |

| 10. | Luxor Capital Partners Offshore, Ltd. |

| 1. | The performance table does not reflect the deduction of taxes that a shareholder would pay on distributions or Fund-share redemptions. Total returns reflect the maximum applicable sales charge as indicated in the table above, changes in share price, and reinvestment of dividend and capital gain distributions. Performance figures reflect certain fee waivers and/or expense limitations, without which total returns may have been lower. For more information on current fee waivers and/or expense limitations, please refer to the notes to the financial statements. |

| 2. | The gross expense ratios presented reflect a Fund’s “Total Annual Fund Operating Expenses” from the most recent Prospectus and may differ from other expense ratios disclosed in this report. |

| 3. | The HFRI Fund of Funds Diversified Index is a non-investable product of diversified fund of funds. The index is weighted (fund weighted) with an inception of January 1990. An investment cannot be made directly in an index. |

| 4. | “S&P 500®” is a trademark of the McGraw-Hill Companies, Inc. The S&P 500® Index is widely regarded as the standard index for measuring large-cap U.S. stock market performance. Results assume reinvestment of all dividends and capital gains. An investment cannot be made directly in an index. |

| 5. | The Barclays U.S. Aggregate Bond Index is a broad-based benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market, including Treasurys, government-related and corporate securities, mortgage-backed securities (agency fixed-rate and hybrid adjustable rate mortgage pass-throughs), asset-backed securities, and commercial mortgage-backed securities. Results assume reinvestment of all income and capital gains. An investment cannot be made directly in an index. |

| Private Advisors Funds | 5 |

Portfolio Management Discussion and Analysis (Unaudited)

For the 12 months ended March 31, 2016, Private Advisors Alternative Strategies Master Fund (“Master Fund”) returned –6.76%. Private Advisors Alternative Strategies Fund (“Feeder Fund”) returned –7.45%, excluding all sales charges. See page 5 for Feeder Fund returns with applicable sales charges. The Master Fund and the Feeder Fund are collectively referred to herein as “Funds.” The Funds underperformed the –3.53% return of the HFRI Fund of Funds Diversified Index1 and the 1.96% return of the Barclays U.S. Aggregate Bond Index.1 The Funds underperformed the 1.78% return of the S&P 500® Index1 during the reporting period.

The Private Advisors Alternative Strategies Fund is a “feeder” fund in what is known in the investment company industry as a master-feeder structure. The Feeder Fund invests substantially all of its assets, net of reserves maintained for reasonably anticipated expenses, in the Master Fund. The Master Fund, which has the same investment objective as the Feeder Fund, seeks to achieve its investment objective by investing principally in private investment funds or “hedge funds” managed by third-party portfolio managers who employ diverse styles and strategies. In the process of preparing for the liquidation of the Fund, it ceased pursuing its investment objective effective December 1, 2015.

Fund Performance

The Master Fund had a loss of 6.76% for the 12-month reporting period ended March 31, 2016, versus a loss of 3.53% for the HFRI Fund of Funds Diversified Index. Not surprisingly, the Master Fund underperformed the 1.78% return of the S&P 500® Index for the reporting period as growth and momentum stocks had dominated performance. The Master Fund’s allocation to the global macro strategy was the only positive contributor to performance for the 12-month reporting period. Meanwhile, event equity, U.S. long/short equity, and long/short credit strategies were the largest detractors from the Master Fund’s performance during the reporting period.

Market Summary

Equities

U.S. equity markets rebounded sharply in March 2016, and large-cap growth stocks in particular finished the 12-month reporting period in positive territory, reversing losses from December 2015 through February 2016. Not all equities fared as well, however, as equity market leadership has narrowed

considerably with mega-caps and momentum stocks dominating performance. The mildly positive return for the S&P 500® Index provided little indication of the significant intra-month volatility that has occurred early in 2016 and also the end of 2015. January 2016 was the worst start to a year for equities since 2009, and the rally in March was driven more by macro factors (a dovish Fed, more quantitative easing from the ECB, a weaker U.S. dollar, and a more stable China) than fundamentals. In fact, fundamentals appeared less attractive as first quarter 2016 corporate earnings were revised downward substantially. Performance dispersion by sector and market cap has been increasing steadily over the last 12 months with large-cap stocks outperforming small-caps by more than 11% (as measured by Russell indices). S&P 500® Index sector performance in the first quarter was led by telecommunications (+16.6%) and utilities (+15.6%); while health care (–5.5%) and financials (–5.0%) underperformed by a significant margin.

Positive economic signals from China, a dovish Fed, a weakened dollar, and a rally in oil prices set the stage for a large gain in emerging markets in March. In fact, the MSCI Emerging Markets Index2 posted its largest monthly return in over six years, up 13.3%, and it is now outperforming most equity indices for the year. The MSCI EAFE® Index3 generated a return of –2.9% for the quarter, due to its sizable loss in January. That said, several European equity markets performed well in the first quarter including Austria, Germany, Norway, and Sweden, according to MSCI country indices.

Fixed Income

With a less certain U.S. economic outlook, the Federal Reserve reduced the expected pace of upcoming rate hikes in 2016 from four to only two of 25 basis points. Concurrently, a substantial amount of capital flowed into fixed-income ETFs during the first quarter of 2016, boosting returns in corporate credit in particular. Widening spreads created potential opportunities in the middle band of the credit spectrum. Fixed-income performance was decidedly positive in the first quarter as the BofA Merrill Lynch U.S. Corporate Index4 was up 3.9%, and the BofA Merrill Lynch CCC & Lower U.S. High Yield Index5 was up 3.8%, in spite of significant drawdowns in the first six weeks of the year. Meanwhile, longer maturity government debt had gains early in the year when investors became concerned about the return of market volatility. The BofA Merrill Lynch Current 10-Year U.S. Treasury Index6 produced a gain of 4.8% during the first quarter as the yield decreased to 1.8%.

| 1. | See page 5 for more information on this index. |

| 2. | The MSCI Emerging Markets Index is a free float-adjusted market-capitalization index that is designed to measure equity market performance in the global emerging markets. An investment cannot be made directly in an index. |

| 3. | The MSCI EAFE® Index consists of international stocks representing the developed world outside of North America. An investment cannot be made directly in an index. |

| 4. | The BofA Merrill Lynch U.S. Corporate Index an unmanaged index comprised of U.S. dollar denominated investment grade corporate debt securities publicly issued in the U.S. domestic market with at least one year remaining term to final maturity. An investment cannot be made directly in an index. |

| 5. | The BofA Merrill Lynch CCC & Lower U.S. High Yield Index tracks the performance of U.S. dollar denominated below investment grade corporate debt publicly issued in the U.S. domestic market including all securities rated CCC or lower. An investment cannot be made directly in an index. |

| 6. | The BofA Merrill Lynch Current 10-Year U.S. Treasury Index is a one-security index comprised of the most recently issued 10-year Treasury note. An investment cannot be made directly into an index. |

| 6 | Private Advisors Funds |

Contributors & Detractors

Hedge fund performance had been challenged during the reporting period, as macro forces such as commodities and interest rates dominated news and market performance, making alpha generation extremely difficult to achieve through bottom-up fundamental security selection. In fact, many hedge funds reported their worst quarter of alpha generation in more than five years during the first quarter of 2016. While fundamentally oriented investing has clearly been out of favor, we believe it is unlikely that this trend will continue in the long run. A lack of liquidity within credit markets continued to be a serious concern for investors. Regardless, returns in high yield and distressed credit markets benefited in March from more dovish central bank policies and a sharp rebound in many of the weaker, more heavily shorted sectors. The Fed became an immediate trigger for market volatility, whereby indications of a rate increase result in the appreciation of the dollar, widening credit spreads, and a drop in equity markets. Meanwhile, reducing its forecasts has had the opposite effect (as evidenced in March).

The global macro strategy was the best performer for the 12-month reporting period driven entirely by one underlying fund, Autonomy Global Macro Fund. Autonomy was also the top performer for the portfolio overall. Autonomy has generated differentiated positive performance in the global macro strategy that was driven by positions in Brazilian nominal and inflation-linked bonds, as well as in Colombian, Greek, and Ukrainian sovereign bonds. Other positive contributors within the portfolio for the reporting period included long/short equity manager SRS Partners. Although SRS experienced a pull-back in 2016 in several of its more concentrated positions, those same positions delivered very strong results in 2015, which put the manager in positive territory for the 12-month reporting period. Similarly, long/short credit manager Apollo Credit Short Opportunities posted strong results over the last 12 months and is among the top contributors due to its short credit bias. However, Apollo’s performance suffered more recently as high yield prices quickly reversed course in March.

Event equity manager Luxor Capital Partners Offshore was the largest detractor within the portfolio for the 12-month reporting period. Luxor performed poorly in December 2015 as the

manager wrote down the convertible and preferred equity that it held in one company to zero based on an imminent bankruptcy filing. These holdings accounted for a significant portion of the manager’s decline and over-shadowed other gains and losses in its portfolio. Just prior to this development, we made the decision to redeem from Luxor. The manager’s focus on softer catalyst value positions (events without a definitive timeline) did not produce the strong returns that the firm had delivered historically across asset classes (long and short). Fir Tree International Value Fund II also underperformed for the 12-month reporting period, primarily due to energy infrastructure-related investments that have experienced weakness along with commodities. There have been many companies overly penalized by their indirect affiliation with the energy sector. Long/short equity manager North Run Offshore Partners also underperformed for the reporting period as its long book, which has a value-oriented focus, has suffered in the current environment.

Although North Run’s short portfolio has performed well, it has not been able to offset weaker results in its long portfolio, which is much larger.

We anticipate that performance will become less representative of the portfolio’s historical profile as the Fund winds down, as some manager and strategy weights will become a larger portion of the overall portfolio.

Portfolio Activity

Pursuant to the Board’s approval to liquidate the Funds on November 2, 2015, redemptions were placed with underlying managers and third-party shareholders received payment in the amount equal to the net asset value per share of the Funds as of March 31, 2016. The remaining assets are held by Private Advisors’ affiliated parties.

Thank you.

Tim Berry

Portfolio Manager

Charles Honey

Portfolio Manager

| Private Advisors Funds | 7 |

Report of Independent Registered Public Accounting Firm

To the Board of Trustees and Shareholders of

Private Advisors Alternative Strategies Fund:

In our opinion, the accompanying statement of assets and liabilities and the related statements of operations, of changes in net assets, and of cash flows and the financial highlights present fairly, in all material respects, the financial position of Private Advisors Alternative Strategies Fund (the “Fund”) at March 31, 2016, the results of its operations and its cash flows for the year then ended, the changes in its net assets for each of the two years in the period then ended and the financial highlights for each of the periods presented, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

As discussed in Note 1 to the financial statements, on November 2, 2015, the Board of Trustees approved the liquidation of the Fund. Our opinion is not modified with respect to this matter.

PricewaterhouseCoopers LLP

New York, New York

May 26, 2016

| 8 | Private Advisors Alternative Strategies Fund |

Private Advisors Alternative Strategies Fund

(A Delaware Statutory Trust)

Statement of Assets and Liabilities as of March 31, 2016

| Assets | ||||

Investment in Private Advisors Alternative Strategies Master Fund, at fair value (8,271.411 Shares) | $ | 7,882,165 | ||

Cash | 102,485 | |||

Due from Master Fund | 14,138,819 | |||

Due from Manager (See Note 4) | 53,661 | |||

Prepaid assets | 4,078 | |||

|

| |||

Total assets | 22,181,208 | |||

|

| |||

| Liabilities | ||||

Redemptions payable | 14,138,819 | |||

Accrued expenses and other liabilities | 96,883 | |||

|

| |||

Total liabilities | 14,235,702 | |||

|

| |||

Net Assets | $ | 7,945,506 | ||

|

| |||

| Composition of Net Assets: | ||||

Paid-in capital | $ | 10,372,650 | ||

Distributions in excess of net investment income | (40,751 | ) | ||

Accumulated net realized gain (loss) on investment | (1,723,015 | ) | ||

Net unrealized appreciation (depreciation) on investment | (663,378 | ) | ||

|

| |||

Net Assets | $ | 7,945,506 | ||

|

| |||

| Net Asset Value Per Share: | ||||

8,314.38 Shares issued and outstanding, par value $0.001 per share 250,000 registered shares of beneficial interest | $ | 955.63 | ||

|

| |||

| Maximum Offering Price Per Share: | ||||

($955.63 plus sales load of up to 3% of net asset value per share) | $ | 984.30 | ||

|

| |||

| The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. | Private Advisors Alternative Strategies Fund | 9 |

Private Advisors Alternative Strategies Fund

(A Delaware Statutory Trust)

Statement of Operations for the year ended March 31, 2016

Income | ||||

Dividend from Private Advisors Alternative Strategies Master Fund | $ | 284,826 | ||

|

| |||

Expenses | ||||

Management Fee (see Note 4) | 258,816 | |||

Shareholder Service fees (see Note 4) | 200,061 | |||

Professional fees | 71,349 | |||

Insurance fees | 48,969 | |||

Transfer agent fees | 32,059 | |||

Registration | 24,108 | |||

Shareholder communication | 21,347 | |||

Administration fees | 17,500 | |||

Trustees | 1,277 | |||

Miscellaneous | 4,857 | |||

|

| |||

Total expenses before waiver/reimbursement | 680,343 | |||

|

| |||

Expense waiver/reimbursement from Manager | (503,818 | ) | ||

|

| |||

Net expenses | 176,525 | |||

|

| |||

Net investment income (loss) | 108,301 | |||

|

| |||

| Net realized and unrealized gain (loss) on investment | ||||

Net realized gain (loss) on investment in Private Advisors Alternative Strategies Master Fund | (1,712,521 | ) | ||

Net change in unrealized appreciation (depreciation) on investment in Private Advisors Alternative Strategies Master Fund | (168,694 | ) | ||

|

| |||

Net realized and unrealized gain (loss) on investment | (1,881,215 | ) | ||

|

| |||

Net increase (decrease) in net assets resulting from operations | $ | (1,772,914 | ) | |

|

| |||

| 10 | Private Advisors Alternative Strategies Fund | The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. |

Private Advisors Alternative Strategies Fund

(A Delaware Statutory Trust)

Statement of Changes in Net Assets

| Year ended March 31, 2016 | Year March 31, | |||||||

| Increase (decrease) in net assets resulting from operations: | ||||||||

Net investment income (loss) | $ | 108,301 | $ | 328,056 | ||||

Net realized gain (loss) on investment in Private Advisors Alternative Strategies Master Fund | (1,712,521 | ) | (5,628 | ) | ||||

Net change in unrealized appreciation (depreciation) on investment in Private Advisors Alternative Strategies Master Fund | (168,694 | ) | (113,992 | ) | ||||

|

|

|

| |||||

Net increase (decrease) in net assets resulting from operations | (1,772,914 | ) | 208,436 | |||||

|

|

|

| |||||

Distributions to Shareholders from: | ||||||||

Net investment income | (105,612 | ) | (344,502 | ) | ||||

Net realized gain | — | (8,283 | ) | |||||

|

|

|

| |||||

| (105,612 | ) | (352,785 | ) | |||||

|

|

|

| |||||

Capital share transactions: | ||||||||

Subscriptions (representing 97.68 and 7,712.40 Shares) | 100,000 | 8,008,590 | ||||||

Redemptions (representing 16,534.53 and 943.10 Shares) | (15,947,306 | ) | (967,650 | ) | ||||

Distributions reinvested (representing 107.21 and 339.32 Shares) | 105,219 | 345,424 | ||||||

|

|

|

| |||||

Net increase (decrease) in net assets derived from capital share transactions | (15,742,087 | ) | 7,386,364 | |||||

|

|

|

| |||||

Net increase (decrease) in net assets | (17,620,613 | ) | 7,242,015 | |||||

Net assets, beginning of year (representing 24,644.02 and 17,535.40 Shares) | 25,566,119 | 18,324,104 | ||||||

|

|

|

| |||||

Net assets, end of year (representing 8,314.38 and 24,644.02 Shares) | $ | 7,945,506 | $ | 25,566,119 | ||||

|

|

|

| |||||

Distributions in excess of net investment income at end of year | $ | (40,751 | ) | $ | (43,440 | ) | ||

|

|

|

| |||||

| The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. | Private Advisors Alternative Strategies Fund | 11 |

Private Advisors Alternative Strategies Fund

(A Delaware Statutory Trust)

Statement of Cash Flows for the year ended March 31, 2016

| Cash flows from operating activities | ||||

Net increase (decrease) in net assets resulting from operations | $ | (1,772,914 | ) | |

Adjustments to reconcile net increase (decrease) in net assets resulting from operations to net cash provided by (used in) operating activities: | ||||

Purchase of investment in Private Advisors Alternative Strategies Master Fund | (299,432 | ) | ||

Proceeds from sale of investment in Private Advisors Alternative Strategies Master Fund | 16,072,306 | |||

Net realized (gain) loss on investment in Private Advisors Alternative Strategies Master Fund | 1,712,521 | |||

Net change in unrealized (appreciation) depreciation on investment in Private Advisors Alternative Strategies Master Fund | 168,694 | |||

Changes in operating assets and liabilities: | ||||

Due from Master Fund | (13,841,057 | ) | ||

Due from Manager | (25,589 | ) | ||

Prepaid assets | 34,104 | |||

Accrued expenses and other liabilities | 32,275 | |||

|

| |||

Net cash provided by (used in) operating activities | 2,080,908 | |||

|

| |||

| Cash flows from financing activities | ||||

Subscriptions | 100,000 | |||

Redemptions, net of redemptions payable | (2,106,249 | ) | ||

Distributions paid | (393 | ) | ||

|

| |||

Net cash provided by (used in) financing activities | (2,006,642 | ) | ||

|

| |||

Net increase (decrease) in cash | 74,266 | |||

Cash, beginning of year | 28,219 | |||

|

| |||

Cash, end of year | $ | 102,485 | ||

|

| |||

Supplemental disclosure of cash flow information: | ||||

Distributions reinvested | $ | 105,219 | ||

|

| |||

| 12 | Private Advisors Alternative Strategies Fund | The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. |

Private Advisors Alternative Strategies Fund

(A Delaware Statutory Trust)

Financial Highlights selected per share data and ratios

| Year ended March 31, | May 1, 2012 (commencement March 31, | |||||||||||||||

| 2016 | 2015 | 2014 | 2013 | |||||||||||||

Per Share operating performance: | ||||||||||||||||

Net asset value at beginning of year | $ | 1,037.42 | $ | 1,044.98 | $ | 1,061.34 | $ | 1,000.00 | ||||||||

Net investment income (loss) (a) | 4.87 | 14.47 | 113.06 | (0.85 | ) | |||||||||||

Net realized and unrealized gain (loss) on investment | (82.06 | ) | (7.81 | ) | (46.70 | ) | 67.51 | |||||||||

|

|

|

|

|

|

|

| |||||||||

Net increase (decrease) resulting from operations | (77.19 | ) | 6.66 | 66.36 | 66.66 | |||||||||||

|

|

|

|

|

|

|

| |||||||||

Distributions paid from: | ||||||||||||||||

Net investment income | (4.60 | ) | (13.89 | ) | (82.72 | ) | (5.32 | ) | ||||||||

Net realized gain on investment | — | (0.33 | ) | — | — | |||||||||||

|

|

|

|

|

|

|

| |||||||||

| (4.60 | ) | (14.22 | ) | (82.72 | ) | (5.32 | ) | |||||||||

|

|

|

|

|

|

|

| |||||||||

Net asset value at end of year | $ | 955.63 | $ | 1,037.42 | $ | 1,044.98 | $ | 1,061.34 | ||||||||

|

|

|

|

|

|

|

| |||||||||

Total investment return (b) | (7.45 | %) | 0.66 | % | 6.37 | % | 6.69 | % (c) | ||||||||

Ratios (to average net assets)/Supplemental Data | ||||||||||||||||

Net investment income (loss) | 0.48 | % | 1.40 | % | 10.62 | % | (0.09 | %)†† | ||||||||

Net expenses (d) | 1.97 | % | 2.25 | % | 2.25 | % | 2.25 | % †† | ||||||||

Expenses (before waiver/reimbursement) (d) | 4.21 | % | 4.35 | % | 5.30 | % | 50.97 | % †† | ||||||||

Portfolio turnover rate (e) | 9 | % | 9 | % | 10 | % | 0 | % (f) | ||||||||

Net assets at end of year (in 000’s) | $ | 7,946 | $ | 25,566 | $ | 18,324 | $ | 1,385 | ||||||||

| †† | Annualized. |

| (a) | Per share data based on average shares outstanding during the year/period. |

| (b) | Total investment return is calculated exclusive of sales charges and assumes the reinvestment of dividends and distributions. |

| (c) | Total investment return is not annualized. |

| (d) | Ratio includes indirect expenses of the Master Fund, after waivers and reimbursements of Master Fund expenses. Without such waivers and reimbursements, the ratio would have been 4.89%, 4.59%, 5.92% and 52.31%, for the periods ending March 31, 2016, 2015, 2014 and 2013, respectively. |

| (e) | The portfolio turnover rate reflects the investment activities of the Master Fund. |

| (f) | Portfolio turnover was calculated at 0.00% as a result of no securities sold during the year from May 1, 2012 (commencement of operations) through March 31, 2013. |

The above ratios and total return have been calculated for the Shareholders taken as a whole. An individual Shareholder’s ratios and total return may vary from these due to the timing of capital share transactions.

| The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. | Private Advisors Alternative Strategies Fund | 13 |

Private Advisors Alternative Strategies Fund

(A Delaware Statutory Trust)

1. Organization and Business

Private Advisors Alternative Strategies Fund (the “Feeder Fund”) was organized on December 15, 2011 as a Delaware statutory trust pursuant to an Agreement and Declaration of Trust (“Declaration of Trust”) dated December 14, 2011 and amended and restated June 4, 2015. The Feeder Fund is a non-diversified, closed-end management investment company registered under the Investment Company Act of 1940, as amended (“1940 Act”). The Feeder Fund commenced investment operations on May 1, 2012 (“Commencement of Operations”).

The Feeder Fund is a “Feeder” fund within what is known in the investment company industry as a “master-feeder” structure. Within this structure, the Feeder Fund invests substantially all of its assets, net of reserves maintained for reasonably anticipated expenses, in another closed-end, non-diversified management investment company, Private Advisors Alternative Strategies Master Fund (the “Master Fund,” and together with the Feeder Fund, the “Funds”).

On November 2, 2015, the Board of Trustees (the “Board”) of the Feeder Fund, upon the recommendation of New York Life Investment Management LLC (“New York Life Investments” or the “Manager”), approved a proposal to liquidate the Feeder Fund and a plan of liquidation for the Feeder Fund. The Feeder Fund was closed to any subscriptions as of December 1, 2015 and will not make any further tender offers to repurchase the Feeder Fund’s shares of beneficial interest (“Shares”).

Upon the repurchase of all of the outstanding shares of any third-party investors, the Master Fund intends promptly to de-register under the 1940 Act.

The investment objective of the Master Fund, which has the same investment objective as the Feeder Fund, is to seek long-term capital appreciation above equity returns over a full market cycle with volatility that is lower than that of the equity market and returns that demonstrate a low correlation to both traditional equity and fixed income markets. The Master Fund seeks to achieve this investment objective by investing principally in private investment funds or “hedge funds” managed by third-party portfolio managers (“Portfolio Managers”) who employ diverse styles and strategies (“Hedge Funds”). The Master Fund generally seeks to invest in Hedge Funds managed by Portfolio Managers who have proven investment management experience and who invest in the Hedge Funds they manage alongside their client capital. The investment strategies employed by the Portfolio Managers selected may include, among others, credit, convertible arbitrage, event-driven, distressed debt, global macro, income, long/short credit and equity, and relative value/arbitrage strategies (please see the Funds’ prospectuses for more information on strategies employed by the Portfolio Managers). In the process of preparing for the liquidation of the Funds, effective December 1, 2015, the Funds were no longer pursuing their investment objectives or being managed consistent with their investment strategies as stated in the prospectuses.

As of March 31, 2016, the Feeder Fund represented $7,882,165 or 18.08% of the Master Fund’s net assets. The financial statements of the Master Fund, including the Schedule of Investments, are attached to

this report and should be read in conjunction with the Feeder Fund’s financial statements.

New York Life Investments, a Delaware limited liability company, is registered as an investment adviser under the Investment Advisers Act of 1940, as amended (“Advisers Act”), and serves as the Funds’ investment manager. New York Life Investments has in turn delegated its portfolio management responsibilities to Private Advisors LLC, a Virginia limited liability company, (“Private Advisors”), which serves as the Funds’ subadvisor (together with New York Life Investments, the “Advisors”). Private Advisors is an affiliate of New York Life Investment Management Holdings LLC. Subject to policies adopted by the Board, Private Advisors, among other things, (i) manages the day-to-day investment operations of the Funds, (ii) seeks investment opportunities for the Funds, and (iii) monitors the performance of and makes investment and trading decisions with respect to the Funds’ investment portfolio.

Private Advisors is subject to supervision by the Manager in its management of the Funds. The Board has overall responsibility for oversight of the Funds. A majority of the Trustees are “Independent Trustees” who are not “interested persons” (as defined by the 1940 Act) of the Funds.

2. Significant Accounting Policies

The Feeder Fund prepares its financial statements, which are expressed in U.S. dollars, in accordance with generally accepted accounting principles in the United States of America (“GAAP”) and follows significant accounting policies described below.

Management has determined that the Feeder Fund is an investment company in accordance with Accounting Standards Codification Topic 946, Investment Companies, for the purpose of financial reporting.

Investment in the Fund

NYLIFE Distributors LLC (“Distributor”), an affiliate of the Advisors, acts as the distributor of the Shares. The Distributor may enter into selected dealer arrangements with various brokers, dealers, banks and other financial intermediaries (“Financial Intermediaries”) to sell Shares.

The Feeder Fund was closed to any subscriptions effective December 1, 2015. Although Shares are registered under the Securities Act of 1933, as amended (“Securities Act”), investments in the Feeder Fund generally could be made only by investors that satisfy the definition of “accredited investors” as defined in Rule 501(a) of Regulation D under the Securities Act (“Eligible Investors”). Prior to December 1, 2015, Eligible Investors who subscribed for Shares and were admitted to the Feeder Fund became shareholders (“Shareholders”) of the Feeder Fund. Generally, Shares were continuously offered on a monthly basis at a price equal to their then current net asset value (“NAV”) per Share, plus a sales load. The minimum initial subscription for Shares was $50,000, and the minimum subsequent subscriptions were $10,000. The Feeder Fund could accept subscriptions for lesser amounts at the discretion of the Advisors. Shares were offered for purchase as of the first business day of each month or at such other times as determined in the discretion of the Board. Shares were subject to substantial restrictions on transferability and resale, and could not be transferred or resold except as permitted

| 14 | Private Advisors Alternative Strategies Fund |

under the Feeder Fund’s Declaration of Trust. As described below, the Feeder Fund, however, offered to repurchase Shares pursuant to written tenders by Shareholders at those times, in those amounts, and on such terms and conditions as the Board determined in its sole discretion.

The Feeder Fund did not make any further tender offers to repurchase Shares effective December 1, 2015. No Shareholder or other person holding Shares acquired from a Shareholder had the right to require the Feeder Fund to redeem Shares. Prior to December 1, 2015, however, the Feeder Fund from time to time offered to repurchase Shares from its Shareholders in accordance with written tenders by Shareholders. Each tender offer was limited and was generally applied to up to 20% of the net assets of the Feeder Fund at that time. If a tender offer was oversubscribed, the Feeder Fund, in its sole discretion, either (a) accepted the additional Shares permitted to be accepted pursuant to Rule 13e-4(f)(1) under the Securities Exchange Act of 1934, as amended; (b) extended the tender offer, if necessary, and increased the number of Shares that the Feeder Fund was offering to repurchase to a number it believed sufficient to accommodate the excess Shares tendered as well as any Shares tendered during the extended offer; or (c) accepted Shares tendered on or before the expiration date of the tender offer for payment on a pro rata basis based on the number of tendered Shares. In determining whether the Feeder Fund offered to repurchase Shares from Shareholders, the Board considered the recommendations of the Advisors as to the timing of such a tender offer, as well as a variety of operational, business and economic factors. In the event that the Feeder Fund did not at least once during any 24 consecutive month period beginning after January 1, 2013, offer to repurchase Shares tendered in accordance with such terms and conditions as the Board determined in its sole discretion, the Board was required to call a meeting of Shareholders for the purposes of considering whether to dissolve the Feeder Fund.

The Feeder Fund was not required to conduct a tender offer and was less likely to conduct tenders during periods of exceptional tender conditions or when Hedge Funds suspend redemptions. The Feeder Fund required that each tendering Shareholder tender a minimum of $25,000 worth of Shares, subject to the Board’s ability to permit a Shareholder to tender a lesser amount in its discretion.

The Feeder Fund reserved the right to reject any subscription to purchase, and the Board could suspend or terminate the sale of Shares at any time, in whole or in part.

A 5.00% early repurchase fee (“Repurchase Fee”) was assessed to any Shareholder that tendered his or her Shares to the Feeder Fund prior to the business day immediately preceding the one-year anniversary of the Shareholder’s purchase of the respective Shares. The Repurchase Fee applied separately to each purchase of Shares made by a Shareholder. The amount received from the Repurchase Fee stayed in the Funds. The purpose of the Repurchase Fee was to, among other things, discourage short-term investments, which are generally disruptive to the Feeder Fund’s investment program. The Repurchase Fee was not assessed in connection with the redemption to external shareholders as a result of the liquidation.

Investment in the Master Fund

The Feeder Fund invests substantially all of its assets, net of reserves for reasonable anticipated expenses, in the Master Fund. The Feeder Fund’s investment in the Master Fund is valued at the Master Fund’s NAV as a practical expedient, as the Master Fund does for its investments in Hedge Funds as discussed in Note 4 of the Master Fund’s financial statements. The performance of the Feeder Fund is directly affected by the performance of the Master Fund. The financial statements of the Master Fund, which are attached, are an integral part of these financial statements. Please refer to the accounting policies disclosed in the financial statements of the Master Fund for additional information regarding significant accounting policies that affect the Feeder Fund. The Feeder Fund records its investment in the Master Fund at fair value which is represented by the Feeder Fund’s proportionate interest in the net assets of the Master Fund.

The Feeder Fund will record security transactions in shares of the Master Fund on the trade date. Realized gains and losses on security transactions are determined using the identified cost method.

The Feeder Fund purchased 305.479 shares of the Master Fund in the amount of $299,432. The Feeder Fund sold 16,704.513 shares of the Master Fund in the amount of $16,072,306.

Distribution of Income and Gains

The Feeder Fund intends to distribute all of its net investment income, and net short-term and long-term capital gain, if any, to Shareholders each year as required to maintain regulated investment company (“RIC”) status. Distributions will be made to each Shareholder pro rata based upon the number of Shares held by such Shareholder on the record date and will be net of expenses. Dividends and distributions are recorded on the ex-dividend date. Pursuant to the plan of liquidation for the Feeder Fund, Shareholders will also receive payment in the amount equal to the NAV per Share of the Feeder Fund as of March 31, 2016 (the “Valuation Date”). Payment was made in cash on or about 45 business days after the Valuation Date. The Feeder Fund has determined not to hold back any amount payable to repurchase the Shares. At this same time, the Feeder Fund will pay-out any net realized capital gains and income realized from the Feeder Fund’s tax year-end through the Valuation Date as well as any amounts due to Shareholders as post-audit payments from previous tender offers. Dividends and distributions to shareholders are determined in accordance with federal income tax regulations and may differ from GAAP. Dividends from net investment income for the year ended March 31, 2016 represent distributions from ordinary income for tax purposes arising primarily from mark-to-market adjustments relating to investments in passive foreign investment companies held in the Master Fund.

In order to satisfy the diversification requirements under Subchapter M of the Internal Revenue Code, of 1986, as amended (the “Code”), the Master Fund generally invests its assets in Hedge Funds organized outside the United States that are treated as corporations for U.S. tax purposes and are expected to be classified as passive foreign invest-

| Private Advisors Alternative Strategies Fund | 15 |

Private Advisors Alternative Strategies Fund

(A Delaware Statutory Trust)

Notes to Financial Statements (continued)

ment companies (“PFICs”). As such, the Master Fund expects that its distributions generally will be taxable as ordinary income to the Shareholders.

Pursuant to the dividend reinvestment plan established by the Feeder Fund (“DRIP”), each Shareholder whose Shares are registered in its own name will automatically be a participant under the DRIP and have all income, dividends and/or capital gains distributions automatically reinvested in additional Shares at NAV unless such Shareholder specifically elects to receive all income, dividends and capital gain distributions in cash.

Statement of Cash Flows

The cash amount shown in the Statement of Cash Flows of the Feeder Fund is the amount included in the Feeder Fund’s Statement of Assets and Liabilities and represents the cash on hand at its custodian and does not include any short-term investments or restricted cash.

Income and Operating Expenses

The Feeder Fund bears its own expenses including, but not limited to, legal expenses, accounting expenses (including third-party accounting services), auditing and other professional expenses, and administration expenses. In addition, the Feeder Fund indirectly bears a pro rata share of the fees and expenses of the Master Fund and the Hedge Funds in which the Master Fund invests. Because the Hedge Funds have varied expense and fee levels and the Master Fund may own different proportions of the Hedge Funds at different times, the amount of fees and expenses incurred indirectly by the Feeder Fund may vary. These indirect expenses of the Master Fund and Hedge Funds are reflected in net realized gain/(loss) and net change in unrealized appreciation/(depreciation) on investments on the Feeder Fund’s Statement of Operations. Operating expenses are recorded as incurred.

Income is derived from distributions from the Master Fund arising from mark to market adjustments relating to investments in passive foreign investment companies held in the Master Fund.

Use of Estimates

In preparing financial statements in conformity with GAAP, management makes estimates and assumptions that affect the reported amounts and disclosures in the financial statements. Actual results could differ from those estimates.

3. Income Taxes

Federal Income Taxes

The Feeder Fund intends to comply with the requirements of the Code applicable to regulated investment companies (“RICs”) and to distribute substantially all of its taxable income to its Shareholders. Therefore, no provision for federal income taxes is required. The Feeder Fund has adopted a tax year-end of October 31. The Feeder Fund files tax returns with the U.S. Internal Revenue Service and various states. The Feeder

Fund may be subject to taxes imposed by countries in which it invests. Such taxes are generally based on income earned or gains realized or repatriated. Taxes are accrued and applied to net investment income, net realized capital gains and net unrealized appreciation, as applicable, as the income is earned or capital gains are recorded. Management evaluates its tax positions to determine if the tax positions taken meet the minimum recognition threshold in connection with accounting for uncertainties in income tax positions taken or expected to be taken for the purposes of measuring and recognizing tax liabilities in the financial statements. Recognition of tax benefits of an uncertain tax position is required only when the position is “more likely than not” to be sustained assuming examination by taxing authorities. Management has analyzed the Feeder Fund’s tax positions taken on federal, state and local income tax returns for the open tax years (for up to three tax years), and has concluded that no provision for federal, state and local income tax is required in the Feeder Fund’s financial statements. The Feeder Fund’s federal, state and local income and federal excise tax returns for tax years for which the applicable statutes of limitation have not expired are subject to examination by the U.S. Internal Revenue Service and state and local departments of revenue.

The tax character of distributions paid for the year ended March 31, 2015 of $352,785 of which $345,384 was ordinary income and $7,401 was long-term capital gain. The tax character of distributions for the year ended March 31, 2016 of $105,612 was ordinary income, and is subject to recharacterization until the end of the Feeder Fund’s tax year end on October 31, 2016.

As of October 31, 2015, the components of distributable earnings on a tax basis were as follows:

Unrealized appreciation (depreciation) | $ | (1,273,596 | ) | |

Other temporary differences | (150,338 | ) | ||

Capital loss carryforward | (70,607 | ) |

As of October 31, 2015, capital loss carryforwards available for federal income tax purposes were $70,607 for long-term. This amount has no expiration.

The difference between book-basis and tax-basis unrealized appreciation (depreciation) is primarily due to wash sale adjustments. Other temporary differences are related to late year ordinary loss deferrals.

As of October 31, 2015, the cost and related gross unrealized appreciation and depreciation for tax purposes were as follows:

Cost of investments for tax purposes | $ | 24,132,462 | ||

Gross tax unrealized appreciation | $ | — | ||

Gross tax unrealized depreciation | (1,273,596 | ) | ||

Net tax unrealized appreciation (depreciation) on investments | $ | (1,273,596 | ) |

4. Fees and Related Party Transactions

The Feeder Fund bears all of the expenses of its own operations, including, but not limited to, expenses borne indirectly through the

| 16 | Private Advisors Alternative Strategies Fund |

Feeder Fund’s investment in the Master Fund. The Feeder Fund and its Shareholders are indirectly subject to the investment management fee charged to the Master Fund by New York Life Investments. Please refer to Note 5 of the Master Fund’s financial statements for a discussion of the computation of the investment management fee.

The Feeder Fund’s investment management fee (“Management Fee”) is 0.0917% (1.10% on an annual basis) of the Feeder Fund’s month-end NAV; however, New York Life Investments has contractually agreed to waive the Management Fee paid by the Feeder Fund as long as the Feeder Fund remains in the “master-feeder” structure, and invests substantially all of its assets, net of reserves maintained for reasonably anticipated expenses, in the Master Fund.

Effective December 1, 2015, New York Life Investments also began waiving the Master and Feeder Funds management fees.

New York Life Investments has contractually agreed to waive fees and/or reimburse the Master Fund for expenses (excluding taxes, interest, litigation, extraordinary expenses, brokerage and other transaction expenses relating to the purchase or sale of portfolio investments, and Acquired (Underlying) Fund Fees and Expenses (i.e., the expenses of the Underlying Hedge Funds)) to the extent necessary in order to cap the Master Fund’s total annual operating expenses at 1.50% of its average month-end net assets. New York Life Investments has contractually agreed to reimburse the Feeder Fund for expenses (including the Feeder Fund’s pro rata share of the Master Fund’s expenses but excluding taxes, interest, litigation, extraordinary expenses, brokerage and other transaction expenses relating to the purchase or sale of portfolio investments and Acquired (Underlying) Fund Fees and Expenses) to the extent necessary in order to cap the Feeder Fund’s total annual operating expenses at 2.25% of the Feeder Fund’s average month-end net assets. These agreements will remain in effect until August 1, 2016, and shall renew automatically for one-year terms unless New York Life Investments provides written notice of termination prior to the start of the next term or upon approval of the Board. As of March 31, 2016, $53,661 is due from the Manager.

The Feeder Fund has retained State Street Bank and Trust Company (“State Street”) to provide administrative and accounting services to the Feeder Fund. State Street also serves as the Feeder Fund’s transfer agent and custodian. Under the terms of an administration agreement with the Feeder Fund (“Administration Agreement”), State Street is responsible for, among other things: (i) reconciling cash and investment balances; (ii) maintaining the general ledger and sub-ledger accounts and arranging for the computation of the Feeder Fund’s NAV; (iii) preparing the Feeder Fund’s annual and semi-annual reports; (iv) maintaining the register of Shareholders; (v) processing matters relating to subscriptions for, and repurchases of Shares; and (vi) issuing reports and transaction statements to Shareholders. For its services, State Street is paid a monthly fee directly from the Feeder Fund. For the year ended March 31, 2016, the Feeder Fund incurred transfer agent fees and administration fees of $32,059 and $17,500, respectively.

Prior to December 1, 2015, when the Feeder Fund was closed to subscriptions, Shares were sold subject to a maximum sales load of up to 3.00%. The actual sales load paid by investors may vary in the Distributor’s discretion and/or among Financial Intermediaries. The Distributor or Financial Intermediaries may waive or reduce the sales load at its discretion for any investor. Investors should consult with their Financial Intermediaries about any additional fees or charges they might impose.

The Feeder Fund has adopted a shareholder services plan (“Services Plan”). Under the terms of the Services Plan, the Feeder Fund is authorized to pay to New York Life Investments, its affiliates, or the Financial Intermediaries, as compensation for services rendered to Shareholders, a shareholder service fee at the rate of 0.85% on an annualized basis of the Feeder Fund’s average month-end net assets. Pursuant to the Services Plan, the Feeder Fund may pay for Shareholder services or account maintenance services, including assistance in establishing and maintaining shareholder accounts, processing subscription and repurchase orders, communicating periodically with Shareholders and assisting Shareholders who have questions or other needs relating to their account. Because service fees are ongoing, over time they will increase the cost of an investment in the Feeder Fund and may cost more than certain types of sales charges. The Feeder Fund incurred Shareholder Service fees of $200,061 for the year ended March 31, 2016.

From time to time, the Feeder Fund may have a concentration of Shareholders holding a significant percentage of its net assets. Investment activities of these Shareholders could have a material impact on the Feeder Fund. As of the March 31, 2016 record date, New York Life Investment Management Holdings, LLC, an affiliate of the Advisors, maintains a significant holding in the Feeder Fund which represents 100.00% of the Feeder Fund’s NAV.

5. Offering of Shares

The Feeder Fund’s Share activities for the year ended March 31, 2016 were as follows:

Balance April 1, | Sub- scriptions | Red- emptions | Distributions Reinvested | Balance March 31, | ||||

| 24,644.02 | 97.68 | (16,534.53) | 107.21 | 8,314.38 |

6. Concentration Risk

The Feeder Fund’s investment in the Master Fund has no ready market to provide liquidity. This strategy presents a high degree of business and financial risk due to the Hedge Funds in which the Master Funds invests. The Master Fund’s investments in Hedge Funds are also subject to the risk associated with investing in Hedge Funds. The Hedge Funds are generally illiquid, and thus there can be no assurance that the Master Fund will be able to realize the value of such investments in Hedge Funds in a timely manner. Since many of the Hedge Funds may involve a high degree of investment risk, poor performance by one or more of the Hedge Funds could severely affect the total returns of the Master Fund and the Feeder Fund.

| Private Advisors Alternative Strategies Fund | 17 |

Private Advisors Alternative Strategies Fund

(A Delaware Statutory Trust)

Notes to Financial Statements (continued)

7. Contractual Obligations

The Feeder Fund enters into contracts that contain a variety of indemnifications. The Feeder Fund’s maximum exposure under these arrangements is unknown. However, the Feeder Fund has not had prior claims or losses pursuant to these contracts and expects the risk of loss to be remote.

8. Subsequent Events

In connection with the preparation of the financial statements of the Feeder Fund for the year ended March 31, 2016, events and transactions subsequent to March 31, 2016 through the date the financial statements were issued have been evaluated by the Feeder Fund’s management for possible adjustment and/or disclosure. No subsequent events requiring financial statement adjustment or disclosure have been identified, other than the following:

Pursuant to the plan of liquidation, all third-party shareholders have had their account balances redeemed.

| 18 | Private Advisors Alternative Strategies Fund |

Report of Independent Registered Public Accounting Firm

To the Board of Trustees and Shareholders of

Private Advisors Alternative Strategies Master Fund:

In our opinion, the accompanying statement of assets and liabilities, including the schedule of investments, and the related statements of operations, of changes in net assets, and of cash flows and the financial highlights present fairly, in all material respects, the financial position of Private Advisors Alternative Strategies Master Fund (the “Fund”) at March 31, 2016, the results of its operations and its cash flows for the year then ended, the changes in its net assets for each of the two years in the period then ended and the financial highlights for each of the periods presented, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at March 31, 2016 by correspondence with the custodian and underlying portfolio funds, provide a reasonable basis for our opinion.

As discussed in Note 1 to the financial statements, on November 2, 2015, the Board of Trustees approved the liquidation of the Fund. Our opinion is not modified with respect to this matter.

PricewaterhouseCoopers LLP

New York, New York

May 26, 2016

| Private Advisors Alternative Strategies Master Fund | 19 |

Private Advisors Alternative Strategies Master Fund

(A Delaware Statutory Trust)

Schedule of Investments as of March 31, 2016

| First Acquisition Date | Cost | Fair Value | Percent of Net Assets | Next Available Redemption Date* | Liquidity** | |||||||||||||||||||

| Investments in Hedge Funds Cayman Islands Domiciled | ||||||||||||||||||||||||

Distressed Debt | ||||||||||||||||||||||||

Redwood Offshore Fund, Ltd. | 5/1/2012 | $ | 1,200,000 | $ | 1,530,277 | 3.51 | % | 6/30/2016 | Bi-Annually | |||||||||||||||

North America | ||||||||||||||||||||||||

Aurelius Capital International, Ltd. | 5/1/2012 | 1,600,000 | 2,057,264 | 4.72 | 6/30/2016 | Semi-Annually | ||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Total Distressed Debt | 2,800,000 | 3,587,541 | 8.23 | |||||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Event Equity | ||||||||||||||||||||||||

Luxor Capital Partners Offshore, Ltd. | 5/1/2012 | 1,892,110 | 1,367,607 | 3.14 | 6/30/2016 | Quarterly | ||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Global Equity | ||||||||||||||||||||||||

Sheffield International Partners, Ltd. | 5/1/2012 | 1,695,000 | 1,885,284 | 4.33 | 6/30/2016 | Quarterly | ||||||||||||||||||

SRS Partners, Ltd. | 5/1/2012 | 1,248,332 | 1,695,629 | 3.89 | 6/30/2016 | Quarterly | ||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Total Global Equity | 2,943,332 | 3,580,913 | 8.22 | |||||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Global Macro | ||||||||||||||||||||||||

Autonomy Global Macro Fund Ltd. | 6/1/2013 | 526,432 | 647,452 | 1.48 | 4/30/2016 | Monthly | ||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Long/Short Corporate Credit | ||||||||||||||||||||||||

Archer Capital Offshore Fund, Ltd. | 5/1/2012 | 1,801,542 | 1,866,074 | 4.28 | 6/30/2016 | Quarterly | ||||||||||||||||||

Panning Overseas Fund, Ltd. | 6/1/2013 | 1,258,506 | 1,199,669 | 2.75 | 6/30/2016 | Quarterly | ||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Total Long/Short Corporate Credit | 3,060,048 | 3,065,743 | 7.03 | |||||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Multi-Strategy | ||||||||||||||||||||||||

Empyrean Capital Overseas Fund, Ltd. | 8/1/2015 | 1,500,000 | 1,424,842 | 3.27 | 6/30/2016 | Quarterly | ||||||||||||||||||

Fir Tree International Value Fund II, Ltd. | 5/1/2012 | 2,210,000 | 2,149,635 | 4.93 | 4/30/2016 | Annually | ||||||||||||||||||

HBK Multi-Strategy Offshore Fund, Ltd. | 5/1/2012 | 2,009,913 | 2,157,889 | 4.95 | 6/30/2016 | Quarterly | ||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Total Multi-Strategy | 5,719,913 | 5,732,366 | 13.15 | |||||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

U.S. Equity | ||||||||||||||||||||||||

Marble Arch Offshore Partners, Ltd. | 7/1/2012 | 1,200,000 | 1,520,422 | 3.49 | 6/30/2016 | Quarterly | ||||||||||||||||||

North Run Offshore Partners, Ltd. | 5/1/2012 | 1,142,664 | 1,021,810 | 2.35 | 6/30/2016 | Quarterly | ||||||||||||||||||

Southpoint Qualified Offshore Fund, Ltd. | 5/1/2012 | 925,358 | 1,069,600 | 2.45 | 6/30/2016 | Quarterly | ||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Total U.S. Equity | 3,268,022 | 3,611,832 | 8.29 | |||||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Total Cayman Islands Domiciled | 20,209,857 | 21,593,454 | 49.54 | |||||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Total Investments in Hedge Funds | $ | 20,209,857 | 21,593,454 | 49.54 | ||||||||||||||||||||

|

| |||||||||||||||||||||||

Other Assets, less Liabilities | 21,991,565 | 50.46 | ||||||||||||||||||||||

|

|

|

| |||||||||||||||||||||

Net Assets | $ | 43,585,019 | 100.00 | % | ||||||||||||||||||||

|

|

|

| |||||||||||||||||||||

| * | Investments in Hedge Funds may be composed of multiple series. The Next Available Redemption Date refers to the earliest date after March 31, 2016 that redemption from a series is available. Other series may have an available redemption date that is after the Next Available Redemption Date. Redemptions from Hedge Funds may be subject to fees. |

| ** | Available frequency of redemption after initial lock-up period, if any. Different series may have different liquidity terms. |

| 20 | Private Advisors Alternative Strategies Master Fund | The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. |

Private Advisors Alternative Strategies Master Fund

(A Delaware Statutory Trust)

Statement of Assets and Liabilities as of March 31, 2016

| Assets | ||||

Investments in Hedge Funds, at fair value | $ | 21,593,454 | ||

Cash | 26,414,978 | |||

Receivable for investments sold | 16,377,076 | |||

Due from Manager (See Note 5) | 50,575 | |||

Prepaid assets | 3,482 | |||

|

| |||

Total assets | 64,439,565 | |||

|

| |||

| Liabilities | ||||

Redemptions payable | 20,687,102 | |||

Accrued expenses and other liabilities | 167,444 | |||

|

| |||

Total liabilities | 20,854,546 | |||

|

| |||

Net Assets | $ | 43,585,019 | ||

|

| |||

| Composition of Net Assets: | ||||

Paid-in capital | $ | 48,062,875 | ||

Distributions in excess of net investment income | (9,824,643 | ) | ||

Accumulated net realized gain (loss) on investments in Hedge Funds | 3,963,190 | |||

Net unrealized appreciation (depreciation) on investments in Hedge Funds | 1,383,597 | |||

|

| |||

Net Assets | $ | 43,585,019 | ||

|

| |||

| Net Asset Value Per Share: | ||||

45,737.39 Shares issued and outstanding, par value $0.001 per share 450,000 registered shares of beneficial interest | $ | 952.94 | ||

|

| |||

| The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. | Private Advisors Alternative Strategies Master Fund | 21 |

Private Advisors Alternative Strategies Master Fund

(A Delaware Statutory Trust)

Statement of Operations for the year ended March 31, 2016

Expenses | ||||

Management Fee (See Note 5) | $ | 746,138 | ||

Professional fees | 183,587 | |||

Administration and custody fees | 173,377 | |||

Insurance fees | 49,686 | |||

Transfer agent fees | 32,059 | |||

Registration | 22,576 | |||

Shareholder communication | 9,658 | |||

Trustees | 3,631 | |||

Miscellaneous | 7,633 | |||

|

| |||

Total expenses before waiver/reimbursement | 1,228,345 | |||

Expense waiver/reimbursement from Manager | (447,600 | ) | ||

|

| |||

Net expenses | 780,745 | |||

|

| |||

Net investment income (loss) | (780,745 | ) | ||

|

| |||

| Net realized and unrealized gain (loss) on investments | ||||

Net realized gain (loss) on investments in Hedge Funds | 5,890,174 | |||

Net change in unrealized appreciation (depreciation) on investments in Hedge Funds | (9,801,656 | ) | ||

|

| |||

Net realized and unrealized gain (loss) on investments | (3,911,482 | ) | ||

|

| |||

Net increase (decrease) in net assets resulting from operations | $ | (4,692,227 | ) | |

|

| |||

| 22 | Private Advisors Alternative Strategies Master Fund | The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. |

Private Advisors Alternative Strategies Master Fund

(A Delaware Statutory Trust)

Statement of Changes in Net Assets

| Year Ended March 31, 2016 | Year March 31, | |||||||

| Increase (decrease) in net assets resulting from operations: | ||||||||

Net investment income (loss) | $ | (780,745 | ) | $ | (1,002,145 | ) | ||

Net realized gain (loss) on investments in Hedge Funds | 5,890,174 | (705,994 | ) | |||||

Net change in unrealized appreciation (depreciation) on investments in Hedge Funds | (9,801,656 | ) | 2,741,104 | |||||

|

|

|

| |||||

Net increase (decrease) in net assets resulting from operations | (4,692,227 | ) | 1,032,965 | |||||

|

|

|

| |||||

Distributions to shareholders from: | ||||||||

Net investment income | (831,075 | ) | (1,367,396 | ) | ||||

|

|

|

| |||||

Capital share transactions: | ||||||||

Subscriptions (representing 699.28 and 11,019.44 Shares) | 730,000 | 11,418,590 | ||||||

Redemptions (representing 24,225.41 and 3,050.52 Shares) | (23,268,000 | ) | (3,169,817 | ) | ||||

Distributions reinvested (representing 825.37 and 1,302.08 Shares) | 806,333 | 1,320,257 | ||||||

|

|

|

| |||||

Net increase (decrease) in net assets derived from capital share transactions | (21,731,667 | ) | 9,569,030 | |||||

|

|

|

| |||||

Net increase (decrease) in net assets | (27,254,969 | ) | 9,234,599 | |||||

Net assets, beginning of year (representing 68,438.15 and 59,167.15 Shares) | 70,839,988 | 61,605,389 | ||||||

|

|

|

| |||||

Net assets, end of year (representing 45,737.39 and 68,438.15 Shares) | $ | 43,585,019 | $ | 70,839,988 | ||||

|

|

|

| |||||

Distributions in excess of net investment income at end of year | $ | (9,824,643 | ) | $ | (8,862,045 | ) | ||

|

|

|

| |||||

| The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. | Private Advisors Alternative Strategies Master Fund | 23 |

Private Advisors Alternative Strategies Master Fund

(A Delaware Statutory Trust)

Statement of Cash Flows for the year ended March 31, 2016

| Cash flows from operating activities | ||||

Net increase (decrease) in net assets resulting from operations | $ | (4,692,227 | ) | |

Adjustments to reconcile net increase (decrease) in net assets resulting from operations to net cash provided by (used in) operating activities: | ||||

Purchases of investments in Hedge Funds | (5,400,000 | ) | ||

Proceeds from sales of investments in Hedge Funds | 47,506,898 | |||

Net realized (gain) loss on investments in Hedge Funds | (5,890,174 | ) | ||

Net change in unrealized (appreciation) depreciation on investments in Hedge Funds | 9,801,656 | |||

Changes in operating assets and liabilities: | ||||

Receivable for investments sold | (14,799,209 | ) | ||

Due from Manager | (50,575 | ) | ||

Prepaid assets | 32,381 | |||

Accrued expenses and other liabilities | 57,172 | |||

Management fee payable | (34,270 | ) | ||

|

| |||

Net cash provided by (used in) operating activities | 26,531,652 | |||

|

| |||

| Cash flows from financing activities | ||||

Subscriptions | 730,000 | |||

Redemptions, net of redemptions payable | (2,888,768 | ) | ||

Distributions paid | (24,742 | ) | ||

|

| |||

Net cash provided by (used in) financing activities | (2,183,510 | ) | ||

|

| |||

Net increase (decrease) in cash | 24,348,142 | |||

Cash, beginning of year | 2,066,836 | |||

|

| |||

Cash, end of year | $ | 26,414,978 | ||

|

| |||

Supplemental disclosure of cash flow information: | ||||

Distributions reinvested | $ | 806,333 | ||

|

| |||

In-kind redemptions from Hedge Funds | $ | 70,377 | ||

|

| |||

| 24 | Private Advisors Alternative Strategies Master Fund | The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. |

Private Advisors Alternative Strategies Master Fund

(A Delaware Statutory Trust)

Financial Highlights selected per share data and ratios

| Year ended March 31, | May 1, 2012 (commencement March 31, | |||||||||||||||

| 2016 | 2015 | 2014 | 2013 | |||||||||||||

Per Share operating performance: | ||||||||||||||||

Net asset value at beginning of year | $ | 1,035.10 | $ | 1,041.21 | $ | 1,054.76 | $ | 1,000.00 | ||||||||

Net investment income (loss) (a) | (11.86 | ) | (15.48 | ) | (16.35 | ) | (13.87 | ) | ||||||||

Net realized and unrealized gain (loss) on investments in Hedge Funds | (57.86 | ) | 29.69 | 90.05 | 86.21 | |||||||||||

|

|

|

|

|

|

|

| |||||||||

Net increase (decrease) resulting from operations | (69.72 | ) | 14.21 | 73.70 | 72.34 | |||||||||||

|

|

|

|

|

|

|

| |||||||||

Distributions paid from: | ||||||||||||||||

Net investment income | (12.44 | ) | (20.32 | ) | (87.25 | ) | (17.58 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

Net asset value at end of year | $ | 952.94 | $ | 1,035.10 | $ | 1,041.21 | $ | 1,054.76 | ||||||||

|

|

|

|

|

|

|

| |||||||||

Total investment return (b) | (6.76 | %) | 1.40 | % | 7.12 | % | 7.32 | % (c) | ||||||||

Ratios (to average net assets)/Supplemental Data | ||||||||||||||||

Net investment income (loss) (d) | (1.18 | %) | (1.50 | %) | (1.50 | %) | (1.50 | %)†† | ||||||||

Net expenses (d) | 1.18 | % | 1.50 | % | 1.50 | % | 1.50 | % †† | ||||||||

Expenses (before waiver/reimbursement) (d) | 1.86 | % | 1.74 | % | 2.12 | % | 2.84 | % †† | ||||||||

Portfolio turnover rate (e) | 9 | % | 9 | % | 10 | % | 0 | % (f) | ||||||||

Net assets at end of year (in 000’s) | $ | 43,585 | $ | 70,840 | $ | 61,605 | $ | 44,987 | ||||||||

| †† | Annualized. |

| (a) | Per share data based on average shares outstanding during the year/period. |

| (b) | Total investment return is calculated exclusive of sales charges and assumes the reinvestment of dividends and distributions. |

| (c) | Total investment return is not annualized. |

| (d) | Ratios of expenses and net investment income (loss) do not include the impact of expenses and incentive allocations or incentive fees related to the Underlying Hedge Funds. |

| (e) | The portfolio turnover rate reflects the investment activities of the Master Fund. |

| (f) | Portfolio turnover was calculated at 0.00% as no securities were sold during the year from May 1, 2012 (commencement of operations) through March 31, 2013. |

The above ratios and total return have been calculated for the Shareholders taken as a whole. An individual Shareholder’s ratios and total return may vary from these due to the timing of capital share transactions.

| The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. | Private Advisors Alternative Strategies Master Fund | 25 |

Private Advisors Alternative Strategies Master Fund

(A Delaware Statutory Trust)

1. Organization and Business

Private Advisors Alternative Strategies Master Fund (the “Master Fund”) was organized on December 15, 2011 as a Delaware statutory trust pursuant to an Agreement and Declaration of Trust (“Declaration of Trust”) dated December 14, 2011 and amended and restated June 4, 2015. The Master Fund is a non-diversified, closed-end management investment company registered under the Investment Company Act of 1940, as amended (“1940 Act”). The Master Fund commenced investment operations on May 1, 2012 (“Commencement of Operations”).

The Master Fund is a “Master” fund within what is known in the investment company industry as a “master-feeder” structure. Within this structure, another closed-end, non-diversified management investment company, Private Advisors Alternative Strategies Fund (the “Feeder Fund”), invests substantially all of its assets, net of reserves maintained for reasonably anticipated expenses, in the Master Fund. The Master Fund may also accept investments from certain other investors as well, including, among others, investors purchasing shares through (i) certain “wrap fee” or other programs sponsored by financial intermediary firms and (ii) certain non-broker/dealer registered investment advisory firms.

On November 2, 2015, the Board of Trustees (the “Board”) of the Master Fund, upon the recommendation of New York Life Investment Management LLC (“New York Life Investments” or the “Manager”), approved a proposal to liquidate the Master Fund and a plan of liquidation for the Master Fund. The Master Fund was closed to any subscriptions as of December 1, 2015 and will not make any further tender offers to repurchase the Master Fund’s shares of beneficial interest (“Shares”).

New York Life Investments began waiving the management fees for the Master Fund starting December 1, 2015.

Upon the repurchase of all of the outstanding shares of any third-party investors, the Master Fund intends promptly to de-register under the 1940 Act.