![]()

March 13, 2012

Via EDGAR and overnight mail

Ms. Mara L. Ransom

Assistant Director

Division of Corporation Finance

Securities and Exchange Commission

100 F Street, NE

Washington, DC 20549

| Re: | Contemporary Signed Books, Inc. | |

| Amendment No. 1 to Registration Statement on Form S-1 | ||

| Filed February 3, 2012 | ||

| File No. 333-178490 |

Dear Ms. Ransom:

We are counsel to Contemporary Signed Books, Inc. (the “Company” or “our client”). On behalf of our client, we respond as follows to the staff of the Division of the Corporation Finance (the “Staff”) of the Securities and Exchange Commission (the “SEC”)’s comment letter dated February 29, 2012 relating to the above-captioned filing. Captions and section headings herein will correspond to those set forth in Amendment No. 2 to the Registration Statement on Form S-1 (“Registration Statement”), a copy of which has been marked with the changes from Amendment No.1 to Registration Statement on Form S-1, and is enclosed herein. Please note that for the Staff’s convenience, we have recited each of the Staff’s comments and provided the Company’s response to each comment immediately thereafter.

| 1 |

General

Comment 1. We note your response to comment 7 in our letter dated January 11, 2012. Because the terms of the promissory note have not yet been determined by you and will be determined at the time of each sale, please indicate as much throughout your prospectus and include an appropriate risk factor concerning the fact that the terms are unknown and that investors will not be able to assess the risk of the promissory notes to the company. Please also address the following:

| • | Please provide us with your counsel’s analysis as to how the issuance of stock pursuant to the unknown terms of a promissory note satisfies Section 152 of the Delaware General Corporation Law, which requires that consideration be paid in such form as the board of directors shall authorize such as cash, any tangible or intangible property or any benefit to the corporation. In doing so, please tell us at what point any shares that have been issued in partial consideration of a promissory note will be considered “fully paid and nonassessable;” |

| • | If the terms of the promissory notes are unknown, please also tell us what consideration you have given as to how your shares are being offered at a price that is fixed when it would appear that the consideration is variable depending upon the terms negotiated between the investor and the company; and |

| • | We note your indication that you cannot file a form of promissory note. Please file a form of promissory note that reflects as many of the terms that you anticipate requiring, including duration, interest rate and recourse provisions. |

Response: The Registration Statement has been revised throughout to indicate that the Company may choose to accept the payment in the form of promissory note, provided however, that payment by promissory notes shall be for the same price of $0.05 and shall be limited to 25% of the aggregate purchase proceeds. Please see page ii, 3, 13, 21, and 44 of the Registration Statement. In addition, we have included the requested risk factor. Please see page 11 of the Registration Statement.

The Company’s counsel has been advised by the Company that before promissory notes are accepted as a payment for the shares being offered, such will be approved by the Company’s Board of Directors in accordance with the Delaware General Corporation Law. In addition, the shares shall be deemed to be “fully paid and non-assessable” only upon full payment of the promissory note.

The Company intends that the purchase price for the shares will be set at $0.05 regardless of the payment method. In the event that the Board of Directors chooses to accept payment in the form of promissory notes, the only variable terms would be those relating to the duration of the note or the events of default.

A form of the promissory note has been filed as Exhibit 99.1 to this Registration Statement.

| 2 |

Registration Statement Facing Page

Comment 2. We note that you have reduced the number of shares you are offering. Please revise your fee table to reflect the reduction in shares being registered.

Response: The fee table has been revised to reflect that the Company has reduced the number of shares the Company is offering. Please see the Registration Statement Cover Page.

Prospectus Summary, page 1

Corporate Background and Business Overview, page 1

Comment 3. The amount of cumulative losses disclosed in the second paragraph differs from the net loss from inception to November 30, 2011 disclosed in the unaudited statements of operations. Please revise or clarify your disclosure accordingly.

Response: The amount of cumulative losses disclosed in the second paragraph has been revised to conform to the net loss disclosed in the unaudited statement of operations. Please see page 1 of the Registration Statement.

Going Concern Consideration, page 1

Comment 4. The reference to footnote 3 to your financial statements is incorrect. Please revise to reference footnote 6 to your financial statements.

Response: The Registration Statement has been revised in response to this comment. Please see page 1 of the Registration Statement.

Summary Financial Information, page 1

Comment 5. The net loss for the three months ended November 30, 2011 differs from the amount of net income reported in the unaudited statements of operations. Please revise or advise.

Response: The net loss for the three months ended November 30, 2011 has been revised to conform to the amount of net income reported in the unaudited statement of operations. Please see page 1 of the Registration Statement.

Plan of Distribution, page 21

Comment 6. On page 22, in the last sentence of the first full paragraph you state “Sales by the selling stockholders must be made at the fixed price of $0.05 until a market develops for our common stock.” Please revise this sentence to state that selling shareholders will sell at the fixed price until your shares are quoted on the OTC Bulletin Board.

| 3 |

Response: The Registration Statement has been revised in response to the comment. Please see page 22 of the Registration Statement.

Our Business, page 27

Overview, page 27

Comment 7. The amount of cumulative losses disclosed in the first paragraph differs from the net loss from inception to November 30, 2011 disclosed in the unaudited statements of operations. Please revise or clarify your disclosure accordingly.

Response: The amount of cumulative losses disclosed in the first paragraph has been revised to conform to the net loss disclosed in the unaudited statement of operations. Please see page 27 of the Registration Statement.

Market Opportunity, page 28

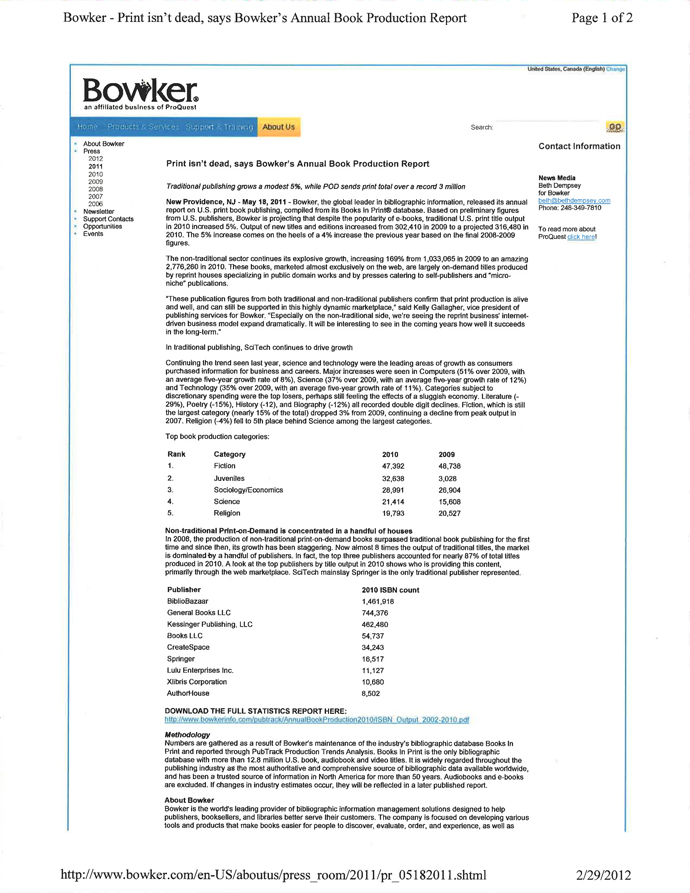

Comment 8. We note your response to comment 15 in our letter dated January 11, 2012. Please provide us with a copy of the report released by Bowker.

Response: A copy of the report released by Bowker has been filed supplementally as Exhibit 1 to this Response Letter. In addition, the Company has revised paragraph 2 and footnote (2) in the section entitled “Product Development” according to the updated report. Please see page 34 of the Registration Statement.

Revenue, page 36

Comment 9. We note that the amount of revenue disclosed in the first paragraph differs from the amount of revenue reported in the statements of operations. Please revise.

Response: The amount of revenue disclosed in the first paragraph has been revised to conform to the unaudited statement of operations. Please see page 36 of the Registration Statement.

Executive Compensation, page 40

Comment 10. We note that you updated this information as of a more recent date, however, it is not clear why you updated it through November 30, 2010, as opposed to August 31, 2011, the most recent fiscal year end. Please revise.

| 4 |

Response: The Executive Compensation has now been updated through November 30, 2011. Please see page 40 of the Registration Statement.

Management’s Discussion and Analysis of Financial Condition and Results of Operations, page 42

Going Concern Consideration, page 45

Comment 11. The reference to footnote 3 in the last sentence is incorrect. Please revise to reference footnote 6 to the financial statements.

Response: The Registration Statement has been revised to refer to footnote 6 in response to this comment. Please see page 45 of the Registration Statement.

Financial Statements, page 48

Statements of Cash Flows (Unaudited), page 4

Comment 12. Please disclose the cumulative gain on forgiveness of debt for the period from inception to November 30, 2011.

Response: The unaudited financial statement has been revised to disclose the cumulative gain on forgiveness of debt for the period from inception to November 30, 2011. Please see page Q4 of the unaudited financial statements.

Exhibit 23.1

Comment 13. We note that the consent does not refer to the statements of operations, changes in stockholders’ equity and cash flows for the year ended August 31, 2011. Please revise.

Response: The Auditor’s Consent has been revised to specifically refer to the statement of operations, changes in stockholders’ equity and cash flows for the year ended August 31, 2011. Please see Exhibit 23.1 of the Registration Statement.

************

We trust that the foregoing is responsive to the Staff’s comments. Please do not hesitate to contact the undersigned at (212) 752-9700 if you have any questions. Thank you.

| Very truly yours, | |

| /s/ Arthur S. Marcus | |

| Arthur S. Marcus, Esq. |

| 5 |