Exhibit 99.1

INDEPENDENCE CONTRACT DRILLING

ICD LISTED NYSE

Scotia Howard Weil 2016 Energy Conference

March 22, 2016

IADC

MEMBER

www.icdrilling.com

ICD LISTED NYSE

CUSTOMER FOCUS

HSE

Vision

Our vision is to be the premier US land drilling company who provides best in class drilling services with a focus on our employees, technology and HSE. We will continuously strive to understand and exceed our customers’ expectations and in so doing, maximize value for all stakeholders.

FINANCIAL STEWARDSHIP

INTEGRITY

PEOPLE

INDEPENDENCE CONTRACT DRILLING

2

Forward Looking Statements and Non-GAAP Financial Measures

Shale Driller

Various statements contained in this presentation, including those that express a belief, expectation or intention, as well as those that are not statements of historical fact, are forward-looking statements. These forward-looking statements may include projections and estimates concerning the timing and success of specific projects and our future revenues, income and capital spending. Our forward-looking statements are generally accompanied by words such as “estimate,” “project,” “predict,” “believe,” “expect,” “anticipate,” “potential,” “plan,” “goal,” “will” or other words that convey the uncertainty of future events or outcomes. The forward-looking statements in this presentation speak only as of the date of this presentation; we disclaim any obligation to update these statements unless required by law, and we caution you not to rely on them unduly. We have based these forward-looking statements on our current expectations and assumptions about future events. While our management considers these expectations and assumptions to be reasonable, they are inherently subject to significant business, economic, competitive, regulatory and other risks, contingencies and uncertainties, most of which are difficult to predict and many of which are beyond our control. These and other important factors, including those discussed under “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in the Company’s filings with the Securities and Exchange Commission, including the Company’s Annual Report on Form 10-K, may cause our actual results, performance or achievements to differ materially from any future results, performance or achievements expressed or implied by these forward-looking statements. These risks, contingencies and uncertainties include, but are not limited to, the following:

our inability to implement our business and growth strategy;

a sustained decrease in domestic spending by the oil and natural gas exploration and production industry;

decline in or substantial volatility of crude oil and natural gas commodity prices;

fluctuation of our operating results and volatility of our industry;

inability to maintain or increase pricing on our contract drilling services;

delays in construction or deliveries of our new land drilling rigs;

the loss of our customer, financial distress or management changes of potential customers or failure to obtain contract renewals and additional customer contracts for our drilling services;

an increase in interest rates and deterioration in the credit markets;

our inability to raise sufficient funds through debt financing and equity issuances needed to maintain financial liquidity and fund our planned operations and capital expenditures;

our inability to comply with the financial and other covenants in debt agreements that we may enter into as a result of reduced revenues and financial performance;

a substantial reduction in borrowing base under our revolving credit facility as a result of a decline in the appraised value of our drilling rigs or rigs losing eligibility for inclusion in the borrowing base;

overcapacity and competition in our industry;

unanticipated costs, delays and other difficulties in executing our long-term growth strategy;

the loss of key management personnel;

new technology that may cause our drilling methods or equipment to become less competitive;

labor costs or shortages of skilled workers;

the loss of or interruption in operations of one or more key vendors;

the effect of operating hazards and severe weather on our rigs, facilities, business, operations and financial results, and limitations on our insurance coverage;

increased regulation of drilling in unconventional formations;

the incurrence of significant costs and liabilities in the future resulting from our failure to comply with new or existing environmental regulations or an accidental release of hazardous substances into the environment;

the potential failure by us to establish and maintain effective internal control over financial reporting;

lack of operating history as a contract drilling company; and

uncertainties associated with any registration statement, including financial statements, we may be required to file with the SEC.

All forward-looking statements are necessarily only estimates of future results, and there can be no assurance that actual results will not differ materially from expectations, and, therefore, you are cautioned not to place undue reliance on such statements. Any forward-looking statements are qualified in their entirety by reference to the factors discussed throughout this presentation. Further, any forward-looking statement speaks only as of the date on which it is made, and we undertake no obligation to update any forward-looking statement to reflect events or circumstances after the date on which the statement is made or to reflect the occurrence of unanticipated events.

Each of EBITDA and Adjusted EBITDA is a supplemental non-GAAP financial measure that is used by management and external users of our financial statements, such as industry analysts, investors, lenders and rating agencies. We define “EBITDA” as earnings (or loss) before interest, taxes, depreciation, and amortization, and we define “Adjusted EBITDA” as EBITDA before stock-based compensation, gain/loss on warrant derivative liability and non-cash asset impairments. Adjusted EBITDA is not a measure of net income as determined by U.S. generally accepted accounting principles (“GAAP”). Management believes each of EBITDA and Adjusted EBITDA is useful because it allows us and our stockholders to more effectively evaluate our operating performance and compare the results of our operations from period to period and against our peers without regard to our financing methods or capital structure. We exclude the items listed above from net income (loss) in calculating EBITDA and Adjusted EBITDA because these amounts can vary substantially from company to company within our industry depending upon accounting methods and book values of assets, capital structures and the method by which the assets were acquired. EBITDA and Adjusted EBITDA should not be considered an alternative to, or more meaningful than, net income (loss), the most closely comparable financial measure calculated in accordance with GAAP or as an indicator of our operating performance or liquidity. Certain items excluded from EBITDA and Adjusted EBITDA are significant components in understanding and assessing a company’s financial performance, such as a company’s cost of capital and tax structure, as well as stock-based compensation and the historic costs of depreciable assets, none of which are components of EBITDA or Adjusted EBITDA. Our presentation of EBITDA and Adjusted EBITDA should not be construed as an inference that our results will be unaffected by unusual or non-recurring items. Our computations of EBITDA and Adjusted EBITDA may not be comparable to other similarly titled measures of other companies.

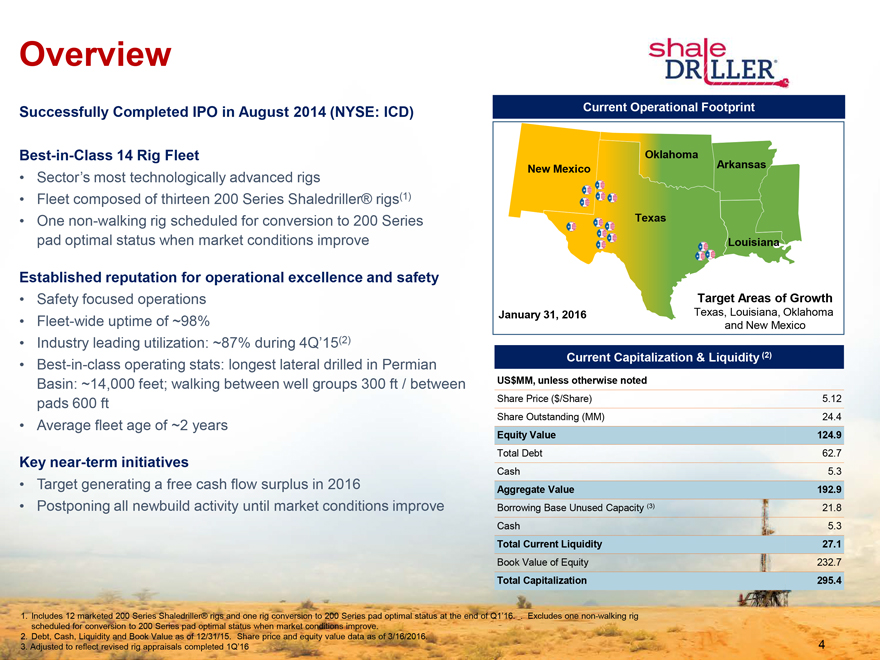

Overview

shale DRILLER

Successfully Completed IPO in August 2014 (NYSE: ICD)

Best-in-Class 14 Rig Fleet

Sector’s most technologically advanced rigs

Fleet composed of thirteen 200 Series Shaledriller® rigs(1)

One non-walking rig scheduled for conversion to 200 Series pad optimal status when market conditions improve

Established reputation for operational excellence and safety

Safety focused operations

Fleet-wide uptime of ~98%

Industry leading utilization: ~87% during 4Q’15(2)

Best-in-class operating stats: longest lateral drilled in Permian Basin: ~14,000 feet; walking between well groups 300 ft / between pads 600 ft

Average fleet age of ~2 years

Key near-term initiatives

Target generating a free cash flow surplus in 2016

Postponing all newbuild activity until market conditions improve

Current Operational Footprint

New Mexico

Oklahoma

Arkansas

Texas

Louisiana

January 31, 2016

Target Areas of Growth

Texas, Louisiana, Oklahoma and New Mexico

Current Capitalization & Liquidity (2)

US$MM, unless otherwise noted

Share Price ($/Share) 5.12

Share Outstanding (MM) 24.4

Equity Value 124.9

Total Debt 62.7

Cash 5.3

Aggregate Value 192.9

Borrowing Base Unused Capacity (3) 21.8

Cash 5.3

Total Current Liquidity 27.1

Book Value of Equity 232.7

Total Capitalization 295.4

1. Includes 12 marketed 200 Series Shaledriller® rigs and one rig conversion to 200 Series pad optimal status at the end of Q1’16. . Excludes one non-walking rig scheduled for conversion to 200 Series pad optimal status when market conditions improve.

2. Debt, Cash, Liquidity and Book Value as of 12/31/15. Share price and equity value data as of 3/16/2016.

3. Adjusted to reflect revised rig appraisals completed 1Q’16

4

Key Differentiators Driving ICD’s Value Proposition

shale DRILLER

ICD is a leader in the rig replacement cycle – pad optimal rigs are critical in the progression of the U.S. unconventional drilling evolution

With industry leading fleet utilization, ICD is the rig provider of choice

By driving faster cycle times, ICD’s rigs bend the E&P cost curve down

ICD’s standardized fleet supports lower capital intensity

Modular manufacturing gives ICD a low cost rig fleet, and provides a compounding capital advantage

ICD’s “Big Data” generation capability allows ICD to participate in the next wave in drilling technology innovation

ICD’s rigs provide high quality EBITDA with a high cash conversion rate

Balance sheet supported by the highest quality asset base in the industry – average age of fleet is ~2 years

5

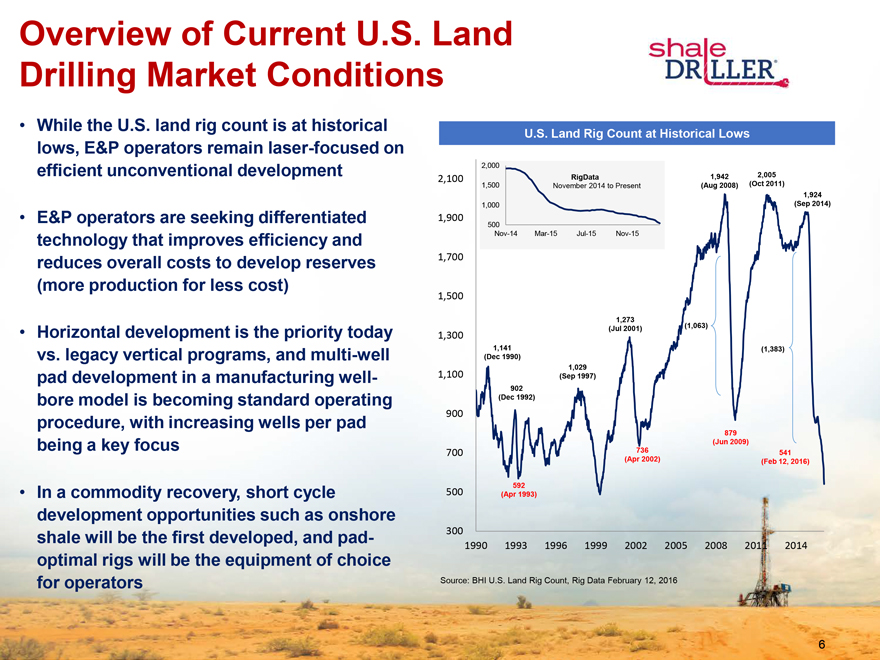

Overview of Current U.S. Land Drilling Market Conditions

shale DRILLER

While the U.S. land rig count is at historical lows, E&P operators remain laser-focused on efficient unconventional development

E&P operators are seeking differentiated technology that improves efficiency and reduces overall costs to develop reserves (more production for less cost)

Horizontal development is the priority today vs. legacy vertical programs, and multi-well pad development in a manufacturing well- bore model is becoming standard operating procedure, with increasing wells per pad being a key focus

In a commodity recovery, short cycle development opportunities such as onshore shale will be the first developed, and pad- optimal rigs will be the equipment of choice for operators

U.S. Land Rig Count at Historical Lows

2,100

1,900

1,700

1,500

1,300

1,100

900

700

500

300

2,000

1,500

1,000

500

Nov-14 Mar-15 Jul-15 Nov-15

RigData

November 2014 to Present

1,942

(Aug 2008)

2,005

(Oct 2011)

1,924

(Sep 2014)

1,141

(Dec 1990)

902

(Dec 1992)

592

(Apr 1993)

1,273

(Jul 2001)

1,029

(Sep 1997)

736

(Apr 2002)

(1,063)

879

(Jun 2009)

(1,383)

541

(Feb 12, 2016)

1990 1993 1996 1999 2002 2005 2008 2011 2014

Source: BHI U.S. Land Rig Count, Rig Data February 12, 2016

6

Market Conditions

shale DRILLER

North American E&P operators developing unconventional shale resources have become the global swing producer

To continue in prominence in this role, North American E&P’s must have the lowest cost operations in the most economic basins available

Achieving this goal requires E&Ps to embrace technological innovation, value-added processes and services that drive major operating efficiencies

ICD is a technological disruptor in North American unconventional drilling – pad-optimal rigs (as defined by the E&P industry) deployed on multi-well pads in a wellbore manufacturing model materially reduce cycle times and operating costs for E&P operators

7

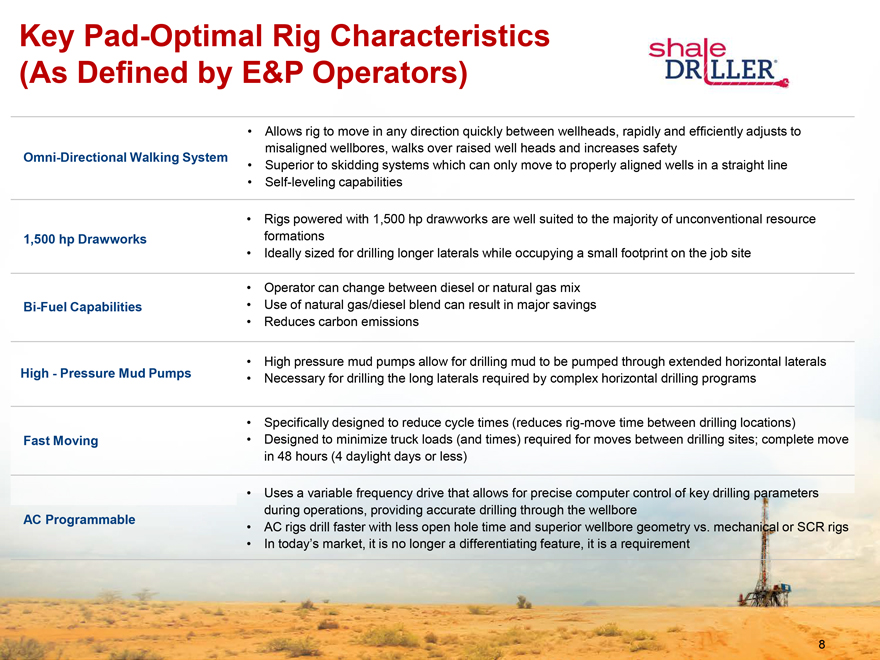

Key Pad-Optimal Rig Characteristics (As Defined by E&P Operators)

shale DRILLER

Omni-Directional Walking System

Allows rig to move in any direction quickly between wellheads, rapidly and efficiently adjusts to misaligned wellbores, walks over raised well heads and increases safety

Superior to skidding systems which can only move to properly aligned wells in a straight line

Self-leveling capabilities

1,500 hp Drawworks

Rigs powered with 1,500 hp drawworks are well suited to the majority of unconventional resource

formations

Ideally sized for drilling longer laterals while occupying a small footprint on the job site

Bi-Fuel Capabilities

Operator can change between diesel or natural gas mix

Use of natural gas/diesel blend can result in major savings

Reduces carbon emissions

High - Pressure Mud Pumps

High pressure mud pumps allow for drilling mud to be pumped through extended horizontal laterals

Necessary for drilling the long laterals required by complex horizontal drilling programs

Fast Moving

Specifically designed to reduce cycle times (reduces rig-move time between drilling locations)

Designed to minimize truck loads (and times) required for moves between drilling sites; complete move in 48 hours (4 daylight days or less)

AC Programmable

Uses a variable frequency drive that allows for precise computer control of key drilling parameters during operations, providing accurate drilling through the wellbore

AC rigs drill faster with less open hole time and superior wellbore geometry vs. mechanical or SCR rigs

In today’s market, it is no longer a differentiating feature, it is a requirement

8

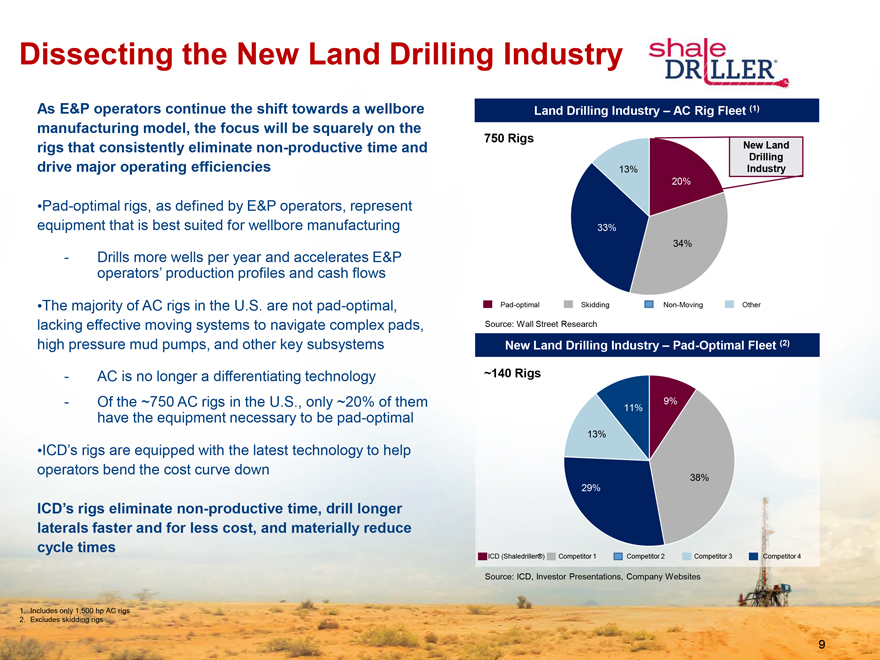

Dissecting the New Land Drilling Industry

shale DRILLER

As E&P operators continue the shift towards a wellbore manufacturing model, the focus will be squarely on the rigs that consistently eliminate non-productive time and drive major operating efficiencies

Pad-optimal rigs, as defined by E&P operators, represent equipment that is best suited for wellbore manufacturing

Drills more wells per year and accelerates E&P operators’ production profiles and cash flows

The majority of AC rigs in the U.S. are not pad-optimal, lacking effective moving systems to navigate complex pads, high pressure mud pumps, and other key subsystems

AC is no longer a differentiating technology

Of the ~750 AC rigs in the U.S., only ~20% of them have the equipment necessary to be pad-optimal

ICD’s rigs are equipped with the latest technology to help operators bend the cost curve down

ICD’s rigs eliminate non-productive time, drill longer laterals faster and for less cost, and materially reduce cycle times

Land Drilling Industry – AC Rig Fleet (1)

750 Rigs

New Land Drilling Industry

13%

33%

20%

34%

Pad-optimal Skidding Non-Moving Other

Source: Wall Street Research

New Land Drilling Industry – Pad-Optimal Fleet (2)

140 Rigs

13%

11%

9%

38%

29%

ICD (Shaledriller®) Competitor 1 Competitor 2 Competitor 3 Competitor 4

Source: ICD, Investor Presentations, Company Websites

1. Includes only 1,500 hp AC rigs

2. Excludes skidding rigs .

9

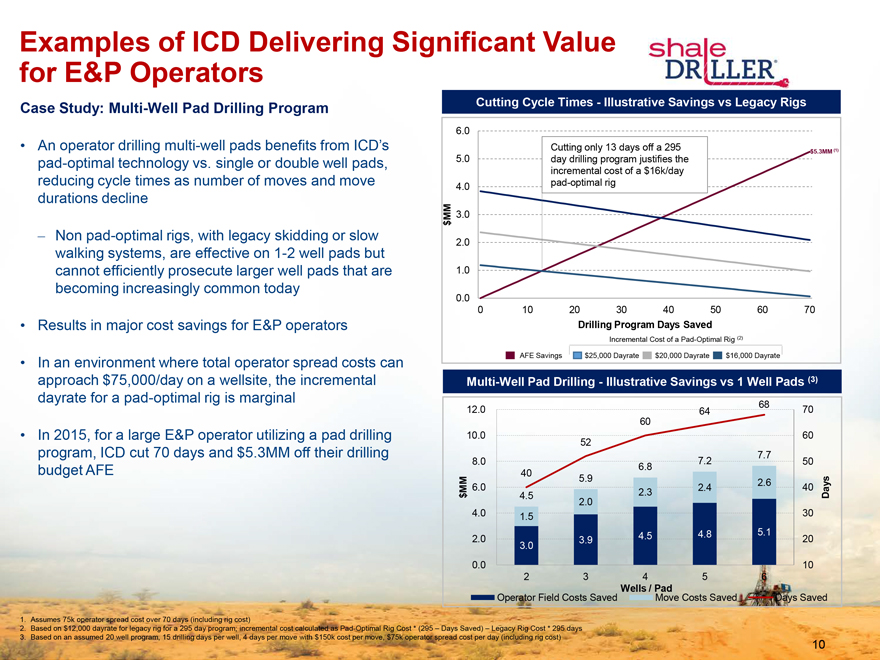

Examples of ICD Delivering Significant Value for E&P Operators

shale DRILLER

Case Study: Multi-Well Pad Drilling Program

An operator drilling multi-well pads benefits from ICD’s pad-optimal technology vs. single or double well pads, reducing cycle times as number of moves and move durations decline

Non pad-optimal rigs, with legacy skidding or slow walking systems, are effective on 1-2 well pads but cannot efficiently prosecute larger well pads that are becoming increasingly common today

Results in major cost savings for E&P operators

In an environment where total operator spread costs can approach $75,000/day on a wellsite, the incremental dayrate for a pad-optimal rig is marginal

In 2015, for a large E&P operator utilizing a pad drilling program, ICD cut 70 days and $5.3MM off their drilling budget AFE

Cutting Cycle Times - Illustrative Savings vs Legacy Rigs

$MM

6.0 5.0 4.0 3.0 2.0 1.0 0.0

Cutting only 13 days off a 295 day drilling program justifies the incremental cost of a $16k/day pad-optimal rig

$5.3MM (1)

0 10 20 30 40 50 60 70

Drilling Program Days Saved

Incremental Cost of a Pad-Optimal Rig (2)

AFE Savings $25,000 Dayrate $20,000 Dayrate $16,000 Dayrate

Multi-Well Pad Drilling - Illustrative Savings vs 1 Well Pads (3)

$MM

12.0 10.0 8.0 6.0 4.0 2.0 0.0

40 4.5 1.5 3.0

52 5.9 2.0 3.9

60 6.8 2.3 4.5

64 7.2 2.4 4.8

68 7.7 2.6 5.1

70 60 50 40 30 20 10

Days

2 3 4 5 6

Wells / Pad

Operator Field Costs Saved Move Costs Saved Days Saved

1. Assumes 75k operator spread cost over 70 days (including rig cost)

2. Based on $12,000 dayrate for legacy rig for a 295 day program; incremental cost calculated as Pad-Optimal Rig Cost * (295 – Days Saved) – Legacy Rig Cost * 295 days

3. Based on an assumed 20 well program, 15 drilling days per well, 4 days per move with $150k cost per move, $75k operator spread cost per day (including rig cost)

10

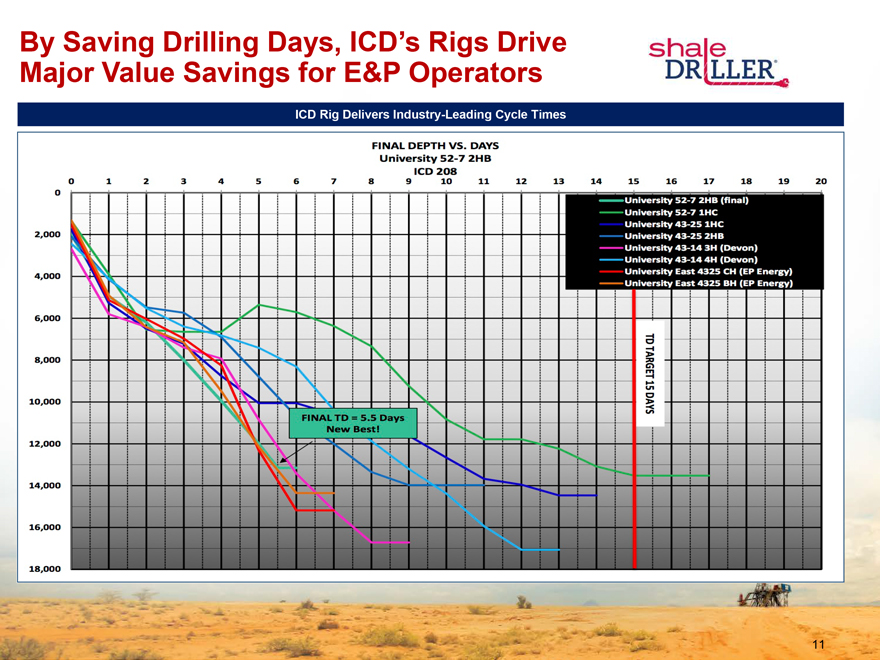

By Saving Drilling Days, ICD’s Rigs Drive Major Value Savings for E&P Operators

shale DRILLER

ICD Rig Delivers Industry-Leading Cycle Times

FINAL DEPTH VS. DAYS University 52-7 2HB ICD 208

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

University 52-7 2HB (final)

University 52-7 1HC University 43-25 1HC

University 43-25 2HB

University 43-14 3H (Devon)

University 43-14 4H (Devon)

University East 4325 CH (EP Energy)

University East 4325 BH (EP Energy)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

FINAL TD = 5.5 Days New Best!

TD TARGET 15 DAYS

11

ICD Initiatives

shale DRILLER

Postponing all new build activities until market improves

Postponing commencement of second rig conversion until market improves

Since June 30, 2015:

Removed approximately $1.0 million from run rate SG&A costs.

Removed approximately $1.0 million from construction overhead costs while maintaining internal build expertise

Removed approximately $600 per day of rig operating costs.

12

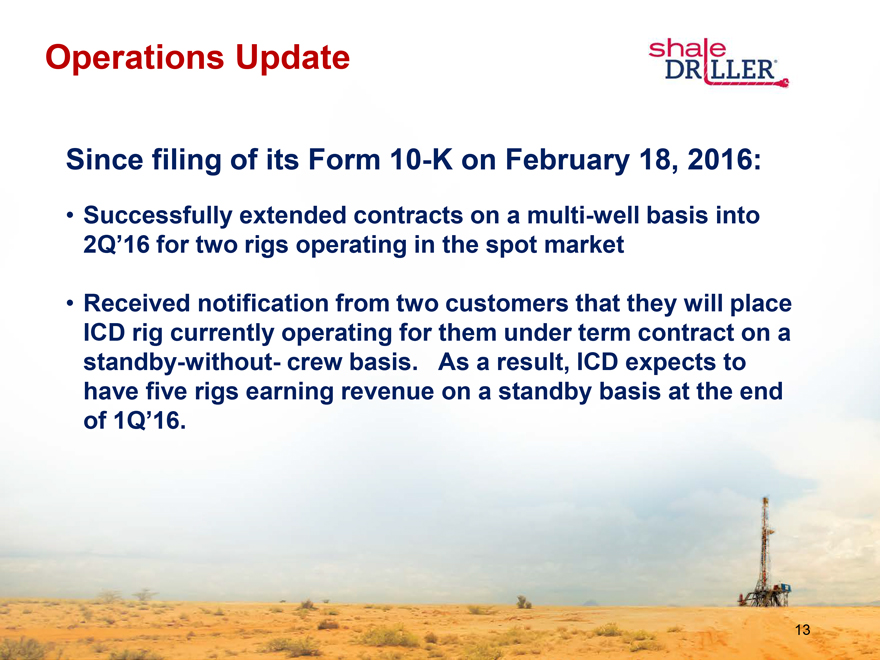

Operations Update

shale DRILLER

Since filing of its Form 10-K on February 18, 2016:

Successfully extended contracts on a multi-well basis into 2Q’16 for two rigs operating in the spot market

Received notification from two customers that they will place ICD rig currently operating for them under term contract on a standby-without- crew basis. As a result, ICD expects to have five rigs earning revenue on a standby basis at the end of 1Q’16.

13

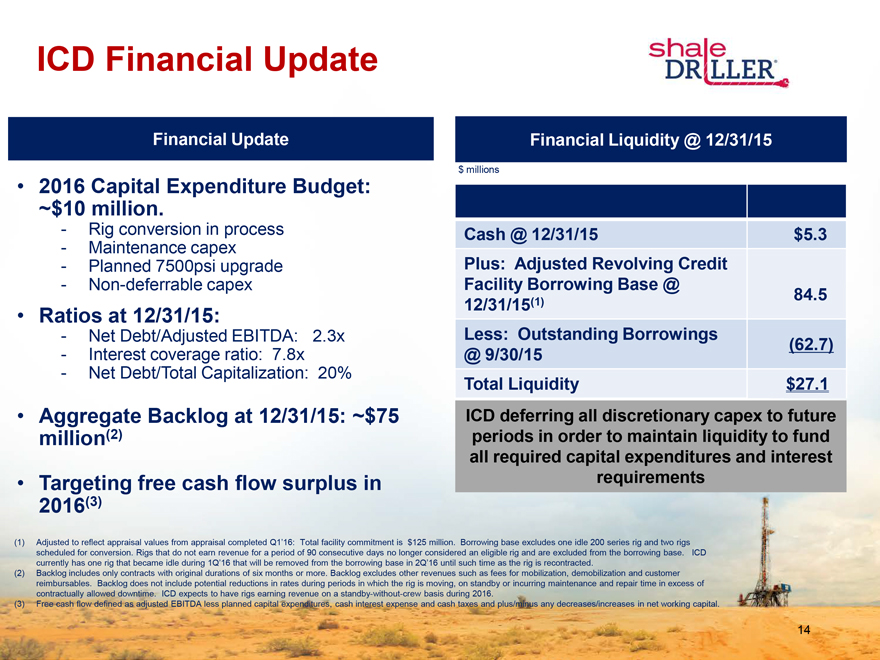

ICD Financial Update

shale Driller

Financial Update

2016 Capital Expenditure Budget: ~$10 million.

- Rig conversion in process

- Maintenance capex

- Planned 7500psi upgrade

- Non-deferrable capex

Ratios at 12/31/15:

- Net Debt/Adjusted EBITDA: 2.3x

- Interest coverage ratio: 7.8x

- Net Debt/Total Capitalization: 20%

Aggregate Backlog at 12/31/15: ~$75 million(2)

Targeting free cash flow surplus in 2016(3)

Financial Liquidity @ 12/31/15

$ millions

Cash @ 12/31/15 $5.3

Plus: Adjusted Revolving Credit Facility Borrowing Base @ 12/31/15(1) 84.5

Less: Outstanding Borrowings @ 9/30/15(62.7)

Total Liquidity $27.1

ICD deferring all discretionary capex to future periods in order to maintain liquidity to fund all required capital expenditures and interest requirements

(1) Adjusted to reflect appraisal values from appraisal completed Q1’16: Total facility commitment is $125 million. Borrowing base excludes one idle 200 series rig and two rigs scheduled for conversion. Rigs that do not earn revenue for a period of 90 consecutive days no longer considered an eligible rig and are excluded from the borrowing base. ICD currently has one rig that became idle during 1Q’16 that will be removed from the borrowing base in 2Q’16 until such time as the rig is recontracted.

(2) Backlog includes only contracts with original durations of six months or more. Backlog excludes other revenues such as fees for mobilization, demobilization and customer reimbursables. Backlog does not include potential reductions in rates during periods in which the rig is moving, on standby or incurring maintenance and repair time in excess of contractually allowed downtime. ICD expects to have rigs earning revenue on a standby-without-crew basis during 2016.

(3) Free cash flow defined as adjusted EBITDA less planned capital expenditures, cash interest expense and cash taxes and plus/minus any decreases/increases in net working capital.

14

I INDEPENDENCE CONTRACT DRILLING

Right Equipment

RIGHT PEOPLE

Right Time

15

Delivering Value to Stakeholders

shale DRILLER

Large Operators are Leading Unconventional Resource Capture

ShaleDriller Offers a Compelling Value Proposition to E&P Customers

Major Secular Shift in Unconventional Development is Underway

Vertically Integrated Model Provides a Compounding Capital Advantage

Ongoing Resource Play Development Driving a Rig Replacement Cycle

Major Barriers to Entry Exist for New Contract Drillers

Pad Optimal AC Drilling Rigs are in Short Supply

I INDEPENDENCE CONTRACT DRILLING

Land Drilling’s Only Pure-Play, Pad Optimal, Growth Story

16

Supplemental Materials

shale DRILLER

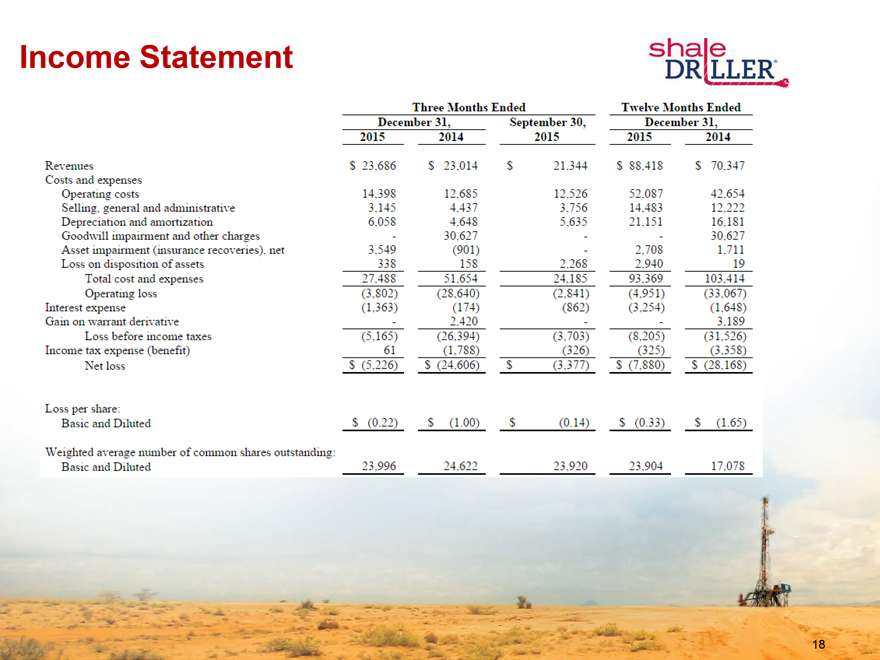

Income Statement

shale DRILLER

Three Months Ended Twelve Months Ended

December 31, September 30, December 31,

2015 2014 2015 2015 2014

Revenues $23,686 $23,014 $21,344 $88,418 $70,347

Costs and expenses

Operating costs 14,398 12,685 12,526 52,087 42,654

Selling, general and administrative 3,145 4,437 3,756 14,483 12,222

Depreciation and amortization 6,058 4,648 5,635 21,151 16,181

Goodwill impairment and other charges - 30,627 - - 30,627

Asset impairment (insurance recoveries), net 3,549 (901) - 2,708 1,711

Loss on disposition of assets 338 158 2,268 2,940 19

Total cost and expenses 27,488 51,654 24,185 93,369 103,414

Operating loss (3,802) (28,640) (2,841) (4,951) (33,067)

Interest expense (1,363) (174) (862) (3,254) (1,648)

Gain on warrant derivative - 2,420 - - 3,189

Loss before income taxes (5,165) (26,394) (3,703) (8,205) (31,526)

Income tax expense (benefit) 61 (1,788) (326) (325) (3,358)

Net loss $(5,226) $(24,606) $(3,377) $(7,880) $(28,168)

Loss per share:

Basic and Diluted $(0.22) $(1.00) $(0.14) $(0.33) $(1.65)

Weighted average number of common shares outstanding:

Basic and Diluted 23,996 24,622 23,920 23,904 17,078

18

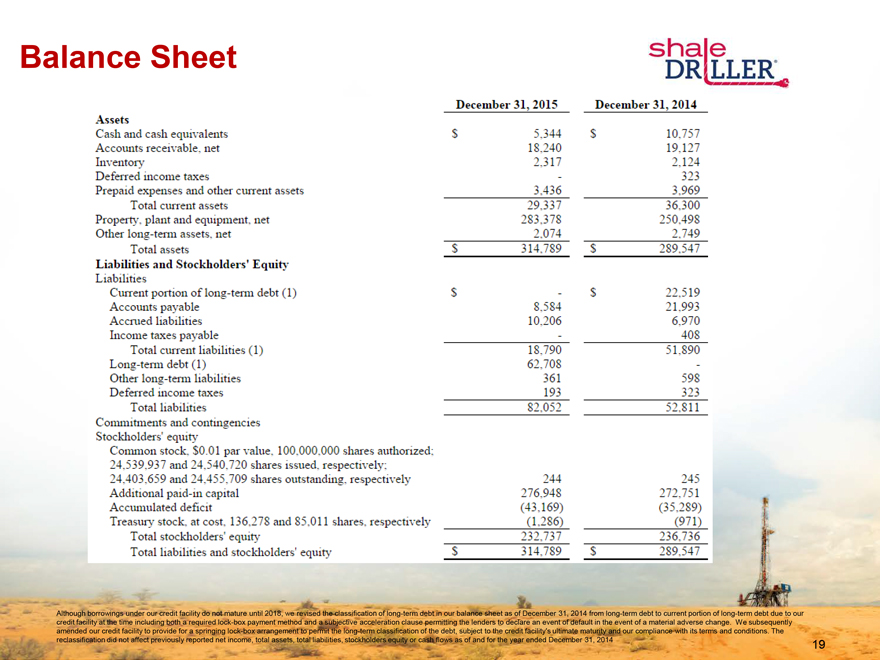

Balance Sheet

shale DRILLER

December 31, 2015 December 31, 2014

Assets

Cash and cash equivalents $5,344 $10,757

Accounts receivable, net 18,240 19,127

Inventory 2,317 2,124

Deferred income taxes - 323

Prepaid expenses and other current assets 3,436 3,969

Total current assets 29,337 36,300

Property, plant and equipment, net 283,378 250,498

Other long-term assets, net 2,074 2,749

Total assets $314,789 $289,547

Liabilities and Stockholders’ Equity

Liabilities

Current portion of long-term debt (1) $- $22,519

Accounts payable 8,584 21,993

Accrued liabilities 10,206 6,970

Income taxes payable - 408

Total current liabilities (1) 18,790 51,890

Long-term debt (1) 62,708 -

Other long-term liabilities 361 598

Deferred income taxes 193 323

Total liabilities 82,052 52,811

Commitments and contingencies

Stockholders’ equity

Common stock, $0.01 par value, 100,000,000 shares authorized; 24,539,937 and 24,540,720 shares issued, respectively; 24,403,659 and 24,455,709 shares outstanding, respectively 244 245

Additional paid-in capital 276,948 272,751

Accumulated deficit (43,169) (35,289)

Treasury stock, at cost, 136,278 and 85,011 shares, respectively (1,286) (971)

Total stockholders’ equity 232,737 236,736

Total liabilities and stockholders’ equity $314,789 $289,547

Although borrowings under our credit facility do not mature until 2018, we revised the classification of long-term debt in our balance sheet as of December 31, 2014 from long-term debt to current portion of long-term debt due to our credit facility at the time including both a required lock-box payment method and a subjective acceleration clause permitting the lenders to declare an event of default in the event of a material adverse change. We subsequently amended our credit facility to provide for a springing lock-box arrangement to permit the long-term classification of the debt, subject to the credit facility’s ultimate maturity and our compliance with its terms and conditions. The reclassification did not affect previously reported net income, total assets, total liabilities, stockholders equity or cash flows as of and for the year ended December 31, 2014

19

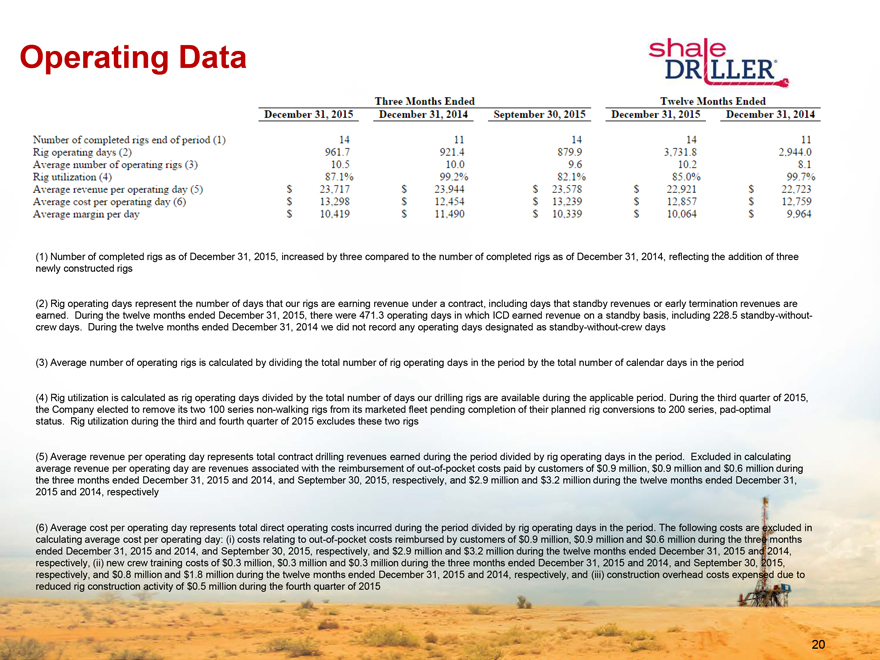

Operating Data

shale DRILLER

Three Months Ended Twelve Months Ended

December 31, 2015 December 31, 2014 September 30, 2015 December 31, 2015 December 31, 2014

Number of completed rigs end of period (1) 14 11 14 14 11

Rig operating days (2) 961.7 921.4 879.9 3,731.8 2,944.0

Average number of operating rigs (3) 10.5 10.0 9.6 10.2 8.1

Rig utilization (4) 87.1% 99.2% 82.1% 85.0% 99.7%

Average revenue per operating day (5) $23,717 $23,944 $23,578 $22,921 $22,723

Average cost per operating day (6) $13,298 $12,454 $13,239 $12,857 $12,759

Average margin per day $10,419 $11,490 $10,339 $10,064 $9,964

(1) Number of completed rigs as of December 31, 2015, increased by three compared to the number of completed rigs as of December 31, 2014, reflecting the addition of three newly constructed rigs

(2) Rig operating days represent the number of days that our rigs are earning revenue under a contract, including days that standby revenues or early termination revenues are earned. During the twelve months ended December 31, 2015, there were 471.3 operating days in which ICD earned revenue on a standby basis, including 228.5 standby-without-crew days. During the twelve months ended December 31, 2014 we did not record any operating days designated as standby-without-crew days

(3) Average number of operating rigs is calculated by dividing the total number of rig operating days in the period by the total number of calendar days in the period

(4) Rig utilization is calculated as rig operating days divided by the total number of days our drilling rigs are available during the applicable period. During the third quarter of 2015, the Company elected to remove its two 100 series non-walking rigs from its marketed fleet pending completion of their planned rig conversions to 200 series, pad-optimal status. Rig utilization during the third and fourth quarter of 2015 excludes these two rigs

(5) Average revenue per operating day represents total contract drilling revenues earned during the period divided by rig operating days in the period. Excluded in calculating average revenue per operating day are revenues associated with the reimbursement of out-of-pocket costs paid by customers of $0.9 million, $0.9 million and $0.6 million during the three months ended December 31, 2015 and 2014, and September 30, 2015, respectively, and $2.9 million and $3.2 million during the twelve months ended December 31, 2015 and 2014, respectively

(6) Average cost per operating day represents total direct operating costs incurred during the period divided by rig operating days in the period. The following costs are excluded in calculating average cost per operating day: (i) costs relating to out-of-pocket costs reimbursed by customers of $0.9 million, $0.9 million and $0.6 million during the three months ended December 31, 2015 and 2014, and September 30, 2015, respectively, and $2.9 million and $3.2 million during the twelve months ended December 31, 2015 and 2014, respectively, (ii) new crew training costs of $0.3 million, $0.3 million and $0.3 million during the three months ended December 31, 2015 and 2014, and September 30, 2015, respectively, and $0.8 million and $1.8 million during the twelve months ended December 31, 2015 and 2014, respectively, and (iii) construction overhead costs expensed due to reduced rig construction activity of $0.5 million during the fourth quarter of 2015

20

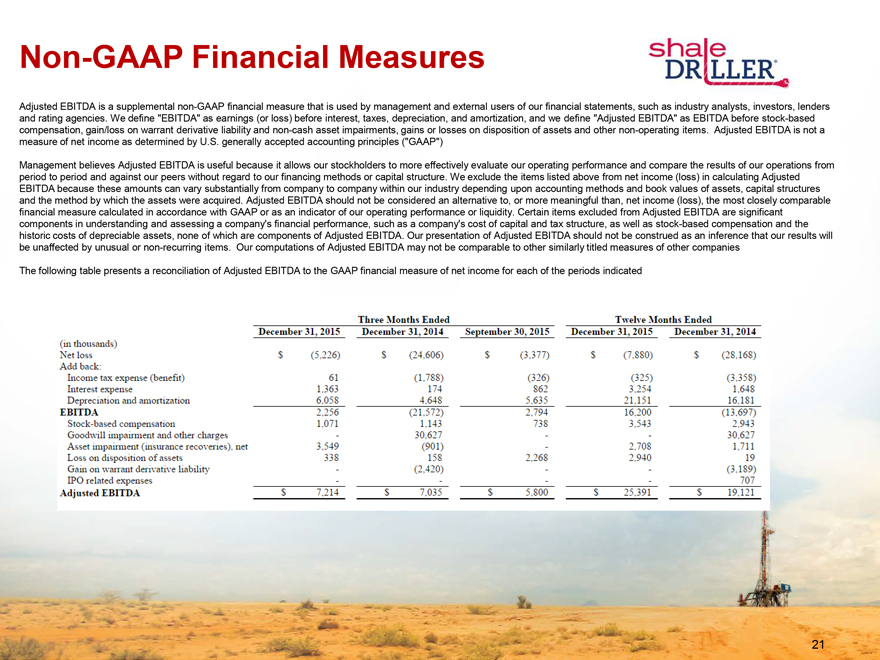

Non-GAAP Financial Measures

shale DRILLER

Adjusted EBITDA is a supplemental non-GAAP financial measure that is used by management and external users of our financial statements, such as industry analysts, investors, lenders and rating agencies. We define “EBITDA” as earnings (or loss) before interest, taxes, depreciation, and amortization, and we define “Adjusted EBITDA” as EBITDA before stock-based compensation, gain/loss on warrant derivative liability and non-cash asset impairments, gains or losses on disposition of assets and other non-operating items. Adjusted EBITDA is not a measure of net income as determined by U.S. generally accepted accounting principles (“GAAP”)

Management believes Adjusted EBITDA is useful because it allows our stockholders to more effectively evaluate our operating performance and compare the results of our operations from period to period and against our peers without regard to our financing methods or capital structure. We exclude the items listed above from net income (loss) in calculating Adjusted EBITDA because these amounts can vary substantially from company to company within our industry depending upon accounting methods and book values of assets, capital structures and the method by which the assets were acquired. Adjusted EBITDA should not be considered an alternative to, or more meaningful than, net income (loss), the most closely comparable financial measure calculated in accordance with GAAP or as an indicator of our operating performance or liquidity. Certain items excluded from Adjusted EBITDA are significant components in understanding and assessing a company’s financial performance, such as a company’s cost of capital and tax structure, as well as stock-based compensation and the historic costs of depreciable assets, none of which are components of Adjusted EBITDA. Our presentation of Adjusted EBITDA should not be construed as an inference that our results will be unaffected by unusual or non-recurring items. Our computations of Adjusted EBITDA may not be comparable to other similarly titled measures of other companies

The following table presents a reconciliation of Adjusted EBITDA to the GAAP financial measure of net income for each of the periods indicated

Three Months Ended Twelve Months Ended December 31, 2015 December 31, 2014 September 30, 2015 December 31, 2015 December 31, 2014

(in thousands)

Net loss $(5,226) $(24,606) $(3,377) $(7,880) $(28,168)

Add back:

Income tax expense (benefit) 61 (1,788) (326) (325) (3,358)

Interest expense 1,363 174 862 3,254 1,648

Depreciation and amortization 6,058 4,648 5,635 21,151 16,181

EBITDA 2,256 (21,572) 2,794 16,200 (13,697)

Stock-based compensation 1,071 1,143 738 3,543 2,943

Goodwill impairment and other charges - 30,627 - - 30,627

Asset impairment (insurance recoveries), net 3,549 (901) - 2,708 1,711

Loss on disposition of assets 338 158 2,268 2,940 19

Gain on warrant derivative liability - (2,420) - - (3,189)

IPO related expenses - - - - 707

Adjusted EBITDA $7,214 $7,035 $5,800 $25,391 $19,121

21

I INDEPENDENCE CONTRACT DRILLING

22